Stepsto Develop AuditObjectives Understandsobjectivesand responsibilitiesforthe audit Divide financial statem ents into cycles Know m anagem entassertions aboutfinancial statem ents Know general auditobjectives forclassesoftransactions, accounts, and disclousers Know specificauditobjectives forclassesoftransactions, accountsand disclousers

Transcript

Steps to Develop Audit Objectives

Understands objectives and responsibilities for the audit

Divide financial statements into cycles

Know management assertions about financial statements

Know general audit objectives for classes of transactions, accounts, and disclousers

Know specific audit objectives for classes of transactions, accounts and disclousers

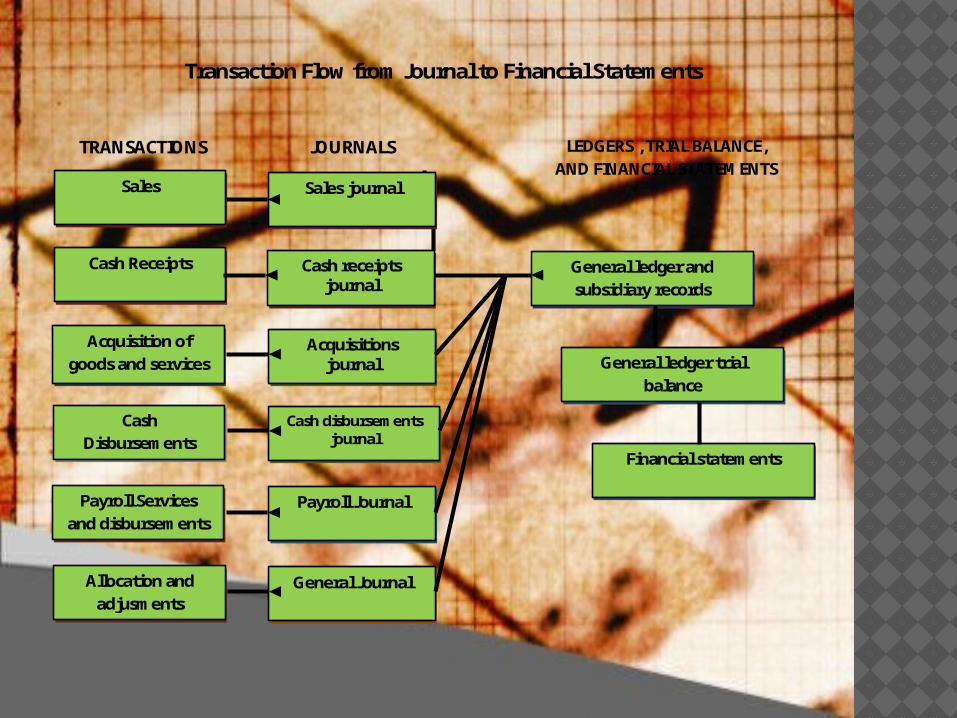

Transaction Flow from Journal to Financial Statements

Allocation and adjusments

Sales

Cash Receipts

Cash Disbursements

Payroll Services and disbursements

Acquisition of goods and services

TRANSACTIONS

Sales journal

Cash receipts journal

Acquisitions journal

Cash disbursements journal

Payroll Journal

General Journal

General ledger and subsidiary records

General ledger trial balance

Financial statements

JOURNALS LEDGERS , TRIAL BALANCE, AND FINANCIAL STATEMENTS

Balance Sheet Income StatementSales Journal Cash In bank Advertising s

Cash disbursement journal Inventories Travel and entertainment s

General Journal Prepaid expenses Sales meetings and training s

Land Miscellaneous sales expense s

Building Sales and promotial literature s

Computer and other equipment Travel and entertainment A

Furniture and fixtures Stationery and supplies A

Accumulated despreciation Postage A

Trade accounts payable Telephone and fax A

Other accrued payables Computer maintence and supplies A

Accrued income tax Depreciation A

Deferred tax Rent A

Legal fees and retainers A

Auditing and related services A

Insurerance A

Offi ce repairs and maintenace expense A

Expense A

Miscellaneous offi ce expense A

Miscellaneous general expense A

Gain on sale of assetsIncome taxes

Payroll Payroll journal Cash in bank Salaries and commisions S

and personnel General journal Accrued payroll Sales payroll taxes S

Accrued payroll taxes Executive and offi ce salaries A

Adminastrative payroll taxes A

Inventory Acquisitions journal Inventories cost of goods soldand warehousing Sales journalCapital Acquisition Acquisition journal Cash in bank Interest expenseand repayment Cash disbursements journal Nites payable

General journal Long-term notes payableAccrued interestCapital stockcapital in excess of par valueRetained earningsDevidensDevidens payable

General Ledger Accounts Included in the Cycle (See Figure 6-4)Journals Included in the Cycle (See Figure 6-3, p.

170)CycleSales and Colection

Cycles Applied to Hillsburg Hardware Co.

Relationships Among Transaction Cycles

General cash

Sales and collection cycle

Acquisition and payment cycle

Payroll and personel cycle

Capital acquisition and repayment cycle

Inventory and warehousing cycle

Four Phase of a Financial Statement Audit

Phase l Plan and design an audit approach

Phase ll

Phase lll

Phase lV

Perform tests of controls and substantive tests of transactions

Perform analytical procedures and tests of details of balance

Complete the audit and issue an audit report

Relationships Among Auditing Standards, Types of Evidence, and the Four Audit Evidence Decisions

Broad guidelines concerning auditor qualifications and

conduct, evidence, accumulation, and reporting

Auditing standards

Qualifications and conduct

Evidence accumulation

Sample size and items to select

Reporting

Types of evidence

Audit procedures

Broad categories of evidence available for the

auditor’s accumulation

Specific instructions for the accumulation of types

of evidence

Timing of tests

FOUR AUDIT EVIDENCE DECISIONS

Physical examination confirmation

documentation analytical procedures

inquiries of client recalculation

reperformance observation

Information Source

AssetsCash In bank BankMarketable securities Investment custodianAccounts receivable CustomerNotes receivable MakerOwned inventory out on consignment ConsigneeInventory held in public warehouses Public warehouseCash surrender value of life insurance Insurance company

Owners EquityShares outstanding Registar and transfer agent

Other InformationInsurance coverage Insurance companyContingent liabilities Bank, lender, and client's legal counselbond indenture agreements BondholderCollateral held by creditors Creditor

Information Often Confirmed

Term and Definition Illustrative Audit Procedure Type of Evidence

Documentation

Analytical procedures

Documentation

Analytical procedures

Recalculation

Recalculation

Documentation

Reperformance

Documentation.

Physical examination

Observation

Inquiries of client

Documentation

Compute inventory turnover ratios and compare with those of previous years as a test of inventory obsolescence.

Recompute -A calculation done to determine whetever a client's calculation is correct.

Recompute the unit sales price times the number of units for a sample of duplicate sales invoices and compare the totals with the calculations.

Read the minutes of a board of directors meeting and summarize all information that is pertinent to the financial statements in an audit file.

Read -An examination of written information to determaine facts pertinent to the audit.

Trace postings from the sales journal to the general ledger accounts.

Observe- The act of observation should be associated with the type of evidence defined as observation.

Inquire-The act of inquiry should be associated with the type of evidence defined as inquiry.

Inquire of management whetever there is any obsolete inventory on hand at the balance sheet date.

Foot the sales journal for a 1-month period and compare all totals with the general ledger.

Examine-A reasonably detailed study of a document or record to determine specific facts about it.

Examine a sample of vendor's inboices to determine whetever the goods or services received are reasonable and of the type normally used by the client's business.

Scan-A less-detailed examination of a document or record to determine whetever there is something unusual warranting further investigation.

Scan the sales journal, looking for large and unusual transactions.

Foot -Addition of a column of numbers to determine whetever the total is the same as the client's.

Compute -A calculation done by the auditor independent of the client.

Terms, Audit Procedures, and Types of Evidence

Vouch -The use of documents to verify recorded transactions or amounts.

Trace- An instruction normally associated with documentation or reperformance. The instruction should state what the auditor is tracing and where it is being traced from and to. Often, an audit procedure that includes the term trace will also include a second instruction, such as compare or recalculate.

Trace a sample of sales transactions from sales invoices to the sales journal, and compare customer name, date and the dollar value of the sale.

Vouch a sample of recorded acquisition transactions to vendor's invoices and receiving reports.

Observe whetever the two inventory caount teams independently count and record invntory counts.

Select a sample of sales invoices and compare the unit selling price as stated on the invoice to the list of unit selling prices authorized by management.

Compare -A comparison of information in two different locations. The instruction should state which information is being compared in as much detail as pratical.

Count a sample 100 inventory items and compare quantity and description to client's counts.

Count-A determination of assets on hand at a given time. This term should be associated with the type of evidence defined as physical examination.

Set materiality and assess acceptable audit risk and

inherent risk

Perform preliminary analytical procedures

Understand internal control and assess control

risk

Gather information to assess fraud risks

Develop overall audit plan and audit program

Strategic Systems Understanding of the Client’s Business and Industry

Understand Client’s Business and lnustry

Industry and External Environment

Bussines Operations and Processes

Management and Governance

Objectives and Strategies

Measurement and Performance

Understanding the Client’s Business and Industry, Client Business Risk, and Risk of Material Misstatement

Industry and External Environment

Bussines Operations and Processes

Management and Governance

Objectives and Strategies

Measurement and Performance

Understand Cleint’s Business and Industry

Asess Client Business Risk

Assess Risk of Material Misstatements

Hillsburg is a continuing audit client. No circumstances were identified in the conticuation review to cause discontinuance

New client acceptance and continuance

There are two primary reasons. Company is publicly traded and audit is required by bank due to large notes payable outstanding

Obtained an engagement letter before starting field work.

Partner - Joe Anthony Manager - Leslie Franklin Senior - Fran Moore Assistant – Mich Bray and one person ro be named later

Iddentify client’s reasons for audit

Obtain an understanding with the client

Staff the engagement

Accept client and perform initial panning

Understand the client’s business and industry

Understand client’s industry and external environment

Understand client’s operations, strategies, and performance system

Assess client business risk

Assess client business risk

Evaluate management controls affecting business risk

Assess risk of material misstatements

See Figure 8-3 (p. 217). Moore discussed with CEO and CFO, read minutes, and reviewed other key reports and performance indicators

Anthony and Franklin subscride to industry publications. Moore reviewed industry data and reports in several database and online sources

Moore used her understanding of the client and industry to evaluate business risk.

Moore reviewed management and governance controls and their effct on business risk.

Moore used her assessment of client business risk and management controls to identify audit areas with increased risk of misstatement.

Perform preliminary analytical procedures

Moore compared 12-31-11 anaudited balances to the prior year. She calculated key ratios and compared them with prior years and industry averages. All significant differences were identified for follow-up.

Phase(Required) Planning

Phase Testing Phase(Required)

Completion PhasePurpose

Timing and Purposes of Analytical Procedures

Understand the client's business and industry

Indicate possible misstatements (attetion directing)

Recorded interest expense per general ledger 2.408.642

Difference-over (under) expectation 9.327

Conclusion : Interest expense appears fairly stated as recordedAmount is within 9.327 (4.%) of expected amount.

Tickmark Legend :

1. Monthly balances obtained from general ledger for each month2. Estimated based on examination of several notes outsanding each month3. Agreed to prior year audit workpapers4. Agrees with December 31, 2011 general ledger and working trial balance5. Agrees with permanent file schedule of long-term debt.

12/13/2011

Hilssburg Hardware Overall Test of Interest Expense December 31, 2011

Cash + marketable securitiesCurrent liabilities

Current liabilities 13,126

Current assetscurrent liabilities

Quick ratio =

8,2813,216

828 + 18,957 + 945 =

51,02713,216

= 3.86

Short Term Debt Paying Ability

Cash Ratio =

Cash + marketable + securities + net accounts receivable

Current ratio =

157

Account receivable Net salesturnover average gross receivable

Days to collect 365 daysreceivable account receivable turnover

Inventory Cost of goods soldTurnover Average inventoy

Current assetsCurrent liabilities

7.59((18,957 + 1,240) + (16,210 + 1,311)) /2

103,241

=

Liquidity Activity Ratios

=

=

=

143,086

48.09 days

3

=

Days to sell inventory

=

7.59365 days

108.63 days

=

=

365 days3.36

(29,865 + 31,600) /2

Total liabilitiesTotal equity

operating incomeinterest expense

13,216 + 25,68822,463

=

=

1.73

3.06

Ability to Meet Long-term Debt Obligations

=Debt to equity

Times interset earned

= 7,3702,409

3,9345,000

Net sales - cost of goods sold

7,370143,086

5,681(91,367 + 60,791)/2

(22,463 + 20,429)/2

= 27.85%

= 0.05

=

= 0.26

0.09

5,681 - 0Common equity

= Income before taxes-preferred dividendsAverage stockholders equity

Return on assets

= Income before taxesAverage total assets

=

143,086143,086 - 103,241

0,79

Profit Margin

=Net sales

Operating Income

Earning per share

=

Gross profit percent

=Net sales

Net incomeAverage common shares outstanding

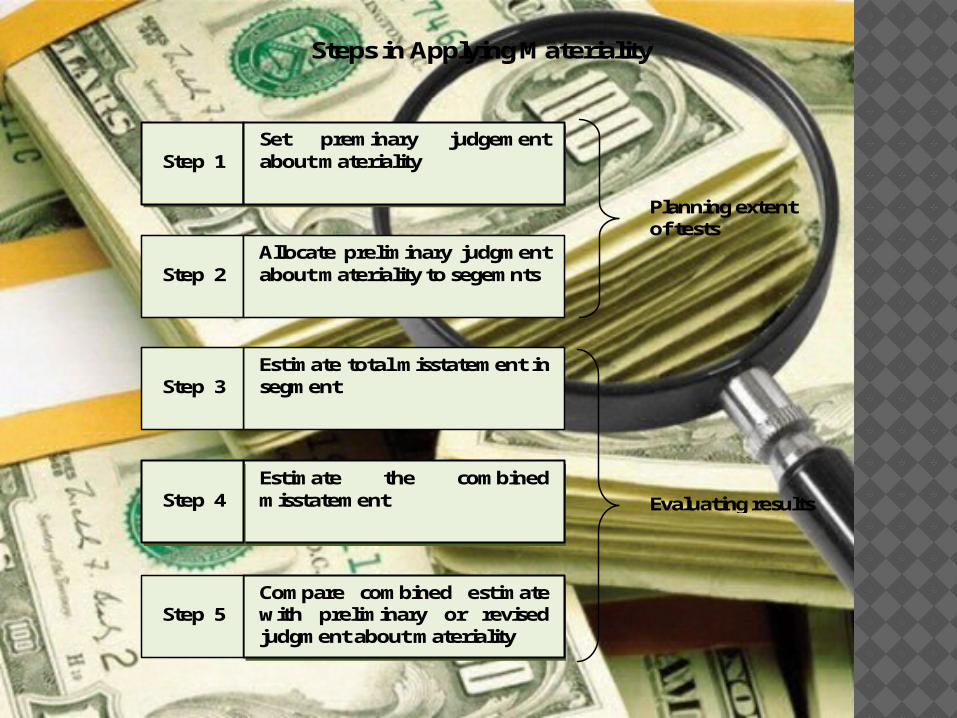

Steps in Applying Materiality

Step 1

Set preminary judgement about materiality

Step 2

Allocate preliminary judgment about materiality to segemnts

Planning extent of tests

Estimate total misstatement in segment

Step 3

Estimate the combined misstatement

Step 4

Compare combined estimate with preliminary or revised judgment about materiality

Step 5

Evaluating results

Audit Risk Model and Understanding the Client’s Business and Industry

Industry and External Environment

Business Operations and Processes

Management and Governance

Objectives and Strategies

Measurenment and Performance

Understand Client’s Business and Industry

Understand Client’s Business and Industry

Understand Client’s Business and Industry

Inherent Risk (IR)

Control Risk (CR)

AUDIT RISK MODEL

PDR = AAR IR x CR

(medium) (high) (Low) (high) (low)

(medium) (Low) (Low) (high) (medium)

(Low) (Low) (Low) (Low) (Low)

(medium) (medium) (high) (Low) (medium)

Capital Acquisition and Repaymeny

Cycle

AExpect some

misstatemensExpect many

misstatementsExpect few

misstatementsExpect many

misstatements

High effectiveness

Medium effectiveness

low effectiveness

Illustration of Differing Evidence Among Cycles

Sales and Collection Cycle

Acquisition and Payment Cycle

Payroll and Personel Cycle

Inventory and Warehousing

Cycle

Expect few misstatements

Auditor's assessment of expectation of material mistatement before considering internal control (inherent risk)

B

Auditor's willingness to permit material misstatements to exist after completing the audit (acceptable audit risk)

C

Extent of evidence the auditor plan accumulate (planned detection risk)

Medium level Medium levelD

Auditor's assessment of effectiveness of internal controls to prevent or detect material misstatements (control risk)

Relationship of Factors Influencing Risks to Risks and Risks to Planned Evidence

Reliance by external users Likelihood of financial failure Intergrity of management

Nature of business Results of previous audit Initial versus repeat

engagement Related parteis Nonroutine transactions Judgement required Makeup of population Factors related to

misstatements arising from fraudelent financial reporting *

Susceptibility of assets to misappropriation*

Acceptable audit risk

Planned audit

evidence

Planned detection

risk

Inherent

risk

Effectiveness of internal controls

Planned reliance

Control risk

D = Direct relationship ; l = inverse relationship

*Fraud risk factors. These may also affect acceptable audit risk and controls risk

l

l l

l D

D D

1 High Low Low High Low2 Low Low Low Medium Medium3 Low High High Low High4 Medium Medium Medium Medium Medium5 High Low Medium Medium Medium

Planned Detection

Risk

Amount of Evidence Required

Relationships of Risk to Evidence

SituationAcceptable Audit Risk

Inherent Risk

Control Risk

Deta

il tie

-in

Exis

tenc

e

Com

plet

ense

ss

Accu

ranc

y

Clas

sific

ation

Cuto

ff

Real

izab

le v

alue

Righ

ts

LowLow Low Medium

Evidence-Planning Worksheet to decide Tests of Details of Blances for Hillsburg Hardware CO. - Accounts Receivable

Subtantive tests of transaction-salesSubtantive tests of transactions-cash receiptsAnalytical proceduresPlanned detection risk for tests of details of balances

Acceptable audit risk

Medium Medium Medium Medium

Planned audit evidence for tests of details of balances

Medium Medium Medium Medium

Control risk- sales

Medium

Control risk- Additional controls

Control risk- cash receipts

inherent risk Low Medium Low

Relationship of Tolerable Misstatement and Riks to Planned Evidence

Acceptable audit risk

Inherent Risk

Control Risk

Tolerable misstatement

Planned detection risk

Planned audit evidence

D = Direct Relationship ; l = Inerverse relationship

D

D I

D

I

I

I

I

TOLERABLE MISSTATEMENT AND RISKS

PLANNED AUDIT EVIDENCE

Five Components of Internal Control

Risk Assesment

Control Activities

Information and Communication

Monitoring

Control Environment

Component Description of Component Further Subdivision (if applicable)Control Enivronment Subcomponents of the control environment :

Intergrity and ethical values Commutment to competence Board of director and audit committee participation Management's philosophy and operating style Organizational sturture Human Resource policies and practices

Riks Assessment Risk assessment processes : Identify factors affecting risks Assess significance of risks and likelihood of occurrence Determine actions necesarry to manage risks

Categories of management assertions that must be satisfied : Assertions about classes of transactions and other events Assertions about account balances Assertions about presentation and disclosure

Control Activities Types of specific control activities : Adequate separation of duties Proper authorization of transaction and other occurence Adequate documents and records Physical control over assets and records Independent checks on performance

Transaction-related audit objectives that must be satisfied : Occurrence Completeness Accuracy Posting and summarization Classification Timing

Monitoring Not Applicable

Information and communication

Methods used to initiate, record, process, and report an entity's transactions and to maintain accountability for related assets

Management's on going and periodic assessment of the quality of internal control performance to determine whether contorls are operating as intended and are modified when needed

COSO Components of Internal Control

INTERNAL CONTROL

Actions, policies and procedures that reflect the overall attitude of top management, directors, and owners of an entity about internal control and its importance

Management's identification and analysis of risks relevant to the preparation of financial statements in accordance with appropriate accounting frameworks such as GAAP or IFRS

Policies and procedures that management has established to meet its objectives for financial reporting

Obtain and document understanding of internal

control desihn and operation

Assess control risk

Design, perform and evaluate tests of controls

Decide planned detection risk and substantive tests

Phase 1

Phase 4

Phase 3

Phase 2

Process for Understanding Internal Control and Assessing Control Risk

INTERNAL CONTROL Re

cord

ed

sa

les

are

fo

r sh

ipm

en

ts a

ctu

all

y m

ad

e

to n

oti

ctiti

on

s cu

sto

me

rs (

occ

urr

en

ce)

Ex

isti

ng

sa

les

tra

nsa

ctio

n a

re r

eco

rde

d

(co

mp

lete

ne

ss)

Re

cord

ed

sa

les

are

fo

r th

e a

mo

un

t o

f g

oo

ds

ship

pe

d a

nd

are

co

rre

ctly

bil

led

an

d r

eco

rde

d

(acc

ura

cy)

Sa

les

tra

nsa

ctio

ns

are

co

rre

ctly

in

clu

de

d i

n t

he

acc

ou

nts

re

ceiv

ab

le m

ast

er

file

an

d a

re c

orr

ect

ly

sum

ma

rize

d (

po

stin

g a

nd

su

mm

ari

zati

on

)

Sa

les

tra

nsa

ctio

n a

re c

orr

ect

ly c

lass

ifie

d

(cla

ssifi

cati

on

)

Sa

les

are

re

cord

ed

on

th

e c

orr

ect

da

tes

(tim

ing

)

SALES TRANSACTION-RELATED AUDIT OBJECTIVES

Control Risk Matrix for Hillsburg Hardware Co.-Sales

Credit is approved automatically by computer by comparison to authorized credit limits (C1).

C

CO

NT

RO

LS

Separation of duties exists among billing, recording of sales, and handling of cash receipts (C3).

Shipping documents are prenumbered and accounted for weekly (C5).

Shipping documents are forwarded to billing daily and are billed the subsequent day (C4).

Batch totals of quantities shipped are compared with quantities biled (C6).Unit selling prices are obtained from the price list master file of approved prices (C7).

Sales Transaction are internally verified (C8).

C C C

Recorded sales are supported by authorized shipping documents and approved customer orders (C2).

C C

C C

Statements are mailed to customers each month (C9).Computer automatically posts transactions to the accounts receivable subsidiary records and to the general ledger (C10).Account receivable master file is reconciled to the general ledger on monthly basis (C11).

C

C

CC

C

C

C

C

C C C

C

DE

FIC

IEN

CE

S

Med. Low Low Low Low * Med.

DThere is lack of internal verification for the possibility of sales invoices being recorded more than once (D1).

There is a lack of control to test for timely recording (D2).

Assessed control risk

Evaluating Significant Control Deficiencies

SIGNIFICANCE

Material

Reasonably Possible

Material Weakness

Remote

LIKELIHOOD

Immaterial

Source : Adapted from Michael Ramos,”Section 404 Compliance in the Annual Report,”Journal of accountancy, October 2004, pp. 43-48

Differences in Scope of Controls Tested in an Audit of Internal Control and an Audit of Financial Statements

Internal Controls Over Financial Reporting

Internal Controls Used to Assess Control Risk Below Maximum

Controls that must be tested in an audit of financial statements

Controls that must be tested in an audit of internal controls

Summary of Understanding Internal Control and Assessing Control Risk

Intergrated Audit of Financial Statements and Internal Control over Financial Reporting

Sufficient to audit internal control over financial reporting

Financial Statement Audit

Sufficient to audit financial statements

Obtain an understanding of internal control design

and operation

Decide control risk at the objective level for each

transaction type

Varies depending on extent and effectiveness of controls and the auditor’s planned reliance on controls

Decide low for all objectives unless there are significant deficiencies or material weaknesses

Intermediate

Three alternatives

Maximum Low PHASE 2

PHASE 1

Plan and perform tests of controls and evaluate

results

Revise assessed control risk if appropriate

Varies depending on assessed level of controls risk

Revise for tests of controls results

Extensive tests for all objectives

Revise for tests of controls results

Likely to be more reliance on substantive tests, depending on assessed control risk option selected

Must communicate in writing to those charged with governance describsing significant deficiencies or material weaknesses

Plan detection risk and perform substantive tests considering control risks

and other audit risk model factors

Issue internal control report or letter

Likely to be less reliance on substantive tests due to extentive tests of controls

Must issue report on internal control over financial reporting and issue a written communication to audit commutte describing significant deficiencies or material weakness