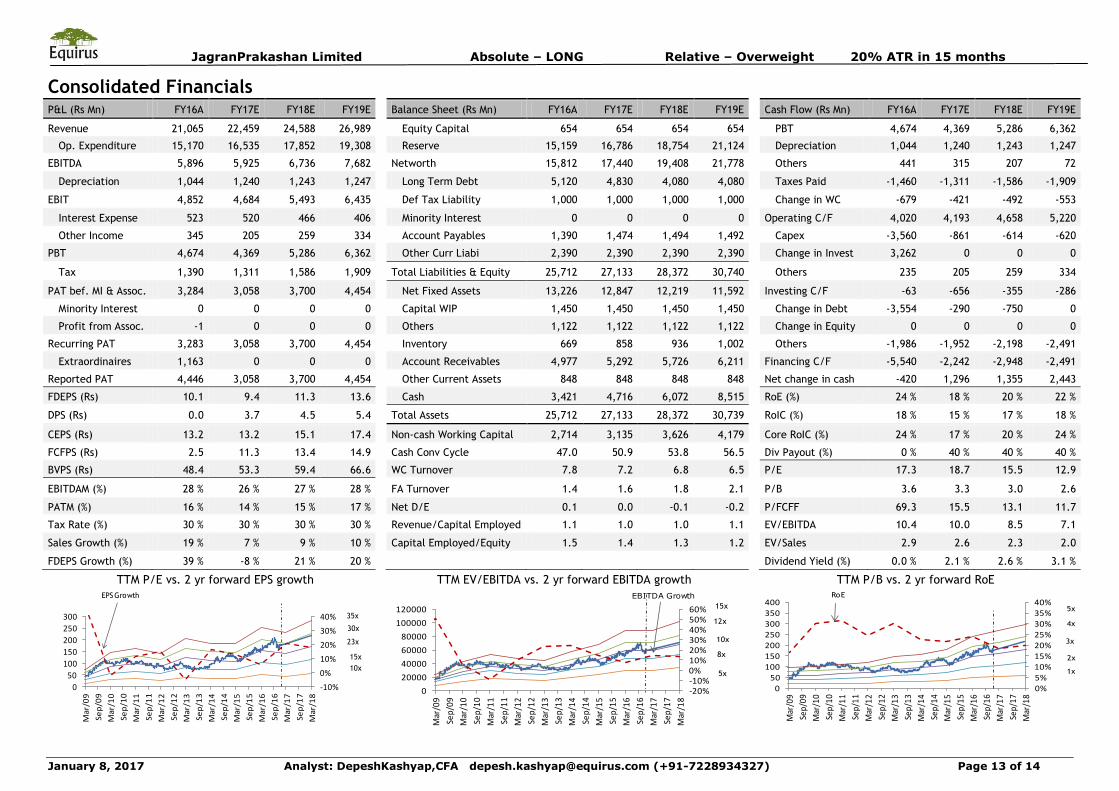

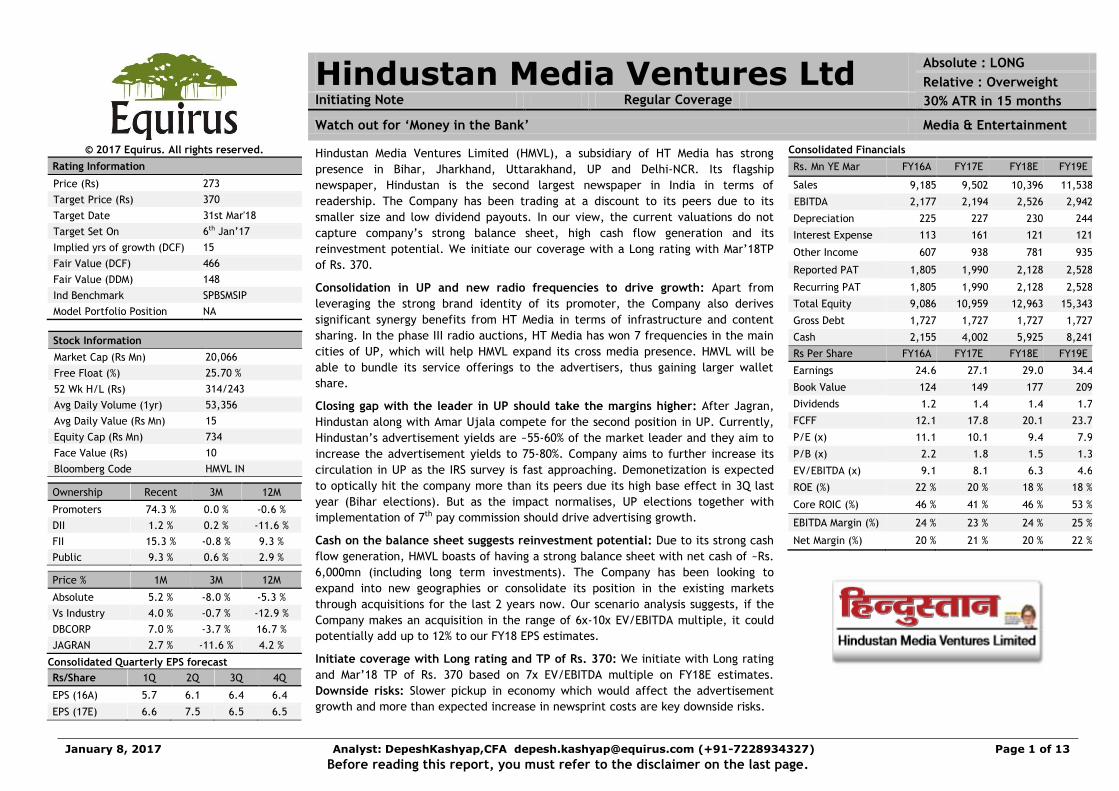

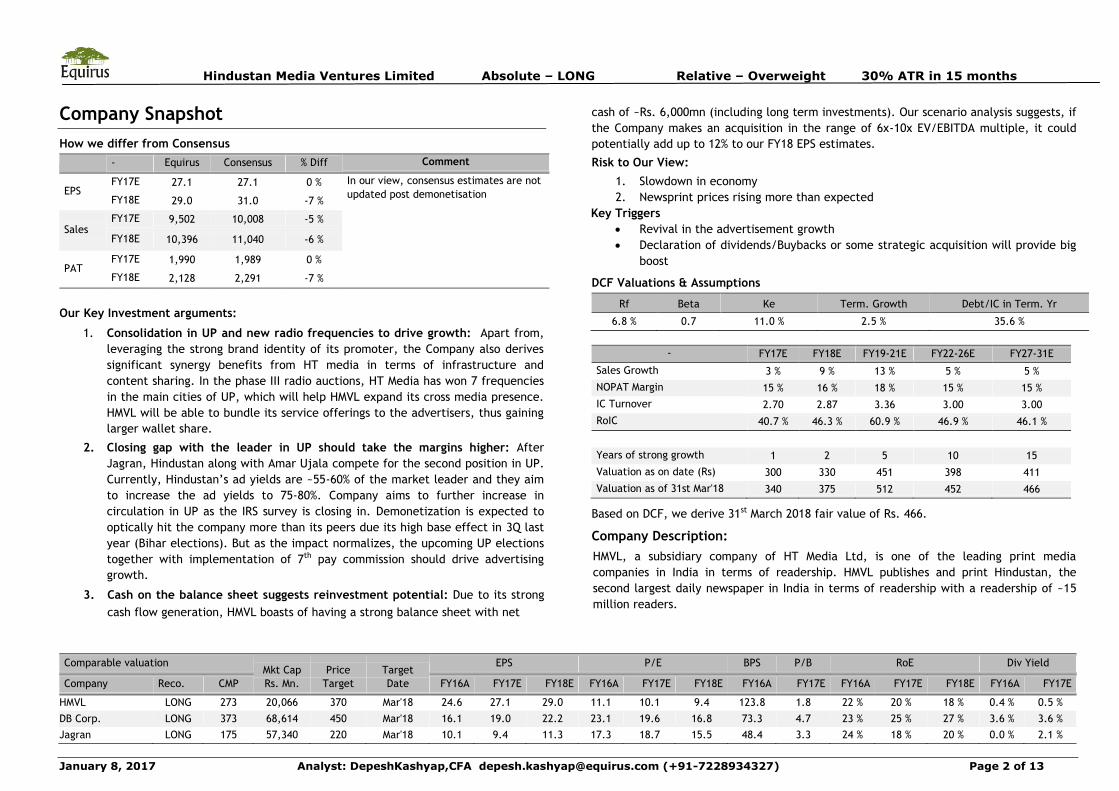

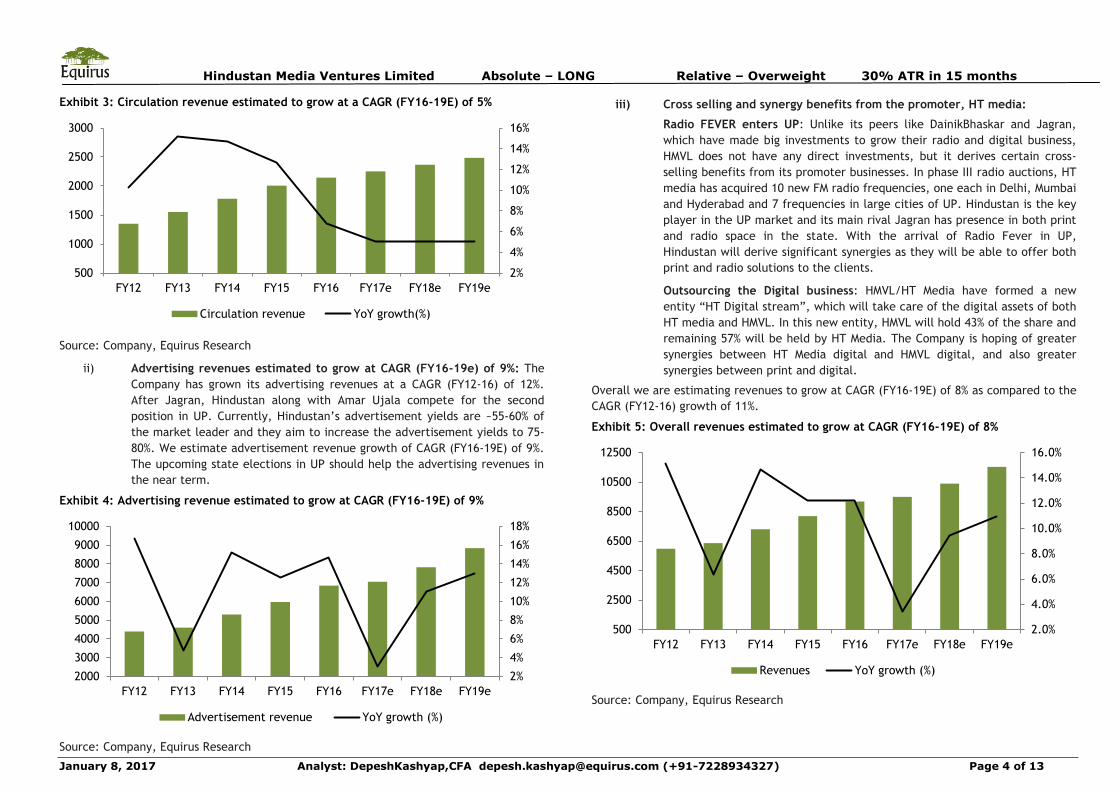

Page 1

January 8, 2017 Analyst: Depesh Kashyap,CFA [email protected] (+91-7228934327) Page 1 of 35

Before reading this report, you must refer to the disclaimer on the last page.

© 2017 Equirus All rights reserved

Print Media

Overweight

Initiating coverage: India still waking up to newspapers

S

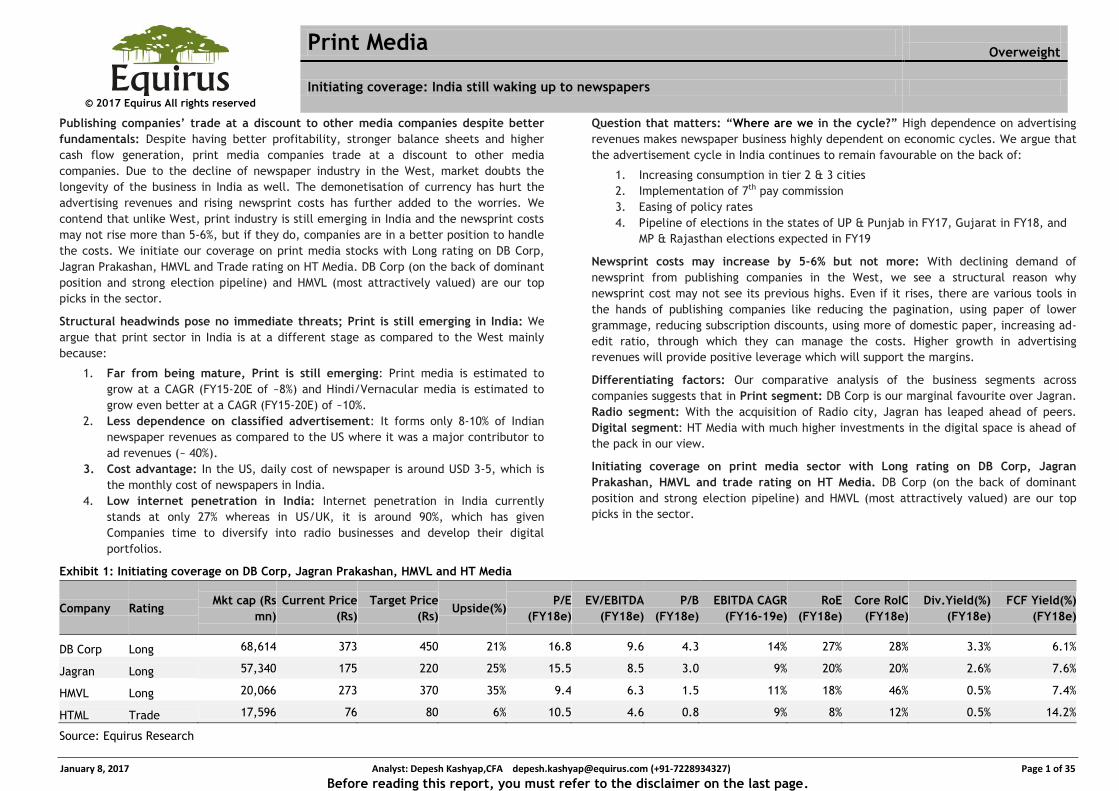

Publishing companies’ trade at a discount to other media companies despite better

fundamentals: Despite having better profitability, stronger balance sheets and higher

cash flow generation, print media companies trade at a discount to other media

companies. Due to the decline of newspaper industry in the West, market doubts the

longevity of the business in India as well. The demonetisation of currency has hurt the

advertising revenues and rising newsprint costs has further added to the worries. We

contend that unlike West, print industry is still emerging in India and the newsprint costs

may not rise more than 5-6%, but if they do, companies are in a better position to handle

the costs. We initiate our coverage on print media stocks with Long rating on DB Corp,

Jagran Prakashan, HMVL and Trade rating on HT Media. DB Corp (on the back of dominant

position and strong election pipeline) and HMVL (most attractively valued) are our top

picks in the sector.

Structural headwinds pose no immediate threats; Print is still emerging in India: We

argue that print sector in India is at a different stage as compared to the West mainly

because:

1. Far from being mature, Print is still emerging: Print media is estimated to

grow at a CAGR (FY15-20E of ~8%) and Hindi/Vernacular media is estimated to

grow even better at a CAGR (FY15-20E) of ~10%.

2. Less dependence on classified advertisement: It forms only 8-10% of Indian

newspaper revenues as compared to the US where it was a major contributor to

ad revenues (~ 40%).

3. Cost advantage: In the US, daily cost of newspaper is around USD 3-5, which is

the monthly cost of newspapers in India.

4. Low internet penetration in India: Internet penetration in India currently

stands at only 27% whereas in US/UK, it is around 90%, which has given

Companies time to diversify into radio businesses and develop their digital

portfolios.

Exhibit 1: Initiating coverage on DB Corp, Jagran Prakashan, HMVL and HT Media

Question that matters: “Where are we in the cycle?” High dependence on advertising

revenues makes newspaper business highly dependent on economic cycles. We argue that

the advertisement cycle in India continues to remain favourable on the back of:

1. Increasing consumption in tier 2 & 3 cities

2. Implementation of 7th pay commission

3. Easing of policy rates

4. Pipeline of elections in the states of UP & Punjab in FY17, Gujarat in FY18, and

MP & Rajasthan elections expected in FY19

Newsprint costs may increase by 5-6% but not more: With declining demand of

newsprint from publishing companies in the West, we see a structural reason why

newsprint cost may not see its previous highs. Even if it rises, there are various tools in

the hands of publishing companies like reducing the pagination, using paper of lower

grammage, reducing subscription discounts, using more of domestic paper, increasing ad-

edit ratio, through which they can manage the costs. Higher growth in advertising

revenues will provide positive leverage which will support the margins.

Differentiating factors: Our comparative analysis of the business segments across

companies suggests that in Print segment: DB Corp is our marginal favourite over Jagran.

Radio segment: With the acquisition of Radio city, Jagran has leaped ahead of peers.

Digital segment: HT Media with much higher investments in the digital space is ahead of

the pack in our view.

Initiating coverage on print media sector with Long rating on DB Corp, Jagran

Prakashan, HMVL and trade rating on HT Media. DB Corp (on the back of dominant

position and strong election pipeline) and HMVL (most attractively valued) are our top

picks in the sector.

Company Rating Mkt cap (Rs

mn)

Current Price

(Rs)

Target Price

(Rs) Upside(%)

P/E

(FY18e)

EV/EBITDA

(FY18e)

P/B

(FY18e)

EBITDA CAGR

(FY16-19e)

RoE

(FY18e)

Core RoIC

(FY18e)

Div.Yield(%)

(FY18e)

FCF Yield(%)

(FY18e)

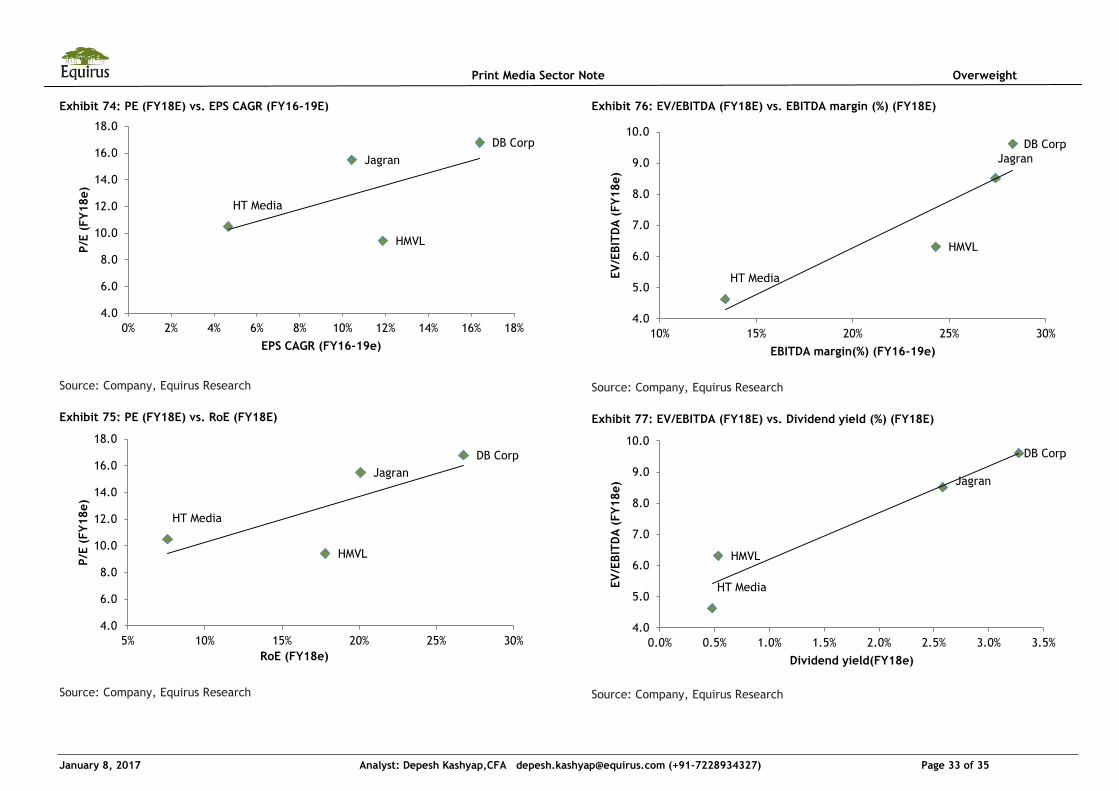

DB Corp Long 68,614 373 450 21% 16.8 9.6 4.3 14% 27% 28% 3.3% 6.1%

Jagran Long 57,340 175 220 25% 15.5 8.5 3.0 9% 20% 20% 2.6% 7.6%

HMVL Long 20,066 273 370 35% 9.4 6.3 1.5 11% 18% 46% 0.5% 7.4%

HTML Trade 17,596 76 80 6% 10.5 4.6 0.8 9% 8% 12% 0.5% 14.2%

Source: Equirus Research

Page 2

Print media Sector Note Overweight

January 8, 2017 Analyst: Depesh Kashyap,CFA [email protected] (+91-7228934327) Page 2 of 35

Contents

Structural downturn argument poses no immediate concerns ........................... 4

Threat of Digital: How are we placed vs. Developed world? ................................ 4 What led to decline of newspapers in developed world?: US Case study ....... 4 Why Indian print sector is different from the developed world? ..................... 6

Print media in India is still emerging ....................................................................... 8

Mind the language: Regional to outperform English on the back of large

untapped rural population .......................................................................................... 9

Future ready: Diversifying business ........................................................................ 12 Expanding the digital bouquet ............................................................................. 12 Emergence of radio as “Reach” platform .......................................................... 13

Question that matters: “Where are we in the cycle”? .......................................15

Business economics: How do newspapers make money? ...................................... 15

Print advertisement cycle: Remains favourable? ................................................. 17

Newsprint cycle: Rising costs a concern… .............................................................. 21

…but margins may not have much effect ............................................................... 22 1. Decreasing demand from the global publishing companies: ................. 22 2. Few tools in the hands of newspaper companies .................................... 23 3. Case of positive operating leverage .......................................................... 24

Differentiating factors: A bare comparison ...........................................................24

Dainik Bhaskar has the most diversified print business ................................... 25 Jagran clearly leads the pack with its Radio business ..................................... 27 HT media is way ahead with its Digital strategy .............................................. 29

Valuation: EV/EBITDA is our preferred methodology ..........................................31

Valuation summary ..................................................................................................... 31

Demonetisation: Curious case of 3QFY17 .............................................................34

Company Sections DB Corp: Diversified play on India’s print story....................................36

Jagran Prakashan: Tuning in to the right frequency................................50

HMVL: Watch out for ’Money in the Bank’...........................................64

HT Media: Still time before it Shines.................................................77

Page 3

Print media Sector Note Overweight

January 8, 2017 Analyst: Depesh Kashyap,CFA [email protected] (+91-7228934327) Page 3 of 35

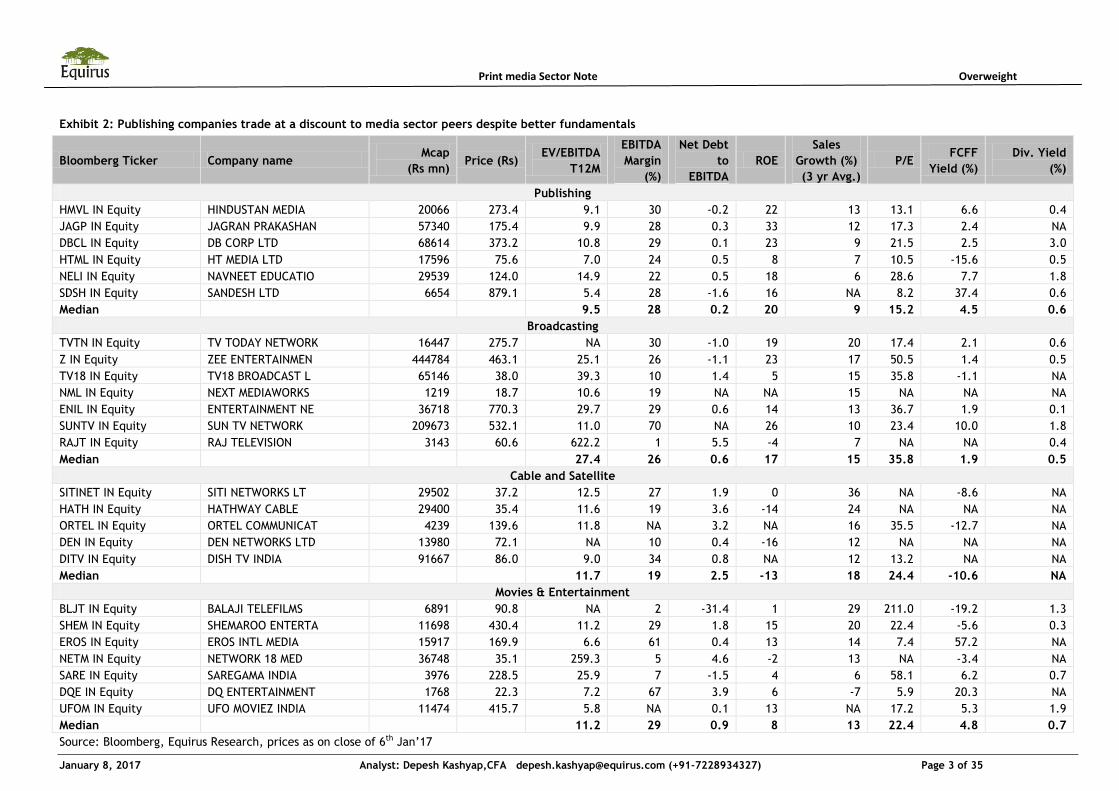

Exhibit 2: Publishing companies trade at a discount to media sector peers despite better fundamentals

Bloomberg Ticker Company name Mcap

(Rs mn) Price (Rs)

EV/EBITDA

T12M

EBITDA

Margin

(%)

Net Debt

to

EBITDA

ROE

Sales

Growth (%)

(3 yr Avg.)

P/E FCFF

Yield (%)

Div. Yield

(%)

Publishing

HMVL IN Equity HINDUSTAN MEDIA 20066 273.4 9.1 30 -0.2 22 13 13.1 6.6 0.4

JAGP IN Equity JAGRAN PRAKASHAN 57340 175.4 9.9 28 0.3 33 12 17.3 2.4 NA

DBCL IN Equity DB CORP LTD 68614 373.2 10.8 29 0.1 23 9 21.5 2.5 3.0

HTML IN Equity HT MEDIA LTD 17596 75.6 7.0 24 0.5 8 7 10.5 -15.6 0.5

NELI IN Equity NAVNEET EDUCATIO 29539 124.0 14.9 22 0.5 18 6 28.6 7.7 1.8

SDSH IN Equity SANDESH LTD 6654 879.1 5.4 28 -1.6 16 NA 8.2 37.4 0.6

Median

9.5 28 0.2 20 9 15.2 4.5 0.6

Broadcasting

TVTN IN Equity TV TODAY NETWORK 16447 275.7 NA 30 -1.0 19 20 17.4 2.1 0.6

Z IN Equity ZEE ENTERTAINMEN 444784 463.1 25.1 26 -1.1 23 17 50.5 1.4 0.5

TV18 IN Equity TV18 BROADCAST L 65146 38.0 39.3 10 1.4 5 15 35.8 -1.1 NA

NML IN Equity NEXT MEDIAWORKS 1219 18.7 10.6 19 NA NA 15 NA NA NA

ENIL IN Equity ENTERTAINMENT NE 36718 770.3 29.7 29 0.6 14 13 36.7 1.9 0.1

SUNTV IN Equity SUN TV NETWORK 209673 532.1 11.0 70 NA 26 10 23.4 10.0 1.8

RAJT IN Equity RAJ TELEVISION 3143 60.6 622.2 1 5.5 -4 7 NA NA 0.4

Median

27.4 26 0.6 17 15 35.8 1.9 0.5

Cable and Satellite

SITINET IN Equity SITI NETWORKS LT 29502 37.2 12.5 27 1.9 0 36 NA -8.6 NA

HATH IN Equity HATHWAY CABLE 29400 35.4 11.6 19 3.6 -14 24 NA NA NA

ORTEL IN Equity ORTEL COMMUNICAT 4239 139.6 11.8 NA 3.2 NA 16 35.5 -12.7 NA

DEN IN Equity DEN NETWORKS LTD 13980 72.1 NA 10 0.4 -16 12 NA NA NA

DITV IN Equity DISH TV INDIA 91667 86.0 9.0 34 0.8 NA 12 13.2 NA NA

Median

11.7 19 2.5 -13 18 24.4 -10.6 NA

Movies & Entertainment

BLJT IN Equity BALAJI TELEFILMS 6891 90.8 NA 2 -31.4 1 29 211.0 -19.2 1.3

SHEM IN Equity SHEMAROO ENTERTA 11698 430.4 11.2 29 1.8 15 20 22.4 -5.6 0.3

EROS IN Equity EROS INTL MEDIA 15917 169.9 6.6 61 0.4 13 14 7.4 57.2 NA

NETM IN Equity NETWORK 18 MED 36748 35.1 259.3 5 4.6 -2 13 NA -3.4 NA

SARE IN Equity SAREGAMA INDIA 3976 228.5 25.9 7 -1.5 4 6 58.1 6.2 0.7

DQE IN Equity DQ ENTERTAINMENT 1768 22.3 7.2 67 3.9 6 -7 5.9 20.3 NA

UFOM IN Equity UFO MOVIEZ INDIA 11474 415.7 5.8 NA 0.1 13 NA 17.2 5.3 1.9

Median

11.2 29 0.9 8 13 22.4 4.8 0.7

Source: Bloomberg, Equirus Research, prices as on close of 6th Jan’17

Page 4

Print media Sector Note Overweight

January 8, 2017 Analyst: Depesh Kashyap,CFA [email protected] (+91-7228934327) Page 4 of 35

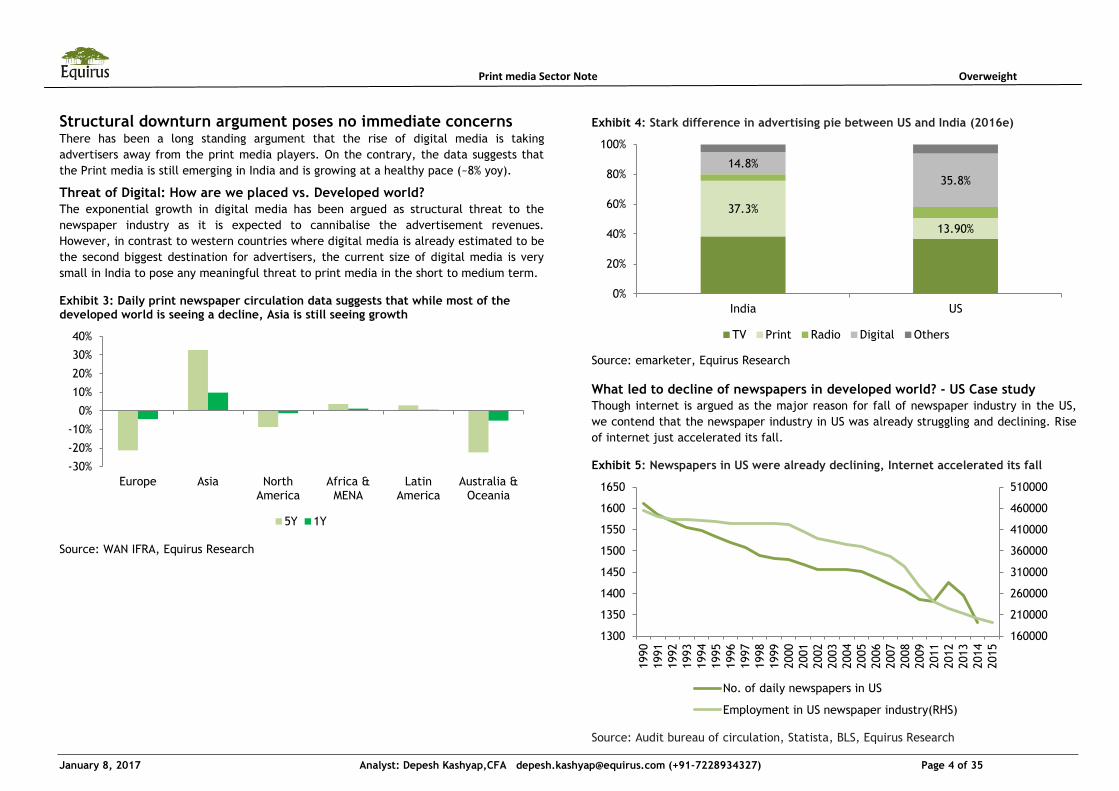

Structural downturn argument poses no immediate concerns There has been a long standing argument that the rise of digital media is taking

advertisers away from the print media players. On the contrary, the data suggests that

the Print media is still emerging in India and is growing at a healthy pace (~8% yoy).

Threat of Digital: How are we placed vs. Developed world?

The exponential growth in digital media has been argued as structural threat to the

newspaper industry as it is expected to cannibalise the advertisement revenues.

However, in contrast to western countries where digital media is already estimated to be

the second biggest destination for advertisers, the current size of digital media is very

small in India to pose any meaningful threat to print media in the short to medium term. Exhibit 3: Daily print newspaper circulation data suggests that while most of the developed world is seeing a decline, Asia is still seeing growth

Source: WAN IFRA, Equirus Research

Exhibit 4: Stark difference in advertising pie between US and India (2016e)

Source: emarketer, Equirus Research

What led to decline of newspapers in developed world? - US Case study

Though internet is argued as the major reason for fall of newspaper industry in the US,

we contend that the newspaper industry in US was already struggling and declining. Rise

of internet just accelerated its fall. Exhibit 5: Newspapers in US were already declining, Internet accelerated its fall

Source: Audit bureau of circulation, Statista, BLS, Equirus Research

-30%

-20%

-10%

0%

10%

20%

30%

40%

Europe Asia North America

Africa & MENA

Latin America

Australia & Oceania

5Y 1Y

37.3%

13.90%

14.8%

35.8%

0%

20%

40%

60%

80%

100%

India US

TV Print Radio Digital Others

160000

210000

260000

310000

360000

410000

460000

510000

1300

1350

1400

1450

1500

1550

1600

1650

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2011

2012

2013

2014

2015

No. of daily newspapers in US

Employment in US newspaper industry(RHS)

Page 5

Print Media Sector Note Overweight

January 8, 2017 Analyst: Depesh Kashyap,CFA [email protected] (+91-7228934327) Page 5 of 35

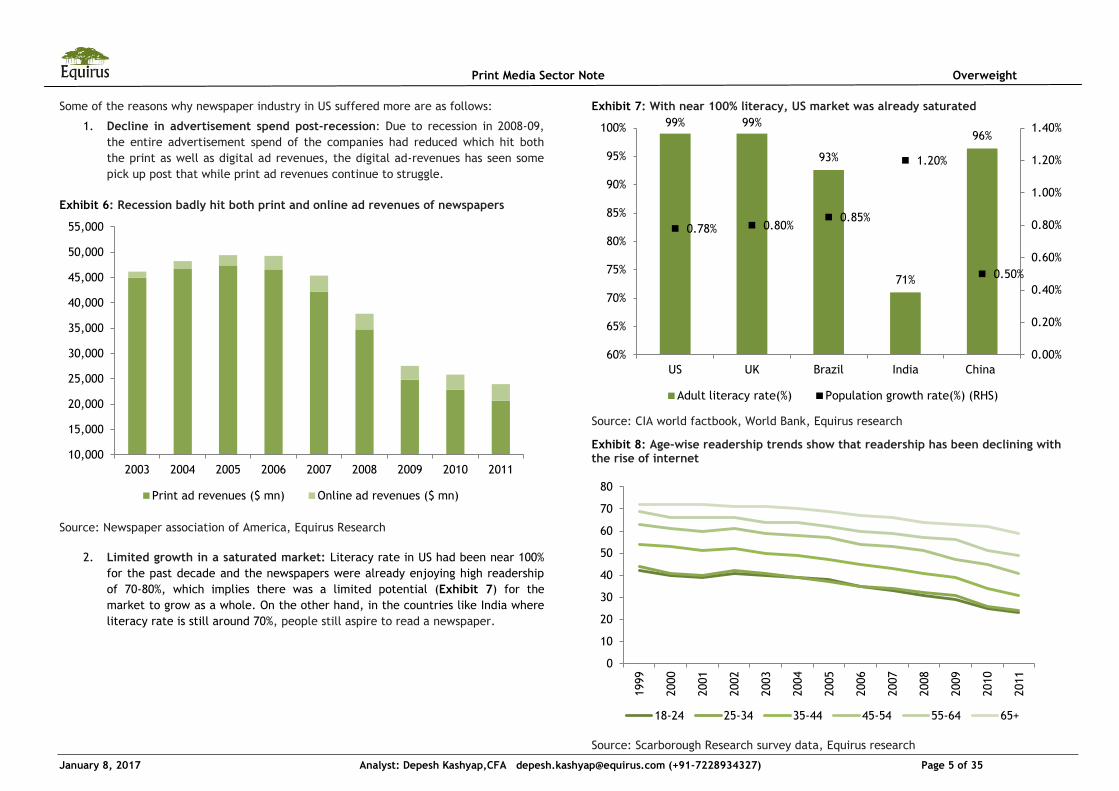

Some of the reasons why newspaper industry in US suffered more are as follows:

1. Decline in advertisement spend post-recession: Due to recession in 2008-09,

the entire advertisement spend of the companies had reduced which hit both

the print as well as digital ad revenues, the digital ad-revenues has seen some

pick up post that while print ad revenues continue to struggle.

Exhibit 6: Recession badly hit both print and online ad revenues of newspapers

Source: Newspaper association of America, Equirus Research

2. Limited growth in a saturated market: Literacy rate in US had been near 100%

for the past decade and the newspapers were already enjoying high readership

of 70-80%, which implies there was a limited potential (Exhibit 7) for the

market to grow as a whole. On the other hand, in the countries like India where

literacy rate is still around 70%, people still aspire to read a newspaper.

Exhibit 7: With near 100% literacy, US market was already saturated

Source: CIA world factbook, World Bank, Equirus research

Exhibit 8: Age-wise readership trends show that readership has been declining with the rise of internet

Source: Scarborough Research survey data, Equirus research

10,000

15,000

20,000

25,000

30,000

35,000

40,000

45,000

50,000

55,000

2003 2004 2005 2006 2007 2008 2009 2010 2011

Print ad revenues ($ mn) Online ad revenues ($ mn)

99% 99%

93%

71%

96%

0.78% 0.80% 0.85%

1.20%

0.50%

0.00%

0.20%

0.40%

0.60%

0.80%

1.00%

1.20%

1.40%

60%

65%

70%

75%

80%

85%

90%

95%

100%

US UK Brazil India China

Adult literacy rate(%) Population growth rate(%) (RHS)

0

10

20

30

40

50

60

70

80

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

18-24 25-34 35-44 45-54 55-64 65+

Page 6

Print Media Sector Note Overweight

January 8, 2017 Analyst: Depesh Kashyap,CFA [email protected] (+91-7228934327) Page 6 of 35

3. High dependence on classified revenues: Revenues from classified

advertisements contributed nearly 40% to the total revenues of the newspaper

company, with main contributions from recruitment, real estate and auto

advertisements. With the rise of free classified sites like Craigslist.org,

Realtor.com, Monster.com etc all these advertisements shifted to various

job/housing portals which led to significant decline in revenues (see Exhibit 9).

Exhibit 9: Internet hurt classified revenues the most

Source: Newspaper association of America, Equirus Research

4. Limited number of large national players: Of the large number of US dailies,

there are only 3 major newspapers (The Wall Street Journal, The New York

Times and USA Today) which circulate at national level. Most of the other

newspapers serve local communities and generally have monopoly in their

localities. So, this was the main reason, why various newspapers were not able

to grow their circulation levels beyond a certain level and were heavily

dependent on the advertisement revenues.

Why Indian print sector is different from the developed world?

The major reason for difference in India and other western countries is low internet

penetration in India (see Exhibit 10). Exhibit 10: Internet penetration is very low in India as compared to rest of the world

Source: FICCI KPMG, Equirus Research

Though internet penetration is increasing rapidly, there are few structural factors which

give us confidence that digital media will not be able to disrupt Indian print media in the

medium term:

i) Classified ads have a very small share: Before the digital era, Classified

ads used to constitute 40% of total ad revenues in US which has depleted to

18% as most of the classified ads have shifted to digital media. In India,

however, classified ads constitute only 7-8% of total ad revenue, so even if

that shifts to digital, the impact will not be big. The diversion of the

revenues in India started with the job market when a lot of jobs classified

had moved to digital medium like Naukri.com, Shine.com etc. Housing and

matrimonial ads are also getting threatened by the new housing/matrimony

portals.

ii) Cost advantage: Newspapers in India are priced very low, which make them

very affordable. They cost no more than Rs. 200 per month (roughly USD 3)

which is close to the cost of a single newspaper per day in the US.

0.0

5.0

10.0

15.0

20.0

25.0

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

Total classified ad revenues ( $bn) Auto classifieds($bn)

Real estate classifieds ($bn) Recruitment classifieds ($bn)

Other classifieds ($ bn)

90% 87% 86%

60% 53%

46%

27%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

UK US Japan Russia Brazil China India

Internet penetration

Page 7

Print Media Sector Note Overweight

January 8, 2017 Analyst: Depesh Kashyap,CFA [email protected] (+91-7228934327) Page 7 of 35

Exhibit 11: Cover prices in India are very affordable as compared to other countries

Source: FICCI-KPMG, Equirus Research

iii) Easy availability: Most of the newspapers in India are delivered to

customer’s home every morning, which makes it very accessible whereas in

the West, people generally buy newspapers from the stands or the metro

stations.

iv) Readership habits of the people: Most of the people start their day reading

a newspaper (see Exhibit 12: Indians start their day by reading a

newspaperExhibit 12); it has become a habit which is not easy to break.

While the youth in a household might have shifted to digital media, but the

members aged 35 years and above still prefer a physical copy.

Exhibit 12: Indians start their day by reading a newspaper

Source: FICCI KPMG report, Equirus Research

v) Just like TV, Digital media may end up complementing Print: Few years

back, most of the people argued that TV will take away the revenues from

Print media, but in hindsight, TV news channels, especially in regional

languages, have had a positive impact on newspaper circulation, as people

often turn to newspapers for elaborate analysis of the facts they see on TV.

In a similar manner, we digital news websites may end up complementing

newspapers.

It remains to be seen how the future pans out but one thing is certain that due to low

internet penetration, unlike the West, the disruption of print media will not be a near

term event. In the following section, we will see how the existing players in the print

media are already making huge investments to build a strong online presence and are

getting ready for the future.

2-3

4-6

18-20

22-24 23-25

0

5

10

15

20

25

30

India Pakistan Malaysia Hong Kong Singapore

Average monthly cover price ( in USD)

0%

2%

4%

6%

8%

10%

12%

14%

16%

6am

to 7

am

7am

to 8

am

8am

to 9

am

9am

to 1

0am

10am

to 1

1am

11am

to 1

2pm

12pm

to 1

pm

1pm

to 2

pm

2pm

to 3

pm

3pm

to 4

pm

4pm

to 5

pm

5pm

to 6

pm

6pm

to 7

pm

7pm

to 8

pm

Avg. consumption of newspaper by hour (%)

Page 8

Print Media Sector Note Overweight

January 8, 2017 Analyst: Depesh Kashyap,CFA [email protected] (+91-7228934327) Page 8 of 35

Print media in India is still emerging

The total media and entertainment industry in India has grown at a CAGR 12% in the last

5 years, and according to FICCI estimates, the industry as a whole is expected to grow at

CAGR 14% for the next 5 years. Exhibit 14 suggests that the media spend as % of GDP is

one of the lowest in India at 0.3%, so there remains a huge potential to grow in the long

term. The gap between ‘can read’ and ‘do read’ categories in the regional markets also

remain supportive of the growth of newspapers.

Exhibit 13: Indian M&E industry has grown at a CAGR of 12% in the last 5 years and is expected to grow at faster pace in the next 5 years

Source: FICCI-KPMG report 2016, Equirus Research

Exhibit 14: Media spend in India has a huge upside potential

Source: Group M estimates, Equirus Research

Exhibit 15: Number of registered newspapers and periodicals (‘000s) are still rising

Source: The registrar of newspaper in India, Equirus Research

As Exhibit 16 depicts, print media is still the largest component of advertising as a % of

overall ad pie at 40%. According to FICCI-KPMG estimates, print media is likely to lose its

leadership position to TV in the next 5 years and closely followed by the Digital media.

We argue that digital media is most likely to disrupt the English print space the most

while the regional print is likely to see strong growth in the years to come. We discuss

this in detail in the following section.

Exhibit 16: Print media still has the largest share in the advertising pie

Rs. bn 2012 2013 2014 2015 2016e 2017e 2018e 2019e 2020e CAGR(12-

15)

CAGR(15-

20e)

TV 125 136 155 181 210 242 276 320 365 13.3% 15.0%

Print 150 163 176 189 204 222 242 263 286 8.2% 8.6%

Radio 13 15 17 20 23 28 33 38 43 16.0% 16.9%

OOH 18 19 22 24 28 32 35 40 45 10.3% 13.1%

Digital 22 30 44 60 81 114 153 199 255 40.4% 33.5%

Total 327 363 414 475 547 637 739 860 994 13.2% 15.9%

Source: FICCI-KPMG report 2016, Equirus Research

652 728 821 918

1026 1157

2228

0

500

1000

1500

2000

2500

2010 2011 2012 2013 2014 2015 2020p

M&E industry size ( Rs bn)

0.33%

0.85%

0.97%

0.76% 0.86%

0.76%

0.00%

0.20%

0.40%

0.60%

0.80%

1.00%

1.20%

India UK US China Japan World

Media spend as % of GDP

2%

3%

4%

5%

6%

7%

8%

9%

0

20

40

60

80

100

120

2005 2006 2007 2010 2011 2012 2013 2014

Dailies Periodicals YoY growth (%) (RHS)

Page 9

Print Media Sector Note Overweight

January 8, 2017 Analyst: Depesh Kashyap,CFA [email protected] (+91-7228934327) Page 9 of 35

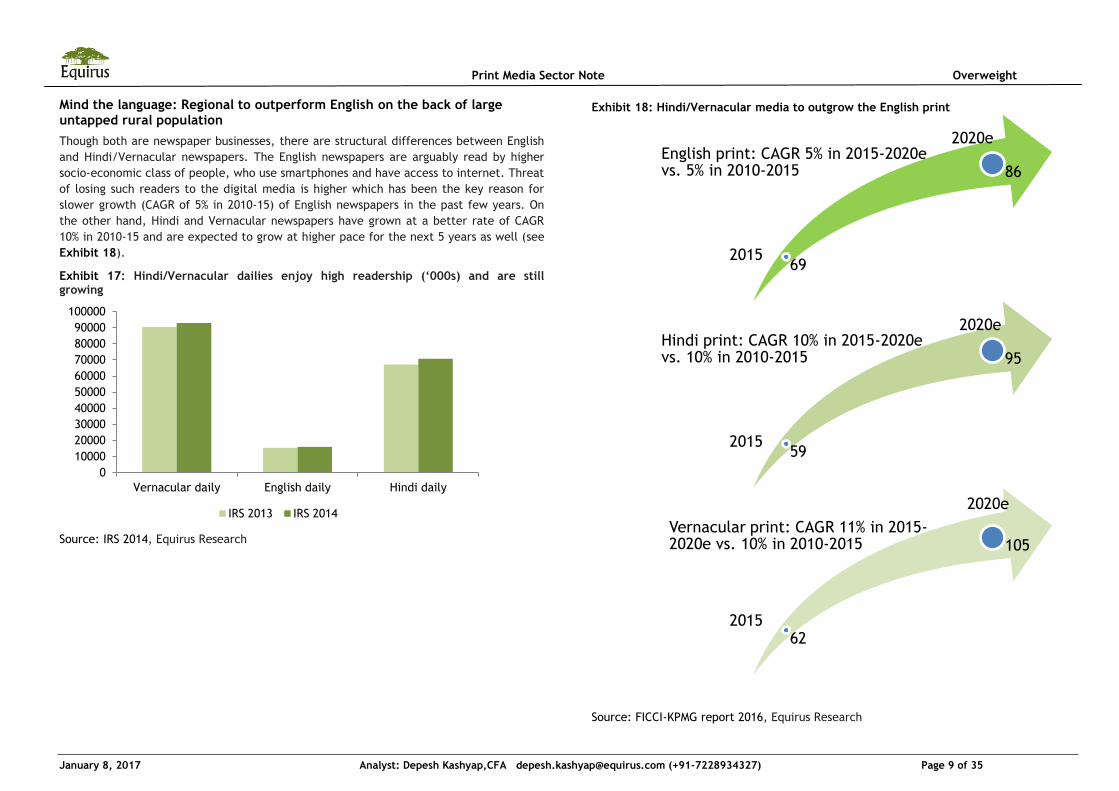

Mind the language: Regional to outperform English on the back of large untapped rural population

Though both are newspaper businesses, there are structural differences between English

and Hindi/Vernacular newspapers. The English newspapers are arguably read by higher

socio-economic class of people, who use smartphones and have access to internet. Threat

of losing such readers to the digital media is higher which has been the key reason for

slower growth (CAGR of 5% in 2010-15) of English newspapers in the past few years. On

the other hand, Hindi and Vernacular newspapers have grown at a better rate of CAGR

10% in 2010-15 and are expected to grow at higher pace for the next 5 years as well (see

Exhibit 18).

Exhibit 17: Hindi/Vernacular dailies enjoy high readership (‘000s) and are still growing

Source: IRS 2014, Equirus Research

Exhibit 18: Hindi/Vernacular media to outgrow the English print

Source: FICCI-KPMG report 2016, Equirus Research

0

10000

20000

30000

40000

50000

60000

70000

80000

90000

100000

Vernacular daily English daily Hindi daily

IRS 2013 IRS 2014

69 2015

English print: CAGR 5% in 2015-2020e vs. 5% in 2010-2015

2020e

86

59 2015

Hindi print: CAGR 10% in 2015-2020e vs. 10% in 2010-2015

2020e

95

62 2015

Vernacular print: CAGR 11% in 2015-2020e vs. 10% in 2010-2015

2020e

105

Page 10

Print Media Sector Note Overweight

January 8, 2017 Analyst: Depesh Kashyap,CFA [email protected] (+91-7228934327) Page 10 of 35

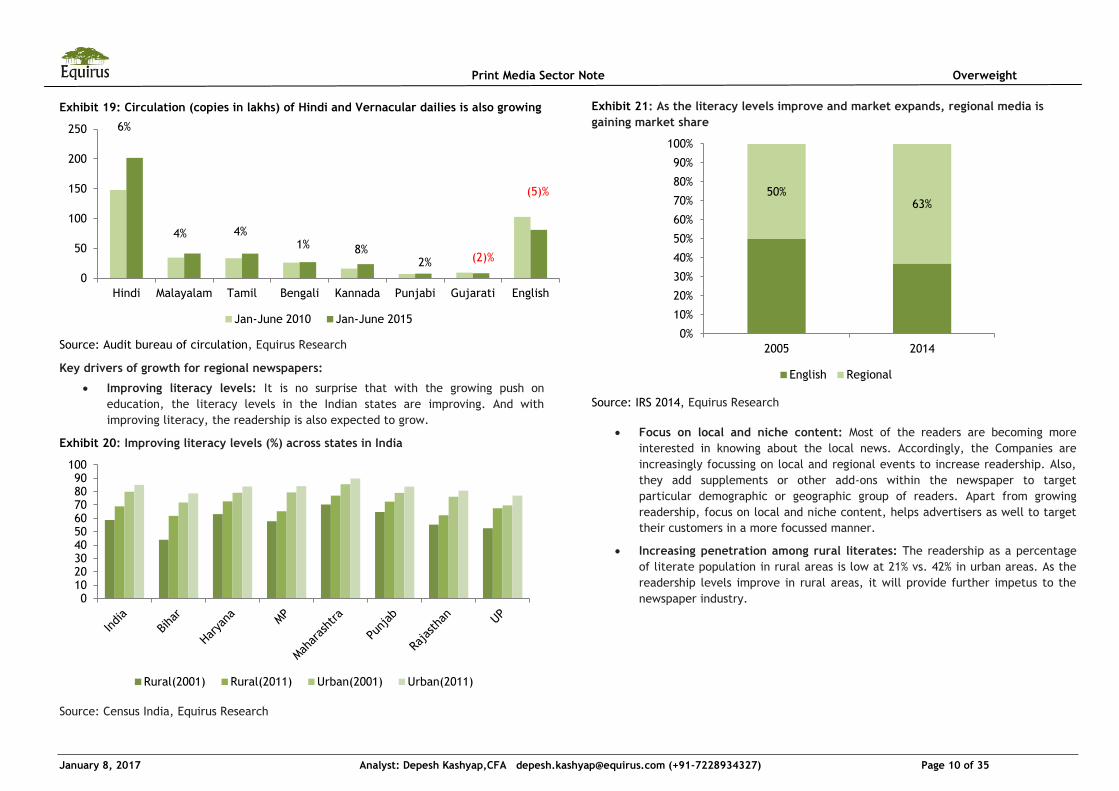

Exhibit 19: Circulation (copies in lakhs) of Hindi and Vernacular dailies is also growing

Source: Audit bureau of circulation, Equirus Research

Key drivers of growth for regional newspapers:

Improving literacy levels: It is no surprise that with the growing push on

education, the literacy levels in the Indian states are improving. And with

improving literacy, the readership is also expected to grow.

Exhibit 20: Improving literacy levels (%) across states in India

Source: Census India, Equirus Research

Exhibit 21: As the literacy levels improve and market expands, regional media is

gaining market share

Source: IRS 2014, Equirus Research

Focus on local and niche content: Most of the readers are becoming more

interested in knowing about the local news. Accordingly, the Companies are

increasingly focussing on local and regional events to increase readership. Also,

they add supplements or other add-ons within the newspaper to target

particular demographic or geographic group of readers. Apart from growing

readership, focus on local and niche content, helps advertisers as well to target

their customers in a more focussed manner.

Increasing penetration among rural literates: The readership as a percentage

of literate population in rural areas is low at 21% vs. 42% in urban areas. As the

readership levels improve in rural areas, it will provide further impetus to the

newspaper industry.

0

50

100

150

200

250

Hindi Malayalam Tamil Bengali Kannada Punjabi Gujarati English

Jan-June 2010 Jan-June 2015

6%

4%

4% 1%

8% 2%

(2)%

(5)%

0 10 20 30 40 50 60 70 80 90

100

Rural(2001) Rural(2011) Urban(2001) Urban(2011)

50% 63%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2005 2014

English Regional

Page 11

Print Media Sector Note Overweight

January 8, 2017 Analyst: Depesh Kashyap,CFA [email protected] (+91-7228934327) Page 11 of 35

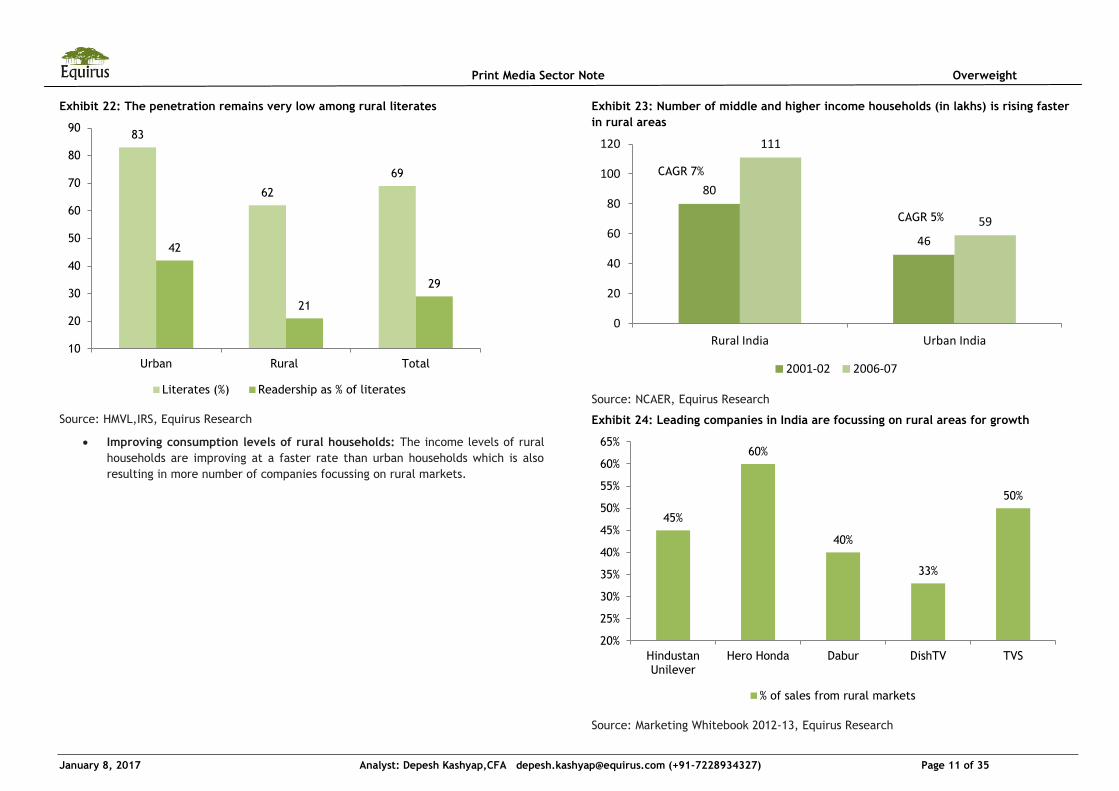

Exhibit 22: The penetration remains very low among rural literates

Source: HMVL,IRS, Equirus Research

Improving consumption levels of rural households: The income levels of rural

households are improving at a faster rate than urban households which is also

resulting in more number of companies focussing on rural markets.

Exhibit 23: Number of middle and higher income households (in lakhs) is rising faster

in rural areas

Source: NCAER, Equirus Research

Exhibit 24: Leading companies in India are focussing on rural areas for growth

Source: Marketing Whitebook 2012-13, Equirus Research

83

62

69

42

21

29

10

20

30

40

50

60

70

80

90

Urban Rural Total

Literates (%) Readership as % of literates

80

46

111

59

0

20

40

60

80

100

120

Rural India Urban India

2001-02 2006-07

CAGR 7%

CAGR 5%

45%

60%

40%

33%

50%

20%

25%

30%

35%

40%

45%

50%

55%

60%

65%

Hindustan Unilever

Hero Honda Dabur DishTV TVS

% of sales from rural markets

Page 12

Print Media Sector Note Overweight

January 8, 2017 Analyst: Depesh Kashyap,CFA [email protected] (+91-7228934327) Page 12 of 35

Future ready: Diversifying business

Being fully aware of the trends of the newspaper industry in the West, the Indian print

companies have been investing proactively and aggressively in the digital media and

already have a significant presence in online space. Though digital business models of the

companies are still evolving and the primary focus of the companies is mainly on

leveraging their brands in the online world. The companies are focussed on maximising

page views and unique visitors on their websites. Though the base remains very small but

all companies have seen exponential growth in the digital space in the last few years and

the trend is estimated to remain strong.

Exhibit 25: Digital advertisement revenues expected to grow at a CAGR (2015-20E) of 34%

Source: FICCI-KPMG, Equirus Research

Expanding the digital bouquet

Most of the Companies have been leveraging their brand in the print space to expand

their digital portfolio. Almost all the Companies have established their news websites,

and have also ventured into job, housing and education portals. Exhibit 28 lists websites

of various Companies in the sector. Though the total contribution of the digital segment

in the overall revenues of the Companies remains very low but it’s a high growth segment

and all the Companies are investing heavily in it.

Exhibit 26: High local language users in India will help in faster expansion of

Vernacular print companies

Source: FICCI-KPMG, Equirus Research

Exhibit 27: Digital revenue comparison of the Companies

Source: Company, Equirus Research

0

50

100

150

200

250

300

2012 2013 2014 2015 2016e 2017e 2018e 2019e 2020e

Digital advertisement revenues( Rs bn)

CAGR(2011-15) 41%

CAGR(2015-20E) 34%

47%

43%

57%

0%

10%

20%

30%

40%

50%

60%

0

50

100

150

200

250

300

All India Urban India Rural India

Internet users Local language users

460

213

1403 65%

38%

2% 1% 6%

0%

10%

20%

30%

40%

50%

60%

70%

0

200

400

600

800

1000

1200

1400

1600

DB Corp Ltd Jagran HT Media

Revenues from Digital (FY16) ( Rs mn)

Revenue CAGR(FY13-16) (RHS)

Digital as % of total revenues (FY16) (RHS)

Page 13

Print Media Sector Note Overweight

January 8, 2017 Analyst: Depesh Kashyap,CFA [email protected] (+91-7228934327) Page 13 of 35

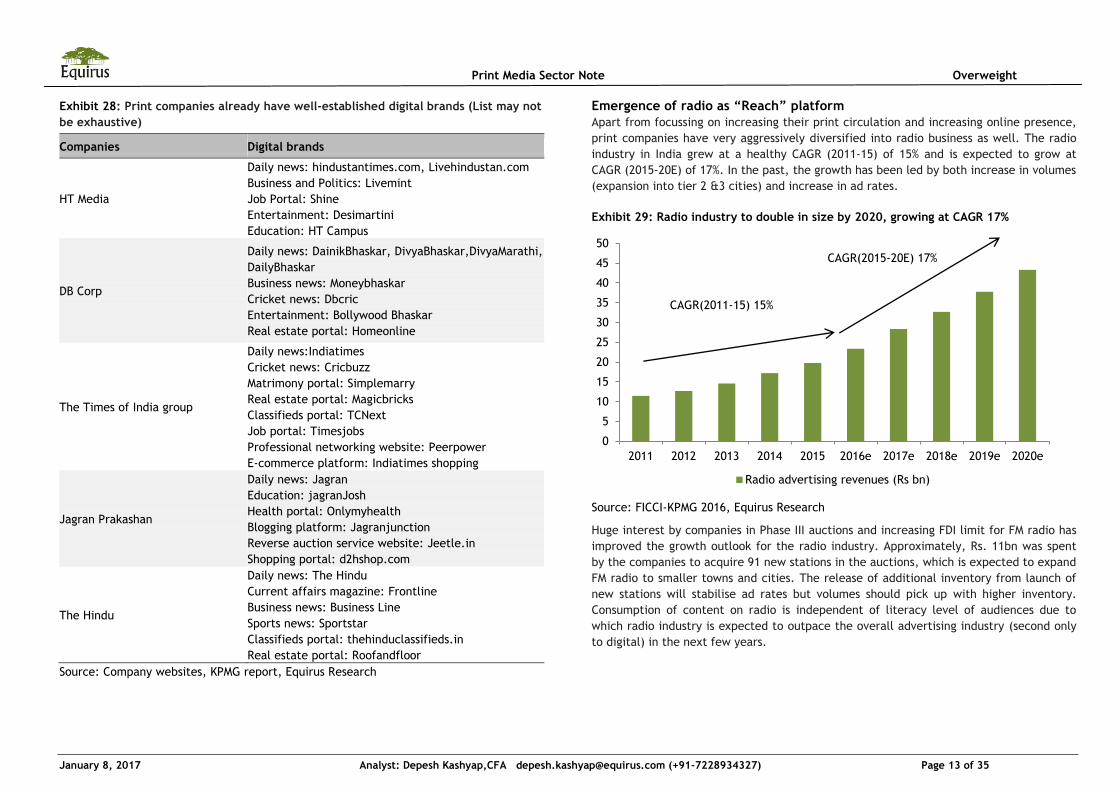

Exhibit 28: Print companies already have well-established digital brands (List may not

be exhaustive)

Companies Digital brands

HT Media

Daily news: hindustantimes.com, Livehindustan.com

Business and Politics: Livemint

Job Portal: Shine

Entertainment: Desimartini

Education: HT Campus

DB Corp

Daily news: DainikBhaskar, DivyaBhaskar,DivyaMarathi,

DailyBhaskar

Business news: Moneybhaskar

Cricket news: Dbcric

Entertainment: Bollywood Bhaskar

Real estate portal: Homeonline

The Times of India group

Daily news:Indiatimes

Cricket news: Cricbuzz

Matrimony portal: Simplemarry

Real estate portal: Magicbricks

Classifieds portal: TCNext

Job portal: Timesjobs

Professional networking website: Peerpower

E-commerce platform: Indiatimes shopping

Jagran Prakashan

Daily news: Jagran

Education: jagranJosh

Health portal: Onlymyhealth

Blogging platform: Jagranjunction

Reverse auction service website: Jeetle.in

Shopping portal: d2hshop.com

The Hindu

Daily news: The Hindu

Current affairs magazine: Frontline

Business news: Business Line

Sports news: Sportstar

Classifieds portal: thehinduclassifieds.in

Real estate portal: Roofandfloor

Source: Company websites, KPMG report, Equirus Research

Emergence of radio as “Reach” platform

Apart from focussing on increasing their print circulation and increasing online presence,

print companies have very aggressively diversified into radio business as well. The radio

industry in India grew at a healthy CAGR (2011-15) of 15% and is expected to grow at

CAGR (2015-20E) of 17%. In the past, the growth has been led by both increase in volumes

(expansion into tier 2 &3 cities) and increase in ad rates.

Exhibit 29: Radio industry to double in size by 2020, growing at CAGR 17%

Source: FICCI-KPMG 2016, Equirus Research

Huge interest by companies in Phase III auctions and increasing FDI limit for FM radio has

improved the growth outlook for the radio industry. Approximately, Rs. 11bn was spent

by the companies to acquire 91 new stations in the auctions, which is expected to expand

FM radio to smaller towns and cities. The release of additional inventory from launch of

new stations will stabilise ad rates but volumes should pick up with higher inventory.

Consumption of content on radio is independent of literacy level of audiences due to

which radio industry is expected to outpace the overall advertising industry (second only

to digital) in the next few years.

0

5

10

15

20

25

30

35

40

45

50

2011 2012 2013 2014 2015 2016e 2017e 2018e 2019e 2020e

Radio advertising revenues (Rs bn)

CAGR(2011-15) 15%

CAGR(2015-20E) 17%

Page 14

Print Media Sector Note Overweight

January 8, 2017 Analyst: Depesh Kashyap,CFA [email protected] (+91-7228934327) Page 14 of 35

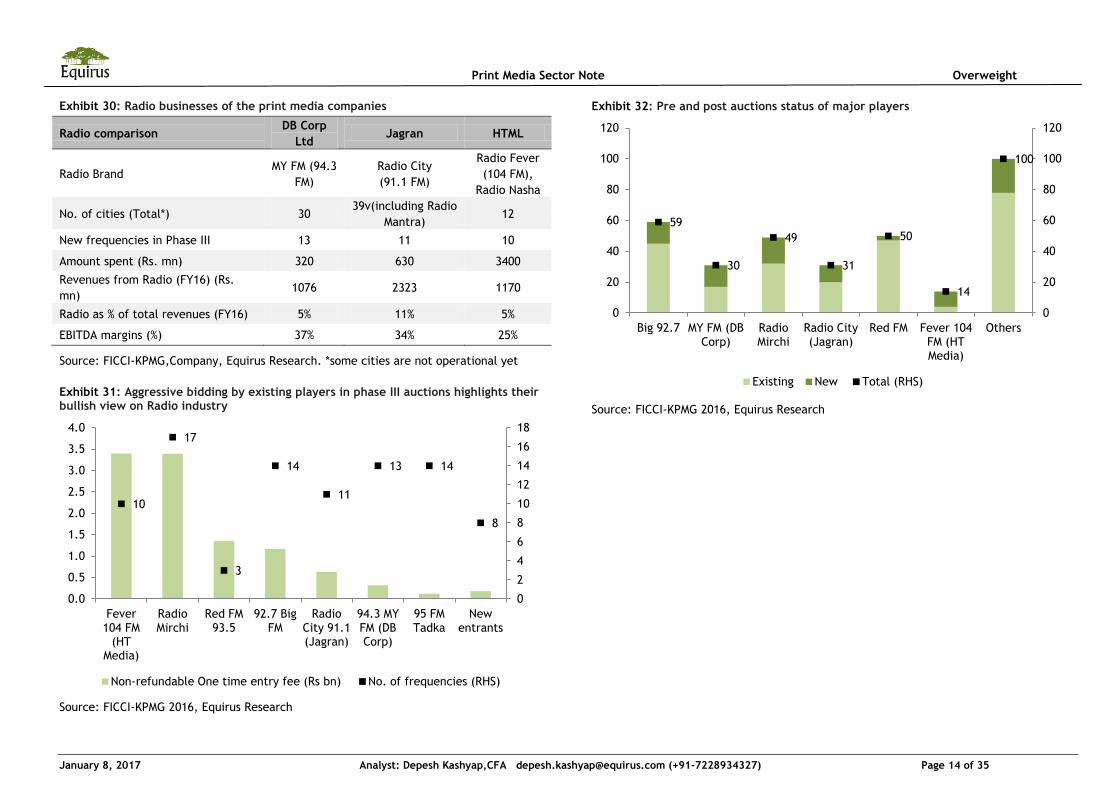

Exhibit 30: Radio businesses of the print media companies

Radio comparison DB Corp

Ltd Jagran HTML

Radio Brand MY FM (94.3

FM)

Radio City

(91.1 FM)

Radio Fever

(104 FM),

Radio Nasha

No. of cities (Total*) 30 39v(including Radio

Mantra) 12

New frequencies in Phase III 13 11 10

Amount spent (Rs. mn) 320 630 3400

Revenues from Radio (FY16) (Rs.

mn) 1076 2323 1170

Radio as % of total revenues (FY16) 5% 11% 5%

EBITDA margins (%) 37% 34% 25%

Source: FICCI-KPMG,Company, Equirus Research. *some cities are not operational yet

Exhibit 31: Aggressive bidding by existing players in phase III auctions highlights their bullish view on Radio industry

Source: FICCI-KPMG 2016, Equirus Research

Exhibit 32: Pre and post auctions status of major players

Source: FICCI-KPMG 2016, Equirus Research

10

17

3

14

11

13 14

8

0

2

4

6

8

10

12

14

16

18

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

Fever 104 FM

(HT Media)

Radio Mirchi

Red FM 93.5

92.7 Big FM

Radio City 91.1 (Jagran)

94.3 MY FM (DB Corp)

95 FM Tadka

New entrants

Non-refundable One time entry fee (Rs bn) No. of frequencies (RHS)

59

30

49

31

50

14

100

0

20

40

60

80

100

120

0

20

40

60

80

100

120

Big 92.7 MY FM (DB Corp)

Radio Mirchi

Radio City (Jagran)

Red FM Fever 104 FM (HT Media)

Others

Existing New Total (RHS)

Page 15

Print Media Sector Note Overweight

January 8, 2017 Analyst: Depesh Kashyap,CFA [email protected] (+91-7228934327) Page 15 of 35

Question that matters: “Where are we in the cycle”?

On the revenue side, newspaper industry is highly dependent on the advertising revenues

and on the cost side it is mainly dependent on the newsprint prices. Both components

depend on various macro variables and hence earnings of the newspaper business are

highly cyclical. We briefly discuss the business economics of the newspaper industry to

understand these variables in a better way.

Business economics: How do newspapers make money?

Newspaper publishers mainly have 2 sources of revenue:

a) Circulation revenues (sale of newspapers) which is mainly a function of i) total

newspaper circulation (Volumes) and

ii) Average realisation per copy (Pricing)

b) Advertising revenues (sale of advertising space) which is generally a function of

i) Ad space sold commercially (sq cm) (Volumes) and

ii) Average yield (Rs per sq cm) (Pricing)

Exhibit 33: Advertising revenue contributes nearly 70% of total revenues

Source: FICCI-KPMG 2016, Equirus Research

English newspapers are generally sold at lower prices (even lower than cost of

production) due to stiff competition in the market, on other hand Hindi/Vernacular

newspapers have higher cover prices. However, on the advertising side, English

newspaper generally command a premium on the ad-rates than Hindi/Vernacular

newspapers, mainly because higher income people whom advertisers are targeting read

English newspapers.

Exhibit 34: English newspaper revenues are more skewed towards advertising than Hindi

Source: FICCI-KPMG 2016, Equirus Research

On the cost side, the main operating costs for a newspaper publisher are:

a) Production costs mainly newsprint costs

b) Employee costs

c) Marketing and distribution costs

d) Content cost if procured from other agencies

67% 67% 67% 67% 67% 67% 67% 68% 68% 69%

33% 33% 33% 33% 33% 33% 33% 32% 32% 31%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2011 2012 2013 2014 2015 2016e 2017e 2018e 2019e 2020e

Advertising revenue (%) Circulation revenue(%)

68% 65%

32% 35%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

English Hindi

Advertising Circulation

Page 16

Print Media Sector Note Overweight

January 8, 2017 Analyst: Depesh Kashyap,CFA [email protected] (+91-7228934327) Page 16 of 35

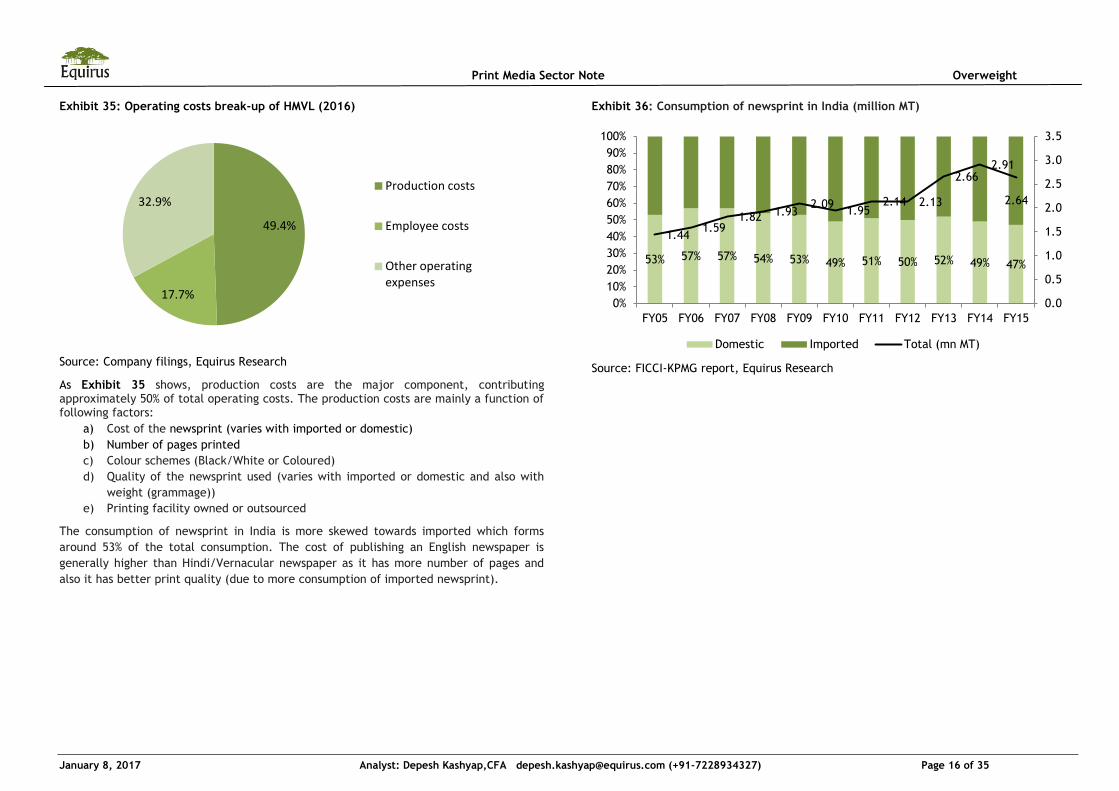

Exhibit 35: Operating costs break-up of HMVL (2016)

Source: Company filings, Equirus Research

As Exhibit 35 shows, production costs are the major component, contributing approximately 50% of total operating costs. The production costs are mainly a function of following factors:

a) Cost of the newsprint (varies with imported or domestic)

b) Number of pages printed

c) Colour schemes (Black/White or Coloured)

d) Quality of the newsprint used (varies with imported or domestic and also with

weight (grammage))

e) Printing facility owned or outsourced

The consumption of newsprint in India is more skewed towards imported which forms

around 53% of the total consumption. The cost of publishing an English newspaper is

generally higher than Hindi/Vernacular newspaper as it has more number of pages and

also it has better print quality (due to more consumption of imported newsprint).

Exhibit 36: Consumption of newsprint in India (million MT)

Source: FICCI-KPMG report, Equirus Research

49.4%

17.7%

32.9% Production costs

Employee costs

Other operating expenses

53% 57% 57% 54% 53% 49% 51% 50% 52% 49% 47%

1.44 1.59

1.82 1.93 2.09

1.95 2.14 2.13

2.66 2.91

2.64

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

FY05 FY06 FY07 FY08 FY09 FY10 FY11 FY12 FY13 FY14 FY15

Domestic Imported Total (mn MT)

Page 17

Print Media Sector Note Overweight

January 8, 2017 Analyst: Depesh Kashyap,CFA [email protected] (+91-7228934327) Page 17 of 35

Print advertisement cycle: Remains favourable?

High dependence on advertising revenues makes the newspaper business highly

dependent on economic cycles. Exhibit 37 shows that cyclical sectors like Auto, Real

estate etc as among the top sectors which advertise heavily in the newspapers. Our

analysis of the past economic cycles shows that print advertising revenues closely lag the

Indian macroeconomic indicators like the real GDP growth rates (Exhibit 38), IIP index

(Exhibit 39) and the GDP per capita (Exhibit 40). The important point to note is that

even in the downturns, the print advertising growth rates had always stayed positive.

In our view, the advertising revenues are set to improve due to following key drivers:

1. Increasing media spend as % of GDP

2. Improving macroeconomic indicators

3. Easing of policy rates

4. Increase in discretionary spends by consumers

5. Rise of consumers in Tier 2 and 3 cities

6. Increase in ad-rates for Hindi/regional newspapers

7. Upcoming state elections and revised DAVP policy

8. Growth in emerging sectors like education, organised retail and

telecommunication

Exhibit 37: Top categories in the print advertising pie

Source: FICCI-KPMG report, Equirus Research

Exhibit 38: Real GDP growth leads the advertising revenue growth

Source: Bloomberg, FICCI-KPMG report, Equirus Research

Exhibit 39: IIP and the advertising revenue growth

Source: Bloomberg, FICCI-KPMG report, Equirus Research

14.6%

12.8%

9.8%

7.0%

6.0%

4.3% 3.8%

5.6%

4.7% 0.0%

4.6% 1.9%

1.3%

1.0%

22.4%

FMCG

Auto

Education

Real estate

Clothing/fashion/jewellery

E-com

Telecom/DTH

Retail

BFSI

Election/political ads

HH Durables

Travel and tourism

Corporate

Media

Others

0%

5%

10%

15%

20%

25%

5.0%

5.5%

6.0%

6.5%

7.0%

7.5%

8.0%

8.5%

9.0%

9.5%

10.0%

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

GDP growth (%) Print advertising revenue (YoY %) (RHS)

0%

5%

10%

15%

20%

25%

-4.0

-2.0

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

16.0

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

IIP index Print advertising revenue (YoY %) (RHS)

Page 18

Print Media Sector Note Overweight

January 8, 2017 Analyst: Depesh Kashyap,CFA [email protected] (+91-7228934327) Page 18 of 35

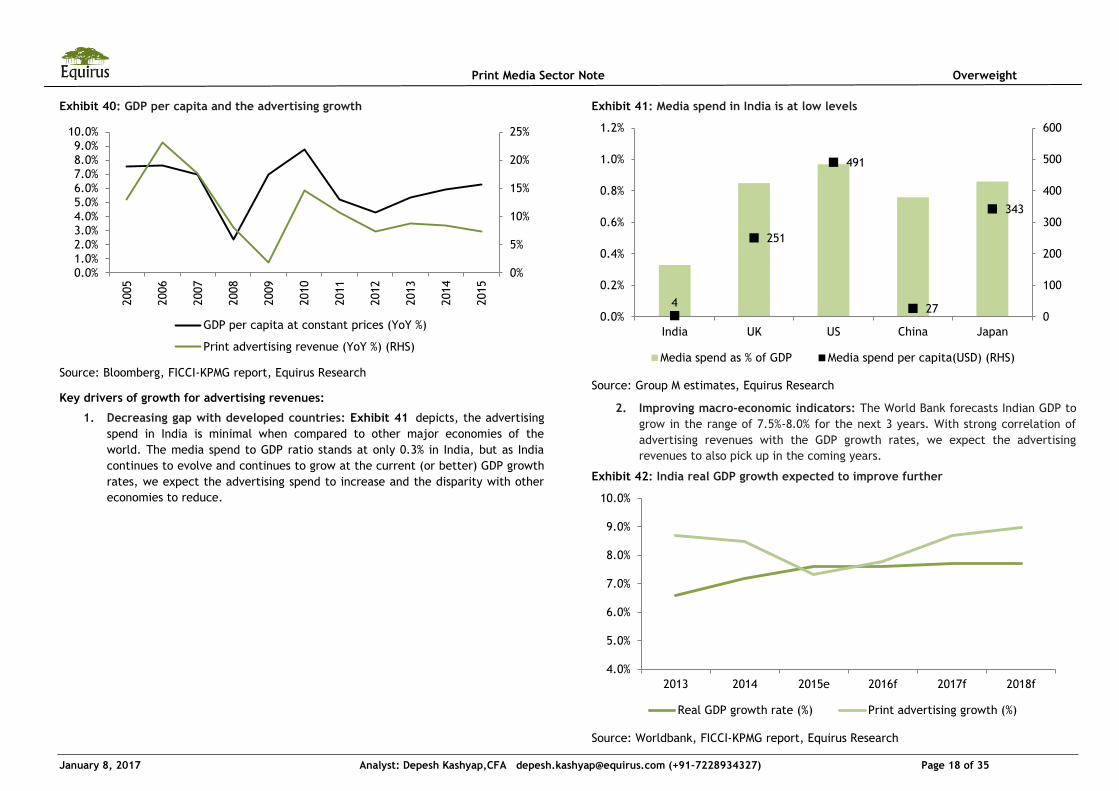

Exhibit 40: GDP per capita and the advertising growth

Source: Bloomberg, FICCI-KPMG report, Equirus Research

Key drivers of growth for advertising revenues:

1. Decreasing gap with developed countries: Exhibit 41 depicts, the advertising

spend in India is minimal when compared to other major economies of the

world. The media spend to GDP ratio stands at only 0.3% in India, but as India

continues to evolve and continues to grow at the current (or better) GDP growth

rates, we expect the advertising spend to increase and the disparity with other

economies to reduce.

Exhibit 41: Media spend in India is at low levels

Source: Group M estimates, Equirus Research

2. Improving macro-economic indicators: The World Bank forecasts Indian GDP to

grow in the range of 7.5%-8.0% for the next 3 years. With strong correlation of

advertising revenues with the GDP growth rates, we expect the advertising

revenues to also pick up in the coming years.

Exhibit 42: India real GDP growth expected to improve further

Source: Worldbank, FICCI-KPMG report, Equirus Research

0%

5%

10%

15%

20%

25%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

8.0%

9.0%

10.0% 2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

GDP per capita at constant prices (YoY %)

Print advertising revenue (YoY %) (RHS)

4

251

491

27

343

0

100

200

300

400

500

600

0.0%

0.2%

0.4%

0.6%

0.8%

1.0%

1.2%

India UK US China Japan

Media spend as % of GDP Media spend per capita(USD) (RHS)

4.0%

5.0%

6.0%

7.0%

8.0%

9.0%

10.0%

2013 2014 2015e 2016f 2017f 2018f

Real GDP growth rate (%) Print advertising growth (%)

Page 19

Print Media Sector Note Overweight

January 8, 2017 Analyst: Depesh Kashyap,CFA [email protected] (+91-7228934327) Page 19 of 35

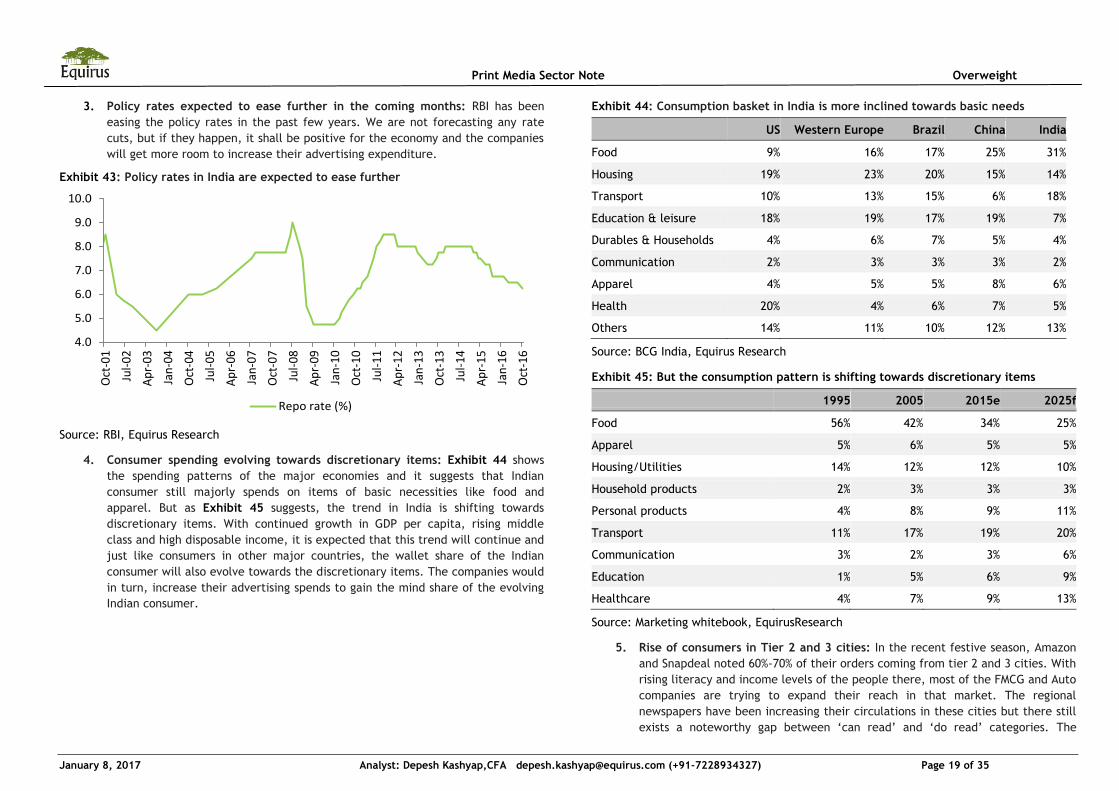

3. Policy rates expected to ease further in the coming months: RBI has been

easing the policy rates in the past few years. We are not forecasting any rate

cuts, but if they happen, it shall be positive for the economy and the companies

will get more room to increase their advertising expenditure.

Exhibit 43: Policy rates in India are expected to ease further

Source: RBI, Equirus Research

4. Consumer spending evolving towards discretionary items: Exhibit 44 shows

the spending patterns of the major economies and it suggests that Indian

consumer still majorly spends on items of basic necessities like food and

apparel. But as Exhibit 45 suggests, the trend in India is shifting towards

discretionary items. With continued growth in GDP per capita, rising middle

class and high disposable income, it is expected that this trend will continue and

just like consumers in other major countries, the wallet share of the Indian

consumer will also evolve towards the discretionary items. The companies would

in turn, increase their advertising spends to gain the mind share of the evolving

Indian consumer.

Exhibit 44: Consumption basket in India is more inclined towards basic needs

US Western Europe Brazil China India

Food 9% 16% 17% 25% 31%

Housing 19% 23% 20% 15% 14%

Transport 10% 13% 15% 6% 18%

Education & leisure 18% 19% 17% 19% 7%

Durables & Households 4% 6% 7% 5% 4%

Communication 2% 3% 3% 3% 2%

Apparel 4% 5% 5% 8% 6%

Health 20% 4% 6% 7% 5%

Others 14% 11% 10% 12% 13%

Source: BCG India, Equirus Research

Exhibit 45: But the consumption pattern is shifting towards discretionary items

1995 2005 2015e 2025f

Food 56% 42% 34% 25%

Apparel 5% 6% 5% 5%

Housing/Utilities 14% 12% 12% 10%

Household products 2% 3% 3% 3%

Personal products 4% 8% 9% 11%

Transport 11% 17% 19% 20%

Communication 3% 2% 3% 6%

Education 1% 5% 6% 9%

Healthcare 4% 7% 9% 13%

Source: Marketing whitebook, EquirusResearch

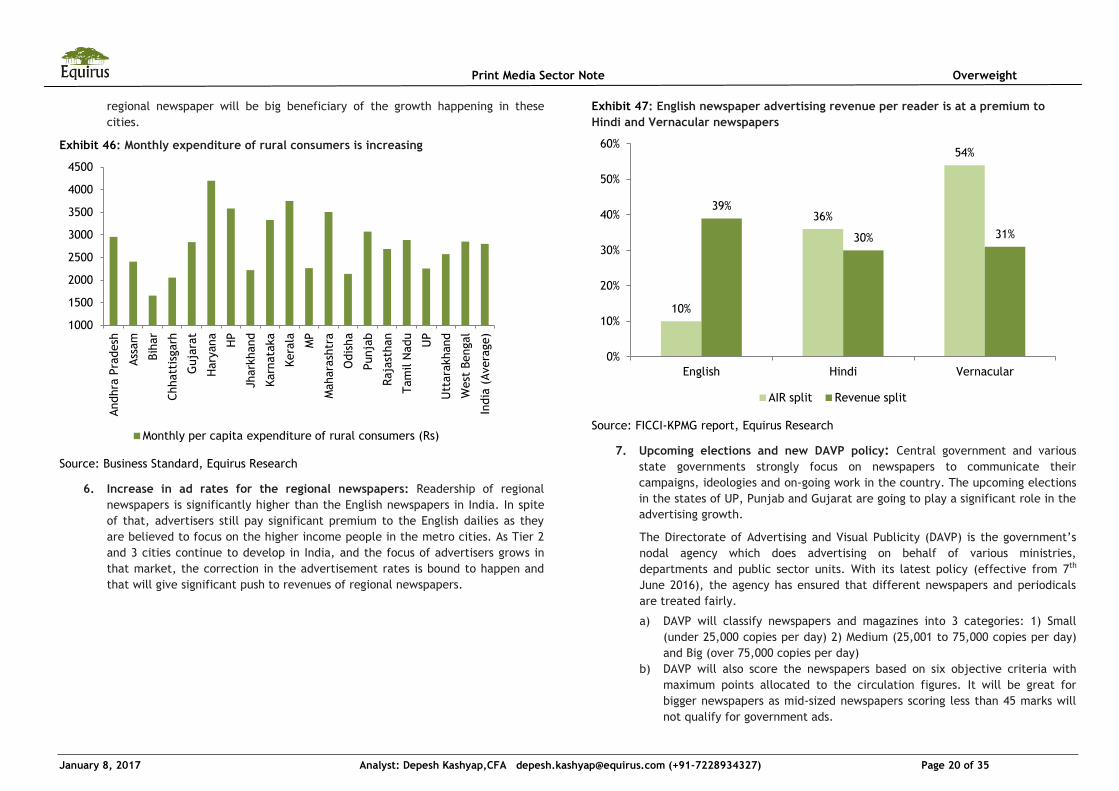

5. Rise of consumers in Tier 2 and 3 cities: In the recent festive season, Amazon

and Snapdeal noted 60%-70% of their orders coming from tier 2 and 3 cities. With

rising literacy and income levels of the people there, most of the FMCG and Auto

companies are trying to expand their reach in that market. The regional

newspapers have been increasing their circulations in these cities but there still

exists a noteworthy gap between ‘can read’ and ‘do read’ categories. The

4.0

5.0

6.0

7.0

8.0

9.0

10.0

Oct

-01

Jul-

02

Ap

r-03

Jan

-04

Oct

-04

Jul-

05

Ap

r-06

Jan

-07

Oct

-07

Jul-

08

Ap

r-09

Jan

-10

Oct

-10

Jul-

11

Ap

r-12

Jan

-13

Oct

-13

Jul-

14

Ap

r-15

Jan

-16

Oct

-16

Repo rate (%)

Page 20

Print Media Sector Note Overweight

January 8, 2017 Analyst: Depesh Kashyap,CFA [email protected] (+91-7228934327) Page 20 of 35

regional newspaper will be big beneficiary of the growth happening in these

cities.

Exhibit 46: Monthly expenditure of rural consumers is increasing

Source: Business Standard, Equirus Research

6. Increase in ad rates for the regional newspapers: Readership of regional

newspapers is significantly higher than the English newspapers in India. In spite

of that, advertisers still pay significant premium to the English dailies as they

are believed to focus on the higher income people in the metro cities. As Tier 2

and 3 cities continue to develop in India, and the focus of advertisers grows in

that market, the correction in the advertisement rates is bound to happen and

that will give significant push to revenues of regional newspapers.

Exhibit 47: English newspaper advertising revenue per reader is at a premium to

Hindi and Vernacular newspapers

Source: FICCI-KPMG report, Equirus Research

7. Upcoming elections and new DAVP policy: Central government and various

state governments strongly focus on newspapers to communicate their

campaigns, ideologies and on-going work in the country. The upcoming elections

in the states of UP, Punjab and Gujarat are going to play a significant role in the

advertising growth.

The Directorate of Advertising and Visual Publicity (DAVP) is the government’s

nodal agency which does advertising on behalf of various ministries,

departments and public sector units. With its latest policy (effective from 7th

June 2016), the agency has ensured that different newspapers and periodicals

are treated fairly.

a) DAVP will classify newspapers and magazines into 3 categories: 1) Small

(under 25,000 copies per day) 2) Medium (25,001 to 75,000 copies per day)

and Big (over 75,000 copies per day)

b) DAVP will also score the newspapers based on six objective criteria with

maximum points allocated to the circulation figures. It will be great for

bigger newspapers as mid-sized newspapers scoring less than 45 marks will

not qualify for government ads.

1000

1500

2000

2500

3000

3500

4000

4500

Andhra

Pra

desh

Ass

am

Bih

ar

Chhatt

isgarh

Guja

rat

Hary

ana

HP

Jhark

hand

Karn

ata

ka

Kera

la

MP

Mahara

shtr

a

Odis

ha

Punja

b

Raja

sthan

Tam

il N

adu

UP

Utt

ara

khand

West

Bengal

India

(Avera

ge)

Monthly per capita expenditure of rural consumers (Rs)

10%

36%

54%

39%

30% 31%

0%

10%

20%

30%

40%

50%

60%

English Hindi Vernacular

AIR split Revenue split

Page 21

Print Media Sector Note Overweight

January 8, 2017 Analyst: Depesh Kashyap,CFA [email protected] (+91-7228934327) Page 21 of 35

c) Overall, English newspapers will receive 30% of spend, Hindi 35% and

regional will receive remaining 35%.

d) DAVP will offer premium for specific placement of ads in the dailies, earlier

there was no premium for the pages or placements. Now, it will pay 50%

premium above its normal rates for front page, 20% premium for third page,

10% premium for fifth page and 30% premium for back page.

e) It has also streamlined the procedure for quick and timely payment by

ministries to DAVP.

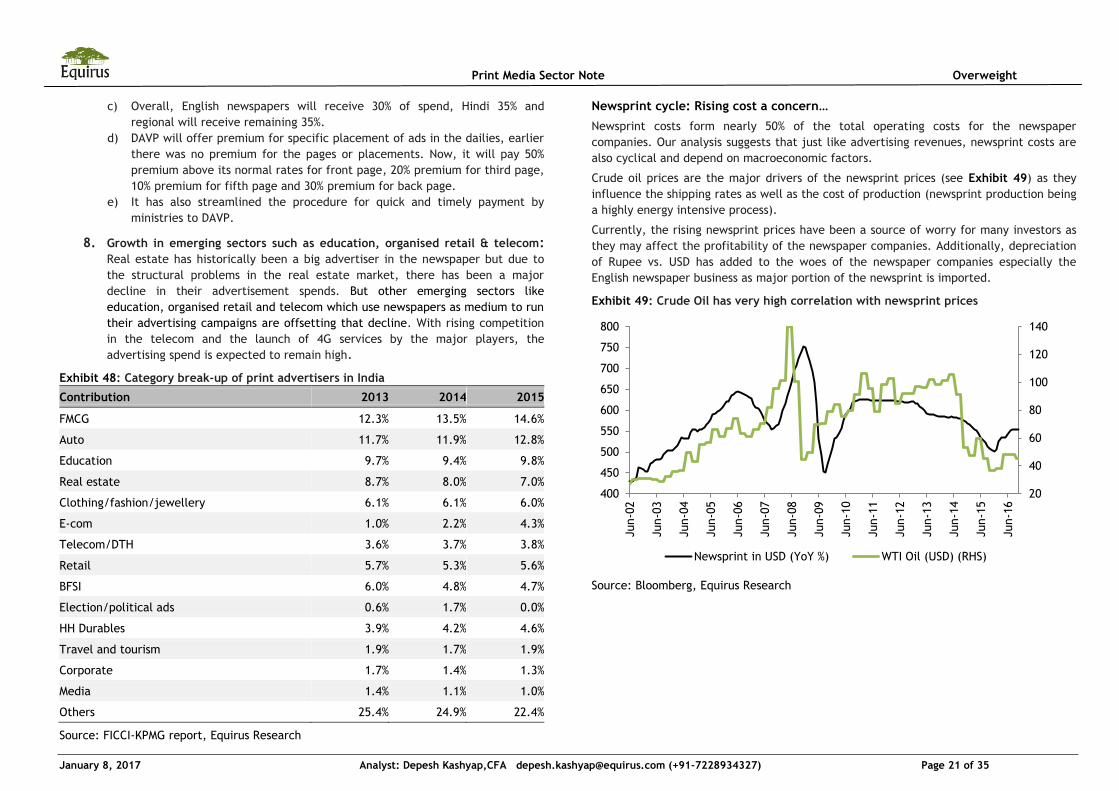

8. Growth in emerging sectors such as education, organised retail & telecom:

Real estate has historically been a big advertiser in the newspaper but due to

the structural problems in the real estate market, there has been a major

decline in their advertisement spends. But other emerging sectors like

education, organised retail and telecom which use newspapers as medium to run

their advertising campaigns are offsetting that decline. With rising competition

in the telecom and the launch of 4G services by the major players, the

advertising spend is expected to remain high.

Exhibit 48: Category break-up of print advertisers in India

Contribution 2013 2014 2015

FMCG 12.3% 13.5% 14.6%

Auto 11.7% 11.9% 12.8%

Education 9.7% 9.4% 9.8%

Real estate 8.7% 8.0% 7.0%

Clothing/fashion/jewellery 6.1% 6.1% 6.0%

E-com 1.0% 2.2% 4.3%

Telecom/DTH 3.6% 3.7% 3.8%

Retail 5.7% 5.3% 5.6%

BFSI 6.0% 4.8% 4.7%

Election/political ads 0.6% 1.7% 0.0%

HH Durables 3.9% 4.2% 4.6%

Travel and tourism 1.9% 1.7% 1.9%

Corporate 1.7% 1.4% 1.3%

Media 1.4% 1.1% 1.0%

Others 25.4% 24.9% 22.4%

Source: FICCI-KPMG report, Equirus Research

Newsprint cycle: Rising cost a concern…

Newsprint costs form nearly 50% of the total operating costs for the newspaper

companies. Our analysis suggests that just like advertising revenues, newsprint costs are

also cyclical and depend on macroeconomic factors.

Crude oil prices are the major drivers of the newsprint prices (see Exhibit 49) as they

influence the shipping rates as well as the cost of production (newsprint production being

a highly energy intensive process).

Currently, the rising newsprint prices have been a source of worry for many investors as

they may affect the profitability of the newspaper companies. Additionally, depreciation

of Rupee vs. USD has added to the woes of the newspaper companies especially the

English newspaper business as major portion of the newsprint is imported.

Exhibit 49: Crude Oil has very high correlation with newsprint prices

Source: Bloomberg, Equirus Research

20

40

60

80

100

120

140

400

450

500

550

600

650

700

750

800

Jun-0

2

Jun-0

3

Jun-0

4

Jun-0

5

Jun-0

6

Jun-0

7

Jun-0

8

Jun-0

9

Jun-1

0

Jun-1

1

Jun-1

2

Jun-1

3

Jun-1

4

Jun-1

5

Jun-1

6

Newsprint in USD (YoY %) WTI Oil (USD) (RHS)

Page 22

Print Media Sector Note Overweight

January 8, 2017 Analyst: Depesh Kashyap,CFA [email protected] (+91-7228934327) Page 22 of 35

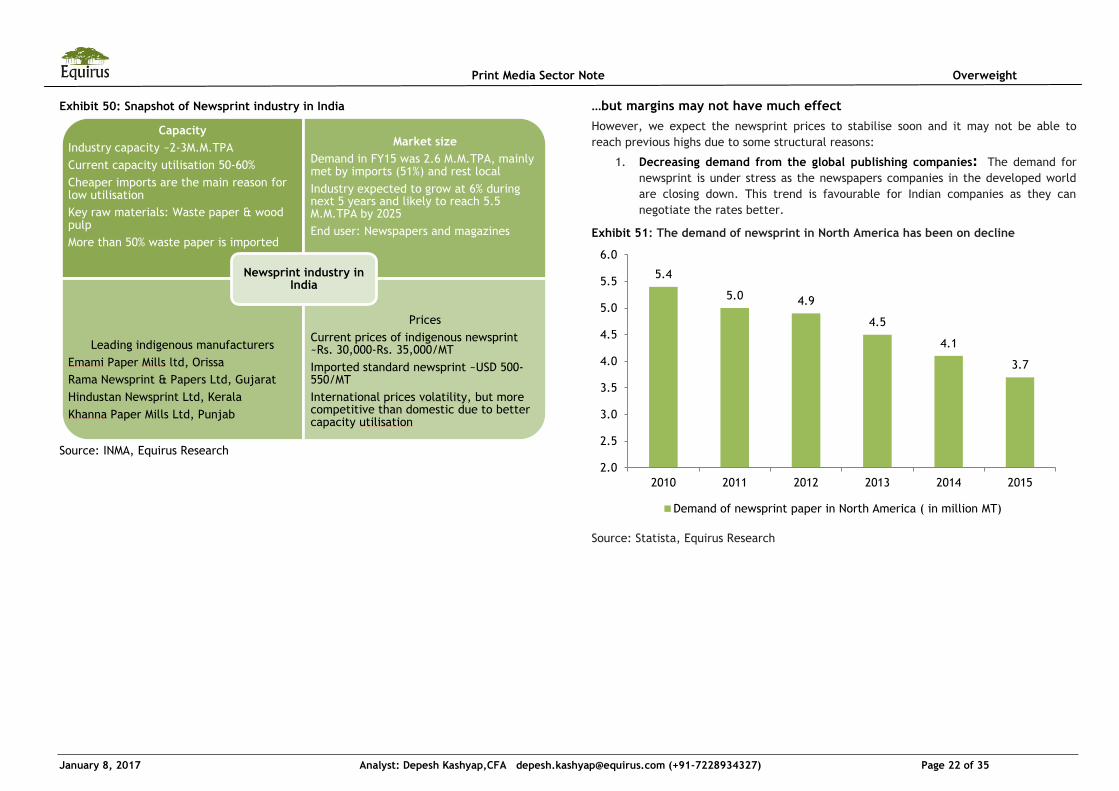

Exhibit 50: Snapshot of Newsprint industry in India

Source: INMA, Equirus Research

…but margins may not have much effect

However, we expect the newsprint prices to stabilise soon and it may not be able to

reach previous highs due to some structural reasons:

1. Decreasing demand from the global publishing companies: The demand for

newsprint is under stress as the newspapers companies in the developed world

are closing down. This trend is favourable for Indian companies as they can

negotiate the rates better.

Exhibit 51: The demand of newsprint in North America has been on decline

Source: Statista, Equirus Research

Capacity

Industry capacity ~2-3M.M.TPA

Current capacity utilisation 50-60%

Cheaper imports are the main reason for low utilisation

Key raw materials: Waste paper & wood pulp

More than 50% waste paper is imported

Market size

Demand in FY15 was 2.6 M.M.TPA, mainly met by imports (51%) and rest local

Industry expected to grow at 6% during next 5 years and likely to reach 5.5 M.M.TPA by 2025

End user: Newspapers and magazines

Leading indigenous manufacturers

Emami Paper Mills ltd, Orissa

Rama Newsprint & Papers Ltd, Gujarat

Hindustan Newsprint Ltd, Kerala

Khanna Paper Mills Ltd, Punjab

Prices

Current prices of indigenous newsprint ~Rs. 30,000-Rs. 35,000/MT

Imported standard newsprint ~USD 500-550/MT

International prices volatility, but more competitive than domestic due to better capacity utilisation

Newsprint industry in India

5.4

5.0 4.9

4.5

4.1

3.7

2.0

2.5

3.0

3.5

4.0

4.5

5.0

5.5

6.0

2010 2011 2012 2013 2014 2015

Demand of newsprint paper in North America ( in million MT)

Page 23

Print Media Sector Note Overweight

January 8, 2017 Analyst: Depesh Kashyap,CFA [email protected] (+91-7228934327) Page 23 of 35

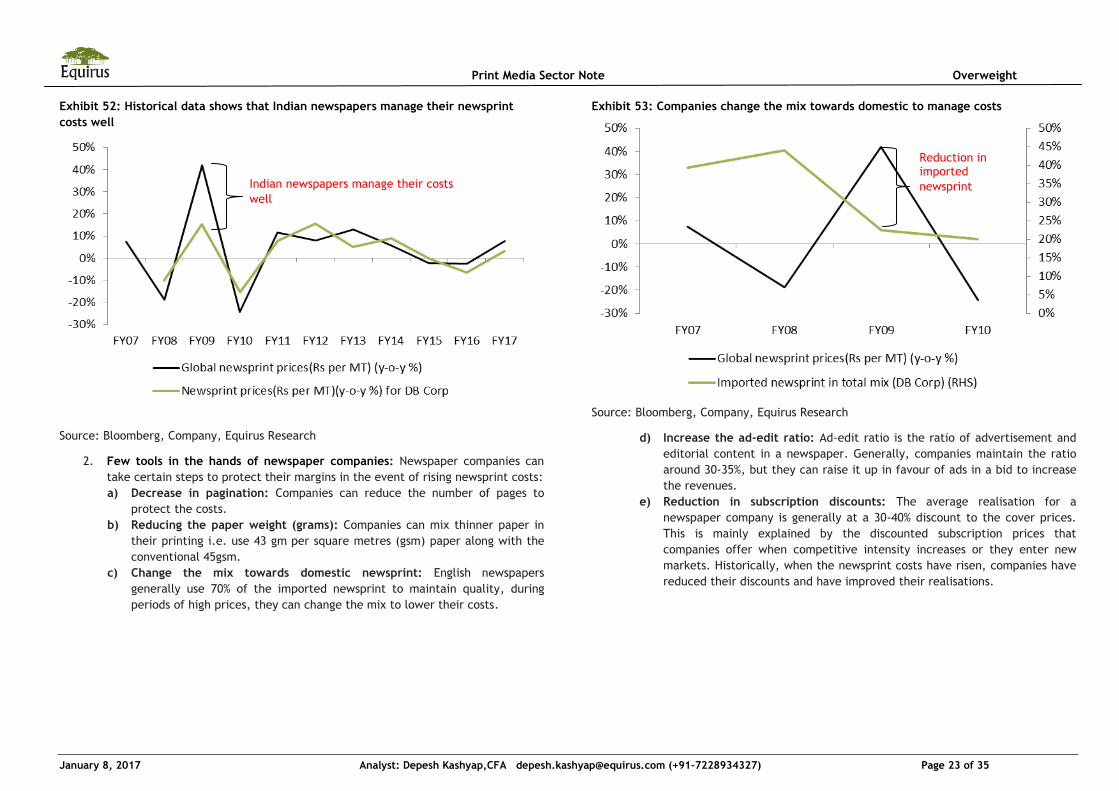

Exhibit 52: Historical data shows that Indian newspapers manage their newsprint

costs well

Source: Bloomberg, Company, Equirus Research

2. Few tools in the hands of newspaper companies: Newspaper companies can

take certain steps to protect their margins in the event of rising newsprint costs:

a) Decrease in pagination: Companies can reduce the number of pages to

protect the costs.

b) Reducing the paper weight (grams): Companies can mix thinner paper in

their printing i.e. use 43 gm per square metres (gsm) paper along with the

conventional 45gsm.

c) Change the mix towards domestic newsprint: English newspapers

generally use 70% of the imported newsprint to maintain quality, during

periods of high prices, they can change the mix to lower their costs.

Exhibit 53: Companies change the mix towards domestic to manage costs

Source: Bloomberg, Company, Equirus Research

d) Increase the ad-edit ratio: Ad-edit ratio is the ratio of advertisement and

editorial content in a newspaper. Generally, companies maintain the ratio

around 30-35%, but they can raise it up in favour of ads in a bid to increase

the revenues.

e) Reduction in subscription discounts: The average realisation for a

newspaper company is generally at a 30-40% discount to the cover prices.

This is mainly explained by the discounted subscription prices that

companies offer when competitive intensity increases or they enter new

markets. Historically, when the newsprint costs have risen, companies have

reduced their discounts and have improved their realisations.

Indian newspapers manage their costs

well

Reduction in imported

newsprint

Page 24

Print Media Sector Note Overweight

January 8, 2017 Analyst: Depesh Kashyap,CFA [email protected] (+91-7228934327) Page 24 of 35

Exhibit 54: Reduction in subscription discounts to counter newsprint costs

Source: Company, Equirus Research

3. Case of positive operating leverage: Due to higher dependence on advertising

revenues, earnings are more sensitive to changes in advertising revenues than

changes in newsprint costs. We estimate that the earnings of the sector are

~1.2x more sensitive to changes in advertising than changes in newsprint costs.

So, even if newsprint costs rise more than expected, in our view the strong

advertising growth shall be able to drive the earnings forward.

Differentiating factors: A bare comparison

We compared the Print, Radio, Digital and overall business on some common parameters.

Following are our conclusions of the same:

1. Print business: In our view, if we look only at print businesses of these

Companies, Dainik Bhaskar looks marginal favourite. It has highest daily

circulation amongst the competitors and has more diversified readership across

various states whereas Jagran and Hindustan are more focussed on UP & Bihar.

The Company has proven track record of making strong entry in new markets

and becoming No.1 from Day1 of launch.

2. Radio business: On comparing radio businesses of these companies, Jagran is

clearly ahead of the rest. The upcoming IPO of Radio City (91.1 FM) will further

unlock value of its radio business. All Companies have different strategies with

their radio businesses; while some operate the business as complementary

platform to their print business, others operate it more independently.

3. Digital Business: Though digital is still a very small component of the overall

business, but all the companies have been proactively establishing their brands

in the digital space. In this space, HT media has clearly made the biggest

investments amongst its peers. Apart from working on the news daily websites

like other players, the Company has established Shine.com which has become

no.2 jobs portal in India after Naukri.com. It has also ventured into education

space which is seen as high growth industry. As far as only news websites/portals

are concerned, Dainik Bhaskar attracts the maximum traffic along with Times of

India.

-20%

-15%

-10%

-5%

0%

5%

10%

15%

20%

FY08 FY09 FY10 FY11 FY12 FY13 FY14 FY15 FY16

Newsprint cost per MT (Rs) Average realisation(Rs)

Page 25

Print Media Sector Note Overweight

January 8, 2017 Analyst: Depesh Kashyap,CFA [email protected] (+91-7228934327) Page 25 of 35

Exhibit 55: DB Corp stands out with its Print strategy, Jagran has the best Radio

business, and HT Media leads with its Digital investments

Ranking DB Corp Jagran HT Media/

HMVL Comments

Print 1 2 3

Well proven market entry

strategy, diversified

readership makes DB Corp

our top pick in terms as far

as Print is concerned

Radio 3 1 2

Radio City(Jagran) is our top

pick because of its reach

and popularity.

Digital 2 3 1

HT Media has diversified its

digital investments in News,

jobs and education portals.

In terms of brand recall, DB

Corp is getting maximum

traffic on its websites.

Source: Company, Equirus Research

Below we look into detail all the three segments of these Companies.

DainikBhaskar has the most diversified print business

For the key Hindi print players in the industry, India can be broadly divided into 2 broad

categories as shown in Exhibit 56. 1) Focus markets- which include major Hindi speaking

states of UP, MP, Chattisgarh, Rajasthan, Bihar, Haryana, Punjab, Himachal Pradesh,

Uttarakhand, Jharkhand and J&K. The focus is also on regional markets where majority

understand Hindi like West Bengal, Orissa, Maharashtra and Gujarat. 2) Non Focus

markets- Rest of the markets like North-eastern states, Southern states of Tamil Nadu,

Karnataka, Kerala, AP& Telangana are not priority for the industry players at the

moment. Also the major metros are considered as majorly an English print market, with

Delhi being an exception as it is also a strong market for Hindi players.

Exhibit 56: Print media Landscape in India

Source: Company, Equirus Research * Delhi which is a metro is a also a strong market for

Hindi newspapers

In the print space, we rank DB Corp higher than others mainly due to following factors:

1. Diversified readership base: DB Corp is present in the highest number of states

(14) as compared to its peers and has the most diversified (see Exhibit 57)

readership base across various states whereas both Jagran and Hindustan are

more focussed on UP and Bihar. This diversification makes DB Corp more immune

to floods and other calamities which may disrupt any particular state. Though

UP, due to its large population is the largest market for advertisers in India, but

the states like Bihar, MP and Jharkhand are growing at faster rates. Also, having

a diverse readership like Dainik Bhaskar, makes a Company immune to slowdown

in any particular states.

2. Proven track record of entering new markets: Generally, newspaper

companies try to maintain their leadership in one or two states. But Dainik

Bhaskar has been able to grow beyond its MPCG market and expand into newer

territories like Gujarat and Rajasthan. From the day 1 of its launch, it was able

Print Media landscape

Focus markets

Remaining states

Hindi

UP, MP, Chattisgarh, Rajasthan, Haryana, Punjab, Himachal, Uttarakhand, Jharkhand, J&K, Bihar

Bengali/Oriya/Marathi/Gujarati

Non-focus markets

7 NE states 5 Southern

states

7 Metros (English

Play)

Page 26

Print Media Sector Note Overweight

January 8, 2017 Analyst: Depesh Kashyap,CFA [email protected] (+91-7228934327) Page 26 of 35

to displace the market leader of that particular state. This speaks a lot about

the strong brand recognition of Bhaskar.

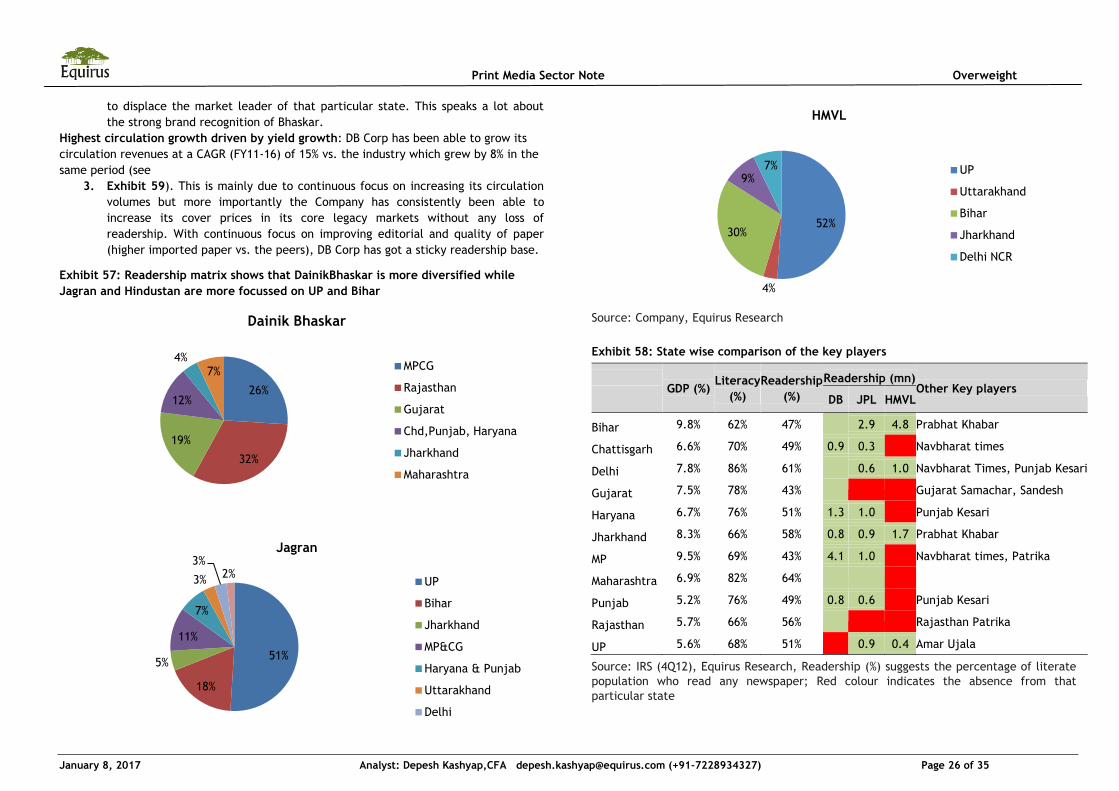

Highest circulation growth driven by yield growth: DB Corp has been able to grow its

circulation revenues at a CAGR (FY11-16) of 15% vs. the industry which grew by 8% in the

same period (see

3. Exhibit 59). This is mainly due to continuous focus on increasing its circulation

volumes but more importantly the Company has consistently been able to

increase its cover prices in its core legacy markets without any loss of

readership. With continuous focus on improving editorial and quality of paper

(higher imported paper vs. the peers), DB Corp has got a sticky readership base.

Exhibit 57: Readership matrix shows that DainikBhaskar is more diversified while

Jagran and Hindustan are more focussed on UP and Bihar

Source: Company, Equirus Research

Exhibit 58: State wise comparison of the key players

GDP (%)

Literacy

(%)

Readership

(%)

Readership (mn) Other Key players

DB JPL HMVL

Bihar 9.8% 62% 47%

2.9 4.8 Prabhat Khabar

Chattisgarh 6.6% 70% 49% 0.9 0.3

Navbharat times

Delhi 7.8% 86% 61%

0.6 1.0 Navbharat Times, Punjab Kesari

Gujarat 7.5% 78% 43%

Gujarat Samachar, Sandesh

Haryana 6.7% 76% 51% 1.3 1.0

Punjab Kesari

Jharkhand 8.3% 66% 58% 0.8 0.9 1.7 Prabhat Khabar

MP 9.5% 69% 43% 4.1 1.0

Navbharat times, Patrika

Maharashtra 6.9% 82% 64%

Punjab 5.2% 76% 49% 0.8 0.6

Punjab Kesari

Rajasthan 5.7% 66% 56%

Rajasthan Patrika

UP 5.6% 68% 51%

0.9 0.4 Amar Ujala

Source: IRS (4Q12), Equirus Research, Readership (%) suggests the percentage of literate

population who read any newspaper; Red colour indicates the absence from that

particular state

26%

32%

19%

12%

4% 7%

Dainik Bhaskar

MPCG

Rajasthan

Gujarat

Chd,Punjab, Haryana

Jharkhand

Maharashtra

51%

18%

5%

11%

7%

3%

3% 2%

Jagran

UP

Bihar

Jharkhand

MP&CG

Haryana & Punjab

Uttarakhand

Delhi

52%

4%

30%

9% 7%

HMVL

UP

Uttarakhand

Bihar

Jharkhand

Delhi NCR

Page 27

Print Media Sector Note Overweight

January 8, 2017 Analyst: Depesh Kashyap,CFA [email protected] (+91-7228934327) Page 27 of 35

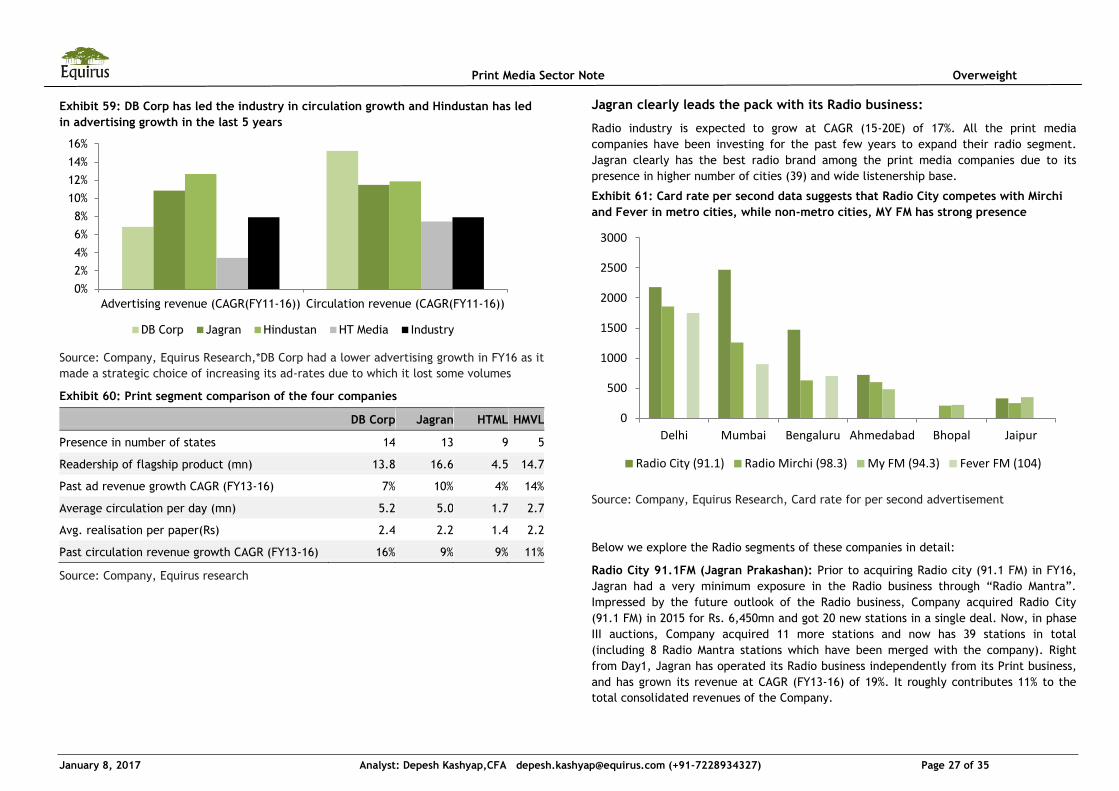

Exhibit 59: DB Corp has led the industry in circulation growth and Hindustan has led

in advertising growth in the last 5 years

Source: Company, Equirus Research,*DB Corp had a lower advertising growth in FY16 as it

made a strategic choice of increasing its ad-rates due to which it lost some volumes

Exhibit 60: Print segment comparison of the four companies

DB Corp Jagran HTML HMVL

Presence in number of states 14 13 9 5

Readership of flagship product (mn) 13.8 16.6 4.5 14.7

Past ad revenue growth CAGR (FY13-16) 7% 10% 4% 14%

Average circulation per day (mn) 5.2 5.0 1.7 2.7

Avg. realisation per paper(Rs) 2.4 2.2 1.4 2.2

Past circulation revenue growth CAGR (FY13-16) 16% 9% 9% 11%

Source: Company, Equirus research

Jagran clearly leads the pack with its Radio business:

Radio industry is expected to grow at CAGR (15-20E) of 17%. All the print media

companies have been investing for the past few years to expand their radio segment.

Jagran clearly has the best radio brand among the print media companies due to its

presence in higher number of cities (39) and wide listenership base.

Exhibit 61: Card rate per second data suggests that Radio City competes with Mirchi

and Fever in metro cities, while non-metro cities, MY FM has strong presence

Source: Company, Equirus Research, Card rate for per second advertisement

Below we explore the Radio segments of these companies in detail:

Radio City 91.1FM (Jagran Prakashan): Prior to acquiring Radio city (91.1 FM) in FY16,

Jagran had a very minimum exposure in the Radio business through “Radio Mantra”.

Impressed by the future outlook of the Radio business, Company acquired Radio City

(91.1 FM) in 2015 for Rs. 6,450mn and got 20 new stations in a single deal. Now, in phase

III auctions, Company acquired 11 more stations and now has 39 stations in total

(including 8 Radio Mantra stations which have been merged with the company). Right

from Day1, Jagran has operated its Radio business independently from its Print business,

and has grown its revenue at CAGR (FY13-16) of 19%. It roughly contributes 11% to the

total consolidated revenues of the Company.

0%

2%

4%

6%

8%

10%

12%

14%

16%

Advertising revenue (CAGR(FY11-16)) Circulation revenue (CAGR(FY11-16))

DB Corp Jagran Hindustan HT Media Industry

0

500

1000

1500

2000

2500

3000

Delhi Mumbai Bengaluru Ahmedabad Bhopal Jaipur

Radio City (91.1) Radio Mirchi (98.3) My FM (94.3) Fever FM (104)

Page 28

Print Media Sector Note Overweight

January 8, 2017 Analyst: Depesh Kashyap,CFA [email protected] (+91-7228934327) Page 28 of 35

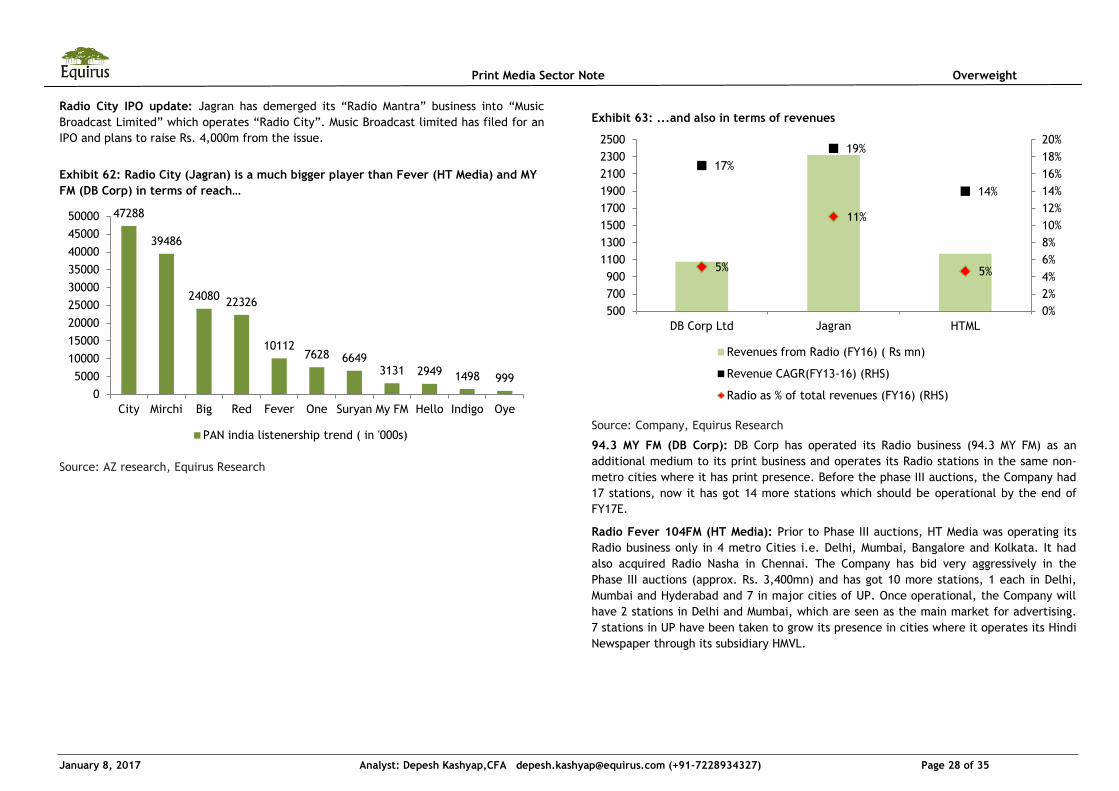

Radio City IPO update: Jagran has demerged its “Radio Mantra” business into “Music

Broadcast Limited” which operates “Radio City”. Music Broadcast limited has filed for an

IPO and plans to raise Rs. 4,000m from the issue.

Exhibit 62: Radio City (Jagran) is a much bigger player than Fever (HT Media) and MY

FM (DB Corp) in terms of reach…

Source: AZ research, Equirus Research

Exhibit 63: ...and also in terms of revenues

Source: Company, Equirus Research

94.3 MY FM (DB Corp): DB Corp has operated its Radio business (94.3 MY FM) as an

additional medium to its print business and operates its Radio stations in the same non-

metro cities where it has print presence. Before the phase III auctions, the Company had

17 stations, now it has got 14 more stations which should be operational by the end of

FY17E.

Radio Fever 104FM (HT Media): Prior to Phase III auctions, HT Media was operating its

Radio business only in 4 metro Cities i.e. Delhi, Mumbai, Bangalore and Kolkata. It had

also acquired Radio Nasha in Chennai. The Company has bid very aggressively in the

Phase III auctions (approx. Rs. 3,400mn) and has got 10 more stations, 1 each in Delhi,

Mumbai and Hyderabad and 7 in major cities of UP. Once operational, the Company will

have 2 stations in Delhi and Mumbai, which are seen as the main market for advertising.

7 stations in UP have been taken to grow its presence in cities where it operates its Hindi

Newspaper through its subsidiary HMVL.

47288

39486

24080 22326

10112 7628 6649

3131 2949 1498 999

0

5000

10000

15000

20000

25000

30000

35000

40000

45000

50000

City Mirchi Big Red Fever One Suryan My FM Hello Indigo Oye

PAN india listenership trend ( in '000s)

17%

19%

14%

5%

11%

5%

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

20%

500

700

900

1100

1300

1500

1700

1900

2100

2300

2500

DB Corp Ltd Jagran HTML

Revenues from Radio (FY16) ( Rs mn)

Revenue CAGR(FY13-16) (RHS)

Radio as % of total revenues (FY16) (RHS)

Page 29

Print Media Sector Note Overweight

January 8, 2017 Analyst: Depesh Kashyap,CFA [email protected] (+91-7228934327) Page 29 of 35

Exhibit 64: Aggressive bidding by existing players in phase III auctions highlights their

bullish view on Radio industry

Source: FICCI-KPMG 2016, Equirus Research

HT media is way ahead with its Digital strategy:

Though digital revenues form very small part of the overall revenues of the print media

companies, but they are investing heavily to expand their digital presence. The digital

businesses of all companies are currently loss making as the industry still trying to figure

out the best business model. All the Companies have developed several news

websites/apps, jobs website, housing websites etc. In terms of news websites, DB Corp

has been able to attract maximum traffic as it has been able to leverage its strong brand

in the print space. HT media has made large investments in terms of Jobs portal like

Shine.com and has also ventured into education portals. Jagran has been a late starter

but is catching up fast with the peers.

Exhibit 65: HT Media is way ahead of peers as far as Digital revenues are concerned

Source: Company, Equirus Research

Exhibit 66: DB Corp leads in terms of attracting maximum traffic on its website

Source: Similarweb, Equirus Research

10

17

3

14

11

13 14

8

0

2

4

6

8

10

12

14

16

18

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

Fever 104 FM

(HT Media)

Radio Mirchi

Red FM 93.5

92.7 Big FM

Radio City 91.1 (Jagran)

94.3 MY FM (DB Corp)

95 FM Tadka

New entrants

Non-refundable One time entry fee (Rs bn) No. of frequencies (RHS)

5.4 5.4

2.5

5.3

0

1

2

3

4

5

6

0

5

10

15

20

25

30

35

Bhask

ar.

com

Jagra

n.c

om

hin

dust

anti

mes.

com

Liv

ehin

dust

an.c

om

Average traffic in Nov'16 (mn) Average visit duration(mins) (RHS)

460

213

1403 65%

38%

2% 1% 6%

0%

10%

20%

30%

40%

50%

60%

70%

0

200

400

600

800

1000

1200

1400

1600

DB Corp Ltd Jagran HT Media

Revenues from Digital (FY16) ( Rs mn)

Revenue CAGR(FY13-16) (RHS)

Digital as % of total revenues (FY16) (RHS)

Page 30

Print Media Sector Note Overweight

January 8, 2017 Analyst: Depesh Kashyap,CFA [email protected] (+91-7228934327) Page 30 of 35

Exhibit 67: Visitors spend more time on DB Corp’s website than others

Source: Similarweb, Equirus Research

Exhibit 68: Most of the traffic is routed through Social media or search engines

Source: Similarweb, Equirus Research

Exhibit 69: Standardised P&L (FY16) comparison of print companies

FY16, Rs. mn DB Corp Jagran HT Media HMVL

Revenues 100 100 100 100

RM Cost 30 30 29 38

Gross profit 70 70 71 62

Employee expenses 19 15 22 14

Other expenses 25 27 37 25

EBITDA 26 28 12 24

Conversion ratio (EBITDA/GP) 37% 40% 17% 38%

Depreciation 4 5 4 2

EBIT 22 23 8 21

Other Income/Expenses 1 -1 4 5

PBT 23 22 12 27

Tax 8 7 3 7

Tax rate(%) 36% 30% 28% 26%

Net Income 14 16 9 20

EBITDA margins (%) for FY16 26% 28% 12% 24%