Page 1

SMART BOOK

ACCOUNTANCY 1

SMART BOOK SMART BOOK SMART BOOK INTERMEDIATE - FIRST YEAR

ACCOUNTANCY SMART BOOK

UNIT –I CONCEPT OF BUSINESS

1) From the following Trial Balance of Mr. Johnson, prepare the

Trading, Profit and Loss Account and Balance Sheet for the year

ended 31-3-2014:

Dr Trial Balance as on 31-3-2014 Cr

Particulars

Amount

Rs.

Particulars

Amount

Rs.

Cash in hand

Cash at Bank

Purchases

Sales Returns

Wages

Salaries

Advertisement

Insurance

Furniture

Opening Stock

Machinery

Debtors

Carriage Inwards

Carriage outwards

Rent & Taxes

Drawings

Bills Receivable

6,000

12,500

78500

2000

8,000

12,500

3,000

1,100

12,000

40,000

35,000

23,000

1,000

1,500

2,500

4,800

9,000

2,52,400

Sales

Capital

Purchase Returns

Interest

Creditors

Bills Payable

Discount

1,32,000

95,000

1,000

900

10,000

11,500

2,000

2,52,400

Page 2

SMART BOOK

ACCOUNTANCY 2

Adjustments:

1) Value of Stock as on 31-3-2014 is Rs. 37000.

2) Outstanding Wages Rs. 1,200; Salaries Rs. 2,900

3) Prepaid Insurance Rs. 450

4) Depreciate Furniture by 5%; Machinery by 10%

5) Write off Bad debts Rs. 2,000 and provide Bad debts reserve 5%.

Ans: Trading and Profit & Loss A/c of Mr. Johnson

Dr for the year ending 31-03-2014 Cr

Particulars Amount Rs.

Amount Rs.

Particulars Amount Rs.

Amount Rs.

To Opening Stock

To Purchases

Less : Returns

To Wages

Add : Outstanding

To Carriage In-

wards

To Gross Profit

To Salaries

Add : Outstanding

To Insurance

Less : Prepaid

To Advertisement

To Carriage Out-

wards

To Rent, taxes

To Bad debts

To Bad Debts Re-

serve

To Dep. On Furni-

ture

To Dep. On Ma-

chinery

To Net profit

78,500 1,000 8,000 1,200

12,500 2,900 1,100

450

40,000

77500

9,200

1,000 39,300

1,67,000

15,400

650 3,000

1,500 2,500 2,000

1150

600

3,500 11,900

42,200

By Sales Less : Re-

turns By Closing

Stock By Gross

Profit By Interest By Discount

1,32,000

2,000

1,30,000

37,000

1,67,000

39,300

900 2,000

42,200

Page 3

SMART BOOK

ACCOUNTANCY 3

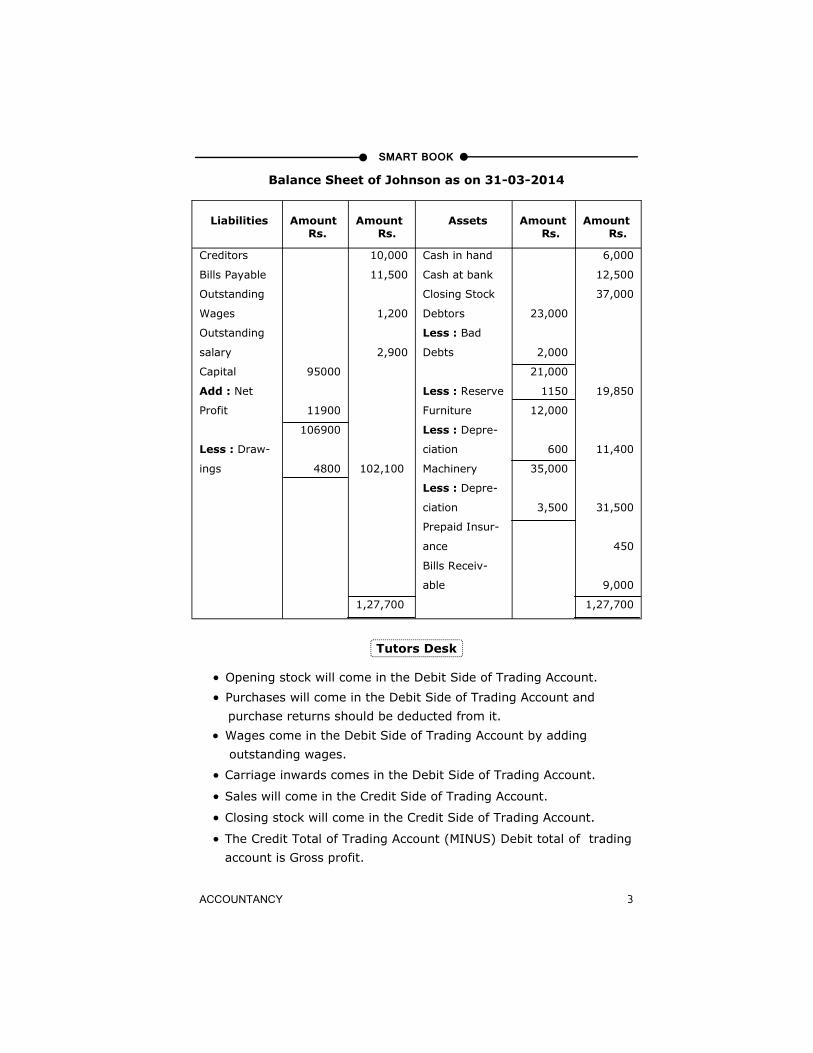

Balance Sheet of Johnson as on 31-03-2014

Tutors Desk

Opening stock will come in the Debit Side of Trading Account.

Purchases will come in the Debit Side of Trading Account and

purchase returns should be deducted from it.

Wages come in the Debit Side of Trading Account by adding

outstanding wages.

Carriage inwards comes in the Debit Side of Trading Account.

Sales will come in the Credit Side of Trading Account.

Closing stock will come in the Credit Side of Trading Account.

The Credit Total of Trading Account (MINUS) Debit total of trading

account is Gross profit.

Liabilities

Amount Rs.

Amount Rs.

Assets

Amount Rs.

Amount Rs.

Creditors

Bills Payable

Outstanding

Wages

Outstanding

salary

Capital

Add : Net

Profit

Less : Draw-

ings

95000

11900

106900

4800

10,000

11,500

1,200

2,900

102,100

1,27,700

Cash in hand

Cash at bank

Closing Stock

Debtors

Less : Bad

Debts

Less : Reserve

Furniture

Less : Depre-

ciation

Machinery

Less : Depre-

ciation

Prepaid Insur-

ance

Bills Receiv-

able

23,000

2,000

21,000

1150

12,000

600

35,000

3,500

6,000

12,500

37,000

19,850

11,400

31,500

450

9,000

1,27,700

Page 4

SMART BOOK

ACCOUNTANCY 4

Salaries will come in the Debit Side of profit and Loss Account and

outstanding salaries will be added to it.

Insurance will come in the Debit Side of profit and Loss Account and

prepaid Insurance will be deducted from it.

Advertisement will come in the Debit Side of profit and Loss

Account.

Carriage outwards will come in the Debit Side of profit and Loss

Account.

Rent, taxes will come in the Debit Side of profit and Loss Account.

Bad Debts will come in the Debit side of profit and Loss Account.

Bad Debts Reserve will come in the Debit Side of profit and Loss

Account.

Depreciation on Furniture and Depreciation on machinery will come

in the Debit Side of profit and Loss Account.

Interest Received comes in the Credit Side of profit and Loss

Account .

Discount Received comes in the Credit Side of profit and Loss

Account.

The Total credit of profit and Loss Account (MINUS) Total Debit of

profit and Loss Account is Net profit.

Creditors will come in the liabilities side of Balance Sheet.

Bill payable will come in the liabilities side of Balance Sheet.

Outstanding wages will come in the liabilities side of Balance Sheet.

Outstanding salary will come in the liabilities side of Balance Sheet.

Capital will come in the liabilities side of Balance sheet. And Net

profit should be added to capital.

Drawings should be deducted from capital

Cash in hand will come in the Assets side of Balance sheet.

Cash at Bank will come in the Assets side of Balance sheet.

Closing stock will come in the Assets side of Balance sheet.

Debtors will come in the Assets side of Balance sheet and Bad Debt

and Reserve for Bad Debts will be deducted from Debtors.

Furniture will come in the Assets side of Balance Sheet and

depreciation on Furniture will be deducted from it.

Machinery will come in the Assets side of Balance sheet and

depreciation on machinery will be deducted from it.

Page 5

SMART BOOK

ACCOUNTANCY 5

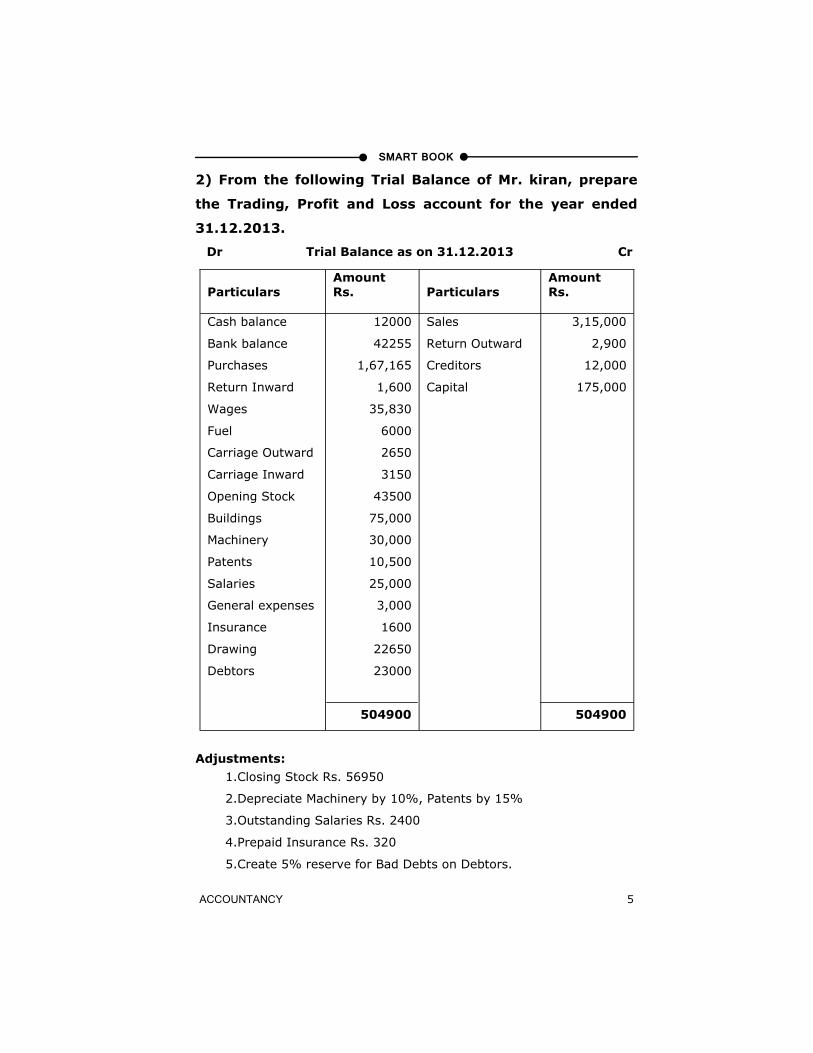

2) From the following Trial Balance of Mr. kiran, prepare

the Trading, Profit and Loss account for the year ended

31.12.2013.

Dr Trial Balance as on 31.12.2013 Cr

Adjustments:

1.Closing Stock Rs. 56950

2.Depreciate Machinery by 10%, Patents by 15%

3.Outstanding Salaries Rs. 2400

4.Prepaid Insurance Rs. 320

5.Create 5% reserve for Bad Debts on Debtors.

Particulars

Amount Rs.

Particulars

Amount Rs.

Cash balance

Bank balance

Purchases

Return Inward

Wages

Fuel

Carriage Outward

Carriage Inward

Opening Stock

Buildings

Machinery

Patents

Salaries

General expenses

Insurance

Drawing

Debtors

12000

42255

1,67,165

1,600

35,830

6000

2650

3150

43500

75,000

30,000

10,500

25,000

3,000

1600

22650

23000

504900

Sales

Return Outward

Creditors

Capital

3,15,000

2,900

12,000

175,000

504900

Page 6

SMART BOOK

ACCOUNTANCY 6

Ans. Trading and Profit & Loss A/c of Mr Kiran

Dr for the year ending 31-12-2013 Cr

Particulars Amount Rs.

Amount Rs.

Particulars Amount Rs.

Amount Rs.

To Opening Stock To Purchases Less : Returns To Wages To Fuel To Carriage

Inward To Gross Profit To Salaries Add : Out-

standing To General

Expenses To Insurance Less : Prepaid To Carriage Out-

wards To Dep. On

Machinery To Dep. On

Patents To Bad Debts

Reserve To Net Profit

167165 2,900

25,000

2,400

1600 320

43,500

1,64,265 35,830 6,000

3,150 1,17,605 3,70,350

27,400

3,000

1280

2,650

3,000

1,575

1150 77550

117605

By Sales Less : Re-

turns By Closing

Stock By Gross

Profit

315000

1600

313400 56950

3,70,350

1,17605

117605

Page 7

SMART BOOK

ACCOUNTANCY 7

Balance Sheet of Mr. kiran as on 31-12-2013

Opening stock will come in the Debit Side of Trading Account.

Purchases will come in the Debit Side of Trading Account and

purchase returns should be deducted from it.

Wages come in the Debit Side of Trading Account.

Carriage inwards comes in the Debit Side of Trading Account.

Fuel comes in the Debit Side of Trading Account.

Sales will come in the Credit Side of Trading Account

Closing stock will come in the Credit Side of Trading Account

The Credit Total of Trading Account (MINUS) Debit total of Trading

Account is Gross profit.

Liabilities Amount Rs.

Amount Rs.

Assets Amount Rs.

Amount Rs.

Outstanding

Salaries

Creditors Capital Add :

Net Profit

Less : Draw-

ings

175,000

77,550

2,52,550

22650

2,400

12,000

229900

2,44,300

Prepaid In-

surance Cash

Balance Bank

Balance Closing

Stock Debtors Less : Bad

Debts Machinery Less :

Depreciation Patents Less :

Depreciation

Buildings

23,000

1150 30,000

3,000 10,500

1,575

320

12000

42255

56950

21,850

27,000

8,925

75,000

2,44,300

Tutors Desk

Page 8

SMART BOOK

ACCOUNTANCY 8

Salaries will come in the Debit Side of profit and Loss Account and

outstanding salaries will be added to it

Insurance will come in the Debit Side of profit and Loss Account and

prepaid Insurance will be deducted from it

General expenses will come in the debit side of profit and loss

account.

Carriage outwards will come in the Debit Side of profit and Loss

account.

Bad Debts Reserve will come in the Debit Side of profit and Loss

account.

Depreciation on patents and Depreciation on machinery will come in

the Debit Side of profit and Loss Account.

The Total credit of profit and Loss Account (MINUS) Total Debit of

profit and Loss Account is Net profit.

Creditors will come in the liabilities side of Balance Sheet.

Outstanding salary will come in the liabilities side of Balance Sheet.

Capital will come in the liabilities side of Balance sheet. And Net

profit should be added to capital.

Drawings should be deducted from capital.

Cash balance will come in the Assets side of Balance sheet.

Bank balance will come in the Assets side of Balance sheet.

Closing stock will come in the Assets side of Balance sheet.

Debtors will come in the Assets side of Balance sheet and Reserve

for Bad Debts will be deducted from Debtors.

Patents will come in the Assets side of Balance Sheet and

Depreciation on patents will be deducted from it.

Machinery will come in the Assets side of Balance sheet and

Depreciation on machinery will be deducted from it.

Prepaid insurance will come in the Assets side of Balance Sheet.

Building will come in the assets of the balance sheet.

Page 9

SMART BOOK

ACCOUNTANCY 9

3) From the following Trial Balance of Mr. Manohar, prepare the

Trading, Profit & Loss account and Balance Sheet for the year

ended 31.12.2010.

Dr Trial Balance as on 31.12.2010 Cr

Adjustments:

1) Outstanding Wages Rs. 3,100 and Outstanding Salaries Rs. 2,225

2) Prepaid Insurance Rs. 125

3) Create 5% reserve for Bad Debts on Debtors

4) Depreciate Furniture by Rs. 500 and Machinery by Rs. 1300

5) Closing Stock Rs. 24,500

Particulars Amount

Rs.

Particulars Amount

Rs.

Salaries

Purchases

Wages

Carriage on Purchases

Office Expenses

Commission

Debtors

Furniture

Machinery

Insurance

Bills Receivable

Cash balance

Bank balance

9,800

21,600

12000

1300

850

500

15,000

5,000

13,000

500

2,300

23000

42,750

1,47,600

Sales

Creditors

Capital

Bills Payable

87,000

12,000

45,000

3,600

1,47,600

Page 10

SMART BOOK

ACCOUNTANCY 10

Ans.

Trading and Profit & Loss A/c of Mr. Manohar

for the year ended 31-12-2010

Dr Cr

Particulars Amount

Rs.

Amount

Rs.

Particulars Amount

Rs.

Amount

Rs.

To Purchases To Wages Add : Out-

standing To Carriage on

Purchases To Gross Profit To Salaries Add : Out-

standing To Office Ex-

penses To Commission To Insurance Less : Prepaid To Reserve for

Bad Debts To Dep. On

Furniture To Dep. On

Machinery To Net Profit (Transferred to

Capital A/c)

12,000

3,100

9,800 2,225

500 125

21,600

15100

1,300 73,500 1,11,500

12,025

850 500

375

750

500

1300

57200

73,500

By Sales By Closing

Stock

By Gross

Profit

87,000

24,500

1,11500

73,500

73,500

Page 11

SMART BOOK

ACCOUNTANCY 11

Balance Sheet of Mr. Manohar as on 31-12-2010

Purchases will come in the Debit Side of Trading Account.

Wages come in the Debit Side of Trading Account by adding

outstanding wages. Carriage on purchases is also known as

carriage inward, it comes in the debit side of trading account.

Sales will come in the Credit Side of Trading Account.

Closing stock will come in the Credit Side of Trading Account

The Credit Total of Trading Account (MINUS) Debit total of trad-

ing account is Gross profit.

Salaries will come in the Debit Side of profit and Loss Account and

outstanding salaries will be added to it.

Insurance will come in the Debit Side of profit and Loss Account

and prepaid Insurance will be deducted from it.

Office Expenses will come in the Debit Side of profit and Loss

Account.

Liabilities

Amount Rs.

Amount Rs.

Assets

Amount Rs.

Amount Rs.

Capital

Add : Net

Profit

Creditors

Bills Payable

Outstanding

Wages

Outstanding

Salaries

45,000

57,200

102200

12,000

3,600

3,100

2225

123125

Cash in hand Cash at bank Bills Receiv-

able Machinery Less : Depre-

ciation Furniture Less : Depre-

cation

Debtors Less: Re-

serves for Bad

debts Closing Stock Prepaid Insur-

ance

13,000

1300 5,000

500 15,000

750

23,000

42,750

2,300

11,700

4500

14,250

24,500

125

123125

Tutors Desk

Page 12

SMART BOOK

ACCOUNTANCY 12

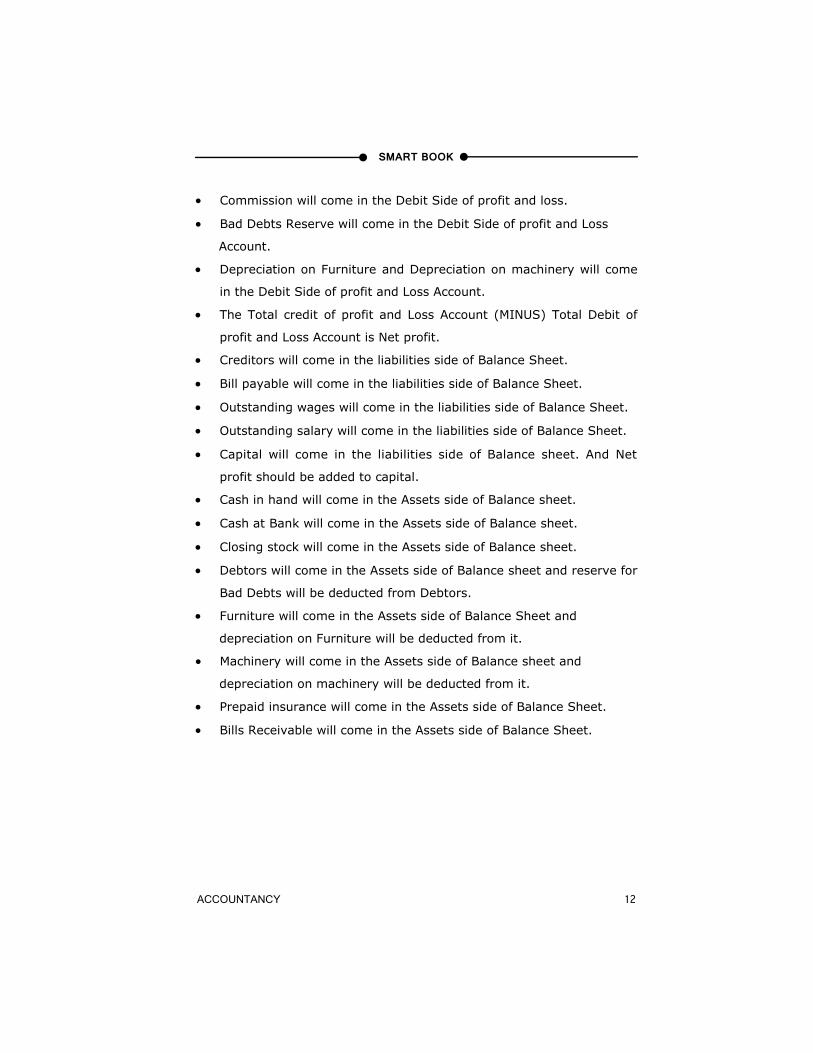

Commission will come in the Debit Side of profit and loss.

Bad Debts Reserve will come in the Debit Side of profit and Loss

Account.

Depreciation on Furniture and Depreciation on machinery will come

in the Debit Side of profit and Loss Account.

The Total credit of profit and Loss Account (MINUS) Total Debit of

profit and Loss Account is Net profit.

Creditors will come in the liabilities side of Balance Sheet.

Bill payable will come in the liabilities side of Balance Sheet.

Outstanding wages will come in the liabilities side of Balance Sheet.

Outstanding salary will come in the liabilities side of Balance Sheet.

Capital will come in the liabilities side of Balance sheet. And Net

profit should be added to capital.

Cash in hand will come in the Assets side of Balance sheet.

Cash at Bank will come in the Assets side of Balance sheet.

Closing stock will come in the Assets side of Balance sheet.

Debtors will come in the Assets side of Balance sheet and reserve for

Bad Debts will be deducted from Debtors.

Furniture will come in the Assets side of Balance Sheet and

depreciation on Furniture will be deducted from it.

Machinery will come in the Assets side of Balance sheet and

depreciation on machinery will be deducted from it.

Prepaid insurance will come in the Assets side of Balance Sheet.

Bills Receivable will come in the Assets side of Balance Sheet.

Page 13

SMART BOOK

ACCOUNTANCY 13

4) From the following particulars, prepare Trading, Profit & Loss

Account and balance Sheet for the year ended 31-03-2013

Dr Cr

Adjustments:

1) Closing Stock Rs. 84,800

2) Interest on Capital 6%, is to be provided

3) Write off Rs. 3,800 as Bad Debts and provide 5% Reserve for

Doubtful Debts.

4) Outstanding Wages Rs. 2,600

Particulars Amount

Rs.

Particulars Amount

Rs. Cash

Factory Insurance

Audit Charges

Goodwill

Wages

Debtors

Opening Stock

Machinery

Purchases

Carriage Inwards

Salaries

Office Rent

bank

Rent paid in advance

98,200

4250

3,500

30,000

8500

40,000

28500

56400

126500

2,000

32,500

8,000

100000

1000

539350

43,000

14,500

1,78000

16500

273000

3,000

7850

3,500

539350

Creditors

Bills Payable

Capital

Commission

received

Sales

Return Out-

wards

Interest

received

Outstanding

Salaries

Page 14

SMART BOOK

ACCOUNTANCY 14

By Sales

By Closing

Stock

By Gross

Profit

By Commis-

sion Re-

ceived

By Interest

Received

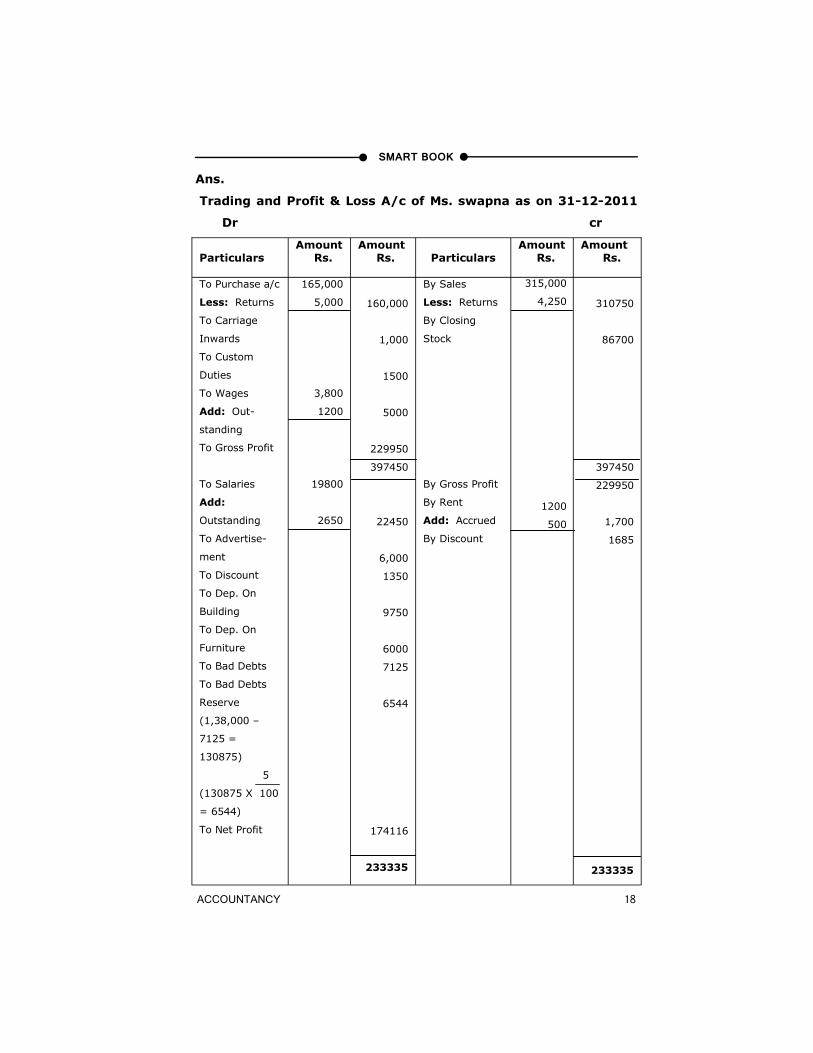

Ans. Trading and Profit & Loss A/c for the year ended Dr 31-03-2013 Cr

Particulars

Amount

Rs.

Amount

Rs.

Particulars

Amount

Rs.

Amount

Rs.

To Opening

Stock

To Purchases

Less: Returns

To Carriage In-

wards

To Factory In-

surance

To Wages

Add: Out-

standing

To Gross Profit

To Audit

Charges

To Salaries

To Office Rent

To Interest on

Capital

To Bad Debts

To Bad Debts

Reserve

To Net Profit

126500

3,000

8,500

2,600

28,500

123500

2000

4250

11,100

188,450

3,57,800

3,500

32,500

8,000

10,680

3,800

1,810

152,510

212,800

2,73,000

84,800

3,57,800

188,450

16,500

7,850

212,800

Page 15

SMART BOOK

ACCOUNTANCY 15

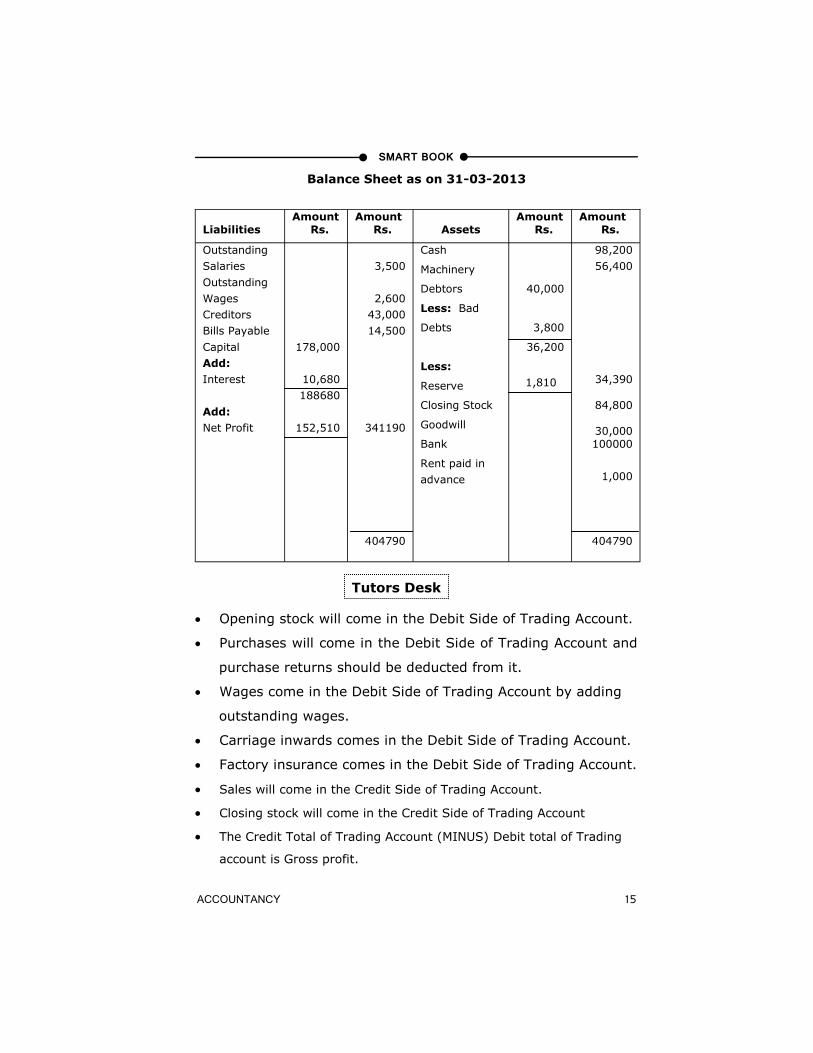

Balance Sheet as on 31-03-2013

Opening stock will come in the Debit Side of Trading Account.

Purchases will come in the Debit Side of Trading Account and

purchase returns should be deducted from it.

Wages come in the Debit Side of Trading Account by adding

outstanding wages.

Carriage inwards comes in the Debit Side of Trading Account.

Factory insurance comes in the Debit Side of Trading Account.

Sales will come in the Credit Side of Trading Account.

Closing stock will come in the Credit Side of Trading Account

The Credit Total of Trading Account (MINUS) Debit total of Trading

account is Gross profit.

Liabilities

Amount Rs.

Amount Rs.

Assets

Amount Rs.

Amount Rs.

Outstanding

Salaries

Outstanding

Wages

Creditors

Bills Payable

Capital

Add:

Interest

Add:

Net Profit

178,000

10,680

188680

152,510

3,500

2,600

43,000

14,500

341190

404790

Cash

Machinery

Debtors

Less: Bad

Debts

Less:

Reserve

Closing Stock

Goodwill

Bank

Rent paid in

advance

40,000

3,800

36,200

1,810

98,200

56,400

34,390

84,800

30,000 100000

1,000

404790

Tutors Desk

Page 16

SMART BOOK

ACCOUNTANCY 16

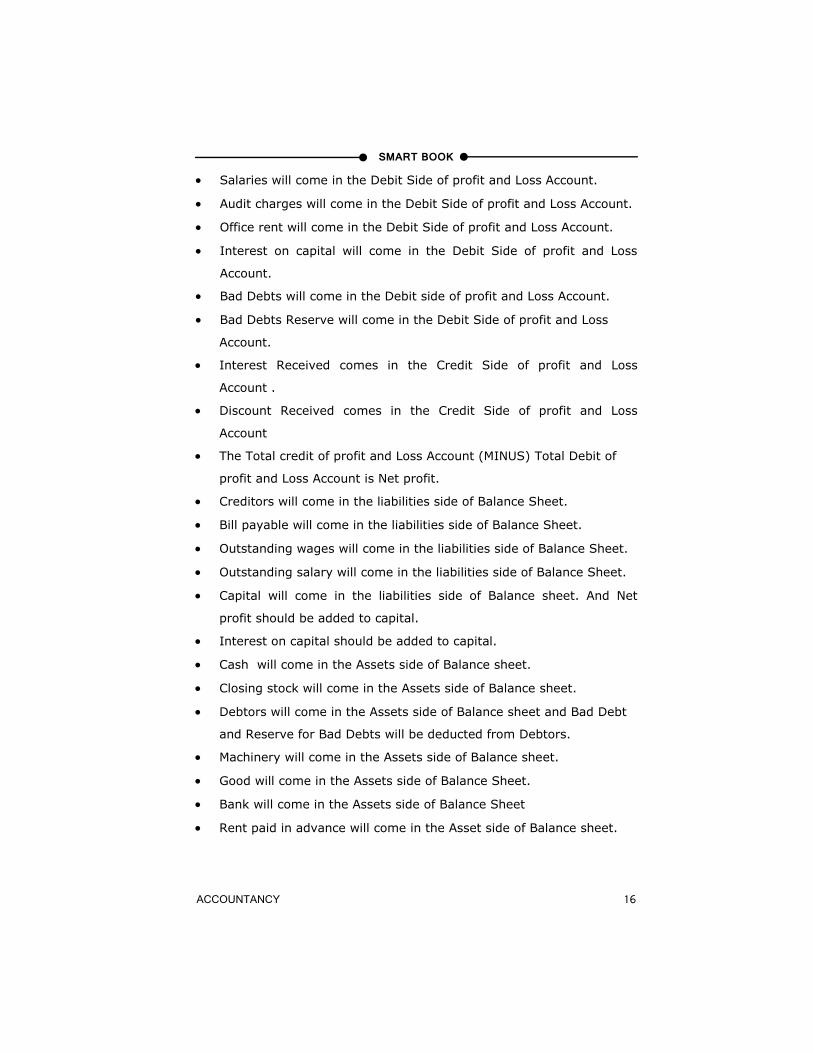

Salaries will come in the Debit Side of profit and Loss Account.

Audit charges will come in the Debit Side of profit and Loss Account.

Office rent will come in the Debit Side of profit and Loss Account.

Interest on capital will come in the Debit Side of profit and Loss

Account.

Bad Debts will come in the Debit side of profit and Loss Account.

Bad Debts Reserve will come in the Debit Side of profit and Loss

Account.

Interest Received comes in the Credit Side of profit and Loss

Account .

Discount Received comes in the Credit Side of profit and Loss

Account

The Total credit of profit and Loss Account (MINUS) Total Debit of

profit and Loss Account is Net profit.

Creditors will come in the liabilities side of Balance Sheet.

Bill payable will come in the liabilities side of Balance Sheet.

Outstanding wages will come in the liabilities side of Balance Sheet.

Outstanding salary will come in the liabilities side of Balance Sheet.

Capital will come in the liabilities side of Balance sheet. And Net

profit should be added to capital.

Interest on capital should be added to capital.

Cash will come in the Assets side of Balance sheet.

Closing stock will come in the Assets side of Balance sheet.

Debtors will come in the Assets side of Balance sheet and Bad Debt

and Reserve for Bad Debts will be deducted from Debtors.

Machinery will come in the Assets side of Balance sheet.

Good will come in the Assets side of Balance Sheet.

Bank will come in the Assets side of Balance Sheet

Rent paid in advance will come in the Asset side of Balance sheet.

Page 17

SMART BOOK

ACCOUNTANCY 17

5) The following is the Trial Balance of Ms. swapna. Prepare

Trading and Profit & Loss account for the year ending 31-12-

2011 and Balance Sheet as on that date.

Ans:

Trial Balance

Adjustments:

1) Closing Stock as on 31.12.2011 Rs. 86700

2) Rent Accrued Rs. 500

3) Outstanding Wages Rs.1200, Salaries Rs. 2650

4) Depreciation on Buildings 5%, Furniture 10%

5) Bad Debts Rs. 7125, Provision for Bad Debts 5% maintained

Particulars

Debit

Rs.

Credit

Rs.

Purchases, Sales

Returns

Capital

Drawings

Advertisement

Salaries

Carriage Inwards

Custom Duties

Wages

Buildings

Furniture

Rent

Discount

Debtors, Creditors

Bank Loan

165000

4250

4,000

6,000

19800

1,000

1500

3,800

195,000

60,000

1350

138000

599700

315000

5000

138000

1200

1685

16000

122815

599700

Page 18

SMART BOOK

ACCOUNTANCY 18

Ans.

Trading and Profit & Loss A/c of Ms. swapna as on 31-12-2011

Dr cr

Particulars

Amount Rs.

Amount Rs.

Particulars

Amount Rs.

Amount Rs.

To Purchase a/c

Less: Returns

To Carriage

Inwards

To Custom

Duties

To Wages

Add: Out-

standing

To Gross Profit

To Salaries

Add:

Outstanding

To Advertise-

ment

To Discount

To Dep. On

Building

To Dep. On

Furniture

To Bad Debts

To Bad Debts

Reserve

(1,38,000 –

7125 =

130875)

5

(130875 X 100

= 6544)

To Net Profit

165,000

5,000

3,800

1200

19800

2650

160,000

1,000

1500

5000

229950

397450

22450

6,000

1350

9750

6000

7125

6544

174116

233335

By Sales

Less: Returns

By Closing

Stock

By Gross Profit

By Rent

Add: Accrued

By Discount

310750

86700

397450

229950

1,700

1685

233335

315,000 4,250

1200 500

Page 19

SMART BOOK

ACCOUNTANCY 19

Balance sheet of Ms. Swapna as on 31-12-2011

Purchases will come in the Debit Side of Trading Account and

purchase returns should be deducted from it.

Wages come in the Debit Side of Trading Account by adding

outstanding wages.

Carriage inwards comes in the Debit Side of Trading Account.

Custom Duty comes in the Debit Side of Trading Account.

Sales will come in the Credit Side of Trading Account.

Closing stock will come in the Credit Side of Trading Account.

The Credit Total of Trading Account (MINUS) Debit total of Trading

Account is Gross profit.

Salaries will come in the Debit Side of profit and Loss Account and

outstanding salaries will be added to it.

Liabilities

Amount Rs.

Amount Rs.

Assets

Amount Rs.

Amount Rs.

Outstanding

Wages

Outstanding

salaries

Creditors

Bank Loan

Capital

Add: Net

Profit

Less:

Drawings

138000

174116

312116

4000

1200

2650

16000

122815

308116

450781

Closing

Stock

Debtors

Less: Bad

Debts

Less:

Reserve

Furniture

Less:

Depreciation

Buildings

Less:

Depreciation

Accrued

Rent

138000

7125

130875

6544

60000

6000

195000

9750

86700

124331

54000

185250

500

450781

Tutors Desk

Page 20

SMART BOOK

ACCOUNTANCY 20

Advertisement will come in the Debit Side of profit and Loss Account.

Discount will come in the Debit Side of profit and Loss Account.

Bad Debts will come in the Debit side of profit and Loss Account.

Bad Debts Reserve will come in the Debit Side of profit and Loss

account.

Depreciation on Furniture and Depreciation on building will come in

the Debit Side of profit and Loss Account.

Discount Received comes in the Credit Side of profit and Loss

account.

Rent Received comes in the Credit Side of profit and Loss Account

and it will added by Accrued Rent.

The Total credit of profit and Loss Account (MINUS) Total Debit of

profit and Loss Account is Net profit.

Creditors will come in the liabilities side of Balance Sheet.

Bank loan will come in the liabilities side of Balance Sheet.

Outstanding wages will come in the liabilities side of Balance Sheet.

Outstanding salary will come in the liabilities side of Balance Sheet.

Capital will come in the liabilities side of Balance sheet. And Net

profit should be added to capital.

Drawings should be deducted from capital

Closing stock will come in the Assets side of Balance sheet.

Debtors will come in the Assets side of Balance sheet and Bad Debt

and Reserve for Bad Debts will be deducted from Debtors.

Furniture will come in the Assets side of Balance Sheet and

Depreciation on Furniture will be deducted from it.

Building will come in the Assets side of Balance sheet and

depreciation on machinery will be deducted from it.

Accrued rent will come in the Assets side of Balance Sheet.