207

04/06/11 1 STRATEGIC COST MANAGEMENT By A Aruldoss Vithakan

| Date post: | 08-Apr-2018 |

| Category: |

Documents |

| Upload: | anshul-singh-gehlot |

| View: | 222 times |

| Download: | 0 times |

8/7/2019 Presentation3 for CSM

http://slidepdf.com/reader/full/presentation3-for-csm 1/207

04/06/11 1

STRATEGIC COST MANAGEMENT

By A Aruldoss Vithakan

8/7/2019 Presentation3 for CSM

http://slidepdf.com/reader/full/presentation3-for-csm 2/207

04/06/11 2

Strategic Management

• Traditional Management accounting is based oncomparing actual results against pre setstandard (Typically budget), identifying andanalysing variances and taking remedial

action to ensure that future outcomes confirmwith budgeted outcomes.• Existing activities are not reviewed.• They are based on cost containment rather than

cost reduction.• But strategic management is focuses on cost

reduction and continuous improvement.

•

8/7/2019 Presentation3 for CSM

http://slidepdf.com/reader/full/presentation3-for-csm 3/207

04/06/11 3

Cost Management And Strategy-

An Overview• Wall Mart- The world’s largest retail Chain- hasgrown to that stage by scrupulously followingtheir mission-”We exist to provide value to thecustomer”

• They achieved such a growth by following astringy of using extensively the technologyand opportunity oriented management stylethat values change and experimentation

• It focus on friendly customer service andaggressive efforts to grow the businessglobally.

8/7/2019 Presentation3 for CSM

http://slidepdf.com/reader/full/presentation3-for-csm 4/207

04/06/11 4

Strategic Cost Management:Strategic Cost Management:Basic ConceptsBasic Concepts

Strategic decision making is choosing amongalternative strategies with the goal of selectinga strategy, or strategies, that provides acompany with reasonable assurance of long-

term growth and survival.The key to achieving this goal is to gain acompetitive advantage.Strategic cost management is the use of cost

data to develop and identify superior strategiesthat will produce a sustainable competitiveadvantage.

•

8/7/2019 Presentation3 for CSM

http://slidepdf.com/reader/full/presentation3-for-csm 5/207

04/06/11 5

General StrategiesGeneral Strategies

• There are three general strategies thathave been identified:

ücost leadership

üproduct differentiation

üfocusing

•

8/7/2019 Presentation3 for CSM

http://slidepdf.com/reader/full/presentation3-for-csm 6/207

04/06/11 6

General StrategiesGeneral Strategies

• A cost leadership strategy happens whenthe same or better value is provided tocustomers at a lower cost than a

company’s competitors.• Example: A company might redesign a

product so that fewer parts are needed,

lowering production costs and the costsof maintaining the product after purchase

8/7/2019 Presentation3 for CSM

http://slidepdf.com/reader/full/presentation3-for-csm 7/207

04/06/11 7

General StrategiesGeneral Strategies

• A differentiation strategy strives toincrease customer value by increasingwhat the customer receives (customer

realization).– Example: A retailer of computers

might offer on-site repair service, a

feature not offered by other rivals inthe local market.

8/7/2019 Presentation3 for CSM

http://slidepdf.com/reader/full/presentation3-for-csm 8/207

04/06/11 8

General StrategiesGeneral Strategies

A focusing strategy happens when a firmselects or emphasizes a market or customer segment in which to compete.

Example: Paging Network, Inc., apaging services provider, hastargeted particular kinds of customers and is in the

process of weeding out thenontargeted customers.

8/7/2019 Presentation3 for CSM

http://slidepdf.com/reader/full/presentation3-for-csm 9/207

04/06/11 9

COST MANAGEMENT SYSTEM

• Cost management is focusing on not on the measurement per se but on the identification these measures that are criticalto future success of the firm.

• Phases of the development of the cost management system:

1. CMS are basic information reporting system.2. Focus on external financial reporting objectives are reliable

financial reporting, accordingly the usefulness of CMS islimited.

3. CMS track key operating data and develop more accurate and

relevant cost information.4. Strategically relevant cost management information is integral

part of the system.

8/7/2019 Presentation3 for CSM

http://slidepdf.com/reader/full/presentation3-for-csm 10/207

04/06/11 10

CONTEMPORARY MANAGEMENTTECHNIQUES

• Bench marking.

• Total quality management (TQM).

• Activity based costing and management.

• Reengineering.

• The theory of constraints (TOC)- eliminateobstacles/constraints to effectively improve the cycletime.

• Mass customization-a larger number of smaller production units in manufacturing and speciallydeigned marketing and service functions.

• Just-in Time system

•

•

8/7/2019 Presentation3 for CSM

http://slidepdf.com/reader/full/presentation3-for-csm 11/207

04/06/11 11

• Computer aided design and manufacturing.

• Automation

• Target costing.

• Life cycle costing.• The value chain.

• Balanced score card \Financial performance

-customer satisfaction. -internal business processes. -Innovation and training

8/7/2019 Presentation3 for CSM

http://slidepdf.com/reader/full/presentation3-for-csm 12/207

04/06/11 12

COSTING FOR DECISIONMAKING

• Managerial decision making is the process of makingchoices.

• Relevant information has to be used for evaluatingalternatives and making decisions.

• Relevant information implies relevant costs( refers toincrease or decrease in cost expected from aparticular decision or course of action) and relevantrevenue (refers to increase or decrease in revenue

expected from a particular decision or course of action)

8/7/2019 Presentation3 for CSM

http://slidepdf.com/reader/full/presentation3-for-csm 13/207

04/06/11 13

COST ANALYSIS FOR DECISIONMAKING

• Fixed and variable cost analysis

• Differential cost and incremental revenue analysis

• Cost benefit analysis

• Opportunity costing technique• Cost effectiveness analysis

• Sunk cost

• Relevant cost analysis

• Engineered cost, committed cost and managedcost

• Learning curve effect

8/7/2019 Presentation3 for CSM

http://slidepdf.com/reader/full/presentation3-for-csm 14/207

04/06/11 14

COST ANALYSIS FOR DECISION

MAKING• Order getting & order filling costs.

• Target costing.

• Life cycle costing.

• Cost estimating

• Bench marking

• Quality cost analysis.

8/7/2019 Presentation3 for CSM

http://slidepdf.com/reader/full/presentation3-for-csm 15/207

04/06/11 15

COSTS FOR DECISION MAKING<PLANNING ANF CONTROL

• Opportunity cost- it is the cost of opportunity lost.It isthe benefit given uo or sacrificed when one alternativeis chosen over another

• Sunk costs- cost already incurred.

• Relevant costs are costs which is a s result of adecision /course of action ot the difference betweenvarious alternatives.

• Differential cost: It is the total costs between any two

alternatives and it is equal to: Additional variableexpenses incurred in respect of additional output+increase in fixed cost, if any.

8/7/2019 Presentation3 for CSM

http://slidepdf.com/reader/full/presentation3-for-csm 16/207

04/06/11 16

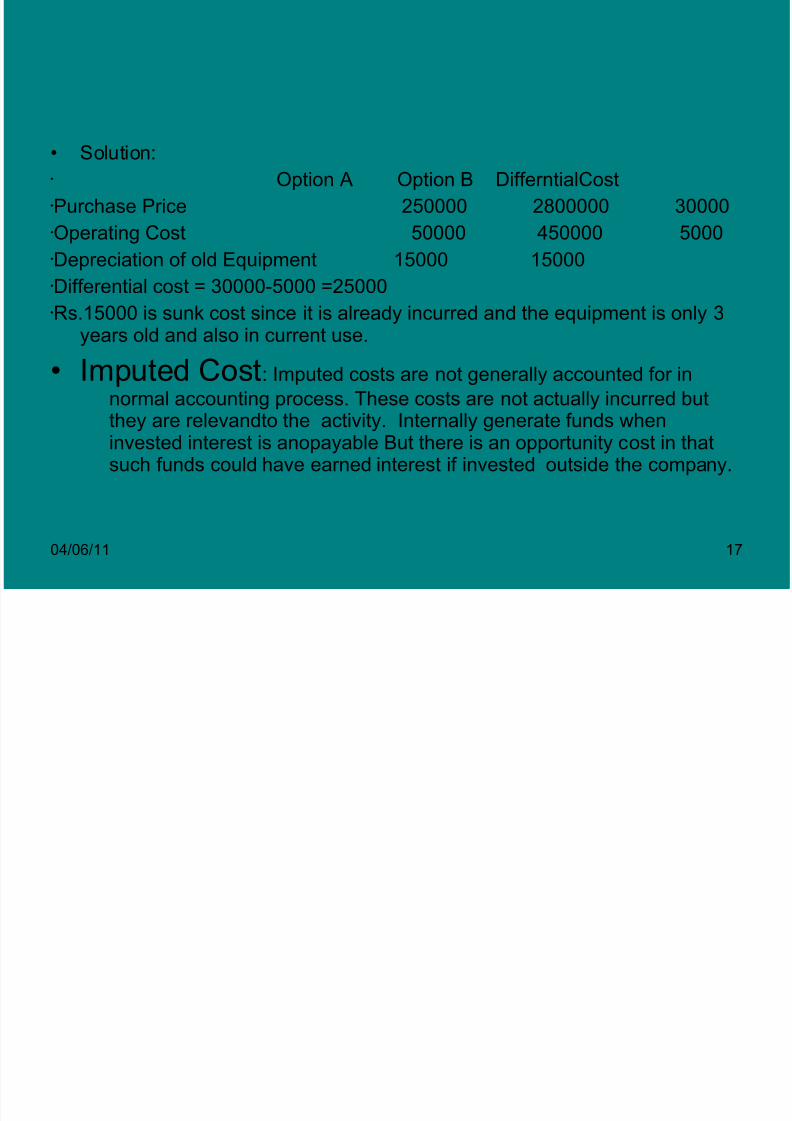

Example : A printer is planning to replace an oldmachine purchased at Rs.1,50,000. The oldmachine is 3 years old and being depreciated atRs.50000 per year. There is two machines in the

market suitable at a cost of Rs.250000 withoperating cost of Rs. 50000 and the other alternative is priced at Rs.280000 with anoperating cost of Rs.45000.

1. What are the incremental cost ,if any, in thealternative choice of the equipment?

2. What are the sunk costs , if any, in this solution?

8/7/2019 Presentation3 for CSM

http://slidepdf.com/reader/full/presentation3-for-csm 17/207

04/06/11 17

• Solution: Option A Option B DifferntialCostPurchase Price 250000 2800000 30000Operating Cost 50000 450000 5000Depreciation of old Equipment 15000 15000Differential cost = 30000-5000 =25000Rs.15000 is sunk cost since it is already incurred and the equipment is only 3

years old and also in current use.

• Imputed Cost: Imputed costs are not generally accounted for in

normal accounting process. These costs are not actually incurred but

they are relevandto the activity. Internally generate funds wheninvested interest is anopayable But there is an opportunity cost in thatsuch funds could have earned interest if invested outside the company.

8/7/2019 Presentation3 for CSM

http://slidepdf.com/reader/full/presentation3-for-csm 18/207

04/06/11 18

• Out –of-Pocket cost : If a companyaccepts a special order, it maynecessitate consideration of out-of-

pocket costs that need not be incurred incase the order is not accepted. For example if a restaurant takes specialorder involving additional transport cost,such cost is considered as out of pocketcost.

8/7/2019 Presentation3 for CSM

http://slidepdf.com/reader/full/presentation3-for-csm 19/207

04/06/11 19

RELEVANT COSTING-DECISION MAKINGPROBLEMS

• Relevant information.

• Relevant revenues

• Relevant costSome Decision making Types:

1. Make or buy2. Drop or add a product

3. Sell or process further

4. Operate or shut down

5. Special orders6. Replace or retain

7. Buy or lease

8/7/2019 Presentation3 for CSM

http://slidepdf.com/reader/full/presentation3-for-csm 20/207

04/06/11 20

Make or Buy Decision

• When a company has unused capacities the followingalternatives are considered:

-To maximize production e capacity utilisation andfinaancialresources available to them they may consider

producing required raw materials or sub assemblies OR - to buy them from outside suppliers

• Such decision also depends on other than financial gainsuch as – strategic importance/quality/reliability of

supplies etc.

8/7/2019 Presentation3 for CSM

http://slidepdf.com/reader/full/presentation3-for-csm 21/207

04/06/11 21

Drop or Add A product

• The decision to eliminate non profitable product istob primarily based on its impact on futureincome if the firm.

• therefore one has to develop appropriate cost and

profit measures either to drop or add a product.• It is also necessary to evaluate how the sales of

other products will get adversely affected if oneproduct is removed.

• A customer may buy a highly profitable productsince the unprofitable product is also availablefrom the same company.

8/7/2019 Presentation3 for CSM

http://slidepdf.com/reader/full/presentation3-for-csm 22/207

04/06/11 22

SELL OR PROCESS FURTHER

• It is a decision to sell a product at spin oo point or toprocess further.

• Further process adds value tom the product and will getmore price.

• Further process may incur additional cost.

• Therefore the increase in revenue should be more thanthe additional cost incurred.

8/7/2019 Presentation3 for CSM

http://slidepdf.com/reader/full/presentation3-for-csm 23/207

04/06/11 23

• There are generally two conditions prevail : a)Additional process may call for additional

equipment and/or fixed costs.

b) Company already processes beyond spin-off point and invested in equipments andrequired personnel.

•

8/7/2019 Presentation3 for CSM

http://slidepdf.com/reader/full/presentation3-for-csm 24/207

04/06/11 24

OPERATE OR SHUTDOWN

• A company may face a situation that even when they areoperating at lesser percentage of installed capacitythey expect further fall in sales volume or reduction inprofit margin due to:

• Reduction in demand.• Economic slow down

• Stiff domestic or international competition.

• Political instability

• Increase in cost of inputs•

8/7/2019 Presentation3 for CSM

http://slidepdf.com/reader/full/presentation3-for-csm 25/207

04/06/11 25

SPECIAL ORDERS

• Such an option is considered by a company when theyhave surplus or unutilized production capacity isavilable.

• Special orders should not affect existing sales of the

product.• Pricing for special order may not take into account fixed

costs unless incurred for such orders a sotherwise thefirm may lose the order.

• Contribution approach may be an useful technique inpricec determination for special orders.

8/7/2019 Presentation3 for CSM

http://slidepdf.com/reader/full/presentation3-for-csm 26/207

04/06/11 26

Replace or Retain

• It is capital investment decision to be takencarefully.

• Differential cost and benefits are critical inputs

for making this decision.• Relevant cost and relevant revenue are to be

considered.

• Replacement cost to include cost of equipment

at site, cost of capital, training cost of operators etc.

8/7/2019 Presentation3 for CSM

http://slidepdf.com/reader/full/presentation3-for-csm 27/207

04/06/11 27

Assignment-1 (due on 12nd jul2009)1.A firm needs an assembly component. If it needs to produce an

equipment costing 4 lakhsis needed which will lost for 4 years withno salvage value. Manufacturing costs are in each year is 6 L , 7L,8L and 10 L. IN case of buying it cost 9L, 10L, 11L and 14 L in eachof the four years. The new machine would occupy space of an

existing machine used for production which would be hired toproduce an item generates cash flow of Rs. 2 L per year in each of the 4 years. I t is impossible to find room for both machines andthere are no external effects. The cost of capital is 10% and thepresent value for each of the 4 years are;00-1; 1-0.909; 2-0.826;3.0.751; 4- 0.683

• Should the firm make the component or buy. (10 Marks)

8/7/2019 Presentation3 for CSM

http://slidepdf.com/reader/full/presentation3-for-csm 28/207

04/06/11 28

2.Based on the following data you are required to advice themanagement the area of cultivation which would maximize theprofits of the company:

Particulars Apple Lemons Oranges PeachesSelling Price/unit1 15 15 30 45Yield/acre(Boxes) 500 150 100 200Cost/acre(Materials) 270 105 50 150Labour-Cultivation 300225 150 195Pick-up & Packing 1.50 1.50 3 4.50

Transport cost 3.00 3.00 1.50 4.50

8/7/2019 Presentation3 for CSM

http://slidepdf.com/reader/full/presentation3-for-csm 29/207

04/06/11 29

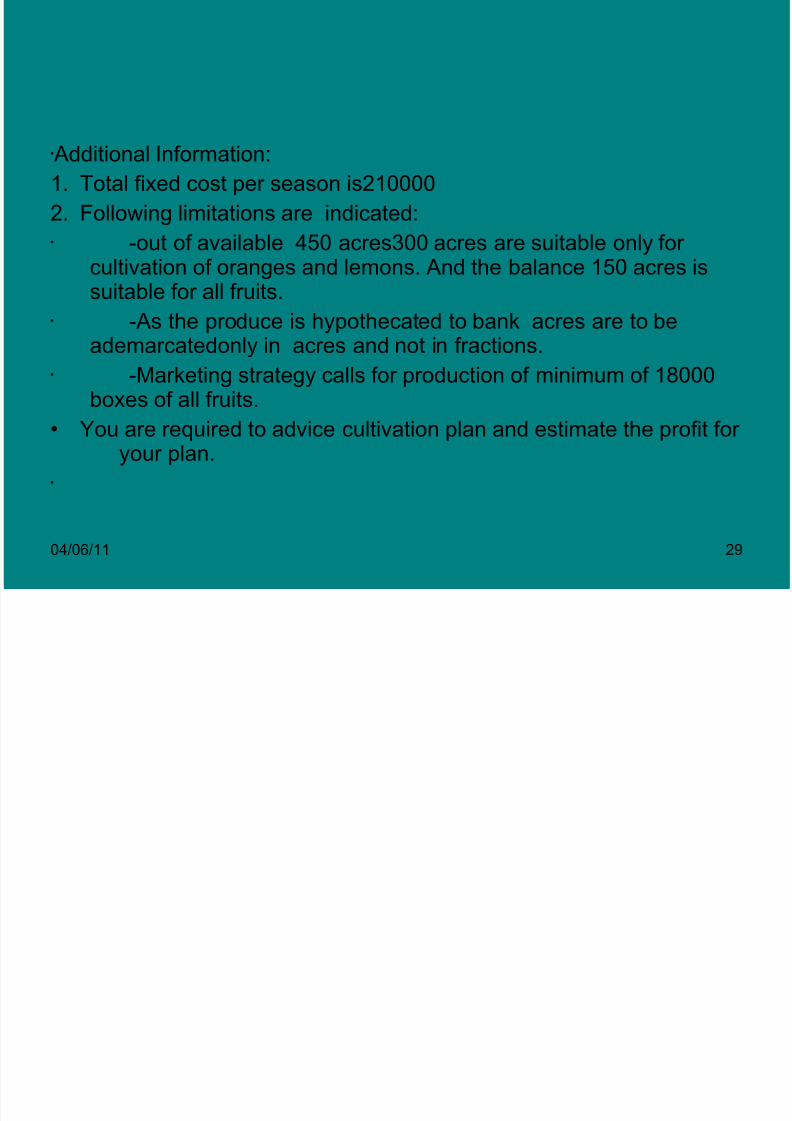

Additional Information:

1. Total fixed cost per season is210000

2. Following limitations are indicated: -out of available 450 acres300 acres are suitable only for

cultivation of oranges and lemons. And the balance 150 acres issuitable for all fruits.

-As the produce is hypothecated to bank acres are to beademarcatedonly in acres and not in fractions.

-Marketing strategy calls for production of minimum of 18000boxes of all fruits.

• You are required to advice cultivation plan and estimate the profit for your plan.

8/7/2019 Presentation3 for CSM

http://slidepdf.com/reader/full/presentation3-for-csm 30/207

04/06/11 30

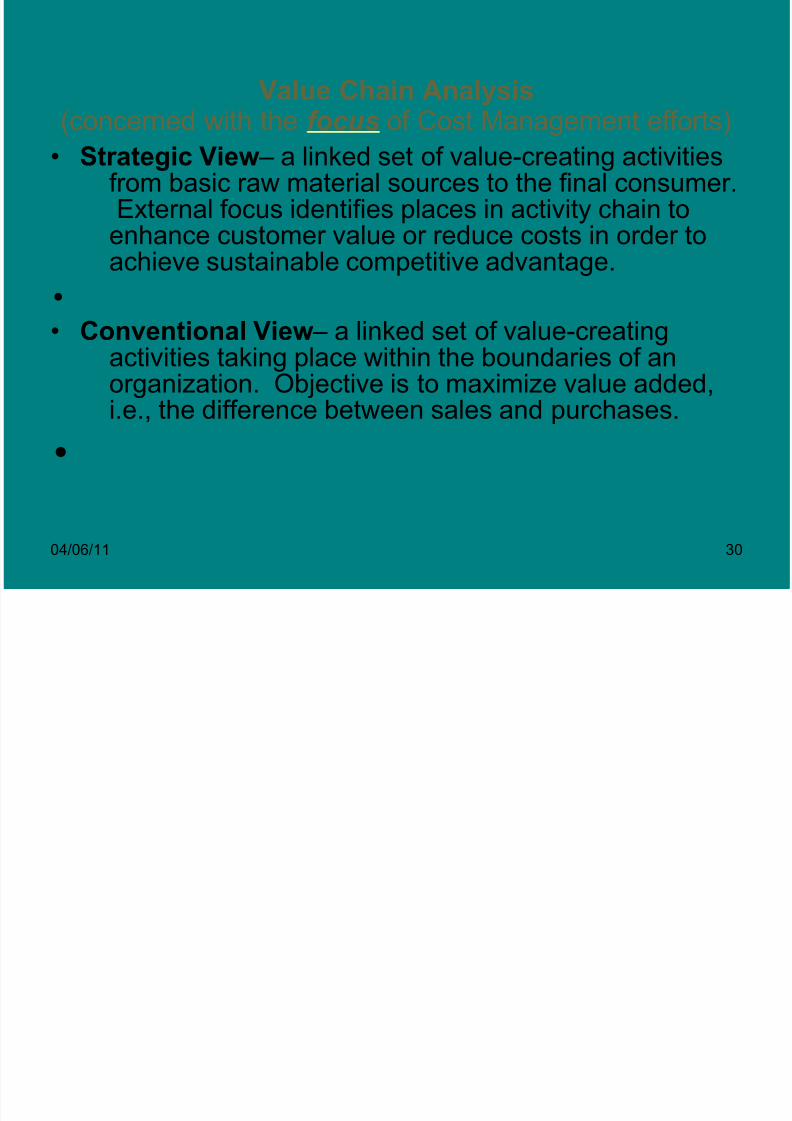

Value Chain Analysis(concerned with the focus of Cost Management efforts)

• Strategic View– a linked set of value-creating activitiesfrom basic raw material sources to the final consumer.External focus identifies places in activity chain to

enhance customer value or reduce costs in order toachieve sustainable competitive advantage.

•

• Conventional View– a linked set of value-creatingactivities taking place within the boundaries of anorganization. Objective is to maximize value added,

i.e., the difference between sales and purchases.•

8/7/2019 Presentation3 for CSM

http://slidepdf.com/reader/full/presentation3-for-csm 31/207

04/06/11 31

Value Chain Analysis

• A strategic analytical tool used to identify wherevalue to customers can be increased or costsreduced.

• To enable better understanding of the linkages

with suppliers, customers and other.• Value chain in PC Industry: Personal Computers---Software—Peripherals—

service

Operating Margins 5 20 10 15(revenue- Cost)

8/7/2019 Presentation3 for CSM

http://slidepdf.com/reader/full/presentation3-for-csm 32/207

04/06/11 32

STEPS INVOLVED IN VALUEANALYSIS

• Identify the value chain activities

• Develop a competitive advantage by reducing cost or adding value.

• Identify competitive advantage (cost leadership or

differentiation.• Identify opportunities for added value.

• Identify opportunities for reduced cost.

• Exp[lain linkges among activities in the value chain

8/7/2019 Presentation3 for CSM

http://slidepdf.com/reader/full/presentation3-for-csm 33/207

04/06/11 33

Value Chain for a Computer Manufacturing Industry

Step-1 Design Research &Development Product designStep-2 Raw Materialsacquisition

Mining,, developing& refining

Silicon, plastics &various materialsStep-3 Materials

assembled into partsConversion process Desired components

and partsStep-4 Intermediateassembly

Conversion process Boards andcomponentsStep-5 Computer

Manufacturing

Final assembly Completed computer

Step-^ Wholesaling,Warehousing &Distribution

Moving products Truck, rail & air

Step-7 Retail sales Making sale Cash Received

Step-8 Customer Service

Provide service Serviced units &customer Satisfaction

8/7/2019 Presentation3 for CSM

http://slidepdf.com/reader/full/presentation3-for-csm 34/207

04/06/11 34

BALANCED SCORECARD

• BSC provides a system for measuring andmanaging all aspects of the Company’sperformance.

• Score card balances traditional financialmeasure of success, such as profits andreturns on capital with non financial measuresof drivers of future financial performance.

•

8/7/2019 Presentation3 for CSM

http://slidepdf.com/reader/full/presentation3-for-csm 35/207

04/06/11 35

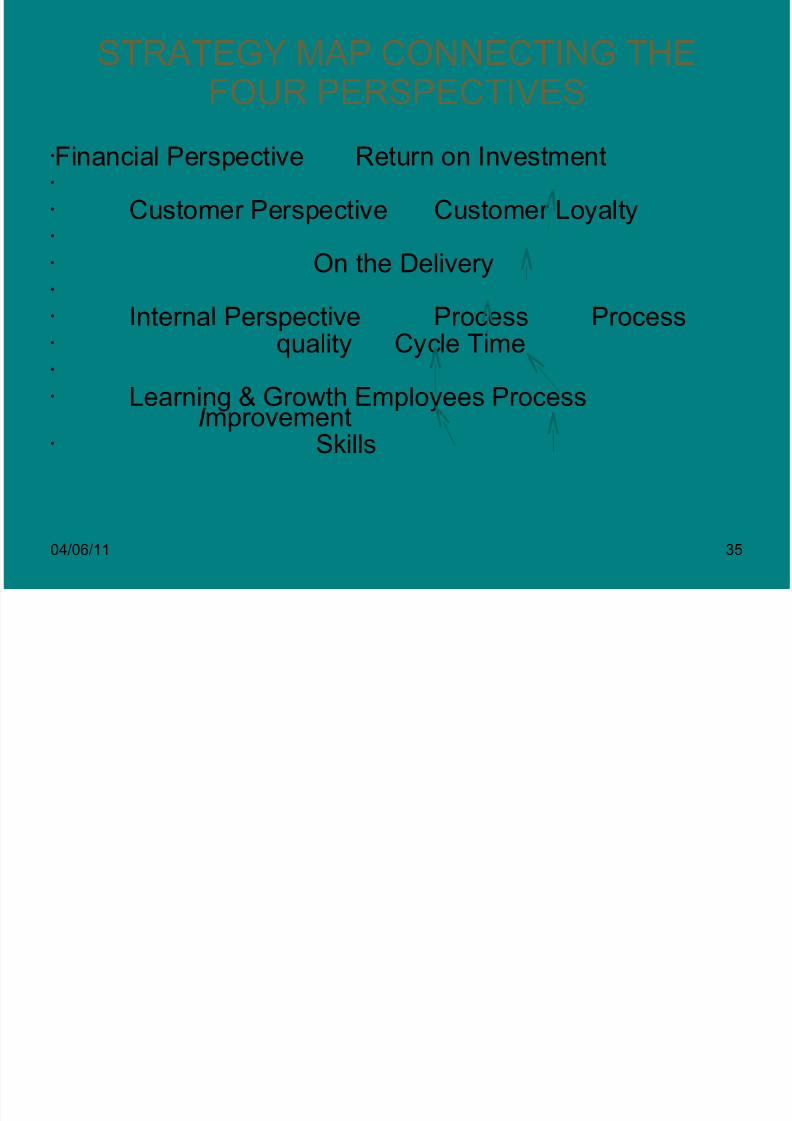

STRATEGY MAP CONNECTING THEFOUR PERSPECTIVES

Financial Perspective Return on Investment

Customer Perspective Customer Loyalty

On the Delivery

Internal Perspective Process Process quality Cycle Time

Learning & Growth Employees Process

I mprovement Skills

8/7/2019 Presentation3 for CSM

http://slidepdf.com/reader/full/presentation3-for-csm 36/207

04/06/11 36

ILLUSTRATIVE EXAMPLE OF LOW COSTAIRLINE

Financial Profits, Return On Assets

Grow Revenues Fewer

aircrafts

Customer Attract, retain More customers

On time services Lowest prices Internal Fast Ground Turnout Learning Trained motivated Ground Crew

•

8/7/2019 Presentation3 for CSM

http://slidepdf.com/reader/full/presentation3-for-csm 37/207

8/7/2019 Presentation3 for CSM

http://slidepdf.com/reader/full/presentation3-for-csm 38/207

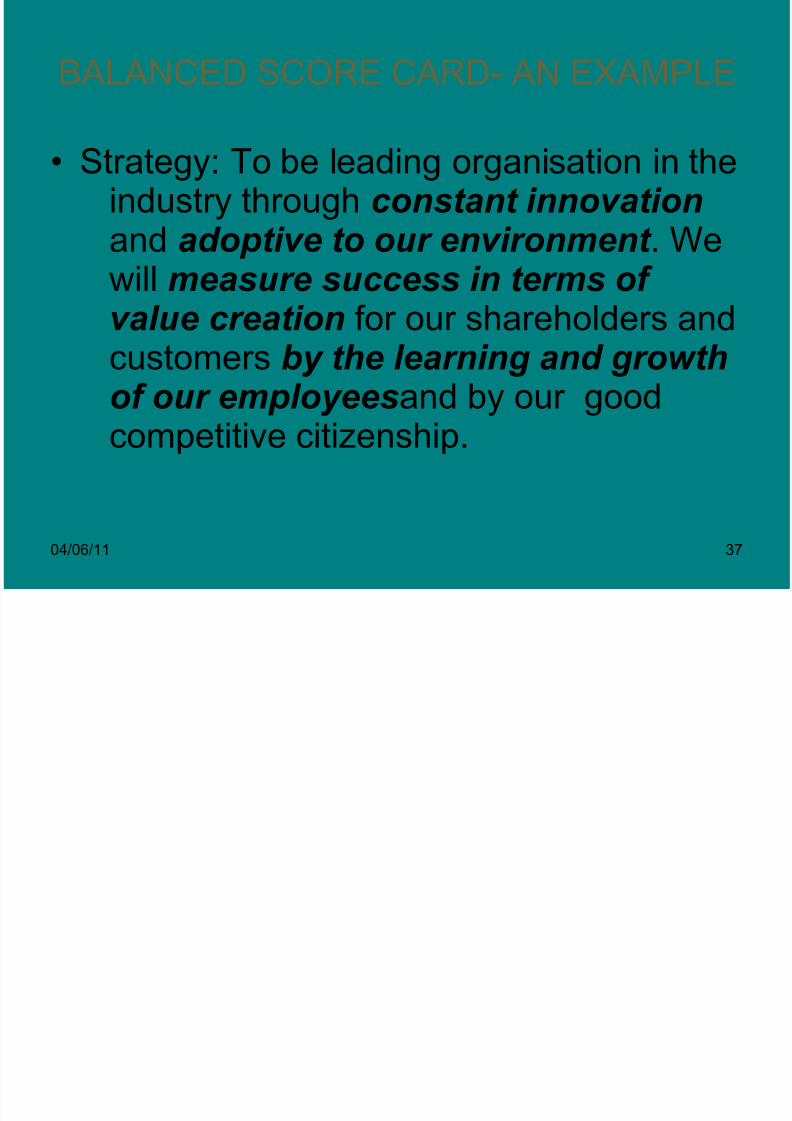

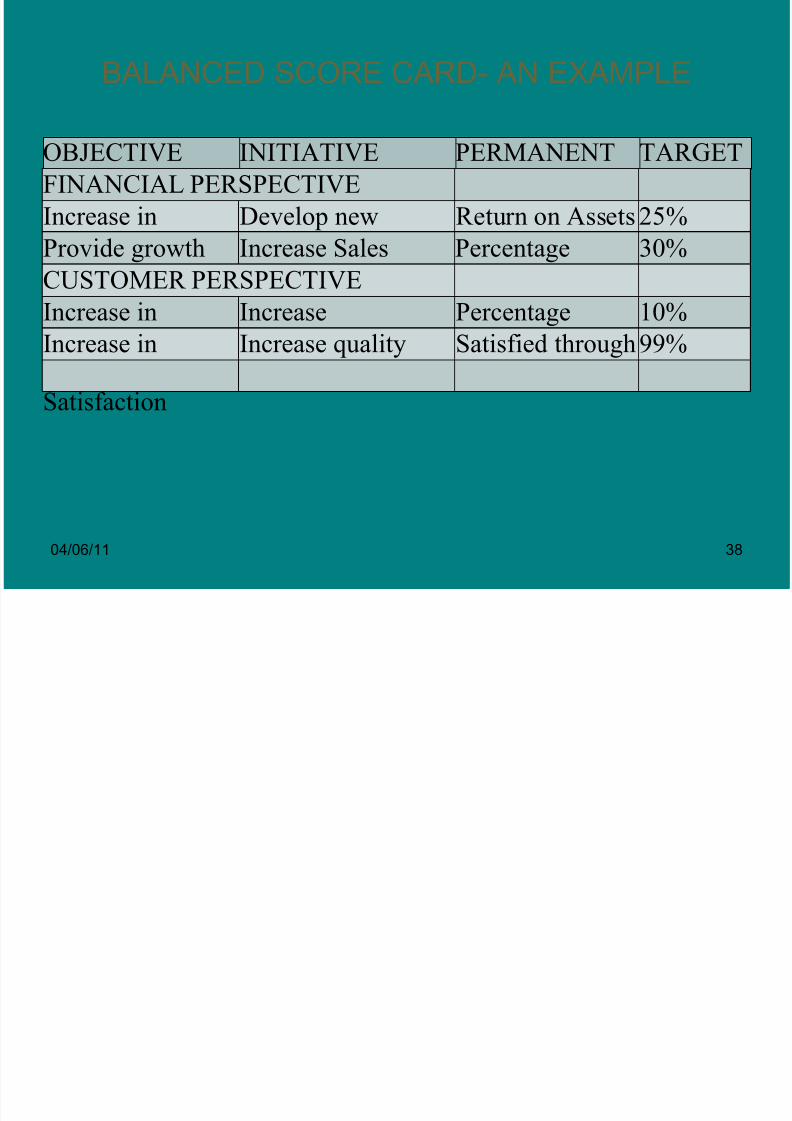

BALANCED SCORE CARD AN EXAMPLE

8/7/2019 Presentation3 for CSM

http://slidepdf.com/reader/full/presentation3-for-csm 39/207

04/06/11 39

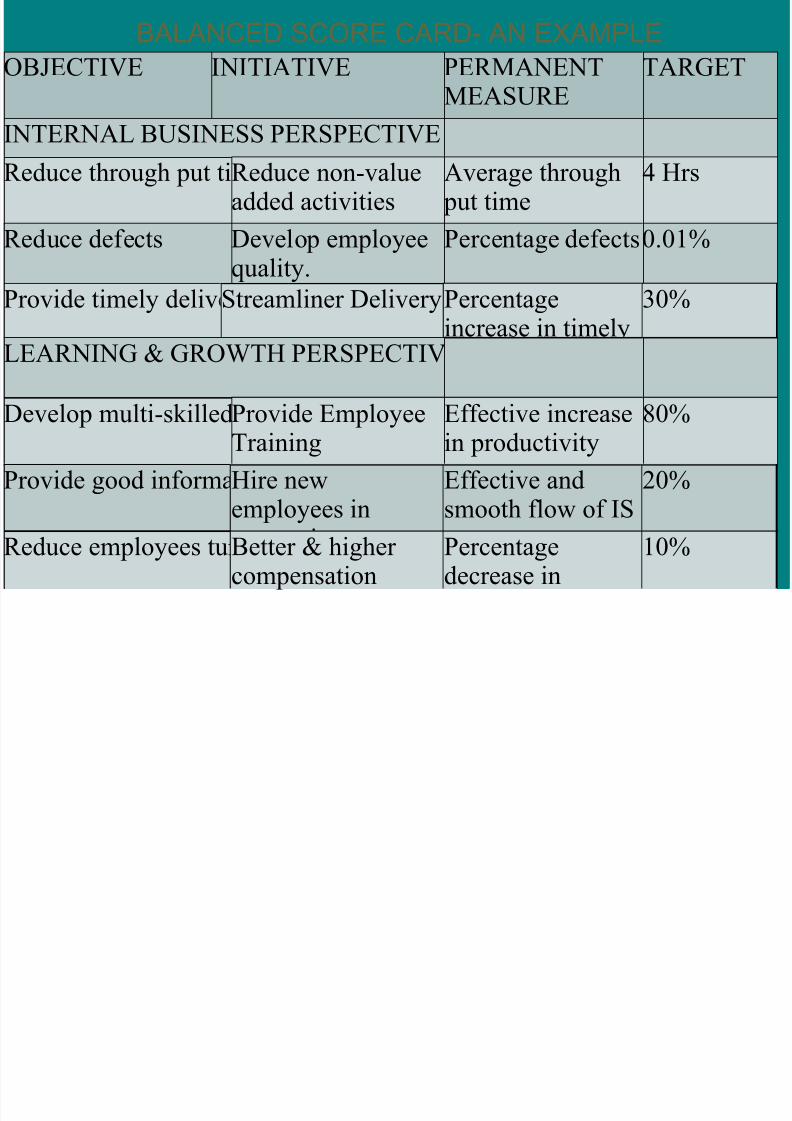

BALANCED SCORE CARD- AN EXAMPLE

OBJECTIVE INITIATIVE PERMANENTMEASURE

TARGET

INTERNAL BUSINESS PERSPECTIVEReduce through put timeReduce non-value

added activitiesAverage throughput time

4 Hrs

Reduce defects Develop employeequality.

Percentage defects0.01%

Provide timely deliveryStreamliner Delivery ProcessPercentageincrease in timelydelivery

30%

LEARNING & GROWTH PERSPECTIVE

Develop multi-skilled workforceProvide EmployeeTraining

Effective increasein productivity

80%

Provide good information systemHire newemployees incomputing

Effective andsmooth flow of IS

20%

Reduce employees turnover Better & higher compensation Percentagedecrease in 10%

8/7/2019 Presentation3 for CSM

http://slidepdf.com/reader/full/presentation3-for-csm 40/207

04/06/11 40

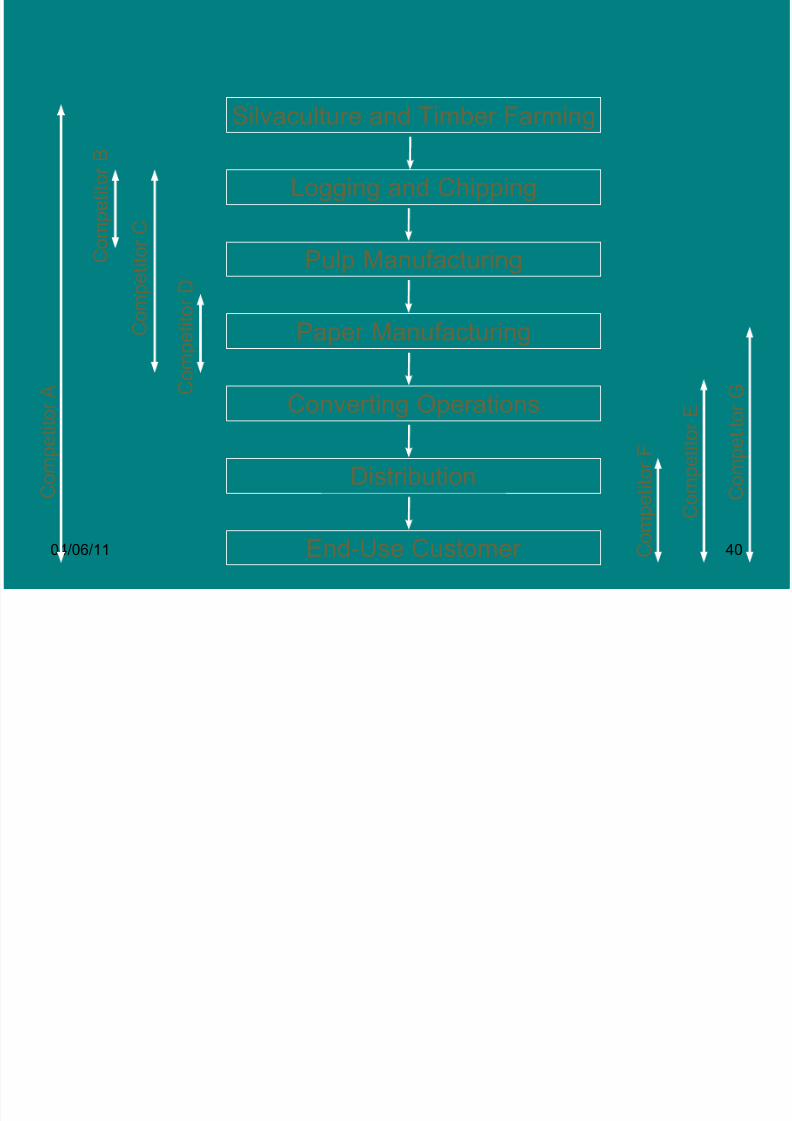

Silvaculture and Timber Farming

Logging and Chipping

Pulp Manufacturing

Paper Manufacturing

Converting Operations

Distribution

End-Use Customer

Compe

titorD

Compe

titorC

CompetitorB

Compe

titorA

Compe

tito

rG

Compe

titorE

Compe

titorF

8/7/2019 Presentation3 for CSM

http://slidepdf.com/reader/full/presentation3-for-csm 41/207

04/06/11 41

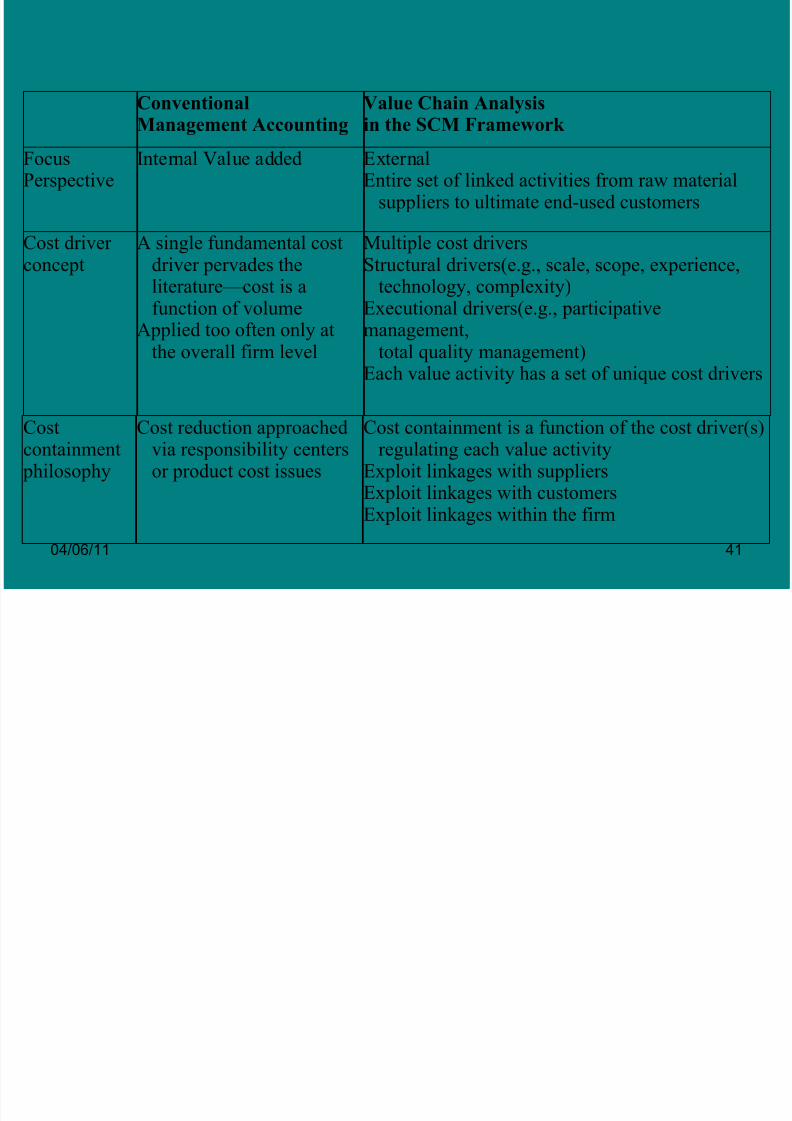

ConventionalManagement Accounting

Value Chain Analysisin the SCM Framework

FocusPerspective

Internal Value added ExternalEntire set of linked activities from raw material

suppliers to ultimate end-used customers

Cost driver concept

A single fundamental costdriver pervades the

literature—cost is afunction of volume

Applied too often only atthe overall firm level

Multiple cost driversStructural drivers(e.g., scale, scope, experience,

technology, complexity)Executional drivers(e.g., participativemanagement,

total quality management)Each value activity has a set of unique cost drivers

Costcontainmentphilosophy

Cost reduction approachedvia responsibility centersor product cost issues

Cost containment is a function of the cost driver(s)regulating each value activity

Exploit linkages with suppliersExploit linkages with customersExploit linkages within the firm

8/7/2019 Presentation3 for CSM

http://slidepdf.com/reader/full/presentation3-for-csm 42/207

04/06/11 42

Conventional Management

Accounting

Value Chain Analysis

in the SCM Framework Insights for strategicdecisions

None are readily apparent.This is a major reasonwhy strategy consultingfirms typically throw awayconventional reports as they

begin their cost analysis

Identify cost drivers at the individual activitylevel; develop cost/differentiation advantageeither by controlling those drivers better thancompetitors or by reconfiguring the value chain

For each value activity, ask strategic questionspertaining to make versus buy and forwardversus backward integration

Quantify and assess supplier power and buyer power; exploit linkages with suppliers and

buyers

8/7/2019 Presentation3 for CSM

http://slidepdf.com/reader/full/presentation3-for-csm 43/207

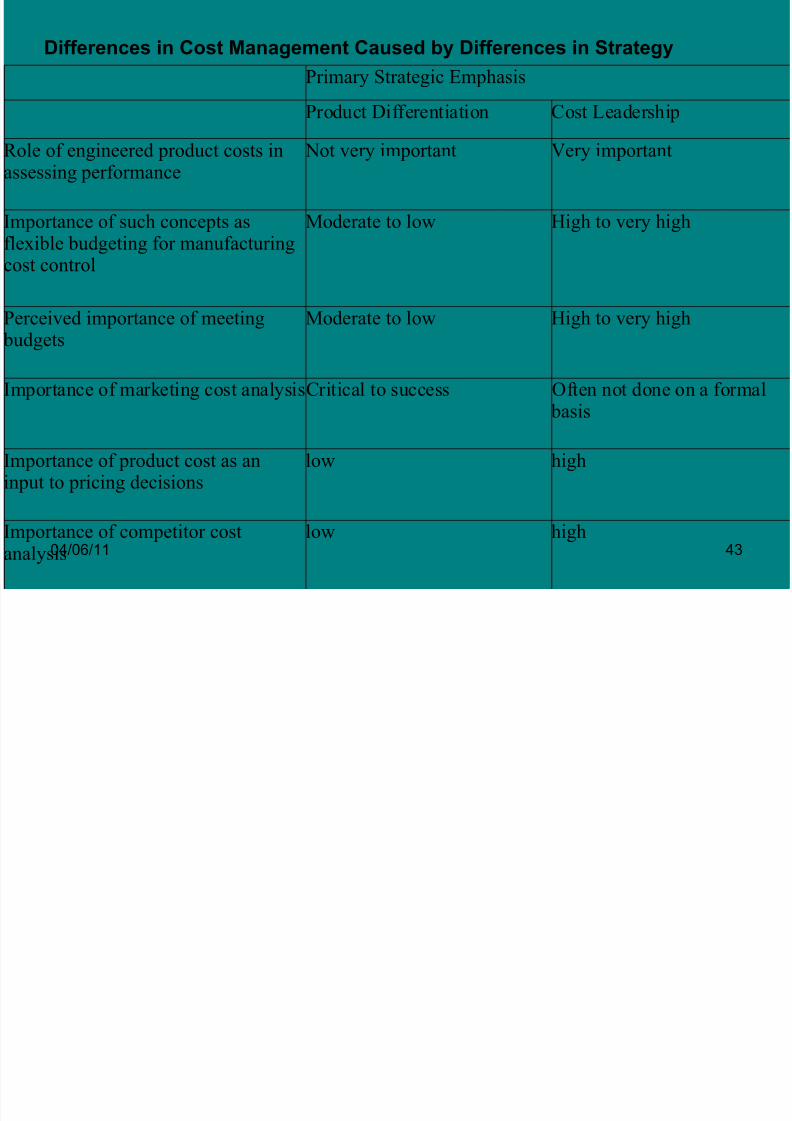

04/06/11 43

Differences in Cost Management Caused by Differences in Strategy

Primary Strategic Emphasis

Product Differentiation Cost Leadership

Role of engineered product costs inassessing performance

Not very important Very important

Importance of such concepts asflexible budgeting for manufacturingcost control

Moderate to low High to very high

Perceived importance of meetingbudgets

Moderate to low High to very high

Importance of marketing cost analysisCritical to success Often not done on a formal

basis

Importance of product cost as aninput to pricing decisions

low high

Importance of competitor cost

analysis

low high

8/7/2019 Presentation3 for CSM

http://slidepdf.com/reader/full/presentation3-for-csm 44/207

04/06/11 44

ABC Costing Technique

• Focuses on activity than on productsproduced.

• Costs are first traced to activities then toProducts.

• ABC assumes that activities are responsiblefor incurrence of costs and products createdemand for activities..

• Costs are charged to products based on

usage of activities. Traditional systemtraces costs to products and ABC tracescosts to activities.

•

8/7/2019 Presentation3 for CSM

http://slidepdf.com/reader/full/presentation3-for-csm 45/207

04/06/11 45

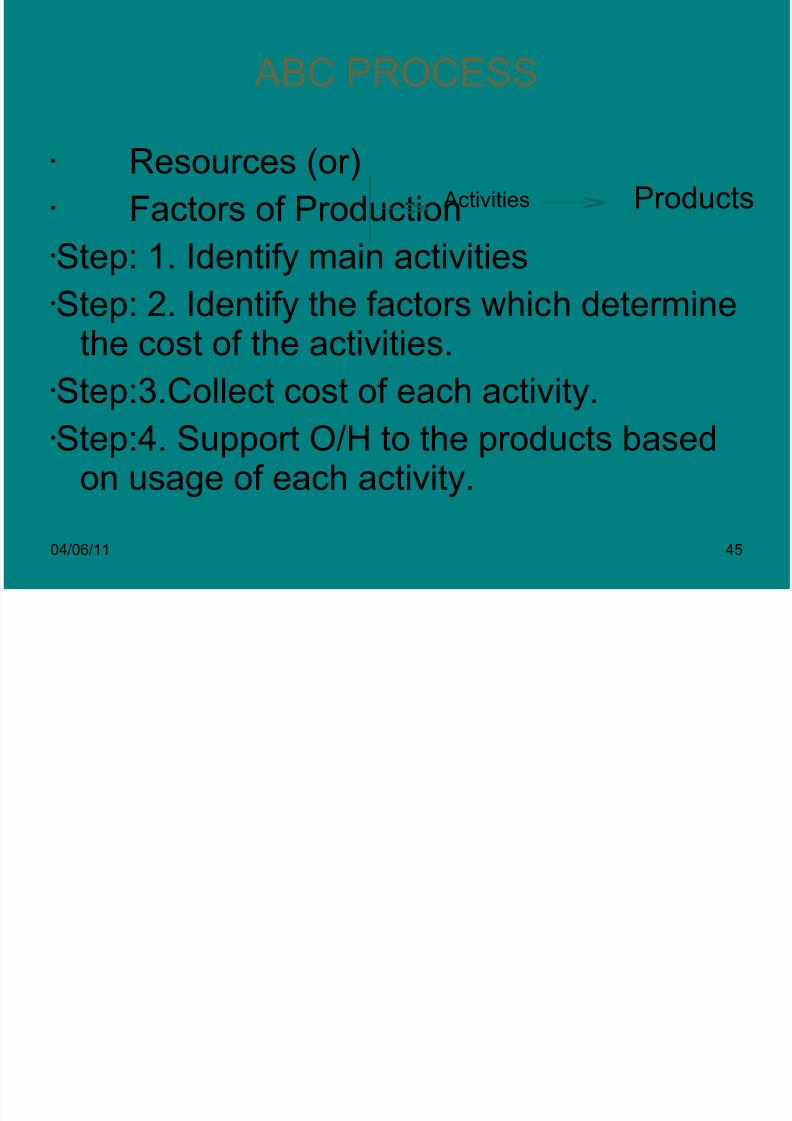

ABC PROCESS

Resources (or) Factors of ProductionStep: 1. Identify main activitiesStep: 2. Identify the factors which determine

the cost of the activities.Step:3.Collect cost of each activity.Step:4. Support O/H to the products based

on usage of each activity.

Activities Products

8/7/2019 Presentation3 for CSM

http://slidepdf.com/reader/full/presentation3-for-csm 46/207

04/06/11 46

Cost ManagementCost management is amisnomer

It is revenue and costmanagementThe objective is to enhancevalue to the firmPrice is external and cost is

internal

8/7/2019 Presentation3 for CSM

http://slidepdf.com/reader/full/presentation3-for-csm 47/207

04/06/11 47

Contemporary Cost Management

TechniquesManage cost at the point of commitmentand not at the point of incidence

Trace cost and revenue to cost objectsasmuch as possible

Cost management should be allpervasiveCost management should be made a

culture within the organisation

8/7/2019 Presentation3 for CSM

http://slidepdf.com/reader/full/presentation3-for-csm 48/207

04/06/11 48

Survival triplet

Survival Zone

Cost/Price

QualityAttributes

8/7/2019 Presentation3 for CSM

http://slidepdf.com/reader/full/presentation3-for-csm 49/207

04/06/11 49

COST DRIVERS

• Business Definition for: Cost Driver

• a factor that determines the cost of an activity.Cost drivers are analyzed as part of activitybased costing and can be used in continuous

improvement programs. They are usuallyassessed together as multiple drivers rather than singly. There are two main types of costdriver: the first is a resource driver, which refersto the contribution of the quantity of resourcesused to the cost of an activity; the second is anactivity driver, which refers to the costs incurredby the activities required to complete aparticular task or project.

8/7/2019 Presentation3 for CSM

http://slidepdf.com/reader/full/presentation3-for-csm 50/207

04/06/11 50

COST DRIVER ANALYSIS

C t D i

8/7/2019 Presentation3 for CSM

http://slidepdf.com/reader/full/presentation3-for-csm 51/207

04/06/11 51

Cost Drivers

• Manage cost drivers to manage costs

• Location of cost drivers might be differentfrom the location of cost incidence

• Map cost drivers

8/7/2019 Presentation3 for CSM

http://slidepdf.com/reader/full/presentation3-for-csm 52/207

04/06/11 52

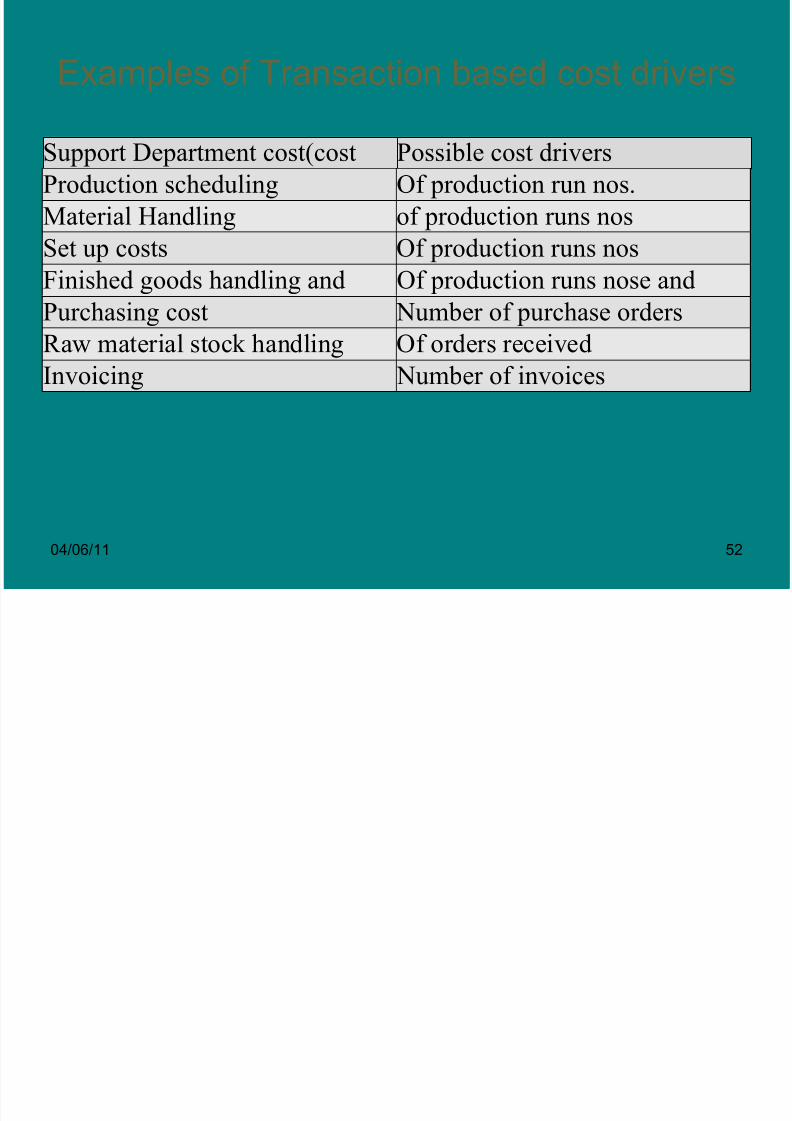

Examples of Transaction based cost drivers

Support Department cost(costpool)

Possible cost driversProduction scheduling Of production run nos.

Material Handling of production runs nos

Set up costs Of production runs nos

Finished goods handling anddispatch of goods

Of production runs nose andnumber of destinations anddeliver ordesr

Purchasing cost Number of purchase orders

Raw material stock handling Of orders received

Invoicing Number of invoices

8/7/2019 Presentation3 for CSM

http://slidepdf.com/reader/full/presentation3-for-csm 53/207

04/06/11 53

CLASSIFICATION OF ACTIVITIES IN AMANUFACTURING ORGANISATION

1. Unit level activities- activities performed wheneach unit is produced.

2. Batch level activities-. activities performed wheneach batch is produced.

3. Product level activities- activities to supportproduction of each different types of products ;maintenance and operation of equipments andtesting / engineering charges.

4. Facility level cost-general manufacturing process.These activities are common to variety of products

Cost Driver Analysis

8/7/2019 Presentation3 for CSM

http://slidepdf.com/reader/full/presentation3-for-csm 54/207

04/06/11 54

Cost Driver Analysis(concerned with analyzing cost behavior in a manner supportive to strategic choices)

Understanding cost behavior requiresidentifying the cost drivers present in anygiven situationUnderstanding cost behavior depends on

understanding the complex interplay amongthe relevant cost drivers in any givensituation

Cost Driver Categories

8/7/2019 Presentation3 for CSM

http://slidepdf.com/reader/full/presentation3-for-csm 55/207

04/06/11 55

Structural -- related to strategicchoices that drive costsExecutional – related to anorganization’s ability to executesuccessfully

Structural Cost Drivers (Related to organizational choices)

8/7/2019 Presentation3 for CSM

http://slidepdf.com/reader/full/presentation3-for-csm 56/207

04/06/11 56

(Related to organizational choices)

Scale: Investment size in manufacturing,

R&D, and marketingScope: Degree of vertical integrationExperience: Previous repetitions of currentwork

Technology: Process technologies used ateach step in value chainComplexity: Broadness of product line

Executional Cost Drivers (Related to organizational skills)

8/7/2019 Presentation3 for CSM

http://slidepdf.com/reader/full/presentation3-for-csm 57/207

04/06/11 57

(Related to organizational skills)

Work Force Involvement: participation;

empowerment; commitment to continuousimprovementCapacity Utilization: given scale choices onplant construction

Plant Layout Efficiency: compared to currentnormsProduct Configuration: design or formulationeffectiveness

Exploiting Linkages withSuppliers/Customers: in relation to the valuechain

Cost Driver Analysis – Some Key Ideas

8/7/2019 Presentation3 for CSM

http://slidepdf.com/reader/full/presentation3-for-csm 58/207

04/06/11 58

Volume is usually not the best way to explain

cost behavior More useful to explain cost position in terms of structural choices and executional skills

Not all strategic cost drivers operable or

equally important all the time but some areprobably very important in every instance

Linkages Among Value Chain Analysis, Strategic PositioningAnalysis and Cost Driver Analysis

8/7/2019 Presentation3 for CSM

http://slidepdf.com/reader/full/presentation3-for-csm 59/207

04/06/11 59

Analysis and Cost Driver Analysis

Understanding the value chain

helps define the optimal positioningstrategy

Understanding the value chain andpositioning strategy helps identifythe relevant cost drivers

8/7/2019 Presentation3 for CSM

http://slidepdf.com/reader/full/presentation3-for-csm 60/207

04/06/11 60

Advantages of ABC

• Brings accuracy and reliability in product cost determination.

• ABC provides realistic product cost where advanced manufacturingenvironment and technologies were to support overhead costs.

• ABC identifies real cost behaviour and helps in reducing cost.

• Uses multiple cost drivers most of which are transaction based and

not volume based.

• Traces cost to areas of managerial responsibility, processes,customers,depart,ent beyond product cost.

• Improve manager’s decision making.

• Provides reliable and correct product cost.

• Provides cost for cost driversand information on transaction volume.

8/7/2019 Presentation3 for CSM

http://slidepdf.com/reader/full/presentation3-for-csm 61/207

04/06/11 61

De-merits of ABC

• More complex in nature.

• Difficult to implement.

• ABC has different level of activity for different organisation.ABC in Service Organisation:

• Unlike in manufacturing organation, in sevice organisation costs aremostly fixeed and indirect and therfore ABC seems irrelevent.

•

8/7/2019 Presentation3 for CSM

http://slidepdf.com/reader/full/presentation3-for-csm 62/207

04/06/11 62

Activity LevelsActivit level Reason for activity Examples of activityUnit level Performed for each

unit of productproduced or sold

-Raw material cost-Cost of inserting acomponentUtilities cost of operations

Batch Level Performed for eachunit of product

produced or sold

Cost of processingsales order

-cost of inspection

Product Level Performed to support

each different productthat can be produced

Cost of product

developmentCost of Special M/CFacility Level Performed tomaintain general mfg.facilities

Cost of maintenance.Cost of nonspecialisecd equiment

8/7/2019 Presentation3 for CSM

http://slidepdf.com/reader/full/presentation3-for-csm 63/207

04/06/11 63

Product Differentiation

• In form-size, colour, shape, physical structure, design, coating, actiontime.

• Features.

• Performance quality

• Conformance quality.

• Durability.• Reliability.

• Style.

• Service differentiation.

• Ordering ease

• Installation.

• Customer training.

• Maintenance &repair

• Customer consulting

•

8/7/2019 Presentation3 for CSM

http://slidepdf.com/reader/full/presentation3-for-csm 64/207

04/06/11 64

Positioning Analysis

• Organizational analysis

• Organizational structure design / structurealignment

• Staffing studies

• Job analysis / job description projects

• Long-range organization planning

8/7/2019 Presentation3 for CSM

http://slidepdf.com/reader/full/presentation3-for-csm 65/207

04/06/11 65

Positioning Analysis

• Strategic positioning analysis (SPA) is developed as aspecific analytical approach consisting of a productportfolio analysis,

• Shift-share analysis and a Diversification analysis.

• The SPA describes the performance of ports andtraffic categories within ports in terms of marketshare, growth rate, diversification and value added.

• The SPA needs to be used taking into account theport's position with regard to value-added createdby the different traffic categories.

• By using this integrative instrument, indications on theoverall strategic position of ports are provided andwill benefit strategy formulation and decision-makingon port development.

•

8/7/2019 Presentation3 for CSM

http://slidepdf.com/reader/full/presentation3-for-csm 66/207

04/06/11 66

Positioning Analysis

• Predicting Relative Competitive Position of anOrganization

• Commonly used methods for analyzingcompetitive strength including SWOT (Strength,

weakness, Opportunity ,Threat)VRIO( Valuable, Rare, Imitable , Organizationready)portfolio models and competitor ranking-key success factors (KSF).

• A method for predicting relative competitiveposition of an organization is proposed todetermine a numerical relative strength score for a firm.

8/7/2019 Presentation3 for CSM

http://slidepdf.com/reader/full/presentation3-for-csm 67/207

04/06/11 67

Positioning Analysis

• To achieve maximum profitability a firm must find a way toachieve meaningful competitive advantage over itscompetitors.

• Unequal command of valuable resources forms the basis of competitive advantage for a firm.

• Competitive advantage is connected to relative competitivestrength which is the net value of a firms strengths andweaknesses comparative to benchmarks usually thestrengths and weaknesses of key industry rivals.

• Competitive analysis involves the organization looking bothinward to its internal environment as well as outward to its

competitors and other forces in the external environment.The analysis will generally include the following elements:identifying potential competitors, economic growth of thecountry, financial markets, capital markets, customer etc.

8/7/2019 Presentation3 for CSM

http://slidepdf.com/reader/full/presentation3-for-csm 68/207

04/06/11 68

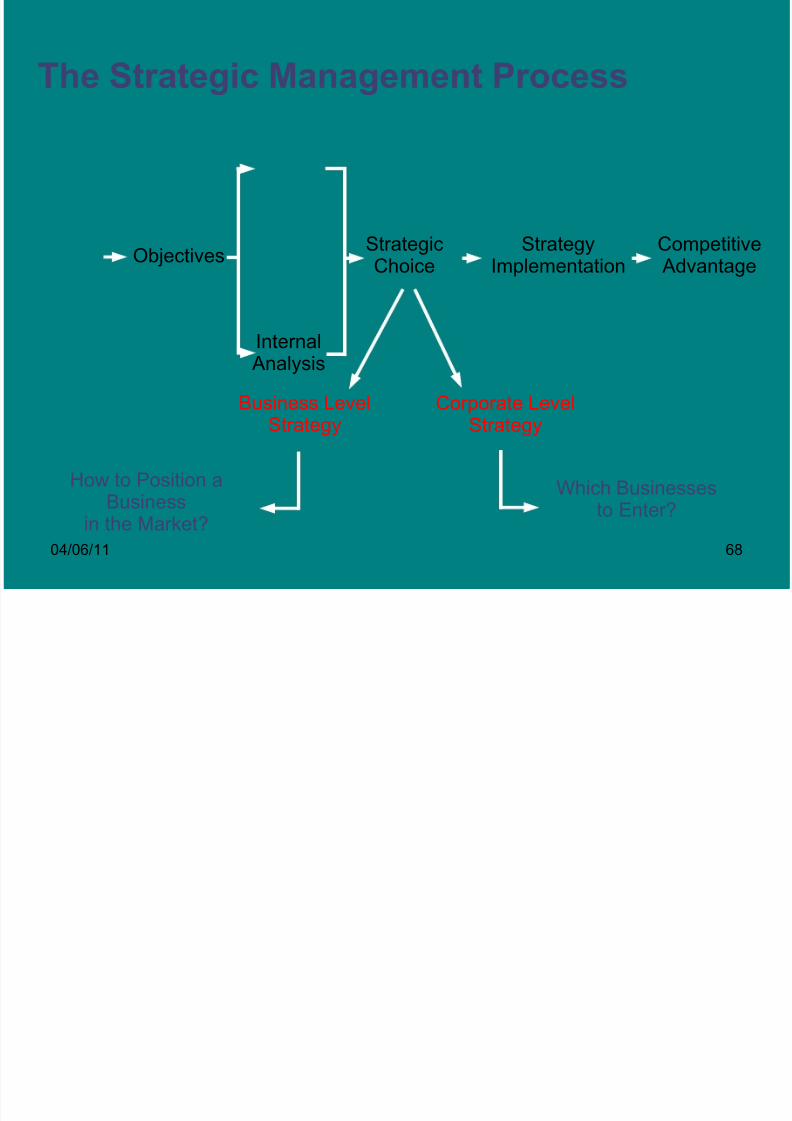

The Strategic Management Process

Objectives

InternalAnalysis

StrategicChoice

StrategyImplementation

CompetitiveAdvantage

Business Level

Strategy

Corporate Level

Strategy

How to Position aBusiness

in the Market?

Which Businessesto Enter?

8/7/2019 Presentation3 for CSM

http://slidepdf.com/reader/full/presentation3-for-csm 69/207

04/06/11 69

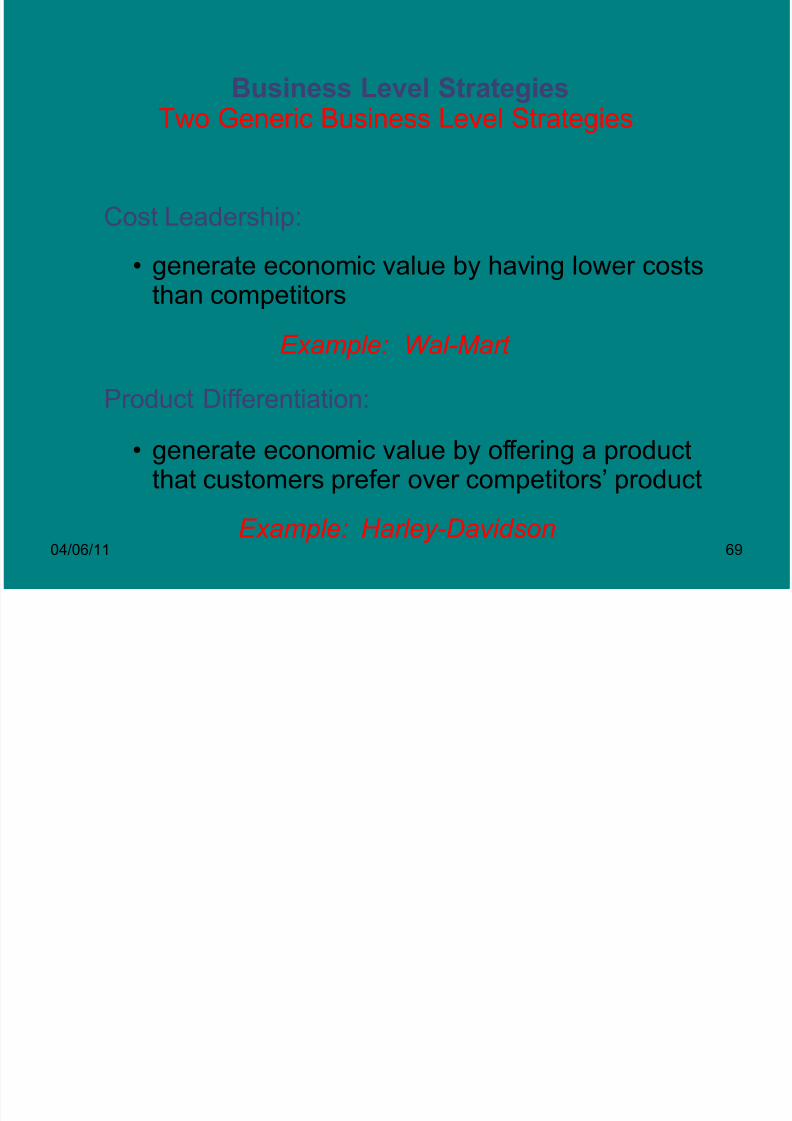

Business Level StrategiesTwo Generic Business Level Strategies

Cost Leadership:

• generate economic value by having lower costs

than competitors

Product Differentiation:

• generate economic value by offering a productthat customers prefer over competitors’ product

Example: Wal-Mart

Example: Harley-Davidson

8/7/2019 Presentation3 for CSM

http://slidepdf.com/reader/full/presentation3-for-csm 70/207

04/06/11 70

Understanding Cost Advantage

Managers need to understand who hasthe cost advantage in their market

• it could be the focal firm

• it could be a competitor

• develop a strategy to exploit the advantage

• develop a strategy to either capture theadvantage or compete on some other basis

Sources of Cost Advantage

8/7/2019 Presentation3 for CSM

http://slidepdf.com/reader/full/presentation3-for-csm 71/207

04/06/11 71

Sources of Cost Advantage

Economies of Scale

• average cost per unit falls as quantity increases-until the minimum efficient scale is reached

• are a cost advantage because competitors maynot be able to match the scale because of capitalrequirements (barrier to entry)

• international expansion may allow a firm to haveenough sales to justify investing in additionalcapacity to capture economies of scale

8/7/2019 Presentation3 for CSM

http://slidepdf.com/reader/full/presentation3-for-csm 72/207

04/06/11 72

• are an advantage for those who do not havediseconomies of scale

• are a risk of international expansion

Learning Curve Economies

8/7/2019 Presentation3 for CSM

http://slidepdf.com/reader/full/presentation3-for-csm 73/207

04/06/11 73

Learning Curve Economies

• a firm gets more efficient at a process with experience

• the more complicated/technical the process,the greater the experience advantage

Example: Fuel Injectors

• international expansion may propel a firm down theexperience curve because of higher volumes

Differential Low-Cost Access to Productive Inputs

8/7/2019 Presentation3 for CSM

http://slidepdf.com/reader/full/presentation3-for-csm 74/207

04/06/11 74

Differential Low Cost Access to Productive Inputs

• may result from:

• history—being in the right place at the right time

• being first into a market—esp. foreign markets

• natural endowment—owning a mineral deposit

• locking up a source—buying all of its output

Example: Quantity Carpet Buys

8/7/2019 Presentation3 for CSM

http://slidepdf.com/reader/full/presentation3-for-csm 75/207

04/06/11 75

Cost-leadership Strategy

• Do everything to achieve a CA through producingproducts or services at a lower unit cost (loweringcost structure) charge a lower price.

•

• Increase efficiency and lower costs – the

manufacturing and materials managementfunctions are the center of attention

•

• A low-level of product differentiation – it means thatyou do not want to be the industry leader indifferentiation.

•

• Target the average customer – Scale and Focus,not Product Variety

- ignores the different market segments –focuses on mass market.

Technology Independent of Scale

8/7/2019 Presentation3 for CSM

http://slidepdf.com/reader/full/presentation3-for-csm 76/207

04/06/11 76

Technology Independent of Scale

Example: Vegetable Inspection

• may allow small firms to become cost competitive

• advantage typically accrues to the ‘owner’ of thetechnology—may or may not be the ones who actuallyuse the technology

• size of the advantage depends both on how valuableand protectable the technology is

8/7/2019 Presentation3 for CSM

http://slidepdf.com/reader/full/presentation3-for-csm 77/207

04/06/11 77

Policy Choices

• firms get to choose how they will serve the market

• we’ll offer level of quality that is inexpensive toproduce

• firms can make policy choices that give peopleincentives to reduce cost at every opportunity

Example: Deccan Airways

8/7/2019 Presentation3 for CSM

http://slidepdf.com/reader/full/presentation3-for-csm 78/207

8/7/2019 Presentation3 for CSM

http://slidepdf.com/reader/full/presentation3-for-csm 79/207

04/06/11 79

Value of a Cost Advantage

Rivalry

Entry Buyers

SuppliersSubstitutes

• increases capitalrequirementsfor entrants

• competitors rationallyavoid price competition

• limitsattractivenessof substitutes

• increasesimportance of the

focal firm to thesupplier

• lowers incentivesfor buyers to

verticallyintegrate

8/7/2019 Presentation3 for CSM

http://slidepdf.com/reader/full/presentation3-for-csm 80/207

04/06/11 80

Rareness of aCost Advantage The rareness of a source of cost advantage

depends heavily on the industry life cycle:

Economies of Scale

Diseconomies of Scale

Learning Curve Economies

Technology

Differential Input Access

Not Rare Rare

Emerging Mature

Rare Rare

Not RareRare

Rare Rare

Not RareRare

Rare Rare

Generally…

8/7/2019 Presentation3 for CSM

http://slidepdf.com/reader/full/presentation3-for-csm 81/207

04/06/11 81

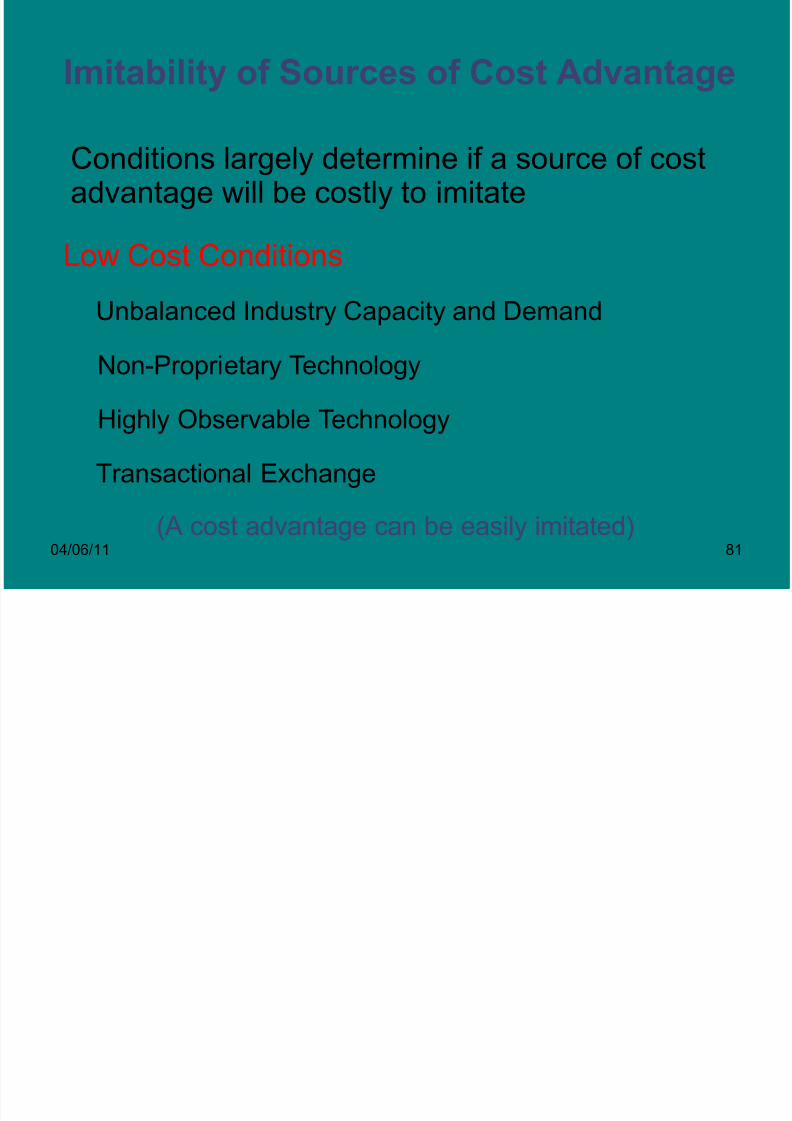

Imitability of Sources of Cost Advantage

Conditions largely determine if a source of costadvantage will be costly to imitate

Low Cost Conditions

Unbalanced Industry Capacity and Demand

Non-Proprietary Technology

Highly Observable Technology

Transactional Exchange

(A cost advantage can be easily imitated)

Implementing a Cost Leadership Strategy

8/7/2019 Presentation3 for CSM

http://slidepdf.com/reader/full/presentation3-for-csm 82/207

04/06/11 82

p g p gy

High Cost Conditions

Balanced Industry Capacity and Demand

Path Dependence (Historical Uniqueness)

Protected Technology

Highly Unobservable Technology (Causal Ambiguity)

Relational Exchange (Social Complexity)

(A cost advantage cannot be easily imitated)

A strategy is only as good as its

8/7/2019 Presentation3 for CSM

http://slidepdf.com/reader/full/presentation3-for-csm 83/207

04/06/11 83

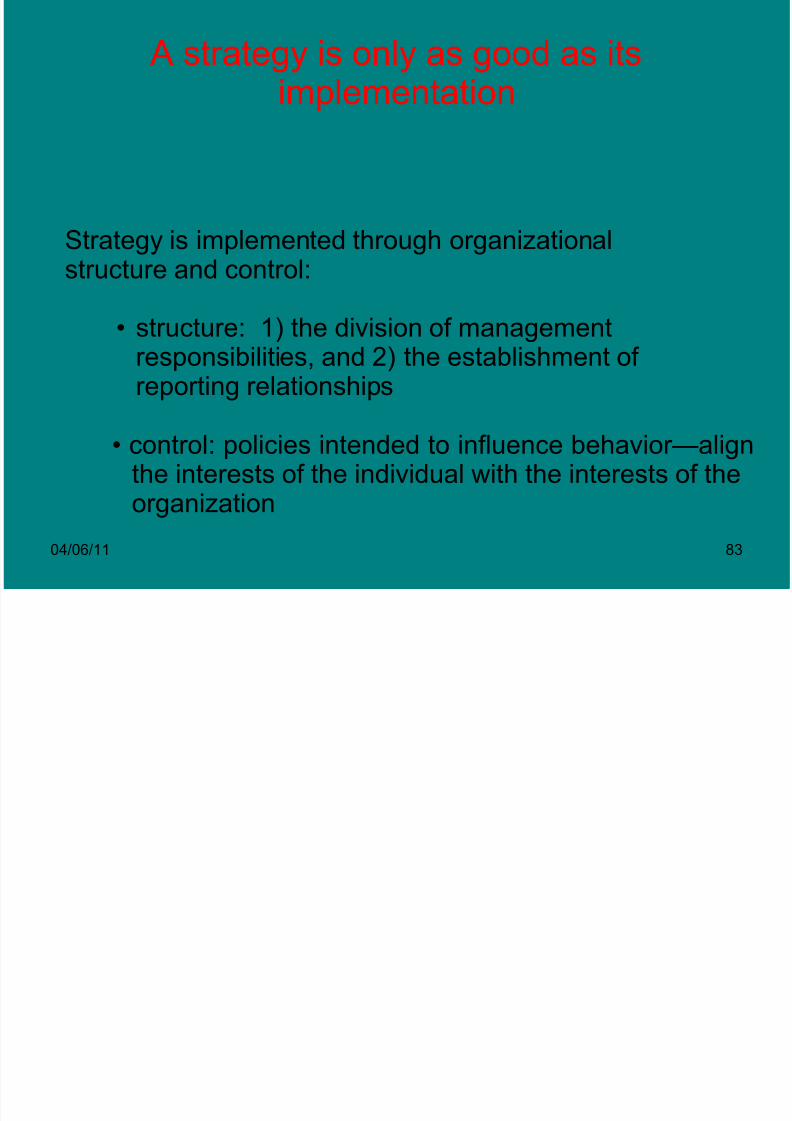

A strategy is only as good as itsimplementation

Strategy is implemented through organizationalstructure and control:

• structure: 1) the division of managementresponsibilities, and 2) the establishment of reporting relationships

• control: policies intended to influence behavior—alignthe interests of the individual with the interests of theorganization

O i ti l St t

8/7/2019 Presentation3 for CSM

http://slidepdf.com/reader/full/presentation3-for-csm 84/207

04/06/11 84

Organizational Structure

Three Organizational Structures

Simple

Functional

Multi-Divisional

8/7/2019 Presentation3 for CSM

http://slidepdf.com/reader/full/presentation3-for-csm 85/207

04/06/11 85

Simple Structure

Owner / Manager

• Owner/Manager makes all major decisionsdirectly and monitors all activities

• difficult to maintain this structure as the firmgrows in size and complexity

8/7/2019 Presentation3 for CSM

http://slidepdf.com/reader/full/presentation3-for-csm 86/207

04/06/11 86

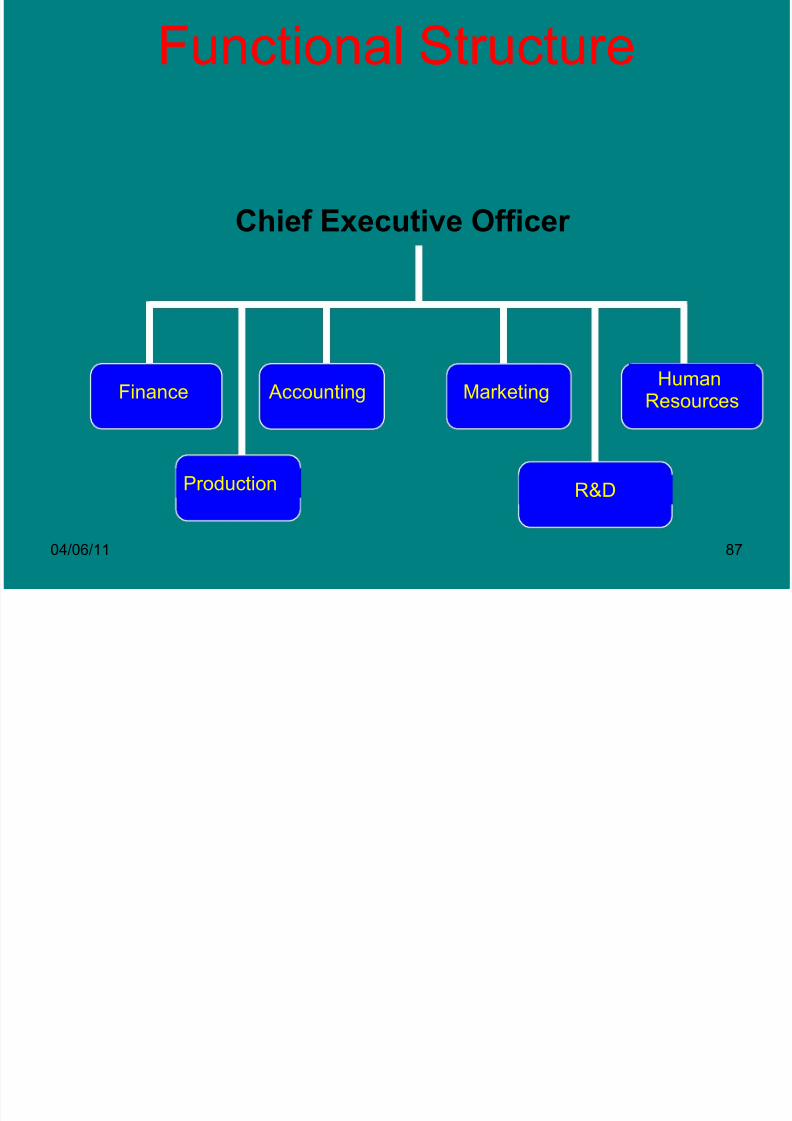

Functional Structure (U-Form: Unitary)

• divides management responsibilities by function

• marketing

• finance

• accounting

• procurement

• production

• R&D

• HR

• logistics

• etc.

• CEO is the only executive with enterprise-wideperspective

• CEO is responsible for strategy & coordinationof functions

Functional Structure

8/7/2019 Presentation3 for CSM

http://slidepdf.com/reader/full/presentation3-for-csm 87/207

04/06/11 87

Functional Structure

Production

Finance

R&D

Accounting MarketingHuman

Resources

Chief Executive Officer

8/7/2019 Presentation3 for CSM

http://slidepdf.com/reader/full/presentation3-for-csm 88/207

04/06/11 88

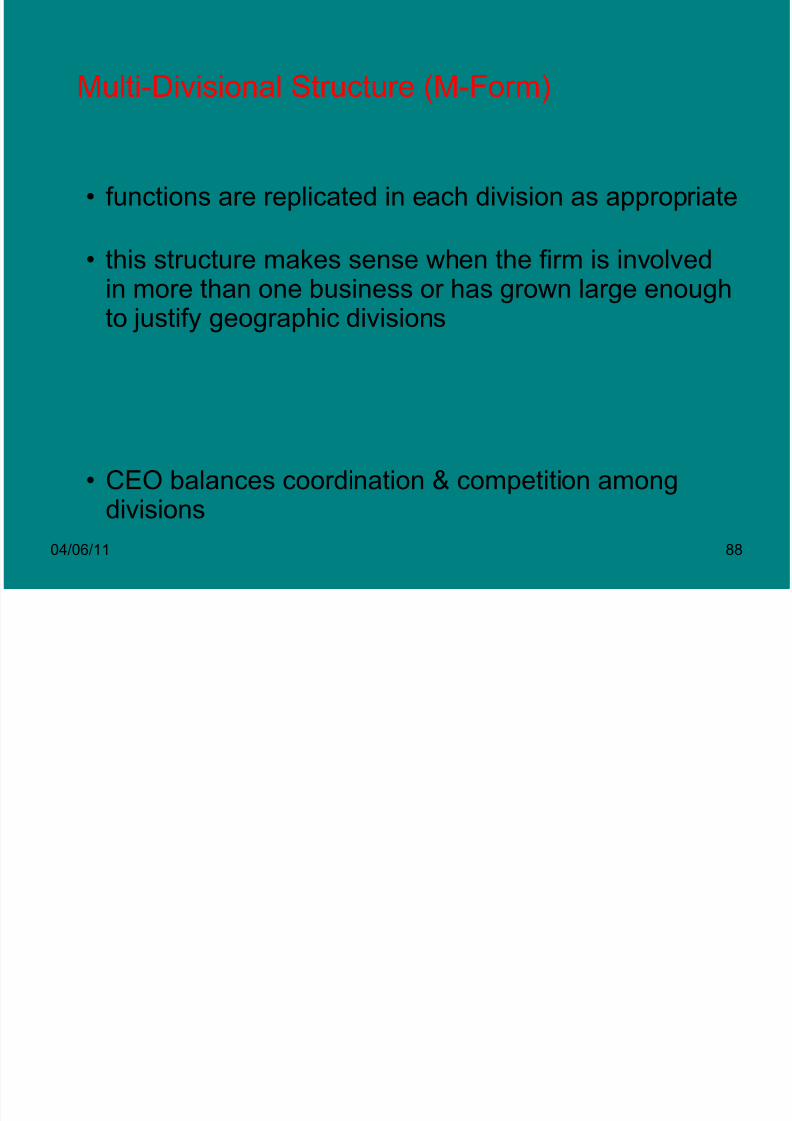

Multi-Divisional Structure (M-Form)

• functions are replicated in each division as appropriate

• this structure makes sense when the firm is involved

in more than one business or has grown large enoughto justify geographic divisions

• CEO balances coordination & competition amongdivisions

8/7/2019 Presentation3 for CSM

http://slidepdf.com/reader/full/presentation3-for-csm 89/207

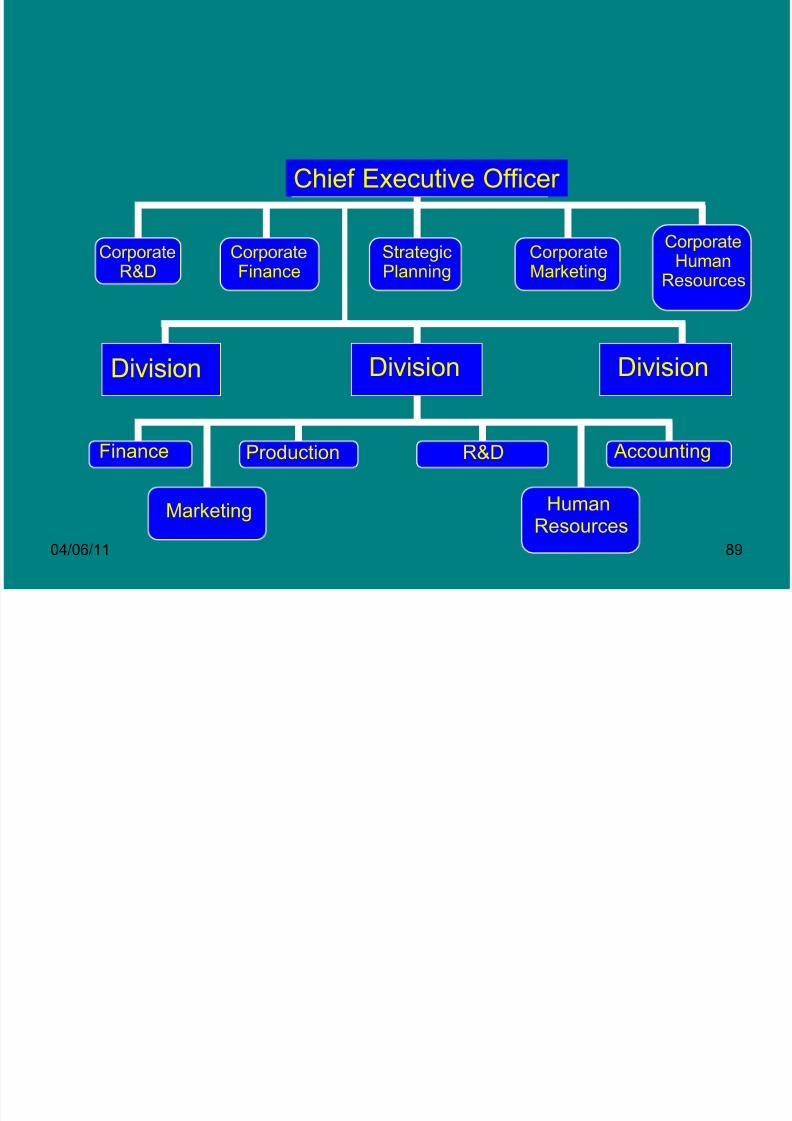

04/06/11 89

StrategicPlanning

CorporateFinance

CorporateR&D

CorporateMarketing

ProductionFinance R&D Accounting

HumanResources

Division Division Division

Marketing

Chief Executive Officer

CorporateHuman

Resources

The Functional Structure and Cost

8/7/2019 Presentation3 for CSM

http://slidepdf.com/reader/full/presentation3-for-csm 90/207

04/06/11 90

The Functional Structure and CostLeadership

• specialization within functions facilitates cost reduction

• CEO can use this structure to:

• ensure best cost reduction practices areshared among divisions

• allow and encourage decision-making by thosewho are in the best positions to do so—those

close to decisions

• ensure that functions are coordinating efforts inpursuit of a common strategy

O C

8/7/2019 Presentation3 for CSM

http://slidepdf.com/reader/full/presentation3-for-csm 91/207

04/06/11 91

Organizational Controls

Policies intended to influence behavior by aligningthe interests of the individual with the interests of the organization

Management Controls

Formal Informal

• culture• budgeting policies

• credit policies

• spending policies• travel policies

• purchasing policies

• attitudes

• leadership styles

8/7/2019 Presentation3 for CSM

http://slidepdf.com/reader/full/presentation3-for-csm 92/207

04/06/11 92

Compensation Policies

• stock options

• bonuses based on:• cost reduction

• financial performance

• non-monetary awards

• vacations

• parking places

Compensation Policies Should ReinforceFormal and Informal Management Controls

• office decor

8/7/2019 Presentation3 for CSM

http://slidepdf.com/reader/full/presentation3-for-csm 93/207

04/06/11 93

Organizational Controls and Cost Leadership

• management controls and compensationpolicies can be focused on cost reduction

• supply contracts that stipulate cost reductionsover time

• tight credit policies

• austere travel policies (e.g., no first class)

• bonuses tied to cost reduction targets

Example: Wal-Mart & Southwest Airlines

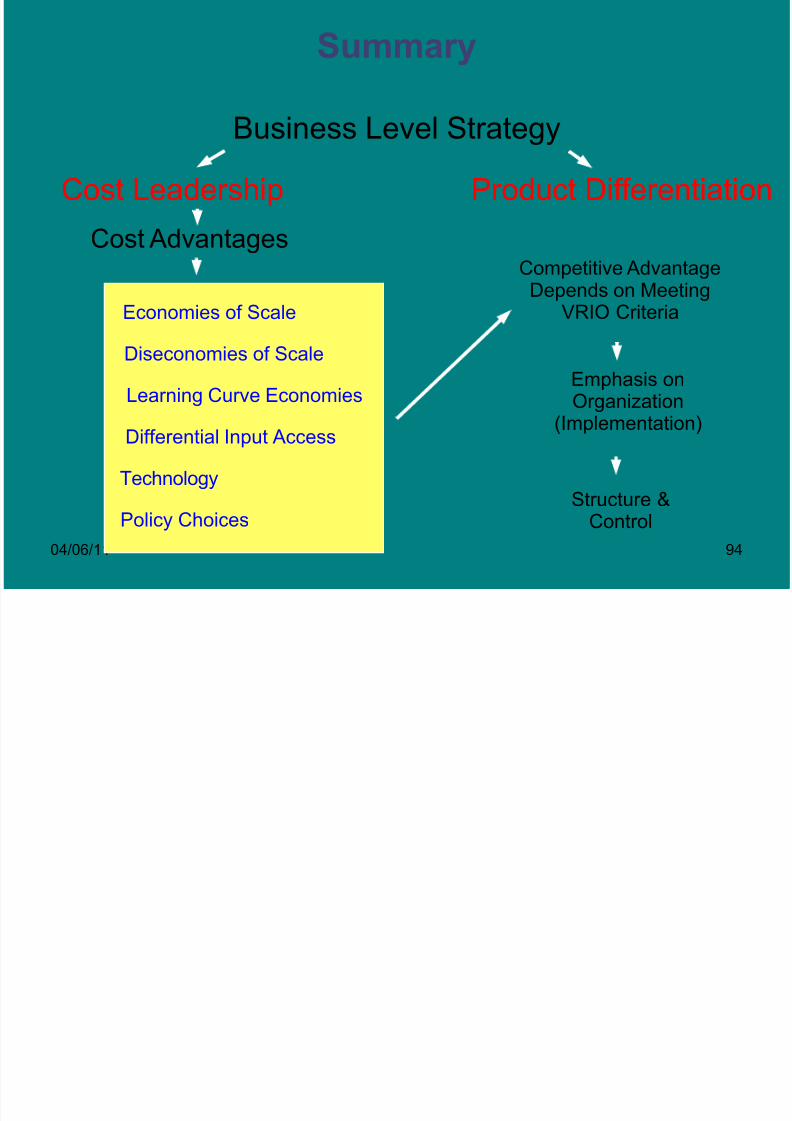

Summary

8/7/2019 Presentation3 for CSM

http://slidepdf.com/reader/full/presentation3-for-csm 94/207

04/06/11 94

Business Level Strategy

Cost Leadership Product Differentiation

Cost Advantages

Economies of Scale

Diseconomies of Scale

Learning Curve Economies

Differential Input Access

Technology

Policy Choices

Competitive Advantage

Depends on MeetingVRIO Criteria

Emphasis onOrganization

(Implementation)

Structure &Control

Advantages and Disadvantages of

8/7/2019 Presentation3 for CSM

http://slidepdf.com/reader/full/presentation3-for-csm 95/207

04/06/11 95

g gCost-leadership Strategy

• Advantages - charge a lower price yet make the same

level of profit. - win in the price war. - low-cost as an entry barrier. - protected from rivals. - less affected by powerful buyers and

suppliers. - room to reduce its price to compete with

substitute products.

•

8/7/2019 Presentation3 for CSM

http://slidepdf.com/reader/full/presentation3-for-csm 96/207

04/06/11 96

• Disadvantages - technological advancement makes the low

cost advantage outdated. - imitation ability of competitors. - lose sight of changes in customers’ tastes

•

Differentiation Strategy

8/7/2019 Presentation3 for CSM

http://slidepdf.com/reader/full/presentation3-for-csm 97/207

04/06/11 97

Differentiation Strategy

• Do everything to achieve a CA through producingproducts or services that are unique to customers charge a premium price.

•

• Achieved in 3 principal ways – quality, innovation, &

responsiveness to customers•

• Try to differentiate along as many dimensions aspossible – the bases of differentiation are endless(prestige, status,…)

•

• R&D, Sales, & Marketing functions are center of attention.

•

• Serve many market segments (i.e., a broad

Advantages and Disadvantages of

8/7/2019 Presentation3 for CSM

http://slidepdf.com/reader/full/presentation3-for-csm 98/207

04/06/11 98

g gDifferentiation Strategy

• Advantages - Premium price.

- Protected from rivals. (i.e., brand loyalty,customer loyalty..)

- Brand loyalty as an entry barrier.

- Less affected by powerful buyers andsuppliers.

•

8/7/2019 Presentation3 for CSM

http://slidepdf.com/reader/full/presentation3-for-csm 99/207

04/06/11 99

• Disadvantages - Substitutes can be a possible threat.

- Difficult to maintain a product’s uniquenessin customers’ eyes for a long time.

Focus Strategy

8/7/2019 Presentation3 for CSM

http://slidepdf.com/reader/full/presentation3-for-csm 100/207

04/06/11 100

Focus Strategy

• Try to achieve a CA by serving the needs of a specificmarket segment or niche (i.e. geographically, productline, customer type,..).

•

• Pursue a focus strategy through either a low-cost

approach or a differentiation - focused cost-leadership - focused differentiation (i.e., a specialized

differentiator)

•

• Try to build market share in one or a few marketsegments and, if successful, then begin to serve moresegments.

•

• Pursue any distinctive competency

Advantages and Disadvantages of

8/7/2019 Presentation3 for CSM

http://slidepdf.com/reader/full/presentation3-for-csm 101/207

04/06/11 101

Focused Strategy

• Advantages - Exploration of a gap in the market

customer loyalty.

- Stay close to its customers and respond totheir changing needs. (faster in innovations).

- In general, a focused firm is O.K. againstthe threats of five forces.

•

8/7/2019 Presentation3 for CSM

http://slidepdf.com/reader/full/presentation3-for-csm 102/207

04/06/11 102

• Disadvantages - Cost disadvantage relative to low-cost

leader b/c of a small volume.

- Susceptible to attack from a broaddifferentiator.

- Technological change or changes incustomers’ tastes can make a niche marketdisappear.

•

Just-in time system

8/7/2019 Presentation3 for CSM

http://slidepdf.com/reader/full/presentation3-for-csm 103/207

04/06/11 103

Just-in time system

• The star recognition of Japan's distinguishing features.• The most distinctive feature of Japan is the lack of natural

resources, which makes it necessary to import vast amounts of materials

including food.

• The second distinctive feature is that Japanese concept of work,such

as consciousness and attitude, differed from that held by theEuropean and

American workers. The Japanese traits include: (

• 1) group consciousness, sense of equality, desire to improve, and

diligence born from !L long history of' a homogeneous race;• (2) high degree of ability resulting from higher education brought by desire to improve;

• (3) centering their daily living around work.

8/7/2019 Presentation3 for CSM

http://slidepdf.com/reader/full/presentation3-for-csm 104/207

04/06/11 104

• Upon recognition of the matters related above, Toyota planned andfollowed the following two basic concepts:

• Attain low cost production is "reduction of cost through elimination of waste".

• This involves making up a system that will thoroughly eliminatewaste by assuming that anything other than the minimum amount

of equipment, materials, parts, and workers (working time) whichare absolutely essential to production are merely surplus thatonly raises the cost.

• The second recognition of Japanese diligence, high degree of ability, and favoured labour environment is " to make full use of the workers' capabilities". In short, treat the workers as human

beings and with consideration. Build up a system that will allowthe workers to and with consideration. Build up a system that willallow the workers to display their full capabilities by themselves

•

•

•

8/7/2019 Presentation3 for CSM

http://slidepdf.com/reader/full/presentation3-for-csm 105/207

04/06/11 105

• Cost cutting by through removal of waste• Just in time production:

• shorten the lead time from the entry of materials

• to the completion of vehicle. by maintainingthe conformity to changes by having " allprocesses produce the necessary parts at

the necessary time and have on hand onlythe minimum stock necessary to hold theprocesses together".

• In addition, by checking the degree of

inventory quantity and production lead time

8/7/2019 Presentation3 for CSM

http://slidepdf.com/reader/full/presentation3-for-csm 106/207

04/06/11 106

• Withdrawal by subsequent processes: The first requirement of just-in-time production is to enableall processes to quickly gain accurate knowledgeof , timing and quantity required'.

• In order to materialize the first requirement, Toyota

adopted a reverse method of " the following processwithdrawing the parts from the preceding process "instead of the "the preceding process supplying theparts to the following process ".

• The reason for this is as follows: Just-in-timeproduction is production of parts by the variousprocesses in the necessary amounts at necessarytiming for assembling a vehicle as a final product of the company.

•

•

8/7/2019 Presentation3 for CSM

http://slidepdf.com/reader/full/presentation3-for-csm 107/207

04/06/11 107

• One piece production and conveyance:The second requirement of justin-timeproduction is that all processes

approach the condition where eachprocess can produce only one piece,can convey it one at a time, and inaddition, have only one piece in stock

both between the equipment and theprocesses.

• This means that no process for any

reason is allowed to produce extra

8/7/2019 Presentation3 for CSM

http://slidepdf.com/reader/full/presentation3-for-csm 108/207

04/06/11 108

• Leveling of production: Provided that all processes perform small lot process variesconsiderably, the processes within thecompany as well as the production and

conveyance, if the quantity to be withdrawnby the subsequent subcontractors willmaintain peak capacity or holdingexcessive inventory at subcontractors willmaintain peak capacity or holding

excessive inventory at all times.• Therefore, in order to make a just-in-time

production possible, the prerequisite will beto level the production at the. finalassembly line (the most important line that

ives out the roduction instructions to all

8/7/2019 Presentation3 for CSM

http://slidepdf.com/reader/full/presentation3-for-csm 109/207

8/7/2019 Presentation3 for CSM

http://slidepdf.com/reader/full/presentation3-for-csm 110/207

04/06/11 110

• Jidoka: The term' Jidoka' as used at Toyota means' to make the equipmentor operation stop whenever an abnorm

al or defective condition arises '.• In short, its distinctive feature lies in the

fact that when an equipment trouble or machining defect happens, the

equipment or entire line stops, and anyline with workers can be stopped bythem.

•

8/7/2019 Presentation3 for CSM

http://slidepdf.com/reader/full/presentation3-for-csm 111/207

04/06/11 111

• The reasons for' Jidoka ' being so important are asfollows:

• (1) To prevent making too much. If the equipment ismade to stop

when the required amount is produced, making too

much cannot arise.• Consequently, the just-in-time production can be

accurately carried out.

• (2) Control of abnormality becomes easy. It will only'be necessary to

make improvements by directing attention to thestopped equipment

• and the worker who did the stopping. This is animportant requirement when making up the systemof ' full utilization of workers'

8/7/2019 Presentation3 for CSM

http://slidepdf.com/reader/full/presentation3-for-csm 112/207

8/7/2019 Presentation3 for CSM

http://slidepdf.com/reader/full/presentation3-for-csm 113/207

04/06/11 113

• Considerations to workers' safety:• Self-display of workers' ability:

• Aim of Kanban System

• A production control system for just-in-time production and making full use of workers' capabilities is the Kanban

System• . Utilizing Kanban System, workshops of

Toyota have no longer relied upon anelectronic computer.

8/7/2019 Presentation3 for CSM

http://slidepdf.com/reader/full/presentation3-for-csm 114/207

04/06/11 114

• The reasons to have employedKanbanSystem instead. of computerizedsystem are as follows:

• (1) Reduction of cost processing information.

• (2) Rapid and precise acquisition of facts.

• (3) Limiting surplus

• 3.2 Description of Kanban system

• (I) In the Kanban System, a form of order card called Kanban is used. These come intwo kinds, one of which is called'conveyance Kanban ' that is carried when

going from one process to the preceding

8/7/2019 Presentation3 for CSM

http://slidepdf.com/reader/full/presentation3-for-csm 115/207

04/06/11 115

• , production Kanban' and is used to order production of the portion withdrawn by thesubsequent process.

• These two kinds of Kanban are always attached tothe containers holding parts.

• (2) When content of a container begins to beused, conveyance Kanban is removed from thecontainer. A worker takes this conveyanceKanban and goes to the stock point of thepreceding process to pick up this part.

• He then attaches this conveyance Kanban to thecontainer holding this part.

8/7/2019 Presentation3 for CSM

http://slidepdf.com/reader/full/presentation3-for-csm 116/207

04/06/11 116

• (3) Then, the' production Kanban 'attached to the container is removedand becomes a dispatching information

for the process. They produce the part toreplenish it withdrawn as early aspossible

• (4) Thus, the production activities of the

final assembly line are connected in amanner like a chain to the precedingprocesses or to the subcontractors and

materialize the just-in-time production of

8/7/2019 Presentation3 for CSM

http://slidepdf.com/reader/full/presentation3-for-csm 117/207

04/06/11 117

• In the past, economic assessment of alternative

designs, constructions, or other

investments has been based on initial (first) cost which ignores

the total cost

incurred for the investment throughout itslifetime.

• The concept of life cycle costing providesan

LIFE CYCLE COSTING

8/7/2019 Presentation3 for CSM

http://slidepdf.com/reader/full/presentation3-for-csm 118/207

04/06/11 118

• Life Cycle Costing (LCC) also called Whole Life Costing is atechnique to establish the total cost of ownership. It is astructured approach that addresses all the elements of this costand can be used to produce a spend profile of the product or service over its anticipated life-span. The results of an LCC

analysis can be used to assist management in the decisionmakingprocess where there is a choice of options. The accuracy

• of LCC analysis diminishes as it projects further into the future,so it is most valuable as a comparative tool when long termassumptions apply to all the options and consequently have thesame impact.This briefing provides general guidance on LCC.

8/7/2019 Presentation3 for CSM

http://slidepdf.com/reader/full/presentation3-for-csm 119/207

8/7/2019 Presentation3 for CSM

http://slidepdf.com/reader/full/presentation3-for-csm 120/207

04/06/11 120

• The life cycle costing can be defined asfollows:

an economic assessment of alternatives

designs,construction, or other investment

considering all

significant costs of initial costs andownership costsover economic life of each alternative,

expressed in

8/7/2019 Presentation3 for CSM

http://slidepdf.com/reader/full/presentation3-for-csm 121/207

04/06/11 121

Introduction Growth Maturity Saturation Decline

Small number of innovativecustomers

Imitators/customersunwilling to

change

Increase incompetitiveproducts

Pressure for new product

TechnologyChangePrefer security

of tried brandsMarketbroadened

Marketleadership

under pressure

Profit fall Change infashion/

tastesDifficulties ineffectivedistribution

Productimprovements

Costeconomiesused up

Intensifiedmarketingeffortprolong

ReducedprofitabilityTechnical

problemsDistributorsincrease.

Prices soften

LimitedCapacity

Product Life Cycle and Cost control

8/7/2019 Presentation3 for CSM

http://slidepdf.com/reader/full/presentation3-for-csm 122/207

04/06/11 122

y

• The life cycle costing analysis can not be carried out without considering the followings:

• A - Total Costs

• B - The concept of the time value of money

• A - Total Costs- Initial costs- Owner costs

• Initial costs. They include the followings:- initial construction costs- design costs-and costs-finance costs

Product Life Cycle and Cost control

8/7/2019 Presentation3 for CSM

http://slidepdf.com/reader/full/presentation3-for-csm 123/207

04/06/11 123

y

• Product life cycle costing is the process of enhancing control over manufacturing costs during different product life stages .

• It is therefore necessary to track and measure cost at every stage.LCCused to provide long term profitability of the product

• What are product life cycle cost?

1. Acquisition Cost- Research. Design testing, production, construction or

purchase of capital equipment.2. Transportation and handling costs.

3. Equipment maintenance cost.

4. Operation costs.

5. Training costs.

6. Inventory costs.

7. Technical costs.

8. Retirement and disposal costs.

9.

10.

11.

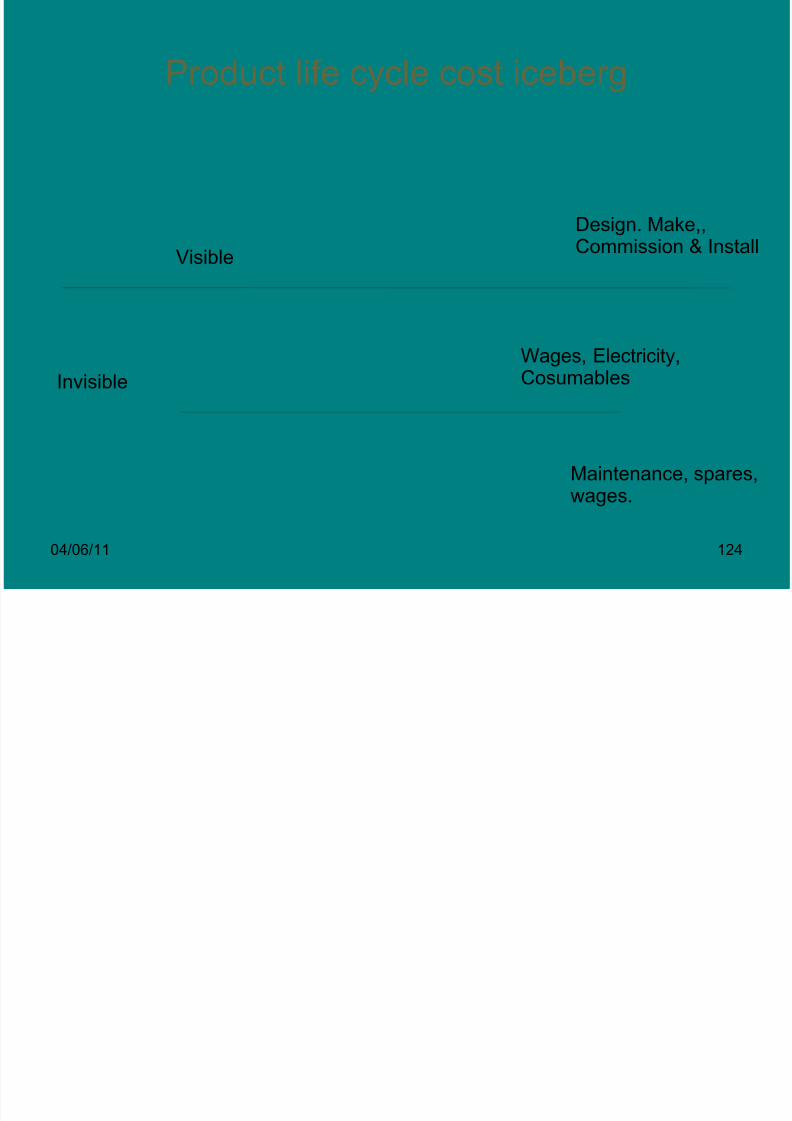

Product life cycle cost iceberg

8/7/2019 Presentation3 for CSM

http://slidepdf.com/reader/full/presentation3-for-csm 124/207

04/06/11 124

y g

Visible

Invisible

Design. Make,,Commission & Install

Wages, Electricity,Cosumables

Maintenance, spares,wages.

8/7/2019 Presentation3 for CSM

http://slidepdf.com/reader/full/presentation3-for-csm 125/207

04/06/11 125

•

•

• Life cycle cost: sum of money expended in termsof labor, materials, use of equipment, etc to

produce a product or service during the lifecycle

• Management related costs: research anddevelopment

• Design related costs

8/7/2019 Presentation3 for CSM

http://slidepdf.com/reader/full/presentation3-for-csm 126/207

04/06/11 126

• Design related costs (Cost Breakdown Structure)• Production and construction cost

• Manufacturing management, manufacturing, quality control,initial logistic support …

• Operation and support cost (the most significant andthe most difficult to predict)• Product operation, product distribution, product maintenance,inventory inventory…

• Retirement and disposal cost (difficult to assessquantitatively)

• Disposal of non non-repairable, product retirement, documentation

•

8/7/2019 Presentation3 for CSM

http://slidepdf.com/reader/full/presentation3-for-csm 127/207

8/7/2019 Presentation3 for CSM

http://slidepdf.com/reader/full/presentation3-for-csm 128/207

04/06/11 128

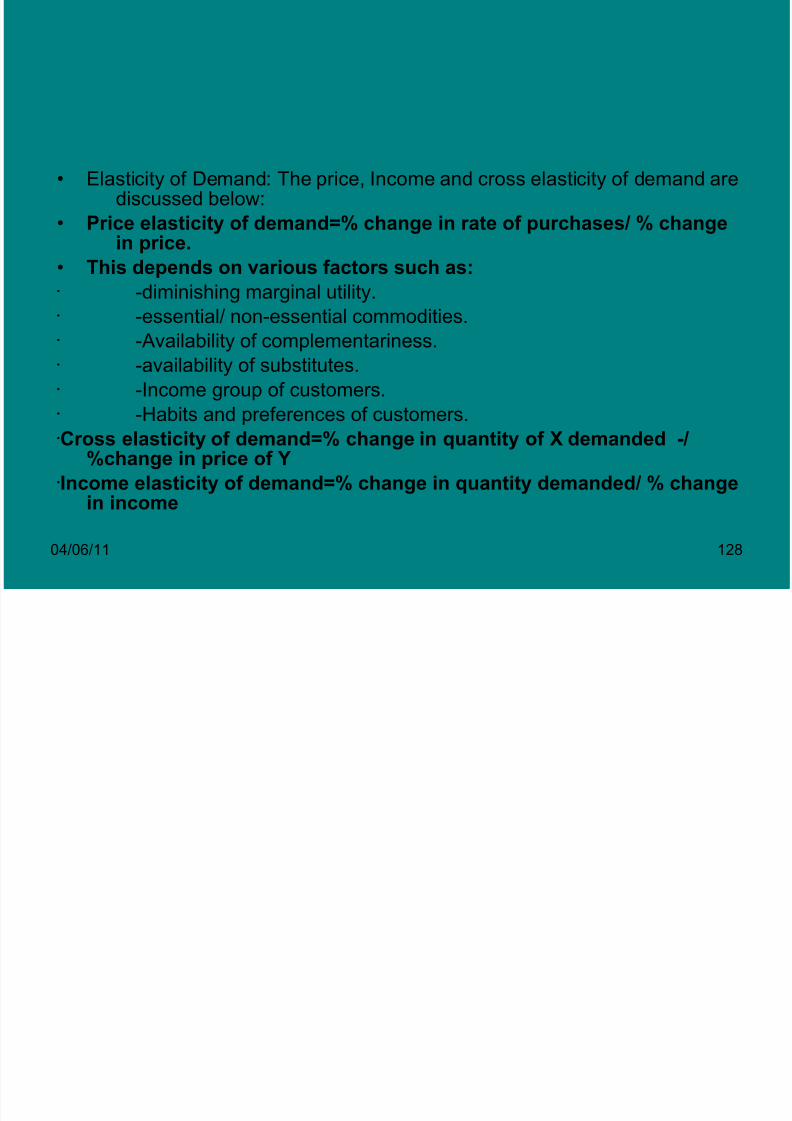

• Elasticity of Demand: The price, Income and cross elasticity of demand arediscussed below:

• Price elasticity of demand=% change in rate of purchases/ % changein price.

• This depends on various factors such as:

-diminishing marginal utility. -essential/ non-essential commodities. -Availability of complementariness. -availability of substitutes. -Income group of customers. -Habits and preferences of customers.Cross elasticity of demand=% change in quantity of X demanded -/

%change in price of YIncome elasticity of demand=% change in quantity demanded/ % change

in income

8/7/2019 Presentation3 for CSM

http://slidepdf.com/reader/full/presentation3-for-csm 129/207

8/7/2019 Presentation3 for CSM

http://slidepdf.com/reader/full/presentation3-for-csm 130/207

04/06/11 130

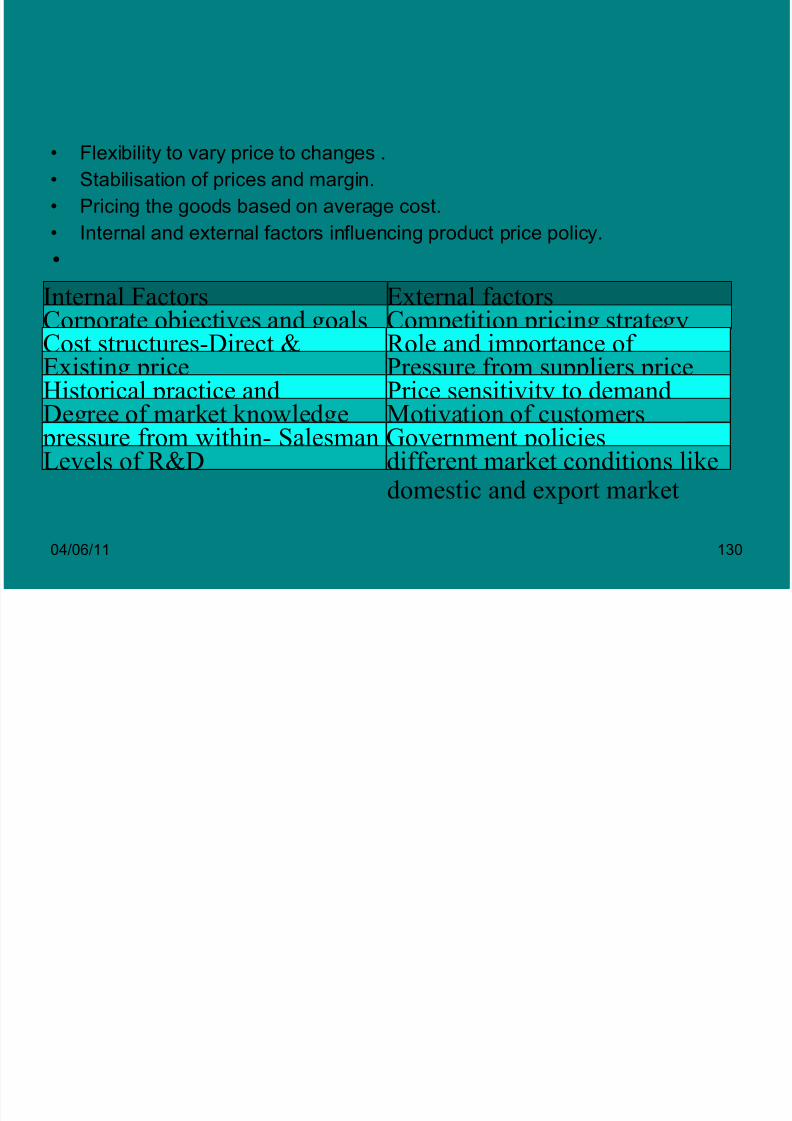

• Flexibility to vary price to changes .• Stabilisation of prices and margin.

• Pricing the goods based on average cost.

• Internal and external factors influencing product price policy.

•

Internal Factors External factorsCorporate objectives and goals Competition pricing strategyCost structures-Direct &Indirect

Role and importance of distributor Existing price Pressure from suppliers price

Historical practice andprecedent

Price sensitivity to demandDegree of market knowledge Motivation of customers

pressure from within- Salesman Government policiesLevels of R&D different market conditions like

domestic and export market

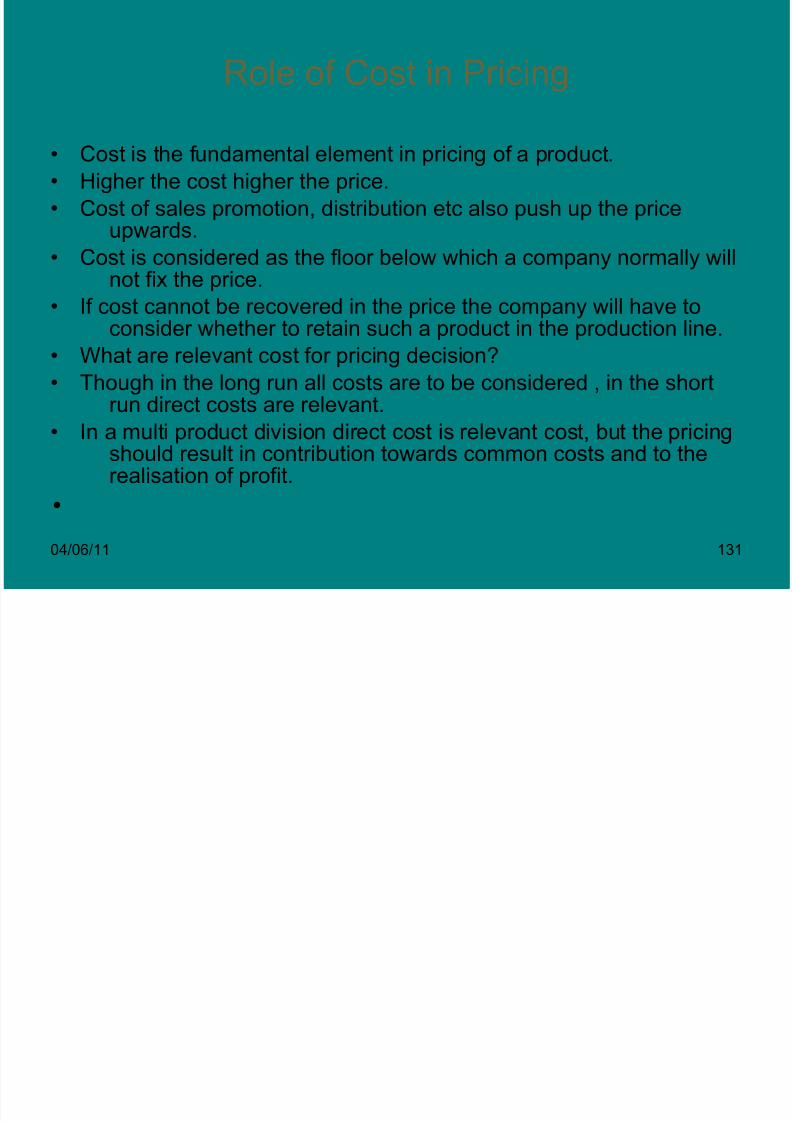

Role of Cost in Pricing

8/7/2019 Presentation3 for CSM

http://slidepdf.com/reader/full/presentation3-for-csm 131/207

04/06/11 131

• Cost is the fundamental element in pricing of a product.• Higher the cost higher the price.

• Cost of sales promotion, distribution etc also push up the priceupwards.

• Cost is considered as the floor below which a company normally willnot fix the price.

• If cost cannot be recovered in the price the company will have toconsider whether to retain such a product in the production line.

• What are relevant cost for pricing decision?

• Though in the long run all costs are to be considered , in the shortrun direct costs are relevant.

• In a multi product division direct cost is relevant cost, but the pricingshould result in contribution towards common costs and to therealisation of profit.

•

Cost based Pricing

8/7/2019 Presentation3 for CSM

http://slidepdf.com/reader/full/presentation3-for-csm 132/207

04/06/11 132

• Full cost pricing- This is most conventional and popular method of costing of a product or service.. Indirect taxes like Excise duty,forwarding charges are to be included in the price.

•

8/7/2019 Presentation3 for CSM

http://slidepdf.com/reader/full/presentation3-for-csm 133/207

8/7/2019 Presentation3 for CSM

http://slidepdf.com/reader/full/presentation3-for-csm 134/207

04/06/11 134

• Cost control from the beginning– 70-90% of costs are committed to at the

design stage– Focus on product and process design to

engineer out costs from the beginning• Saves costly changes later on

• Product, manufacturing process, deliveryprocess designed simultaneously

– Ensures features customers demand, but

within acceptable cost parameters– Eliminates the temptation to add costly

features• Customers may not value the added features

– Forces consideration of manufacturability• Reduces the need for subse uent chan es

8/7/2019 Presentation3 for CSM

http://slidepdf.com/reader/full/presentation3-for-csm 135/207

04/06/11 135

• Cost control at all phases of the productlife cycle

– Design

– Production

– Delivery/setup

– Customer’s cost of ownership

• Emphasizes future sales instead of currentcost savings

– Service and repair – Disposal and recycling

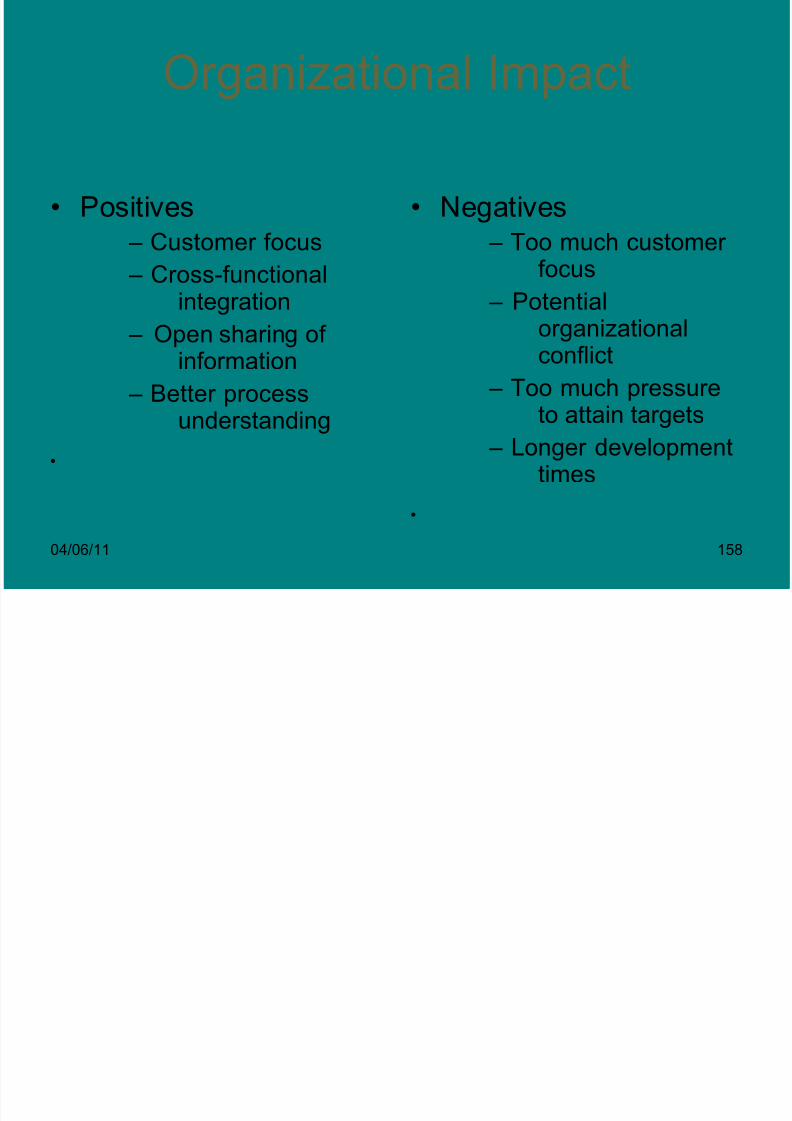

Cross Functional Team

8/7/2019 Presentation3 for CSM

http://slidepdf.com/reader/full/presentation3-for-csm 136/207

04/06/11 136

• Marketing

• Design/engineering

• Manufacturing• Purchasing

– Including suppliers

• Distribution

• Service/support

• Cost accounting

• Finance

• Legal

Target Costing Process

8/7/2019 Presentation3 for CSM

http://slidepdf.com/reader/full/presentation3-for-csm 137/207

04/06/11 137

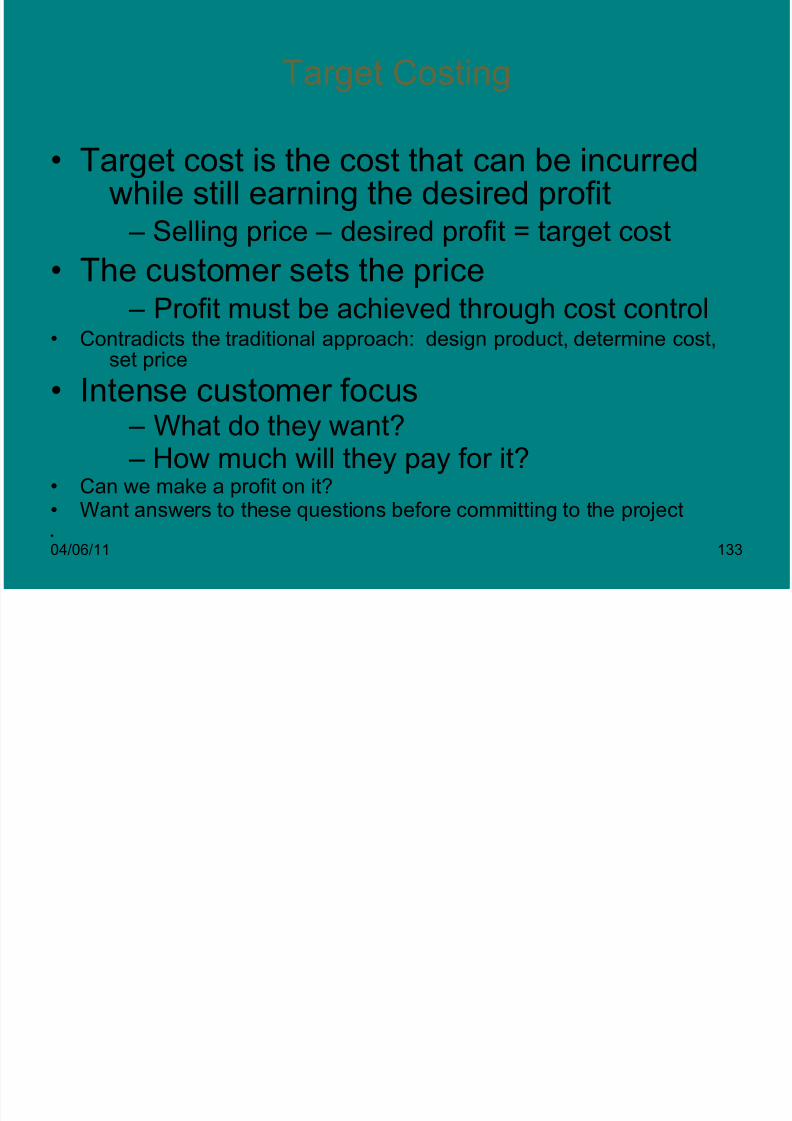

Two stage processEstablish the target cost

Market research

Product planning, concept developmentstages

Achieve the target costValue engineering, continuous

improvementDesign stage

Continuous improvement in later stages

Establishing the Target Cost

8/7/2019 Presentation3 for CSM

http://slidepdf.com/reader/full/presentation3-for-csm 138/207

04/06/11 138

• Determine the product and its market– Who is the target market?

– What do they want?

– What do competitors offer?• Introduce concept or prototype

– Evolutionary or revolutionary?

– Refine until it meets customer needs

8/7/2019 Presentation3 for CSM

http://slidepdf.com/reader/full/presentation3-for-csm 139/207

04/06/11 139

• Determine the selling price– Must be acceptable to the customer

– Must be able to withstand competition

– Techniques• Existing price +/- value of features added or

deleted

• Consensus of focus group

• Price predicted to achieve a desired marketshare

8/7/2019 Presentation3 for CSM

http://slidepdf.com/reader/full/presentation3-for-csm 140/207

04/06/11 140

• Determine the required profit– Return on sales

• Desired return

• Historical return for similar products

• Industry average for similar products

– Return on sales will fluctuate over the lifeof the product

• Price and costs fluctuate• Unit price, cost and profit are almost

meaningless because they fluctuate

– Life cycle totals are more meaningful

8/7/2019 Presentation3 for CSM

http://slidepdf.com/reader/full/presentation3-for-csm 141/207

04/06/11 141

• Total expected revenue throughout product life- -Total desired profit throughout product life Total target costAchieving the Target Cost

• Must include the features the customer

wants while maintaining cost at or belowtarget

– Want to meet the customers needs, but notexceed them

• Eliminating desired features will result in anundesirable product

• Adding unwanted features will increase cost

– Failing to keep cost at or below target will

result in unacceptable profits

8/7/2019 Presentation3 for CSM

http://slidepdf.com/reader/full/presentation3-for-csm 142/207

04/06/11 142

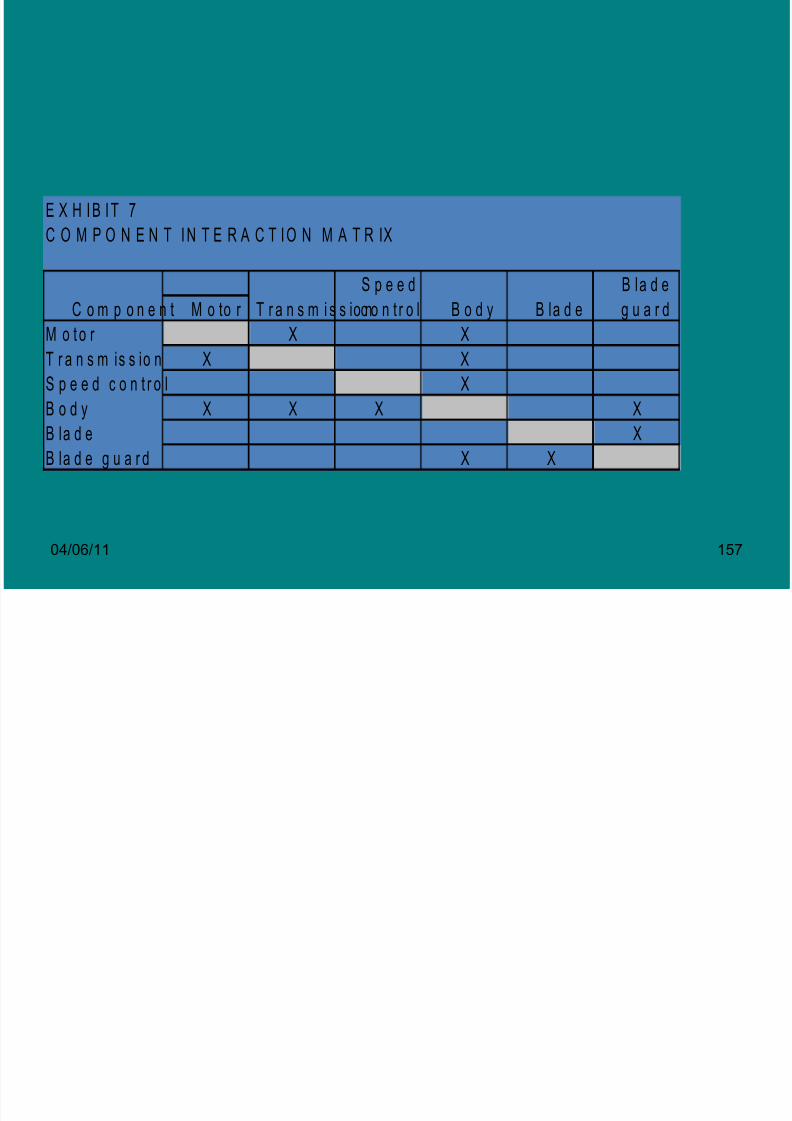

EXHIBIT 1CUSTOMER REQUIREMENT RANKINGS

Less More Raw % of Total

Customer Requirement Important Score Raw Score

1 2 3 4 5 1 2 3 4 5

Multiple speeds 4 4 14.8%

Horizontal oscillation 3 3 11.1%

Vertical oscillation 1 1 3.7%Light weight 4 4 14.8%

Adjustable height 1 1 3.7%

Airflow capacity 4 4 14.8%

Quietness 5 5 18.5%

Compact size 3 3 11.1%

Looks nice 2 2 7.4%

Total 27 100%

Us

Competitor

Both

Important

Competitive

Comparison

Ranking

8/7/2019 Presentation3 for CSM

http://slidepdf.com/reader/full/presentation3-for-csm 143/207

8/7/2019 Presentation3 for CSM

http://slidepdf.com/reader/full/presentation3-for-csm 144/207

04/06/11 144

• Determine the cost gap between currentcost and allowable cost

– Current cost is based on

• Currently used components

• Current suppliers

• Current manufacturing processes

• Current distribution network

• Etc.

8/7/2019 Presentation3 for CSM

http://slidepdf.com/reader/full/presentation3-for-csm 145/207

04/06/11 145

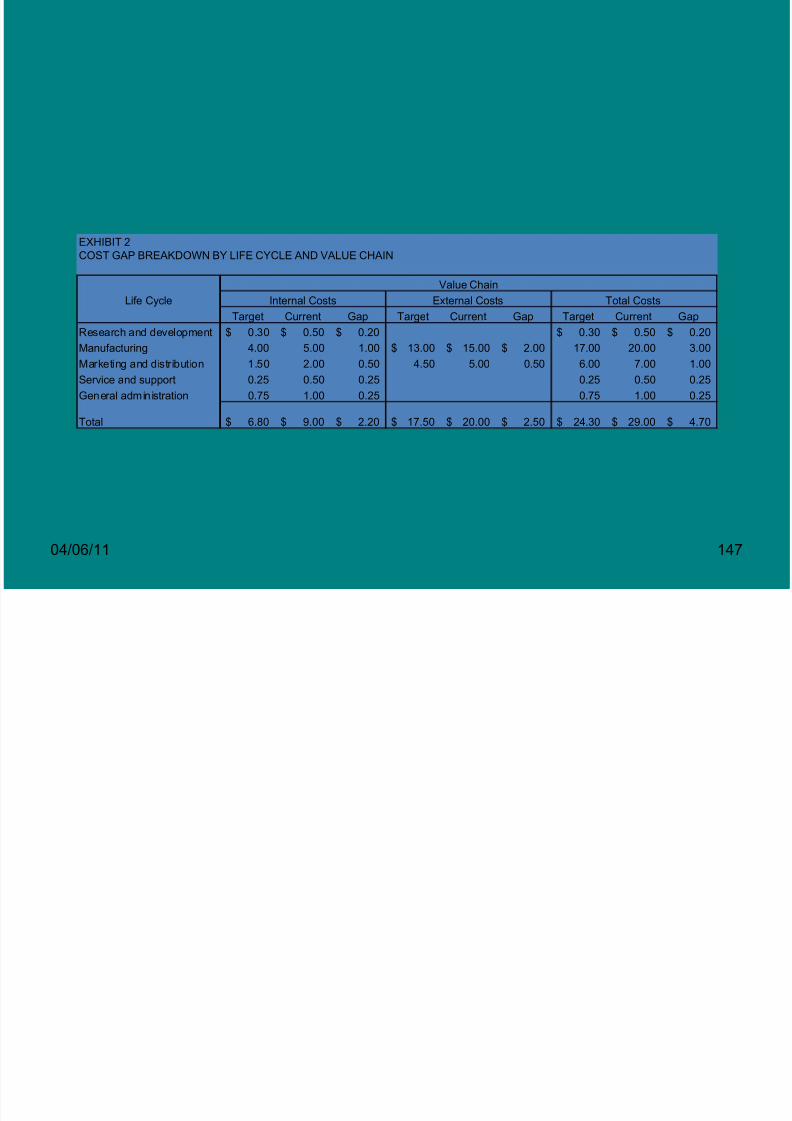

• Decompose the cost gap(Exibit 2)– Life cycle decomposition

• Cost reduction goals are divided among thefunctions in the product’s life cycle

– Design/engineering– Manufacturing

– Sales/distribution

– Service/support

– General administration– Etc.

8/7/2019 Presentation3 for CSM

http://slidepdf.com/reader/full/presentation3-for-csm 146/207

04/06/11 146

– Value chain decomposition• Cost reduction targets are divided among

internal and external activities

– Internal costs

» Labor, overhead, selling andadministrative costs, etc.

– External costs

» Components and servicesacquired from suppliers, etc.

» Often represent a largeproportion of total cos

8/7/2019 Presentation3 for CSM

http://slidepdf.com/reader/full/presentation3-for-csm 147/207

04/06/11 147

EXHIBIT 2COST GAP BREAKDOWN BY LIFE CYCLE AND VALUE CHAIN

Life CycleTarget Current Gap Target Current Gap Target Current Gap

Research and development 0.30$ 0.50$ 0.20$ 0.30$ 0.50$ 0.20$

Manufacturing 4.00 5.00 1.00 13.00$ 15.00$ 2.00$ 17.00 20.00 3.00

Marketing and distribution 1.50 2.00 0.50 4.50 5.00 0.50 6.00 7.00 1.00

Service and support 0.25 0.50 0.25 0.25 0.50 0.25

General administration 0.75 1.00 0.25 0.75 1.00 0.25

Total 6.80$ 9.00$ 2.20$ 17.50$ 20.00$ 2.50$ 24.30$ 29.00$ 4.70$

Internal Costs External Costs Total Costs

Value Chain

8/7/2019 Presentation3 for CSM

http://slidepdf.com/reader/full/presentation3-for-csm 148/207

04/06/11 148

• Perform value engineering to design outcosts without sacrificing needed features

– Perform a cost analysis of major components and activities

• List components or activities and their functions

• Calculate a cost breakdown (exhibit 3)

– Determine the current cost of each

component or activity and convert topercentage of total cost

» Costs include materials, labor,overhead, etc.

8/7/2019 Presentation3 for CSM

http://slidepdf.com/reader/full/presentation3-for-csm 149/207

04/06/11 149

EXHIBIT 3COMPONENT COST BREAKDOWN

Percent of

Component Function Cost total costMotor Turns blade 8$ 40%

Transmission Provides oscillation capabilities 4 20%

Speed control/switch Controls blade speed 3 15%

Body Houses motor, transmission, speed control 2 10%

Blade Moves air 1 5%

Blade guard Protects blade from contacting objects 2 10%

Total 20$ 100%

8/7/2019 Presentation3 for CSM

http://slidepdf.com/reader/full/presentation3-for-csm 150/207

04/06/11 150

– Relate the components to customer requirements (exhibit 4)

• Develop Quality-Function-Deploymentmatrix

– Indicates which components have thegreatest impact on customer requirements

– Develop a functional ranking (exhibit 5)

• Indicates the importance of eachcomponent to the customer

– Based on the component’s contributionto providing the desired functions

8/7/2019 Presentation3 for CSM

http://slidepdf.com/reader/full/presentation3-for-csm 151/207

04/06/11 151

EXHIBIT 4QUALITY-FUNCTION-DEPLOYMENT (QFD) MATRIX

Speed Blade

Motor Transmission control Body Blade guard

Multiple speeds

Horizontal oscillationVertical oscillation

Light weight

Adjustable height

Airflow capacity

Quietness

Compact size

Looks nice

Strong correlationModerate correlationWeak correlation

Components

Customer Requirements

8/7/2019 Presentation3 for CSM

http://slidepdf.com/reader/full/presentation3-for-csm 152/207

04/06/11 152

E X H IB IT 5

C O M P O N E N T C O N T R IB U T IO N T O C U S T O M E R R E Q U IR E M E N T S

C u s t o m e r R e q u i r e m e n t s S p e e d B la d e

M o t o r T r a n s m is s io n c o n t r o l B o d y B l a d e g u a r d

M u l t ip le s p e e d s 4 0 X 1 4 . 8 = 5 . 9 2 6 0 X 1 4 . 8 = 8 . 8 8

H o r iz o n t a l o s c i l la t io n 8 0 X 1 1 . 1 = 8 .8 8 2 0 X 1 1 .1 = 2 . 2 2

V e r t ic a l o s c i l la t io n 8 0 X 3 .7 = 2 . 9 6 2 0 X 3 .7 = 0 .7 4

L ig h t w e ig h t 7 0 X 1 4 .8 = 1 0 . 3 61 0 X 1 4 . 8 = 1 . 4 8 2 0 X 1 4 . 8 = 2 . 9 6

A d ju s t a b le h e ig h t 1 0 0 X 3 .7 = 3 . 7 0

A ir f lo w c a p a c i t y 5 0 X 1 4 . 8 = 7 . 4 0 5 0 X 1 4 .8 = 7 .4 0

Q u ie tn e s s 4 0 X 1 8 . 5 = 7 . 4 0 6 0 X 1 8 . 5 = 1 1 .1 0C o m p a c t s iz e 5 X 1 1 . 1 = 0 . 5 65 X 1 1 .1 = 0 . 5 6 3 0 X 1 1 . 1 = 3 . 3 33 0 X 1 1 . 1 = 3 .3 33 0 X 1 1 .1 =

L o o k s n ic e 5 0 X 7 .4 = 3 .7 0 5 0 X 7 . 4 =

T o t a l c o n t r ib u t io n p e r c e n t a g e 3 1 . 6 4 % 1 3 .8 8 % 8 . 8 8 % 1 6 . 6 5 % 2 1 . 8 3 % 7 . 0 3

C o m p o n e n ts

8/7/2019 Presentation3 for CSM

http://slidepdf.com/reader/full/presentation3-for-csm 153/207

04/06/11 153

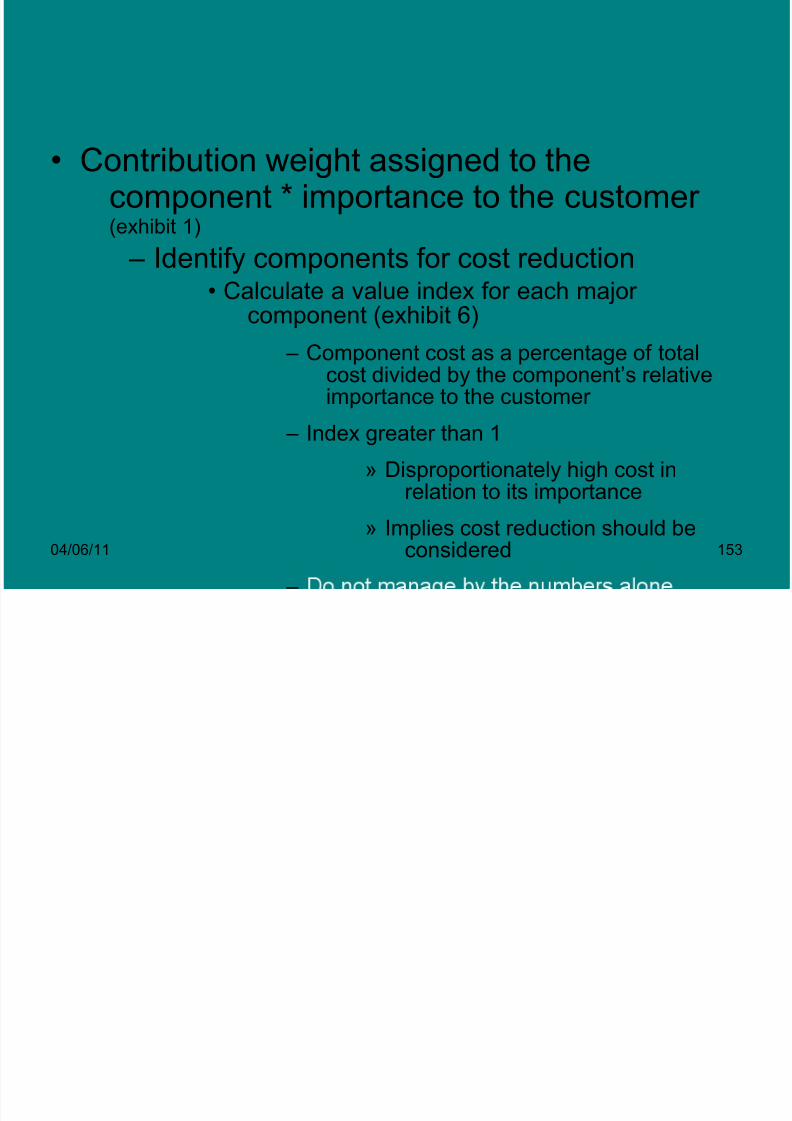

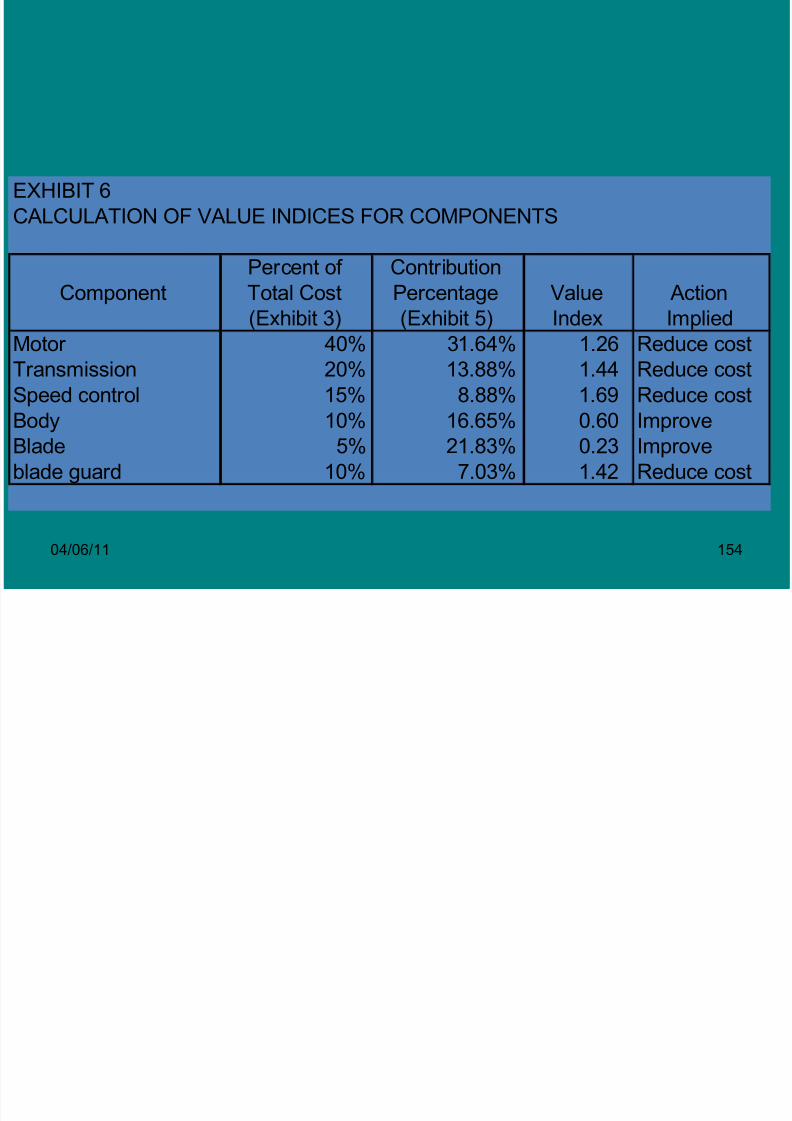

• Contribution weight assigned to thecomponent * importance to the customer (exhibit 1)

– Identify components for cost reduction

• Calculate a value index for each major component (exhibit 6)

– Component cost as a percentage of totalcost divided by the component’s relativeimportance to the customer

– Index greater than 1» Disproportionately high cost in

relation to its importance

» Implies cost reduction should beconsidered

–