19

Presentation on Remittance & Cash Management Banking Day 2006

| Date post: | 28-Dec-2015 |

| Category: |

Documents |

| Upload: | esmond-crawford |

| View: | 219 times |

| Download: | 0 times |

Presentation on Remittance & Cash Management

Banking Day 2006

Agenda

Inward Remittance

Cash Management

Q&A

Business Challenges

Market Today

About CashTech

Transactional Complexities

Segmentation

ComplexityVolumes

Transaction

Corporate Treasury View

Corporate Size

Large Corporate

Small Businesses

Global Corporation

Medium-Size Businesses

Treasury Management FunctionsLiquidityTransactions Information Risk

Payments clearing & settlement

Payments clearing & settlement, electronic banking, Sweeping

Payments clearing & settlement, electronic banking, Pooling & LM, Supply Chain support

Payments clearing & settlement, electronic banking, Netting, Pooling & LM, Supply Chain Support, FX and Interest risk monitoring

Value

High

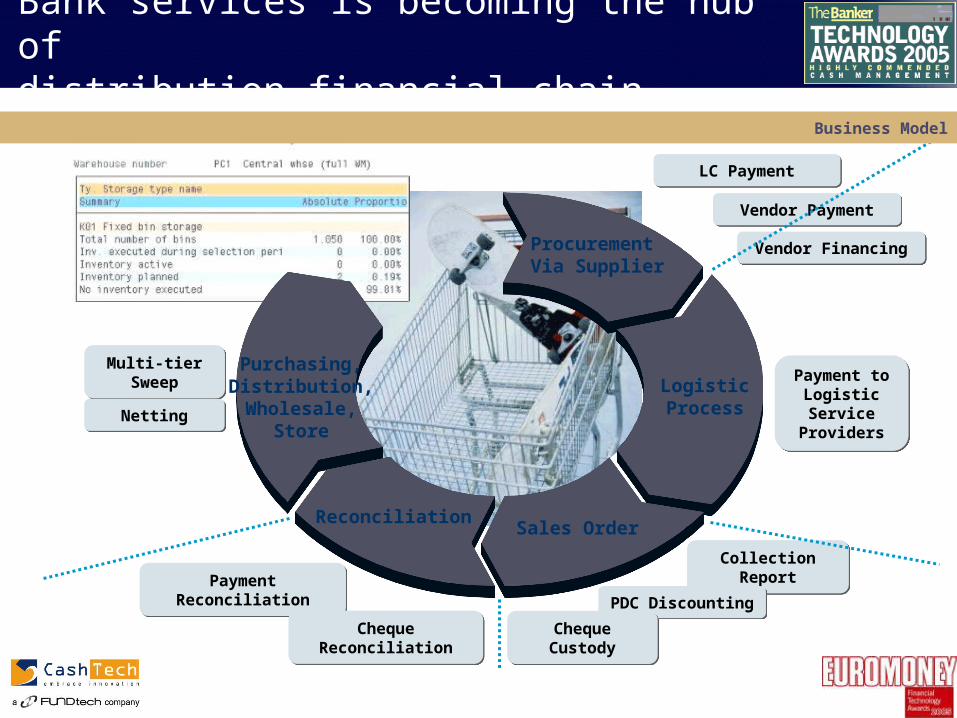

Bank services is becoming the hub of distribution financial chain

Payment ReconciliationPayment Reconciliation

Multi-tier Sweep

Multi-tier Sweep

NettingNetting

ProcurementVia Supplier

LC PaymentLC Payment

Vendor PaymentVendor Payment

Payment to Logistic Service

Providers

Payment to Logistic Service

Providers

Collection ReportCollection Report

Purchasing,Distribution,Wholesale,

Store

ReconciliationSales Order

LogisticProcess

PDC DiscountingPDC Discounting

Cheque CustodyCheque CustodyCheque ReconciliationCheque Reconciliation

Vendor FinancingVendor Financing

Business Model

Agenda

Inward Remittance

Cash Management

Q&A

Business Challenges

Market Today

About CashTech

Current Business Challenges

How do I distinguish my bank’s

offering

How do I increase

fee based revenue and

improve float management

How do I increase

fee based revenue and

improve float management

How can I provide better

solution to provide

customer profitability,

acquisition &

retention

How can I provide better

solution to provide

customer profitability,

acquisition &

retention

How do I compete

with multinational banks and

Domestic banksHow do I c

ompete

with multinational banks and

Domestic banks

How do I leverage existing systems to launch new products

How do I leverage existing systems to launch new products

How do I respond to customized corporate

requirements

How do I respond to customized corporate

requirements

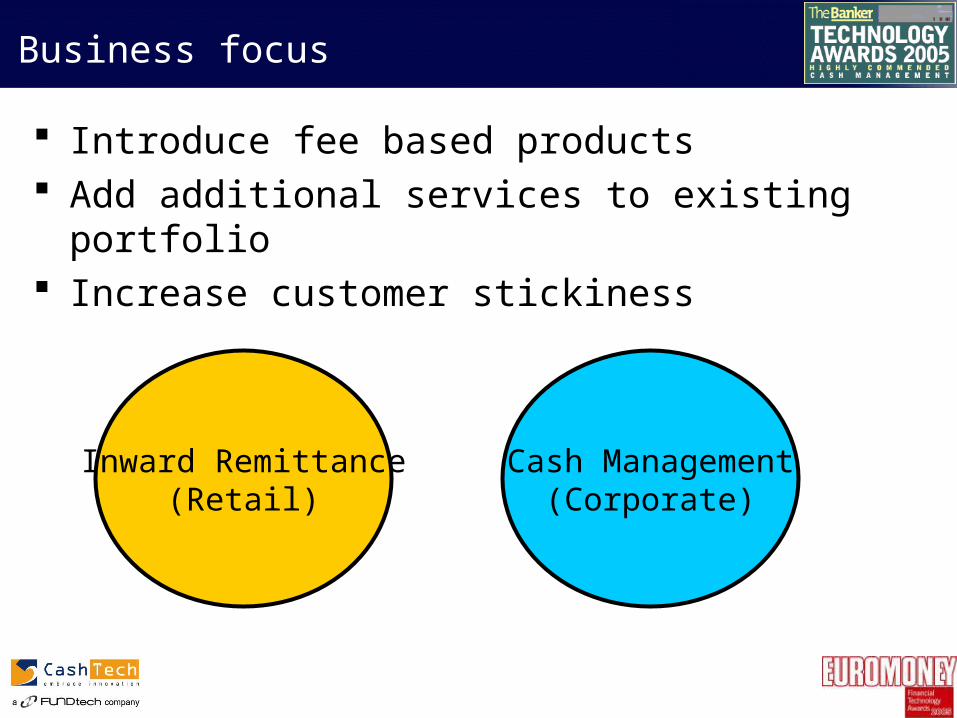

Business focus

Introduce fee based products Add additional services to existing portfolio Increase customer stickiness

Inward Remittance(Retail)

Cash Management(Corporate)

Agenda

Inward Remittance

Cash Management

Q&A

Business Challenges

Market Today

About CashTech

Why Inward Remittance

The market– 3 million Vietnamese working abroad who send money regularly back

into Vietnam– Approx USD 3 billion worth of inward remittances in 2004.

The revenue– Fee Based Revenue

Anywhere between USD 5-10 per transaction

– F/X Spread Earnings Anywhere between 120-200 basis points

– Float Earnings – Revenue from cross selling banks products:

House Loan for the remitter Fixed deposit for remitters savings, etc.

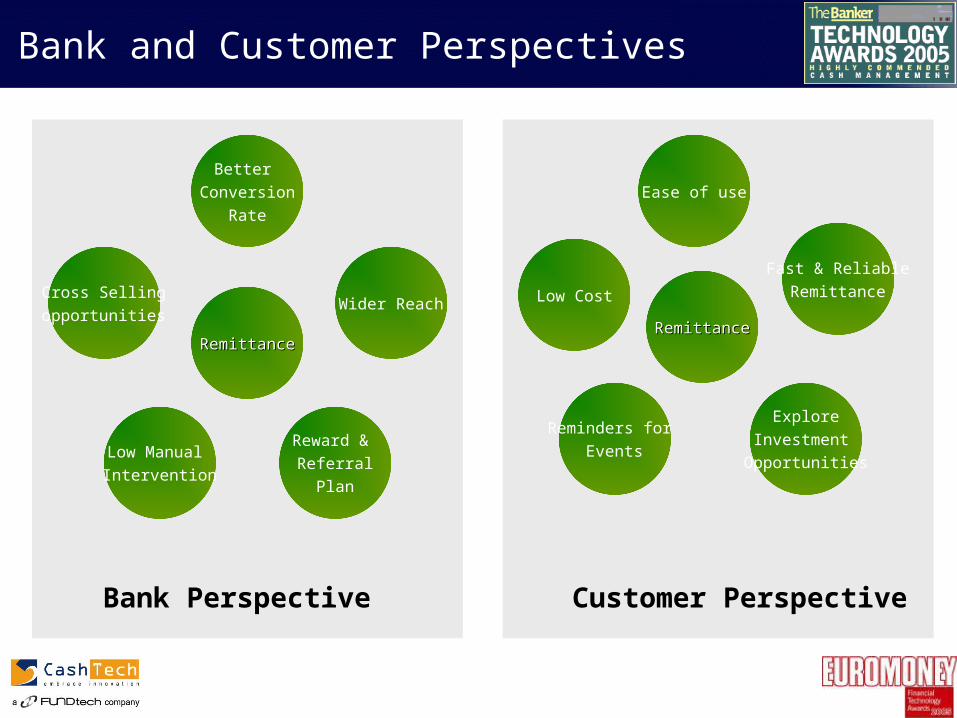

Bank and Customer Perspectives

Cross Selling

opportunities

Low Manual

Intervention

Reward &

Referral

Plan

Wider Reach

Better

Conversion

Rate

RemittanceRemittance

Reminders for

Events

Explore

Investment

Opportunities

Fast & Reliable

Remittance

Ease of use

RemittanceRemittance

Bank Perspective Customer Perspective

Low Cost

Agenda

Inward Remittance

Cash Management

Q&A

Business Challenges

Market Today

About CashTech

Why Cash Management

Traditional lending relationships are becoming more demanding

Management of Fee based and control of float based income is a necessity

Cash Management has been a flagship offering of MNC banks and Vietnamese banks should capitalize on their distribution network

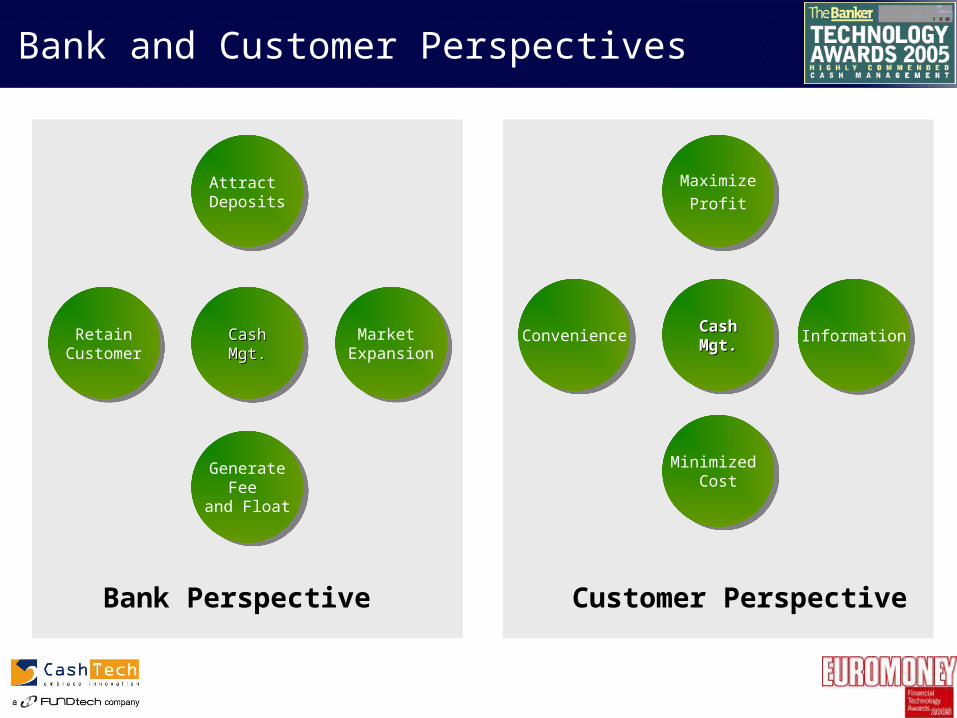

Bank and Customer Perspectives

RetainCustomer

RetainCustomer

GenerateFee

and Float

GenerateFee

and Float

Market Expansion

Market Expansion

Attract Deposits

Attract Deposits

CashCashMgt.Mgt.

CashCashMgt.Mgt.

ConvenienceConvenience

Minimized Cost

Minimized Cost

InformationInformation

Maximize

Profit

Maximize

Profit

CashCashMgt.Mgt.

CashCashMgt.Mgt.

Bank Perspective Customer Perspective

Agenda

Inward Remittance

Cash Management

Q&A

Business Challenges

Market Today

About CashTech

CashTech Fact Sheet

More than 700 banks as customers, with over 150 sites on Cash Management

Customers include HSBC, Deutsche Bank, Citi, BNP Paribas, ABN Amro Bank, Kasikorn, Maybank……

Cash Management expertise spanning over a decade

Local expertise with implementations at large local banks in the region

Europe45%

US50%

650 Full Time Employees

SupportSupportSG&ASG&A

ServicesServices TechnologyTechnology

180

5585

240

SupportSupportSG&ASG&A

ServicesServices TechnologyTechnology

180

5585

240

SupportSupportSG&ASG&A

ServicesServices TechnologyTechnology

180

5585

240

Geography – 12 locations, 4 continents

BostonNew Jersey

Atlanta

San Francisco

London

Australia

Zurich / Geneva

Pune

Singapore

Tokyo

Geography – 12 locations, 4 continents

BostonNew Jersey

Atlanta

San Francisco

London

Australia

Zurich / Geneva

Pune

Singapore

Tokyo

Geography – 12 locations, 4 continents

BostonNew Jersey

Atlanta

San Francisco

London

Australia

Zurich / Geneva

Pune

Singapore

Tokyo

Tel Aviv

Revenue

$ 39.8 m

$47.6 m

$58.5 m

$74.0 M.

0

$10m

$20m

$30m

$40m

$50m

$60m

$70m

2002 2003 2004 2005

CashTech 230+ FTE

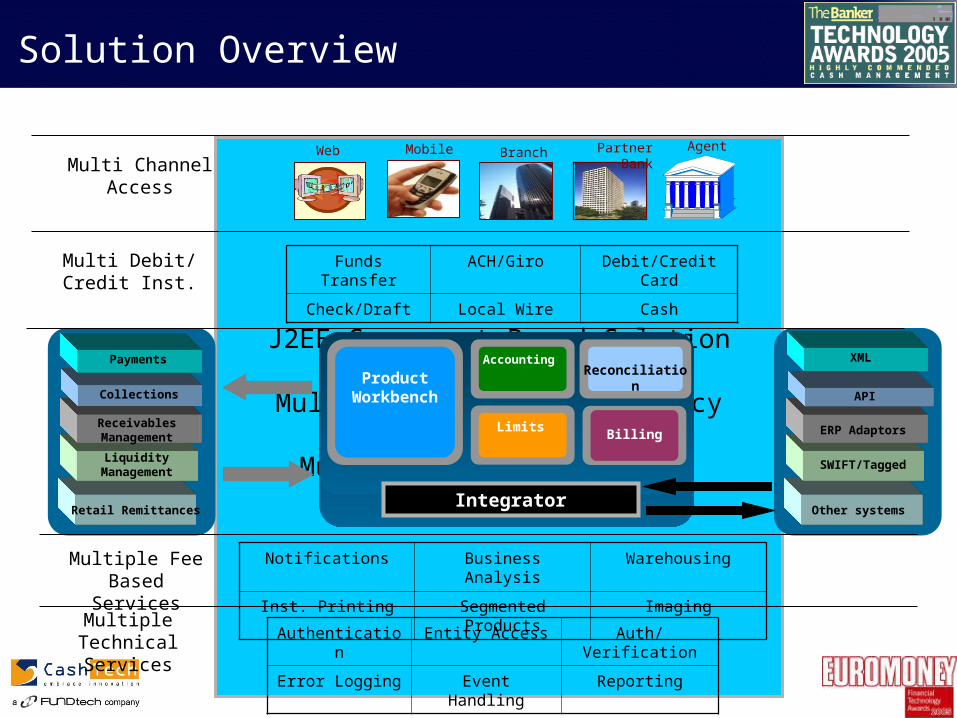

J2EE Component Based Solution

Multi-Lingual Multi-Currency

Multi-Bank Multi Entity

Solution Overview

Authentication Entity Access Auth/Verification

Error Logging Event Handling Reporting

Funds Transfer ACH/Giro Debit/Credit Card

Check/Draft Local Wire Cash

Integrator

Billing

ReconciliationAccounting

Product Workbench

Limits

Retail Remittances

Liquidity Management

Receivables Management

Collections

Payments

Other systems

SWIFT/Tagged

ERP Adaptors

API

XML

Web Partner BankBranch AgentMobileMulti Channel

Access

Multi Debit/ Credit Inst.

Multiple Technical Services

Multiple Fee Based Services

Notifications Business Analysis Warehousing

Inst. Printing Segmented Products Imaging

Credentials

Rated by the Tower Group as the “Leading Cash Management

Solution provider in the Asia Pacific”

As per Celent “Strong Player in

Asia Pacific”

Meridian Research says “Leading vendor with

Asian experience”

JPMorgan Internet Based Cash

Management 2001 “Customizable Screen,

Workflow, and multi currency product

Support”Bank Technology Report: 10 to Watch!

“100% J2EE, ability to differentiate Bank’s

offerings from the rivals”

Euromoney 2005 Rates CashTech as the best cash

management solution provider

globally

Bank Technology 2005 Award

Thank you

Your questions…..