34

CHARACTERISTICS THAT BANKS EVALUATE BEFORE EXTENDING LOANS TO BORROWERS Presented to: Ms. Sana Farooq Presented by: Sania Moazzam 09U0153 Thursday, April 04, 2013

| Date post: | 26-Dec-2015 |

| Category: |

Documents |

| Upload: | alice-carpenter |

| View: | 217 times |

| Download: | 0 times |

CHARACTERISTICS THAT BANKS EVALUATE BEFORE EXTENDING LOANS TO BORROWERS

Presented to: Ms. Sana Farooq

Presented by: Sania Moazzam09U0153

Thursday, April 04, 2013

INTRODUCTION

Non-performing or 'infected loans’ have reached a staggering Rs.653 billion in Pakistan(Sabir, 2012)

Important to screen loan applicants to determine the creditworthiness of borrowers

Sample size:100 respondents Analysis of socio-demographic and

financial variables in Stata 11 software

HYPOTHESIS 1: DEBT BURDEN Ho: There is no significant relationship between the debt

burden of the prospective borrower and the subsequent approval of loan request.

H1: There is an inverse relationship between the debt burden of the prospective borrower and the subsequent approval of loan request.

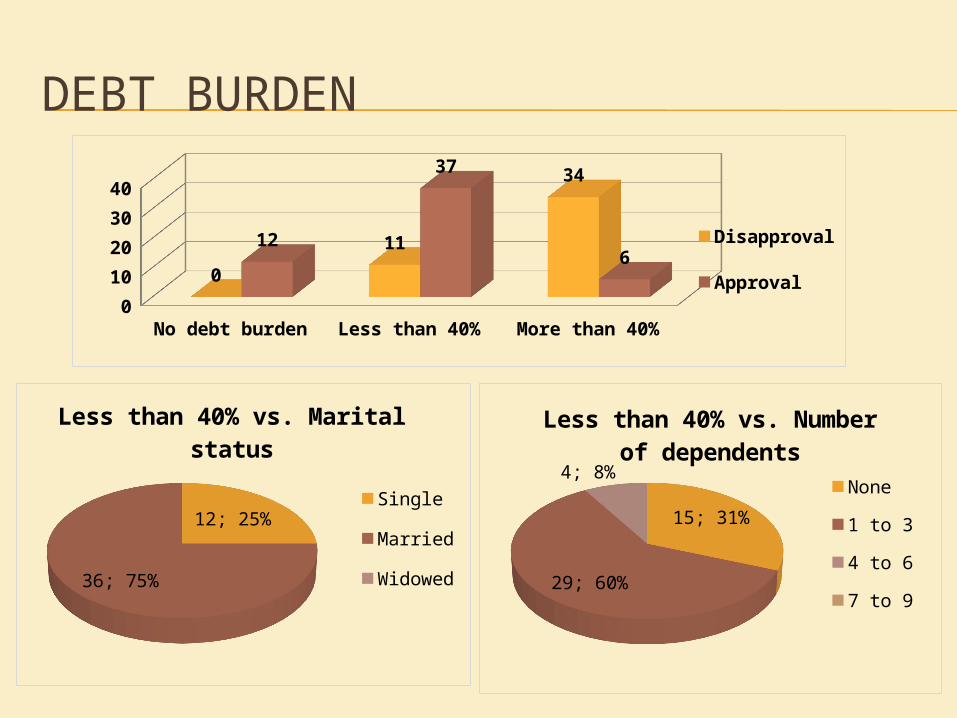

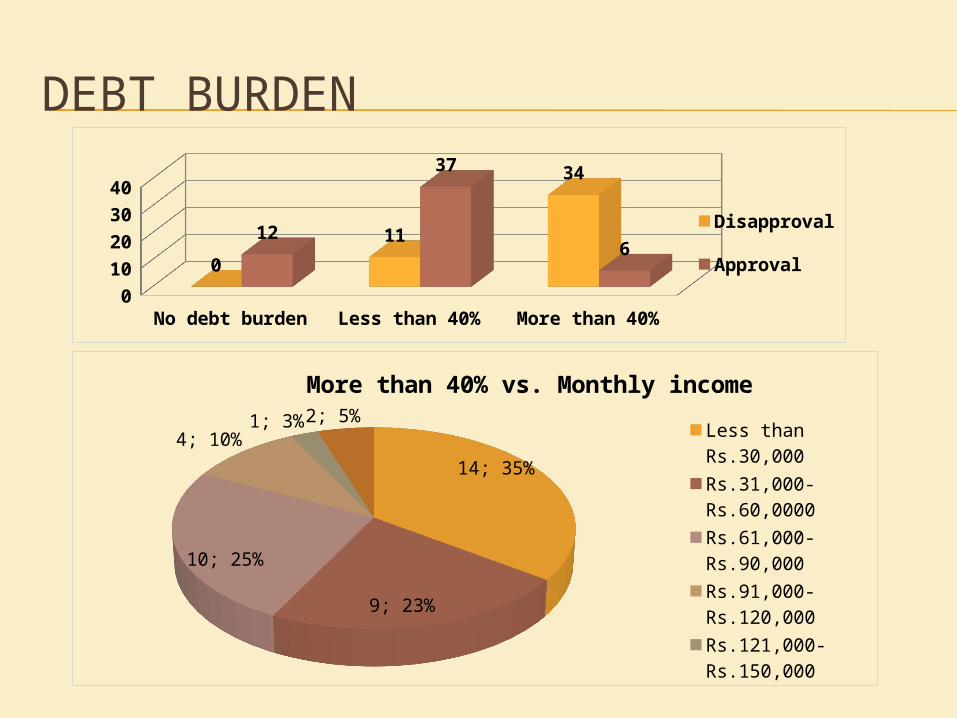

Has the bank approved or disapproved the loan request?

Debt burden Disapproval Approval Total

No debt burden 0 12 12

Less than 40% 11 37 48

More than 40% 34 6 40

Total 45 55 100

DEBT BURDEN

No debt burden

Less than 40% More than 40%0

10

20

30

40

0

11

34

12

37

6

Dis-ap-provalApproval

12; 100%

No debt burden vs. Have you taken loans

from other banks?

YesNo

4; 33%

1; 8%2; 17%

5; 42%

No debt burden vs. Monthly income Less than

Rs.30,000Rs.31,000- Rs.60,0000Rs.61,000-Rs.90,000Rs.91,000-Rs.120,000Rs.121,000-Rs.150,000Rs. 150,000+

DEBT BURDEN

9; 75%

3; 25%

No debt burden vs. Are you self em-

ployed?

Yes

No

3; 25%

6; 50%

3; 25%

No debt burden vs. Years of running business 1-3 years

4-6 years

7-9 years

10-12 years

13-15 years

16+ years

I don’t run my own business

No debt burden

Less than 40% More than 40%0

10

20

30

40

0

11

34

12

37

6

Dis-ap-provalApproval

DEBT BURDEN

2; 17%

6; 50%

1; 8%

3; 25%

No debt burden vs. Number of dependents

None

1 to 3

4 to 6

7 to 9

No debt burden

Less than 40% More than 40%0

10

20

30

40

0

11

34

12

37

6

Dis-ap-provalApproval

DEBT BURDEN

12; 25%

36; 75%

Less than 40% vs. Marital status

Single

Married

Widowed

15; 31%

29; 60%

4; 8%

Less than 40% vs. Number of dependents

None

1 to 3

4 to 6

7 to 9

No debt burden

Less than 40% More than 40%0

10

20

30

40

0

11

34

12

37

6

Dis-ap-provalApproval

DEBT BURDEN

7; 15%

6; 13%

17; 35%7; 15%

7; 15%

4; 8%

Less than 40% vs. Current employer

Less than 1 year

2-4 years

5-7 years

8-10 years

11+ years

I run my own business

29; 60%7; 15%

2; 4%4; 8%

6; 13%

Less than 40% vs. Monthly income

Less than Rs.30,000

Rs.31,000- Rs.60,0000

Rs.61,000-Rs.90,000

Rs.91,000-Rs.120,000

Rs.121,000-Rs.150,000

Rs. 150,000+

No debt burden

Less than 40% More than 40%0

10

20

30

40

0

11

34

12

37

6

Dis-ap-provalApproval

DEBT BURDEN

14; 35%

9; 23%

10; 25%

4; 10%1; 3%2; 5%

More than 40% vs. Monthly income

Less than Rs.30,000Rs.31,000- Rs.60,0000Rs.61,000-Rs.90,000Rs.91,000-Rs.120,000Rs.121,000-Rs.150,000Rs. 150,000+

No debt burden

Less than 40% More than 40%0

10

20

30

40

0

11

34

12

37

6

Dis-ap-provalApproval

DEBT BURDEN

10; 25%

13; 33%

11; 28%

3; 8%3; 8%

More than 40% vs. Monthly installment

Less than Rs.20, 000

Rs.21, 000- Rs.40, 000

Rs.41, 000- Rs.60, 000

Rs.61, 000- Rs.80, 000

Rs.81, 000+

No monthly in-stallment

No debt burden

Less than 40% More than 40%0

10

20

30

40

0

11

34

12

37

6Dis-ap-provalApproval

DEBT BURDEN

Both Sullivan and Fisher (1988) and Canner and Luckett (1991) found that the likelihood of late or missed payments on the borrowers’ auto loans and credit cards tend to arise in households that have a high ratio of monthly consumer debt payment to the monthly disposable income (Sullivan, 1988).

HYPOTHESIS 2: AGE Ho: There is no significant relationship between the age of

the potential borrowers and the subsequent approval of loan request.

H1:There is a significant relationship between the age of the potential borrowers and the subsequent approval of loan request.

Has the bank approved or disapproved the loan

request?

Age Disapproval Approval Total

21-25 5 4 9

26-30 6 20 26

31-35 16 10 26

36-40 2 4 6

41-45 4 10 14

46+ 12 7 19

Total 45 55 100

AGE

21-25 26-30 31-35 36-40 41-45 46+0

5

10

15

20

5 6

16

24

12

4

20

10

4

107

DisapprovalApproval

2; 22%

6; 67%

1; 11%

Age:21-25 vs. Current employer

Less than 1 year

2-4 years

5-7 years

8-10 years

11+ years

I run my own business

4; 15%

19; 73%

3; 12%

Age: 26-30 vs. Debt burden

No debt burden

Less than 40%

More than 40%

AGE

7; 27%

12; 46%

6; 23%

1; 4%

Age: 31-35 vs. Monthly income

Less than Rs.30,000

Rs.31,000- Rs.60,0000

Rs.61,000-Rs.90,000

Rs.91,000-Rs.120,000

Rs.121,000-Rs.150,000

Rs. 150,000+

21-25 26-30 31-35 36-40 41-45 46+05

101520

5 6

16

2 4

12

4

20

10

4

107

DisapprovalApproval

20; 77%

6; 23%

Age:31-35 vs. Have you ever taken loans from

other banks?

Yes

No

AGE

17; 65%

6; 23%

2; 8%

1; 4%

Age: 31-35 vs. Monthly installment

Less than Rs.20, 000Rs.21, 000- Rs.40, 000Rs.41, 000- Rs.60, 000Rs.61, 000- Rs.80, 000Rs.81, 000+No monthly installment

21-25 26-30 31-35 36-40 41-45 46+05

101520

5 6

16

2 4

12

4

20

10

4

107

DisapprovalApproval

11; 42%

15; 58%

Age: 31-35 vs. Debt burden

No debt burden

Less than 40%

More than 40%

AGE

21-25 26-30 31-35 36-40 41-45 46+05

101520

5 6

16

2 4

12

4

20

10

4

107

DisapprovalApproval

15; 79%

4; 21%

Age: 46+ vs. Have you taken loans from other banks?

Yes

No

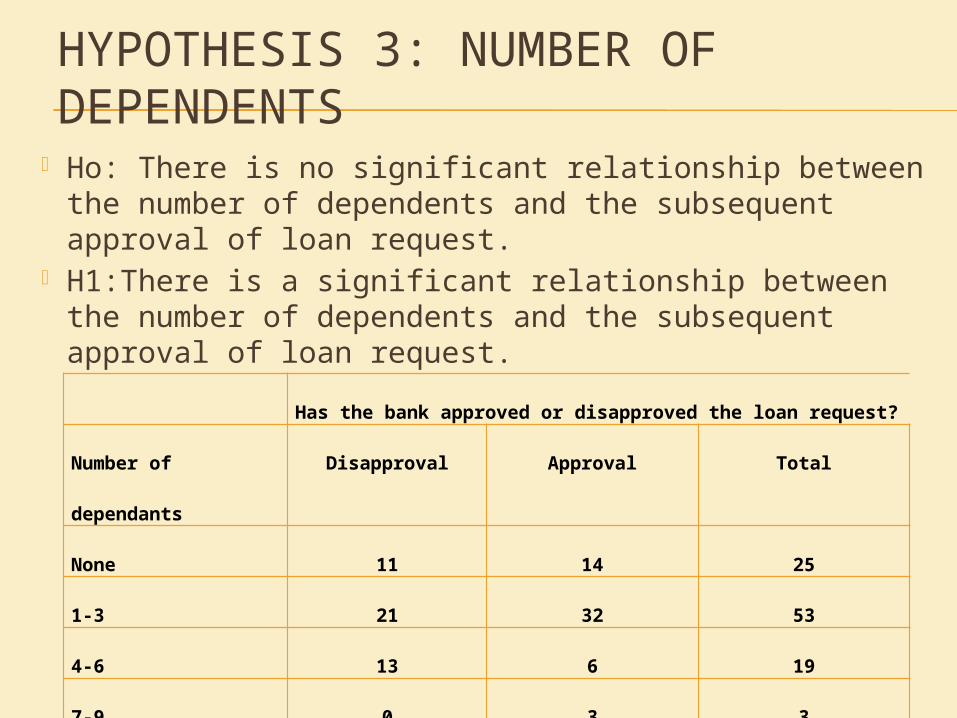

HYPOTHESIS 3: NUMBER OF DEPENDENTS

Ho: There is no significant relationship between the number of dependents and the subsequent approval of loan request.

H1:There is a significant relationship between the number of dependents and the subsequent approval of loan request.

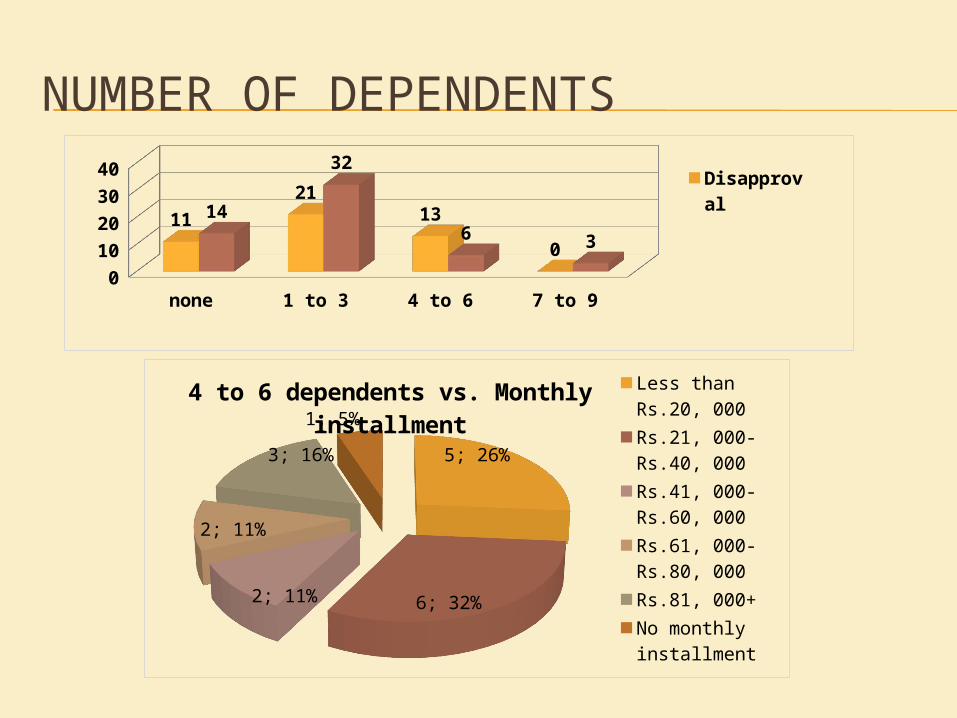

Has the bank approved or disapproved the loan request?

Number of

dependants

Disapproval Approval Total

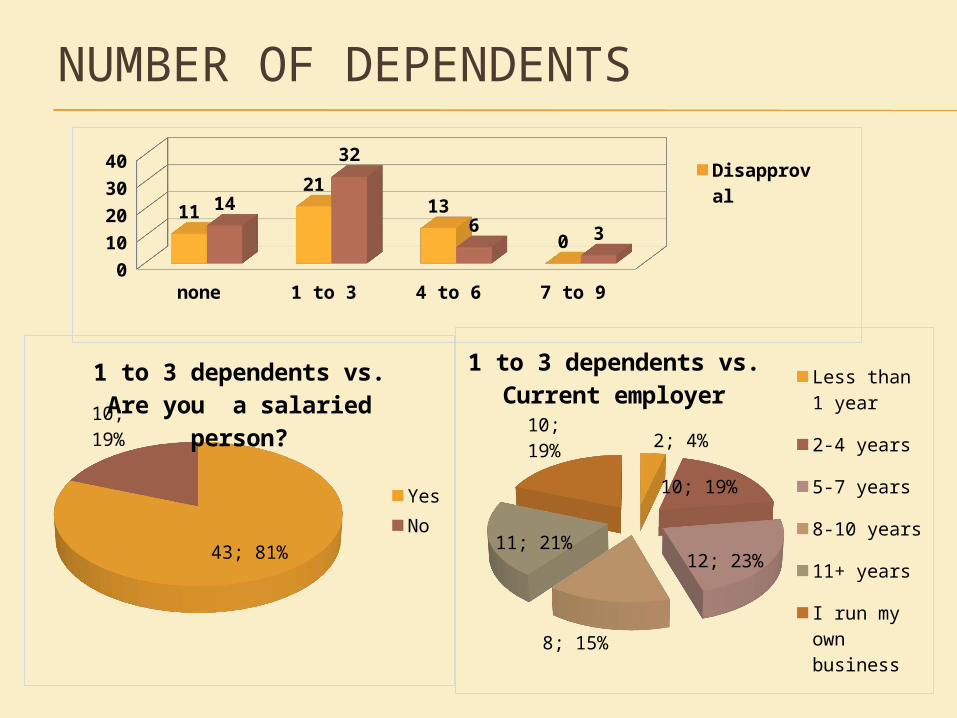

None 11 14 25

1-3 21 32 53

4-6 13 6 19

7-9 0 3 3

Total 45 55 100

NUMBER OF DEPENDENTS

none 1 to 3 4 to 6 7 to 90

10

20

30

40

11

2113

0

14

32

6 3

Dis-ap-proval

20; 80%

5; 20%

No dependents vs. Mar-ital status

Single

Married

Wid-owed 22; 88%

3; 12%

No dependents vs. Are you a salaried person?

Yes

No

NUMBER OF DEPENDENTS

7; 28%

16; 64%

2; 8%

No dependents vs. Monthly income

Less than Rs.30,000Rs.31,000- Rs.60,0000Rs.61,000-Rs.90,000Rs.91,000-Rs.120,000Rs.121,000-Rs.150,000Rs. 150,000+

none 1 to 3 4 to 6 7 to 90

10

20

30

40

11

2113

0

14

32

6 3

Dis-ap-proval

20; 80%

2; 8%3; 12%

No dependents vs. Employment status

Per-ma-nentContract

I run my own business

NUMBER OF DEPENDENTS

2; 4%

10; 19%

12; 23%

8; 15%

11; 21%

10; 19%

1 to 3 dependents vs. Current employer Less than 1

year

2-4 years

5-7 years

8-10 years

11+ years

I run my own business

43; 81%

10; 19%

1 to 3 dependents vs. Are you a salaried

person?

YesNo

none 1 to 3 4 to 6 7 to 90

10

20

30

40

11

2113

0

14

32

6 3

Dis-ap-proval

NUMBER OF DEPENDENTS

18; 95%

1; 5%

4 to 6 dependents vs. Have you taken loans

from other banks?

YesNo

2; 11%

5; 26%

4; 21%

1; 5%1; 5%

6; 32%

4-6 dependents vs. Monthly income

Less than Rs.30,000

Rs.31,000- Rs.60,0000

Rs.61,000-Rs.90,000

Rs.91,000-Rs.120,000

Rs.121,000-Rs.150,000

none 1 to 3 4 to 6 7 to 90

10203040

1121

13

0

14

32

6 3

Dis-ap-proval

NUMBER OF DEPENDENTS

5; 26%

6; 32%2; 11%

2; 11%

3; 16%

1; 5%

4 to 6 dependents vs. Monthly installment

Less than Rs.20, 000

Rs.21, 000- Rs.40, 000

Rs.41, 000- Rs.60, 000

Rs.61, 000- Rs.80, 000

Rs.81, 000+

No monthly installment

none 1 to 3 4 to 6 7 to 90

10

20

30

40

11

2113

0

14

32

6 3

Dis-ap-proval

3; 100%

7-9 dependents vs. Are you self employed?

Yes

No

3; 100%

7-9 dependents vs. Years of running business

1-3 years

4-6 years

7-9 years

10-12 years

13-15 years

16+ years

I don’t run my own business

NUMBER OF DEPENDENTS

none 1 to 3 4 to 6 7 to 90

10203040

1121

13

0

14

32

6 3

Dis-ap-proval

3; 100%

7 to 9 dependents vs. Have you taken loans

from other banks?

Yes

No

NUMBER OF DEPENDENTS

none 1 to 3 4 to 6 7 to 90

10

20

30

40

11

2113

0

14

32

6 3

Dis-ap-proval

3; 100%

7-9 dependents vs. Monthly income Less than

Rs.30,000

Rs.31,000- Rs.60,0000

Rs.61,000-Rs.90,000

Rs.91,000-Rs.120,000

Rs.121,000-Rs.150,000

Rs. 150,000+

NUMBER OF DEPENDENTS

3; 100%

7 to 9 dependents vs. Monthly installment Less than

Rs.20, 000

Rs.21, 000- Rs.40, 000

Rs.41, 000- Rs.60, 000

Rs.61, 000- Rs.80, 000

Rs.81, 000+

No monthly installment

none 1 to 3 4 to 6 7 to 90

10

20

30

40

11

2113

0

14

32

6 3

Dis-ap-proval

HYPOTHESIS 4: EDUCATIONAL QUALIFICATION Ho: There is no significant relationship between the

educational qualification of the borrowers and the subsequent approval of loan request.

H1: There is a significant positive relationship between the educational qualification of the borrowers and the subsequent approval of loan request.

Has the bank approved or disapproved the loan request?

Educational

Qualification

Disapproval Approval Total

Matric/O Level 1 0 1

Intermediate/ A

Level

3 1 4

Undergraduate 3 2 5

Graduate 21 26 47

Postgraduate 17 26 43

Total 45 55 100

EDUCATIONAL QUALIFICATION

39; 91%

1; 2%

3; 7%

Postgraduate vs. Em-ployment status

PermanentContractI run my own business

0

10

20

30

1 3 3

2117

0 1 2

26 26

Disapproval

Approval

EDUCATIONAL QUALIFICATION

highly qualified individuals are normally considered to get highly paid jobs (I.L. Ali, personal communication, February 15, 2013). Ali (2013) claims that with a better qualification on hand, they are likely to get hired by cash rich multinational companies

EDUCATIONAL QUALIFICATION

1; 25%

3; 75%

Intermediate vs. Are you self employed?

Yes

No

1; 25%

3; 75%

Intermediate vs. Age

21-2526-3031-3536-40 41-4546+

0

10

20

30

1 3 3

2117

0 1 2

26 26

Disapproval

Approval

EDUCATIONAL QUALIFICATION

82; 82%

18; 18%Are you self employed? Vs. Are

you salaried

salaried

self em-ployed

0

10

20

30

1 3 3

2117

0 1 2

26 26

Disapproval

Approval

CONCLUSION The thesis intended to investigate the

characteristics that banks evaluate before giving out loans to borrowers

According to this research, all four variables have a significant relationship with obtaining the loan approval Higher the debt burden, lower the chances are of

obtaining approval. The likelihood of loan approval is less in the early

twenties and late forties Lesser the number of dependents, the higher the

chances are of obtaining approval. Higher the educational qualification, higher the

chances are of obtaining approval.

FUTURE

Impact of economic environment must also be studied

Need to investigate the credit history of borrowers

The study must be conducted on more banks

Lending policies must be tightened Aggressive promotion of credit cards

must be avoided

REFERENCES

Aazim, M. (2012, June 11). Imbalance in Bank Lending. Retrieved February 14, 2013, from The Dawn: http://dawn.com/2012/06/11/imbalance-in-bank-lending/

Ali, I. L. (2013, February 14). Credit Officer Soneri Bank. (S. Moazzam, Interviewer)

Canner, G.B., & Luckett, C.A. (1991). Payment of household debts. Federal Reserve Bulletin, 77(April), 218-229.

Meyer, M. B. (1993). The Political Economy of Rural Loan Recovery: Evidence From Bangladesh. Savings and Development , 17 (1), 23-38.

Peterson, CM., & Peterson, R.L. (1981). Down payments, borrower characteristics, and defaults. Journal of Retail Banking, 3( 1, March), 1-6.

Sabir, M. A. (2012, August 27). Banking Sector: Non-performing Loans on the Rise. Retrieved February 14, 2013, from Investor Guide: http://investorguide360.com/latest-economic-news/banking-sector-non-performing-loans-on-the-rise-investcap-research/

Sullivan, C., & Fisher, R.M. (1988). Consumer credit delinquency risk: Characteristics of consumers who fall behind. Journal of Retail Banking, 10(3, Fall), 53-64.

THANK YOU