Wild, Shaw, and ChiappettaFinancial & Managerial Accounting6th Edition

Wild, Shaw, and ChiappettaFinancial & Managerial Accounting6th Edition

16-C1: Process Operations

2

Used for production of small, identical, low-cost items.

Mass produced in automated continuous production process.

Costs cannot be directly traced to each unit of product.

Used for production of small, identical, low-cost items.

Mass produced in automated continuous production process.

Costs cannot be directly traced to each unit of product.

Process Operations

C 13

16-A1: Comparing Process and Job Order Costing Systems

4

Comparing Job Orderand Process Operations

Job Order Systems

Custom orders

Heterogeneous products

Low production volume

High product flexibility

Low to medium standardization

Process Systems

Repetitive operations

Homogeneous products

High production volume

Low product flexibility

High standardization

A 15

Comparing Job Orderand Process Operations

A 16

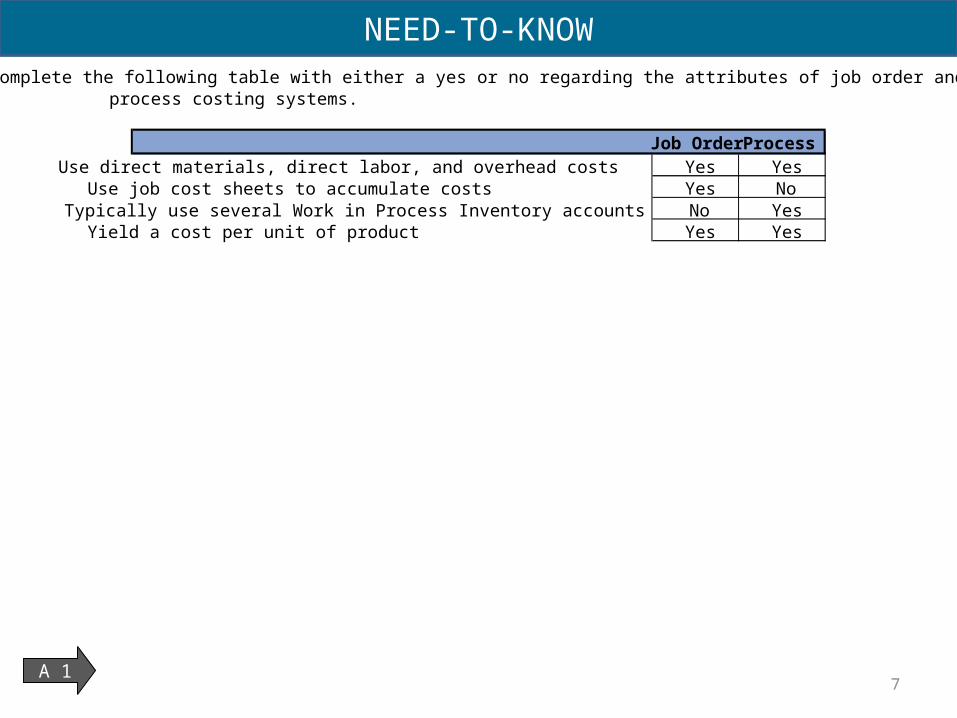

NEED-TO-KNOWComplete the following table with either a yes or no regarding the attributes of job order and process costing systems.

Job Order ProcessUse direct materials, direct labor, and overhead costs Yes YesUse job cost sheets to accumulate costs Yes NoTypically use several Work in Process Inventory accounts No YesYield a cost per unit of product Yes Yes

A 17

16-C2: Equivalent Units of Production

8

Equivalent Units of Production (EUP)

C 2

EUP must be calculated for the Work in Process account.

9

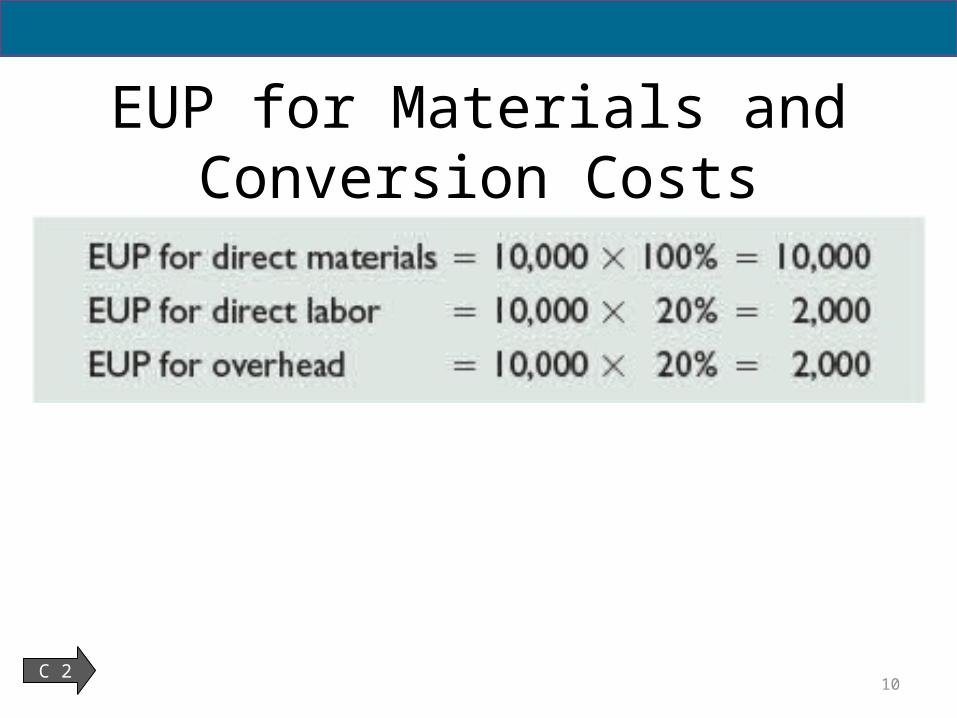

EUP for Materials and Conversion Costs

C 210

Weighted Average versus FIFO

C 2

versus

FIFO

Weighted Average

11

16-C3: Process Costing

12

Process Costing IllustrationGenX uses a weighted average cost flow

system with the following four steps:

Determine physical flow of units. Compute equivalent units of production. Compute cost per equivalent unit. Assign and reconcile costs.

GenX uses a weighted average cost flow system with the following four steps:

Determine physical flow of units. Compute equivalent units of production. Compute cost per equivalent unit. Assign and reconcile costs.

C313

Overview of GenX Company’s Process Operation

C 314

Process Operations – GenX

C 315

Step 1: Determine Physical Flow of Units

C 316

Step 2: Compute Equivalent Units of Production

C 317

NEED-TO-KNOWA department began the month with 8,000 units in work in process inventory. These units were 100%complete with respect to direct materials and 40% complete with respect to conversion. During the month,the department started 56,000 units and completed 58,000 units. Ending work in process inventory includes6,000 units, 100% complete with respect to direct materials and 70% complete with respect toconversion. Use the weighted-average method of process costing to:

1. Compute the department’s equivalent units of production for the month for direct materials. 64,0002. Compute the department’s equivalent units of production for the month for conversion. 62,200

Beginning Units 8,000

Started 56,000

Total Units 64,000

Transferred out 58,000

Ending Units 6,000

Work in Process Inventory - Units

Units in Beginning Inventory 8,000 Units completed and transferred out 58,000Units Started 56,000 Units in Ending Inventory 6,000Total Units to Account For 64,000 Total Units Accounted For 64,000

Physical Units Materials Conversion Materials ConversionTransferred out 58,000 100% 100% 58,000 58,000Ending Inventory 6,000 100% 70% 6,000 4,200Total units 64,000 64,000 62,200

% Completion EUP

Units Schedule (Physical Flow Reconciliation)

C 318

Step 3: Compute Cost per Equivalent Unit

C 319

Step 4: Assign and Reconcile Costs

C 320

NEED-TO-KNOWA department began the month with conversion costs of $65,000 in its beginning work in process inventory.During the month, the department incurred $55,000 of conversion costs. Equivalent units of productionfor conversion for the month was 15,000 units. The department completed and transferred 12,000units to the next department.1. Compute the department’s cost per equivalent unit for conversion for the month.2. Compute the department’s conversion cost of units transferred to the next department for the month.

EUP Cost AllocatedConversion per EUP Cost

Transferred out 12,000 $8.00 $96,000Ending Inventory 3,000 $8.00 24,000Total units 15,000 $120,000

Beginning Inventory 65,000

DL and OH 55,000

120,000

Transferred out 96,000

Ending Inventory 24,000

Cost per Equivalent Unit $120,00015,000

$8.00 per equivalent unit of conversion

Total EUP

Work in Process Inventory

Cumulative Costs

$8.00$96,000

C 321

Process Cost Summary

C 322

Cost Data For GenX

C 323

16-P1: Accounting for Materials Costs

24

Accounting for Material Costs

P 125

16-P2: Accounting for Labor Costs

26

Accounting for Labor Costs

P 227

16-P3: Accounting for Factory Overhead

28

Accounting for Factory Overhead

P 329

NEED-TO-KNOWTower Mfg. estimates it will incur $200,000 of total overhead costs during the year. Tower allocates overheadbased on machine hours; it estimates it will use a total of 10,000 machine hours during the year. DuringFebruary, the assembly department of Tower Mfg. uses 375 machine hours. In addition, Tower incurred

actual overhead costs as follows during February: indirect materials, $1,800; indirect labor, $5,700;depreciation on factory equipment, $8,000; factory utilities, $500.

1. Compute the company’s predetermined overhead rate for the year.

= $20 per machine hour

Machine Hours Used

Assembly Dept.

Actual OH Incurred OH Applied to Production

Factory Overhead

375 hours

x Predetermined OH rate

x $20 per hour

= OH Applied

= $7,500 OH applied

$200,000Estimated Activity Base 10,000 machine hours

NEED-TO-KNOWTower Mfg. estimates it will incur $200,000 of total overhead costs during the year. Tower allocates overheadbased on machine hours; it estimates it will use a total of 10,000 machine hours during the year. DuringFebruary, the assembly department of Tower Mfg. uses 375 machine hours. In addition, Tower incurred

actual overhead costs as follows during February: indirect materials, $1,800; indirect labor, $5,700;depreciation on factory equipment, $8,000; factory utilities, $500.

2. Prepare journal entries to record (a) overhead applied for the assembly department for the month and(b) actual overhead costs used during the month.

Debit Credita) Work in Process Inventory 7,500

Factory Overhead (375 machine hours x $20 per MH) 7,500

16-P4: Accounting for Transfers across Departments

32

Accounting for Transfers

P 433

Trends in Process OperationsProcess design

Just-in-time

production

AutomationServices

Customer orientation

P 4

Continuous Processing

34

Global ViewAs part of a series of global environmental goals,

Anheuser-Busch InBev set targets to reduce its water usage. The company uses massive amounts of water in

beer production and in its cleaning and cooling processes. To meet these goals, the company followed

recent trends in process operations. These included extensive redesign of production processes and the use

of advanced technology to increase efficiency at wastewater treatment plants. As a result water usage

decreased by almost 37 percent in its global operations.

35

16-C4: FIFO Method of Process Costing

36

Appendix 16A: FIFO Methodof Process Costing

C 4The same GenX data for April will also be used to illustrate the FIFO method.

37

Determine PhysicalFlow of Units

C 4

Units from beginning inventory 30,000

Units started this period 70,000

Total units transferred 100,000

38

Compute Equivalent Units of Production

C 4

*Units completed this period 100,000

Less units in beginning goods in process 30,000

Units started and completed this period 70,000 39

NEED-TO-KNOWA department began the month with 50,000 units in work in process inventory. These units were 60%complete with respect to direct materials and 40% complete with respect to conversion. During the month,the department started 286,000 units; 220,000 of these units were completed during the month. TheRemaining 66,000 units are in ending work in process inventory, 80% complete with respect to direct materialsand 30% complete with respect to conversion. Use the FIFO method of process costing to:

1. Compute the department’s equivalent units of production for the month for direct materials.2. Compute the department’s equivalent units of production for the month for conversion.

Beginning Units 50,000 Beginning Units 50,000

Started 286,000 Started and Completed 220,000

Total units 336,000

Transferred out 270,000

Ending Units 66,000

Units Schedule (Physical Flow Reconciliation)Units in Beginning Inventory 50,000 Units completed and transferred out 270,000Units Started 286,000 Units in Ending Inventory 66,000Total Units to Account For 336,000 Total Units Accounted For 336,000

Physical Units Materials Conversion Materials Conversion

NEED-TO-KNOWA department started the month with beginning work in process inventory of $130,000 ($90,000 for directmaterials and $40,000 for conversion). During the month, the department incurred additional direct materialscosts of $700,000 and conversion costs of $500,000. Assume that, using the FIFO method, equivalent unitsfor the month were computed as 250,000 for materials and 200,000 for conversion.

1. Compute the department’s cost per equivalent unit of production for the month for direct materials.2. Compute the department’s cost per equivalent unit of production for the month for conversion.

Cost per Equivalent Unit of Direct Materials:

$700,000250,000

$2.80 per equivalent unit of direct materials

Cost per Equivalent Unit of Conversion:

$500,000200,000

$2.50 per equivalent unit of conversion

Direct Material costs added in the current monthEquivalent units of Production - Current Month

Conversion costs added in the current monthEquivalent units of Production - Current Month