28

Presented by Ed Slott, CPA and Jeffrey Levine, CPA Ed Slott and Company, LLC

Presented by Ed Slott, CPA and Jeffrey Levine, CPA

Ed Slott and Company, LLC

The Only Thing Constant is Change

• Each year the rules and/or the interpretation of the rules

for retirement accounts change dramatically.

• There are always new

• Laws

• Revenue rulings

• Private letter rulings

• Tax Court cases

• IRS notices

• IRS announcements and other guidance

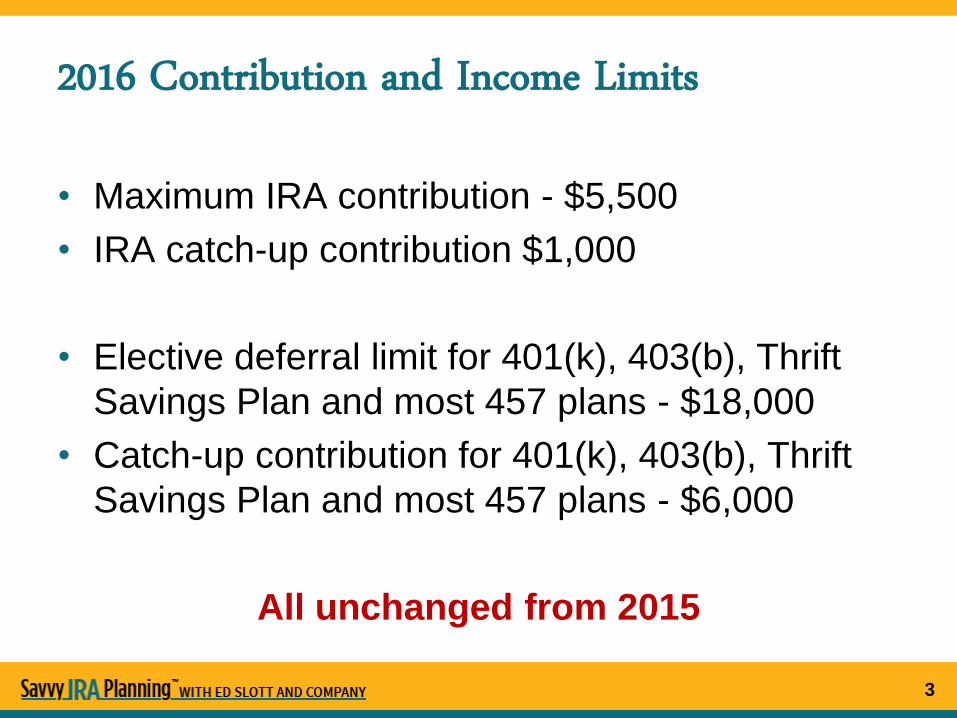

2016 Contribution and Income Limits

• Maximum IRA contribution - $5,500

• IRA catch-up contribution $1,000

• Elective deferral limit for 401(k), 403(b), Thrift

Savings Plan and most 457 plans - $18,000

• Catch-up contribution for 401(k), 403(b), Thrift

Savings Plan and most 457 plans - $6,000

All unchanged from 2015

3

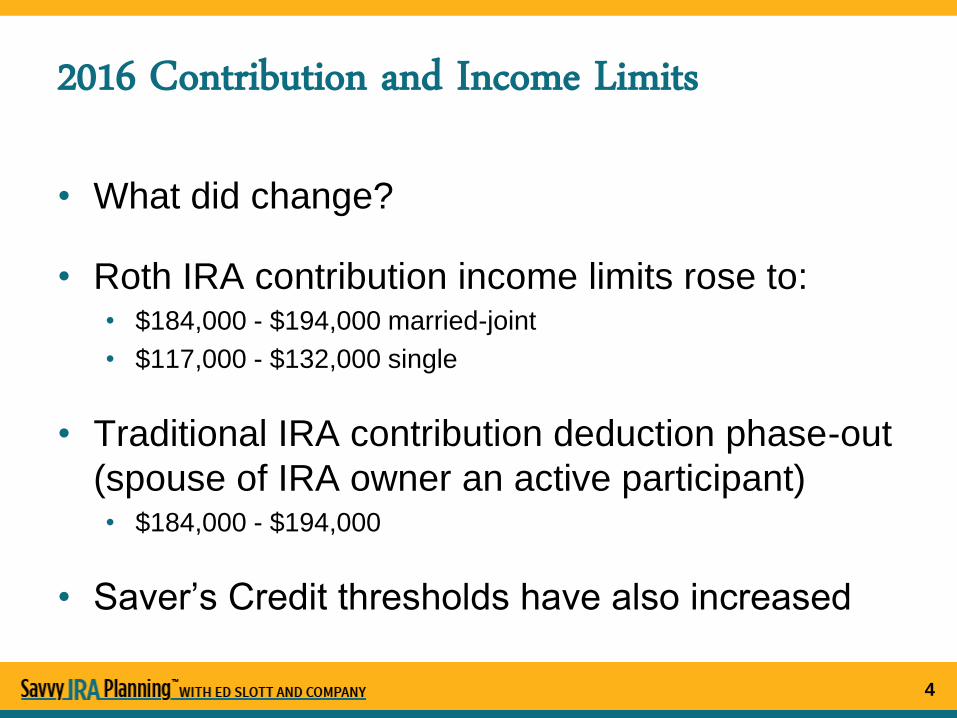

2016 Contribution and Income Limits

• What did change?

• Roth IRA contribution income limits rose to: • $184,000 - $194,000 married-joint

• $117,000 - $132,000 single

• Traditional IRA contribution deduction phase-out

(spouse of IRA owner an active participant) • $184,000 - $194,000

• Saver’s Credit thresholds have also increased

4

The “New” Once-Per-Year Rollover Rule Transition Relief Expired

• Only one 60-day IRA-to-IRA or Roth IRA-to-Roth IRA

each year (365 days)

• Bobrow decision changes rule from per-account-rule to

an aggregate rule

• Trustee-to-trustee transfers do not count

• The following rollovers also do not count:

• Plan-to-IRA rollovers

• IRA-to-plan rollovers

• Roth IRA conversions

The “New” Once-Per-Year Rollover Rule Transition Relief Expired

• New interpretation of the once-per-year

rollover rule was effective January 1, 2015,

BUT...

• Clients had a (somewhat) fresh start in 2015 • 2014 60-day rollovers were disregarded for NEW interpretation

• That transition relief will have fully expired by

January 1, 2016

Qualified Charitable Distributions

• NOT CURRENTLY IN EFFECT

FOR 2015 OR BEYOND!!!

• Each time the provision has expired in the past, it’s been reinstated

retroactively.

• No guarantees that will happen this time though!

Qualified Charitable Distributions

• QCD vs. “regular” charitable contribution

• QCD

• No deduction

• Not added to income

• “Regular” charitable contribution

• IRA distribution added to income

• Itemized deduction • Charitable deductions may be limited

• Clients may not itemize

• Does not prevent reduction of tax benefits tied to AGI/MAGI

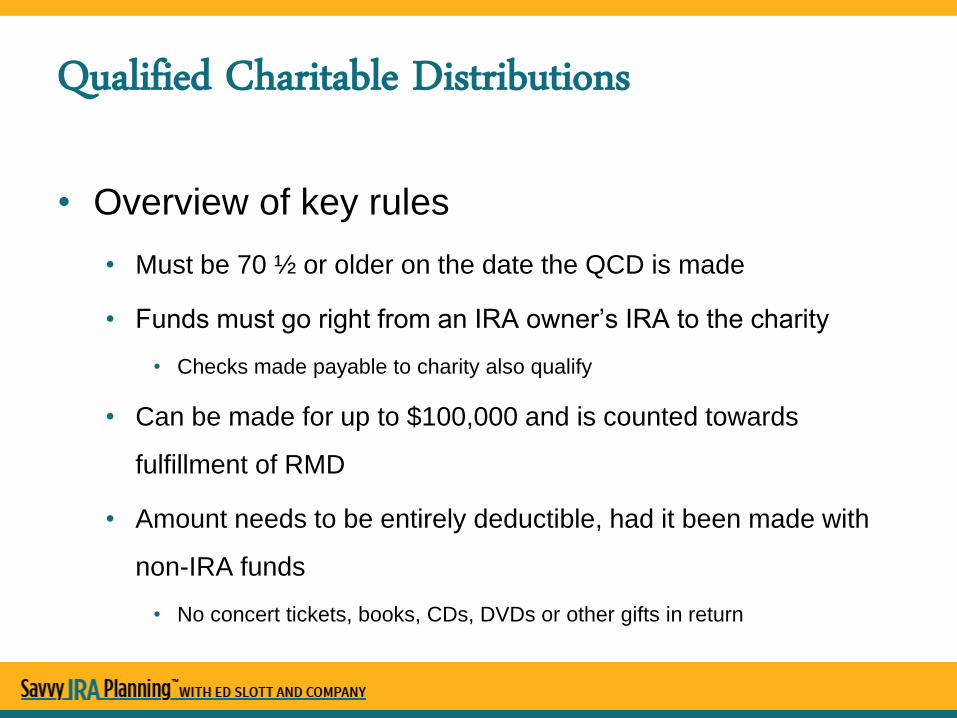

Qualified Charitable Distributions

• Overview of key rules

• Must be 70 ½ or older on the date the QCD is made

• Funds must go right from an IRA owner’s IRA to the charity

• Checks made payable to charity also qualify

• Can be made for up to $100,000 and is counted towards

fulfillment of RMD

• Amount needs to be entirely deductible, had it been made with

non-IRA funds

• No concert tickets, books, CDs, DVDs or other gifts in return

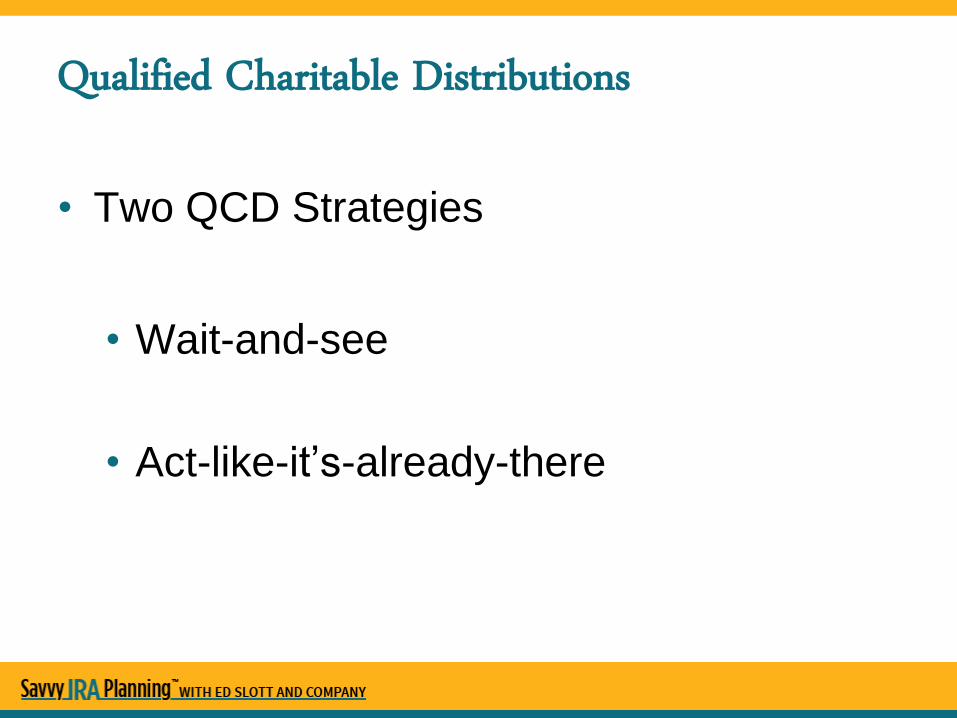

Qualified Charitable Distributions

• Two QCD Strategies

• Wait-and-see

• Act-like-it’s-already-there

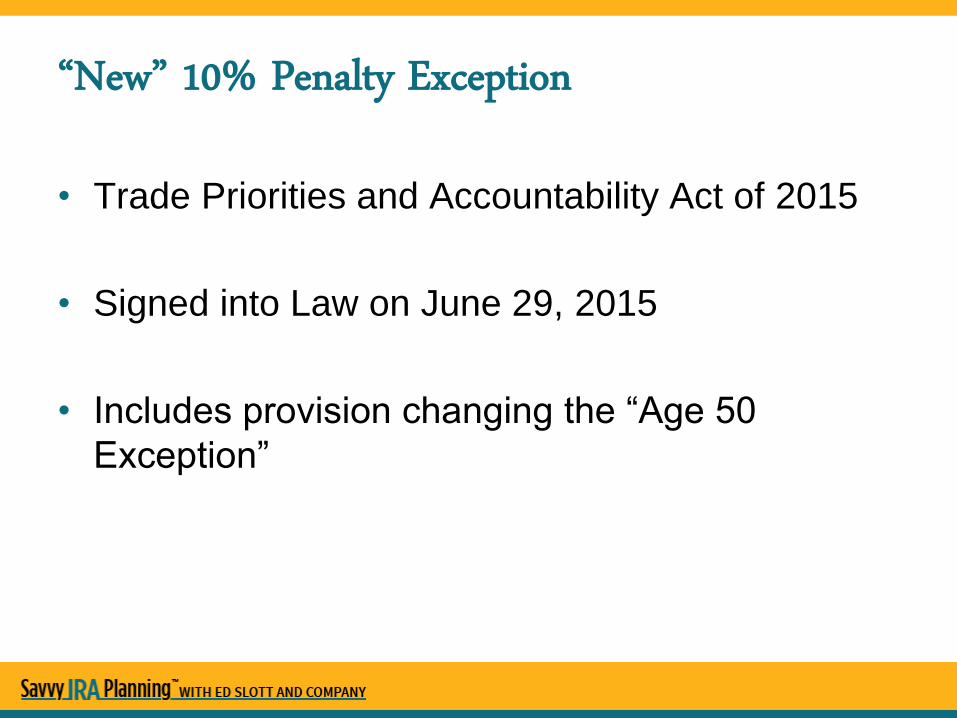

“New” 10% Penalty Exception

• Trade Priorities and Accountability Act of 2015

• Signed into Law on June 29, 2015

• Includes provision changing the “Age 50

Exception”

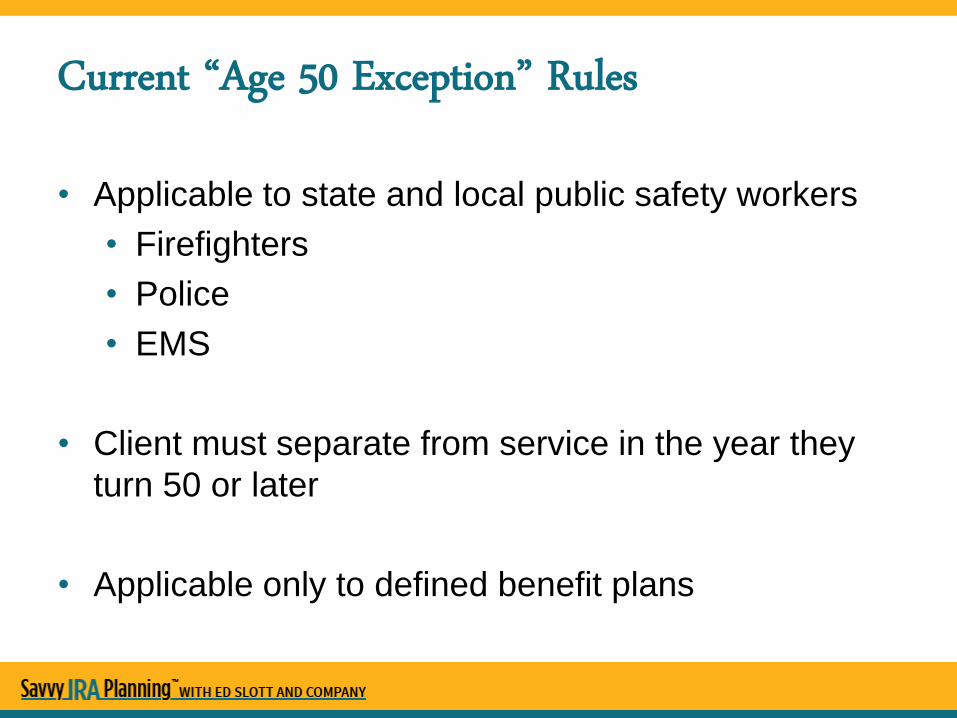

Current “Age 50 Exception” Rules

• Applicable to state and local public safety workers

• Firefighters

• Police

• EMS

• Client must separate from service in the year they

turn 50 or later

• Applicable only to defined benefit plans

The “New” Age 50 Exception

• Expands availability to additional professions

• Federal law enforcement

• Federal Firefighters

• Border Patrol

• Customs

• Air Traffic Controllers

The “New” Age 50 Exception

• Will apply to both defined benefit and defined

contribution plans

• Can be used in conjunction with 72(t)

distributions!

• THE CHANGES DO NOT TAKE EFFECT UNTIL

JANUARY 1, 2016

Review Retirement Income Plans to Account for Budget Act’s Changes

• Bipartisan Budget Act of 2015

• Eliminates file-and-suspend strategy • Effective 180 days after signing of the law

• After grace period expires: • Clients still allowed to suspend benefit at FRA or

later, BUT

• If benefits are suspended, all other benefits

received based on individuals earnings history are

also suspended

Review Retirement Income Plans to Account for Budget Act’s Changes

• Bipartisan Budget Act of 2015

• Eliminates restricted application strategy • Effective for individuals turning reaching age 62 on

or after January 2, 2016

• After grace period expires: • Regardless of client’s age, they will not be able to

restrict their application to just their spousal benefit

• No more “free” spousal benefits

Review Retirement Income Plans to Account for Budget Act’s Changes

• Both strategies may have a significant

impact on a client’s retirement income

• In the most severe of cases, clients could

see over a $60,000 decrease in retirement

income over a 4 year period

• What will they do to offset the effects?

Review Retirement Income Plans to Account for Budget Act’s Changes

• Will clients still delay Social Security benefits

• Will they have to withdraw more from their IRA in the

interim years?

• How will this impact them?

• Will clients claim Social Security benefits

sooner?

• Will they have to withdraw larger than previously

anticipated amounts from their IRA to account for

smaller Social Security benefits?

• How will this impact them?

New Reporting Requirements for Hard-to-Value Assets

• New reporting for IRS forms

• 5498, IRA Contribution Information

• 1099-R, Distributions From Pensions, Annuities,

Retirement or Profit Sharing Plans, IRAs, Insurance

Contracts, etc.

• Was optional for 2014

• Mandatory for 2015 an beyond

• 2015 1099-Rs and 5498s received in 2016

• First time many clients/CPAs will see the changes

More Options for QLACs

• Qualifying longevity annuity contracts (QLACs)

• Established July 2014

• Initially only a few carriers had QLAC-qualifying

products available

• More carriers have begun to offer these

products and additional options are expected to

continue to come on line

20

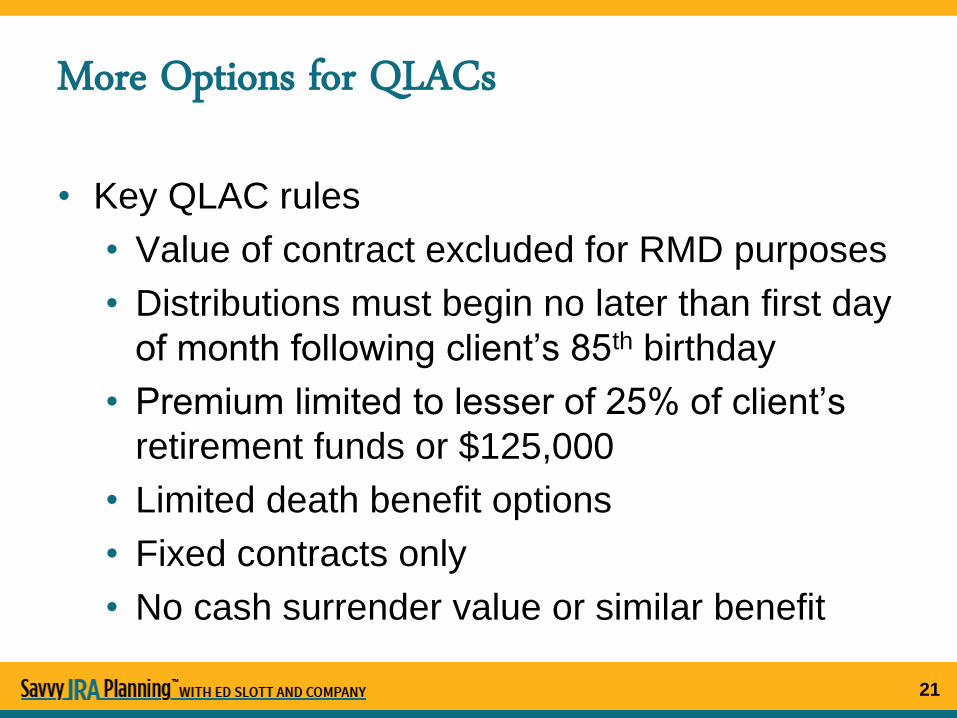

More Options for QLACs

• Key QLAC rules

• Value of contract excluded for RMD purposes

• Distributions must begin no later than first day

of month following client’s 85th birthday

• Premium limited to lesser of 25% of client’s

retirement funds or $125,000

• Limited death benefit options

• Fixed contracts only

• No cash surrender value or similar benefit

21

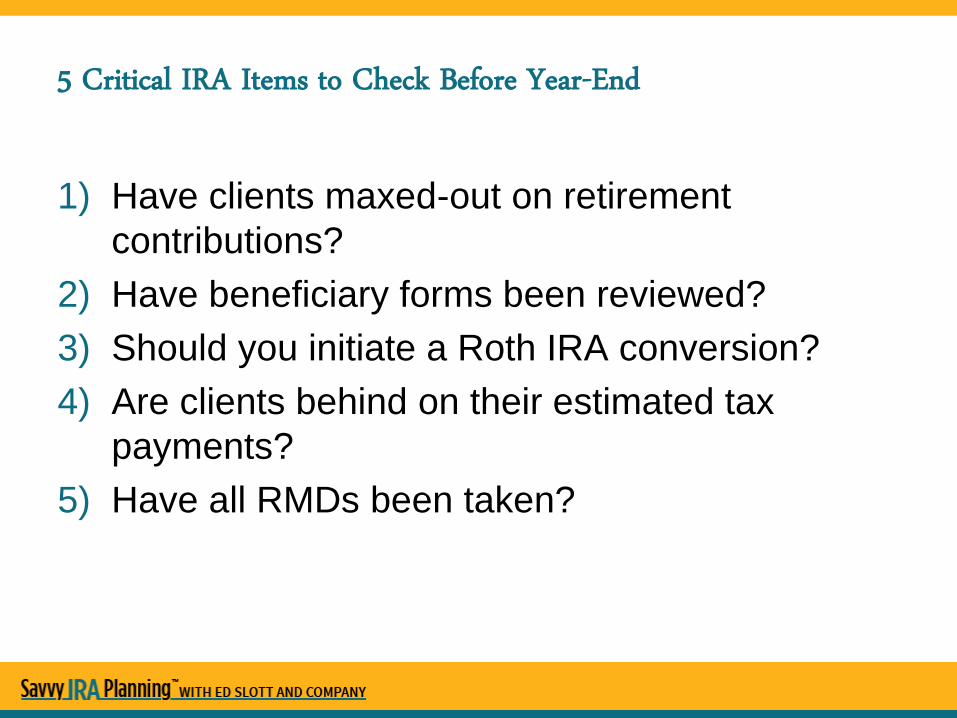

5 Critical IRA Items to Check Before Year-End

1) Have clients maxed-out on retirement

contributions?

2) Have beneficiary forms been reviewed?

3) Should you initiate a Roth IRA conversion?

4) Are clients behind on their estimated tax

payments?

5) Have all RMDs been taken?

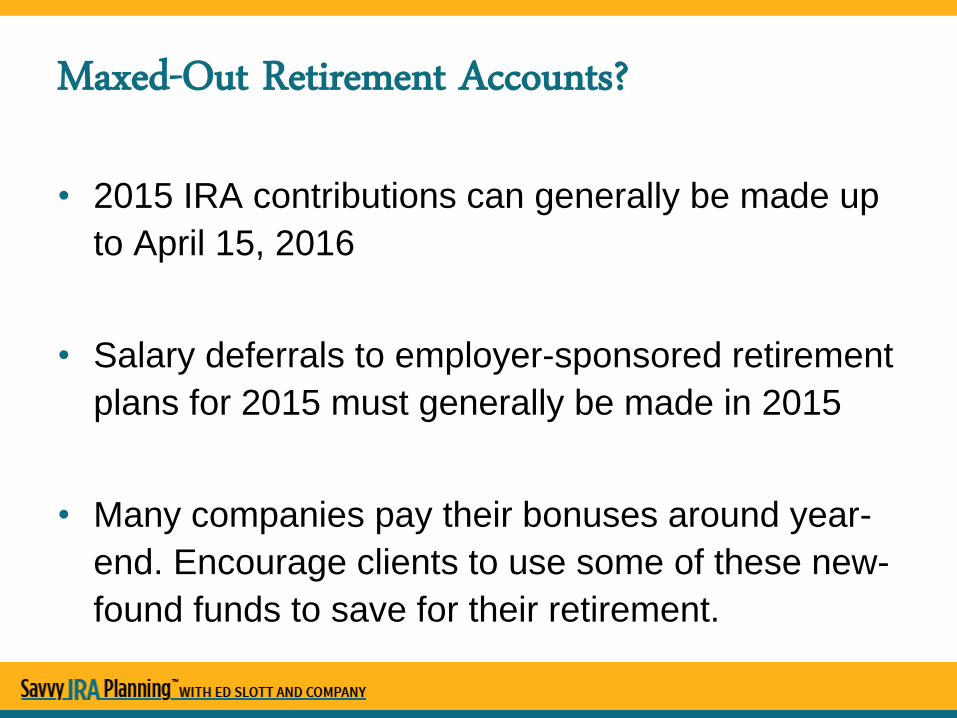

Maxed-Out Retirement Accounts?

• 2015 IRA contributions can generally be made up

to April 15, 2016

• Salary deferrals to employer-sponsored retirement

plans for 2015 must generally be made in 2015

• Many companies pay their bonuses around year-

end. Encourage clients to use some of these new-

found funds to save for their retirement.

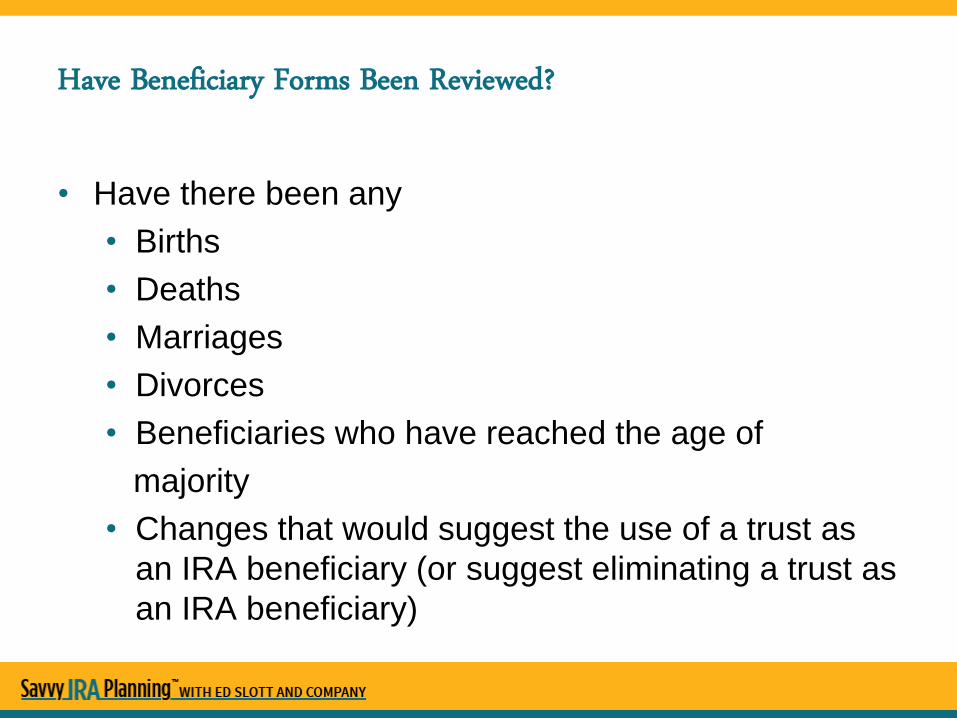

Have Beneficiary Forms Been Reviewed?

• Have there been any

• Births

• Deaths

• Marriages

• Divorces

• Beneficiaries who have reached the age of

majority

• Changes that would suggest the use of a trust as

an IRA beneficiary (or suggest eliminating a trust as

an IRA beneficiary)

Roth IRA Conversion Before Year-End?

• Can always be recharacterized up to October 15,

2016

• As long as the funds leave a client’s traditional

account by December 31, 2015, it will be considered

a 2015 Roth IRA conversion... Even if the funds

don’t get into the Roth IRA until 2016

• May effectively turn the 5-year rule into a 4-year rule

Short on Estimated Tax Payments? Use This Trick! • Take a distribution from the client’s IRA for an amount equal to the

estimated tax shortfall.

• Withhold 100% of the distribution

• Eliminates estimated tax penalty

• Withholdings are treated as paid in ratably throughout the year

• Take other, non-IRA money and, within 60-days, rollover an amount

equal to the distribution.

• Restores client’s IRA and eliminates the tax on the distribution.

***Be careful of the once-per-year rollover rule***

Have All RMDs Been Taken?

• Verify that all RMDs have been correctly calculated

• Ensure that an RMD has been taken from each of a client’s

employer-sponsored retirement plans

• Exception – RMDs for 403(b) plans can be aggregated

• Make sure that clients have taken a distribution from at least one of

their IRAs large enough to satisfy the RMD requirement for all of

their IRAs

• Double-check to make sure RMDs have been correctly distributed

from any inherited retirement accounts a client may have

Introducing Savvy IRA Planning With Ed Slott and Company

A comprehensive new resource to help you

attract more clients, including: • 4-part IRA webinar training series delivered by the Ed Slott and Company

team (CE credit)

• Seminar presentations to deliver to clients and prospects (FINRA -reviewed)

• 2 IRA study guides to support your learning and expertise

• Live webinars with Ed Slott and Company experts answering select

subscriber questions

• Marketing toolkit to promote the seminar presentations

• IRA article reprints and IRA Boomer guides to hand out

• Plus, lots more.

28

Join now and save! •Questions: [email protected] | More Info: www.horsesmouth.com/ira

![Levine Complaint [1]](https://static.documents.pub/doc/80x56/55cf9026550346703ba353fe/levine-complaint-1.jpg)