David Hamilton, PhD Managing Director, Singapore Glenn Levine Senior Economic Research Analyst, New York Preparing for Defaults in China’s Corporate Credit Market 1 Irina Baron Quantitative Credit Risk, New York

Transcript

David Hamilton, PhDManaging Director, Singapore

Glenn LevineSenior Economic Research Analyst, New York

Preparing for Defaults in

China’s Corporate Credit

Market

1

Irina BaronQuantitative Credit Risk, New York

Today’s Presenters

2

David Hamilton, PhD

Managing DirectorStress Testing and Credit Risk Analytics, Asia-Pacific

Singapore

Glenn Levine

Corporate Stress Testing Model Lead, Capital Markets Research Group

New York

Irina Baron

Quantitative Credit Risk Research Analyst, Capital Markets Research Group

New York

About Moody’s Analytics

3

Credit RatingsCredit Research

Credit Risk and Macroeconomic ModelsSoftwareDataMacroeconomic and Credit ResearchTraining and CertificationConsulting and Advisory Services

Global Presence, Local Expertise

Preparing for Defaults in China’s Corporate

Credit Market

4

1. China’s macroeconomic and credit risk outlook

What are key statistics telling us about future risk?

2. Measuring and managing the default risk of Chinese firms

What strategies are effective for spotting the riskiest exposures in a credit portfolio?

3. Incorporating macroeconomic variables into default risk forecasts

How can we condition PDs on macroeconomic variables?

How can we utilize such conditioned PDs for stress testing and IFRS 9 impairment calculations?

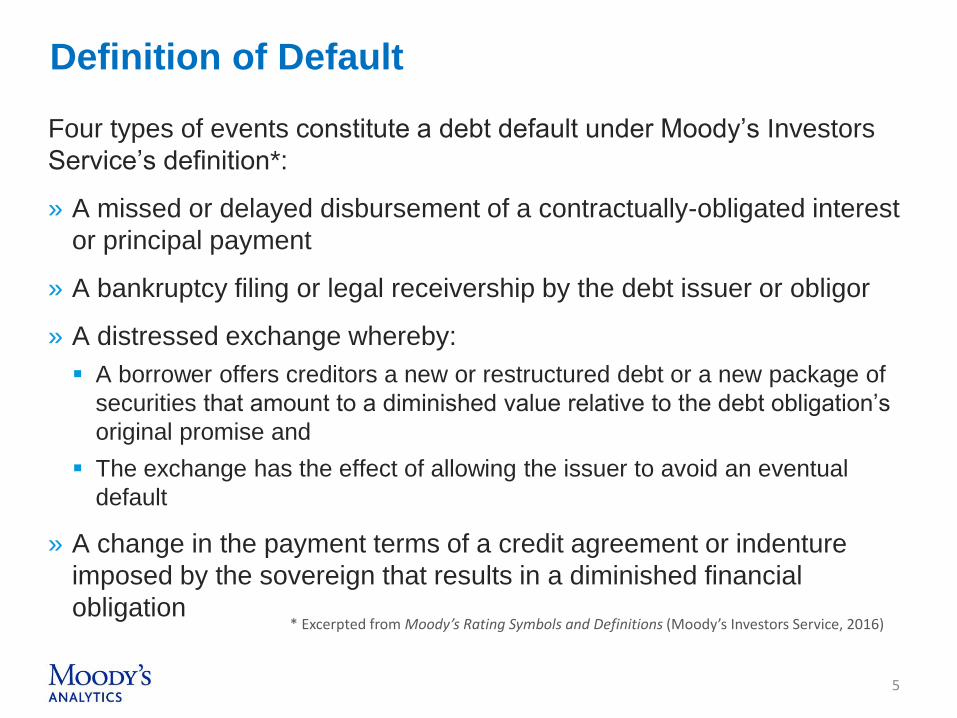

Definition of Default

5

Four types of events constitute a debt default under Moody’s Investors

Service’s definition*:

» A missed or delayed disbursement of a contractually-obligated interest

or principal payment

» A bankruptcy filing or legal receivership by the debt issuer or obligor

» A distressed exchange whereby:

A borrower offers creditors a new or restructured debt or a new package of

securities that amount to a diminished value relative to the debt obligation’s

original promise and

The exchange has the effect of allowing the issuer to avoid an eventual

default

» A change in the payment terms of a credit agreement or indenture

imposed by the sovereign that results in a diminished financial

obligation* Excerpted from Moody’s Rating Symbols and Definitions (Moody’s Investors Service, 2016)

Corporate Debt in China Has Grown Rapidly

Since 2008

6

China’s corporate debt as a percent of GDP has grown sharply since 2008…

… and has surpassed most other major economies globally.

Data sources: Moody’s Investors Service and Bank for International Settlements

Growth in Risky Corporate Debt Has

Historically Led to Surges in Default Rates

7

Data set includes US bond and loan issuers rated by Moody’s Investors Service between 1992 and 2015

An Independent, Quantitative Credit Risk Model

Can Be Useful

8

AA-3.3%

Distribution of China Onshore Ratings by 10 Domestic Ratings Agencies

Distribution of Ratings Implied by Moody’s Analytics’ Probabilities of Default

Non-Investment Grade0.05%

Data sources: Financial Times (Wind Information) and Moody’s Analytics

The Number of Firms with EDFs Has Nearly

Tripled Since 2002 as Listings Have Boomed

9

Data source: Moody’s Analytics

10

China’s

Macroeconomic and

Credit Risk Outlook

Despite Challenges, China’s Economy Has

Been Proven to Be Resilient

11

GDP Growth, % Change Year Ago

Sources: National Bureau of Statistics, Moody’s Analytics

Moody’s Analytics Baseline Outlook is for Solid

Economic Growth

12

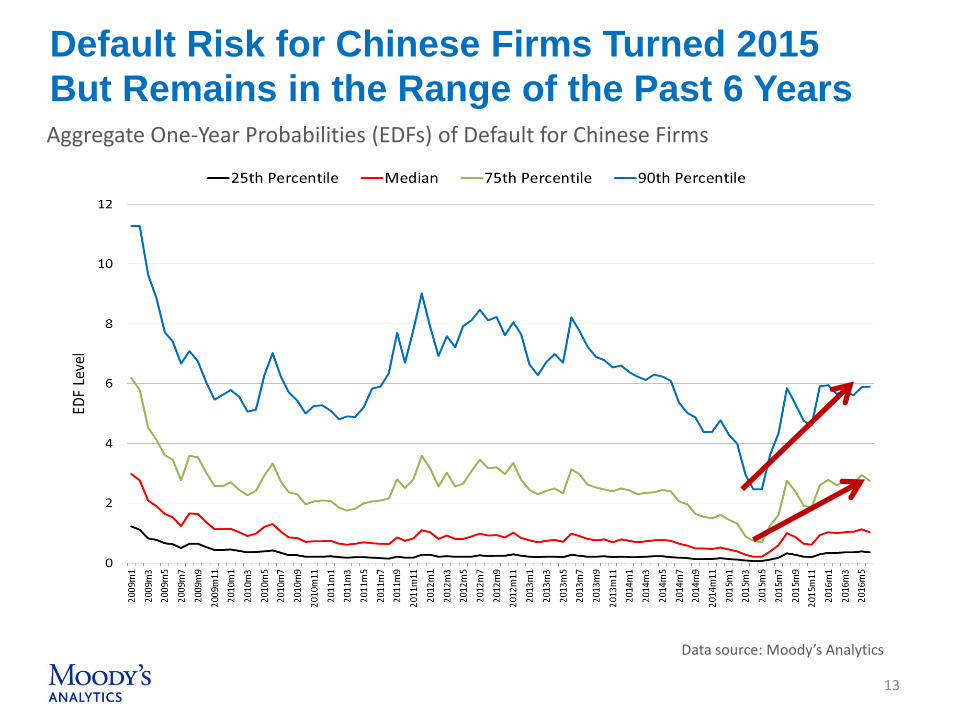

13

Aggregate One-Year Probabilities (EDFs) of Default for Chinese Firms

Default Risk for Chinese Firms Turned 2015

But Remains in the Range of the Past 6 Years

Data source: Moody’s Analytics

Sources: National Bureau of Statistics, Moody’s Analytics

14

China’s Economic Outlook + 4 Alternative

Macroeconomic ScenariosGDP Growth, % Change Year Ago

Default Risk Forecasts Under Alternative

Macroeconomic Scenarios

China – All sectors Consumer Discretionary

Health CareEnergy

Median One-Year Default Probabilities (EDFs) for Selected Industry Sectors

15Data source: Moody’s Analytics

16

Measuring and Managing

the Default Risk of Chinese

Firms

∙ 𝑒−𝑟𝑇Φ(𝑑2)Default Point

Measuring PD: Moody’s Analytics’ Expected

Default Frequency Model

17

Assets =Assets Equity+ Φ(𝑑1)

Expected Default Frequencies (EDFs) are derived from a causal model driven by

fundamental credit risk factors: when the market value of a firm’s assets is insufficient to

cover its liabilities, then the firm defaults.

The market value of a firm’s assets is not directly observable. The EDF model utilizes a

key insight to estimate the market value of assets: a firm’s equity is like a call option on

its asset value, with a strike price equal to liabilities due.

There are 3 main drivers of the EDF model:

1. The default point: derived from a firm’s liability structure

2. Market value of assets: inferred from equity prices

3. Volatility of the market value of assets: inferred from equity volatility

Do Models Informed by Equity Market Prices

“Work” for Chinese Companies?

18

» Model accuracy depends on the availability and quality of input data. A major

advantage of Moody’s Analytics models is the decades of experience developing

models for many different economies world-wide.

» EDF measures have proven to be effective measures of default risk in markets

with distinctive or unique institutional features (e.g. Japan).

» EDF measures do not include the effect of external support. They are useful

stand-alone measures of risk that can and should be compared with measures

that do include external support (e.g. ratings).

» Chinese share prices (as well as other asset prices) are reliable enough that the

PBOC uses them in policy decision making.

» Institutional or market features that attempt to mitigate default may affect the

expected level of PD at a given point in time, but as we will show effective early

warning can still be achieved by observing relative PDs.

One-Year Accuracy Ratios for Chinese

Companies Compare Favorably to Other Markets

19

1-Year Accuracy Ratio # Firms # Defaults

China 62.64% 3,724 77

Japan 77.88% 4,558 93

Australia 70.06% 2,525 171

USA 78.14% 9,243 1,126

W. Europe 68.40% 7,459 509

Data set includes all firms in respective countries between 2007 and 2015.

The Accuracy Ratio is a rank correlation statistic that tell us how well a forward-looking risk scoring system identifies defaulters as well as non-defaulters.

Data source: Moody’s Analytics

Developing Strategies for Early Warning of

Default Risk

20

» One of the primary use cases for EDF measures is for early warning

of potential credit events.

» Monitoring and early warning are problems of classification: which

firms in a portfolio should be considered relatively more risky, and

therefore merit deeper investigation?

» Moody’s Analytics’ research has identified several useful strategies for

developing early warning signals:

1. Absolute EDF level

2. Relative EDF level

3. EDF change

4. Relative EDF change

5. Slope of PD term structure

The EDF Measure for Hidili Surpassed the Early

Warning Level in Mid-2011 and Stayed On Alert

Strategy 1: EDF Level vs. Warning Level

21

Data source: Moody’s Analytics

Hidili’s EDF Measure Began to Underperform

Its Industry 63 Months Prior To Default

Hidili’s EDF measure broke above the median of its industry peer group

The company’s EDF measure crossed and remained above the 90th percentile of its peer group

The EDF measure for Ansteeltracked the trigger level from 2011 until late 2014. The company's current EDF measure of 1.78% is below the China steel and metal products group's trigger of 5.76%.

Ansteel’s EDF measure has deteriorated to the point that it is worse than over 75% of firms in its industry sector.

Data source: Moody’s Analytics

24

Incorporating Macroeconomic

Variables Into Default Risk

Forecasts

25

EDF Stressed EDF

Unconditional PD (no assumption about the economy) Conditional PD (based on an economic forecast)

The 1-year PD forecast as of today Output is a 60 month time series forecast of the 1-year PD

1 to 10 year term structure; longer available 1-year horizon only

Around 40,000 firms daily, globally 20,000 firms daily in North America, Western Europe, Japan, Australia/NZ, China/HK

EDF and Stressed EDF Measures

Data source: Moody’s Analytics

Stressed EDF Models Are Historically Accurate

Australia & New ZealandChina & Hong Kong

Japan Western Europe North America

In-Sample, Perfect Foresight Median Stressed EDF vs. Median Unconditional EDF

26Data source: Moody’s Analytics

CCAR Simulations Using Stressed EDFs Yielded EL

Rates for Corporate Exposures Very Close to the Fed’s

27

Moody’s Analytics Forecasted C&I Portfolio EL Rates vs. FRB Reported C&I EL Rates

Data Sources: Moody’s Analytics and The Federal Reserve Board

IFRS 9 Compliant PD Models Must Satisfy

Several Requirements

28

(IFRS 9减值计提要求)

Economic Scenarios (GDP)

Probability-Weighted EDF

1

4

Stressed EDF Measures

Probability Density Function (GDP)

2

3

IFRS 9 Scenario-Conditioned, Probability-

Weighted PDs

29

Data Source: Moody’s Analytics

Bank of China Stressed EDFs and IFRS 9

Probability-Weighted PDs

30

%

Data Source: Moody’s Analytics

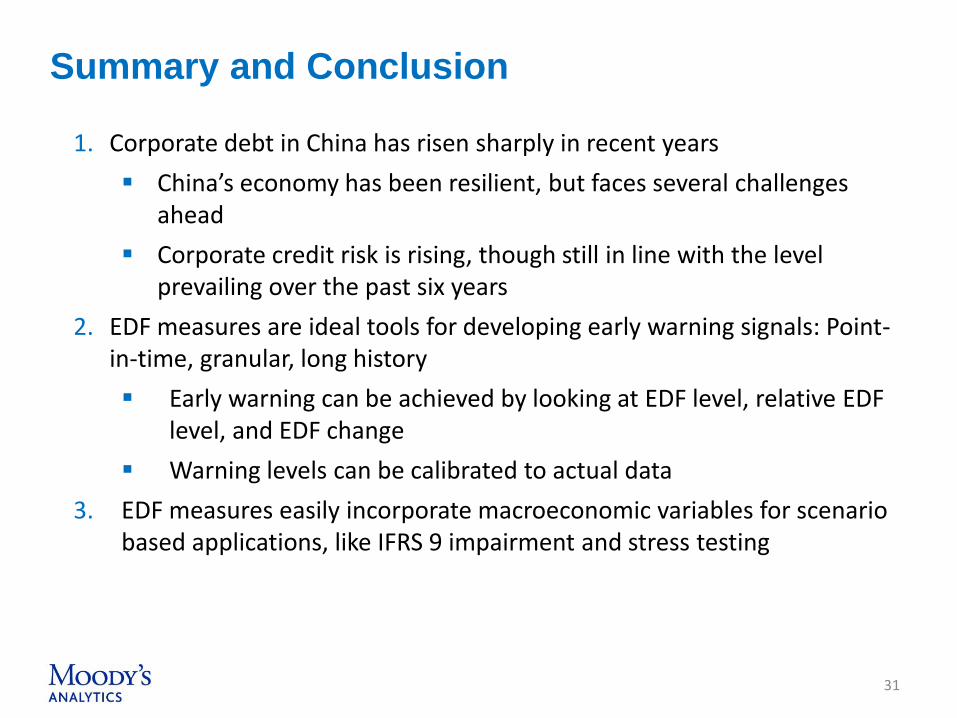

Summary and Conclusion

31

1. Corporate debt in China has risen sharply in recent years

China’s economy has been resilient, but faces several challenges ahead

Corporate credit risk is rising, though still in line with the level prevailing over the past six years

2. EDF measures are ideal tools for developing early warning signals: Point-in-time, granular, long history

Early warning can be achieved by looking at EDF level, relative EDF level, and EDF change

Warning levels can be calibrated to actual data

3. EDF measures easily incorporate macroeconomic variables for scenario based applications, like IFRS 9 impairment and stress testing

Contact Us

32

David Hamilton

Managing DirectorStress Testing and Credit Risk Analytics, Asia Pacific+65 6511 4650 tel+65 9236 1556 [email protected]

Moody’s Analytics6 Shenton Way #14-08OUE Downtown 2Singapore 068809

Glenn Levine

Corporate Stress Testing Model Lead, Capital Markets Research Group+1 212 553-9595 tel+1 646 28077-44 [email protected]

Moody’s Analytics7 World Trade CenterNew York, NY 10007USA

Irina Baron

Quantitative Credit Risk Research Analyst, Capital Markets Research Group+1 212 553-4307 [email protected]

Moody’s Analytics7 World Trade CenterNew York, NY 10007USA

Research Insights

33

From Moody’s Analytics

From Moody’s Investors Service

China Outlook: The Cycle Turns Up, July 2016

Probability-Weighted Outcomes Under IFRS 9: A Macroeconomic Approach, in Moody’s Analytics Risk Perspectives, June 2016

Using EDF Measures to Identify At-Risk Names – A Monitoring & Early Warning Toolkit, April 2016

Spillover from Potential Dislocation in Onshore Bond Market Would Be Limited, August 2016

Authorities Have Tools to Avert Financial Crisis, but Erosion of Credit Quality Likely, June 2016

Estimating US Credit Risk Under the Fed's CCAR 2016 Severely Adverse Scenario, May 2016