36

Product Governance Arrangements under MiFID II and IDD Inez De Meuleneere & Hugo Verschaetse Compliance Day 7 June 2016

| Date post: | 20-Apr-2018 |

| Category: |

Documents |

| Upload: | duonghuong |

| View: | 222 times |

| Download: | 4 times |

Product Governance Arrangementsunder MiFID II and IDD

Inez De Meuleneere & Hugo Verschaetse

Compliance Day 7 June 2016

Overview

• Aim of POG-Arrangements, their legal basis andscope of application

• Who are manufacturers and distributors andwhat are their obligations

• The Potential and Identified Target Market

• Guidelines contained in the Final EIOPA report

• Liability regimes for info in product documentation

• IDD vs Assur-MiFID

Compliance Day 7 June 2016 Inez De Meuleneere & Hugo Verschaetse 2

Aim of new EU Product Oversight andgovernance (POG) arrangements regime• POG arrangements are considered to be fundamental

for investor protection purposes• Specific oversight, control and governance obligations

must insure due consideration given to interests of investors during whole life cycle of product

• Avoid and reduce from the start, potential mis-sellingrisks and help ensure that products and services are provided to the right customers

• Intended to reduce need for product intervention• Pro-active approach from the start of design phase,

instead of only reaction when detriment becomesapparent

Inez De Meuleneere & Hugo Verschaetse 3Compliance Day 7 June 2016

Conflicts of interest management

• Conflicts of interest managing role of the product approval process (see MiFID II Art. 16 (3) sub§1) makesit a key process, especially on the distribution side (because MiFID duty of care requirements rely on the MiFID service provider)

• Potential conflict areas:– correct pricing of illiquid financial instruments– self placements (cf. bail-inable instruments)– distribution of financial instruments issued by corporates

to which a closely related entity or department providedadvisory services

– cost and charges (structure)

Inez De Meuleneere & Hugo Verschaetse 4Compliance Day 7 June 2016

POG- arrangements under MiFID II

• Level 1 EU Directive 2015/65 (MiFID II) – Organisational requirements: Rec. (54), (71) to (73) and

Art. 9 (3) sub§ b, Art. 16 (3)– Investor protection: Rec. (86), (87) and Art. 24 (2) – Application date = 3 Jan 2017 – but Commission proposal

to postpone with 1 year

• Commission Delegated Directive adopted on 7 April 2016 - C (2016) 2031 final (Del. Dir.)– Rec (15) – (20)– Articles 9 and 10

• ESMA Technical Advice - Final Report 2014/1569 of 19 Dec 2014 (ESMA FR)

Inez De Meuleneere & Hugo Verschaetse 5Compliance Day 7 June 2016

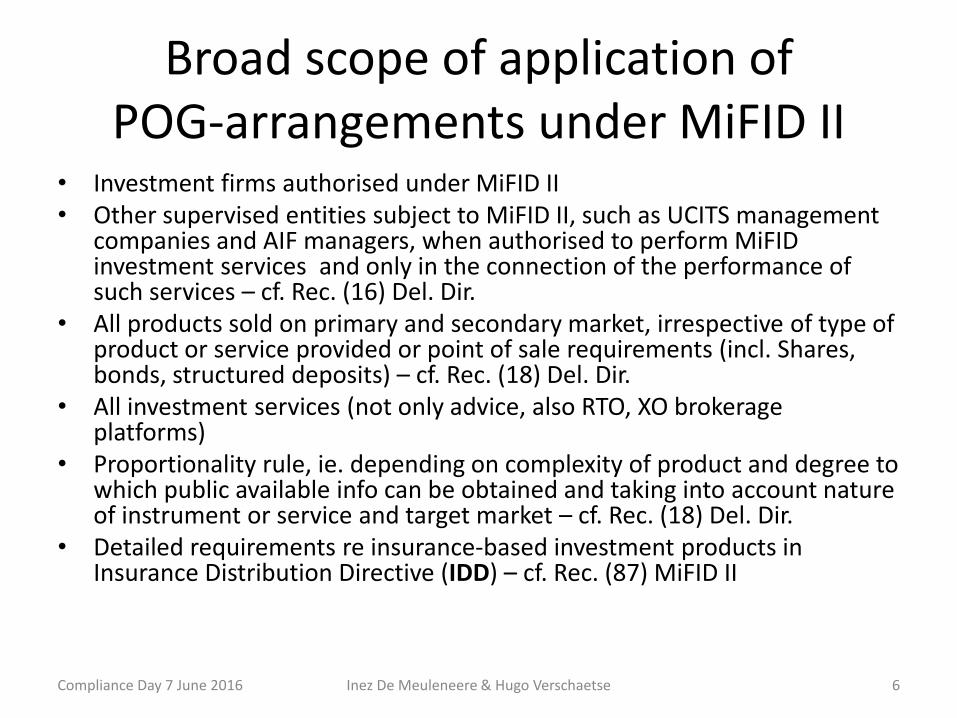

Broad scope of application of POG-arrangements under MiFID II

• Investment firms authorised under MiFID II• Other supervised entities subject to MiFID II, such as UCITS management

companies and AIF managers, when authorised to perform MiFIDinvestment services and only in the connection of the performance of such services – cf. Rec. (16) Del. Dir.

• All products sold on primary and secondary market, irrespective of type of product or service provided or point of sale requirements (incl. Shares, bonds, structured deposits) – cf. Rec. (18) Del. Dir.

• All investment services (not only advice, also RTO, XO brokerageplatforms)

• Proportionality rule, ie. depending on complexity of product and degree towhich public available info can be obtained and taking into account natureof instrument or service and target market – cf. Rec. (18) Del. Dir.

• Detailed requirements re insurance-based investment products in Insurance Distribution Directive (IDD) – cf. Rec. (87) MiFID II

Inez De Meuleneere & Hugo Verschaetse 6Compliance Day 7 June 2016

POG-arrangements for insuranceproducts

• Solvency II: requirement for firms to put in place organisationalarrangements which aim to ensure a correct design, developmentand monitoring of insurance products and customer protection– Rec. (16), Art. 27, 40 and 41 (1) sub§ 1– Implementation deadline = 1 January 2016

• IDD: customer protection and adding requirements for distributorswhich are not in scope of Solvency II: – Art. 25– Implementation deadline = 23 February 2018

• EIOPA Preparatory Guidelines on POG arrangements by insuranceundertakings and distributors – Final report of 6 April 2016– EIOPA’s Board of Supervisors adopted the Guidelines– Guidelines are addressed to competent authorities: how to proceed in

the preparatory period leading up to transposition of IDD andDelegated Acts – principle of ‘comply or explain’.

Inez De Meuleneere & Hugo Verschaetse 7Compliance Day 7 June 2016

…with again a broad scope of application

• Manufacturers: insurance undertakings and intermediaries who manufacture products(‘design’ of products by intermediaries for a group of (potential) clients, setting-proposingcoverage requirements, limits of indemnity, exclusions, …).

• Distributors: involved in insurance distribution activities;must have in place ‘ adequate arrangements’ to obtain the info from the manufacturer andto understand the identified target market.All types of distribution channels are in scope: (tied) agents, brokers, direct channels (online sales included), full and ancillary insurance intermediaries.The EIOPA Guidelines specify a separate adapted set of rules for distributors.

• For all ‘customers’: natural-legal persons (SME included, large risks excluded).

• All insurance products ie. life (including insurance-based investment products, 2nd pillarpension products) and non-life – exempted for insurance of large risks;– Exempted for the services and products on an ancillary basis as defined in art 1,3 IDD;– proportionality rule depending on nature of product.

• For products ‘newly designed or substantially modified’ as of date of entry into force. For ‘products still being distributed or brought to the market prior, authorities may considerrequiring compliance with ‘Product monitoring’ and ‘Remedial action’ (Guideline 8-9).

Inez De Meuleneere & Hugo Verschaetse 8Compliance Day 7 June 2016

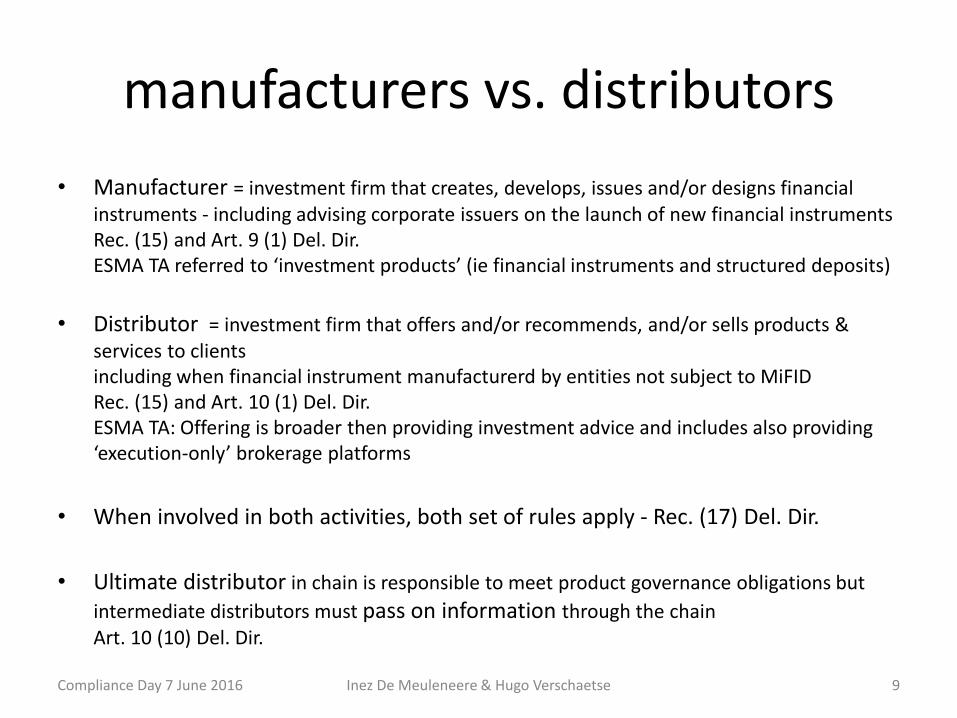

manufacturers vs. distributors

• Manufacturer = investment firm that creates, develops, issues and/or designs financial instruments - including advising corporate issuers on the launch of new financial instrumentsRec. (15) and Art. 9 (1) Del. Dir.ESMA TA referred to ‘investment products’ (ie financial instruments and structured deposits)

• Distributor = investment firm that offers and/or recommends, and/or sells products & services to clientsincluding when financial instrument manufacturerd by entities not subject to MiFIDRec. (15) and Art. 10 (1) Del. Dir.ESMA TA: Offering is broader then providing investment advice and includes also providing‘execution-only’ brokerage platforms

• When involved in both activities, both set of rules apply - Rec. (17) Del. Dir.

• Ultimate distributor in chain is responsible to meet product governance obligations but

intermediate distributors must pass on information through the chainArt. 10 (10) Del. Dir.

Inez De Meuleneere & Hugo Verschaetse 9Compliance Day 7 June 2016

manufacturer’s obligations…• Install a product approval process to ensure that

– product design complies with proper management of conflicts of interest

– manufacturing staff posses the necessary expertise or receive the appropriate training to understand characteristics and risks of manufactured products

– management body has effective control over the product governance process; info andstrategy re products to be included in compliance reports

• When manufacturing a new product

– identify a Potential Target Market of end clients (PTM)

– assess the risks of the product

– consider whether product meets identified needs, characteristics and objectives of the PTM

– consider the charging structure proposed for the product

• Information flows and reviews

– inform any distributor about all appropriate information on the product and the PTM

– regularly review the products and the PTM

– Best effort to identify crucial events that would affect the potential risk or return of the product and take appropriate action

Inez De Meuleneere & Hugo Verschaetse 10Compliance Day 7 June 2016

and distributor’s obligations• Install and maintain a product governance process to ensure

– Effective management control over determined range of investment products

– compliance with MiFID requirements (disclosure, AT/ST, inducements, COI mngt)

– oversight by compliance function; info and strategy re products in compliance reports

• When considering distribution of a new product or service

– define the target market (when product is manufactured by non-MiFID manufacturer)

– check compatibility with needs, characteristics and objectives of the Identified Target Market (ITM)

– arrange to obtain info to gain necessary understanding and knowledge of products

– ensure that relevant staff posses necessary expertise, or receive appropriate training tounderstand characteristics of the products and the needs, characteristics and objectivesof the ITM

• Sales – aftercare

– undertake regularly review of the product and services, assessing whether product remains consistent with needs of ITM

– Reconsider the distribution of a product when becoming aware to have mis-judged the target market or that the product does not longer meet the circumstances of the ITM

– provide the manufacturer with sales informationInez De Meuleneere & Hugo Verschaetse 11Compliance Day 7 June 2016

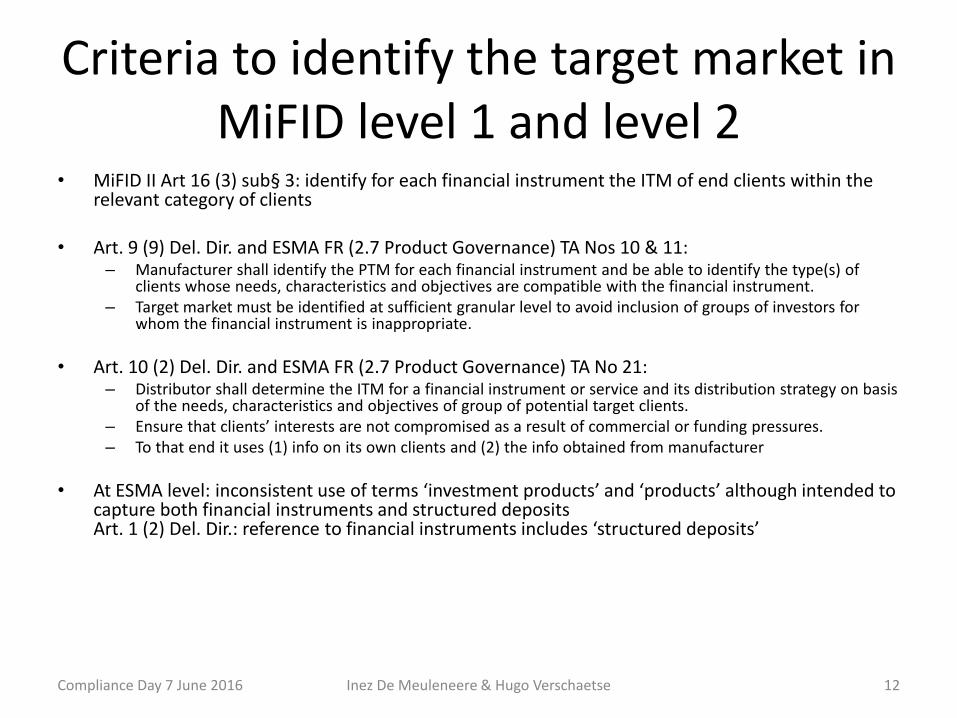

Criteria to identify the target market in MiFID level 1 and level 2

• MiFID II Art 16 (3) sub§ 3: identify for each financial instrument the ITM of end clients within the relevant category of clients

• Art. 9 (9) Del. Dir. and ESMA FR (2.7 Product Governance) TA Nos 10 & 11: – Manufacturer shall identify the PTM for each financial instrument and be able to identify the type(s) of

clients whose needs, characteristics and objectives are compatible with the financial instrument. – Target market must be identified at sufficient granular level to avoid inclusion of groups of investors for

whom the financial instrument is inappropriate.

• Art. 10 (2) Del. Dir. and ESMA FR (2.7 Product Governance) TA No 21:– Distributor shall determine the ITM for a financial instrument or service and its distribution strategy on basis

of the needs, characteristics and objectives of group of potential target clients.– Ensure that clients’ interests are not compromised as a result of commercial or funding pressures.– To that end it uses (1) info on its own clients and (2) the info obtained from manufacturer

• At ESMA level: inconsistent use of terms ‘investment products’ and ‘products’ although intended tocapture both financial instruments and structured depositsArt. 1 (2) Del. Dir.: reference to financial instruments includes ‘structured deposits’

Inez De Meuleneere & Hugo Verschaetse 12Compliance Day 7 June 2016

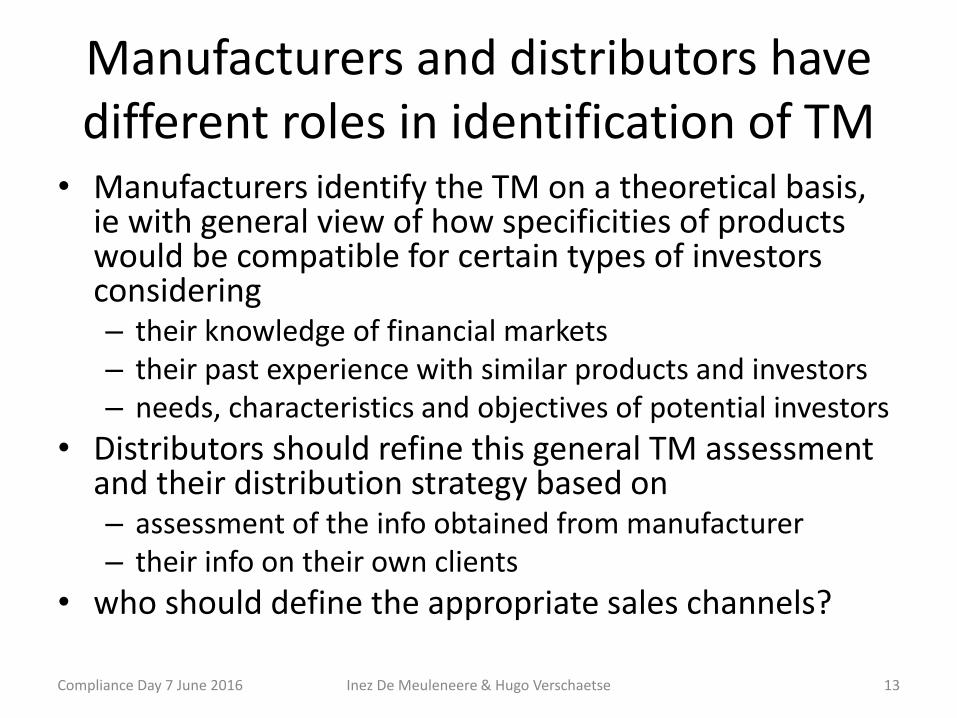

Manufacturers and distributors have different roles in identification of TM

• Manufacturers identify the TM on a theoretical basis, ie with general view of how specificities of productswould be compatible for certain types of investorsconsidering– their knowledge of financial markets– their past experience with similar products and investors– needs, characteristics and objectives of potential investors

• Distributors should refine this general TM assessment and their distribution strategy based on– assessment of the info obtained from manufacturer– their info on their own clients

• who should define the appropriate sales channels?

Inez De Meuleneere & Hugo Verschaetse 13Compliance Day 7 June 2016

Which criteria define the TM?

• ESMA refused to clarify the level of granularityrequired when identifying the TM > to be determinedon a case by case basis.

• Different other texts may help:– IOSCO Regulation of Retail Structured Products Final

Report 14/13 of December 2013– ESMA opinion 2014/332 of 27 March 2014 – Good

practices for products governance arrangements forStructured Retail Products

– EBA Final Report 2015/18 of 15 July 2015 – Guidelines on product oversight and governance arrangements for retailbanking products

– PRIIPs Regulation

Inez De Meuleneere & Hugo Verschaetse 14Compliance Day 7 June 2016

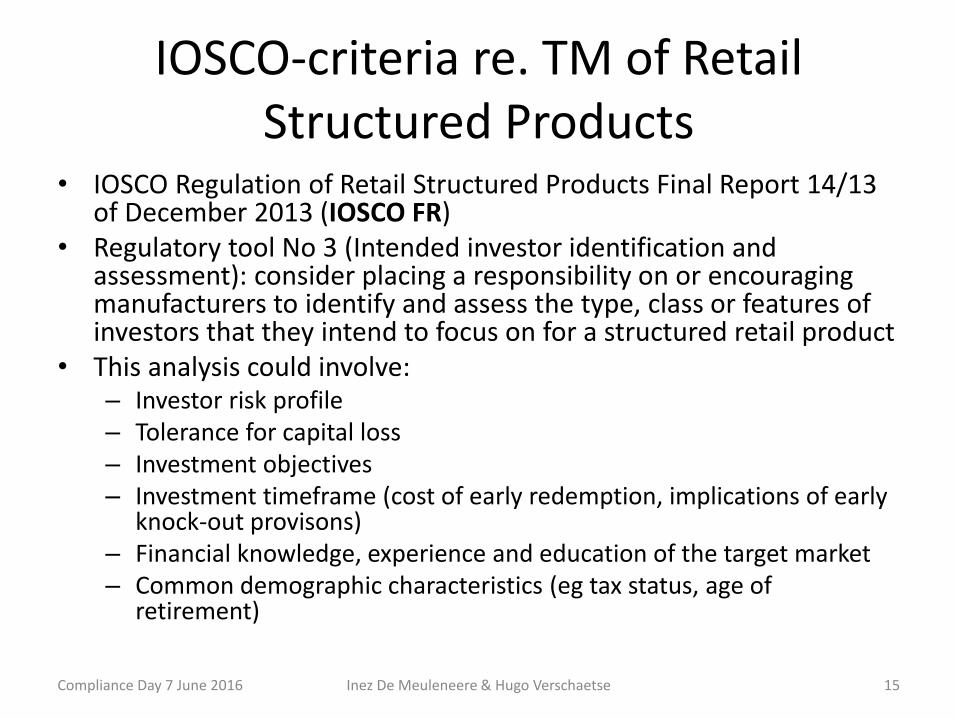

IOSCO-criteria re. TM of Retail Structured Products

• IOSCO Regulation of Retail Structured Products Final Report 14/13 of December 2013 (IOSCO FR)

• Regulatory tool No 3 (Intended investor identification andassessment): consider placing a responsibility on or encouragingmanufacturers to identify and assess the type, class or features of investors that they intend to focus on for a structured retail product

• This analysis could involve: – Investor risk profile– Tolerance for capital loss– Investment objectives– Investment timeframe (cost of early redemption, implications of early

knock-out provisons)– Financial knowledge, experience and education of the target market– Common demographic characteristics (eg tax status, age of

retirement)

Inez De Meuleneere & Hugo Verschaetse 15Compliance Day 7 June 2016

ESMA-criteria re. TM of Structured Retail Products (SRP)

• ESMA opinion 2014/332 of 27 March 2014 – Goodpractices for products governance arrangements forStructured Retail Products (SRPs)

• Define target market via assessment of which investorsare most appropriate to invest in SRPs, based on – To which market does this SRP provide exposure

– What is the needed investment horizon of a prospectiveinvestor to this SRP

– Limits of secondary markets for SRPs

– Risk absorbing capacity of potential investors

Inez De Meuleneere & Hugo Verschaetse 16Compliance Day 7 June 2016

EBA-criteria re. TM of retail banking products

• EBA Final Report 2015/18 of 15 July 2015 – Guidelines on product oversight and governance arrangements for retail banking products(EBA FR)

• Good practice examples re. target market, manufacturers couldconsider:– Tax status implications for different products– Level of risk of the product to be designed– Liquidity accessibility that the customer is expected to get– Level of risk that the customer is willing to bear– Demographic factors– Level of knowledge and understanding of the complexity of the

product, or– Potential creditworthiness of the consumer or financial capability of

the consumer

Inez De Meuleneere & Hugo Verschaetse 17Compliance Day 7 June 2016

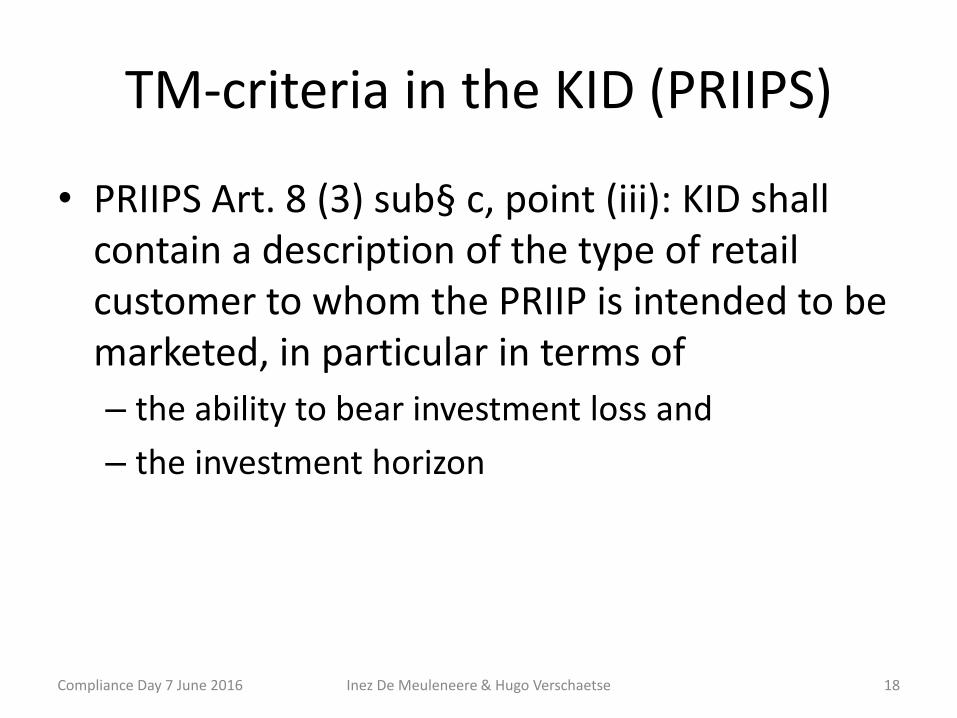

TM-criteria in the KID (PRIIPS)

• PRIIPS Art. 8 (3) sub§ c, point (iii): KID shallcontain a description of the type of retailcustomer to whom the PRIIP is intended to bemarketed, in particular in terms of

– the ability to bear investment loss and

– the investment horizon

Inez De Meuleneere & Hugo Verschaetse 18Compliance Day 7 June 2016

Relation to product info disclosure andto other MiFID requirements ?

• Manufacturer must make available to distributors all appropriateinfo on the product and on the product approval process, includingthe identified TM (MiFID Art. 16 (3) sub§ 3)

• Criteria to define TM and appropriate distribution channels overlap with or rely on (at least to a large extent) the characteristics andrisks of the product or MiFID client categories, which are disclosedin the product documentation and marketing material

• Definition of target market does not affect other COB requirementsof distributor (MiFID Art. 16 (3) sub§ 7), eg – appropriateness test needed when complex products or – suitability test in case of investment advise

• Distribution of products to clients outside TM is possible but onlyon a justified and exceptional basis (ESMA FR No 14 and 18, EBA FR p. 21)

Inez De Meuleneere & Hugo Verschaetse 19Compliance Day 7 June 2016

Insurance - Final EIOPA Report 6 April 2016 – highlightsGuidelines

• Guideline 1 – Establishment of POG arrangements – appropriatemeasures and procedures aimed at designing, monitoring, reviewing anddistributing products for customers – avoid that products may lead todetriment to customers – Guideline 4 Regular review of POG arrangements

• The manufacturer should not bring a product to the market if the product testingresults show that the product is not aligned with the interests, objectives andcharacteristics of the target market.

• The manufacturer should set out the POG arrangements in a written document (sufficient to refer to existing documents)…

• … and make it available to relevant staff, who should have knowledge of andobserve these arrangements.

Inez De Meuleneere & Hugo Verschaetse 20Compliance Day 7 June 2016

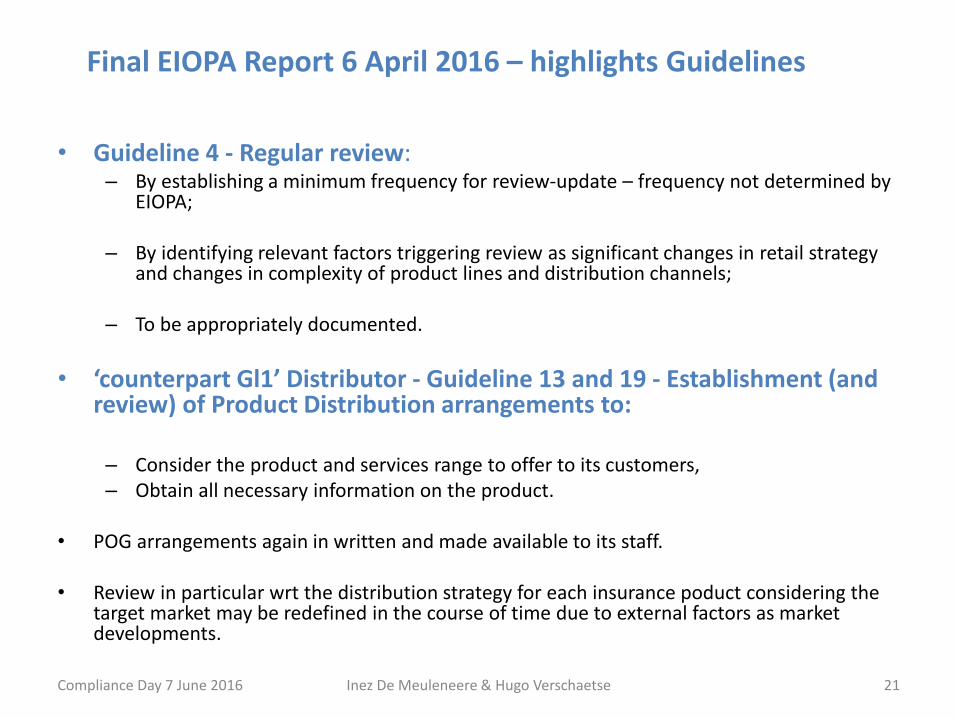

Final EIOPA Report 6 April 2016 – highlights Guidelines

• Guideline 4 - Regular review:– By establishing a minimum frequency for review-update – frequency not determined by

EIOPA;

– By identifying relevant factors triggering review as significant changes in retail strategyand changes in complexity of product lines and distribution channels;

– To be appropriately documented.

• ‘counterpart Gl1’ Distributor - Guideline 13 and 19 - Establishment (andreview) of Product Distribution arrangements to:

– Consider the product and services range to offer to its customers, – Obtain all necessary information on the product.

• POG arrangements again in written and made available to its staff.

• Review in particular wrt the distribution strategy for each insurance poduct considering the target market may be redefined in the course of time due to external factors as market developments.

Inez De Meuleneere & Hugo Verschaetse 21Compliance Day 7 June 2016

Final EIOPA Report 6 April 2016 – highlights Guidelines

• Guideline 2 – Objectives of the POG arrangements - in line with the MiFID II approach.

• Principle: The POG arrangements should aim to prevent and mitigate customer detriment, support a proper management of Conflicts of interest, and shouldensure that the objectives, interests and characteristics of the customers are dulytaken into account.

• Customer detriment when ‘not acting in accordance to the best interests of the customers’; ‘broader than a strict tick-box approach for compliance withregulation’. Concrete ‘cases due to poor product design and insufficient product governance, in Cz, ES, NL , IT, UK, … in life and non-life (payment protectioninsurance), products with limited coverage excluding main risks’.

• Conflicts of Interest: Specific chapter IDD for specific product scope: Insurance based investment products; but in BE -due to AssurMiFID- CoI already in force forlife and non-life.

• Principle of proportionality, taking into consideration the complexity of the product and the business of the manufacturer.

• Principle of appropriateness to account for the risks borne by policyholders for a product, both individual and collective policyholders interest.

Inez De Meuleneere & Hugo Verschaetse 22Compliance Day 7 June 2016

Final EIOPA Report 6 April 2016 – highlights Guidelines

• Counterpart Gl2 - Distributor Gl 14 Objectives of ‘product distributionarrangements’ – same principle, but other focus:

Not on product design and review, but on ‘preparation of the distribution of the products’, obtaining all relevant information from the manufacturer, and defining a distribution strategy.’

• Important check of Conflicts of Interest and the ‘best interest of the customer’: ‘this may implythat distributors abstain from distributing specific insurance products, for example in cases whereproducts do not offer any value to the customer, but only a high commission’.

• Distributor is not intended to make his own target market.

• For all distributors, even on ancillary basis, but ‘competent authorities need to take a proportionateand risk-based approach when applying these Guidelines’.

• Authorities have to take into account also whether the distributor is acting as a tied agent or as anindependent broker. Insurers with tied agents are anyhow responsible for insurance mediationactivities of tied agents (based on AssurMiFID).

Inez De Meuleneere & Hugo Verschaetse 23Compliance Day 7 June 2016

Final EIOPA Report 6 April 2016 – highlights Guidelines

• Guideline 3 – Role of Management – the ultimate responsibility for the procedures andmeasures lies with the top management of an entity.

• Any relevant key function of the manufacturer can be involved in the establishment andreviews of the POG arrangements.

• No EIOPA-rules regarding the role of the key functions, while MiFID II is more explicit: the compliance function monitors the development and periodic review of product governancearrangements.

• Compliance also reports systematically to the Board about products offered and services provided (MiFID II). In practice similar important role for compliance function in insurance?

• Counterpart Distributor Gl 15.

• Guideline 5 – Target market (positive and negative) – the manufacturer has to includesuitable steps in order to identify the relevant target market (positive and negative).

• The ‘good practice’-examples (on slide 17) listed in the EBA Report 2015/ 18 of 15/7/2015 are taken over in the EIOPA Report of 6/4/2016.

• Is added in the EIOPA report and typical for insurance products: ‘insurance coverage andexclusions’.

• The negative target market is helpful in order to get a clear picture of the boundaries of a product. Example given: a life insurance policy running for 30 y for a 97 y old lady.

• What about the target market group for a lot of non-life products? The target market group is very broad for most of these products … mass retail market.

Inez De Meuleneere & Hugo Verschaetse 24Compliance Day 7 June 2016

Final EIOPA Report 6 April 2016 – highlights Guidelines

• Counterpart Distributor Gl 16 -17: obtaining all necessary information on the target market / product from the manufacturer.

• The target market info is needed for setting up a distribution strategy, and to assess to whichcustomers to advertise the product.

• When acting as manufacturer and distributor (eg insurer with tied agents), only one target market assessment is required (MiFID II-based statement).

• The product info includes info on the main product characteristics, its risks and costs, andcircumstances which may cause a conflict of interest.

• Counterpart Distributor Guideline 18 the distribution strategy should notcontradict or has to be consistent with the distribution strategy and the target market defined by the manufacturer.

• Circumstances may be outlined defining under which distribution of products outside the target market is permitted exceptionnally;

• In case of sale outside the target market, the distributor has to be able to justify that the product fits with the best interest of the customer, and this has to be documented.

Inez De Meuleneere & Hugo Verschaetse 25Compliance Day 7 June 2016

Final EIOPA Report 6 April 2016 – highlights Guidelines

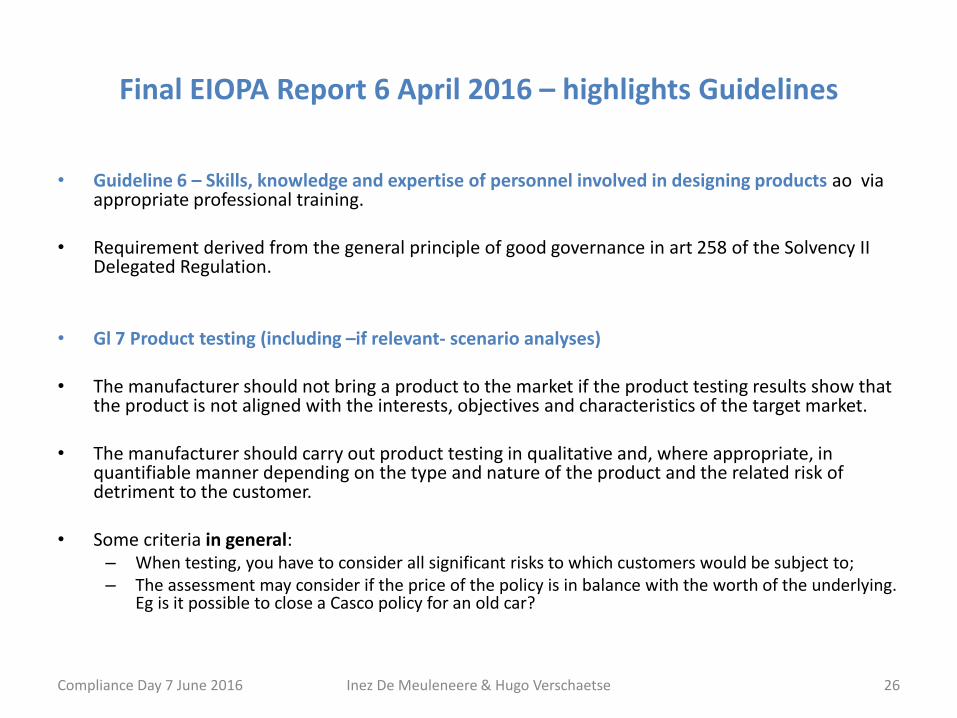

• Guideline 6 – Skills, knowledge and expertise of personnel involved in designing products ao via appropriate professional training.

• Requirement derived from the general principle of good governance in art 258 of the Solvency II Delegated Regulation.

• Gl 7 Product testing (including –if relevant- scenario analyses)

• The manufacturer should not bring a product to the market if the product testing results show thatthe product is not aligned with the interests, objectives and characteristics of the target market.

• The manufacturer should carry out product testing in qualitative and, where appropriate, in quantifiable manner depending on the type and nature of the product and the related risk of detriment to the customer.

• Some criteria in general: – When testing, you have to consider all significant risks to which customers would be subject to;– The assessment may consider if the price of the policy is in balance with the worth of the underlying.

Eg is it possible to close a Casco policy for an old car?

Inez De Meuleneere & Hugo Verschaetse 26Compliance Day 7 June 2016

Final EIOPA Report 6 April 2016 – highlights Guidelines

• Gl 7 Product testing• Examples for insurance based investment products: - inspired by ‘suitable advice’

– Impact on the risk and reward profile of the product following changes to the value and liquidity of underlying assets;

– What happens in case of changes in the tax environment?– What happens in case the manufacturer has financial problems?– What in case of surrender by the policy holder?– How is the risk-reward profile of the product balanced taking into account its cost structure?

• Examples for non-life of topics to be considered : concerns going from ‘clear information tothe customer’ to ‘value for money for the customer’ – ‘what’s in it for me’? How to balance?– Do the expected claims ratio and claims payment policy suggest that the product is of monetary

benefit for customers? ‘Value for money’; – Does the coverage of one product potentially overlap with the coverage of another product? This ha

been one of the main points of attention for the need analysis within the AssurMiFID legislation.– Does the coverage reflects sufficiently the future needs of the target group? – Does the customer understand the terms and limitations of the policy?

• Introduction of a general price control - how far in theory and in practice? Different EIOPA point of view in ‘Summary of responses to online survey in preparation of …. the delegated acts under IDD of 2/3/2016’: ‘There should be no interference in a market process for price determination. Subjectiveterms as ‘fairly priced’ should be avoided’.

Inez De Meuleneere & Hugo Verschaetse 27Compliance Day 7 June 2016

Final EIOPA Report 6 April 2016 – highlights Guidelines

• Product monitoring (guideline 8) and 9 Remedial action - Once the product is distributed, the manufacturer should monitor on an ongoing basis that the product continues to be in line with the interests, objectives and characteristics of the target market.

• Examples in general – related to: ‘is the customer getting a ‘fair deal’ – ‘value for money’ – The manufacturer takes into account the level of the claims ratio as well as the claims

policy; – The manufacturer takes into account the causes of customer complaints;– Pricing seems to become an essential part of the POG.

• Remedial action – Should the manufacturer identify, during the lifetime of the product, circumstances related to the product and giving rise to the risk of customer detriment, he should take appropriate action to mitigate the situation.

• If relevant, he should notify any relevant remedial action promptly to the distributorsinvolved and to the customers.

• The product lifetime is understood as ‘capturing the entire life cycle of a product fromproduct design over distribution of the product until withdrawal of the last policy-product from the market’.

• Examples given are very general – just a more concrete example: in case the risk profile – risk score of a product has changed due to market developments.

Inez De Meuleneere & Hugo Verschaetse 28Compliance Day 7 June 2016

Final EIOPA Report 6 April 2016 – highlights Guidelines

• Counterpart Distributor Guideline 20 Info from distributor to manuafacturer• Obligation for distributor to inform the manufacturer without undue delay when he becomes aware that

the product is not aligned (any longer) with the interest, objectives of the target market or there is a risk of customer detriment.

• This is info about the amount of sales made outside the target market, summary info on the customers or summary of the complaints related to a product -> allowing the manufacturer to monitor the product;

• This is not about regular reporting about all sales, or a confirmation that each transaction was distributedto the correct target market.

• Guideline 10 – The manufacturer should select distribution channels that are appropriate for the target market considering the particular product characteristics.

• The manufacturer should provide information to distributors, including the details of the products. The information should be sufficient to enable the distributor to understand and place the product properlyon the target market, and to identify the client target group in a positive and negative way.

• Manufacturers may eg survey a number of customers to find out if they understood the product features and to see if they fit into the target market.

• Manufacturers should monitor whether the product is distributed to customers belonging to the target market, and take remedial action to the distribution channel if this channel does not meet the objectivesof the POG arrangements. This can mean to cease to make a product available for a distributor.

Inez De Meuleneere & Hugo Verschaetse 29Compliance Day 7 June 2016

Final EIOPA Report 6 April 2016 – highlights Guidelines

• Guideline 11 In case of outsourcing of the product design, the manufacturershould retain full responsibility for compliance with the POF arrangements.

• Guideline 12 Documentation – Actions taken by the manufacturer should bedocumented, kept for audit purposes and made available to competent authorities upon request.

• Recommended holding period of records: in a durable medium for a period of 5y, startingwhen the relevant action is taken...

• … Or longer, eg due to the lifetime of a product.

• Counterpart Guideline 21 for Distributors – same approach as for manufacturer• The distributor also has to document all necessary target market and product related info

from the manufacturer.

• IDD- Recital 55 related to POG quote versus the EIOPA Report:

• This Directive should not limit the variety and flexibility of the approaches whichundertakings use to develop new products.

Inez De Meuleneere & Hugo Verschaetse 30Compliance Day 7 June 2016

Overview of liability regimes for product info in documentation

• PROSPECTUS DIRECTIVE - Art. 6 (2): no civil liability for summary unless– it is misleading, inaccurate or inconsistent when read together with the other

parts of the prospectus or – it does not provide, when read together with other parts of the prospectus,

key information in order to aid investors to make investment decision

• UCITS IV – Art. 79: no civil liability solely on the basis of the KII unless it is misleading, inaccurate or inconcistent with the relevant parts of prospectus

• PRIIPS – Art. 11 (1): manufacturer shall not incur civil liability solely on the basis of the KID unless it is misleading, inaccurate or inconsistent with the relevant parts of legally binding pre-contractual and contractualdocuments or with the requirements cf. Art. 8 (ie. the list of info to becontained in KID)

• MiFID II – Art. 24: information duty of the distributor to provide (potential) clients with fair, clear and not misleading info re. the service, financial instruments, investment strategies, execution venues and costs & charges

Inez De Meuleneere & Hugo Verschaetse 31Compliance Day 7 June 2016

IDD – ‘Specific Conduct of Business rulesfor Insurance-based investment

products’ – going further than TwinPeaks II – AssurMiFID?

Hugo Verschaetse

Compliance Day 7 June 2016

IDD – Product scope – Insurance-based investment products – same definition as in PRIIPS (Key

Information Document)

• Product Scope IDD: out of scope are ‘non life’, ‘pure protection life’ and ‘pension products’

• This means that are out of scope:

• Non-life insurance products, including health products;

• Life insurance contracts where benefits are only paid in case of death or incapacity (due to injury, sickness or incapacity);

• Pension Products:

• 3d pillar: ‘pension products (and annuities) which under national law are recognized as having the primary purpose of providing the investor with an income in retirement;

• 2nd pillar as group insurance: officially recognized as occupational pension schemes (and annuities) as far as officially falling under the scope of Directive 2003/41/EC (EIORP) or Directive 2009/138/EC (Solvency II).

• Conclusion: In scope are:

• all unit linked life products, and

• all ‘with profit’ universal life and classic life products with savings component and with guarantee by the insurer,

• With regular and single premium payment options,

• except for ‘pure protection life’ and ‘pension products’. Remark: 3d pillar pension products are within the scope of Twin Peaks II.

Conflicts of Interest (CoI) (art 27-28 IDD) - Identify, prevent and mitigate, have a CoI policy and disclose CoI

These topics are included in the AssurMiFID chapter about Conflicts of Interest, even for a broader product range including non-life products and most life products (2nd pillar pension excluded).

Suitable advice and appropriateness for insurance-based investment products

Suitable advice: When advising these products, a suitability test is obligatory: .

Knowledge & experience of the client is checked, mainly knowledge of the risks of the productsoffered to the customer;

His investment objectives, his financial capacity and risk tolerance are checked;

In case of ‘no advice’, appropriateness test about the ‘knowledge and experience’ of the customer’ is obligatory.

This is all included in the AssurMiFID chapter about Duty of Care – Suitable Advice; feedback byFSMA about FSMA Inspections re the implementation of Duty of Care for Branch 21 and 23 products in the insurance sector.

The advice has to be specified with a statement in a durable medium (eg in writing), specifying the advice given and how that advice meets the preferences, objectives and othercharacteristics of the customer, and this before the conclusion of the contract. Entirely based on MiFID II Directive.

IDD – Insurance-based investment productsConflicts of Interest (art 27-28 IDD)Duty of Care (art. 30 IDD)

NEW

TwinPeaks

TwinPeaks

‘In good time prior to the conclusion of the contract, the insurance distributor has toinform the customer:

1 when advice is provided, whether or not he will receive a periodic assessment of the suitability of the recommended products;

2 about appropriate guidance and warnings of the risks associated with the products /or particularinvestment strategies proposed;

3 about ‘all costs and associated charges’, information related to the distribution of the product, including the cost of advice, where relevant, the cost of the product recommended or marketed to the customer and how the customer may pay for it, alsoencompassing any 3d party payments (art 29,1,c): In principle aggregated; Itemized breakdown on request of the customer;

Recital 42 ‘KID+’ The IDD cost disclosure will have to be coordinated with the obligatory content of the KeyInformation Document (PRIIPS Regulation): ‘In addition to the information required to be provided in the form of the key information document, distributors should provide additional information detailing any cost of distribution that is not already included in the costs specified in the KID, so as to enable the customer tounderstand the cumulative effect that aggregated costs have on the return of the investment’.

Info has to be given not only ‘prior to the conclusion of the contract’,

but also ‘where applicable, such information shall be provided to the customer on a regular basis, at leastannually, during the life-cycle of the investment’. This recurring obligation is even broader than in MiFID II (linked to ‘ongoing advice’ – with periodic suitability assessment).

IDD – Insurance-based investment products -Inform Your Customer – full cost transparency(art. 29 IDD) – ‘copy paste MiFID II ’

NEW

NEW

Where inducements (fees, commissions, non-monetary benefits) are received/paid to or by any party except the customer (or a person on behalf of the customer), the inducements: May not have a detrimental impact on the quality of the relevant service to the customer and; May not impair with the MiFID principle (the insurance distributor has to act honestly, fairly and

professionally in accordance with the best interest of its customers).

Comment: In the MiFID Directive, the inducement has to ‘contribute to the quality of the service’ while here the inducement ‘may not have a detrimental impact’ -> a ‘light enhancement check’ in IDD? In AssurMiFID the ‘MiFID enhancement check’ has been included.

The Commission is empowered to adopt Delegated Acts ao to determine the criteria for assessingwhether inducements have a detrimental impact; EIOPA is to inspire the Commission.

IDD stimulates ‘gold plating’ by Member States: ‘in particular, MS may additionally prohibit or furtherrestrict the offer or acceptance of fees,commissions or non-monetary benefits’.

The stricter rules for ‘independent advice’ including interdiction of commission and (obligatory) fee payment (by customer directly to intermediary) in the IMD II Commission draft and MiFID II, are notincluded in IDD.

IDD – Insurance-based investment products -Rules Inducements (art. 29 IDD)

IDD

=/=MiFID

II

IDD

=/=MiFID

II

TwinPeaks

![How PET and Personalized Onco-Genomic (POG) Trial are Able ... · CCNA2 [92%] TYMS [99%] 6 673 SNV = hypermutated. Genomic based treatment ... •Biopsied for study Dec 2012. POG](https://static.documents.pub/doc/80x56/5e30bde903120c1add16f137/how-pet-and-personalized-onco-genomic-pog-trial-are-able-ccna2-92-tyms.jpg)

![Blast Boxers / POG [UK]](https://static.documents.pub/doc/80x56/568bdc2b1a28ab2034b13634/blast-boxers-pog-uk.jpg)