Private equity roundup is a quarterly newsletter on trends and perspectives related to private equity (PE) activity in India. In this edition Key economic indicators 3 Funds 5 Transactions and exits 6 Tax and regulatory updates 10 Outlook 16 which accounted for 54% of the total deal volume. Growth deals also contributed 39% of the total deal volume, but more importantly, increased by almost 50% compared to the previous quarter, possibly reflecting improving investor and corporate confidence. E-commerce, technology and real estate sectors were the most active, accounting for 60% of deal volumes and 55% of the total deal value during the quarter. Primafacie, the fundraising numbers were better than the last couple of quarters, but a significant part (79%) of successful fund closures was contributed by two main funds — Fairfax Holdings maiden India fund of US$1 billion and IVFA’s first close of its new fund, Indium-V, of US$500 million. There were 12 new fundraising plans announced, with half of these being venture capital (VC) funds, focused on early-stage investing. Foreword PE/VC investments were at US$3.4 billion in 1Q15, spread across 181 deals, as compared with US$4.8 billion across 125 deals in 4Q14. Though the aggregate deal value declined by 29% in 1Q15 compared to the previous quarter, the number of deals increased by 45% on the back of a spike in early-stage investments in e-commerce companies and higher growth-stage deal activity across a number of sectors, including real estate, financial services and technology. The quarter recorded 50 investments in early-stage e-commerce companies, compared to 20 in the previous quarter. There were six big-ticket deals (US$100 million or above) in 1Q15, aggregating around US$950 million, as compared with nine in 4Q14, aggregating US$2.8 billion. This led to a decrease in the total deal value and average deal size, which fell to US$22 million from US$45 million in the previous quarter. Deal volumes were driven by early-stage investments, 1Q 2015 Private equity roundup India

Transcript

Private equity roundup is a quarterly newsletter on trends and perspectives related to private equity (PE) activity in India

In this edition

Key economic indicators 3

Funds 5

Transactions and exits 6

Tax and regulatory updates 10

Outlook 16

which accounted for 54 of the total deal volume Growth deals also contributed 39 of the total deal volume but more importantly increased by almost 50 compared to the previous quarter possibly reflecting improving investor and corporate confidence E-commerce technology and real estate sectors were the most active accounting for 60 of deal volumes and 55 of the total deal value during the quarter

Primafacie the fundraising numbers were better than the last couple of quarters but a significant part (79) of successful fund closures was contributed by two main funds mdash Fairfax Holdings maiden India fund of US$1 billion and IVFArsquos first close of its new fund Indium-V of US$500 million There were 12 new fundraising plans announced with half of these being venture capital (VC) funds focused on early-stage investing

ForewordPEVC investments were at US$34 billion in 1Q15 spread across 181 deals as compared with US$48 billion across 125 deals in 4Q14 Though the aggregate deal value declined by 29 in 1Q15 compared to the previous quarter the number of deals increased by 45 on the back of a spike in early-stage investments in e-commerce companies and higher growth-stage deal activity across a number of sectors including real estate financial services and technology The quarter recorded 50 investments in early-stage e-commerce companies compared to 20 in the previous quarter There were six big-ticket deals (US$100 million or above) in 1Q15 aggregating around US$950 million as compared with nine in 4Q14 aggregating US$28 billion This led to a decrease in the total deal value and average deal size which fell to US$22 million from US$45 million in the previous quarter Deal volumes were driven by early-stage investments

1Q 2015

Private equity roundup India

2 | Private equity roundup mdash India

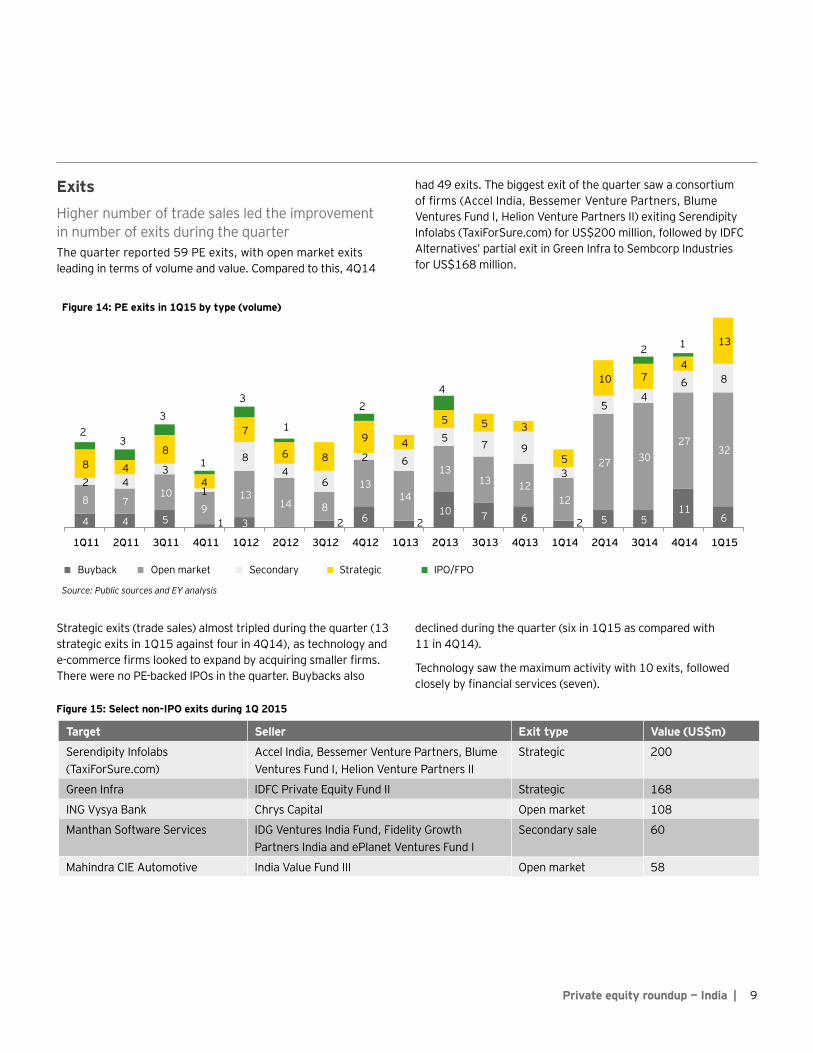

Exits through open market continued to dominate overall exits The quarter reported 59 exits out of which 32 were open market Strategic exits also improved (13 in 1Q15 compared to four in 4Q14) The biggest exit of the quarter saw consolidation in the online taxi operators where Taxiforsurecom (Serendipity Infolabs) was acquired by Olacabs (ANI Technologies) for US$200 million in a cash plus stock deal The PE investors in Taxiforsurecom (Accel India Bessemer Venture Partners Blume Ventures Helion Venture Partners) swapped their shareholding for a stake in ANI Technologies Pvt Ltd In terms of deal volumes the technology sector registered maximum exit activity

During the quarter the NDA Government presented its first full Union Budget Generally speaking the budget was forward looking and had positive intent It did have some positives for the PEVC industry but it could have done more to put at rest some of the long-standing concerns of the PEVC industry We have summarized some of the key budget changes that impact the PEVC industry in this document

3Private equity roundup mdash India |

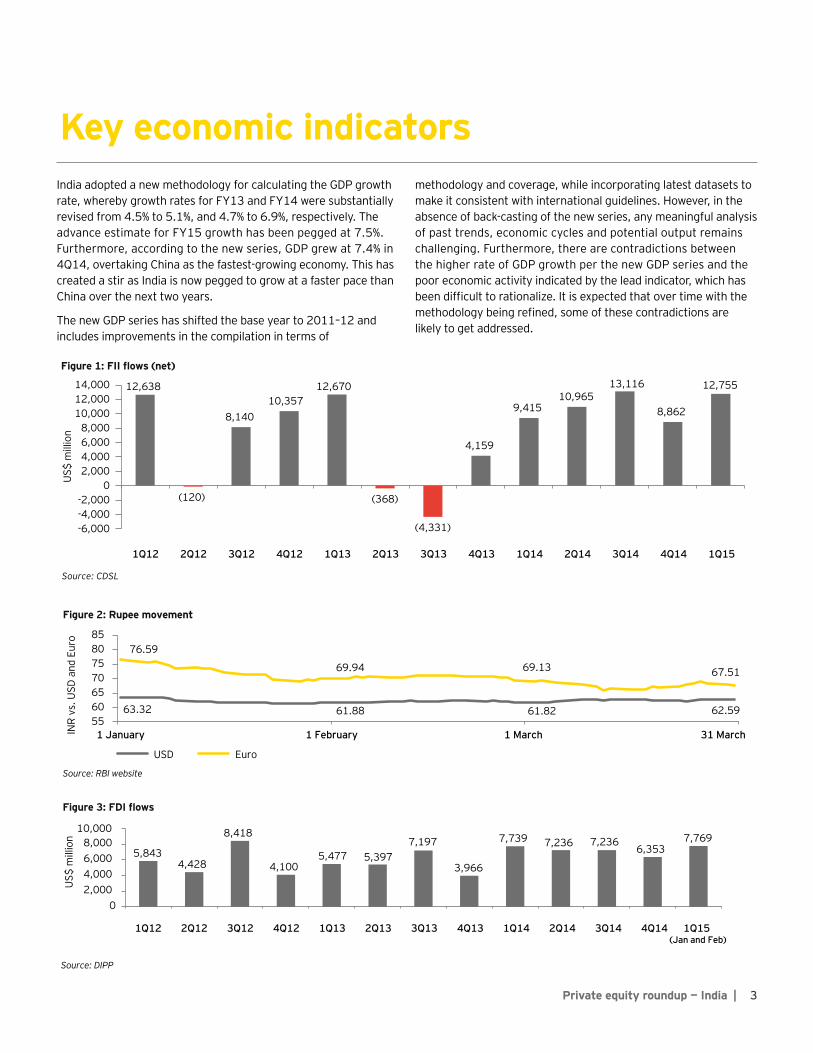

Key economic indicatorsIndia adopted a new methodology for calculating the GDP growth rate whereby growth rates for FY13 and FY14 were substantially revised from 45 to 51 and 47 to 69 respectively The advance estimate for FY15 growth has been pegged at 75 Furthermore according to the new series GDP grew at 74 in 4Q14 overtaking China as the fastest-growing economy This has created a stir as India is now pegged to grow at a faster pace than China over the next two years

The new GDP series has shifted the base year to 2011ndash12 and includes improvements in the compilation in terms of

methodology and coverage while incorporating latest datasets to make it consistent with international guidelines However in the absence of back-casting of the new series any meaningful analysis of past trends economic cycles and potential output remains challenging Furthermore there are contradictions between the higher rate of GDP growth per the new GDP series and the poor economic activity indicated by the lead indicator which has been difficult to rationalize It is expected that over time with the methodology being refined some of these contradictions are likely to get addressed

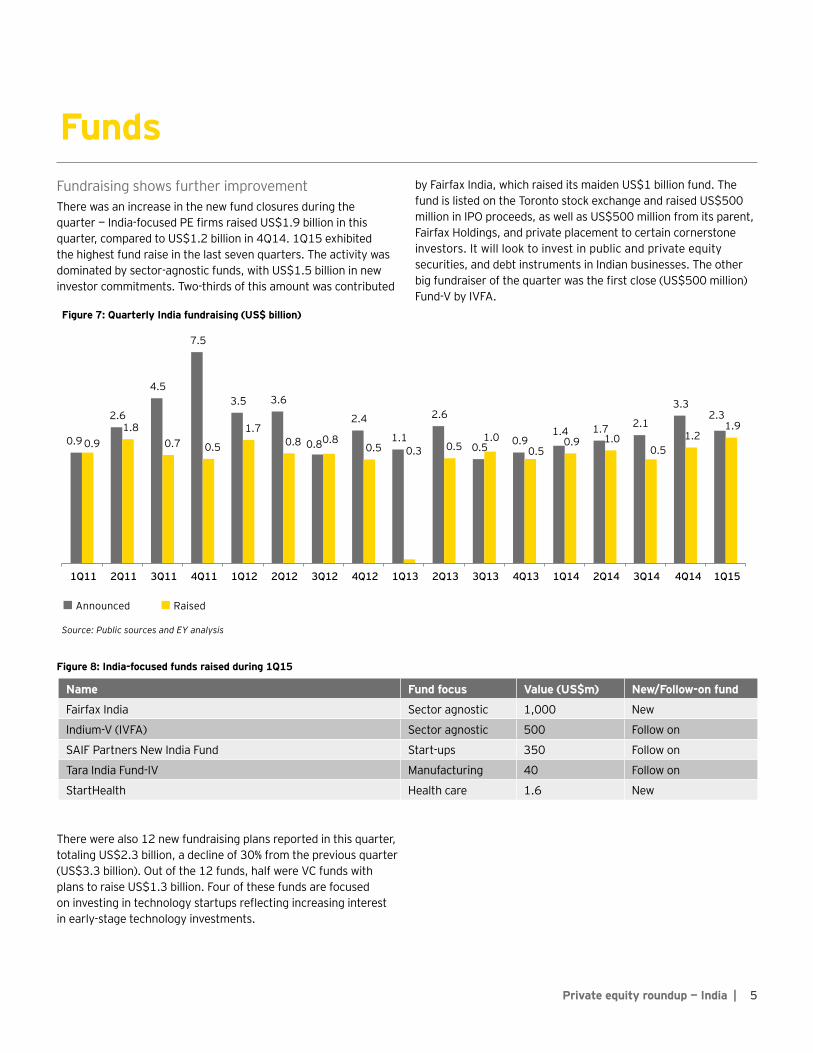

Fundraising shows further improvementThere was an increase in the new fund closures during the quarter mdash India-focused PE firms raised US$19 billion in this quarter compared to US$12 billion in 4Q14 1Q15 exhibited the highest fund raise in the last seven quarters The activity was dominated by sector-agnostic funds with US$15 billion in new investor commitments Two-thirds of this amount was contributed

by Fairfax India which raised its maiden US$1 billion fund The fund is listed on the Toronto stock exchange and raised US$500 million in IPO proceeds as well as US$500 million from its parent Fairfax Holdings and private placement to certain cornerstone investors It will look to invest in public and private equity securities and debt instruments in Indian businesses The other big fundraiser of the quarter was the first close (US$500 million) Fund-V by IVFA

Funds

Figure 7 Quarterly India fundraising (US$ billion)

SAIF Partners New India Fund Start-ups 350 Follow on

Tara India Fund-IV Manufacturing 40 Follow on

StartHealth Health care 16 New

There were also 12 new fundraising plans reported in this quarter totaling US$23 billion a decline of 30 from the previous quarter (US$33 billion) Out of the 12 funds half were VC funds with plans to raise US$13 billion Four of these funds are focused on investing in technology startups reflecting increasing interest in early-stage technology investments

Figure 8 India-focused funds raised during 1Q15

6 | Private equity roundup mdash India

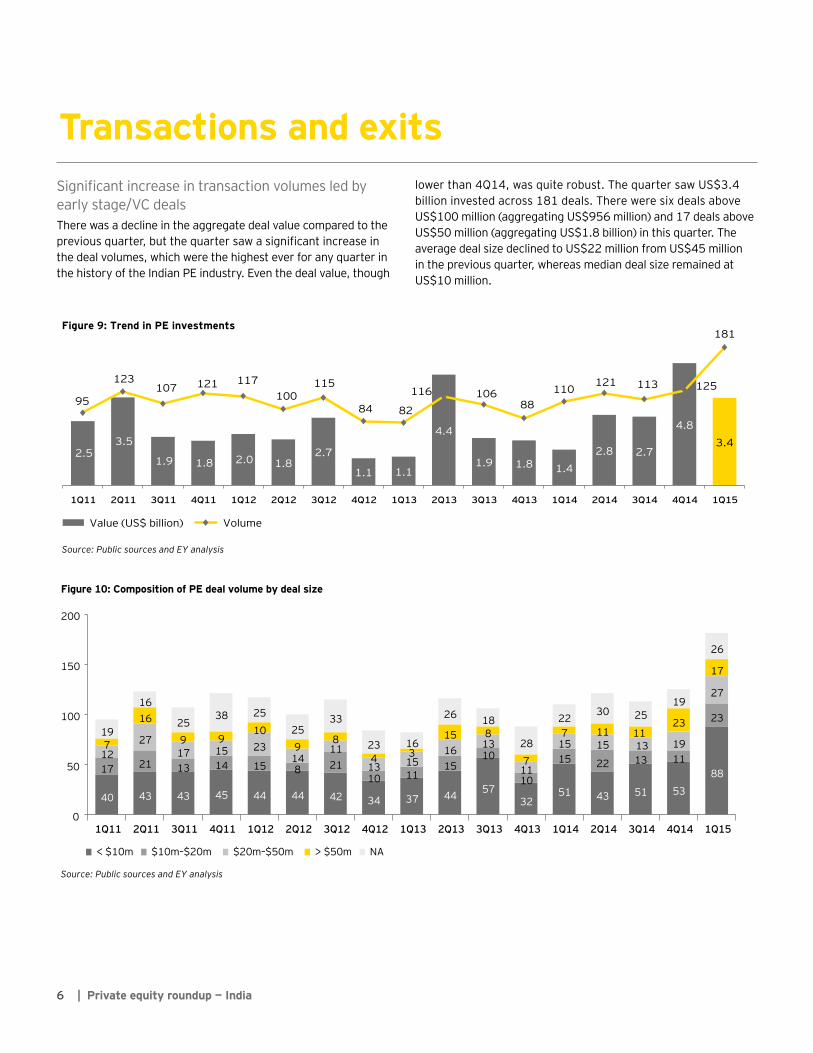

Transactions and exitsSignificant increase in transaction volumes led by early stageVC dealsThere was a decline in the aggregate deal value compared to the previous quarter but the quarter saw a significant increase in the deal volumes which were the highest ever for any quarter in the history of the Indian PE industry Even the deal value though

lower than 4Q14 was quite robust The quarter saw US$34 billion invested across 181 deals There were six deals above US$100 million (aggregating US$956 million) and 17 deals above US$50 million (aggregating US$18 billion) in this quarter The average deal size declined to US$22 million from US$45 million in the previous quarter whereas median deal size remained at US$10 million

Omkar Realtors and Developers Mumbai luxury project

Piramal Fund Management Real estate 191

Assetz Property and Homes Equis Fund Group Real estate 116

Clues Network (shopcluescom) Nexus India Capital Advisors Tiger Global Management Helion Venture Partners

E-commerce 100

Ujjivan Financial Services CDC Group CX Capital Management NewQuest Capital Partners

Financial services 96

Emaar MGF Land SSG Capital Management Real estate 96

Lodha Group Kotak Realty Fund Real estate 87

Diligent Power project IDFC Alternatives Power and utilities 81

Figure 11 Select PE investments in 1Q15

8 | Private equity roundup mdash India

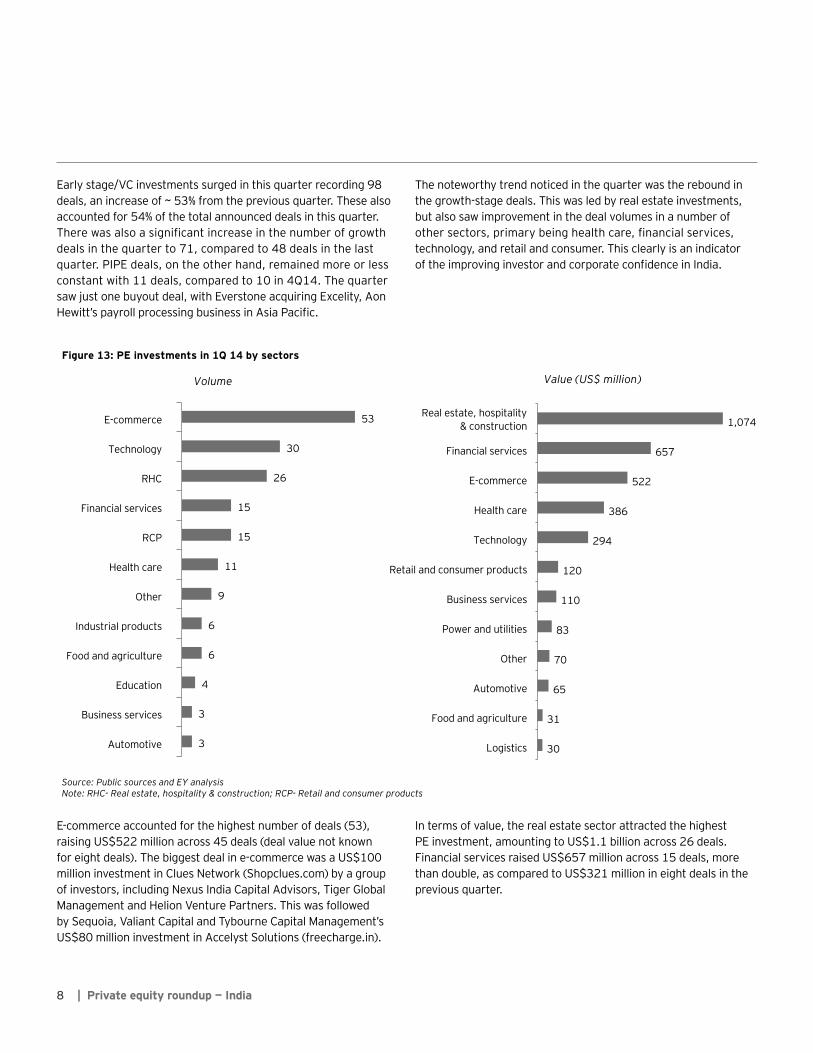

Early stageVC investments surged in this quarter recording 98 deals an increase of ~ 53 from the previous quarter These also accounted for 54 of the total announced deals in this quarter There was also a significant increase in the number of growth deals in the quarter to 71 compared to 48 deals in the last quarter PIPE deals on the other hand remained more or less constant with 11 deals compared to 10 in 4Q14 The quarter saw just one buyout deal with Everstone acquiring Excelity Aon Hewittrsquos payroll processing business in Asia Pacific

The noteworthy trend noticed in the quarter was the rebound in the growth-stage deals This was led by real estate investments but also saw improvement in the deal volumes in a number of other sectors primary being health care financial services technology and retail and consumer This clearly is an indicator of the improving investor and corporate confidence in India

Figure 13 PE investments in 1Q 14 by sectors

Source Public sources and EY analysisNote RHC- Real estate hospitality amp construction RCP- Retail and consumer products

Volume Value (US$ million)

3

3

4

6

6

9

11

15

15

26

30

53

Automotive

Business services

Education

Food and agriculture

Industrial products

Other

Health care

RCP

Financial services

RHC

Technology

E-commerce

30

31

65

70

83

110

120

294

386

522

657

1074

Logistics

Food and agriculture

Automotive

Other

Power and utilities

Business services

Retail and consumer products

Technology

Health care

E-commerce

Financial services

Real estate hospitality amp construction

E-commerce accounted for the highest number of deals (53) raising US$522 million across 45 deals (deal value not known for eight deals) The biggest deal in e-commerce was a US$100 million investment in Clues Network (Shopcluescom) by a group of investors including Nexus India Capital Advisors Tiger Global Management and Helion Venture Partners This was followed by Sequoia Valiant Capital and Tybourne Capital Managementrsquos US$80 million investment in Accelyst Solutions (freechargein)

In terms of value the real estate sector attracted the highest PE investment amounting to US$11 billion across 26 deals Financial services raised US$657 million across 15 deals more than double as compared to US$321 million in eight deals in the previous quarter

9Private equity roundup mdash India |

ExitsHigher number of trade sales led the improvement in number of exits during the quarterThe quarter reported 59 PE exits with open market exits leading in terms of volume and value Compared to this 4Q14

had 49 exits The biggest exit of the quarter saw a consortium of firms (Accel India Bessemer Venture Partners Blume Ventures Fund I Helion Venture Partners II) exiting Serendipity Infolabs (TaxiForSurecom) for US$200 million followed by IDFC Alternativesrsquo partial exit in Green Infra to Sembcorp Industries for US$168 million

Strategic exits (trade sales) almost tripled during the quarter (13 strategic exits in 1Q15 against four in 4Q14) as technology and e-commerce firms looked to expand by acquiring smaller firms There were no PE-backed IPOs in the quarter Buybacks also

declined during the quarter (six in 1Q15 as compared with 11 in 4Q14)

Technology saw the maximum activity with 10 exits followed closely by financial services (seven)

Target Seller Exit type Value (US$m)

Serendipity Infolabs (TaxiForSurecom)

Accel India Bessemer Venture Partners Blume Ventures Fund I Helion Venture Partners II

Strategic 200

Green Infra IDFC Private Equity Fund II Strategic 168

ING Vysya Bank Chrys Capital Open market 108

Manthan Software Services IDG Ventures India Fund Fidelity Growth Partners India and ePlanet Ventures Fund I

Secondary sale 60

Mahindra CIE Automotive India Value Fund III Open market 58

Figure 15 Select non-IPO exits during 1Q 2015

10 | Private equity roundup mdash India

Tax and regulatory updatesThe new Government presented its first full budget amidst great expectations from various stakeholders and paved the way for key tax and regulatory changes in 1Q15 In this edition we are pleased to bring you the key amendments brought about by Budget 2015 to the direct and indirect taxes and brief on the income computation and disclosure standards notified by the Government of India (Gol) We also touch upon regulatory updates such as RBIrsquos stand on deviation from pricing guidelines and some key amendments notifed by the Securities and Exchange Board of India (SEBI) in ldquoDelisting of Equity Shares Regulations 2009rdquo ldquoSubstantial Acquisition and Takeover Regulations 2011rdquo and ldquoBuy Back of Securities Regulations 1998rdquo

Tax updatesFinance Bill 2015The Finance Minister (FM) presented the Finance Bill 2015 (Bill) as part of the Union Budget 2015ndash16 before the Indian Parliament on 28 February 2015 The Bill contained a number of proposals to amend the Indian Tax Laws (ITLs) The FM then moved certain amendments to the Bill at the time of its debate before the Lok Sabha (the lower house of the Indian Parliament) and the Bill in its revised form (Revised Bill) was recently passed by both houses of Parliament The Revised Bill is now awaiting the assent of the President of India to become law We have summarized below the key amendments brought about by the Finance Bill 2015 (including amendments) relevant to the PEVC sector

1 Corporate tax rate to be brought down to 25

bull Basic corporate tax rate for Indian companies shall be reduced to 25 over the next four years and shall be accompanied by phased reduction in exemptions available to corporates

bull The basic corporate tax rate for FY15-16 remains unchanged at 30 However with the additional surcharge of 2 this could go up to 3461 for 2015-16

bull Similarly the dividend distribution tax and buyback tax would also increase due to the higher surcharge

2 Much awaited clarity in taxation on indirect transfer of Indian company shares

bull It is proposed that indirect transfer rules in India will be triggered only if the value of the Indian assets exceeds INR10 crores and represents at least 50 of the value of global operations transferred Valuation methodology for this will be separately prescribed

bull Specific exemptions have been provided for

a Amalgamationsdemergers being undertaken outside India and satisfying certain conditions (however tax neutrality for foreign shareholders of such amalgamating or demerged companies has not been discussed)

b Small shareholders holding less than 5 stake and not having management and control

bull It has also been clarified that the tax liability in India will be based on proportionate gains attributable to India vis-agrave-vis total gains

bull The issue of applicability of indirect transfer rules in multilayer investment structures and transfer of investorsrsquo interest (gt 5) in a fund structure remains unaddressed

bull These amendments will take effect from FY15-16

bull Separately the Central Board of Direct Taxes (CBDT) the apex administrative body for taxation in India issued Circular 4 of 2015 (dated 26 March 2015) clarifying that declaration of dividend outside India by a foreign company would not be taxable in India under the indirect transfer provisions of the Indian Tax Laws since such declaration and payment of dividend does not have an effect of transfer of any underlying asset located in India This is a welcome clarification from the CBDT and it addresses the concern which had risen on account of the wide scope of the indirect transfer provisions The CBDT Circular being clear in nature should apply to all pending cases

3 Applicability of GAAR (General Anti-Avoidance Rules deferred by two years

bull GAAR is proposed to be deferred by two years ie it will be applicable from 1 April 2017

bull Investments made up to 31 March 2017 are proposed to be protected from the applicability of GAAR

11Private equity roundup mdash India |

4 Applicability of Minimum Alternate Tax to foreign companies

bull The bill proposed an exclusion of specified Captial gains earned by Foreign Institutional Investors (FIIs)Foreign Portfolio Investors (FPIs) on sale of Indian securities and corresponding expenditure if any to be added back in computing the book profit for levy of Minimum Alternate Tax (MAT) This amendment was proposed to be effective from financial year 2015-16

bull This proposal generated considerable debate as the generally understood position was that MAT is not applicable for a foreign company not having a place of business in India and this led to questions on the applicability of MAT to incomes of FIIs arising during past years and on the interest incomes which could arise to FIIs (and are taxable at a rate lower than the MAT rate) in FY2015-16 and thereafter

bull Also the applicability of MAT on foreign SPVscompanies of PEs earning income from India was also under a cloud of uncertainty

bull Certain FIIsPEs were issued draft assessment orders proposing to levy MAT for FY2011ndash12 and past assessments were also sought to be reopened

bull With a view to clarify the tax position as applicable to foreign companies the Revised Bill provides that in the cases of following specified income (all) foreign companies will be excluded from the purview of MAT from FY2015ndash16 onwards Consequently corresponding expenses for earning the said income are also proposed to be excluded while computing MAT as follows

bull Capital gains (whether long-term or short-term) arising on transactions in securities

bull Interest royalty or fees for technical services chargeable to tax

bull The FM also clarified in the Parliament that assessments for past years will be concluded as per the outcome of the Indian judicial process

bull While the intent of the FM to provide relief to foreign companies from the levy of MAT (on a going-forward basis) is evident the language of the revised proposals may still contain some uncertainty mdash more particularly for other incomes earned by foreign companies from India liable to tax at a rate lower than the MAT rate

5 Welcoming qualifying fund managers to India

bull Provisions are proposed to be introduced for conditions under which qualifying fund management activity from India shall not constitute business connection in India for an off-shore fund or impact the residential status of the off-shore fund

bull These provisions are intended to facilitate the location of fund managers of off-shore funds in India without impacting the fundrsquos tax liability

bull Many of the conditions prescribed in the tax law for eligibility are onerous

bull Given that a large number of existing funds (based on their fact pattern) were not able to satisfy the conditions prescribed for qualifying as an eligible investment fund and an eligible fund manager representations were made on several aspects to encourage relocation of fund management activities from outside India to India without subjecting the fund managers or the funds being managed by them to any onerous conditions

bull Based on the industry representations the bill has now been amended to provide that the following conditions will not apply in case of an investment fund set up by the Government or the central bank of a foreign state or a sovereign fund or such fund as the Central Government may notify (subject to conditions)

a There should be a minimum of 25 members who directly or indirectly are not connected persons

b No member of the fund along with connected persons should have participation interest directly or indirectly of more than 10 in the fund

c Aggregate participation interest of 10 or fewer members (directly or indirectly) along with their connected persons in the fund should be less than 50

bull Additionally it has been provided that the special regime shall be applied in accordance with guidelines and in such a manner as the CBDT may prescribe

12 | Private equity roundup mdash India

6 Tax ldquopass throughrdquo status provided to Category I and II Alternative Investment Fund (AIF)

bull Tax ldquopass throughrdquo status is accorded to income (other than business income) earned by Category I and II AIF business income taxable at AIF level

bull Any income (other than income taxable at AIF level) payable to an investor is subject to deduction of tax at 10

bull Loss of the AIF cannot be passed to the investor as it has to be set offcarried forward at the AIF level

bull While the proposed amendment addresses most of the key concerns of the AIFs it has generated uncertainty on issues such as characterization of AIFrsquos income by the tax authorities as business income so as to apply tax at maximum marginal rate (MMR) 10 withholding tax on exempt incomenonresident investors eligible for beneficial provisions of a double tax avoidance agreement

bull While representations were filed on the above and other relevant issues no changes have been made in the taxation of Category I and II AIFs as proposed in the Bill

7 Tax provisions pertaining to Real Estate Investment Trusts (REITs) and Infrastructure Investment Trusts (InVITs)

bull Provisions were introduced to provide parity in taxation to sponsor on exchange of shares of special purpose vehicle (SPV) for units of business trust vis-agrave-vis the sale of shares of SPV under an initial public offering (IPO)

bull Rental income earned by REITs on a self-owned real estate asset is proposed to be exempt from tax in its hands and shall be taxable in the hands of unitholders on distribution by REITs

bull REITs shall deduct tax at the following rates with respect to rental income allowed to be passed through 10 in case of resident unitholders and applicable rates in force in case of a nonresident unitholder

bull Concerns were however raised by the sponsor on the prospects of MAT applicability at the stage of exchange of shares against the units allotted by the business trust The concern was all the more valid considering that it would impact cash flow without realization of gain Addressing the concerns the Bill has now been amended to provide for deferment of MAT applicability to the stage of transfer of units by the sponsor

8 Extension of concessional withholding tax rate on interest payments

bull Concessional withholding tax rate of 5 on interest paid and corporate bonds (such as listed nonconvertible debentures [NCDs]) to FPIsFIIs is proposed to be extended on interest payable up to 30 June 2017

9 Residential status

bull The original bill had proposed to provide that a foreign company will be treated as a resident of India for a financial year if its place of effective management (POEM) is in India at any time in that year

bull The use of the phrase ldquoat any timerdquo could have an adverse impact on foreign companies where only one board meeting is held in India or even where one strategic decision was made in India The FM has now proposed to delete the phrase ldquoat any timerdquo Therefore from FY2015ndash16 onwards a foreign company is now proposed to be regarded as being a resident in India if its POEM in that financial year is in India

bull POEM continues to be defined to mean a place where key management and commercial decisions that are necessary for the conduct of the business of an entity as a whole are in substance made

10 Global Depository Receipts (GDRs)

bull The ITLs provide for a concessional tax rate for nonresidents (NRs) on income earned by way of dividends on and by way of capital gains from the transfer of GDRs purchased in foreign currency Further the ITLs exempt capital gains on the transfer of GDR from one NR to another NR outside India and on conversion of GDR into shares

bull Earlier GDRs were governed by the ldquoIssue of Foreign Currency Convertible Bonds and Ordinary Shares (through depository receipts mechanism) Scheme 1993rdquo (1993 Scheme) The scheme was limited to issue of Depository Receipts (DRs) based on the underlying shares or foreign currency convertible bonds of a listed Indian company Also the 1993 Scheme laid down the tax treatment on GDRs

bull The Gol recently notified a new Depository Receipts Scheme 2014 (which replaced the 1993 Scheme on GDRs) Under the new scheme GDRs can be issued against securities of listed unlisted or private or public companies against underlying securities However the 2014 Scheme is silent on the tax treatment

13Private equity roundup mdash India |

bull In order to provide for the tax implications on redemption of GDR (under the new scheme) into shares of a listed company and thereby to consider and align with the tax treatment prescribed in the 1993 Scheme the ITL is proposed to be amended to provide that

bull The period of holding of shares will be reckoned from the date on which a request for redemption is made

bull The cost of acquisition of shares will be the price of such shares prevailing on any recognized stock exchange in India on the date on which a request for redemption is made

bull The amendment is limited in its implications to redemption of GDRs issued by listed companies The tax treatment of other GDRs has not been proposed

11 Direct Taxes Code

bull The FM clarified that he sees no great merit in going ahead with the Direct Tax Code as it exists today

12 Increase in rate of service tax

bull The service tax rates are proposed to be increased to 14 with an additional Swacch Bharat Cess of 2 on notified services (making the effective rate 16 on such services)

Source wwwindiabudgetnicin

Income computation and Disclosure Standards (ICDS)The Gol has vide notification dated 31 March 2015 notified 10 ICDS for compliance by all taxpayers following the mercantile system of accounting for the purposes of computation of income chargeable to income tax under the heading ldquoProfits and gains of business or professionrdquo or ldquoIncome from other sourcesrdquo ICDS shall apply immediately effective from tax year 2015ndash16 and onwards

While the objective of ICDS was to standardize one or more accounting alternatives so that taxable income can be computed precisely the deviationscarve-outs in ICDS as compared to ICAI AS (Accounting Standards as notified by The Institute of Chartered Accountants of India) appear to go beyond this objective and may significantly increase compliance burden for taxpayers Potentially there could be ambiguity as to whether ICDS may require accelerated recognition of income or deferment of expenditureloss for tax purposes as compared to recognition as per ICAI AS in certain cases There may also exist scope for varied interpretations of ICDS leading to uncertainty and increased litigation

New legislation for Ordinary Residents (taxpayers) on the taxation of undisclosed overseas income or foreign assetsOn 20 March 2015 the Indian Government proposed a new legislation for Ordinary Residents (taxpayers) on the taxation of undisclosed overseas income or foreign assets

The law allows for a special 30 tax rate on the income penalties of up to 300 of the tax due and criminal prosecution However for a limited period there will be a one-off amnesty for those who make a full disclosure with no prosecution and reduced penalties

The legislation will apply to Ordinarily Resident taxpayers including expatriate employees who qualify as Ordinary Residents due to their physical presence in India Overseas income or assets which were not reported by taxpayers on their income tax return will be taxed at a rate of 30 and no claim for reductions allowances or offsetting against losses will be allowed for such income Income and assets taxed under this legislation would then not be subject to tax again under regular domestic income tax laws The legislation is at present subject to approval by the Indian Parliament

Regulatory updatesIncrease in limits under the Liberalized Remittance Scheme (LRS)In its monetary policy statement dated 3 February 2015 the RBI decided to enhance the limit under LRS to US$250000 per person per year Furthermore in order to ensure ease of transactions it has also been decided in consultation with the Government that all the facilities for release of exchangeremittances for current account transactions available to resident individuals under Schedule III to Foreign Exchange Management (Current Account Transactions) Rules 2000 as amended from time to time shall also be subsumed under this limit

Increase in limits for FDI in insurance sectorThe GoI increased the Foreign Direct Investment (FDI) limit in the insurance sector from 26 to 49 and opened it for FPIs to invest within the 49 limit as well vide Press Note 3 of 2015 Furthermore the Government has also notified the Indian Insurance Companies (Foreign Investment) Rules 2015 These rules lay down the procedure with regards to the recent amendments pertaining to increase in foreign investment limit in Indian insurance companies introduced by the Insurance Laws (Amendment) Ordinance 2014

RBI rejects application for deviation from pricing guidelinesA few months ago the Tata Group had approached RBI for an approval to acquire NTT DoCoMorsquos stake in the JV Tata Teleservices at a pre-determined price in accordance with their JV agreement The RBI in turn had sought the Finance Ministryrsquos view on the matter We understand based on press reports that the Ministry had requested RBI to adhere to the extant guidelines

As per current foreign exchange regulations price for acquisition of shares in an Indian company by a resident from a nonresident cannot exceed the fair value Application for special permission was made to the RBI since the price sought to be paid was higher than the price permitted under these regulations

We now understand that RBI has recently conveyed to the Tata Group that it cannot accede to its request as the same is not in conformity with the extant FEMA regulations and has advised that any such purchase of shares be at current fair value of shares

This reiterates the position that pricing guidelines under FEMA need to be strictly adhered to and RBI is not willing to make any exceptions even where agreements specifically provide for downside protection

Amendments to delisting takeover and buyback of shares regulations by SEBI notified on 24 March 2015On 19 November 2014 SEBI in its meeting approved certain amendments in ldquoSEBI (delisting of equity shares) Regulations 2009rdquo (delisting regulations) Now SEBI has notified the amendments to delisting regulations on 24 March 2015 The key amendments are enunciated below

Joint framework with SEBI (substantial acquisition of shares and takeovers) Regulations 2011 (takeover regulations)

bull An option has been granted to the acquirer pursuant to triggering takeover regulations (except in case of competing offer) to delist the shares of company directly through delisting regulations instead of making the offer under takeover regulations The acquirer is required to declare his intention of delisting at the time of making a detailed public statement

bull Acquirer shall complete acquisition of shares triggering takeover offer only after making the public announcement regarding the success of the delisting proposal

bull In case of a failed delisting the acquirer is to proceed with an open offer according to takeover regulations In that case interest of 10 per annum for the period between the scheduled date of payment of consideration and the actual date of payment of consideration would be payable

15Private equity roundup mdash India |

Change in the threshold limit for successful delisting

Under the delisting regulations delisting was considered successful when promotersrsquo shareholding (along with persons acting in concert) reached above 90 of the total issued shares or aggregate of pre-offer promoter shareholding and 50 of offer size Now delisting regulations have been amended to consider delisting successful when promoters shareholding reaches

bull 90 of the total issued shares of the company (excluding shares held by the custodian against which depository receipts were issued overseas)

bull At least 25 of the number of public shareholders (holding shares in demat mode as on date of Board of Directors meeting approving such delisting proposal) participate in Reverse Book Building (RBB) process This requirement has however been dispensed with where the acquirer and merchant banker are able to demonstrate that they have delivered the offer letter to all public shareholders either through registered speed post courier hand delivery email etc

Determination of floor price

The floor price shall now be determined in terms of Regulation 8 of SEBI (substantial acquisition of shares and takeovers) Regulations 2011 thus also taking into consideration the price paid for any acquisition during the specified period prior to delisting

Determination of offer price

Under the delisting regulations the offer price was determined through the RBB process (price at which maximum public shareholders tender their shares) The amendment brings modification to the RBB process according to which the offer price would be one at which shareholding of promoteracquirer (along with persons acting in concert) reaches the prescribed threshold limit of 90 of the total issued shares excluding the shares held by the custodian and against which depository receipts issued overseas

Use of stock exchange platform

Under the delisting regulations tendering of shares was earlier carried out as an off-market transaction thus resulting in tax costs in the hands of public shareholders tendering their shares However with the amendment transfer of shares pursuant to delisting shall now be done on the stock exchange This shall enable public shareholders to enjoy favorable capital gains exemption as available for on-market transactions

Timeline

The delisting timeline has been reduced substantially

bull In principle approval by stock exchange to be given in five working days from earlier 30 working days

bull Dispatch of offer letter within two working days from the date of public announcement (earlier maximum period prescribed of 45 working days)

bull Opening of offer not later than seven working days from the date of public announcement (earlier 55 working days prescribed)

Exemption from delisting process

Earlier companies with paid-up capital of INR1 crore were exempted from the delisting process subject to fulfillment of prescribed conditions However now this clause has been amended to exempt companies with paid-up capital not exceeding INR10 crores and net worth not exceeding INR25 crores subject to compliance of prescribed conditions

Use of stock exchange platform under buyback of Securities Regulations 1998

The revised buyback norms require acquirers to facilitate tendering of shares and their settlements through the stock exchange thus enabling the public shareholders to enjoy favorable capital gains exemption as available for on-market transactions

In a move to ease the delisting process SEBI has made significant changes in the delisting regulations SEBI has moved delisting regulations in the right direction and has tried to address certain significant concerns arising to promotersminority shareholders in the past

From a PE standpoint the amendments are a welcome step and appear reasonable to all stake holders with reduced timelines simplification in the delisting process and availability of tax efficiency due to introduction of stock exchange platform for delisting buy-back and open offer thereby ensuring an efficient manner of buy-outs

Introduction of Goods and Services Tax (GST)

The FM in his Budget Speech reiterated the Governmentrsquos intention to introduce the GST with effect from 1 April 2016 The 122nd Constitutional Amendment Bill has been passed by the Lok Sabha in May 2015 and has been placed before the Rajya Sabha for consideration Passage of this Constitutional Amendment Bill will be a significant stepping stone on the road to implementation of this new tax

16 | Private equity roundup mdash India

OutlookStrong VC activity and rebound in the growth capital deals were reported this quarter The VCearly stage ecosystem in India is very vibrant now and has seen unprecedented activity levels as with most of the VC hotbeds globally but there were no tangible reasons for the increase in growth deal activity Positive investor and consumer sentiment brought about by the new Government at the Centre would have somewhat contributed to the increased activity but to sustain this momentum more concrete changes in the business environment will need to be seen The industrial activity (as reflected by IIP) has been patchy over the last six to nine months and the financial results for FY15 have also been a mixed bag In this background not a lot of change is expected in the PE activity in the near term and there may actually be some drop in the deal volumes from the high of 1Q 2015 The Government has lined up a host of actions (Land Bill GST Infrastructure sector reforms) which if implemented as currently envisaged by the Government can definitely lead to stronger PE activity in the medium term There are initial signs of investor and corporate frustration and impatience which can grow stronger if the Government-planned initiatives are not acted upon soon and this can adversely affect the PE activity

Encouragingly the early-stageVC investing has delineated itself from the PE industry and to that extent has not been affected as much by the issues faced by the PE industry such as lack of growth etc Given the different deal drivers and market dynamics for early-stage businesses we expect the VC activity levels to remain robust in the foreseeable future

Fundraising trends have been reassuring and have clearly underlined the fact that LPs are open to invest in India with experience and track record of fund managers being the critical success factors

Overall the next 6 to 12 months are important as a host of Government initiatives are expected to see the light of the day and a lot of foreign investment into India including PE is riding on successful implementation of those

17Private equity roundup mdash India |

EYEY is a global leader in assurance tax transaction and advisory services Worldwide our 200000+ people are united by our shared values and an unwavering commitment to quality We make a difference by helping our people our clients and our wider communities achieve their potential

In IndiaEY India has offices in Ahmedabad Bengaluru Chandigarh Chennai Hyderabad Kochi Kolkata Mumbai Pune and NCR (New Delhi + Gurgaon + Noida) Its workforce of more than 10000 people work toward the organizationrsquos vision of being a trusted business advisor that contributes to the success of its clients by creating confidence and value We help our clients achieve their potential through our leading approach which incorporates various service dynamics including

bull An industry-aligned delivery model that harnesses our broad range Practices focused on specific industries draw on knowledge skills and our experiences of that industry in India and around the world This helps us customize our approach to the unique needs of each client

bull Our services are broadly classified as four service lines Assurance Tax Transactions and Advisory Each service line is further streamlined into niche competencies and focused groups which enable us to strengthen our outreach and offer a compelling portfolio of broad and well-defined services

bull Each team is built as a multidimensional group of professionals from diverse backgrounds with a range of perspectives They understand and address our clientsrsquo concerns from a variety of standpoints while using highly evolved tools and approaches to offer inputs in a structured and compelling manner

bull Values and ethics unite us ensuring cohesive work toward the shared goal of making a difference A special energy that we bring to each assignment defines the way we work and is our key characteristic

Today we are recognized as leaders in the professional services industry and the accolades we receive encourage us to continue striving for excellence

bull ldquoMost Attractive Employerrdquo award in the consulting sector by Randstad

bull Indiarsquos tier-one tax firm for the 12th consecutive year mdash Euromoney ITR World Tax Guide 2014

bull Ranked 1 Financial Advisor in India for 13 consecutive years for most number of deals from 2002ndash14 mdash Bloomberg

bull The most reputed Tax Firm in India consecutively for four years mdash TNS Global Tax Monitor Survey 2012

bull International AccountingDue Diligence firm of the year 2012 mdash MampA Advisory

bull Most Active Transaction Advisor Award PE and MampA for three consecutive years (2009ndash11) mdash Venture Intelligence

bull Financial Advisor of the Year Award for two consecutive years (2011ndash12) mdash Asian Venture Capital Journal India Awards

bull Financial Advisor of the Year MampA Award mdash India 2011 2009 and 2008 mdash Financial Times and Mergermarket

bull Investment Bank of the Year mdash Private Equity 2011 mdash VCCircle Awards

bull Overall winner mdash consultancy rankings in survey of risk and compliance professionals mdash OpRisk amp Compliance magazine

bull Risk and business advisory relationship with 160 of the BSE300 companies

bull ldquoExcellence in Trainingrdquo award in the Employer Branding Awards for three years (2007mdash08 2009ndash10 2010ndash11)

bull ldquoContinuous Innovation in HR strategy at workrdquo award in the Employer Branding Awards 2011

About EY

Methodologybull Private equity roundup is based on EYrsquos analysis of

announced PE deals as well as other PE-related news and information reported in secondary sources and VCCEdge

bull PE deal values used in this document are based on those provided in press releases pertaining to deal announcements The conversion rate (INR to US$) is based on the exchange rates prevalent on the dates of the deal announcements

bull The deals have been reclassified wherever required based on EYrsquos sector-classification policy

bull The figures have been rounded off to the nearest whole number

The numbers include personnel from other member firms of EY Global based in India

18 | Private equity roundup mdash India

EYrsquos Private Equity practice

At EY our Private Equity practice offers a broad range of services to assist you and your investee companies every step of the way mdash from your fund setup to the transaction life cycle

Our teams work closely with you offering incisive and proven industry experience coupled with integrated objective practical advice and support to help you meet your needs Itrsquos how EY makes a difference

Partnersbull Personal taxFundraisingbull Audit of fund performance

Fund assurancebull Assurancebull Tax structuring

Sell-side advisorybull Mergers and acquisitionsbull Valuations

Buy-side support bull Due diligencebull Tax structuringbull 1048733Environmental compliancebull 1048733Human capitalbull Valuations

Exit readinessbull IPO readinessbull Sale mandates

Kolkata22 Camac Street 3rd Floor Block Crdquo Kolkata-700 016 Tel +91 33 6615 3400 Fax +91 33 2281 7750

Mumbai14th Floor The Ruby 29 Senapati Bapat Marg Dadar (west) Mumbai-400 028 India Tel +91 22 6192 0000 Fax +91 22 6192 1000

5th Floor Block B-2 Nirlon Knowledge Park Off Western Express Highway Goregaon (E) Mumbai-400 063 India Tel +91 22 6192 0000 Fax +91 22 6192 1000

NCRGolf View Corporate Tower mdash B Near DLF Golf Course Sector 42 Gurgaonndash122 002 Tel +91 124 464 4000 Fax +91 124 464 4050

6th floor HT House 18-20 Kasturba Gandhi Marg New Delhi-110 001 Tel +91 11 4363 3000 Fax +91 11 4363 3200

4th amp 5th Floor Plot No 2B Tower 2 Sector 126 NOIDA-201 304 Gautam Budh Nagar UP India Tel +91 120 671 7000 Fax +91 120 671 7171

PuneC-401 4th Floor Panchshil Tech Park Yerwada (Near Don Bosco School) Pune-411 006 Tel +91 20 6603 6000 Fax +91 20 6601 5900

EY | Assurance | Tax | Transactions | AdvisoryAbout EY

EY is a global leader in assurance tax transaction and advisory services The insights and quality services we deliver help build trust and confidence in the capital markets and in economies the world over We develop outstanding leaders who team to deliver on our promises to all of our stakeholders In so doing we play a critical role in building a better working world for our people for our clients and for our communities

EY refers to the global organization and may refer to one or more of the member firms of Ernst amp Young Global Limited each of which is a separate legal entity Ernst amp Young Global Limited a UK company limited by guarantee does not provide services to clients For more information about our organization please visit eycom

How EYrsquos Global Private Equity Sector can help your business

Value creation goes beyond the private equity investment cycle to portfolio company and fund advice EYrsquos Global Private Equity Sector offers a tailored approach to the unique needs of private equity funds their transaction processes investment stewardship and portfolio companiesrsquo performance We focus on the market sector and regulatory issues If you lead a private equity business we can help you meet your evolving requirements and those of your portfolio companies from acquisition to exit through a Global Private Equity network of 5000 professionals around the world Working together we can help you meet your goals and compete more effectively

Ernst amp Young LLP is a client-serving member firm of Ernst amp Young Global Limited operating in the US

copy 2015 Ernst amp Young LLP All Rights Reserved

EYG no FR0167

1507-1572791 ED None

This material has been prepared for general informational purposes only and is not intended to be relied upon as accounting tax or other professional advice Please refer to your advisors for specific advice

eycomprivateequity

EY refers to the global organization andor one or more of the independent member firms of Ernst amp Young Global Limited

2 | Private equity roundup mdash India

Exits through open market continued to dominate overall exits The quarter reported 59 exits out of which 32 were open market Strategic exits also improved (13 in 1Q15 compared to four in 4Q14) The biggest exit of the quarter saw consolidation in the online taxi operators where Taxiforsurecom (Serendipity Infolabs) was acquired by Olacabs (ANI Technologies) for US$200 million in a cash plus stock deal The PE investors in Taxiforsurecom (Accel India Bessemer Venture Partners Blume Ventures Helion Venture Partners) swapped their shareholding for a stake in ANI Technologies Pvt Ltd In terms of deal volumes the technology sector registered maximum exit activity

During the quarter the NDA Government presented its first full Union Budget Generally speaking the budget was forward looking and had positive intent It did have some positives for the PEVC industry but it could have done more to put at rest some of the long-standing concerns of the PEVC industry We have summarized some of the key budget changes that impact the PEVC industry in this document

3Private equity roundup mdash India |

Key economic indicatorsIndia adopted a new methodology for calculating the GDP growth rate whereby growth rates for FY13 and FY14 were substantially revised from 45 to 51 and 47 to 69 respectively The advance estimate for FY15 growth has been pegged at 75 Furthermore according to the new series GDP grew at 74 in 4Q14 overtaking China as the fastest-growing economy This has created a stir as India is now pegged to grow at a faster pace than China over the next two years

The new GDP series has shifted the base year to 2011ndash12 and includes improvements in the compilation in terms of

methodology and coverage while incorporating latest datasets to make it consistent with international guidelines However in the absence of back-casting of the new series any meaningful analysis of past trends economic cycles and potential output remains challenging Furthermore there are contradictions between the higher rate of GDP growth per the new GDP series and the poor economic activity indicated by the lead indicator which has been difficult to rationalize It is expected that over time with the methodology being refined some of these contradictions are likely to get addressed

Fundraising shows further improvementThere was an increase in the new fund closures during the quarter mdash India-focused PE firms raised US$19 billion in this quarter compared to US$12 billion in 4Q14 1Q15 exhibited the highest fund raise in the last seven quarters The activity was dominated by sector-agnostic funds with US$15 billion in new investor commitments Two-thirds of this amount was contributed

by Fairfax India which raised its maiden US$1 billion fund The fund is listed on the Toronto stock exchange and raised US$500 million in IPO proceeds as well as US$500 million from its parent Fairfax Holdings and private placement to certain cornerstone investors It will look to invest in public and private equity securities and debt instruments in Indian businesses The other big fundraiser of the quarter was the first close (US$500 million) Fund-V by IVFA

Funds

Figure 7 Quarterly India fundraising (US$ billion)

SAIF Partners New India Fund Start-ups 350 Follow on

Tara India Fund-IV Manufacturing 40 Follow on

StartHealth Health care 16 New

There were also 12 new fundraising plans reported in this quarter totaling US$23 billion a decline of 30 from the previous quarter (US$33 billion) Out of the 12 funds half were VC funds with plans to raise US$13 billion Four of these funds are focused on investing in technology startups reflecting increasing interest in early-stage technology investments

Figure 8 India-focused funds raised during 1Q15

6 | Private equity roundup mdash India

Transactions and exitsSignificant increase in transaction volumes led by early stageVC dealsThere was a decline in the aggregate deal value compared to the previous quarter but the quarter saw a significant increase in the deal volumes which were the highest ever for any quarter in the history of the Indian PE industry Even the deal value though

lower than 4Q14 was quite robust The quarter saw US$34 billion invested across 181 deals There were six deals above US$100 million (aggregating US$956 million) and 17 deals above US$50 million (aggregating US$18 billion) in this quarter The average deal size declined to US$22 million from US$45 million in the previous quarter whereas median deal size remained at US$10 million

Omkar Realtors and Developers Mumbai luxury project

Piramal Fund Management Real estate 191

Assetz Property and Homes Equis Fund Group Real estate 116

Clues Network (shopcluescom) Nexus India Capital Advisors Tiger Global Management Helion Venture Partners

E-commerce 100

Ujjivan Financial Services CDC Group CX Capital Management NewQuest Capital Partners

Financial services 96

Emaar MGF Land SSG Capital Management Real estate 96

Lodha Group Kotak Realty Fund Real estate 87

Diligent Power project IDFC Alternatives Power and utilities 81

Figure 11 Select PE investments in 1Q15

8 | Private equity roundup mdash India

Early stageVC investments surged in this quarter recording 98 deals an increase of ~ 53 from the previous quarter These also accounted for 54 of the total announced deals in this quarter There was also a significant increase in the number of growth deals in the quarter to 71 compared to 48 deals in the last quarter PIPE deals on the other hand remained more or less constant with 11 deals compared to 10 in 4Q14 The quarter saw just one buyout deal with Everstone acquiring Excelity Aon Hewittrsquos payroll processing business in Asia Pacific

The noteworthy trend noticed in the quarter was the rebound in the growth-stage deals This was led by real estate investments but also saw improvement in the deal volumes in a number of other sectors primary being health care financial services technology and retail and consumer This clearly is an indicator of the improving investor and corporate confidence in India

Figure 13 PE investments in 1Q 14 by sectors

Source Public sources and EY analysisNote RHC- Real estate hospitality amp construction RCP- Retail and consumer products

Volume Value (US$ million)

3

3

4

6

6

9

11

15

15

26

30

53

Automotive

Business services

Education

Food and agriculture

Industrial products

Other

Health care

RCP

Financial services

RHC

Technology

E-commerce

30

31

65

70

83

110

120

294

386

522

657

1074

Logistics

Food and agriculture

Automotive

Other

Power and utilities

Business services

Retail and consumer products

Technology

Health care

E-commerce

Financial services

Real estate hospitality amp construction

E-commerce accounted for the highest number of deals (53) raising US$522 million across 45 deals (deal value not known for eight deals) The biggest deal in e-commerce was a US$100 million investment in Clues Network (Shopcluescom) by a group of investors including Nexus India Capital Advisors Tiger Global Management and Helion Venture Partners This was followed by Sequoia Valiant Capital and Tybourne Capital Managementrsquos US$80 million investment in Accelyst Solutions (freechargein)

In terms of value the real estate sector attracted the highest PE investment amounting to US$11 billion across 26 deals Financial services raised US$657 million across 15 deals more than double as compared to US$321 million in eight deals in the previous quarter

9Private equity roundup mdash India |

ExitsHigher number of trade sales led the improvement in number of exits during the quarterThe quarter reported 59 PE exits with open market exits leading in terms of volume and value Compared to this 4Q14

had 49 exits The biggest exit of the quarter saw a consortium of firms (Accel India Bessemer Venture Partners Blume Ventures Fund I Helion Venture Partners II) exiting Serendipity Infolabs (TaxiForSurecom) for US$200 million followed by IDFC Alternativesrsquo partial exit in Green Infra to Sembcorp Industries for US$168 million

Strategic exits (trade sales) almost tripled during the quarter (13 strategic exits in 1Q15 against four in 4Q14) as technology and e-commerce firms looked to expand by acquiring smaller firms There were no PE-backed IPOs in the quarter Buybacks also

declined during the quarter (six in 1Q15 as compared with 11 in 4Q14)

Technology saw the maximum activity with 10 exits followed closely by financial services (seven)

Target Seller Exit type Value (US$m)

Serendipity Infolabs (TaxiForSurecom)

Accel India Bessemer Venture Partners Blume Ventures Fund I Helion Venture Partners II

Strategic 200

Green Infra IDFC Private Equity Fund II Strategic 168

ING Vysya Bank Chrys Capital Open market 108

Manthan Software Services IDG Ventures India Fund Fidelity Growth Partners India and ePlanet Ventures Fund I

Secondary sale 60

Mahindra CIE Automotive India Value Fund III Open market 58

Figure 15 Select non-IPO exits during 1Q 2015

10 | Private equity roundup mdash India

Tax and regulatory updatesThe new Government presented its first full budget amidst great expectations from various stakeholders and paved the way for key tax and regulatory changes in 1Q15 In this edition we are pleased to bring you the key amendments brought about by Budget 2015 to the direct and indirect taxes and brief on the income computation and disclosure standards notified by the Government of India (Gol) We also touch upon regulatory updates such as RBIrsquos stand on deviation from pricing guidelines and some key amendments notifed by the Securities and Exchange Board of India (SEBI) in ldquoDelisting of Equity Shares Regulations 2009rdquo ldquoSubstantial Acquisition and Takeover Regulations 2011rdquo and ldquoBuy Back of Securities Regulations 1998rdquo

Tax updatesFinance Bill 2015The Finance Minister (FM) presented the Finance Bill 2015 (Bill) as part of the Union Budget 2015ndash16 before the Indian Parliament on 28 February 2015 The Bill contained a number of proposals to amend the Indian Tax Laws (ITLs) The FM then moved certain amendments to the Bill at the time of its debate before the Lok Sabha (the lower house of the Indian Parliament) and the Bill in its revised form (Revised Bill) was recently passed by both houses of Parliament The Revised Bill is now awaiting the assent of the President of India to become law We have summarized below the key amendments brought about by the Finance Bill 2015 (including amendments) relevant to the PEVC sector

1 Corporate tax rate to be brought down to 25

bull Basic corporate tax rate for Indian companies shall be reduced to 25 over the next four years and shall be accompanied by phased reduction in exemptions available to corporates

bull The basic corporate tax rate for FY15-16 remains unchanged at 30 However with the additional surcharge of 2 this could go up to 3461 for 2015-16

bull Similarly the dividend distribution tax and buyback tax would also increase due to the higher surcharge

2 Much awaited clarity in taxation on indirect transfer of Indian company shares

bull It is proposed that indirect transfer rules in India will be triggered only if the value of the Indian assets exceeds INR10 crores and represents at least 50 of the value of global operations transferred Valuation methodology for this will be separately prescribed

bull Specific exemptions have been provided for

a Amalgamationsdemergers being undertaken outside India and satisfying certain conditions (however tax neutrality for foreign shareholders of such amalgamating or demerged companies has not been discussed)

b Small shareholders holding less than 5 stake and not having management and control

bull It has also been clarified that the tax liability in India will be based on proportionate gains attributable to India vis-agrave-vis total gains

bull The issue of applicability of indirect transfer rules in multilayer investment structures and transfer of investorsrsquo interest (gt 5) in a fund structure remains unaddressed

bull These amendments will take effect from FY15-16

bull Separately the Central Board of Direct Taxes (CBDT) the apex administrative body for taxation in India issued Circular 4 of 2015 (dated 26 March 2015) clarifying that declaration of dividend outside India by a foreign company would not be taxable in India under the indirect transfer provisions of the Indian Tax Laws since such declaration and payment of dividend does not have an effect of transfer of any underlying asset located in India This is a welcome clarification from the CBDT and it addresses the concern which had risen on account of the wide scope of the indirect transfer provisions The CBDT Circular being clear in nature should apply to all pending cases

3 Applicability of GAAR (General Anti-Avoidance Rules deferred by two years

bull GAAR is proposed to be deferred by two years ie it will be applicable from 1 April 2017

bull Investments made up to 31 March 2017 are proposed to be protected from the applicability of GAAR

11Private equity roundup mdash India |

4 Applicability of Minimum Alternate Tax to foreign companies

bull The bill proposed an exclusion of specified Captial gains earned by Foreign Institutional Investors (FIIs)Foreign Portfolio Investors (FPIs) on sale of Indian securities and corresponding expenditure if any to be added back in computing the book profit for levy of Minimum Alternate Tax (MAT) This amendment was proposed to be effective from financial year 2015-16

bull This proposal generated considerable debate as the generally understood position was that MAT is not applicable for a foreign company not having a place of business in India and this led to questions on the applicability of MAT to incomes of FIIs arising during past years and on the interest incomes which could arise to FIIs (and are taxable at a rate lower than the MAT rate) in FY2015-16 and thereafter

bull Also the applicability of MAT on foreign SPVscompanies of PEs earning income from India was also under a cloud of uncertainty

bull Certain FIIsPEs were issued draft assessment orders proposing to levy MAT for FY2011ndash12 and past assessments were also sought to be reopened

bull With a view to clarify the tax position as applicable to foreign companies the Revised Bill provides that in the cases of following specified income (all) foreign companies will be excluded from the purview of MAT from FY2015ndash16 onwards Consequently corresponding expenses for earning the said income are also proposed to be excluded while computing MAT as follows

bull Capital gains (whether long-term or short-term) arising on transactions in securities

bull Interest royalty or fees for technical services chargeable to tax

bull The FM also clarified in the Parliament that assessments for past years will be concluded as per the outcome of the Indian judicial process

bull While the intent of the FM to provide relief to foreign companies from the levy of MAT (on a going-forward basis) is evident the language of the revised proposals may still contain some uncertainty mdash more particularly for other incomes earned by foreign companies from India liable to tax at a rate lower than the MAT rate

5 Welcoming qualifying fund managers to India

bull Provisions are proposed to be introduced for conditions under which qualifying fund management activity from India shall not constitute business connection in India for an off-shore fund or impact the residential status of the off-shore fund

bull These provisions are intended to facilitate the location of fund managers of off-shore funds in India without impacting the fundrsquos tax liability

bull Many of the conditions prescribed in the tax law for eligibility are onerous

bull Given that a large number of existing funds (based on their fact pattern) were not able to satisfy the conditions prescribed for qualifying as an eligible investment fund and an eligible fund manager representations were made on several aspects to encourage relocation of fund management activities from outside India to India without subjecting the fund managers or the funds being managed by them to any onerous conditions

bull Based on the industry representations the bill has now been amended to provide that the following conditions will not apply in case of an investment fund set up by the Government or the central bank of a foreign state or a sovereign fund or such fund as the Central Government may notify (subject to conditions)

a There should be a minimum of 25 members who directly or indirectly are not connected persons

b No member of the fund along with connected persons should have participation interest directly or indirectly of more than 10 in the fund

c Aggregate participation interest of 10 or fewer members (directly or indirectly) along with their connected persons in the fund should be less than 50

bull Additionally it has been provided that the special regime shall be applied in accordance with guidelines and in such a manner as the CBDT may prescribe

12 | Private equity roundup mdash India

6 Tax ldquopass throughrdquo status provided to Category I and II Alternative Investment Fund (AIF)

bull Tax ldquopass throughrdquo status is accorded to income (other than business income) earned by Category I and II AIF business income taxable at AIF level

bull Any income (other than income taxable at AIF level) payable to an investor is subject to deduction of tax at 10

bull Loss of the AIF cannot be passed to the investor as it has to be set offcarried forward at the AIF level

bull While the proposed amendment addresses most of the key concerns of the AIFs it has generated uncertainty on issues such as characterization of AIFrsquos income by the tax authorities as business income so as to apply tax at maximum marginal rate (MMR) 10 withholding tax on exempt incomenonresident investors eligible for beneficial provisions of a double tax avoidance agreement

bull While representations were filed on the above and other relevant issues no changes have been made in the taxation of Category I and II AIFs as proposed in the Bill

7 Tax provisions pertaining to Real Estate Investment Trusts (REITs) and Infrastructure Investment Trusts (InVITs)

bull Provisions were introduced to provide parity in taxation to sponsor on exchange of shares of special purpose vehicle (SPV) for units of business trust vis-agrave-vis the sale of shares of SPV under an initial public offering (IPO)

bull Rental income earned by REITs on a self-owned real estate asset is proposed to be exempt from tax in its hands and shall be taxable in the hands of unitholders on distribution by REITs

bull REITs shall deduct tax at the following rates with respect to rental income allowed to be passed through 10 in case of resident unitholders and applicable rates in force in case of a nonresident unitholder

bull Concerns were however raised by the sponsor on the prospects of MAT applicability at the stage of exchange of shares against the units allotted by the business trust The concern was all the more valid considering that it would impact cash flow without realization of gain Addressing the concerns the Bill has now been amended to provide for deferment of MAT applicability to the stage of transfer of units by the sponsor

8 Extension of concessional withholding tax rate on interest payments

bull Concessional withholding tax rate of 5 on interest paid and corporate bonds (such as listed nonconvertible debentures [NCDs]) to FPIsFIIs is proposed to be extended on interest payable up to 30 June 2017

9 Residential status

bull The original bill had proposed to provide that a foreign company will be treated as a resident of India for a financial year if its place of effective management (POEM) is in India at any time in that year

bull The use of the phrase ldquoat any timerdquo could have an adverse impact on foreign companies where only one board meeting is held in India or even where one strategic decision was made in India The FM has now proposed to delete the phrase ldquoat any timerdquo Therefore from FY2015ndash16 onwards a foreign company is now proposed to be regarded as being a resident in India if its POEM in that financial year is in India

bull POEM continues to be defined to mean a place where key management and commercial decisions that are necessary for the conduct of the business of an entity as a whole are in substance made

10 Global Depository Receipts (GDRs)

bull The ITLs provide for a concessional tax rate for nonresidents (NRs) on income earned by way of dividends on and by way of capital gains from the transfer of GDRs purchased in foreign currency Further the ITLs exempt capital gains on the transfer of GDR from one NR to another NR outside India and on conversion of GDR into shares

bull Earlier GDRs were governed by the ldquoIssue of Foreign Currency Convertible Bonds and Ordinary Shares (through depository receipts mechanism) Scheme 1993rdquo (1993 Scheme) The scheme was limited to issue of Depository Receipts (DRs) based on the underlying shares or foreign currency convertible bonds of a listed Indian company Also the 1993 Scheme laid down the tax treatment on GDRs

bull The Gol recently notified a new Depository Receipts Scheme 2014 (which replaced the 1993 Scheme on GDRs) Under the new scheme GDRs can be issued against securities of listed unlisted or private or public companies against underlying securities However the 2014 Scheme is silent on the tax treatment

13Private equity roundup mdash India |

bull In order to provide for the tax implications on redemption of GDR (under the new scheme) into shares of a listed company and thereby to consider and align with the tax treatment prescribed in the 1993 Scheme the ITL is proposed to be amended to provide that

bull The period of holding of shares will be reckoned from the date on which a request for redemption is made

bull The cost of acquisition of shares will be the price of such shares prevailing on any recognized stock exchange in India on the date on which a request for redemption is made

bull The amendment is limited in its implications to redemption of GDRs issued by listed companies The tax treatment of other GDRs has not been proposed

11 Direct Taxes Code

bull The FM clarified that he sees no great merit in going ahead with the Direct Tax Code as it exists today

12 Increase in rate of service tax

bull The service tax rates are proposed to be increased to 14 with an additional Swacch Bharat Cess of 2 on notified services (making the effective rate 16 on such services)

Source wwwindiabudgetnicin

Income computation and Disclosure Standards (ICDS)The Gol has vide notification dated 31 March 2015 notified 10 ICDS for compliance by all taxpayers following the mercantile system of accounting for the purposes of computation of income chargeable to income tax under the heading ldquoProfits and gains of business or professionrdquo or ldquoIncome from other sourcesrdquo ICDS shall apply immediately effective from tax year 2015ndash16 and onwards

While the objective of ICDS was to standardize one or more accounting alternatives so that taxable income can be computed precisely the deviationscarve-outs in ICDS as compared to ICAI AS (Accounting Standards as notified by The Institute of Chartered Accountants of India) appear to go beyond this objective and may significantly increase compliance burden for taxpayers Potentially there could be ambiguity as to whether ICDS may require accelerated recognition of income or deferment of expenditureloss for tax purposes as compared to recognition as per ICAI AS in certain cases There may also exist scope for varied interpretations of ICDS leading to uncertainty and increased litigation

New legislation for Ordinary Residents (taxpayers) on the taxation of undisclosed overseas income or foreign assetsOn 20 March 2015 the Indian Government proposed a new legislation for Ordinary Residents (taxpayers) on the taxation of undisclosed overseas income or foreign assets

The law allows for a special 30 tax rate on the income penalties of up to 300 of the tax due and criminal prosecution However for a limited period there will be a one-off amnesty for those who make a full disclosure with no prosecution and reduced penalties

The legislation will apply to Ordinarily Resident taxpayers including expatriate employees who qualify as Ordinary Residents due to their physical presence in India Overseas income or assets which were not reported by taxpayers on their income tax return will be taxed at a rate of 30 and no claim for reductions allowances or offsetting against losses will be allowed for such income Income and assets taxed under this legislation would then not be subject to tax again under regular domestic income tax laws The legislation is at present subject to approval by the Indian Parliament

Regulatory updatesIncrease in limits under the Liberalized Remittance Scheme (LRS)In its monetary policy statement dated 3 February 2015 the RBI decided to enhance the limit under LRS to US$250000 per person per year Furthermore in order to ensure ease of transactions it has also been decided in consultation with the Government that all the facilities for release of exchangeremittances for current account transactions available to resident individuals under Schedule III to Foreign Exchange Management (Current Account Transactions) Rules 2000 as amended from time to time shall also be subsumed under this limit

Increase in limits for FDI in insurance sectorThe GoI increased the Foreign Direct Investment (FDI) limit in the insurance sector from 26 to 49 and opened it for FPIs to invest within the 49 limit as well vide Press Note 3 of 2015 Furthermore the Government has also notified the Indian Insurance Companies (Foreign Investment) Rules 2015 These rules lay down the procedure with regards to the recent amendments pertaining to increase in foreign investment limit in Indian insurance companies introduced by the Insurance Laws (Amendment) Ordinance 2014

RBI rejects application for deviation from pricing guidelinesA few months ago the Tata Group had approached RBI for an approval to acquire NTT DoCoMorsquos stake in the JV Tata Teleservices at a pre-determined price in accordance with their JV agreement The RBI in turn had sought the Finance Ministryrsquos view on the matter We understand based on press reports that the Ministry had requested RBI to adhere to the extant guidelines

As per current foreign exchange regulations price for acquisition of shares in an Indian company by a resident from a nonresident cannot exceed the fair value Application for special permission was made to the RBI since the price sought to be paid was higher than the price permitted under these regulations

We now understand that RBI has recently conveyed to the Tata Group that it cannot accede to its request as the same is not in conformity with the extant FEMA regulations and has advised that any such purchase of shares be at current fair value of shares

This reiterates the position that pricing guidelines under FEMA need to be strictly adhered to and RBI is not willing to make any exceptions even where agreements specifically provide for downside protection

Amendments to delisting takeover and buyback of shares regulations by SEBI notified on 24 March 2015On 19 November 2014 SEBI in its meeting approved certain amendments in ldquoSEBI (delisting of equity shares) Regulations 2009rdquo (delisting regulations) Now SEBI has notified the amendments to delisting regulations on 24 March 2015 The key amendments are enunciated below

Joint framework with SEBI (substantial acquisition of shares and takeovers) Regulations 2011 (takeover regulations)

bull An option has been granted to the acquirer pursuant to triggering takeover regulations (except in case of competing offer) to delist the shares of company directly through delisting regulations instead of making the offer under takeover regulations The acquirer is required to declare his intention of delisting at the time of making a detailed public statement

bull Acquirer shall complete acquisition of shares triggering takeover offer only after making the public announcement regarding the success of the delisting proposal

bull In case of a failed delisting the acquirer is to proceed with an open offer according to takeover regulations In that case interest of 10 per annum for the period between the scheduled date of payment of consideration and the actual date of payment of consideration would be payable

15Private equity roundup mdash India |

Change in the threshold limit for successful delisting

Under the delisting regulations delisting was considered successful when promotersrsquo shareholding (along with persons acting in concert) reached above 90 of the total issued shares or aggregate of pre-offer promoter shareholding and 50 of offer size Now delisting regulations have been amended to consider delisting successful when promoters shareholding reaches

bull 90 of the total issued shares of the company (excluding shares held by the custodian against which depository receipts were issued overseas)

bull At least 25 of the number of public shareholders (holding shares in demat mode as on date of Board of Directors meeting approving such delisting proposal) participate in Reverse Book Building (RBB) process This requirement has however been dispensed with where the acquirer and merchant banker are able to demonstrate that they have delivered the offer letter to all public shareholders either through registered speed post courier hand delivery email etc

Determination of floor price

The floor price shall now be determined in terms of Regulation 8 of SEBI (substantial acquisition of shares and takeovers) Regulations 2011 thus also taking into consideration the price paid for any acquisition during the specified period prior to delisting

Determination of offer price