Property Council of Australia (SA Division) Pre Budget Submission 09-10

129

. . . . . . 142 GAWLER PLACE, ADELAIDE SA 5000 PH 08 8236-0900 - FAX 08 8223-6451 www.propertyoz.com.au The Voice of Leadership Pre-Budget Pre-Budget Submission: Submission: 2009-2010 2009-2010 SA State Budget SA State Budget Property Council of Australia Property Council of Australia February, 2009 February, 2009 Alliance Partner

Pre-Budget Pre-Budget Submission:Submission:2009-2010 2009-2010 SA State BudgetSA State Budget

Property Council of AustraliaProperty Council of AustraliaFebruary, 2009February, 2009

Alliance Partner

.........

Table of ContentsExecutive Summary...............................................................................iiiThe Property Council in Brief.................................................................iv2008 in Review .....................................................................................vRecommendations.................................................................................viA Guide to Reading this Submission......................................................x1. Building SA for Growth.....................................................................1

1.1 Urban Renewal Initiative .................................................21.2 Local Action Plans............................................................5

2. Climate Change and the Environment.............................................72.1 A Climate Change Policy for the Built Environment..........82.2 The Second Plank: Green Depreciation.............................112.3 Delivering Water Use Reductions.....................................13

3. Community Dividends......................................................................143.1 Corporate Responsibility..................................................................154. Governing Smarter...........................................................................164.1 Modernising Metropolitan Governance.............................................174.2 Modernising Local Governance........................................................205. Fairer Taxes.....................................................................................21

5.1 Broad tax review..............................................................225.2 Land tax...........................................................................235.3 Stamp duty.......................................................................255.4 Rationalisation Program...................................................26

Attachment 1: Recycled Water Pipeline Position Paper..........................28Attachment 2: Cost Benefit Evaluation of Reducing Taxes....................36Attachment 3: Unit Trust Rationalisation Model.....................................73Attachment 4: Unit Trust Gap Analysis..................................................79Attachment 5: Unit Trust CRE Rationalisation Model..............................83Attachment 6: Unit Trust CRE Gap Analysis...........................................88

- ii -

.........

Executive SummaryThis submission focuses on the contribution of the property investment and development sectors to the broader community. The Property Council supports a budget that delivers: a return to strong, ongoing economic growth of three to

four per cent; a public policy reform framework for long-term sustainable

growth; and programs that build community capacity and better balance

the social, environmental and economic targets of South Australia’s Strategic Plan.

In addition, the Property Council contends that a new approach to setting fiscal policy – based on the following concepts – should inform the design of the 2009/2010 budget: Key performance indicators – greater clarity about the

measurable goals of all budget programs; Community capacity building – lifting the ability of

individuals, families and firms to make the most of their relative talents and opportunities;

Sustainability – optimising governance, economic, social and environmental assets for the long-term benefit of the community;

A war on red tape – more efficient regulation, less duplication and minimal conflict of policy settings;

Tax reform – lower taxes achieved through more efficient tax design that also delivers lower compliance costs and promotes a competitive economy;

Modern policy assessment instruments – adoption of methodologies that better allocate scarce resources (such as capital spending on infrastructure) on a triple bottom line basis, and allow for more effective assessment of regulatory impacts;

Accounting for spatial implications – an understanding of the spatial consequences of all policy programs; and,

Incentives – the use of incentives to transform market behaviour to meet community goals as an alternative to regulation.

These concepts are not all directly addressed in this submission however the Property Council (SA Division) will be addressing each of these areas in the leadup to the State Election in March 2010. The Property Council is available to discuss each of the areas outlined above.

- iii -

.........

The Property Council in BriefThe Property Council represents the property investment sector in Australia.

Its members include every major property investor in the State.

Members are engaged in the entire property investment universe, which includes all:

dimensions of property activity (financing, funds management, development, ownership, asset management, transaction and leasing);

major property types (offices, shopping centres, residential development, industrial, tourism, leisure, aged care, retirement and infrastructure);

major regions of Australia and international markets; and,

the four quadrants of investment – public, private, equity and debt.

Some key statistics:

the value of investment grade stock under management in South Australia is $3.5 billion;

more than half a million South Australians collectively own major segments of the state’s most valuable commercial property assets;

the market value of foreign assets owned by Australians is $50 billion;

Total construction spending across South Australia in 2009 is forecast to be $9.46 billion; comprising $4.3 billion in residential construction, $1.5 billion in commercial construction and $3.6 billion in infrastructure1 (this does not take into account the recent Federal Government Economic Stimulus Package);

$61 million flows in to the property sector from super funds in an average week; and,

$1.5 billion in property specific taxes are paid annually to the State Government.

1 Construction Forecasting Council [http://www.cfc.acif.com.au/] January 2009

- iv -

.........

2008 in Review Globally, 2008 was a tough year. While the year started well, the gradual collapse of the financial sector in the US and UK culminated in a market meltdown in the last quarter.

The flow-on effects of this are expected to felt until late 2010.

While the global financial crisis has had an impact on Australia, the overall impact on South Australia to date has been comparatively limited; in the main it has resulted in fewer options for financing and downward pressure on property values.

In 2008, the Government put into place a range of reforms that will ensure a bright future for the State including planning reforms incorporating delivery of transit oriented developments, a new planning instrumentality, and significant infrastructure investment that will enable the State to meet the needs of a growing population while delivering increased prosperity.

In 2009 it is expected that there will be an increase in the numbers of commercial properties transacted but at lower values than have been seen over the last 12 to 24 months. It is also expected that finance will become easier to source over the year, reducing pressure on the economy and facilitating delivery of more critical projects.

While the State Budget is under pressure from reduced GST revenues and stamp duty receipts, the medium to long term outlook for the state economy remains positive with growth in the resources and defence sectors.

The big negative for 2008 was the significant increase in property valuations which resulted in sudden and unexpected increases in land tax bills. These increases were unwelcome in a softening climate and it is worth noting that the Queensland Government took immediate action to freeze land tax valuations to protect jobs and bolster the economy. The impact has already been seen in a reduction in forward development, declining employment levels and falling investment levels. The key issue is the uncompetitively high levels of land tax in South Australia compared to every other jurisdiction in Australia, compounded by the fact that land tax bills cannot be budgeted for.

It is imperative that the Government use this time to prepare the State for prosperity. The State must be moving onto a ‘war footing’ so that the potential prosperity does not pass us by.

- v -

.........

Recommendations Building SA for Growth

Urban Renewal Initiative – Recommendations:

First: Establish an Urban Renewal Initiative, overseen by the Urban Renewal Unit.

Second: Establish an Urban Renewal Unit, to deliver the Urban Renewal Initiative.

Third: Develop community capacity building KPIs, to be used to guide for State Government funding support. Such KPIs could underpin a sustainability and growth charter along lines recommended by the House of Representatives reports on Sustainable Cities (2005) and Sustainability for Survival (2007).

Fourth: Identify and fund five catalyst urban renewal projects (confirm five years of State Government financial support).

Local Action Plans – Recommendations:First: Establish a working group to develop and deliver Local

Action Plans.

Second: Deliver better governance by making financial support contingent on the achievement of community capacity building KPIs.

Third: Use PPPs and other innovative funding mechanisms to accelerate the delivery of infrastructure projects.

Climate Change and Environment

A Strategy for Transforming Market Behaviour – Recommendations:

First: Develop voluntary interim performance targets across all eco efficiency categories – energy/greenhouse abatement, water, waste and indoor environmental quality – to enable to achievement of targets in South Australia’s Strategic Plan.

Second: Provide $300,000 over two years to the Property Council to enhance the Government/Property Council Green Buildings Tune-Ups Program, specifically to develop and disseminate

- vi -

.........information such as a tune-up and retro-greening toolkit and help to build industry capacity.

Fourth: Cut environmental red tape. Fifth: Establish a state demonstration program that makes the

business case for green development/buildings and promotes innovative practices.

Sixth: Develop a One Stop Shop for all water, waste and energy reduction stratgies, directing building owners to sources of financial and non-financial incentives.

Green Depreciation – Recommendation:

First: Support the introduction of accelerated depreciation for buildings that retrofit (retro-green) to meet higher environmental standards.

Delivering Water Use Reductions – Recommendations: The Property Council proposes the following package of measures: First: Cut water connection charges by 50 per cent for

commercial properties that deliver significant reductions in potable water use.

Second: Finance the extension of the recycled water pipeline through the CBD.

Community Dividends

Corporate Responsibility – Recommendation:

Note the existence of the Property Council’s draft template for corporate responsibility reporting and the Code of Conduct for the property investment and development sectors.

First: Adopt the Property Council’s proposed Metropolitan Governance Principles and work with local government to deliver.

Modernising Local Governance - Recommendations:

First: Help to reform and improve the performance of local government with the following programs:

- institute an inquiry into the optimal size of local councils that balances democratic representation, efficient delivery of services, environmental catchments, funding powers and ability to attract (and retain) professional staff;

- support a constitutional commission to develop a model for establishing councils as local parliaments. A key feature of the model would be the application of the separation of powers doctrine to key local government activities;

- require all councils to develop local action plans based on key performance indicators (KPIs), similar to South Australia’s Strategic Plan. All councils should develop 25-year infrastructure plans;

- require councillors who sit on planning committees to undertake professional development provided by a registered training provider;

- offer incentive payments to, and abolish rate capping for, local governments that undertake reforms; and

- establish a fiscal responsibility protocol for local government.

- viii -- viii -

......... Fairer Taxes A broad tax review – Recommendations:First: Immediately undertake a broad review of South Australia’s

taxation base with a view to aligning with the Federal Henry Review of Taxation.

Second: Examine and remove financial disincentives to skilled employees and investors considering South Australia as an employment and investment destination.

Third: Ensure that existing and proposed tax measures do not constrain the ability of the property industry to adjust to environmental demands.

Land Tax – Recommendations: First: Immediately freeze property valuation increases to provide

relief to businesses and investors in South Australia.Second: Increase the base threshold to $250,000 and the maximum

threshold to $2.5 million at a rate of 2.5c per dollar.

Stamp Duty on Non-Residential Conveyances– Recommendations: First: Immediately abolish Stamp Duty on Non-Residential

Conveyances.

Rationalisation Program – Recommendations: First: Immediately adopt and implement the rationalisation models.

- ix -

.........

A Guide to Reading this SubmissionThis submission provides recommendations on 12 policy topics grouped by five broad themes:

1. Building SA for growth

2. Climate change and the environment

3. Community dividends

4. Governing smarter

5. Fairer taxes

This submission focuses on policy issues with implications for the 2009-2010 State budget. In general, one to two pages of commentary and recommendations are provided for each topic. As each section has been written to assist the State to meet targets in South Australia’s Strategic Plan, each applicable target is identified.

The Property Council of Australia can provide considerably more detail for each subject area, including extensive research reports prepared by Australia’s leading independent consultants and academics.

We are keen to share these resources with the South Australian Government.

the creation of local action plans. the need for an urban renewal program in South Australia to

revitalise Adelaide and provide a diverse range of housing products to meet growing demand;

Fiscal Implications – 2009 State Budget:Urban Renewal Commission – minimal fiscal impact in year one.Local Action Plans – minimal fiscal impact in year one.

The Property Council welcomes the establishment of the State Government’s commitment to urban renewal and investment in the rail network.

We believe this is a good first step, but to achieve the targets established by South Australia’s Strategic Plan an Urban Renewal Unit, similar to the Major Cities Unit at the federal level, should be created to be responsible for developing and implementing an Urban Renewal Initiative, which would link all aspects of urban infrastructure to economic, livability, environmental and governance KPIs.

South Australia’s next leap in competitiveness and living standards will occur in Adelaide and the State’s major regional centers.

While ongoing reform programs focus on key sectoral drivers, such as transport, health, education and infrastructure, we need to hardwire these programs into an overarching strategy that addresses the urban communities that generate 80 per cent of the State’s GSP.

There are already myriad government programs that touch on the State’s major cities and townships. However, outside of South Australia’s Strategic Plan there is little public policy logic that ties these programs into a coherent community capacity building strategy.

Urban Renewal Initiative: Principal Proposition

The concept of a national urban renewal action plan is based on these basic propositions:

renewal plans are needed for major locales in Adelaide based on medium and long-term targets for community capacity building;

such targets should address factors that drive prosperity, including health services, education, transport, information connectivity, and the natural environment – as they relate to local communities;

renewal plans should be linked to infrastructure delivery programs;

each plan should be financed by modern public and private funding practices;

each plan would provide an assessment of estimated dividends versus the total cost of implementation; and,

- 2 -

......... the Urban Renewal Initiative should work in conjunction with other

government objectives to reduce red tape, improve governance and ensure the optimal democratic involvement of local communities.

What Would the Urban Renewal Initiative Aim to Achieve?

The Urban Renewal Initiative would seek to facilitate a major boost to both South Australia’s competitiveness and living standards.

To be successful the state’s cities and major regional centres need diverse, vibrant and inclusive communities.

They must be exciting, accessible and safe places where we can build the social capital that reduces poverty and unleashes creativity.

In short, our cities must be magnets that attract and leverage both capital and talent.

The centrepiece of the Urban Renewal Initiative is a concept of sustainability that involves better managing the community's economic, social, environmental and governance assets to produce dividends that improve opportunities for all citizens.

Delivering the Urban Renewal Initiative (URI) – Role of the Urban Renewal Unit

An Urban Renewal Unit Board compromising senior government, industry and community representatives should be established to guide and oversee the work of the Commission. A property industry representative should be included on the Board – reflecting the significance of integrating land use and infrastructure planning. A work program for the Urban Renewal Unit should be established by December 2009. The community capacity building KPIs developed by the Unit should be applied as a basis for determining continued access to State funding. The Urban Renewal Unit should identify and seed fund major projects that demonstrate governance reform. Five catalyst urban renewal projects should be identified and provided with five years of State support (a five year program). These should be selected on merit (projects which would deliver the greatest community capacity building dividends). Detailed renewal plans should be agreed and implemented for selected precincts, including land use and infrastructure plans. The Urban Renewal Unit should also link into the State Government’s systemic reform to improve Australia’s land use and infrastructure planning system. Specifically, the Property Council asks the South Australian Government to:

- 3 -

.........

Urban Renewal Initiative – Recommendations:

First: Establish an Urban Renewal Initiative, overseen by the Urban Renewal Unit.

Second: Establish an Urban Renewal Unit, to deliver the Urban Renewal Initiative.

Third: Develop community capacity building KPIs, to be used to guide for State Government funding support. Such KPIs could underpin a sustainability and growth charter along lines recommended by the House of Representatives reports on Sustainable Cities (2005) and Sustainability for Survival (2007).

Fourth: Identify and fund five catalyst urban renewal projects (confirm five years of State Government financial support).

Sources:

Tax Increment Financing to Fund Infrastructure in Australia, PricewaterhouseCoopers (2008, forthcoming)Funding Urban Public Infrastructure, Allen Consulting Group (2003)Recapitalising Australia’s Cities, Allen Consulting Group (2002)

Sustainable Communities: a national plan of action, Centre for International Economics (2006)

Sustainable Cities, House of Representatives Standing Committee on Environment and Heritage (2005)

Sustainability for Survival, House of Representatives Standing Committee on Environment and Heritage (2007)

- 4 -

.........

1.2 Local Action Plans

South Australia's next leap in competitiveness and living standards will occur in its cities and towns. While ongoing reform programs focus on key sectoral drivers, such as transport, health, education and infrastructure, we need to hardwire these programs into an overarching strategy that addresses the urban communities that generate 80 per cent of the state’s GSP. In doing so, we should aim to forge far-sighted reform strategies that are sustainable. This action plan for urban South Australia outlines a model for achieving these goals. The concept of a local action plan is based on these basic propositions:

there should be a plan for every locale in South Australia that sets targets for building community capacity – aligned to South Australia’s Strategic Plan;

these targets would address all factors that drive prosperity - health services, education, transport, information connectivity, the natural environment (to name a few) - as they relate to local communities;

each local plan would be backed by an infrastructure delivery program that would help achieve these targets;

each plan would be financed by modern public and private funding practices;

each plan would provide an assessment of the dividends it is expected to deliver versus its total cost of implementation;

each plan would strive to reduce red tape, improve governance and ensure the optimal democratic involvement of local communities

The State Government should tie financial assistance (or project funding) to Local Governments achieving agreed, common objectives (or KPIs).

More use should be made of PPPs and innovative funding mechanisms to accelerate the delivery of key infrastructure projects.

The Property Council commissioned research by PricewaterhouseCoopers into tax increment financing (TIF) techniques employed successfully in the United States and Europe.

TIFs involve appropriating increases in tax revenue arising from an investment in infrastructure to amortise the cost of providing infrastructure.

TIFs draw on the financial dividend that infrastructure delivers over time to help fund up front costs. There are no additional taxes.

The recommendation is based on a National Report titled, Sustainable Communities: a national plan of action, developed by the Centre for

- 5 -

.........International Economics, following extensive stakeholder consultation over the past four years.

Specifically, the Property Council asks the South Australian Government to:

Local Action Plans – Recommendations:First: Establish a working group to develop and deliver Local Action

Plans.

Second: Deliver better governance by making financial support contingent on the achievement of community capacity building KPIs.

Third: Use PPPs and other innovative funding mechanisms to accelerate the delivery of infrastructure projects.

Sources:

Tax Increment Financing to Fund Infrastructure in Australia, PricewaterhouseCoopers (2008, forthcoming) Funding Urban Public Infrastructure, Allen Consulting Group (2003)Recapitalising Australia’s Cities, Allen Consulting Group (2002)

- 6 -

.........

2. Climate Change and the Environment

This chapter recommends an overarching strategy for dealing with climate change and the built environment, including the extension of the Green Buildings Tune-Ups Program; promoting accelerated green depreciation; and reforms to deliver increased waste water re-use.

The Property Council commends the State Government on its forward-thinking legislation to establish targets aimed at reducing greenhouse gas emissions and its budgetary support for the Green Building Tune-Ups Program. The Property Council has concluded a Sector Agreement with the State Government as provided by Legislation.

The Property Council sees programs that focus on broad-scale improvements in the energy efficiency of the built environment (and building users) as a crucial pathway to achieving deep cuts in greenhouse gases and water use.

Fiscal Implications – 2009 State Budget:Climate change and the built environment – repackaging of existing programs. Enhanced Green Buildings Tune-Ups Program –$300,000 over two years. Support for accelerated depreciation – no fiscal impact to South Australia.Water Use Minimisation Strategy – estimated to cost $5m.

2.1 A Climate Change Policy for the Built Environment

The Property Council and the State Government are working together to deliver a greener built environment; a partnership based on a Sector Agreement. The recommendations in this section are designed to build on the existing strong relationship.

“…in order to make an overall longer term impact on drawing down carbon emissions…energy efficiency [is the] second plank.”

Kevin Rudd, Prime Minister of Australia, 19 August, 2008

Buildings and their occupants account for 23% of Australian’s greenhouse gas emissions (GHG).2

The Built Environment Offers a Ready Source of GHG Savings

Research conducted by the Australian Sustainable Built Environment Council (ASBEC)3 showed that significant abatement can be achieved with properly targeted incentives.

Relying on the Carbon Pollution Reduction Scheme (CPRS) alone the building sector is expected to reduce emissions by around 8 Mt a year.

The ASBEC research demonstrates that with complementary measures and incentives, abatement of around 60 Mt per annum is achievable by 2030.

The Opportunity

A strategic approach to building energy efficiency could:

halve electricity use in commercial building stock by 2030 and 70% by 2050;

reduce GHG emissions by 30% within two decades;

cut the cost of carbon abatement by 14% or $30 per tonne by 2050;

return $38 billion each year to the GDP compared to conventional GHG abatement programs by 2050;

provide breathing space for the development of clean energy alternatives; and,

help the country reduce its carbon footprint faster and with less fuss.

2 Capitalising on the Building Sector’s Potential to Lessen the Cost of a Broad Based GHG Emissions Cut, Centre for International Economics (September, 2007)3 The Second Plank – Building A Low Carbon Economy With Energy Efficient Buildings, Centre for International Economics for ASBEC (August, 2008)

- 8 -

.........Eco-efficiency in the Built Environment

Energy efficiency does not provide the only opportunity for the built environment. A focus on eco-efficiency could deliver other significant sustainability dividends:

new commercial buildings and their occupants could:

o consume 60%-70% less water;

o generate 40% less waste; and,

o deliver higher indoor environmental quality;

new dwellings and their occupants could halve their eco footprint compared to business as usual performance; and

retrofitted existing commercial buildings could achieve at least half the efficiencies of new buildings over the next decade.

The Second Plank

The ASBEC/CIE paper proposed three specific policy measures that would allow energy efficiency in the building sector to deliver greater abatement opportunities:

a national white certificate scheme;

provision of green depreciation; and,

public funding for building retrofits – aimed at both the retail (residential and commercial buildings) and wholesale (energy retailer) sectors.

These recommendations are covered in more detail in the next section.

Sources:

Capitalising on the Building Sector’s Potential to Lessen the Cost of a Broad Based GHG Emissions Cut, Centre for International Economics (September, 2007)

The Second Plank – Building A Low Carbon Economy With Energy Efficient Buildings, Centre for International Economics for ASBEC (August, 2008)

- 9 -

.........The recommendations outlined below will enable South Australia to achieve significant social and economic benefits while also ensuring we meet our national and international obligations. The requested funding of an additional $300,000 over two years will enable the Property Council to deliver education programs and materials that encourage the property sector to refurbish existing buildings. This expenditure will enhance the Government/Property Council Green Buildings Tune-Ups Program announced in the 2008/09 State Budget.

Specifically, the Property Council asks the South Australian Government to:

A Strategy for Transforming Market BehaviourThe Property Council proposes the following package of measures: First: Develop voluntary interim performance targets across

all eco efficiency categories – energy/greenhouse abatement, water, waste and indoor environmental quality – to enable to achievement of targets in South Australia’s Strategic Plan.

Second: Provide $300,000 over two years to the Property Council to enhance the Government/Property Council Green Buildings Tune-Ups Program, specifically to develop and disseminate information such as a tune-up and retro-greening toolkit and help to build industry capacity.

Fourth: Commit to reducing environmental red tape. Fifth: Establish a state demonstration program that makes the

business case for green development/buildings and promotes innovative practices.

Sixth: Develop a One Stop Shop for all water, waste and energy reduction strategies, directing building owners to sources of financial and non-financial incentives.

- 10 -

.........

2.2 The Second Plank: Green Depreciation

The quickest way to achieve deep emissions cuts is to improve energy efficiency in existing buildings.

There are 330 million square metres of existing non-residential property stock in Australia.

Accelerated ‘green’ depreciation would fast track efforts to rebuild existing stock to higher environmental standards.

Green depreciation would cost $2.3 billion over 10 years, starting with a $90 million annual outlay.

Independent research indicates the investment would save 203 Mt of carbon over the first decade. That equates to removing 6.4 million cars from our roads every year.4

What is Green Depreciation?

Green depreciation is accelerated depreciation for buildings that meet an environmental standard.

The standard, to be set by government, would be based on scientific and engineering advice.

Australian governments have traditionally used accelerated depreciation to stimulate the economy.

In the 1992 One Nation package, then Prime Minister Paul Keating introduced an accelerated depreciation scheme to stimulate the economy:

“The Government has decided to provide substantial acceleration of depreciation deductions for plant and equipment for tax purposes….The tax preference….will encourage [domestic plant and equipment] investment relative to alternatives, including foreign investment abroad…The acceleration of depreciation for plant and equipment will be focussed particularly on assets with long lives.”

Paul Keating, Prime MinisterOne Nation, 26 February 1992, pp71-72

In the current economic climate, an accelerated depreciation scheme for green building retrofits will help to stimulate the economy and deliver sustainability dividends.

The Property Council proposes accelerated depreciation be used to stimulate a massive investment in improved environmental performance.

4 Green Depreciation: A Preliminary Analysis, Centre for International Economics, (November, 2007)

- 11 -

.........

How Would Green Depreciation Work?

Green depreciation involves the provision of accelerated depreciation allowances for building investments that install specific energy efficient fittings, fixtures and fabric or raise the overall energy performance of the building to a predetermined standard.

It would play a key role in overcoming timing gap problems, allowing investors to defer tax payments in exchange for bringing forward energy efficiency and GHG reductions.

Accelerated depreciation would establish an important foundation for a Green New Deal program recently announced by a coalition including the ACF, the ACTU, ACOSS and the Property Council.

The SA Government should advocate in favour of Accelerated Green Depreciation with its COAG counterparts.

Specifically, the Property Council asks the South Australian Government to:

Green Depreciation – Recommendation:

First: Support the introduction of accelerated depreciation for buildings that retrofit (retro-green) to meet higher environmental standards.

Sources:

Capitalising on the Building Sector’s Potential to Lessen the Cost of a Broad Based GHG Emissions Cut, Centre for International Economics (September, 2007)

Green Depreciation: A Preliminary Analysis, Centre for International Economics (November, 2007)

The Second Plank – Building A Low Carbon Economy With Energy Efficient Buildings, Centre for International Economics for ASBEC (August, 2008)

Towards a Green New Deal: Economic stimulus and policy action for the double crunch, Australian Conservation Foundation, Australian Council of Social Services, The Climate Institute, Property Council of Australia, Australian Council of Trade Unions, Australian Green Infrastructure Council, Australian Institute of Superannuation Trustees (December, 2008)

- 12 -

.........

2.3 Delivering Water Use Reductions

As the community and the Government recognises, one the State’s biggest challenge is future supplies of potable water.The Property Council supports the Government’s efforts to reduce potable water use through desalination, stormwater harvesting, and the recycled water pipeline to the Adelaide Parklands. However, more must be done to reduce usage of potable water for non-essential purposes.The greatest economic barriers to improved water efficiency in non-residential buildings is the annual supply charge for connection to mains water. The low cost of water mean there is little or no incentive to cut usage levels as the significant cost for non-residential users is the annual supply charge.The implication of this is that there is no incentive for reducing water usage in non-residential properties.

Case Study on World Park One

World Park One is a new campus-style development just outside of the Adelaide CBD. The development is designed to be water neutral, delivering outcomes for the community as a whole. However, despite this, the owners and tenants will continue to pay about $120,000 per annum in connection charges (based on a property value of $150 million).

The State and Federal Governments are making a major investment in the Glenelg to Adelaide Parklands Recycled Water Pipeline to provide water for the parklands. For a minimal additional investment, a spur of this pipeline could be run through the CBD to allow commercial buildings to plumb in cooling towers and other non-potable uses to this water source. This adds an economic benefit to the project and clearly has the potential to deliver significant water savings.Specifically, the Property Council asks the South Australian Government to:

Delivering reduced Water UseThe Property Council proposes the following package of measures: First: Cut water connection charges by 50 per cent for

commercial properties that deliver significant reductions in potable water use.

Second: Finance the extension of the recycled water pipeline through the CBD.

Attachment:1. Recycled Water Pipeline Position Paper (April 2008)

- 13 -

.........

3. Community DividendsThis chapter provides a recommendation on:

corporate responsibility.

Fiscal Implications – 2009 State Budget:

Corporate responsibility – no fiscal implications.

3.1 Corporate ResponsibilityThe Property Council has developed a corporate responsibility (CR) reporting template for the property sector.

This is part of a broader Code of Practice for the property and capital markets communities.

The template takes the form of a voluntary industry standard.

It will integrate with the de facto global standard developed by the Global Reporting Initiative and conforms to the United Nations Global Compact’s 10 principles of social responsibility.

The template is also consistent with the Dow Jones Sustainability Index and the FTSE For Good reporting scheme.

While there are no fiscal implications for the 2009 State Budget, the voluntary standard is an alternative to any mandated reporting requirement.

Specifically, the Property Council asks the South Australian Government to:

Corporate Responsibility – Recommendation:

Note the existence of the Property Council’s draft template for corporate responsibility reporting and the Code of Conduct for the property investment and development sectors.

Sources:

A Guide to Corporate Responsibility Reporting in the Property Sector, Version 2.1, Property Council of Australia (2009, forthcoming)

Draft Code of Practice, Property Council of Australia (2009, forthcoming)

- 15 -

.........

4. Governing SmarterThree issues are addressed in this chapter:

a methodological approach to modernising metropolitan governance;

delivering improved local governance.

Fiscal Implications – 2009 State Budget:

Modernising metropolitan governance – no fiscal implications.

Modernising local governance – minimal fiscal impact in 2009.

South Australia’s Strategic Plan Targets:T1.1, T1.2, T1.5, T1.6, T1.7, T1.8, T.19, T1.10, T1.11, T1.12, T1.14, T1.16, T2.21, T 5.4, T5.5

- 16 -

.........

4.1 Modernising Metropolitan Governance

Toward an Australian set of leading practice urban governance principles“…cities will face growing social exclusion and increasing financial pressure in a more complex, fragmented institutional environment.

“Cities will need to be more creative, more institutionally innovative…the challenge of devising effective models of governance will become increasingly urgent.”

Michael Parkinson “Developing Competitive and Cohesive European Cities”, European Institute for Public Affairs, 2002

The early 1990s witnessed a revival of programs that aimed to improve competitiveness and social opportunity in cities.

A decade later, many policy makers concluded that urban strategies often failed in the face of outmoded governance arrangements.

Causes of Urban Governance Failure

The 2001 OECD report Cities for Citizens: Improving Governance in Metropolitan Areas, identified three main failures of urban governance:

the fragmentation of administrative jurisdictions within metro areas;

the financial/fiscal strain faced by local authorities at a time when major investment in infrastructure is required; and

the absence of transparent, accountable decision-making frameworks at the local level.

The OECD encouraged its members to develop governance models that addressed these shortcomings.

Modern Governance Principles

More recently, the United Nations5 identified seven principles of leading practice urban governance:

sustainability in all dimensions of urban development;

subsidiarity of authority and resources to the appropriate level;

equity of access to decision-making processes and the basic necessities of urban life;

5 Global Campaign on Urban Governance (Concept Paper), UN-HABITAT (2002)

- 17 -

......... efficiency in the delivery of public services and in promoting local

economic development;

transparency and accountability of decision makers and all stakeholders;

civic engagement and citizenship; and,

security of individuals and their living environment

These principles were employed to develop a performance measure called the “urban governance index”.

There are many other menus of urban governance principles, all of which cover similar territory.

Metropolitan Governance Principles for Australia

To kick start debate, the following metropolitan governance principles are proposed:

1. Commit to strategic sustainability that aims to maximise multiple economic, social, ecological and governance dividends.

2. Increased competitiveness based on long-term investments in social development and economic infrastructure.

3. Place-shaping that increases local choice, diversity and opportunity within broader regional/national contexts.

4. Greater transparency, accountability and probity that enhances trust in metropolitan government.

5. Greater fiscal capacity to capitalise city services and investment programs adequately, while minimising deadweight taxes/charges.

6. Improved equity and access to opportunity across the community.

7. Greater subsidiarity, participation and civic engagement that refreshes civic mandates.

8. Greater efficiency, coordination and integration of public service delivery.

9. A commitment to innovation and inspiring leadership that continuously improves city governments’ capacity to meet evolving community needs.

10. Rational and coherent spatial boundaries that establish a logical nexus between the responsibilities of city government and the communities they serve.

Specifically, the Property Council asks the South Australian Government to:

First: Adopt the Property Council’s proposed Metropolitan Governance Principles and work with local government to deliver.

Sources:

Modernising Metropolitan Governance: Toward an Australian set of leading practice urban governance principles, Version 2.0, Property Council of Australia (December, 2008)

Developing Competitive and Cohesive European Cities”, Michael Parkinson European Institute for Public Affairs (2002)

Cities for Citizens: Improving Governance in Metropolitan Areas, Organisation for Economic Co-operation and Development (2001)

Global Campaign on Urban Governance (Concept Paper), UN-HABITAT (2002)

Cities Strategy, Version 3.0 Property Council of Australia (October, 2008) (See Appendix 2)

- 19 -

.........

4.2 Modernising Local Governance

In addition to Federal-State reforms that are currently being negotiated through COAG, local government also needs to be modernised.

The recommendations outlined below provide a clear pathway to improved local governance that will benefit all levels of government, and more importantly, the community.

Specifically, the Property Council asks the South Australian Government to:

Modernising Local Governance - Recommendations:

First: Help to reform and improve the performance of local government with the following programs:

- institute an inquiry into the optimal size of local councils that balances democratic representation, efficient delivery of services, environmental catchments, funding powers and ability to attract (and retain) professional staff;

- support a constitutional commission to develop a model for establishing councils as local parliaments. A key feature of the model would be the application of the separation of powers doctrine to key local government activities;

- require all councils to develop local action plans based on key performance indicators (KPIs), similar to South Australia’s Strategic Plan. All councils should develop 25-year infrastructure plans;

- require councillors who sit on planning committees to undertake professional development provided by a registered training provider;

- offer incentive payments to, and abolish rate capping for, local governments that undertake reforms; and

- establish a fiscal responsibility protocol for local government.

- 20 -

.........

5. Fairer TaxesThis chapter addresses the need for local tax reform in the areas of:

A broad tax review Stamp duty Land tax

The State Government adjusted Payroll Tax rates in the last two State Budgets and while times are tough, it is now time for property tax reform, reforms that will deliver the greatest economic benefit for every South Australia.The Federal Government has instigated the Henry Review of Taxation that will seek to deliver ‘root and branch’ reform to taxation. The State Government must work collaboratively with this review to maximise the economic benefit for South Australia.

Fiscal Implications – 2009 State Budget:Tax review – minimal fiscal impact in year one.Land Tax – about $80 million in year one.Stamp Duty on non-residential conveyances – $250 million in year one.Unit Trust and CRE Rationalisation – minimal fiscal impact.

As South Australia continues to gear up for the opportunities in the mining and defence industries, it is in competition with other states and jurisdictions for investment, jobs and population. Despite commitments within South Australia’s Strategic Plan, the State seriously lags in instituting a competitive taxation regime that balances fairness, social and economic needs and the demands of a growing economy. Particularly in these challenging times, our tax system must be designed to attract skills and investment, not repel them.The recent global economic turmoil has exposed the risk to the State’s finances of overly relying on the property market, which can fluctuate dramatically. Additionally, the recent increases in land valuations have significantly increased the land tax bills of mums and dads, businesses and investors. These increases have resulted in employees being laid off, increasing prices of goods and services and has threatened the future of the economic prosperity of South Australia. Equally, the increase in land tax bills is working counter to many initiatives aimes at improving environmental efficiency in the built environment.The Property Council recommends that South Australia initiate a taxation review and implement a broad tax review as a matter of urgency.

Specifically, the Property Council asks the South Australian Government to undertake:

A broad tax review – Recommendations:First: Immediately undertake a broad review of South Australia’s

taxation base with a view to aligning with the Federal Henry Review of Taxation.

Second: Examine and remove financial disincentives to skilled employees and investors considering South Australia as an employment and investment destination.

Third: Ensure that existing and proposed tax measures do not constrain the ability of the property industry to adjust to environmental demands.

- 22 -

.........

5.2 Land TaxLand tax in South Australia is the most uncompetitive State tax, impacting on South Australian businesses and private land investors.Almost every other State has reformed their land tax regimes over the last couple of years, leaving South Australia in a precarious competitive situation. As can be seen from the graph below, the land tax bill on a property worth $25 million in South Australia is about $283,000 more than the same investment scenario in Tasmania, the next highest jurisdiction, about $435,000 more than in Western Australia and around $500,000 more than in Queensland. This is clearly uncompetitive and urgent action is required.

Land tax paid by State (commercial)

$0

$100,000

$200,000

$300,000

$400,000

$500,000

$600,000

$700,000

$800,000

$900,000

$2,500,000 $5,000,000 $10,000,000 $25,000,000

unimproved land value

tax

paid

Vic NSW QLD WA* SA TAS ACT

The two key concerns in South Australia remain the significant valuation increases in 2008/09 and the unchanged rates and thresholds in the face of recent significant valuation increases. It is simply inconceivable with property values being what they are and the absence of purchasers that the base threshold in South Australia is $110,000 and the maximum $1 million. The Property Council believes that in order to alleviate the severe uncompetitiveness in the system, the State Government must immediately freeze all property valuations at last year’s value and further to this, increase the base threshold to $250,000, the maximum threshold to $2.5 million at a maximum rate of 2.5c per dollar in this year’s State Budget. Recently the Queensland Government put a freeze on land tax valuations to provide desperately needed relief for small businesses and investors. The situation in South Australia is no different with the significant increases in land valuations severly hurting small businesses in the State. The State Government must provide immediate relief for these businesses by freezing property values at the previous year’s value.A report prepared for the Property Council by Hudson Howells indicates that the proposal to increase the thresholds and lower the rates is estimated to cost $80 million in year one, and would deliver an additional 1,650 jobs within the State. It would also increase state incomes in real terms by 0.23 per cent as a result of new build activity.

- 23 -

.........This clearly demonstrates significant benefits of reducing land tax through increased investment, increased jobs and increased state incomes.

Specifically, the Property Council asks the South Australian Government to:

Land Tax – Recommendations: First: Immediately freeze property valuation increases to provide

relief to businesses and investors in South Australia.Second: Increase the base threshold to $250,000 and the maximum

threshold to $2.5 million at a rate of 2.5c per dollar.

Attachments:2. A Cost Benefit Evaluation of Reducing Taxes on Property in South

Australia (Hudson Howell) 2008.

- 24 -

.........

5.3 Stamp Duty

Stamp duty on non-residential conveyances continues to impact on investment in South Australia.This is the most inefficient state tax and has potential to yield the greatest economic benefit from reduction or abolition than any other state tax. Economic modelling commissioned by the Property Council indicates that the cost of this reform is in the order of $250m per year. The principal benefits of this reform are the creation of an estimated 6,900 jobs within the state and an increase of state incomes, in real terms, by 0.9 per cent. This is clearly the most beneficial property tax reform and should be adopted immediately by the Government. The modeled growth stems from the instantaneous creation of an improved business environment.The advantage of this reform is that it will make South Australia the first and only jurisdiction to abolish this tax – thereby making investment in this state far more attractive and giving a notable point of difference for investors.

Specifically, the Property Council asks the South Australian Government to:

Stamp Duty on Non-Residential Conveyances– Recommendations: First: Immediately abolish Stamp Duty on Non Residential

Conveyances.

Attachments:2. A Cost Benefit Evaluation of Reducing Taxes on Property in South

Australia (Hudson Howell) 2008.

- 25 -

.........

5.4 Rationalisation Program

As the State Government is already aware, the Property Council has been undertaking a program to rationalise land rich stamp duty definitions and provisions across Australia. Our recommendations have been adopted in Western Australia and are being favourably considered in other jurisdictions.Stamp duty on property is collected by all states however, the definitions and provisions applying stamp duty are different in each jurisdiction. The delivery of this program will encourage domestic property investment and improve international competitiveness.The lack of consistency between jurisdictions creates unnecessary complexity for property owners who want to invest across multiple jurisdictions or from overseas. These investors incur additional legal and administrative costs to comply with different state taxes and the movement of capital into and across Australia is made more difficult by the complex variation in state stamp duty regimes. It makes investment in some jurisdictions unattractive and uncompetitive. This inhibits capital investment in Australian property. Copies of the Rationalisation Models and Gap Analyses are attached for detailed consideration.

Specifically, the Property Council asks the South Australian Government to:

Rationalisation Program – Recommendations: First: Immediately adopt and implement the rationalisation

models.

Attachments:3. Unit Trust Rationalisation Model

4. Unit Trust Gap Analysis

5. Unit Trust CRE Rationalisation Model

6. Unit Trust CRE Gap Analysis

- 26 -

.........

ContactPlease contact the following about any aspect of this submission:

Nathan PaineExecutive Director – South AustraliaProperty Council of Australia

142 Gawler Place Adelaide SA 5000t. 08 8236 0900m. 0448 445 177e. [email protected]

Attachment 1:Recycled Water Pipeline Position Paper

- 28 -

.........Recommendations

1. Immediately support the proposed extension of the Glenelg-City Pipeline.2. Provide funding for the extension of the pipeline. 3. Establish a Working Group to clarify the route of the pipeline and resolve any

technical issues.4. Deliver a publicity campaign highlighting the benefits of the project. 5. Charge a water learning hub with raising awareness levels around issues of

recycled water.

Support for these recommendations will assist the State Government in achieving the following targets in South Australia’s Strategic Plan: T1.1, T1.10, T1.22, T3.7, T3.9, T3.10 and T3.11.

About the Property Council of Australia

The Property Council of Australia is the nation’s chief advocate for the property investment, development and property services sector. It champions members' interests by engaging governments on key public policy issues, as well as creating a more informed and connected marketplace.

Our members help shape, build and finance our cities. These organisations have a long-term interest in the future of Australia’s urban areas. They include the bulk of the State's investors in office towers, shopping centres, industrial parks, tourism accommodation and residential developments.

The South Australian Division represents members with interest in more than $33 billion of property investment, of which, nearly $5 billion is invested by superannuation funds in South Australian property. More than 500,000 South Australians now have a stake in these investments through their superannuation, life insurance, managed fund property trusts, syndicates and direct ownership investments.

- 29 -

.........Our proposal

The Property Council of Australia (SA Division) recognises that the property industry is in a unique position to improve the State’s environmental performance. The Property Council has been examining opportunities arising from the proposed recycled water pipeline from the Glenelg treatment works to the Adelaide parklands for irrigation purposes.

The Property Council believes there is potential to extend this water supply into the CBD for use in cooling towers of commercial buildings. There is some urgency attached to this proposal as supplying additional buildings could necessitate a larger diameter pipe than currently proposed. Changing the pipe size would have minor fiscal and logistical impact on the project as it stands, especially when compared with the potential benefits.

It should be noted that this proposal holds national significance. The proposed use of highly treated waste water in cooling towers has not been investigated interstate, positioning South Australia as a pioneer in this field.

Background

The State and Federal Governments have committed to building a new recycled water supply pipeline from Glenelg to the Adelaide parklands to provide non-potable water for the irrigation purposes. The Property Council supports this initiative as amenable public space is crucial to the health of our community and the parklands are a key natural attribute of the city. The current proposal is to install a pipeline along ANZAC Highway and complete a ring around the city. In an effort to reduce pressures on Adelaide’s potable water supply it is intended to use highly treated waste water as the source water for this irrigation project.

The owners of the new SA Water Building in Victoria Square (VS1), in their endeavours to develop a water-efficient building, have already reached an agreement with SA Water to run an extension of the pipeline from the parklands to VS1.

- 30 -

.........The Property Council believes that this program can be easily and cheaply extended to include all commercial buildings. Conversations with SA Water and the South Australian Department of Health have indicated that this proposal is achievable. As noted earlier, a larger pipe size may be required to transfer the larger volumes of water needed. In addition, as ANZAC highway is a potential development corridor, the pipeline design should allow for other developments along the route to ‘bolt on’ to the recycled water supply. In any event it is less costly to over-engineer the pipe before it is installed than to replace it to meet increased demand in years to come.

Discussion

The Property Council has held extensive discussions with SA Water and the South Australian Department of Health and has determined that significant savings of potable water can be made by extending the proposed pipeline into the CBD and running supplies into the cooling towers of major buildings.

Initial preliminary calculations have revealed that running recycled water into commercial building cooling towers could save in the realm of one billion litres of potable water annually, enough water to fill 4,000 Olympic sized swimming pools or alternatively supply the needs of all the flats, units and apartments in the City of Holdfast Bay council area (based on usage of 250 kilolitres per home; Australian Bureau of Statistics, Census Data, 2006 Community Profiles).

Cooling towers are a typical air conditioning component of buildings world-wide. And while the property industry in South Australia is extremely proactive in making new buildings as environmentally friendly as possible, there are limitations to greening the existing built environment. For example, while new buildings can be plumbed to run recycled water to toilets and cooling towers, this is more complex to implement in existing buildings.

Running a dedicated feed to an existing roof-mounted cooling tower is one immediately feasible means of using recycled water in existing buildings. As cooling towers are one of the biggest users of water in a commercial building, they present an effective use of this new water supply in a way that also contributes to economic development.

- 31 -

.........As mentioned earlier, this opportunity has already been identified by the owners of Adelaide’s first – and Australia’s highest design rated - Six Star Green Star Building, the VS1 building scheduled for completion in the final quarter of 2008. Recycled water from this supply will be used for the building’s cooling towers and toilet flushing systems.

The Property Council, through its membership base, is aware of many new developments which could promptly connect into the proposed scheme if the opportunity existed. It is therefore imperative that the pipeline be extended throughout the core of the CBD.

Financial issues

The current proposed pipeline from Glenelg to Adelaide is expected to cost $30 million and the additional treatment plant to be developed as part of the project another $30 million. This is a significant outlay and it makes sense to maximise the State’s environmental return for this investment. The Property Council estimates the government’s additional contribution for the extension of the project through the CBD to be in the order of $5 million. This is based on a generous costing of $500 per metre cost for additional in-ground pipe work - an insignificant outlay when considering the benefit to the State and the River Murray in saving one billion litres of potable water a year.

Costs that might be associated with this project are: building alteration and maintenance costs; the cost of increasing the size of the pipe work already under consideration;

and any requirements to expand the capacity of water treatment facilities.

Compared with these relatively low costs the benefits are significant: savings of up to one billion litres of potable water per year; substantially increased use of recycled water; bolstering South Australia’s water security credentials; positive messaging to the public around water reuse and recycling; and asserting South Australia’s leadership in innovative water security policy.

- 32 -

.........Implementation

The Property Council has discussed a possible route for the pipeline extension with the SA Water’s Project Manager for the current scheme. This proposal runs the extension past a concentration of major commercial buildings to maximise usage of this recycled water. A draft map is attached but the Property Council would welcome the opportunity to discuss the practicalities of implementation with the Project team.

Timing

Although the Glenelg Pipeline scheme has not yet entered construction phase, it is imperative the issues of main pipe size and treatment plant capacity are reviewed urgently in the light of the proposition to extend the pipeline. The pipe size might need to be doubled or even tripled to account for significantly increased volumes of water. To do this at the planning stage is relatively inexpensive. Enhancing public awareness of recycled water use

The successful achievement of this project would be a milestone in the South Australian Government’s Waterproofing Adelaide strategy to secure a reliable potable water supply. The Property Council is also an Alliance Partner in South Australia’s Strategic Plan and, as such, the South Australian Government and the Property Council should cooperate in developing and implementing a communications strategy that shows South Australia as an exemplar in major water-saving projects and simultaneously promotes the use of recycled water to the public.

Ongoing public education on these matters is vital. Practical initiatives such as these can contribute significantly to the increased usage of recycled water but public awareness of recycled water is very limited. In these times of extended drought it is imperative that these awareness levels are raised substantially to facilitate ever-greater uptake of recycled water.

The Property Council would therefore also advocate that the South Australian Government charge the “water learning hub” – currently in development – with increasing public understanding of the issues of recycled water and the importance of its use.

The hub should act as a single clearing house for policy ideas and messages around recycled water to ensure that the public receives clear and reliable messages that encourage the uptake of recycled water and water reuse technology.

- 33 -

.........

Recommendations

1. Immediately support the proposed extension of the Glenelg-City Pipeline.2. Provide funding for the extension of the pipeline. 3. Establish a Working Group to clarify the route of the pipeline and resolve any

technical issues.4. Deliver a publicity campaign highlighting the benefits of the project. 5. Charge a water learning hub with raising awareness levels around issues of

recycled water.

- 34 -

.........Proposed Pipeline Extension

- 35 -

.........

Attachment 2:Reducing Taxes on Property Cost Benefit Analysis of Tax Reform A Report by The Property Council of Australia (SA Division)

9th February 2008

This paper has been prepared under the auspices of the Property Council of Australia, with the assistance of Hudson Howells Pty Ltd. . This study, while embodying the best efforts of the investigators, is but an expression of the issues considered most relevant, and neither the individuals nor the associated organisations can be held responsible for any consequences that ensue from the use of the information herein.

- 36 -

.........

Table of ContentsEXECUTIVE SUMMARY....................................................................37INTRODUCTION.............................................................................37

TAXATION SYSTEMS – THE CONTEXT...............................................37THE AUSTRALIAN TAXATION SYSTEM....................................................................37REGIONAL TAXATION.........................................................................................37

State Taxation in South Australia.........................................................37Local Government Revenues...............................................................37

A THEORETICAL CONTEXT – A VIEW ON TAX....................................37CORE TAXATION PRINCIPLES...............................................................................37PROPERTY TAX – THE THEORETICAL CONTEXT........................................................37

LITERATURE REVIEW......................................................................37AXING THE ALCABALA: A PROGRAM FOR A 21ST CENTURY STATE TAX SYSTEM................37HENDY-WARBURTON INTERNATIONAL COMPARISON OF AUSTRALIA’S TAXES.................37REAL ESTATE INSTITUTE....................................................................................37PROPERTY COUNCIL..........................................................................................37OTHER RESEARCH............................................................................................37

A DETAILED DESCRIPTION OF PROPERTY TAX PARAMETERS.............37LAND TAX:......................................................................................................37STAMP DUTIES.................................................................................................37

Stamp Duty on Transfer of Real Property (Land).................................37Stamp Duty on Mortgages...................................................................37

Water Supply Charges.........................................................................37Council Rates.......................................................................................37

TAX COMPARISONS...........................................................................................37Bracket Creep - Tax implications over time.........................................37Interstate Competitiveness..................................................................37

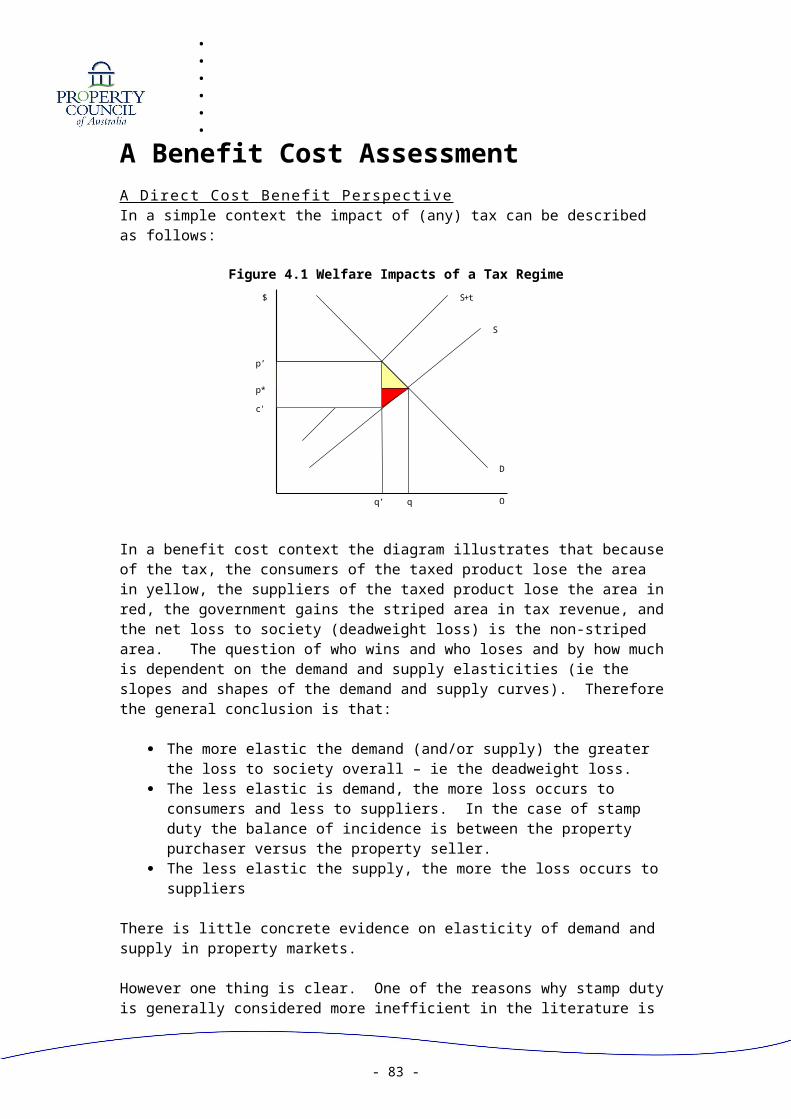

A BENEFIT COST ASSESSMENT.......................................................37A DIRECT COST BENEFIT PERSPECTIVE.................................................................37

Benefit/cost analysis of abolishing Stamp Duty on Non-Residential Conveyances.......................................................................................37Benefit/cost analysis of abolishing Stamp Duty on new homes...........37Benefit/cost analysis of land tax reform scenarios:..............................37A flat rate of 1.7c/$ at a threshold of $250,000...................................37

A BROADER BENEFIT COST PERSPECTIVE..............................................................37CONCLUSIONS...............................................................................37

- 37 -

.........

Executive SummaryThe objectives of this project were to undertake a

Benefit/Cost analysis of abolishing Stamp Duty on Non-Residential Conveyances.

Benefit/Cost analysis of abolishing Stamp Duty on new homes. Benefit/Cost analysis of the following land tax reform scenarios:

Raising the base threshold from $110,000 to $250,000 and raising the maximum threshold from $1m to $2.5m with a top rate of 2.5c/$

A flat rate of 1.7c/$ at a threshold of $250,000.

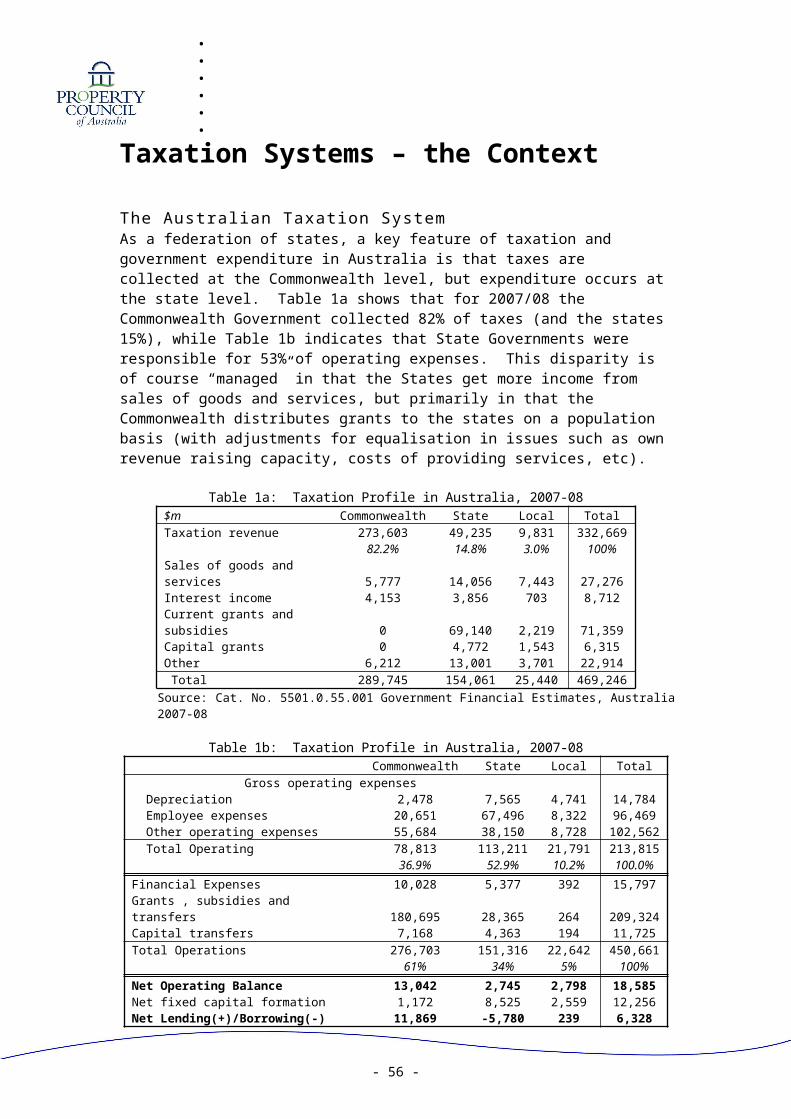

To set the context of the analysis we note that: State Governments raise only 15% of taxes raised in Australia, but

undertake 53% of operational expenditure and 37% of capital expenditure. State Governments are therefore heavily dependent on grants from the Commonwealth – and own taxation revenue is a critical part of economic management.

Commonwealth Government budgets are in significant surplus, while State Governments in aggregate require external financing.

There has been extensive growth in the contribution of property tax to State Government’s own purpose revenue. Property tax has grown at 9.5% per annum over the last 5 years, while State Government taxation has grown by 7.3% per annum.

From a South Australian perspective the evidence suggests that On average, the SA Government is at the upper end of reliance on

property tax compared with other states, both in percentage terms (of GSP), and in relative impact on property prices – particularly higher value properties (note this may in large part be due to the smaller number and proportion of higher valued properties in the state. In summary - property taxes amount to 39.5% of the state government tax take, and specifically conveyancing taxes make up 21%.

Therefore a benefit/cost analysis of property tax reductions must recognise that the State Government is limited in reducing property tax per se, they must either persuade the Commonwealth Government to provide a proportion of their surpluses to the States, reduce expenditures, or modernise the State Taxation regime. While the need to do this is recognised, it is beyond the scope of this paper to make these comparisons. However it is noted that the off-setting benefits of reductions in property tax will ameliorate the direct revenue impact.

- 38 -

.........While no tax is “desirable”, the theory gives the following principles for selecting the “best taxes”:

Equity in burden distribution –there should be both horizontal and vertical equity – in terms of those who can afford to pay the tax.

Efficiency in resource use – the tax should not distort production and consumption decisions significantly – and this is best achieved when demand for product is relatively inelastic.

Consistency re goals of macro policy – where macroeconomic policy is ensuring stability in business cycles and encouraging growth.

Ease of administration

The literature and other analyses critically suggest that stamp duties on conveyancing are very inefficient taxes, while land tax is a fairly inefficient tax. On the other hand, state government taxes that are considered more efficient include payroll tax and gambling taxes. But we note there is also significant opposition to these taxes from a political perspective.A literature review makes the point that Australia is a low-tax country. Australia’s overall tax burden (31.6 per cent), measured as the tax to GDP ratio, is the eighth lowest of the 30-member OECD countries. Australia’s mix of direct and indirect taxation is in line with other OECD countries, although the composition differs. Australia’s reliance on property and transaction taxes is the seventh highest of the OECD, but its tax burden from taxes on immovable property is below the unweighted average of the OECD-10, while Australia has the highest financial and capital transaction burden (which includes taxes such as stamp duties on conveyances).Therefore the conclusion to be reached is that Australia should reorient its tax system away from stamp duties on conveyances and taxes on fixed property (land tax), and replace them with other taxation bases.The first step in undertaking a benefit/cost evaluation of the suggested policy changes is to estimate the revenue change associated with the policy shift. There is no robust data publicly or easily available to model these changes (the data required is the number of “transactions” AND the distribution of values involved). A further unknown is that there will be price and value shifts as a consequence of the policy changes, which are dependent on the elasticity of demand and supply. However the result is modelled (indicatively at this point) using simple normal distributions around average values.On the basis of this indicative modelling:

Abolishing Stamp Duty on Non-Residential Conveyances would reduce the taxation take of the state government by an estimated $250 million (4% of total taxation).

Abolishing Stamp Duty on new homes would reduce the taxation take by $100 million (around 2% of total revenue).

- 39 -

......... In terms of land tax:

Raising the base threshold from $110,000 to $250,000 and raising the maximum threshold from $1m to $2.5m with a top rate of 2.5c/$ would reduce taxation revenues by $80 million (around 2%). This reduction is made up of: $15 million in private residential rental property. $9 million in public rental property. $54 million in commercial property (both public and private).

A flat rate of 1.7c/$ at a threshold of $250,000 would reduce taxation revenues by $72 million. This reduction is made up of: Increase in $10 million in private residential rental property. Increase in $9 million in public rental property. A $90 million benefit in commercial property (both public and

private).

Reductions in taxation revenue do not tell us fully about the economic or benefit cost improvements that will result from the taxation fall. The impact, and who it falls on is a consequence of supply and demand factors – the elasticity of demand and supply. Put simply, the more price sensitive the demand for a product, the more distorting is a given tax change. The second factor of course is also how big the tax is in relation to the taxation base. The conclusion of the literature is that property taxes are amongst the most distorting of the state government taxation methods – a consequence of both of these points.

So what are the implications of these reductions in taxation revenue from a benefit cost perspective:

Abolishing Stamp Duty on Non-Residential Conveyances would see the prime benefit being for users and suppliers of commercial property. The implication would be to reduce costs for business, and therefore increase the relative competitiveness of firms/industries facing external competition, and reduce costs for firms supplying the local market with limited competition.

Abolishing Stamp Duty on new homes would improve new house affordability but not directly improve affordability of established homes. There are some 28,000 sales of established homes per year, and 8,000 new home builds. Stamp duty will be paid on the land in some cases, but in speculative build will be paid on both land and property. While having some effect on improving housing affordability, it complicates the relationship between the new and established housing market – producing something of a bias or stimulus for new home builds. But the implications of the way this affects the market need to be considered.

Reducing land tax – provides a gain to the private rental market, and for commercial property. The gains for commercial property are as discussed above. The gains for the rental market again provide for some distortions between interacting markets, but in the context of existing distortions, and further given the current tightness in the rental market.

One of the issues that will have led to the distorting effects being at the level noted above is the structure of the tax base. In the same way that

- 40 -

.........bracket creep has led to increased takes of individual income tax revenue, bracket creep is an issue in property tax as well – meaning that the tax revenue will grow simply because of inflation. The analysis suggests that over the last 8 years, average property prices have grown at 11% per year, but there have only been 2 adjustments of the tax rate parameters, and therefore the tax on a median value property is 155% more than it was in 2000 in real terms.

The above represents outcomes from a direct and tangible benefit context. In addition, outcomes need to consider indirect and intangible benefits and costs. The major source of indirect impact is in terms of impact on industry competitiveness and therefore economic activity.

In the case of stamp duty on owner occupied residences, the tax represents a decline in real income over what would otherwise be the case.

In the case of land tax and stamp duty on rental residences, the tax represents a decline in real income for renters, and a shortage of supply from the perspective of the market.

In the case of land tax and stamp duty on commercial property, the tax represents an increased cost of doing business, and therefore produces a decrease in competitiveness.

In summary, it is estimated that: A $100 million decline in tax payments on residential property will

create of the order of 700 jobs in the state and increase real incomes (GDP) by 0.12%.

A $100 million decline in tax payments on commercial property will create of the order of 2,800 jobs in the state and increase real incomes by 0.38%.

Therefore for the policy changes assessed in this paper: Abolishing Stamp Duty on Non-Residential Conveyances would

create an estimated 6,900 jobs within the state, and increase state incomes in real terms by 0.9%.

Abolishing Stamp Duty on new homes would create an estimated 670 jobs within the state, and increase state incomes in real terms by 0.1%.

In terms of land tax: o Raising the base threshold from $110,000 to