29

THE GOODMAN AND CARR LLP REPORT ON THE CANADIAN PRIVATE EQUITY MARKET IN 2001 An in-depth review of key trends in the Canadian Private Equity Market in 2001 RESEARCH CONDUCTED BY

| Date post: | 06-May-2015 |

| Category: |

Economy & Finance |

| Upload: | freddy56 |

| View: | 2,004 times |

| Download: | 4 times |

THE GOODMAN AND CARR LLP

REPORT ON THE CANADIAN

PRIVATE EQUITY

MARKET IN 2001

An in-depth

review of key

trends in the

Canadian Private

Equity Market in

2001

RESEARCHCONDUCTED BY

THE GOODMAN AND CARR LLP

REPORT ON THE CANADIAN

PRIVATE EQUITY

MARKET IN 2001

An in-depth

review of key

trends in the

Canadian Private

Equity Market in

2001

RESEARCHCONDUCTED BY

- 1 -

CANADA’S PRIVATE EQUITY MARKET IN 2001

Introduction

This report, prepared for Goodman and Carr LLP, documents current trends in Canadianprivate equity market, including buyout activity, mezzanine financing and venture capital. Dataanalyzed for the purposes of this report were drawn from The Private Equity Activity Survey,designed by Macdonald & Associates Ltd, and conducted by them over the period August-September, 2001. The format and analytical framework of the report are consistent with thoseissued by Macdonald & Associates in the past.

***

Canada’s private equity market, characterized chiefly by activity in three distinct marketsegments – buyout and related corporate finance, mezzanine investment and venture capital –experienced major growth and diversification over the course of the 1990s, which has included asteady increase in the number of national and local investor groups and funds, as well as the sizeof capital pools managed by them.

Since the late 1980s, multiple factors have contributed to this growth. One influence, ofcourse, has been mounting demand for risk financing, from established middle market firms, inthe case of buyout/mezzanine activity, and from emerging technology firms, in the case ofventure capital. Another variable has been changes to the organization and structure of thefinancial system, as well as government regulation of that system, which has greatly facilitatedsupply. Still another has been the proximity of massive and highly sophisticated private equitymarkets in the United States, fueled by an ever-expanding volume of assets from institutionalinvestors (i.e., pension funds, insurance companies, endowments/foundations, etc.).

Due to its identification with fast-growing technology sectors in the national economy,venture financing perhaps enjoys the highest profile of the three market segments. Suchfinancing is typified by an investor focus on company movement along a growth path, from start-up and early stage development to expansion, culminating in public offering or acquisition by alarger business entity, among other outcomes. To bring young firms to this point, investorscommonly inject round after round of financing, often in strategic syndication with others, andgive entrepreneurs access to management expertise, networks and other resources.

For 16 years, Macdonald & Associates has tracked Canada’s venture capital industry,reporting capital under management totaling $18.9 billion at the beginning of 2001. Last year,the industry enjoyed record-breaking activity, with disbursements of $6.6 billion.

- 2 -

Buyout and related types of corporate investment experienced a sea change in the pastdecade. In contrast with the leveraged buyout craze of the 1980s, buyout transactions in amodern context are often equity-based, with investors pursuing a value-adding strategy that helpsbusinesses meet their goals. Buyout activity targets mature firms, typically situated in suchtraditional sectors as manufacturing and services, that are addressing a particular “event”, such asa significant management change, an inter-generational transfer of ownership, acquisition of – ormerger with – another corporate entity, expansion, divestiture of product divisions, or a situationof financial distress.

Generally speaking, mezzanine financing is conducted in the same middle market territory asbuyout activity. However, the former is distinguished by the financial instrument utilized, withsubordinated debt occupying an integral position in certain event transactions, alongside equityor, in some instances, acting as a viable alternative to equity. Consequently, mezzanine investorgroups are highly specialized and frequently organized in dedicated pools.

***

The Private Equity Activity Survey was sent out to major private equity investor groupslocated predominantly in Ontario and Quebec, representing a balance of buyout, mezzanine andventure investment mandates, as well as the lion’s share of assets and deal activity in nationalmarkets as a whole. In all, 62 investor groups were contacted, with 48 (or 77%) responding withcompleted survey questionnaires over the period of issue. These respondents provided data forover 85 funds.

The survey sought to obtain data pertinent to the operational mandate of investor groups and,where relevant, the essential characteristics of specific funds within these groups, includingcapital under management, sources of capital supply, investment objectives and portfolioholdings. For groups/funds that raise capital from external sources, questions were also posedconcerning the terms and conditions of limited partnerships.

The Private Equity Activity Survey represents a useful early effort in describing the fulluniverse of Canadian private equity investing. In so doing, it has gathered much original datathat have heretofore been unavailable to industry professionals, agents and informed observers.To assist analysis of these data, Macdonald & Associates has provided a broad methodologicalframework that is comparable to recognized market parameters in the United States. This said, itis important to note that the first-time nature of this exercise, plus the limited sample on which itis grounded, prevent an in-depth understanding of the current state of the national private equitymarket. For this reason, readers of this report should view survey findings as a first step in thisdirection.

- 3 -

(I.I) Size and Dimensions of Canada’s Private Equity Marketin 2001

CANADIAN PRIVATE EQUITY MARKET ON THE RISE

By focusing on many of the largest investor groups and funds with headquarters or asignificant presence in Ontario and Quebec, The Private Equity Activity Survey was able tocapture a sizeable proportion of the private equity market universe in Canada. Taken together,surveyed fund assets were a whopping $23.5 billion.

By a small margin, the biggest share of this dollar amount was held by funds residing in theventure capital market: $10.8 billion, or 46% of the aggregate. The second largest share – $10.1billion, or 43% of the total – was held by funds concentrating on buyout and related corporatefinance activity. The balance, or $2.6 billion and 11% of the pool overall, was situated in fundsspecializing in mezzanine investment.

According to Macdonald & Associates, the survey’s venture capital portion accounts for justover half of total capital under management by the industry, nationwide, which stood at $18.9billion at the beginning of 2001. It is estimated that there are more than 150 groups in Canadamanaging funds with a dedicated mandate for venture financing.

Total Private Equity Capital Under Management By Survey Respondents By Market Segment, 2001

46%

43%

11%

Venture Capital Buy-Out/Corporate Finance Mezzanine Capital

$23.5 Billion

© 2001 Macdonald & Associates Limited. All rights reserved.

- 4 -

As there have been no published estimates of the magnitude of Canadian buyout andmezzanine activity prior to now, it is impossible to state precisely what proportion has beencaptured by the survey. However, Macdonald & Associates estimates that buyout andmezzanine capital under management totals well in excess of $17 billion, nationwide. It isfurther estimated that between 40-45 investor groups have funds with dedicated buyoutmandates, or with significant exposure to the buyout market. Working in the same environmentare an estimated 25-30 investor groups with dedicated mezzanine pools, or pools with somefocus on such activity.

When actual venture capital resources and actual/estimated buyout and mezzanine resourcesare added, the estimated size of the Canadian private equity market in aggregate is shown to be atleast $36 billion in 2001. This compares against the American private equity market, the capitalunder management of which has been estimated at over $680 billion (US dollars) in the sameyear.

These statistics point to remarkable growth and development in Canada’s private equitymarkets – from a nascent period in the 1980s, when private equity activity was limited in massand scope and largely undifferentiated regarding its business targets, through the 1990s, when asteady increase in the number of Canadian-based investor groups and funds was accompanied byheightened market specialization. As in the United States, time and experience led to the threefairly distinct market segments identified here.

Further data taken from the survey suggest that much of this market growth occurred veryrecently, as a great number of funds polled saw inception in the period 2000-2001. In thebuyout/mezzanine arena, some the newest (and largest) funds include Borealis Private Equity,CCFL Subordinated Debt Fund III, Clairvest Equity Partners, Kilmer Capital Fund, NB CapitalMezzanine Partners II, ONCAP, RBC Capital Partners Mezzanine Fund, Schroders CanadianBuyout Fund II, TD Canadian Private Equity Partners and the Tricap Restructuring Fund. Inventure financing, examples include Borealis Financial Technology Fund, Brightspark Ventures,Celtic House Fund II, Skypoint Telecom Fund II, the latest Technocap Fund, VenGrowthInvestment Fund V, Ventures West VII and the Working Ventures Technology Fund. Inaddition, the new Novacap II features both buyout and venture sides to its mandate.

This accelerated spurt in new fund formation is confirmed by Macdonald & Associates in theventure capital industry, which witnessed particularly large inflows of new resources between1999 and 2000, with the national pool expanding by 56%.

- 5 -

(I.II) Capital Under Management by Investor Type

STRUCTURE OF CANADIAN PE FUNDS DIVERSE

In the United States, private independent funds – based predominantly on the limitedpartnership model – dominate private equity markets, accounting for close to 80% of buyout,mezzanine and venture investment. Canadian markets are very differently structured. Despitethe critical importance of private funds in this country, they reflect a comparatively smaller shareof capital under management. This is the case for several reasons, not the least of which is therestricted exposure of Canadian pension funds and other institutional investors to private equityas an asset class.

Resources managed by private independents responding to the survey totaled $9.0 billion, or38% of aggregate capital under management. Such funds have been fully active across thespectrum since the earliest days of private equity in Canada, evident in the activity of suchveterans as CAI Capital Group, CCFL, McKenna Gale Capital, Penfund and Schroders &Associates in buyout and mezzanine markets and McLean Watson, Novacap, Quorum FundingCorporation, Technocap, VenGrowth Capital Partners and Ventures West Management inventure financing.

Private Equity Capital Under Management of Survey Respondents By Investor Type, 2001

18%

3%

14%

27%

38%

Corporate Government Institutional LSVCC Private Independent

$23.5 Billion© 2001 Macdonald & Associates Limited. All rights reserved.

- 6 -

Since 1997, Macdonald & Associates has reported some renewal in commitments of pensionfund and other institutional capital to limited partnerships in the venture capital realm. Thistrend has also led to a modest proliferation of new buyout funds in the past couple of years.

Beginning in 1983, labour-sponsored venture capital corporations (LSVCCs) have beenestablished by federal and provincial government statutes and tax credits on a national basis, andin eight out of ten provinces, to fill a perceived gap in the supply of risk financing. Today, thereare approximately two dozen LSVCCs in existence, including the Canadian Science andTechnology Growth Fund, CI Covington Fund, First Ontario, Fonds de solidarite des travailleursdu Quebec (FTQ) and Working Ventures Canadian Fund.

The LSVCCs responding to the survey manage $6.4 billion, or 27% of private equityresources represented by the survey as a whole. The primary venue for LSVCC investing is theventure capital market, where they are currently responsible for 39% of all national resources,according to Macdonald & Associates.

Representing 18% of the total pool described by the survey, or $4.1 billion, corporateinvestor groups – or the subsidiaries of major Canadian financial and industrial corporations –assumed a highly influential position in private equity markets during the past decade. By acountry mile, corporate-financials represent the most sizeable component of these groups andare, in turn, dominated by the country’s largest banks.

Since the restructuring of the banking sector in the 1980s, which included new freedoms andstrictures offered by government regulatory changes, corporate-financials have graduallyestablished a comprehensive presence in all three market segments – buyout, mezzanine andventure capital – though strategic emphasis of these differs among them. Today, nearly all ofCanada’s leading banks and non-bank financial institutions have a stake in private equity, led bysuch subsidiary operations as BMO Nesbitt Burns (and BMO Capital Corporation), HSBCCapital, RBC Capital Partners, Scotia Merchant Capital Corporation (and Scotia-owned Roynat)and TD Capital.

Along with private independent funds, corporate-financials have become especiallyinfluential as drivers of the recent expansion in new Canadian buyout pools. Indeed, thesegroups are converging – for instance, in the launching of TD Canadian Private Equity Partners.

Corporate-industrial funds are more prominent in venture financing, as these funds typicallyhave a dual interest in returns and having a strategic window on up-and-coming products andcompanies in technology sectors. Two high profile examples of this trend in Canada are BCECapital and the venture arm of Telesystem.

- 7 -

In American private equity markets, the involvement of pension funds, insurance companiesand other institutional investors is predominantly facilitated by limited partnerships and relatedvehicles. In Canada, several large institutional investors, such as Manulife, OMERS and OntarioTeachers PPB, have taken the unique step of hiring in-house teams of senior private equityprofessionals who conduct a significant portion of their overall activity on a direct basis. Likebank subsidiaries, the internally directed activity of such institutional investors is frequently feltright across the three market segments.

Because of the sheer volume of assets allocated to direct institutional investment, suchgroups have very recently emerged as a powerful force in buyout, mezzanine and ventureinvestment in Canada, accounting for $3.2 billion, or 14% of total capital under management inthis survey.

Government-owned investor groups usually undertake investments that might not otherwisebe made in private equity markets, such as small deals or activity located in rural or remotecommunities and regions of the country. This is the rationale behind the integral role of theBusiness Development Bank of Canada in mezzanine and venture capital markets, as well as thatof Innovatech du Grand Montreal in Quebec. This survey found government funds accountingfor 3% of capital under management, or $810 million.

- 8 -

(I.III) Capital Supply of Private Equity Funds

INSTITUTIONS AND INDIVIDUALS KEY TO PE SUPPLY

Despite the fact that Canadian pension funds make significantly fewer capital commitmentsto private equity markets, as compared to their counterparts in the United States, they remain acrucial supply source in this country. Indeed, according to this survey, pension funds wereresponsible for $7.0 billion of the supply to buyout, mezzanine and venture investment, or 30%of aggregate amounts contributed. These dollar totals take into account the commitments ofpension funds to limited partnerships and other externally managed vehicles, as well as in-houseallocations to direct investment activity.

It should be noted that the bulk of pension fund resources flowing to private equity can beattributed to a small handful of public sector organizations, among the largest of which are theBritish Columbia Investment Management Corporation, Hospitals of Ontario Pension Plan,OMERS, Ontario Teachers PPB and Quebec’s CDP Capital. Several new entrants to privateequity markets, such as CPP Investment Board, may substantially increase the supply role ofpension funds in the near future.

Capital Supply for Private Equity Survey RespondentsBy Source, 2001

$23.5 Billion© 2001 Macdonald & Associates Limited. All rights reserved.

30%

5%

25%

32%

4% 1% 3%

Pension Insurance Corporations Individual Government Foreign Other

- 9 -

Like pension funds, insurance companies constitute a key source of private equity supply inthe United States, a situation that is not comparably reflected in Canada, despite the activemarket engagement of such groups as Clarica Life Insurance Company and Manulife Capital.Nonetheless, insurance companies accounted for $1.2 billion of the commitments supportingbuyout, mezzanine and venture capital industries, or 5% of the total. As in the case of pensionfunds, this share captures both direct and indirect investment activity.

Interestingly, the supply levels of pension funds and insurance companies, as described inthis survey, surpass those that are typically attributed to them by Macdonald & Associates forventure financing. This suggests, as will be expected, that these institutional investors preferbuyout and mezzanine investing, chiefly because the latter are associated with larger funds andlarger transactions, shorter investment horizons, and less perceived risk, among other factors.

In what is a sharp contrast between Canadian and American private equity markets withrespect to capital supply infrastructure, individual investors occupy an especially importantposition in this country, representing $7.5 billion or 32% of aggregate sources, as determined byrespondents to this survey.

There are two essential components to the individual investor category in Canadian supplyconditions. The first is the literally hundreds of thousands of Canadian individuals that ownshares in LSVCCs. Indeed, with the use of government tax incentives, LSVCCs havedemonstrated a remarkably potent capacity for raising capital on a retail basis, ensuring thatindividuals leveraged 55% of all new commitments to the venture capital industry alone in 2000,according to Macdonald & Associates. The second component is high net worth individuals – insome instances, angel investors – seeking participation in corporate and private independentfunds. A high profile illustration in venture financing is the privately backed Celtic House.

Based on survey responses, major Canadian financial and industrial corporations contributed$5.8 billion to the dollar value of buyout, mezzanine and venture capital funds, or one-quarter ofamounts recorded overall. The lion’s share of this supply constitutes the internal allocations ofcorporations to their private equity subsidiaries. In addition, several banks and non-bankfinancial institutions are pivotal to the capitalization of numerous limited partnerships.

As well as backing their own venture and/or mezzanine divisions, Canadian governmentsalso provide resources to some private independent funds. The survey found over $1.0 billion ingovernment-sourced capital supply, or 4% of the aggregate.

As private equity increasingly becomes cross-border in nature, American and other foreigninvestors will more regularly form a vital part of limited partnership supply. Survey respondentsreported $291 million from this source, or 1% of the whole.

Other capital sources identified in the survey, totaling $758 million and 3% of all privateequity suppliers, comprise a diverse category. Much of this amount was simply undisclosed,with the balance made up by the contributions of general partners to funds managed by them,other institutional sources, etc.

- 10 -

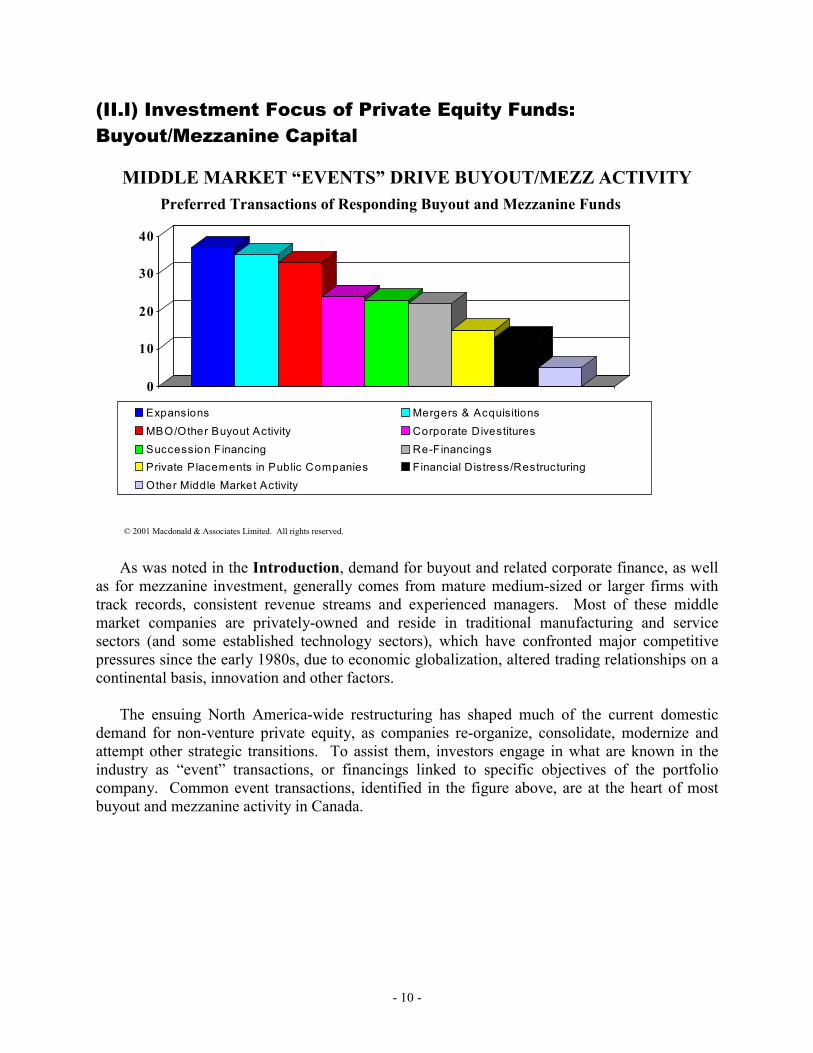

(II.I) Investment Focus of Private Equity Funds:Buyout/Mezzanine Capital

MIDDLE MARKET “EVENTS” DRIVE BUYOUT/MEZZ ACTIVITY

As was noted in the Introduction, demand for buyout and related corporate finance, as wellas for mezzanine investment, generally comes from mature medium-sized or larger firms withtrack records, consistent revenue streams and experienced managers. Most of these middlemarket companies are privately-owned and reside in traditional manufacturing and servicesectors (and some established technology sectors), which have confronted major competitivepressures since the early 1980s, due to economic globalization, altered trading relationships on acontinental basis, innovation and other factors.

The ensuing North America-wide restructuring has shaped much of the current domesticdemand for non-venture private equity, as companies re-organize, consolidate, modernize andattempt other strategic transitions. To assist them, investors engage in what are known in theindustry as “event” transactions, or financings linked to specific objectives of the portfoliocompany. Common event transactions, identified in the figure above, are at the heart of mostbuyout and mezzanine activity in Canada.

Preferred Transactions of Responding Buyout and Mezzanine Funds

0

10

20

30

40

Expansions Mergers & AcquisitionsMBO/Other Buyout Activity Corporate DivestituresSuccession Financing Re-FinancingsPrivate Placements in Public Companies Financial Distress/RestructuringOther Middle Market Activity

© 2001 Macdonald & Associates Limited. All rights reserved.

- 11 -

Of buyout and mezzanine investor groups/funds responding to the survey, over 80%identified three types of transactions that are key to their mandates: medium-sized/large companyexpansions, mergers/acquisitions and management buyout-outs (MBOs), along with other typesof buyouts. These results are consistent with research attesting to increasing middle marketdemand for expansion/buyout capital and the rising rate of mergers and acquisitions, amongother trends in both Canada and the United States.

Weighted almost as heavily were corporate divestitures, which have also been in growthmode since the late 1980s, succession financing, which is vital to a growing number of family-owned businesses started in the postwar years (and that seek to transfer ownership to youngergenerations), and company re-financings.

Somewhat less priority was given to investment in publicly listed firms, which may involveso-called “orphans” or deal making that is too complex or cumbersome to be handled inexchanges. This was also the case with transactions emphasizing financial distress, restructuringor turnaround.

Despite some of the differences in survey ratings, what stands out is the relatively equal meritgiven to most event transactions by respondents. This suggests that most Canadian buyout andmezzanine investor groups/funds are pursuing a “balanced” strategy and are not as yet asspecialized as their counterparts in the United States. There, an exclusive focus on core activityis quite common. This conclusion vis-à-vis the Canadian situation was confirmed in interviewsconducted prior to the release of The Private Equity Activity Survey, with buyout/mezzanineprofessionals arguing that domestic deal opportunities were too few, and the market too under-developed, to permit extensive specialization at this juncture.

However, notable exceptions to this general rule have emerged very recently. Examples ofspecialized approaches include the Shotgun Fund and Succession Fund of Argosy Partners, theTricap Restructuring Fund, which focuses on under-performing companies that requirecomprehensive restructuring plans, and several sector-specific funds, such as those managed byRBC Capital Partners and TD Capital.

Buyout/mezzanine professionals interviewed prior to the survey’s issue also noted thatpreferred investment size was probably the more appropriate measure of market distinctions atthe present time. This observation was also borne out in the data.

The average preferred investments of responding buyout/mezzanine funds ranged between$10 million and $50 million. However, certain groups – such as some corporate investor groupsand institutional investors – clearly favoured the upper end of the financing spectrum (e.g., $20-75 million and above), while private independent funds were more inclined towards the low end(e.g., $5-20 million, with many fund ranges below the $10 million level, especially in themezzanine segment).

- 12 -

(II.II) Investment Focus of Private Equity Funds: VentureCapital

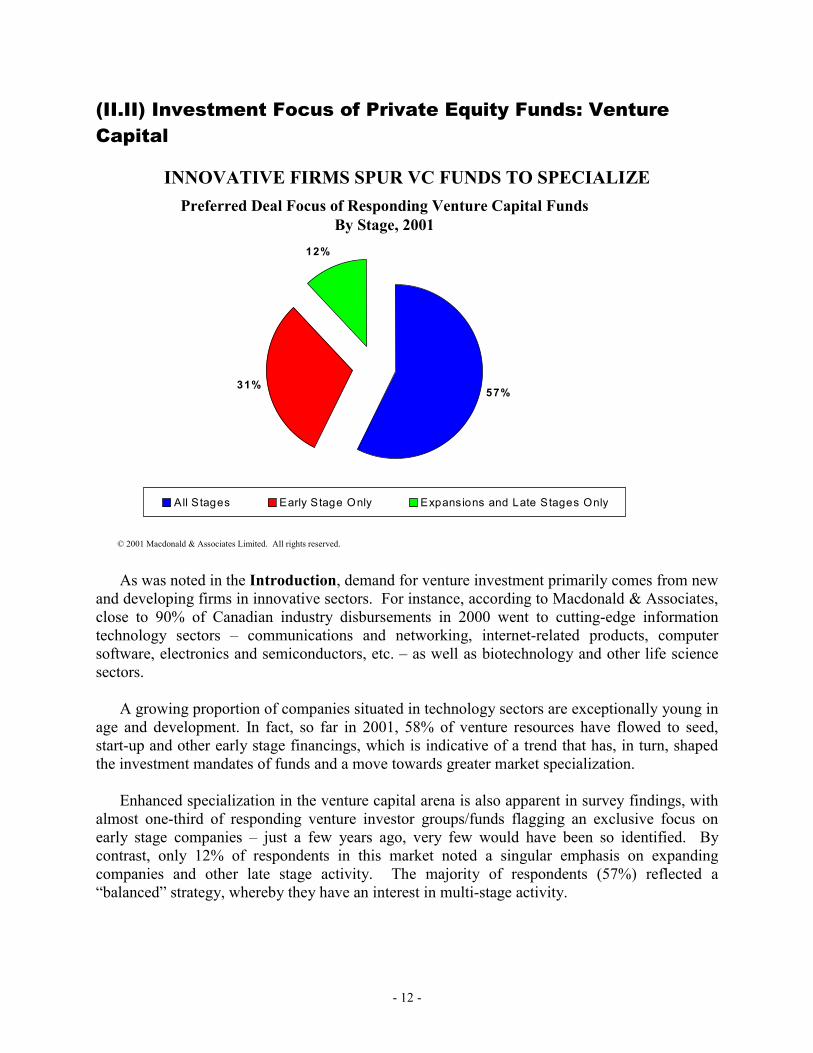

INNOVATIVE FIRMS SPUR VC FUNDS TO SPECIALIZE

As was noted in the Introduction, demand for venture investment primarily comes from newand developing firms in innovative sectors. For instance, according to Macdonald & Associates,close to 90% of Canadian industry disbursements in 2000 went to cutting-edge informationtechnology sectors – communications and networking, internet-related products, computersoftware, electronics and semiconductors, etc. – as well as biotechnology and other life sciencesectors.

A growing proportion of companies situated in technology sectors are exceptionally young inage and development. In fact, so far in 2001, 58% of venture resources have flowed to seed,start-up and other early stage financings, which is indicative of a trend that has, in turn, shapedthe investment mandates of funds and a move towards greater market specialization.

Enhanced specialization in the venture capital arena is also apparent in survey findings, withalmost one-third of responding venture investor groups/funds flagging an exclusive focus onearly stage companies – just a few years ago, very few would have been so identified. Bycontrast, only 12% of respondents in this market noted a singular emphasis on expandingcompanies and other late stage activity. The majority of respondents (57%) reflected a“balanced” strategy, whereby they have an interest in multi-stage activity.

Preferred Deal Focus of Responding Venture Capital Funds By Stage, 2001

57%31%

12%

All Stages Early Stage Only Expansions and Late Stages Only

© 2001 Macdonald & Associates Limited. All rights reserved.

- 13 -

This degree of attention paid to the early stage end of the investment spectrum is illustratedby the recent rise in seed financing, or financing of the initial commercialization of laboratoryresearch and technical innovation. Prior to the late 1990s, seed deals were almost unheard of,however, they are now a substantial fraction of industry activity (4% of disbursements in 2000),as groups like Brightspark and Ventures West Management have gained expertise in this field.

Another measure of specialization is the increased propensity of investor groups/funds toadopt sector-specific mandates. This is a key aspect of industry evolution, as the diversity andcomplexity of new technology products require more focused expertise among ventureprofessionals. Examples abound among the respondents to the survey, including Celtic House(communications and electronics), Skypoint Capital Corporation (communications and computersoftware), RBC Capital Partners’ Life Science Fund and XDL Intervest Capital Corporation(communications and internet-related products).

Not surprisingly, preferred investment sizes among venture capital industry respondentsranged far below those on the buyout and mezzanine sides of private equity. The averagecaptured by this survey was between $3 million to $8 million. Venture investment ranges werealmost uniformly below the $10 million dollar mark, with only a handful of funds expressingpreferences for a maximum level of $20 million. It is worth noting however, that venturefinancing is more likely to be syndicated, with larger deals often attracting four or five differentinvestors.

- 14 -

(II.III) Investment Activity of Private Equity Funds: Portfolios

PE DISBURSEMENTS EXPERIENCING GROWTH

Of all the data collected by The Private Equity Activity Survey, those pertaining to portfoliosand recent transactional activity and disbursements of buyout, mezzanine and venture investorgroups/funds were the least robust. This is because a substantial fraction of respondents viewedsuch information as too sensitive and proprietary, and much of the data provided wereincomplete. In addition, some very major funds, established only in recent months, are not yetactively investing. As a consequence, the statistics compiled here, though representative andimportant as a snapshot of trends in private equity investment and portfolio holdings, understatewhat is actually taking place overall.

In total, approximately three-quarters of responses to the survey gave full or partialinformation about their market activity to date, with their existing investment portfolios holding1,981 companies. The current at-cost value of these portfolios in aggregate is estimated to be$11.7 billion.

Buyout portfolios held 319 companies of this total, while mezzanine portfolios featured 451firms. As was mentioned previously, these typically are well-established, middle marketbusinesses. Survey responses confirmed this fact, with those from the buyout/mezzanine realmmost frequently citing the range $10-100 million as an appropriate level of annual sales, and atleast 5 years of operation as an appropriate age, for a company first entering a portfolio. Asignificant minority of respondents had a higher minimum threshold for sales (e.g., $25-50million).

Private Equity Disbursements of Respondents2000 – Q2, 2001

$0

$500

$1,000

$1,500

$2,000

$2,500

$3,000

2000 Q2, 2001

Buy-Out Mezzanine Venture Capital

$2.8 Billion $1.8 Billion

© 2001 Macdonald & Associates Limited. All rights reserved.

- 15 -

Venture portfolios held 1,210 companies of the total. As was also noted earlier, these areoften fledgling technology companies, without a history of profitability. For this reason, veryfew venture investor groups/funds specified preferred characteristics with regard to revenues orage for target investments. Those functioning with a threshold suggested a minimum of $1million in annual sales and one year of operation.

The rate of capital invested across the Canadian private equity spectrum appears to havegained considerable momentum in the past couple of years, which is in line with the recent rateof new fund formation. Disbursements by responding investor groups/funds stood at $2.8 billionin 2000, with venture capital leading at 62% of the total, followed by buyout activity at 27%mezzanine financing at 11%.

Despite volatility in public markets and an uncertain economic climate, capital flows appearto be as strong, or even stronger, in 2001, with respondents perhaps finishing the year at over $3billion, though amounts invested to date may be heavily influenced by a small number ofexceptionally large buyout transactions in the first six months.

Generally consistent with these findings, Macdonald & Associates has recently reportedsizeable deployments by the entire venture capital industry, including $6.6 billion invested acrossthe country in 2000. Thus far in 2001, capital invested has remained remarkably durable underthe circumstances, totaling $3.8 billion in the first nine months. In other words, the Canadianindustry continues to invest at 2000-like levels, unlike the industry in the United States, wheredisbursements this year have now fallen by more than 60% back to pre-1999 levels.

The bulk of the $4.5 billion disbursed during 2000-2001 by groups responding to the surveyshould find its way to Canadian companies. This statement is based on the expressed intentionof most respondents to invest primarily in this country (an estimated 72% of managed resources).This includes the vast majority of venture investors, which are traditionally active close to home– and, in particular, LSVCCs, which are legally required to do so – in contrast with buyoutinvestors, which frequently function with mandates that extend into North American and otherinternational spheres.

When it comes to deal making, roughly half of all respondents to the survey indicated apreference for syndication and assuming a lead among co-investors. The vast majority of thesewere venture investors – a trend that is increasingly evident in large financings in technologysectors. Less than 20% of respondents preferred co-investment on a more passive basis.

Close to half of buyout and mezzanine investor groups/funds signaled a strategy ofinfrequent syndication, which is quite common in non-venture private equity markets.

- 16 -

(II.IV) Investment Activity of Private Equity Funds: ExitStrategies and IRR Targets

When it comes to strategic plans for exiting investments and projecting returns at the time ofdispositions or fund liquidations, buyout, mezzanine and venture investors reveal key similaritiesand differences. Responding investor groups/funds to the survey provided important informationon these matters by indicating their anticipated timing for exits, and the typical nature of these, aswell as target returns, by fund and by transaction.

While investment duration is highly dependent on economic and market cycles, on average,respondents aimed to exit – or based on recent history, expected to exit – a portfolio companywithin 5-6 years, with few distinctions apparent between the three private equity segments.

When exits take place, most respondents (61%) hoped they would occur through companyacquisition by, or merger with, another business entity. Initial public offerings accounted forclose to one-fifth of anticipated exits, though this was largely driven by the responses of ventureinvestor groups/funds. Very few other exit opportunities were preferred, with the exception ofcompany buybacks, which represented somewhat less than 10% of the total.

Most private equity investor groups surveyed had established target rates of return (IRRs) ona per fund basis, while a sizeable fraction also had such benchmarks on a per transaction basis.Target IRRs by fund in the buyout and venture capital domains were largely comparable,typically ranging from 25% to 35% (though a minority of funds had higher and lowerbenchmarks). Where these existed, target IRRs by deal were more variable, but most tended tofall within the higher range of 30% to 40%.

Because they feature quasi-equity instruments (which include characteristics of debt),mezzanine investor groups indicated lower target IRRs for their activity, with these ranging from15% to 25% for projections per fund. Most funds used the upper end of this range (i.e., 20-25%)for benchmarks on a transactional basis.

- 17 -

(III) Limited Partnerships: Key Terms and Conditions

The terms and conditions of a limited partnership are vital to both limited partners (LPs) andgeneral partners (GPs) and can be the subject of intense discussion as the two sides hammer outagreements and negotiate issues over a partnership’s lifetime.

In interviews conducted prior to the release of The Private Equity Activity Survey, seniorfund managers expressed doubt about whether partnership terms were likely to vary substantiallyacross Canada – regardless of the private equity market segment. This view was borne out onmany items discussed by respondents to the survey. One of the reasons for this result is that LPsand GPs have apparently worked hard to advance their primary concerns. In so doing, they havesought to observe “best practices” recognized among management professionals and institutionalinvestors across North America on matters pertaining to fund management, organization andfinancial arrangements.

Like investment data, data relevant to partnership terms and conditions suffer somewhat fromreticence on the part of some investor groups/funds to share details of their operations, as well asthe limited sample on which the survey is grounded. Nonetheless, the survey findingssummarized below – derived from 45 Canadian private equity funds – do provide an interestingand informative sketch of this evolving business.

On the whole, this survey picked up relatively few differences between the essentialframeworks of funds residing in the buyout/corporate finance, mezzanine and venture capitalsegments of private equity investment. As key differences have been reported in much largerand more comprehensive treatments of this topic in the United States, including Key Terms andConditions for Private Equity Investing (William M. Mercer, 1996) and Private EquityPartnership Terms and Conditions (Asset Alternatives, 1999), it is likely this is due to Canada’ssmaller and still developing market.

The following findings on partnership terms and conditions are generally presented in theorder questions were asked on the survey questionnaire.

1. Practices in Fund Management/Organization

Limits on Fund Size

The vast majority of survey respondents (84%) indicated pre-established limits on the size oftheir private equity funds, though very few specific details were given. For the most part,upward limits were provided, with respondents pointing to the final levels at which funds closed,suggesting they had met their targets. A small handful of respondents noted the use of ranges todetermine the targeted size of funds, reflecting minimum and maximum parameters.

- 18 -

Life of the Partnership

Consistent with standard practice in American and Canadian private equity markets, theaverage lifetime of a partnership, according to survey respondents, was 10 years. Several fundsalso noted an option to extend terms, subject to the approval of the LPs (and sometimes at thediscretion of the GPs) for 2 years or more.

Investment Restrictions

Virtually all respondents to the survey identified restrictions of some type on the investmentactivity of a given fund.

The most commonly identified restriction referred to the percentage of fund capital investedin a single company in the portfolio. 45% of respondents cited 20-25% of total fund assets as thestandard limit in this regard, with other answers ranging widely, from as low as 10% to as highas 49.9%. Lower threshold levels were more typical in venture capital funds, while higher levelswere more typical in buyout funds.

Approximately one-third of respondents highlighted prohibitions on investment in particularsectors, such as real estate, natural resource extraction, the financial sector, gaming, etc. Severalventure capital funds also specifically ruled out non-technology sectors.

Other investment strictures were less frequently mentioned, but were clearly important toindividual funds. In the case of several buyout and mezzanine funds, there were prohibitions ontransactions involving start-up and other early stage companies in the domain of venture capital,while some venture capital funds excluded deals involving publicly listed firms. Other excludedactivity included particularly long investment horizons (e.g., 10 years) and investments in otherprivate equity funds.

Non-resident Participation

Over two-thirds of survey respondents (68%) indicated a policy enabling the participation ofnon-resident investors in fund activity. A common method for implementing this policy was theestablishment of parallel funds.

Co-investment Rights

Reflecting the strong and growing interest of many LPs to obtain rights of co-investmentalongside on-going fund activity, 82% of survey responses flagged this particular provision.

About one-fifth of respondents confirming the existence of co-investment features said theyextended these rights to all LPs – in some cases, at the discretion of the GPs. However, themajority specified that such rights exist only for “lead investors” or “significant limitedpartners” – in other words, LPs with very substantial equity stakes in funds (e.g., in excess of10% or 20% or total capital under management).

- 19 -

GP Co-investment Rights

Only 10% of survey respondents indicated the existence of rights to co-investmentopportunities for GPs and their affiliates (e.g., employees in a given investor group). Suchprovisions tended to be found where major corporate investor groups were thesponsors/managers of funds and, consequently, sought co-investment rights that approximatedtheir equity stake.

Post-expiry Capital Calls

Forty-six percent of survey respondents indicated that capital calls could be made followingthe expiry of the commitment period for specific uses, the most frequently cited beingcompletion of pre-determined investments, follow-on financings of existing portfolio companiesand significant expenses of the fund.

Re-investment of Capital Gains

A minority of survey respondents (32%) confirmed an ability to re-invest a given fund’scapital gains, usually within specified limits of time (i.e., only within the first 1 to 5 years of thepartnership’s term).

Advisory Committees

Eighty-four percent of survey respondents confirmed there was a formal advisory committeeattached to their funds.

According to respondents, committee functions tend to be chiefly input-oriented and relatedto broad matters of fund governance. These matters pertain to the resolution of conflicts ofinterest, changes to LP agreements, issues that were not covered by LP agreements, and thereview and approval of valuations, et al. Committees also act as forums for GP status reports tothe LPs, as well as other kinds of information sharing. They may also feature consultativediscussion of fund strategy, private equity market trends, potential deal opportunities, etc.,however, almost all respondents were clear that these bodies had no direct role in investmentdecision-making.

- 20 -

Key Person Provisions

To address LP concerns about a potential loss during the partnership’s term of managerspossessing essential skills and experience, the vast majority of survey respondents (77%) flaggedthe existence of key person provisions.

In general, key person provisions dealt with the possibility of turnover of certain namedindividuals in GP management groups or retention of a specific number of managers (e.g., one-fifth or one-half of the overall GP team), since the fund’s inception. Some funds specify an LPnotification process in the event of management turnover and “exceptional circumstances” ifturnover cannot be reasonably prevented.

Depending on the nature of the turnover, respondents identified several allowable actions onthe part of the LPs, including suspension of any further capital calls (beyond those alreadyadvanced) or termination of the fund. Another action may be postponement of any newinvestment activity until LPs agree on the replacements for lost managers.

Guidelines for Fund Wind-downs/Liquidations

Concerning the act of winding-down or liquidating funds, very little information wassupplied by respondents to the survey, with several stating they had no formal policy in place.

Those that did comment on this topic cited standard procedures in private equity marketswhereby GPs or their agents assume full responsibility for settling accounts and distributing allremaining cash proceeds and in-kind assets linked to the partnership at its termination date. Themanner and timeframe for this process are usually at the discretion of GPs, though somerespondents mentioned a requirement for input from LPs/Advisory Committees in certaincircumstances.

Defaulting LPs

Although examples of LPs defaulting when a capital call is made are considered fairly rare,79% of respondents to the survey identified policies and processes for handling such an event.

In general, GPs introduce penalties, such as forfeiture of the LP’s stake in the partnership oraccess to profits, as a means of discouraging defaults. Other legal actions may also be pursued.In addition, GPs look to fill the capital supply gap by offering all or part of the defaulting LPs’interest up for sale to other investors.

- 21 -

2. Financial Terms and Conditions

GP Capital Commitments

LPs are strongly interested in a GP equity stake in private equity funds – reflecting acommitment over and above their responsibilities as managers – as a way of more closingaligning interests between the two parties. It may not be surprising then to see that virtually allsurvey respondents indicated some level of GP capital commitment to their funds, usually withina range of 1-5%. A handful of respondents reported GP commitments that surpassed the 5%level.

Management Fees

Management fees were reported by all respondents to the survey, calculated as a percentageof total capital commitments in a given fund. The average fee was 2%, with only minor variancein some funds.

Investment-Related Fees

The extent to which portfolio firms were charged investment-related fees for such services asoriginating the transaction, monitoring company progress over time, and other kinds ofconsultation, etc., varied among surveyed funds. Only about one-third of respondents (34 %)observed this general practice and most of these were in the buyout/mezzanine fund segments ofprivate equity, as is commonly the case.

Organizational Expenses

Very few survey responses were given with respect to organizational expenses (e.g., travel,legal, accounting and other expenses), as a percentage of total fund size, often because thecalculation was infrequently made. Those responses that were obtained indicated organizationalexpenses to be 0.2%, on average. This is an interesting finding, as LPs in American privateequity markets are increasingly trying to gain insights into such expenses, and to control them.

- 22 -

Carried Interest

Almost universally, survey respondents indicated the rate of carried interest to GPs to be20%, which is, of course, standard practice in American and Canadian private equity markets.In a few funds, carried interest was directly linked to performance and could, as a consequence,vary by several percentage points, plus-or-minus, from the 20% standard. In this way, treatmentof carried interest complemented or replaced the use of preferred returns (see below) in thesefunds.

For reasons of confidentiality, most survey respondents declined to disclose the portion ofcarried interest that is held by, or is available to, fund managers.

Close to two-thirds of funds (64%) indicated a policy whereby carried interest was subject toclaw-back if judged too high relative to overall returns at the time of termination.

Preferred Returns

The large majority of survey respondents (79%) indicated having a preferred (or hurdle) rateof return that is generally available to the LPs prior to GP receipt of carried interest. Thepreferred rate differed from fund to fund (i.e., from a low of 5% to a high of 25%), with anaverage set return of 8%, on balance.

For the most part, the policy for LP distributions prior to GP receipt of carried interest –where it was articulated by survey respondents – is clearly linked to the delivery of preferredreturns and other essential items, such as return of original capital contributions, repayment offees, etc. A small number of respondents noted detailed schedules for making these minimumdistributions over the lifetime of the partnership.

Nature of LP Distributions

Survey responses provided little information about frequency of cash/in-kind distributions toLPs over the course of a fund’s term. Most respondents noted that major distributions weremade only when investments were fully matured, while shorter-term streams tended to comprisedividend, interest or fee income, et al, when realized. Some funds had schedules for distributions(i.e., annually, semi-annually, quarterly, and where divestments have occurred), whiledistributions in other funds were more at the discretion of GPs.

Placement Fees

Forty-one percent of survey respondents acknowledged incurring placement fees in theirfunds. GPs bore this expense in approximately 60% of the reported cases (with LPs assumingsuch costs in the others).

- 23 -

Fund Valuations

Valuation practices in private equity investing vary quite widely from fund to fund, with fewbroadly accepted guidelines in the industry. It is not surprising then that only 43% of surveyrespondents reported the existence of a clearly defined policy regarding the determination offund holding values. It is likely that such policies exist among other funds polled, however,several respondents were reluctant to disclose these for reasons of confidentiality.

Where guidelines were noted, illustrative details were restricted. Some funds rely on formalmethodologies established for evaluating privately owned assets, supplied by auditors, and asdescribed by the British Venture Capital Association or the National Venture Capital Association(in the United States). Others rely on recognized “best practices” in private equity markets inCanada and the United States, such as GP-LP agreement on fair value based on recent marketexperience, peer performance, benchmarks against public markets, and other credible financialtechniques. A reliable means for some fund managers is basing valuations on the last round offinancing in a portfolio firm that is conducted with the participation of a third party investor.Other approaches were also mentioned.

Fifty-seven percent of respondents indicated that fund valuations were performed by GPs –often subject, however, to the review of independent auditors, as well as LPs/AdvisoryCommittees – 20% indicated valuations were undertaken externally by independent auditingfirms, and the rest declined to answer.

- 24 -

Conclusion

It is evident from the findings of The Private Equity Activity Survey that the Canadianmarket is currently enjoying an unprecedented period of expansion and diversification, rooted inmounting business demand and improving supply conditions underlying the activity of privateindependent funds, corporate funds, LSVCCs and other major investor groups. These trends arebest documented for the venture capital industry; however, this survey indicates that the samemay be broadly asserted in the case of buyout and related corporate investment activity andmezzanine financing as well.

Nonetheless, all segments of the private equity market in Canada remain in an early phase ofgrowth, as compared to the United States, and are likely to encounter significant challenges inthe years ahead. Among the most critical to longer-term market development is a still reticentcommunity of Canadian pension funds, insurance companies, endowments/foundations and otherinstitutional investors, which largely remains uninformed about private equity as a viable andstrategically important asset class. This is no small point, as American institutional capitalinfusions over the 1990s effectively led dynamic market growth in that country and continuesuninterrupted today. It is difficult to imagine a comparable Canadian experience without thisinstitutionally sourced participation.

As was noted in the Introduction, this survey has been a major first step in describing thesize, scope and dimensions of Canada’s entire private equity universe. More work will berequired to flesh out the details of evolving market segments to give industry professionals,institutional investors, market intermediaries and observers the data and analysis they need toaddress challenges and monitor trends in capital supply, deal opportunities and investments overtime.

- 25 -

List of Respondents to The Private Equity Survey

Argosy PartnersBCE CapitalBusiness Development Bank of CanadaBMO Nesbitt BurnsBorealis Capital CorporationBrightspark VenturesCAI Capital GroupCCFL Mezzanine PartnersCanadian Science and Technology Growth FundCeltic House InternationalCovington CapitalClairvest GroupFirst Ontario Labour-sponsored Investment FundFonds de solidarité des travailleurs du Québec (FTQ)HSBC Capital (Canada)Innovatech du Grand MontrealJefferson Partners CapitalJL Albright Venture PartnersKilmer Capital PartnersManulife CapitalMcCarvill Mezzanine Financial CorporationMcKenna Gale CapitalMcLean Watson CapitalMiddlefield BancorpMM Venture Partners

MWI and Partners Merchant BankingNB Capital PartnersNovacap InvestmentsONCAP LPOntario Municipal Employees Retirement SystemOntario Teachers Pension Plan BoardOrchard Capital GroupPenfund ManagementPrimaxis Technology VenturesQuorum Funding CorporationRoynat MB I & CompanyRBC Capital PartnersScotia Merchant Capital CorporationSchroders and Associates CanadaSkypoint Capital CorporationTechnocapTelsoft VenturesTD CapitalTricap Restructuring FundVenGrowth Capital PartnersVentures West ManagementWorking Ventures Canadian FundXDL Intervest Capital