66

PRELIMINARY RESULTS PRESENTATION YEAR ENDED 31 MARCH 2010 www.britishland.com

| Date post: | 04-Jun-2018 |

| Category: |

Documents |

| Upload: | truongtram |

| View: | 216 times |

| Download: | 0 times |

PRELIMINARY RESULTSPRESENTATIONYEAR ENDED 31 MARCH 2010 www.britishland.com

CHRIS GRIGGChief Executive

3

Today’s Agenda

Chris Grigg Overview

Graham Roberts Financial Performance

Steve Smith Portfolio & Market Outlook

Chris Grigg Looking Forward

4

Strong Recovery In Valuation

Portfolio Valuation Movement1

‐5

0

5

10

15

20

1H 2H FY

British Land

Annual Capital Return vs. IPD2

0

2

4

6

8

10

12

14

16

18

Retail Offices Total Portfolio

British Land IPD

1 Valuation movement (net of capital expenditure) of properties held at the balance sheet date2 Calculated by IPD for UK assets on average capital employed and excluding capitalised interest

+16.0%

+13.5%

‐2.1%

change (%) YoY change (%)

5

Strong NAV Growth And Total Returns

Q4 FY

Y/E 31 Mar 2009 2010 2009 2010

Net Asset Value1 £3,387m £4,407m £3,387m £4,407m

Net Asset Value1 per share 398p 504p 398p 504p

Underlying Profit Before Tax2 £61m £62m £268m £249m

Underlying Diluted EPS2 8.7p 7.0p 41.0p 28.4p

Dividend per share 6.5p 6.5p 29.8p 26.0p

Total Return +16.6% +33.5%

1 EPRA (European Public Real Estate) basis2 Excluding gains on property revaluations & disposals, and intangible asset movements

6

Retail: Performance Highlights

• Leasing activity up 30%

• Average length of new leases broadly in line with portfolio

• £12m added to rent roll in 09/10

• Occupancy levels increased from 98% to 99%1

• Tenants in administration down from 2.2% to 0.6%

• Improving rental value trends

New Lettings, Renewals and Rent Reviews

Y/E 31 Mar 2010 New Lettings

Renewals Reviews Total

Number 255 121 224 600

Sq ft (’000s) 864 977 3,593 5,434

Lease to first break (yrs) 9.9 14.5 n/a n/a

Annual Rent Increase £5.5m ‐£1.5m £7.7m £11.7m

1 Includes accommodation subject to asset management and under offer

7

Offices: Performance Highlights

• Occupancy levels 93%1

• Over 1m sq ft of developments completed: substantially let or sold

• Deals accretive to value: rents at 9% premium to ERV

• £25m added to rent roll in 09/10

Lettings of Buildings Completed in 2009/10

As at 31 Mar 2010 Sq ft (’000s)

Let Lease to 1st Break

ContractedRent (£m)

Of which let in 09/10 (£m)

Ropemaker Place, EC2 594 91% 16.3 years 25 15

Regent’s Place –10 & 20 Triton Street

3762 59% 15.8 years 10 10

Total 9702 77% 16.1 years 35 25

1 Includes accommodation subject to asset management and under offer2 Excludes residential units sold in 08/09

8

Asset Disposals Improve Portfolio Balance

Disposals• £1.3bn1

Retail• Reduced exposure to declining high street

locations• Sale of £84m1 mature/low growth retail

warehouses

Offices• Reduced exposure to large single assets • Greater ability to trade City cycles• Improved balance between City & West End

Property Disposals in 2009/10

BL Share £m

Broadgate JV 1,066

20 Department Stores & Shops 144

9 Retail Parks 84

Other 18

Total 1,312

1 BL share

9

Excellent Investments In Retail And Offices

• £247m1 of investments in retail and office sectors

• Potential to add value through asset management and development

− 50% stake in Tesco JV at Surrey Quays & Clifton Moor

− Sainsbury’s, Macclesfield

− 39 Victoria Street

• £29m on 2‐14 Baker Street (post year end)

1 BL share

10

New Developments Create Further Value

Regent’s Place (NEQ)• 500,000 sq ft1

• £232m development cost2

• Completion 2013

2‐14 Baker Street• 139,000 sq ft• £79m development cost2

• Completion 2013

4 & 6 Broadgate• c.700,000 sq ft• c.£175m development cost2,3

• Target completion 2014

1 Includes 120,000 sq ft of residential2 Cost to complete (excluding land and notional interest)3 BL Share – detailed cost, areas and planning subject to agreement and planning

11

Strengthened Management Team

Graham RobertsFinance Director

Steve SmithChief Investment

Officer

Tim RobertsHead of Offices

Charles MaudsleyHead of Retail and

Business Development

Chris GriggChief Executive

GRAHAM ROBERTSFinance Director

13

Financial Review

• 13.5%1 portfolio valuation uplift driving NAV2 growth of 27% to 504p

• Underlying profits3 down 7% to £249m, reflecting disposals and completion of new developments

• 2009/10 dividend of 26p – maintained for 2010/11

• Lower gearing at 47% LTV with investment capacity

1 Valuation movement (net of capital expenditure) for properties held at the balance sheet date, including developments and purchases2 EPRA basis3 Excludes gains on property revaluations and disposals, and intangible asset movements

14

Gross Asset Value

Reconciliation of Gross Asset Value

0

2

4

6

8

10

2009 Broadgate JV Disposals Investment Revaluations 2010

Equity Financed Debt Financed

Portfolio£8.6bn

Portfolio£8.5bn

Gross Asset Value (£bn)

15

Net Asset Value Per Share 504p

Reconciliation of Net Asset Value1 NAV Growth

Q42010

FY2010

NAV per share growth 15.1% 26.6%

Drivers of Valuation Increase

Q42010

FY2010

Valuation increase 7.5% 13.5%

Initial yield compression 33 bps 75bps

ERV growth2 1.2% ‐6.2%0

1

2

3

4

5

2009 Disposals RetainedEarnings

Revaluations 2010

£3.4bn

£4.4bn

1 EPRA basis2 Standing investments like for like, IPD basis (excluding Europe)

Net Asset Value (£bn)

Retail Performance

• Portfolio outperformed IPD by 4.8% (Q4 by 1.7%)1

• £4m pa2 of new rent from lettings & rent reviews in Q4

• Pace of ERV decline slowed in Q4 to ‐0.2%

16

Retail Performance

Y/E 31 Mar 2010 Value

£m

Increase ERVGrowth

%3

Initial yieldcompression

Top‐up initial yield4£m %

Retail warehouses 2,675 345 14.8 ‐3.7 122 bps 6.3%

Superstores 1,302 202 18.4 1.2 87 bps 5.5%

Shopping centres 1,189 36 3.2 ‐5.7 15 bps 7.0%

Department stores 436 77 21.5 ‐9.0 103 bps 6.9%

All Retail 5,602 660 13.4 ‐3.7 90bps 6.3%

1 BL capital return relative to IPD (calculated by IPD)2 Increase in BL share of net effective rent (taking into account tenant incentives)3 Standing investments like for like, IPD basis (excluding Europe)4 Gross yield (without notional purchaser’s costs), adding back rent frees and contracted rental uplifts

17

1 BL capital return relative to IPD (calculated by IPD)2 Increase in BL share of net effective rent (taking into account tenant incentives)3 Standing investments like for like, IPD basis (excluding Europe)4 Gross yield (without notional purchaser’s costs), adding back rent frees and contracted rental uplifts5 Principally development land

Office Performance

• Portfolio outperformed IPD by 3.8% (Q4 by 5.3%)1

• £66m valuation uplift in Q4 from lettings agreed above ERV

• £20m pa2 of new rent from lettings & rent reviews in Q4

Office Performance

Y/E 31 Mar 2010 Value

£m

Increase ERVGrowth

%3

Initial yieldcompression

Top‐up initial yield4£m %

City 1,735 203 13.3 ‐9.3 29 bps 7.3%

West End 967 132 15.8 ‐8.0 51 bps 6.1%

Provincial 34 (1) ‐2.3 n/a5 n/a5 n/a5

All Office 2,736 334 13.9 ‐8.0 37 bps 6.9%

18

Underlying Profit Before Tax

0

50

100

150

200

250

Q1 ‐ Q3 Q4 Full Year

Summary Income Statement1

Q4 2010£m

FY 2010£m

Gross rental income 132 561

Property outgoings (6) (16)

Fees & other income 8 15

Admin expenses (16) (65)

Net interest costs2 (56) (246)

Underlying Profit 62 249

1 With proportional consolidation of Funds & Joint Ventures2 Interest capitalised on developments £13m (Q4: £nil)

£249m

£187m

£62m

Underlying Profit Before Tax £249m (Q4: £62m)

£m

191 With proportional consolidation of Funds & Joint Ventures

Summary Income Statement1

Year ended 31 Mar 2009 2010

Gross rental income 650 561

Property outgoings (52) (16)

Fees & other income 20 15

Administrative expenses (58) (65)

Net interest costs (292) (246)

Underlying Profit 268 249

Underlying EPS 41.0 28.4p

Dividend per share 29.8p 26.0p

Reconciliation of Underlying Profit1

Underlying Profit – Y/E 31 Mar 2009 268

Credit risk provision 17

Share incentive write back (7)

Y/E 31 Mar 2009 ‐ adjusted 278

Disposals less acquisitions(Broadgate £12m & Meadowhall £8m)

(33)

Rent reviews, new lettings and renewals 14

Lease determinations & expiries (7)

Developments (22)

Impact of rights issue proceeds 8

Current year release of credit provision 16

Management & performance fees (5)

Underlying Profit – Y/E 31 Mar 2010 249

Income Statement

20

Analysis of Gross Rental Income1

Year ended 31 Mar 2009 2010

Properties owned throughout2

Retail

Offices

Other

Total – like for like

270

111

4

385

275

110

5

390

+ 2.1%

‐ 0.4%

+2.6%

+ 1.4%

Fixed & minimum uplifts3 63 63

Acquisitions 4 22

Disposals 183 63

Developments 11 19

Other4 4 4

Total 650 561 ‐ 13.7%

1 With proportional consolidation of Funds & JVs2 Investment properties subject to open market reviews and owned throughout the current and comparative periods 3 Rental income from fixed and minimum guaranteed rent reviews is recognised on a straight line basis4 Includes surrender premiums, asset management determinations, back rents and other accounting adjustments

Rental Income Growth

• Gross rental income down 13.7%

• 1.4% like for like income growth

− Retail warehouses up 3.7%

− Superstores up 3.1%

− West End offices up 2.1%

− City offices down 1.2%

− Shopping centres down 2.2%

21

Analysis of Gross Reversion1 – Cash & Accounting basis

£m pa Cash flow basis

Accounting basis

Annualised rents 485

524Expiry of rent frees and fixed/minimum uplifts

61

Total contracted 546 524

Letting of current vacant space

23 19

Rent reviews 8 8

Gross reversion 577 551

• High quality existing income flow

• Only 7% of rent expiring over next 3 years

• Gross reversion of £577m (or £551m on accounting basis) excludes:

− Future lettings & lease renewals

− Future rental growth

− Future investment

− c.£500m of developments

Future Income Growth Potential

1 Within 5 years – includes rent reviews and letting of vacant space at current ERV (as determined by external valuers)

22

Dividends

• Q4 Dividend 6.5p1, giving 26p for full year

• Full year 2010/11 dividend of 26p reflecting

− Strong income profile from prime portfolio

− Embedded growth potential from lettings and asset management

− Future earnings growth from capital recycling and investments

• Approach remains to pass income through to investors consistent with sustainable rental growth

FY 2010 Dividend Cover

On Earnings 1.1x

On cash profits2 0.9x

Cash dividend (i.e. exc. scrip) on cash profits2,3

1.4x

1 Property Income Distribution (PID) of the cash dividend is nil2 Underlying EPS less spreading of tenant incentives & guaranteed rent increases, and non‐cash administrative expenses3 40% scrip take up for last 4 quarters

231 With proportional consolidation of Funds & JVs (unless stated as Group)2 Annualised rent plus expiry of rent frees & contracted rental increases (net of lease expiries)

Financing statistics

As at 31 Mar1 2009 2010

Portfolio valuation £8.6bn £8.5bn

EPRA Net debt £4.9bn £4.1bn

LTV 57% 47%

LTV ‐ Group 46% 25%

Average debt maturity 12.7 years 11.1 years

Group debt maturing over the next 3 years

£531m £431m

Committed undrawn facilities – Group

£3.0bn £2.9bn

Strong Balance Sheet And Liquidity

Prime assets

• Retail occupancy 99%

• Office occupancy 93%

• High % of modern buildings

• 13 years average lease length

• 98% of current rent contracted in 3 years time

Finance

• Long average debt maturity

• Broad sources of existing drawn debt

• Substantial committed undrawn facilities

• Improving trend for lending markets

Gearing policy adapted to market cycles –maximum 55% LTV

STEVE SMITHChief Investment Officer

25

Retail: Strong Demand For Large Flexible Formats

• Large retailers significantly increase market share

• Increased competition and margin pressure

IPD income growth – last 5 years3 % pa

Retail Parks +4.1%

Superstores +5.3%

Shopping Centres +1.8%

High Street shops +1.1%

All Retail +2.8%

• Concentration of sales in fewer larger formats

• 50% of retail sales in 200 locations in 1971 vs 90 locations in 20082

• Polarisation of performance between different formats and locations

1 ONS2 CBRE3 IPD Quarterly Index

15%

20%

25%

30%

35%

40%

45%

88 90 92 94 96 98 00 02 04 06 08

Share of all UK Retail Sales1

Large Food Retailers

Small Retailers

Large Non‐Food Retailers

% All Retail Sales

26

Meeting Retailer And Consumer Needs: Glasgow Fort

• Premier 390,000 sq ft open A1 fashion park built in 2005

• Well located, adjacent to M8

• Convenient out of town location

• Flexible and low cost

− Average rent at £39psf

− Average ERV at £43psf

27

Meeting Retailer And Consumer Needs: Glasgow Fort

• High occupancy rate 97%

• Income growth of 7.4% pa since 2005

• Annual footfall of c.13m

• 10 new lettings in 09/10 at 4% above ERV

• 175,000 sq ft consented extensions, 80,000 sq ft M&S pre let

Food Outlets4%

General Retail 17%

Fashion & Footwear

50%

Other 7%

Strong Mix of 67 High Quality Occupiers

Health & Beauty 10%

Home, Books, Entertainment

13%

28

Offices: Demand For Modern Working Environment

Average City Development Size1

0

25

50

75

100

125

150

175

82 85 88 91 94 97 00 03 06 09

City & West End Take‐up1

0

3

6

9

12

FY 05 FY 06 FY 07 FY 08 FY 09 Q1 10

Other Grade A

1 Jones Lang LaSalle

’000 sq ft m sq ft

29

Meeting Office Occupiers Needs: Regent’s Place

• 1.2 m sq ft of mixed office and retail

• Further 500,000 sq ft: starting soon

• Good infrastructure (national rail/6 tube lines)

30

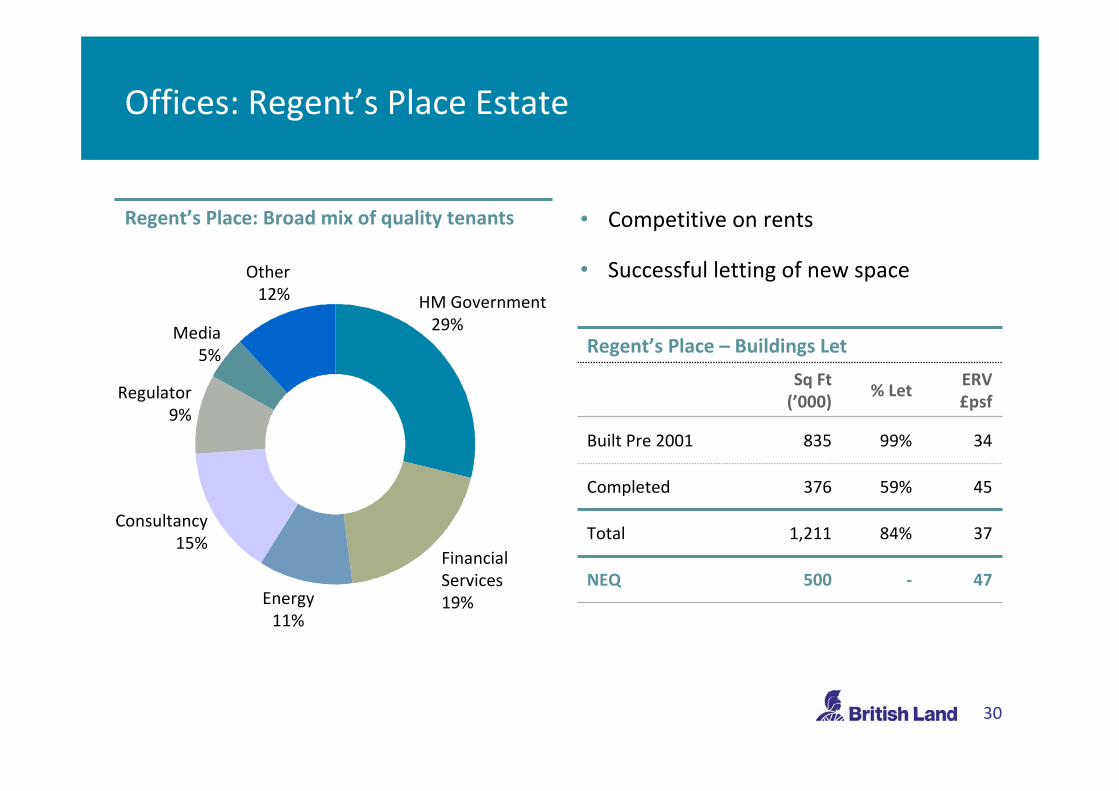

Offices: Regent’s Place Estate

• Competitive on rents

• Successful letting of new space

Regent’s Place – Buildings Let

Sq Ft(’000)

% LetERV£psf

Built Pre 2001 835 99% 34

Completed 376 59% 45

Total 1,211 84% 37

NEQ 500 ‐ 47

Regent’s Place: Broad mix of quality tenants

HM Government29%

FinancialServices19%Energy

11%

Consultancy15%

Regulator9%

Media5%

Other12%

31

Offices: Benefiting From Demand For Modern Space

• Average age 15 years versus 32 for IPD

• 37% of portfolio less than 5 years old (IPD: 9%, exc. BL)

• High occupancy and long lease length

• Strong letting performance in 2009/10

− BL lettings = 10% of all Grade A lettings

− Rents achieved at 11% above ERV

British Land Office Portfolio vs IPD

At 31 Mar 2010 Average Age

Occupancy Rate

Lease Length

British Land 15 years 93% 9.6 years

IPD 32 years 88% 7.2 years

32

Capital Recyling To Strengthen The Portfolio

• Reduced exposure to the high street

• Sold low growth, mature properties

• Reduced exposure to large assets through joint ventures

• Focused portfolio on properties most likely to deliver future income and capital growth

Portfolio Weighting by Value

As at 31 Mar 2005 2010

High Street Shops 10% 5%

Retail Warehouses 13% 32%

Superstores 12% 15%

Shopping Centres 19% 14%

City Offices 31% 20%

West End Offices 5% 11%

Other 10% 3%

33

Portfolio Positioned For Growth

ERV Growth Forecasts by Sector1

0 2 4 6 8 10

Industrial

Provincial offices

West End offices

City offices

Shops

Shopping Centres

Superstores

Retail Parks

YOY Change (%) ‐ next 5 years

BL Sector Weightings Relative to IPD

‐15 ‐10 ‐5 0 5 10 15 20

Industrial

Provincial offices

West End offices

City offices

Shops

Department Stores

Shopping Centres

Superstores

Retail Parks

1 PMA Spring 2010 forecast

34

Offices: A Shift In Emphasis

• City offices volatile

− Supply/demand dynamic impacted by Canary Wharf

− Adopting a more tactical strategy

• West End greater long‐term growth potential

− Increase weighting over time

− Adopting long‐term strategy

35

Market Outlook: Shortage Of Prime London Office Space

0

2

4

6

2010 2011 2012 2013 2014 2015

City West End

0

2

4

6

8

10

12

14

16

85 87 89 91 93 95 97 99 01 03 05 07 09 11 130

2

4

6

8

10

12

14

16

18

20

Available u/c

Completed

Vacancy %

%

Central London Development & Vacancy1

(m sq ft)City & West End Lease Expiries1

(m sq ft)

1 Drivers Jonas Deloitte

36

Market Outlook: Retail Polarising Between Key Locations And The Rest

• Weak consumer demand – impact of fiscal measures

• Overall retail rents expected to

− decline in 2010

− grow by 2.6% pa1 between 2011 and 2015

• Continued demand for key locations

• British Land portfolio well positioned to deliver rental and value growth

1 PMA Spring 2010 forecast

37

Market Outlook: Investment Opportunities

• Shortage of prime with significant investor demand

• Distressed assets beginning to come to market but generally poor quality

• Secondary values set to move out

• Continuing to screen significant number of opportunities

• Better value where assets require repositioning

38

Future Income Potential

• Reversionary potential ahead of IPD

• Additional reversionary potential from above market ERV growth

Reversionary Profile compared with IPD1

‐10% 0% 10% 20% 30%

IPD

British Land

Over‐renting < 5yrs Over‐renting > 5 yrs Rent FreesReversions < 5yrs Vacancies Reversions > 5yrsDevelopments

1 As calculated by IPD

39

Future Potential From Developments

Potential Retail Extensions

Sq ft (’000)

BLShare

Whiteley Village 322 50%

Glasgow Fort 175 36%

Broughton Park 140 36%

Fort Kinnaird 110 16%

Total 747

Office Developments

Sq ft (’000s)

Development Cost1

Total Cost2,3Current ERV £psf4

Completion

Baker Street 139 £79m £100m 68 2013

NEQ, Regent’s Place 500 £232m £294m 47 2013

Broadgate c.700 c.£175m c.£250m n/a5 2014

1 Including residential 2 BL Share3 Including land and notional interest 4 Current estimated headline rent (excluding provision for tenants’ incentives)5 Non‐binding Heads of Terms agreed with UBS for pre‐let of entire building

40

CHRIS GRIGGChief Executive

• Outperformed IPD in volatile market conditions

• Made excellent purchases in both retail and offices

• New office developments offer strong returns

41

Generating Superior Total ReturnsGenerating Superior Total Returns

A Good Year

• Focused on areas predicted to outperform

• Creating value through asset management

− Rental growth

− New lettings

− Reversion

42

Well Positioned For Growth From Existing Portfolio

Generating Superior Total ReturnsGenerating Superior Total Returns

• Demand for prime property continues

• Drivers of value – buying, developing and managing assets well

• Property expertise and access to capital give us a competitive edge

43

Opportunity For Further Value Creation

Generating Superior Total ReturnsGenerating Superior Total Returns

44

APPENDIX

45

£m GroupFunds& JVs

Mar 2010 Mar 2009

Total properties 4,152 4,387 8,539 8,625

Net debt (1,511) (2,570) (4,081) (4,941)

Other net liabilities 81 (132) (51) (297)

EPRA Net Assets 2,722 1,685 4,407 3,387

EPRA Diluted NAV per share 504p 398p

Loan to value ratio – Group 25% 46%

Loan to value ratio – inc. share of Funds & JVs 47% 57%

EPRA Balance Sheet (Proportional Consolidation)

46

Mar 2010 £m Pence per share Mar 2009 £m

Balance sheet (IFRS) net assets 4,208 481 3,209

Deferred tax arising on revaluation movements 43 5 25

Mark to market on effective cash flow hedges and related debt adjustments

126 15 153

Adjust to fully diluted on exercise of share options 30 3 ‐

EPRA NAV 4,407 504 3,387

Deferred tax arising on revaluation movements (43) (5) (25)

Mark to market of debt and derivatives 156 18 963

EPRA NNNAV 4,520 517 4,325

Reconciliation Of EPRA NAV & NNNAV

47

£m Group Funds & JVs 2009/10 2008/9

Net rental income 337 208 545 598

Fees and other income 13 2 15 20

Administrative expenses (55) (10) (65) (58)

Net interest costs (127) (119) (246) (292)

Underlying profit before tax 168 81 249 268

Net valuation movement (includes disposals) 496 412 908 (4,074)

Realisation of cash flow hedges/non‐recurring items ‐ (9) (9) (119)

Amortisation of intangible asset (15) ‐ (15) (14)

Tax ‐ Tax charge relating to underlying profit (2) (3) (5) (9)

‐ Other tax arising 14 (2) 12 67

Profit/(Loss) for the full year after tax 661 479 1,140 3,881

Income Statement (Proportional Consolidation)

48

£m 2009/10 2008/9

IFRS Profit/(Loss) before tax 1,128 (3,928)

Net valuation movement (includes disposals) (908) 4,074

Deferred and current taxation of joint ventures & funds 5 (11)

Amortisation of intangible asset 15 14

Realisation of cash flow hedges/non‐recurring items 9 119

Underlying profit before tax 249 268

Reconciliation Of Underlying Profit Before Tax

49

Gross Rental Income (£m pa) 12 months to 31 Mar 20101 Annualised as at 31 Mar 20102

Group Funds & JVs Total Group Funds & JVs Total

Retail Warehouses 102 63 165 102 65 167

Superstores 8 60 68 10 60 70

Shopping Centres 17 57 74 16 59 75

Department Stores3 36 2 38 33 ‐ 33

All Retail 163 182 345 161 184 345

City Offices 116 36 153 24 86 110

West End Offices 40 ‐ 40 51 ‐ 51

Provincial 1 ‐ 1 1 ‐ 1

All Offices 157 36 193 76 86 163

Other 18 ‐ 18 17 ‐ 17

Total – recurring items 338 219 557 254 270 524

– non‐recurring items4 4 ‐ 4

Total 342 219 561

1 Gross rental income per Income Statement under IFRS (proportionally consolidated) analysed by sector2 Annualised contracted gross rental income under IFRS (proportionally consolidated) analysed by sector as at 30 September 20093 Including High Street4 Including surrender premiums and back rents

Gross (Accounting) Rental Income – Sectoral Analysis

50

Under IFRS contracted rent and cash flows will differ 1 During rent free periods, IFRS requires rent to be recognised ahead of the related cash flow and allocated evenly over the lease term to the earliest termination date

2 IFRS requires the total rental income relating to fixed and minimum guaranteed rent reviews to be recognised ahead of the related cash flow and allocated evenly over the lease term to the earliest termination date

Gross Rental Income £m 2009/10 2010/11 2011/12 2012/13 2013/14 2014/15

Lettings with rent free periods1

Retail 42 46 46 44 43 28

Offices & other 37 51 53 53 52 51

Total rent (accounting basis) 79 97 99 97 95 79

Of which total cash flow 64 74 80 84 97 88

Of which SIC 15 rent free adjustment 15 23 19 14 (2) (9)

Lettings with fixed and minimum uplifts2

Retail 38 40 40 40 40 40

Offices & other 30 32 32 32 32 32

Total rent (accounting basis) 68 72 72 72 72 72

Of which total cash flow 55 60 62 65 66 68

Of which IAS 17 fixed uplift adjustment 13 12 10 7 6 4

Contracted Rental Increases

511 Excludes mark to market on effective cash flow hedges and related debt adjustments2 Underlying profit before interest and tax (UPBIT)/net interest

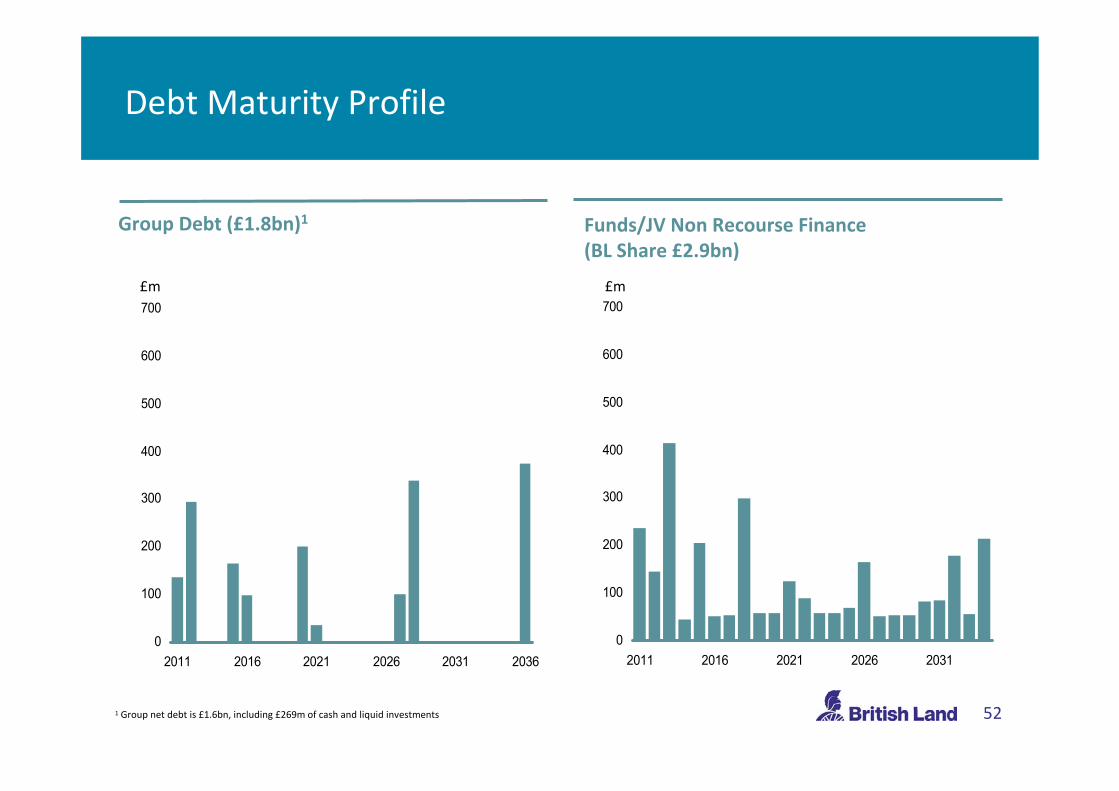

Group £m

Funds & JVs £m

Total £m

Gross debt 1,781 2,888 4,669

Market value of derivatives 38 99 137

Cash & liquid investments (269) (327) (596)

EPRA adjustments1 (39) (90) (129)

EPRA Net debt 1,511 2,570 4,081

Average interest rate 5.3% 5.1% 5.2%

Interest cover2 2.3x 1.7x 2.0x

Net Debt

52

Funds/JV Non Recourse Finance (BL Share £2.9bn)

0

100

200

300

400

500

600

700

2011 2016 2021 2026 20310

100

200

300

400

500

600

700

2011 2016 2021 2026 2031 2036

Group Debt (£1.8bn)1

1 Group net debt is £1.6bn, including £269m of cash and liquid investments

Debt Maturity Profile

£m £m

53

Sales £m

Price BL Share

50% interest in Broadgate, EC2 1,066 1,066

18 Department Stores 209 139

9 Retail Warehouses 252 84

8‐10 Throgmorton, EC2 7 7

2 High Street Shops 5 5

Other 14 11

Total 1,553 1,312

Purchases £m

BL Share

Surrey Quays Shopping Centre 49

Clifton Moor Retail Park 39

Hylton Riverside Retail Park 7

Sainsbury’s, Macclesfield 32

39 Victoria Street, SW1 40

HUT Convertible Bonds 43

Additional PREF Units 35

Other 2

Total 247

2‐14 Baker Street (post year end) 29

Sales & Purchases

54

1 Hercules Unit Trust (HUT)2 Joint Venture with The Crown Estate3 Joint Venture with Universities Superannuation Scheme4 Joint Venture with Goodman Real Estate (UK) Limited

5 Subject to development agreement with Countryside Properties Limited6 In partnership with Network Rail7 Joint Venture with Canada Quays Limited

Sector Sq ft (’000) Planning

Fort Kinnaird1,2 Retail Warehouses 110 Detailed

Glasgow Fort1 Retail Warehouses 175 Detailed

Broughton Park1 Retail Warehouses 140 Detailed

Whiteley Village3 Retail Warehouses 322 Outline/Detailed

The Leadenhall Building City Office 610 Detailed

Colmore Row Provincial Office 280 Detailed

Meadowhall Additional Land Mixed Use 2,200 Outline

New Century Park4 Mixed Use 1,000 Outline

Theale5 Residential Potential Land Sale Detailed

Euston Station6 Mixed Use Master Planning in Progress Pending

Canada Water7 Mixed Use Master Planning in Progress Outline/Detailed

Prospective Developments

55

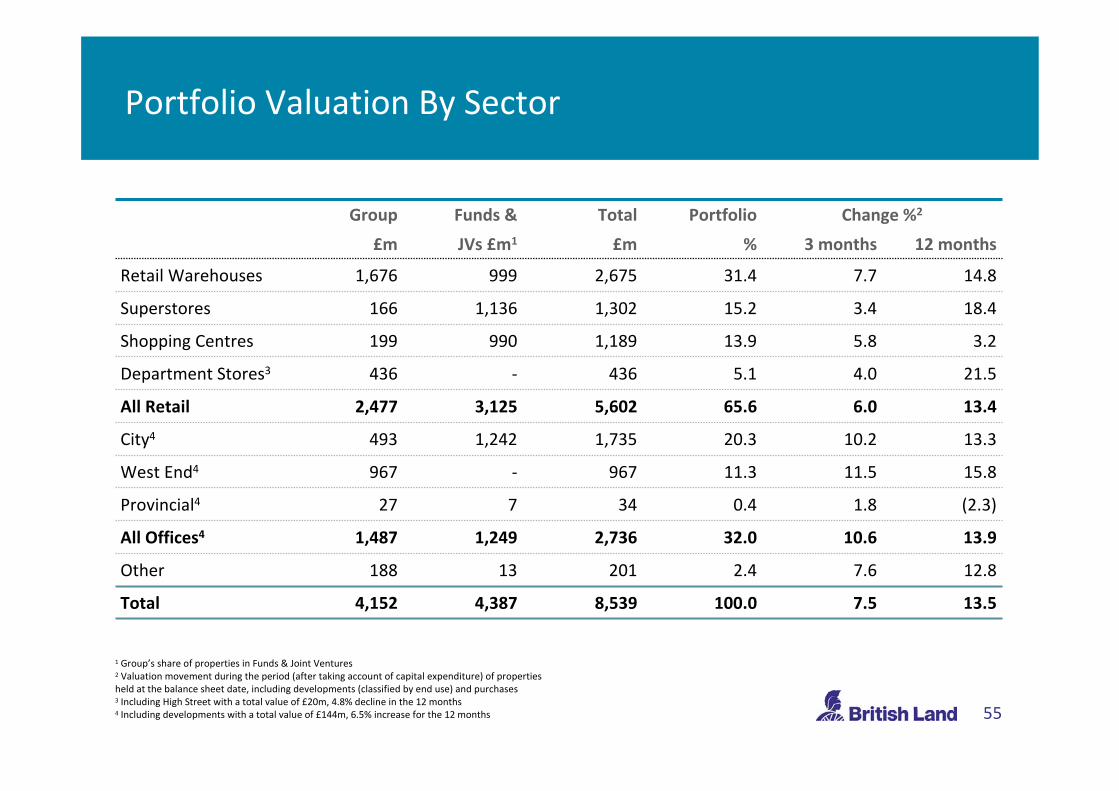

Group Funds & Total Portfolio Change %2

£m JVs £m1 £m % 3 months 12 months

Retail Warehouses 1,676 999 2,675 31.4 7.7 14.8

Superstores 166 1,136 1,302 15.2 3.4 18.4

Shopping Centres 199 990 1,189 13.9 5.8 3.2

Department Stores3 436 ‐ 436 5.1 4.0 21.5

All Retail 2,477 3,125 5,602 65.6 6.0 13.4

City4 493 1,242 1,735 20.3 10.2 13.3

West End4 967 ‐ 967 11.3 11.5 15.8

Provincial4 27 7 34 0.4 1.8 (2.3)

All Offices4 1,487 1,249 2,736 32.0 10.6 13.9

Other 188 13 201 2.4 7.6 12.8

Total 4,152 4,387 8,539 100.0 7.5 13.5

1 Group’s share of properties in Funds & Joint Ventures2 Valuation movement during the period (after taking account of capital expenditure) of properties held at the balance sheet date, including developments (classified by end use) and purchases3 Including High Street with a total value of £20m, 4.8% decline in the 12 months 4 Including developments with a total value of £144m, 6.5% increase for the 12 months

Portfolio Valuation By Sector

56

£m

Valuation as at 31 Mar 2009 8,625

Broadgate JV (1,096)

Disposals (363)

Purchases, development & other capex 352

Change in ownership in PREF 108

Revaluations 935

Decrease in head lease liabilities 6

Other1 (28)

Valuation as at 31 Mar 2010 8,539

1 Other adjustments relating to accounting adjustments for equalising rents (tenant incentives and guaranteed uplifts), as well as foreign exchange movements

Reconciliation Of Portfolio Valuation

57

1 Annualised contracted rent (100% basis)2 Including accommodation subject to asset management and under offer3 To first break 4 Excluding NEQ

Sq ft’000

BL Share

Rent£m pa1

Occupancyrate %2

Lease length, yrs3

1 Broadgate 4,400 50% 184 95.9 8.2

2 Meadowhall Shopping Centre 1,400 50% 78 98.1 11.2

3 Regent’s Place4 1,210 100% 42 83.7 9.8

4 Ropemaker Place 590 100% 25 91.1 16.9

5 Fort Kinnaird Shopping Park 510 18% 20 100.0 7.7

6 New Mersey Shopping Park 470 18% 16 100.0 10.1

7 Glasgow Fort Shopping Park 390 36% 16 97.3 8.6

8 Teesside Shopping Park 410 100% 13 100.0 10.5

9 Bon Accord Shopping Centre 490 50% 15 96.6 7.5

10 Parkgate Shopping Park 560 36% 12 100.0 10.0

Top 10 Properties

58

1 Within next 5 years2 Of which £29m pa within next 3 years 3 Including future portfolio voids on break/expiry

Annualised Rent – Cash Flow Basis

Retail£m pa

Office£m pa

Other£m pa

Total£m pa

Annualised rents 338 131 16 485

Contracted from fixed uplifts and expiry of rent free periods1,2

12 47 2 61

Rent reviews & lease renewals1,3 9 (23) ‐ (14)

Letting of current vacant space 7 15 1 23

Reversionary income 366 170 19 555

Future Rent Profile

59

Office

% of total rent

UBS 4

HM Government 2

RBS 2

Macquarie Group 2

Bank of Tokyo‐Mitsubishi UFJ 2

Herbert Smith 2

JP Morgan 1

Reed Smith 1

Deutsche Bank 1

Mayer Brown 1

Retail

% of total rent

Tesco 8

Sainsbury’s 7

Debenhams 4

Homebase 2

Kingfisher (B&Q) 2

Next 2

Asda 1

Boots 1

Curry’s 1

M&S 1

Top 10 Retail & Office Customers

60

1 Average contracted passing rent (post expiry of rent free periods) 2 Average Headline ERV3 Including High Street

Excluding developments (£psf pa) Rent1 ERV2

Retail Warehouses 22 23

Superstores 21 21

Shopping Centres 26 29

Department Stores3 11 13

All Retail 21 22

City 46 39

West End 40 38

All Offices 44 39

Other 16 18

Total 25 25

Average Rent psf

61

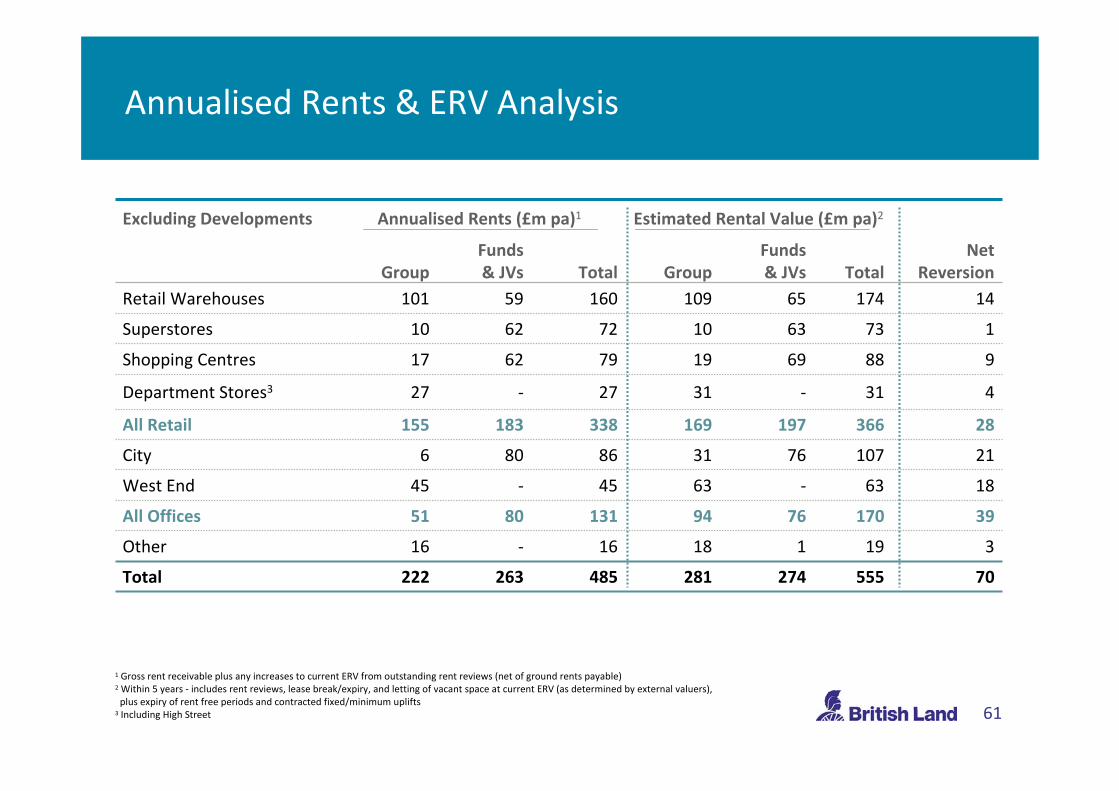

1 Gross rent receivable plus any increases to current ERV from outstanding rent reviews (net of ground rents payable) 2 Within 5 years ‐ includes rent reviews, lease break/expiry, and letting of vacant space at current ERV (as determined by external valuers), plus expiry of rent free periods and contracted fixed/minimum uplifts

3 Including High Street

Excluding Developments Annualised Rents (£m pa)1 Estimated Rental Value (£m pa)2

GroupFunds& JVs Total Group

Funds& JVs Total

Net Reversion

Retail Warehouses 101 59 160 109 65 174 14

Superstores 10 62 72 10 63 73 1

Shopping Centres 17 62 79 19 69 88 9

Department Stores3 27 ‐ 27 31 ‐ 31 4

All Retail 155 183 338 169 197 366 28

City 6 80 86 31 76 107 21

West End 45 ‐ 45 63 ‐ 63 18

All Offices 51 80 131 94 76 170 39

Other 16 ‐ 16 18 1 19 3

Total 222 263 485 281 274 555 70

Annualised Rents & ERV Analysis

62

1 After purchaser’s costs2 Without notional purchaser’s costs3 Adding back rent frees and contracted rental uplifts 4 Including High Street

Excluding developments (%) NetInitialYield1

GrossInitial Yield2

GrossTop‐up

Initial Yield2,3

GrossReversionary

Yield2

NetEquivalent

Yield1

Retail Warehouses 5.7 6.1 6.3 6.7 6.0

Superstores 5.2 5.5 5.5 5.6 5.2

Shopping Centres 6.0 6.7 7.0 7.4 6.4

Department Stores4 5.7 6.1 6.9 7.0 6.7

All Retail 5.6 6.1 6.3 6.6 6.0

City 4.9 5.2 7.3 6.5 6.1

West End 4.4 4.8 6.1 6.7 5.7

All Offices 4.7 5.1 6.9 6.5 5.9

Other 8.4 8.6 9.4 10.3 9.8

Total 5.4 5.8 6.6 6.7 6.0

Yield Profile

631 Including accommodation subject to asset management and under offer2 Including High Street

Excluding developments Average Lease Length (yrs) Occupancy Rate (%)

To Expiry To First Break Underlying1 Overall

Retail Warehouses 12.4 11.4 98.9 97.9

Superstores 17.6 17.6 100.0 100.0

Shopping Centres 11.4 10.8 97.9 95.9

Department Stores2 30.0 26.8 98.7 98.7

All Retail 14.8 13.9 98.9 97.9

City 12.2 10.0 95.0 93.3

West End 11.6 8.8 88.1 87.1

Provincial 22.0 18.9 100.0 100.0

All Offices 11.9 9.6 92.6 91.0

Other 21.2 20.9 93.8 93.8

Total 14.0 12.6 96.6 95.5

Lease Length & Occupancy

64

1 Excluding developments2 Including rent reviews currently outstanding3 Based on current ERV and assuming nil increase where ERV is lower than current passing rent4 Including High Street

Year to 31 March (£m pa)1 Annualised Rent Potential Uplift3

20112 2012 2013 Total 20112 2012 2013 Total

Retail Warehouses 54 18 24 96 2 1 ‐ 3

Superstores 14 6 2 22 1 ‐ ‐ 1

Shopping Centres 20 7 11 38 1 ‐ ‐ 1

Department Stores4 ‐ ‐ ‐ ‐ ‐ ‐ ‐ ‐

All Retail 88 31 37 156 4 1 ‐ 5

City 11 2 17 30 ‐ ‐ ‐ ‐

West End 4 5 7 16 ‐ ‐ ‐ ‐

All Offices 15 7 24 46 ‐ ‐ ‐ ‐

Other 2 ‐ ‐ 2 ‐ ‐ ‐ ‐

Total 105 38 61 204 4 1 ‐ 5

Rental Income Subject To Rent Review

651 Including High Street

Year to 31 March (£m pa) 2011 2012 2013 2014 2015 2011‐13 2011‐15

Retail Warehouses 2 2 3 6 4 7 17

Superstores ‐ ‐ ‐ ‐ ‐ ‐ ‐

Shopping Centres 4 2 3 6 3 9 18

Department Stores1 ‐ ‐ ‐ ‐ ‐ ‐ ‐

All Retail 6 4 6 12 7 16 35

City 8 ‐ ‐ 12 10 8 30

West End 2 4 8 ‐ 1 14 15

Provincial ‐ ‐ ‐ ‐ ‐ ‐ ‐

All Offices 10 4 8 12 11 22 45

Other ‐ ‐ 1 1 ‐ 1 2

Total 16 8 15 25 18 39 82

% of Total Rent 3% 1% 3% 4% 3% 7% 14%

Rental Income Subject To Lease Break Or Expiry

66

The information contained in this presentation has been extracted largely from the Half Year Results Announcement for the year ended 31 March 2010.

This presentation may contain certain “forward‐looking” statements. By their nature, forward‐looking statements involve risk and uncertainty because they relate to future events and circumstances. Actual outcomes and results may differ materially from any outcomes or results expressed or implied by such forward‐looking statements. Any forward‐looking statements made by or on behalf of British Land speak only as of the date they are made and no representation or warranty is given in relation to them, including as to their completeness or accuracy or the basis on which they were prepared. British Land does not undertake to update forward‐looking statements to reflect any changes in British Land’s expectations with regard thereto or any changes in events, conditions or circumstances on which any such statement is based.

This presentation is made only to investment professionals as defined in Article 19 of the Financial Services and Markets Act 2000 (Financial Promotion) Order 2005 ('the FP Order'). The content of this presentation has not been approved by a person authorised under the Financial Services and Markets Act 2000 (“FSMA”). Accordingly, this presentation may only be communicated in the UK with the benefit of an exemption set out in the FP Order. An investment professional includes:

(i) a person who is authorised or exempt under FSMA; and

(ii) a person who invests, or can reasonably be expected to invest, on a professional basis for the purposes of a business carried on by him; and

(iii) a government, local authority (whether in the United Kingdom or elsewhere) or an international organisation; and

(iv) any director, officer, executive or employee of any such person when acting in that capacity.

This presentation is published solely for information purposes. This presentation does not constitute an offer to sell or the solicitation of an offer to subscribe for or buy any security, nor a solicitation of any vote or approval in any jurisdiction, nor shall there be any sale, issuance or transfer of the securities referred to in this presentation in any jurisdiction in contravention of applicable law. No representation or warranty, either express or implied, is provided in relation to the accuracy, completeness or reliability of the information contained herein.

The distribution of this presentation in jurisdictions other than the UK may be restricted by law and therefore any persons who are subject to the laws of any jurisdiction other than the UK should inform themselves about, and observe, any applicable requirements. This presentation has been prepared for the purpose of complying with English law and the City Code and the information disclosed may not be the same as that which would have been disclosed if this presentation had been prepared in accordance with the laws of jurisdictions outside the UK.

All opinions expressed in this presentation are subject to change without notice and may differ from opinions expressed elsewhere.

Disclaimer