Presented by Matti Amukwa Chairman – Confederation of Namibian Fishing Associations November 2012 European Commission Regional Seminar on the EU- SADC Economic Partnership Agreement in Botswana, 14-15 November 2012

Transcript

Presented by Matti Amukwa

Chairman – Confederation of Namibian Fishing Associations

November 2012

European Commission Regional Seminar on the EU-SADC Economic Partnership Agreement in Botswana,

14-15 November 2012

Namibia’s fishing industry Since Namibia Independence, based on a fisheries

development policy which promotes Namibianisation through fishing joint ventures (JV’s).

Namibia’s hake and monk fish sectors in particular export to the EU, and have a significant number of joint ventures with EU partners, involving large investment in vessels at sea and onshore processing.

Through careful fisheries management the sector which inherited a heavily overfished resource at Independence, now has growing fish stocks which are fished throughout Namibia’s 200 mile Exclusive Economic Zone (EEZ), to the benefit of Namibian and EU JV partners.

Total allowable catches in tonnes – recovery trend

Source: Ministry of Fisheries and Marine Resources

Year Pilchard Hake Horse Mackerel

Red Crab

Rock Lobster

Monk

1990 40,000 60,000 150,000 n.a. n.a. n.a

1997 25,000 120,000 350,000 2,000 260 n.a.

2005 25,000 180,000 350,000 2,300 420 11,500

2012 31,000 170,000 320,000 3,100 350 14,000

Namibia seafood export trade statistics – growth trend but higher costs – especially fuelSource: National Planning Commission Namibia Statistics Agency

Year 2007 2008 2009 2010 2011

Value Namibia $ billions (equivalent to South Africa Rand)

3.140 4.228 4.581 4.804 5.076

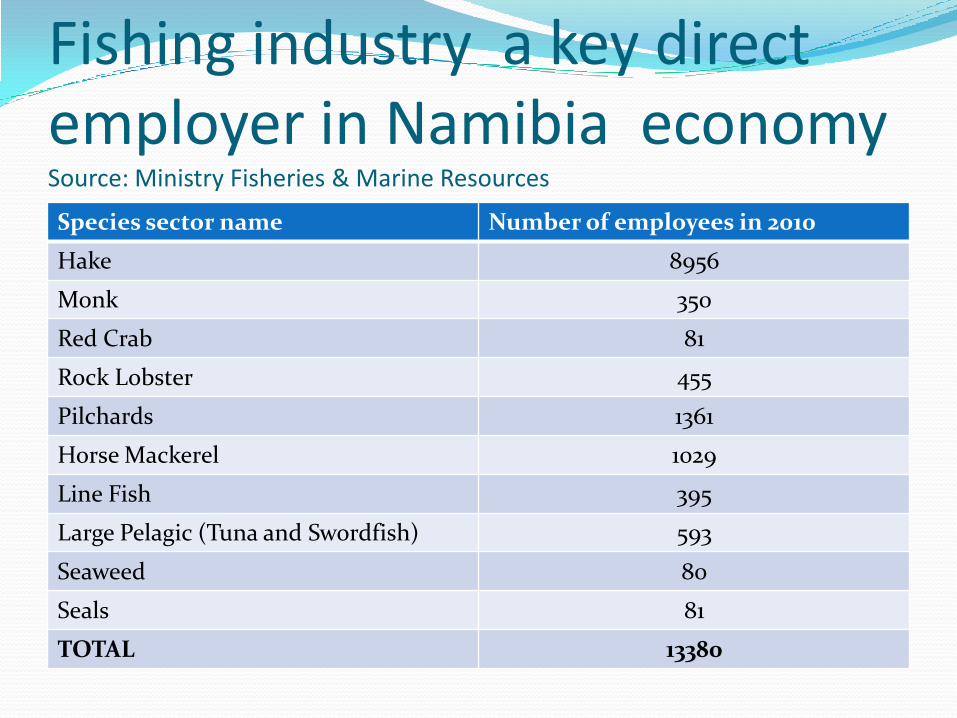

Fishing industry a key direct employer in Namibia economy Source: Ministry Fisheries & Marine Resources

Species sector name Number of employees in 2010

Hake 8956

Monk 350

Red Crab 81

Rock Lobster 455

Pilchards 1361

Horse Mackerel 1029

Line Fish 395

Large Pelagic (Tuna and Swordfish) 593

Seaweed 80

Seals 81

TOTAL 13380

Products & market destinations for Namibian fishery productsSpecies Main Products Main Markets

Hake Headed & gutted; skin on & skin off fillets; calibrated portions in retail packs; whole gutted fresh chilled.

Spain; South Africa;Germany; Italy; Holland

Horse mackerel

Whole frozen; fishmeal Regional Africa: DR Congo; Mozambique; South Africa; Zimbabwe

Export destinations for Namibia Hake 2010/11 Source: Ministry of Fisheries & Marine Resources

Spain 40%

South Africa 17%

Germany 13%

Italy 9%

Holland 5%

Australia 3%

France 3%

Other SADC 3%

Portugal 2%

UK 1%

EU TOTAL 73%

The wetfish hake industry

Landing of iced wetfish hake from a trawler

Large numbers of staff characterise onshore wetfish hake processing

8

Current value added onshore processing Hangana Seafood factory

processing wetfish hake Merlus Seafood Processors

processing sea frozen hake

Value added products from onshore processing factories Hake tongues and monk

tails for the retail market Retail ‘central’ portions

of the fillet

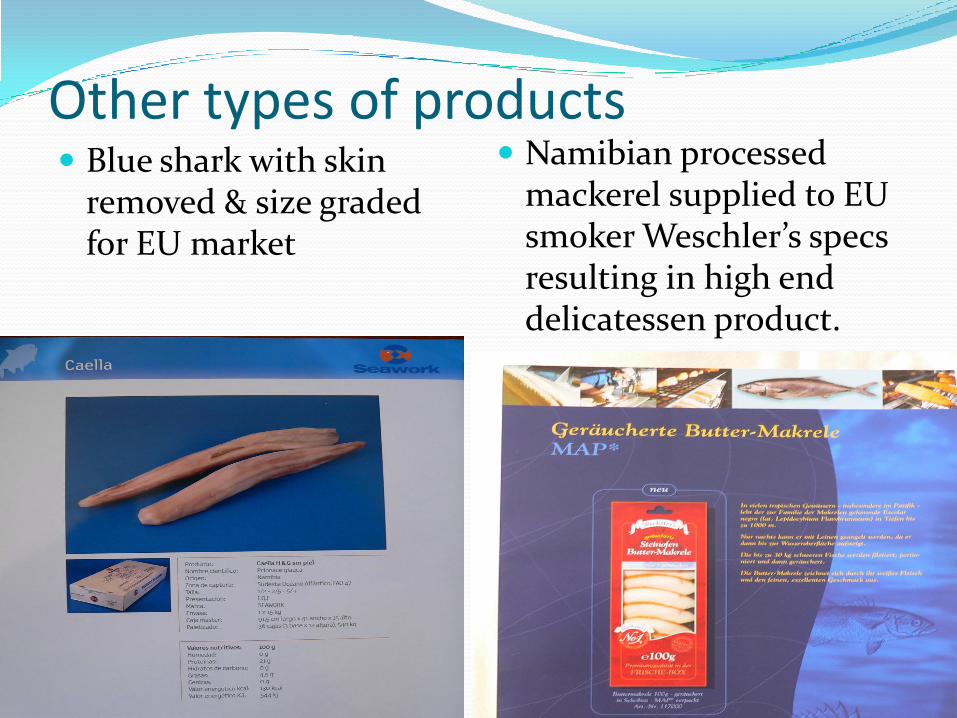

Other types of products Blue shark with skin

removed & size graded for EU market

Namibian processed mackerel supplied to EU smoker Weschler’s specs resulting in high end delicatessen product.

Key concerns Members of the European Parliament International

Trade Committee voted in favour of a European Commission proposal to update the Generalised System of Preferences (GSP) Scheme to exclude Botwana and Namibia, classified as upper middle-income countries. This means we would no longer qualify for EU market access under the new GSP provisions which provide zero or reduced tariffs for developing countries exports to the EU market. This will come into force by 1 January 2014.

Currently the EPA ratification deadline is also 1 January 2014 meaning Namibia’s fishing industry which at the moment pays zero tariffs to the EU is facing being forced to pay the much higher Most Favoured Nation (MFN) tariffs. This threatens the future economic viability of the Namibian fishing industry.

Key concerns continued The fishing industry agrees with the Namibia Ministry

of Fisheries and Marine Resources (MFMR) proposal to reject the EC proposal to amend Annex 1 of Market Access Regulation 1528/2007 which in broad terms is about the exclusion of countries, from the list of regions or states that have not concluded EPA negotiations.

Supports the position that negotiations should be allowed to continue until an agreement that is mutually beneficial can be reached, or to increase the proposed timeline for the conclusion of the negotiations.

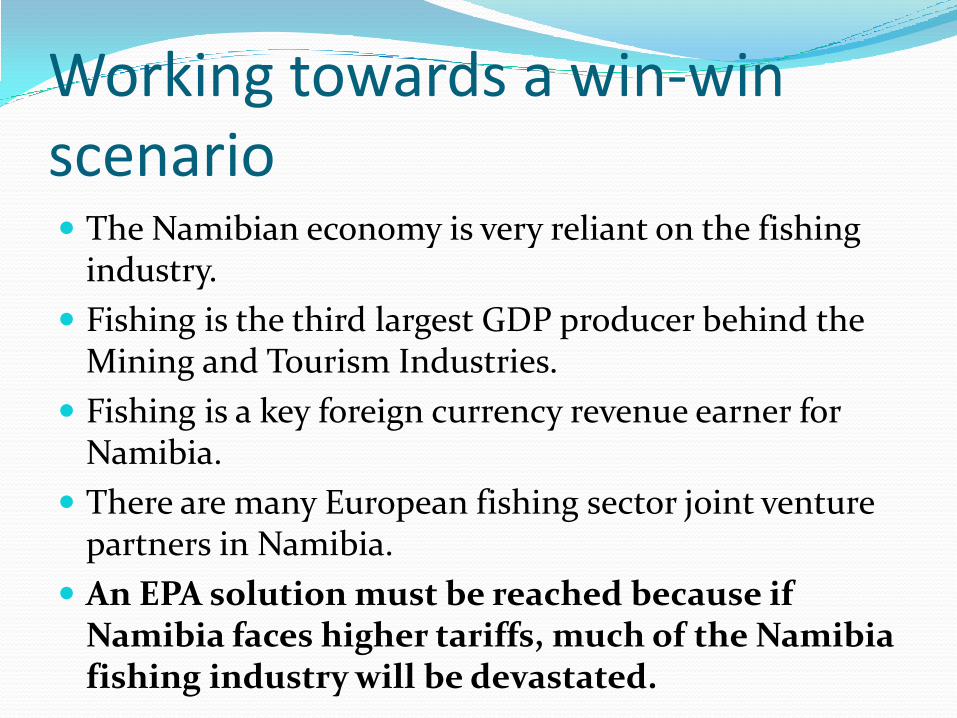

Working towards a win-win scenario The Namibian economy is very reliant on the fishing

industry.

Fishing is the third largest GDP producer behind the Mining and Tourism Industries.

Fishing is a key foreign currency revenue earner for Namibia.

There are many European fishing sector joint venture partners in Namibia.

An EPA solution must be reached because if Namibia faces higher tariffs, much of the Namibia fishing industry will be devastated.

Reciprocity – first right of refusal By Namibia signing the EPA, in return for duty free

access for fish products into the EU, the EU wants first right of refusal regarding their vessels being chartered or incorporated into joint ventures. In the past this has resulted in Namibia ending up with old de-commissioned EU vessels, where the EU joint venture partner got a subsidy for shifting the vessel to Namibia. Now Namibia sits with many fuel inefficient vessels over 30 years old, susceptible to breaking down, and does not have local access to finance on good financial terms to modernise its fleet.

Namibia, to break this cycle, wants to source vessels from the most competitive options internationally.

Rules of origin The EU states that for Namibia fish to be “wholly

obtained”, claiming full duty free access, it must have been caught within Namibia’s 12 nautical mile territorial waters.

Namibia’s fisheries policy has received prizes internationally for effective resource management. Namibia fishes the full extent of its 200 nautical mile exclusive economic zone (EEZ).

Namibia has a 200 metre depth restriction inside which no fish can be caught to preserve the breeding stock. Due to the gentle slope of the continental shelf, 200 metres depth can be a number of miles out to sea. Following the EU approach would threaten resource conservation in Namibia.

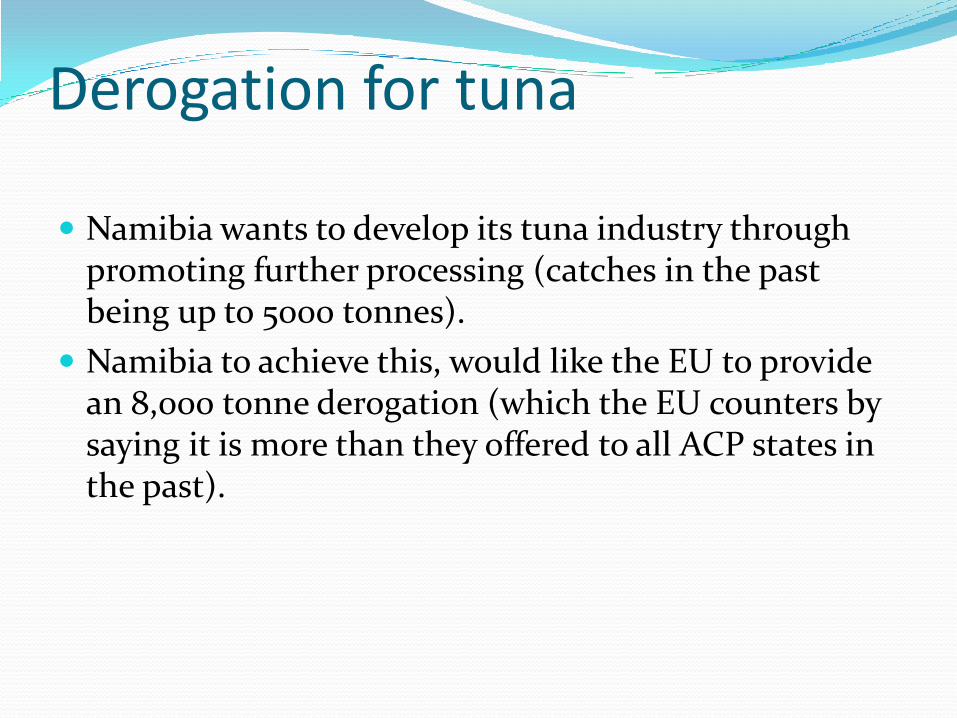

Derogation for tuna

Namibia wants to develop its tuna industry through promoting further processing (catches in the past being up to 5000 tonnes).

Namibia to achieve this, would like the EU to provide an 8,000 tonne derogation (which the EU counters by saying it is more than they offered to all ACP states in the past).

Need to promote secondary processing in Namibia Under GSP or MFN status, high EU taxes on secondary

processed products would severely impact Namibia’s fisheries development strategy of creating more value added products and consequent income, as well as providing more jobs for Namibia, including broadening Namibia’s economic base through developing the support service sector. Namibia has 50% unemployment and must strengthen its economy.

Even for European JV partners working in Namibia, it makes sense to develop secondary processing in Namibia, as wages are lower and the final exported product will be more competitively priced.

Crucial position for hake Namibia exports an estimated 70,000mt of hake fish

and fish products to the EU annually which is far higher than the proposed annual quota of the European Commission. A large percentage of this is raw material that currently benefits EU processors in terms of further processing.

If Namibia is subject to higher tariffs, due to high operational costs it will find itself unable to compete with hake products from countries such as Argentina, South Africa, Chile, and Uruguay, as well as other similar products such as hoki from New Zealand and Alaska pollock from USA.

In conclusion

The international economic crisis has resulted in depressed export markets, combined with escalating fuel prices. Most supplies for the Namibian fishing industry come from South Africa, resulting in higher costs to the Namibian industry.

Due to the current marginal profitability the seafood industry in Namibia is experiencing (those companies exporting to the EU), further reductions in margins will inevitably lead to financial losses.

Finally.... Namibian fishing sectors such as hake and monk fish

are heavily reliant on the EU as a market.

The hake wetfish sector in particular provides the bulk of the Namibian fishing industry jobs, and without a signed EPA agreement few of the companies in this sector are likely to survive.

The EU obviously wants Namibia fish. It is absolutely vital for the Namibia fishing industry, particularly the hake sector that agreement is reached on the EPA.