28

Premium Mobile Apps in North America -- Enterprise Preferences and Plans -- Jeanine Sterling, Senior Industry Analyst Mobile and Wireless Communications June 30, 2009

| Date post: | 20-Aug-2015 |

| Category: |

Business |

| Upload: | frost-sullivan |

| View: | 1,173 times |

| Download: | 1 times |

Premium Mobile Apps in North America-- Enterprise Preferences and Plans --

Jeanine Sterling, Senior Industry Analyst

Mobile and Wireless Communications

June 30, 2009

2

Today’s Focus Points

• Premium Mobile Apps in the Workplace: A Market Overview

• Enterprise Preferences and Plans (1Q Survey Results)

� Level of Perceived Need

� Deployment Plans

� Barriers to Implementation

� ROI Metrics

• Conclusions

3

Economic Downturn – Impacts Still Raining Down

• Financial crisis continues to strongly influence individual enterprise wireless strategies and expenditures.

• Companies remain in wait-and-see mode: Consumer sentiment is improving; however, unemployment figures remain high and conditions remain volatile.

• Frost & Sullivan Mobile and Wireless Advisory Board feedback:

o Cautious optimism

o Solid ROI a must on any new purchase

o Deployment slow-down remains in place

o SaaS model gaining in popularity

4

On the flip side…

• Mobile worker population is growing.

• A “changing of the guard” is taking place at management levels.

• Strong worker expectations exist re: mobile access to corporate applications and information.

• Both hard and soft benefits of premium mobile apps are being recognized and valued.

• IT software typically survives economic downturns in better shape than hardware.

However…. Is the North American enterprise really ready to deploy more than just wireless

email and mobile Internet access to its growing population of mobile workers?

5

Premium Mobile Apps in the Workplace-- A Market Overview --

6

Mobile Data Services: Continued Growth

0.0

20000.0

40000.0

60000.0

80000.0

100000.0

120000.0

140000.0

160000.0

180000.0

200000.0

2007 2008 2009 2010 2011 2012 2013 2014

Revenues (

$ M

illio

n)

0

5

10

15

20

25

30

35

40

Year

% o

f R

evenues

Mobile Service Revenues($ Million)

Mobile Data Revenues($ Million)

% of Revenues

• 2009 Mobile Data Services revenues are expected to comprise ~25% -- or $40.9 billion – of total mobile services revenues in U.S.

7

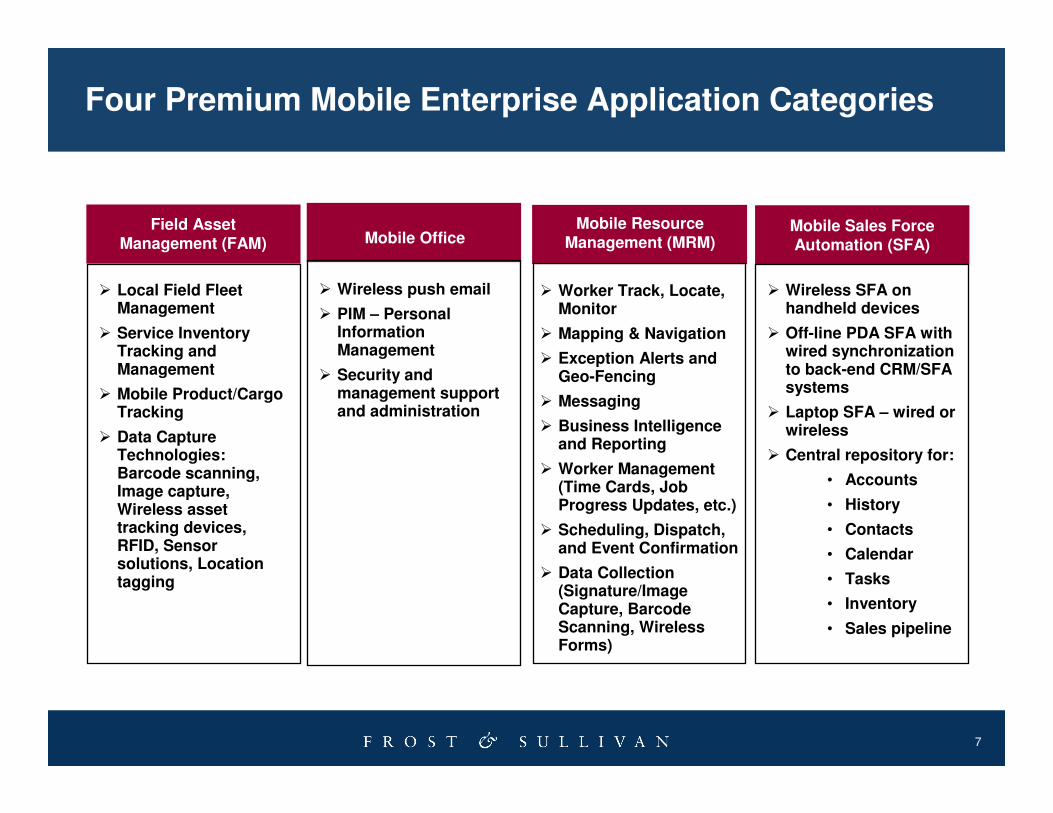

Four Premium Mobile Enterprise Application Categories

� Local Field Fleet Management

� Service Inventory Tracking and Management

� Mobile Product/Cargo Tracking

� Data Capture Technologies: Barcode scanning, Image capture, Wireless asset tracking devices, RFID, Sensor solutions, Location tagging

Field Asset Management (FAM) Mobile Office

� Wireless push email

� PIM – Personal Information Management

� Security and management support and administration

� Worker Track, Locate, Monitor

� Mapping & Navigation

� Exception Alerts and Geo-Fencing

� Messaging

� Business Intelligence and Reporting

� Worker Management (Time Cards, Job Progress Updates, etc.)

� Scheduling, Dispatch, and Event Confirmation

� Data Collection (Signature/Image Capture, Barcode Scanning, Wireless Forms)

Mobile Resource Management (MRM)

Mobile Sales Force Automation (SFA)

� Wireless SFA on handheld devices

� Off-line PDA SFA with wired synchronization to back-end CRM/SFA systems

� Laptop SFA – wired or wireless

� Central repository for:

• Accounts

• History

• Contacts

• Calendar

• Tasks

• Inventory

• Sales pipeline

8

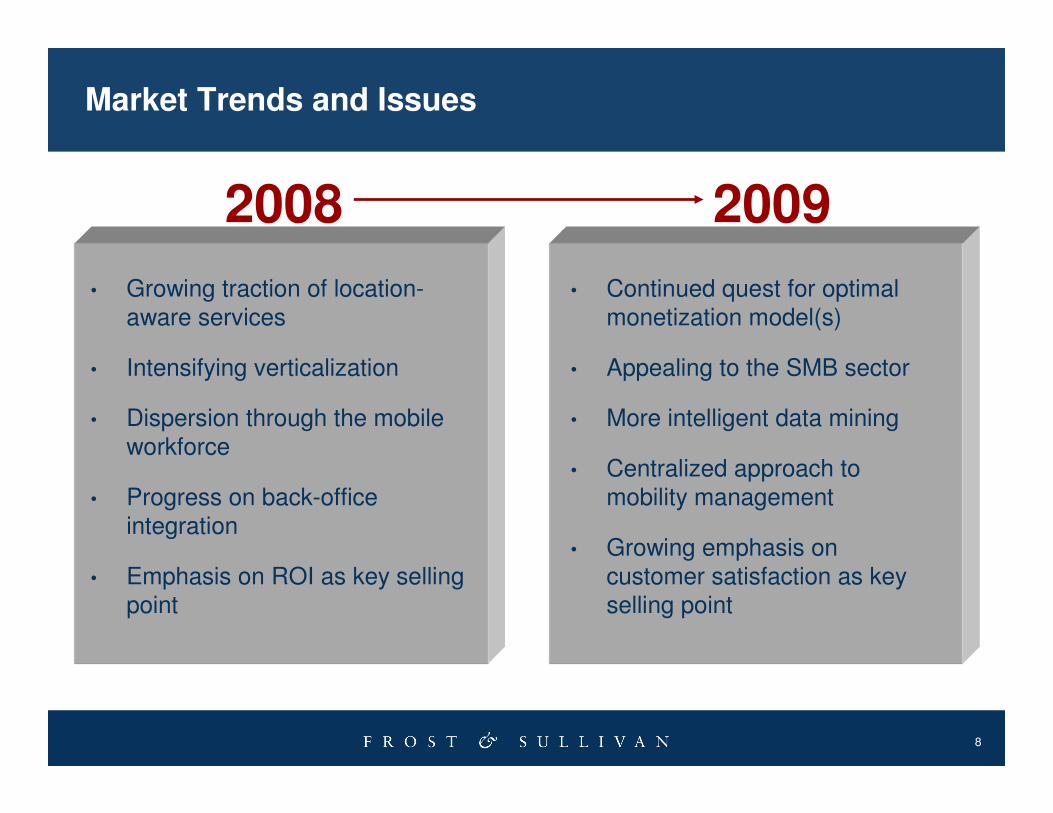

Market Trends and Issues

• Growing traction of location-aware services

• Intensifying verticalization

• Dispersion through the mobile workforce

• Progress on back-office integration

• Emphasis on ROI as key selling point

2008

• Continued quest for optimal monetization model(s)

• Appealing to the SMB sector

• More intelligent data mining

• Centralized approach to mobility management

• Growing emphasis on customer satisfaction as key selling point

2009

9

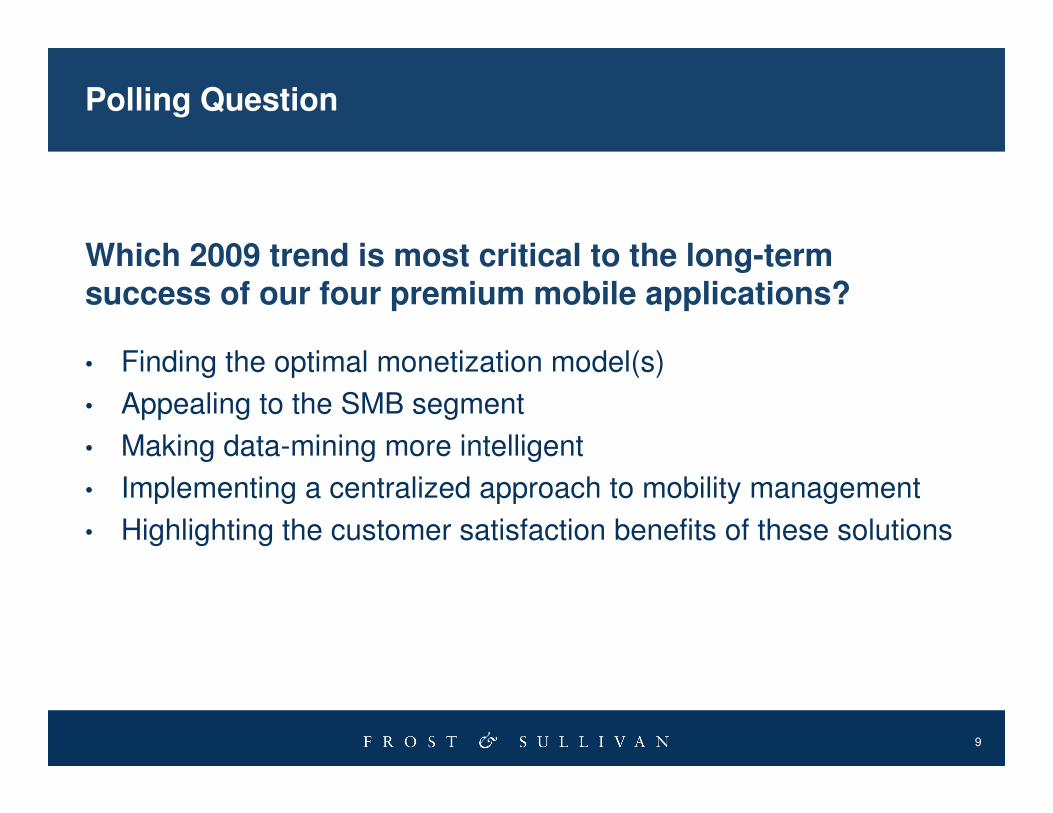

Polling Question

• Finding the optimal monetization model(s)

• Appealing to the SMB segment

• Making data-mining more intelligent

• Implementing a centralized approach to mobility management

• Highlighting the customer satisfaction benefits of these solutions

Which 2009 trend is most critical to the long-term success of our four premium mobile applications?

10

Premium Mobile Apps-- Enterprise Preferences and Plans --

11

First Quarter 2009 Mobile Apps Survey

• January 2009 online research survey.

• 150 enterprise mobile and wireless decision-makers.

• Sample divided evenly in terms of company size:• Fewer than 500 employees

• 500+ employees

• Wide range of industries represented, including:• Business/Professional Services

• Manufacturing and Distribution

• Telecommunications/IT

• Financial/Insurance Services

• Retail

• Healthcare

• U.S. vs. Canada representation.

12

Four Areas of Questioning

• Level of Perceived Need

• Plans for Deployment

• Barriers to Implementation

• Measures of Success

� Local Field Fleet Management

� Service Inventory Tracking and Management

� Mobile Product/Cargo Tracking

� Data Capture Technologies: Barcode scanning, Image capture, Wireless asset tracking devices, RFID, Sensor solutions, Location tagging

Field Asset Management (FAM) Mobile Office

� Wireless push email

� PIM – Personal Information Management

� Security and management support and administration

� Local Field Fleet Management

� Service Inventory Tracking and Management

� Mobile Product/Cargo Tracking

� Data Capture Technologies: Barcode scanning, Image capture, Wireless asset tracking devices, RFID, Sensor solutions, Location tagging

Field Asset Management (FAM) Mobile Office

� Wireless push email

� PIM – Personal Information Management

� Security and management support and administration

� Worker Track, Locate, Monitor

� Mapping & Navigation

� Exception Alerts and Geo-Fencing

� Messaging

� Business Intelligence and Reporting

� Worker Management (Time Cards, Job Progress Updates, etc.)

� Scheduling, Dispatch, and Event Confirmation

� Data Collection (Signature/Image Capture, Barcode Scanning, Wireless Forms)

Mobile Resource Management (MRM)

Mobile Sales Force Automation (SFA)

� Wireless SFA on handheld devices

� Off-line PDA SFA with wired synchronization to back-end CRM/SFA systems

� Laptop SFA – wired or wireless

� Central repository for:

• Accounts

• History

• Contacts

• Calendar

• Tasks

• Inventory

• Sales pipeline

� Worker Track, Locate, Monitor

� Mapping & Navigation

� Exception Alerts and Geo-Fencing

� Messaging

� Business Intelligence and Reporting

� Worker Management (Time Cards, Job Progress Updates, etc.)

� Scheduling, Dispatch, and Event Confirmation

� Data Collection (Signature/Image Capture, Barcode Scanning, Wireless Forms)

Mobile Resource Management (MRM)

Mobile Sales Force Automation (SFA)

� Wireless SFA on handheld devices

� Off-line PDA SFA with wired synchronization to back-end CRM/SFA systems

� Laptop SFA – wired or wireless

� Central repository for:

• Accounts

• History

• Contacts

• Calendar

• Tasks

• Inventory

• Sales pipeline

13

0

5

10

15

20

25

30

35

40

45

50

Very Necessary Somewhat

Necessary

Not Necessary

at All

Perc

ent of R

espondents

(%

)

Field Asset ManagementField Asset ManagementField Asset ManagementField Asset Management

Mobile OfficeMobile OfficeMobile OfficeMobile Office

Mobile Resource ManagementMobile Resource ManagementMobile Resource ManagementMobile Resource Management

Mobile Sales Force Automation Mobile Sales Force Automation Mobile Sales Force Automation Mobile Sales Force Automation

Question: How necessary is this solution in helping to meet your organization’s business goals?

North America

Level of Perceived Need – All Respondents

14

Level of Perceived Need -- U.S. vs. Canada

Very Very Very Very Necessary Necessary Necessary Necessary

18%18%18%18%

Somewhat Somewhat Somewhat Somewhat Necessary Necessary Necessary Necessary

26%26%26%26%

Not at All Not at All Not at All Not at All Necessary Necessary Necessary Necessary

56%56%56%56%

Canadian RespondentsCanadian RespondentsCanadian RespondentsCanadian Respondents

Very Very Very Very Necessary Necessary Necessary Necessary

41%41%41%41%Somewhat Somewhat Somewhat Somewhat Necessary Necessary Necessary Necessary

34%34%34%34%

Not at All Not at All Not at All Not at All Necessary Necessary Necessary Necessary

25%25%25%25%

U.S. RespondentsU.S. RespondentsU.S. RespondentsU.S. Respondents

Very Very Very Very Necessary Necessary Necessary Necessary

30%30%30%30%

Somewhat Somewhat Somewhat Somewhat Necessary Necessary Necessary Necessary

24%24%24%24%

Not at All Not at All Not at All Not at All Necessary Necessary Necessary Necessary

46%46%46%46%

Canadian RespondentsCanadian RespondentsCanadian RespondentsCanadian Respondents

Very Very Very Very Necessary Necessary Necessary Necessary

54%54%54%54%Somewhat Somewhat Somewhat Somewhat Necessary Necessary Necessary Necessary

31%31%31%31%

Not at All Not at All Not at All Not at All Necessary Necessary Necessary Necessary

15%15%15%15%

U.S. RespondentsU.S. RespondentsU.S. RespondentsU.S. Respondents

Mobile Resource Management (MRM) Mobile Office

Question: How necessary is this solution in helping to meet your organization’s

business goals?

• U.S. companies significantly more likely to see value in Premium Mobile apps

• Most valued app – Mobile Office – still shows wide divergence in U.S. vs. Canada perceptions

15

Deployment Plans – All Respondents

0

5

10

15

20

25

30

35

40

45

50

Have app,

Expanding within 12

months

Have app, No plans

to expand

Plan to intro app

within 3 years

No app, No plans to

deploy

Perc

ent of R

espondents

(%

)

Question: Please indicate your organization’s current plans for implementing this solution.

Field Asset ManagementField Asset ManagementField Asset ManagementField Asset Management

Mobile OfficeMobile OfficeMobile OfficeMobile Office

Mobile Resource ManagementMobile Resource ManagementMobile Resource ManagementMobile Resource Management

Mobile Sales Force Automation Mobile Sales Force Automation Mobile Sales Force Automation Mobile Sales Force Automation

North America

16

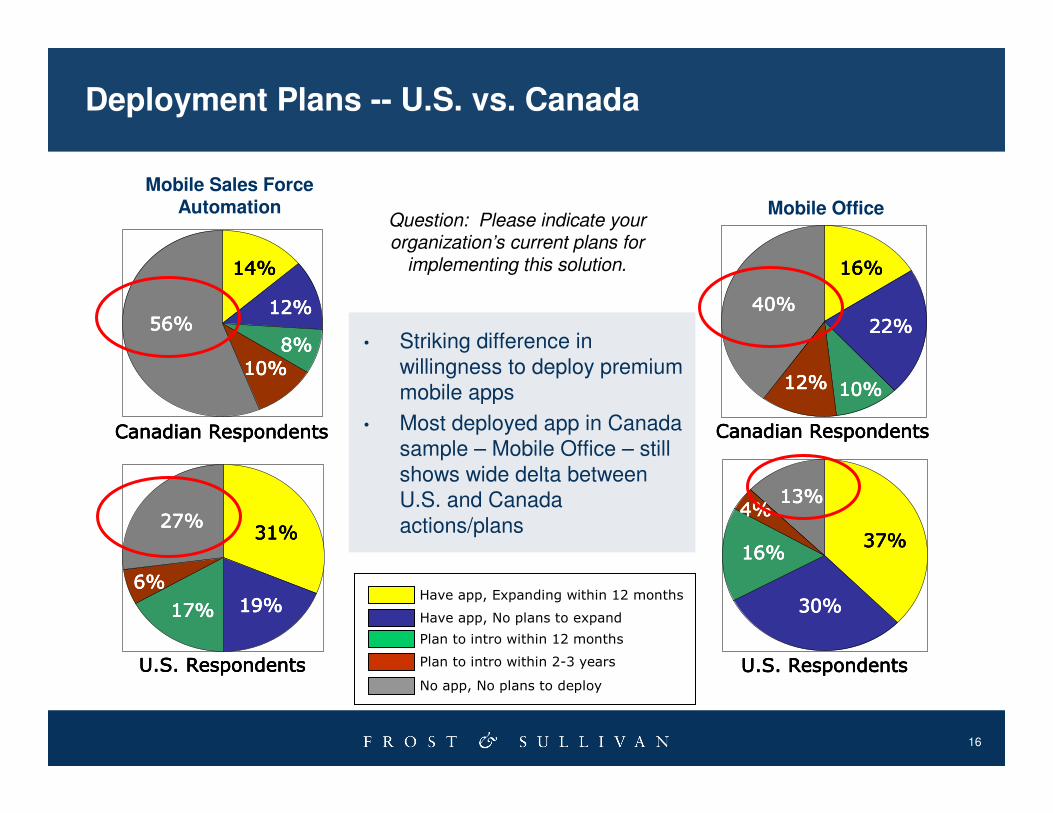

Deployment Plans -- U.S. vs. Canada

Canadian RespondentsCanadian RespondentsCanadian RespondentsCanadian Respondents

U.S. RespondentsU.S. RespondentsU.S. RespondentsU.S. Respondents

Canadian RespondentsCanadian RespondentsCanadian RespondentsCanadian Respondents

U.S. RespondentsU.S. RespondentsU.S. RespondentsU.S. Respondents

Mobile Sales Force Automation Mobile Office

Question: Please indicate your organization’s current plans for

implementing this solution.

• Striking difference in willingness to deploy premium mobile apps

• Most deployed app in Canada sample – Mobile Office – still shows wide delta between U.S. and Canada actions/plans

14%14%14%14%

8%8%8%8%56%56%56%56%

12%12%12%12%

10%10%10%10%

31%31%31%31%

19%19%19%19%

27%27%27%27%

17%17%17%17%

6%6%6%6%

16%16%16%16%

10%10%10%10%

40%40%40%40%22%22%22%22%

12%12%12%12%

37%37%37%37%

30%30%30%30%

13%13%13%13%

16%16%16%16%

4%4%4%4%

Have app, Expanding within 12 months

Have app, No plans to expand

Plan to intro within 12 months

Plan to intro within 2-3 years

No app, No plans to deploy

17

0 20 40 60 80 100

Implementation Barriers – For Those With No Plans to Deploy

Question: Please indicate which of the following are the most significant barriers to implementing this solution within your company.

Average Percentage of Respondents (%)

No perceived need

Cost of implementation

High TCO

ROI benefits are unclear

Other

Security concerns

Lack of internal expertise

Lack of knowledge re: vendors/solutions

Difficulty integrating into back-office systems

Employee resistance

Privacy concerns

79.5%

22.7%

19.2%

9.5%

9.0%

7.2%

6.5%

5.7%

4.5%

4.5%

4.0% North America

18

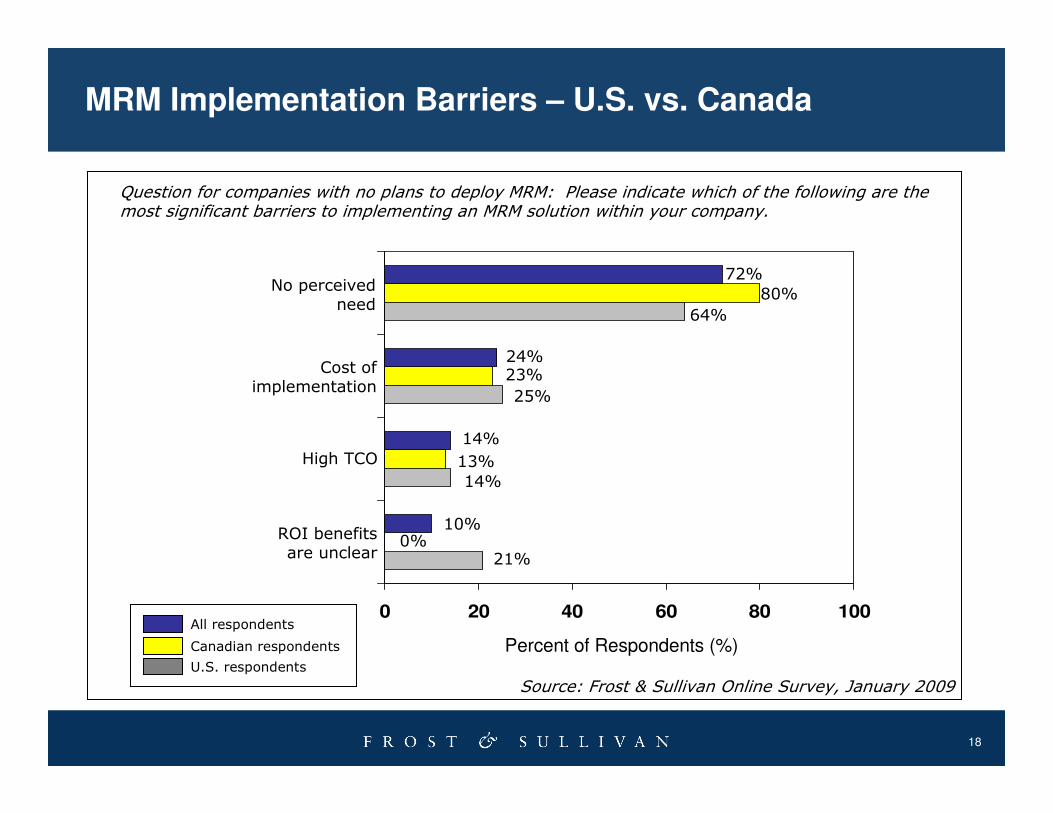

MRM Implementation Barriers – U.S. vs. Canada

Question for companies with no plans to deploy MRM: Please indicate which of the following are the most significant barriers to implementing an MRM solution within your company.

Source: Frost & Sullivan Online Survey, January 2009

0 20 40 60 80 100

No perceived need

Cost of implementation

High TCO

ROI benefits are unclear

72%

80%

64%

24%23%

25%

14%

13%

14%

10%0%

21%

All respondents

Canadian respondents

U.S. respondents

Percent of Respondents (%)

19

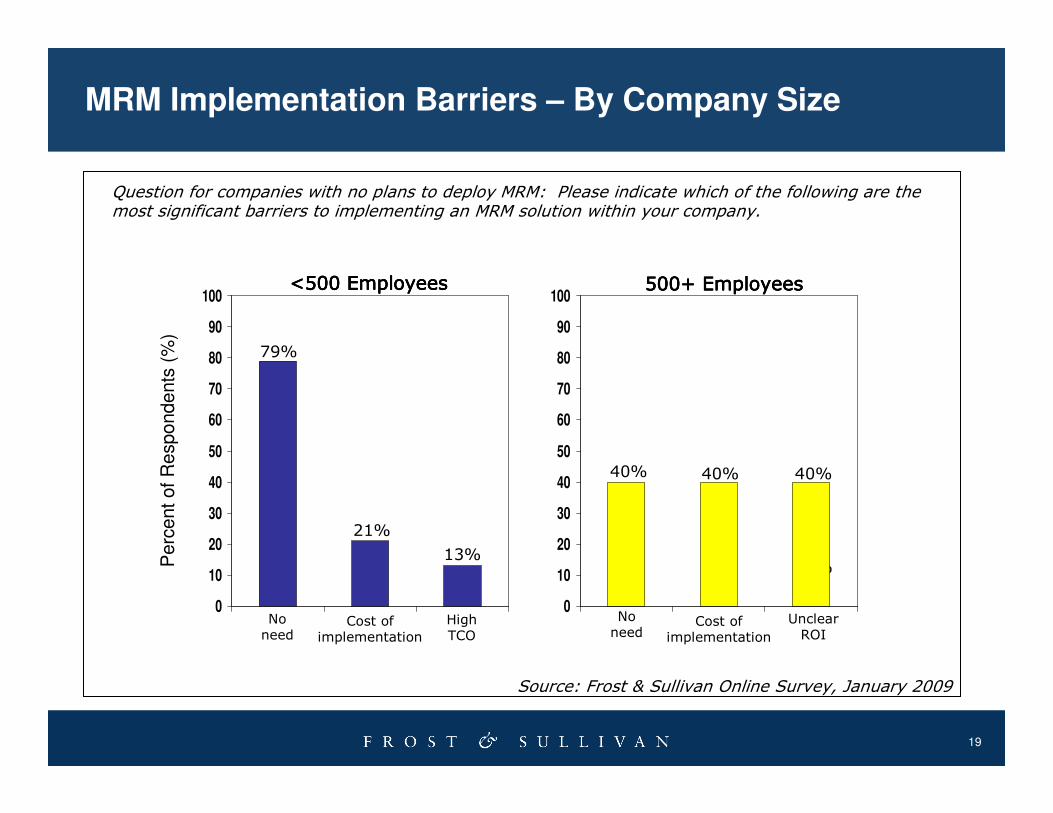

MRM Implementation Barriers – By Company Size

Question for companies with no plans to deploy MRM: Please indicate which of the following are the most significant barriers to implementing an MRM solution within your company.

Source: Frost & Sullivan Online Survey, January 2009

0

10

20

30

40

50

60

70

80

90

100

No need

Cost of implementation

79%

21%

57%

40%40%

Perc

ent of R

espondents

(%

)

No need

Cost of implementation

Unclear ROI

<500 Employees<500 Employees<500 Employees<500 Employees 500+ Employees500+ Employees500+ Employees500+ Employees

0

10

20

30

40

50

60

70

80

90

100

13%

High TCO

40%

20

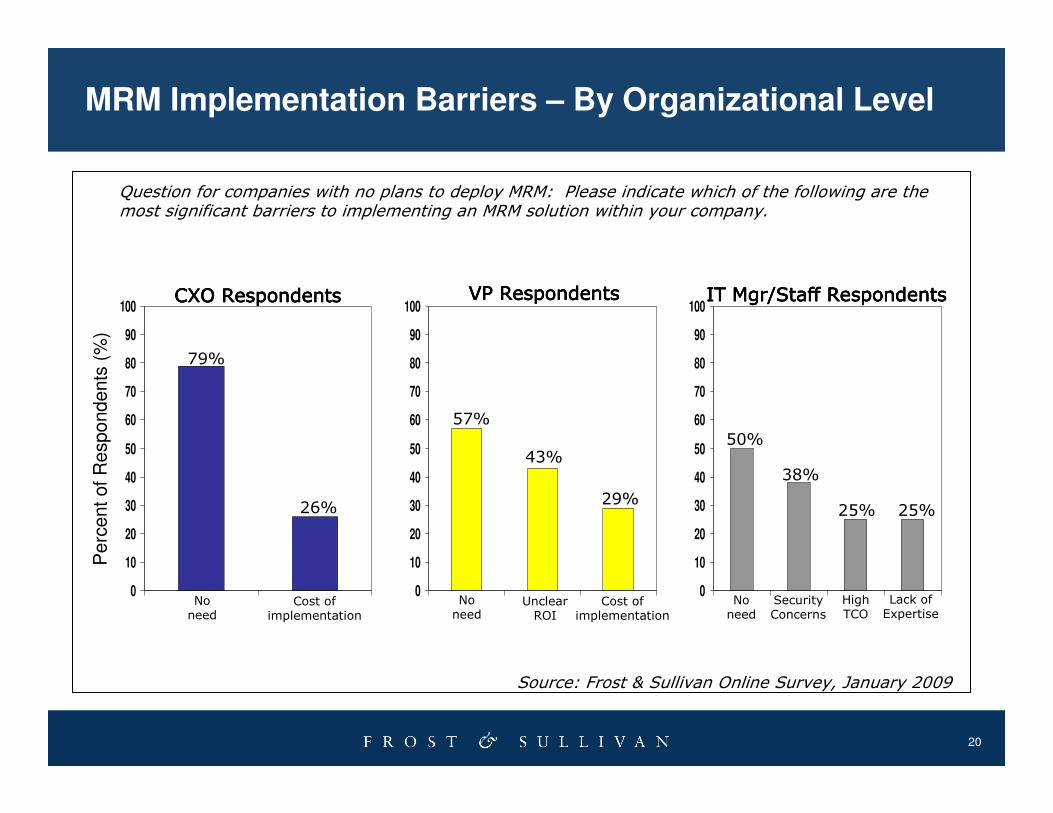

MRM Implementation Barriers – By Organizational Level

0

10

20

30

40

50

60

70

80

90

100

0

10

20

30

40

50

60

70

80

90

100

Question for companies with no plans to deploy MRM: Please indicate which of the following are the most significant barriers to implementing an MRM solution within your company.

Source: Frost & Sullivan Online Survey, January 2009

0

10

20

30

40

50

60

70

80

90

100

No need

Cost of implementation

79%

57%

Perc

ent of R

espondents

(%

)

CXO Respondents CXO Respondents CXO Respondents CXO Respondents VP RespondentsVP RespondentsVP RespondentsVP Respondents

26%

IT Mgr/Staff RespondentsIT Mgr/Staff RespondentsIT Mgr/Staff RespondentsIT Mgr/Staff Respondents

43%

29%

No need

Cost of implementation

Unclear ROI

No need

Security Concerns

High TCO

Lack of Expertise

50%

38%

25% 25%

21

Implementation Barriers – For Those Planning to Deploy Within Next Three Years

Question: Please indicate which of the following are the most significant barriers as to why your organization has yet to implement this solution.

0 20 40 60

Average Percentage of Respondents (%)

Cost of implementation

Security concerns

High TCO

ROI benefits are unclear

Privacy concerns

Lack of knowledge re: vendors/solutions

Lack of internal expertise

Difficulty integrating into back-office systems

Employee resistance

Technology not ready

50.0%

32.0%

31.5%

29.7%

24.5%

15.5%

13.2%

11.7%

11.0%

9.7% North America

22

Polling Question

• Creating the right product

• Selling through the right channels

• Pricing the solution appropriately

• Identifying key target markets

• Crafting effective marketing messages

If you’re a vendor or channel for enterprise mobile apps, which is your biggest challenge at this time?

23

Primary ROI Metrics for Current Users

43% - Improved service response times

29% - Faster trouble ticket resolution

29% - Increase in customer satisfaction

29% - Decrease in overtime hours

46% - Increase in customer satisfaction

41% - Improved service response times

40% - Increased sales

30% - More accurate billing

24% - Reduced paperwork

Field Asset Management Mobile Office

Mobile Resource Management

41% - Reduced paperwork

41% - Increase in customer satisfaction

36% - Increased job completion rates

28% - More accurate billing

39% - Increase in customer satisfaction

34% - Increased sales

30% - Improved service response times

28% - Increased job completion rates

22% - Reduced paperwork

Mobile Sales Force Automation

24

Conclusions

• Premium mobile applications are already viewed as business enablers by a sizeable percentage of companies.

• Current users are ready to expand.

• Fence-sitters present a manageable array of concerns.

• Adoption barriers focus on lack of need, cost concerns, and security/privacy issues. These barriers vary in intensity by geography, company size, and organizational level.

• Marketing strategy is critical.

• These apps provide a competitive advantage now; but will soon morph to become a competitive requirement.

25

Next Steps

� Request a proposal for a Growth Partnership Service to support you and your team to accelerate the growth of your company. ([email protected])1-877-GoFrost (1-877-463-7678)

� Join us at our annual Growth, Innovation, and Leadership 2009: A Frost & Sullivan Global Congress on Corporate Growth, September 13-16 2009, Hyatt Scottsdale Resort & Spa at Gainey Ranch, Scottsdale, AZ(www.gil-global.com)

� Register for the next Chairman’s Series on Growth:

The CEO's Growth Team™: Research & Development Driving Growth and

Innovation (April 7th) (http://www.frost.com/growth)

� Register for Frost & Sullivan’s Growth Opportunity Newsletter and keepabreast of innovative growth opportunities(www.frost.com/news)

26

Poll Question

Which of the following would you like to discuss in more depth? (Select all that apply)

• A Growth Partnership Services Proposal: A discussion proposal which will illustrate how Frost & Sullivan works with you to accelerate growth

• Growth Strategy Dialogue: Schedule a one-on-one industry specific strategy session

• Review a proposal for conducting a 360 Degree Visionary Workshop

• Growth Consulting: consult with us on a specific project in progress: i.e. new product launch; geographic expansion strategy; M&A; etc.

• GIL 2009: Obtaining more information on attending the Growth, Innovation and Leadership Global Congress

*Turn off your pop-up blocker, so you can respond to the next polling question

27

Your Feedback is Important to Us

Growth Forecasts?

Competitive Structure?

Emerging Trends?

Strategic Recommendations?

Other?

Please inform us by taking our survey.

What would you like to see from Frost & Sullivan?

28

For Additional Information

Naylor Gray

Global Marketing

(210) 247-24376

Craig Hays

Director of Sales

Information and Communications Technologies

(210) 247-2460

Jeanine Sterling

Senior Industry Analyst

Mobile and Wireless Communications

(586) 263-4454