21

1 Presentation on Annual Results Analyst Meet May 2014

| Date post: | 21-Mar-2018 |

| Category: |

Documents |

| Upload: | trinhhuong |

| View: | 217 times |

| Download: | 4 times |

1

Presentation on Annual Results

Analyst Meet

May 2014

2

Agenda

Key Themes

Performance Highlights

Key Operating Highlights

Operating Performance Review

Financial Review

3

Key Themes for 2013-14

Brands and products • Various re-launches in the year.

• 13% increase in A&P cost over prior year .

Incubation of businesses for the future • Tata Starbuck – now 46 stores, store profitability robust.

• Nourishco – improved sales backed by growing distribution network

• Mid size acquisition in Australia in the coffee category, post year end

Geographies • Our Super Premium blend - Tea Pigs now in USA, Canada

and Australia

• Czech Republic – Turns profitable.

• France – brand turnaround. Increase in market shares on MAT basis

Route to market development • Broker Model Restructure

• Build competitive advantage and social capital in rural India.

4

6000

6200

6400

6600

6800

7000

7200

7400

7600

7800

2014 2013 2012

7738

7351

6640

Performance Highlights for the year – Operating Income

5

0

50

100

150

200

250

300

350

400

450

500

2014 2013 2012

481

373 356

Performance Highlights for the year – Group

Net Profits

6

Key Operating Highlights

1. India - tea : continuing strong branded tea top line performance.

2. India – Iconic Power of 49 campaign integrating brand messaging with social cause.

3. India – coffee : good performance by plantations.

4. Australia : Significant bottom-line improvement continues

5. USA Coffee: Significant growth in PODs. Sales of bags impacted on structural shift to Pods.

6. India : “Starbucks – a Tata Alliance” expands to 46 stores till date.

7. UK – continued strong performance by Tea Pigs. UK market impacted by tough trading environment.

8. Strong Performance in some European countries. Czech Republic turns profitable.

9. Water Vertical shows excellent growth

10. Cost interventions results in significant savings

11. Sri Lankan brands, Zesta and Watawala Kahata performed well

7

Operating Performance Review – South Asia

15% Top line growth across the portfolio with volume and value

increases.

Maintained market volume and value leadership at 20.1% and

22.3% respectively.

Tata Tea Gold restaged with primary TV campaign – Tata Tea

Gold Power of 49 campaign and IIFA integration.

• Iconic Power of 49 campaign integrating brand messaging

with social cause.

Chakra Gold and Kanan Devan restage in Q4.

Tetley Green tea re-launched in January with an impactful

campaign with Kareena Kapoor.

Various consumer promotions were undertaken to drive sales

growth. Competition has launched aggressive promotions.

8

Operating Performance Review – CAA

Canada

• A massive integrated promotion between Cirque du Soleil and Tetley has run over Q4. Top line improves.

• Tassimo/ Kraft – Tetley Pods make good progress.

• Tetley 100% steamed green teas (pure, lemon and ginger) launched and gaining distribution

USA

• EOC K-Cups (with Keurig) – Volumes continue to grow. Significant improvement in market shares.

• K Cup launch recognised as one of the most successful beverages launches according to IRI’s 2013 “New Product Pacesetters” list.

• Tetley launched a new Black & Green tea product in a snap-top box that is unique to the USA market.

• Good Earth tea re-launched with a new pack design continue to get press coverage

Australia

• Profitability continues to remain robust.

• Tetley’s new pyramid range and Tetley Greens with the launch of steamed green doing well.

• Mid Size Acquisition of MAP brand, a player in the POD’s category has been completed post year end.

9

Operating Performance Review – EMEA

Europe/United Kingdom /Middle East and Africa

• In UK - Overall tea category has declined by single digits on a MAT basis.

• Market leadership in Redbush tea maintained despite increased pressure.

• New Tetley advertisement using the iconic Teafolk was aired during Q4 with 360 degree support.

• 4 new flavoured green teas launched in March in UK.

• Tea Pigs topline grows by a handsome % - reflecting significant growth in all channels.

• Tea pigs in already present in US, Australia and Canada.

• Sales improvement in Joekels continue, post new acquisition in the private label market.

• France continues on its path of significant growth and brand share recovery mode.

• Pilot launch in Kuwait successful with Tetley reaching No 2 in value share.

• Czech Republic turns profitable with price increases, cost reduction. Short TV Campaign with retailer further boosts sales.

10

Operating Performance Review – Other Branded

Business

Other Branded Business

• Significant improvement in water business.

• Himalayan sales continue to grow with increase in key accounts.

• Grape and Apple Cinnamon variants were launched during the year under Tata Gluco Plus

• Tata Starbucks –Now has 46 stores between Mumbai, Delhi, Bangalore and Pune. Store profitability continues to be robust.

• Tata Starbucks celebrates its first year in India with launch of India Estates Blend developed exclusively with Tata Coffee

11

Non Branded Business

• Tata Coffee plantations record a good year. Pepper registers excellent results.

• Tea plantations - KDHP and APPL register significant profit increases led by higher crop, productivity and better tea prices

• India and US instant tea operation stable

• China instant tea operation – Sales effort remains the key

Operating Performance Review Non branded

businesses

12

Other Key Highlights

Accolades and Awards

• Tetley Factory in Eaglescliff featured in the Manufacturers Magazine , UK.

• Watawala Plantations were given best presented Annual report awards under the agriculture sector category.

• Tata Coffee recognised at the first ever Tata Engage workshop and won the award for “highest contribution to the experience hub” in the midsize company subcategory.

• Product of the Year 2014 - 100% Steamed Green Tea Pyramid Infusers (Australia)

• Tetley UK recent won the grocer award for a new product launch – Tetley Blend of Both

13

Sustainability initiatives

13

Other Key Highlights

Ethical Sourcing

• Tea Board launched Trustea : the India Sustainable Tea Code with TGBL & HUL.

• Tetley RA certified tea crosses 50% volumes.

• KDHP & Watawala also receive RA certification for all sites.

CLIMATE CHANGE

• TGB ranked 1st in the Consumer Staples sector/ 6th overall in Carbon Disclosure Leadership Index (CDLI – 2013.

• Climate change strategy focus on energy efficiency, renewable energy, sustainable agriculture and sustainable forestry

WATER MANAGEN

T

• Water Champions Workshop with TQMS and Water Footprint Network Netherlands trainee 20 participants.

• Water footprint initiated and future objective to co-create TGBL’s water response strategy.

COMMUNICTY WORK

• World Environment Day on the June 5th 2013 in the organization across over 70 units.

• Tata Volunteering Week organized volunteering activity with Unnati.

• Improvement in Affirmative Action assessment scores and promotion to next band.

• Swastha students win 3 medals at Special Asia Pacific Games in Australia.

14

Analyst Meet

Financial Review

15

15

Financial Highlights for the year

Operating income growth understated due to revenue model for pods and

restructuring.

Good performance in South Asia and Coffee Plantation Businesses.

Difficult market environment in eastern Europe and some developed markets.

Additional capacity in instant coffee plant in India.

Investment in new businesses progressing well

Cost savings initiatives on track

Lower Operating EBIT also reflect

• Significantly higher A&P spend

• Investment in new initiatives

Higher exceptional items increases Consolidated Group Net profit for the year.

16

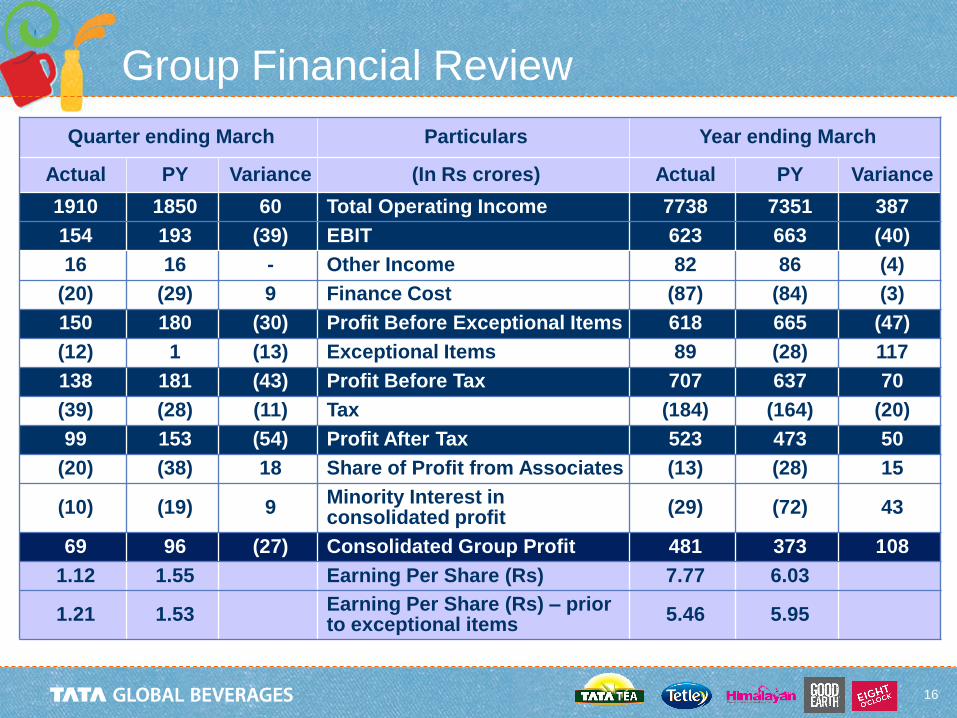

Group Financial Review

Quarter ending March Particulars Year ending March

Actual PY Variance (In Rs crores) Actual PY Variance

1910 1850 60 Total Operating Income 7738 7351 387

154 193 (39) EBIT 623 663 (40)

16 16 - Other Income 82 86 (4)

(20) (29) 9 Finance Cost (87) (84) (3)

150 180 (30) Profit Before Exceptional Items 618 665 (47)

(12) 1 (13) Exceptional Items 89 (28) 117

138 181 (43) Profit Before Tax 707 637 70

(39) (28) (11) Tax (184) (164) (20)

99 153 (54) Profit After Tax 523 473 50

(20) (38) 18 Share of Profit from Associates (13) (28) 15

(10) (19) 9 Minority Interest in consolidated profit

(29) (72) 43

69 96 (27) Consolidated Group Profit 481 373 108

1.12 1.55 Earning Per Share (Rs) 7.77 6.03

1.21 1.53 Earning Per Share (Rs) – prior to exceptional items

5.46 5.95

17

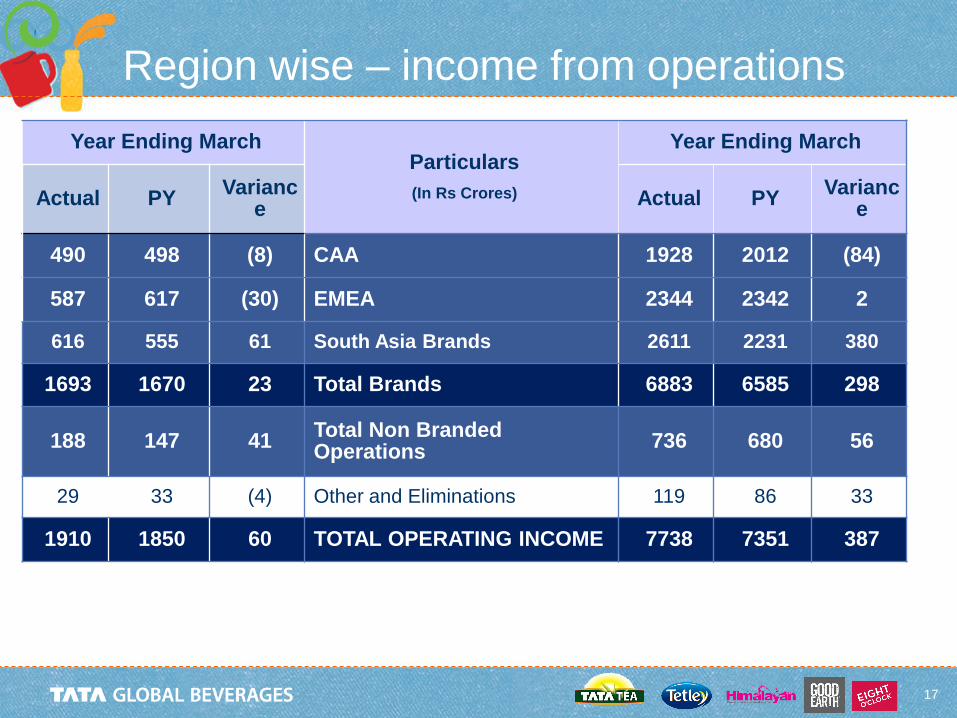

Year Ending March Particulars

(In Rs Crores)

Year Ending March

Actual PY Varianc

e Actual PY

Variance

490 498 (8) CAA 1928 2012 (84)

587 617 (30) EMEA 2344 2342 2

616 555 61 South Asia Brands 2611 2231 380

1693 1670 23 Total Brands 6883 6585 298

188 147 41 Total Non Branded Operations

736 680 56

29 33 (4) Other and Eliminations 119 86 33

1910 1850 60 TOTAL OPERATING INCOME 7738 7351 387

Region wise – income from operations

18

Balance Sheet Particulars

(In Rs Crores)

March 2014 March 2013

SOURCES OF FUNDS

Shareholder’s Funds 6773 5624

Borrowings 1438 1390

Non Current Liabilities 345 349

Current Liabilities 1355 1431

TOTAL 9911 8794

APPLICATION OF FUNDS

Fixed Assets:

Goodwill 4188 3598

Others Fixed Assets 1052 926

Investments 611 578

Cash & Other Deposits 1474 1364

Non Current Assets 131 59

Current Assets 2455 2269

TOTAL 9911 8794

19

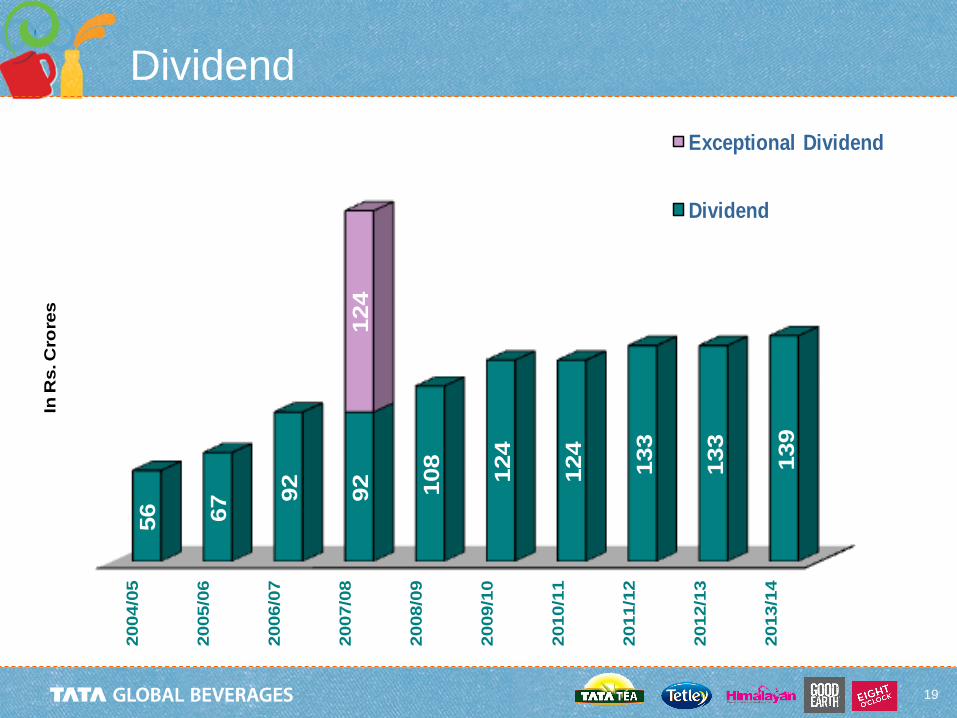

Dividend

2004/0

5

2005/0

6

2006/0

7

2007/0

8

2008/0

9

2009/1

0

2010/1

1

2011/1

2

2012/1

3

2013/1

4

56 67 9

2

92 108

124

124

133

133

139

124

In R

s. C

rore

s

Exceptional Dividend

Dividend

THANK YOU 20

21