B efore considering the risk management protocols in Liquified Natural Gas (LNG), it is important to provide a small preface about LNG and its development. LNG is natural gas (predominantly methane, CH4) that has been converted to liquid form for ease of storage or transport. LNG is principally used for transporting natural gas to markets, where it is re-gasified and distributed as pipeline natural gas. It can be used in natural gas vehicles, although it is more common to design vehicles to use compressed natural gas. Its relatively high cost of production and the need to store it in expensive cryogenic tanks has hindered widespread commercial use. The increase in gas demand has brought about the emergence of Floating Storage Re-gasification Units (FSRU). One reason for their growing popularity is the significant reduction in construction speed. It takes approximately 40 months to construct a conventional LNG re-vaporisation terminal, whereas an FSRU using an LNG carrier can be constructed in just 24 months. FSRUs are also able to move location, something that onshore re-gasification facilities cannot do, enabling them to relocate from one region to another as demand shifts, while retaining the ability to trade as an LNG carrier. COMMERCIAL ASPECTS In the commercial development of an LNG value chain, suppliers first confirm sales to the downstream buyers and then sign long-term Making LNG a viable proposition Storage and transport of natural gas is indeed a risky, yet cost-effective venture. Aftab Hasan outlines the risks associated with LNG and mitigating them. contracts (typically 20–25 years) with strict terms and structures for gas pricing. Only when the customers are confirmed and the development of a Greenfield project is deemed economically feasible, can the sponsors of an LNG project invest in their development and operation. Thus, the LNG liquefaction business has been limited to players with strong financial and political resources. Major international oil companies (IOCs) such as ExxonMobil, Royal Dutch Shell, BP, BG Group, Chevron, and national oil companies (NOCs) such as PERTAMINA and PETRONAS are active players. MARKET TREND AND CAPACITY Various state governments may be opposed to Floating LNG technology due to diminished employment opportunities, but commercial reality is that Floating LNG technology is more cost effective. Insurance arrangement for Floating LNG is under pressure due to lack of underwriting appetite and limited capacity in the international market. PREMIUM-ME.COM| ISSUE 37 | JULY/AUGUST 2014 16 COVER STORY The Definitive Middle East Insurance Magazine

Transcript

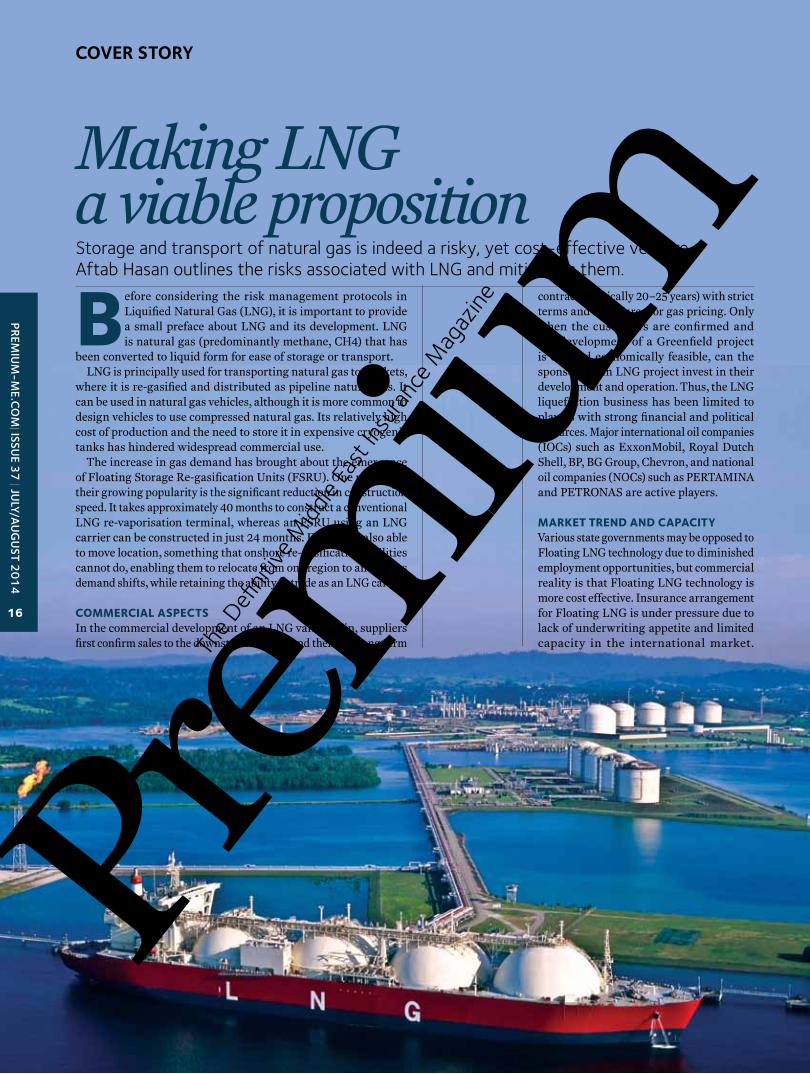

Before considering the risk management protocols in Liquified Natural Gas (LNG), it is important to provide a small preface about LNG and its development. LNG is natural gas (predominantly methane, CH4) that has

been converted to liquid form for ease of storage or transport. LNG is principally used for transporting natural gas to markets,

where it is re-gasified and distributed as pipeline natural gas. It can be used in natural gas vehicles, although it is more common to design vehicles to use compressed natural gas. Its relatively high cost of production and the need to store it in expensive cryogenic tanks has hindered widespread commercial use.

The increase in gas demand has brought about the emergence of Floating Storage Re-gasification Units (FSRU). One reason for their growing popularity is the significant reduction in construction speed. It takes approximately 40 months to construct a conventional LNG re-vaporisation terminal, whereas an FSRU using an LNG carrier can be constructed in just 24 months. FSRUs are also able to move location, something that onshore re-gasification facilities cannot do, enabling them to relocate from one region to another as demand shifts, while retaining the ability to trade as an LNG carrier.

CommerCial aspeCts In the commercial development of an LNG value chain, suppliers first confirm sales to the downstream buyers and then sign long-term

Making LNG a viable propositionStorage and transport of natural gas is indeed a risky, yet cost-effective venture. Aftab Hasan outlines the risks associated with LNG and mitigating them.

contracts (typically 20–25 years) with strict terms and structures for gas pricing. Only when the customers are confirmed and the development of a Greenfield project is deemed economically feasible, can the sponsors of an LNG project invest in their development and operation. Thus, the LNG liquefaction business has been limited to players with strong financial and political resources. Major international oil companies (IOCs) such as ExxonMobil, Royal Dutch Shell, BP, BG Group, Chevron, and national oil companies (NOCs) such as PERTAMINA and PETRONAS are active players.

market trend and CapaCity Various state governments may be opposed to Floating LNG technology due to diminished employment opportunities, but commercial reality is that Floating LNG technology is more cost effective. Insurance arrangement for Floating LNG is under pressure due to lack of underwriting appetite and limited capacity in the international market.

PREM

IUM

-ME.C

OM

| IssUE 3

7 | JU

LY/AU

GU

sT 20

14

16

Cover Story

The

Definit

ive M

iddle

East

Insu

ranc

e M

agaz

ine

Offshore energy insurance is usually placed in the international insurance market, such as Lloyd’s or major continental underwriters. Accepted, specialised policy wordings are utilised in the offshore energy insurance market with limited number of underwriters participating.

Current capacity of the energy insurance market is considered to be around USD3.5 billion, which is low compared with the exposures or sums insured of hull and topsides. Advent of new and unproven technology has created difficulties for the underwriting markets. The current trend is to support proven and validated technology.

risks of lnG Carrier » Accidents during sea voyage: › Grounding – Navigation error › Striking a fixed object or a wreck – Navigation

error › Collision (with vessel or object) – Navigation

error › Unloading/loading » Sudden pull-away and damage of loading/

discharging arms and human injury › Cracking of ship steel hull due to spill of LNG

(super cold shock of -161 degrees Celsius) › Terrorism – Missile attack, boat based

explosive and hijacking› Cargo machinery and cargo containment

failures › Natural risks – Lightning, typhoon,

hurricanes, and tsunami› Other hull/machinery accidents, such as

a fire in engine room on bridge and in accommodation, boilers, steam turbines, main reduction gears, diesel engine damages, and hull structural failures

» Gas cloud » Collision events » Fire in engine room, accommodation and Navigation Bridge » Release of bunker oil » Collisions, groundings of any kind » Man overboard, or piracy » Contact with quay/cargo tank releases of LNG

reduCinG risk and loss preventionSince risk is quite prevalent in such large scale projects, it pays to take measures to reduce risk and prevent losses, especially on LNG carriers in operation, under repair or under construction. Safety in such an operation is key and it goes without saying that reduction of spillage, sloshing, overpressure, vacuum and accidental leaks is crucial. A regular inspection or audit by the crew or ship managers should be practiced daily, yearly or at every arrival. There should also be a safety, security, operational and management inspection or audit carried out every 2.5 years by external surveyors during scheduled dry-docking and maintenance in a shipyard.

Of course, it is also imperative to have improved cargo containment systems. In addition, having a competitive fire fighting and gas detection systems is crucial in reducing risk. Gas detection, safety and firefighting equipment for manual and automatic gas detections such as foam, powder, water curtains and fire hydrants should be readily available.

More importantly, a Home Doctor (Designated Shipyard) concept, standard specification and pricing, crew preventive maintenance plan and master maintenance plan on all vital machineries and systems should be handy.

As a practice, longevity studies for LNG carriers should be undertaken at 20 years for ones that are 25 years’ time chartered. Manufacturer’s service engineers should be used for all vital machineries and systems. Water ballast tanks should be re-coated after 15 to 20 years. With regard to the crew, there should be adequate pre-employment security screening, medical tests rendered and training as well as licensing taken care of; in fact training for crew and ship managers should be continuous.

Proper exclusion and buffer zones (remote area) should be set out between public areas, ships and LNG terminals. In order to prevent terrorist risk, there should be regular security checks at

PREM

IUM

-ME.C

OM

| IssUE 3

7 | JU

LY/AU

GU

sT 20

14

17

Cover Story

CateGory responsiBle party insuranCe

Oil Pollution Liability from wells Oil Company Operator's Extra Expense 1. Clean up cost 1. Cost of Control 2. Liability 2. Redrilling Expense 3. Cost of Control 3. Seepage & PollutionOil Pollution Liability from Rig's fuel Rig Contractor Protection & Indemnity (Third Party Liability)Damage to the Rig Rig Contractor Hull & Machinery 1. Rig itself 2. Sue & Labour 3. Wreck of RemovalDeath/Injury of workers on board Employer Worker's Compensation Injury free offshore evacuation of all 69 personnel onboard the drilling rigFines/Penalties/Punitive Damage Oil Company Contractor No Insurance

from an underwriter’s perspeCtive

SOuRCE: HTTP://WWW.HOPSEMa.gOv.au

The

Definit

ive M

iddle

East

Insu

ranc

e M

agaz

ine

the main gate, berth and on the ship. Entry and routine condition surveys should be taken on behalf of P&I Clubs such as: › JH115A/JH 722 general condition/structural survey on behalf of

hull insurers › JH2006/010 A, B, C, engine room and office management and

condition surveys on behalf of hull insurers and› JH143 risk assessment and loss prevention surveys on construction/

conversion.

Risks to underwriters include:› Untested technologies › More shipyards are building of LNG Carriers› Shortage of skill and trained workers › Use of Sub-contractors › Poorly targeted risk assessment and unrealistic emergency response. › The ship owner and shipyard project teams skill base make a big

difference in the risk profile and quality during construction of LNG carriers.

risk in the lnG supply Chain With the dramatic growth of the liquefied natural gas (LNG) trade worldwide and increased dependence on LNG as the gas fuel of the future, gas-utility companies at the end of the chain need to question whether the LNG chains are still safe, reliable, and well managed. But before diving in to some of the risks, it should be pointed out that historically LNG chains have been safe.

Since its start up in 1964, the LNG industry has proven itself to be well managed. This is because of many factors: › A large proportion of the world’s LNG projects have been managed

in association with the major global oil and gas companies which have applied rigorous standards to safety design and management of plant operations through the chain.

› Major contractors have played their part in building quality facilities with significant risk quality.

› LNG is a clean fuel and as such is considered safer to produce than other fuels. Although there are areas of potential corrosion in gas treatment process upstream of the liquefaction process, the industry has shown itself to have a far better record of reliability and safety than other sectors of the energy industry. Insurance ratings bear this out.

› The LNG shipping industry, which consists of approximately 174 tankers, has accumulated a safety record featuring well in excess of 40,000 cargoes delivered without mishap or major accident.

› Long-term gas supply contracts have provided the framework of successful risk allocation and sharing in the LNG value chain with the bulk of LNG being sold to Japan and Korea.

The current market conditions are now causing insurers to think again about long term policies as this industry is growing with the demand of LNG. There are plenty of options open for LNG operators which should be taken with a comprehensive understanding of the long-term implications covering the risk.

An intelligent insurance broker can help identify and quantify risks and bring them under control. They can create and implement customised solutions employing the most effective blend of risk mitigation, risk transfer, and advanced risk financing. These solutions go beyond traditional property/ casualty insurance programmes to encompass strategies that can help increase a firm's revenue growth, enhance its net income, and strengthen its balance sheet.