19

Privatisation & Investment Privatisation & Investment Dr. Abdul Hafeez Shaikh Minister for Investment & Privatisation April, 2005

Privatisation & InvestmentPrivatisation & Investment

Dr. Abdul Hafeez ShaikhMinister for Investment & Privatisation

April, 2005

Key FeaturesKey FeaturesHighly Centralized Economy

Dominant Role of State

High Population Growth

Low Exports and Low Investment Growth

Low Emphasis on Human Development

Declining Development Expenditure

Infrastructure Constraints Population, UrbanisationIncreasing GDP

33

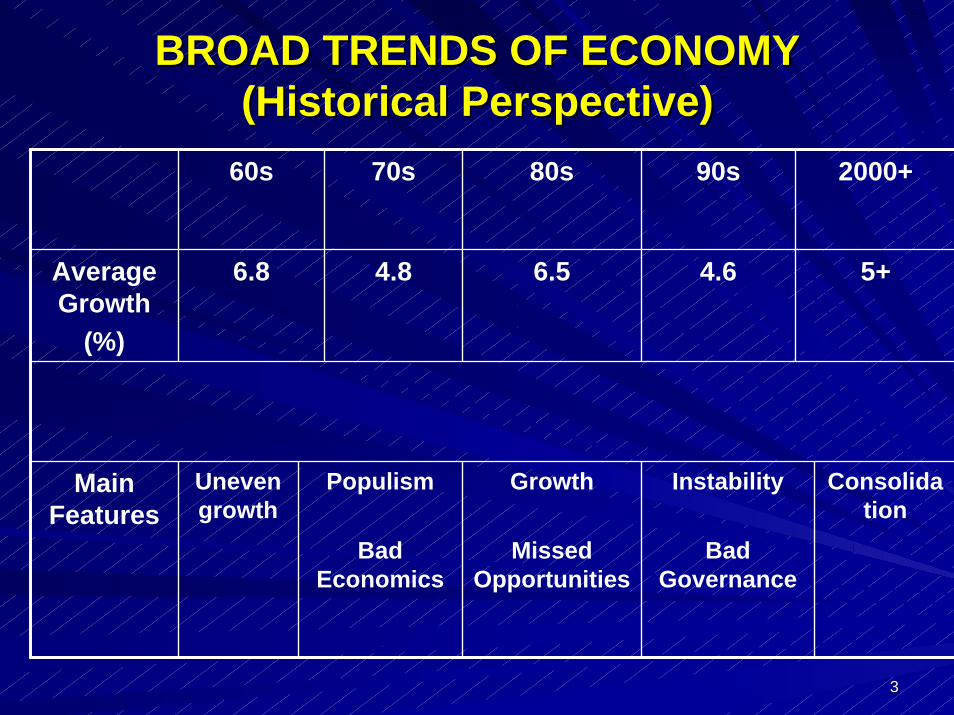

BROAD TRENDS OF ECONOMYBROAD TRENDS OF ECONOMY(Historical Perspective)(Historical Perspective)

Consolidation

Instability

Bad Governance

Growth

Missed Opportunities

Populism

Bad Economics

Uneven growth

Main Features

5+4.66.54.86.8Average Growth

(%)

2000+90s80s70s60s

44

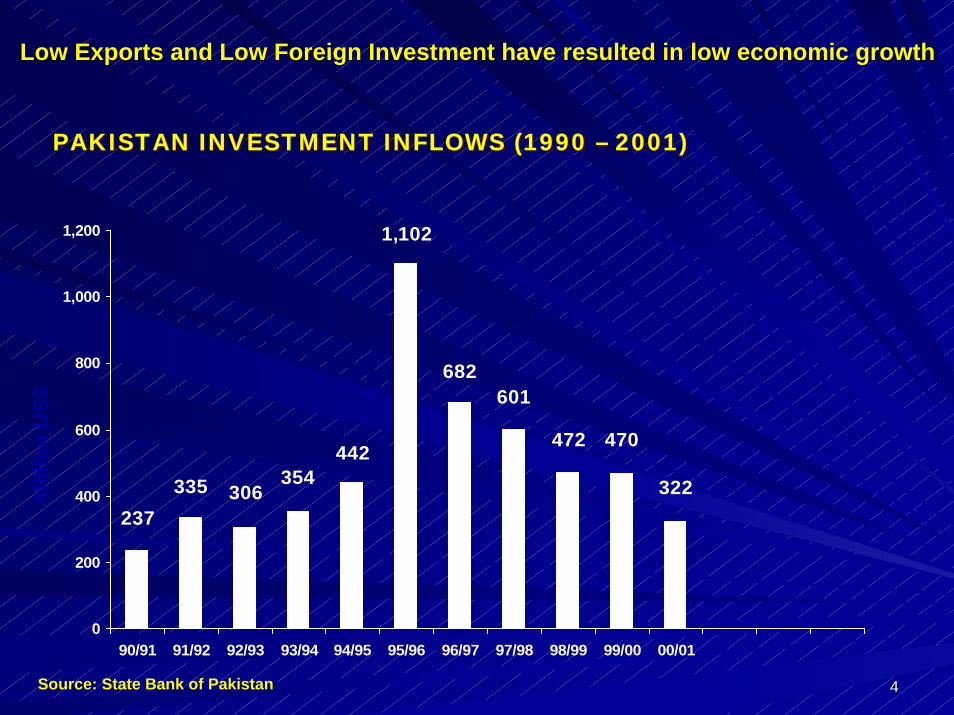

Low Exports and Low Foreign Investment have resulted in low econLow Exports and Low Foreign Investment have resulted in low economic growthomic growth

PAKISTAN INVESTMENT INFLOWS (1990 – 2001) PAKISTAN INVESTMENT INFLOWS (1990 PAKISTAN INVESTMENT INFLOWS (1990 –– 2001) 2001)

237335 306

354442

1,102

682601

472 470

322

0

200

400

600

800

1,000

1,200

90/91 91/92 92/93 93/94 94/95 95/96 96/97 97/98 98/99 99/00 00/01

Source: State Bank of Pakistan

Mill

ion

US$

55

Pakistan’s Investment & Infrastructure Pakistan’s Investment & Infrastructure Needs are EnormousNeeds are Enormous

Investment in infrastructure has been Stagnant Investment in infrastructure has been Stagnant

Public Sector Infrastructure Investment Unlikely to Public Sector Infrastructure Investment Unlikely to Increase in a Big Way:Increase in a Big Way:

-- Fiscal Constraint Fiscal Constraint –– Deficit TargetsDeficit Targets-- competing Needs from Social Sector and Irrigationcompeting Needs from Social Sector and Irrigation

The Private Sector has beenThe Private Sector has been Missing in InfrastructureMissing in Infrastructure

Lack of Private Sector Investment in Infrastructure Lack of Private Sector Investment in Infrastructure Connected to Other Connected to Other Long Term Trends in FDI and Long Term Trends in FDI and PrivatisationPrivatisation

66

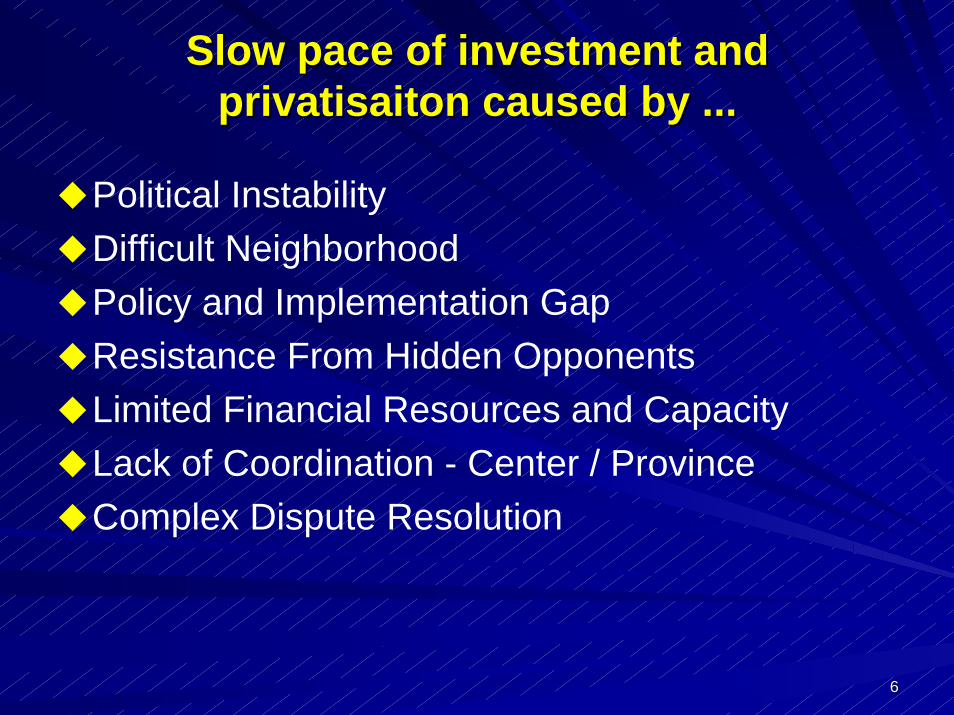

Slow pace of investment and Slow pace of investment and privatisaitonprivatisaiton caused by ...caused by ...

Political InstabilityDifficult NeighborhoodPolicy and Implementation GapResistance From Hidden OpponentsLimited Financial Resources and Capacity Lack of Coordination - Center / Province Complex Dispute Resolution

77

RECENT CONSOLIDATIONRECENT CONSOLIDATION

Debt Position

GDP Growth

FDI Increasing

PS Credit Increasing

Privatisation Success

88

Situation Improving …Situation Improving …

Policy Regime StablePro Business Investment PoliciesImproved Regulation

Regulatory Bodies set up in various sectors: PTA, OGRA, NEPRA etc.

Financial Sector & Capital Market Reform

99

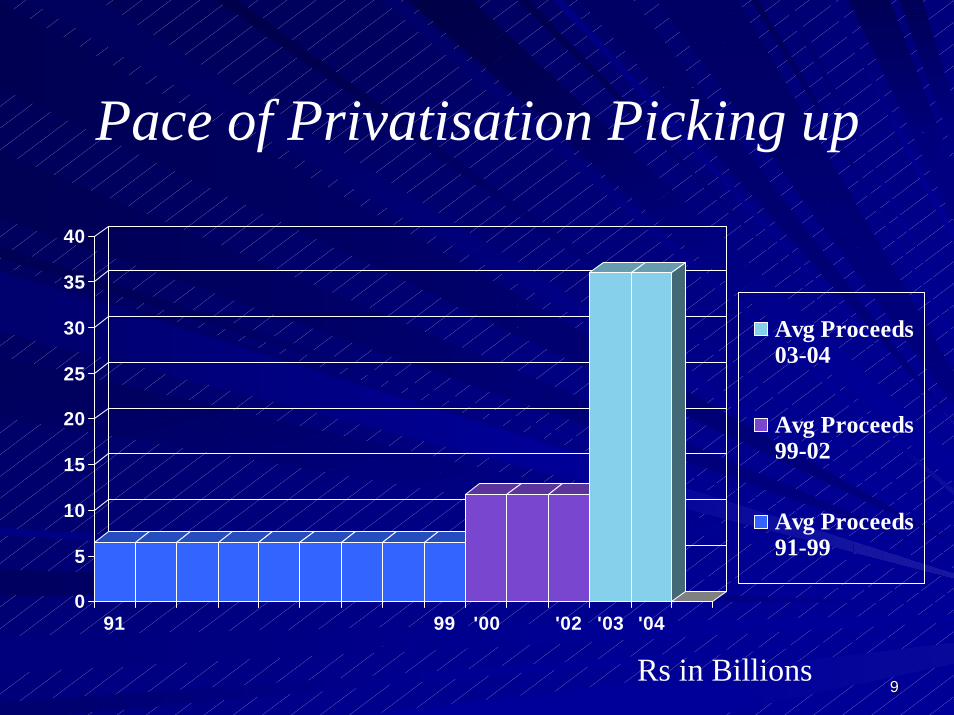

Pace of Privatisation Picking up

0

5

10

15

20

25

30

35

40

91 99 '00 '02 '03 '04

Avg Proceeds03-04

Avg Proceeds99-02

Avg Proceeds91-99

Rs in Billions

1010

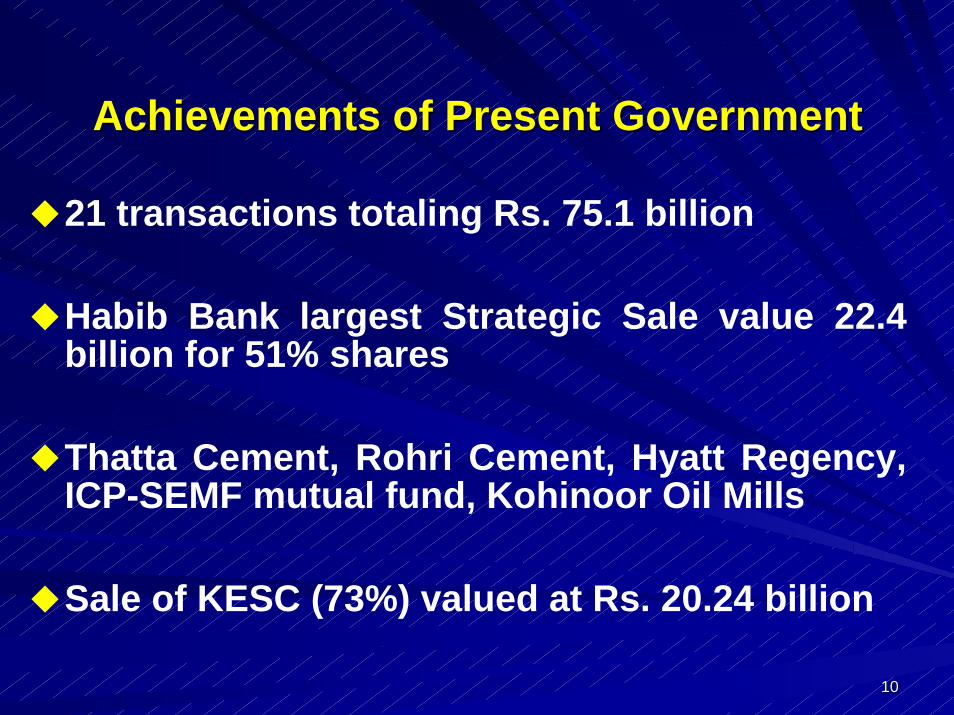

Achievements of Present GovernmentAchievements of Present Government

21 transactions totaling Rs. 75.1 billion

Habib Bank largest Strategic Sale value 22.4 billion for 51% shares

Thatta Cement, Rohri Cement, Hyatt Regency, ICP-SEMF mutual fund, Kohinoor Oil Mills

Sale of KESC (73%) valued at Rs. 20.24 billion

1111

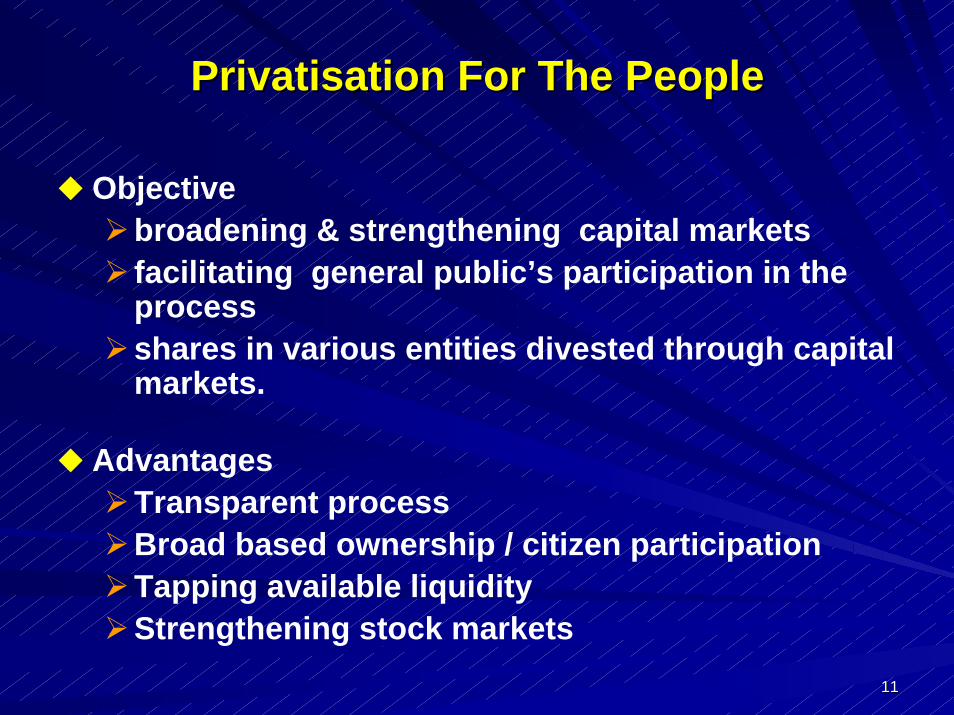

PrivatisationPrivatisation For The PeopleFor The People

Objectivebroadening & strengthening capital marketsfacilitating general public’s participation in the processshares in various entities divested through capital markets.

AdvantagesTransparent processBroad based ownership / citizen participationTapping available liquidityStrengthening stock markets

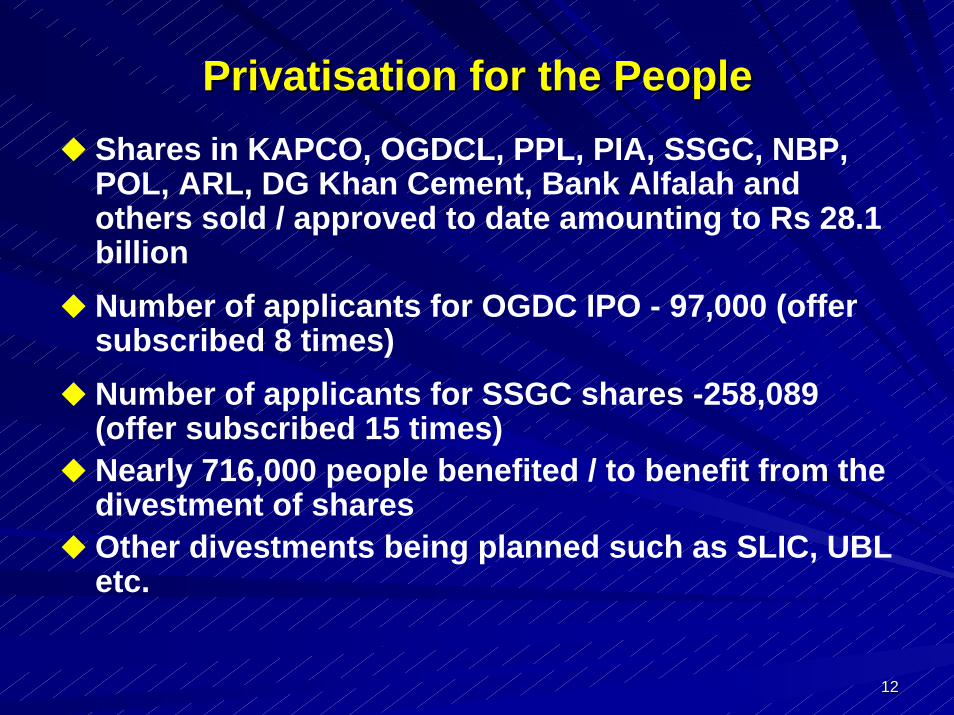

1212

PrivatisationPrivatisation for the Peoplefor the PeopleShares in KAPCO, OGDCL, PPL, PIA, SSGC, NBP, POL, ARL, DG Khan Cement, Bank Alfalah and others sold / approved to date amounting to Rs 28.1 billionNumber of applicants for OGDC IPO - 97,000 (offer subscribed 8 times)Number of applicants for SSGC shares -258,089 (offer subscribed 15 times)Nearly 716,000 people benefited / to benefit from the divestment of sharesOther divestments being planned such as SLIC, UBL etc.

1313

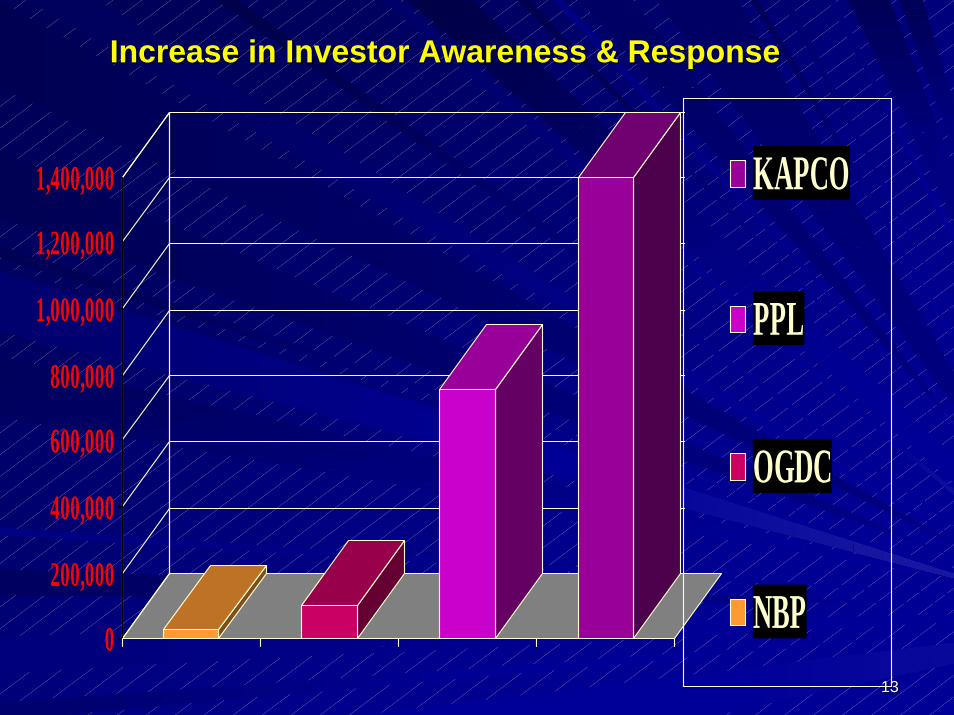

Increase in Investor Awareness & ResponseIncrease in Investor Awareness & Response

0

200,000

400,000

600,000

800,000

1,000,000

1,200,000

1,400,000 KAPCO

PPL

OGDC

NBP

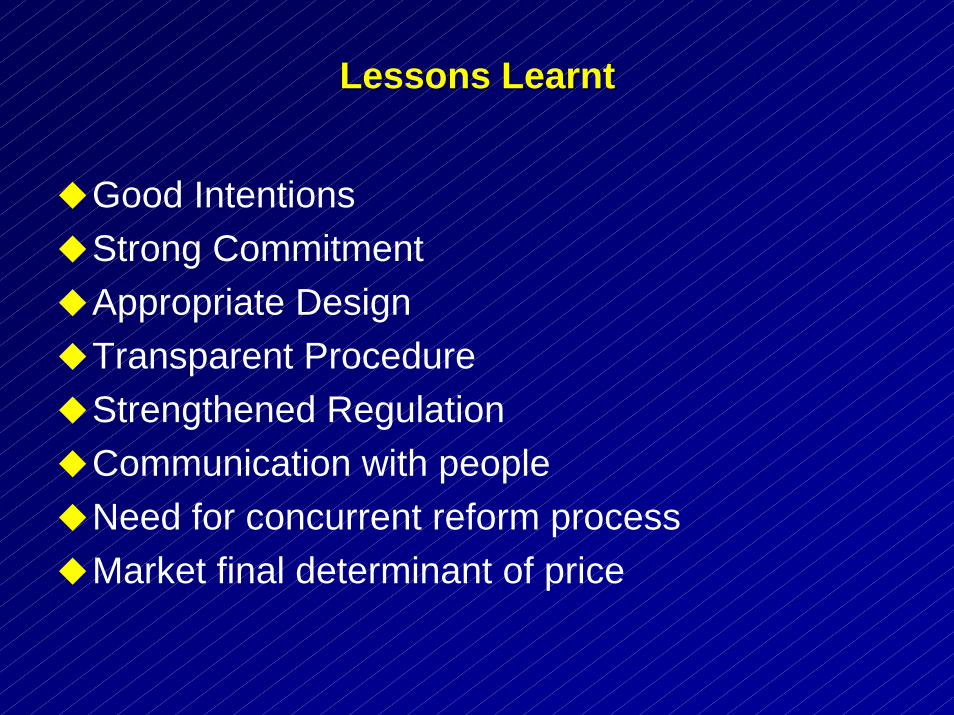

Lessons LearntLessons Learnt

Good IntentionsStrong CommitmentAppropriate DesignTransparent ProcedureStrengthened RegulationCommunication with peopleNeed for concurrent reform processMarket final determinant of price

1515

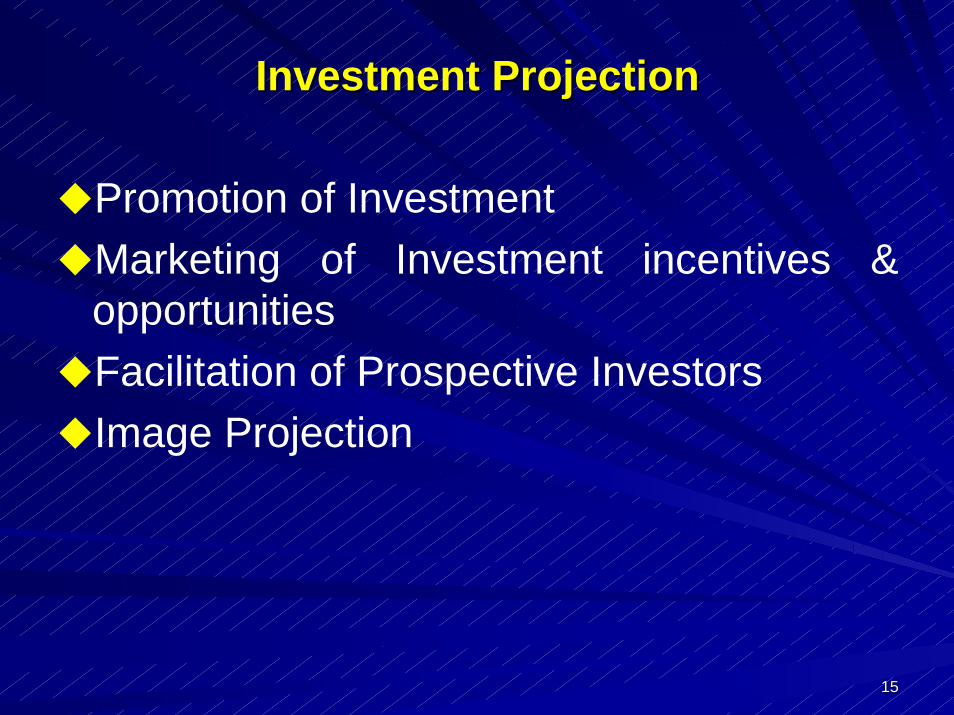

Investment ProjectionInvestment Projection

Promotion of Investment Marketing of Investment incentives & opportunitiesFacilitation of Prospective Investors Image Projection

1616

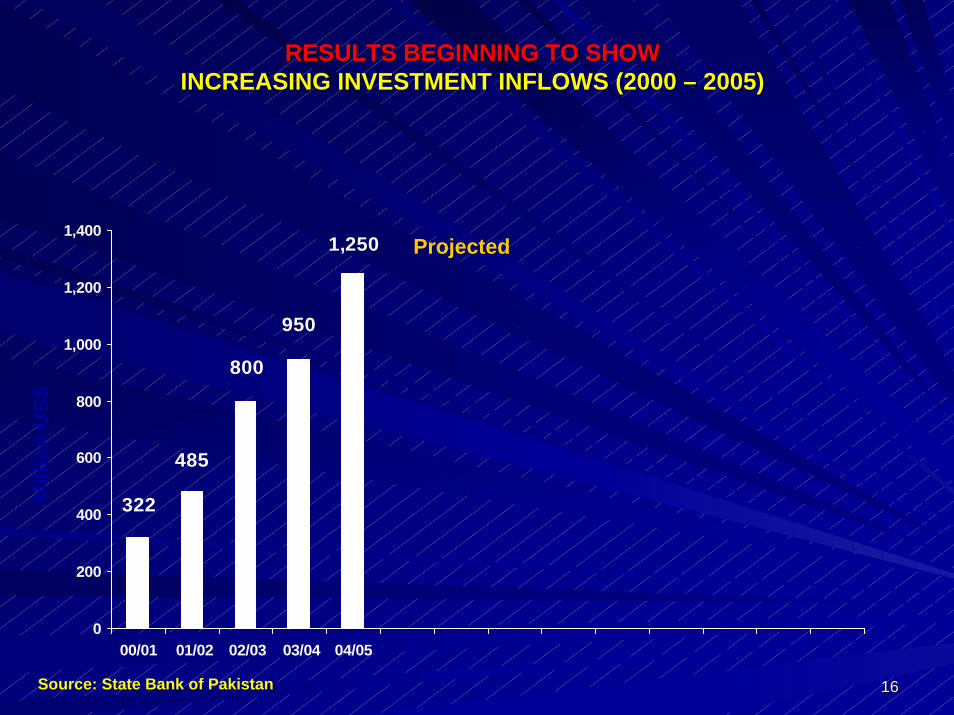

RESULTS BEGINNING TO SHOWRESULTS BEGINNING TO SHOWINCREASING INVESTMENT INFLOWS (2000 INCREASING INVESTMENT INFLOWS (2000 –– 2005) 2005)

322

485

800

950

1,250

0

200

400

600

800

1,000

1,200

1,400

00/01 01/02 02/03 03/04 04/05

Source: State Bank of Pakistan

Mill

ion

US$

Projected

1717

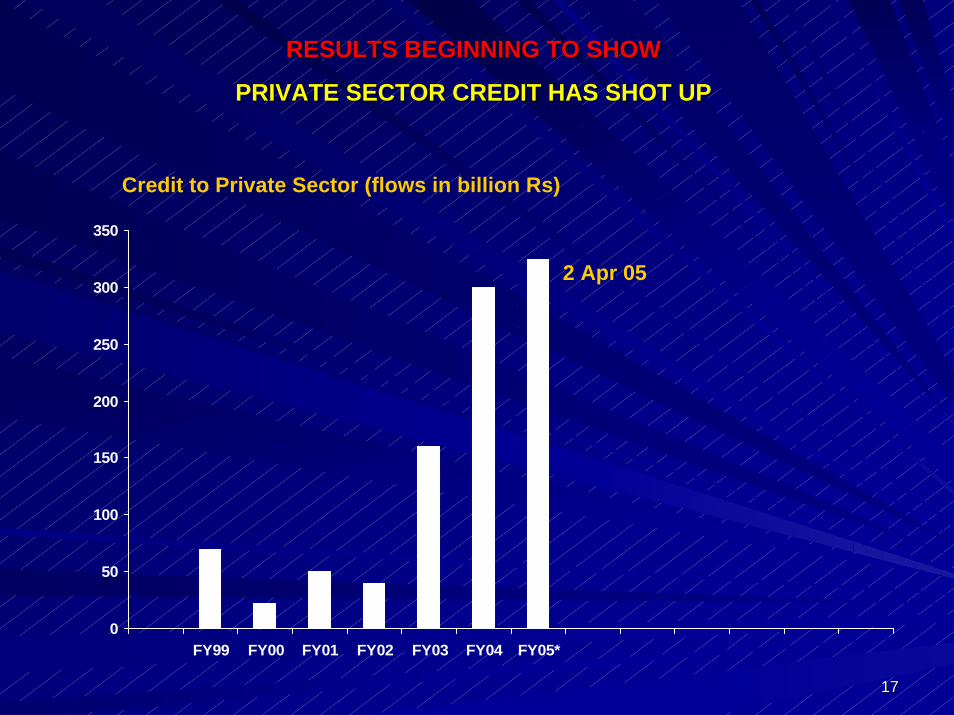

RESULTS BEGINNING TO SHOWRESULTS BEGINNING TO SHOW

PRIVATE SECTOR CREDIT HAS SHOT UP PRIVATE SECTOR CREDIT HAS SHOT UP

0

50

100

150

200

250

300

350

FY99 FY00 FY01 FY02 FY03 FY04 FY05*

2 Apr 05

Credit to Private Sector (flows in billion Rs)

1818

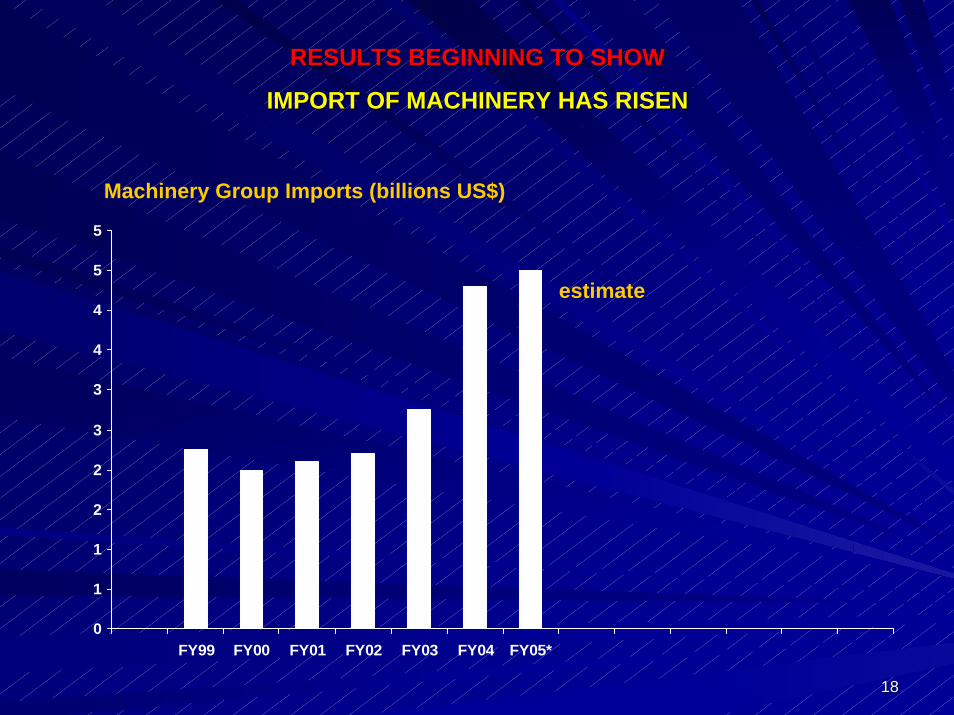

RESULTS BEGINNING TO SHOWRESULTS BEGINNING TO SHOW

IMPORT OF MACHINERY HAS RISEN IMPORT OF MACHINERY HAS RISEN

0

1

1

2

2

3

3

4

4

5

5

FY99 FY00 FY01 FY02 FY03 FY04 FY05*

estimate

Machinery Group Imports (billions US$)

CONCLUDING REMARKSCONCLUDING REMARKS