28

Analysis, Preparation, and Working to Minimize Impact and Streamline Processes MYRA L WILKERSON, MD Chair of Laboratory Medicine Geisinger Health Danville, PA Preparing for PAMA

Analysis, Preparation, and Working to Minimize Impact and Streamline Processes MYRA L WILKERSON, MD Chair of Laboratory Medicine Geisinger Health Danville, PA

Preparing for PAMA

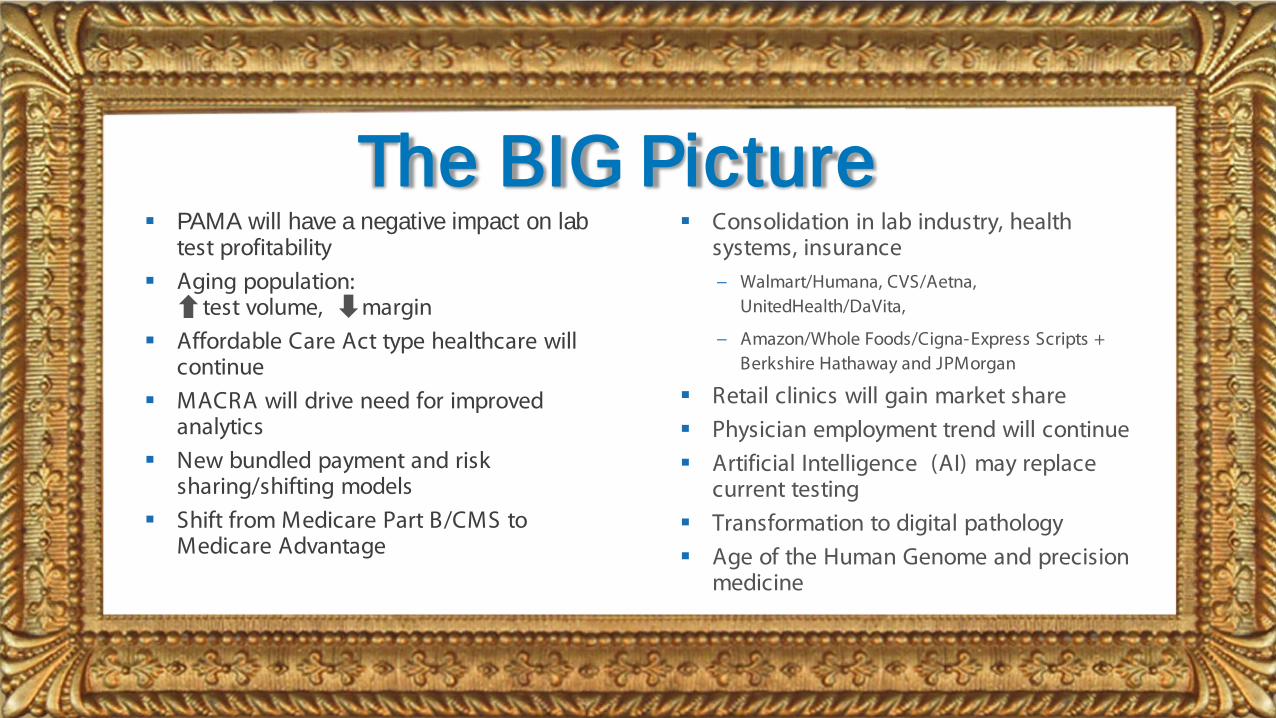

PAMA will have a negative impact on lab test profitability

Aging population: test volume, margin

Affordable Care Act type healthcare will continue

MACRA will drive need for improved analytics

New bundled payment and risk sharing/shifting models

Shift from Medicare Part B/CMS to Medicare Advantage

The BIG Picture

Consolidation in lab industry, health systems, insurance − Walmart/Humana, CVS/Aetna,

UnitedHealth/DaVita,

− Amazon/Whole Foods/Cigna-Express Scripts + Berkshire Hathaway and JPMorgan

Retail clinics will gain market share Physician employment trend will continue Artificial Intelligence (AI) may replace

current testing Transformation to digital pathology Age of the Human Genome and precision

medicine

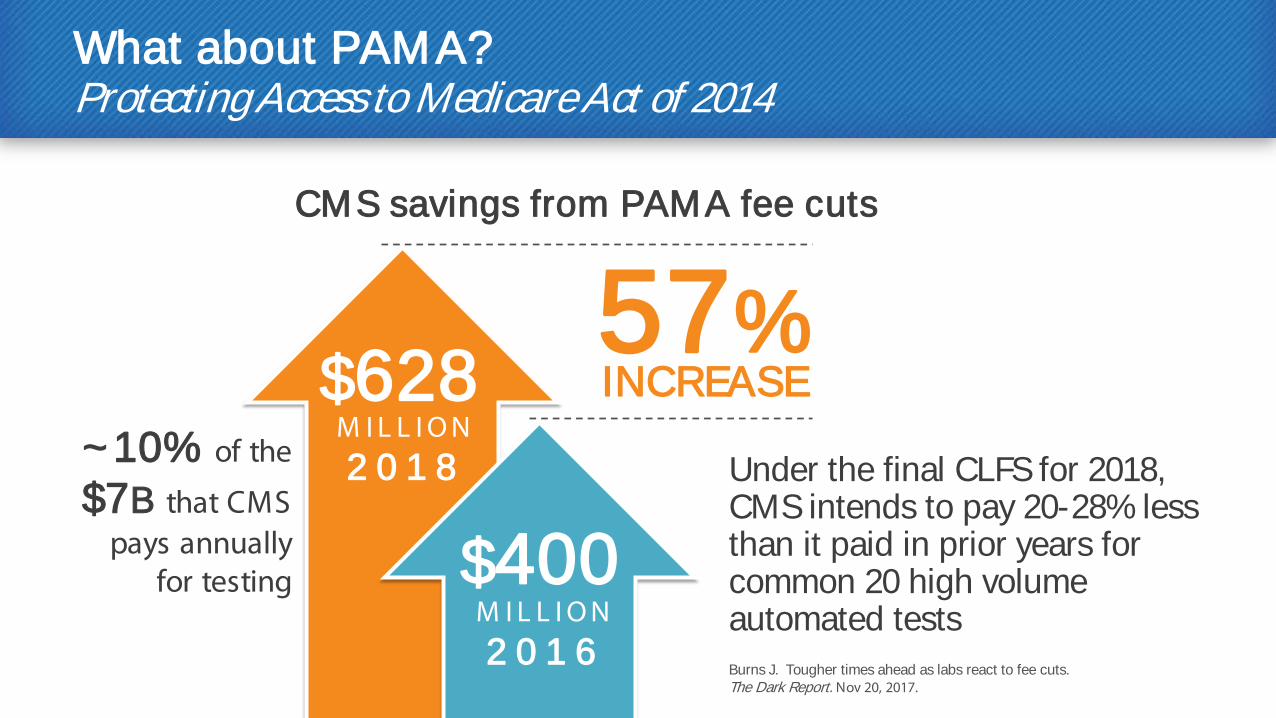

What about PAMA? Protecting Access to Medicare Act of 2014

Under the final CLFS for 2018, CMS intends to pay 20-28% less than it paid in prior years for common 20 high volume automated tests Burns J. Tougher times ahead as labs react to fee cuts. The Dark Report. Nov 20, 2017.

INCREASE 57%

$628 M I L L I O N 2 0 1 8

$400 M I L L I O N 2 0 1 6

CMS savings from PAMA fee cuts

~10% of the

$7B that CMS pays annually

for testing

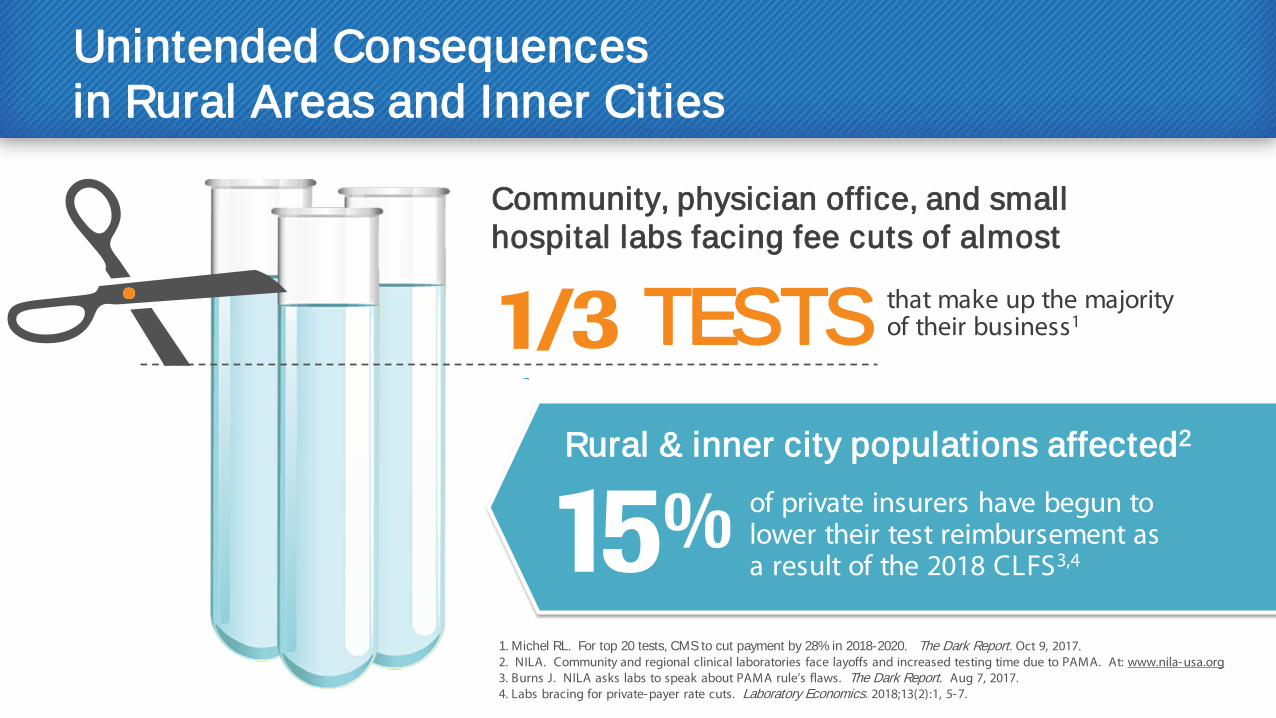

Unintended Consequences in Rural Areas and Inner Cities

1. Michel RL. For top 20 tests, CMS to cut payment by 28% in 2018-2020. The Dark Report. Oct 9, 2017. 2. NILA. Community and regional clinical laboratories face layoffs and increased testing time due to PAMA. At: www.nila-usa.org 3. Burns J. NILA asks labs to speak about PAMA rule’s flaws. The Dark Report. Aug 7, 2017. 4. Labs bracing for private-payer rate cuts. Laboratory Economics. 2018;13(2):1, 5-7.

Rural & inner city populations affected2

Community, physician office, and small hospital labs facing fee cuts of almost

that make up the majority of their business1 TESTS

of private insurers have begun to lower their test reimbursement as a result of the 2018 CLFS3,4

What about large commercial labs?

Pathology Groups & Large Commercial Labs May attempt to charge higher

prices to commercial payers to make up lost revenue

Vulnerable because of current deeply discounted rates, sometimes at or below marginal cost to perform tests

Burns J. Tougher times ahead as labs react to fee cuts. The Dark Report. Nov 20, 2017.

Large Health Insurers may have difficulty getting testing at

current fees unless they open, or buy,

their own labs

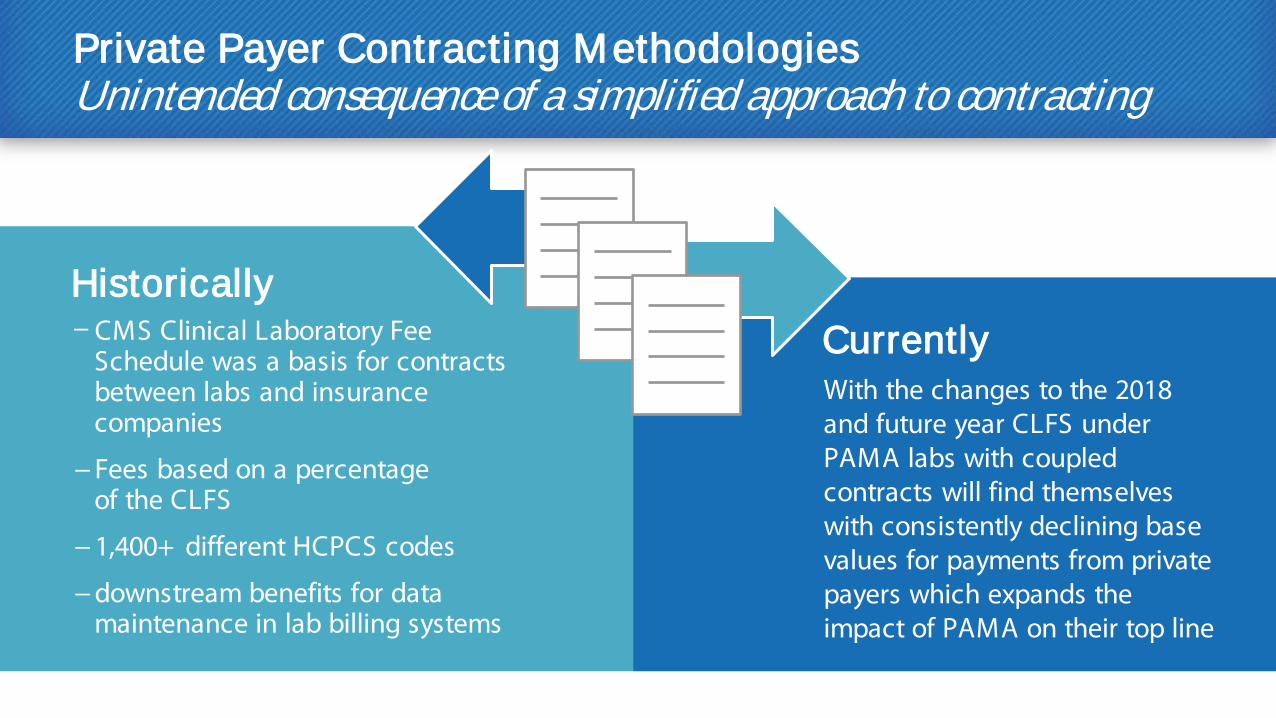

Private Payer Contracting Methodologies Unintended consequence of a simplified approach to contracting

Historically Currently − CMS Clinical Laboratory Fee

Schedule was a basis for contracts between labs and insurance companies

− Fees based on a percentage of the CLFS

− 1,400+ different HCPCS codes

− downstream benefits for data maintenance in lab billing systems

With the changes to the 2018 and future year CLFS under PAMA labs with coupled contracts will find themselves with consistently declining base values for payments from private payers which expands the impact of PAMA on their top line

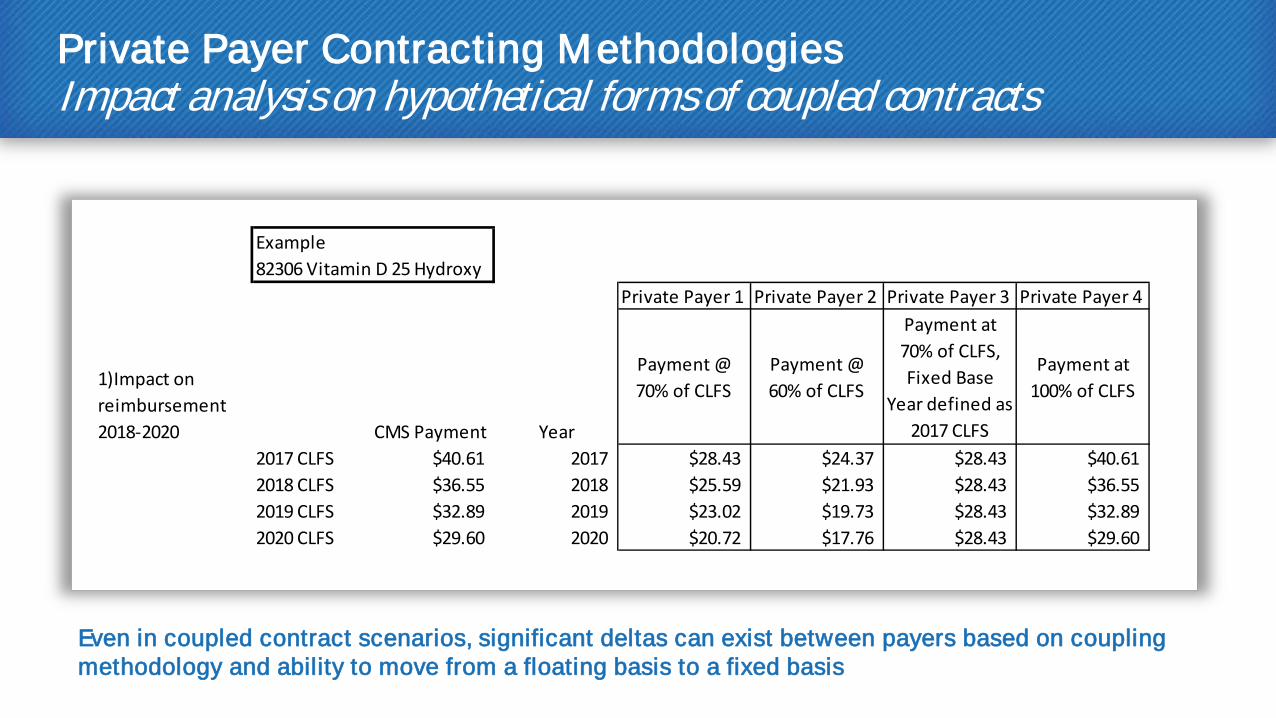

Private Payer Contracting Methodologies Impact analysis on hypothetical forms of coupled contracts

Even in coupled contract scenarios, significant deltas can exist between payers based on coupling methodology and ability to move from a floating basis to a fixed basis

Example82306 Vitamin D 25 Hydroxy

Private Payer 1 Private Payer 2 Private Payer 3 Private Payer 4

1)Impact on reimbursement 2018-2020 CMS Payment Year

Payment @ 70% of CLFS

Payment @ 60% of CLFS

Payment at 70% of CLFS, Fixed Base

Year defined as 2017 CLFS

Payment at 100% of CLFS

2017 CLFS $40.61 2017 $28.43 $24.37 $28.43 $40.612018 CLFS $36.55 2018 $25.59 $21.93 $28.43 $36.552019 CLFS $32.89 2019 $23.02 $19.73 $28.43 $32.892020 CLFS $29.60 2020 $20.72 $17.76 $28.43 $29.60

Private Payer Contracting Methodologies

2) Potential Impact on reimbursement 2021-2023 Private Payer 1 Private Payer 2 Private Payer 3 Private Payer 4

2020 CLFS $29.60 2020 $20.72 $17.76 $28.43 $29.60

CMS will run a second PAMA data collection to determine the CLFS rates for 2021-2023

The more labs participating in the data collection which have remained in coupled contracts with payers as illustrated by Payer 1 & Payer 2, the greater the potential for disparity between CMS rates and "market rates" as determined by the CMS data collection

As a result, the CLFS for 2021-2023 could reflect additional reductions in reimbursement rates

Why action now can drive future sustainability: avoiding the “ Death Spiral”

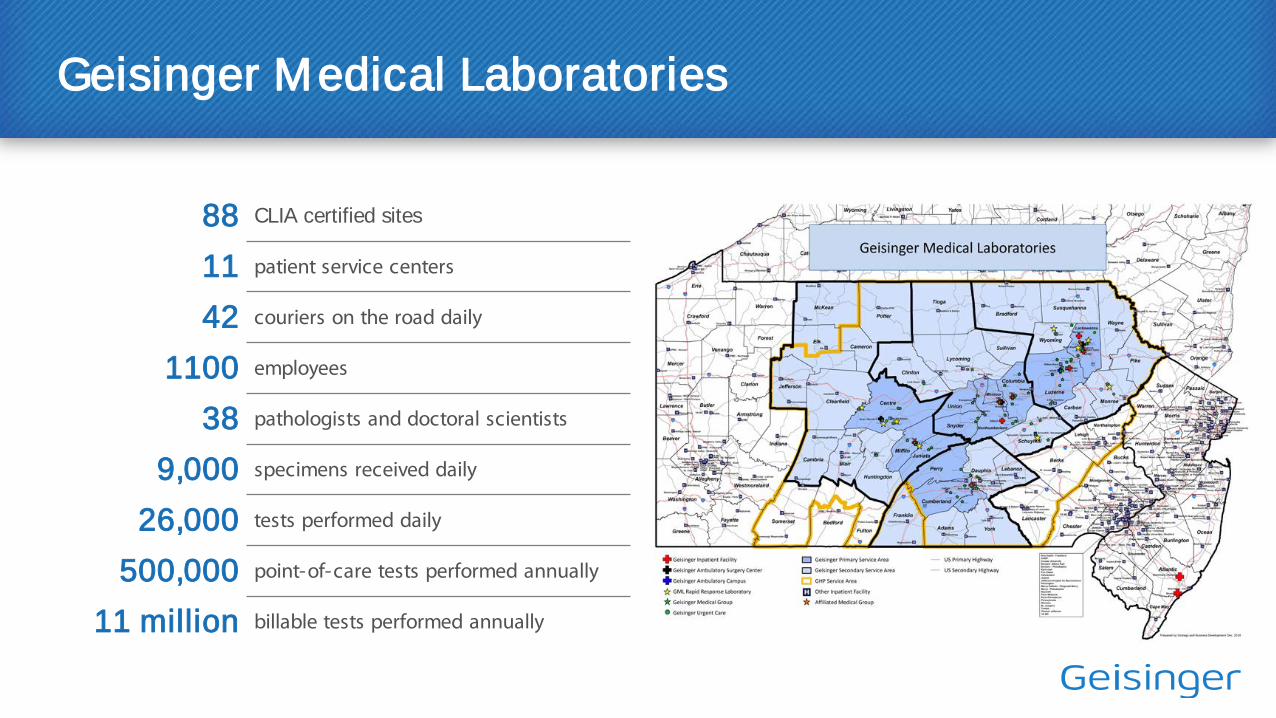

Geisinger Medical Laboratories

88 CLIA certified sites

11 patient service centers

42 couriers on the road daily

1100 employees

38 pathologists and doctoral scientists

9,000 specimens received daily

26,000 tests performed daily

500,000 point-of-care tests performed annually

11 million billable tests performed annually

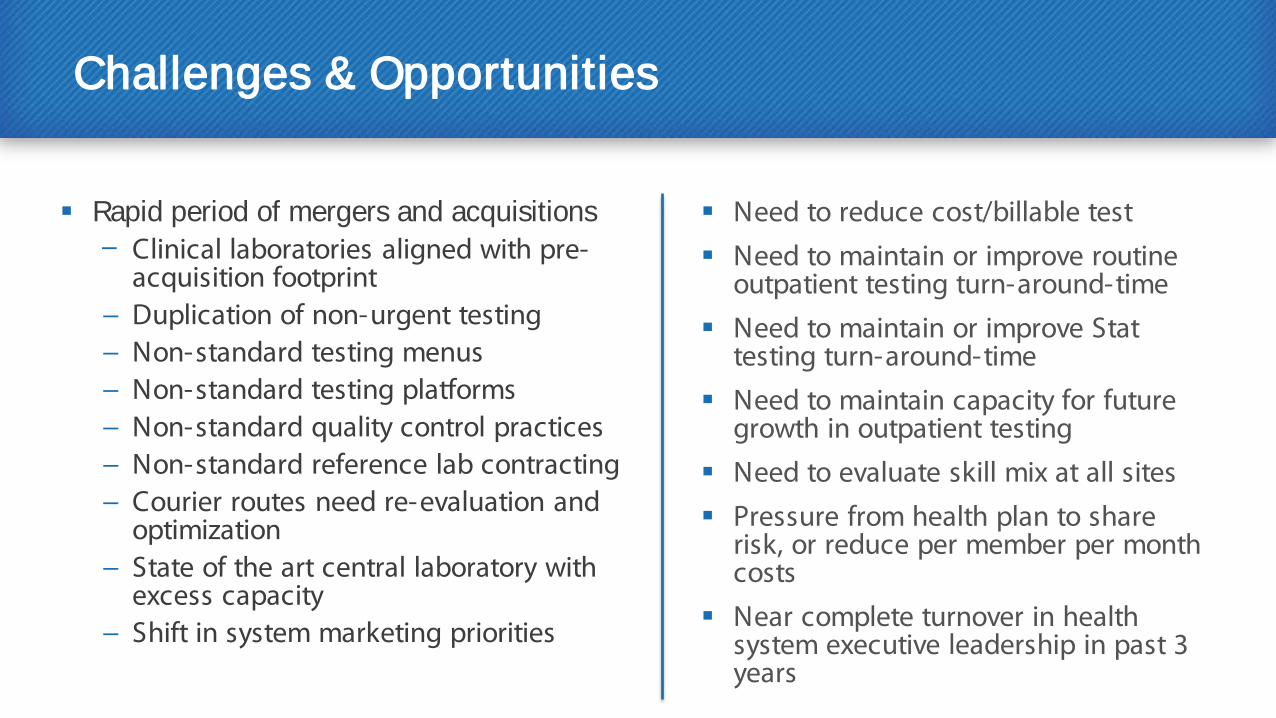

Challenges & Opportunities

Rapid period of mergers and acquisitions − Clinical laboratories aligned with pre-

acquisition footprint − Duplication of non-urgent testing − Non-standard testing menus − Non-standard testing platforms − Non-standard quality control practices − Non-standard reference lab contracting − Courier routes need re-evaluation and

optimization − State of the art central laboratory with

excess capacity − Shift in system marketing priorities

Need to reduce cost/billable test

Need to maintain or improve routine outpatient testing turn-around-time

Need to maintain or improve Stat testing turn-around-time

Need to maintain capacity for future growth in outpatient testing

Need to evaluate skill mix at all sites

Pressure from health plan to share risk, or reduce per member per month costs

Near complete turnover in health system executive leadership in past 3 years

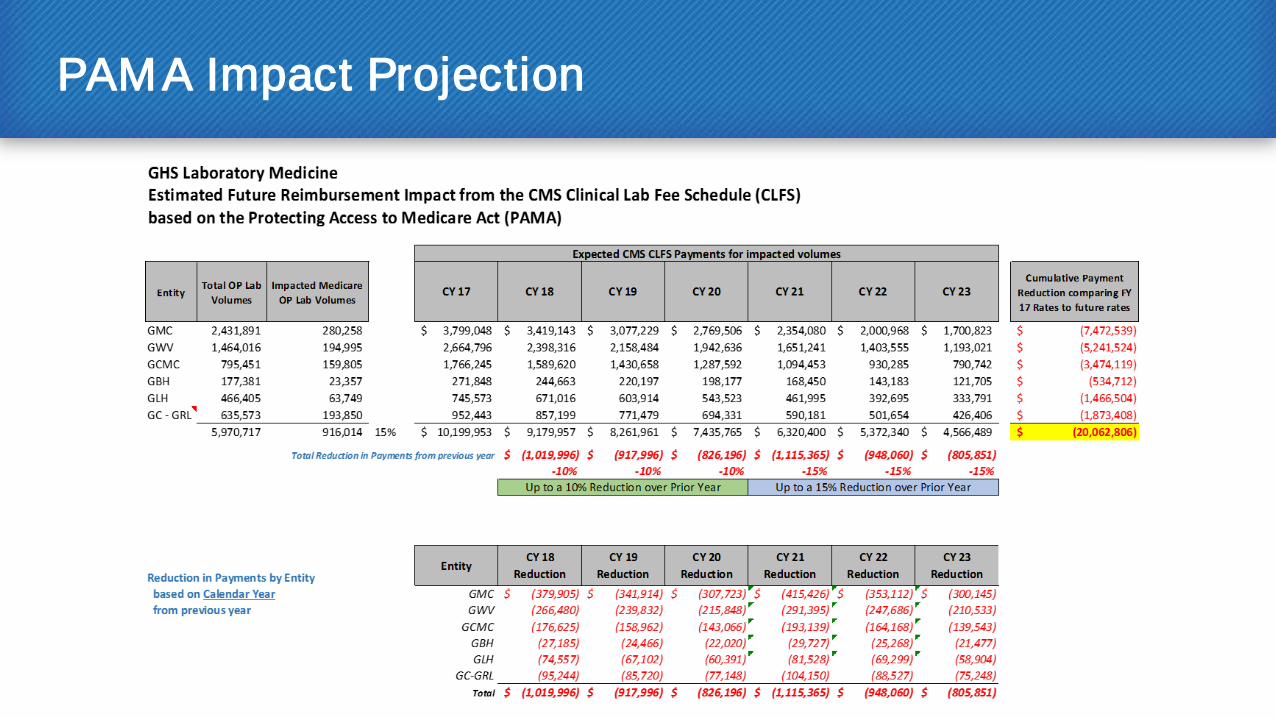

PAMA Impact Projection

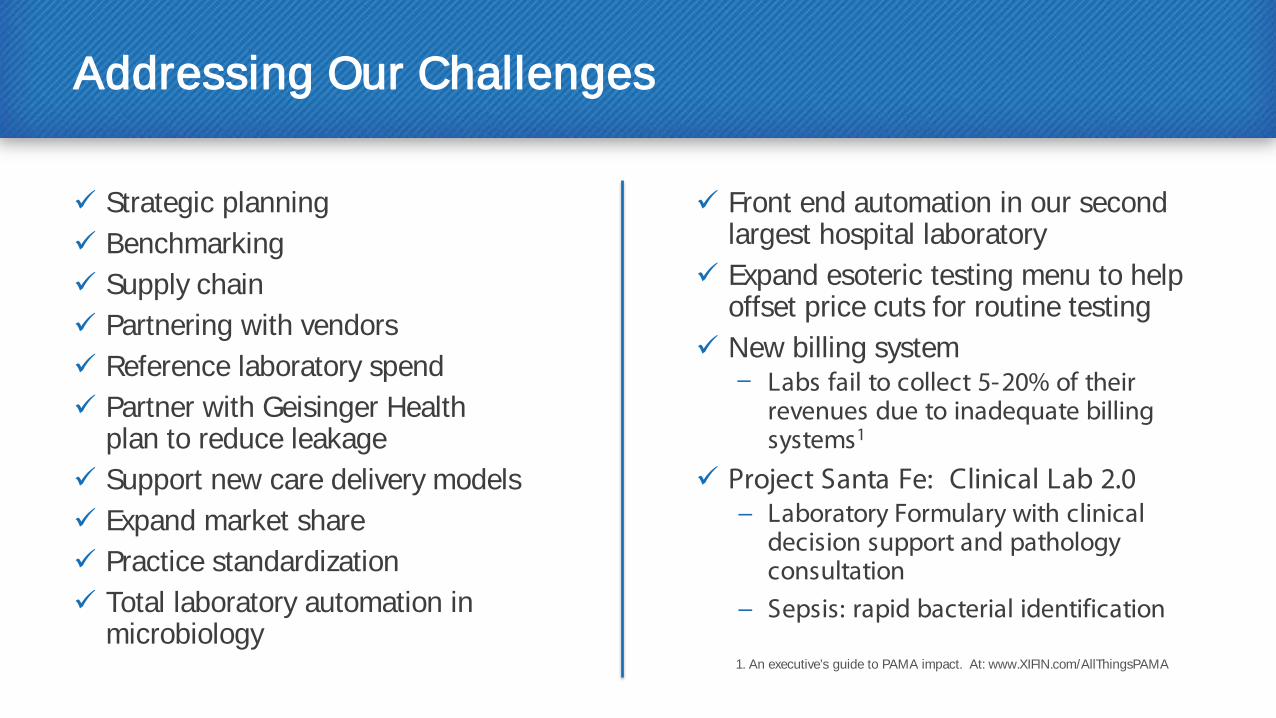

Addressing Our Challenges

Strategic planning Benchmarking Supply chain Partnering with vendors Reference laboratory spend Partner with Geisinger Health

plan to reduce leakage Support new care delivery models Expand market share Practice standardization Total laboratory automation in

microbiology 1. An executive’s guide to PAMA impact. At: www.XIFIN.com/AllThingsPAMA

Front end automation in our second largest hospital laboratory

Expand esoteric testing menu to help offset price cuts for routine testing

New billing system − Labs fail to collect 5-20% of their

revenues due to inadequate billing systems1

Project Santa Fe: Clinical Lab 2.0 − Laboratory Formulary with clinical

decision support and pathology consultation

− Sepsis: rapid bacterial identification

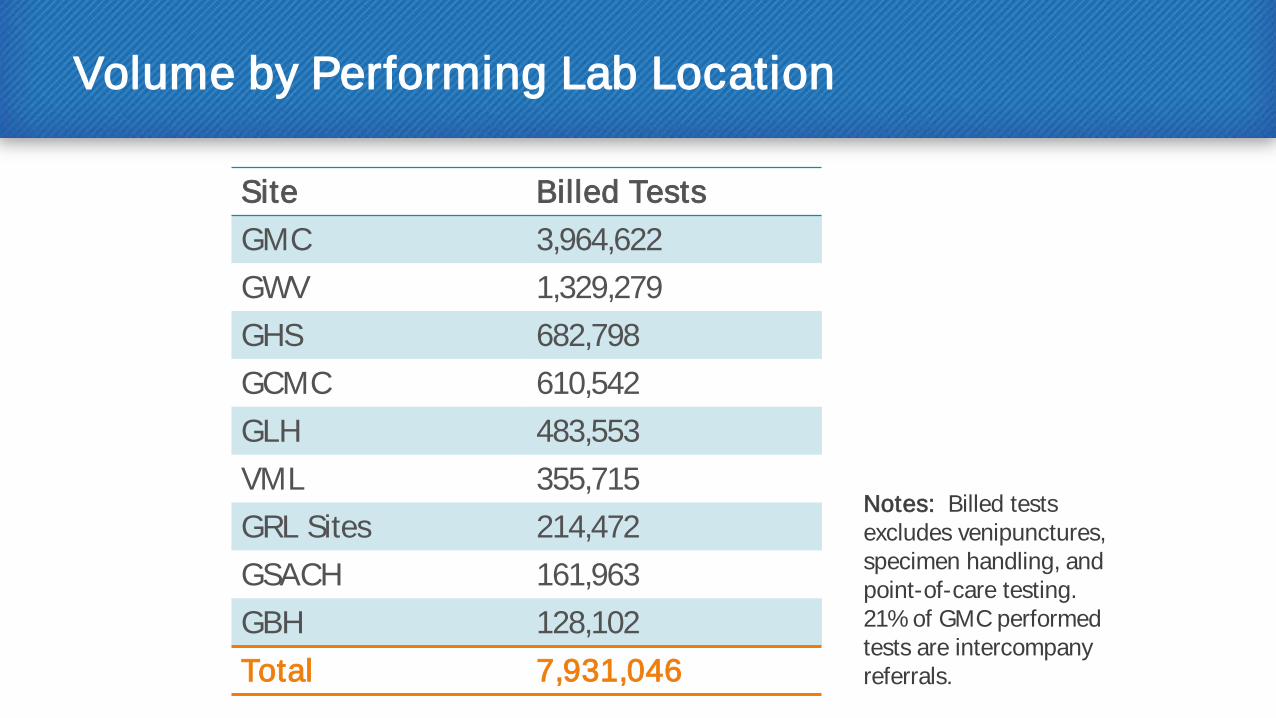

Volume by Performing Lab Location

Site Billed Tests GMC 3,964,622 GWV 1,329,279 GHS 682,798 GCMC 610,542 GLH 483,553 VML 355,715 GRL Sites 214,472 GSACH 161,963 GBH 128,102 Total 7,931,046

Notes: Billed tests excludes venipunctures, specimen handling, and point-of-care testing. 21% of GMC performed tests are intercompany referrals.

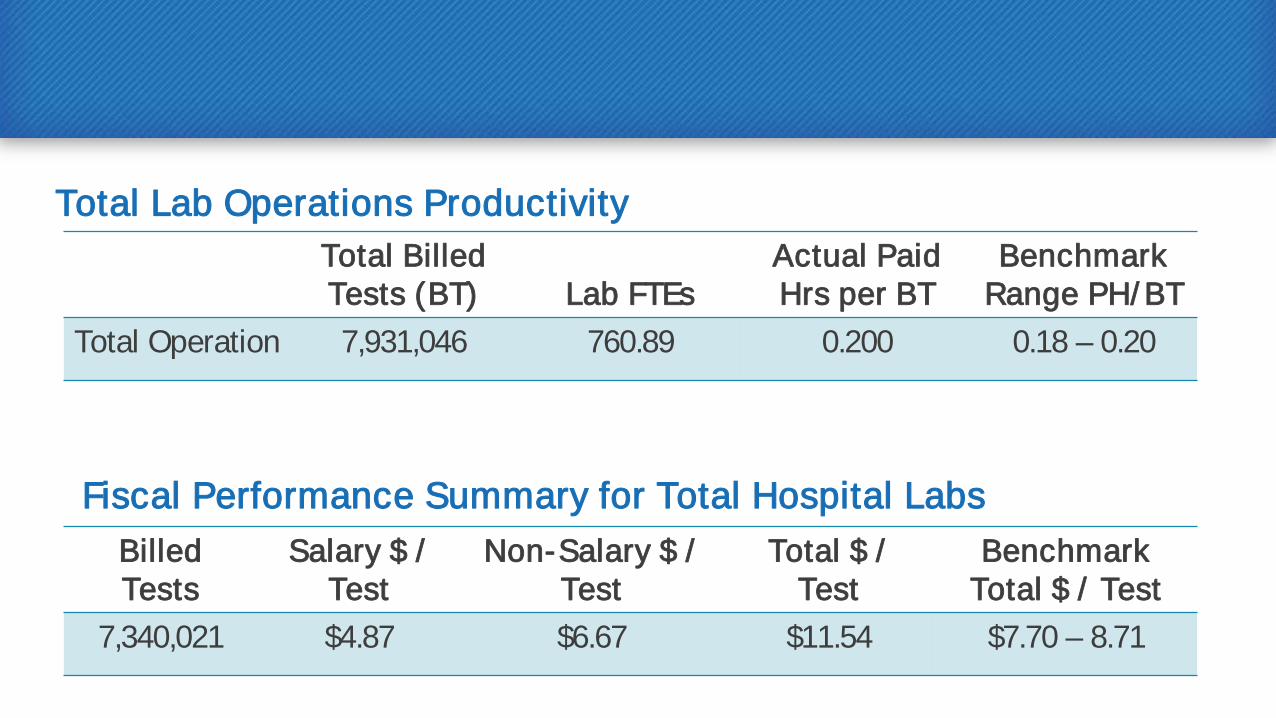

Total Lab Operations Productivity Total Billed Tests (BT) Lab FTEs

Actual Paid Hrs per BT

Benchmark Range PH/ BT

Total Operation 7,931,046 760.89 0.200 0.18 – 0.20

Fiscal Performance Summary for Total Hospital Labs Billed Tests

Salary $ / Test

Non-Salary $ / Test

Total $ / Test

Benchmark Total $ / Test

7,340,021 $4.87 $6.67 $11.54 $7.70 – 8.71

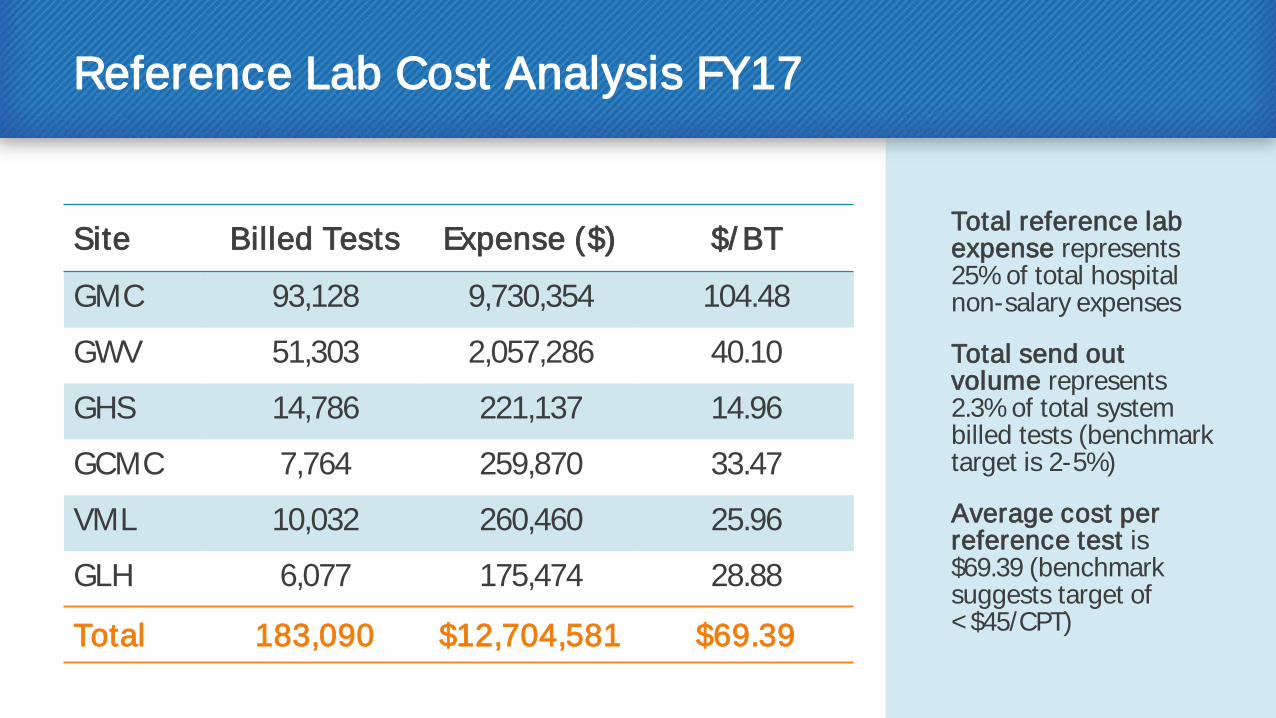

Reference Lab Cost Analysis FY17

Site Billed Tests Expense ($) $/ BT

GMC 93,128 9,730,354 104.48

GWV 51,303 2,057,286 40.10

GHS 14,786 221,137 14.96

GCMC 7,764 259,870 33.47

VML 10,032 260,460 25.96

GLH 6,077 175,474 28.88

Total 183,090 $12,704,581 $69.39

Total reference lab expense represents 25% of total hospital non-salary expenses

Total send out volume represents 2.3% of total system billed tests (benchmark target is 2-5%)

Average cost per reference test is $69.39 (benchmark suggests target of < $45/CPT)

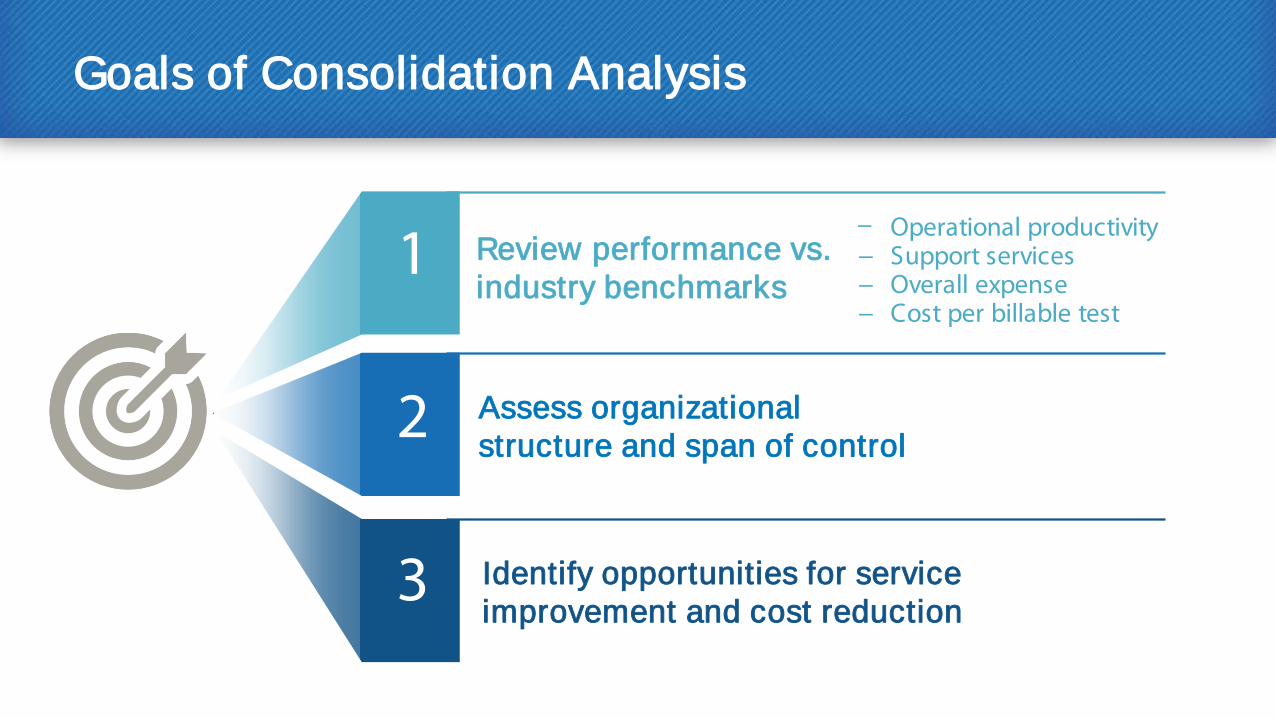

Goals of Consolidation Analysis

− Operational productivity − Support services − Overall expense − Cost per billable test

1

2

3 Identify opportunities for service improvement and cost reduction

Assess organizational structure and span of control

Review performance vs. industry benchmarks

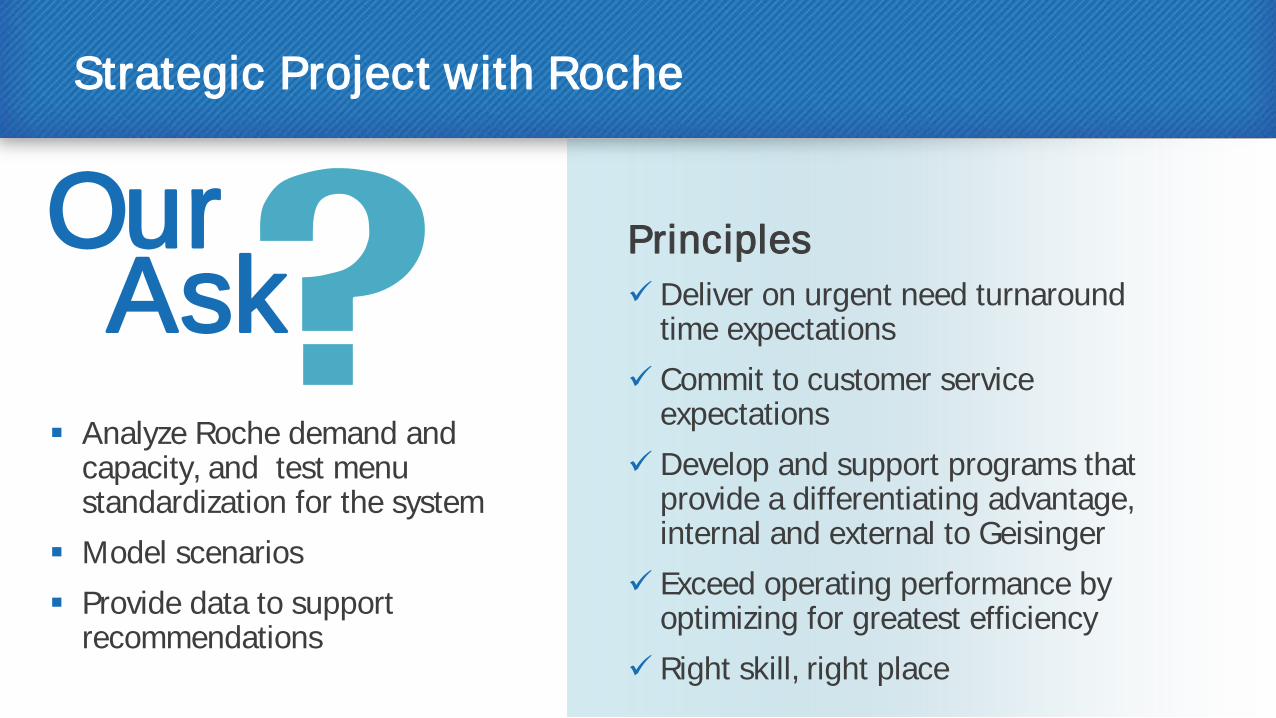

Strategic Project with Roche

Analyze Roche demand and capacity, and test menu standardization for the system

Model scenarios Provide data to support

recommendations

Principles Deliver on urgent need turnaround

time expectations Commit to customer service

expectations Develop and support programs that

provide a differentiating advantage, internal and external to Geisinger

Exceed operating performance by optimizing for greatest efficiency

Right skill, right place

Our Ask

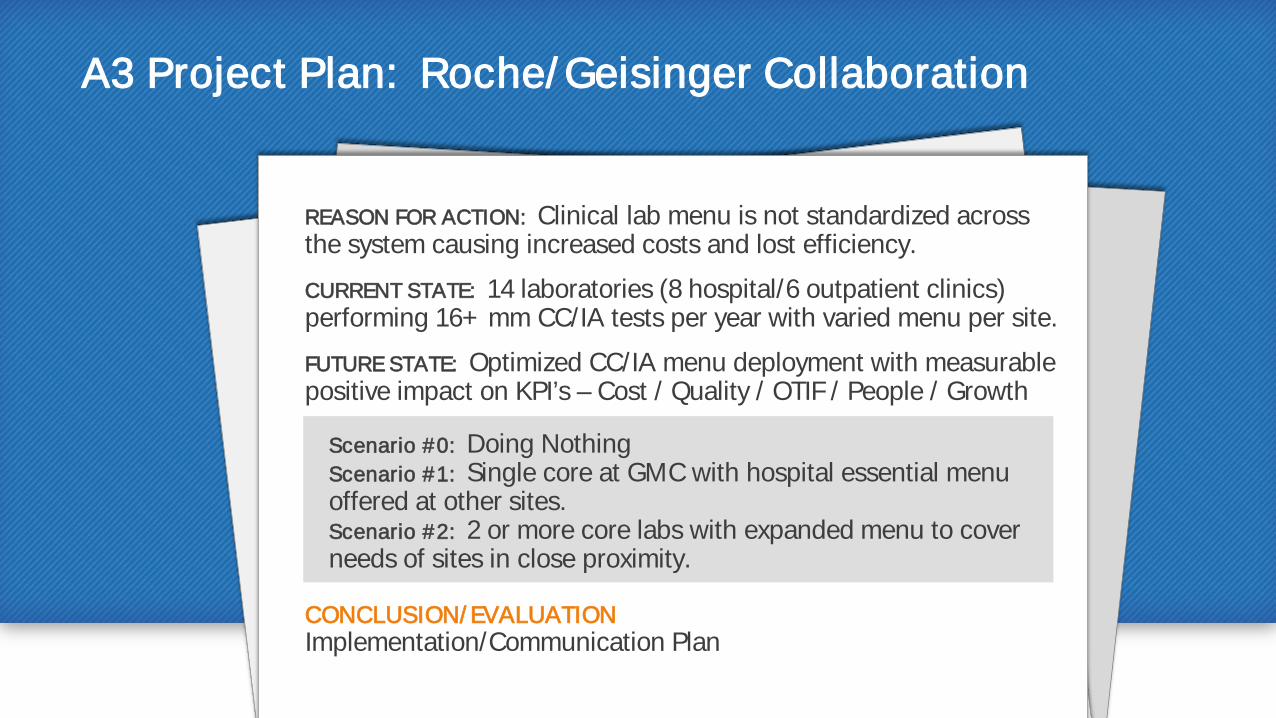

A3 Project Plan: Roche/ Geisinger Collaboration

REASON FOR ACTION: Clinical lab menu is not standardized across the system causing increased costs and lost efficiency.

CURRENT STATE: 14 laboratories (8 hospital/6 outpatient clinics) performing 16+ mm CC/IA tests per year with varied menu per site.

FUTURE STATE: Optimized CC/IA menu deployment with measurable positive impact on KPI’s – Cost / Quality / OTIF / People / Growth

Scenario #0: Doing Nothing Scenario #1: Single core at GMC with hospital essential menu offered at other sites. Scenario #2: 2 or more core labs with expanded menu to cover needs of sites in close proximity.

CONCLUSION/ EVALUATION Implementation/Communication Plan

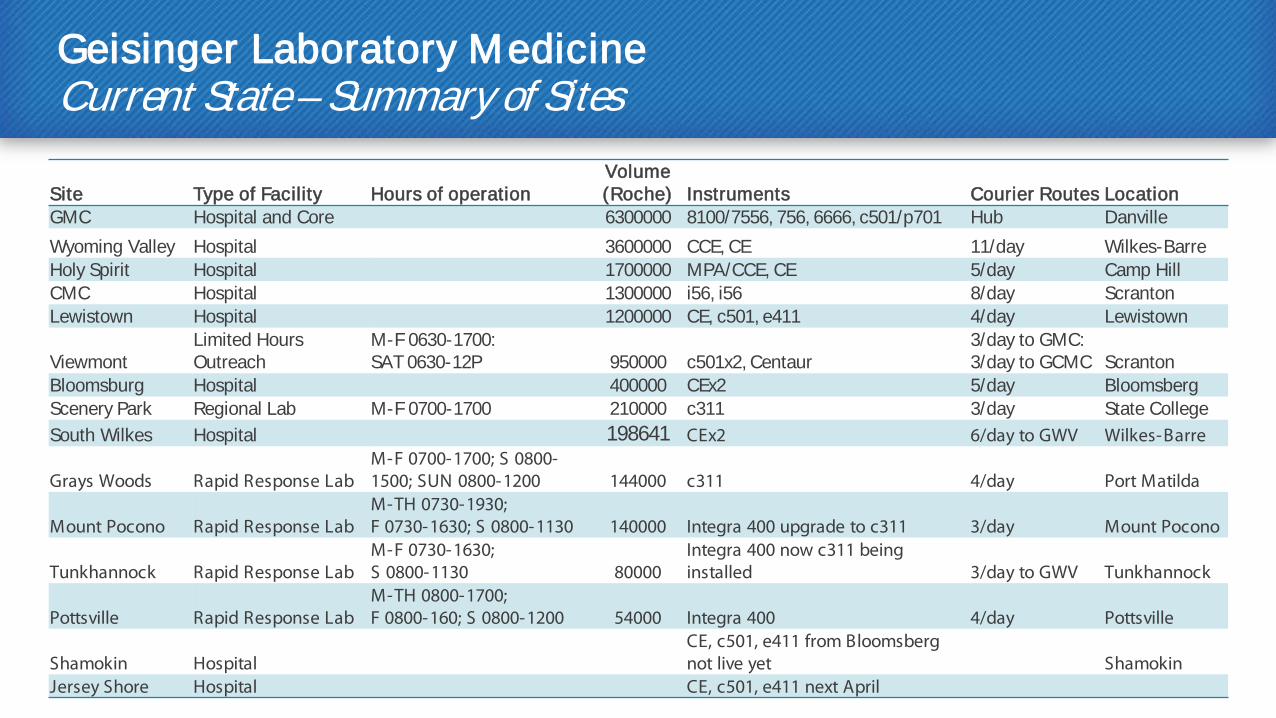

Geisinger Laboratory Medicine Current State – Summary of Sites

Site Type of Facility Hours of operation Volume (Roche) Instruments Courier Routes Location

GMC Hospital and Core 6300000 8100/7556, 756, 6666, c501/p701 Hub Danville Wyoming Valley Hospital 3600000 CCE, CE 11/day Wilkes-Barre Holy Spirit Hospital 1700000 MPA/CCE, CE 5/day Camp Hill CMC Hospital 1300000 i56, i56 8/day Scranton Lewistown Hospital 1200000 CE, c501, e411 4/day Lewistown

Viewmont Limited Hours Outreach

M-F 0630-1700: SAT 0630-12P 950000 c501x2, Centaur

3/day to GMC: 3/day to GCMC Scranton

Bloomsburg Hospital 400000 CEx2 5/day Bloomsberg Scenery Park Regional Lab M-F 0700-1700 210000 c311 3/day State College South Wilkes Hospital 198641 CEx2 6/day to GWV Wilkes-Barre

Grays Woods Rapid Response Lab M-F 0700-1700; S 0800-1500; SUN 0800-1200 144000 c311 4/day Port Matilda

Mount Pocono Rapid Response Lab M-TH 0730-1930; F 0730-1630; S 0800-1130 140000 Integra 400 upgrade to c311 3/day Mount Pocono

Tunkhannock Rapid Response Lab M-F 0730-1630; S 0800-1130 80000

Integra 400 now c311 being installed 3/day to GWV Tunkhannock

Pottsville Rapid Response Lab M-TH 0800-1700; F 0800-160; S 0800-1200 54000 Integra 400 4/day Pottsville

Shamokin Hospital CE, c501, e411 from Bloomsberg not live yet Shamokin

Jersey Shore Hospital CE, c501, e411 next April

0

500

1000

1500

2000

2500

3000

3500

4000

Num

ber o

f Tes

tsDemand vs Capacity Integrated 8000 Lines

GMC Core Lab Clinical Chemistry/ Immunoassay (CC/ IA) Capacity

100% Capacity – 3,710 tests/ hour

Current Peak Demand – 1,600 tests/ hour

Demand vs Capacity Integrated 8000 Lines N

umbe

r of T

ests

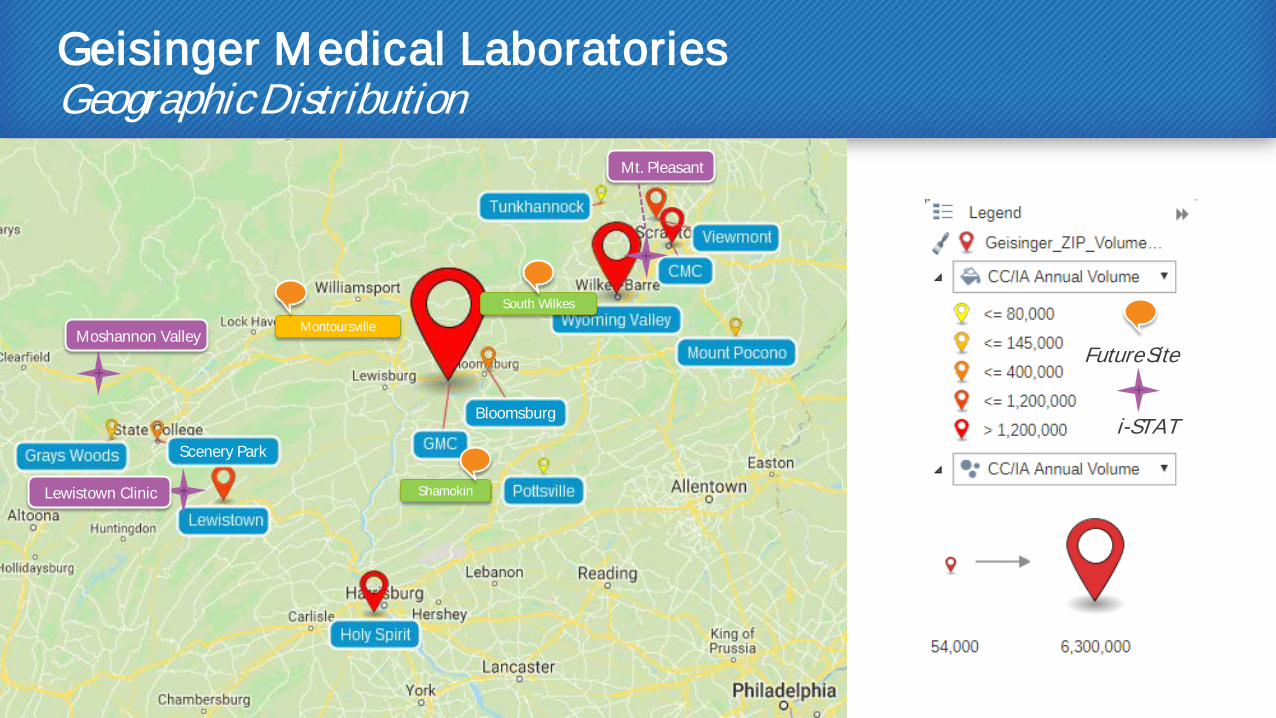

Geisinger Medical Laboratories Geographic Distribution

Future Site

i-STAT

Shamokin

South Wilkes

Montoursville Moshannon Valley

Scenery Park

Bloomsburg

Lewistown Clinic

Mt. Pleasant

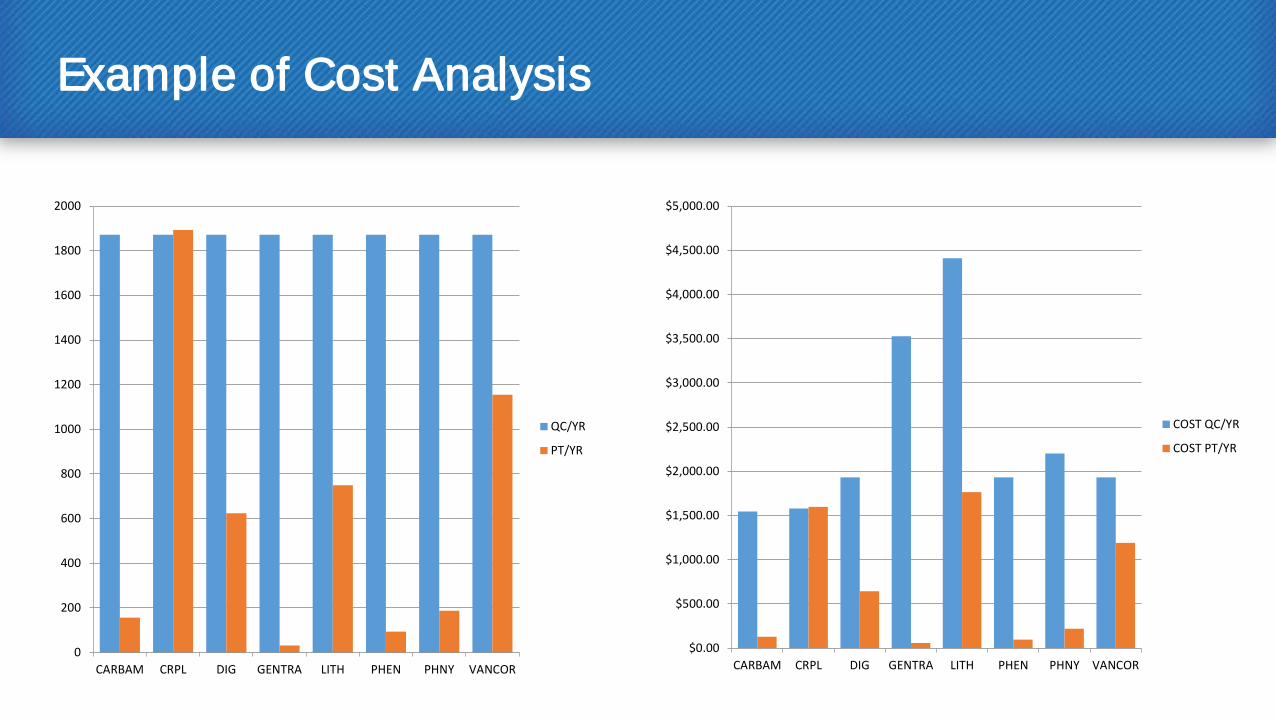

Expense Reduction Opportunities Centralizing Non-essential Testing

What do we spend on Quality Control expense for a particular test that is currently run at 10 sites? Can that test be run at fewer sites?

Are the functions of our current equipment appropriate for the needs of the site? Replace it with something more appropriate?

Looked at the potential savings from

the viewpoint of our system as a whole

Reviewed processes for efficiencies to save on expenses

Example of Cost Analysis

0

200

400

600

800

1000

1200

1400

1600

1800

2000

CARBAM CRPL DIG GENTRA LITH PHEN PHNY VANCOR

QC/YR

PT/YR

$0.00

$500.00

$1,000.00

$1,500.00

$2,000.00

$2,500.00

$3,000.00

$3,500.00

$4,000.00

$4,500.00

$5,000.00

CARBAM CRPL DIG GENTRA LITH PHEN PHNY VANCOR

COST QC/YR

COST PT/YR

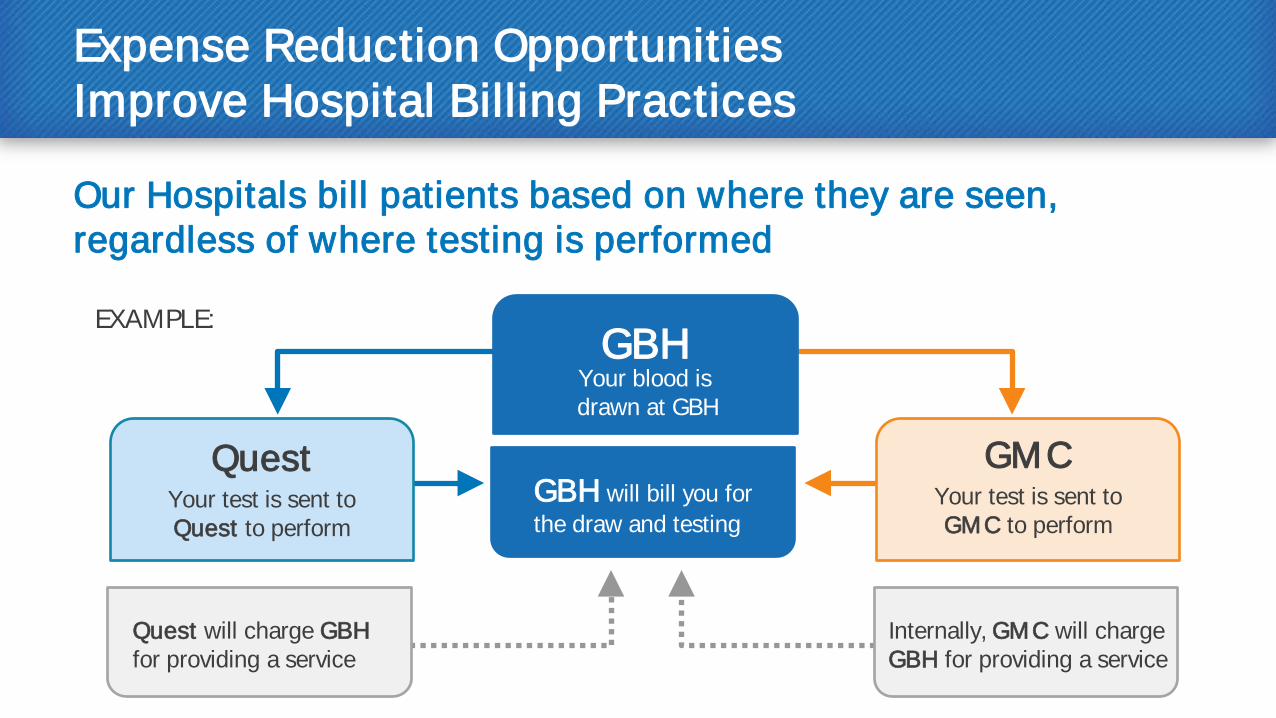

Expense Reduction Opportunities Improve Hospital Billing Practices

Our Hospitals bill patients based on where they are seen, regardless of where testing is performed EXAMPLE:

Your test is sent to Quest to perform

Your test is sent to GMC to perform

GBH will bill you for the draw and testing

Quest will charge GBH for providing a service

Internally, GMC will charge GBH for providing a service

Quest GMC

GBH Your blood is drawn at GBH

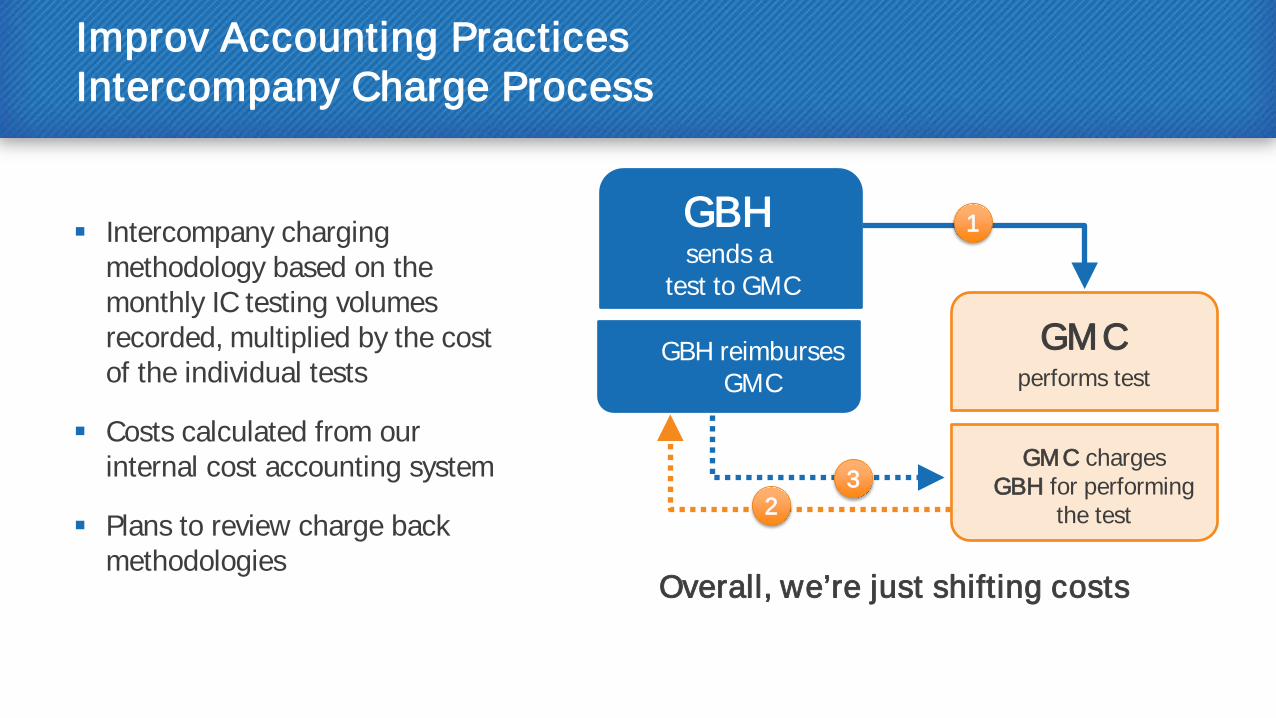

Improv Accounting Practices Intercompany Charge Process

Intercompany charging methodology based on the monthly IC testing volumes recorded, multiplied by the cost of the individual tests

Costs calculated from our internal cost accounting system

Plans to review charge back methodologies

Overall, we’re just shifting costs

performs test GBH reimburses

GMC

GMC charges GBH for performing

the test

GMC

GBH sends a

test to GMC

3

1

2

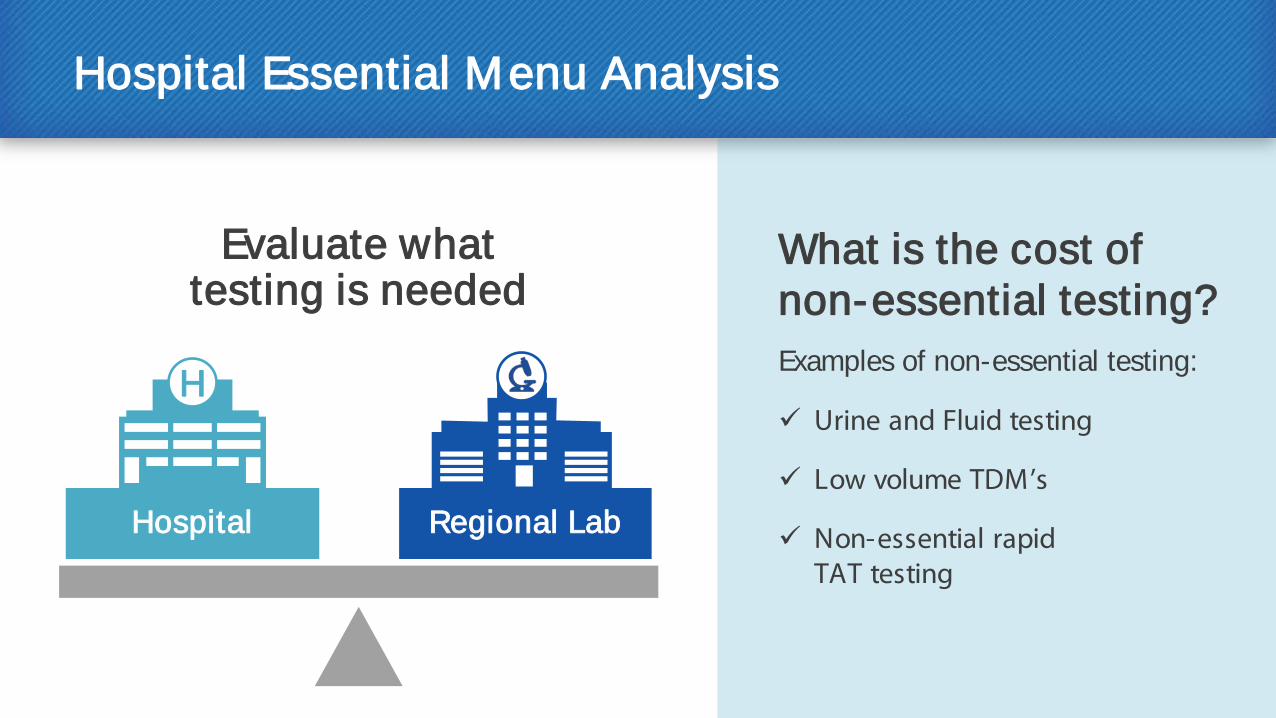

Hospital Essential Menu Analysis

Evaluate what testing is needed

Examples of non-essential testing:

Urine and Fluid testing

Low volume TDM’s

Non-essential rapid TAT testing

Regional Lab Hospital

What is the cost of non-essential testing?

H

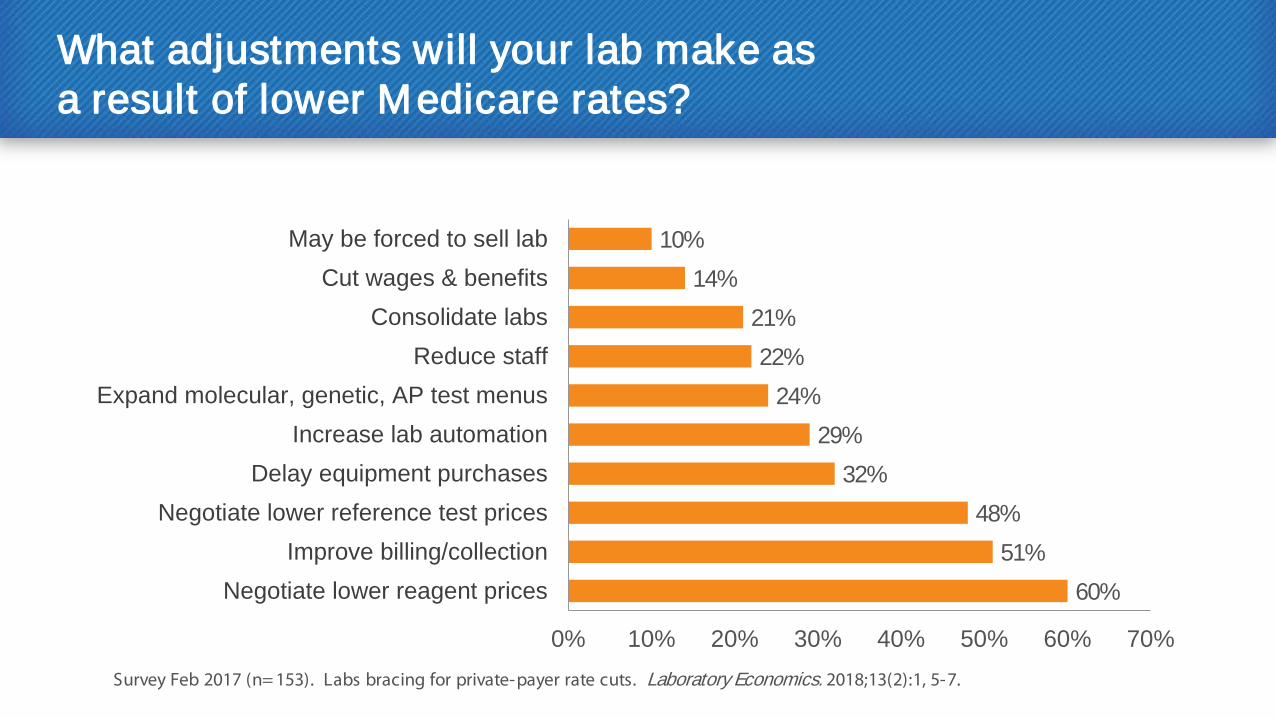

What adjustments will your lab make as a result of lower Medicare rates?

60% 51%

48% 32%

29% 24%

22% 21%

14% 10%

0% 10% 20% 30% 40% 50% 60% 70%

Negotiate lower reagent pricesImprove billing/collection

Negotiate lower reference test pricesDelay equipment purchases

Increase lab automationExpand molecular, genetic, AP test menus

Reduce staffConsolidate labs

Cut wages & benefitsMay be forced to sell lab

Survey Feb 2017 (n= 153). Labs bracing for private-payer rate cuts. Laboratory Economics. 2018;13(2):1, 5-7.

Acknowledgements for Providing Data

Roche Diagnostics Tracy Steffen

Jason Jackson

Ray O’Donnell

Applied Management Systems Paul Camara Sharon Brommer