33

Group Presentation Association of Greek Institutional Investors 24 June 2009

| Date post: | 26-Aug-2018 |

| Category: |

Documents |

| Upload: | truongdiep |

| View: | 214 times |

| Download: | 0 times |

Group Presentation

Association of Greek Institutional Investors

24 June 2009

2

DISCLAIMER

These preliminary materials and any accompanying oral presentation (together, the “Materials”) have been prepared by Mytilineos Holdings SA (the “Company”) and are intended solely for the information of the Recipient. The Materials are in draft form and the analyses and conclusions contained in the Materials are preliminary in nature and subject to further investigation and analysis. The Materials are not intended to provide any definitive advice or opinion of any kind and the Materials should not be relied on for any purpose. The Materials may not be reproduced, in whole or in part, nor summarised, excerpted from, quoted or otherwise publicly referred to, nor discussed with or disclosed to anyone else without the prior written consent of the Company.

The Company has not verified any of the information provided to it for the purpose of preparing the Materials and no representation or warranty, express or implied, is made and no responsibility is or will be accepted by the Company as to or in relation to the accuracy, reliability or completeness of any such information. The conclusions contained in the Materials constitute the Company’s preliminary views as of the date of the Materials and are based solely on the information received by it up to the date hereof. The information included in this document may be subject to change and the Company has no obligation to update any information given in this report. The Recipient will be solely responsible for conducting its own assessment of the information set out in the Materials and for the underlying business decision to effect any transaction recommended by, or arising out of, the Materials. The Company has not had made an independent evaluation or appraisal of the shares, assets or liabilities (contingent or otherwise) of the Company .

All projections and forecasts in the Materials are preliminary illustrative exercises using the assumptions described herein, which assumptions may or may not prove to be correct. The actual outcome may be materially affected by changes in economic and other circumstances which cannot be foreseen. No representation or warranty is made that any estimate contained herein will be achieved.

3

� Group Overview

� Financial Review

� Areas of Activity

�Metallurgy & Mining

�Energy

�Engineering Procurement Construction (EPC)

� Stock Data

� Summary

AGENDA

4

Group Overview

5

GROUP HISTORY

2007 -20082006200520021998-20001995-19971908-1994

1908: Company founded by Mytilineos family members in Athens, Greece.

1995: Company listed on the Athens Stock Exchange.

1996: Signing of strategic agreements with metal, mining & mineral companies in Southeast Europe.

1998: Hostile acquisition of Metka S.A. the leading electromechanical and metallic construction company in Greece.

2000: Participation in state –owned ELVO S.A., major supplier of the Hellenic Armed Forces of trucks, armoured vehicles and other appropriately modified military vehicles.

2005: Acquisition of Aluminium of Greece S.A. one of the largest vertical integrated alumina and aluminium producers in Europe.

1998: Acquisition of Romania - based Sometra S.A. the largest South Eastern Europe’s Lead (Pb) and Zinc (Zn) producer.

1999: Acquisition of Cyprus-based Hellenic Copper Mines.

2002: Establishment of Mytilineos Power Generation and Supplies S.A. (MPGS). and Mytilineos Hellenic Wind Power S.A. (MHWP).

2006: Acquisition of Delta Project S.A. a company engaging in the development, construction and operation of hydroelectric power stations and wind parks.

2008: Motor Oil and Mytilineos Group sign major deal in the Energy Sector to construct and operate a 437 MW CCGT.

Source: Company Information.

2008: COGEN successfully dispatched. The first thermal power plant of Mytilineos Group has started its commissioning period.

2007: Merger by absorption of Aluminium of Greece and Delta Project by Mytilineos Holdings. Delisting of both subsidiaries.

2007: Strategic Partnership with Endesa. Endesa (Hellas) is created – a reference player in the Greek Energy Market seeking to expand into S.E. Europe.

6

GROUP OVERVIEW

Metallurgy& Mining

Energy

EPC

• Largest Aluminium (Al) and Alumina (Ox) producer in South Eastern Europe with international presence through Aluminium of Greece S.A.

• Second largest Bauxite producer in Greece through Delphes-Distomon S.A.

• Endesa Hellas: JV with Endesa, with a significant portfolio in the pipeline and under construction and a well balanced mix between thermal and RES soon to become the largest independent power operator in Greece. Current Portfolio includes:

– 334 MW CHP – Combined Heat & Power Plant in Viotia Region (in operation).

– 444 MW CCGT – Merchant Power Plant in Viotia Region (to be completed by March 10).

– 437 MW CCGT – Merchant Power Plant in Korinthos Region (to be completed by April 11).

– 437 MW CCGT – Merchant Power Plant in Volos Region (to be completed by January 12).

– Portfolio of Renewable Energy Generation Assets (RES) (Wind parks, Hydroelectric Power Stations and Photovoltaic Parks) of total capacity of 1,000 MW. 45MW RES in full commercial operation.

– Electricity Trading Licence of 310 MW.

– CO2 Emission Trading Platform.

– Production Licence for a 600 MW Coal – Fired Power Plant in Viotia Region.

• Leading Greek EPC company through METKA S.A. and Subsidiaries and one of the most reliable EPC Contractors throughout Europe.

Source: Company Information.

7

GROUP’S CORPORATE STRUCTURE

Source: Company Information.Note: Market data 22 June 2009.METKA is the only remaining listed subsidiary.

MYTILINEOS HOLDINGS

METKA(56.6%*)

ALUMINA & ALUMINIUM(100%)

54.0%METALLURGY & MINING

ENERGY EPC

ENDESA (HELLAS) (49.99%)

ELVO (43%)

DELPHI DISTOMON (100%) Non Core Sector

Mkt Cap*: € 695 mn

Mkt Cap*: € 421 mn

VEHICLE MANUFACTURING

8

Financial Review

9

238

283

281

103

132194

708

634

66166

302

779

857

509

196185

402

800

773

877

268

219

631

901

902

868

367

501

368

542

FINANCIAL REVIEW

Source: Company Information.

* Net Debt = Debt – Cash Position.To note that Net Debt does not include the share % of the Group in Endesa.

2004

2005

2006

2007

Total Equity

Fixed Assets

Current Assets

Net Debt

Long TermLiabilities

Short TermLiabilities

Balance Sheet

� Solid Balance Sheet.� Healthy Debt to Equity Ratio.� Substantial Growth of Equity.

2008

10

509

877 868

402

631

368

542

281 302194

1.3

2.4

1.5

1.8

1.4

0

100

200

300

400

500

600

700

800

900

1,000

2004 2005 2006 2007 2008

0.0

0.5

1.0

1.5

2.0

2.5

Current Assets Current Liabilities Current Ratio

FINANCIAL REVIEW

Evolution of Group Turnover, EBITDA & Earnings after Taxes

Source: Company Information.

(in € mn)

Financial Performance

779 800

901

196268

367238

708

103 66

25.1%

40.7%

33.5%

9.3%

43.2%

0

100

200

300

400

500

600

700

800

900

1,000

2004 2005 2006 2007 2008

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

35.0%

40.0%

45.0%

50.0%

Equity Net Debt Net Debt / Equity

837913

976

157 21131

311

747

20256

18.8%

3.2%

23.1%

34.3%

6.4%

0

200

400

600

800

1,000

1,200

2004 2005 2006 2007 2008

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

35.0%

40.0%

Turnover EAT EAT %

837913

976

187 154 118

311

747

42 158

22.3%

12.1%

16.9%

21.2%

13.5%

0

200

400

600

800

1,000

1,200

2004 2005 2006 2007 2008

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

Turnover EBITDA EBITDA%

11

Areas of Activity

Metallurgy & Mining

12

M & M – BUSINESS OUTLOOK

� Facilities established in 1960’s. Leading industrial producer of alumina and aluminium in South Eastern Europe.

� Production facilities occupy an area of 7,035,700m2 and constitute a vertically integrated production unit.

� Owner of port facilities for large tonnage ships.

� Low cost production base in Europe both for Alumina and Aluminium - production in half of cost curve in Europe.

� Enough alumina to cover own aluminium production needs and to export 460,000 tn per annum.

� 10-year contract with Glencore AG regarding 100% of excess alumina production.

� Steam is produced by the 334 MW CHP Plant of Endesa Hellas, 50% owned by Mytilineos Group.

� Exploitation of bauxite reserves by the 100% owned subsidiary Delphes – Distomon S.A. covering half of its Bauxite requirements. Long term contracts with other suppliers (Alcan, S&B, Glencore AG).

� Efficient risk management strategy. The Group acting proactively secured Aluminum sales in prices well above current market levels for 2009 and 2010. Hedging book currently valued over $300m.

Alumina & AluminumBusiness Overview Operational & Financial Overview

Key Strengths

Source: Company Information.

788,900 771,769

164,500 168,000 162,339

780,000782,000

165,300

0

100,000

200,000

300,000

400,000

500,000

600,000

700,000

800,000

900,000

2005 2006 2007 2008

tn OX AL

471

73 4952 77 37 20

469382

471

79110

10.4%

23.4%

20.7%

15.5%

0

50

100

150

200

250

300

350

400

450

500

2005 2006 2007 2008

€ mil

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

Turnover EBITDA EAT % EBITDA

13

Other Raw

Materials Cost

10%

Average

Delivered

Alumina Cost

25%

Total Other

Costs 15%

Labour Cost

10%

Total Energy

Cost 40%

Other Raw

Materials Cost

16%

Total Energy

Cost 29%

Labour Cost 6%

Total Other

Costs 9%

Average

Delivered

Alumina Cost

40%

M & M – BUSINESS OUTLOOK

Source: Company Information, CRU ANALYSIS.

Aluminum Cost Analysis

Total Market AoG

95 82 78124 109 107 72 5773 67 59 63 75100109

0

20

40

60

80

100

120

140

2008 2007 2006 2005 2004

€ mil

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

Raw M. Energy Fabrication

Raw M.% Energy% Fabrication%

95 82 78124 109 107 72 5773 67 59 63 75100109

0

20

40

60

80

100

120

140

2008 2007 2006 2005 2004

€ mil

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

Raw M.

95 82 78124 109 107 72 5773 67 59 63 75100109

0

20

40

60

80

100

120

140

2008 2007 2006 2005 2004

€ mil

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

Raw M. Energy Fabrication

Raw M.% Energy% Fabrication%

AL Division – Cost Structure

14

North America

15%

Europe

14%Asia

42%

CIS

12%C&S America

7%Australia

6%

Africa

4%

North America

16%

Europe

24%Asia

54%

Africa

1%

Australia

1%

C&S America

4%

North America

14%

Europe 25%

C&S America

7%Australia 6%

Africa 4%

Asia 44%

Europe 7%

North America

7%C&S America

20%

Australia 25%

Africa 1%

CIS 8%

Asia 33%

M & M – INDUSTRY OUTLOOK

Alumina & Aluminum

Alumina Supply (2008) Aluminium Supply (2008)

Total Market 79 MT Total Market 40 MT

Source: CRU ANALYSIS.

Alumina Demand (2008) Aluminium Demand (2008)

Total Market 78 MT Total Market 38 MT

15

ALUMINIUM

� The average Aluminum price the 1st Quarter of 2009 has settled at $1,360 down 50.2% y-o-y and well below the Group’s hedged price level.

� Inventory Level: Production cuts seem still not enough to prevent total reported stocks from rising at 5.5 Mt at the end of the 1st

Quarter. Stocks have risen around the globe with the only exception of Asia mainly due to Chinese imports.

� Supply: Global surplus the 1st Quarter of 2009 has reached nearly 1.3 Mt. Total world supply is down 9.1% y-o-y however cutback announcements from producers have slowed considerably after March 2009.

� Demand: Consumption outside China remains weak with leading indicators pointing towards stabilization in Europe and the USA.

AL Consumption Analysis 1Q09

North America

16%

Africa

2%Australia

1%

C&S America

4%

Asia

54%

Europe

23%

Announced Production Cuts by March 09

North America

17%

China

54%

Rest of the

world

3%

South America

1%Europe

25%

M&M - INDUSTRY & MACRO ENVIRONMENT

6Mt which represents 15% of 2008 total Production

Source: Company Information, CRU ANALYSIS.

7.6Mt, down 20% y-o-y

16

Areas of Activity

Energy

17

ENERGY - INDUSTRY OUTLOOK

The Greek Electricity Market

Source: Endesa Hellas.

Key Characteristics and Trends

Demand

Supply

Market Equilibrium

Competitive Dynamics

Future Outlook

�Consumption has grown with a yearly average of 3,7% in the decade 1998-2007, peaking during the summer (strong air cooling penetration in the commercial and residential sectors).

�The percentage of domestic lignite in generation, in the interconnected System, is around 56-60%, and Greece has reserves for another 50 years.

�Gas’s share is rising, 25% in 2007 and 26% in 2008, as most planned recent investments have been in CCGTs. Greece is importing gas (DEPA), mainly from Russia and Turkey via pipeline and LNG from Algeria and occasionally from the spotmarket.

�Wind only accounts for 3 percent of the mix, but Greece relies on important wind and solar potential and strong incentives estimated at more than 6 GW.

�Greece is not self-sufficient as it relies on imports between 7 and 11 percent of its consumption.

�Remaining capacity (UCTE definitions) is positive throughout the year, and higher than 5% of net generating capacity but remaining margin is negative in July-August period.

�PPC is the incumbent with >99% market share in retail and around 95% in the wholesale market. Currently, there are 3 independent units in the market but PPC has overtaken the operation of Heron’s 147 MW OCGT.

�Foreign players have entered the market since 2006, teaming up with local (non-operator) investors (Endesa-Mytilineos, Edison-ELPE, …). Mytilineos has replaced Iberdrola in the joint venture with Motor-Oil. GDF-Suez will cooperate with the Greek company Terna.

�The low demand scenario of HTSO predicts a 2,5% yearly growth rate in demand up to 2012. However, the economic slump could keep the growth rate for 2009-2010 around zero.

�Lignite will remain a cornerstone, though its share will decrease.

�All the new capacity up to 2012, at least, will be in CCGTs and perhaps some hundreds MW of OCGTs.

�Renewable generation is also set to rise as a very favorable framework has been put into place. Feed-in tariff for the energy and up to 40% subsidy for construction of wind and solar parks.

� Imports rise even though Bulgaria has closed two nuclear units. New nuclear capacity in Romania, high prices in Greece and new interconnection lines in region will keep that trend.

�Remaining capacity will be decreased in the next couple of years with few new capacity coming online.

�PPC is looking for strategic partners to finance new commissioning plan.

�Private players might concentrate.

18

Energy Market – Developments in 2009

� Total Power production during 1Q 2009: 12.1 m MWh (down 1.67% y-o-y).

� Net Imports amounted 1.1 m MWh (down 23.1% y-o-y).

� Hydro production was up 61.5% when on the contrary Natural Gas production decreased by 54% y-o-y.

� Aggregate demand is decreased by 3.8% mainly due to lower demand from the industrial sector (19%).

Capacity per Technology GW

10.9 10.911.6 12.1 12.4 12.7

13.8 13.9 14.114.6

15.3

0

2

4

6

8

10

12

14

16

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

Coal Oil Natural Gas Hydro Renewables

ENERGY - INDUSTRY & MACRO ENVIRONMENT

The Greek Electricity Market

Source: Endesa Hellas, HTSO.

4,0%p.a.

2,7%p.a.

10,000

15,000

20,000

25,000

30,000

35,000

40,000

45,000

50,000

55,000

60,000

2000 2002 2004 2006 2008 2010

Demand GWh

-1,000

1,000

3,000

5,000

7,000

9,000

11,000

13,000

Peak MW

Demand Peak

19

ENERGY - INDUSTRY OUTLOOK

The Greek Electricity Market

Source: Endesa Hellas.

1.772

738

1.034

2.500

3.000

5.502

2.108

Commissioning Decommissioning New Net CapacityPlanned

New Net CapacityPlanned

New Net CapacityNeeded

3.394

Projected (De)/Commissioning schedule for all players in Greece

Strategic Plan of PPC (November 2007)

GAP1.466-

1.966

2008 - 2010 2011 - 2020

40% of

current

system

Commissioning Decommissioning

MW

20

ENERGY – BUSINESS OUTLOOK

Endesa Hellas

• Mytilineos’ assets valued at Euro 600 mn.

• Endesa participates in Endesa Hellas through consecutive share capital increases already effected – to be finalized within November 2008.

Strategic Partnership Overview – a Euro 1.2 bn Company is Formed

Endesa

• Cash (€ 600 mn)

Mytilineos

• Assets (Valued at € 600 mn)

ENDESA HELLAS

• Endesa Hellas valued at € 1.2 bn, while enjoying significant financial firepower to fund its ambitious expansion programme.

Total Firing Power Total Firing Power €€ 3 3 bnbn

• The two parties have agreed to leverage the company 60:40 Debt/Equity – raising € 1.8 bn to invest in Greece and SE Europe territory (Albania, FYROM, Bulgaria, Turkey, Cyprus).

Source: Endesa Hellas.

21

CHP334 MW

CCGT444 MW

CCGT437 MW

GAS1,652 MW

RES

RES

RES

2008 2009 2010 2011 2012 2012

RES

RES

379 MW

406 MW

966 MW

1,417 MW

1,928 MW

Installed Generation

45 MW

27 MW

116 MW

14 MW

74 MWSt. Nicholas

Volos

Target GreekMarket Share

14%

RES276 MW

Power

MW

1,000

2,000

Korinthos

CCGT437 MW

1,928 MW

Endesa Hellas – Generation (2008 – 2012)

ENERGY - BUSINESS OUTLOOK

Source: Endesa Hellas.

22

Areas of Activity

EPC

23

**Source: EC/World Bank, GIS for SEE report, 2004-05.

•Tight supply – demand balance expected to continue despite new CCGT projects.

•Majority of existing capacity is old and inefficient.

•PPC Megalopolis 800MW CCGT – first part of PPC’smajor new-build program.

•EPC for continuation of Endesa Hellas’ investment program: 400MW IPP plant in Volos.

Fundamentals Prospects

•SEE: 11,000 MW new capacity needed up to 2020. Rehabilitation of 11,500 MW of existing generation - €4.8bn**

•Turkey: major investments in gas and indigenous coal plants.

•EU membership and convergence impose obligations for plant upgrades and/or closures whilst power consumption increasing.

•Years of near zero investment.

•Government support and relatively high level of acceptance for nuclear.

Greece

South-East

& Central

Europe,

Turkey

•Combined cycle projects across the Middle East.

•Numerous Integrated Water & Power Plant (IWPP) projects in the Gulf.

•Emphasis on mega-projects in the Gulf, several affected by global financial crisis.

•Gas for power generation becoming scarce –increased need for fuel efficiency.

Middle East

•Pakistan: multiple IPP projects under development.

•Despite global economic slow-down there is continued power demand growth in developing countries.

•Power shortages common.

•Massive need for energy infrastructure investments, often on fast-track basis.

Developing

Countries

EPC - INDUSTRY & MACRO ENVIRONMENT

24

EPC – INDUSTRY OUTLOOK

Source: Credit Suisse.

• Economic downturn impacts investment plans. Spending has only marginally

deteriorated.

• Evidence that interest on coal powered generation equipment retreats and a

shift is noticed towards natural gas and clean power technologies.

• The priorities set by the various fiscal spending programs around the globe are

expected to play an important role in the coming future.

Investments Plans over 2009

Credit Suisse Global Infrastructure Survey on investment plans evolution covering 300 Utilities globally.

25

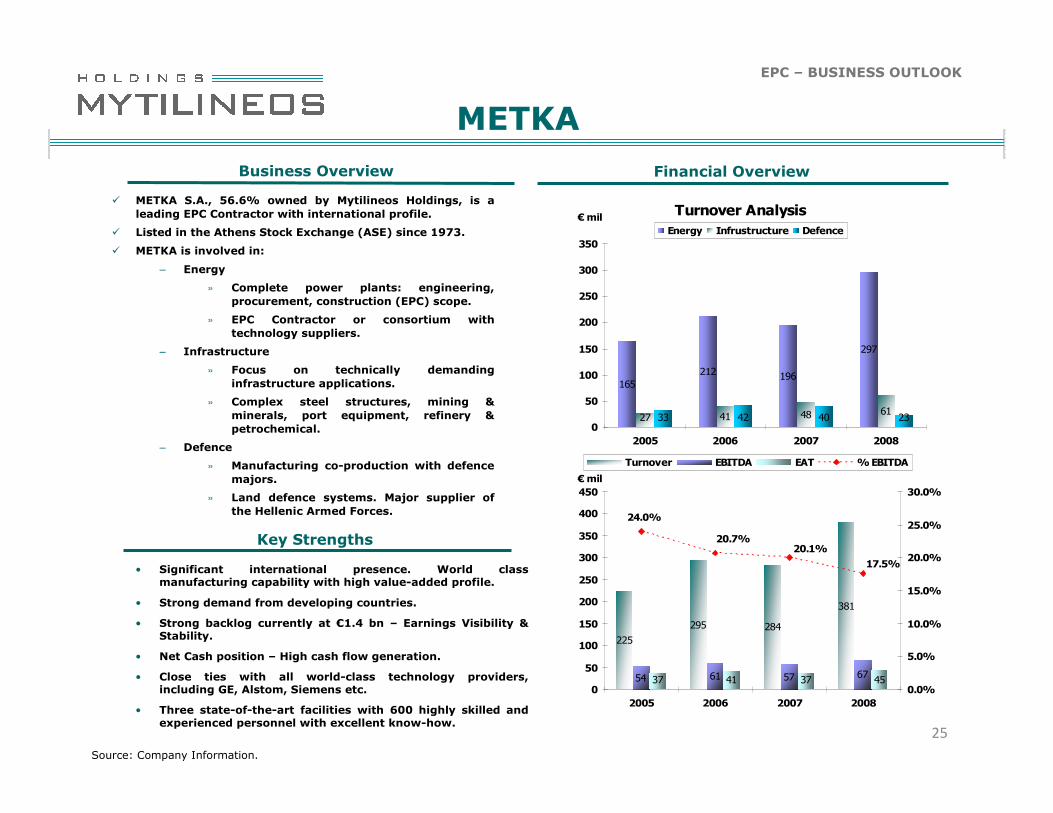

EPC – BUSINESS OUTLOOK

METKA

Business Overview Financial Overview

Key Strengths

• Significant international presence. World class manufacturing capability with high value-added profile.

• Strong demand from developing countries.

• Strong backlog currently at €1.4 bn – Earnings Visibility & Stability.

• Net Cash position – High cash flow generation.

• Close ties with all world-class technology providers, including GE, Alstom, Siemens etc.

• Three state-of-the-art facilities with 600 highly skilled and experienced personnel with excellent know-how.

Source: Company Information.

Turnover Analysis

212 196

297

48 6133 42 40 23

165

27 410

50

100

150

200

250

300

350

2005 2006 2007 2008

€ mil

Energy Infrustructure Defence

284

381

57 6737 41 37 45

295

225

6154

20.1%

24.0%

20.7%

17.5%

0

50

100

150

200

250

300

350

400

450

2005 2006 2007 2008

€ mil

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

Turnover EBITDA EAT % EBITDA

� METKA S.A., 56.6% owned by Mytilineos Holdings, is a

leading EPC Contractor with international profile.

� Listed in the Athens Stock Exchange (ASE) since 1973.

� METKA is involved in:

– Energy

» Complete power plants: engineering,

procurement, construction (EPC) scope.

» EPC Contractor or consortium with

technology suppliers.

– Infrastructure

» Focus on technically demanding

infrastructure applications.

» Complex steel structures, mining &

minerals, port equipment, refinery &

petrochemical.

– Defence

» Manufacturing co-production with defence

majors.

» Land defence systems. Major supplier of

the Hellenic Armed Forces.

26

PROJECTS

ABROAD

60%

PPC

11%

ENDESA HELLAS

25%

OTHER

4%

EPC - BACKLOG

Source: Company Information.

�Strong Backlog – Visibility – International Profile

� PPC: 417 MW in Aliveri, Natural Gas Fired combined cycle. Alstom

sub supplier for the main equipment. Contract value of €219 m.

� ENDESA HELLAS : 444 MW in Ag. Nikolaos, Natural Gas Fired

combined cycle. GE sub supplier for the main equipment. Contract

value of €232 m.

� OMV PETROM: 860 MW in Romania, Natural Gas fired. 50-50

Consortium with GE. Contract value of €210 m.

� PEEGT: 700 MW in Syria, Natural Gas fired. METKA leader of

Consortium with Ansaldo. Contract value of €650 m (contract

award).

� KORINTHOS POWER: 437 MW in Ag. Theodoroi, Natural Gas Fired

combined cycle. GE sub supplier for the main

equipment. Contract value of €285.

€1.4 bn

Backlog - Sales Evolution

230

605

1,460

284381

165 212 196 297

450295

225

0

200

400

600

800

1,000

1,200

1,400

1,600

2005 2006 2007 2008

€ mil

Backlog Evolution Group Sales of which EPC Sales

27

Stock Data

28

0.02 0.03 0.070.14

0.21

0.51

0.10

2002 2003 2004 2005 2006 2007 2008

Dividend

STOCK DATA – MYTILINEOS HOLDINGS S.A.

Share Price Information

� Market Cap: € 695 mn

� Avg. Trading Value: € 1.9 mn

� Total No of shares: 116,984,338

� Free Float: 61%

� Listing FTSE/ASE 20 FTSE INTERNATIONAL, MSCI Small Cap and HSBC Small Cap

Notes: Data as of 22 June 2009.

Source: Company Information.

Stock Symbols

� ASE: MYTIL

� Reuters: MYTr.AT

� Bloomberg: MYTIL GA

Shareholder Structure

Dividend Per Share (€)

Dividend Distribution Table

Mytilineos

Family 30.3% Retail 32.9%

Greek Institutional

Investors 12.8%

Foreign Institutional

Investors 15.1%

Treasury

Stock 8.9%

(€ mn) 2003 2004 2005 2006 2007 2008

Profit After Taxes 10.308 14.399 44.834 52.632 161.073 21.592

Total Dividend 4.052 8.104 16.208 24.312 59.662 11.698

Dividend Payout % 39.3% 56.3% 36.2% 46.2% 37.0% 54.2%

29

0.16 0.160.20

0.30

1.35

0.40

0.50

0.40

2002 2003 2004 2005 2006 2007 2008

Dividend

STOCK DATA – METKA S.A.

Share Price Information

� Market Cap: € 421 mn

� Avg. Trading Value: € 0.5 mn

� Total No of shares: 51,950,600

� Free Float: 43.4%

� Listing FTSE/ASE Mid-40,FTSEINTERNATIONAL,

MSCI Small Cap

and HSBC Small Cap

Stock Symbols

� ASE: METK

� Reuters: MTKr.AT

� Bloomberg: METTK GA

Shareholder Structure

Dividend Per Share (€)

Dividend Distribution Table

Mytilineos Holdings

56.6%

Retail 12.3%

Greek Institutional Investors 13.4%

Foreign Institutional Investors 17.7%

Notes: Data as of 22 June 2009.

Source: Company Information.

Capital Return

(€ mn) 2003 2004 2005 2006 2007 2008

Profit After Taxes 11.202 16.371 34.339 40.764 37.288 44.785

Total Dividend 8.312 10.390 15.585 20.780 25.975 20.780

Dividend Payout % 74.2% 63.5% 45.4% 51.0% 69.7% 46.4%

30

Summary

31

STRATEGY

Awards and recognition for community safety and environment. Very valuable operating assets.

Explore investment opportunities in SE Europe, North Africa, Middle East through organic growth and/or acquisitions in all sectors of activity.

GrowthOptions

Project Pipeline

Fianancial Strength and Discipline

Significant Assets

Licence to Operate

People

3,000 employees, operations and project contractors.

EBITDA margins around 12% and EBITDA over € 110 mil.

Source: Company Information.

Strategic Focus

• Bauxite Residue Treatment Facility.

• Aluminum Wagstaf -Enhancement of the Final Product.

• CAPEX in the Energy Sector over € 1bn within the next 3 years.

• Largest vertical integrated Alumina and Aluminum producer in SE Europe.

• CHP Plant 334MW.• RES 45 MW.• 444 MW / 437 MW CCGT’s (under construction).

• World – class manufacturing capabilities in EPC.

32

SUMMARY

� With a well balanced business portfolio the Group is well placed:

� To benefit from the imminent liberalization of the domestic energy market.

� To benefit from the massive need for energy infrastructure investments in the wider

SE Europe region.

� Good organic growth potential in all areas of activities to maintain strong cash

flows and support future CAPEX.

� Attractive Debt/Equity ratio to support further expansion.

� The company has issued a bond loan up to €465 mil. in order to secure adequate

funding requirements necessary for executing its demanding development plan.

� Strong Cash flows supported significantly by the effective risk management

strategy.

� Growth projects are gathering momentum and remain largely on track.

� Attractive dividend policy.

� Successful management’s track record in value creation through a series of value

enhancing deals.

Investment Highlights

Source: Company Information.

33

CONTACT INFORMATION

Nikos KontosGroup Investor Relations OfficerEmail: [email protected]: +30-210-6877395Fax: +30-210-6877400

Mytilineos Holdings S.A.5-7 Patroklou Str.15125 MaroussiAthensGreeceTel: +30-210-6877300Fax: +30-210-6877400

www.mytilineos.grwww.metka.gr

Dimitris KatralisFinancial AnalystEmail:[email protected]: +30-210-6877476Fax: +30-210-6877400

Mytilineos Holdings S.A.5-7 Patroklou Str.15125 MaroussiAthensGreeceTel: +30-210-6877300Fax: +30-210-6877400

www.mytilineos.grwww.metka.gr