15 Problems and Solutions 3 CHAPTER 3 — Problems Exercise 3.1 We consider three zero-coupon bonds (strips) with the following features: Bond Maturity (years) Price Bond 1 1 96.43 Bond 2 2 92.47 Bond 3 3 87.97 Each strip delivers $100 at maturity. 1. Extract the zero-coupon yield curve from the bond prices. 2. We anticipate a rate increase in one year so the prices of strips with residual maturity 1 year, 2 years and 3 years are respectively 95.89, 90.97 and 84.23. What is the zero-coupon yield curve anticipated in one year? Solution 3.1 1. The 1-year zero-coupon rate denoted by R(0, 1) is equal to 3.702% R(0, 1) = 100 96.43 − 1 = 3.702% The 2-year zero-coupon rate denoted by R(0, 2) is equal to 3.992% R(0, 2) = 100 92.47 1/2 − 1 = 3.992% The 3-year zero-coupon rate denoted by R(0, 3) is equal to 4.365% R(0, 2) = 100 87.97 1/3 − 1 = 4.365% 2. The 1-year, 2-year and 3-year zero-coupon rates become respectively 4.286%, 4.846% and 5.887%. Exercise 3.3 We consider the following decreasing zero-coupon yield curve: Maturity (years) R(0,t) (%) Maturity (years) R(0,t) (%) 1 7.000 6 6.250 2 6.800 7 6.200 3 6.620 8 6.160 4 6.460 9 6.125 5 6.330 10 6.100 where R(0,t) is the zero-coupon rate at date 0 with maturity t . 1. Compute the par yield curve. 2. Compute the forward yield curve in one year. 3. Draw the three curves on the same graph. What can you say about their relative position?

Transcript

15Problems and Solutions

3 CHAPTER 3—Problems

Exercise 3.1 We consider three zero-coupon bonds (strips) with the following features:

where R(0, t) is the zero-coupon rate at date 0 with maturity t .

1. Compute the par yield curve.2. Compute the forward yield curve in one year.3. Draw the three curves on the same graph. What can you say about their relative

position?

16Problems and Solutions

Solution 3.3 1. Recall that the par yield c(n) for maturity n is given by the formula

c(n) =1 − 1

(1+R(0,n))n∑ni=1

1(1+R(0,i))i

Using this equation, we obtain the following par yields:

3. The graph of the three curves shows that the forward yield curve is below thezero-coupon yield curve, which is below the par yield curve. This is always thecase when the par yield curve is decreasing.

5.75

6.00

6.25

6.50

6.75

7.00

7.25

1 2 3 4 5 6 7 8 9 10

Maturity

Yie

ld (

%)

Par yield curve

Zero-coupon yield curve

Forward yield curve

17Problems and Solutions

Exercise 3.8 When the current par yield curve is increasing (respectively, decreasing), the cur-rent zero-coupon rate curve is above (respectively, below) it, so as to offset the factthat the sum of the coupons discounted at the coupon rate is inferior (respectively,superior) to the sum of the coupons discounted at the zero-coupon rate. Give aproof of this assertion.

Solution 3.8 Let us denote by c(i) , the par yield with maturity i and by R(0, i), the zero-couponrate with maturity i.

Let us assume for k < n that c(n) > c(k)

At the first rank, we have R(0, 1) = c(1)

At the second rank,

c(2)

1 + c(2)+ 1 + c(2)

(1 + c(2))2= c(2)

1 + R(0, 1)+ 1 + c(2)

[(1 + R(0, 2)]2

Let us do a limited development at the first order of this last expression. Then

1. What are the 1-year maturity forward rates implied by the current term structure?2. Over a long period, we observe the mean spreads between 1-year maturity for-

ward rates and 1-year maturity realized rates in the future. We find the followingliquidity premiums:

Taking into account these liquidity premiums, what are the 1-year maturityfuture rates expected by the market?

Solution 3.11 1. 1-year maturity forward rates are given by the following formula:

[1 + R(0, T )]T = [1 + R(0, T − 1)]T −1 . [1 + F(0, T − 1, 1)]

where R(0, T ) is the zero-coupon rate at date t = 0 with T -year maturityand F(0, T − 1, 1) is the 1-year maturity forward rate observed at date t = 0,starting at date t = T − 1 and maturing one year later.

F(0, 4, 1) is obtained by solving the following equation:

Exercise 3.12 Monetary policy and long-term interest ratesConsider an investor with a 4-year investment horizon. The short-term (long-

term respectively) yield is taken as the 1-year (4-year respectively) yield. Themedium-term yields are taken as the 2-year and 3-year yields. We assume, fur-thermore, that the assumptions of the pure expectations theory are valid.

For each of the following five scenarios, determine the spot-yield curve atdate t = 1. The yield curve is supposed to be initially flat at the level of 4%, atdate t = 0.

(a) Investors do not expect any Central Bank rate increase over four years.(b) The Central Bank increases its prime rate, leading the short-term rate

from 4 to 5%. Investors do not expect any other increase over four years.(c) The Central Bank increases its prime rate, leading the short-term rate from

4 to 5%. Investors expect another short-term rate increase by 1% at the beginningof the second year, then no other increase over the last two years.

(d) The Central Bank increases its prime rate, leading the short-term ratefrom 4 to 5%. Nevertheless, investors expect a short-term rate decrease by 1% atthe beginning of the second year, then no other change over the last two years.

(e) The Central Bank increases its prime rate, leading the short-term ratefrom 4 to 5%. Nevertheless, investors expect a short-term rate decrease by 1%each year, over the following three years.

What conclusions do you draw from that as regards the relationship existingbetween monetary policy and interest rates?

Solution 3.12 Let us denote Fa(1, n, m), the m-year maturity future rate anticipated by the mar-ket at date t = 1 and starting at date t = n, and R(1, n) the n-year maturityzero-coupon rate at date t = 1.

In each scenario, we have

Scenario a Scenario b Scenario c Scenario d Scenario e% % % % %

In the framework of the pure expectations theory, monetary policy affectslong-term rates by directly impacting spot and forward short-term rates, whichare supposed to be equal to market short-term rate expectations. But what aboutthese expectations? The purpose of the exercise is to show that market short-term rate expectations play a determining role in the response of the yield curveto monetary policy. More meaningful than the Central Bank action itself is theway market participants interpret this action. Is it a temporary action or rather thebeginning of a series of similar actions. . . ? We can draw three conclusions fromthe exercise.

First, the direction taken by interest rates compared with that of the Cen-tral Bank prime rate depends on the likelihood, perceived by the market, that theCentral Bank will question its action in the future through reversing its stance.Under the (b) and (c) scenarios, the Central bank action is perceived to either fur-ther increase its prime rate or leave things as they are. Consequently, long-termrates increase following the increase in the prime rate. Under the (d) scenario, theCentral Bank is expected to exactly offset its increasing action in the future. Nev-ertheless, its action on short-term rates still remains positive over the period. Asa result, long-term interest rates still increase. In contrast, under the (e) scenario,the Central Bank is expected to completely reverse its stance through a decreas-ing action in the future, that more than offsets its initial action. Consequently,long-term interest rates decrease.

Second, the magnitude of the response of long-term rates to monetary pol-icy depends on the degree of monetary policy persistence that is expected by themarket. Under the (b) and (c) scenarios, the Central Bank action is viewed as rel-atively persistent. Consequently, the long-term interest-rate change either reflectsthe instantaneous change in the prime rate or exceeds it. Under the (d) scenario, asthe Central Bank action is perceived as temporary, the change in long-term ratesis smaller than the change in the prime rate.

Third, the reaction of long-term rates to monetary policy is more volatilethan that of short-term rates. That is, the significance of the impact of marketexpectations on interest rates increases with the maturity of interest rates. Theseexpectations only play a very small role on short-term rates. As illustrated bythe exercise, the variation margin of the 2-year interest rate following a 100-bpsincrease of the Central Bank prime rate is contained between 50 and 150 bps, whilethe variation margin of the 4-year interest rate is more volatile (between −50 bpand +175 bps).

21Problems and Solutions

Exercise 3.13 Explain the basic difference that exists between the preferred habitat theory andthe segmentation theory.

Solution 3.13 In the segmentation theory, investors are supposed to be 100% risk-averse. Sorisk premia are infinite. It is as if their investment habitat were strictly con-strained, exclusive.

In the preferred habitat theory, investors are not supposed to be 100% riskaverse. So, there exists a certain level of risk premia from which they are readyto change their habitual investment maturity. Their investment habitat is, in thiscase, not exclusive.

4 CHAPTER 4—Problems

Exercise 4.1 At date t = 0, we consider five bonds with the following features:

AnnualCoupon Maturity Price

Bond 1 6 1 year P 10 = 103

Bond 2 5 2 years P 20 = 102

Bond 3 4 3 years P 30 = 100

Bond 4 6 4 years P 40 = 104

Bond 5 5 5 years P 50 = 99

Derive the zero-coupon curve until the 5-year maturity.

Solution 4.1 Using the no-arbitrage relationship, we obtain the following equations for the fivebond prices:

Now, we consider the following bonds priced by the market until the 4-year matu-rity:

Maturity Annual Coupon (%) Gross Price1 Year and 3 Months 4 102.81 Year and 6 Months 4.5 102.5

2 Years 3.5 98.33 Years 4 98.74 Years 5 101.6

The compounding frequency is assumed to be annual.

1. Using the bootstrapping method, compute the zero-coupon rates for the follow-ing maturities: 1 year and 3 months, 1 year and 6 months, 2 years, 3 years and4 years.

2. Draw the zero-coupon yield curve using a linear interpolation.

Solution 4.3 1. We first extract the 1-year-and-3-month maturity zero-coupon rate. In the ab-sence of arbitrage opportunities, the price of this bond is the sum of its futurediscounted cash flows:

102.8 = 4

(1 + 3.5%)1/4+ 104

(1 + x)1+1/4

where x is the 1-year-and-3-month maturity zero-coupon rate to be determined.Solving this equation (for example with the Excel solver), we obtain 4.16% forx. Applying the same procedure with the 1-year and 6-month maturity and the2-year maturity bonds, we obtain respectively 4.32% and 4.41% for x. Next,

23Problems and Solutions

we have to extract the 3-year maturity zero-coupon rate, solving the followingequation:

98.7 = 4

(1 + 4%)+ 4

(1 + 4.41%)2+ 104

(1 + y%)3

y is equal to 4.48% and finally, we extract the 4-year maturity zero-coupon ratedenoted by z, solving the following equation:

101.6 = 5

(1 + 4%)+ 5

(1 + 4.41%)2+ 5

(1 + 4.48%)3+ 105

(1 + z%)4

z is equal to 4.57%.2. Using the linear graph option in Excel, we draw the zero-coupon yield

curve

3.00

3.20

3.40

3.60

3.80

4.00

4.20

4.40

4.60

4.80

0 1 2 3 4

Maturity

Zer

o-c

ou

po

n r

ate

(%)

Exercise 4.4 1. The 10-year and 12-year zero-coupon rates are respectively equal to 4% and4.5%. Compute the 111/4 and 113/4-year zero-coupon rates using linear inter-polation.

2. Same question when you know the 10-year and 15-year zero-coupon rates thatare respectively equal to 8.6% and 9%.

Solution 4.4 Assume that we know R(0, x) and R(0, z) respectively as the x-year and thez -year zero-coupon rates. We need to get R(0, y), the y-year zero-coupon ratewith y ∈ [x; z]. Using linear interpolation, R(0, y) is given by the following for-mula:

R(0, y) = (z − y)R(0, x) + (y − x)R(0, z)

z − x

1. The 111/4 and 113/4-year zero-coupon rates are obtained as follows:

R(0, 111/4) = 0.75 × 4% + 1.25 × 4.5%

2= 4.3125%

24Problems and Solutions

R(0, 113/4) = 0.25 × 4% + 1.75 × 4.5%

2= 4.4375%

2. The 111/4 and 113/4-year zero-coupon rates are obtained as follows:

R(0, 111/4) = 3.75 × 8.6% + 1.25 × 9%

5= 8.70%

R(0, 113/4) = 3.25 × 8.6% + 1.75 × 9%

5= 8.74%

Exercise 4.7 From the prices of zero-coupon bonds quoted in the market, we obtain the follow-ing zero-coupon curve:

where R(0, t) is the zero-coupon rate at date 0 for maturity t , and B(0, t) is thediscount factor at date 0 for maturity t .

We need to know the value for the 5-year and the 8-year zero-coupon rates.We have to estimate them and test four different methods.

1. We use a linear interpolation with the zero-coupon rates. Find R(0, 5), R(0, 8)

and the corresponding values for B(0, 5) and B(0, 8).2. We use a linear interpolation with the discount factors. Find B(0, 5), B(0, 8)

and the corresponding values for R(0, 5) and R(0, 8).

3. We postulate the following form for the zero-coupon rate function−R(0, t):

−R(0, t) = a + bt + ct2 + dt3

Estimate the coefficients a, b, c and d, which best approximate the given zero-coupon rates using the following optimization program:

Mina,b,c,d

∑i

(B(0, i) − −B(0, i))2

where B(0, i) are the zero-coupon rates given by the market.

Find the value for R(0, 5) = −R(0, 5), R(0, 8) = −

R(0, 8), and the corre-sponding values for B(0, 5) and B(0, 8).

25Problems and Solutions

4. We postulate the following form for the discount function−B(0, t):

−B(0, t) = a + bt + ct2 + dt3

Estimate the coefficients a, b, c and d, which best approximate the givendiscount factors using the following optimization program:

Mina,b,c,d

∑i

(B(0, i) − −B(0, i))2

where B(0, i) are the discount factors given by the market.

Obtain the value for B(0, 5) = −B(0, 5), B(0, 8) = −

B(0, 8), and the corre-sponding values for R(0, 5) and R(0, 8).

5. Conclude.

Solution 4.7 1. Consider that we know R(0, x) and R(0, z) respectively as the x-year and thez-year zero-coupon rates and that we need R(0, y), the y-year zero-coupon ratewith y ∈ [x; z]. Using linear interpolation, R(0, y) is given by the followingformula:

R(0, y) = (z − y)R(0, x) + (y − x)R(0, z)

z − x

From this equation, we find the value for R(0, 5) and R(0, 8)

R(0, 5) = (6 − 5)R(0, 4) + (5 − 4)R(0, 6)

6 − 4= R(0, 4) + R(0, 6)

2= 6.375%

R(0, 8) = (9 − 8)R(0, 7) + (8 − 7)R(0, 9)

9 − 7= R(0, 7) + R(0, 9)

2= 6.740%

Using the following standard equation in which lies the zero-coupon rate R(0, t)

and the discount factor B(0, t)

B(0, t) = 1

(1 + R(0, t))t

we obtain 0.73418 for B(0, 5) and 0.59345 for B(0, 8).2. Using the same formula as in question 1 but adapting to discount factors

B(0, y) = (z − y)B(0, x) + (y − x)B(0, z)

z − x

we obtain 0.73478 for B(0, 5) and 0.59449 for B(0, 8).Using the following standard equation

R(0, t) =(

1

B(0, t)

)1/t

− 1

we obtain 6.358% for R(0, 5) and 6.717% for R(0, 8).3. Using the Excel function “Linest”, we obtain the following values for the param-

“Rates Interpol.” stands for interpolation on rates (question 1). “DF Interpol.”stands for interpolation on discount factors (question 2). “Rates Min” stands forminimization with rates (question 3). “DF Min.” stands for minimization withdiscount factors (question 4).

The table shows that results are quite similar according to the two methodsbased on rates. Differences appear when we compare the four methods. In par-ticular, we can obtain a spread of 7.5 bps for the estimation of R(0, 5) between“Rates Min.” and “DF Min.”, and a spread of 8.8 bps for the estimation of R(0, 8)

between the two methods based on discount factors. We conclude that the zero-coupon rate and discount factor estimations are sensitive to the method that is used:interpolation or minimization.

Exercise 4.8 From the prices of zero-coupon bonds quoted in the market, we obtain the follow-ing zero-coupon curve:

where R(0, t) is the zero-coupon rate at date 0 with maturity t , and B(0, t) is thediscount factor at date 0 with maturity t .

We need to know the value for R(0, 0.8), R(0, 1.5), R(0, 3.4), R(0, 5.25),R(0, 8.3) and R(0, 9), where R(0, i) is the zero-coupon rate at date 0 with maturityi. We have to estimate them, and test two different methods.

1. We postulate the following form for the zero-coupon rate function−R(0, t):

−R(0, t) = a + bt + ct2 + dt3

(a) Estimate the coefficients a, b, c and d, which best approximate the givenzero-coupon rates using the following optimization program:

Mina,b,c,d

∑i

(R(0, i) − −R(0, i))2

28Problems and Solutions

where R(0, i) are the zero-coupon rates given by the market. Compare these

rates R(0, i) to the rates−R(0, i) given by the model.

(b) Find the value for the six zero-coupon rates that we are looking for.(c) Draw the two following curves on the same graph:

• The market curve by plotting the market points.• The theoretical curve as derived from the prespecified functional

form.

2. Same question as the previous one. But we now postulate the following form

for the discount function−B(0, t):−B(0, t) = a + bt + ct2 + dt3

Estimate the coefficients a, b, c and d, which best approximate the givendiscount factors using the following optimization program:

Mina,b,c,d

∑i

(B(0, i) − −B(0, i))2

where B(0, i) are the discount factors given by the market.3. Conclude.

Solution 4.8 1. (a) Using the Excel function “Linest”, we obtain the following values for theparameters

(b) We find the value for the six other zero-coupon rates we are looking for inthe following table:

Maturity (years)−R(0, t) (%)

0.8 7.2911.5 7.4913.4 8.051

5.25 8.5458.3 9.0029 9.007

(c) We now draw the graph of the market curve and the theoretical curve. Wesee that the three-order polynomial form used to model the zero-coupon ratesis not well adapted to the market configuration, which is an inverted curveat the short-term segment.

7.00

7.50

8.00

8.50

9.00

0 1 2 3 4 5 6 7 8 9 10

Maturity

Zer

o-c

ou

po

n r

ates

(%

)

2. (a) We first note that there is a constraint in the minimization because we musthave

B(0, 0) = 1

So the value for a is necessarily equal to 1.Using the Excel function “Linest”, we obtain the following values

(c) We now draw the graph of the market curve and the theoretical curve. Wecan see that the three-order polynomial form used to model the discountfunction is not well adapted to the market configuration considered.

7.00

7.50

8.00

8.50

9.00

0 1 2 3 4 5 6 7 8 9 10

Maturity

Zer

o-c

ou

po

n r

ates

(%

)

31Problems and Solutions

3. Note first that this is a case of an inverted zero-coupon curve at the short-termend. We conclude that the two functional forms we have tested are unadaptedto fit with accuracy the observed market zero-coupon rates.

Exercise 4.10 Consider the Nelson and Siegel model

Rc(0, θ) = β0 + β1

[1 − exp

(− θτ

)θτ

]+ β2

[1 − exp

(− θτ

)θτ

− exp

(−θ

τ

)]Our goal is to analyze the impact of the parameter 1/τ on the zero-coupon

curve for three different configurations, an increasing curve, a decreasing curveand an inverted curve at the short-term end.

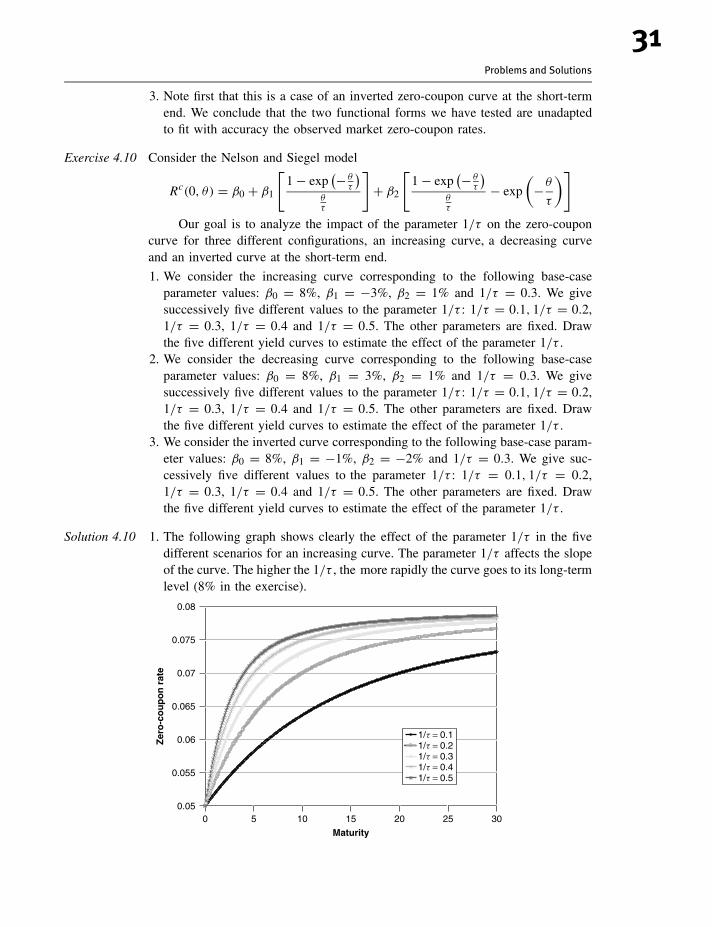

1. We consider the increasing curve corresponding to the following base-caseparameter values: β0 = 8%, β1 = −3%, β2 = 1% and 1/τ = 0.3. We givesuccessively five different values to the parameter 1/τ : 1/τ = 0.1, 1/τ = 0.2,1/τ = 0.3, 1/τ = 0.4 and 1/τ = 0.5. The other parameters are fixed. Drawthe five different yield curves to estimate the effect of the parameter 1/τ .

2. We consider the decreasing curve corresponding to the following base-caseparameter values: β0 = 8%, β1 = 3%, β2 = 1% and 1/τ = 0.3. We givesuccessively five different values to the parameter 1/τ : 1/τ = 0.1, 1/τ = 0.2,1/τ = 0.3, 1/τ = 0.4 and 1/τ = 0.5. The other parameters are fixed. Drawthe five different yield curves to estimate the effect of the parameter 1/τ .

3. We consider the inverted curve corresponding to the following base-case param-eter values: β0 = 8%, β1 = −1%, β2 = −2% and 1/τ = 0.3. We give suc-cessively five different values to the parameter 1/τ : 1/τ = 0.1, 1/τ = 0.2,1/τ = 0.3, 1/τ = 0.4 and 1/τ = 0.5. The other parameters are fixed. Drawthe five different yield curves to estimate the effect of the parameter 1/τ .

Solution 4.10 1. The following graph shows clearly the effect of the parameter 1/τ in the fivedifferent scenarios for an increasing curve. The parameter 1/τ affects the slopeof the curve. The higher the 1/τ , the more rapidly the curve goes to its long-termlevel (8% in the exercise).

0.05

0.055

0.06

0.065

0.07

0.075

0.08

0 5 10 15 20 25 30

Maturity

Zer

o-c

ou

po

n r

ate

1/t = 0.11/t = 0.21/t = 0.31/t = 0.41/t = 0.5

32Problems and Solutions

2. The following graph shows clearly the effect of the parameter 1/τ in the fivedifferent scenarios for a decreasing curve. The parameter 1/τ affects the slope ofthe curve. The higher 1/τ , the more rapidly the curve goes to its long-term level(8% in the exercise). The effect for a decreasing curve is exactly symmetricalto the effect for an increasing curve.

0.08

0.085

0.09

0.095

0.1

0.105

0.11

0 5 10 15 20 25 30

Maturity

Zer

o-c

ou

po

n r

ate

1/t = 0.11/t = 0.21/t = 0.31/t = 0.41/t = 0.5

3. The following graph shows clearly the effect of the parameter 1/τ in the fivedifferent scenarios for an inverted curve. The parameter 1/τ affects the slopeof the curve, and the maturity point where the curve becomes increasing. Thehigher 1/τ , the lower the maturity point where the curve becomes increasing.For example, this maturity point is around 1.5 years for 1/τ equal to 0.5, andaround 8 years for 1/τ equal to 0.1.

Maturity

Zer

o-c

ou

po

n r

ate

0.068

0.069

0.07

0.071

0.072

0.073

0.074

0.075

0.076

0.077

0.078

0 5 10 15 20 25 30

1/t = 0.11/t = 0.21/t = 0.31/t = 0.41/t = 0.5

33Problems and Solutions

Exercise 4.15 Consider the Nelson and Siegel Extended model

Rc(0, θ) = β0 + β1

1 − exp(− θ

τ1

)θτ1

+ β2

1 − exp(− θ

τ1

)θτ1

− exp

(− θ

τ1

)+ β3

1 − exp(− θ

τ2

)θτ2

− exp

(− θ

τ2

)with the following base-case parameter values: β0 = 8%, β1 = −3%, β2 = 1%,β3 = −1%, 1/τ1 = 0.3 and 1/τ2 = 3.

We give successively five different values to the parameter β3: β3 =−3%, β3 = −2%, β3 = −1%, β3 = 0% and β3 = 1%. The other parameters arefixed. Draw the five different yield curves to estimate the effect of the curvaturefactor β3.

Solution 4.15 The following graph shows clearly the effect of the curvature factor β3 for the fivedifferent scenarios:

0.04

0.045

0.05

0.055

0.06

0.065

0.07

0.075

0.08

0 5 10 15 20 25 30

Maturity

Zer

o-c

ou

po

n r

ate

b3 = −3%b3 = −2%base caseb3 = 0%b3 = 1%

Exercise 4.16 Deriving the Interbank Zero-coupon Yield Curve

On 03/15/02, we get from the market the following Euribor rates, futurescontract prices and swap rates (see Chapters 10 and 11 for more details aboutswaps and futures)

Note that the underlying asset of the futures contract is a three-month Euriborrate. For example, the first contract matures on 06/15/02, and the underlying assetmatures three months later on 09/15/02.

1. Extract the implied zero-coupon rates from market data.2. Draw the zero-coupon yield curve by building a linear interpolation between

the implied zero-coupon rates.

Solution 4.16 1. We first extract the implied zero-coupon rates from the Euribor rates using thefollowing formula:

R(

0,x

365

)=

(1 + x

360.Euriborx

) 365x − 1

where R(0, x

365

)and Euriborx are respectively the zero-coupon rate and the

Euribor rate with residual maturity x (as a number of days).We obtain the following results:

We now extract the implied zero-coupon rates from the futures price usingthe following formula:

Bf(

0,x

365,

y

365

)= B

(0,

y365

)B

(0, x

365

)

35Problems and Solutions

which transforms into(1 + (100 − Futures Price)%.

(y − x

360

))= B

(0, x

365

)B

(0,

y365

)and finally enables to obtain

R(

0,y

365

)=

[1

B(0, x

365

) .

(1 + (100 − Futures Price)%.

(y − x

360

))] 365y

− 1

where B(0, t) is the discount factor with maturity t and Bf (0, t, T ) the forwarddiscount factor determined at date 0, beginning at date t and finishing at date T .

Using the last equation, we obtain the following results (FP stands forFutures Price)

2. We obtain the following interbank zero-coupon yield curve:

4.00

4.20

4.40

4.60

4.80

5.00

5.20

5.40

5.60

5.80

6.00

0 1 2 3 4 5 6 7 8 9 10

Maturity

Zer

o-c

ou

po

n r

ate

(%)

5 CHAPTER 5—Problems

Exercise 5.1 Calculate the percentage price change for 4 bonds with different annual couponrates (5% and 10%) and different maturities (3 years and 10 years), starting witha common 7.5% YTM (with annual compounding frequency), and assuming suc-cessively a new yield of 5%, 7%, 7.49%, 7.51%, 8% and 10%.

Solution 5.1 Results are given in the following table: