26

| Date post: | 14-Dec-2015 |

| Category: |

Documents |

| Upload: | horatio-anderson |

| View: | 216 times |

| Download: | 0 times |

Process CostingUsed by manufacturers who mass produce large quantities of identical units in a continuous flow.

Process costing involves averaging costs for a particular period in order to obtain departmental unit costs.

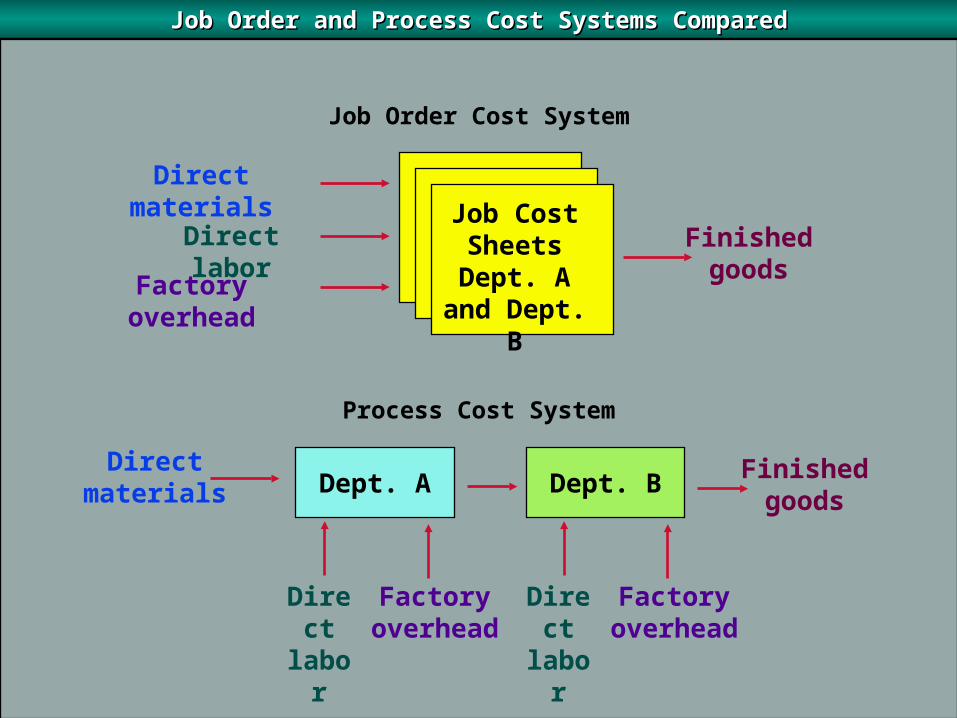

Job Order Cost System

Job Order and Process Cost Systems ComparedJob Order and Process Cost Systems Compared

Job CostSheets

Dept. A and Dept. B

Process Cost System

Direct materials

Direct labor

Factory overhead

Finished goods

Dept. A Dept. B

Factoryoverhead

Directlabor

Directmaterials

Factoryoverhead

Directlabor

Finished goods

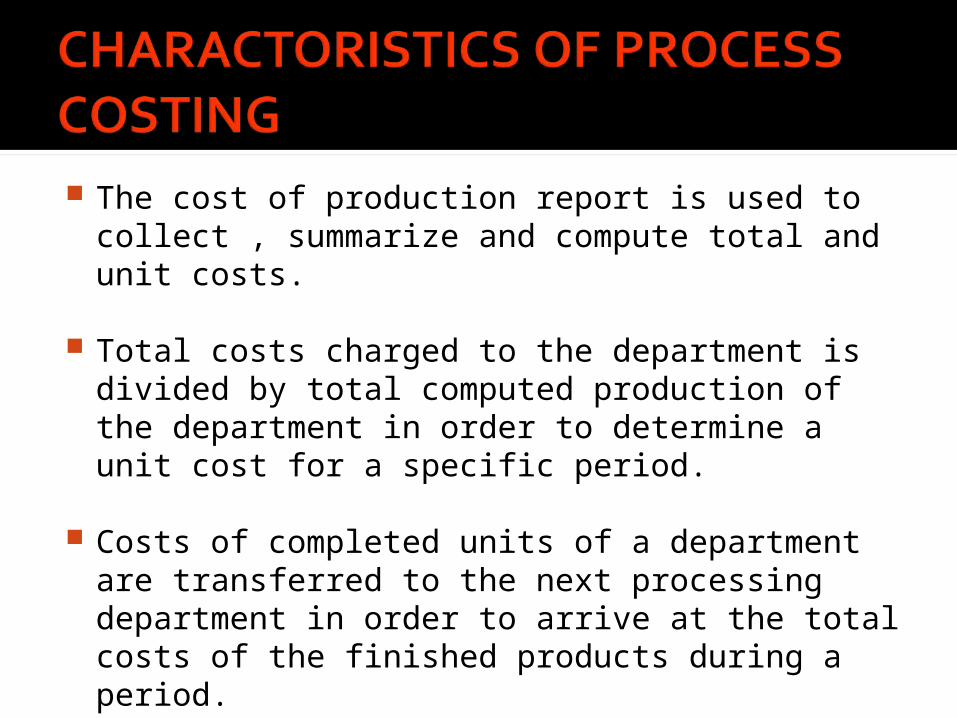

The cost of production report is used to collect , summarize and compute total and unit costs.

Total costs charged to the department is divided by total computed production of the department in order to determine a unit cost for a specific period.

Costs of completed units of a department are transferred to the next processing department in order to arrive at the total costs of the finished products during a period.

Accumulate materials , labor and factory overheads costs by departments

Determine a unit cost for each department

Transfer costs from one department to the next and to finished goods

Assign costs to the inventory of work still in process .

Three product flow formats associated with process costing

Sequential product flowParallel product flowSelective product flow

In a sequential product flow, each item manufactured goes through the same set of operations .e.g

Materials are placed into production in the Blending department and labor and FOH are added. When the work is finished in the Blending department , it moves to the Testing department. The same procedure is applied again and after the completion of work , it moves to the Terminal department. After this department the product is completed and becomes the part of the finished goods.

In a parallel product flow, certain portions of the work are done simultaneously and then brought together in a final process or processes for completion and transfer to the finished goods.

The product moves to different departments within the plant, depending upon the desired final product. E.g meat processing

An entry to record direct materials used in a period is as follows:

Summary labor charges are made to departments through an entry which distributes the direct material payroll:

Predetermined overhead rates for producing departments should be used if:

Production is not stable Factory overhead , especially fixed

overhead , is a significant cost.

The use of predetermined rates is highly recommended for improving cost control and facilitating cost analysis

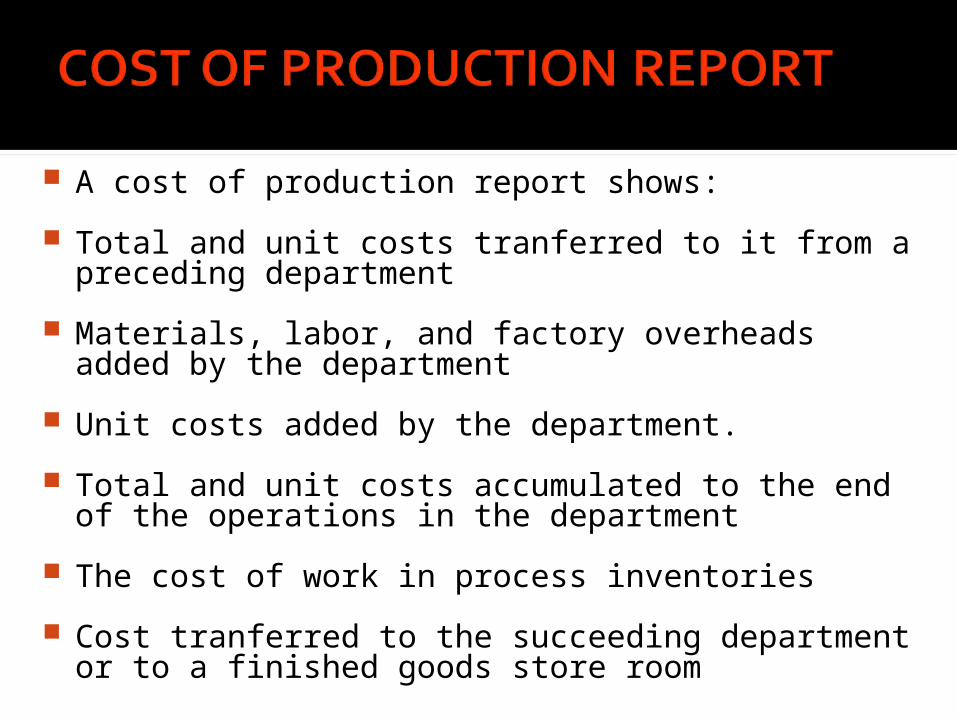

A departmental cost of production report shows all costs chargeable to a department.

It is the most conveniant vehicle for presenting and disposing of costs accumulated during the month.

A cost of production report shows:

Total and unit costs tranferred to it from a preceding department

Materials, labor, and factory overheads added by the department

Unit costs added by the department.

Total and unit costs accumulated to the end of the operations in the department

The cost of work in process inventories

Cost tranferred to the succeeding department or to a finished goods store room

Information in the cost of production report is adjusted for equivalent production.

To condense the illustrated cost of production report , only total materials , labor and factory overhead charged to the departments are considered.

The Clonex CorporationBlending Department

Cost of Production ReportFor the month of January , 2010

Quantity ScehduleUnits started in process 50,000Units tranferred to the next department 45,000Units still in process(all materials-1/2 labor and factory overhead) 4,000Units lost in process 1,000

50,000 Cost charged to the departmentCost added by department: Total Cost

Unit costMaterials 24,500 0.50Labor 29,140 0.62Factory Overhead 28,200 0.60Total cost to be accounted for 81,840 1.72 Cost accounted for as followsTranferred to the next department (45,000*1.72)

77,400Work in process-ending inventory:Materials (4,000*0.50) 2,000Labor (4,000*1/2*0.62) 1,240Factory overhead (4,000*1/2*0.60) 1,200 4,440

Total cost to be accounted for 81,840

The Clonex CorporationTesting Department

Cost of Production ReportFor the month of January , 2009

Quantity Scehdule Units recieved from the preceding department

45,000 Units tranferred to the next department 40,000 Units still in process(1/3 labor and factory overhead) 3,000 Units lost in process 2,000

45,000 Cost charged to the department Cosr from the preceding department: Total Cost

Unit cost Tranferred in during the month (45,000 units) 77,400 1.72 Cosrt added by the department: Labor 37,310 0.91 Factory Overhead 32,800 0.80 Total cost added 70,110 1.71 Adjustment for lost units 0.08 147,410 3.51

Cost accounted for as follows Tranferred to the next department (40,000*3.51)

140,400 Work in process-ending inventory: Adjusted cost from preceding department(3,000*(1.72+0.08) 5,400 Labor (3,000*1/3*0.91) 910 Factory overhead (3,000*1/3*0.80) 800 7,110

Total cost to be accounted for147,510

Method 1: 77,400 = 1.80-1.72=0.08 per unit 43,00043,000

Method 2:Method 2: 2,000 units*1.72= 3,4402,000 units*1.72= 3,440 3,440/43,000=0.08 per unit3,440/43,000=0.08 per unit

The greater the number of units lost , The greater the number of units lost , the greater will be the unit costs.the greater will be the unit costs.

Entry:

Work in process-Terminal Department xx

Work in process-Testing Department xx

Labor:$37,310/43,000=$0.87 per unit

Factory overhead:$32,800/43,000=$0.76 per unit

Lost unit cost:3.35*2000 units=$6,700; $6,700/40,000= $0.1675 per unitTotal cost to be transferred:

3.35+0.1675=$3.5175

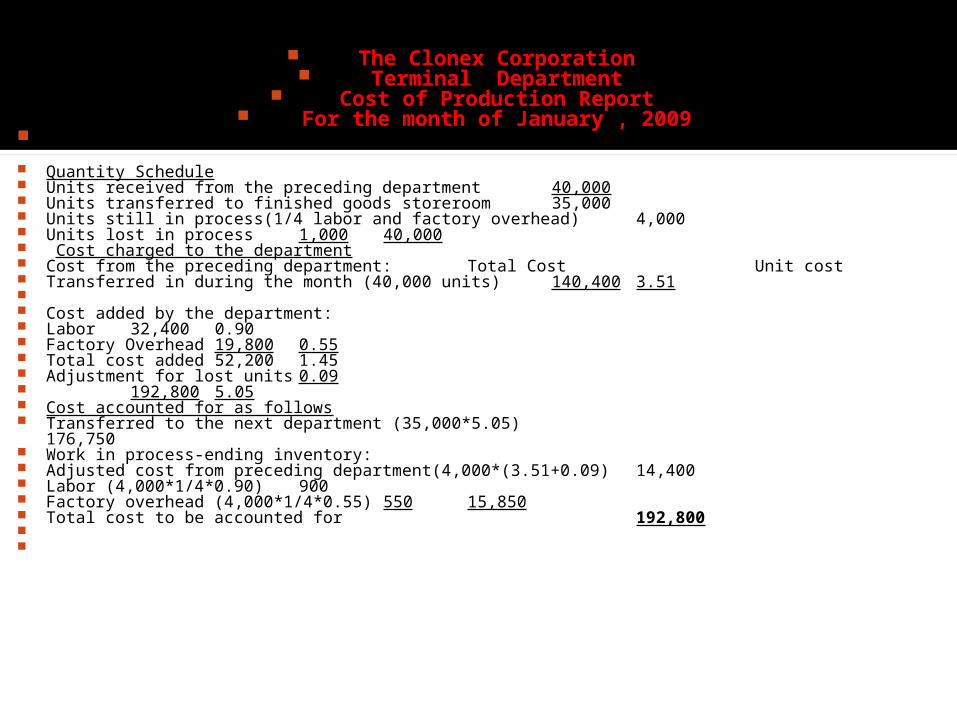

The Clonex Corporation Terminal Department

Cost of Production Report For the month of January , 2009

Quantity Schedule Units received from the preceding department 40,000 Units transferred to finished goods storeroom 35,000 Units still in process(1/4 labor and factory overhead) 4,000 Units lost in process 1,000

40,000 Cost charged to the department Cost from the preceding department: Total Cost Unit cost Transferred in during the month (40,000 units) 140,400 3.51 Cost added by the department: Labor 32,400 0.90 Factory Overhead 19,800 0.55 Total cost added 52,200 1.45 Adjustment for lost units 0.09 192,800 5.05 Cost accounted for as follows Transferred to the next department (35,000*5.05) 176,750 Work in process-ending inventory: Adjusted cost from preceding department(4,000*(3.51+0.09) 14,400 Labor (4,000*1/4*0.90) 900 Factory overhead (4,000*1/4*0.55) 550 15,850 Total cost to be accounted for

192,800

Method 1:$140,400/39,000= $3.603.60-3.51= $0.09 per unit

Method 2:1000 units * $3.51= $3,510$3,510/39,000= $0.09 per unit

An entry to transfer finished units to the finished goods store room:

Finished goods xxx Work in process-Terminal Department

xxx