31

Price volatility in agricultural markets: drivers and implications 18 December 2012 DG Agriculture and Rural Development European Commission

Price volatility in agricultural markets: drivers and implications

18 December 2012

DG Agriculture and Rural Development

European Commission

Outline

1. Driver(s) of price volatility: no "smoking gun"?

2. What people says. What data shows

3. Implications

2

Long term commodity price trends

0

50

100

150

200

250

300

350

400

450

1948

1950

1952

1954

1956

1958

1960

1962

1964

1966

1968

1970

1972

1974

1976

1978

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008

2010

2012

(World Bank MUV-deflated indices, 2005 = 100)

Agriculture Fertilizers Energy Metals

Source: World Bank. Note: 2012 figures are forecasts as of September 2012.

3

4

While the commodity price boom has been attributed to many factors…

Common/macro factors

• Economic growth

• Weak dollar

• Fiscal expansion

• Low cost of capital

• Financialisation of commodities

Sector-specific factors

Exogenous to agriculture

• Energy prices

• Weather

• Food demand

• Biofuels

Endogenous to agriculture

• Policies

• Underinvestment

• Low stocks

5

… the "perception" attributes the 2007-2008 agricultural price boom to a selective few

Common/macro factors

• Economic growth

• Weak dollar

• Fiscal expansion

• Low cost of capital

• Financialisation of commodities

Sector-specific factors

Exogenous to agriculture

• Energy prices

• Weather

• Food demand

• Biofuels

Endogenous to agriculture

• Policies

• Underinvestment

• Low stocks

6

Four basic questions to understand high and volatile commodity prices

1. Is price volatility higher than in the past?

2. Is this driven by higher yield variability?

3. Is it due to a sharp increase in food demand?

4. Are agricultural prices more sensitive to stock changes?

7

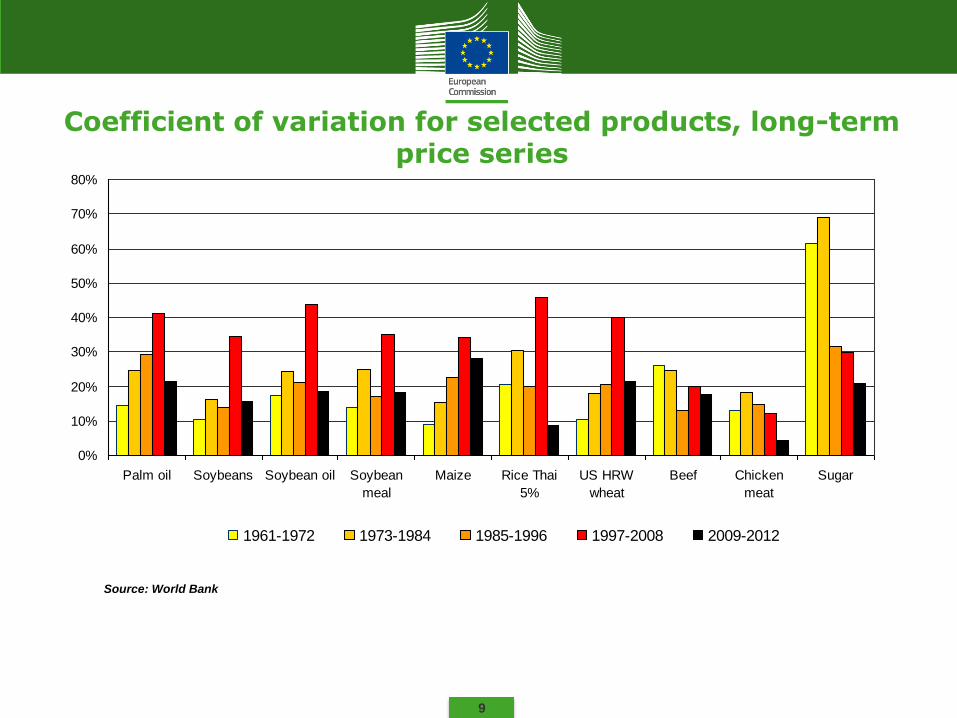

1. Is price volatility higher than in the past?

The analysis over the last 50 years shows:

• Price volatility higher in recent decade for most products, but lower lately

• Exception only for beef, poultry, sugar (higher in the 70s)

• EU price volatility was higher than at world level (CAP reform process of market orientation)

8

Long term price developments for key agricultural commodities

Source: World Bank

USD/mt in current USD

0

200

400

600

800

1000

1200

1400

1600

1960

1962

1964

1966

1968

1970

1972

1974

1976

1978

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008

2010

2012

Wheat (HRW) Soybeans Maize Soybean oil Rice

9

Coefficient of variation for selected products, long-term price series

Source: World Bank

0%

10%

20%

30%

40%

50%

60%

70%

80%

Palm oil Soybeans Soybean oil Soybean

meal

Maize Rice Thai

5%

US HRW

wheat

Beef Chicken

meat

Sugar

1961-1972 1973-1984 1985-1996 1997-2008 2009-2012

10

Coefficient of variation for comparable products, 1997-2003 vs 2004-2010, EU and World

Sources: Agriview and World Bank

0%

5%

10%

15%

20%

25%

30%

35%

40%

1997 -

2003

2004 -

2010

1997 -

2003

2004 -

2010

1997 -

2003

2004 -

2010

1997 -

2003

2004 -

2010

1997 -

2003

2004 -

2010

1997 -

2003

2004 -

2010

1997 -

2003

2004 -

2010

Barley Wheat (Int. SRW,

EU Bread)

Maize Butter SMP Chicken Beef

EU (Agriview) World (WB)

11

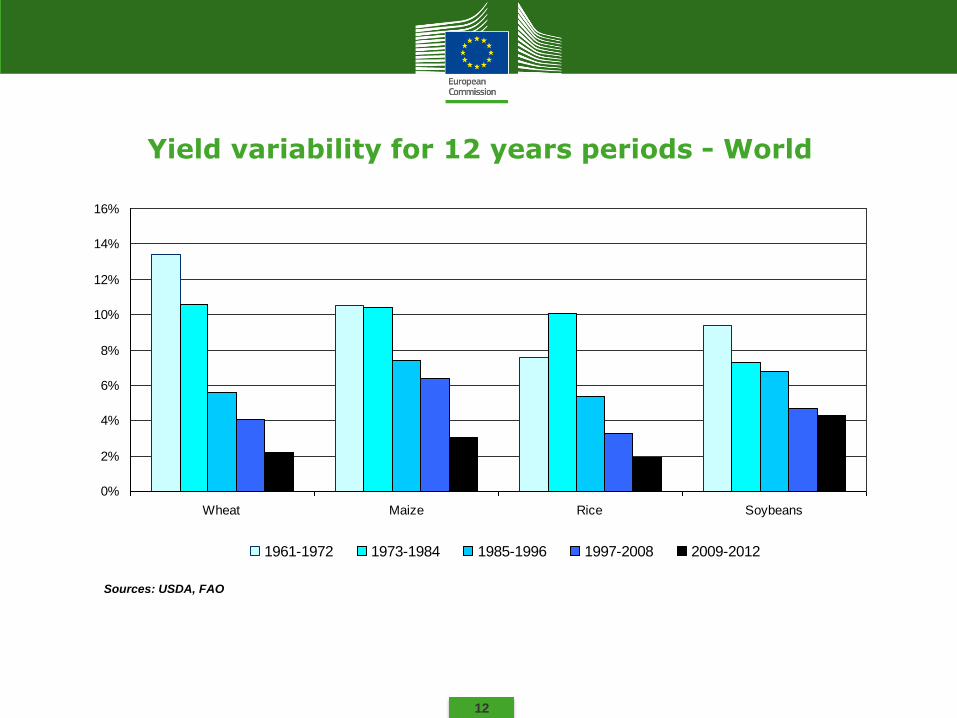

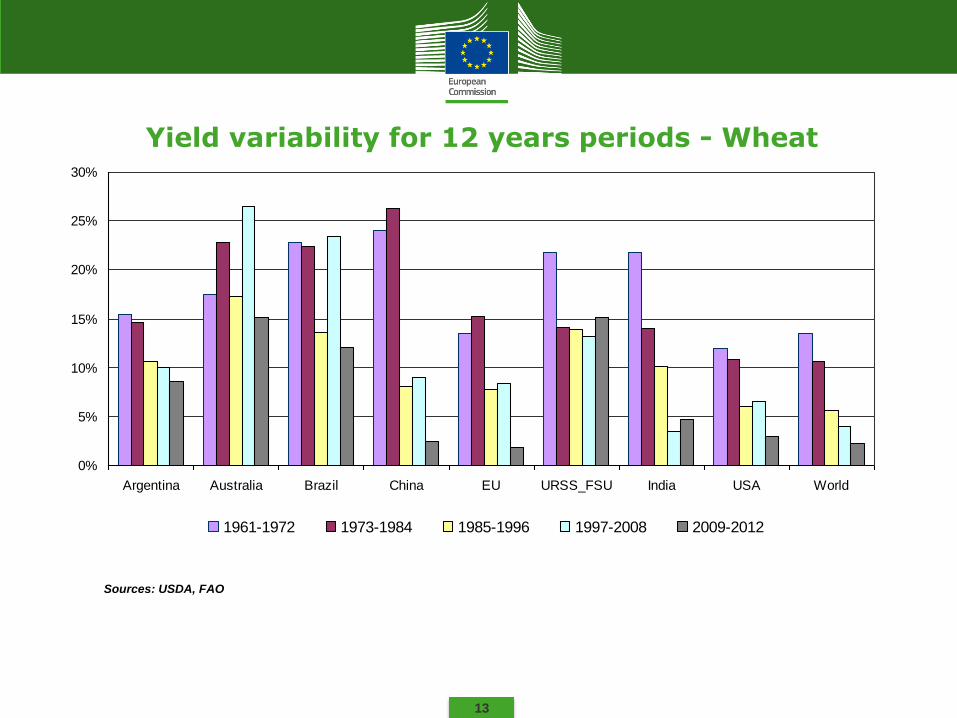

2. Is higher price volatility driven by higher yield variability?

The analysis shows:

• No straightforward conclusions can be drawn

• Different between countries and commodities

12

Yield variability for 12 years periods - World

Sources: USDA, FAO

0%

2%

4%

6%

8%

10%

12%

14%

16%

Wheat Maize Rice Soybeans

1961-1972 1973-1984 1985-1996 1997-2008 2009-2012

13

Yield variability for 12 years periods - Wheat

0%

5%

10%

15%

20%

25%

30%

Argentina Australia Brazil China EU URSS_FSU India USA World

1961-1972 1973-1984 1985-1996 1997-2008 2009-2012

Sources: USDA, FAO

14

Yield variability for 12 years periods - Maize

0%

5%

10%

15%

20%

25%

30%

Argentina Australia Brazil China EU URSS-FSU India USA World

1961-1972 1973-1984 1985-1996 1997-2008 2009-2012

Sources: USDA, FAO

15

Yield variability for 12 years periods - Rice

0%

5%

10%

15%

20%

25%

30%

Argentina Australia Brazil China EU URSS-FSU India USA World

1961-1972 1973-1984 1985-1996 1997-2008 2009-2012

Sources: USDA, FAO

16

Yield variability for 12 years - Soybeans

0%

5%

10%

15%

20%

25%

30%

Argentina Australia Brazil China EU URSS-FSU India USA World

1961-1972 1973-1984 1985-1996 1997-2008 Column 5

Sources: USDA, FAO

17

Yield variability for 12 years - Sugar

0%

5%

10%

15%

20%

25%

30%

Australia

(cane)

Brazil (cane) China (cane) EU (beet) USSR-FSU

(beet)

USA (cane) India (cane) World (cane) World (beet)

1961-1972 1973-1984 1985-1996 1997-2008

Sources: USDA, FAO

18

3. Is higher price volatility driven by sharp increase in food demand?

The analysis shows:

• Agricultural products: Demand growth has decreased over the last 50 years for most products and countries (exception veg. oils and dairy products)

• Energy and minerals/metals: Demand growth is on the increase since mid 80s (iron, aluminium) and mid 90s (crude oil)

19

Growth rates for main agricultural products, crude oil and selected minerals/metals

-4%

-2%

0%

2%

4%

6%

8%

10%

Grains Grains for

feed

Vegetable

oils

Meats Dairy

products

Iron ore Aluminium Crude oil

1961-1972

1973-1984

1985-1996

1997-2008

World per capita demand growth for agricultural commodities, USDA, FAO. World production growth for crude oil (International Energy Agency) and Metals/minerals (U.S. Geological Survey)

20

4. Are agricultural prices more sensitive to stock changes?

The analysis shows:

• The relationship between stock-to-use and world prices did not change much over the last 50 years.

• A certain increase in responsiveness can be observed for the main crops (wheat, maize, soybean) in the two past decades.

• Sugar prices on the other hand were more sensitive to stock changes in the 70s and 80s than recently (link with oil price).

• No significant linkage for rice and vegetable oils.

21

Yearly changes in stocks to use and prices Maize

Source: World Bank, USDA

-40%

-30%

-20%

-10%

0%

10%

20%

30%

40%

50%

60%

1961-6

2

1963-6

4

1965-6

6

1967-6

8

1969-7

0

1971-7

2

1973-7

4

1975-7

6

1977-7

8

1979-8

0

1981-8

2

1983-8

4

1985-8

6

1987-8

8

1989-9

0

1991-9

2

1993-9

4

1995-9

6

1997-9

8

1999-0

0

2001-0

2

2003-0

4

2005-0

6

2007-0

8

2009-1

0

2011-1

2

Change in World prices Change in stocks to use

22

Yearly changes in stocks to use and prices Wheat

Source: World Bank, USDA

-40%

-30%

-20%

-10%

0%

10%

20%

30%

40%

50%

60%

70%

80%

1961-6

2

1963-6

4

1965-6

6

1967-6

8

1969-7

0

1971-7

2

1973-7

4

1975-7

6

1977-7

8

1979-8

0

1981-8

2

1983-8

4

1985-8

6

1987-8

8

1989-9

0

1991-9

2

1993-9

4

1995-9

6

1997-9

8

1999-0

0

2001-0

2

2003-0

4

2005-0

6

2007-0

8

2009-1

0

2011-1

2

Change in World prices Change in stocks to use

23

Yearly changes in stocks to use and prices Soybeans

Source: World Bank, USDA

-60%

-40%

-20%

0%

20%

40%

60%

80%

100%

120%

1961-6

2

1963-6

4

1965-6

6

1967-6

8

1969-7

0

1971-7

2

1973-7

4

1975-7

6

1977-7

8

1979-8

0

1981-8

2

1983-8

4

1985-8

6

1987-8

8

1989-9

0

1991-9

2

1993-9

4

1995-9

6

1997-9

8

1999-0

0

2001-0

2

2003-0

4

2005-0

6

2007-0

8

2009-1

0

2011-1

2

Change in World prices Change in stocks to use

24

Yearly changes in stocks to use and prices Rice

Source: World Bank, USDA

-60%

-40%

-20%

0%

20%

40%

60%

80%

100%

1961-6

2

1963-6

4

1965-6

6

1967-6

8

1969-7

0

1971-7

2

1973-7

4

1975-7

6

1977-7

8

1979-8

0

1981-8

2

1983-8

4

1985-8

6

1987-8

8

1989-9

0

1991-9

2

1993-9

4

1995-9

6

1997-9

8

1999-0

0

2001-0

2

2003-0

4

2005-0

6

2007-0

8

2009-1

0

2011-1

2

Change in World prices Change in stocks to use

Evolution of stock-to-use ratio - wheat

0

50

100

150

200

250

300

350

400

450

500

1960

1962

1964

1966

1968

1970

1972

1974

1976

1978

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008

2010

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%2005 $/mt % of use

Stock-to-use ratio Price (HRW)

25

Sources: USDA for stocks and use, World Bank for prices (nominal prices)

Evolution of stock-to-use ratio - maize

0

50

100

150

200

250

300

350

400

450

500

1960

1962

1964

1966

1968

1970

1972

1974

1976

1978

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008

2010

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%2005 $/mt % of use

Stock-to-use ratio Price

26

Sources: USDA for stocks and use, World Bank for prices (nominal prices)

Stock-to-use / price relation: wheat

27 Sources: USDA for stocks and use, World Bank for prices (nominal prices)

R² = 0,0933

0

50

100

150

200

250

300

350

400

450

500

0% 5% 10% 15% 20% 25% 30% 35% 40% 45% 50%

Stock-to-use ratio

Wheat real price

Stock-to-use / price relation: maize

28 Sources: USDA for stocks and use, World Bank for prices (nominal prices)

R² = 0,3448

0

50

100

150

200

250

300

350

400

450

500

0% 5% 10% 15% 20% 25% 30% 35% 40% 45% 50%

Stock-to-use ratio

Maize real price

29

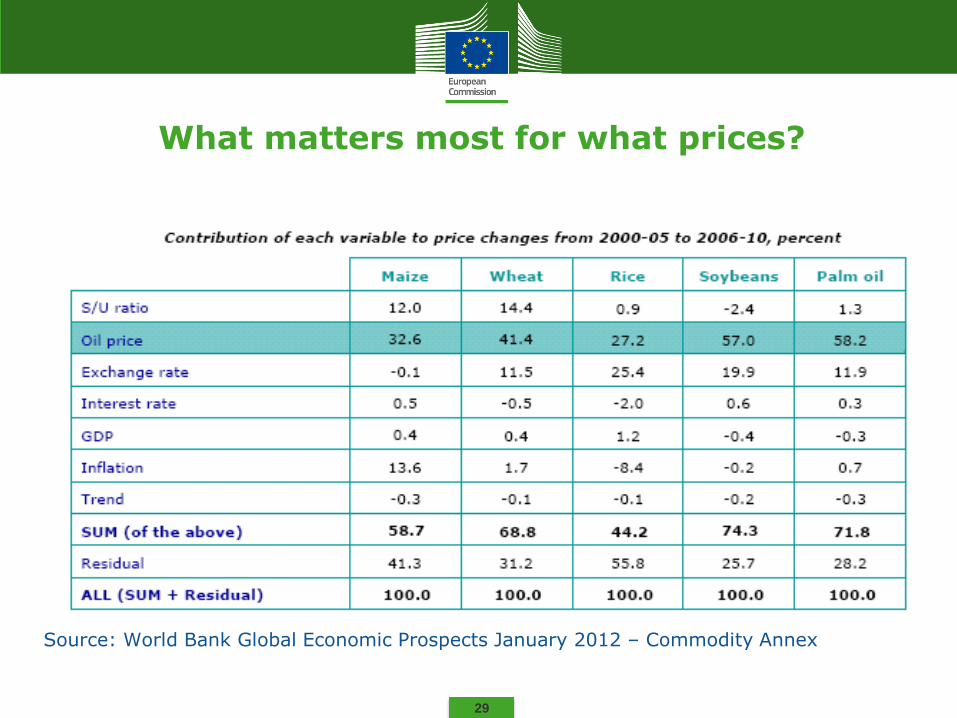

What matters most for what prices?

Source: World Bank Global Economic Prospects January 2012 – Commodity Annex

30

Ongoing research: are there distortions?

Spot market

Futures market

Options market

Convergence close to maturity

• High frequency volatility estimation

• Historical vs risk neutral measure for put&call pricing

31

Implications

• Higher prices for agricultural commodities will not necessarily result in higher income for farmers, especially if their margins are squeezed by increased costs

• With higher output prices expected, there is less and less scope for "traditional" intervention tools, such as price support

• Excessive price volatility affects profitability and hinders investments in the agricultural sector

• Ad-hoc policy intervention in agriculture to address volatility may be questionable if volatility is "imported" from outside agriculture