25

Prestasi Ekonomi Suku Keempat Tahun 2018 Gabenor Bank Negara Malaysia 14 Februari 2019 Sidang Akhbar

Prestasi Ekonomi Suku Keempat Tahun 2018

Gabenor

Bank Negara Malaysia

14 Februari 2019

Sidang Akhbar

Sidang akhbar akan meliputi:

Prestasi ekonomi pada suku keempat tahun 2018

Perkembangan monetari dan kewangan

2

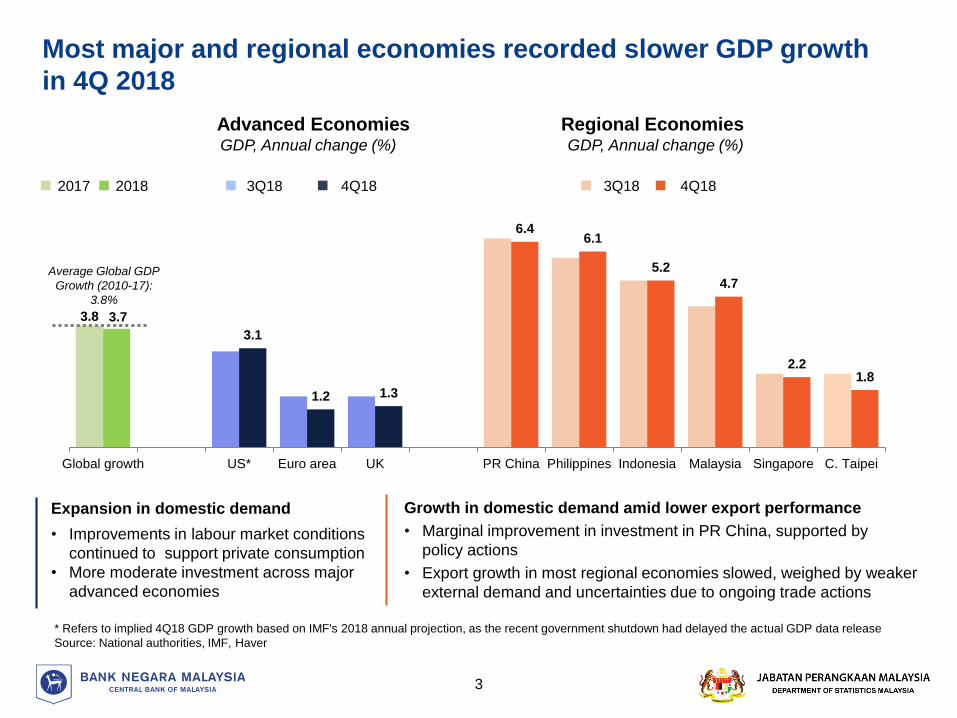

Most major and regional economies recorded slower GDP growth

in 4Q 2018

Advanced Economies

3.8 3.7

3.1

1.2 1.3

6.46.1

5.2

4.7

2.21.8

Global growth US* Euro area UK PR China Philippines Indonesia Malaysia Singapore C. Taipei

Regional EconomiesGDP, Annual change (%) GDP, Annual change (%)

* Refers to implied 4Q18 GDP growth based on IMF's 2018 annual projection, as the recent government shutdown had delayed the actual GDP data release

Source: National authorities, IMF, Haver

3

3Q18 4Q18

Growth in domestic demand amid lower export performance

• Marginal improvement in investment in PR China, supported by

policy actions

• Export growth in most regional economies slowed, weighed by weaker

external demand and uncertainties due to ongoing trade actions

Expansion in domestic demand

• Improvements in labour market conditions

continued to support private consumption

• More moderate investment across major

advanced economies

3Q18 4Q18

Average Global GDP

Growth (2010-17):

3.8%

2017 2018

4Q 2018 growth was supported by resilient private consumption and

some recoveries from the earlier supply disruptions

Source: Department of Statistics, Malaysia and Bank Negara Malaysia

• Resilient private

consumption

• Improvements in

commodity-

related sectors

• Stronger growth

in private

consumption

due to tax

holiday

• Lingering

commodity-

specific supply

shocks

1Q 2018 2Q 2018 3Q 2018 4Q 2018

5.4

4.54.4

4.7

• Private sector

spending

anchored

growth

• Strong net

exports growth

• Continued

private sector

spending

• Disruptions in

commodity-

related sectors

Drivers of GDP Growth (Annual change, %)

4

The Malaysian economy expanded by 4.7% in 4Q 2018

On the supply side, services and manufacturing

sectors remained the key drivers of growth

1 Numbers may not add up due to rounding and exclusion of import duties

Source: Department of Statistics, Malaysia and Bank Negara Malaysia

On the demand side, growth continued to be

anchored by the private sector

Annual change, % /

Ppt contribution to GDP

5

-2

0

2

4

6

8

4Q-17 1Q-18 2Q-18 3Q-18 4Q-18

Agriculture Mining Construction

Manufacturing Services GDP Growth

Annual change, % /

Ppt contribution to GDP1

4.75.9 5.4 4.5 4.45.9 5.4 4.5 4.4 4.7

-4

-2

0

2

4

6

8

4Q-17 1Q-18 2Q-18 3Q-18 4Q-18

Private consumption Private investmentPublic consumption Public investmentChange in stocks Net exportsGDP growth

Growth expanded by 4.7% in 2018 supported by resilient private

sector activities amid temporary supply disruptions

Commendable growth in 2018

Source: Department of Statistics, Malaysia and Bank Negara Malaysia

Annual change, %

GDP

6

6.0

5.1

4.2

5.9

4.7

0

1

2

3

4

5

6

7

2014 2015 2016 2017 2018

Factors Influencing Growth in 2018

• Resilient private sector spending

• Lift from net exports

• Continued expansion in the services

and manufacturing sectors

• Disruptions in commodity-related

sectors in 2Q and 3Q 2018

• Government spending rationalisation

1.1

3.0

-6

-4

-2

0

2

4

6

8

-30

-20

-10

0

10

20

30

40

4Q-17 1Q-18 2Q-18 3Q-18 4Q-18

% of GNIRM billion

Secondary Income

Primary Income

Services

Goods

Current Account Balance, % of GNI (RHS)

7

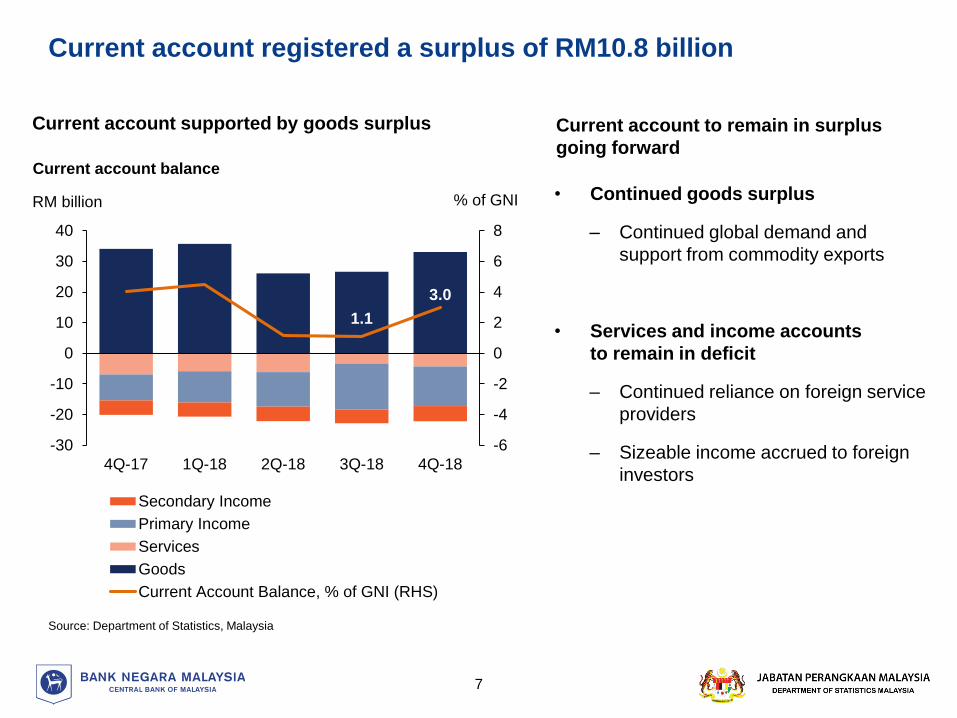

Current account registered a surplus of RM10.8 billion

Current account supported by goods surplus Current account to remain in surplus

going forwardCurrent account balance

• Continued goods surplus

– Continued global demand and

support from commodity exports

• Services and income accounts

to remain in deficit

– Continued reliance on foreign service

providers

– Sizeable income accrued to foreign

investors

Source: Department of Statistics, Malaysia

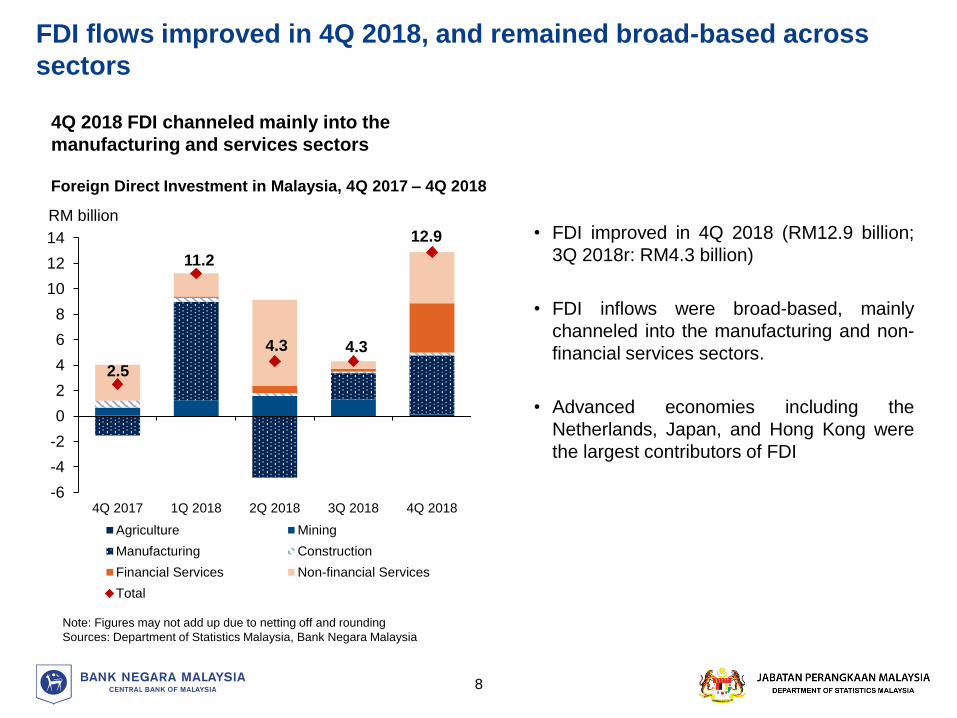

FDI flows improved in 4Q 2018, and remained broad-based across

sectors

Note: Figures may not add up due to netting off and rounding

Sources: Department of Statistics Malaysia, Bank Negara Malaysia

Foreign Direct Investment in Malaysia, 4Q 2017 – 4Q 2018

2.5

11.2

4.3 4.3

12.9

-6

-4

-2

0

2

4

6

8

10

12

14

4Q 2017 1Q 2018 2Q 2018 3Q 2018 4Q 2018

Agriculture Mining

Manufacturing Construction

Financial Services Non-financial Services

Total

4Q 2018 FDI channeled mainly into the

manufacturing and services sectors

8

• FDI improved in 4Q 2018 (RM12.9 billion;

3Q 2018r: RM4.3 billion)

• FDI inflows were broad-based, mainly

channeled into the manufacturing and non-

financial services sectors.

• Advanced economies including the

Netherlands, Japan, and Hong Kong were

the largest contributors of FDI

RM billion

Monetary and Financial Developments

9

Headline inflation declined in 4Q 2018

• In 2018, headline inflation averaged 1.0%

– Headline inflation during the quarter

declined as transport inflation turned

negative.

• In 2019, inflation is expected to average

moderately higher

– Impact of the consumption tax policy will

start to lapse towards the end of the year.

– The inflation outlook is subject to risks

related to the trajectory of global oil prices.

– Underlying inflation is expected to be

broadly stable.

*Note: Core inflation, which is a measure of underlying inflation, excludes the estimated direct impact of changes in consumption tax policies

Source: Department of Statistics, Malaysia and Bank Negara Malaysia

Contribution to Headline Inflation by Component

-2

-1

0

1

2

3

4

5

3Q 4Q 1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q

2017 2018

Net impact of consumption tax policy changes

Other price-administered items

Fuel

Price-volatile items (e.g. fresh food items)

Core inflation (ppt)

Headline inflation (%)

Core inflation* (%)

10

Annual change, % /

Ppt contribution to GDP

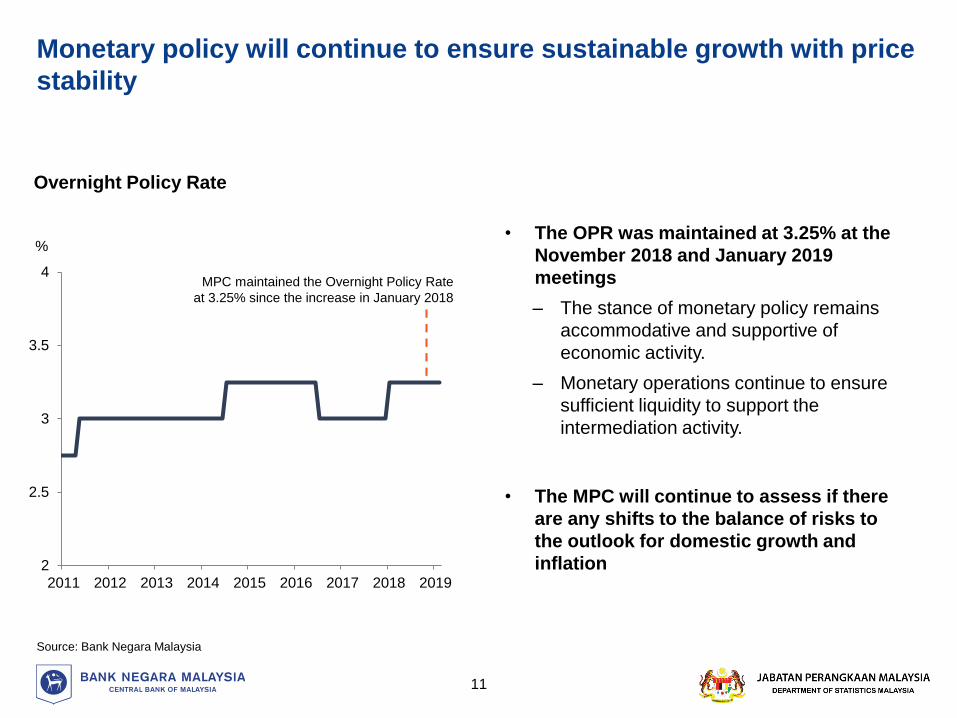

Monetary policy will continue to ensure sustainable growth with price

stability

• The OPR was maintained at 3.25% at the

November 2018 and January 2019

meetings

– The stance of monetary policy remains

accommodative and supportive of

economic activity.

– Monetary operations continue to ensure

sufficient liquidity to support the

intermediation activity.

• The MPC will continue to assess if there

are any shifts to the balance of risks to

the outlook for domestic growth and

inflation

Source: Bank Negara Malaysia

%

Overnight Policy Rate

2

2.5

3

3.5

4

2011 2012 2013 2014 2015 2016 2017 2018 2019

MPC maintained the Overnight Policy Rate

at 3.25% since the increase in January 2018

R

11

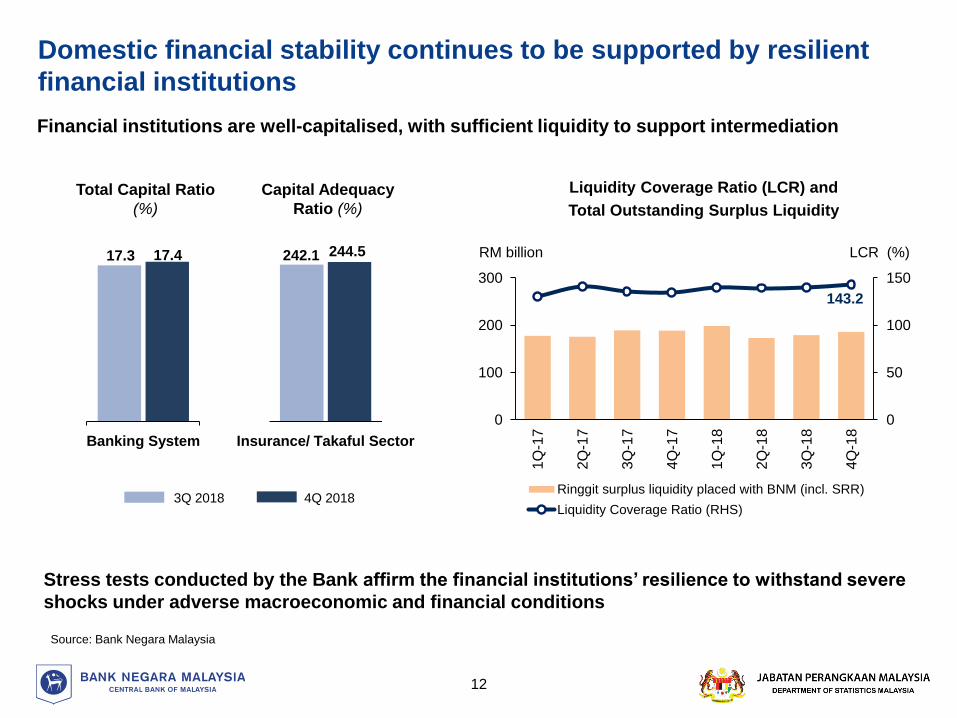

Financial institutions are well-capitalised, with sufficient liquidity to support intermediation

Stress tests conducted by the Bank affirm the financial institutions’ resilience to withstand severe

shocks under adverse macroeconomic and financial conditions

Source: Bank Negara Malaysia

RM billion LCR (%)

0

50

100

150

0

100

200

300

1Q

-17

2Q

-17

3Q

-17

4Q

-17

1Q

-18

2Q

-18

3Q

-18

4Q

-18

Ringgit surplus liquidity placed with BNM (incl. SRR)

Liquidity Coverage Ratio (RHS)

Liquidity Coverage Ratio (LCR) and

Total Outstanding Surplus Liquidity

Total Capital Ratio

(%)

Capital Adequacy

Ratio (%)

4Q 20183Q 2018

Insurance/ Takaful SectorBanking System

Domestic financial stability continues to be supported by resilient

financial institutions

12

242.1 244.517.3 17.4

143.2

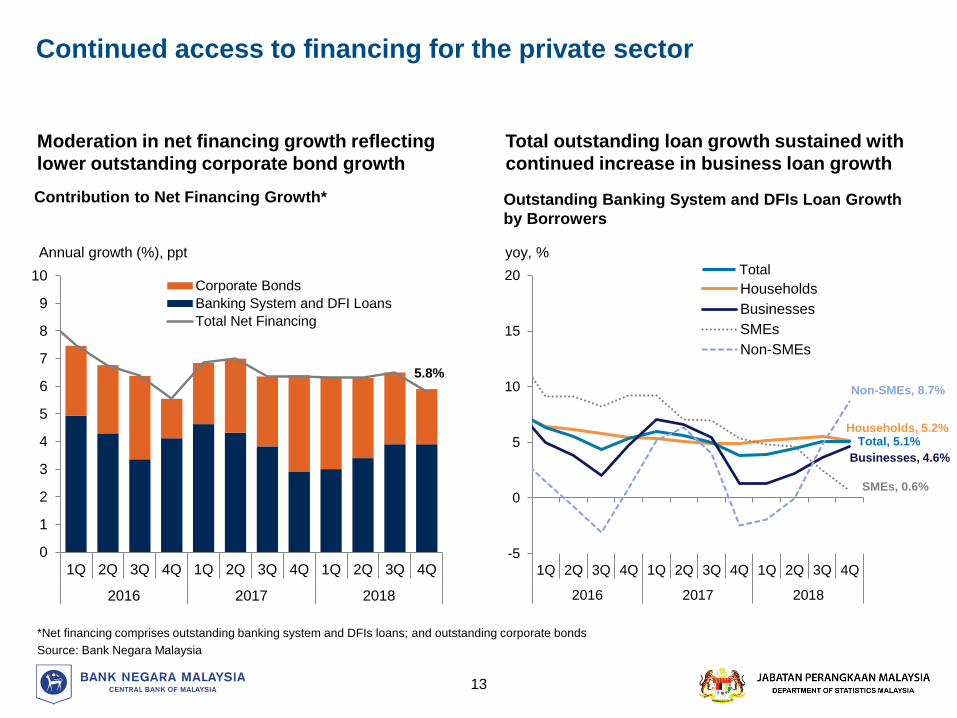

Continued access to financing for the private sector

Moderation in net financing growth reflecting

lower outstanding corporate bond growth

*Net financing comprises outstanding banking system and DFIs loans; and outstanding corporate bonds

Source: Bank Negara Malaysia

Total outstanding loan growth sustained with

continued increase in business loan growth

Contribution to Net Financing Growth*

0

1

2

3

4

5

6

7

8

9

10

1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q

2016 2017 2018

Corporate Bonds

Banking System and DFI Loans

Total Net Financing

Annual growth (%), ppt

-5

0

5

10

15

20

1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q

2016 2017 2018

Households

Businesses

SMEs

Non-SMEs

Outstanding Banking System and DFIs Loan Growth

by Borrowers

13

5.8%

Businesses, 4.6%

Total, 5.1%Households, 5.2%

yoy, %

Non-SMEs, 8.7%

SMEs, 0.6%

Total

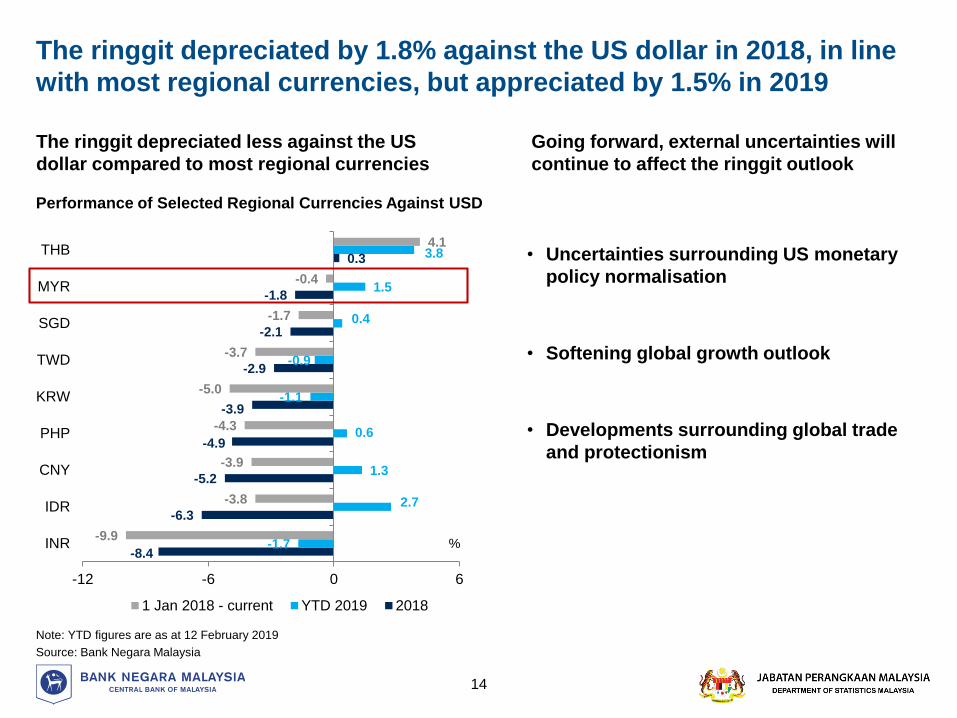

The ringgit depreciated less against the US

dollar compared to most regional currencies

-8.4

-6.3

-5.2

-4.9

-3.9

-2.9

-2.1

-1.8

0.3

-1.7

2.7

1.3

0.6

-1.1

-0.9

0.4

1.5

3.8

-9.9

-3.8

-3.9

-4.3

-5.0

-3.7

-1.7

-0.4

4.1

-12 -6 0 6

INR

IDR

CNY

PHP

KRW

TWD

SGD

MYR

THB

1 Jan 2018 - current YTD 2019 2018

The ringgit depreciated by 1.8% against the US dollar in 2018, in line

with most regional currencies, but appreciated by 1.5% in 2019

%

Going forward, external uncertainties will

continue to affect the ringgit outlook

• Uncertainties surrounding US monetary

policy normalisation

• Softening global growth outlook

• Developments surrounding global trade

and protectionism

Performance of Selected Regional Currencies Against USD

Note: YTD figures are as at 12 February 2019

Source: Bank Negara Malaysia

14

External debt edged lower and continues to remain manageable

Note: Numbers may not add up due to rounding

Source: Department of Statistics, Malaysia and Bank Negara Malaysia

Limited rollover risk as more

than half is represented by

medium- to long-term debt

Malaysia’s External Debt by MaturityEnd-4Q 2018: RM924.9 bn; % share

Close to a third is denominated

in ringgit……while risks from FX debt is

mostly subject to prudential

safeguards

Medium- to long-term

56%

Short-term

44%

Malaysia’s External Debt by Currency End-4Q 2018: RM924.9 bn; % share

Ringgit-denominated debt

31%

Foreign currency-denominated debt

69%

Trade credits

• Backed by export earnings

and self-liquidating

13%

24%

Intercompany loans

• Flexible/concessionary

terms

Interbank borrowings

(31.6%) and non-

resident deposits (7.3%)

• Banks required to hold

liquidity buffers and observe

the limits on funding and

maturity mismatches

Malaysia’s foreign-currency

denominated external debt in 4Q 2018 % share

39%

16%

8%

Bonds and notes

Others

63%

15

Reserves remain adequate and are not the only means to meet

external obligations

1.0

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1.4

1.6

1.8

2.0

0

20

40

60

80

100

120

140

160

180

200

2010 2012 2014 2016 2018

Net International Reserves

Reserves/ST ext debt (RHS)

Reserves-to-ST external debt

coverage at 1.0x adequate to

facilitate international transactions

Net International Reserves

USD billion Times

Banks account for about 75%

of short-term external debt

Banks have sufficient FCY

liquid assets to meet

external debt obligations

RM billion

16

* Comprises exposures to unrelated counterparties that can be susceptible to sudden withdrawal shocks

** STED refers to Short-Term External Debt

Source: Department of Statistics, Malaysia and Bank Negara Malaysia

Debt-at-risk1

64

251

136

0

50

100

150

200

250

300

Banks'FCY STED**

Banks' FCYliquid assets

Interbank borrowing

(intragroup)38%

Interbank borrowing (non

intragroup)12%

NR deposits24%

Intercompany loans4%

Trade credits13%

Others6%

External debt of the

banking sector (75%)

Loans

3%

Breakdown of Malaysia’s Short-Term

External Debt by Instrument

(End-4Q 2018: RM405.3 bn; % share)

In 2019, the Malaysian economy is likely to remain on a steady

growth path

17

2018

• Trend moderation after an exceptionally strong performance in 2017

• Economy impacted by one-off factors, namely, supply side shocks and post-

elections policy uncertainty

2019

• Global growth reverting to long-term trajectory

• Resilience of private consumption and continuation of civil engineering projects

• Recovery from supply side shocks

• Commencement of new production facilities (RAPID, E&E, retail outlet expansion)

• Materialisation of approved manufacturing investment

Q & A

18

Additional Information

19

The Malaysian economy grew by 4.7% in the fourth quarter

21

Note: 2 Numbers do not add up due to rounding and exclusion of import duties

component

Source: Department of Statistics, Malaysia

Note: 1 Numbers do not add up due to rounding

Source: Department of Statistics, Malaysia

Real GDP

(Annual change, %)

Share,

%

(2018)

2017 2018

2018

1Q 2Q 3Q 4Q

Domestic demand

(excluding stocks)91.6 6.5 5.6 4.1 5.6 6.9 5.6

Private Sector 72.8 7.5 7.2 5.2 7.5 8.5 7.7

Consumption 55.5 7.0 8.1 6.9 8.0 9.0 8.5

Investment 17.4 9.3 4.5 0.5 6.1 6.9 4.4

Public Sector 20.1 3.3 0.1 -0.1 -1.4 1.1 0.4

Consumption 12.8 5.4 3.3 0.4 3.1 5.2 4.0

Investment 7.3 0.1 -5.2 -1.0 -9.8 -5.5 -4.9

Net exports of

goods

and services

8.4 -1.9 13.4 62.4 1.7 -7.5 9.9

Exports 70.6 9.4 1.5 3.7 2.0 -0.8 1.3

Imports 62.2 10.9 0.1 -2.0 2.1 0.1 0.2

Change in stocks

(RM billion)-1.3 1.1 -16.2 -5.0 2.8 -6.5 -2.1

GDP (y-o-y) 1001 5.9 4.7 5.4 4.5 4.4 4.7

GDP (q-o-q growth,

seasonally

adjusted)

- - - 1.4 0.3 1.6 1.4

Real GDP

(Annual change, %)

Share, %

(2018)2017 2018

2018

1Q 2Q 3Q 4Q

Services 55.5 6.2 6.8 6.5 6.5 7.2 6.9

Manufacturing 23.0 6.0 5.0 5.3 4.9 5.0 4.7

Mining and

Quarrying7.9 1.0 -1.5 0.1 -2.2 -4.6 0.5

Agriculture 7.8 7.2 -0.4 2.8 -2.5 -1.4 -0.4

Construction 4.5 6.7 4.2 4.9 4.7 4.6 2.6

Real GDP 1002 5.9 4.7 5.4 4.5 4.4 4.7

20

Add. Info

1

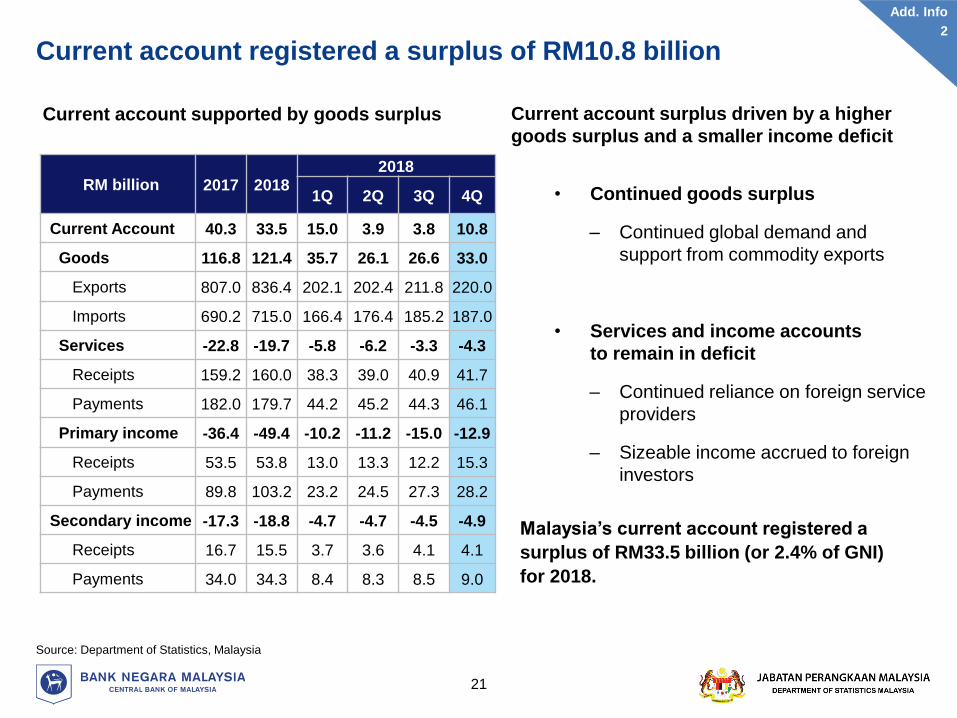

Current account registered a surplus of RM10.8 billion

Source: Department of Statistics, Malaysia

RM billion 2017 20182018

1Q 2Q 3Q 4Q

Current Account 40.3 33.5 15.0 3.9 3.8 10.8

Goods 116.8 121.4 35.7 26.1 26.6 33.0

Exports 807.0 836.4 202.1 202.4 211.8 220.0

Imports 690.2 715.0 166.4 176.4 185.2 187.0

Services -22.8 -19.7 -5.8 -6.2 -3.3 -4.3

Receipts 159.2 160.0 38.3 39.0 40.9 41.7

Payments 182.0 179.7 44.2 45.2 44.3 46.1

Primary income -36.4 -49.4 -10.2 -11.2 -15.0 -12.9

Receipts 53.5 53.8 13.0 13.3 12.2 15.3

Payments 89.8 103.2 23.2 24.5 27.3 28.2

Secondary income -17.3 -18.8 -4.7 -4.7 -4.5 -4.9

Receipts 16.7 15.5 3.7 3.6 4.1 4.1

Payments 34.0 34.3 8.4 8.3 8.5 9.0

Current account supported by goods surplus Current account surplus driven by a higher

goods surplus and a smaller income deficit

Malaysia’s current account registered a

surplus of RM33.5 billion (or 2.4% of GNI)

for 2018.

• Continued goods surplus

– Continued global demand and

support from commodity exports

• Services and income accounts

to remain in deficit

– Continued reliance on foreign service

providers

– Sizeable income accrued to foreign

investors

21

Add. Info

2

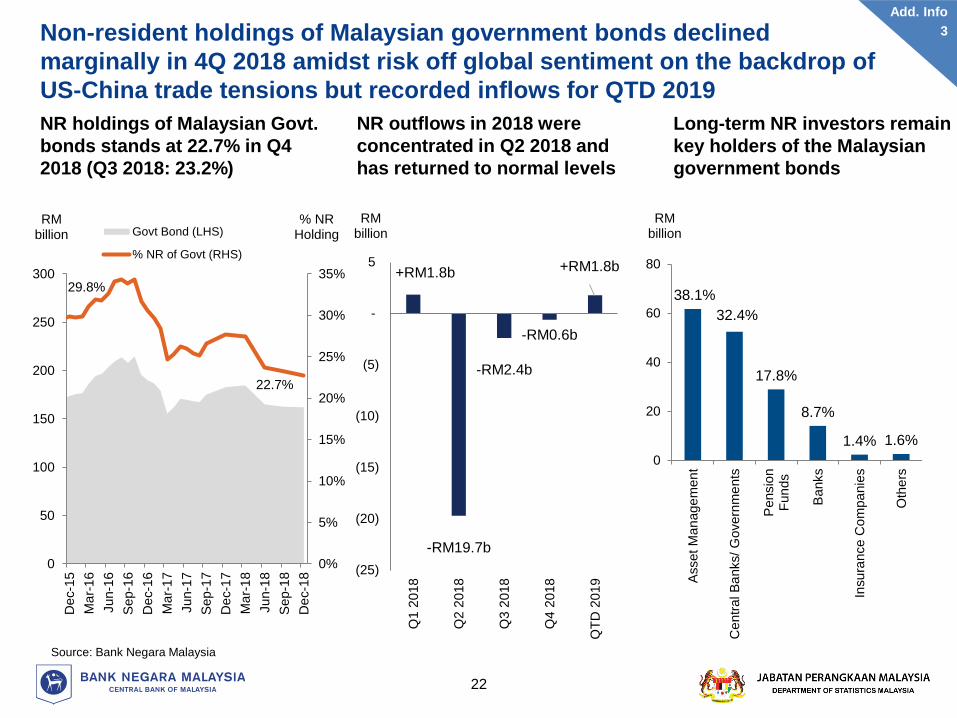

Non-resident holdings of Malaysian government bonds declined

marginally in 4Q 2018 amidst risk off global sentiment on the backdrop of

US-China trade tensions but recorded inflows for QTD 2019

22.7%

0%

5%

10%

15%

20%

25%

30%

35%

0

50

100

150

200

250

300

De

c-1

5

Ma

r-1

6

Jun-1

6

Sep-1

6

De

c-1

6

Ma

r-1

7

Jun-1

7

Se

p-1

7

De

c-1

7

Ma

r-1

8

Jun-1

8

Sep-1

8

De

c-1

8

% NR Holding

RM billion Govt Bond (LHS)

% NR of Govt (RHS)

29.8%

NR holdings of Malaysian Govt.

bonds stands at 22.7% in Q4

2018 (Q3 2018: 23.2%)

NR outflows in 2018 were

concentrated in Q2 2018 and

has returned to normal levels

Long-term NR investors remain

key holders of the Malaysian

government bonds

+RM1.8b

-RM19.7b

-RM2.4b

-RM0.6b

+RM1.8b

(25)

(20)

(15)

(10)

(5)

-

5

Q1 2

018

Q2 2

018

Q3 2

018

Q4 2

018

QT

D 2

019

RM billion

38.1%

32.4%

17.8%

8.7%

1.4% 1.6%

0

20

40

60

80

Asset

Man

age

men

t

Ce

ntr

al B

anks/

Govern

me

nts

Pensio

nF

un

ds

Banks

Insu

rance C

om

pa

nie

s

Oth

ers

RM billion

Source: Bank Negara Malaysia

Add. Info

3

22

Add. Info

3

2.4

2010 2012 2014 2016 2018

56

23

8 8 5

Services Mfg. Mining Agri. Const.

76.3 98.5

12.617.4

0

10

20

0

50

100

150

2008 2018

Size of Bond MarketCapital Ratio (RHS)

Malaysia’s macroeconomic fundamentals continue to remain strong

despite domestic and external headwinds/challenges

Broad-based sources of growth Favourable labour market

conditions

Deeper financial markets,

resilient banking system and

strong financial buffers

Continued current account

surplus

% of GNI

Current Account Balance

Malaysia GDP by Economic Sectors (2018)

% share of GDP

% of

nominal

GDP

Size of Bond Market

and Banking Capital Ratio %

Source: Department of Statistics, Malaysia and Bank Negara Malaysia p preliminary

Employment

Growth %

2017 2018

2.0

2.4*

* Bank Negara Malaysia estimates using data from the Quarterly Labour Force Survey published by DOSM

** Note: HK= Hong Kong, CN=China, SG= Singapore, UK= United Kingdom, JP=Japan, DE=Germany, ID=Indonesia, KR=South Korea, LU= Luxembourg, NIEs include Hong Kong, Chinese Taipei and Korea

10.8

2017 2018

8.6

Manufacturing

Wage Growth %

Conducive investment

destination for foreign investors

Outstanding FDI of RM 631bn

by Source Country (as at 4Q 2018)

RM Billion120

75 74

43 41 3927 22 21 18

SG JP HK NL US CH DE UK VG NO

ROW

Market

% share of exports

Diversified export market

and productProduct

% share of exports

E&E

Non-E&E

Commodities

PR ChinaNIEs

G3

ASEAN

38

46

16

2018

26

29

1414

18

2018

Add. Info

4

23

Add. Info

4

-4

-2

0

2

4

6

8

10

19

80

19

82

19

84

19

86

19

88

19

90

19

92

19

94

19

96

19

98

20

00

20

02

20

04

20

06

20

08

20

10

20

12

20

14

20

16

20

18

Global growth reverting to its long term growth trajectory

Note: The long term growth rates (1980-2018) for global, advanced and emerging market are 3.5%, 2.4% and 4.5%, respectively.

Source: National authorities and IMF

2.9

1.8

6.6

2.5

1.6

6.2

US Euro Area China

• 2018 • 2019f

Avg. GDP Growth

(2000-18): 2.1%

Avg. GDP Growth

(2000-18): 1.4%

Avg. GDP Growth

(2000-18): 9.1%

GDP growth in most major economies are trending towards their long term trend

Selected Major EconomiesGDP, Annual change (%)

Emerging Market Economies

World growthAdvanced Economies

Global Growth and Major RegionsGDP, Annual change (%)

Long-term avg. (1980 – 2018)

World: 3.5%

Advanced: 2.4%

EME: 4.5%

24

Add. Info

5

Add. Info

5

End

25