Page 1

PROBLEMS AND PROSPECTS OF MUTUAL FUND

INVESTMENTS-A PERSPECTIVE STUDY ON

KERALITES

Submitted to the University Grand’s Commission,New Delhi

In partial fulfillment of the requirements for the Minor Research Project.

By

RATHEESH.K.NAIR

POST GRADUATE & RESEARCH DEPARTMENT OF COMMERCE

GOVT.COLLEGE MADAPPALLY

VADAKARA,

KOZHIKODE

January 2016

Page 2

Declaration

I hereby declare that the project report entitled "PROBLEMS AND

PROSPECTS OF MUTUAL FUND INVESTMENTS-A PERSPECTIVE

STUDY ON KERALITES" is a bonafide project work done by me and I further

declare that this project work has not been submitted to any University or

Institution.

Kollam Ratheesh.K.Nair

Date: 03.01.2017

Page 3

Acknowledgement

It is with a sense of achievement and pride that I complete my project work.

It has been made possible by the unstinting support of many people. These few

words only convey my formal thanks but cannot convey the depth of my gratitude to

them.

I express my sincere gratitude to the Principal, Govt.College Madappally,

faculty members at Department of Commerce and staff for their valuable

suggestions and kind cooperation.

I am deeply indebted to University Grants Commission for allotting the

funds for the smooth conduct of the project.

I take this opportunity to thank my fellow Ph.D. students and friends who

were always there in times of need.

I am deeply indebted to my parents and my wife for the moral support and

encouragement in my academic pursuits.

Above all I am thankful to the God, Almighty who has given me the

strength,power and opportunity to complete this work successfully.

Ratheesh.K.Nair

Page 4

Abstract

Kerala, obviously, one of the leading States in India in terms of both human

development and literacy. Unfortunately, the State could not realize such growth in

capital market investments. The conditions are not different in mutual fund

investments also. Hence, this research took efforts to investigate the underlying

reasons for such financial market lagging in Kerala through the assessment of the

problems and prospects of mutual fund investments from the perspectives of Investors

there. The study also analysed the behavior and perception of investors for looking into

the potentials of mutual fund investment in the State. Under a descriptive research

framework, through rigorous statistical procedures on the multiple responses of

investors, the study was able to make out prolific findings relevant to the development

and growth of mutual fund market in Kerala.

In Kerala, because of insufficient savings, the people prefer to invest in riskless

assets like bank deposits, post office savings etc. However, investors surveyed in this

research convinced their interests in market linked assets given the conditions of

improved earnings. Inadequate investor protection measures and imperfect market

conditions often perceived as the main risk factors that persuade the investors to keep

their place outside the fund markets. Fund management still is a problem exists at

aggravate level even among the mutual fund investors of the state. Better governance,

customised investment products with more innovative features enable the Mutual

Funds to penetrate more even into rural parts thereby can widen their client base in

Kerala. Such actions can improve the investment conditions of the State thereby

contribute more to its economic growth.

Page 5

Contents

Chapter 1 Introduction ------------------------------------------------------ 1

1.1 Introduction --------------------------------------------------------- 1

1.2 Statement of the Problem------------------------------------------ 1

1.3 Significance of the study ------------------------------------------ 3

1.4 Scope of the Study ------------------------------------------------- 4

1.5 Objectives of the Study -------------------------------------------- 4

1.6 Operational Definitions -------------------------------------------- 5

1.7 Hypotheses ---------------------------------------------------------- 7

1.8 Research Design ---------------------------------------------------- 7

1.8.1 Source of Data --------------------------------------------- 7

1.8.2 Survey Instrument ----------------------------------------- 8

1.8.3 Survey Area ------------------------------------------------ 8

1.8.4 Measurement of Variables ------------------------------- 8

1.9 Sampling Design -------------------------------------------------- 10

1.10 Period of Reference ---------------------------------------------- 14

1.11 Tools of Analysis -------------------------------------------------- 14

1.12 Limitations of the Study ------------------------------------------ 15

1.13 Chapter Framework ----------------------------------------------- 15

References ----------------------------------------------------------------- 16

Chapter 2 Review of Literature ------------------------------------------- 17

Chapter 3 Mutual Funds and Regulation in Indi ------------------------ 3.1 Introduction 60

3.2 Trends in Resource Mobilisation by Private and public

Sector Mutual Funds in India. ----------------------------------- 61

3.3 Mutual Fund schemes ------------------------------------------- 64

3.4 Scheme –wise Resource Mobilisation -------------------------- 66

3.5 Asset Under Management in India:Geographical

Distribution ---------------------------------------------------- 67

3.6 State wise Penetration of Mutual Fund ---------------------------- 72

3.7 Mutual Fund investors -------------------------------------------- 78

Page 6

3.7.1 Investor interest in Mutual Fund investment in

India ------------------------------------------------------- 79

3.8 Private and public Sector Mutual Funds, investor

participation and resource mobilisation -------------------------- 86

3.9 Preferences of Kerala Investors in Mutual Funds ------------ 86

3.10 Preferences of Kerala Investors in Mutual Fund schemes 87

3.11 Investor protection and regulatory mechanism of

Mutual Fund ----------------------------------------------- 83

3.11.1 Securities and Exchange Board of India --------------- 84

3.11.2 Association of Mutual Fund Industry ------------------ 84

3.11.3 Stock exchanges ------------------------------------------- 85

3.11.4 Reserve Bank of India ----------------------------------- 85

3.12 Rights with respect to Management of the fund --------------- 89

3.13 Regulatory Developments ---------------------------------------- 99

3.13.1 Investor Grievances and Redressal ------------------ 102

3.13.2 Redressal of complaints received against popular

mutual funds…………………….…………105

3.17 Conclusion -------------------------------------------------------- 114

Chapter 4 Problems and prospects of Mutual Fund Investments in

Kerala 117

4.1 Introduction ------------------------------------------------------ 117

4.2 Banking and Insurance products and Number of AMC

Branches in Kerala ------------------------------------- 127

4.3 AUM by Geography - Consolidated data for MF

Industry in Kerala ---------------------------------------- 128

4.4 Investors in Kerala ---------------------------------------------- 142

4.5 Behaviour of Individual Investors of Kerala ---------------- 176

4.6 Preference of Investment Avenues ---------------------------- 176

4.6.1 Investor Profile and Investment Preferences:

Test of Association ------------------------------------- 177

Page 7

4.6.2 Relationship between Investor Category and

Preference of Investment ------------------------------------ 178

4.7 Perceived change in investment avenues given the

increased savings ------------------------------------------------ 191

4.8 Investor‟s priorities over investment features of

Mutual fund ------------------------------------------------------ 201

4.9 Investors perception towards Problems in Mutual Fund

Investment --------------------------------------------------------------- 203

4.10 Prospects of Mutual Fund Investments in Kerala ------------ 233

4.10.1 Prospective features in Mutual Fund

Investment 235

4.10.2 Factors influencing the prospects of mutual

Fund Investment ---------------------------------------- 235

4.10.2.1 Fund Promotion ------------------------------ 237

4.10.2.2 Role of Regulators --------------------------- 238

4.10.2.4 Service provided by Mutual funds -------- 239

4.10.2.4 Fund performance --------------------------- 239

4.10.2.5 Fund quality ---------------------------------- 239

4.11 Prospects of Mutual Fund investment-Discriminant

analysis ------------------------------------------------------------ 239

4.11.1 Canonical Discriminant Functions ------------------- 241

4.12 Conclusion -------------------------------------------------------- 245

Chapter 5 Summary, Findings and Suggestions ----------------------- 246

5.1 Introduction ------------------------------------------------------ 246

5.2 Regulatory mechanism of Mutual Fund ---------------------- 248

5.3 Public and Private Sector Institutional Participation ------- 249

5.4 Investor Behaviour in Kerala ---------------------------------- 251

5.5 Problems of Mutual Funds ------------------------------------ 253

5.6 Services for Mutual Fund Investment ---------------------------- 254

5.7 Suggestions and Recommendations -------------------------- 256

5.7.1 Product Design ----------------------------------------- 256

5.7.2 Use of Technology ------------------------------------ 258

5.7.3 Investor Awareness ------------------------------------ 258

Page 8

8.3 Conclusion -------------------------------------------------------- 259

8.4 Contributions of the Study ------------------------------------- 260

8.5 Scope for Further Research ------------------------------------ 260

Bibliography -------------------------------------------------------------------------- 262

Appendix ------------------------------------------------------------------------------ 277

List of Presentations & Publication --------------------------------------------- 282

Page 9

List of Tables

Table 1.1: Unit holding pattern of Mutual Funds Industry in India and

Kerala-31.03.2010 ------------------------------------------------------- 15

Table 1.2: Selection of sample units from sample frame ----------------------- 17

Table 3.1: Worldwide Number of Mutual Fund Schemes and Net Assets

-2014 ---------------------------------------------------------------------- 105

Table 3.2: Trends in Resource Mobilisation by Mutual Funds 2000 to

2015 ----------------------------------------------------------------------- 106

Table 3.3: Mutual Fund schemes as on 31-March 2015 ------------------------ 72

Table 3.4: Scheme-wise Resource Mobilisation and Assets under

Management by Mutual Funds as on March 31, 2015 ----------------- 75

Table 3.5: AUM by Geography - Consolidated data for Mutual Fund

Industry ------------------------------------------------------------------- 109

Table 3.6: State Wise Penetration of Mutual Funds in India- November

2015 ----------------------------------------------------------------------- 113

Table 3.7: Unit holding pattern of all mutual funds as on March 31,

2015 ------------------------------------------------------------------------ 80

Table 3.8: Private and public Sector Sponsored Mutual Funds, investor

participation and resource mobilisation-2014-15 ------------------ 111

Table 3.9: Number of Respondents preferred different Mutual Funds ------- 220

Table 3.10: Number of Respondents preferred different Mutual Fund

Scheme ------------------------------------------------------------------- 222

Table 3.11: Receipt and Redressal of Investor Grievances by SEBI-2000

to 2015 -------------------------------------------------------------------- 103

Table 3.12: Complaints received against Mutual Funds (MFs) during 2013-

2014-which are top six mutual funds in Kerala as on 31-03-

2014 --------------------------------------------------------------------------- 226

Table 4.1: Geographical Factors of Kerala --------------------------------------- 118

Table 4.2: Demographic Factors- Population (As Per 2011 Census) -------- 120

Table 4.3: Average Banking &Insurance product in Lakhs &Total

No.Of AMC Branches in Kerala ------------------------------------- 127

Table 4.4: AUM by Geography - Consolidated data for MF Industry ------- 129

Table 4.5: Penetration of Mutual Fund in Kerala - November 2015 --------- 130

Table 4.6: Mutual Fund wise contribution to AAUM of category of

schemes for Mar-2015 in Kerala ------------------------------------- 131

Table 4.7: Household use banking services – Kerala --------------------------- 142

Page 10

Table 4.8: Preference of Investment by investors in Kerala ------------------- 176

Table 4.9: Association between Investor Category and Preference of

Investment --------------------------------------------------------------- 178

Table 4.10: Change investor preference under the condition of increased

savings -------------------------------------------------------------------- 191

Table 4.11: Change in investor preference at the increased saving level:

Paired t test results ------------------------------------------------------ 193

Table 4.12: Investor‟s expectation about investment features of Mutual

fund ----------------------------------------------------------------------- 202

Table 4.13: Investors perception towards problems in Mutual fund

investment --------------------------------------------------------------- 205

Table 4.14: KMO and Bartlett's Test of Sphericity------------------------------- 206

Table 4.15: Total Variance Explained ---------------------------------------------- 207

Table 4.16: Key factors affecting selection of mutual fund products ---------- 208

Table 4.17: Tests of Equality of Group Means- With factor scoring ---------- 240

Table 4.18: Eigen values - With factor scoring ----------------------------------- 241

Table 4.19: Functions at Group Centroids - With factor scoring --------------- 241

Table 4.20: Wilks' Lambda - With factor scoring -------------------------------- 242

Table 4.21: Standardized Canonical Discriminant Function Coefficients -

With factor scoring ----------------------------------------------------- 243

Table 4.22: Structure Matrix- With factor scoring ------------------------------- 243

Table 4.23: Classification Results a, c - With factor scoring ------------------- 244

Page 11

List of Figures

Fig. 3.1: The graph indicates the growth of AUM over the years in

India -------------------------------------------------------------------------- 108

Fig. 3.2: Mutual fund schemes as on 31-March 2015 ----------------------------- 72

Fig. 3.3: AUM by Geography - Consolidated data for MF Industry-

AMFI ------------------------------------------------------------------------- 110

Fig. 3.4: Composition of AAUM in Kerala as on November 2015 ------------ 114

Fig. 3.5: Unit holding pattern of all mutual funds as on March 31, 2015 ---------- 80

Fig. 3.6: Private and public Sector Sponsored Mutual Funds, investor

participation and resource mobilisation-2014-15 ---------------------- 111

Fig. 3.7: Preference of Mutual funds ----------------------------------------------- 221

Fig.3.8: Preference of Mutual fund schemes ------------------------------------- 222

Fig. 4.1: Average Banking &Insurance product in crores & Total

No.Of AMC Branches in Kerala ----------------------------------------- 128

Fig. 4.2: AUM by Geography - Consolidated data for MF Industry ----------- 129

Fig. 4.3: Preference of Investment by investors in Kerala ---------------------- 177

Fig. 4.4: Relationship of Investor Category and Preference of

Investment ------------------------------------------------------------------- 178

Fig. 4.5: Change investor preference under the condition of increased

savings ----------------------------------------------------------------------- 192

Page 12

Abbreviations

AAUM Average Asset Under Management

ACE AMFI's Code of Ethics

AGNI AMFI's Guidelines and Norms for Intermediaries

AMC Asset Management Company

AMFI Association of Mutual Funds in India

ARN AMFI Registration Number

ASBA Application Supported by Blocked Amount

AUM Asset under Management

CAGR Compounded Annual Growth Rate

CII Confederation of Indian Industry

CRM Customer Relationship Management

CSE Cochin Stock Exchange

DP Depository Participant

ECS Electronic Clearing Service

ELSS Equity Linked Savings Scheme

ETF Exchange Traded Funds

FCNR Foreign Currency Non-Resident account

FEMA Foreign Exchange Management Act, 1999

FII Foreign Institutional Investor

FIRC Foreign Inward Remittance Certificate

FMCG Fast Moving Consumer Goods

FMP Fixed Maturity Plan

FOF Fund of Funds

FPI(s) Foreign Portfolio Investor(s)

GDP Gross Domestic Product

GIC General Insurance Corporation

GSDP Gross State Domestic Product

HNI High Net worth Investors

HUF Hindu Undivided Family

IDFs Infrastructure Debt Funds

IFA Independent Financial Advisor

Page 13

IRDA Insurance Regulatory and Development Authority

ISC Investor Service Centre

KIM Key Information Memorandum

KVP Kisan Vikas Patra

KYC Know Your Customer

LIC Life Insurance Corporation of India

MF Mutual Fund

MFI Mutual Fund Investors

MIN Mutual Fund Identification Number

MMMF Money Market Mutual Fund

NAV Net Asset Value

NBFC Non-Banking Finance Company

NCAER National Council for Applied Economic Research

NEFT National Electronic Funds Transfer

NFO New Fund Offer

NISM National Institute of Securities Markets

NMFI Non Mutual Fund Investors.

NNP Net National Product.

NOC No Objection Certificate

NPA Non-Performing Asset

NRE Non-Resident External account

NRI Non-Resident Indian

NRO Non-Resident Ordinary account

NSC National Savings Certificate

NSDP Net State Domestic Product

NSFE National Strategy for Financial Education

OCBs Offshore Corporate Bodies

PAN Permanent Account Number

PFRDA Pension Fund Regulatory & Development Authority

PIO Person of Indian Origin

PPF Public Provident Fund

PWC PricewaterhouseCoopers

Page 14

QFIs Qualified Foreign Investors

R& T Agents Registrar and Transfer Agent

RBI Reserve Bank of India

REMFs Real estate mutual funds

RGESS Rajiv Gandhi Equity Savings Scheme

ROI Return on Investment.

RTA Registrars & Transfer Agents

RTGS Real Time Gross Settlement

SAI Statement of Additional Information

SAT Securities Appellate Tribunal

SCORES Sebi COmplaints REdress System

SEBI Securities and Exchange Board of India

SHGs Self Help Groups

SID Scheme Information Document

SIP Systematic Investment Plans

SMS Short Message Service

SoA Statement of account

SRO Self Regulatory Organisation

STP Systematic Transfer Plan

STT Securities Transaction Tax

SWP Systematic Withdrawal Plan

TER Total Expense Ratio

UTI Unit Trust of India

` (Rs.) Rupees

Page 15

1.1 Introduction

Mutual funds are the trusts which pool the scattered savings of investors and

invest in marketable security portfolios. The term 'fund' is used to indicate the

mutual fund, or any of its schemes. They create a range of products from

investment avenues called mutual fund schemes to meet the varying needs and

preferences of investors. Investors choose mutual funds based on the objective of

the fund and their own investment objectives. Professional fund managers take care

of the funds of investors and ensure steady return and capital appreciation.

The benefits from the investment of the pooled financial resources accrue to

the investors who contribute to the pool. Thus, there is mutuality in the contribution

and the benefit between the fund and the investors. That is why the fund is known

as 'mutual fund‟. In United States, mutual funds have already been taken over by

financial institutions and banks in offering the best possible returns on a set of

diversified portfolios. In India many financial institutions and public sector banks

have started their own mutual funds in line with global trend. But, this does not

imply that mutual funds are full of benefits or intrinsic worth. They have their own

set of problems relating to regulations, services, costs, performance, profitability,

financial instability, decline of Net Asset Values (NAVs) which have been causing

big concern to investors. The growing awareness of such issues discourages the

prospective investors of mutual funds in many states of India including Kerala.

However, favourable economic variables in the country indicate that Kerala has a

bright future for mutual funds. It is highly useful to examine the factors

responsible for this incongruous state of mutual fund investment in Kerala so as to

throw light on its future prospects.

Page 16

1.2 Statement of the Problem

A mutual fund, in its rudimentary conceptualisation, is a collection of stocks

and/or bonds, where an investor holds a unit, which represents a part of the fund

holding thereof. A proportionate sharing of income earned through such investors and

capital appreciations witnessed by the schemes are duly carried out. It must, however,

be mentioned that this proportional sharing by the unit holders is governed by the

number of units owned by them. Mutual fund is, therefore, the most suitable

investment option available to a common man as it provides an opportunity to invest in

a diversified, yet professionally managed portfolio. Mutual funds act as a gateway to

invest in big companies to an ordinary investor with his small investment.

Mutual funds offer benefits such as diversification, access to equity and debt

markets at low transaction costs, liquidity etc. to the investors. Given these

benefits, one would imagine that Indian households, characterized with gross

domestic savings close to 28 per cent of the total GDP, one of the highest in the

world, would congregate to invest their savings in mutual funds. Moreover mutual

fund industry needs to get healthy participation from all states of the country.

However, while considering the data published by AMFI the geographical

distribution of assets under management (AUM) across cities in India is highly

skewed in favour of the top five cities (Mumbai, Delhi, Chennai, Kolkata and

Bangalore) which contribute over 70 per cent of the entire AUM in the country.

The remaining 30 per cent is shared by the rest of the country.

The AUM/GDP ratio is the best indicator of the portion of income in a

given state or district is being invested in mutual funds (SEBI, 2014).On looking at

the investment conditions in India as a whole, the AUM/GDP ratio stand at 7 per

cent while that of Kerala it is only at 3 per cent (AMFI,2015).Being a state with

higher literacy rate of 93.91 per cent (Economic review,2012),the state expects to

create a good investment culture among the people .However, relatively large

Page 17

deviation from the national average in AUM /GDP ratio signals the importance of

many questions to answer :Why the investors of Kerala are showing less interest in

mutual fund investment? What are the factors affecting the investment behaviour of

Keralites? What are the problems faced by mutual fund investors in Kerala? Do the

market regulators take appropriate measures to market the mutual fund products

among investors? Since there is no prior study investigating these issues are

available, particularly in the context of Kerala the present study makes a serious

attempt to probe into these issues in detail.

1.3 Significance of the study

The Indian mutual fund industry has developed rapidly over the past ten

years. The industry achieved a high AUM from Rs. 3.6 trillion in 2007 to Rs. 6.13

trillion in 2010, with an impressive growth rate of 16.2 per cent per year. From an

average GDP growth rate of 8 to 9 per cent during the period from 2008 to 2011, the

Indian economy is now growing at 7.4 percent in 2014-1 15(Annual report, 2015).

Economic growth of a country is closely associated with its domestic

savings (Jangili, 2011) .No country can grow without having sound capital base

supplied with its domestic savings and investment. The nature and rate of savings

in an economy implies the rate of economic growth. Mutual fund investment

schemes contribute good channel for profitable investments to households. So a

study analysing the mutual fund markets definitely help investors including

household investors to know more about the benefits of the schemes and motivate

them to park their savings with the fund investments. This can lead economic

growth through capital formation and financial market stability.

Financial markets are exposed to fast change in the modern globalised

world. More innovative products, but with complex features, are emerging into the

market and the investment of which demand sound knowledge base and good

analytical skills. Normally it is beyond the reach of investors to gain mastery over

Page 18

investment science while optimising their investment function. Mutual funds are

the creations of professional investment managers who have substantive knowledge

in investment finance. Through this study ,both actual and potential investors can

make out the various attributes of mutual fund schemes in terms of its risk, return

and fund management efficiency that enable them to reap the benefits of

professional investments with minimal complexity.

Professional investment managers can understand the general investor

preferences and behaviour of Keralites. They can also identify the prime forces that

restraining the investors of the state to be part of the mutual fund market .The

information on both of these shall enable them to design fund scheme that has a

perfect match with the investor expectations.

Policy makers of the country can grab useful insights on the problems of

mutual fund investments from the perspective of investors in terms of the fund

quality, fund distribution and fund performance. This may provide valid inputs for

them to draft apposite policy framework conducive for the growth of mutual fund

market in the state.

1.4 Scope of the Study

The study emphasises the problems and prospects of Mutual fund

investment with respect to Keralites. The study covers both rural and urban

counterparts. The research primarily aims at tracking investors‟ preferences and

priorities of different investment avenues and identifying the key features of a

mutual fund. Such information helps to design a new mutual fund product or

redesign the existing schemes suitable for the financial market conditions of the

economy. Besides the factors identified, the study provides key information inputs

regarding problems of mutual fund investment and the expectations of investors in

deciding marketing mix variables that guide the fund managers in designing

profitable investment schemes in future for the Indian market.

Page 19

1.5 Objectives of the Study

The clear definition of the research problem precincts its objectives as follows.

1. To identify the public and private sector institutional participation in

Mutual fund.

2. To examine the regulatory mechanism of Mutual fund.

3. To study the extent of responsibility on the part of Mutual fund financial

institutions in the reduction of investor grievances.

4. To assess the investor behaviour and mutual help of investors and experts in

Mutual Fund Investment.

5. To evaluate the service provided by Mutual fund financial institutions in

Kerala.

1.6 Operational Definitions

The variables, terms of specific measurement and testing criteria used in this

study defined as follows.

♦Asset Management Company

Asset Management Company (AMC) is the asset manager of the mutual

fund and is responsible for running the day to day operations of the mutual fund.

The AMC is appointed by the trustees in consultation with the sponsor of the fund

and with the approval of SEBI.

♦Assets Under Management (AUM)

Assets of a mutual fund refer to the market value of the securities held in the

portfolio. There may be few receivables and accrued income, which are current

assets. These are added to the portfolio value to get the total Assets Under

Page 20

Management (AUM) of the fund, its average for a period is known as Average

Asset Under Management (AAUM).

♦ Centroids

It is the mean discriminant score of members in the group. It used for

designing a decision rule to classify an investor into MFI/NMFI category.

♦Discriminant coefficient

It is similar to regression coefficient, reflects the relative contribution of

each of the predictor variable on the discriminant function. A small value of the

discriminant coefficient means that the impact of a unit change in a predictor

variable is small in the discriminant function score.

♦Fund Manager

Fund Manager is the person who handles the money of the investors. He is

concerned with decision regarding the investments, protection of value of the

original investments and generation of a steady return on the original investment.

♦Intermediaries

All persons or entities concerned in selling and distribution of mutual fund

products including inter alia brokers, consultants, sub-brokers, financial advisors,

channel partners, sole proprietor firms, partnership firms, companies or called by

any other name, but shall not consist of collection centers, where there is no

element of advice, and it is only a counter for issuing forms and collecting

completed applications.

♦Investor Categories

Investor Categories or Investor type is referred to as an individual or retail

investor who has currently invested in any investment products. It includes Mutual

fund Investor and Non Mutual Fund Investor. An investor whose name appears in

Page 21

the portfolio records of different mutual funds is Mutual fund Investors‟ (MFIs); all

other investors are Non Mutual fund Investors‟ (NMFIs).

♦Investment Features.

Investment features include Safety, Liquidity, Return, Tax Savings, Govt.

Regulation and Innovative Services. Among these safety, liquidity, return, tax

savings are grouped into investor objectives. Government Regulation and

contemporary services are grouped into investor requirements.

♦Investment Risk

Risk refers to the volatility of portfolio‟s value. Protection from volatility of

portfolio‟s value or risk is Safety. Risk perception of the investors towards the

mutual fund products is one of the factors to be analysed for studying the level of

risk aversion.

♦Net Asset Value

Net assets of a fund refer to the market value of the portfolio, plus accrued

incomes, less current liabilities and accrued expenses.Net Asset Value (NAV) is the

value per unit at current market prices computed as net assets divided by units

outstanding. Net Asset Value indicates the intrinsic worth of a scheme.

1.7 Hypotheses

The major hypotheses for the study include

1. Private sector Mutual Funds help to satisfy the investment needs of Mutual

fund investors than Public sector Mutual funds.

2. Stringent regulatory frame work restricts the volume of Mutual Fund

Investment.

Page 22

3.The greater the reduction of investors grievance by Mutual Fund institution

the lower the mutual fund investment.

4. Investors in Kerala are showing diverging behaviour in terms of their mutual

help of investors and experts in Mutual Fund Investment.

5.There is no relationship between after investment service provided by Mutual

Fund companies and investment in Mutual funds.

1.8 Research Design

The research design for the study is basically descriptive in nature but the

objective of the study is to explore and obtain clarity about the problem situation

and factors influencing the prospects of mutual fund investment. Here, the study

makes use of discriminant model for deciphering sustainable marketing mix

variables in the design and distribution of a new mutual fund product.

1.8.1 Source of Data

The study is based on primary as well as secondary data. Data collection

process was made in two different stages. In the first stage, a review of literature

was undertaken so as to acquaint with the various aspects of the study to formulate

the conceptual framework for the research. In the second stage, primary data were

collected with the help of a pre-tested and structured questionnaire that was

finalised after a pilot study. The model of the questionnaire is given in Appendix.

Web sites of RBI, SEBI and AMFI constitute the prime secondary data

sources. Many published and unpublished reports, text books, periodicals, journals,

seminar proceedings, government publications and commission reports were also

used for hypothesis designing, sampling consideration and for validating the

information collected through primary source.

Page 23

1.8.2 Survey Instrument

After discussion with officials of AMCs, stock broking firms, agents and

distributors of MF products and experts in this field, a structured and quantifiable

questionnaire was developed. The questionnaire consists of three parts. First part

comprises of questions related to demographic features and saving/investment

avenue preferences of investors. The second part of the instrument deals with

questions for assessing the problems and prospects of mutual fund investment from

the perspectives of Investors, and the last part consists of questions related to

selection of mutual funds by the Mutual fund investors.

1.8.3 Survey Area

The present study focuses on the investors residing at Kerala. Kerala is a

small state in India blessed with good climate and abundant natural resources. For

the purpose of study Kerala grouped into three regions, it includes, Northern region

(Kasargode, Kannur, Kozhikode, Wayanad, Malappuram) Central region

(Palakkad, Thrissur, Ernakulam, Idukki,) Southern region (Alappuzha, Kottayam

Pathanamthitta, Kollam, Thiruvanathapuram). Central region is the main centers

for mutual fund business in Kerala since they have highest AUM(AMFI,2015).

The study was conducted across Central region districts in Kerala.

1.8.4 Measurement of Variables

The concepts and constructs of this study converted into empirically testable

and observable variables. It includes dichotomous, categorical, continuous and

other indefinite set variables.

♦ Saving and investment avenue preferences

For measuring the Preference of Investment Avenue by investors in Kerala,

multiple responses was used, the researcher has considered ten investment

Page 24

alternatives which have been measured by marking top three investment options by

investor preference on investment with current saving and that with increase in

saving. For knowing priorities‟ the investor‟s preferences ranking and rating

methodology were followed.

♦ Perception towards Investment Avenues

The analysis of perception towards investment avenues are measured in

terms of the investors‟ priority of investment features. Ranking and rating

methodology was followed to prioritize the investor‟s preferences.

♦ Risk Perception for Mutual Funds

Risk perception has been measured on a 5 point scale ranging from low risk

„1‟ to high risk „5‟.

♦ Perception towards Mutual fund investment

In order to measure the investor‟s perception towards Mutual fund

investment, six investment features, such as safety, liquidity, return, tax saving,

Govt. regulation and service are considered and these variables were measured on a

five point Likert-type scale ranging from „least requirement‟ to „most requirement‟.

♦ Problems of Investors

In order to measure the problems of investors regarding the mutual fund

investment 15 variables were considered and these variables were measured through

five point Likert-type scales ranging „least considered‟ to „most considered‟.

♦ Mutual fund selection parameters

In order to measure the investment decision parameters for selecting Mutual

fund Investment four factors were considered and these factors were measured by

marking appropriate decision option for mutual fund investment.

♦ Mutual Fund services

Page 25

For measuring the Mutual Fund services, considered by the investor while

selecting mutual fund products, four variables of mutual fund service were taken

into consideration and these items were measured through five point Likert-type

scale ranging from „least considered‟ to „most considered‟.

♦ Prospective features in Mutual Fund Investment

The prospective features in mutual fund investment have measured with

fifteen variables of investors‟ expectations in mutual fund investment and these

items were measured through a five point Likert-type scale ranging from „least

considered‟ to „most considered‟.

♦ Prospects of mutual fund investment

For measuring the prospects of mutual fund investment in Kerala four

factors of investors‟ expectations in mutual fund investment (through factor

analysis) were taken into consideration. Discriminant analysis is used to estimate

the per cent of investors correctly classified as Mutual Fund Investor/Non Mutual

Fund Investor (to predict group membership), to find out the predictor variables are

relatively better in discriminating between Mutual Fund Investor/Non Mutual Fund

Investor, to classify a investor into one of the two groups by building a decision

rule and cut-off score.

1.9 Sampling Design

It includes the process of selecting sample of investors from the population

of investors.

♦ Population for the Study

Page 26

Individual investors in Kerala form the universe or population for the study.

In this study particularly for analysing the prospects of mutual fund investment in

Kerala, the opinion of both mutual fund investors and non mutual fund investors

are highly essential. Accordingly the population has two parts in this research.

As per the data collection plan, primary data were collected from the

individual Mutual fund investors living in Kerala and invested in mutual fund

schemes. As on March-2010 there are nearest 19 Lakh Mutual Fund investors folio

with 27 AMC‟s in Kerala (AMFI, 2010).According to the data Compiled from the

records of SEBI and AMFI). The unit holding pattern of all mutual funds in India

stood at 4,63,27,683 folios by the end of March 2010 among these, 4.1per cent

folios from Kerala which constitute 18,99,435 folios (Table 1.1).

As per the data collection plan of the researcher, primary data were

collected from the individual Mutual fund investors living in central region of

Kerala and invested in mutual fund schemes. The investors in central region of

Kerala who have so far not invested in mutual funds provide the universe for

NMFI.

Page 27

Table 1.1 Unit holding pattern of Mutual Funds Industry in India and

Kerala-31.03.2010

Unitholding pattern of Mutual Funds Industry -INDIA AND KERALA.

Category

Number of

investors

Accounts

% to total

investors

Accounts

Net assets (Rs.crore)

% to total net

assets

Individuals 46,327,683* 97.07 245,390.28 39.77

NRIs 943,482 1.98 27,428.86 4.45

FIIs 216 0.00 6,335.00 1.03

Corporates/

Institutions/ Others 452,330 0.95 337,812.58 54.75

TOTAL 47,723,711 100.00 616,966.72 100.00

Individuals in Kerala 18,99,435* 4.1 4588.01 0.02

Source: Compiled from the Official Records of SEBI -Annual Report-2010 and AMFI-

geographical distribution of Mutual Fund Investors.

*there may be more than one folio of an investor which might have been counted

more than once and therefore actual number of investors may be less.

Page 28

The entire population (universe-18, 99,435 folios and approximately 19 lakh

Mutual fund investors) is divided into strata (grouped into three regions) which are

mutually exclusive and collectively exhaustive. Northern region (Kasargode,

Kannur, Kozhikode, Wayanad, Malappuram) Central region (Palakkad, Thrissur,

Ernakulam, Idukki and Southern region (Alappuzha, Kollam, Kottayam,

Pathanamthitta, Thiruvanathapuram).

The investors in Kerala who have so far not invested in mutual funds

provide the universe for NMFI. Financial advisors from the central region (from

four districts) include 230 ARN holder‟s (Table 1.2). They provide a list of NMFI

which might be the prospective investors in Mutual Fund investment from their

district.

♦Sample size

Since the investor populations in Kerala are quite large, the study

determined the sample size of Investors using the approach of Cochran (1963). The

equation used for this purpose is:

Where, n is the sample size, Z2

is the abscissa of the normal curve that cuts

off an area α at the tails (1 - α equals the desired confidence level), e is the desired

level of precision, p is the estimated proportion of an attribute that is present in the

population, and q is 1-p. The value for Z is found in statistical tables which contain

the area under the normal curve.

In this study, assuming p=0.5 (maximum variability under normal

distribution with 95 per cent confidence level and ±5 per cent precision. The

resulting sample size is 385, i.e.

Page 29

= 385

The study rounded off this figure to 400. Accordingly 200 MFIs and 200

NMFIs were selected.

♦ Sample Frame and Selection of Sample units

The population of 19 lakh Mutual fund investors have their accounts (folio)

in 27 AMC‟s in Kerala, these AMC have 58 branches all over Kerala (AMFI,

2010).The size of sample in each region is proportional to the number of AMC

branches in each region. In central region 24 AMC branches and 230 ARN holders.

Page 30

Source:Compiled from the official records of AMFI*No of AMC Branches

Financial advisors with ARN Holders in Kerala as on 31March 2015.

Sample Frame

S.No. Region District

MFI NMFI

Total sample size of

Investors

AMC Branches

% Sample size-MFI

Total no of Financial advisors with ARN Holders

% Sample size NMFI

1

CENTRAL

Palakkad 2 8.33 17 29 12.61 25 42

2 Thrissur 7 29.17 58 65 28.26 57 115

3 Ernakulum 15 62.50 125 112 48.70 97 222

4 Idukki 0 0.00 0 3 1.30 3 3

Total 24 100 200 230 100.00 200 400

Page 31

The final sampling units of 200 MFIs were selected from the list provided

by AMCs‟ and was based on judgment sampling method. The active involvement

of fund investors measured in terms of frequency of investment, amount of

investment and number of schemes they held provide the basis for judgment in

sample selection.

For a comprehensive analysis of the problems and prospects related to

mutual fund in Kerala a sample of 200 Non Mutual Fund Investors (NMFI) were

also selected. Financial advisors from the three regions include 520 ARN Holder's.

The size of sample in central region is proportional to the number of financial

advisors in the region. At first advisors are selected on simple random basis from

the list of ARN holders (central region) in the AMFI website. The selected ARN

holders has provided a list of 2002 investors who have not so far preferred mutual

funds as the destination point of their investment .To ensure parity in comparison

200 NMFI were selected on systematic random basis .For this purpose the study fix

10 (2002/200) as the sampling interval. From the numbers included in the interval,

six has randomly chosen, thereafter every 6th

investor in the list provided has been

selected as the final sample unit of NMFI for the study and the procedure has

completed the selection of 200 NMFIs. Thus the total sample size for the study

became 400 investors: 200 MFIs and 200 NMFIs.

1.10 Period of Reference

Data required from the investors is very sensitive and indicative in nature as it

comprises of the information regarding their savings and investments. Most of the

investors are hesitant and unsecure in providing this kind of data on mails and phone

calls. Hence, only possible way was self administered questionnaire. The survey was

conducted during the period of 2013 January to 2014 March. Secondary data collected

for the study were relating Mutual funds from 1964 to 2013-14.However, a longer

duration and latest improvements has also been considered wherever necessary.

Page 32

1.11 Tools of Analysis

The researcher has administrated rigorous statistical procedure for drawing useful

inference from the collected data. The selection of the statistical design was based on

both the objective pursued and the nature of the data used. The analytical methodology

covered wide range of statistical tools of parametric or non parametric nature.

Chi square analysis as a test of association of attributes has been extensively

used in this study. Association of attributes like demographic features, investor

preferences and that of investor category with perception towards investment

features, the level of risk perception and decision parameters for mutual fund

investment were examined using Chi square analysis.

Independent sample t test verified the statistical significance of differences

in mean perception score of MFIs and NMFIs towards various aspects of their

investment programmes. Paired occurred t test examined whether there was any

significant changes in investor preference at the increased savings levels.

Exploratory factor analysis was employed to reduce the number of

variables/statements representing various problems of mutual fund investments into

specific number of factors explaining the related problems. Such procedure can

simplify the inference process; similarly the same methodology was adopted to

identify the prospective features of mutual fund investment. Again using the same

factor loading canonical discriminant analysis predict the investment features in the

order of their priority which possibly included in the mutual fund innovation in

future for canvassing more number of investors from NMFI group to MFI group.

1.12 Limitations of the Study

The present study is subject to the following limitations.

1. Some of the respondents are not ready to disclose their full investment

details.

Page 33

2. The study is based on primary data; hence personal bias of the respondents

might have affected the results of the study.

3. The finding and implementation of the study are limited to 800 selected

investors in Kerala.

1.13 Chapter Framework

In order to present the research report in a perfect and easily understandable

manner, it is classified into seven chapters.

The Chapter -1: INTRODUCTION -This chapter focuses on the introduction,

statement of the problem, significance of the study, scope of the study, objectives

of the study, operational definition, hypotheses, research design, sampling design,

reference period, primary data collection, tools of analysis, limitations and chapter

frame work.

Chapter 2: REVIEW OF LITERATURE- In this chapter, an effort is made to

review the available literature. It specifically reviewed the saving and investment,

laws, regulations, literacy and marketing, analysis of financial intermediation, fund

performance and investor behaviour. It helps to identify the research gap in the

field of mutual fund.

Chapter 3: MUTUAL FUNDS AND REGULATION IN INDIA: The third

chapter gives an overview of Trends in Resource Mobilisation by Private

and public Sector Mutual Funds in India. State Wise Penetration of Mutual

Fund , Mutual Fund investors , Preferences of Kerala Investors in

Mutual Funds and schemes, Investor protection and regulatory

mechanism of Mutual fund, regulatory developments, Investor Grievances

and Redressal.

Page 34

Chapter 4: Problems And Prospects Of Mutual Fund Investments In Kerala.

: This chapter deals with geographic, demographic and economic factors in

Kerala,Investors in Kerala, , behaviour of individual investors includes preference

and perception towards investment avenues of Keralites. It also analyses the

problems of quality and performance of Mutual fund investment, decision

parameters for selecting mutual fund investment in Kerala. This chapter finally

reports the statistical procedures adopted for analysing the prospects of MF

investment, investors‟ expectations, prospective features in mutual fund investment

and factors influencing the prospects of mutual fund investment. It is also devoted

to discriminant model for deciphering sustainable marketing mix variables in the

design of a new mutual fund product.

Chapter 5: SUMMARY, FINDINGS AND SUGGESTIONS- The last chapter

presents the major findings of the study, summary of findings and implications,

suggestions and recommendations, conclusion and scope for future research in the

field.

References

1. AMFI (2010) Geographical distribution of Mutual Fund Investors.

Geographical distribution of Mutual Fund Investors and Compiled from the

records of AMCs.

2. AMFI (2015) Industry Trends, https://www.amfiindia.com/Themes/

Theme1/ downloads/home/ industry-trends-may-2015.pdf, http://www. amfiindia.

com/research-information/aum-data/classified-average-aum-31/3/2015

3. Annual Report (2014-15) Ministry of finance (budget division- Advance

Estimates) Govt.of India: Page V.

4. Cochran, W. G. (1963). Sampling Techniques, 2nd Ed., New York: John

Wiley and Sons, Inc.

Page 35

5. Economic Review (2012) State Planning Board,Thiruvanathapuram, Kerala,

India.

6. Jangili Ramesh (2011) Causal Relationship between Saving, Investment

and Economic Growth for India – What does the Relation Imply? - Reserve

Bank of India Occasional Papers, Vol. 32(1), pp25-39.

7. SEBI (2014) Development Research Group Studies 2013 - 14, Securities

and Exchange Board of India: p66.

………….………….

Page 36

2.1 Introduction

The Indian mutual fund industry has developed rapidly over the past 10

years. Although a large number of studies have been carried out on the growth and

financial performance of mutual funds in India, not much light has been shed on

the causes for the low penetration of mutual funds in Kerala. The earlier studies

paid more focus to performance measures, structure of fund, fund characteristics,

managerial skills and behavioural patterns over time. The existing studies are very

few and very little information is available about investor perceptions towards the

problems and prospects of a mutual fund in Kerala. The following studies justify

the relevance and importance this study and helps to identify the variables for the

problems and prospects of a mutual fund investment in Kerala.

Nalini (1996) pointed that, mutual funds create awareness among urban and

rural middle class people about the benefits of investment in capital market,

through profitable and safe avenues. Mutual fund could be able to make up a large

amount of the surplus funds by making people invest these funds.

Ramamurthy and Reddy (2005) conducted a study to evaluate recent trends

in the mutual fund industry and draw a conclusion that the main beneficiaries will

be the small investors “due to efficient management, diversification of investment,

easy administration, nice return potential, liquidity, transparency, flexibility,

affordability, wide range of choices and a proper regulation governed by SEBI”.

Mohanty (2006) analyzed the weakness of mutual funds. They are non

availability of tailor-made schemes; no guarantee of returns, no control over costs,

problem of managing large corpus, volatility of return depends on market

conditions, which is subject to frequent market volatility. Market mutual funds

Page 37

scheme is for short period where return is not profitable and the instruments are

lesser in number.

Surjit (2006) analysed the relationship between investors and mutual funds.

Investors have started believing in mutual funds to manage their hard- earned money.

Mutual funds are those institutions that can give maximum satisfaction to their

investors by diversifying the portfolio. The mutual funds are becoming popular among

the people who are more risk-averse than pure equity investors. Carefully managed

mutual funds can ensure optimum returns even during turbulent times in the market

and that makes the mutual fund a good choice among the retail investors. Due to the

reduction in the bank interest rates and high degree of volatility in the Indian stock

market, investors are looking for an alternative for their small time investment which

can provide them a higher return and also safety to their investments.

Ahmed and Ahuja (2006) evaluated the cause and effect relationship

between mutual fund investment decision and fund family, fund size, type of fund,

type of portfolio and schemes, risk involved of the fund manager, past performance

of the fund, liquidity factors and current market conditions.

Sasaki and Rathiha (2008) pointed out that the different variables which

influence to invest on mutual funds are safety, liquidity, stability, speculative

values, diversification and low cost. Through the study the researcher found that,

the most important factors leading to mutual fund investments are risk freeness ,

income, savings and cost.

Thompson and Choi (2001) examined the role of laws governing investor

protection, transparency of reporting, Insider trading, Taxation, the quality of

enforcement of the laws, potential conflicts of interest between the fund and the

fund investors and the ownership concentration across several countries and their

financial development.

Page 38

Bhalla (2004) concluded that investors do not need to be familiar with the

characteristics of the different types of mutual funds. Many investors do not

understand what they are buying. With so many choices, investors risk making the

wrong ones. Besides investing in appropriate and high-cost mutual funds, investors

also buy laggards. There is no shortage of mediocre performers.

Singh and Chander (2004) analysed that, the perceptions about mutual

funds in the view of general investor feels that different regulatory bodies like

SEBI and others have not been able to regulate and control the working of mutual

funds so as to safeguard the small investors‟ interest.

Khorana et al. (2005) found that consistent with related findings from the

law and economics literature, the mutual fund industry is larger in countries with

strong rules, laws, and regulations, specifically where mutual fund investors‟ rights

are better protected. The industry is smaller in countries where barriers to entry are

higher, measured by the effort required to set up a new fund. The fund industry is

larger in countries with a wealthier and more educated population, and where the

industry itself is older. Finally, the fund industry is larger in countries in which

defined contribution pension plans are more prevalent. These results indicate that

laws and regulation, supply-side, and demand-side factors simultaneously affect the

size of the mutual fund industry.

Chander and Singh (2006) studied the preference of investors, the study

revealed that, investor‟s decision to invest in a particular mutual fund is affected by

different sources from where information about working of that fund becomes

available to investor; they also opined that the occupation groups differ

significantly in their perception about the returns received from the mutual fund.

Muller and Weber (2010) investigated the consequences of financial literacy

in the context of mutual fund investments. They found that the level of financial

literacy is not related to the performance of the actively managed funds. In contrast,

Page 39

overconfidence might prevent subjects from investing passively. A positive relation

was found between the belief of being better than average in identifying superior

investments and the likelihood of buying an active fund, thus confirming this

notion. Also, better-than-average thinking is positively correlated with financial

expertise.

Barber et al. (2005) argued that the purchase decisions of mutual fund

investors are influenced by salient, attention-grabbing information. Investors are

more sensitive to salient in-your-face fees, like front-end loads and commissions,

than operating expenses; they are likely to buy funds that attract their attention

through exceptional performance, marketing, or advertising. They found

consistently negative relations between fund flows and front-end load fees. A

negative relation between fund flows and commissions charged by brokerage firms

was also documented. In contrast, no relation (or a perverse positive relation) was

found between operating expenses and fund flows. Additional analyses indicate

that mutual fund marketing and advertising, the costs of which are often embedded

in a fund‟s operating expenses, account for this surprising result.

Gurunathan (2007) examined, the investors need protection from the various

malpractices and unfair practices made by the corporate and intermediaries. As the

individual investors‟ community and the investment avenues are on the rise, it is

interesting to know how the investors shall be protected through various

legislations. The present positive attitude of investors is heartening though investor

sentiments have been shaken by the various scandals.

Confederation of Indian Industry (2010) observed that Indian Mutual fund

Industry is incapacitated by loads, investor awareness, governance and risk

management, technology and low retail participations.

Page 40

Grubber (1996) attempted to study the problem relating to the fast growth of

mutual funds in spite of lower performance of actively managed portfolios. The

study revealed that, mutual funds had negative performance compared to the

market and provided evidence of persistency of underperformance. Sophisticated

clients withdrew money from mutual funds during the period of low performance

whereas mutual funds found money from disadvantaged clientele leading to the

faster growth of funds.

Sondhi and Jain (2005) examined the performance of equity mutual funds

classified on the basis of public sector and private sector. The paper evaluated the

performance by comparing the returns to bench mark indices of Nifty and Sensex

and found that the returns generated by private sector and public sector mutual

funds are very inferior to market returns.

Bello (2005) matched a sample of socially responsible stock mutual funds

matched to randomly select conventional funds of similar net assets to investigate

differences in characteristics of assets held, degree of portfolio diversification and

variable effects of diversification on investment performance. The study found that

socially responsible funds do not differ significantly from conventional funds in

terms of any of these attributes. Moreover, the effect of diversification on

investment performance is not different between the two groups.

Selvaraj and Devi (2007) examined the performance of mutual funds, they

opined that “the performance of an actively managed fund largely depends on the

investment decisions of its manager. Statistically, for every investor who

outperforms the market, there is one who underperforms. Among those who

outperform their index before expenses, though, many end up underperforming

after expenses. Before expenses, a well-run index fund should have average

performance. By minimizing the impact of expenses, index funds should be able to

perform better than average”

Page 41

Agarwal et al. (2009) examined the performance of hedge funds relative to

traditional mutual funds and found that trading strategies will improve the

performance of hedge funds. Gil-Bazo et al. (2009) have examined the market for

equity mutual funds and found that Funds with worse before-fee performance

charge higher fees and that better fund governance may bring fees more in line with

performance.

Gangadhar (1992) identified mutual funds as the prime vehicle for

mobilization of household sector‟s savings as it ensures the triple benefits of steady

return, capital appreciation and low risk. He identified that open-end funds were

very popular in India due to its size, economies of operations and for its liquidity.

Investors opted for mutual funds with the expectation of higher return for a given

risk, greater convenience and liquidity.

Rajan,R.V., (1997) highlighted the segmentation of investors on the basis

of their characteristics, investment size, and the relationship between stage in life

cycle of the investors and their investment.

Massa et al. (1999) identified a set of systematic factors that explain a

significant amount of the variation in flows. They examined common component to

mutual fund investor behaviour and tried to find out which asset classes may be

regarded as economic substitutes by the participants in the market for mutual fund

shares. They found that flows into equity funds, both domestic and international,

are negatively correlated to flows to money market funds and precious metals

funds. This suggests that investor rebalancing between cash and equity explains a

significant amount of trade in mutual fund shares. The negative correlation of

equities to metals suggests that this timing is not simply due to liquidity concerns,

but rather to sentiment about the equity premium. This paper also finds that the

factors derived from flows alone explain as much as 45 per cent of the cross-

sectional variation in mutual fund returns.

Page 42

Walia and Kiran (2009) analysed mutual fund as an investment avenue is

preferred by those investors who don‟t want to take complete risk of capital market

volatility or those investors who want to rely on professional knowledge of mutual

funds AMCs. Survey results reveal the fact that very few investors rank mutual

funds as most preferred investment avenue and rank it at first position.

Basil (2013) the service quality is the dominant factor influencing fund

selection behaviour. The fund preference of mutual fund investors depends on their

time horizon and risk perception. Mutual fund investors in Kerala give more

preferences towards open-ended and growth oriented (equity funds) schemes.

Although research on mutual fund is quite extensive in India and

international context, the studies investigating the behavioural aspects of fund

investment are relatively scanty. Moreover, most of the research has selected

sample from the mutual fund investor group only for surveying their perception or

experience on different aspects of fund investment. No academic research in India,

particularly in Kerala has included the non mutual fund investor group in the

survey. While probing in to the reasons for their apprehensions or difference

towards the fund investment. Thus the present study proposes to carry out survey

among both MFI‟s and NMFI‟s for identifying the problems and prospects of

mutual fund investment in Kerala. With high literacy rate, larger per capita and

lower contribution to the mutual fund segment, Kerala definitely provide a good

representation of sample for studying the problems and prospects of mutual fund

investment.

………….………….

Page 43

Chapter 3

MUTUAL FUNDS AND REGULATION IN INDIA

3.1 Introduction

Worldwide Net Assets shows United States have 15,852.34 USD Billions Total

Net Assets in 2014(Table-3.1). The mutual fund industry in India started in 1963 with

the formation of Unit Trust of India, at the initiative of the Government of India

and Reserve Bank of India. The Indian mutual fund industry is one of the fastest

growing sectors in the Indian capital and financial markets. The latest available

mutual fund data shows that the AUM has risen significantly, to Rs.19,94,985 crore

(USD 192 billion) by May 2015(AMFI,2015). With the bifurcation of the erstwhile

UTI which had in March 2000 more than Rs. 76,000 crores of assets under

management and with the setting up of a UTI Mutual Fund, conforming to the

SEBI Mutual Fund Regulations, and with recent mergers taking place among

different private sector funds, the mutual fund industry has entered its current phase

of consolidation and growth.

Table-3.1 Worldwide Number of Mutual Fund Schemes and Net Assets -2014

Top ten Countries and India’s Total Net Assets (In USD Billions) and Number of Mutual

Fund Schemes #

Sl.No. COUNTRY Total Net Assets (In USD

Billions)

Number of Mutual Fund

Schemes

2010 $ 2014 $ 2010 2014 1 United States 11,832.99 15,852.34 7,554 7,923

2 Luxembourg 2,512.87 3,208.26 9,353 9,839

3 Australia 1,455.85 1,601.13 N/A N/A

4 Ireland 1,014.10 1,547.34 2,899 3,462

5 France 1,617.18 1,391.27 7,791 7,082

6 United Kingdom 854.41 1,182.18 2,204 1,920

7 Brazil 980.45 989.54 5,618 8,560

8 Canada 636.95 981.80 2,117 3,164

9 Japan 785.50 780.64 3,905 5,404

10 China 364.99 708.88 660 1,763

11 INDIA 111.421

*(613979-Crore)

134.63

*(825240-Crore)

658

* (882)

723

*( 1638)

Notes: (1) N/A = not available

Page 44

2-#Country in which more than 700 Billion USD in total Net Asset in 2014.

Source: International Investment Funds Association (2015 Investment Company Fact Book)

*Handbook of Statistics on Indian Securities Market 2014.

3.2 Trends in Resource Mobilisation by Private and public Sector

Mutual Funds in India.

Mutual fund industry continued to exhibit positive growth in assets under

management in 2013-14. The gross mobilisation of resources by all mutual funds

during 2013-14 was at Rs.97, 68,100 crore compared to Rs.72, 67,885 crore during the

previous year indicating an increase of 34.4 percent over the previous year (Table-3.2).

Correspondingly, redemption also increased by 35.1 percent to Rs.97, 14,318 crore in

2013- 14 from Rs.71, 91,346 crore in 2012-13. The net resources mobilised by all the

mutual funds aggregated to Rs.53,782 crore in 2013-14 compared to net inflow of

Rs.76,539 crore in2012-13. As of at the end of March 2014, the cumulative net assets

managed by all the mutual funds totaled to Rs.8, 25,240 crore as against Rs.7,01,443

crore at the end of March 2013, representing a rise 17.6 per cent.

Page 45

Table-3.2: Trends in Resource Mobilisation by Mutual Funds ( Crore)

2000 to 2015

Year Gross

Mobilisation Redemption* Net Inflow

Assets at the

End of Period

(AUM)

1 2 3 4 5

2000-01 92,957 83,829 9,128 90,587

2001-02 1,64,523 1,57,348 7,175 1,00,594

2002-03 3,14,706 3,10,510 4,196 1,09,299

2003-04 5,90,190 5,43,381 46,808 1,39,616

2004-05 8,39,708 8,37,508 2,200 1,49,600

2005-06 10,98,149 10,45,370 52,779 2,31,862

2006-07 19,38,493 18,44,508 93,985 3,26,292

2007-08 44,64,377 43,10,575 1,53,802 5,05,152

2008-09 54,26,353 54,54,650 28,296 4,17,300

2009-10 1,00,19,023 99,35,942 83,080 6,13,979

2010-11 88,59,515 89,08,921 -49,406 5,92,250

2011-12 68,19,679 68,41,702 -22,024 5,87,217

2012-13 72,67,885 71,91,346 76,539 7,01,443

2013-14 97,68,100 97,14,318 53,782 8,25,240

2014-15 1,10,86,259 1,09,82,971 1,03,287 10,82,757

* Includes repurchases as well as redemption.

Source: SEBI Annual Report 2000-01 &2014-15

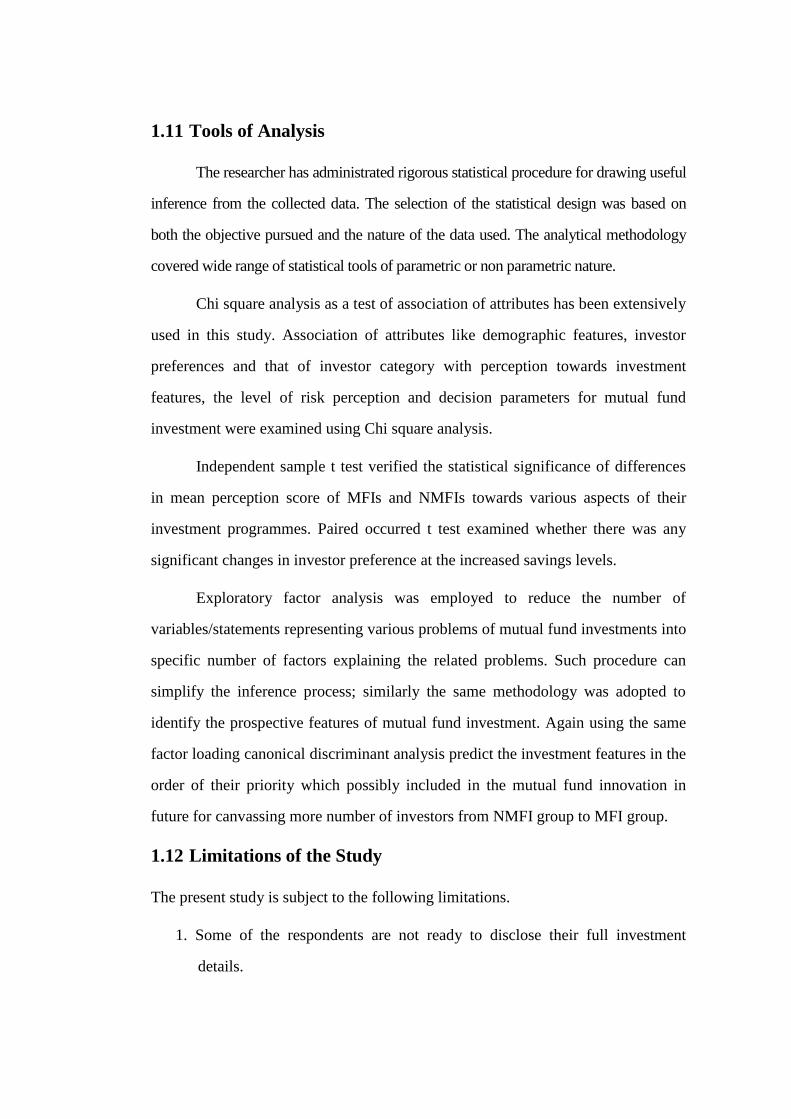

The Fig 3.1 indicates the growth of AUM over the years in India.

Page 46

Figure 3.1 The graph indicates the growth of AUM over the years in India.

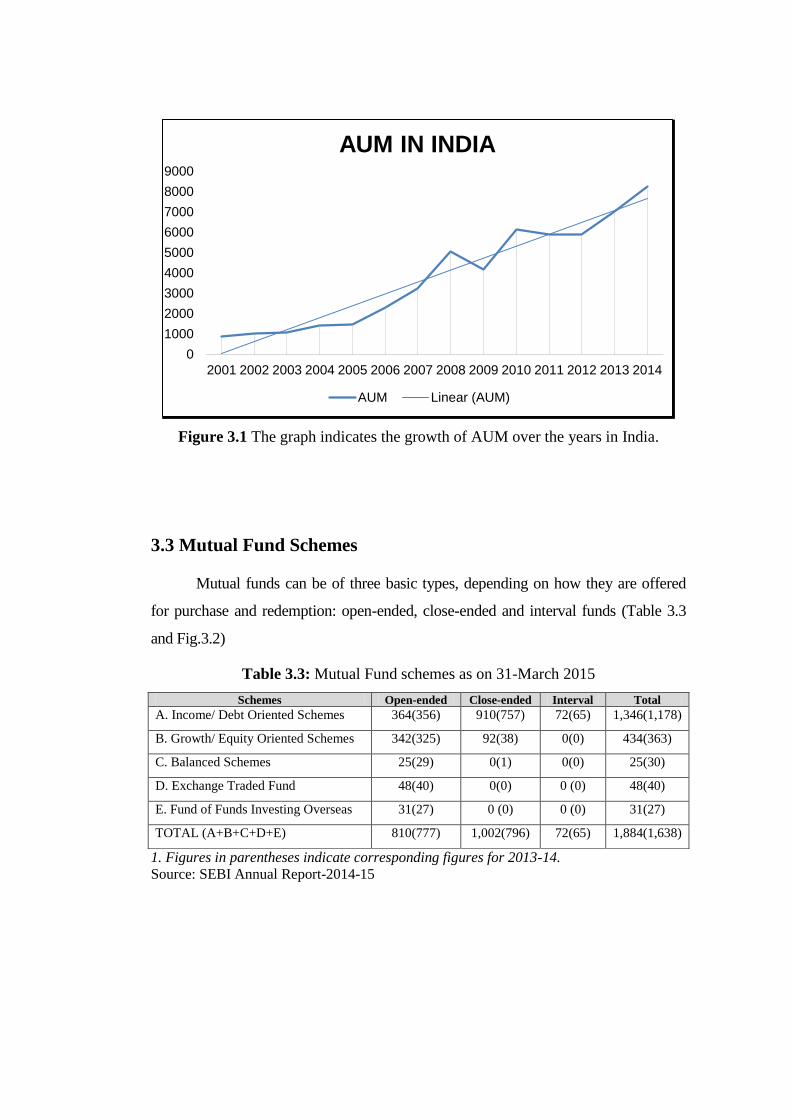

3.3 Mutual Fund Schemes

Mutual funds can be of three basic types, depending on how they are offered

for purchase and redemption: open-ended, close-ended and interval funds (Table 3.3

and Fig.3.2)

Table 3.3: Mutual Fund schemes as on 31-March 2015

Schemes Open-ended Close-ended Interval Total

A. Income/ Debt Oriented Schemes 364(356) 910(757) 72(65) 1,346(1,178)

B. Growth/ Equity Oriented Schemes 342(325) 92(38) 0(0) 434(363)

C. Balanced Schemes 25(29) 0(1) 0(0) 25(30)

D. Exchange Traded Fund 48(40) 0(0) 0 (0) 48(40)

E. Fund of Funds Investing Overseas 31(27) 0 (0) 0 (0) 31(27)

TOTAL (A+B+C+D+E) 810(777) 1,002(796) 72(65) 1,884(1,638)

1. Figures in parentheses indicate corresponding figures for 2013-14.

Source: SEBI Annual Report-2014-15

0

1000

2000

3000

4000

5000

6000

7000

8000

9000

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

AUM IN INDIA

AUM Linear (AUM)

Page 47

Fig-3.2 Mutual fund schemes as on 31-March 2015

Maturity-wise there were 777 open-ended schemes, 796 close-ended

schemes and 65 Interval Schemes as on March 31, 2014. For the income/debt

oriented schemes category, the number of close-ended schemes exceeded open-

ended schemes. In 2015; there were 810 open-ended schemes, 1002 close-ended

schemes and 72 Interval Schemes (Table 3.3).

The simplest way to categories‟ mutual fund products is to look at the

investment objective and the portfolio of the fund. A fund may se3k to invest the

money it mobilises from investors in debt instruments, equity instruments, in

commodities such as gold, in international funds and securities, in other funds, in

derivatives or some combination of these investment options. So the four broad

categories (Mutual fund Schemes) are:

Equity funds investing in equity securities.

Debt funds investing in short and long-term debt instruments.

Hybrid funds investing in a combination of equity and debt.

Other funds including international, commodity, and fund of funds.

The return that a fund may offer and the risk it carries depend on the

investment portfolio.

3.4 Scheme-wise Resource Mobilisation

0

200

400

600

800

1000

1200

Open-ended Close-ended Interval

Fund of Funds InvestingOverseas

Exchange Traded Fund

Balanced Schemes

Growth/ Equity OrientedSchemes

Income/ Debt OrientedSchemes

Page 48

The appropriate fund for investment by an investor is one whose investment objective

matches that of the investor. Mutual fund Schemes may be fitted to investor objectives based on

four basic criteria: risk (safety), return, tax and liquidity. Selection of funds requires evaluation of

these features, before making an investment decision.

As on 31 March 2014, there are 50mutual funds with 1,638 schemes

(29091 scheme NAV names) and the asset under management as Rs 825240

crore(As on 31 March 2015 Rs.10,82,757 crore ) with three scheme type such as

Open-ended, Close-ended & Interval and different scheme category (Portfolios)

such as Growth, Income, Balanced, Equity Linked Savings Scheme (ELSS),

Liquid, Gilt, Fund of Funds(FOF),Gold ETF, Assured Return, Money Market,

Floating Rate, Other ETFs and so on that caters to the investors‟ needs, risk

tolerance and return expectations.

As on 31 March 2015, there are 1884 schemes Out of the total Mutual Fund

Scheme (1884), 1346 were income/debt oriented schemes, 434 were growth/equity

oriented schemes and 25 were balanced schemes. In addition, there were 48

Exchange Traded Funds, of which 14 were Gold ETFs and 34 other ETFs. Also,

there were 31 schemes operating as Fund of Funds which invested in overseas

securities, Table-3.4.

AUM was the highest for income/debt oriented schemes at Rs. 6,94,128

crore with a growth of 15.5 percent while AUM for growth/equity oriented

schemes increased by 80.6 percent to Rs.3,45,139 crore, Table-3.4.

Table 3.4 Scheme-wise Resource Mobilisation and Assets under

Management by Mutual Funds as on March 31, 2015

Schemes

No

. o

f S

chem

es

Ma

rch

31

, 2

01

0

No

. o

f S

chem

es

Ma

rch

31

, 2

01

4

Ass

ets

Un

der

Ma

nag

emen

t

on

3/3

1/2

014

(`cr

ore

)

No

. o

f S

chem

es

Ma

rch

31

, 2

01

5

Ass

ets

Un

der

Ma

nag

emen

t

on

3/3

1/2

015

(`cr

ore

)

1 2 3 4 5 6

A. Income/ Debt Oriented Schemes

i) Liquid/Money Market 56 53 1,33,280 52 162562

ii) Gilt 35 44 6,114 45 14614

Page 49

iii) Debt (other than assured returns) 367 1,077 4,60,672 1245 515772

iv) Infrastructure development 0 4 879 4 1179

Subtotal (i to iv) 458 1,178 6,00,945 1346 694128

B. Growth/ Equity Oriented Schemes

i) ELSS 48 52 25,547 55 39470

ii) Others 307 311 1,65,560 379 305669

Subtotal (i+ii) 355 363 1,91,107 434 345139

C. Balanced Schemes

Balanced schemes 33 30 16,793 25 26368

D. Exchange Traded Funds

i) Gold ETF 7 14 8,676 14 6655

ii) Other ETFs 14 26 4,528 34 8060

Subtotal (i+ii) 21 40 13,204 48 14715

E. Fund of Funds Investing Overseas

Fund of Funds investing overseas 15 27 3,191 31 2408

TOTAL (A+B+C+D+E) 882 1,638 8,25,240 1884 1082757

Source: SEBI Annual Report-2009-10, 2013-14, 2014-15

AUM of gilt schemes in 2014-15 increased by 139 percent, followed by a

rise of 84.6 percent in „others‟ schemes of growth/equity oriented schemes and a

78.0 percent increase in „other‟ ETF schemes. Except the fund of funds investing

overseas schemes and gold ETFs, all the schemes registered an increase in AUM

over the previous year. The highest decline in AUM was registered for fund of

funds investing overseas schemes at 24.5 percent.

3.5 Assets Under Management in India: Geographical Distribution

For savings to be streamlined into the capital market, investors need to first

and foremost be made aware of avenues and opportunities. The mutual fund

industry is yet to spread its reach beyond big cities. The top five cities contribute

72.13per cent of the AUM, the remaining 27.87per cent distributed among other

cities. Statistics show that in December 2014, penetration in the top five cities

increased to 72.13per cent as compared to 71.12per cent in March 2012, whereas

Page 50

for cities beyond the top five, penetration has decreased. One of the prime areas the