PAYROLL CARDS: Regulatory Considerations and Best Practices Ted Teruo Kitada Senior Company Counsel Wells Fargo Bank, National Association Dana Blaylock Sr. AML Risk Manager Bank of America, N.A. American Conference Institute Prepaid Card Compliance Mandarin Oriental, Washington, D.C. June 23-24, 2011

Transcript

PAYROLL CARDS: Regulatory Considerations and Best PracticesTed Teruo KitadaSenior Company CounselWells Fargo Bank, National AssociationDana BlaylockSr. AML Risk ManagerBank of America, N.A.

American Conference InstitutePrepaid Card ComplianceMandarin Oriental, Washington, D.C.June 23-24, 2011

22

Introduction

What are payroll cards? Less costly alternative to payroll checks.

Wages are deposited to a payroll card account electronically, normally through ACH.

Open loop (general purpose reloadable prepaid card).

Employee accesses cash through ATM or pays for goods or services at POS.

Normally not marketed to employees, but to employers.

Used by employees without deposit accounts.

Normally, only an employer may load and reload the card.

33

Introduction

Why do banks like payroll cards? Interchange fees paid by merchants to Visa and MasterCard.

Most of these fees in turn are paid to the banks issuing the payroll cards. (Durbin amendment’s impact?)

Monthly and other service fees paid by employers and employees.

Other fees: card replacement fee; balance inquiry fee; ATM transaction fee; overdraft fee; and dormant account fees. But be mindful of possible limitations for such fees under state law or under Regulation E, as amended by virtue of Title IV of the Credit Card Accountability Responsibility and Disclosure Act of 2009 (“CARD” Act).

44

Introduction

Why do employers like payroll cards? Lower internal costs: no producing, handling, and

distributing payroll checks.

Direct deposit, 20 cents per deposit; paper check, $1 to $2 per check; payroll card, between these two payment methods.

Reduce check fraud losses.

Reduce check reconciliation costs.

Reduce lost/stolen check replacement costs.

No holder in due course of payroll check subject to a stop pay order; simply disable the payroll card.

55

Introduction

Why do employees like payroll cards? No check cashing fee: employees without bank accounts

spend $8 Billion annually in check cashing fees.

Immediate access to cash without cashing a check.

No management of deposit account.

Use of a financial product without the costs of a deposit account.

Lower qualification requirements vis-à-vis a deposit account.

Greater safety for cash.

Protection under Regulation E, effective July 1, 2007.

Branded cards may be used for online transactions, such as shopping or bill payment.

6

Types of payroll cards used by employers

Employer Based prepaid payroll card programs – funds are loaded by employer only.

General Purpose Reloadable (GPR) – in addition to payroll, other funds can be loaded to the card including cash.

Self Enrolled - individual payroll cards are typically marketed to consumers cashing checks with no banking relationship.

7

Legal issues- coverage of payroll cards under Regulation E

Payroll cards covered by Regulation E (12 CFR Part 205), effective July 1, 2007 (71 Fed.Reg. 1473, January 10, 2006; 71 Fed.Reg. 51437, August 30, 2006).

This coverage means:

Issuance of access devices. Section 205.5

Liability of consumer for unauthorized transactions. Section 205.6

Initial disclosures, at the time a consumer contracts for an electronic fund transfer service or before the first EFT is made involving the consumer’s account. Section 205.7.

Change in terms notice; error resolution notice. Section 205.8.

Periodic statements. Sections 205.9 and 205.18.

Preauthorized transfers. Section 205.10.

Error resolution. Section 205.11.

8

Legal issues-compulsory use

Regulation E section 205.10(e)(2) prohibits a financial institution from requiring a consumer to establish an account with a particular institution for receipt of electronic fund transfers as a condition of employment.

However, provided that an employer does not require a consumer to obtain a payroll card account as the method of receiving pay, and permits, for example, a consumer to receive pay via direct deposit to a financial institution selected by the consumer, the compulsory use prohibition should not be implicated. 71 Fed.Reg. 1473, 1479 (January 10, 2006).

9

Legal issues-Regulation P

Regulation P (12 CFR Part 216) is issued under the Gramm-Leach-Bliley Act, Title V. It governs the treatment of nonpublic personal information about consumers by certain financial institutions.

Regulation P section 216.4 requires an initial disclosure of privacy policy not later than when a customer relationship for the purchase of a financial product or service is established with a covered institution.

Thereafter an annual notice of that policy is required under Regulation P section 216.5.

10

Legal issues-Regulation DD

Regulation DD (12 CFR Part 230) issued under the Truth in Savings Act of 1991. An “account” means a deposit account at a depository institution held by or offered to a consumer.

The purpose of this regulation is to enable consumers to make informed decisions about accounts at depository institutions.

With regard to payroll card accounts, the amount of fees are subject to disclosure or an explanation of how the fee will be determined and the conditions under which the fee may be imposed. Section 230.4(b)(4).

Timing of providing the information under Regulation DD: The information must be provided before an account is opened or a service is provided.

11

Legal issues-federal payments

Effective January 21, 2011, under an interim final rule issued by the Financial Management Service, Fiscal Service, U.S. Treasury, 75 Fed.Reg. 80335 (December 22, 2010), prepaid debit cards may receive federal payments though the ACH network, provided:The card must provide the cardholder with pass through

deposit or share insurance.

The issuer of the card must provide the cardholder with all of the protections under Regulation E.

The card account must not have an attached line or credit or loan that trigger automatic repayment from the card .

12

Legal issues-Title IV of the CARD Act.

Final rules under Title IV of the CARD Act, effective August 22, 2010 (74 Fed.Reg. 60986, November 20, 2009).

While the final rule covers “general-use prepaid cards,” (Regulation E section 205.20(3)(3)) payroll cards likely enjoy at least two exclusions. They are “[r]eloadable and not marketed or labeled as a gift card or gift certificate.” Regulation E section 205.20(b)(2). They are also “[n]ot marketed to the general public.” Regulation E section 205.20(b)(4).

13

Legal issues-funds availability

Regulation CC (12 CFR Part 229). Next business day availability for “electronic payments.” Regulation CC section 229.10(b). The terms electronic payments includes ACH credit entries. Regulation CC section 229.2(p).

Regulation CC requires disclosure of funds availability policy prior to opening a covered account, a “transaction account.” Regulation CC Section 229.17.

NACHA Operating Rules section 3.3.1.2: PPD (“Prearranged Payment and Deposit”) credit entry must be made available to a consumer on opening of business on the Settlement Date. One day earlier that as required under Regulation CC.

Regulation E section 205.10(a)(3) requires preauthorized electronic transfers to be credited as of the date the funds for the transfer are received.

14

Legal issues-fees

Arizona H.B. 2151, recently enacted payroll card legislation, effective July 20, 2011. One withdrawal for each deposit of wages per pay period (but not frequently than once a week), free of any service charges to the employee. A.R.S. section 23-351(F).

Other states with payroll card proposals include Connecticut (HB 6407) and California (AB 51).

15

Legal issues-preemption under Dodd-Frank

Preemption of states’ consumer protection laws as to national banks under section 1044 of the Dodd-Frank Wall Street Reform and Consumer Protection Act of 2010 (“Dodd-Frank”).

State consumer financial laws are preempted if “in accordance with the legal standard for preemption in the decision in the decision of the Supreme Court of the United States in Barnett Bank of Marion County, N.A. v. Nelson, Florida Insurance Commissioner, et al., 517 U.S. 25 (1996), the state consumer financial law prevents or significantly interferes with the exercise by a national bank of its powers.”

16

Preemption-recent development

Vida Baptista v. JP Morgan Chase Bank, N.A. , No. 10-13105 (11th Cir. May 11, 2011)(to be published). This case holds that by assessing a $6 check cashing fee, Chase did not violate a Florida law prohibiting such a fee by virtue of preemption under the National Bank Act.

Letter, dated May 12, 2011, issued by the OCC to Senator Thomas R. Carper.

17

Legal issues-International ACH Transactions

Effective September 18, 2009, NACHA Operating Rules require ODFIs and Gateways to identify all international payment transactions transmitted via the ACH Network as International ACH Transactions using the IAT SEC Code. (A “Gateway” is an ACH Operator acting as an entry point to or exit point from the US for ACH payment transactions.)

IAT transactions include data elements defined within BSA’s “Travel Rule,” e.g., name and address of Originator and name and address of Receiver. 31 C.F.R. Part 103.33(g). (The $3,000 threshold not adopted.)

18

Legal issues-International ACH Transactions

IAT means a debit or credit entry that is part of a payment transaction involving a financial agency’s office that is not located in the territorial jurisdiction of the US. The geographical location of the financial agency determines the IAT SEC Code, not the location of the Originator or Receiver.

Ask existing and new employees if they transfer payroll to a financial agency located outside the US. Obtain response in writing and retain that record for compliance purposes (and an OFAC audit).

1919

State recognition of payroll cards

California: opinion of Chief Counsel, under letter dated July 7, 2008, to American EPay, Inc., and Hewitt Associates, LLC.Payroll card an alternative to direct deposit recognized under

Labor Code section 213(d).

Inasmuch as participation in payroll card program must be optional (Regulation E section 205.10(e)), employee must voluntarily participate in payroll card program.

Massachusetts: Attorney general’s opinion of December 27, 2007. Payroll card lawful way to disburse wages, provided

employee may receive direct deposit also as an option.

20

Legal issues-other state law considerations

Unclaimed property: wages, deposits, or miscellaneous property.

Unclaimed property: related accounts.

Small estate affidavit.

Levies, new federal garnishment rule, 76 Fed.Reg. 9939 (February 23, 2011).

Subpoenas.

2121

FDIC insurance for payroll cards

New General Counsel’s Opinion No. 8, 73 Fed.Reg. 67155, November 13, 2008. Funds underlying prepaid cards, including payroll cards, are

“deposits” if they have been placed with an insured depository institution.

“Pass through” coverage.

$250,000, per depositor, permanent under Dodd-Frank section 335.

Dodd-Frank’s unlimited FDIC insurance coverage for noninterest bearing transaction accounts until December 31, 2012, under section 343.

22

AML and Know Your Customer (KYC) requirements

Most issuers determine KYC requirements based on card program criteria: Are cards portable? Can employees take the card with them

when they leave the current employer?

Is the card account number known by the cardholder?

Can funds be loaded from sources other than employer?

Cardholder Terms and Conditions.

When the cardholder is considered a customer of the issuer, full KYC is completed and electronic CIP verification is performed.

23

AML Considerations – Transaction Monitoring

Transaction monitoring for prepaid payroll programs is a requirement for most issuers.

Monitoring scenarios are based on issuers risk tolerance, program functionality, and transactions limits.

Potentially suspicious activity is identified and documented.

Investigation teams determine if a Suspicious Activity Report (SAR) should be filed.

Role of bank, employer, and outside administrator/program manager.

Records for FDIC pass through insurance purposes.

Unclaimed property.

Legal process.

Indemnification.

2525

Overdraft service under payroll cards

The following slides will explore overdraft services under payroll cards.

Payroll cards covered by Regulation E, effective July 1, 2007, 71 Fed.Reg. 1473, January 10, 2006; 71 Fed.Reg. 51437, August 30, 2006.

2626

Background-final rules

Final rule under Regulation E addressing overdraft services. 74 Fed.Reg. 59033, November 17, 2009.

Final rule under Regulation DD addressing the uniformity and adequacy of information provided to consumers when they overdraw their account with financial institutions promoting overdraft services. 70 Fed.Reg. 29582, May 24, 2005.

Final rule under Regulation DD addressing disclosure of aggregate overdraft fees and balance disclosures for all institutions. 74 Fed.Reg. 5584, January 29, 2009, amended 74 Fed.Reg. 17768, April 17, 2009.

2727

Background-clarifications to the final rules

On February 19, 2010, 75 Fed.Reg. 9120, proposed clarifications to the final rule under Regulation E addressing overdraft services as issued on November 17, 2009.

On February 19, 2010, 75 Fed.Reg. 9126, proposed clarifications to the final rule under Regulation DD addressing the uniformity and adequacy of information provided to consumers when they overdraw their account as issued on January 29, 2009.

On April 29, 2010, supplemental guidance on overdraft protections programs issued by OTS, at 75 Fed.Reg. 22681.

2828

Background-clarifications to the final rules

On June 4, 2010, final rule issued under the proposed clarifications to the final rule under Regulation E addressing overdraft services as issued on November 17, 2009. 75 Fed.Reg. 31665.

On June 4, 2010, final rule under the proposed clarifications to the final rule under Regulation DD addressing the uniformity and adequacy of information provided to consumers when they overdraw their account as issued on January 29, 2009. 75 Fed.Reg. 31673.

Final rule under Regulation E prohibits a financial institution from charging overdraft fee against consumer’s account where the institution pays an overdraft due to an ATM or one-time (“everyday”) debit card transaction, unless the consumer has affirmatively consented to the overdraft service for that type of transaction.

Final rule under Regulation DD requires all depository institutions to disclose aggregate fees relating to overdraft services on periodic statements. The final rule also addresses balance disclosures provided to consumers through automated systems.

3030

Key highlights of Regulation E’s final rule

Consumer’s affirmative consent or opt-in .

Covered consumers.

Conditioning the opt-in.

Same account terms, conditions, and features.

Mandatory compliance date.

3131

Opt-in

Opt-in. A financial institution holding a consumer’s account may not assess an overdraft fee for paying an ATM or one-time debit card transaction pursuant to an overdraft service, unless the institution complies with the following steps: Provides the consumer with a notice in writing, or if the consumer agrees,

electronically, describing the service.

Provides a reasonable opportunity for the consumer to consent to the service.

Obtains the consumer’s consent.

Provides the consumer with confirmation of that consent and informs the consumer of the right to revoke that consent.

May assess overdraft fee for other debits (ACH, checks).

But FDIC suggests opt out opportunity for these transactions. FDIC Overdraft Payment Supervisory Guidance, FIL-81-2010, November 24, 2010: http://www.fdic.gov/news/news/financial/2010/fil10081.html

3232

Opt-in notice

Opt-in notice. The notice must be “substantially” similar to Model Form A-9: A brief description of the service and the types of

transactions for which fees may be imposed.

The dollar amount of any fees for the service.

Maximum number of fees assessable daily, if any.

Disclosure of opt-in right.

Options for covering overdrafts.

Permitted modification of model form.

Reasonable method to identify the account for which a consumer submits the opt in notice.

3333

Consumers covered

All consumers are covered: For accounts opened prior to July 1, 2010, the financial

institution must not assess any fee on a consumer’s account on or after August 15, 2010, for paying an ATM or one-time debit card transaction, unless consumer consents.

For accounts opened on or after July 1, 2010, the financial institution must obtain the consumer’s consent before the institution assesses any fee on the consumer’s account for paying an ATM or one-time debit card transaction.

3434

Conditioning the opt-in

A financial institution must not: Condition the payment of overdrafts for checks, ACH, and

other transactions on the consumer consenting to the institution’s payment of ATM and one-time debit card transactions.

Decline to pay checks, ACH, and other transactions overdrawing the consumer’s account because the consumer has not consented to the institution’s payment of ATM and one-time debit card transactions.

Example of condition: Financial institution pays recurring debit card transactions if consumer consents to one-time debit card transactions.

3535

Same account terms, conditions, and features

A financial institution must provide to consumers not consenting to this overdraft service the same account terms, conditions, and features provided to consumers consenting.

Examples: Fees and interest rates; minimum balance requirements; account features, e.g., online bill payment; and the type of ATM or debit card provided to the consumer.

36

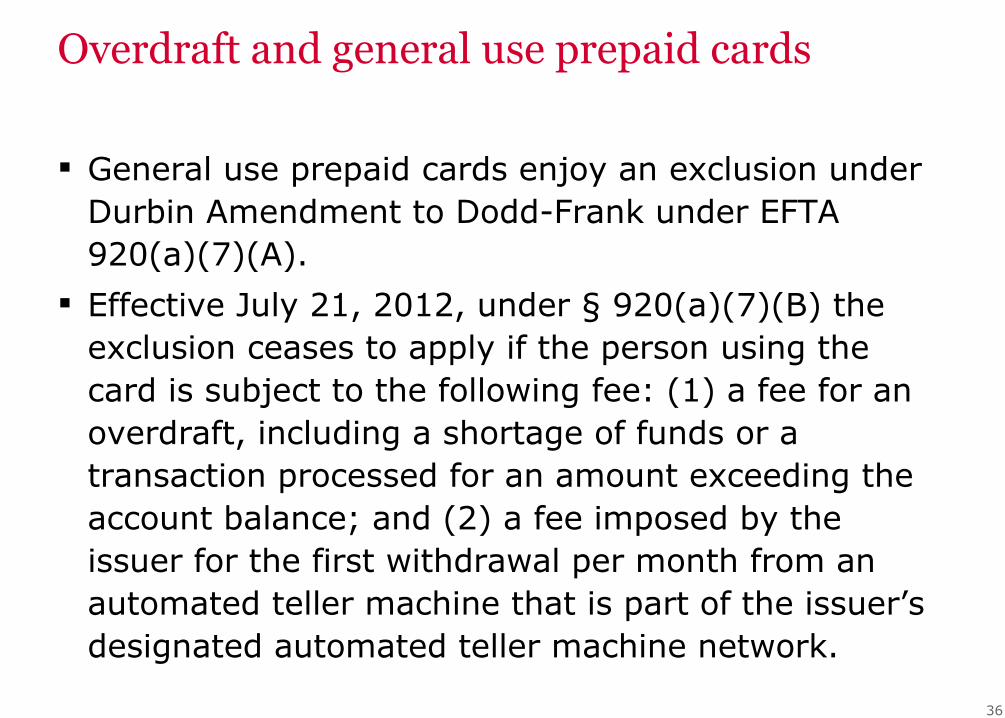

Overdraft and general use prepaid cards

General use prepaid cards enjoy an exclusion under Durbin Amendment to Dodd-Frank under EFTA 920(a)(7)(A).

Effective July 21, 2012, under § 920(a)(7)(B) the exclusion ceases to apply if the person using the card is subject to the following fee: (1) a fee for an overdraft, including a shortage of funds or a transaction processed for an amount exceeding the account balance; and (2) a fee imposed by the issuer for the first withdrawal per month from an automated teller machine that is part of the issuer’s designated automated teller machine network.

3737

Regulation E final rule –questions and issues

Outstanding negative balance: If an overdraft fee is based on the amount of the

outstanding negative balance, an institution is prohibited from assessing any such fee if the negative balance is solely attributable to an ATM or one-time debit card transaction (unless the consumer has opted in).

If a negative balance is attributable in whole or in part to a check, ACH, or other type of transaction not subject to the prohibition on assessing overdraft fees, an institution may assess the fee, even absent an opt-in by the consumer.

3838

Regulation E final rule –questions and issues

If the consumer has not consented to the overdraft service, the prohibition on assessing overdraft fees applies to all overdraft fees, including daily or sustained overdraft, negative balance, or similar fee. Assume $50 available balance on March 1. Bank has $60 one-time

debit card transaction and a $40 check transaction, where the consumer has not opted in. Bank has an overdraft fee of $20 and sustained overdraft fee starting on fifth day. Bank can assess overdraft fee for check. Account is now overdrawn $70. Bank can also assess sustained overdraft fee (on fifth day) as to this overdraft, as overdraft is in part attributable to check.

Same as above but a $40 deposit is made on March 3; credited to debit card transaction first by bank per its posting order. Overdraft reduction to $30. Bank can assess sustained overdraft fee on March 6, as overdraft is attributable to the check transaction.

3939

Regulation E final rule –questions and issues

Note that in the above transaction, had bank applied the $40 deposit to $40 check transaction per posting order, the sustained overdraft fee may not be assessed, as overdraft is due solely to debit card transaction of $60.

Assume $50 available balance on March 1. Bank has $60 one-time debit card transaction, where customer has not opted in. Account is overdrawn $10. Bank cannot assess overdraft fee. Bank has a $100 check on March 3, overdraft is $130. Bank can assess overdraft fee of $20 as to check. Bank can also assess sustained overdraft fee as to this overdraft, but only after March 3 (on March 6, the fifth day).

What about tiered sustained overdraft fee?

4040

Regulation E final rule –questions and issues

Alternative method, for institutions without specific deposit allocation policy. For a consumer not opting in to an overdraft service, an institution may also elect not to assess daily or sustained overdraft, negative balance, or similar fee unless a consumer’s negative balance is attributable solely to check, ACH, or other type of transaction not subject to the fee prohibition.

If an institution so elects, an institution would not have to determine how to allocate subsequent deposits reducing but not eliminating the negative balance.

For example, if a consumer has a negative balance of $30, of which $10 is attributable to a one-time debit card transaction, an institution may elect not to assess a sustained overdraft fee while that balance remains outstanding.

4141

Regulation E final rule –questions and issues

Consent questions: What if the consumer writes in more than one account

number?

What if the consumer writes in the consumer’s debit card number?

Tracking information providing the name of the banker; the date; branch number or name; and bar code or other tracking information.

Does prohibition on overdraft fees apply to expenses and fees for collecting overdraft?

4242

Regulation DD final rule

Effective January 1, 2010, a depository institution must, regardless of whether it promotes overdrafts: Disclose on periodic statements the aggregate dollar amount

totals for overdraft fees and returned item fees, both for the statement period as wells as calendar year-to-date.

For account balance disclosure through an automated system (ATM, online, telephone) exclude additional amounts the institution may provide or that may be transferred from another account of the consumer.

4343

Regulation DD final rule-questions and issues

The disclosure of overdraft fees presents questions: Are continuous overdraft fees captured within the meaning

of an overdraft fee?

If a financial institution charges back a dishonored deposited item causing an overdraft and assesses a fee for that overdraft, is that fee an overdraft fee?

Account balance with a linked, retail sweep account may be disclosed consistent with this rule. Even if that sweep product is an investment product, its balance may be disclosed.