Spring 2011 In this issue The role of trusts in your estate plan ................................ 3 Current Private Investment Counsel strategy ................................ 3 Consolidate to simplify your life and finances ................................ 4 tdwaterhouse.ca 1-866-280-2022 An exclusive quarterly report from TD Waterhouse ® Private Investment Counsel Inc. Private Investment Counsel Investment Outlook A powerful trend unfolds in the markets BY ROBERT J. GORMAN, CFA, CHIEF PORTFOLIO STRATEGIST, TD WATERHOUSE Continued on Page 2 100 Index saw their shares advance 16.5% versus 10.3% for the largest 50 firms. • Shares of the 50 most highly leveraged, or indebted, companies rose 15.4%, compared with 10.4% for the 50 companies with the strongest balance sheets. • The 50 least-profitable companies, measured by return on equity (ROE), generated a return of 15.9%, in contrast with the top 50 ROE firms, which rose 10.8%. A mong the dominant investment themes for 2011 outlined in the last edition of Investment Outlook (Winter 2011), we cited a trend that should have a significant impact on financial markets and your portfolio in the years ahead. This trend now seems to be unfolding as anticipated and further detail is warranted. Small caps lead recoveries Almost invariably, when the U.S. stock market begins to recover after a bear market, as was the case in the spring of 2009, small companies’ shares — small caps — lead the recovery. This reflects the fact that small companies are more economically sensitive than their larger brethren, responding more quickly to the ups and downs of the economy. Right on cue, small caps outperformed in 2009 and continued to do so in 2010. The result is depicted in Chart 1, which shows that the small-cap Russell 2000 Index handily outperformed the broad S&P 500 Index over the past two years, and that the S&P 500 Index in turn bested the large-cap S&P 100 Index. This strong relative performance by smaller firms’ shares is part of a longer-term cycle that saw the large-cap outperformance of the late eighties and nineties give way to small-cap strength over the past decade (see Chart 2). Valuations have become stretched The outperformance in 2010 of smaller, generally lower-quality U.S. companies’ shares is also illustrated by the following comparisons from TD Asset Management Inc.: • The smallest 50 companies within the S&P High-quality investments are set to assume leadership.

Transcript

Spring 2011

In this issue

The role of trusts in your estate plan

................................ 3

Current Private Investment Counsel strategy

................................ 3

Consolidate to simplify your life and finances

................................ 4

tdwaterhouse.ca 1-866-280-2022

An exclusive quarterly report from TD Waterhouse® Private Investment Counsel Inc.

Private Investment Counsel

Investment OutlookA powerful trend unfolds in the markets By RoBeRt J. GoRmAn, CFA, ChieF PoRtFolio StRAteGiSt, tD WAteRhouSe

Continued on Page 2

100 Index saw their shares advance 16.5% versus 10.3% for the largest 50 firms.

• Shares of the 50 most highly leveraged, or indebted, companies rose 15.4%, compared with 10.4% for the 50 companies with the strongest balance sheets.

• The 50 least-profitable companies, measured by return on equity (ROE), generated a return of 15.9%, in contrast with the top 50 ROE firms, which rose 10.8%.

Among the dominant investment themes for 2011 outlined in the last edition of Investment Outlook (Winter

2011), we cited a trend that should have a significant impact on financial markets and your portfolio in the years ahead. This trend now seems to be unfolding as anticipated and further detail is warranted.

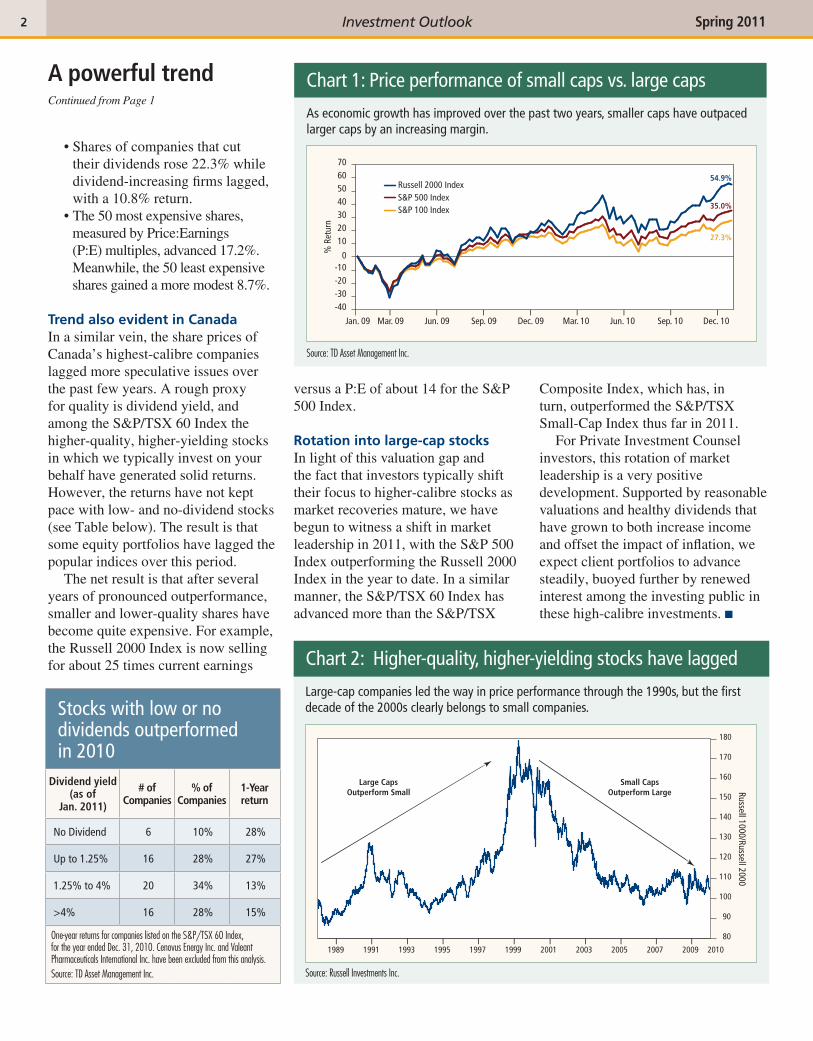

Small caps lead recoveries Almost invariably, when the U.S. stock market begins to recover after a bear market, as was the case in the spring of 2009, small companies’ shares — small caps — lead the recovery.

This reflects the fact that small companies are more economically sensitive than their larger brethren, responding more quickly to the ups and downs of the economy. Right on cue, small caps outperformed in 2009 and continued to do so in 2010.

The result is depicted in Chart 1, which shows that the small-cap Russell 2000 Index handily outperformed the broad S&P 500 Index over the past two years, and that the S&P 500 Index in turn bested the large-cap S&P 100 Index.

This strong relative performance by smaller firms’ shares is part of a longer-term cycle that saw the large-cap outperformance of the late eighties and nineties give way to small-cap strength over the past decade (see Chart 2).

Valuations have become stretchedThe outperformance in 2010 of smaller, generally lower-quality U.S. companies’ shares is also illustrated by the following comparisons from TD Asset Management Inc.:

• The smallest 50 companies within the S&P

high-quality investments are set to

assume leadership.

2 Spring 20112 Investment Outlook

Continued from Page 1

A powerful trend

• Shares of companies that cut their dividends rose 22.3% while dividend-increasing firms lagged, with a 10.8% return.

• The 50 most expensive shares, measured by Price:Earnings (P:E) multiples, advanced 17.2%. Meanwhile, the 50 least expensive shares gained a more modest 8.7%.

Trend also evident in CanadaIn a similar vein, the share prices of Canada’s highest-calibre companies lagged more speculative issues over the past few years. A rough proxy for quality is dividend yield, and among the S&P/TSX 60 Index the higher-quality, higher-yielding stocks in which we typically invest on your behalf have generated solid returns. However, the returns have not kept pace with low- and no-dividend stocks (see Table below). The result is that some equity portfolios have lagged the popular indices over this period.

The net result is that after several years of pronounced outperformance, smaller and lower-quality shares have become quite expensive. For example, the Russell 2000 Index is now selling for about 25 times current earnings

versus a P:E of about 14 for the S&P 500 Index.

Rotation into large-cap stocks In light of this valuation gap and the fact that investors typically shift their focus to higher-calibre stocks as market recoveries mature, we have begun to witness a shift in market leadership in 2011, with the S&P 500 Index outperforming the Russell 2000 Index in the year to date. In a similar manner, the S&P/TSX 60 Index has advanced more than the S&P/TSX

Composite Index, which has, in turn, outperformed the S&P/TSX Small-Cap Index thus far in 2011.

For Private Investment Counsel investors, this rotation of market leadership is a very positive development. Supported by reasonable valuations and healthy dividends that have grown to both increase income and offset the impact of inflation, we expect client portfolios to advance steadily, buoyed further by renewed interest among the investing public in these high-calibre investments. n

Chart 1: Price performance of small caps vs. large caps

Jan. 09 Mar. 09 Jun. 09 Sep. 09 Dec. 09 Mar. 10 Jun. 10 Sep. 10 Dec. 10

54.9%

35.0%

27.3%

Russell 2000 Index

% R

etur

n

S&P 500 IndexS&P 100 Index

-40-30-20-10

0

10203040506070

IIIIIIII

Stocks with low or no dividends outperformed in 2010

Dividend yield (as of

Jan. 2011)

# of Companies

% of Companies

1-year return

No Dividend 6 10% 28%

Up to 1.25% 16 28% 27%

1.25% to 4% 20 34% 13%

>4% 16 28% 15%

One-year returns for companies listed on the S&P/TSX 60 Index, for the year ended Dec. 31, 2010. Cenovus Energy Inc. and Valeant Pharmaceuticals International Inc. have been excluded from this analysis.Source: TD Asset Management Inc.

Chart 2: Higher-quality, higher-yielding stocks have lagged

Large-cap companies led the way in price performance through the 1990s, but the first decade of the 2000s clearly belongs to small companies.

As economic growth has improved over the past two years, smaller caps have outpaced larger caps by an increasing margin.

Do you want to provide income to family members without forcing them to

make investment, taxation, and recordkeeping decisions? Do you have a cottage or a family business? Are you concerned about taxes?

If you’ve answered yes to any of these questions, a trust deserves careful consideration as you plan your estate.

A flexible, lasting solutionA trust can be one of the most effective and flexible ways to ensure property is managed according to your goals of providing financial security for yourself and others over a long period of time. And a trust doesn’t have to be complicated. Here are a few typical uses of a trust:

income for dependants with special needs. Trusts can provide long-term income and capital preservation for minor children or dependants unable to look after their own financial affairs. The trust can be structured to provide funds for the beneficiary without risking other financial assistance the beneficiary may be entitled to, such as disability payments.

asset protection. A trust may be used to protect the assets of professionals or business owners who may be exposed to risk of future litigation because of the nature of their business or profession — for example, medical and legal professionals.

the role of trusts in your estate plan

income-splitting. A trust can be used to split income with adult family members with lower marginal tax rates, to the extent that attribution rules will allow.

changing family situations. A trust can be used to provide for children from a previous marriage and your present spouse during his or her lifetime.

phil anthropic goals. If your estate plan includes a sizable donation to charity, a charitable trust can create significant tax-planning opportunities.

business succession pl anning. Trusts can also play a major role in your business succession. For example, trusts can be used as part of an estate freeze, where asset values are frozen and future capital gains are transferred to the next generation

while the owner-manager retains control over business decisions.

Is a trust right for you?Speak to your Portfolio Manager about whether a trust is right for your needs. Your Portfolio Manager can establish a meeting with our Estate and Trust Specialists who can help you develop a comprehensive, long-term strategy to protect and transfer your assets. n

transferring wealth across generations: how we can helpWe work closely with individuals, families, and foundations, guiding them in the preservation and transfer of wealth across generations.

our experts. Our Private Trust Estate and Trust Specialists are highly experienced professionals who take the time to understand your lifestyle, your family needs, and your financial objectives. Their expertise in investment strategies, estate planning, estate and trust administration, and taxation is focused on developing solutions that reflect your unique situation today and in the future.

our services. We can provide you with professional advice on:

• the role of a trust within your overall financial plan;

• the structure of your trust agreement; • a comprehensive, long-term strategy

to protect and transfer your assets; • creating a charitable trust or foundation

for your philanthropic goal; and• the ongoing management of your trust.

A trust can be an effective strategy to transfer wealth to your loved ones.

Current Private investment Counsel strategy

Portfolio weighting• Moderate overweight in equities

• Position in gold where appropriate within client portfolios

• Moderate underweight in bonds, with a somewhat shorter term than benchmarks

• Overweight corporate bonds, where mandates permit

• Major underweight in European banks within international holdings

Percentage return for indices(For the period December 15, 2010 – March 15, 2011)

DEX Universe Bond Index +1.5%

S&P/TSX Composite Index +3.0%

S&P 500 Index +2.3%

MSCI EAFE Index* -3.8%

*Morgan Stanley Capital International Europe, Australasia and Far East Index

44 Investment Outlook Spring 2011

527142 (0411)

Consolidate to simplify your life and finances

As investors approach or enter retirement, it becomes increasingly common for

them to consolidate their holdings with a single provider. There are a number of reasons why clients consolidate their accounts with Private Investment Counsel.

a streamlined approach. Throughout our working lives, it is common to accumulate a variety of investment accounts — group and individual RSPs, spousal RSPs, Locked-in Retirement Accounts (LIRAs), Individual Pension Plans (IPPs), and assorted other accounts.

This can lead to receiving a number of monthly or quarterly account

statements, along with numerous tax forms and documents — the tracking of which can be time-consuming and confusing.

By consolidating with Private Investment Counsel, clients can focus on one deep relationship with their Portfolio Manager, streamline their accounts, and free up time for other pursuits.

more effective portfolios. Very often, investors who hold multiple accounts may actually have duplicate holdings and investments that work at cross purposes with each other.

This can result in less-than-optimal performance, undue risk, and a lack of a tax-effective strategy — especially

when registered and non-registered assets are involved.

Once assets are consolidated, your Portfolio Manager will be in a much better position to develop a comprehensive approach to managing your family’s investments. The result is generally better performance, less risk, and greater tax-efficiency to improve after-tax returns.

lower costs. Consolidating investment accounts may also lead to cost savings. Often, accounts opened in the past may hold investments aimed at the retail investor, which could have high — though often hidden — costs.

When you consolidate with Private Investment Counsel, costs are generally much lower, befitting the private client with a larger portfolio. In addition, while each account in a Private Investment Counsel relationship is customized to meet its particular objectives, all accounts in the relationship are linked for fee-calculation purposes, which lowers the cost for all accounts.

easy transfers. Simply stated, we take care of everything, so you need not be involved with the transferring firm.

For more information on how consolidating your investments can benefit you, contact your Portfolio Manager. n

Consolidating can improve your portfolio´s tax-effectiveness.

The information in this newsletter is current as at March 16, 2011, and does not necessarily reflect subsequent market events and conditions.The information contained herein has been provided by TD Waterhouse Private Investment Counsel Inc. and is for information purposes only. The information has been drawn from sources believed to be reliable. Where such statements are based in whole or in part on information provided by third parties, they are not guaranteed to be accurate or complete. Graphs and charts are used for illustrative purposes only and do not reflect future values or future performance of any investment. The information does not provide financial, legal, tax or investment advice. Particular investment or trading strategies should be evaluated relative to each individual’s objectives and risk tolerance. TD Waterhouse Private Investment Counsel Inc., The Toronto-Dominion Bank and its affiliates and related entities are not liable for any errors or omissions in the information or for any loss or damage suffered.

The Toronto-Dominion Bank and its affiliates and/or its officers, directors, subsidiaries or representatives may hold some of the securities mentioned herein and may from time to time purchase and/or sell same on the stock market or otherwise.No endorsement of any third-party products, services or information is expressed or implied by any information, material or content referred to or included in this newsletter.TD Waterhouse Private Investment Counsel Inc. is a subsidiary of The Toronto-Dominion Bank.TD Waterhouse Private Trust services are offered by The Canada Trust Company.All trade-marks are property of their respective owners.