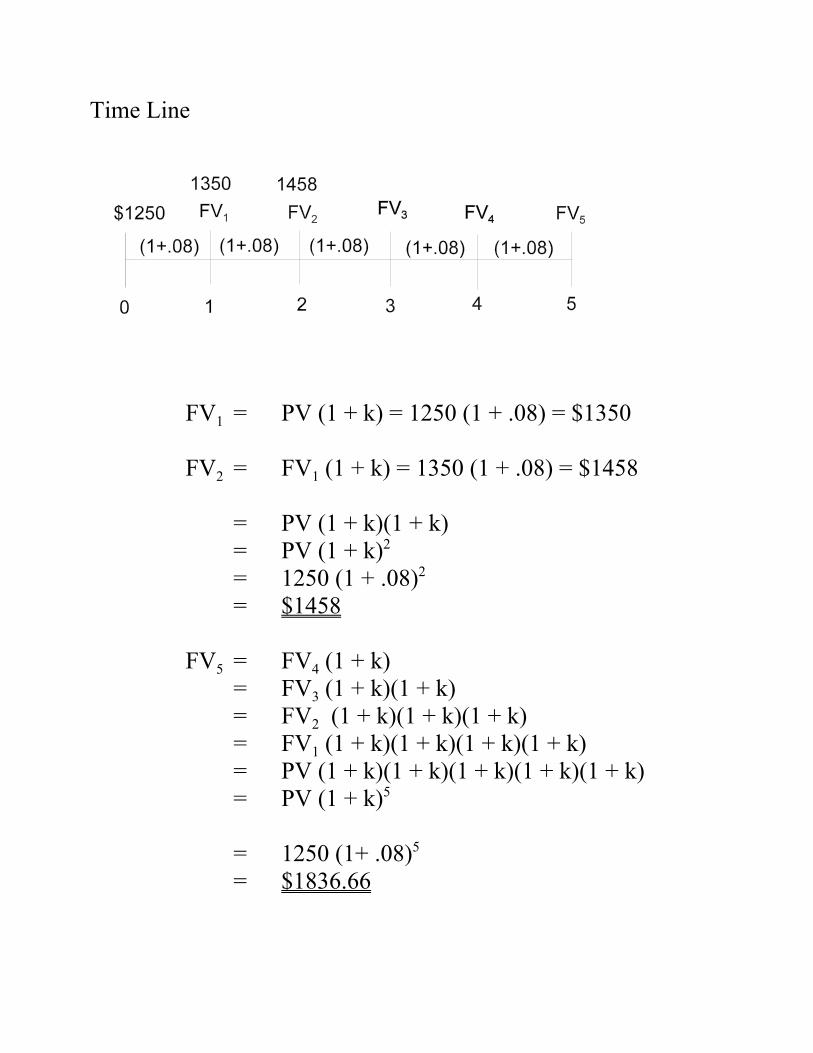

0 1 2 3 $100 $100 $100 PRESENT VALUE ANALYSIS Time value of money — “equal” dollar amounts have different values at different points in time. Present value analysis — tool to convert CFs at different points in time to comparable values at a given point in time. Time Line CF t CF t+1 CF t+2 CF t+3 CF t+4 CF t+5 CF t+6 (cash flows) (time periods) t t+1 t+2 t+3 t+4 t+5 t+6

Transcript

0 1 2 3

$100 $100 $100

PRESENT VALUE ANALYSIS

Time value of money — “equal” dol la r amounts havedifferent values at different points intime.

Present value analysis — tool to convert CFs at differentpoints in time to comparable valuesat a given point in time.

How much must you invest at a particular point in time toobtain a given amount of money on a specific date in thefuture?

General Formula (Inverse of FV):

Suppose you will deposit some money in an account that pays8% interest per year. How much do you need to deposit tohave $1350 in the account after 1 year?

FV1 = $1350n = 1k = 0.08PV = ?

Suppose, instead, that you need to have $1,836.66 in five years inorder to take a trip you’ve been planning. How much should youput in your bank account which pays 8% per year.

Q Most problems can be handled with these formulas

RECOGNIZING PATTERNS IN CF STREAMS

O Most problems can be solved using lump sum formulas.However calculations may become cumbersome

O Calculations can be simplified when CF streams follow certainpatterns

O Perpetuity — constant CF stream that continues forever

PV of the perpetuity is the lump sum amount today that allowsyou to generate the same CF stream that is provided by theperpetuity.

Question: How much do we need today to recreate the sameCF stream as the perpetuity generates?

Note: CF stream continues forever so CFs must be generatedfrom interest without touching principal

So, C = (PVt)k Y PVt =

Formally,

PVt =

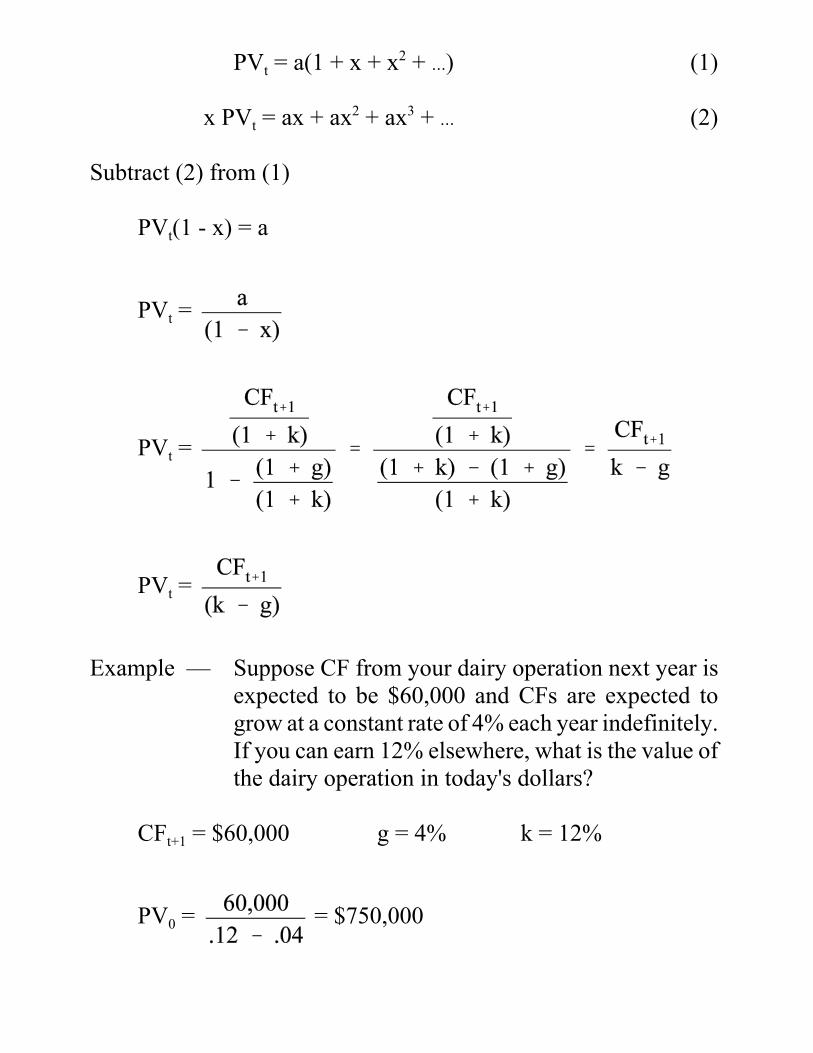

Let and x =

PVt = a (1 + x + x2 + ÿ) (1)

multiply (1) by x

x PVt = ax + ax2 + ÿ (2)

Subtract (2) from (1)

PVt - x PVt = a

PVt (1 - x) = a

PVt =

PVt =

Example — Suppose you receive $1,000 each year foreverstarting 1 year from today. If you can earn10% elsewhere, what is the value of theperpetuity today?

C = $1000 k = 10%

PV0 = = $10,000

Suppose k falls to 7%. What happens to the value of theperpetuity?

PV0 = = $14,285.71

O Growing Perpetuity — CF stream that grows at a constantrate forever

PVt =

CFt+1 = CF at t + 1g = constant growth rate of CF stream (%)k = rate of return elsewhere

Simplifies to

PVt =

Formally

PVt =

Let a = and x =

PVt = a(1 + x + x2 + ÿ) (1)

x PVt = ax + ax2 + ax3 + ÿ (2)

Subtract (2) from (1)

PVt(1 - x) = a

PVt =

PVt =

PVt =

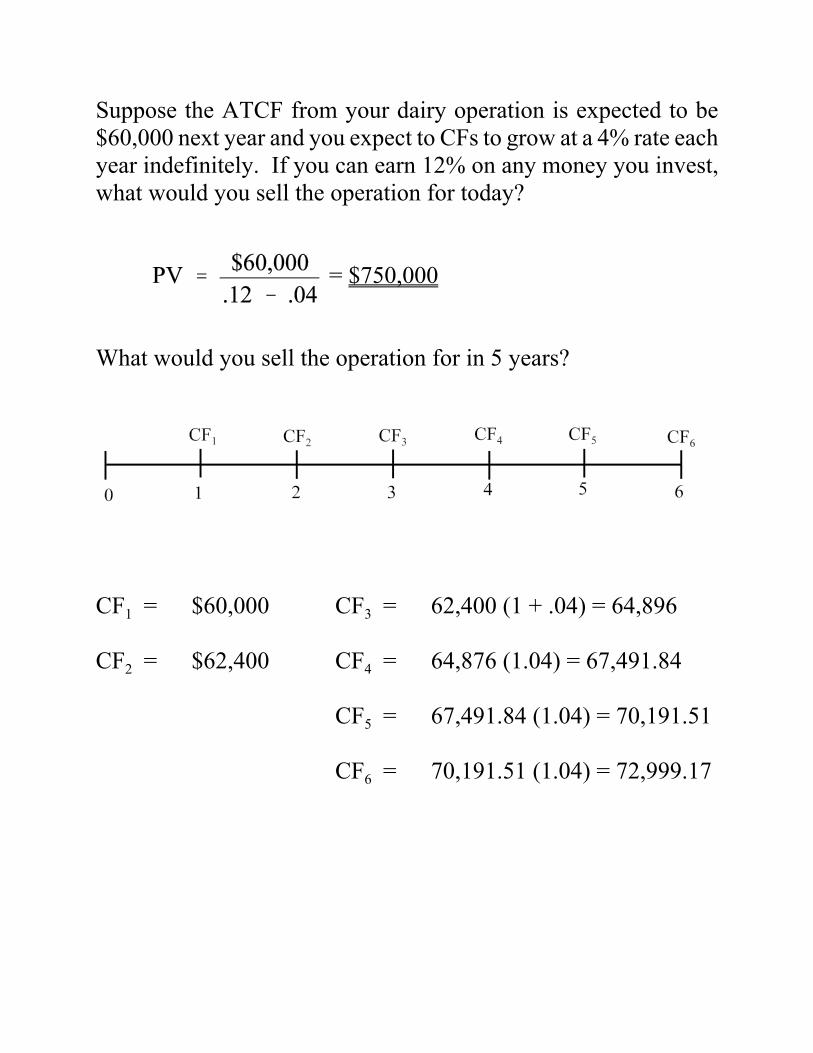

Example — Suppose CF from your dairy operation next year isexpected to be $60,000 and CFs are expected togrow at a constant rate of 4% each year indefinitely.If you can earn 12% elsewhere, what is the value ofthe dairy operation in today's dollars?

CFt+1 = $60,000 g = 4% k = 12%

PV0 = = $750,000

O Important Points

Q Numerator is CF in the next period from the point atwhich you wish to find the PV of the future CF stream

To find the PVt you need CFt+1 in the numerator

Example — Find the PV1 of dairy operation in thelast example

PV1 =

Constant growth formula always gives PV one period beforeCF in the numerator

O Interest rate must be greater than growth rate (k > g)

As k 6 g PV 6 4If k = g PV is undefined

O CFs assumed to occur at regular discrete intervals

Suppose the ATCF from your dairy operation is expected to be$60,000 next year and you expect to CFs to grow at a 4% rate eachyear indefinitely. If you can earn 12% on any money you invest,what would you sell the operation for today?

= $750,000

What would you sell the operation for in 5 years?

CF1 = $60,000 CF3 = 62,400 (1 + .04) = 64,896

CF2 = $62,400 CF4 = 64,876 (1.04) = 67,491.84

CF5 = 67,491.84 (1.04) = 70,191.51

CF6 = 70,191.51 (1.04) = 72,999.17

Or CF6 = CF1 (1 + g)5

= 60,000 (1 + .04)5 = 72,999.17

Or CF6 = CF1 (FVIF4,5) = 72,999.17

PV5 = = $912,489.63

Why can’t we just take

$750,000 (FVIF12,5) = $1,321,756.26?

O Annuity — stream of fixed CFs of the same size thatoccur at equal increment over a finite timehorizon

O Present Value of Annuity — how much do you need todayto generate a stream identicalto the annuity CF

Present value of a perpetuity starting today

P0 =

Present value of a perpetuity starting at n

P0 =

The value of the annuity will be the value of the perpetuity today,less the present value of the CFs that occur after the last annuitypayment.

PVt =

=

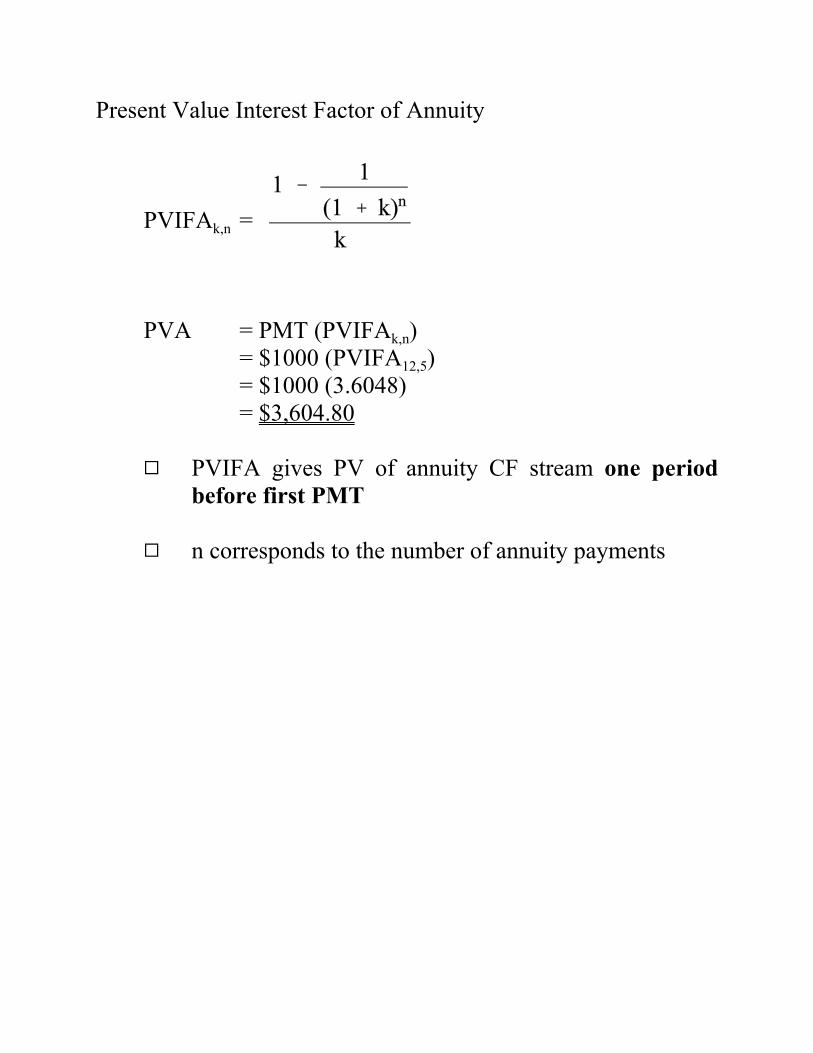

PVIFAk,n =

Suppose C = $1000 n = 5 k = 12%

PV0 = 1000(PVIFA12,5)= 1000(3.6048)= $3,604.80

We can check the answer by using the lump sum formula on eachannuity CF.

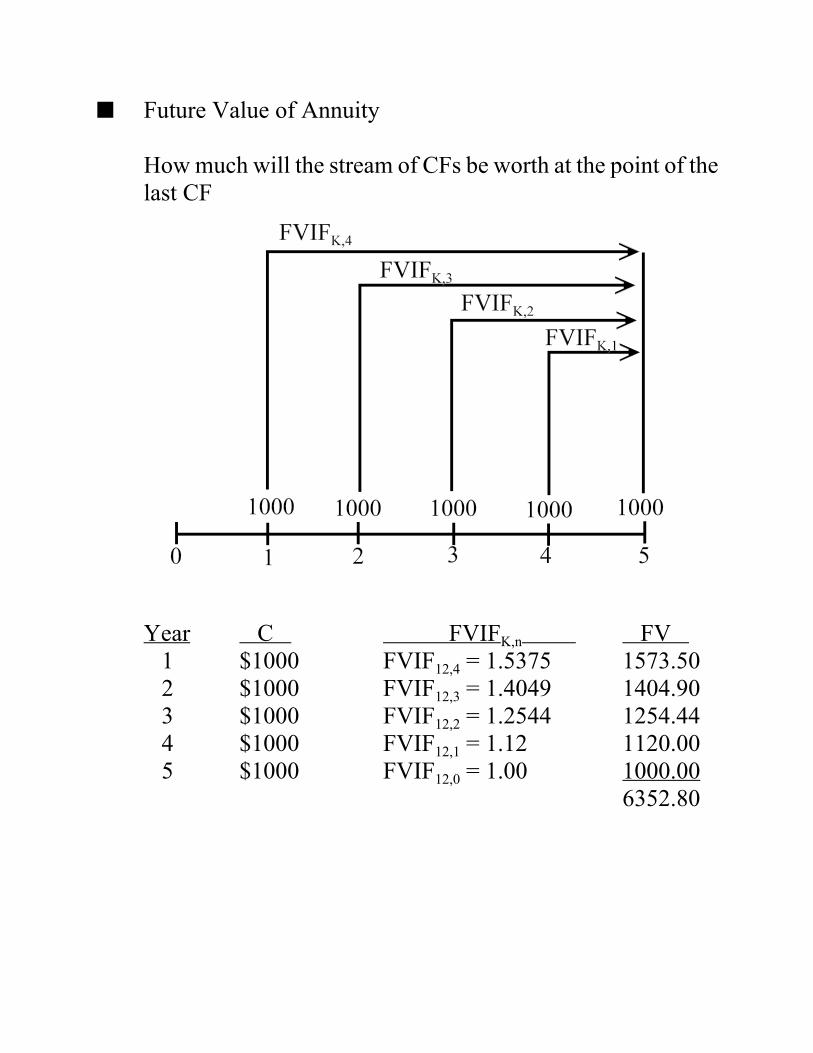

# Present Value of an Annuity — Amount of money youneed to deposit togenerate given annuitystream of CFs.

Suppose you earn 12% on money you invest. How much doyou need to invest today to be able to withdraw $1000 at endof each year for the next 5 years?

This is a lump sum value of the annuity one period before thefirst CF. We can find the value of annuity at the point of thelast CF by moving the PV of the annuity forward as a lumpsum.

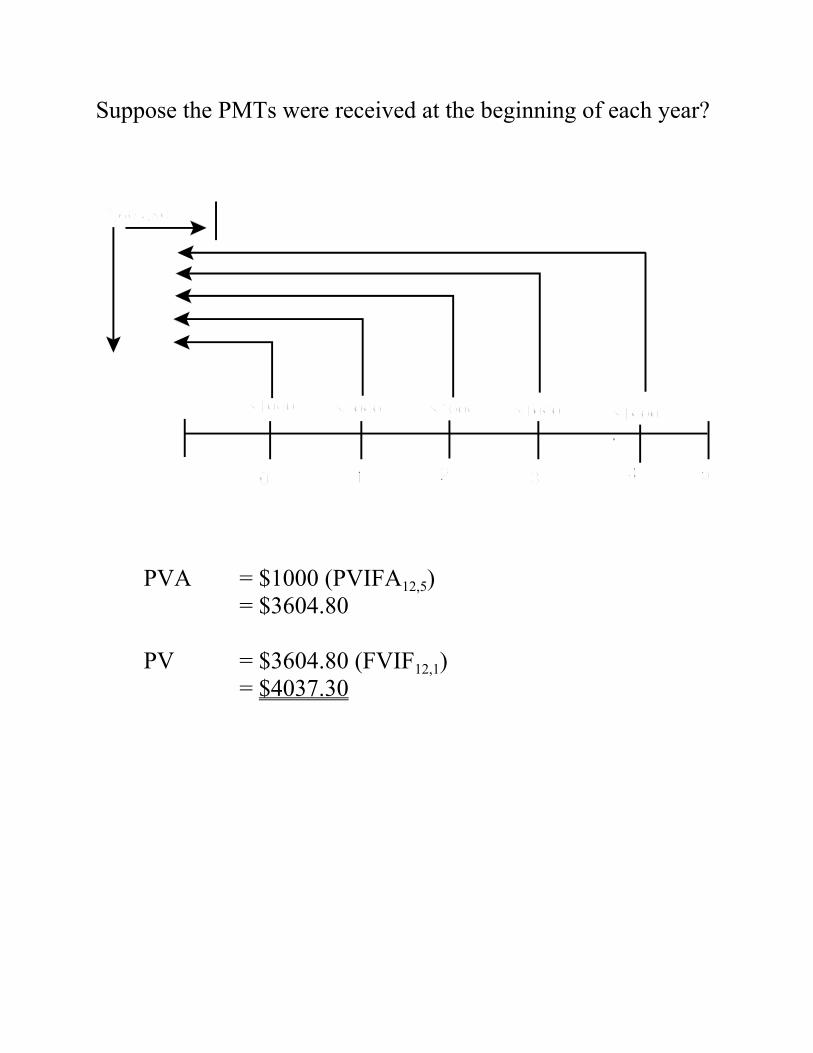

Suppose instead you received the PMTs as an annuity due.

How much would you have after 5 years.

FVA5 = $1000 (FVIFA12,5) = $100 (6.3528)

= $6,352.80 (1.12)

= $7,115.14 (Amount at end of year 5)

Example — Infrequent Annuities

Suppose you receive a $500 annuity every two years for the next10 years. What will be the future value of the annuity at the pointof the last payment if you can earn a return of 8% each year?

The payments occur every 2 years and so to use our formula weneed the rate of return for each 2 year period.

Note: if g = 0 the formula reduces to the PV of an annuity

Proof:

Analogous to the derivation of the annuity formula, we canfind the PV of the growing annuity by subtracting the PV ofCFs after period n from the value of a growing perpetuity.

PV of a growing perpetuity

(1)

PV of CFs after period n

(2)

Subtract (2) from (1) to get the PV of the growing annuity

Example — Suppose you take a job that pays you $40,000/yearafter taxes. You also expect the after-tax salary toincrease by 4% each year for the next 30 years.What is the value of your job if you can earn 12%elsewhere?

PV= $445,871.06

Formula only works for k … g

If k = g

PV =

PV =

=

Example — Suppose you need to make tuition payments eachof the next 4 years. The first payment will be$15,000 next year and the payments will increase8% each year. If you can earn 8% elsewhere, whatis the PV of the tuition payments today? (Howmuch needs to be deposited today to make thepayments?)

PV =

O Uneven Streams of CFs

Treat each CF as a lump sum or look for embedded patternsof CFs that we can simplify

We can find annuity streams given the number of payments,the interest rate, and PV (or FV) of the annuity.

PV = C(PVIFAK,n) Y C =

FV =

Example — Suppose you borrow $10,000 today and agreeto repay the loan in 5 equal sized annualpayments beginning one year from today. Ifthe interest rate is 10%, what is the size ofeach payment?

PV = 10,000, n = 5, k = 10%

CF = = $2637.97

How large is each payment if you make the first payment atthe end of year 2?

3.7908 .9091$10,000 = X(PVIFA10,5)(PVIF10,1)

X = = $2901.76

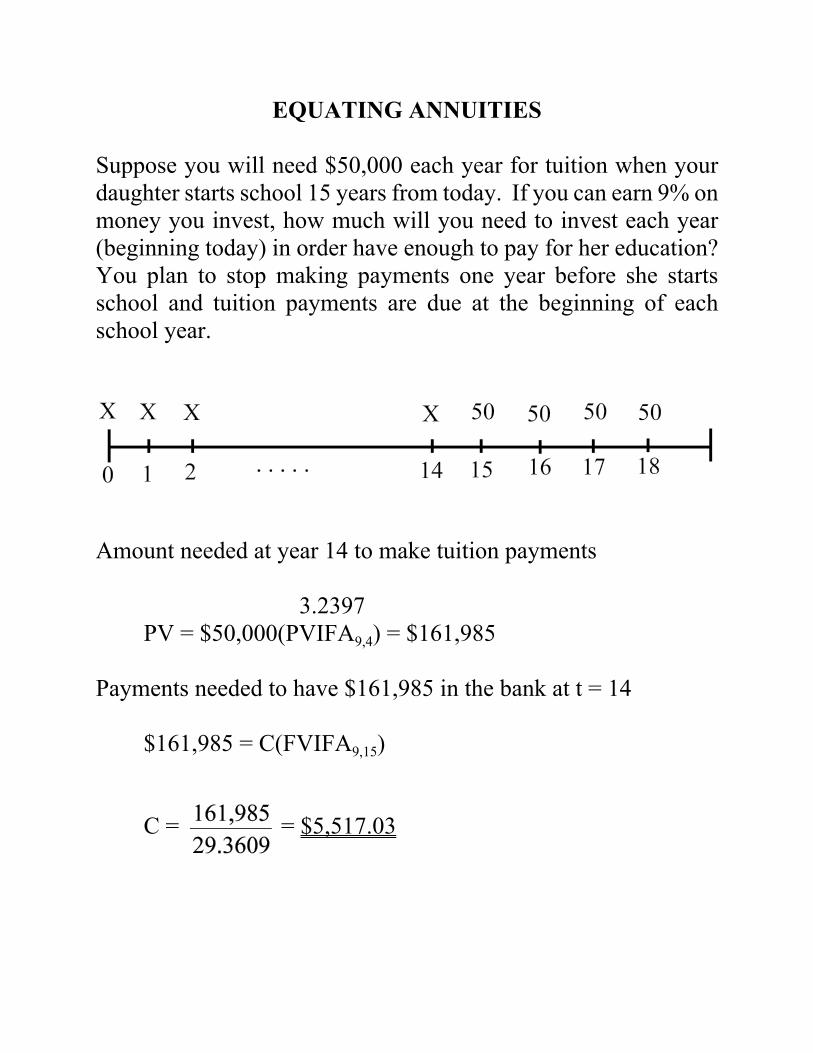

EQUATING ANNUITIES

Suppose you will need $50,000 each year for tuition when yourdaughter starts school 15 years from today. If you can earn 9% onmoney you invest, how much will you need to invest each year(beginning today) in order have enough to pay for her education?You plan to stop making payments one year before she startsschool and tuition payments are due at the beginning of eachschool year.

Amount needed at year 14 to make tuition payments

3.2397PV = $50,000(PVIFA9,4) = $161,985

Payments needed to have $161,985 in the bank at t = 14

$161,985 = C(FVIFA9,15)

C = = $5,517.03

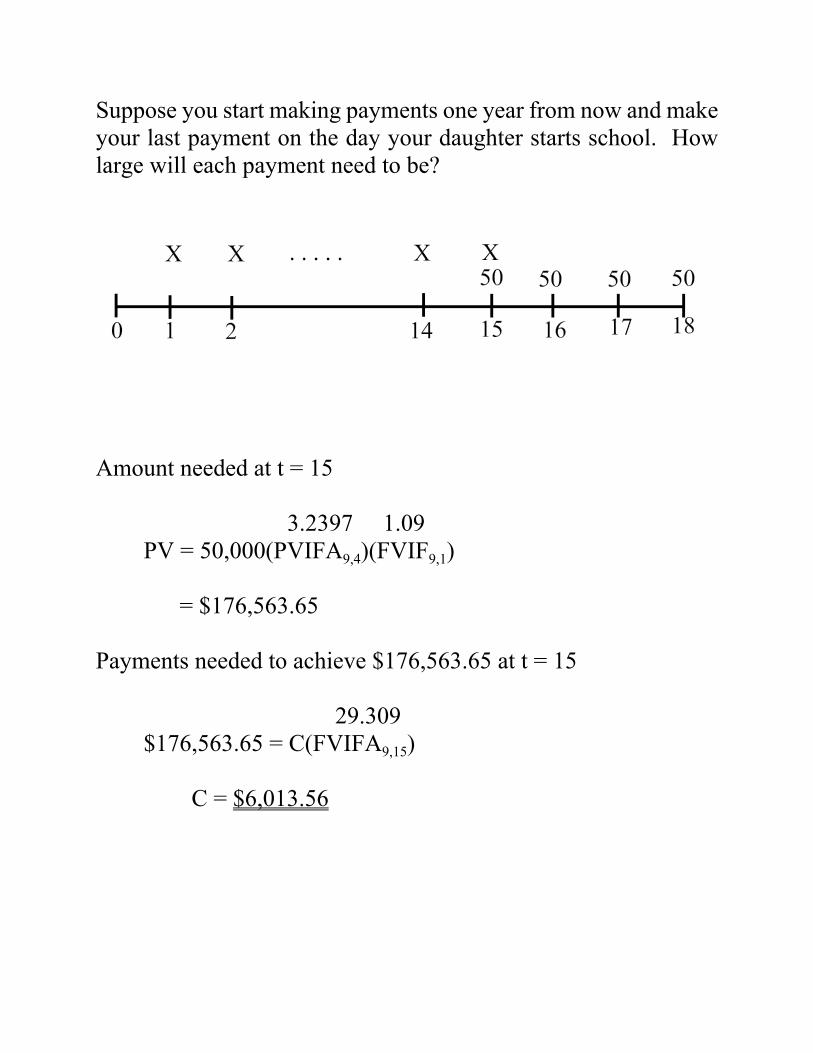

Suppose you start making payments one year from now and makeyour last payment on the day your daughter starts school. Howlarge will each payment need to be?

Amount needed at t = 15

3.2397 1.09PV = 50,000(PVIFA9,4)(FVIF9,1)

= $176,563.65

Payments needed to achieve $176,563.65 at t = 15

29.309$176,563.65 = C(FVIFA9,15)

C = $6,013.56

O Finding Interest Rates

O Lump Sums

Suppose you borrow $5000 today and pay back $7013 at theend of 5 years. What interest rate are you paying on the loan?

PV = $5000 FV = $7013 n = 5 k = ?

$5000 = $7013(PVIFK,5)

PVIFK,5 = 0.713

from table k = 7%

Using formula directly

5000 = 7013

ln(5000) = ln(7013) - 5 ln(1 + k)

ln(1 + k) = = .067666

(1 + k) = e.067666 = 1.07

k = .07 or 7%

O Annuities

Suppose you borrow $5000 and repay $1,285.45 at the end ofeach year for the next 5 years. Find k.

$5000 = $1285.45 (PVIFAK,5)

PVIFAk,5 = = 3.8927

K = 9%

O Linear Interpolation

Suppose you loan $5000 to a friend and require equalinstallments of $1,150 at the end of each year for 5 years.What rate of return did you earn?

.104

k = 4% + (1%) = 4.85%

.1223

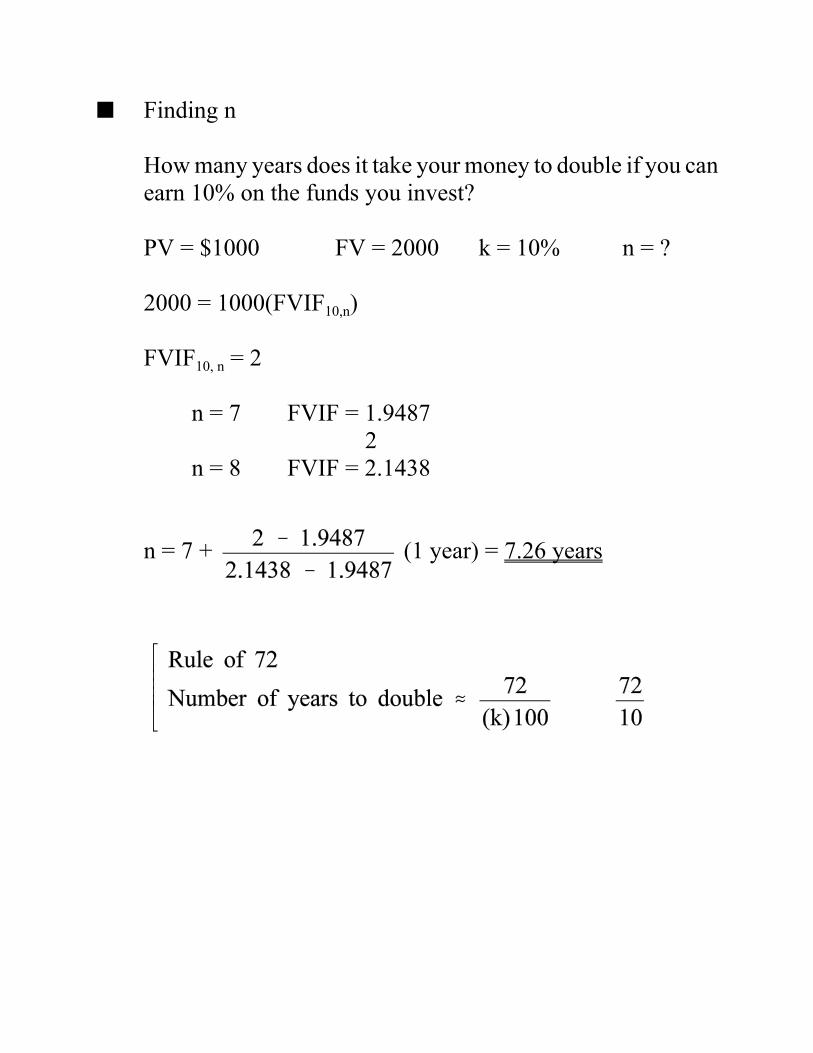

O Finding n

How many years does it take your money to double if you canearn 10% on the funds you invest?

PV = $1000 FV = 2000 k = 10% n = ?

2000 = 1000(FVIF10,n)

FVIF10, n = 2

n = 7 FVIF = 1.9487 2

n = 8 FVIF = 2.1438

n = 7 + (1 year) = 7.26 years

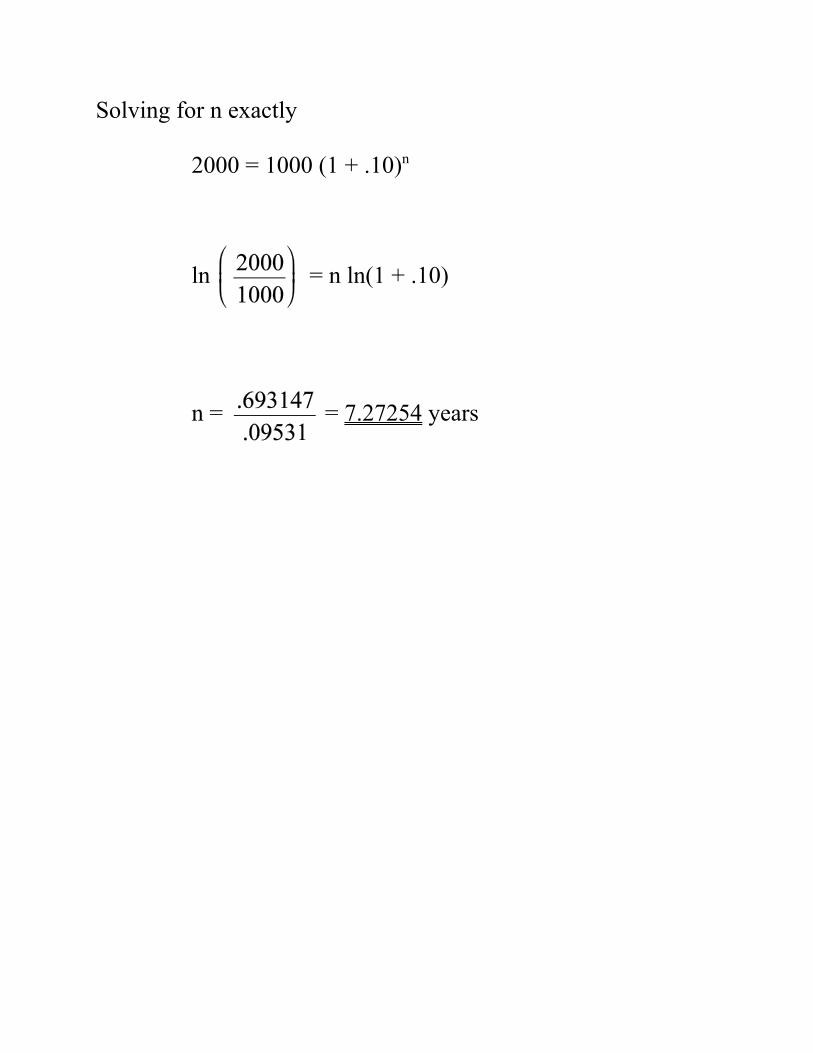

Solving for n exactly

2000 = 1000 (1 + .10)n

ln = n ln(1 + .10)

n = = 7.27254 years

O Compounding More Frequently

Up until now 6 annual compounding

ka = stated annual interest rate (nominal rate)

Compounding may occur at intervals that are less than 1 yearin length

Example — Semiannual compounding mean 1/2 of theannual rate is paid after six months. Duringthe second six months interest is compoundedso you earn interest on the interest paid thefirst six months.

Invest $100 at ka = 10%. Compounding is semiannual. Howmuch will you have after 1 year?

After six months 100(1 + .05) = $105After 1 year 100(1 + .05) (1 +.05) = $110.25

105 Interest on 1st

six months interest

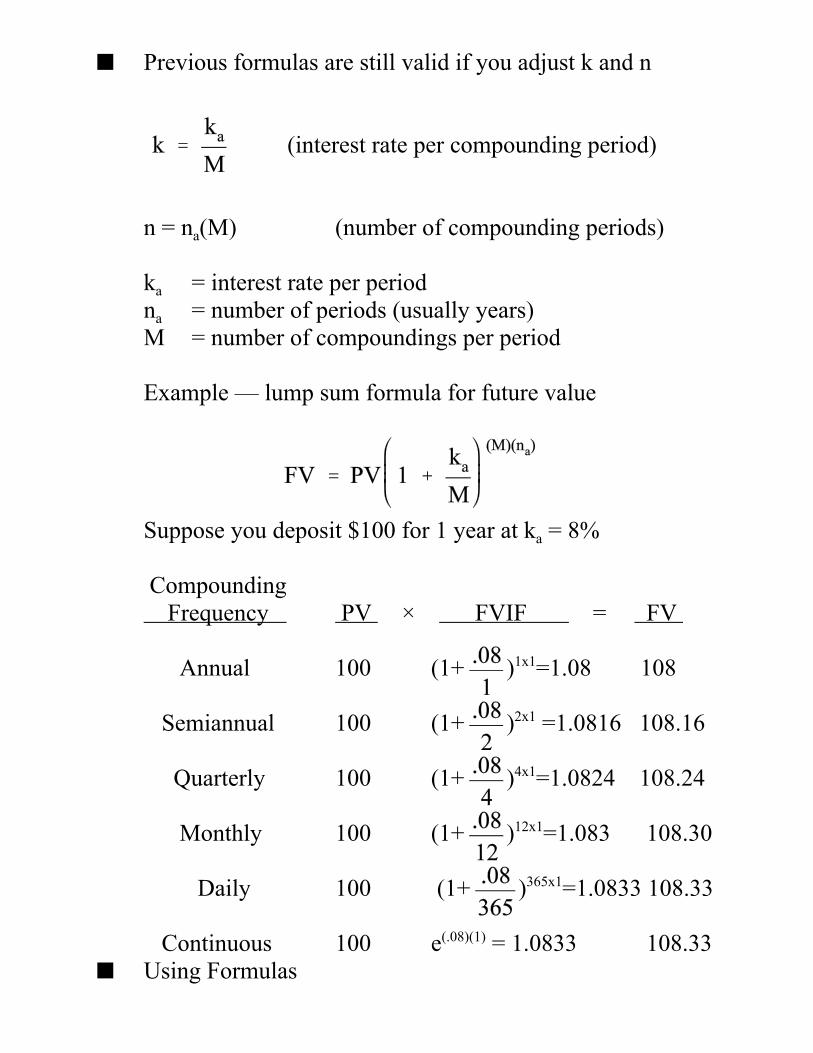

O Previous formulas are still valid if you adjust k and n

(interest rate per compounding period)

n = na(M) (number of compounding periods)

ka = interest rate per periodna = number of periods (usually years)M = number of compoundings per period

Example — lump sum formula for future value

Suppose you deposit $100 for 1 year at ka = 8%

Compounding Frequency PV × FVIF = FV

Annual 100 (1+ )1x1=1.08 108

Semiannual 100 (1+ )2x1 =1.0816 108.16

Quarterly 100 (1+ )4x1=1.0824 108.24

Monthly 100 (1+ )12x1=1.083 108.30

Daily 100 (1+ )365x1=1.0833 108.33

Continuous 100 e(.08)(1) = 1.0833 108.33O Using Formulas

Suppose you deposit $1000 in an account paying 8%compounded semiannually. How much would you have after5 years in the account?

k = = = .04

n = (na) (M) = (5)(2) = 10

FV5 = 1000(FVIF4,10)= 1480.20

Suppose you purchase a new truck and your payments will be$350/month for 5 years. Your parent's want to give you agraduation present and offer to deposit enough in an accountpaying 12% compounded monthly so that you can make yourpayments. How much needs to be deposited today if yourfirst payment is next month?

k = = 1 n = (12)(5) = 60

PV = 350(PVIFA1,50) = 350 144.955)

= $15,734.26

CONTINUOUS COMPOUNDING

O When compounding occurs M times per period then our FVinterest factor for n periods is

Example — 10% semiannually for 2 years (M=2, n=2, ka=.10

FVIF =

O The number e

By definition

FVIF if k = 100% and continuous compounding

Invest $1 at 100% compound continuously gives you $1e = $1(2.71828) = $2.71828 after 1 year

Two years: FV = $1 (e)2 = $7.38906

n years: FV = 1(e)n

O Continuous Compounding at ka

Let w =

FVn =

As M 6 4, w 6 4 Y

Suppose you invest $1000 at an interest rate of 10%compounded continuously. How much do you have after 10years?

Note:

O Continuous CFs — formulas still work — need to use continuous return

O Constant Payment Annuities

Assume asset pays constant amount per unit of time

Ct = C stream of payments starts now andcontinues for n time periods

Continuously compounded discount rate = k

Remember "Fundamental Theorem of Calculus"

Find the indefinite integral of the integral, substitute the upperand lower bound, and find the difference.

Analogous to discrete time annuity factor

where k = discrete rate/period

Suppose n 6 4 (Perpetuity)

where k is continuously compounded return

Example 1 — Suppose you are going to receive a perpetuity of$1000 each year paid continuously during the year.If you can earn 10% compounded continuously,what would you sell the perpetuity for today?

What is the value of the perpetuity if you receive the $1000payments at the end of each year, but you can still earn 10%compounded continuously?

Interest earned during the year

Check: $9508.42 (.10517) = $1000

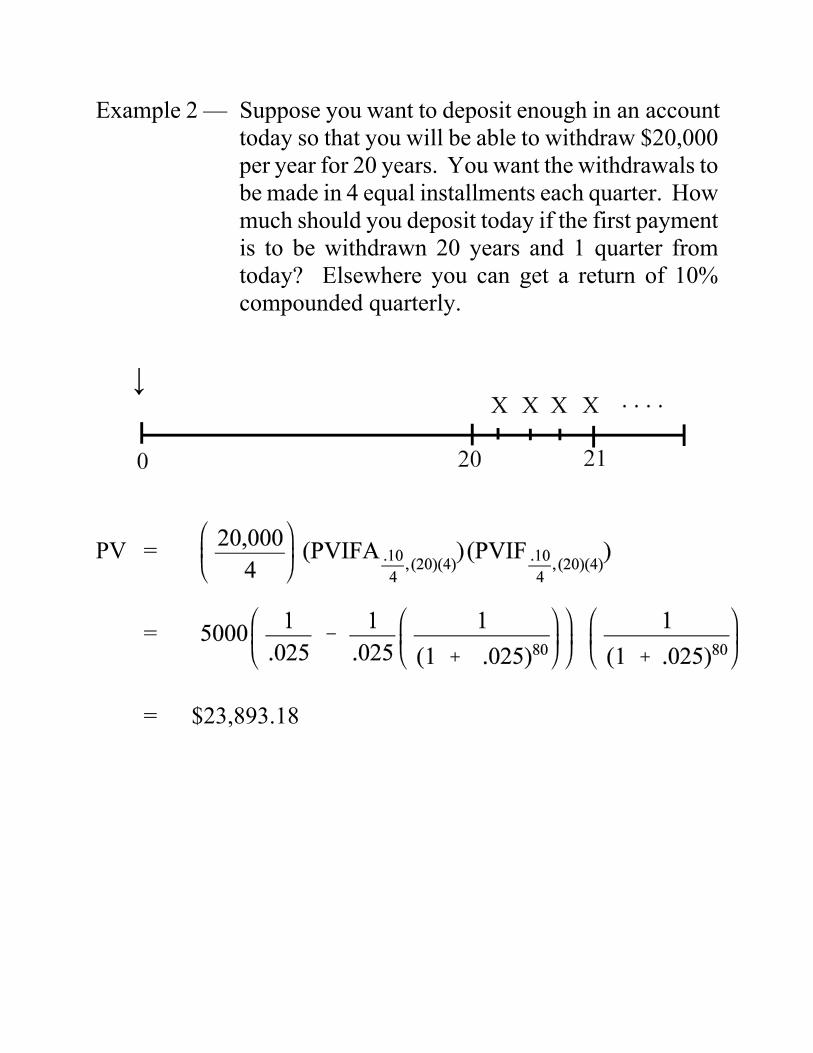

Example 2 — Suppose you want to deposit enough in an accounttoday so that you will be able to withdraw $20,000per year for 20 years. You want the withdrawals tobe made in 4 equal installments each quarter. Howmuch should you deposit today if the first paymentis to be withdrawn 20 years and 1 quarter fromtoday? Elsewhere you can get a return of 10%compounded quarterly.

PV =

=

= $23,893.18

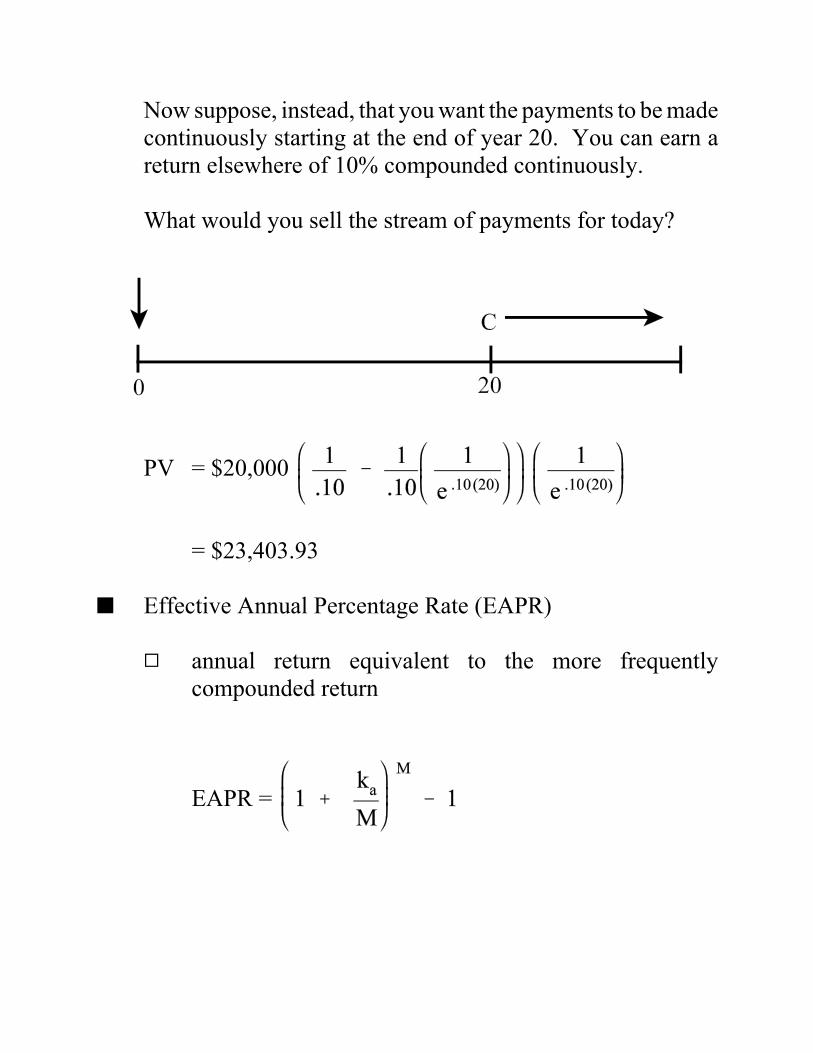

Now suppose, instead, that you want the payments to be madecontinuously starting at the end of year 20. You can earn areturn elsewhere of 10% compounded continuously.

What would you sell the stream of payments for today?

PV = $20,000

= $23,403.93

O Effective Annual Percentage Rate (EAPR)

Q annual return equivalent to the more frequentlycompounded return

EAPR =

Example 1 — Suppose we have

ka = 10% compounded quarterly

ka = 9.8771% compounded continuously

EAPR10,quarterly = = .103813 or 10.38%

EAPR9.871%, continuously = = .103813 or 10.38%

Example 2 — Credit card companies state APR = 18%However, monthly rate is 1.5%

EAPR = = (1 + .015)12 - 1

= .1956 or 19.56%

Annuities with Growing Payments

Let ct = c egt where g is the continuous growth rate

Using rules of integral calculus, the solution to the integral is

Suppose you have growing perpetuity

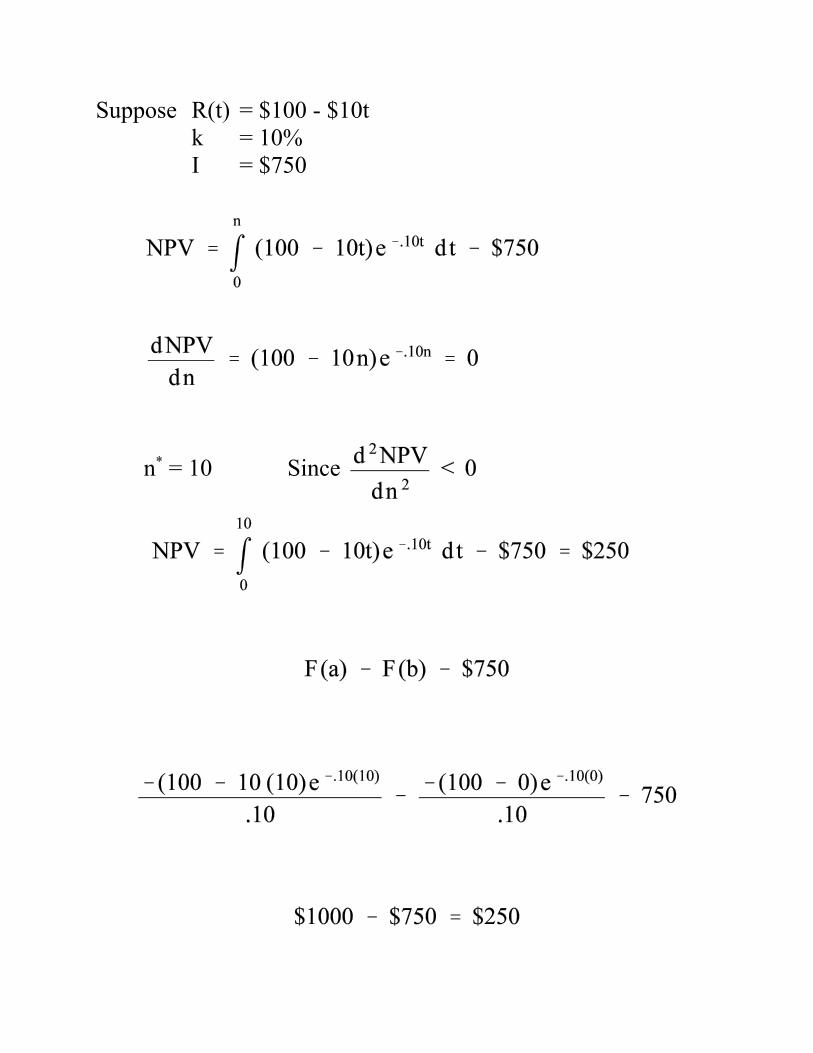

OPTIMAL LIFE WITHOUT REPLACEMENT, DISPOSAL, OR SALVAGE VALUE

whereR(t) = return or cash flow at tI0 = initial investmentk = continuously compounded opportunity costn = life of asset

Rule for differentiating an integral

So

FOC:

SOC:

Suppose R(t) = $100 - $10tk = 10%I = $750

n* = 10 Since

PRICES, RETURNS, AND COMPOUNDING

O Financial Economics Often Works with Returns

Q scale-free summary of investment opportunity

Q more attractive than prices for theoretical and empiricalreasons

e.g. general equilibrium models often yield non-stationary prices, but stationary returns (more later)

Definitions and Conventions

Simple net return

(gross return = 1 + rt)

O Multi-year returns often annualized to make comparison

Annualized

(geometric average)

Approximate Annualized [rt (k)] = `

(arithmetic average)

O Continuous Compounding

Remember:

O Gross returns over most recent k periods (t - k to t) defined as1 + rt (k)

net return = rt(k)

O Multi-period return called compound return

O Returns are scale-free but not unit less

Q always defined w.r.t. some time period 10% return is nota complete description . . . need length of time period

Convention: quote annual rates

O Consider multi-period return

O Simplifies multiplication properties to additive properties

O More importantly: easier to derive time series properties ofadditive process

O Disadvantage with portfolio analysis

portfolio returns

problem - log of sum not the same as sum of log

(can be used as approx.)

O In general

Q use continuous return in temporal analysis Q use simple returns in cross-sectional work