Page 1

This document is presenting the process documentation of the Microinsurance component under DIPECHO

supported project – Building Disaster Resilience of Vulnerable Communities of Odisha and West Bengal states

of India - led by Concern Worldwide India. Society for Women Action Development (SWAD); Centre for

Youth and Social Development (CYSD), and Sabuj Sangha are implementing partner. All India Disaster

Mitigation Institute (AIDMI) and Women Organisation for Social Cultural Awareness (WOSCA) are providing

technical services in the project. AIDMI with Concern Worldwide India prepared this document.

The views expressed in this publication do not necessarily reflect the views of the involved agencies. This report

may be freely quoted but acknowledgement of the source is requested.

2012

Process Documentation Microinsurance for Disaster Risk Reduction: Post-disaster Long-term Recovery of the Poor 2012

Page 2

Page 2 of 36

Prepared by

Concern Worldwide with AIDMI

Page 3

Page 3 of 36

Process Documentation

Microinsurance for Disaster Risk

Reduction

Building Disaster Resilience of Vulnerable Communities

in Odisha and West Bengal States of India

Post-disaster Long-term Recovery of the Poor

Page 4

Page 4 of 36

A process documentation of microinsurance component for

promoting microinsurance protection for the poor

Concern Worldwide India

With

Centre for Youth and Social Development (CYSD)

Sabuj Sangha

Society for Women Action Development (SWAD)

Women’s Organisation for Socio-Cultural Awareness (WOSCA)

And

All India Disaster Mitigation Institute

Supported by

European Commission Humanitarian Aid and Civil Protection (ECHO)

2012

The process documentation is created to share the design of the actions taken under the result 3 -

microinsurance of the project. This is produced with the intention to communicating ideas, works and

plans with other stakeholders working in the DRR or/and microinsurance field. The document

includes the actions from the beginning of the project to end of the project through chapter 1 –

introduction to 8 lessons learnt. The chapters are in the line of the timeline of the microinsurance

actions. With this intention, the document is prepared at the end of the project. The write shop

workshop was organised with the intention to incorporate experience of the project stakeholders.

Page 5

Page 5 of 36

Contents Acknowledgements ................................................................................................................................. 6

Acronyms ................................................................................................................................................ 7

Chapter I Introduction ........................................................................................................................ 9

1.1 Introduction: Project background ........................................................................................... 9

1.2 Microinsurance in the Project ............................................................................................... 10

1.3 Importance of Microinsurance ............................................................................................. 10

1.4 Involved Agencies, Partnership and Roles ............................................................................ 11

Chapter II Odisha ........................................................................................................................... 16

2.1 Risk Profile of Odisha ............................................................................................................ 16

2.2 Socio-economic Aspects ....................................................................................................... 17

Chapter III The Need for the Microinsurance ....................................................................................... 19

Chapter IV The Demand for Microinsurance .................................................................................. 20

4.1 Development of Methodology for Demand Survey .............................................................. 20

4.2 Demand Survey ..................................................................................................................... 20

Chapter V Microinsurance Scoping Study ...................................................................................... 22

5.1 Findings of the Scoping Study ............................................................................................... 22

Chapter VI Capacity Building and Knowledge Management .......................................................... 27

6.1 Knowledge Products ............................................................................................................. 27

6.2 Training with Local Communities .......................................................................................... 27

6.3 Experience sharing – southasiadisasters.net ........................................................................ 27

6.4 Experience sharing – Event Organisations ............................................................................ 27

Chapter VII Microinsurance Product – Afat Vimo ................................................................................. 28

Chapter VIII Reflections ..................................................................................................................... 29

8.1 Challenges ............................................................................................................................. 29

8.2 Lessons Learned and recommendations .............................................................................. 30

8.3 Way Ahead ............................................................................................................................ 31

Annexure ............................................................................................................................................... 32

A. Definitions ................................................................................................................................. 32

Glossary of Microinsurance Related Terms ...................................................................................... 32

B. Afat Vimo for Odisha – Introductory Brochure......................................................................... 33

C. Products under Microinsurance component ............................................................................ 33

References ............................................................................................................................................ 36

Page 6

Page 6 of 36

Acknowledgements

The project, 'Building Disaster Resilience of Vulnerable Communities in Odisha and West Bengal States of India', was implemented with the objective of enhancing the resilience of at-risk communities to disasters in the coastal states of Odisha and West Bengal, India. Numerous agencies contributed their skills, resources and expertise — DIPECHO was the financial support provider, Concern Worldwide India was the project leader, the Centre for Youth and Social Development, Society for Women Action Development and Sabuj Sangha were the implementing agencies, and Handicap International, Women's Organisation for Socio-Cultural Awareness and the All India Disaster Mitigation Institute (AIDMI) were the technical partners. This process documentation of microinsurance component has been developed by AIDMI based upon the valuable comments from project stakeholders. AIDMI's long experience in risk transfer in India and in South Asia also proved to be very useful for the project and for creating this important knowledge resource. We are thankful to our Country Director Mr. Dipankar Datta for encouraging the project team and Mr. Mihir R. Bhatt of AIDMI for his guidance in developing the microinsurance component in the project. We are thankful to Ms. Binapani Mishra, SWAD; Mr. Jitendra Kumar Sundaray, CYSD; Mr. Jyotiraj Patra, Ms. Mamta Sahu, Ms. Jayajyoti, Project team of Concern Worldwide India for contributing in activities of the component. We are also thankful to AIDMI team members for support in achieving result 3 of the project. Finally, we are grateful to the partner agencies for their efforts at the grassroots level to build awareness on microinsurance and reaching out vulnerable communities in the targeted areas and to reduce risks. Chiranjeet Das Project Team Leader Concern Worldwide India

August 2012

Page 7

Page 7 of 36

Acronyms

AIDMI All India Disaster Mitigation Institute

AIC Agriculture Insurance Company of India Limited

BPL Below Poverty Line

BSLI Birla Sun Life Insurance

CBDRR Community Based Disaster Risk Reduction

CYSD Centre for Youth and Social Development

DIPECHO Disaster Preparedness Programme of ECHO

DRR Disaster Risk Reduction

ECHO European Commission Humanitarian Aid

GIC General Insurance Corporation of India

HDFC Housing Development Finance Corporation Limited

HI Handicap International

HVCA Hazard Vulnerability and Capacity Assessment

ICICI Industrial Credit and Investment Corporation of India

IDBI Industrial Development Bank of India

IMR Infant Mortality Rate

INR Indian National Rupees

LIC Life Insurance Corporation of India

MDG Millennium Development Goals

MGNREGA Mahatma Gandhi National Rural Employment Guarantee Act

MMR Maternal Mortality Ratio

MMS Multimedia Messaging Service

MNAIS Modified National Agricultural Insurance Scheme

NABARD National Bank for Agriculture and Rural Development

NAIS National Agricultural Insurance Scheme

NARRI National Alliance for Risk Reduction and Response Initiatives

NPCBB National Project for Cattle and Buffalo Breeding

OLRDS Orissa Livestock Resources Development Society

Page 8

Page 8 of 36

OSDMA Odisha State Disaster Management Authority

PTG Primitive Tribal Group

RFID Radio Frequency Identification Device

RSBY Rashtriya Swasthya Bima Yojana

SBI State Bank of India

SC Scheduled Caste

SEWA Self Employed Women’s Association

SMS Short Message Service

S. P. University Sardar Patel University

ST Scheduled Tribe

SWAD Society for Women Action Development

TATA-AIG TATA – American International Group

TPDS Targeted Public Distribution System

UIIC United India Insurance Company

UNDP United Nations Development Programme

USAID United States Agency for International Development

WBCIS Weather Based Crop Insurance Scheme

WOSCA Women’s Organisation for Socio-Cultural Awareness

Page 9

Page 9 of 36

Chapter I Introduction

1.1 Introduction: Project background The east coast of India is one of the most vulnerable regions to some of the climate-induced natural

hazards like cyclones, flooding and erosion because of changes in the sea level. Coasts and coastal

communities have been bearing the brunt of various natural hazards, most of which are hydro-

meteorological and geologic in nature. Over the years there has been a systematic increase in the

intensity and frequency of some of these natural hazards because of global environmental changes and

the related sea-level changes. The Orissa Super Cyclone (1999), Mahanadi Floods (2008) and

Cyclone Aila (2009) brought about large-scale damages and transformations in the socio-economic

conditions of the communities as well as the ecosystem they are dependent on for their livelihoods.

Faced with the challenges of such large-scale devastations including loss of human lives and

destruction of vital infrastructures, communities of practitioners in the field of disaster response and

emergency have been working towards a more pro-active strategy. Such a paradigm shift has resulted

in the design, development and implementation of the Disaster Risk Reduction (DRR) framework

which addresses the underlying vulnerabilities of these communities and strengthening their capacities

to face any sort of disaster.

Yet, helping the poor in India to reduce their risks effectively remains a distant dream. It has been

repeatedly experienced that locally embedded institutions and partnerships are more likely to be

effective than external interventions. Thus, enhancing coping capacities of the communities at risk,

including local institutions is a key to risk reduction in India.

Concern Worldwide has been working in India since the 1999 Orissa Super Cyclone, providing

support to local organisations to implement relief, rehabilitation and development work. In last decade

or so, Concern has responded to several emergencies in India. Concern interventions support the

actions of state and national governments and also recognise the need for promoting and complying

with the Hyogo Framework for Action 2005—2015.

January 2011, Concern completed an ECHO-supported project on 'Early Recovery Programme for

AILA Affected People in Sundarbans, West Bengal'. To consolidate and strengthen the disaster

preparedness measures initiated during the early recovery phase, now Concern Worldwide India has

received support from the European Commission's Directorate General for Humanitarian Aid (ECHO)

under its Disaster Preparedness Programme (DIPECHO) for 'Building Disaster Resilience of

Vulnerable Communities in Odisha and West Bengal'. This project has specific objective to

strengthen and build up the capacities of these at-risk communities through systematic efforts at the

community, school and individual level. This is moving by developing their capacities to prepare

against and effectively respond to natural disasters.

The project is having three main components – Hazard Vulnerability and Capacity Assessment;

School Safety and Microinsurance.

All the activities and plans were mobilized by the communities themselves including the mitigation

measures. This built-in mechanism of community ownership is to ensure sustainability of the project

Page 10

Page 10 of 36

outputs and outcomes. More importantly, the project has a strong advocacy component to inform,

influence and impact policies and programmes aimed at disaster resilience at various levels of

governance.

1.2 Microinsurance in the Project The needs assessment

1 reveal that insurance penetration among the targeted communities is very low.

A majority of households consulted during the needs assessment do not have any insurance

protection, although majority of them would be interested in taking out an insurance policy in future.

The demand of coverage is varies including life, livelihood, cattle, accident, household equipments

and health insurance. Many households reported that they would like to have more information on

various micro-insurance options available in the area. They also reported that insurance premium

between Rs. 100-200 would be affordable to them and most trusted source for providing insurance to

them would be either Local NGO or government. Based on the assessment following actions were

carried out under the project. The detail description of each action in presented in the following

chapters of this document. Refer to Annexure C for the products developed under the microinsurance

component.

1. Development of methodology for demand survey

2. Scoping study on microinsurance

3. Training module on Microinsurance

4. Training to local communities on microinsurance

5. Developing and running microinsurance product

6. Special issue of southasiadisasters.net on microinsurance theme

7. Process documentation of microinsurance component of the project

1.3 Importance of Microinsurance Millions of people in developing countries live in a state of destitution. Their opportunities for

development are extremely restricted by economic and political conditions as well as their financial

and social situations. Through different micro finance and insurance policies, the poor could attain a

better standard of life through programms prepared in the field of financial business services.

Microinsurance is important because it is affordable to a person who cannot afford a normal insurance

policy2. AIDMI’s ongoing work in 45 districts of India reflects the reality that the demand of

microinsurance is very huge and constantly increasing. There are several factors contributing to this

reality including frequency of disaster event due to high vulnerability, increasing population,

awareness of insurance in compare with rural areas are some.

Microinsurance offers families living under or just above poverty line a safety net and creates

opportunities for economic development. It empowers people to withstand and adapt to situations that

1 Assessment conducted by Concern Worldwide India - 2010.

2 Money, URL : http://www.ehow.com/info_7745761_importance-micro-insurance.html

Page 11

Page 11 of 36

might otherwise threaten their livelihoods. This makes microinsurance a vital tool in helping reduce

poverty.

It has also proved valuable in empowering women. Microinsurance is mostly sold through women's

self-help groups, as usually, women have been found to be more financially literate and responsible. It

has been shown that financial empowerment of women has secondary effects, including improved

self-esteem and respect within communities, decreased domestic violence, and better nutritional care

and education for children.3

Despite the high levels of economic growth seen in India over the past decade, the cycle of disasters

and vulnerability deprives many millions of poor of the human development that might have

accompanied such growth especially in the areas like West Bengal and Odisha. Within Asia, 24

percent of deaths due to disasters occurred in India because of its size, population and vulnerability.4

Within India, poor households are more severely affected and often lack savings and access to other

social safety mechanisms. Microinsurance is one of several risk management tools that allows the

transfer of some of these risks from poor households to insurance and reinsurance markets, and can

result in lower recovery costs for those affected.

The concept is based on the fact that by forging relationships with other community members, low

income households can reduce vulnerability reduction more holistically than they could through

individual strategies. As such, risk is transferred from one household to the community or inter-

community level with groups in different geographic locations that are not exposed to the same

disaster risks.5

Despite the importance of insurance as a central aspect of disaster risk reduction individuals in

developing countries often remain uncovered. When disasters strike, poor households can be forced

into situations where they forgo investments in education, sell livelihood assets, or take on high

interest loans.

1.4 Involved Agencies, Partnership and Roles Partnerships are critical for effective in any humanitarian intervention from relief to long-term

recovery and preparedness. No single individual or group is capable of sufficiently responding to any

crisis. Among the variety of important partnerships, one of the most critical for supporting long-term

recovery is that with local institutions and communities. Multiple agencies are involved in the project

for effective implementation.

3 Official Website of Allianz, URL:

https://www.allianz.com/en/about_allianz/sustainability/microinsurance/importance/page1.html

4 GoI, 2002

5 AIDMI, 2010

Page 12

Page 12 of 36

A. Facilitating Agency

Concern Worldwide India6

Concern Worldwide is a nongovernmental, international, humanitarian organisation dedicated to the

reduction of suffering and working towards the ultimate elimination of extreme poverty in the world's

poorest countries. Our mission is to help people living in extreme poverty achieve major

improvements in their lives which last and spread without ongoing support from Concern. To achieve

this we engage in long term development work, respond to emergency situations, and seek to address

the root causes of poverty through our development education and advocacy work.

In continuance of our long-standing commitment to these multi-level but concerted efforts, we have

organised our actions across five programme areas of Education, Emergencies, HIV & AIDS, Health

and Livelihoods. Our continuous engagement in and support for communities in situations of conflicts

and natural disasters has been with a focus on addressing the 'underlying risk factors' through

appropriate institutional mechanisms of risk reduction at various levels in society. We started our

work through immediate support to local organisations and communities in the aftermath of the Orissa

Super Cyclone in 1999 and since then we have actively responded to many emergencies across India.

Capitalising on many of these opportunities we have successfully demonstrated the potential of

'buildback- better' by linking relief, rehabilitation and development (LRRD) and supported building

resilient communities in these disaster-prone areas.

While most of the initiatives and processes towards this end are designed and developed as part of the

Emergency Programme, cross-sectoral learning and participation has been instrumental in shaping

innovative, adaptive and integrated action plans and strategies. And this has become absolutely

critical in the wake of an emerging risk regime marked by unprecedented surprises and

transformations because of a changing global climate and emerging world order. Our current Strategic

Plan (2010-2015) categorically underscores this by stressing on the need to mainstream or integrate

DRR into all our programmes. The Disaster Risk Reduction Strategy (February 2008) reiterates this as

'reducing risk is fundamental to sustainable development for extremely poor people'. One of our

multi-country initiatives (in India and Bangladesh) at the interface of Climate Change Adaptation and

Disaster Risk Reduction is being supported by the EuropeAid Development and Cooperation.

Our initiatives in these areas have been widely recognised and supported globally. The Humanitarian

Aid and Civil Protection Department of the European Commission (ECHO) through its Disaster

Preparedness (DIPECHO) programme is supporting us under its 6th Action Plan for South Asia. The

project 'Building Disaster Resilience of Vulnerable Communities in Odisha and West Bengal' aims to

strengthen the capacities and enhance the resilience of many of the at-risk coastal communities. The

overall design of the project is based on learning gathered as part of our previous work during Orissa

Flood (2008) and Cyclone Aila (2009) in Puri and the Sunderbans respectively. Systematic efforts of

resilience building at community, school and individual levels will be through capacity building,

enhancing the reach of various social security schemes (through mobile-phone based tracking) and

6 D. Datta (2011), Concern Worldwide India.

Page 13

Page 13 of 36

ensuring the availability of and accessibility to micro-insurance (as an appropriate market-based tool

for risk transfer). Our emphasis on 'risk analysis as a basis for contextual analysis' will be

operationalised in this project through community-led HVCA processes and appropriate risk

mitigation measures. At the larger institutional level the project aims to link disaster risk reduction

into development planning and through some of these initiatives it will contribute to the

internationally agreed Hyogo Framework of Action (HFA, 2005- 2015) on 'Building the Resilience of

Nations and Communities to Disasters'.

B. Implementing Agencies

The implementing local NGO partners for the project 'Building Disaster Resilience of Vulnerable

Communities in Odisha and West Bengal, India' include Society for Women Action Development

(SWAD), and Center for Youth and Social Development (CYSD) from Puri district of Odisha and

Sabuj Sangha from South 24 Parganas of West Bengal. All of them have been Concern partners for

several years.

SWAD is a registered non-government organisation, based in Puri district of Odisha, committed

to the cause of welfare and development of rural poor women and weaker section of society. It

was emerged from the dream of a group of dedicated volunteers on January 15, 1989. Its Mission

is to:

• To facilitate the process of development of marginalised and vulnerable community with

focus on gender equity; and

• Reducing poverty as well as improving quality of life through capacity building, improvement

of livelihood option, greater access to self-governance and basic rights, services and needs.

SWAD is operating in Satyabadi, Gop, Puri Sadar, Pipili and Kakatpur blocks of Puri district and

Tikabali block of Kandhamal district of Odisha within its package of development programmes.

Presently the activities have spread over 160 villages. The focus areas of intervention are women

empowerment, community capacity building, and community based disaster management. The

target groups are rural poor women and children, poverty-stricken underprivileged and

marginalized society, victims of natural calamities.

Programs undertaken by SWAD are:

• Promotion and formation of Self Help Groups (SHGs). SWAD has promoted 206 SHGs in 58

villages.

• Women empowerment through self-help.

• Income generation programme.

• Awareness camp on women trafficking.

CYSD is a 29 year-old non-government, non-profit organisation, established in 1982 at

Bhubaneswar, Odisha. It works for the development of deprived and marginalised people in the

remotest areas of Odisha with a vision of facilitating a society where communities are able to

make their own choices, meet their survival needs, and lead a self-reliant and sustainable life with

Page 14

Page 14 of 36

dignity. Its mission is to enable marginalised women, men and children to improve their quality of

life. To this end, CYSD uses issue based research to influence policies from a pro-poor and rights

based perspective. It also works to ensure transparent, gender sensitive, accountable and

democratic governance by building the capacities of people and organisations in participatory

planning. CYSD’s approach focuses integrated, inclusive and sustainable development with

special emphasis on Rural Livelihoods, Elementary Education and Participatory Governance. It

also addresses issues such as Gender Equity, Disaster Management, Health and Sanitation, Child

Rights, HIV/AIDS prevention and tribal development. At present, through direct interventions,

CYSD reaches out to 1,52,486 poor families across 680 villages of 73 GPs (8 blocks) of 5

districts in state.

Sabuj Sangha is a non-profit, non-government development organisation working in West

Bengal. It was established in 1954 in the Sundarbans region of West Bengal and registered

under Society Registration Act in 1975. Its work has since spread north throughout South 24

Parganas and into Jalpaiguri. It seeks to improve the lives of people less fortunate through

participation and empowerment.

Its Mission is: Sustainable development of marginalized and vulnerable people to ensure a

quality life through empowerment, education, information, infrastructure development,

healthcare service and economic self-reliance through convergence of services provided by

local self governments.

Its operational areas are:

• Health & Nutrition

• Water, Sanitation and Hygiene

• Education and Protection

• Livelihood and Women's Empowerment

• Environment and Disaster Response

The activities include:

• Providing quality and affordable health care services.

• Training and employing local women to work as community health workers.

• Ward nursing training for local women.

• Installation and renovation of new and existing tube-wells.

• Construction of low-cost household latrines.

• Providing immediate emergency response, reducing vulnerabilities of communities etc.

C. Technical Agencies7

The technical partners of Concern Worldwide India under the project include AIDMI, HI and

WOSCA.

7 Understanding Risk and Intervening to Increase Resilience with Vulnerable Communities (2011), southasiadisasters.net,

issue 77, AIDMI with Concern Worldwide.

Page 15

Page 15 of 36

Concern Worldwide India has partnership with AIDMI since 2009 and they are providing

capacity building, research and documentation support to Concern Worldwide India. AIDMI

provided its expertise in the areas of CBDRR, school safety, risk transfer etc. The actions are

including development of training materials, conducting trainings, research, and developing

publications proposed under this action.

Concern Worldwide India has been collaborating with Handicap International for mainstreaming

disability into disaster management and preparedness as part of the just concluded DIPECHO

programme. Handicap International is also helping Concern to mainstream disability into

Concern's other programmes. Concern and Habitat International consulted each other and agreed

to collaborate for the DIPECHO project to promote disability mainstreaming and inclusion in the

disaster risk reduction programme. Handicap International would provide the services of its

technical experts to Concern to sensitise programme team and mainstream disability in the

operational villages.

WOSCA has been a Concern partner since 2002. Under this project, WOSCA is involved to train

local DRR volunteers to use the window based mobile phones to update the status of welfare

schemes meant for the most vulnerable sections of the society as well as MGNREGA schemes,

TPDS and other schemes on a regular basis through the mobile phone. Information will be

transferred to a central server through SMS/MMS for generating reports. The local organisation

will share the report with the communities, who then will share the reports with government

officials and elected representatives. The similar mobile-based setup will be used to communicate

early warnings and other related information at the community level as a pilot.

Page 16

Page 16 of 36

Chapter II Odisha

2.1 Risk Profile of Odisha The 482 sqkm coastal area of Odisha is exposed to floods and cyclones. Western Odisha is prone to

acute droughts and a large part of the State is prone to earthquakes. Flow of water from neighboring

States of Jharkhand and Chhattisgarh also contributes to flooding. The flat coastal belts with poor

drainage, high degree of siltation of the rivers, soil erosion, breaching of the embankments and

spilling of floodwaters over them cause severe floods in the river basin and delta areas. In Odisha,

Mahanadi, Subarnarekha, Brahmani, Baitarani, Rushikulya, Vansadhara rivers and their many

tributaries and branches flowing through the State expose vast areas to floods.

The State is affected by disasters like heat waves, epidemics, forest fire, road accidents etc. The

history of disasters substantiates the fact that about 80% of the State is prone to one or more forms of

natural disasters. Though a large part of the state comes under Earthquake Risk Zone-II (Low Damage

Risk Zone), the Brahmani Mahanadi deltaic areas come under Earthquake Risk Zone-III (Moderate

Damage Risk Zone) covering 43 out of the 103 urban local bodies of the state. Besides these natural

hazards, human-induced disasters such as accidents, stampede, fire, etc, vector borne disasters such as

epidemics, animal diseases and pest attacks and industrial / chemical disasters add to human suffering.

Odisha is highly vulnerable to climate change. It has a 480 km coast line that is subject to climate-

mediated cyclones and coastal erosion8. Agriculture holds a predominant position in the state’s

economy. About 80-85% of the state’s population is rural and virtually all depend on agriculture and

the agriculture sector contributes about 26 per cent of the GSDP. With almost 60% of land devoted to

rain fed agriculture and with a water-dependent crop, rice, as its main crop, the agriculture sector is

vulnerable to the vagaries of climate-induced weather changes. Odisha also remains one of India’s

poorest states.

The estimates from the Planning Commission reflected in indices such as the percentage of population

below the poverty line both in rural and urban areas, and the overall incidence of poverty in Odisha

viz-a-viz rest of India reveal that Odisha remains one of the poorest among all the major states of

India. The major disasters, which occurred in Odisha, are:

• 1999 cyclone: killed more than 15000 people and caused a damage of 4.5 billion US Dollars.

• 2006 floods: 18,912 villages, 67.39 lakh population and 4.90 lakh hectare crop areas of the state

were affected. 105 persons lost their lives due to flood/heavy rain. 28,327 hectares of crop area were

under sand cast due to the floods.

• 2008 floods: 110 people were killed and 4,30,856 people were evacuated to safer places.

8 Orissa Climate Change Action Plan 2010—2015, Government of Orissa. For more information visit,

http://www.indiaenvironmentportal.org.in/files/CAP_Report_Draft.pdf

Page 17

Page 17 of 36

• 2009 floods: In all, 15 districts were affected which claimed 56 lives. Population affected was 3.94

lakh.

2.2 Socio-economic Aspects

With “human development” being on the radar of the world development community, the social

sector has assumed greater importance. The economy of Odisha has been lagging behind the national

economy by several decades. Its per capita net state domestic product, a measure of average income,

stood at Rs.46150 for 2011-12, which falls behind the national average by around 24 per cent. Orissa

has taken rapid strides in recent years towards several social sector indicators and Millennium

Development Goals (MDG).

In 1951, only 15.8 percent of the State’s population was literate. Census 2001 returned 63.1 percent of

Orissa’s population as literate. According to the NSS data of the 64th round, Orissa’s literacy in 2007-

08 has been estimated at 68.3 percent compared to the national average of 71.7 percent. There is an

improvement in literacy rates for both males and females and the gap between them has narrowed

down. The decline in MMR from 346 in 1997-98 to 303 in 2004-06 is moderate compared to

corresponding figures at an all-India level of 398 in 1997-98 to 254 in 2004-06.

IMR has shown a considerable decline from 96 per 1000 live births in 2000 to 69 in 2008. IMR in

rural Orissa was 71 as compared to 49 in urban areas in 2008. At the national level, IMR stood at 53

and varied from 58 in rural areas to 36 in urban areas in 2008. Though the decline in IMR in Orissa

has been significant in recent years, it is still very high. This is mainly due to three factors: (i) poor

availability of professional attendance at birth and high rate of premature deliveries, (ii) high

incidence of malaria, acute respiratory and tetanus infections and anemia among infants and women,

particularly during pregnancy, and (iii) lack of professional pre and post-natal care.

Many health hazards can be overcome by supply of clean and safe drinking water as well as good

sanitation facilities. These facilities are critical components of what may be called “health

infrastructure”. In both rural and urban areas, the coverage in Orissa was higher than national

averages.

However, Orissa lags far behind the national averages as regards access to toilet facilities. Though the

proportion of rural households having access to toilets increased from 3.58 percent in 1991 to 7.71

percent in 2001, only 14.89 percent households had toilet facilities including 59.59 percent urban

households in Orissa in 2001.

ST and SC taken together constitute about 38.66 percent of the State’s total population. Out of 635

tribal communities in India, 62 are found in Orissa and 13 are Primitive Tribal Groups (PTG).

It is heartening to note that there has been a reduction in poverty by 7.25 percentage points between

1999-2000 and 2004-05 and a further reduction of 11.73 percentage points between 2004-05 and

2007-08.

Page 18

Page 18 of 36

In recent years, Orissa has made significant achievements in terms of economic growth, poverty

reduction and other socio-economic indicators. The State Government has been giving emphasis to

the following areas, which need special attention and focus on an overall development approach:

Orissa’s economy needs to grow faster than the national average over a long period of time in

order to catch up with the nation.

Agriculture and allied sectors need to perform above the national average over a long period

of time.

Sustained efforts are needed to mitigate adverse impacts of natural calamities and other

shocks on Orissa’s economy and people.

Special attention needs to be given to depressed regions, marginalized classes including ST,

SC and women to substantially reduce regional, social and gender disparities.

With a view to addressing the problem of unemployment and under-employment, particularly

among educated and uneducated young persons, special efforts are required to improve their

employable skills, education and other soft skills to harness opportunities that may come up

for them in and outside Orissa.

As Orissa has a high incidence of poverty, special efforts are needed to reduce it at a faster

pace.

Page 19

Page 19 of 36

Chapter III The Need for the Microinsurance

The Civil Society Organizations (CSOs) and policy makers are faced with a complex dual agenda of

both reducing poverty and risks to natural hazards in Odisha.

Many sources confirm that communities have their own coping mechanisms to respond and recover

from impacts of natural disasters. In the states of Odisha and West Bengal, the community coping

mechanisms include, migration, borrowing money, selling of land and livestock, eating less, taking

money from savings, take kids out of school, and so on. A majority of respondents that participated in

the needs assessment mentioned about borrowing money, migration, and selling of assets to cope with

disaster situation. The needs assessment reveal that many poor and vulnerable households from the

targeted areas participate in various social protection schemes supported by state and national

government when given the opportunity. Participation in these schemes forms an integral part of

community coping mechanism. However, because of numbers of reasons performance level of these

schemes is low in terms of coverage and impact. Currently there is no system of bottom-up

monitoring and tracking in place to improve governance of these schemes.

Microinsurance products are becoming increasingly important for risk reduction in Odisha. They

transfer financial risk from vulnerable individuals to the insurance market. Microinsurance covers

many losses but is often unavailable to the poor due to the high transaction cost to affordable premium

ratio. Through microinsurance among poor and vulnerable communities we can decreases the need for

humanitarian aid. Additionally, microinsurance offers the disaster affected a more dignified means to

cope with disasters than relying on the generosity of donors after disaster strikes.9 Microinsurance

may also make tracking trends in vulnerability and hazards easier when claims are charted with

geographic information systems.

9 Mechler, R.; Linnerooth-Bayer, J.; and Peppiatt, D. (2006). Microinsurance for Natural Disaster Risks in Developing

Countries: Benefits, Limitations and Viability. Geneva: ProVention/IIASA.

Page 20

Page 20 of 36

Chapter IV The Demand for Microinsurance

4.1 Development of Methodology for Demand Survey While accumulating scientific evidences have established an emerging link between the rise in the

frequency and intensity of extreme weather events to a changing climate10

, these extreme climate-

related hazards are not necessarily synonymous with extreme risks11

. Interactions of these hazards

with the existing socio-economic, political and environmental conditions determine the extent to

which a given society is at risk at a given point in time. Thus, the skewed and uneven distribution of

risk and its differential impacts across socio-economic groups is attributed to the level of preparedness

and degree of capacity a community has.

Approaches designed and adopted to reduce the risks and thereby strengthen the resilience of at-risk

communities aim to address some of these underlying causes of vulnerability. Micro-insurance has

emerged as one of the leading market-linked risk transfer mechanisms which meet the most essential

financial needs of low-income and poor communities in emergencies and thus enables and strengthens

their recovery process.

The workshop was organized for the development of methodology for demand survey with the

following objectives:

to build up the knowledge base of partners, field staff and team members on issues of

microinsurance and disaster risk reduction;

to help participants understand the centrality of a ‘demand-driven’ micro-insurance scheme

which will be able to cater to the need of at-risk communities; and

to discuss and finalize an appropriate methodology to undertake the demand survey among

the communities.

4.2 Demand Survey Microinsurance is new in many places and there is limited experience to draw upon in designing

products, services, and effective delivery systems. In this context, demand survey can help to reduce

the ‘margin of error’ in designing products by assessing what types of insurance best meet client

needs, what premiums they can afford, and what products are feasible to offer.

The demand survey can inform decisions about whether to enter the market, what type of product to

introduce, and what market segments to target. Once a general product concept has been identified,

the demand survey can help to identify specific product attributes that match the needs, preferences,

cash flow patterns, and other capacities of the target market. Demand survey on actual products can

be valuable in addressing issues related to accessibility, timeliness, pricing and effectiveness. Once a

product has proven successful in one place, demand survey can play a role in assessing its potential

for expansion into new markets or new market segments. Demand survey also can identify activities

10 Fourth Assessment Report of the Intergovernmental Panel on Climate Change , IPCC, 2007,Cambridge University Press 11

UNISDR Brief Note 03: Strengthening climate change adaptation through effective disaster risk reduction.

Page 21

Page 21 of 36

that complement or reinforce micro-insurance, for example, preventative health education or health

savings products. Finally, demand survey can reveal people’s understanding, perception, and trust of

insurance, which is crucial for its uptake and important for designing client education and marketing

strategies (USAID, 2006).

Based on the inputs and exercise conducted during workshop on methodology for demand survey, a

questionnaire tool (with around 50 questions) came out with following five sections.

1. Demographic characteristic

2. Saving experience

3. Borrowing experience

4. Occurrence of crisis and coping mechanism used

5. Familiarity with insurance

Involved team covered large number of households during demand survey in short project time. This

was challenging work for the involved team as it having some time consuming process such as

translation and cross check of data and large sample size. The pilot test helped a lot for useful

modification in the line of effective result.

Project team also faced some obstacles which beyond than the control. These includes flood during

demand survey process which not only create the gap in the work but also change the responses of

respondents and team also shifted their focus from data collection to emergency response during and

after flood.

Page 22

Page 22 of 36

Chapter V Microinsurance Scoping Study

As an input to the designing of suitable microinsurance scheme, a scoping study on available

microinsurance options in the areas was conducted. This Scoping Study was an effort to explore and

understand the diverse microinsurance landscape in the state of Odisha. While the overall objective

was to document the range of available microinsurance products, insights around an emerging growth

trend and challenges associated with it further enriched the findings of this study.

The study attempted to answer the following questions:

a. What are the larger policy and legislative frameworks around insurance in general and

microinsurance in particular?

b. What are the microinsurance products and schemes available?

c. Who are the insurers and how do they channelize microinsurance services and products?

d. How have been the trend in terms of microinsurance growth and penetration and the challenges

thereof?

5.1 Findings of the Scoping Study12 Microinsurance (Life): The microinsurance landscape in the state of Odisha is dominated with life

microinsurance products. The following table is presenting different available microinsurance (life)

products in Odisha.

No Insurer Microinsurance Product

01 Life Insurance Corporation of

India (LIC)

JeevanMadhur, JeevanMangal

JanashreeBimaYojna, AamAdmiBimaYojna*

02 SBI Life Insurance

Grammen Shakti

Grammen Super Suraksha

03 Birla Sun Life Insurance

BimaDhanSanchay

BimaSuraksha Super

BimaKavachYojna

04 ICICI Prudential

Srava Jana Suraksha

AnmolNivesh

05 TATA-AIG

SampoornaBimaYojana

NavkalyanYojana

AyushmanYojana

SumangalBimaYojana

06 Bajaj Allianz

Alp NiveshYojana

Jana VikasYojana

SaralSurakshaYojana

07 AVIVA Life Insurance

Amar Suraksha, Jana Suraksha, GrameenSuraksha,

AnmolSuraksha

Credit Suraksha, CreditPlus, CreditNet

08 IFFCO-TOKIO

JantaBimaYojna

Jan KalyanBima

Jan SurakshaBima

MahilaSurakshaBimaYojna

Sankat Haran Policy

12

Microinsurance Scoping Study (2012), DIPECHO Project team, Concern Worldwide India

Page 23

Page 23 of 36

10 MetLife India Insurance Co.

Pvt Ltd

Met Vishwas

Met Suvidha (Rural)

Met GrameenAshray

11 IDBI Federal Life Insurance

Co Ltd

IDBI Federal Group Microinsurance

12 Development Commissioner

(Handicrafts), Ministry of

Textiles, Government of India

in association with LIC of

India

JanshreeBimaYojana (for Handicrafts Artisans)

*Products in italics are group micro-insurance products

Microinsurance (Non-life)

Health: The RashtriyaSwasthyaBimaYojana (RSBY), a unique social security of the Ministry of

Labor and Employment of the Government of India aiming to to provide health insurance coverage

for Below Poverty Line (BPL) families, remains the most popular and well subscribed health micro-

insurance. Beneficiaries under RSBY are entitled to hospitalization coverage up to Rs. 30,000/- for

most of the diseases that require hospitalization. Government has even fixed the package rates for the

hospitals for a large number of interventions. Beneficiaries need to pay only Rs. 30/- as registration

fee while Central and State Government pays the premium to the insurer selected by the State

Government on the basis of a competitive bidding. A host of private insurers are part of this scheme

and around 533627 BPL families (as on 19th January 2012) have enrolled in RSBY; the highest being

in the district of Puri with an enrolment of 131736 BPL families.

Health Micro-insurance Products in Odisha

No Insurer Microinsurance Product

01 Ministry of Labour and Employment, Government

of India in association with private insurers

RashtriyaSwasthyaBimaYoj

ana (RSBY)

02 Development Commissioner (Handicrafts), Ministry

of Textiles, Government of India and ICICI

Lombard General Insurance in Odisha

http://handicrafts.nic.in/welfare/rajivgandhi.htm

Rajiv Gandhi

ShilpiSwasthyaBimaYojana

03 The New India Assurance Co. Ltd Jana ArogyaBima Policy

04 Oriental Insurance Company Limited Jana ArogyaBima Policy

05 TATA AIG Personal Accident Insurance

06 Max Bupa SwasthyaPratham

07 IFFCO-TOKIO Jan SwasthyaBimaYojna

Page 24

Page 24 of 36

Health Systems 20/20 (Better Systems, Better Health) 13 , a USAID initiative identifies the

following responsible for the sub-optimal performance of many health insurance schemes in

India:

Lack of clarity of objectives in implementing a health insurance scheme

Inappropriate benefit design due to absence of beneficiary needs assessment

Lack of health providers in rural area

Weak distribution and enrollment agency at rural level.

Virtual absence of scheme implementation agencies at grassroots level.

Adverse selection since schemes operate on voluntary rather than universal level

Weak communication mechanism for generating awareness of schemes among

beneficiaries.

Crop and Agricultural Micro-insurance

The National Agricultural Insurance Scheme (NAIS) and Modified National Agricultural

Insurance Scheme (MNAIS) are two of the most popular and widely subscribed to crop insurance

programmes of the Government of India. The Agricultural Insurance Company of India Limited is

a unique partnership of shareholding among insurers and the National Bank for Agriculture and

Rural Development (NABARD).

Shareholding of AIC of India Ltd. Based on data at AIC of India Ltd

13

Making Health Insurance Work for the Poor. Available at http://www.healthsystems2020.org/section/where_we_work/india

35%

30%

8%

9%

9% 9%

Shareholding of AIC of India Ltd. General Insurance Corporation of India

NABARD

National Insurance Compnay Limited

The New India Assurance Compnay Limited

Page 25

Page 25 of 36

Agriculture and Crop Microinsurance Products in Odisha

No Insurer Microinsurance Product

01 Agricultural

Insurance Company

of India Limited

Weather Based Crop Insurance Scheme (WBCIS)

In the districts of Nuapada, Bolangir and Bargarh and covers only

paddy crop

02 Agricultural

Insurance Company

of India Limited

RashtriyaKrishiBimaYojana (National Agricultural Insurance

Scheme, NAIS) and Modified National Agricultural Insurance

Scheme (MNAIS)

Coconut Palm Insurance Scheme (CPIS)

Potato Crop Insurance

VarshaVima/Rainfall Insurance

anticipated shortfall in crop yield on account of deficit rainfall

Weather Insurance (Rabi)

protection against adverse deviations in a range of weather

parameters like frost, heat, relative humidity, rainfall etc. between

December and April

03 IFFCO-TOKIO BarishBimaYojna (BBY); MausamBimaYojna (MBY)

The Government of Odisha, for the very first time, decided to go for the Weather Based Crop

Insurance Scheme (WBCIS) on a pilot basis in the districts of Nuapada, Bolangir and Bargarh.14

This

is being implement by AIC and it compensates the insured farmers against the likelihood of financial

loss on account of anticipated loss in crop yield resulting from adverse rainfall incidence such as

deficit rainfall and excess rainfall. The pre-declared limit of insurance coverage has been set at INR

12,000 per hectare.

Livestock: Livestock remains one of the most dependent on and productive asset of the poor and

marginal farmers. Government promotes many Livestock Insurance Schemes through the respective

State Livestock Development Boards. Disease control and improvement of genetic quality of animals

remains the top priority of the boards. With an aim to successfully implement the centrally sponsored

National Project for Cattle & Buffalo Breeding (NPCBB) programme, the government of Odisha in

the year 2000 established the Orissa Livestock Resources Development Society (OLRDS)15

. Details

guidelines for the implementation of the Livestock Insurance Scheme have been annexed to this

report.

14

http://www.hindu.com/2010/06/28/stories/2010062852810300.htm

15http://www.olrds.com/website/home.htm

Page 26

Page 26 of 36

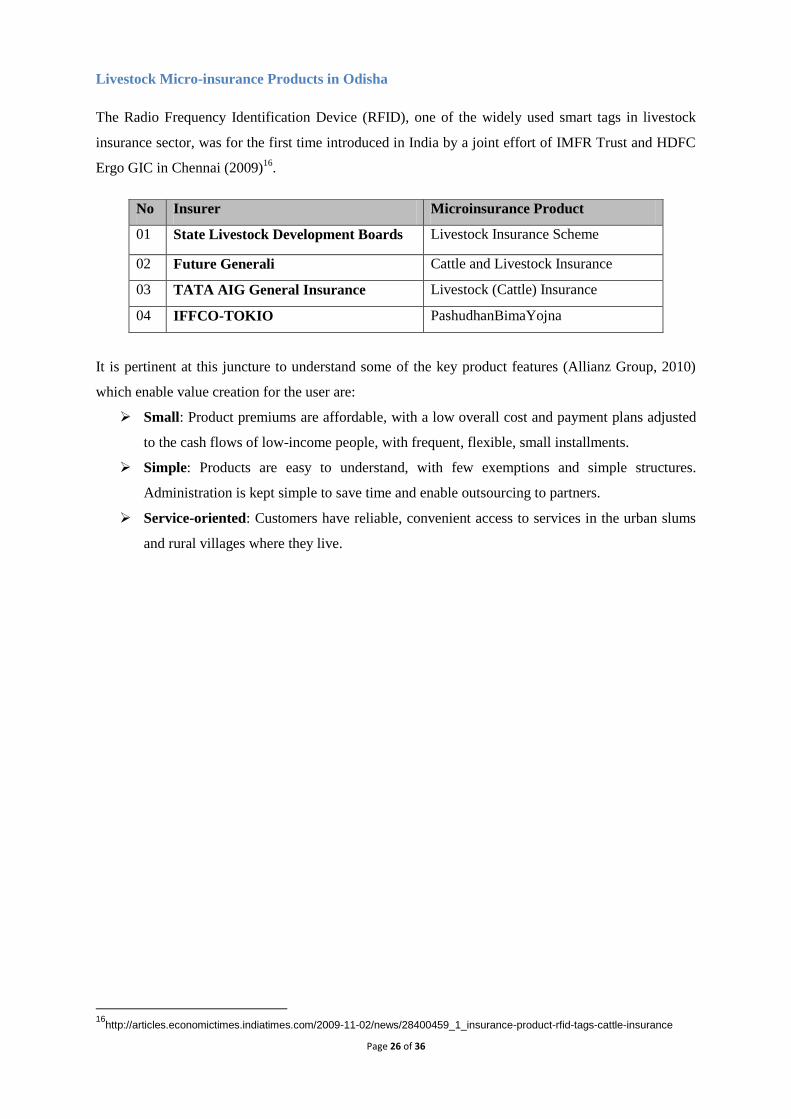

Livestock Micro-insurance Products in Odisha

The Radio Frequency Identification Device (RFID), one of the widely used smart tags in livestock

insurance sector, was for the first time introduced in India by a joint effort of IMFR Trust and HDFC

Ergo GIC in Chennai (2009)16

.

It is pertinent at this juncture to understand some of the key product features (Allianz Group, 2010)

which enable value creation for the user are:

Small: Product premiums are affordable, with a low overall cost and payment plans adjusted

to the cash flows of low-income people, with frequent, flexible, small installments.

Simple: Products are easy to understand, with few exemptions and simple structures.

Administration is kept simple to save time and enable outsourcing to partners.

Service-oriented: Customers have reliable, convenient access to services in the urban slums

and rural villages where they live.

16

http://articles.economictimes.indiatimes.com/2009-11-02/news/28400459_1_insurance-product-rfid-tags-cattle-insurance

No Insurer Microinsurance Product

01 State Livestock Development Boards Livestock Insurance Scheme

02 Future Generali Cattle and Livestock Insurance

03 TATA AIG General Insurance Livestock (Cattle) Insurance

04 IFFCO-TOKIO PashudhanBimaYojna

Page 27

Page 27 of 36

Chapter VI Capacity Building and Knowledge Management The project is highly emphasizing on capacity building of stakeholders. To do this effectively,

different actions for capacity building were conducted, these includes trainings, knowledge products

and workshops.

6.1 Knowledge Products To build the understanding of microinsurance and also encouraging humanitarian agencies to develop

such protection tools, the training module is developed under the project and targeting humanitarian

agencies working directly with local communities for risk reduction and community development.

The module is dividing into following 4 chapters:

1. Introduction to Microinsurance and its Relevance to Risk Reduction

2. Assessing Microinsurance Demand

3. Guideline for Developing Community-driven Microinsurance Products

4. Case Examples of Successful Microinsurance Initiatives in India.

Same module translated into Odia and Bengali languages to build the capacity of local communities

including DRR practitioners. This process is important and challenging too as such detail material

never been develop in local language.

6.2 Training with Local Communities Training programmes were conducted to build local capacities on microinsurance. The trainings were

conducted in local language – Odia – with local communities and implementing agencies. The focus

was given on awareness and available products for the communities while with DRR practitioners

were kept focus on technical aspects of microinsurance from assessment to designing product to

monitoring and evaluation.

6.3 Experience sharing – southasiadisasters.net A special issue of southasiadisasters.net was developed under the microinsurance component. The

objective of development of the issue on microinsurance is to spread the learning under the project

and share experience of DRR practitioners and experts in the field of DRR and Insurance. The theme

of southasiadisasters.net is ‘Microinsurance for Disaster Risk Reduction: Post-disaster Recovery of

the Poor’ – Issue 83. The issue published on March 2012 and shared with project partners and global

DRR community through different electronic media. The issue has contribution from AIDMI, BSLI,

Concern Worldwide, NARRI Bangladesh, SEWA, S. P. University, SWAD, and UIIC.

6.4 Experience sharing – Event Organisations Two experience sharing event were organised to share learning with project stakeholders, insurance

companies and DIPECHO partner agencies. Another objective of such events was to document such

learning to share with DRR community.

Page 28

Page 28 of 36

Chapter VII Microinsurance Product – Afat Vimo

Based on the assessment and scoping study, it was clear that community requires product that cover

both life and non-life and for sustainability of the project premium should remain in the financial

capacity of clients from poor and vulnerable communities. On the other side, community is also

having desire of saving with insurance protection. The project duration is another challenge for

implementing agencies to come out with insurance product.

With all these opportunities and challenges, partners conducted series of consultations with LIC and

UIIC for taking Afat Vimo in Odisha. See Annexure C for details of Afat Vimo product. Under the

project efforts, the product is going to reach 997 clients from the project areas of Odisha. The product

launched during the Stakeholders’ workshop on August 21, 2012 at Bhubaneswar.

The Afat Vimo product modified for Odisha communities based on the need and demand from the

communities and financial capability for long-term sustainability.

The client selection was a challenging work for the involved agencies, as it require to incorporate

long-term perspectives and also in the line with the project objectives. However, the past work of

HVCA helped a lot to identify the client for the Afat Vimo product. Involved team members also did

cross verification through survey data with HVCA and baseline data documents. Later on team came

out with the following criteria for the selection of the client during the first year of the Afat Vimo in

Odisha.

1. Age group – 20 to 60

2. Widow and women headed households

3. Families that have differently abled persons

4. Marginalized and poor families

5. Landless labours

6. Houses in low-lying areas and also fits in the above socio-economic background

7. Families that have migrated labour member/s

Above-mentioned points are came out with consultations between insurance companies (1st point),

partners and communities. Building disaster resilience of vulnerable communities is the main focus

area of the project thus point 2 to 7 were listed out during client indemnification procedure.

Page 29

Page 29 of 36

Chapter VIII Reflections

8.1 Challenges During the project actions under result 3 – microinsurance following are key challenges faced and

observed by project collaborates.

1. A need for large volume in microinsurance products: For successful work in microinsurance

field, operating agencies requires covering large volume and the covered community should

be from poor and needy economic background. The so far work in project created good

environment and result achieved with participation of stakeholders however in terms of

microinsurance field; this is just initial steps in Odisha for implementing partners.

Stakeholders need to make long-term practical and realistic plan to convert this good

beginning into successful intervention where microinsurance product developed specific for

poor and vulnerable communities of Odisha.

2. Low level of awareness on microinsurance: This is one of main and common challenge for

insurer. This challenge sometimes also create myths related to microinsurance product that

run at local level. This is also observed that agencies keeps emphasis on information of their

product rather than the importance of microinsurance. On the other side, for humanitarian

agencies who playing role of insurer also having limitation in terms of administration cost for

conducting awareness related activities time-to-time.

3. Client’s expectations of money back policy with low premium: This is common factor related

to communities with poor background and low awareness. However, this challenge is

addressed under the project where life insurance coverage is design with LIC for long-term

and money back policy.

4. High expectation: Because of poor are more vulnerable to risks, there is an assumed logic that

they have some unmet demand for insurance. Clearly, the poor are in great need of insurance

given the limited social protection afforded to them and their exclusion from most formal

types of insurance. But are we too hasty to assume that in fact, their need for insurance will be

translated into a demand for insurance? We must remember that these people barely earn a

living. Are they too poor to demand insurance? This high expectation is perhaps emphasizing

on low understanding of insurance among poor. Some of them may have some exposure to

insurance but do not have the means to access it. This also create negative perception at local

level. This also requires support mechanism at local level for example integration of micro

mitigation measures by CSOs.

5. Client identification process: This step was challenges process for the project team as the

whole targeted area of the project come under the high risk and with many vulnerable

populations. However, constant and active consultations resulted into good client

Page 30

Page 30 of 36

identification where project also support those families and their disaster resilience level

could increase through the support mechanism.

8.2 Lessons Learned and recommendations 1. Assessment/ scoping study of area is very important for microinsurance work. Documentation of

existing microinsurance practices adopted by MFIs. This will include primary and secondary data

gathering on the various microinsurance practices adopted by different types of institutions

nationwide.

2. Any agencies have interest to work on microinsurance, it is important to review of the current

regulatory environment and the formulation and adoption of appropriate rules and regulations and

guidelines for the safe and sound operation of institutions providing microinsurance.

3. Constant monitoring and evaluation is highly necessary. The points from M & E should be

integrate with the action plan. Such steps are common in most actions and sector however without this

the microinsurance work cannot be sustain.

4. Review of the technical capacity and capability of the insurer and in relation with the target

audience is crucial for moving ahead.

5. Regular meeting with clients to address their need for better operations and addressing challenges

at local level. This is also helpful to avoid myths at local level related to microinsurance product.

6. The success of the product is often depends on the services provided by the involved team

members. This is very important to build the capacity of involved staff so their effective services to

client support to create enabling environment at local level, which ultimately increase the renewal

ratio of the good product. This will also helps to identify latent demand from the clients for moving

ahead effectively.

7. Assessment, demand survey and other such actions requires detail data collection and effective

analysis procedures. This should well followed by the involved experts and partners to come out with

actual need of the clients.

8. Process that not specific to requirement may leads towards high cost, cost sharing among channel

partners, and poor service quality.

9. Service providers should create clear plan of actions while dealing with migratory clients for long -

term association.

Page 31

Page 31 of 36

10. Some simple procedures are normal but very important to have clear design of the same from the

beginning to avoid doing the same repeatedly. Format of client profile, demand survey, assessment

data, client forms are such work where clear, simple and linkages should be set from the beginning.

8.3 Way Ahead

For microinsurance to be successful – for the insureds and for the risk-bearers – many elements are

important; i.e. simple and affordable insurance products reaching large numbers of people; stream-

lined administration, including premium payment; a simplified claims procedures and verifications;

and rapid delivery of benefits. If most of these elements are present, it can be possible for

microinsurance schemes to become sustainable, to perform well and to provide "real value" to the

poor17

. Following are key way ahead decided to move ahead by project stakeholders.

1. The project stakeholders are putting efforts for sustainability of the product so that it not

remains just project output. Project stakeholders are creating links to sustain the product with

interested agencies.

2. The capacity building efforts of insurer is another focus area. The experience of SWAD and

CYSD is helping in this point for moving ahead.

3. It is decided to create a separate document to capture the lessons from the experience of

implementing Afat Vimo product in Odisha. This will be done in the end of 2012. This also

creates the opportunity of moving ahead concretely and bases of the experience.

4. Project stakeholders are planning to create SWAD and CYSD as a learning centre for

spreading lessons and promoting microinsurance services for the poor and vulnerable families

of the Odisha.

5. It is decided to create action plan by project stakeholders for and with SWAD and CYSD for

short-term (around 1 to 2 years) and long-term (5 years). This is towards institutionalizing

microinsurance and sustainability of the product.

6. Development of different IEC tools is another clear way ahead in short term plan.

7. Project stakeholders are also seeking opportunities to replication the Afat Vimo product in

other areas of Odisha and beyond for sustainability through higher volume, low premium and

better services.

17 http://www.microinsurancenetwork.org/history.php.

Page 32

Page 32 of 36

Annexure

A. Definitions

Glossary of Microinsurance Related Terms Term Definition Actuary A person who calculates insurance premiums, reserves, and dividends. Adverse

Selection

Also called anti-selection, the tendency of persons who present a poorer-than

average risk to apply for, or continue, insurance. If not controlled by

Underwriting, results in higher-than-expected loss levels.

Agent An insurance company representative who sells and services insurance

contracts for the insurer; the intermediary between the insurer and the

policyholder.

Beneficiary The person who receives a life insurance benefit in the event of the

policyholder's death.

Claim A request for payment under the terms of an insurance contract when an insured

event occurs.

Commission The part of an insurance premium paid by the insurer to an agent for his or her

services in procuring and servicing the insurance contract.

Covariant Risk A peril that affects a large number of the policyholders at the same, e.g., an

earthquake; or several risks that consistently occur together (at the same time or

under the same circumstances).

Cover or

Coverage

The scope of protection provided under an insurance contract.

Deductible Also known as excess, an amount that a policyholder agrees to pay, per claim or

per accident, toward the total amount of an insured loss. Insurers use this

mechanism to share risk with policyholders and reduce moral hazard.

Fraud Intentional perversion of truth to induce another to part with something of

value.

Insurance A system under which individuals, businesses, and other entities, in exchange

for a monetary payment (a premium), are guaranteed compensation for losses

resulting from certain perils under specified conditions.

Market Research Techniques used to determine a) the strength and characteristics of the demand

for insurance, and b) information about insurance and insurance substitutes

available in both the formal and informal markets.

Moral Hazard A risk that occurs when insurance protection creates incentives for individuals

to cause the insured event; or a behavior that increases the likelihood that the

event will occur, for instance bad habits such as smoking in the case of health

insurance or life insurance.

Policy The legal document issued by the company to the policyholder that outlines the

conditions and terms of the insurance; also called the policy contract or the

contract.

Policyholder A person or entity that pays a premium to an insurance company in exchange

for the coverage provided by an insurance policy.

Premium The sum paid by a policyholder to keep an insurance policy in force

Probability The likelihood that the insured event will occur.

Regulation Government defined requirements for an insurer, such as minimum capital

requirements and necessary expertise; also provides consumer protection

through the oversight of insurers, including pricing policies, form design and

appropriate sales practices.

Reinsurance A form of insurance that insurance companies buy for their own protection

Risk The chance of loss.

Underwriting Process of selecting risks for insurance and determining in what amounts and

on what terms the insurance company will accept the risk.

Page 33

Page 33 of 36

B. Afat Vimo for Odisha – Introductory Brochure Based on the final product. Need to be added once receive from LIC and UIIC.

C. Products under Microinsurance component 1. Module for practitioners

Page 34

Page 34 of 36

2. Southasiadisasters.net on Microinsurance

Page 35

Page 35 of 36

3. Workshop on finalizing Methodology for Microinsurance Demand survey

4. Background note for finalizing Methodology for Microinsurance demand Survey

Page 36

Page 36 of 36

5. Microinsurance Scoping Study

References

1. Background Note for Finalizing Methodology for Microinsurance Demand Survey (2011),

AIDMI and Concern Worldwide India.

2. Bhatt M. (2007), Humanitarian Partnerships: A Rapid Review of Recent Experience, The

Goal of Humanitarian Partnership: Lip Service or A Way of Working?, ICVA Conference,

http://www.icva.ch/doc00002014.html.

3. Economic Survey, 2010-2011 (2011), Planning and Coordination Department, Directorate of

Economics and Statistics, Government of Odisha

4. Microinsurance for Disaster Risk Reduction (2012), Training Module, Concern Worldwide

India with AIDMI.

5. Microinsurance for Disaster Risk Reduction: Post-disaster Recovery of the Poor (2012),

Southasiadisasters.net, Issue 83, AIDMI and Concern Worldwide India, www.aidmi.org.

6. Patra J., and Das C. (2011), Microinsurance Scoping Study, DIPECHO 6th Action Plan for

South Asia, Concern Worldwide India.

7. Workshop Report on Finalizing Methodology for Microinsurance Demand Survey (2011),

AIDMI with Concern Worldwide India.