63

rentice-Hall, Inc. Chapter 16 Retirement Planning

| Date post: | 05-Jan-2016 |

| Category: |

Documents |

| Upload: | allison-carpenter |

| View: | 216 times |

| Download: | 0 times |

Prentice-Hall, Inc. 1

Chapter 16

Retirement Planning

Prentice-Hall, Inc. 2

Retirement – It’s Up to YOU!

Start saving today – although retirement seems a long way away!

Employer benefits are reduced, or simply not available.

The future of government benefits, Social Security, is questionable.

Prentice-Hall, Inc. 3

The Aspects of Social Security

Mandatory federal insurance program providing– retirement, disability, and survivor benefits

Paid for with a federal tax -- FICA– 6.2% of your first $76,200 in 2000 pays for Social

Security– 1.45% of your total earnings pay for Medicare– Equal match by your employer

Prentice-Hall, Inc. 4

Social Security EligibilityTo qualify for full benefits you must earn

40 credits– $780 earned in 2000 equals one credit– Maximum of four credits earned per year

You must be 65 years of age to receive full benefits, but will gradually increase to 67 in 2022.

Reduced benefits may begin at age 62

Prentice-Hall, Inc. 5

Determinants of Social Security Retirement Benefits

Number of years of earnings Average level of earnings Inflation Age you begin receiving benefits Replaces approximately 42% of your lifetime

average annual income, with adjustments down for higher income earners and up for lower income earners

Prentice-Hall, Inc. 6

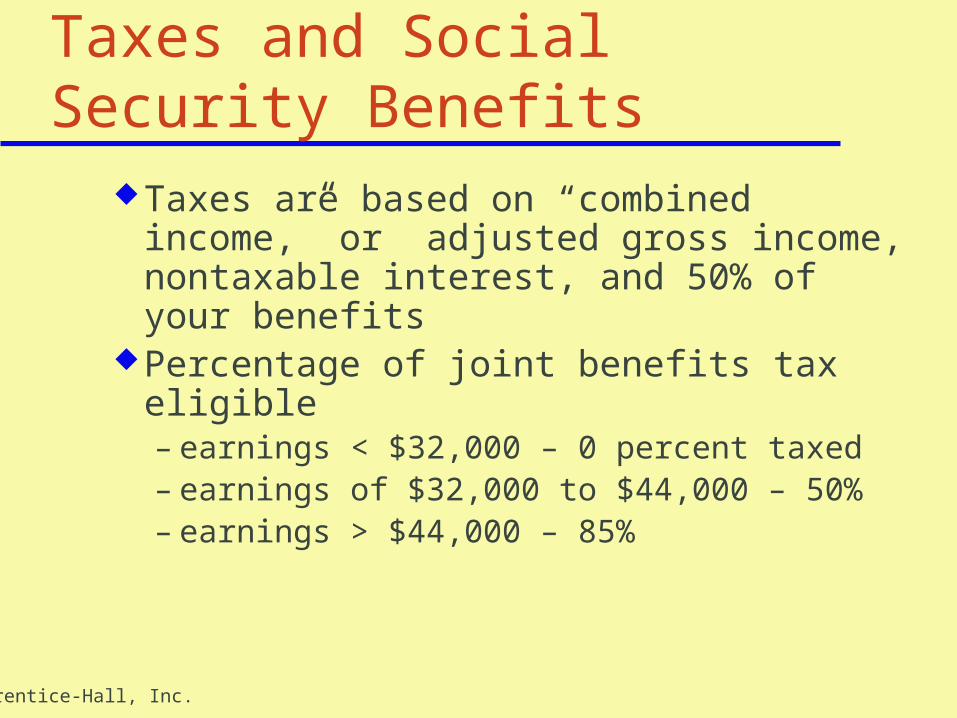

Taxes and Social Security Benefits

Taxes are based on “combined income,” or adjusted gross income, nontaxable interest, and 50% of your benefits

Percentage of joint benefits tax eligible– earnings < $32,000 – 0 percent taxed– earnings of $32,000 to $44,000 – 50%– earnings > $44,000 – 85%

Prentice-Hall, Inc. 7

Taxes and Social Security Benefits (cont’d)

Percentage of individual benefits tax eligible– earnings < $25,000 – 0 percent taxed– earnings of $25,000 to $34,000 – 50%– earnings > $34,000 – 85%

Prentice-Hall, Inc. 8

Earnings Limits on Social Security Benefits

Prior to 2000, earning limits reduced Social Security benefits for many older workers.

Senior Citizens’ Freedom to Work Act of 2000 eliminated the retirement earnings limit.

Prentice-Hall, Inc. 9

Disability and Survivor Benefits

Disability benefits for those physically or mentally impaired– Impairment expected to result in death– Impairment prevents “substantial work” for at least

1 year

Survivor’s benefits– small payment to defray funeral costs– continuing monthly payments to spouse, children,

or parents -- with restrictions

Prentice-Hall, Inc. 10

Employer-Funded Pension Plans

Defined benefit plansCash balance plans

Advantages: – Employer bears investment risk for the

plan.– Most are non-contributory

Prentice-Hall, Inc. 11

Contributory and Noncontributory Plans

Contributory -- both you and your employer pay toward your retirement

Noncontributory -- only your employer pays toward your retirement

Prentice-Hall, Inc. 12

Other Retirement Plan Issues

Funded -- the employer pays into a trustee-managed fund to guarantee future pensions

Unfunded -- pensions are paid out of current company earnings or pay-as-you-go

Vesting period -- required length of employment to be eligible to receive company paid pension benefits

Prentice-Hall, Inc. 13

Defined Benefit Plans

Predetermined pension payment on the basis of a formula. Often based on average salary, years of service, and age at retirement

Monthly benefit =

Average salary for Y last yrs x yrs of service x Z%

Prentice-Hall, Inc. 14

Defined Benefit Plans--Limitations

Lack of portability – pension does not go with you if you leave the company

Company changes in the plan with little notice

Few plans adjust benefits for inflationSome are unfunded plans that lack

safety.

Prentice-Hall, Inc. 15

Cash-Balance Plans: A New Twist on Defined-Benefit Plans

Pension account credited on the basis of a formula:– Percentage of salary (e.g., 4% - 7%)– Predetermined rate of interest earnings

(e.g., 30-year Treasury-bond rate, S & P 500 index rate, or other rate)

Prentice-Hall, Inc. 16

Cash-Balance Plans: Pros and Cons

Pros:– Retirement benefits are easy to track.– Benefit younger employees who can start to build

benefits faster– Portability

Cons:– No choice on investment decisions and earnings

are limited to the stated rate– Reduced benefits for older workers

Prentice-Hall, Inc. 17

Plan Now, Retire Later -- The Steps to Success

Step 1: Set goals.Step 2: Estimate how much you’ll need

to meet your goals.Step 3: Estimate your income available

at retirement.Step 4: Calculate the annual inflation-

adjusted shortfall.

Prentice-Hall, Inc. 18

Plan Now, Retire Later -- The Steps to Success (cont’d)

Step 5: Calculate the funds needed at retirement to cover this shortfall over your entire retirement.

Step 6: Determine how much you must save annually between now and retirement.

Step 7: Put the plan into play and save.

Prentice-Hall, Inc. 19

Step 1: Set Goals. How extravagantly will

you want to live? When will you want to

retire? Who will you have to

care for? Where will you want to

live? Will you want to travel?

Prentice-Hall, Inc. 20

Step 2: Estimate Your Needs to Meet Your Goals.

Estimate future costs based on 70% to 80% of current living expenses.

Establish how much each of your other goals will cost.

Calculate how taxes will erode your spending power.

Prentice-Hall, Inc. 21

Step 3: Estimate Your Income Available at Retirement.

Estimate your Social Security benefits.Calculate your employer-provided

pension.Estimate any other windfall income that

could be used towards retirement, such as an inheritance from your gozillionaire Uncle Morty.

Prentice-Hall, Inc. 22

Step 4: Calculate the Annual Inflation-Adjusted Shortfall.

Compare the difference between your needs and your retirement income.

Take inflation into account when calculating the time value of money.

Use this formula:

FV = PV(FVIF i%, n yr)

Prentice-Hall, Inc. 23

Step 4: Calculate the Annual Inflation-Adjusted Shortfall.

If you fall short, start saving now -- remember Axiom 2: The Time Value of Money.

If you exceed your projected need -- protect yourself against all contingencies.

Prentice-Hall, Inc. 24

Step 5: Calculate the Funds Needed for This Shortfall.

Calculate the present value of all your annual shortfalls by discounting for your inflation-adjusted rate of return -- this is your total need at retirement.

Use this formula:

PV = PMT(PVIFA i%, n yr)

Prentice-Hall, Inc. 25

Step 6: Determine How Much You Must Save Annually.

Your answer in Step 5 is the total dollar amount you need the day you retire.

Determine your annual savings goal by using a future value of an annuity equation.

Use the formula

FV = PMT(FVIFA i%, n yr)

Prentice-Hall, Inc. 26

Step 6: Determine How Much You Must Save Annually.

Note: Always remember to adjust for inflation in each step or you will fall short of your goal.

Prentice-Hall, Inc. 27

Step 7: Put the Plan Into Play and Save.

Save, save, save!!

Determine the combination of retirement plans and products that are best for you.

Prentice-Hall, Inc. 28

Use Tax-Deferred Plans to Save for Retirement

Contributions may be made on a fully or partially tax-exempt basis. You can contribute more.

Earnings are not taxed annually, so that amount stays in the account to continue earning money – or compound growth.

Taxes are deferred until after retirement.

Prentice-Hall, Inc. 29

Employer Sponsored Retirement Plans – Defined Contribution

A personal retirement savings account that passes responsibility for investment risk to the employee.– Employer or employer and employee

contribute.– Benefit depends on investment success.– Employee may choose the investment.– Future benefits are not guaranteed or

insured.

Prentice-Hall, Inc. 30

Defined Contribution Plans: Various Forms

Defined contribution plans– Profit-sharing plans– Money-purchase plans– Thrift and savings plans– Employee stock ownership plan (ESOP)

401(k) plans

Prentice-Hall, Inc. 31

Profit-Sharing Plans

Employer contributions can vary yearly due to profitability.

Contributions can depend on your salary level.

Some firms set minimums and maximums.

Contributions are not guaranteed.

Prentice-Hall, Inc. 32

Money-Purchase Plans

Employer contributions are a set percentage of your salary.

Contributions are guaranteed.Preferred over profit-sharing plans

because of the guaranteed contributions.

Prentice-Hall, Inc. 33

Thrift and Savings Plans

Employers match a set percentage of your contribution to your retirement plan.

Contributions are normally guaranteed.

Prentice-Hall, Inc. 34

Employee Stock Ownership Plan (ESOP)

Employer contributions are made in the form of company stock.

This form of plan is the riskiest because your retirement is dependent on the performance of the company.

This type of plan does not allow for diversification.

Prentice-Hall, Inc. 35

401(k) Plans

Are normally employer-sponsored defined-contribution plans.

Are normally set-up as thrift-and-savings plans in which your employer normally matches a set percentage of your contribution.

Prentice-Hall, Inc. 36

401(k) Plans (cont’d)

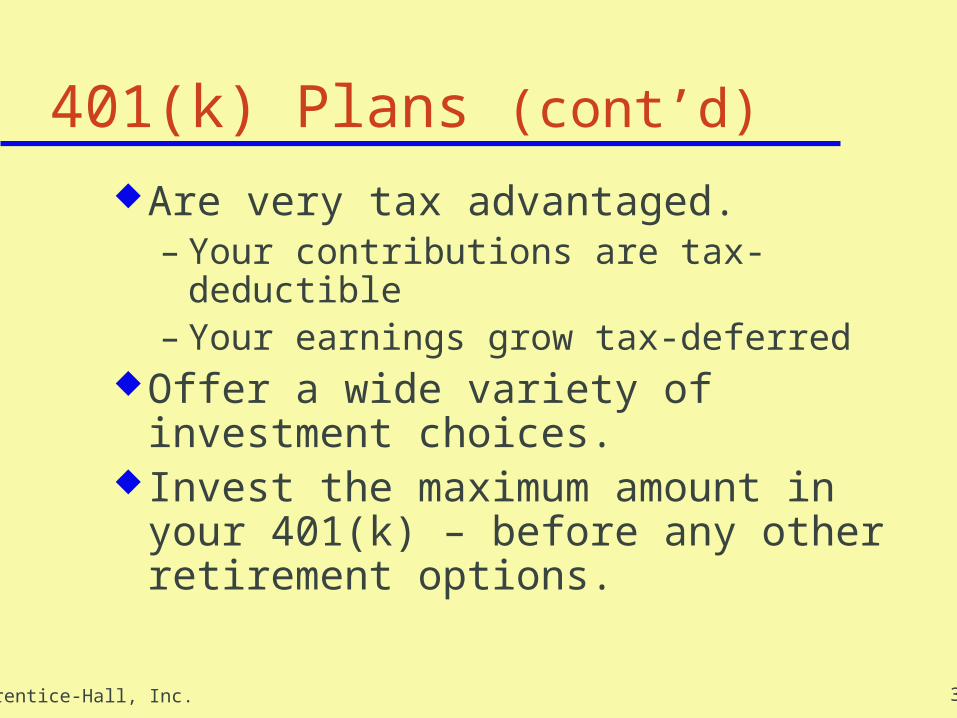

Are very tax advantaged.– Your contributions are tax-deductible – Your earnings grow tax-deferred

Offer a wide variety of investment choices.

Invest the maximum amount in your 401(k) – before any other retirement options.

Prentice-Hall, Inc. 37

Self-Employed or Small Business Retirement Plans

Eligibility: self-employed, small business employee, or part-time free-lance work (even if full-time employee elsewhere)

Benefit: Fully tax-deductible retirement plan

Prentice-Hall, Inc. 38

Self-Employed or Small Business Retirement Plans (cont’d)

Keogh plan Simplified employee

pension plan (SEP-IRA)

Savings incentive match plan for employees (SIMPLE) plans

Prentice-Hall, Inc. 39

Keogh Plans

Are vary similar to corporate profit-sharing plans.

Are either defined-contribution, defined-benefit, or a combination of both.

Are self-directed, which means that you choose the investment.

Contributions are tax-deductible.

Prentice-Hall, Inc. 40

Keogh Plans (cont’d)

Limitations on annual contributions, but liberal (up to $30,000 in 2000)

Withdrawals as early as 59½, but must begin by age 70½

10% early withdrawal penalty, except in cases of illness, disability, or death

Prentice-Hall, Inc. 41

Simplified Employee Pension Plan (SEP-IRA)

Similar to a defined-contribution Keogh plan, but easier to establish.

Used by small business owners with no or few employees.

Contributions are tax-deductible and earnings are tax-deferred.

Prentice-Hall, Inc. 42

Simplified Employee Pension Plan (SEP-IRA) (cont’d)

Limits contributions to 15% of salary, or $30,000, whichever is less.

Flexibility in making contributions – can skip years.

Prentice-Hall, Inc. 43

Savings Incentive Match Plan for Employees (SIMPLE)

Are for employers with less than 100 employees earning more than $5,000.

Contributions are tax-deductible and earnings are tax-deferred.

Some employer matching funds.

Prentice-Hall, Inc. 44

Individual Retirement Accounts (IRAs)

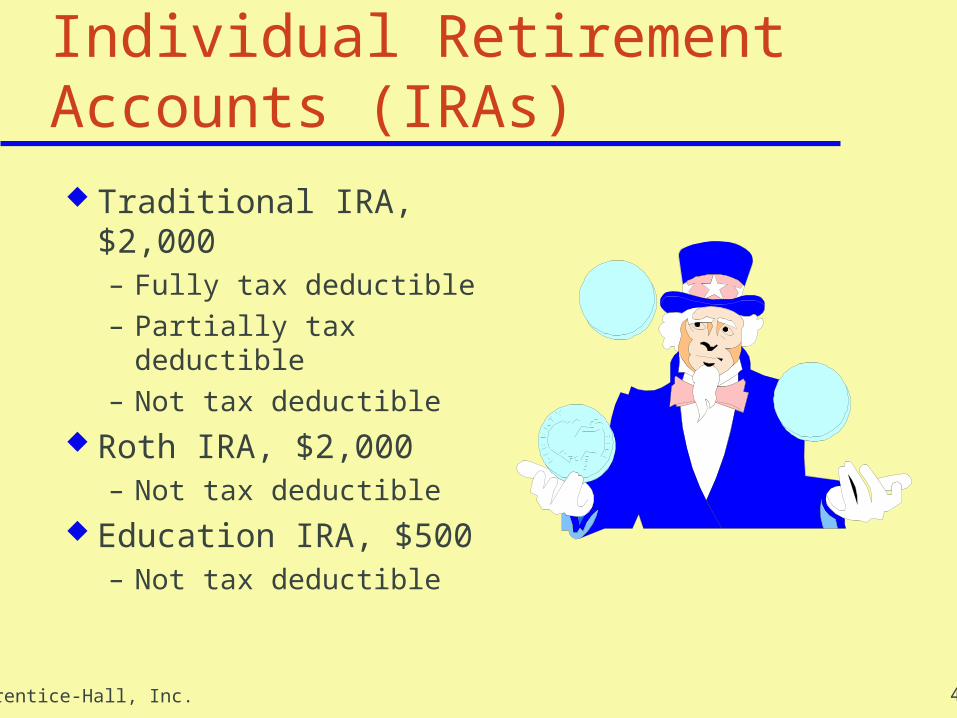

Traditional IRA, $2,000– Fully tax deductible– Partially tax deductible– Not tax deductible

Roth IRA, $2,000– Not tax deductible

Education IRA, $500– Not tax deductible

Prentice-Hall, Inc. 45

Traditional IRA

Contributions grow tax-deferred until withdrawal.

Allows nonworking spouses to make a contribution (spousal IRAs).

Self-directed, but cannot invest in life insurance or collectible, except gold or silver U.S. coins.

Prentice-Hall, Inc. 46

Traditional IRAs (cont’d)

Distributions prior to age 59½ are subject to a 10% tax penalty, with few exceptions– For first home purchase -- up to $10,000– Are paying college expenses– Become disabled– Need for medical expenses or medical insurance

premiums, with restrictions After you turn 70½ you must start receiving

annual distributions or be penalized 50% of your minimum annual distribution.

Prentice-Hall, Inc. 47

Traditional IRAs (cont’d)

Can rollover distributions from a qualified employer plan or other IRA to avoid an early distribution penalty – be careful to avoid taxes.

Cannot use as collateral for a loan.

Prentice-Hall, Inc. 48

To Be A Fully Tax-Deductible Traditional IRA

If not covered by a plan at work, you may contribute $2,000 annually, regardless of income.

A married couple, with one working spouse may contribute $4,000 or 100% of earned income annually, if “modified adjusted gross income” is below $150,000.

A married couple can contribute $4,000 if adjusted gross income is below the IRS cutoff.

Prentice-Hall, Inc. 49

For a Partially Tax-Deductible Traditional IRA: Phaseout Zones

A single person may receive a partial tax deduction if “modified” adjusted gross income falls between $32,000 and $42,000 (2000)

A married couple may receive a partial tax deduction if “modified” adjusted gross income falls between $52,000 and $62,000 (2000)

A married couple, with one working spouse,may receive a partial tax deduction, if “modified adjusted gross income” is between $150,000 and $160,000 (2000)

Prentice-Hall, Inc. 50

Non-deductible Traditional IRA

No annual tax deduction for IRA contribution

Investment grows free of income taxes until withdrawal

Prentice-Hall, Inc. 51

Roth IRAs

Contributions are not tax deductible.Earnings grow tax-free.Withdrawals are tax-free if the Roth IRA

is held for 5 years. Income limits begin at $95,000 per

individual and $150,000 per couple.No distribution requirement.

Prentice-Hall, Inc. 52

Education IRAsContributions are limited to $500

annually per child under 18.Contributions are not tax deductible, but

grow tax-free with no tax due upon withdrawal.

Savings must be withdrawn by the time the child reaches 30, but can be rolled into accounts for younger siblings.

Prentice-Hall, Inc. 53

Education IRAs (cont’d)

Money not used for education, may be subject to income taxes and a 10% penalty upon withdrawal.

Prentice-Hall, Inc. 54

Traditional versus Roth IRAChoose the Roth, if you can afford itAt the 31% tax bracket and a 10%

return for 40 years:– You need $2,899 (pretax) to fund a Roth

and would end up with $90,519 and NO TAXES.

– You need $2,000 to fund a traditional IRA and would end up with $90,519. After taxes at 31%, you would end up with $62,519.

Prentice-Hall, Inc. 55

Facing Retirement -- The Payout

Plan ahead before deciding how a payout is to be received.

Make sure you understand the tax consequences of any move.

Look at all retirement payouts together.Consider pros and cons of an annuity

versus a lump sum payout.

Prentice-Hall, Inc. 56

Types of Retirement Payouts

Single life annuity – payments for life.

Life annuity with “certain period” – payments continue as long as you live; however, if you die the payments continue until the end of the period.

Prentice-Hall, Inc. 57

Types of Retirement Payouts (cont’d)

Joint and survivor annuity -- the payments continue as long as you or your spouse live; however, in some cases the benefits will be reduced when you die.

Lump-sum -- a single payment of all principal and accumulated interest.

Prentice-Hall, Inc. 58

Tax Treatment of DistributionsAnnuity payments will be taxed as

normal income.A lump-sum payment

– will normally be taxed as if you received the money over a 10 year span. This reduces taxes slightly, but you are still liable for all the tax immediately.

– could be rolled over into an ira to avoid taxes and continue tax-deferred growth.

Prentice-Hall, Inc. 59

Putting a Plan Together and Monitoring It

Changes in inflation can have a drastic effect on your retirement planning.

Once you retire, you may live a long time. Monitor your progress and monitor your

company. Don’t neglect your insurance coverage. An investment planning computer program

may make things easier.

Prentice-Hall, Inc. 60

SummarySocial Security benefits

– Retirement benefits– Disability and survivor benefits– Eligibility

The seven-step retirement planning process.

Advantages of tax-deferred retirement plans.

Prentice-Hall, Inc. 61

Summary Employer-funded retirement plans

– Defined-benefit plans– Cash balance plans

Employer-sponsored defined contribution plans– 401(k) or 403(b) plans– Other plans

Self-employment and small business plans– SEP-IRAs– SIMPLE plans– Keogh plans

Prentice-Hall, Inc. 62

Summary (cont’d)

Types of IRAs– Traditional– Roth– Education

Pros and cons of annuity versus lump sum payouts

Prentice-Hall, Inc. 63

Summary (cont’d)

The payout choices– single life annuity– life annuity with “certain period”– joint and survivor annuity– lump-sum

Monitoring your process and progress