Big Data Analytics in the Financial Statement Audit A critical examination of the possible value to the auditors Bachelor thesis Accountancy & Control Ivar van den Boogert 10562079 29 th of June 2016, final draft Professor Brendan O’Dwyer University of Amsterdam, Amsterdam Business School

Transcript

Big Data Analytics in the Financial Statement Audit A critical examination of the possible value to the auditors

Bachelor thesis Accountancy & Control

Ivar van den Boogert

10562079 29th of June 2016, final draft Professor Brendan O’Dwyer

University of Amsterdam, Amsterdam Business School

Statement of Originality

This document is written by Ivar van den Boogert who declares to take full responsibility for the contents of this document.

I declare that the text and the work presented in this document is original and that no sources other than those mentioned in the text and its references have been used in creating it.

The Faculty of Economics and Business is responsible solely for the supervision of completion of the work, not for the contents.

Abstract

Currently the position of the financial statement auditor is under pressure, several reports

such as the Green Paper of 2010 pressure for change in the audit profession. In this thesis I

will answer the question whether big data analytics could be beneficial to the auditors, by

examining in which stages of the audit big data analytics could improve the audit in terms of

efficiency, cost reduction and quality. Big data analytics is a hype of the last five years, and

while interesting applications have found in several fields, there does not yet exist an

application for the assurance service industry. My contribution to the existing literature is

twofold. First of all I synthesize existing literature concerning big data in a fashion suitable to

the auditing profession. Second, in the Big Data forum of the journal Accounting Horizons

(2015) authors were highly positive about the possibilities of big data analytics in the

financial statement audit; however, the authors neglect to argue where the possible benefits

could be realized. In my thesis I will try to specify the areas where big data analytics could

indeed prove to be beneficial. I will answer this research question by performing a literature

review. The main finding is that, despite of the potential of big data analytics, the perceived

value for financial statement auditors is ambiguous in terms of efficiency and quality. Cost

reduction is most certainly not achieved at the moment.

Samenvatting

Momenteel staat de positie van de auditor ter discussie, zoals kan worden afgeleid van

onder meer het Groenboek 2010. De druk voor verandering is aanzienlijk hoger dan

voorheen, daarom onderzoek ik in deze thesis of big data analytics een waardevol

hulpmiddel kan zijn voor auditors in de financial statement audit. Big data is een hype waar

veel over wordt gespeculeerd en tevens zijn er interessante toepassingen waargenomen in

verschillende sectoren. Daarom wordt in deze thesis onderzocht, door middel van een

literatuurstudie, in hoeverre big data analytics waardevol is voor auditors in termen van

efficiëntere, goedkopere en kwalitatief betere audits. Mijn bijdrage aan de bestaande

literatuur is tweeledig. Ten eerste vat ik de bestaande literatuur met betrekking tot big data

samen, waarbij de toepassing op het accountantsberoep centraal staat. Ten tweede toets ik

de zeer positieve houding van auteurs die schreven in het forum Big Data van het journal

Accounting Horizons. De auteurs waren uitermate positief over de mogelijkheden van big

data analytics in de financial statement audit, maar beargumenteerden niet in welke fase(n)

van de audit deze potentiële waarde wordt gerealiseerd. Ik probeer dit in deze thesis wel te

specificeren. Uit mijn onderzoek blijkt dat het niet eenduidig is dat er efficiëntere en

kwalitatief betere audits worden gerealiseerd met big data analytics. Lagere kosten worden

hoogstwaarschijnlijk niet gerealiseerd.

Table of Contents

1. Introduction ................................................................................................................ 6 2 Overview of the theory ............................................................................................. 8 2.1 General context of auditing ......................................................................................... 8 2.2 Performing an audit ................................................................................................... 10 2.3 Big Data ........................................................................................................................... 11

3 How to assess the value of big data analytics for auditors ....................... 16 3.1 The Iron Triangle ......................................................................................................... 16 3.2 Audit Quality .............................................................................................................. 17 3.2.1 Audit input ............................................................................................................................... 17 3.2.2 Audit Process .......................................................................................................................... 18 3.2.3 Audit output ............................................................................................................................ 20

4 Examination of the possible value of big data analytics ............................. 22 4.1 Big Data Analytics and Efficiency ........................................................................... 22 4.2 Big Data Analytics and Audit quality .................................................................... 24 4.3 Potential challenges and hurdles ............................................................................ 28

The auditing profession has been under considerable pressure the last fifteen years, as can

be concluded from the Green Paper issued in 2010 and from the paper of Power (2003, p.

379). First, the major fraud committed by the management of Enron, which became known

in 2001, causing billion-‐dollar damage and the bankruptcy of Arthur & Anderson (Brickley,

2003, p. 1). Arthur & Anderson used to be one of the big 5 auditing firms, but after their

failure with regard to the Enron scandal became public knowledge bankruptcy followed

soon in 2002 according to Brickley (2003, p. 2).

Second, since the global financial crisis, users of financial statements and regulators

of the auditing profession have become more sceptical about the role that the auditor fulfils

in the economy (Green Paper, 2010, p. 6). During and after the peak of the recent financial

crisis many financial institutions went bankrupt without any warning from the auditors

(Green Paper, 2010, p. 9). The auditor has the obligation, since 1989, to evaluate the viability

of the auditee (entity being audited) for a reasonable time, which is outlined in the

Statements on Auditing Standards (SAS) No. 59 (AICPA, 2002). The financial crisis made it

evident that auditors were failing to fulfil this obligation. Consequently, several measures

have been put in place: for example in the United States, the Sarbanes-‐Oxley Act has been

implemented and in Europe the Green Paper 2010 has been issued.

Pressure on the audit profession is not only coming from regulatory bodies,

increased competition in the audit profession is another important factor. The margins on

financial statement audits are extremely tight, because the auditing market is highly

concentrated and regulatory bodies have introduced more competition by mandating firm

rotation (Knechel, 2007, p. 387; AICPA, 2013). In order to remain competitive and credible,

the auditing profession would therefore benefit from new cost-‐reducing and quality-‐

enhancing techniques in financial statement audits.

An important innovation in the business environment the last couple of years is Big

Data. A survey performed by Gartner (2015) showed that 75% of the responding companies

expected to invest or were already investing in big data and analytical tools that could be

used to process big data. In an earlier survey, also performed by Gartner (2012), it was

estimated that the total amount invested in big data would reach 232 billion dollar by 2016.

An example of the application of big data analytics is described by Zang, Yang and

Appelbaum where the researchers successfully predict the change of the Dow Jones

Industrial Average stock exchange, using the mood on Twitter as explanatory variable (2015,

p. 425). Another example comes from Walmart, the retail corporation used weather forecast

information to guide their advertising of flashlights (Dezyre, 2013). By successfully using

information about storms and tornado’s and anticipating on a higher demand for flashlights,

Walmart’s was able to sell more flashlights. More examples can be found in the medical and

the insurance industry.

As shown above, there seems to be a variety of possibilities for big data analytics in

the business environment. However, by my knowledge no successful application can as of

yet be found in the assurance service industry, or more specifically, within the auditing

profession. As mentioned earlier, the auditing profession is under pressure and new

techniques might bring some reprieve to the profession. Therefore, I will research whether

big data analytics could be such a technique, by answering the question whether big data

analytics is beneficial for financial statement auditors in a financial statement audit.

The research will take the form of a literature review. My contribution to the

literature is twofold. First I examine whether the several studies that claim that that big data

analytics will be beneficial for the auditor are correct. Second, I synthesize the existing

literature covering the topic of big data with respect to the auditing profession, which can

serve as reference for further research.

Based on the literature study, it can be concluded that the value of big data analytics

for financial statement auditors is not as obvious as originally thought by authors of the Big

Data forum edition in Accounting Horizons. It is ambiguous whether more efficient audits

are achieved, and cost reductions are definitely not realized with the current competition for

data scientist. Furthermore, increased quality of financial statement audits is ambiguous. Big

data analytics has potential to increase quality, but currently the proven positive effects of

big data analytics are not in the scope of financial statement audits. Rather, more specialized

assurance services such as forensic audits could benefit from these new techniques.

The remainder of this paper is structured as follows. In the second chapter

background information is provided on the financial statement audit and how a financial

statement ought to be performed. Furthermore, chapter 2 will describe big data and several

analytical techniques to analyse big data. In chapter 3 the criteria to assess the value for

auditors of big data analytics are presented, which will be the basis for the analysis in

chapter 4. In chapter 5, a discussion of the results of chapter 4 is presented, followed by a

conclusion.

2 Overview of the theory

2.1 General context of auditing

The business environment has become more complex over the years, especially with the

increased amount of data available (Gray, 2002, p. 9). Therefore, the demand for assurance

services has increased to reduce the information risk associated with the more complex

business world (Arens, Elder & Beasley, 2014, p. 26). Arens et al. define information risk, as

the possibility that the information presented is not entirely truthful and could result in

wrong decisions by internal and external users of the information (2014, p. 26). The

(external) financial statement audit is one of those demanded assurance services and in

general when referred to auditing, this type of assurance service is meant (Arens et al.,

2014, p. 29). The ultimate purpose of the audit is to improve the level of confidence placed

in the financial statements by the users of the financial statements (IAASB, 2012).

Arens et al. present the following definition of auditing: “Auditing is the

accumulation and evaluation of evidence about information to determine and report on the

degree of correspondence between information and established criteria. Auditing should be

done by a competent, independent person” (2014, p. 24). Specifically, the financial

statement audit is performed to verify that the statements are in agreement with criteria

such as general accepted accounting principles (GAAP) (Arens et al., 2014, p. 34).

The above-‐presented definition of auditing will be used to explain which role

auditors fulfil in the business environment and how they fulfil it. According to Arens et al.

the auditor must obtain reasonable assurance about whether the financial statements are

free from material misstatements, and thus present a fair view of the underlying economics

of the entity (2014, p. 164). However, the auditor’s assurance concerns the historical

financial statements, which is termed in literature the ‘rear-‐view window check’ (AIPCA,

2015, p. 53). To increase the relevance of the financial statement audit, auditors are

required to make an assessment whether the auditee is likely to continue as an entity for a

certain period of time (AICPA, 1989, p. 2048).

The assurance, however, is given to the shareholders. So even though the auditee

orders and pays for the audit, it is actually executed for the shareholders of the auditee,

which is a rather unusual construction (Teeter, 2014, p. 2).

To enable the auditor to express an opinion about the financial statements, s/he has

to evaluate the auditee following a structured plan that can be referred to as the audit

approach (Arens et al., 2014, p. 441). There are four general phases in the audit identified by

Arens et al., but each audit firm has the liberty to develop their own specific methodology

that ultimately could lead to a competitive advantage (Jeppesen, 1998, p. 520). In the next

section these four phases will be discussed in depth.

Several important terms from the definition of auditing will be discussed in the

remainder of this section. Evidence as defined by Arens et al. is any form of information

used by the auditor to test assertions made by the management of the auditee (2014, p. 24).

Two aspects are important when discussing evidence within auditing, which are

appropriateness and sufficiency. Appropriateness consists of the relevance and reliability of

the evidence collected (Arens et al., 2014, p. 196). A more thorough explanation can be

found in the third section of this thesis. The auditor has several techniques to collect

evidence, for example physical examination (for inventory items) and analytical procedures

such as financial ratios for risk assessments (Arens et al., 2014, p. 199).

Sufficiency is about the question how much evidence the auditor should gather. The

method used by auditors to determine the amount of evidence that should be aggregated, is

the audit risk model (AICPA, 1983). The following equation adopted from Arens et al. is the

basic form of this method; Planned Detection Risk (PDR) = !""#$�!"#$ !"#$% !"#$ (!!")!"!!"!#$ !"#$ !" × !"#$%"& !"#$(!")

The outcome PDR, which indicates the risk that audit evidence fails at detecting

misstatements, is inversely related to the amount of evidence the auditors have to gather

(Arens et al., 2014, p. 279). Hence, a lower PDR requires more evidence. The next

component, AAR, reflects the risk the auditor (in general the managing partner) is willing to

take that the financial statements contain material misstatements after the audit is

completed (Arens et al., 2014, p. 280).

IR refers to the chance the auditor imputes to the possibility of material

misstatement before taking the internal controls into account (Arens et al., 2014, p. 279). CR

refers to the chance that the internal control system of the auditee is unable to detect

material misstatements. The model as presented above is described in the auditing

standards, which characterizes the auditing profession. These standards contain outlines

that dictate, for la large part, how the audit should be performed. Compared to other

professions, auditing is highly regulated.

Another important term is ‘reasonable assurance’. Auditors do not guarantee that

financial statements are free from material misstatements, since it would not be

economically feasible to check every transaction and every item. However, reasonable

assurance is said to be at least 95% sure that the financial statements do not contain

material misstatements.

Related to reasonable assurance is the term material misstatement. Auditors have

the responsibility to detect material misstatements and not every misstatement. Materiality

is highly subjective and is defined in the following manner: something is considered material

when omission or misstatement of the information is likely to change the decision of a

reasonable person (Chewning, Pany & Wheeler, 1989, pp. 80-‐81). Materiality can vary per

auditee, obviously the monetary material level of an organisation such as Apple Inc. is

different from the local fruit retailer.

2.2 Performing an audit

In this section the different phases of the audit are briefly discussed. As emphasized earlier,

while the precise methodology followed by an audit firm can differ from what is outlined

below, the content will generally be similar.

The first phase is the planning phase. In the planning phase the auditors examine

whether to accept the client by analysing the industry of the auditee and evaluate the

reasons for the audit (Arens et al., 2014, p. 231). Furthermore, the auditor achieves a

sufficient understanding of the business and the industry of the client in order to make a

proper business risk assessment, which will determine the AAR and the risk of material

misstatements (Arens et al., 2014, p. 239). Using the information obtained in the planning

phase, a materiality level is determined. Often a percentage of the net income is used as

value to classify irregularities as either material or immaterial (AICPA, IAS 320). At the end of

the first phase, based on the analysis of the client and its industry, an overall audit approach

is designed.

In the second phase, auditors carry out test of controls and substantive tests on

transactions (Arens et al, 2014, p. 442). By testing the specific internal controls of the

auditee, the auditors can determine the control risk, which is the CR in the audit risk model.

In the case of weak internal control more evidence has to be gathered to verify the

monetary amounts of transactions and balance sheet items in the subsequent phase (Arens

et al., 2014, p. 442).

The third phase of the audit consist of two main activities, which are analytical

procedures and tests of details of balances (Arens et al., 2014, p. 184). The analytical

procedures are used to find patterns and plausible relationships between different balance

sheet items. For example, a ratio of accounts receivable to sales is assumed to remain

stable, when deviations are found large enough the auditor should proceed with a test of

detail of balances. Those tests of detail consist of contacting customers of the auditee to

confirm certain accounts receivable amounts. Conversely to the second phase, evidence is

mostly retrieved from third parties (Arens et al., 2014, p. 184).

After the auditors have completed all procedures and acquired all the evidence to

meet the objectives of the audit, an overall verdict is reached. The auditors draw an overall

conclusion in the final phase of the audit, whether or not the financial statements are free

from material a misstatement, which is referred to as the auditor’s opinion (Arens et al.,

2014, p. 70). For simplicity’s sake one of two opinions can be expressed: either a clean

opinion or a modified opinion. When no material misstatements are detected the auditors

will express a clean opinion (Arens et al., 2014, p. 68). When material misstatements are

detected, the auditor will modify his/her opinion. While there are several different types of

modified opinions, for this thesis the broad distinction above will satisfy.

2.3 Big Data Big data and the analytics performed on them have been quite the hype in numerous

industries for the past few years (Deloitte, 2013, p. 2). But, as with any hype, its true value is

not as evident as people might think. In the introduction, two applications of big data

analytics were mentioned. To make an assessment of the possibilities of big data analytics in

the auditing profession, it is paramount to define big data as well as analytics in a fashion

that suits the auditing profession.

Different professionals in different industries use different definitions of big data

(Alles & Gray, 2015, p. 8). The Mckinsey Global Institute employs the following definition: as

soon as data cannot be captured, analysed and stored by the traditional information

systems, it should be labelled as big data (2011, p. 1). Using this definition any firm is

capable of generating big data if, for instance, when trends on Facebook are used as input

for decision-‐making. This type of information falls outside the scope of traditional

information systems according to Yoon et al. (2015, p. 431). The Mckinsey Global Institute

deliberately established a subjective definition, so that every industry has the liberty to

come up with a specific definition that is most suitable for their particular industry (2011, p.

1). Such a vague definition does make it questionable whether big data is fully understood

by anyone. Nevertheless, by synthesizing what is currently known of big data, I try to

establish an accurate description of big data and provide examples of data analytics relevant

for financial statement audits that can be performed with big data.

In the existing literature, definitions of big data can be divided into two broad

categories. The first category of definitions focuses on specific examples of big data (Alles &

Gray, 2015, p. 8). This definition, however, requires specific examples of big data that can be

used in auditing. Due to the lack of research, specific examples are not available, which

makes this definition unusable. In this thesis we will therefore rely on the second category of

big data definitions. This category, according to Alles and Gray, is based on specific

characteristics of big data (2015, p. 8). Those characteristics are commonly known as the 4

V’s. It must be noted that, since big data is a current issue it is likely more definitions and

characterizations will follow. For example, at the Big Data Summit in Boston two additional

V’s were presented (Normandeau, 2013).

Interestingly, the 4 V’s definition is derived from a blog (META group), now a part of

Gartner, that came up with the taxonomy in 2001, which was before the big data hype

actually started (ACCA, 2013, p. 11). META group defined the first 3 V’s, which are: volume,

velocity and variety, as cited by Alles and Gray (2015, p. 8). The fourth V, veracity, was later

added to these 3 V’s. Big data distinguishes itself from ordinary data due to the 4 V’s

(McAfee & Brynjolfsson, 2012, p. 62). The first 3 V’s will be explained in this section, the

fourth V will be explained in the analysis section.

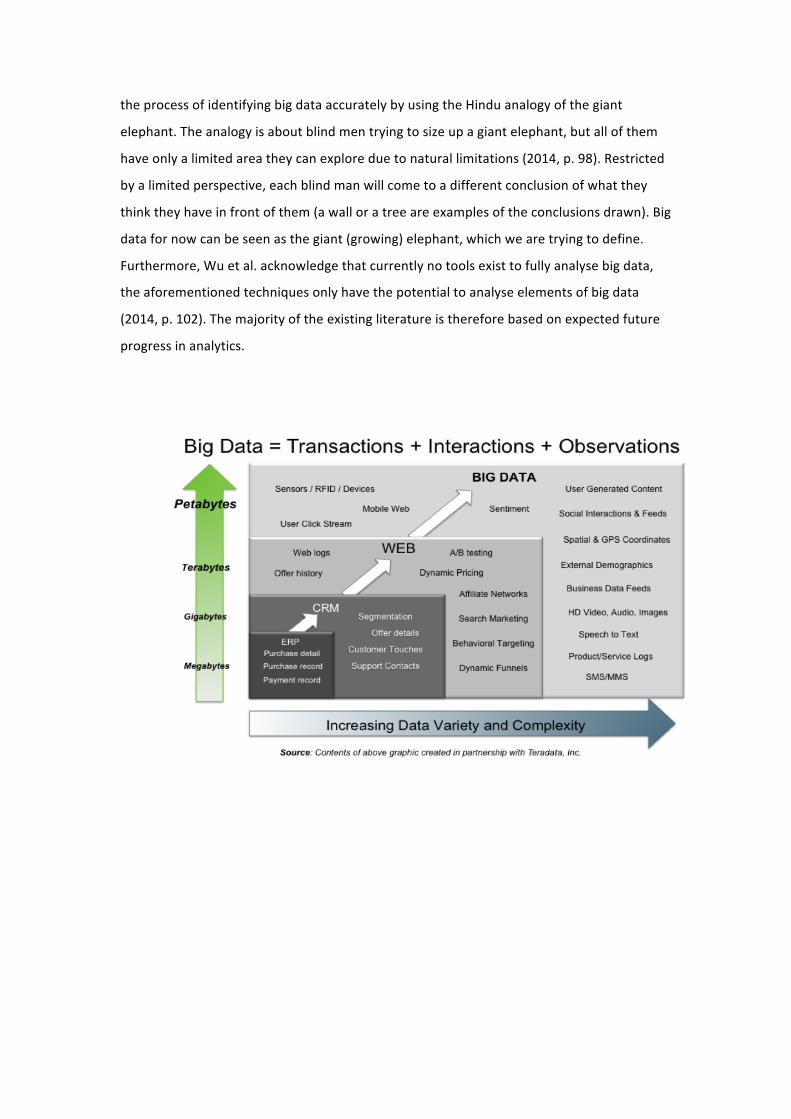

The first V is volume, which refers to the size of the data, as shown in the figure

below. Moffit and Vasarhelyi argue that traditionally information was generated by the

information system of the auditee, but an increasing amount of information is generated by

other sources (2013). The lower left square of the figure below, which represents

transaction data, is currently the most important information for the auditor (Alles & Gray,

p. 10). However the auditee’s information system is not the only data-‐generating system.

Connely identifies the following two additional sources of information: human-‐sourced

information, such as the social medium Facebook, and machine-‐generated information,

which is information from data sensors and mobile tracking sensors (2012). These sources

are an alternative classification of ‘interaction’ and ‘observation’ used in the figure below

(Alles & Gray, 2015, p. 9). Volume also refers to the growth rate of information. According to

Deloitte, the amount of world data increased from 2,5 zettabytes (21 zero’s) to 8 zettabytes

in a five year time span (2013, p. 6). The auditors, when searching for information to test

assertions of the management, might want consider other forms than transactional data.

There will be a more elaborate discussion of the results of this characteristic as well as for

the other characteristics in the analysis section.

The second V, velocity, refers to the rapid pace at which data changes, which means

that information is continuously updated (Alles & Gray, 2015, p. 9). The third V, variety, is

related to the different forms of information that are included in big data. These forms

range from structured internal information, such as transaction history, to unstructured

external information such as social media information (Deloitte, 2013). This unstructured

type of information could be useful for financial statement auditors as described below. The

wide variety of information is a logical consequence of the different information generators

that were identified earlier.

Currently, auditors depend on structured financial information (GAAP-‐compliant

information) as evidence to support the opinion about the financial statements (Cao,

Chychyla & Stewart, 2015, p. 427). Therefore, the ‘new’ information big data adds to the

information currently used by the auditor is unstructured non-‐traditional information

(Moffit & Vasarhelyi, 2013, p. 2). However, without techniques to analyse the new data the

value to auditors derived from big data will be equal to zero. As stated by Alles and Gray,

value from (big) data is determined by the analytics performed with them (2015, p. 13).

Therefore, several data analytical tools are considered below that might be useful to

auditors to analyse big data and hence indicate the relevance of the 3 V’s as explained

above.

Data analytics (also termed business intelligence/artificial intelligence) have been

divided into three levels by Chen, Chiang and Storey in an often-‐cited article. The first level

consists of simple regression techniques on structured databases such as ERP systems of

enterprises (Chen et al., 2012, p. 1166). The second level has been largely developed under

the influence of the Internet, according to Chen et al. (2012, p. 1167). The authors argue

that with the Internet new kind of information came available, which required new

techniques and tools to analyze (2012, p. 1167). The third level is still in its developmental

stage, which incorporates the different information made available by smartphones and

other devices equipped with GPS and other applications (Chen et al., 2012, p. 1167).

Data analytics is the practices of selecting and cleaning data, modelling, and finding

patterns in datasets using data mining tools, which can be used to gain certain insides and

aid the auditor in, for example, risk assessments (Sharma & Panigrahi, 2012, p. 38). Below

several data mining techniques discussed in auditing literature are presented, note that the

list is by no means not exhaustive.

The first tool is neural network (NN); in contrast to standard logistic models, NN uses

non-‐linear models to analyse datasets (Sharma & Panigrahi, 2012, p. 40). By incorporating

complex algorithms multiple pieces of information can be evaluated at the same time

(Calderon & Cheh, 2002, p. 205). In terms of big data, neural network might be able to link

financial and non-‐financial data to find certain patterns or discrepancies (Chen et al., 2012,

p. 1170). A simple example of a discrepancy is higher reported sales, while the amount of

stores decreases. Assuming that Internet sales remain the same, it could indicate suspicious

accounting (Yoon et al., 2015, p. 435). Further, when considering social media, decreasing

popularity, indicated by likes and re-‐tweets, could be an indicator of going concern issues.

In contrast to neural networks the second tool, text mining, is a technique analysing

‘soft’ data rather than financial ‘hard’ data. Different approaches exist to analyse plain text:

searching for specific words, searching for specific word combinations or identifying any

other abnormality in plain text, which is termed text analysis (West & Bhattachrya, 2016, p.

55). This tool might be valuable when considering using social media, emails, management

letters etc. as information source to the auditors, since it consist largely of textual data.

The next tool discussed is process mining, which refers to analysing transactions and

event logs (West & Bhattachrya, 2016, p. 55). When a certain transaction has to be

completed, firms normally have certain protocols that should be followed (Jans, Alles &

Vasarhelyi, 2013). Most mid-‐sized and large firms have Enterprise Resource Planning (ERP)

systems that automatically record the steps taken to complete the transaction. By analysing

this data, auditors could verify whether the actions taken are indeed the actions that should

have been taken (West & Bhattachrya, 2016, p. 55).

Another tool is Benford’s law, which is an example of how suspicious accounts are

identified. The theory is about the probability that certain numbers appear in a certain

order, for example the ‘9’ appears only in 5% of the cases as the first number (Durtschi,

Hillison & Pacini, 2004, p. 19). Benford’s Law, however, has been established in 1938, but

has not been widely accepted as a proven theory, which made it until now a controversial

technique. According to Durtschi et al., Benford’s Law is merely an addition to existing

analytical techniques used by auditors today, without consensus that it actually aids the

auditor in mapping suspicious accounts (2004, p. 21). But its relative ease makes it appealing

to use, one can simply choose an account on the balance sheet/ income statement, which

should be analysed and let the ‘app’ do the work (Cleary & Thibodeau, 2004, p. 6).

All of the above indicates that big data is not easy to define, with all the

complementing and contradictions around. In my opinion Wu, Zhu, Wu and Ding describe

the process of identifying big data accurately by using the Hindu analogy of the giant

elephant. The analogy is about blind men trying to size up a giant elephant, but all of them

have only a limited area they can explore due to natural limitations (2014, p. 98). Restricted

by a limited perspective, each blind man will come to a different conclusion of what they

think they have in front of them (a wall or a tree are examples of the conclusions drawn). Big

data for now can be seen as the giant (growing) elephant, which we are trying to define.

Furthermore, Wu et al. acknowledge that currently no tools exist to fully analyse big data,

the aforementioned techniques only have the potential to analyse elements of big data

(2014, p. 102). The majority of the existing literature is therefore based on expected future

progress in analytics.

3 How to assess the value of big data analytics for auditors

In its most basic form, big data analytics can be seen as a tool for the auditor when

conducting the audit. An audit tool is any technique, manual or computerised, used in the

audit (Curtis & Payne, 2008, p. 105). This section will describe the considerations for the

auditors when they adopt a new audit tool. The umbrella criterion wills that big data

analytics should provide benefits to the auditors in some form. Therefore, this section tries

to define what ‘beneficial’ is for the auditors.

3.1 The Iron Triangle In the article of Vasarhelyi and Romero, the Iron Triangle is used to evaluate whether new

audit technology is beneficial to auditors, and hence should be adopted (2014). The Iron

Triangle will be used as a starting point in this thesis. It consists of three components:

efficiency/effectiveness, cost reduction, and quality (Vasarhelyi & Romero, 2014). As

demonstrated below, efficiency/effectiveness and cost reduction are rather straightforward;

quality, however, is a controversial topic when put in the auditing context (Fischer, 1996, p.

220) and will be discussed in more detail.

Efficiency and effectiveness are often used as complements of one another, which

comes down to the following definition: the degree to which established goals are realized,

and the amount of resources used to do so (IPPF, 2010, p. 2). This is a fairly general

definition and needs further specification in order to be useful for evaluating external

financial audit tools. Efficiency is defined in terms of the resources that are used (Rosenfeld).

One feature of auditing is the labour intensity of the job, with other words the resources

used. Therefore, decreasing the labour hours needed to achieve the same level of assurance

is a good way of defining efficiency without impairing effectiveness, which is maintaining a

certain assurance level. The IAASB further differentiates resources in qualitative and

quantitative resources (2012). For example, hours worked by a managing partner are

different in terms of quality than hours worked by a staff assistant.

Cost reduction is to some extent the logical consequence of fewer resources that are

used. However, there are more considerations with respect to cost reduction, which can be

derived from the diffusion of innovation theory (DOI). For instance, does the new tool

supersede other tools, hence can it replace current tools used (Rosli, Yeow & Eu-‐Gene, 2013,

p. 5). Moreover, education is required to enable auditors to use specific tools (Romero &

Vasarhelyi, 2014), which depends partly on the complexity of the audit tool (Rosli et al.,

2013, p. 5). The cost reduction should be seen in the long term, but the future is often

uncertain. Therefore, the pay-‐off, less resources used, and the cost, for instance of

education, can be hard to estimate (AICPA, 2015, p. 72).

3.2 Audit Quality

The last component of the Iron Triangle is quality. As opposed to other services, financial

statement audits are not transparent. This means that assessing the quality of the audit is

difficult when the audit report is the only outcome to go on (IAASB, 2012). The first

definition of audit quality is from DeAngelo, which underlies many of the other definitions of

audit quality established after DeAngelo (Al-‐Khaddash, Al Nawas & Ramadan, 2013, p. 207).

DeAngelo argues that quality is the joint probability that an auditor will both discover and

report a breach in the client’s accounting system, as cited by Al-‐Khaddash et al. (2013, p.

207).

Furthermore, each stakeholder of financial reporting (auditor, investors, regulators

etc.) will determine the quality of the audit on different criteria (Knechel, Krishman, Pevzner,

Shefchik, Velury, 2013, p. 386). Auditors value the perceived quality of their work by various

stakeholders as well as actual quality, since both will determine the relevance of the

auditor’s work (Al-‐Khaddash et al., 2013, p. 211). Therefore, ‘quality’ should be assessed

from multiple perspectives and not only from the auditor’s perspective.

In the remainder of this section a framework will be presented that tries to capture

a balanced view on different measures of audit quality. The framework will distinguish input

of the audit, the audit process, and the output of the audit when considering audit quality.

Overall, quality is defined by the PCAOB as meeting customer demand (2013).

3.2.1 Audit input

First, the input of the audit. Input refers to what audit firms employ to perform the audit

and achieve the desired result (PCAOB, 2013). From the different inputs for the audit, the

IAASB identifies ‘people’ as most influential on audit quality (2012). Ultimately, the skills and

the personal qualities of audit partners and staff determine the quality of the work

performed (FRC, 2008) as cited by Knechel et al. (2013, p. 388). So what qualities are

perceived as ‘good’ in the auditing literature?

According to Knechel et al., the financial statement audit consists of many

judgement calls that have to be made in the audit process, which in turn determine the

quality of the audit (2013, p. 390). To enable the auditor to make proper decisions, several

personal qualities should be present. One of the most important qualities is professional

scepticism (PCAOB, 2013). Specific examples of qualities of a professional sceptical auditor

are a questioning mind set and the ability to critically evaluate the obtained evidence

(ICAEW, 2013).

Moreover, knowledge, which determines expertise to a large extent (Ashton, 1991,

p. 220), of the industry and the auditee are identified by Knechel et al. as important

contributors to higher quality decision making and hence, higher quality audits (2013, p.

392). Knechel et al. argue that industry-‐specific knowledge could enhance judgement calls

that have to be made by the auditors (2013, p. 392). Hence, being able to analyse industries

more thoroughly has the potential to enhance the quality of the audit.

Furthermore, personnel should be independent and competent to perform high

quality audits (PCAOB, 2013). The independence of the auditor is determined by the

objectivity of the auditor (ICAEW, 2003). One of the threats to the objectivity of auditors is

when they provide other non-‐audit services to a client (Reynolds, Deis, & Francis, 2004, p.

31). Other qualities found in independent auditors are integrity and impartiality of the

auditor (Arens et al., 2014, p. 56). Moreover, personnel should possess the technical

capabilities to execute audit procedures (Khaddash et al., 2013, p. 210).

Another important input factor according to the PCAOB is tone at the top (2013).

Specifically for audit partners and firm managers, a positive relation has been found

between tone at the top and audit quality (PCAOB, 2013). When the top strives for

innovative and high quality audits, it is more likely that staff will do the same (PCAOB, 2013).

3.2.2 Audit Process

The next component of the framework is the ‘process’ of the audit, which refers to the four

phases described in section 2.2. Several important judgements in the audit process

according to auditing literature are: risk assessment, obtaining and evaluating evidence and

review of the work, as cited by Knechel et al. (2013, pp. 393-‐397). Judgements made by the

auditor are structured, semi-‐structured or unstructured, with structured judgements

requiring almost no judgement and unstructured decisions requiring a high level of

judgement (Arens et al., 2014, p. 190).

Knechel et al. identify two potential hazards that impair the auditor’s judgement.

The two hazards are anchoring and adjustment, and representativeness (Knechel et al.,

2013, p. 396). Anchoring and adjustments happen in the ordinary course of the audit. The

expectation is that adjustments to the anchor value are made in the ‘correct’ direction

(Kinney & Uecker, 1982, p. 56). For example, the auditor has an idea about certain book

values, the anchor, and during the audit the auditor finds evidence supporting or

contradicting this expectation, which underlies the adjustment. However, according to

Kinney and Uecker, it does happen that the ‘anchor’ is not sufficiently adjusted because of

sample outcomes (1982, p. 57).

Tversky and Kahneman originally established the definition of representativeness in

1974, as cited by Aston (1984, p. 80). The theory behind representativeness is that auditors

attach a higher probability to uncertain events that are more in line with expectation

(Ashton, 1984, p. 81). The expectation is based on certain resemblance between the

uncertain event and the population, i.e. the representativeness of the uncertain event of the

population (Ashton, 1984, p. 81). For example if we have item A and we want to assess the

probability that it comes from a population A or B, looking at the resemblances with the

population A or B is a logical step to take (Schroeder, Reinstein & Schwartz, 1996, p. 18).

Furthermore, Ashton argues that several factors will influence the likelihood that the

heuristic representativeness occurs (1984, p. 82). The first factor is the correspondence

between the sample and the parent population. When the auditor draws a sample in which

essential properties are more similar with the population, representative of the population,

the auditor will deem this scenario more likely (Ashton, 1984, p. 82). The opposite is true as

well. Therefore, the sample drawn is critical for the judgement of the auditor. In addition,

sample size has an influence on the auditor’s judgement, since in smaller samples extreme

values are more likely (Ashton, 1984, p. 81). However, larger samples, termed

protectiveness, do not guarantee that the above heuristics are prevented (Schroeder et al.,

1996, p. 19).

Another important process in the audit is obtaining and evaluating obtained audit

evidence (Mcknight & Wright, 2011, p. 194). As synthesized by Smith and Kida, audit

evidence has an influence in multiple ways on the auditor’s judgement (1991). Francis

argues that the financial statement audit is only as good as the evidence obtained (2011, p.

135). Arens et al. describe two measures of evidence quality, which are sufficiency and

appropriateness of audit evidence (2014, p. 196). Sufficiency has been explained in section

2.1, whereas appropriateness of evidence deserves further elaboration. According to Arens

et al., appropriateness consists of relevance and reliability of the evidence (2014, p. 196).

Relevance of the evidence refers to the intended use of the evidence in the audit.

For example, when the auditor is testing whether all sales are invoiced, tracking back from

the invoiced sales to shipping records is irrelevant. Relevant evidence would be to consider a

sample of sales shipped and track them back to invoiced sales to see or all are indeed

invoiced. The auditor should therefore obtain evidence that can be used to meet certain

audit objectives (Arens et al., 2014, p. 196).

Reliable evidence has several characteristics as described by Arens et al. (2014, p.

197). First of all, evidence directly obtained by the auditor is considered more reliable than

information obtained indirectly (Arens et al., 2014, p. 197). Second, when information is

obtained indirectly, the source should be qualified to do so. If so, evidence obtained from

outside the firm is regarded as higher quality evidence (Arens et al., 2014, p. 197). Third,

evidence that needs little judgement is regarded more reliable, hence higher quality of

evidence (Arens et al., 2014, p. 197). Finally, timeliness of audit evidence is an indicator of

quality. Arens et al. argue that evidence obtained for balance sheet accounts close to the

balance sheet date is more reliable than evidence obtained a considerable time before the

balance sheet date (2014, p. 197). Timeliness for the income statement is slightly different,

Arens et al. emphasize that evidence should be obtained from the whole year, rather than

only at the end (2014, p. 197).

The last component of the process part of the quality framework is review and

control of the work that has been done, since it is positively related to audit quality

according to Knechel et al. (2013, p. 396). To achieve a high quality review, the PCAOB

argues that the technical competence of the reviewer should be of a considerable level

(2013). Furthermore, reviewers should have enough time to properly review the work that

has been done, which makes a proper planning of the audit essential (PCAOB, 2013).

3.2.3 Audit output

Output is the last component of this quality framework, which will be considered most

important with respect to audit quality by users of financial statements and regulators of the

audit profession (IAASB, 2012). Most indicators are only quantitative and difficult to

transform to criteria. For example, the amount of false positives and false negatives (errors

that arise with going concern opinions) are empirically testable, but hard to define in

qualitative terms. In the end, it depends on how effectively the audit process is executed,

which is determined by the people performing the audit. However, the IAASB found an

important qualitative aspect of ‘output’, which is transparency of the audit performed

(2012). They argue that when the audit is more transparent, it could be considered of higher

quality by different stakeholders (2012). Further, the time-‐lag between the year-‐end and the

issuance of the audit report decreases the relevance for decision making, which decreases

the perceived usefulness of the financial statement audit (Chan & Vasarhelyi, 2011, p. 152).

Therefore, decreasing the time-‐lag would increase the quality, since customer demands are

better satisfied.

4 Examination of the possible value of big data analytics In this section I will assess if and how big data analytics could be valuable to the auditors in

different phases of the financial statement audit. In this section I will examine whether big

data analytics can realize more efficient financial statement audits without impairing

effectiveness, and whether higher quality audits can be achieved. Furthermore, challenges

and obstacles for big data analytics will be discussed.

4.1 Big Data Analytics and Efficiency As described in section 3, big data analytics could be valuable to auditors when it makes the

audit more efficient. This can be achieved by reducing labour hours in quantitative and

qualitative sense. Regardless of specific phases of the audit, it is quite straightforward that

the amount of qualitative resources used is unlikely to decrease when big data analytics are

employed in the financial statement audit. Cao et al. argue that currently there already is a

shortage of people with sufficient knowledge of the auditing process and data analytics

(2015, p. 427), a shortage which is unlikely to decrease with the emphasis on data analytics

in multiple industries at the moment. Data analytics is a complex field of study and requires

sufficiently educated employers (specialists often referred to as data scientists). Hence the

resources used in qualitative terms will increase in order to actually enable audit firms to

use big data analytics in the financial statement audit.

Moreover, the auditing profession is just one of the many professions who use or

intend to use forms of big data analysis. This phenomenon is demonstrated by the search

results on several job applications websites, where big data analysts are in high demand by a

variety of firms. Moreover, since auditors essentially fulfil a public service as explained in

section 2.1, wage-‐growth potential will be significantly lower than with firms such as Google

and Microsoft, thus making audit firms (even) less interesting to potential employees. The

above implies that the competition for data scientists is fierce, consequently increasing the

cost of hiring these data scientist, increasing the cost of the audit. In my opinion,

outsourcing the big data analytics part of the audit could be a way to prevent high cost.

However, hardly any research has been conducted in this area, which makes it difficult to

assess the possibilities and consequences of outsourcing parts of the external audit in terms

of efficiency and quality.

However, the amount of resources used could be reduced if big data analytics has

the potential to replace existing labour-‐intensive parts of the financial statement audit. In

phases two and three one of the main activities is gathering sufficient appropriate evidence

to test assertions made by the auditee’s management. For example, testing the value of the

inventory from a retailer is generally done by obtaining evidence by physical examination1,

which is a labour-‐intensive job (Arens et al., 2014, p. 205). Brown-‐Liburd and Vasarhelyi

argue that using the information of radio frequency identification (RFDI) chips for validating

inventory could make the process more labour efficient (2015, p. 2). The authors, however,

neglect to explain how it could be realized. A possible explanation could be that more

efficient inventory validation is achieved because the auditor can rely on the generated

numbers by RFDI. As argued below in the evidence section, RFDI is a sensor technique

automatically generating information, requiring less verification. It does require that the

auditee uses and stores RFDI data, which is not self-‐evident for every business. Also, RFDI

technology is not a recent development, as it has been around for quite some time.

Nevertheless, there do not seem to be many applications already by financial statement

auditors. Maybe the technology does not satisfy the required assurance level, but pilot

studies should be able to identify the reasons.

Furthermore, assessing the internal control of the auditee is an important task in the

second phase of financial statement audit. Currently, the internal control is validated by

techniques such as reperformance, observations and examination of documents (Arens et

al., 2014, p. 331). These techniques are labour-‐intensive and often have to be performed in

combination with one another in order to suffice in terms of sufficient evidence (Arens et al.,

2014, p. 204). A technique such as process mining, described in section 2.3, has the ability to

replace the above activities, and greatly improve the effectiveness and efficiency of the

control procedures since it requires less personnel (Jans, Alles & Vasarhelyi, 2014, p. 1752).

The authors argue that because of the wide application of (ERP) systems, electronic

verification of the internal processes is more easily done, because the ERP system

automatically records procedures (not) undertaken by personnel (2014, p. 1754). The

strength of this technique lies in the fact that automatically generated data is involved in the

analysis (Jans et al., 2014, p. 1753). Since automatically generated information is hard to

alter, auditors can rely more easily on this data without having to verify every source.

However, process mining is not a widely applied technique in the financial

statement audit to validate the internal control (Stewart, 2015, p. 112). A possible

explanation could be that using a technique such as process mining would require superior

knowledge and experience of the business process of the auditee (Jans et al., 2014, p. 1756).

1 For example by counting the inventory of a retailer, however differences exist across industries audited

Only experienced auditors would be capable of using the technique effectively, which means

more qualitative resources are needed for an audit, which increases the cost of performing

an audit. Considering the low margins on financial statement audits, this would be

undesirable. Procedures such as observation/reperformance can be more easily performed

by inexpensive staff members (inexperienced personnel) (Arens et al., 2014, p. 331).

Also, complete consensus about the auditor’s responsibility with respect to internal

control does not exist. In the United States for example, auditors have the responsibility to

assess the internal control for firms satisfying criteria of the SOX, but for smaller firms and in

Europe there is no such regulation. Therefore, the importance of innovative techniques such

as process mining could be undervalued by external auditors, since the current techniques

suffice and there is not enough pressure from the environment (stakeholders, regulators

etc.) for auditors to consider expensive new techniques.

A better internal control assessment however, is important to the control risk

component of the audit risk model, outlined in section 2.1. Techniques which execute better

and more efficient internal control activities would decrease the control risk, thus

decreasing the amount of evidence that has be accumulated and thus less work that has to

be done. However, risk assessments are rather subjective, which means that reductions in

the risk are not translated 1 to 1 in less evidence, making a solid argument impossible.

4.2 Big Data Analytics and Audit quality

Aside from different phases in the audit, the input of people is an important determinant for

the audit quality. In section 4.1 I argued that more specialists are needed in order to enable

audit firms to incorporate big data analytics in the financial statement audit. Ultimately, a

higher ratio of specialists to staff in the audit engagement team would increase the quality

of the audit (He, 2015, p. 1686). Big data analytics, however, have almost no influence on

the personal qualities of the auditors identified in section 3. Rather, auditors will have to

possess more qualities to use big data. Professional scepticism, one of the most important

qualities according to auditing standards, is hardly influenced by big data analytics.

Moreover, big data analytics demands more professional scepticism from the auditors. For

example, the auditors make several risk assessments during the audit, such as the possibility

of material misstatements, due to error or fraud. As described in section 2.2 Benford’s Law is

an example of a tool that identifies suspicious transactions/accounts. One of the most

important consequences of big data analytics, such as Benford’s Law, is the ability to analyse

the whole population. When analysing millions of transactions, the amount of ‘positives’ will

be substantial (Stewart, 2015, p. 111). Positives in this case are the amount of suspicious

transactions found by the tool. Stewart argues that determining which ‘positives’ should be

further investigated depends on the judgement of the auditor, requiring a certain degree of

professional scepticism and knowledge about the auditee and the industry (2015, p. 111).

Wrong decisions could lead to many ‘false positives’, which could lead to lower quality

financial statement audits.

Industry and auditee specific knowledge could be improved using big data analytics

(Zhang, Yang, Appelbaum; Cao et al.; Yoon et al., 2015), however the general way auditors

become industry specialist is by spending considerable time in a certain industry. The

aforementioned authors apparently think that big data analytics could be some kind of

shortcut, but do not explain how this would work. The same holds true in becoming more

knowledgeable of the auditee, a longer tenure is positively related with auditee specific

knowledge. This fact is often a reason why first time audits are more expensive than

subsequent audits by the same auditor (Simunic, 1980). The knowledge of the industry and

auditee are important determinants with respect to the inherent risk component in the

audit risk model of section 2.1. This type of risk assessment improves with big data analytics

according to Yoon et al., but they do not give a solid argument to support their claim.

A possible positive influence of implementing big data analytics would be on the

‘tone at the top’. When management of the firm incorporates an innovative technique such

as big data analytics into the audit, it is more likely that the rest of the personnel will follow

the good example. Hence, employees will be more motivated to strive for high quality, since

the top of the firm does the same. However, strong empirical prove for this relationship is

absent. Nevertheless, it is imaginable that when your manager puts in more effort, you will

be more willing to do the same than when the manager is rather reluctant in striving for

improvement.

In the third section of this thesis, several characteristics of high quality evidence

were discussed. Francis argues that high quality evidence is of significant influence on the

quality of audits (2011, p. 135). First of all there’s the issue of reliability of audit evidence.

The source of the information is identified as critical in the in the assessment of reliability of

evidence (Brown-‐Liburd & Vasarhelyi, 2015, p. 6). Brown-‐Liburd and Vasarhelyi argue that

because big data is partly generated automatically, the chance of alteration is relatively

smaller than manually generated data (2015, p. 6). This inability to alter data is enhances the

reliability of big data as audit evidence. However, since so many different sources produce

information which is accumulated and called big data, verifying every source would be

cumbersome and even impossible, making big data evidence less reliable. This problem

characterizes big data, and is the fourth V veracity.

Another characteristic of high quality audit evidence is objectivity. Big data will

demand sufficient judgement in what to conclude from the available information and what

is correct or incorrect, as demonstrated by the example of fraud risk assessment above.

Because the whole population is obtained, numerous positives will be present. As described

earlier, the only way to cope with this problem is for the auditor to make a subjective

judgement what to take away from the results. In favour of big data as audit evidence is the

velocity of data, which will provide the most up-‐to-‐date information and evidence. For

instance, when evidence has to be found about accounts receivables, big data could provide

the most current information about a specific creditor.

Moreover, high quality evidence is determined by the sufficiency of aggregated

evidence, as described in section 3. Traditionally the questions that had to be answered with

respect to sufficiency were: adequate sample size and which items to select from the

population (Arens et al., 2014, p. 199). Strongly in favour of big data analytics is the fact that

the whole population is tested, which means no need for sampling and related difficulties.

However, the curse of too much knowledge could in the end impair audit quality because of

the limited amount of information humans, and thus auditors, can process (Knechel et al.,

2013, p. 387).

Another argument in favour of big data, related to the fact the whole population is

tested, is the reduction of two other decision heuristics in the audit process described in

section 3. Both the heuristics adjustment and anchoring, and representativeness occur

because of sample outcomes. When the whole population is tested, decisions are no longer

made on the basis of sample outcomes, thus reducing the chance that auditors are

subjected to decision heuristics in the audit process.

Besides the need for more judgement in evaluating audit evidence obtained with big

data analytics, another drawback can be derived between the difference of current use of

statistical tools and the intended use with big data statistical methods. In the financial

statement audit linear regression models are used often used for analytical review, which

are based on a causal relationship derived from experience and knowledge (Debrencey &

Gray, 2014). An example of such a review method is the relationship between revenues and

cost of goods sold, which is assumed to be fairly stable. Large fluctuations would therefore

be suspicious. In this case we speak of directed data mining (Alles & Gray, 2015, p. 15). The

idea behind big data analytics is undirected data mining, which means that no such causal

relation is established (Chent et al, 2012, p. 1168). This means that decision will be made

based on correlations in data sets (Alles & Gray, 2015, p. 19). According to Cukier and

Mayen-‐Schoenberger, the possible consequence is that auditors will abandon the practice of

finding out why certain relations exist, and simply assume that certain events occur

simultaneously as cited by Alles and Gray (2015, p. 23). For auditors to base their opinion on

correlation instead of causation strokes with their natural conservative attitude (Alles &

Gray, 2015, p. 27). Also, in my opinion it is a lot harder for the auditor defend his/her

opinion based on correlations and no common sense, making it not that appealing to use.

Above, big data analytics were discussed with respect to the audit process and input

and how it could increase the quality of the audit. The last part of the analysis of the

possible value of big data analytics considers the output. The main criterion is the

transparency of the audit process, which is important to various stakeholders to assess the

quality of the financial statement audit. As mentioned several times, big data and analytics

are rather complex subjects. Experts like data scientist already have trouble identifying

opportunities and limits of big data, which makes it unlikely that novices will have a good

understanding of these analytics. Therefore, big data analytics would decrease transparency

rather than increase transparency of the financial statement audit process.

However, big data analytics does nurture more technology-‐driven audits and forces

auditors to rethink their traditional approach (Chan & Vasarhelyi, 2011, p. 153). According to

Chan and Vasarhelyi, more automation in the audit could be the consequence of

incorporating more technology. By automating certain parts of the audit, auditors could

satisfy the demand for more timely or even more audits during a year, hence more real-‐time

assurance (Chan & Vasarhelyi, 2011, p. 153). This would increase the relevance of the

financial statement audit to users of financial statements.

Francis argues that from the most important determinant of audit quality when

looking at output, is the amount of wrong audit reports issued (2011, p. 127). Audit reports

are considered wrong when a clean opinion is given when a qualified opinion should have

been issued and vice versa (Knechel et al., 2013, p. 397). However, it is hard to transform

this determinant for audit quality into a criterion, which was possible with other

determinant as demonstrated in section 3. Nevertheless, an important argument can be

derived from this quality determinant against the use of big data analytics. From several

studies it can be concluded that the very few audits actually go to trial because of wrong

decisions of the auditor, making it questionable whether improvements are actually needed

(Knechel et al., 2013, p. 398). An explanation for the low amount of trials could be the

buyout of the auditee by audit firms when something does go wrong (Allles & Gray, 2015, p.

15). This makes it particularly hard for outsiders, to assess this potential need for higher

quality audits from the perspective of auditors with respect to output.

4.3 Potential challenges and hurdles

Several general difficulties in using big data analytics in the financial statement audit exist.

Below, several challenges and hurdles are explained, but the list is by no means exhaustive.

First of all, much of the literature discusses the benefits of big data under the assumption

that analytical tools exist to analyse big data. The main issue here is that no such technique

is available to analyse big data in a way that is valuable to the auditors. The large variety of

data-‐generators makes it impossible to transform all data into an analysable format (Brown-‐

Liburd, Issa & Lombardi, 2015, p. 458). Techniques that were discussed in section 2.3 have

the potential to analyse small parts of big data, but more research is needed. For instance

more research in the area of ‘Mapreduce’, which is able to analyse several formats at the

same time (Varian, 2014, p. 4). However, a solution could be a partial implementation of big

data analytics.

Moreover, the highly regulated environment of the audit profession makes it rather

difficult to implement new techniques and tools. For example, I argued in section 4.2 (on

reliability and appropriateness of audit evidence) that one possible implementation of big

data was that it could serve as audit evidence. However, the existing standards and rules

limit the possibilities of new types of evidence. Currently, the new Data Audit Standard is

being implemented (Titera, 2013, p. 327), but its precise consequences remains as of yet

unclear.

Another challenge lies in the education of auditors. At this moment, I have had two

years of education in ‘accounting (auditing) and control’, but education in statistical

techniques does not go further than standard linear regression. Furthermore, in audit

courses, only the traditional techniques and audit approaches are discussed, without even

mentioning the current research and progress in the area of new techniques. This inevitably

leads to gaps in the knowledge of future auditors when it comes to such new techniques.

Also, as described in section 4.1, using analytics properly would require more experienced

personnel, demanding a change in the current educational curriculum.

Also, several privacy concerns arise with the use of big data. There exist several

examples of concerns over privacy, such as whether or not corporate emails are property of

the firm or if they should fall under the protection of privacy laws. Big data will go far

beyond the boundaries of corporate email, especially when we consider data from social

media and other Internet applications. However, an example found the newspaper ‘NRC

Handelsblad’ demonstrates the pace at which opinions can change. Chris Hensen describes

an example of a car insurance company (ANWB) that intends to use a tracking device in the

car, which will measure average speed, breaking time etc. of the driver (2016, p. 10). This big

data will than be analysed and car drivers who drive properly and safely are granted a

reduction of insurance fees (Hensen, p. 10). The interesting thing about this example is that

over half a year ago, another Dutch insurance company (Achmea) had an almost identical

idea, unleashing a wave of criticism about privacy concerns. The announcement of ANWB,

however, does not seem to suffer the same fate. It must be noted, however, that the

industries are quite different, which might account the ways in which the media and the

public reacted.

Related to the privacy concern is the possible reluctance of auditees to cooperate

with the audit firms. In general, auditors have to ask for certain information and definitely

do not receive all the information they need up front. On an auditing career day, several

senior auditors emphasized that firms certainly will try to hide certain events, either by

burying information or by omitting information when it’s not specifically asked for. When we

consider the massive amount of information auditors are asking for with respect to big data,

it seems highly unlikely that auditees are willing to provide such information.

5 Discussion In this section the arguments of chapter 4 will be evaluated and at the end of this section a

conclusion will be presented. In chapter 3, three criteria were described and explained,

namely efficiency/effectiveness, cost reduction and audit quality, which are critical in

assessing the value of any tool, such as big data analytics, for the financial statement

auditors.

The first two criteria, efficiency and effectiveness, and cost reduction, are to some

degree interrelated because cost reduction would be the logical consequence of more

efficient financial statement audits. In chapter 4, the analysis whether big data analytics

could increase efficiency in the financial statement audit focused on the required amount of

labour hours. Big data would surely demand more specialists in the audit engagement team,

so in qualitative terms efficiency is unlikely to decrease. In quantitative terms efficiency

improvement is still ambiguous, since big data analytics for now seems to be more of an

additional tool for the auditors rather than an essential tool, at least for the time being.

From the above it becomes clear that cost reduction is not as obvious as one might

think. Several authors who wrote in the Accounting Horizons Big Data forum edition are

extremely positive with respect to efficiency and cost reduction that big data analytics would

bring to financial statement audits. However, they neglect to involve competition of firms

such as Google and Microsoft for sufficiently educated statisticians (data scientists). To

compete with such firms, compensation for data scientists will be high and cost reduction

rather unlikely.

Quality of the financial statement audits is a controversial topic. Since DeAngelo

defined audit quality in 1981, numerous papers have been written about this very topic. The

quality framework described in chapter 3 led to interesting results in chapter 4. First of all,

big data analytics have only a minor influence on the ‘input’ for audits. The only possible

positive influence of big data analytics is found with ‘tone at the top’, but tone at the top is

surely not the most important factor described in chapter 3 with respect to input. Once

again, authors who published in the Big Data forum are very positive, stating that big data

analytics will improve the auditor’s knowledge and will lead to more industry specialists.

Surprisingly, these statements are not backed up with solid argumentation and evidence,

which makes it a rather weak case.

However, in the ‘process’ the second component of the quality framework of

chapter 3, big data analytics does have a certain potential. Big data analytics could serve as

evidence, satisfying the important criteria of high quality evidence as outlined in chapter 3.

Furthermore, techniques such as process mining are likely to lead to an objective evaluation

of the internal control of the auditee and with the growing amount of firms with ERP

systems application of process mining is becoming more likely.

However, an important activity performed at various stages of the audit is the

several risk assessments made by the auditor. In section 2.1 the fraud risk assessment, going

concern assessment and the components of the audit risk model have been explained. The

auditing literature is mainly focused around the big data analytics and fraud risk assessment,

and a strong case is made for the positive results of big data in the fraud risk assessment.

However, detecting fraud is not widely accepted as the job of the auditor in the financial

statement audit. Moreover, several authors (Yoon et al., 2015) have the habit to refer to

‘improved risk assessments’ without specifically referring to a type of risk assessment. In my

opinion they refer to the fraud risk assessment, but the relevance to financial statement

audits is considerably less than for example AAR, IR and CR.

The last component described in the audit quality framework was output.

Transparency has always been the main issue with respect to the financial statement audit,

a reason for the growing criticism that audit firms did not document their steps thoroughly

enough and regulatory bodies had difficulties with monitoring audit firms. Big data analytics

will surely fuel this debate, since big data analytics are complex, require more judgement

and thus leave less space for objective evaluation. The literature around the output

component led to an interesting insight, which is the low amount of trials with respect to

wrong audit opinions, which becomes even less meaningful compared to the amount of

audits performed each year. The Enron case described in the introduction is an extreme

example.

Taking all this into account, I’m of the opinion that big data analytics in the financial

statement audit has been overhyped, demonstrated for instance by Accounting Horizon’s

Big Data forum. Big data analytics does have potential in several areas, but the value for the

auditors in the current state of financial statement audit is negligible. However, which is also

one of the limitations in this thesis, big data analytics is a very recent development. Much

research is currently being undertaken, which could alter literature review performed in this

thesis. Another limitation, because of the novelty of the subject, is the fact that I had to rely

on some unpublished work, because the most recent developments around big data

analytics are not yet published in scientific journals. Furthermore, this thesis is built around

a theoretical framework of how financial statement audits ought to be performed, which

isn’t the same as the real-‐world practice of auditing. Hence, a suggestion for future research

would be to perform case studies with big data analytics. Also, more research should be

conducted in defining big data in a way that’s suitable to auditing. Currently, transaction

data is the most important data for auditors, essentially making anything beyond transaction

big data. When a better definition of big data is established, future research is likely to be

more valuable and better directed, so that the auditing profession might benefit from it.

References ACCA. (2013). Big Data. Retrieved from: http://www.accaglobal.com/bigdata AICPA. (1989). The Auditor’s Consideration of an Entity’s Ability to Continue as a Going

AICPA. (2015). Audit Analytics and continuous audit. Retrieved from: http://www.aicpa.org/interestareas/frc/assuranceadvisoryservices/downloadabledocuments/auditanalytics_lookingtowardfuture.pdf

Al-‐Khaddash, H., Al Nawas, R., & Ramadan, A. (2013). Factors affecting the quality of auditing: The Case of Jordanian Commercial Banks. International Journal of Business and Social science, 4(11), 206-‐222.

Allen, R. D., D. R. Hermanson, T. M. Kozloski, and R. J. Ramsay. 2006. Auditor risk assessment: Insights from the academic literature. Accounting Horizons, 20(2), 157–177.

Alles, M., & Gray, G, L. (2015). The pro’s and cons of using big data in auditing: A synthesis of the literature and a research agenda. Retrieved from: http://jebcl.com/symposium/wp-‐content/uploads/2015/09/The-‐Pros-‐and-‐Cons-‐of-‐Using-‐Big-‐Data-‐in-‐Auditing-‐A-‐Synthesis-‐of-‐the-‐Literature-‐UWCISA-‐Revised.pdf

Arens, A, A., Elder, R, J., & Beasley, M, S. (2014). Auditing and Assurance Services. Harlow, England: Pearson education limited.

Ashton, A, H. (1991). Experience and Error Frequency Knowledge as Potential Determinants of Audit Expertise. The Accounting Review, 66(2), 218-‐239.

Ashton, R, H. (1984). Integrating Research and Teaching in Auditing: Fifteen Cases on Judgement and Decision Making. The Accounting Review, 59(1), 78-‐97.

Bamber, E, M. (1983). Expert Judgement in the Audit Team: A Source Reliability Approach. Journal of Accounting Research, 21(2), 396-‐412.

Brickley, K. F.(2003). From Enron to Worlcom and beyond: life and crime after SOX. Working paper, University in St Louis, School of Law.