198

Didier Faivre

Didier Faivre

2

Digital rate options and applications to exotic swapsComplex Products : digital, steepner, ratchet…Bermuda swaptionsCallablesAppendixes :Standard Deviations vs VolatilitiesSABRCorrelation issuesLGMRisk-Management of exotics

3

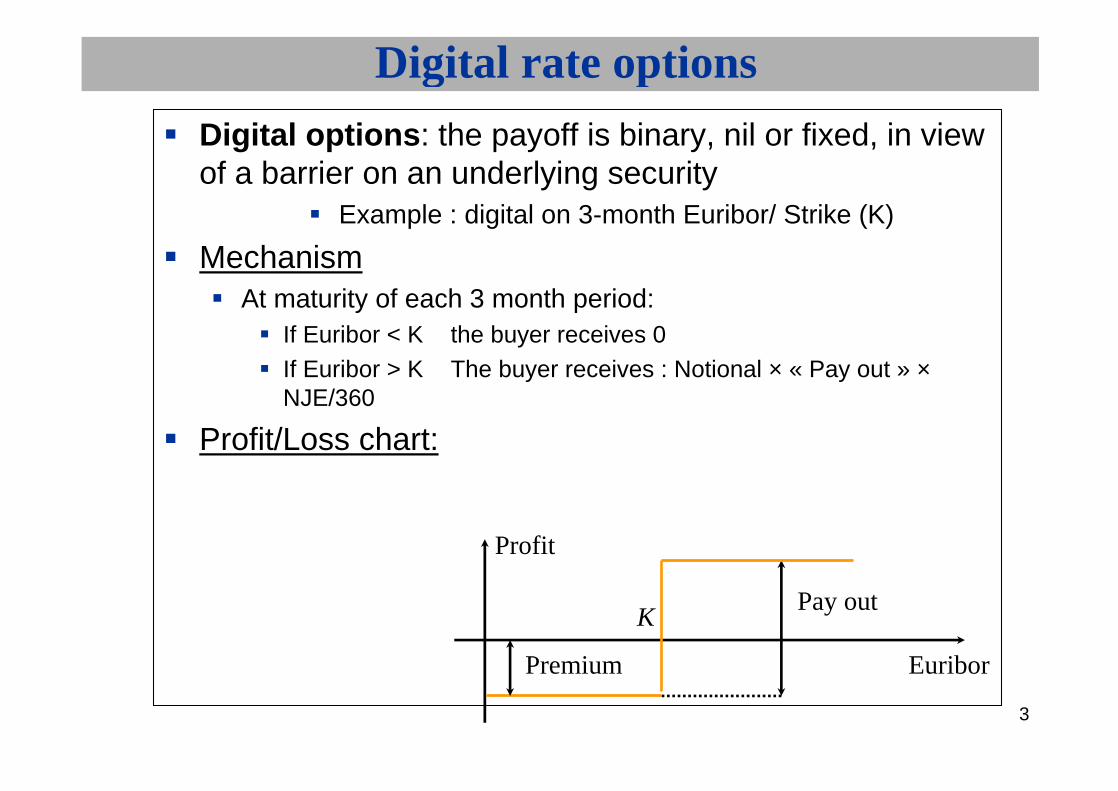

Digital options: the payoff is binary, nil or fixed, in view of a barrier on an underlying security

Example : digital on 3-month Euribor/ Strike (K)

MechanismAt maturity of each 3 month period:

If Euribor < K the buyer receives 0If Euribor > K The buyer receives : Notional × « Pay out » ×NJE/360

Profit/Loss chart:

Euribor

Profit

KPay out

Premium

Digital rate options

4

Profit/Loss chart:

S

Premium

Profit

Euribor

Pay out

Digital rate options

5

example: sell a digital option with payoff equal to 2 % if the 3-month interest rate is higher than 4 %

possible hedging modality: buy a call at 3 % and sell a call at 5 % with same initial nominal amount of the digital option (the approximation of a digital option by using a call spread).

Digital rate options

6

3-month rate

Intrinsic value

barrier

0 5 %

premium

3 % 4 %

digital Call spread

Digital rate options

7

The barrier is suitably replicated by reducing the spread of 200to 20 bp (buying a call at 3.9% and selling a call at 4.10% for the bank selling the digital).

The equalisation of the payoff therefore implies multiplying thenominal amount by 10.

A digital option therefore corresponds to a leverage effect on an options spread.

Digital rate options

8

Digital rate options

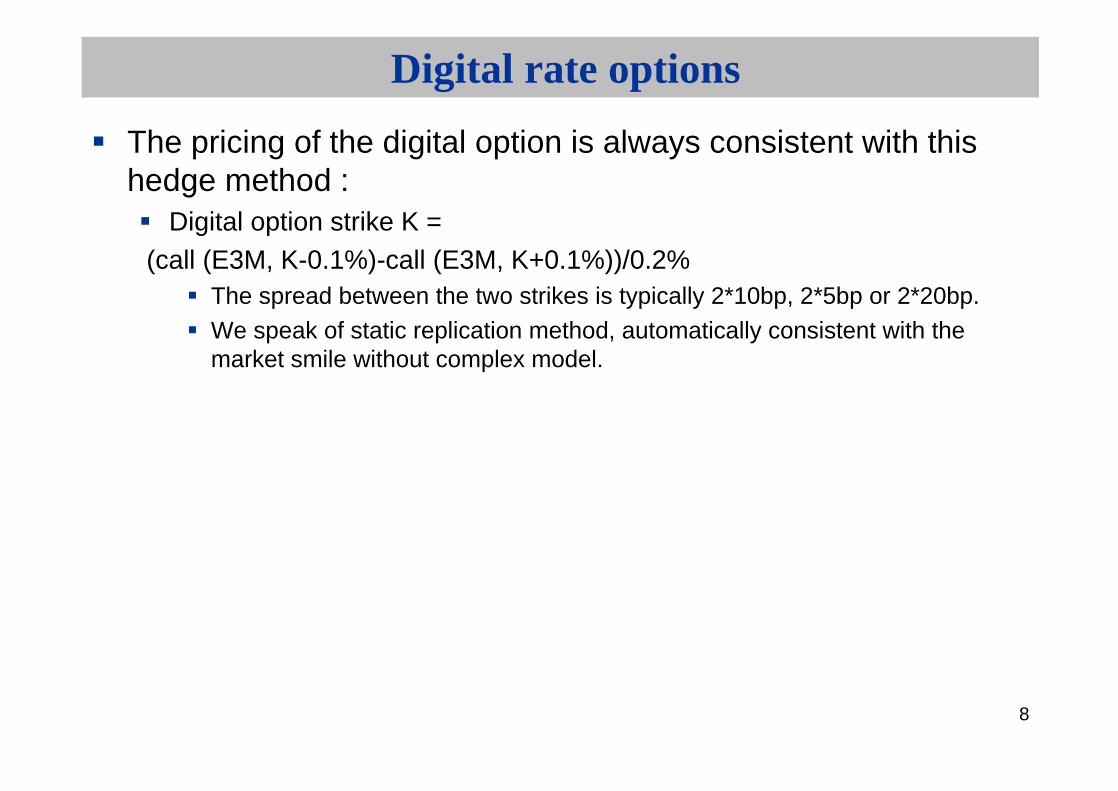

The pricing of the digital option is always consistent with thishedge method :

Digital option strike K =(call (E3M, K-0.1%)-call (E3M, K+0.1%))/0.2%

The spread between the two strikes is typically 2*10bp, 2*5bp or 2*20bp.We speak of static replication method, automatically consistent with the market smile without complex model.

9

Digital rate options

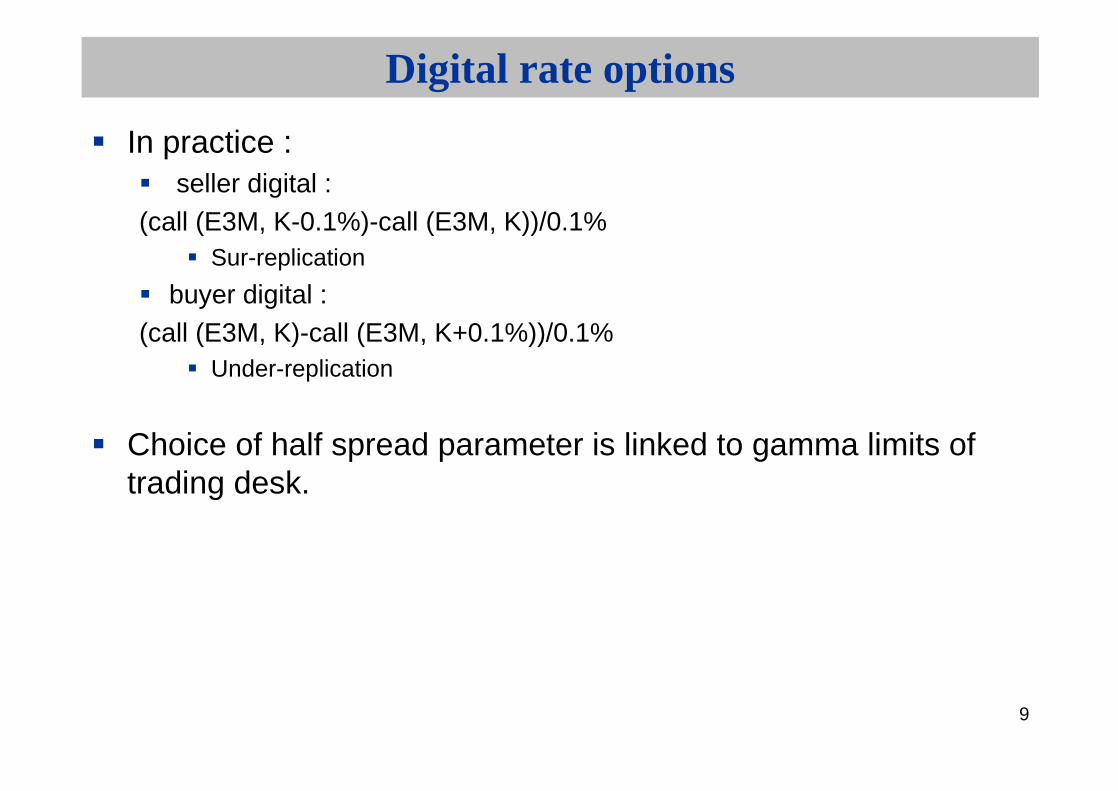

In practice :seller digital :

(call (E3M, K-0.1%)-call (E3M, K))/0.1%Sur-replication

buyer digital : (call (E3M, K)-call (E3M, K+0.1%))/0.1%

Under-replication

Choice of half spread parameter is linked to gamma limits of trading desk.

10

Digital rate options

3-month rate

Intrinsic value

0

KK-0.1 %

1+premium

1%1.0

3 KME

K+0.1 %

1%1.0

3 KME

Sur-replicationUnder-replication

premium

11

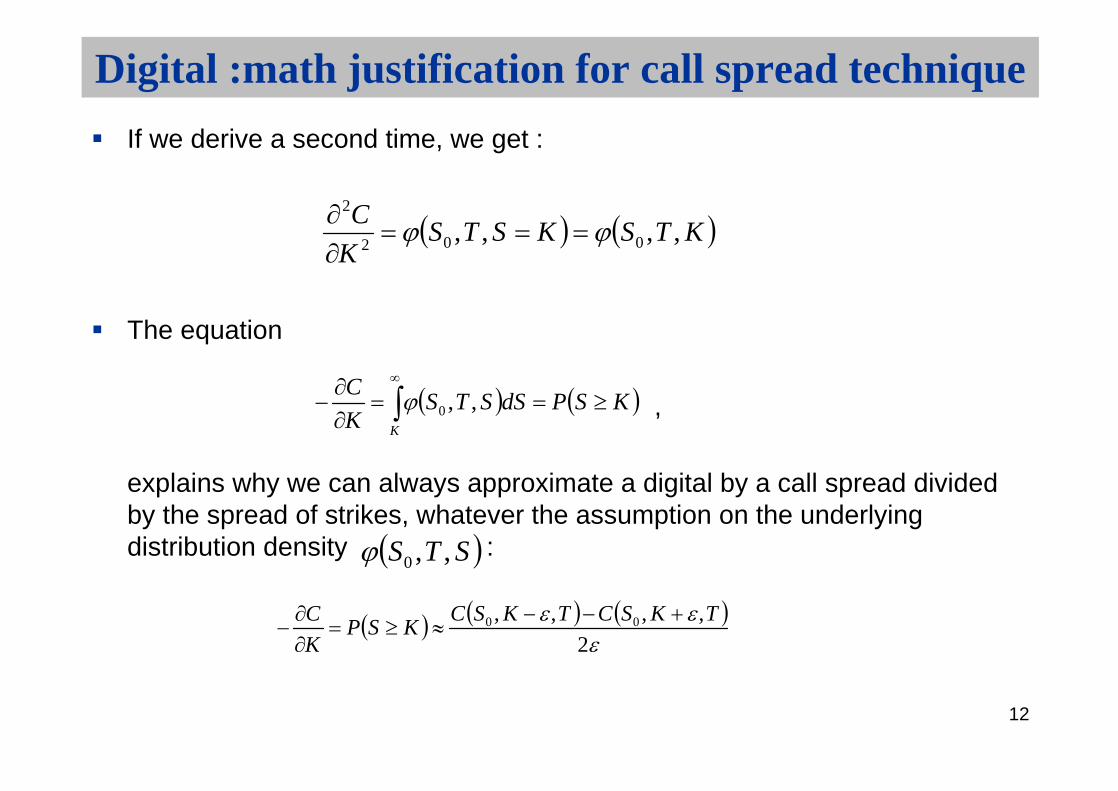

Digital :math justification for call spread technique

Let have and underlying with initial value and density

The price of a call (with premium paid at maturity T) is :

Then

0S

dSSTSKSTKSCK

,,,, 00

STS ,,0

KK

KK

dSSTSdSSTSKSTSKKSTSK

dSSTSKdSSTSSKK

C

,,,,,,,,

,,,,

0000

00

12

Digital :math justification for call spread technique

If we derive a second time, we get :

The equation

,

explains why we can always approximate a digital by a call spread dividedby the spread of strikes, whatever the assumption on the underlyingdistribution density :

KTSKSTSK

C,,,, 002

2

KSPdSSTSK

C

K

,,0

STS ,,0

2

,,,, 00 TKSCTKSCKSP

K

C

13

Digital :math justification for call spread technique

Indeed, it’s important to see the previous demonstration is general and doesn’t rely on any assumption on .

If we now use the (Lognormal) B&S framework, we get :

In pratice, prices of digital using the call-spread method or the analyticalB&S formula (lognormal or normal), leads to very different prices.

2dNKSPK

C

14

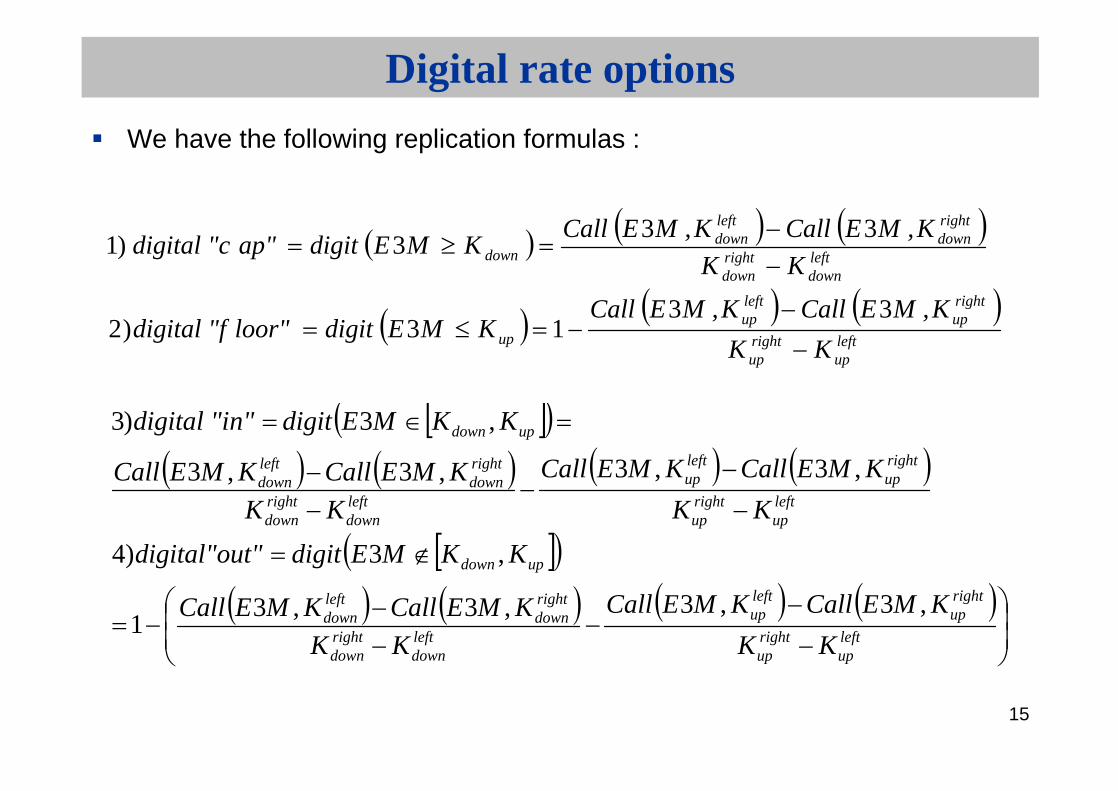

Digital rate options

Other pay-off :Let’s note :

bpKK

bpKK

bpKK

bpKK

KK

uprightup

upleftup

downrightdown

downleftdown

updown

10

10

10

10

15

Digital rate options

We have the following replication formulas :

leftup

rightup

rightup

leftup

up

leftdown

rightdown

rightdown

leftdown

down

KK

K,MECallK,MECallKMEdigitloor"digital "f

KK

K,MECallK,MECallKMEdigitap"digital "c

3313)2

333 )1

leftup

rightup

rightup

leftup

leftdown

rightdown

rightdown

leftdown

updown

leftup

rightup

rightup

leftup

leftdown

rightdown

rightdown

leftdown

updown

KK

KMECallKMECall

KK

KMECallKMECall

KKMEdigitt"digital"ou

KK

KMECallKMECall

KK

KMECallKMECall

KKMEdigitn"digital "i

,3,3,3,31

,3)4

,3,3,3,3

,3 )3

16

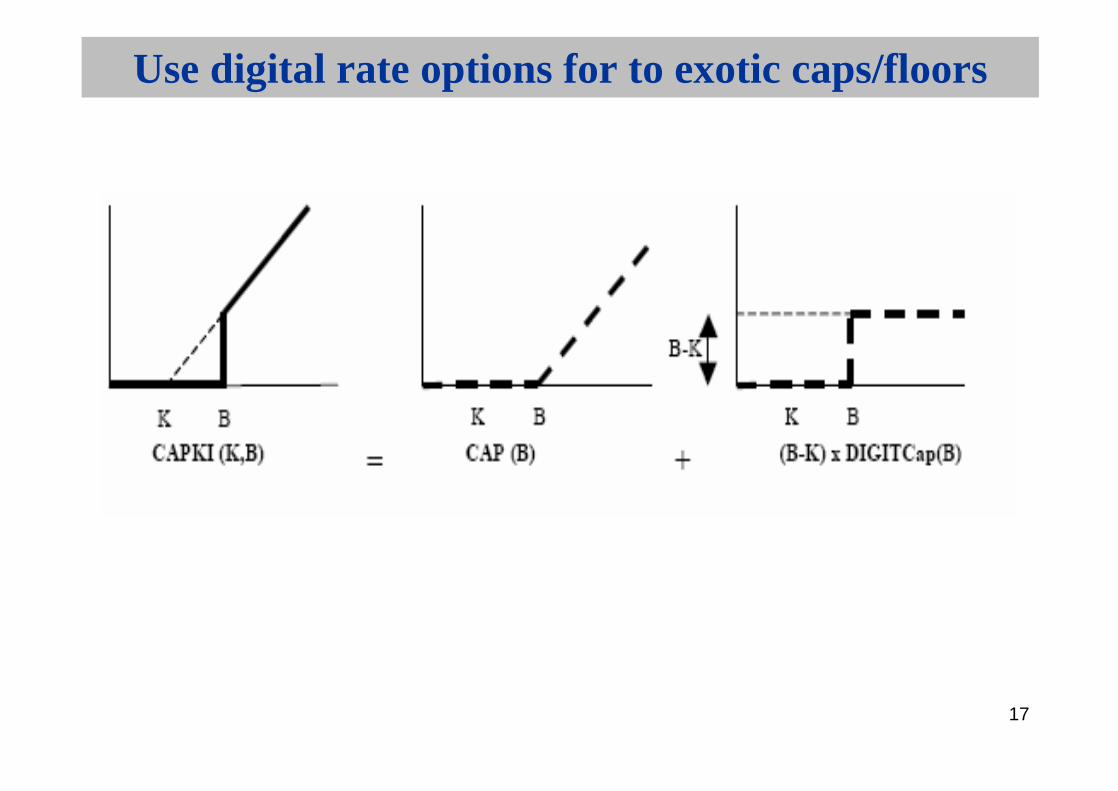

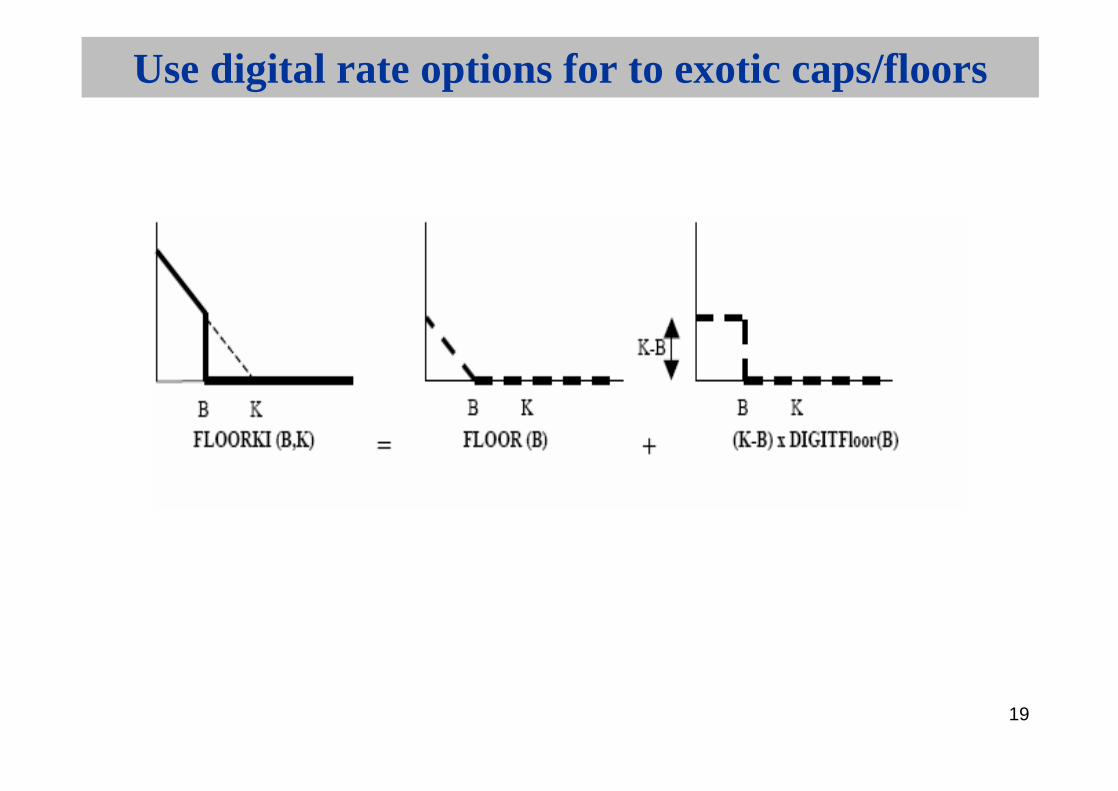

Use digital rate options for to exotic caps/floors

Cap Knock-in :Pay-off :

Valuation :Buyer Cap with the strike set to B (the barrier)A buyer digital “Cap” with barrier B and Fixed rate =

(B-K)

KB

KME BME313

17

Use digital rate options for to exotic caps/floors

18

Use digital rate options for to exotic caps/floors

Floor Knock-in :Pay-off :

Valuation :Buyer Floor with the strike set to B (the barrier)A buyer digital “floor” with barrier B and Fixed rate =

(K-B)

KB

MEK BME313

19

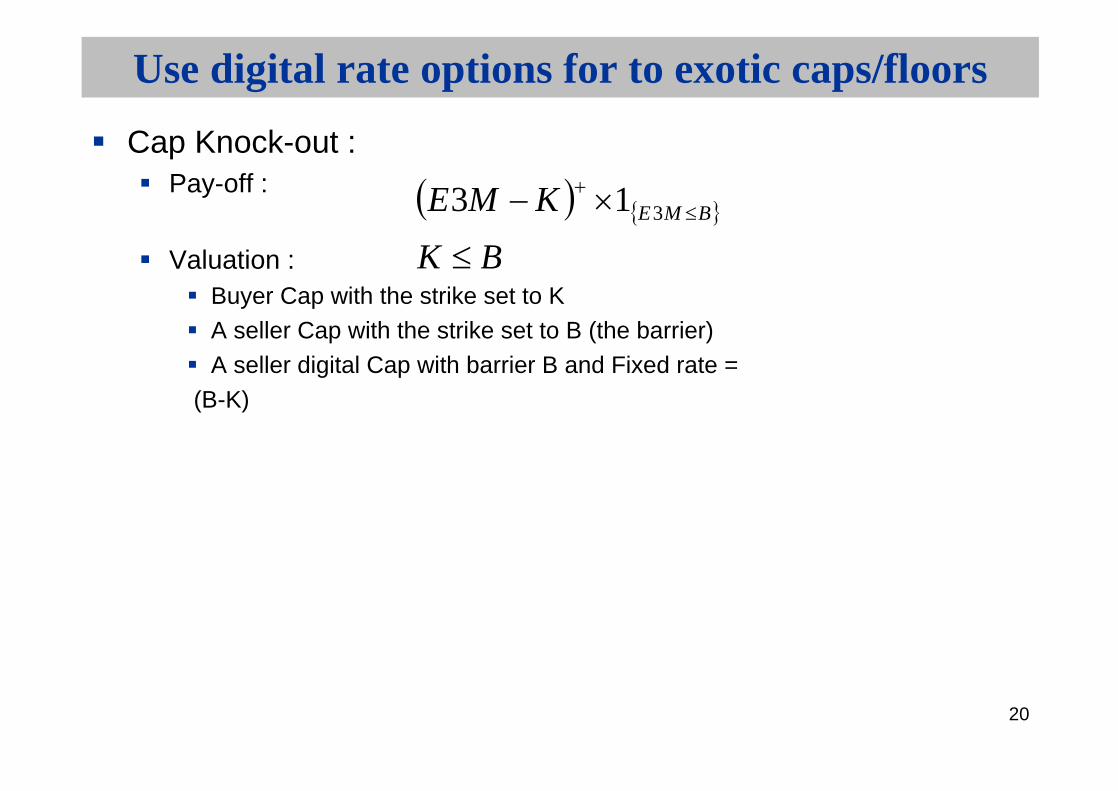

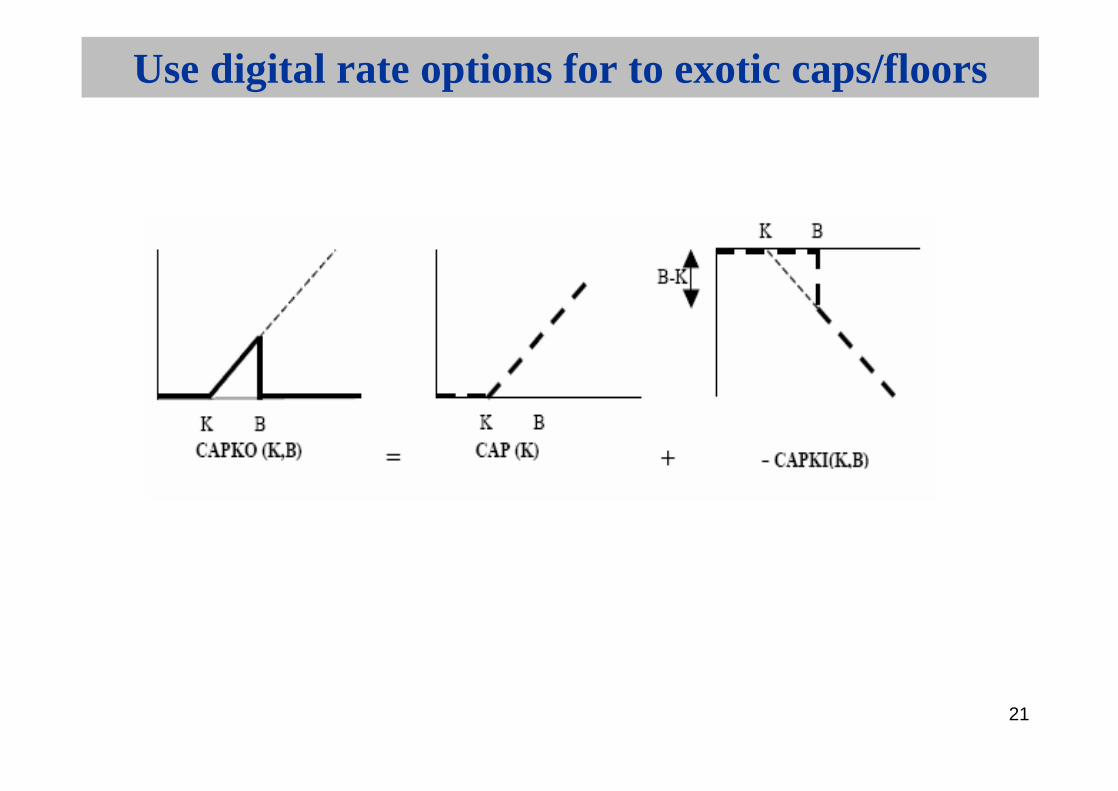

Use digital rate options for to exotic caps/floors

20

Use digital rate options for to exotic caps/floors

Cap Knock-out :Pay-off :

Valuation :Buyer Cap with the strike set to KA seller Cap with the strike set to B (the barrier)A seller digital Cap with barrier B and Fixed rate =

(B-K)

BK

KME BME313

21

Use digital rate options for to exotic caps/floors

22

Use digital rate options for swap KO

Swap KOBank pays

r if index1 < B, index2 + m otherwise

Replication of receiver swap KO:Receiver fixleg rate rPayer floatleg on index2Buyer cap Knock-In on index1

Buyer cap strike B on index1Buyer digital Cap barrier B on index1 and Fixed rate (B+m)-r

23

Digital rate options : application to exotic swaps

24

Digital rate options : application to exotic swaps

Floor Knock-out :Pay-off :

Valuation :Buyer Floor with the strike set to KA seller Floor with the strike set to B (the barrier)A seller digital “Floor” with barrier B and Fixed rate =

(K-B)

KB

MEK BME313

25

Digital rate options and applications to exotic swapsComplex Products : digital, steepner, ratchet…Bermuda swaptionsCallablesAppendixes :Standard Deviations vs VolatilitiesSABRCorrelation issuesLGMRisk-Management of exotics

26

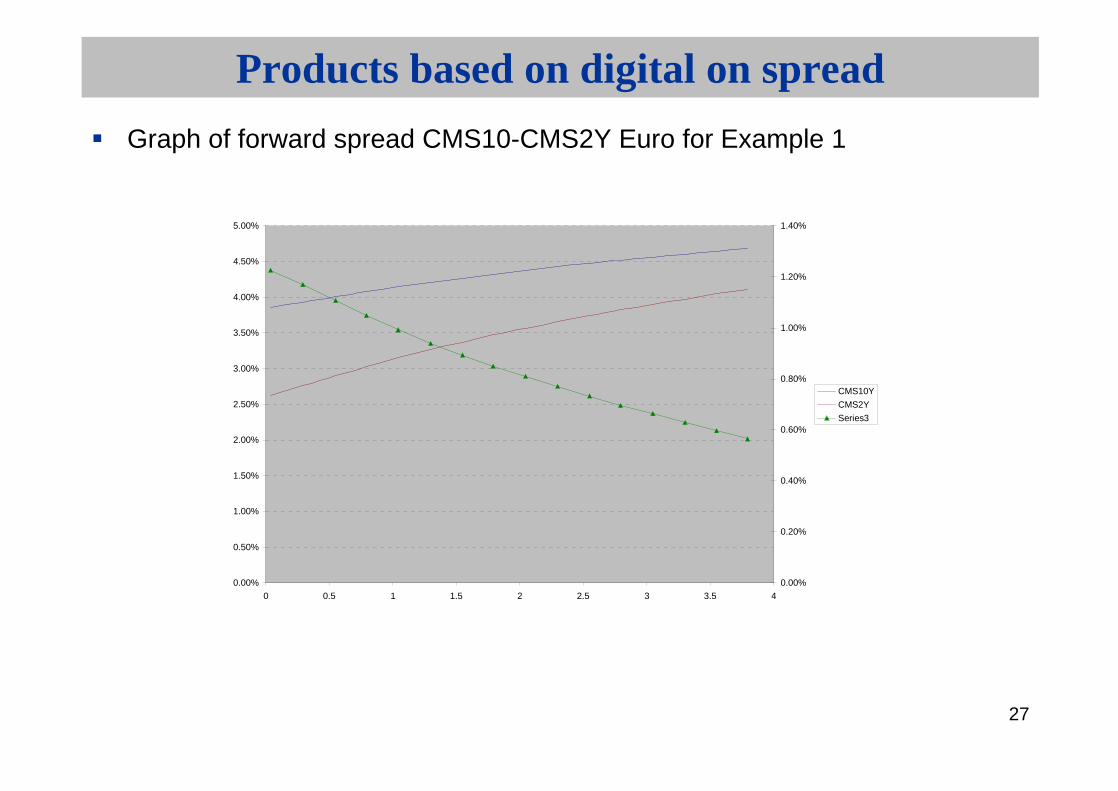

Products based on digital on spread

Example 1 (4Y swap):Client receives 4.65%Pays Euribor3M +n/N*4.65%

n : number of days on the interest period where spread CMS10Y-CMS2Y < BN : number of days on the interest period

4Y swap at pricing date (march 2005) : 3%B = 0.9% year 1, 0.85% year2, 0.8% year3, 0.75% year1

Example 2 (15Y amortizing swap) : Client receives Euribor3MPays 1.9% If CMS10Y-CMS2Y > 0.70%, 4.95% otherwise

In both case :fixing of CMS is in arrearsClient is long digitals on CMS10Y-CMS2Y spread that pays above strike

CMS10Y-2Y spread around 120/110 bp at pricing date

27

Products based on digital on spread

Graph of forward spread CMS10-CMS2Y Euro for Example 1

0.00%

0.50%

1.00%

1.50%

2.00%

2.50%

3.00%

3.50%

4.00%

4.50%

5.00%

0 0.5 1 1.5 2 2.5 3 3.5 4

0.00%

0.20%

0.40%

0.60%

0.80%

1.00%

1.20%

1.40%

CMS10Y

CMS2Y

Series3

28

Products based on digital on spread

Analysis :Both products were for debt liability managementStructured Swap enables the client to switch to fixed/float with enhanced rate if CMS10Y-CMS2Y spread stays above some barriers :

Client view on slope 10Y-2Y curve against the forward slopeRational : low spread = low growth + high inflation, high spread = higher growth + low inflationIssuance of debt + population ageing

Both product can be seen as vanilla swap + digitalAnalysis of the digitals

Sensitivity to the curve slopeFlattening of the curve implies higher probability of paying higher rates for the client, so client looses money on the swap

To analyze sensitivity to volatilities and correlation, let’s move to a basic model

29

Products based on digital on spread

The idea isWe know the basics of greeks on a single underlying digital, assuming this underlying normal or lognormalWhatever the model, it should have similar behaviour with respect to the parameters (volatilities or standard deviation + correlation)

Basic model to analyze a digital on CMS10Y-CMS2Y with maturity T :

Step 1 : Calculate CMS10Y(0,T) and CMS2Y(0,T) at date TStep 2 : calculate implied volatilities or better, implied standard deviation for ATM swaptions on 10Y and 2Y of maturity T

30

Products based on digital on spread

Step 3 : let’s assume the spread is normal with :mean = CMS10Y(0,T)-CMS2Y(0,T)

Standard deviation :

Standard deviation of CMS10Y and CMS2Y

Then the price of a digital with barrier B is given by :

N distribution function of standard gaussian variable mean 0, variance 1.

2122

21 2

21 ,

T

BmNT,B

spread

spread0

spreadm

spread

31

Products based on digital on spread

Basics behaviour of a digital with respect to the volatility (lognormal model) or the standard deviation (normal model) :

vega one year digital

-4

-3

-2

-1

0

1

2

3

60 70 80 90 100 110 120 130 140

spot

veg

a

32

Products based on digital on spread

To see the sensitivity to the standard deviation of each CMS, let’scalculate the derivative of the spread variance with respect to eachstandard deviation :

So even these derivatives are not obvious ; nevertheless, if the two standard deviation are close (usually it’s true) correlation not too high

Then, the standard deviation of the spread is increasing function of eachCMS standard deviationAnyway if both standard deviations increase, the standard deviation of the spread increaseStandard deviation of the spread is decreasing function of the correlation

2

12

2

2

1

21

1

2

1212 spreadspread ,

33

Products based on digital on spread

Digital vega of digital is positive out of the money, negative in the moneySo sensitivity of digital with respect to correlation and eachstandard deviation depends on moneyness

If you are long a digital that pays above the barrier, you are short volatility if forward spread above the strike, so long correlationIf you are long a digital that pays above the barrier, you are long volatilityif forward spread below the strike, so short correlation

Conclusion : The global sensitivities will depend mainly on each digital moneynessand marginally on the discount factors

to understand the various sensitivities always try first to go back to basics, i.e black& Scholes type models…

34

Products based on digital on spread

2005 story :Both Investors and liability management clients long digital that pays above the strikeFor investors, strikes generally below initial forwards spreads (long correlation)For Liability management, strikes generally above initial forwards spreads (short correlation)More risky position for liability management than for investors

LM clients buy digital out the money,Investors buy digital in the money

More products sold to investors, so banks were initially short correlation on digitals

35

Steepener

Typical steepener :Client receives 4*Max(CMS10Y-CMS2Y;0)Client long spread optionClient gains if slope increaseProducts stable with respect to a translation of the curveClient long the volatility of the spread, so short correlation

Banks can offset their short position on correlation due to digital by selling steepener

36

Other Complex products

RatchetsDefinition

The strike of the option or the coupon will depend on the preceding fixing. Common indexation is the following:

Coupon (i) = Notional * max (or min) [E6M(i) + T1; Coupon(i-1) + T2]First coupon is E6M observed at the start date + T1

Example :

Maturity 3Y; index E3M.Customer receives E3MCustomer pays E3M - 25 bps on the first coupon and then Max(E3M-25; Coupon(i-1))

37

Ratchets PricingVery path-dependent products.Main issue is to address the exposure to volatility at a strike that is not yet known. Vega exposure is more on local volatilities than on straight B&S volatilities.Need stochastic volatility model for pricing (same for vol bonds)

Ratchets Pricing useDifferent types that can match various strategies.In general, they are used when customer has a view on market beingeither stable or oriented with a strong, long-term trend. In case of strongmarket moves, they can lead to heavy losses.

Other Complex products

38

Ratchets second type (current version)Also different types that can match various strategies.

Example: Client pays E3M -0.30%+M, with margin M zero on the first year and afterwards previous margin + Max (0, 2%-E3M) It is a risky product.Similar to be short of floorlets strike 2% with cumulative effect in term of risk

There is no need of stochastic vol model, because the product is a series of puts, but one needs proper modeling for long delay adjustment. Ratchet cap or floor are both level and slope curves products

Other Complex products

39

Closed formulae : some limits

Many popular products with European features can be priced with closed formulae, in B&S framework

All variant of Libor Legs, including caps & floorsStandard Spread options

Nevertheless :Quants/Trading have to be careful with choice of parameters, includingparameters you can observe on the markets as volatilitiesExamples : Non standard Libor Legs/CMS spread options

40

Closed formulae : some limits

Non Standard Libor Legs :You pay 6M Libor every 3MFor pricing Cap/Floor on this Leg, needs implied volFor pricing the leg and so the underlying in the cap/floors (convexity adjustment for Non Standard Libor Leg) you need another volHow to deal : proposal

Vol at strike for modeling Lognormal Behavior of LiborVol ATM for modeling convexity adjustment in Leg/Cap/FloorIn this way Call/Put Parity is automatically verified.

41

Closed formulae : some limits

CMS spread optionPay-off :Easy to calculate and compute closed formulae if both CMS assumed lognormal or normalWhich volatilities/standard deviations do take ?Main idea :

Volatilities must depend upon so that specific degenerated cases are consistently treated.We know the price of the spread option if maturity, one of the volatilities or one of the weights is zero.

maturitiesdifferent of being,)()( 2,12211 iCMSKTCMSmTCMSm

Kmm ,, 21

42

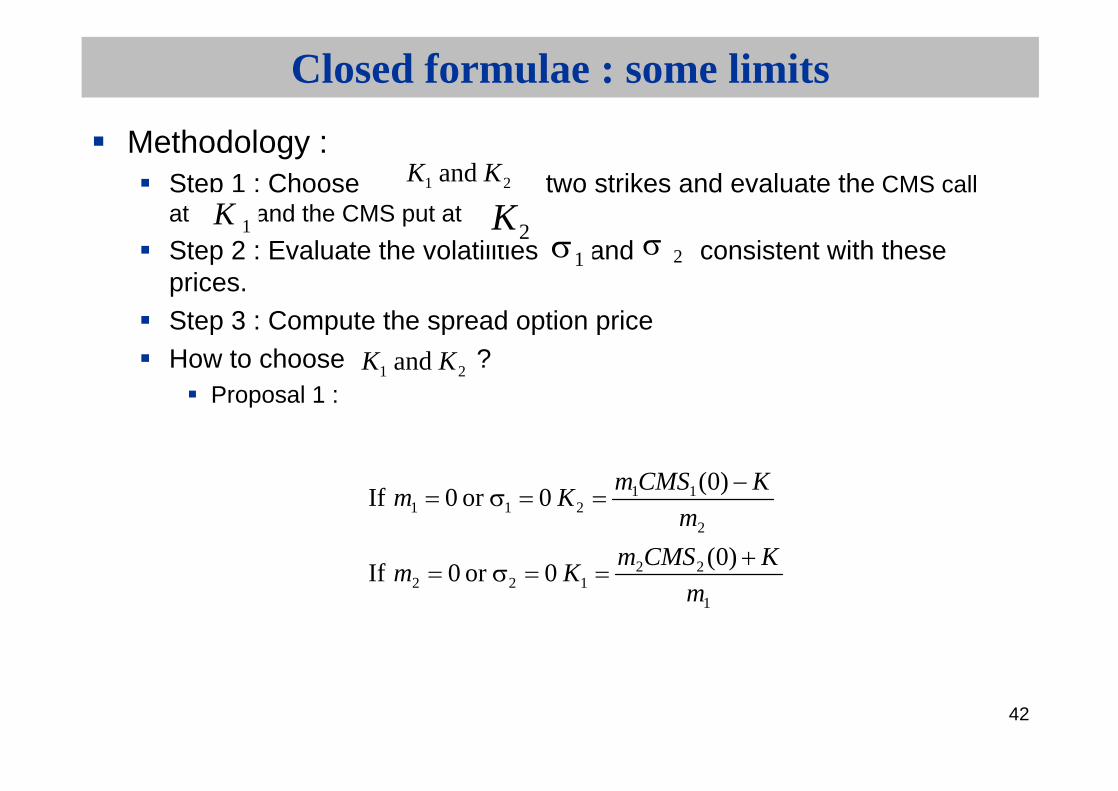

Closed formulae : some limits

Methodology : Step 1 : Choose two strikes and evaluate the CMS call at and the CMS put at

Step 2 : Evaluate the volatilities and consistent with these prices.Step 3 : Compute the spread option priceHow to choose ?

Proposal 1 :

21 and KK

1K2K

1 2

21 and KK

1

22122

2

11211

)0( 0or 0 If

)0( 0or 0 If

m

KCMSmKm

m

KCMSmKm

43

Closed formulae : some limitsProposal 2 :

with s standard deviations now

Best choice according to 2 dimensionnal gaussian law metricThis way stable pricing between normal or lognormal choice

2

112

1

221

)0(

)0(

m

KCMSmK

m

KCMSmK

)(),min(2)()(

),min(

)(),min(2)()(

),min(

2211211212

2221

211

221222222

2211211212

2221

211

22111111

KCMSmCMSmmmTTTmTm

mTTTmCMSK

KCMSmCMSmmmTTTmTm

mTTTmCMSK

44

Complex products

Bermuda Swaptions

Market conditions

The more competition you have between the included swaptions, the more expensive the bermuda.

- flat curve- in a steep curve:

The value of the bermuda is close to the value of the first swaption.This value can be increased thanks to a step up rate.

45

Other Complex products

FlexicapsThe buyer decides to be hedged on a limited number of fixings (1/2 usually).Either he decided himself when he wants the protection: liberty cap.Either it is automatic when the fixing is in the money: autocap.

46

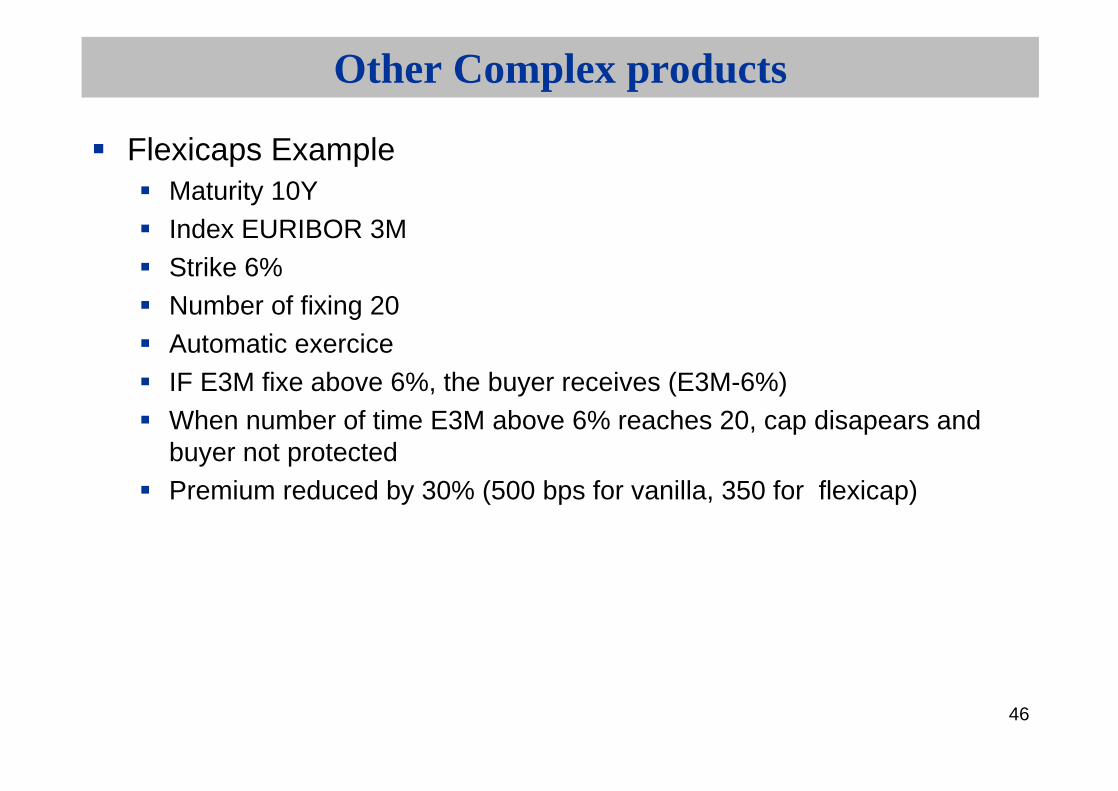

Other Complex products

Flexicaps ExampleMaturity 10YIndex EURIBOR 3MStrike 6%Number of fixing 20Automatic exerciceIF E3M fixe above 6%, the buyer receives (E3M-6%)When number of time E3M above 6% reaches 20, cap disapears and buyer not protectedPremium reduced by 30% (500 bps for vanilla, 350 for flexicap)

47

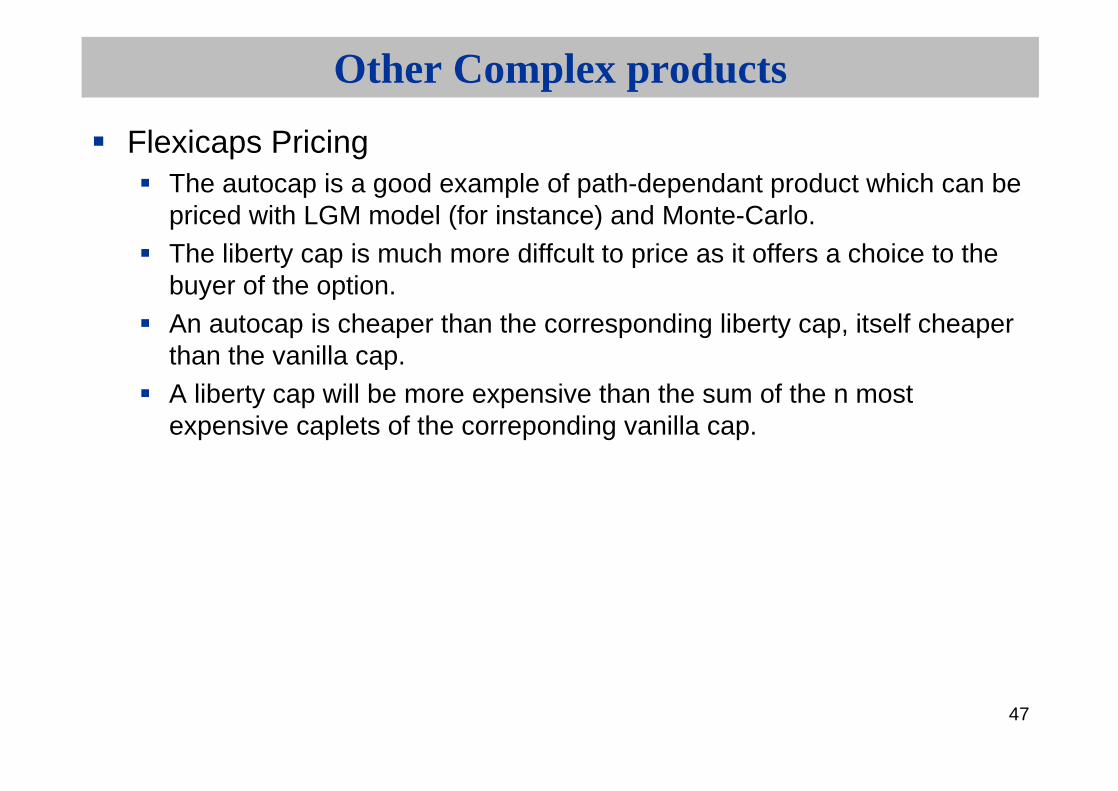

Other Complex products

Flexicaps PricingThe autocap is a good example of path-dependant product which can be priced with LGM model (for instance) and Monte-Carlo.The liberty cap is much more diffcult to price as it offers a choice to the buyer of the option.An autocap is cheaper than the corresponding liberty cap, itself cheaper than the vanilla cap.A liberty cap will be more expensive than the sum of the n most expensive caplets of the correponding vanilla cap.

48

Other Complex products

Flexicaps Use

Premium reductionA good product for a borrower who thinks a monetary crisis can occur but who believes these unlikely will not last for too long ( thanks to central banks).

49

Other Complex products

Flexicaps & Market conditions

Some conditions make them more attractive than vanilla caps:- a flat curve - high volatility- high correlation between forwards (if caps volatility are close to swaptions volatilities for example)

These parameters make them more likely to be in the money at the same time.

50

Other Complex products

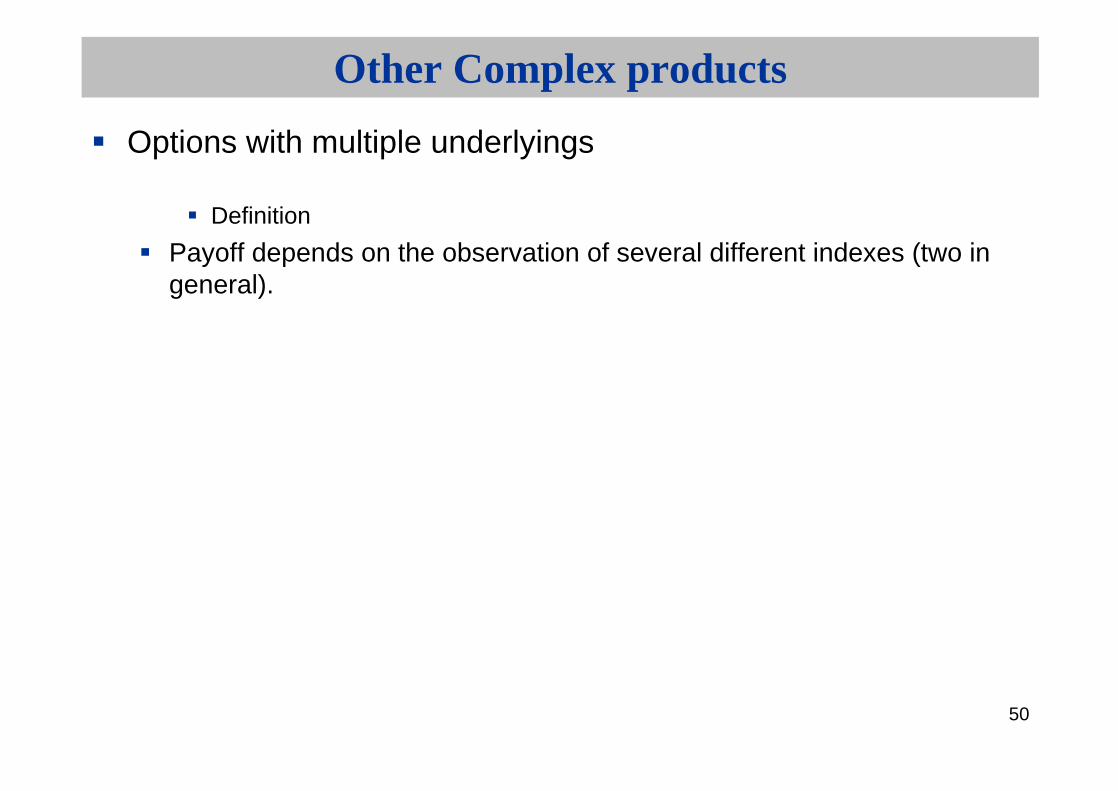

Options with multiple underlyings

Definition

Payoff depends on the observation of several different indexes (two in general).

51

Other Complex products

Options with multiple underlyings ExamplesThey can appear as the conditions of a range :

Range on a spread (customer bets on difference between Libor GBP and E3M being stable)Range with 2 conditions (bet on E3M staying within a range and 10Y swap, within another)

Or as options themselves :Call/Put on the spread on two short-term rates in two currenciesCall/Put on the spread between Long & Short Term rates in one currency (option on the slope of the curve)

Or as European Digitals : A Cap 5% on E3M Knock-Out on CMS10 being above 7% (fixing by fixing)

52

Other Complex products

Options with multiple underlying PricingThese products are priced with closed-formed formulas derived from B&S framework. Though, their pricing involves an crucial additional parameter : the correlation between the two indices.This correlation parameter can be determined as an implicit output of LGM model (for 2 indices of a same currency), or from historical data (for 2 currencies). Very few market prices can sometimes provide the implicit correlation priced by the market.

53

Other Complex products

Options with multiple underlying Use

Options with 2 indices in different currencies are mostly speculation tools as they can leverage a convergence strategy (ex : Forward Range on Stibor - Euribor)Options with 2 indices in the same currency can be used as speculation products too, but also as a balance sheet hedge tool. They are often used in EMTN on spreads, where coupon needs to befloored.

54

Other Complex products

Global Cap DefinitionA Global Cap is a protection on the total amount of interest paid on a debt.This can be seen as an option on the average of E3M

Example

Maturity 5Y; index E3M; strike 5.50%Premium = 160 bp, compared to 215 for vanilla cap (25% premium reduction)In 5 years, if the average of E3M has been below 5.50%, owner of the cap doesn’t receive any payoff, even if some fixings have been above 5.50%If the average of the fixings has been 6%, owner of the option will receive at maturity 0.50% * 5 *365 /360.

55

Other Complex products

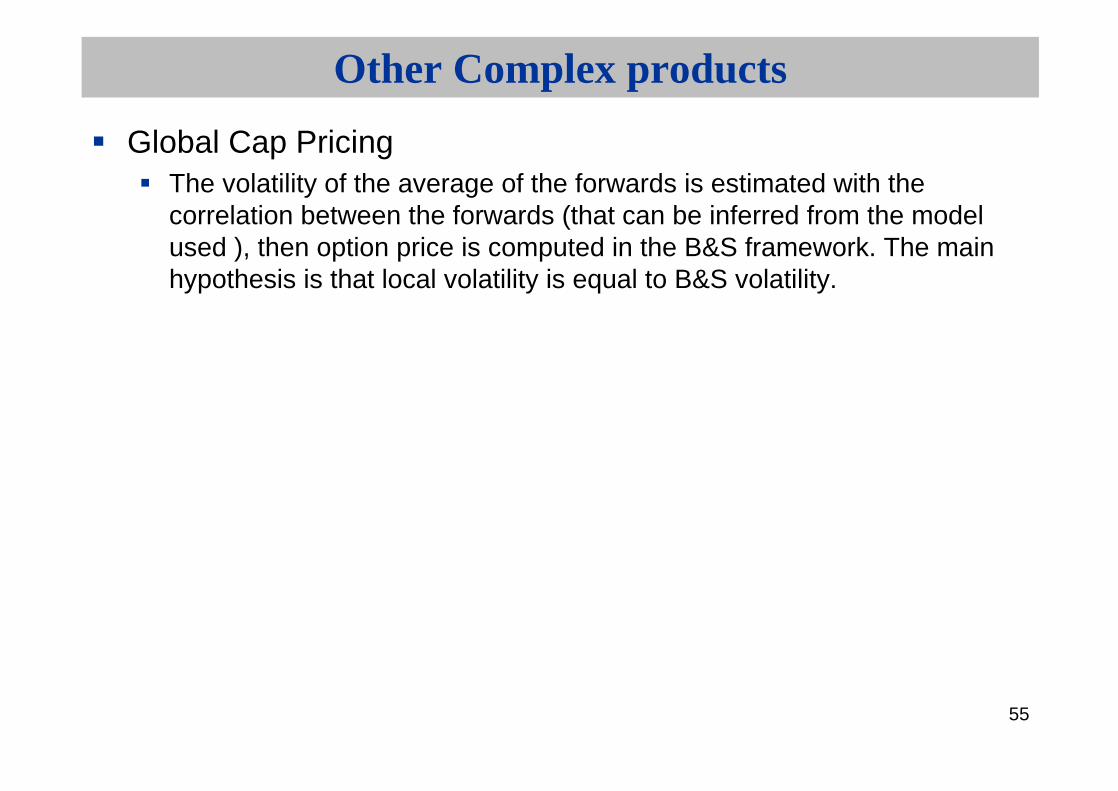

Global Cap PricingThe volatility of the average of the forwards is estimated with the correlation between the forwards (that can be inferred from the model used ), then option price is computed in the B&S framework. The main hypothesis is that local volatility is equal to B&S volatility.

56

Other Complex products

Global Cap UseCan yield to a significant premium reduction.Provides a hedge on the global hedge of a debt even if treasury flows are not perfectly matched (payoff happens at maturity) .

Market conditions :Compared to a vanilla cap, a global cap is cheap when :

- Curve is steep

- Volatility is high- Correlation between the forwards is small

57

Other Complex products

Maturity CapAllows an financial institution to propose a floating rate loan while guaranteeing its customer that he won’t pay back his loan over more than a given period of time. In case capital has not been completely paid back after a given date, the seller of the option pays the remaining part of the debt.

58

Other Complex products

Example : Constant annuities are computed on a 15Y basis with a rate at 5.80%. If floating rates increase, each annuity will pay back less capital than forecasted (actually it can even not be enough to pay interest). The loan can then continue over an unlimited period of time. The ability to cap the maturity can be a marketing advantage.

59

Other Complex products

Maturity CapExample: Loan of 1MEUR on a 15Y basis at 5.80% semi-annually. Constant 6-month annuity is 50 365 EUR.The guarantee loan won’t go over 18 years is worth 150 bps flat, on 20 years it is worth 110 bps.

60

Digital rate options and applications to exotic swapsComplex Products : digital, steepner, ratchet…Bermuda swaptionsCallablesAppendixes :Standard Deviations vs VolatilitiesSABRCorrelation issuesLGMRisk-Management of exotics

61

Bermudas under LGM

Bermudan swaption: option to enter in a swap at severalexercise dates.

Bermuda Swaptions Utilization :

Bermuda swaptions are useful to hedge a callable paper or loan. They can also be packaged with a swap to get a callable swap. It gives a better rate than the boosted rate with a vanilla option.

62

Bermuda swaptions

Bermuda Swaptions

Pricing

PDE (Partial differential equation) or tree. At each nod of the tree, there will correspond an exercise date, the value of the option will be the max between the swap value and the value of the option itself.

Minimum value: a bermuda swaption is more expensive than the most expensive swaption included.Max value: the corresponding cap/floor. In our example, the bermuda is cheaper than the 9Y floor into 1Y 4.80%.

63

Bermudas under LGM

Calibration: One wants to be consistent with the market price of all underlyingswaptions, and especially with the most expensive ones.

Calibrate the diagonal of swaptions with strike the strike of the bermudan option.

64

Bermudas under LGM

Example : Bermuda swaption 10Y in 5Y, strike 5%In 5Y pay-off of a 5Y, 5% strike, European swaption on 10Y swapIn 6Y pay-off of a 6Y, 5% strike, European swaption on 9Y swap…In 14Y pay-off of 14Y, 5% strike, European swaption on 1Y swap

Calibration of LGM1F : for a given mean reversion, calibration of volatilities parameters to the previous europeanswaptions :

00T YT 51 YT 62 YT 1415

65

Bermudas under LGM

constant between and constant between and

And so on…

Calibration of LGM2F is similar as again all parametersexcept volatilities are choosen and not part of the calibration.

1 0T 1T

2

1T2T

66

Bermudas under LGM

Exotic risk: To identify the part of « exotic » risk in the product (i.e. the riskorthogonal to the diagonal of swaptions), we use the followingdecomposition:

Bermuda = Most Expensive swaption + switch option

The most expensive swaption is, viewed from today, the one that is the most likely to be exercised.The switch option accounts for the future possibility to delay (or bring

forward) exercise, if it turns to be more interesting to do so.

67

Bermudas under LGM

Effect of mean reversion on bermuda prices

The switch option value is determined by the way the remainingswaptions are evaluated within the model, from each exercise date.

In other words, the parameters of interest are the model forwardvolatilities of remaining swap rates, computed from each exercise date. The larger the mean reversion, the larger these forward volatilities and thus the larger the price of the switch option.

68

Bermudas under LGM

The larger the mean reversion, the larger the price of the bermudanswaption.

69

Bermudas under LGM

Example : CASA USD deal as of 25/03/2003Deal characteristics : 30Y, no call 9Y. The bank pays fixed rate 6.65% quaterly 30/360 and receives LIBOR USD + 125 BP.

Notional = 650 Mios USD.Bermudan option price (3% mean reversion) :

5.51 % / 35.8 Mios USDCallable Swap (3% mean reversion) :

3.16 % / 20.5 Mios USD

mean reversion option structure

0.01 5.17% 2.82%

0.03 5.51% 3.16%

0.05 5.85% 3.50%

70

Bermudas under LGM

Most expensive (expiry = 9Y / term 21Y) = 4.34 % / 28.2 Mios USDSwitch option = bermudan option – most expensive = 1.17 % / 7.63 MiosUSDVega (1% parallel shift = 0.59 % / 3.87 Mios USD

71

Bermudas under LGM

Question: how to determine the mean reversion?

Market (e.g. on USD, for bermudas of short maturities).Statistical: use statistical methods to estimate the mean reversion fromthe short rate process itself (forget !) Historical vol of FRAs: compare historically the volatility of differentFRAs (e.g. 1Y vs. 20Y).

72

Bermudas under LGM

Long swaption vs. short swaption: each day, calibration to a long swaption. Choose the mean reversion so that, in average, short swaptions are well priced by the model.LGM forward vol vs. market vol: each day, calibrate to a diagonal of swaptions and, from the expiry of the most expensive, compare LGM forward vols of remaining swaptions, to the market (normal) volatilities of swaptions with same underlying / time to maturityBack testing: consider a Bermuda. Each day, and for several values of mean reversion, vega hedge the bermuda, delta hedge the overallposition and study the average / std deviation of daily P&L.

73

Bermudas under LGM

Historical study: long swaptions vs. short swaptions (or cap)Consider a set of historical datas (yield curves, vol curves)For each date, calibrate LGM to the diagonal of swaptions and determine the mean reversion such that the cap with same strike is well priced by the model

USD : mean reversion breakeven to match 10Y 5.00% Cap

2.00%

3.00%

4.00%

5.00%

6.00%

7.00%

May-03 Jul-03 Aug-03 Oct-03 Nov-03

EUR : mean reversion breakeven to match 10Y 4.50% Cap

2.00%

4.00%

6.00%

8.00%

10.00%

12.00%

Mar-03 May-03 Jun-03 Aug-03 Oct-03 Nov-03

74

Historical study: LGM forward vol vs. market volConsider a set of historical datas (yield curves, vol curves).At each date:

Calibrate the model to the diagonal of swaptions.

From the expiry date of the most expensive swaption, compute the normal LGM forward vols of all remaining swaptions.

Bermudas under LGM

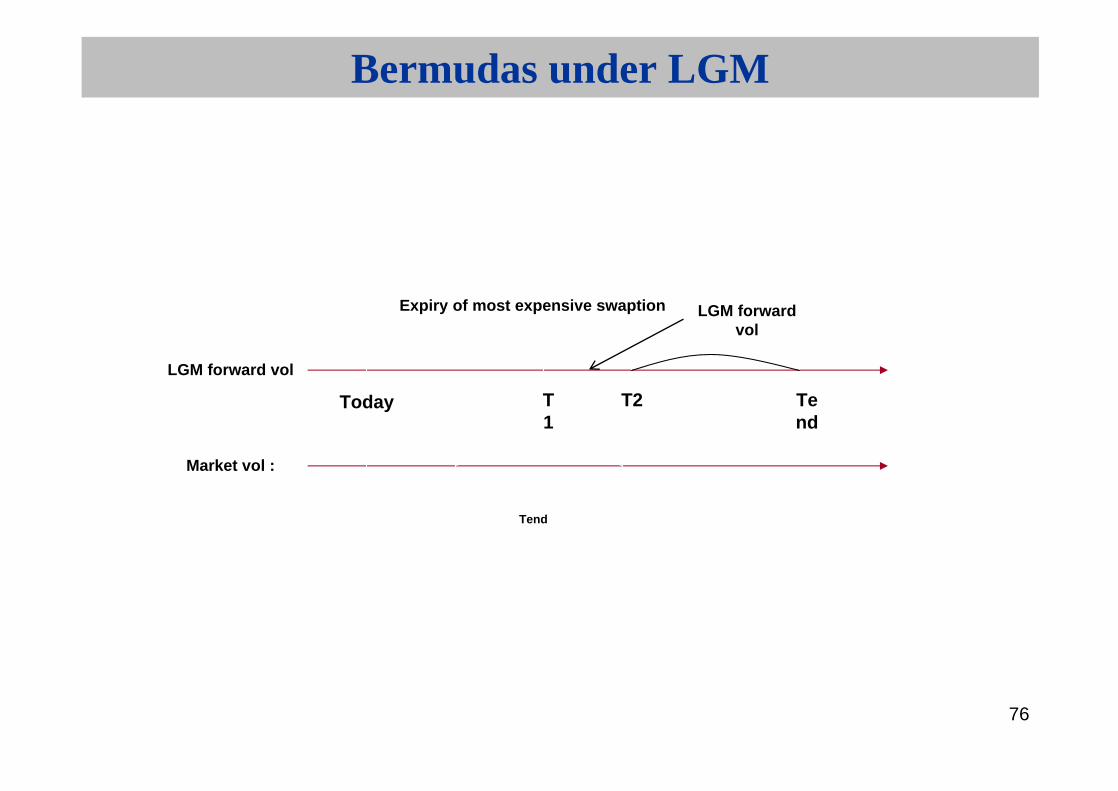

75

Bermudas under LGM

Compare them to (normal) market volatilities of swaptions with same underlying & time to maturity.

Breakeven = mean reversion value such that the average of LGM forward vols matches the average of market normal vols.

76

Bermudas under LGM

Today T1

T2 Tend

Expiry of most expensive swaption LGM forwardvol

T2 – T1 Tend – T2

LGM forward vol:

Market vol :

77

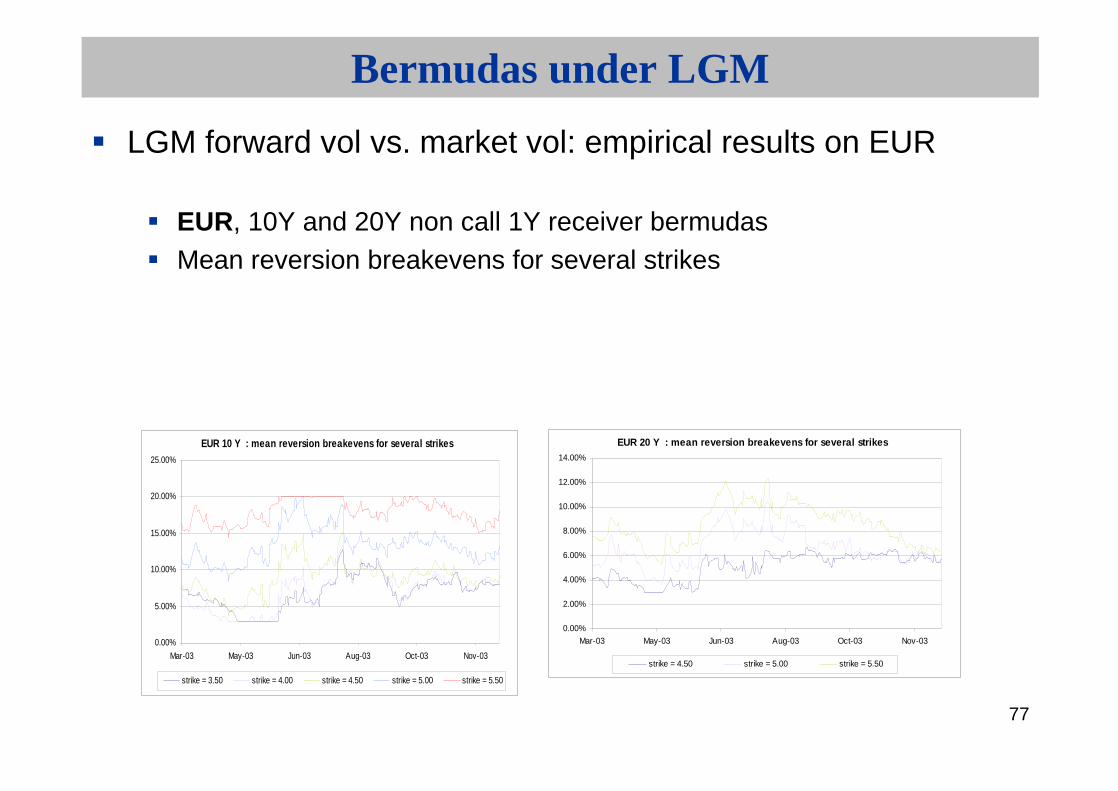

Bermudas under LGM

LGM forward vol vs. market vol: empirical results on EUR

EUR, 10Y and 20Y non call 1Y receiver bermudasMean reversion breakevens for several strikes

EUR 10 Y : mean reversion breakevens for several strikes

0.00%

5.00%

10.00%

15.00%

20.00%

25.00%

Mar-03 May-03 Jun-03 Aug-03 Oct-03 Nov-03

strike = 3.50 strike = 4.00 strike = 4.50 strike = 5.00 strike = 5.50

EUR 20 Y : mean reversion breakevens for several strikes

0.00%

2.00%

4.00%

6.00%

8.00%

10.00%

12.00%

14.00%

Mar-03 May-03 Jun-03 Aug-03 Oct-03 Nov-03

strike = 4.50 strike = 5.00 strike = 5.50

78

Bermudas under LGM

LGM forward vol vs. market vol: empirical results on USD

USD, 10Y and 20Y non call 1Y receiver bermudasMean reversion breakevens for several strikes

USD 10 Y : mean reversion breakevens for several strikes

5.00%

10.00%

15.00%

20.00%

25.00%

May-03 Jul-03 Aug-03 Oct-03 Nov-03

strike = 4.00 strike = 4.50 strike = 5.00 strike = 5.50 strike = 6.00

USD 20 Y : mean reversion breakevens for several strikes

5.00%

10.00%

15.00%

20.00%

25.00%

May-03 Jul-03 Aug-03 Oct-03 Nov-03

strike = 4.50 strike = 5.00 strike = 5.50 strike = 6.00

79

Bermudas under LGM

LGM forward vol vs. market vol: some conclusionsResults:

Slightly high mean reversion breakevens (up to 15 – 20%), especially on USDStrike dependent (especially for 10Y bermudas)Depends on maturity

80

Bermudas under LGM

What to conclude?Avoid being massively short of forward vol. If it is the case, be

conservative (i.e. use a mean reversion greater than 15%), or better, use a stochastic volatility model.

What if doing the same study with LGM 2 Factors?

81

Bermudas under LGM

Risk management back testingConsider a set of historical datas (yield curves, vol curves)Consider a bermuda. For each date of the data set, compute the vegahedge, delta hedge the overall position and compute the P&L at the end of the day.Repeat the operation for several values of mean reversion and compare the results it terms of average and standard deviation of the daily P&L.Try to identify robustness properties on the mean reversion.

82

Bermudas under LGM

25Y non call 5YAverage of daily P&LEUR historical datas

-20

-10

0

10

20

30

-5% 0% 5% 10% 15% 20% 25%

mean reversion

Ave

rag

e o

f d

aily

P&

L

15Y non call 3Y (2 call dates)Average of daily P&L

Simulated datas

-1.5

-1

-0.5

0

0.5

1

0% 5% 10% 15% 20% 25%

mean reversion

Ave

rag

e o

f d

aily

P&

L

83

Bermudas under LGM

LGM 1 Factor vs. LGM 2 FactorsQuestion: is a one factor model appropriate to price and risk manage bermudas? In other words: to what extent decorrelation between rates affects the price of a bermuda ?To understand the effects involved, let us consider a receiver bermuda with only 2 exercise dates:

TodayT2

Tend

Exercise in T1 Delay exercise toT2

84

Bermudas under LGM

The payoff of the bermuda at date T1 looks like:

85

Bermudas under LGM

LGM 1 Factor vs. LGM 2 Factors (continued)Given that the vols of the swap rates S1(T1) an S2(T2) are fixed by the calibration, the price of our 2-exercise-dates bermuda depends mainlyon 2 things:

The forward vol of S2(T2) between dates T1 and T2 (the larger this forwardvolatility, the larger the price of the bermuda).The correlation between swap rate S1(T1) and forward swap rate S2(T1) (the larger this correlation, the smaller the price of the bermuda).

86

Bermudas under LGM

Suppose that we choose model parameters such that the 1 factor and 2 factors model provide the same forward volatilities.

Under LGM 1 Factor, the correlation is equal to 1 whereas it is stricly smallerthan 1 for LGM 2 Factors. Therefore, the LGM 1 Factor price of the bermuda will be smaller thanthe 2 Factors price.In other words, to match LGM-1F & LGM-2F bermuda prices, one has to compensate by increasing the one factor forward vol (i.e. by increasing the 1F mean reversion).

87

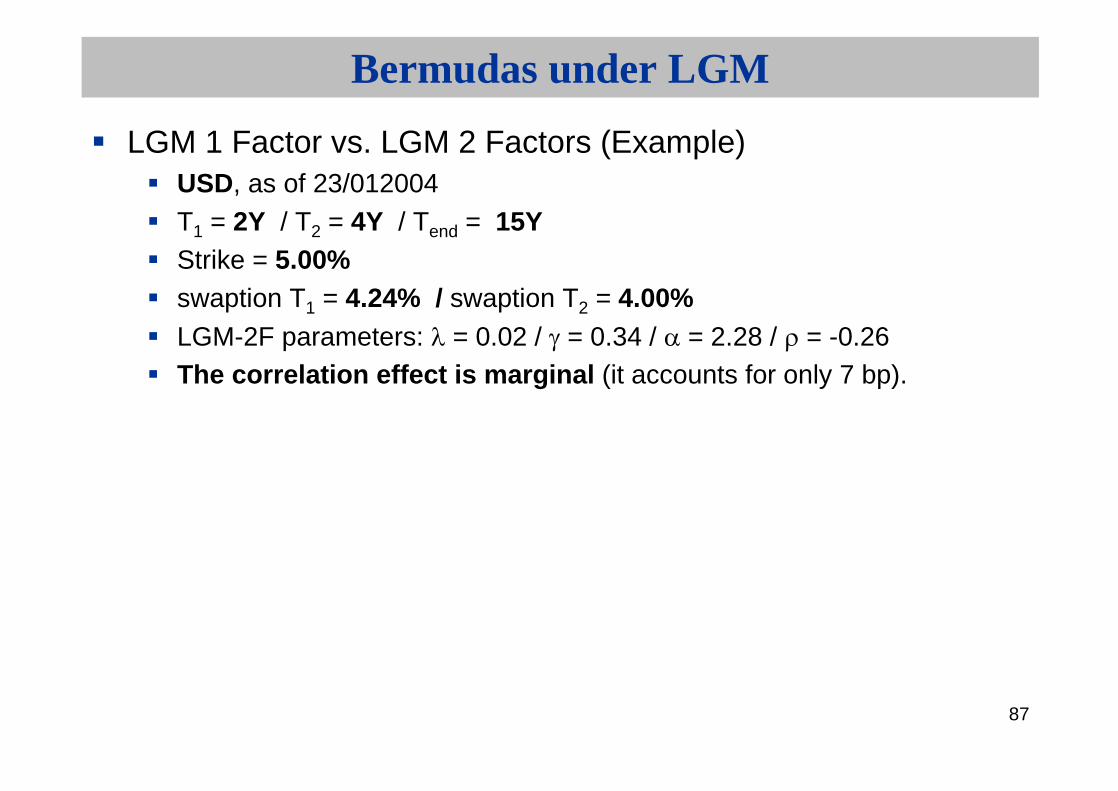

Bermudas under LGM

LGM 1 Factor vs. LGM 2 Factors (Example)USD, as of 23/012004T1 = 2Y / T2 = 4Y / Tend = 15YStrike = 5.00%swaption T1 = 4.24% / swaption T2 = 4.00%LGM-2F parameters: = 0.02 / = 0.34 / = 2.28 / = -0.26The correlation effect is marginal (it accounts for only 7 bp).

88

Bermudas under LGM

LGM-2F bermuda price = 5.17% , therefore switch option = 0.93% LGM-2F correlation S1(T1) / S2(T1) = 0.977LGM-1F mean reversion that matches 2F forward vol = 4.00%LGM-1 bermuda price for this mean reversion = 5.10%The conclusion holds for more than 2 exercise dates. On all exampleswe considered, the discrepancies remain below 10 bp.Basically, what matters is what happens around the most expensiveswaptions.

89

Conclusion / Summary

Bermuda = swaption + exotic risk (switch option)Exotic risk depends on forward volatilityUnder LGM, forward volatility depends on mean reversionMean reversion is chosen historically, using several approachesLGM one factor is appropriate for bermudasTypical mean reversion 1.5% to 5%, nearly market implied parameter

90

Amortizing bermudan swaptions

Standard diagonal calibration on vanilla swaptions is not satisfactory.Idea:

Swap with variable notional = basket of vanilla swaps with various end dates.

91

Amortizing bermudan swaptions

Example : a 3Y annual amortizing swap with notionals 2 mios EUR on first year, 1.5 mios EUR on second year, and 1 mios EUR on third year, is the sum of three vanilla swaps (3Y with notional 1 + 2Y with notional 0.5 + 1Y with notional 0.5) .

The idea is the following:For each exercise date, compute the basket of (forward) vanilla swaps equivalent to the (forward) amortizing swap.For each exercise date, consider the corresponding basket of swaptions (with same coefficients as in the basket of swaps), with strike the strike of the bermudan, and calibrate the model to the market price of this basket.

92

Amortizing bermudan swaptions

Pros:OK for pricing. European amortizing swaptions model price isindependant of the choice of mean reversion.

93

Amortizing bermudan swaptions

For hedging, the gamma replication may be inacurrate : as the swaptions of the basket have fixed strikes, there might be a mismatch between the gamma of the basket of swaptions and the gamma of the amortizingswaption, especially when the amortizing swaption turns to be ATM.

94

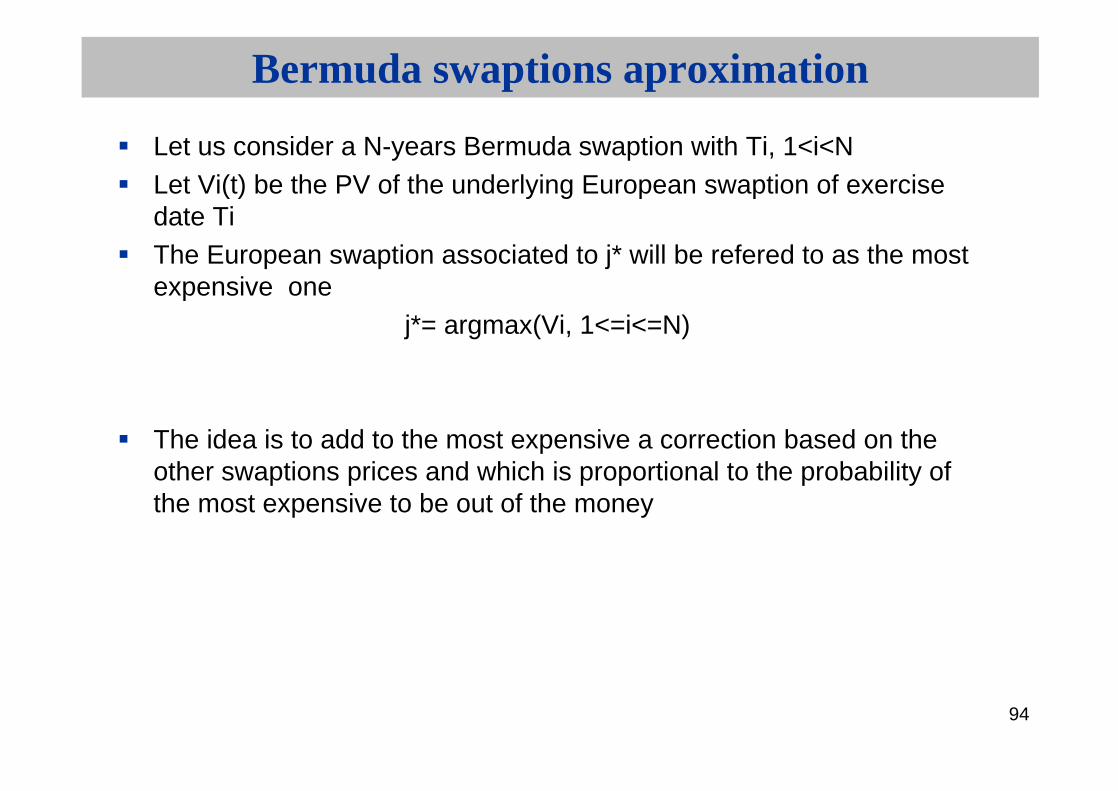

Bermuda swaptions aproximation

Let us consider a N-years Bermuda swaption with Ti, 1<i<NLet Vi(t) be the PV of the underlying European swaption of exercisedate TiThe European swaption associated to j* will be refered to as the mostexpensive one

j*= argmax(Vi, 1<=i<=N)

The idea is to add to the most expensive a correction based on the other swaptions prices and which is proportional to the probability of the most expensive to be out of the money

95

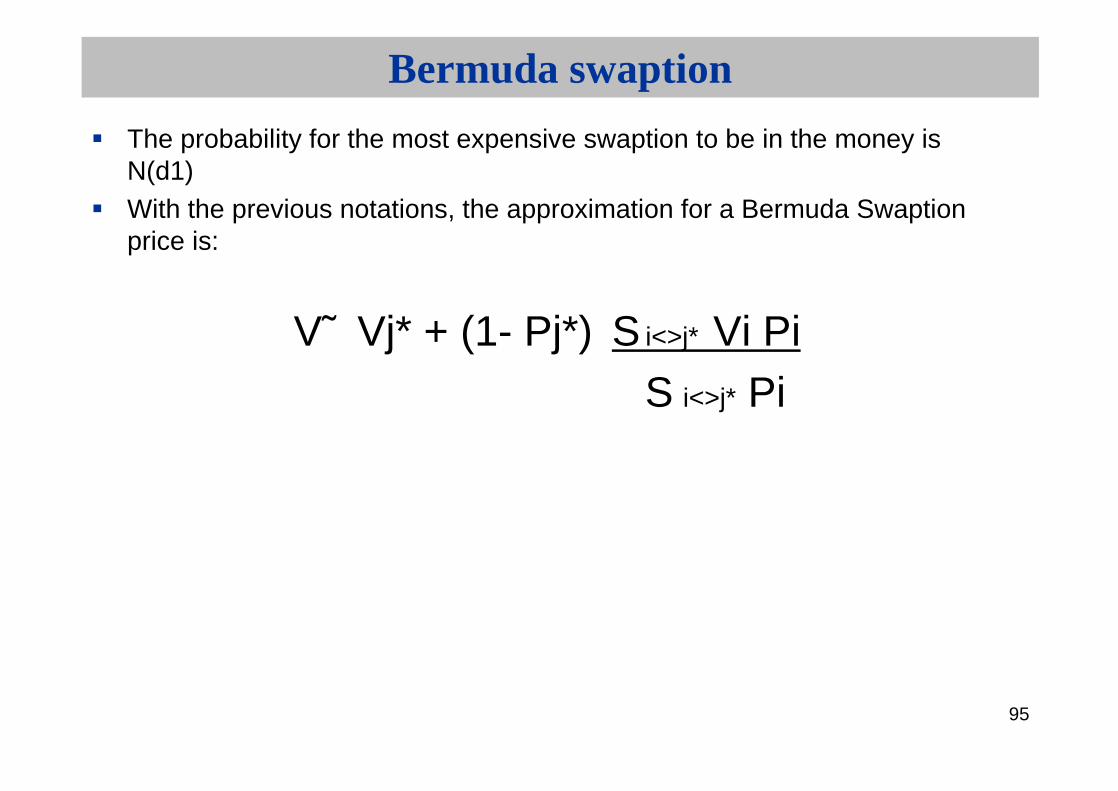

Bermuda swaption

The probability for the most expensive swaption to be in the money isN(d1)With the previous notations, the approximation for a Bermuda Swaptionprice is:

V˜ Vj* + (1- Pj*) S i<>j* Vi PiS i<>j* Pi

96

Digital rate options and applications to exotic swapsComplex Products : digital, steepner, ratchet…Bermuda swaptionsCallablesAppendixes :Standard Deviations vs VolatilitiesSABRCorrelation issuesLGMRisk-Management of exotics

97

Callables products

Bank pays 0.2% + (CMS20Y-CMS2Y)YENReceives Libor YEN6MCallable every 6 months after one yearAt every call date, after exchange of current cash flow

Bank PV = PV future cash flow + call option>=0Cancel option = Max(cancel at the current date, all future call)This is the decision rule between immediate cancel and keep the product Callable structures enable to create the possibility of pick-up for the client whicj is short the call option

98

Exotic products: definition

The main exotic feature of IR exotic products is their illiquidity: a lack of inter-bank market for the most exotic.

Most of them use non quoted parameters such as correlation.

These risks need a specific approach (“worst case”).

99

Exotic products: strategy

Importance of marketing: you need to identify a risk or an opportunity for a customer.

Being able to handle large volumes on vanilla products.

Strong interest of using historical data (for marketing and risk purposes) and a strong analysis of illiquid Greeks on illiquid risks.

Simulation of portfolio on different scenarios (VaR).

100

Exotic products : interest

To find the product which match the exact need and expectations of the customer.

In order to decrease the variance of a portfolio by accepting a lack in the expected return (more important bid/offer than the vanilla products).

And to minimize the future hedging cost.

101

Exotic products : non-hedgeable risk

Three kind of risk can be hedge with vanilla products :Parameters such as correlation between CMS, quanto correlationMean reversion if models use like for BermudaCorrelation between forward rates, model depending

No obvious solutionMeasure your risk wih good mappingLimit controlBuy and sell risk to stay within limits

102

Digital rate options and applications to exotic swapsComplex Products : digital, steepner, ratchet…Bermuda swaptionsCallablesAppendixes :Standard Deviations vs VolatilitiesSABRCorrelation issuesLGMRisk-Management of exotics

103

Standard deviation versus volatility

The diffusion process of a rate (short rate, zero-coupon, swap, whatever..) is typically :

dr = (…)dt + s dz (« normal models »), or dr/r = (…)dt + s ’dz (« lognormal models »)

It’s important to see the difference between s and s ’ : s is a standard deviation (often called volatility in working papers!)s ’ is a volatilty !

104

Standard deviation versus volatility

Central banks of developed countries tend to move short rates by 25 or 50 bp a few times in a year, whatever the level of short/long term rates

So standard deviation is typically 0.50% to 1.30%Volatility is very well approximated (ATM) by : s ’ = s /r(0)

r(0) initial value of r at date 0 Standard deviation is more stable across time for one currencySo volatility tends to increase when rates go down, tends to decrease when rates go-up

105

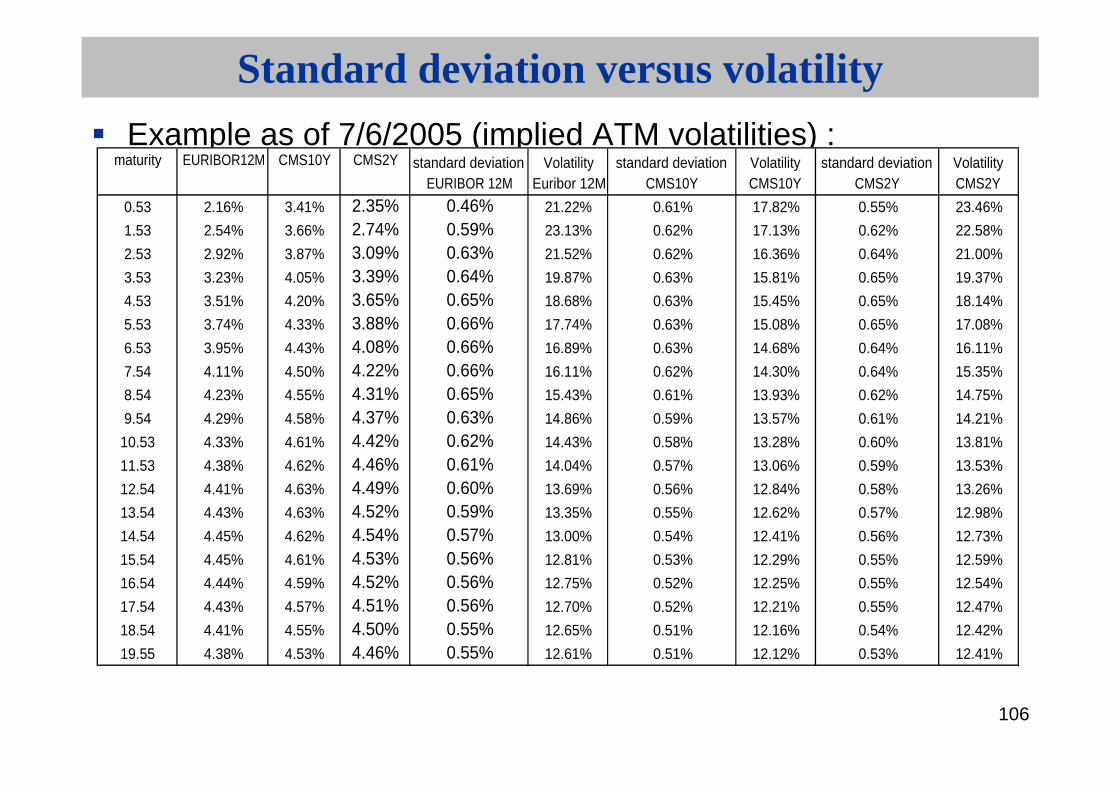

Standard deviation versus volatility

It’s important to keep in mind that what makes the price of interest rates vanilla options (caps/floors/swaptions) is not volatility, it’s standard deviationOf course same thing for exotics!So when comparing two currencies, in terms of cheapness of interest derivatives, look at standard deviations, not volatilitiesSame thing for two type of rates (deposits vs swaps, short maturity swaps vs long term swaps, short maturity options vs long maturity options…)

106

Standard deviation versus volatility

Example as of 7/6/2005 (implied ATM volatilities) :maturity EURIBOR12M CMS10Y CMS2Y

0.53 2.16% 3.41% 2.35% 0.46% 21.22% 0.61% 17.82% 0.55% 23.46%

1.53 2.54% 3.66% 2.74% 0.59% 23.13% 0.62% 17.13% 0.62% 22.58%

2.53 2.92% 3.87% 3.09% 0.63% 21.52% 0.62% 16.36% 0.64% 21.00%

3.53 3.23% 4.05% 3.39% 0.64% 19.87% 0.63% 15.81% 0.65% 19.37%

4.53 3.51% 4.20% 3.65% 0.65% 18.68% 0.63% 15.45% 0.65% 18.14%

5.53 3.74% 4.33% 3.88% 0.66% 17.74% 0.63% 15.08% 0.65% 17.08%

6.53 3.95% 4.43% 4.08% 0.66% 16.89% 0.63% 14.68% 0.64% 16.11%

7.54 4.11% 4.50% 4.22% 0.66% 16.11% 0.62% 14.30% 0.64% 15.35%

8.54 4.23% 4.55% 4.31% 0.65% 15.43% 0.61% 13.93% 0.62% 14.75%

9.54 4.29% 4.58% 4.37% 0.63% 14.86% 0.59% 13.57% 0.61% 14.21%

10.53 4.33% 4.61% 4.42% 0.62% 14.43% 0.58% 13.28% 0.60% 13.81%

11.53 4.38% 4.62% 4.46% 0.61% 14.04% 0.57% 13.06% 0.59% 13.53%

12.54 4.41% 4.63% 4.49% 0.60% 13.69% 0.56% 12.84% 0.58% 13.26%

13.54 4.43% 4.63% 4.52% 0.59% 13.35% 0.55% 12.62% 0.57% 12.98%

14.54 4.45% 4.62% 4.54% 0.57% 13.00% 0.54% 12.41% 0.56% 12.73%

15.54 4.45% 4.61% 4.53% 0.56% 12.81% 0.53% 12.29% 0.55% 12.59%

16.54 4.44% 4.59% 4.52% 0.56% 12.75% 0.52% 12.25% 0.55% 12.54%

17.54 4.43% 4.57% 4.51% 0.56% 12.70% 0.52% 12.21% 0.55% 12.47%

18.54 4.41% 4.55% 4.50% 0.55% 12.65% 0.51% 12.16% 0.54% 12.42%

19.55 4.38% 4.53% 4.46% 0.55% 12.61% 0.51% 12.12% 0.53% 12.41%

standard deviation CMS2Y

Volatility CMS2Y

standard deviation EURIBOR 12M

Volatility Euribor 12M

standard deviation CMS10Y

Volatility CMS10Y

107

Standard deviation versus volatility

0.00%

0.50%

1.00%

1.50%

2.00%

2.50%

3.00%

3.50%

4.00%

4.50%

5.00%

0 5 10 15 20 250.00%

5.00%

10.00%

15.00%

20.00%

25.00%

EURIBOR12M

CMS10Y

CMS2Y

standard deviation EURIBOR 12M

standard deviation CMS10Y

standard deviation CMS2Y

Volatility Euribor 12M

Volatility CMS10Y

Volatility CMS2Y

108

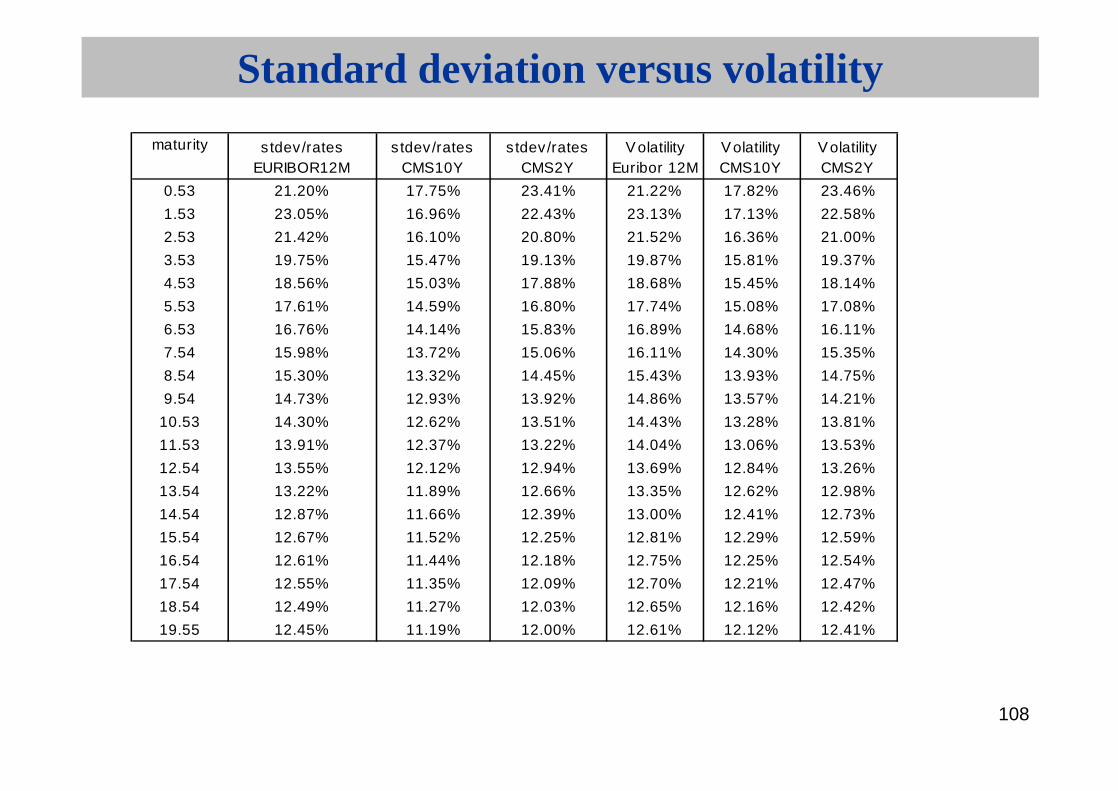

Standard deviation versus volatility

maturity

0.53 21.20% 17.75% 23.41% 21.22% 17.82% 23.46%

1.53 23.05% 16.96% 22.43% 23.13% 17.13% 22.58%

2.53 21.42% 16.10% 20.80% 21.52% 16.36% 21.00%

3.53 19.75% 15.47% 19.13% 19.87% 15.81% 19.37%

4.53 18.56% 15.03% 17.88% 18.68% 15.45% 18.14%

5.53 17.61% 14.59% 16.80% 17.74% 15.08% 17.08%

6.53 16.76% 14.14% 15.83% 16.89% 14.68% 16.11%

7.54 15.98% 13.72% 15.06% 16.11% 14.30% 15.35%

8.54 15.30% 13.32% 14.45% 15.43% 13.93% 14.75%

9.54 14.73% 12.93% 13.92% 14.86% 13.57% 14.21%

10.53 14.30% 12.62% 13.51% 14.43% 13.28% 13.81%

11.53 13.91% 12.37% 13.22% 14.04% 13.06% 13.53%

12.54 13.55% 12.12% 12.94% 13.69% 12.84% 13.26%

13.54 13.22% 11.89% 12.66% 13.35% 12.62% 12.98%

14.54 12.87% 11.66% 12.39% 13.00% 12.41% 12.73%

15.54 12.67% 11.52% 12.25% 12.81% 12.29% 12.59%

16.54 12.61% 11.44% 12.18% 12.75% 12.25% 12.54%

17.54 12.55% 11.35% 12.09% 12.70% 12.21% 12.47%

18.54 12.49% 11.27% 12.03% 12.65% 12.16% 12.42%

19.55 12.45% 11.19% 12.00% 12.61% 12.12% 12.41%

stdev/rates EURIBOR12M

stdev/rates CMS10Y

stdev/rates CMS2Y

V olatility Euribor 12M

Volatility CMS10Y

Volatility CMS2Y

109

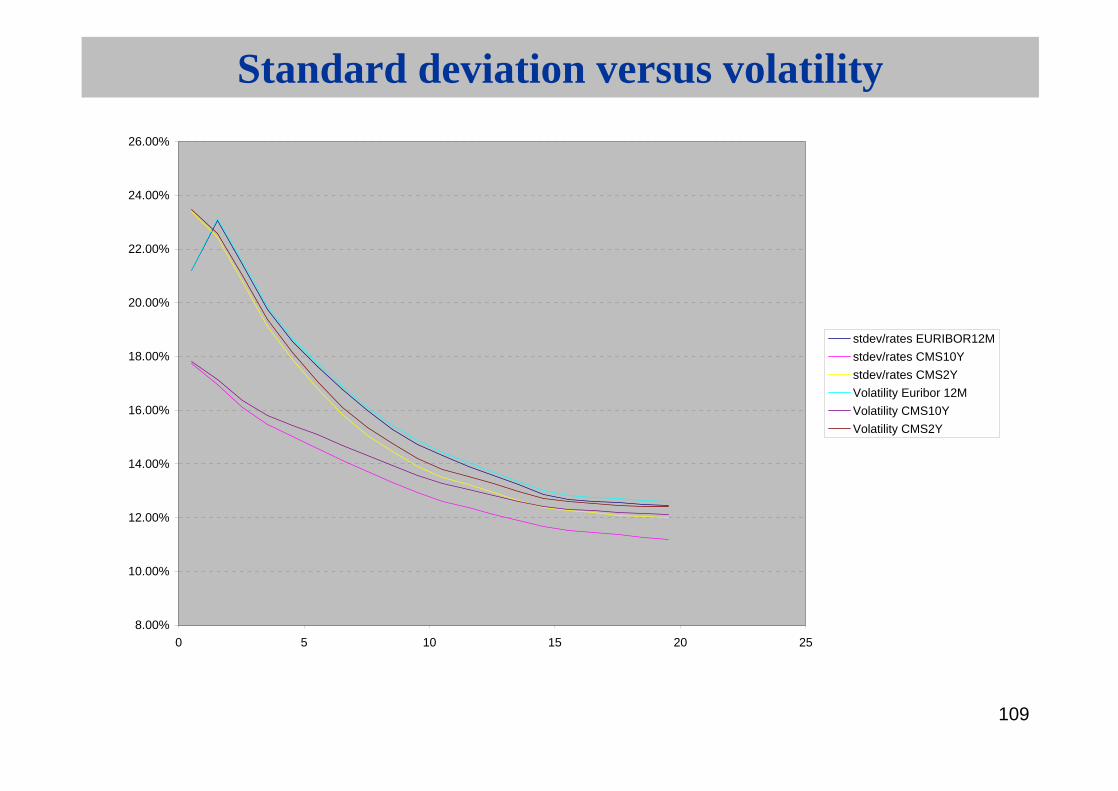

Standard deviation versus volatility

8.00%

10.00%

12.00%

14.00%

16.00%

18.00%

20.00%

22.00%

24.00%

26.00%

0 5 10 15 20 25

stdev/rates EURIBOR12M

stdev/rates CMS10Y

stdev/rates CMS2Y

Volatility Euribor 12M

Volatility CMS10Y

Volatility CMS2Y

110

Standard deviation versus volatility

Remark : the approximation s ’ = s /r(0) is less good for CMS than for EURIBOR12M because implied volatilities were calculated before convexity adjustment.

111

Standard deviation versus volatility

For risk management purpose, it’s important to have the possibility to adjust your smile modelling between :

Full normal models (standard deviation constant when rates move)Full lognormal models (volatilities constant when rates move)Any intermediate version between the two above

SABR model is a good choice

112

Digital rate options and applications to exotic swapsComplex Products : digital, steepner, ratchet…Bermuda swaptionsCallablesAppendixes :Standard Deviations vs VolatilitiesSABRCorrelation issuesLGMRisk-Management of exotics

113

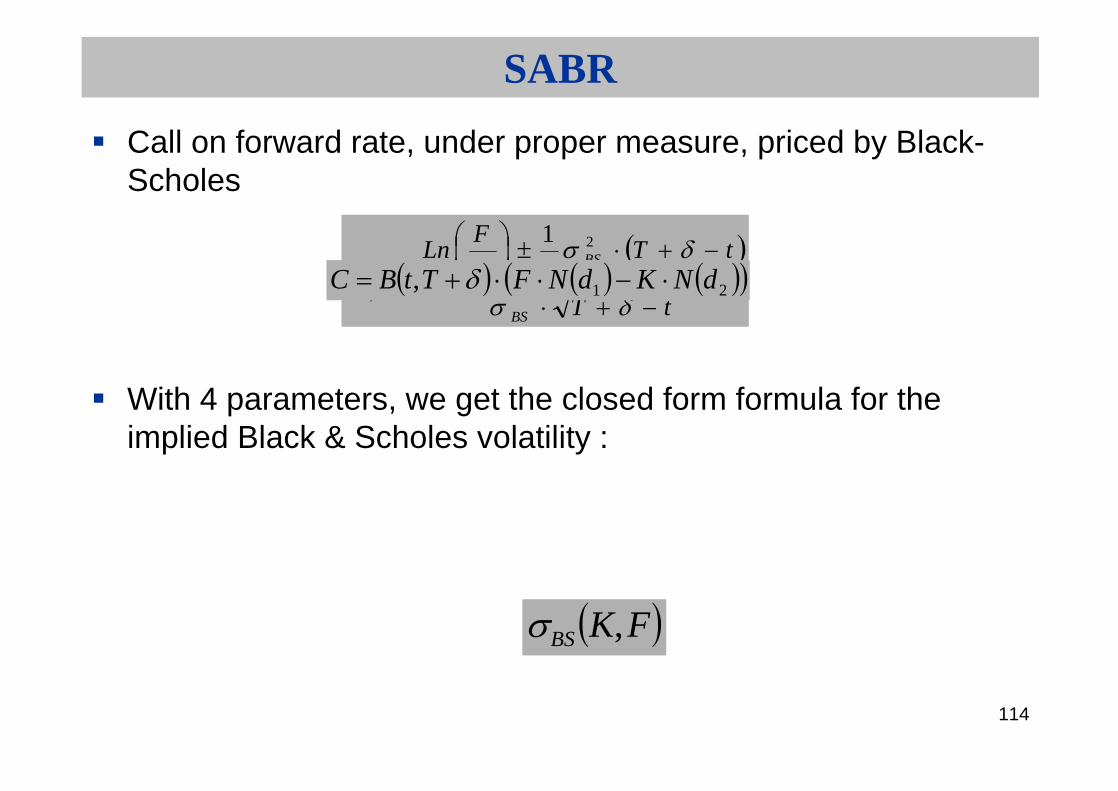

SABR

SABR: Stochastic, Alpha, Beta, RhoDynamic of underlying :

with F forward rate or swap rate

dtdZdW

dZd

dWFdF

,

114

SABR

Call on forward rate, under proper measure, priced by Black-Scholes

With 4 parameters, we get the closed form formula for the implied Black & Scholes volatility :

tT

tTK

FLn

dBS

BS2

2,1

2

1

21, dNKdNFTtBC

FKBS ,

115

SABR

and

TFKFK

xy

x

K

F

K

FFK

FKBS

22

2

11

22

44

22

2

1

24

32

4

1

24

11

log19201

log24

11

,

1

21log

log

2

2

1

xxxxy

K

FFKx

116

SABR

At the money formula:

One can choose between parametrisation or replace by the ATM –normal or lognormal volatility.

TFFF

F,FBS2

2

122

22

1 24

32

4

1

24

11

,,,

117

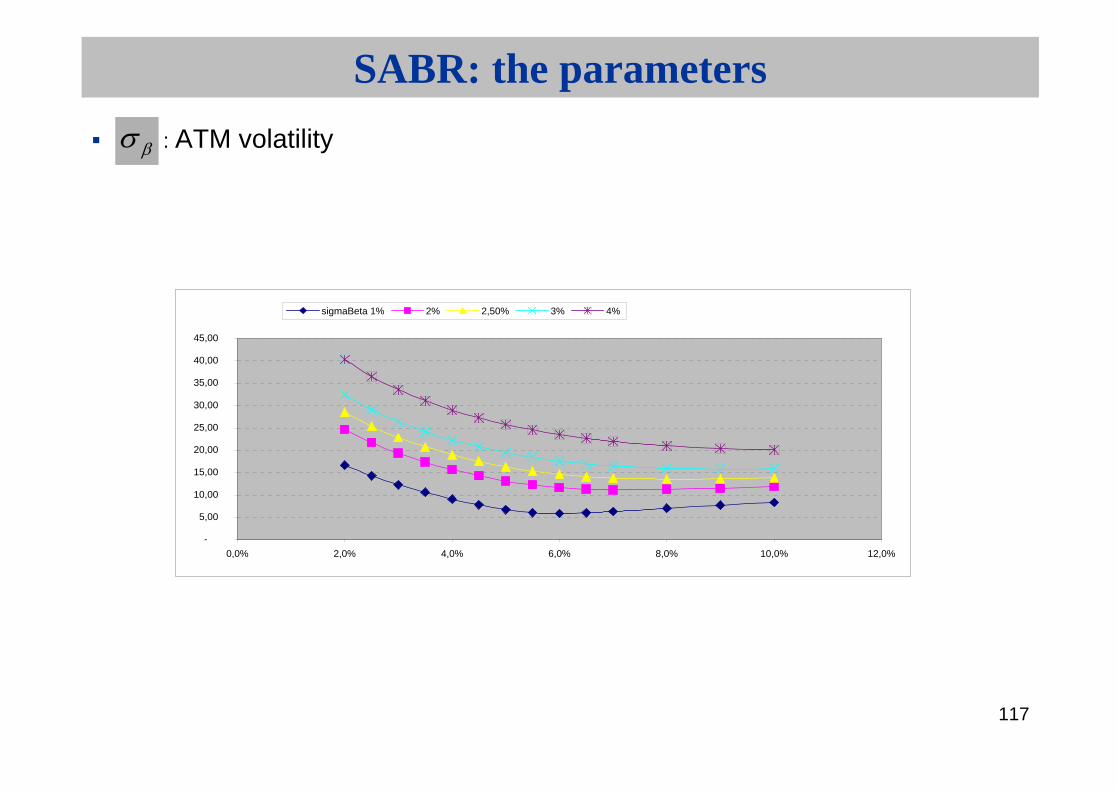

SABR: the parameters

: ATM volatility

-

5,00

10,00

15,00

20,00

25,00

30,00

35,00

40,00

45,00

0,0% 2,0% 4,0% 6,0% 8,0% 10,0% 12,0%

sigmaBeta 1% 2% 2,50% 3% 4%

118

SABR: the parameters

BetaFor Beta=1, lognormal model.For beta = 0, normal model

Enables to know how ATM vol moves when forward moves.

F

dFd

ATM

ATM 1

119

For beta = 1, ATM vol doesn’t move when forward moves

SABR: the parameters

Beta = 1

20,00

20,50

21,00

21,50

22,00

22,50

23,00

23,50

24,00

24,50

25,00

0,0% 2,0% 4,0% 6,0% 8,0% 10,0% 12,0%

Fwd 3%

Fwd 4%

Fwd 5%

120

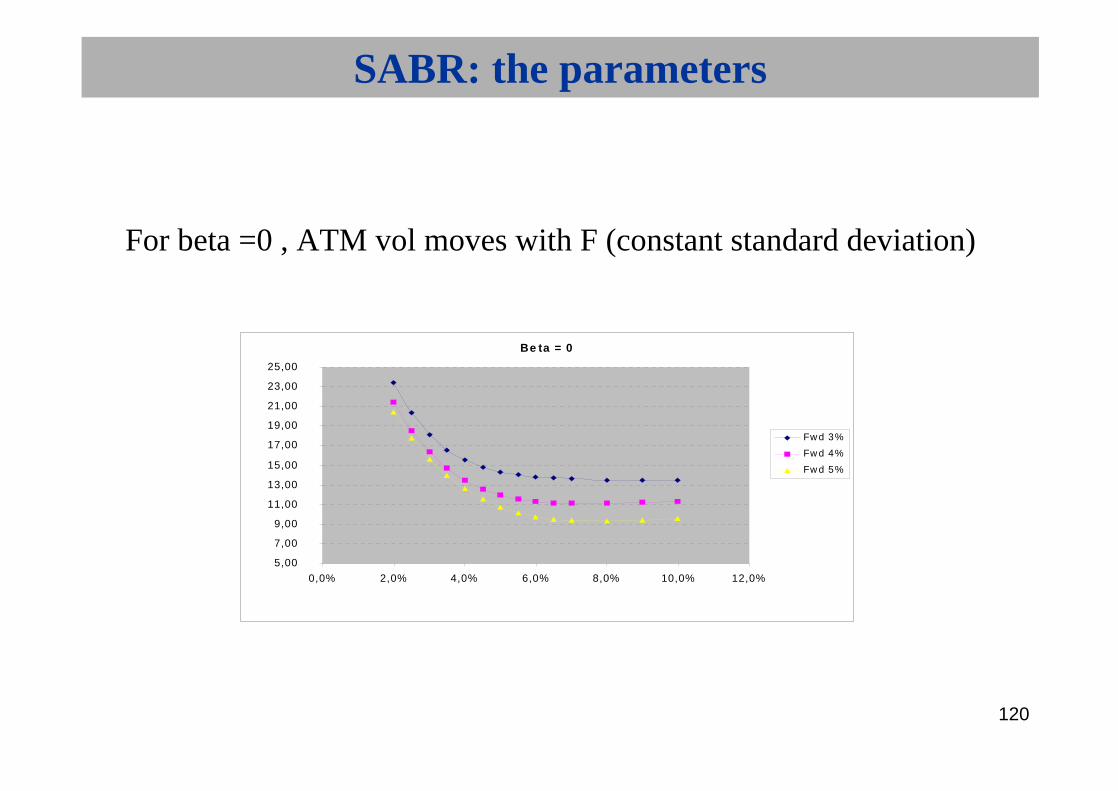

For beta =0 , ATM vol moves with F (constant standard deviation)

SABR: the parameters

Be ta = 0

5,00

7,00

9,00

11,00

13,00

15,00

17,00

19,00

21,00

23,00

25,00

0,0% 2,0% 4,0% 6,0% 8,0% 10,0% 12,0%

Fw d 3%

Fw d 4%

Fw d 5%

121

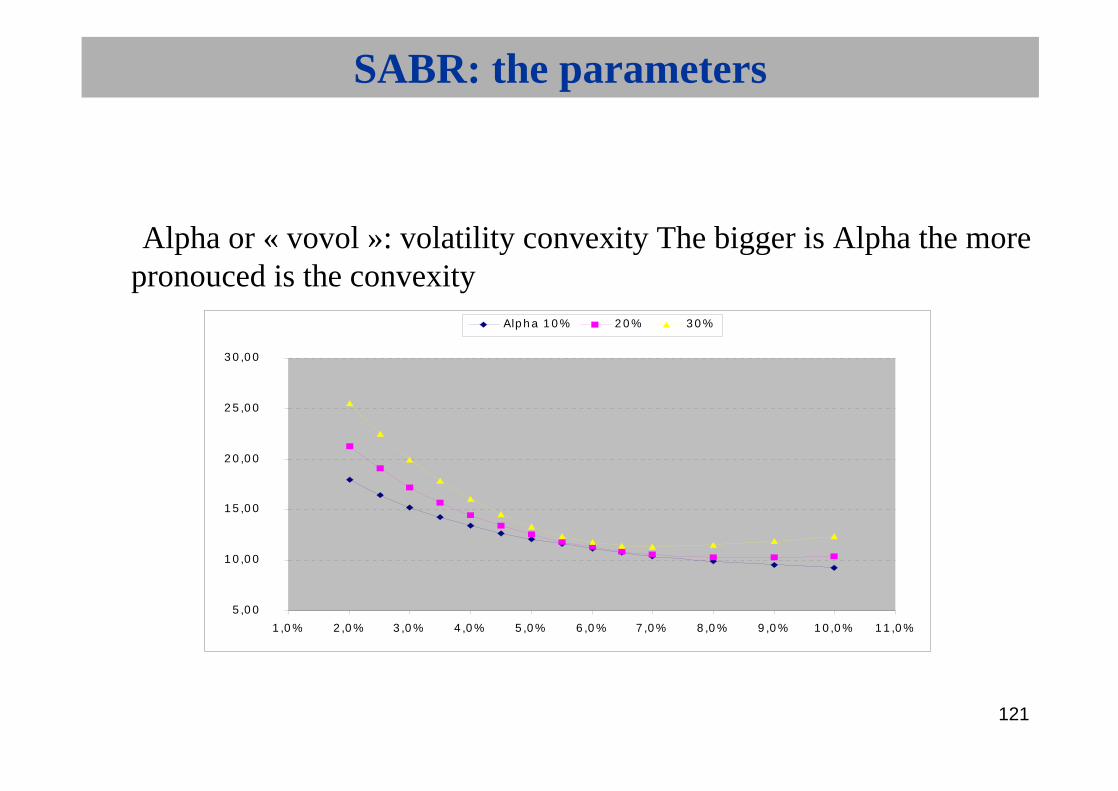

• Alpha or « vovol »: volatility convexity The bigger is Alpha the morepronouced is the convexity.

SABR: the parameters

5 ,0 0

1 0 ,0 0

1 5 ,0 0

2 0 ,0 0

2 5 ,0 0

3 0 ,0 0

1 ,0 % 2 ,0 % 3 ,0 % 4 ,0 % 5 ,0 % 6 ,0 % 7 ,0 % 8 ,0 % 9 ,0 % 1 0 ,0 % 1 1 ,0 %

Alp h a 1 0 % 2 0 % 3 0 %

122

• Rho : correlation between the volatility and the underlying causes whatwe call a Vanna skew : it’s the slope of the tangent line At the Money.

SABR: the parameters

10,00

12,00

14,00

16,00

18,00

20,00

22,00

24,00

26,00

28,00

30,00

1,0% 2,0% 3,0% 4,0% 5,0% 6,0% 7,0% 8,0% 9,0% 10,0% 11,0%

Rho 0,1 0 -0,2

123

SABR: risk management

Delta:

Different from classic delta ! Choose Beta to have stable hedge, so predict smile dynamic (trader work and skill !).Vega: it’s the sensivity of the price to change in the volatility.

F

BS

F

BS

F

C BS

BS

124

SABR: risk management

We can consider an ATM-LogNormal-Vega, an ATM-Normal-Vega or a Sigmabeta-Vega, depending on the shifted volatility type.Drawback of SABR : gives sensitivities with respect to the modelparameters. Sometimes traders need their exposure by strike, need add B&S risk to SABR risk.

125

SABR: risk managementVolga:

Hedged with strangles. If long vovol, buy straddle, sell strangle.

Vanna: qui ressemble à

hedged with collars.

C

F

C2 C

126

SABR : calibration

SABR model should provide a good fit to the observed implied volatility curves. Since SABR parameters have different and complementary effects on the smile, the calibration become easier and intuitive. Nevertheless, an exception has to be made for Beta and Rho. Indeed, those parameters have the same impact on the smile, and more precisely they both impact its skew.

Flndlnd ATM 1

127

SABR : calibration

To avoid over-parameterisation, the Beta is not calibrated but fixed from the smile rollNumerical calibration for other parameters

128

SABR : example : EUR 28/10/05S I G M A 1 M 3 M 6 M 1 Y 2 Y 3 Y 4 Y 5 Y 6 Y 7 Y 8 Y 9 Y 1 0 Y 1 5 Y 2 0 Y 2 5 Y 3 0 Y

1 M 1 . 2 3 % 1 . 1 8 % 1 . 3 0 % 2 . 0 3 % 2 . 5 5 % 2 . 5 4 % 2 . 5 3 % 2 . 5 2 % 2 . 4 4 % 2 . 3 7 % 2 . 3 3 % 2 . 2 9 % 2 . 2 6 % 2 . 1 0 % 2 . 0 5 % 2 . 0 0 % 1 . 9 7 %3 M 1 . 4 8 % 1 . 4 3 % 1 . 6 5 % 2 . 3 0 % 2 . 5 7 % 2 . 6 1 % 2 . 5 8 % 2 . 4 7 % 2 . 3 9 % 2 . 3 4 % 2 . 3 0 % 2 . 2 7 % 2 . 2 4 % 2 . 1 0 % 2 . 0 5 % 2 . 0 1 % 1 . 9 8 %6 M 1 . 9 3 % 1 . 8 8 % 2 . 1 2 % 2 . 3 4 % 2 . 5 8 % 2 . 5 4 % 2 . 5 0 % 2 . 4 6 % 2 . 3 9 % 2 . 3 3 % 2 . 2 9 % 2 . 2 7 % 2 . 2 5 % 2 . 0 9 % 2 . 0 4 % 1 . 9 9 % 1 . 9 7 %9 M 2 . 4 1 % 2 . 3 6 % 2 . 4 0 % 2 . 4 8 % 2 . 5 7 % 2 . 5 6 % 2 . 5 2 % 2 . 4 6 % 2 . 3 8 % 2 . 3 1 % 2 . 2 9 % 2 . 2 7 % 2 . 2 6 % 2 . 1 4 % 2 . 0 6 % 2 . 0 2 % 1 . 9 9 %1 Y 2 . 4 9 % 2 . 4 4 % 2 . 4 4 % 2 . 6 6 % 2 . 6 0 % 2 . 5 8 % 2 . 5 3 % 2 . 4 6 % 2 . 4 2 % 2 . 3 9 % 2 . 3 5 % 2 . 3 2 % 2 . 2 8 % 2 . 1 5 % 2 . 0 8 % 2 . 0 4 % 2 . 0 1 %2 Y 2 . 6 9 % 2 . 6 4 % 2 . 6 4 % 2 . 6 3 % 2 . 5 6 % 2 . 5 3 % 2 . 4 6 % 2 . 4 0 % 2 . 3 8 % 2 . 3 5 % 2 . 3 2 % 2 . 3 0 % 2 . 2 7 % 2 . 1 8 % 2 . 1 1 % 2 . 0 6 % 2 . 0 3 %3 Y 2 . 6 2 % 2 . 6 0 % 2 . 6 0 % 2 . 5 9 % 2 . 5 3 % 2 . 4 7 % 2 . 4 2 % 2 . 3 7 % 2 . 3 5 % 2 . 3 1 % 2 . 3 0 % 2 . 2 8 % 2 . 2 6 % 2 . 1 9 % 2 . 1 2 % 2 . 0 8 % 2 . 0 4 %4 Y 2 . 5 9 % 2 . 5 7 % 2 . 5 7 % 2 . 5 5 % 2 . 4 9 % 2 . 4 4 % 2 . 3 9 % 2 . 3 3 % 2 . 3 2 % 2 . 3 0 % 2 . 2 8 % 2 . 2 6 % 2 . 2 4 % 2 . 1 8 % 2 . 1 3 % 2 . 0 8 % 2 . 0 4 %5 Y 2 . 5 6 % 2 . 5 4 % 2 . 5 4 % 2 . 5 1 % 2 . 4 3 % 2 . 3 8 % 2 . 3 2 % 2 . 3 0 % 2 . 2 8 % 2 . 2 4 % 2 . 2 5 % 2 . 2 3 % 2 . 2 2 % 2 . 1 7 % 2 . 1 2 % 2 . 0 7 % 2 . 0 3 %

7 Y 2 . 4 5 % 2 . 4 4 % 2 . 4 4 % 2 . 3 9 % 2 . 2 9 % 2 . 2 6 % 2 . 2 1 % 2 . 2 0 % 2 . 1 9 % 2 . 1 6 % 2 . 1 7 % 2 . 1 6 % 2 . 1 5 % 2 . 1 1 % 2 . 0 6 % 2 . 0 2 % 1 . 9 8 %

1 0 Y 2 . 3 0 % 2 . 2 9 % 2 . 2 9 % 2 . 2 7 % 2 . 1 5 % 2 . 1 3 % 2 . 1 0 % 2 . 0 7 % 2 . 0 7 % 2 . 0 7 % 2 . 0 7 % 2 . 0 7 % 2 . 0 7 % 2 . 0 1 % 1 . 9 5 % 1 . 9 1 % 1 . 8 8 %

1 5 Y 2 . 0 6 % 2 . 0 4 % 2 . 0 4 % 2 . 0 2 % 1 . 9 4 % 1 . 9 2 % 1 . 9 1 % 1 . 8 9 % 1 . 8 9 % 1 . 9 0 % 1 . 9 0 % 1 . 9 0 % 1 . 9 1 % 1 . 8 5 % 1 . 7 9 % 1 . 7 4 % 1 . 7 2 %

2 0 Y 1 . 8 4 % 1 . 8 3 % 1 . 8 3 % 1 . 8 1 % 1 . 7 6 % 1 . 7 7 % 1 . 7 7 % 1 . 7 7 % 1 . 7 8 % 1 . 7 9 % 1 . 8 0 % 1 . 8 1 % 1 . 8 2 % 1 . 7 6 % 1 . 6 8 % 1 . 6 5 % 1 . 6 4 %

2 5 Y 1 . 7 6 % 1 . 7 4 % 1 . 7 4 % 1 . 7 2 % 1 . 6 9 % 1 . 7 0 % 1 . 7 1 % 1 . 7 2 % 1 . 7 3 % 1 . 7 4 % 1 . 7 5 % 1 . 7 6 % 1 . 7 7 % 1 . 7 1 % 1 . 6 6 % 1 . 6 4 % 1 . 6 3 %

3 0 Y 1 . 6 8 % 1 . 6 7 % 1 . 6 7 % 1 . 6 4 % 1 . 6 2 % 1 . 6 4 % 1 . 6 6 % 1 . 6 8 % 1 . 6 9 % 1 . 7 0 % 1 . 7 1 % 1 . 7 2 % 1 . 7 3 % 1 . 7 0 % 1 . 6 6 % 1 . 6 5 % 1 . 6 4 %

A L P H A 1 M 3 M 6 M 1 Y 2 Y 3 Y 4 Y 5 Y 6 Y 7 Y 8 Y 9 Y 1 0 Y 1 5 Y 2 0 Y 2 5 Y 3 0 Y

1 M 1 5 . 0 0 % 1 5 . 0 0 % 1 5 . 0 0 % 2 6 . 3 3 % 4 9 . 0 0 % 5 7 . 6 7 % 6 6 . 6 7 % 7 5 . 0 0 % 7 5 . 0 0 % 7 5 . 0 0 % 7 5 . 0 0 % 7 5 . 0 0 % 7 5 . 0 0 % 7 0 . 0 0 % 6 5 . 0 0 % 6 5 . 0 0 % 6 5 . 0 0 %

3 M 1 7 . 5 0 % 1 7 . 5 0 % 1 7 . 5 0 % 2 8 . 3 3 % 5 0 . 0 0 % 5 8 . 3 3 % 6 6 . 6 7 % 7 5 . 0 0 % 7 5 . 0 0 % 7 5 . 0 0 % 7 5 . 0 0 % 7 5 . 0 0 % 7 5 . 0 0 % 7 0 . 0 0 % 6 5 . 0 0 % 6 5 . 0 0 % 6 5 . 0 0 %

6 M 2 0 . 0 0 % 2 0 . 0 0 % 2 0 . 0 0 % 2 9 . 2 2 % 4 7 . 6 7 % 5 4 . 2 2 % 5 9 . 7 8 % 6 5 . 3 3 % 6 4 . 8 7 % 6 4 . 4 0 % 6 3 . 9 3 % 6 3 . 4 7 % 6 3 . 0 0 % 5 9 . 8 3 % 5 6 . 6 7 % 5 6 . 6 7 % 5 6 . 6 7 %

9 M 2 3 . 0 0 % 2 3 . 0 0 % 2 3 . 0 0 % 3 0 . 7 8 % 4 6 . 3 3 % 5 0 . 1 1 % 5 2 . 8 9 % 5 5 . 6 7 % 5 4 . 7 3 % 5 3 . 8 0 % 5 2 . 8 7 % 5 1 . 9 3 % 5 1 . 0 0 % 4 9 . 6 7 % 4 8 . 3 3 % 4 8 . 3 3 % 4 8 . 3 3 %

1 Y 3 4 . 0 0 % 3 4 . 0 0 % 3 4 . 0 0 % 3 8 . 0 0 % 4 6 . 0 0 % 4 6 . 0 0 % 4 6 . 0 0 % 4 6 . 0 0 % 4 4 . 6 0 % 4 3 . 2 0 % 4 1 . 8 0 % 4 0 . 4 0 % 3 9 . 0 0 % 3 9 . 5 0 % 4 0 . 0 0 % 4 0 . 0 0 % 4 0 . 0 0 %

2 Y 3 9 . 5 0 % 3 9 . 5 0 % 3 9 . 5 0 % 4 0 . 2 9 % 4 1 . 8 8 % 4 2 . 7 1 % 4 2 . 5 4 % 4 2 . 3 8 % 4 1 . 3 8 % 4 0 . 3 8 % 3 9 . 3 8 % 3 8 . 3 8 % 3 7 . 3 8 % 3 7 . 6 3 % 3 7 . 8 8 % 3 7 . 8 8 % 3 7 . 8 8 %

3 Y 4 1 . 5 0 % 4 1 . 5 0 % 4 1 . 5 0 % 4 0 . 5 8 % 3 8 . 7 5 % 3 9 . 4 2 % 3 9 . 0 8 % 3 8 . 7 5 % 3 8 . 1 5 % 3 7 . 5 5 % 3 6 . 9 5 % 3 6 . 3 5 % 3 5 . 7 5 % 3 5 . 7 5 % 3 5 . 7 5 % 3 5 . 7 5 % 3 5 . 7 5 %

4 Y 4 0 . 5 0 % 4 0 . 5 0 % 4 0 . 5 0 % 3 8 . 8 8 % 3 5 . 6 3 % 3 6 . 1 3 % 3 5 . 6 3 % 3 4 . 1 3 % 3 4 . 9 3 % 3 4 . 7 3 % 3 4 . 5 3 % 3 4 . 3 3 % 3 4 . 1 3 % 3 3 . 8 8 % 3 3 . 6 3 % 3 3 . 6 3 % 3 3 . 6 3 %

5 Y 3 7 . 0 0 % 3 7 . 0 0 % 3 7 . 0 0 % 3 5 . 8 3 % 3 3 . 5 0 % 3 2 . 8 3 % 3 2 . 1 7 % 3 1 . 5 0 % 3 1 . 7 0 % 3 1 . 9 0 % 3 2 . 1 0 % 3 2 . 3 0 % 3 2 . 5 0 % 3 2 . 0 0 % 3 1 . 5 0 % 3 1 . 5 0 % 3 1 . 5 0 %

7 Y 3 2 . 0 0 % 3 2 . 0 0 % 3 2 . 0 0 % 3 1 . 9 3 % 3 1 . 8 0 % 3 1 . 4 0 % 3 1 . 0 0 % 3 0 . 6 0 % 3 0 . 5 4 % 3 0 . 4 8 % 3 0 . 4 2 % 3 0 . 3 6 % 3 0 . 3 0 % 2 9 . 9 0 % 2 9 . 5 0 % 2 9 . 5 0 % 2 9 . 5 0 %

1 0 Y 2 8 . 5 0 % 2 8 . 5 0 % 2 8 . 5 0 % 2 8 . 7 5 % 2 9 . 2 5 % 2 9 . 2 5 % 2 9 . 2 5 % 2 9 . 2 5 % 2 8 . 8 0 % 2 8 . 3 5 % 2 7 . 9 0 % 2 7 . 4 5 % 2 7 . 0 0 % 2 6 . 7 5 % 2 6 . 5 0 % 2 6 . 5 0 % 2 6 . 5 0 %

1 5 Y 2 5 . 5 0 % 2 5 . 5 0 % 2 5 . 5 0 % 2 6 . 3 5 % 2 8 . 0 6 % 2 7 . 8 1 % 2 7 . 5 6 % 2 7 . 3 1 % 2 6 . 8 0 % 2 6 . 2 9 % 2 5 . 7 8 % 2 5 . 2 6 % 2 4 . 7 5 % 2 4 . 5 6 % 2 4 . 3 8 % 2 4 . 3 8 % 2 4 . 3 8 %

2 0 Y 2 5 . 0 0 % 2 5 . 0 0 % 2 5 . 0 0 % 2 5 . 6 3 % 2 6 . 8 8 % 2 6 . 3 8 % 2 5 . 8 8 % 2 5 . 3 8 % 2 4 . 8 0 % 2 4 . 2 3 % 2 3 . 6 5 % 2 3 . 0 8 % 2 2 . 5 0 % 2 2 . 3 8 % 2 2 . 2 5 % 2 2 . 2 5 % 2 2 . 2 5 %

2 5 Y 2 4 . 5 0 % 2 4 . 5 0 % 2 4 . 5 0 % 2 4 . 9 0 % 2 5 . 6 9 % 2 4 . 9 4 % 2 4 . 1 9 % 2 3 . 4 4 % 2 2 . 8 0 % 2 2 . 1 6 % 2 1 . 5 3 % 2 0 . 8 9 % 2 0 . 2 5 % 2 0 . 1 9 % 2 0 . 1 3 % 2 0 . 1 3 % 2 0 . 1 3 %

3 0 Y 2 4 . 0 0 % 2 4 . 0 0 % 2 4 . 0 0 % 2 4 . 1 7 % 2 4 . 5 0 % 2 3 . 5 0 % 2 2 . 5 0 % 2 1 . 5 0 % 2 0 . 8 0 % 2 0 . 1 0 % 1 9 . 4 0 % 1 8 . 7 0 % 1 8 . 0 0 % 1 8 . 0 0 % 1 8 . 0 0 % 1 8 . 0 0 % 1 8 . 0 0 %

R H O 1 M 3 M 6 M 1 Y 2 Y 3 Y 4 Y 5 Y 6 Y 7 Y 8 Y 9 Y 1 0 Y 1 5 Y 2 0 Y 2 5 Y 3 0 Y

1 M 3 3 . 0 0 % 3 3 . 0 0 % 3 3 . 0 0 % 3 3 . 6 7 % 3 5 . 0 0 % 3 0 . 0 0 % 2 5 . 0 0 % 2 0 . 0 0 % 1 8 . 0 0 % 1 6 . 0 0 % 1 4 . 0 0 % 1 2 . 0 0 % 1 0 . 0 0 % 5 . 2 5 % 0 . 5 0 % 0 . 5 0 % 0 . 5 0 %3 M 3 3 . 0 0 % 3 3 . 0 0 % 3 3 . 0 0 % 3 3 . 6 7 % 3 5 . 0 0 % 3 0 . 0 0 % 2 5 . 0 0 % 2 0 . 0 0 % 1 8 . 0 0 % 1 6 . 0 0 % 1 4 . 0 0 % 1 2 . 0 0 % 1 0 . 0 0 % 5 . 2 5 % 0 . 5 0 % 0 . 5 0 % 0 . 5 0 %6 M 3 3 . 0 0 % 3 3 . 0 0 % 3 3 . 0 0 % 3 2 . 5 6 % 3 1 . 6 7 % 2 7 . 0 0 % 2 2 . 3 3 % 1 7 . 6 7 % 1 1 . 3 0 % 9 . 6 0 % 7 . 9 0 % 6 . 2 0 % 8 . 1 7 % 1 . 2 5 % - 0 . 3 0 % - 3 . 5 0 % - 1 . 3 0 %9 M 3 3 . 0 0 % 3 3 . 0 0 % 3 3 . 0 0 % 3 1 . 4 4 % 2 8 . 3 3 % 2 4 . 0 0 % 1 9 . 6 7 % 1 5 . 3 3 % 1 1 . 3 0 % 9 . 6 0 % 7 . 9 0 % 6 . 2 0 % 6 . 3 3 % 1 . 2 5 % - 1 . 2 0 % - 3 . 5 0 % - 3 . 2 0 %1 Y 3 1 . 0 0 % 3 1 . 0 0 % 3 1 . 0 0 % 2 9 . 0 0 % 2 5 . 0 0 % 2 1 . 0 0 % 1 7 . 0 0 % 1 3 . 0 0 % 1 1 . 3 0 % 9 . 6 0 % 7 . 9 0 % 6 . 2 0 % 4 . 5 0 % 1 . 2 5 % - 2 . 0 0 % - 3 . 5 0 % - 5 . 0 0 %2 Y 2 3 . 0 0 % 2 3 . 0 0 % 2 3 . 0 0 % 2 2 . 5 8 % 2 1 . 7 5 % 1 7 . 4 2 % 1 3 . 0 8 % 8 . 7 5 % 7 . 3 8 % 6 . 0 0 % 4 . 6 3 % 3 . 2 5 % 1 . 8 8 % - 0 . 9 0 % - 3 . 8 0 % - 5 . 0 0 % - 6 . 3 0 %3 Y 2 0 . 5 0 % 2 0 . 5 0 % 2 0 . 5 0 % 1 9 . 8 3 % 1 8 . 5 0 % 1 3 . 8 3 % 9 . 1 7 % 4 . 5 0 % 3 . 4 5 % 2 . 4 0 % 1 . 3 5 % 0 . 3 0 % - 0 . 8 0 % - 3 . 1 0 % - 5 . 5 0 % - 6 . 5 0 % - 7 . 5 0 %4 Y 2 0 . 0 0 % 2 0 . 0 0 % 2 0 . 0 0 % 1 8 . 4 2 % 1 5 . 2 5 % 1 0 . 2 5 % 5 . 2 5 % 0 . 2 5 % - 0 . 5 0 % - 1 . 2 0 % - 1 . 9 0 % - 2 . 7 0 % - 3 . 4 0 % - 5 . 3 0 % - 7 . 3 0 % - 8 . 0 0 % - 8 . 8 0 %5 Y 2 0 . 0 0 % 2 0 . 0 0 % 2 0 . 0 0 % 1 7 . 3 3 % 1 2 . 0 0 % 6 . 6 7 % 1 . 3 3 % - 4 . 0 0 % - 4 . 4 0 % - 4 . 8 0 % - 5 . 2 0 % - 5 . 6 0 % - 6 . 0 0 % - 7 . 5 0 % - 9 . 0 0 % - 9 . 5 0 % - 1 0 . 0 0 %7 Y 2 0 . 0 0 % 2 0 . 0 0 % 2 0 . 0 0 % 1 6 . 1 5 % 8 . 4 4 % 3 . 8 9 % - 0 . 7 0 % - 5 . 2 0 % - 5 . 5 0 % - 5 . 8 0 % - 6 . 2 0 % - 6 . 5 0 % - 6 . 8 0 % - 8 . 3 0 % - 9 . 8 0 % - 1 0 . 3 0 % - 1 0 . 8 0 %

1 0 Y 1 8 . 5 0 % 1 8 . 5 0 % 1 8 . 5 0 % 1 3 . 3 7 % 3 . 1 0 % - 0 . 3 0 % - 3 . 6 0 % - 7 . 0 0 % - 7 . 2 0 % - 7 . 4 0 % - 7 . 6 0 % - 7 . 8 0 % - 8 . 0 0 % - 9 . 5 0 % - 1 1 . 0 0 % - 1 1 . 5 0 % - 1 2 . 0 0 %1 5 Y 1 3 . 0 0 % 1 3 . 0 0 % 1 3 . 0 0 % 9 . 4 4 % 2 . 3 3 % - 0 . 3 0 % - 3 . 6 0 % - 8 . 0 0 % - 7 . 2 0 % - 7 . 4 0 % - 7 . 6 0 % - 7 . 8 0 % - 9 . 9 0 % - 1 1 . 3 0 % - 1 2 . 6 0 % - 1 3 . 1 0 % - 1 3 . 5 0 %2 0 Y 7 . 0 0 % 7 . 0 0 % 7 . 0 0 % 5 . 1 8 % 1 . 5 5 % - 0 . 3 0 % - 3 . 6 0 % - 9 . 0 0 % - 7 . 2 0 % - 7 . 4 0 % - 7 . 6 0 % - 7 . 8 0 % - 1 1 . 8 0 % - 1 3 . 0 0 % - 1 4 . 3 0 % - 1 4 . 6 0 % - 1 5 . 0 0 %2 5 Y 3 . 0 0 % 3 . 0 0 % 3 . 0 0 % 2 . 2 6 % 0 . 7 8 % - 0 . 3 0 % - 3 . 6 0 % - 1 0 . 0 0 % - 7 . 2 0 % - 7 . 4 0 % - 7 . 6 0 % - 7 . 8 0 % - 1 3 . 6 0 % - 1 4 . 8 0 % - 1 5 . 9 0 % - 1 6 . 2 0 % - 1 6 . 5 0 %3 0 Y 1 . 0 0 % 1 . 0 0 % 1 . 0 0 % 0 . 6 7 % 0 . 0 0 % - 0 . 3 0 % - 3 . 6 0 % - 1 1 . 0 0 % - 7 . 2 0 % - 7 . 4 0 % - 7 . 6 0 % - 7 . 8 0 % - 1 5 . 5 0 % - 1 6 . 5 0 % - 1 7 . 5 0 % - 1 7 . 8 0 % - 1 8 . 0 0 %

B E T A 1 M 3 M 6 M 1 Y 2 Y 3 Y 4 Y 5 Y 6 Y 7 Y 8 Y 9 Y 1 0 Y 1 5 Y 2 0 Y 2 5 Y 3 0 Y1 M 0 . 4 0 . 4 0 . 4 0 . 4 0 . 4 0 . 4 0 . 4 0 . 4 0 . 4 0 . 4 0 . 4 0 . 4 0 . 4 0 . 4 0 . 4 0 . 4 0 . 43 M 0 . 4 0 . 4 0 . 4 0 . 4 0 . 4 0 . 4 0 . 4 0 . 4 0 . 4 0 . 4 0 . 4 0 . 4 0 . 4 0 . 4 0 . 4 0 . 4 0 . 46 M 0 . 4 0 . 4 0 . 4 0 . 4 0 . 4 0 . 4 0 . 4 0 . 4 0 . 4 0 . 4 0 . 4 0 . 4 0 . 4 0 . 4 0 . 4 0 . 4 0 . 49 M 0 . 4 0 . 4 0 . 4 0 . 4 0 . 4 0 . 4 0 . 4 0 . 4 0 . 4 0 . 4 0 . 4 0 . 4 0 . 4 0 . 4 0 . 4 0 . 4 0 . 41 Y 0 . 4 0 . 4 0 . 4 0 . 4 0 . 4 0 . 4 0 . 4 0 . 4 0 . 4 0 . 4 0 . 4 0 . 4 0 . 4 0 . 4 0 . 4 0 . 4 0 . 42 Y 0 . 4 0 . 4 0 . 4 0 . 4 0 . 4 0 . 4 0 . 4 0 . 4 0 . 4 0 . 4 0 . 4 0 . 4 0 . 4 0 . 4 0 . 4 0 . 4 0 . 43 Y 0 . 4 0 . 4 0 . 4 0 . 4 0 . 4 0 . 4 0 . 4 0 . 4 0 . 4 0 . 4 0 . 4 0 . 4 0 . 4 0 . 4 0 . 4 0 . 4 0 . 44 Y 0 . 4 0 . 4 0 . 4 0 . 4 0 . 4 0 . 4 0 . 4 0 . 4 0 . 4 0 . 4 0 . 4 0 . 4 0 . 4 0 . 4 0 . 4 0 . 4 0 . 45 Y 0 . 4 0 . 4 0 . 4 0 . 4 0 . 4 0 . 4 0 . 4 0 . 4 0 . 4 0 . 4 0 . 4 0 . 4 0 . 4 0 . 4 0 . 4 0 . 4 0 . 47 Y 0 . 4 0 . 4 0 . 4 0 . 4 0 . 4 0 . 4 0 . 4 0 . 4 0 . 4 0 . 4 0 . 4 0 . 4 0 . 4 0 . 4 0 . 4 0 . 4 0 . 4

1 0 Y 0 . 4 0 . 4 0 . 4 0 . 4 0 . 4 0 . 4 0 . 4 0 . 4 0 . 4 0 . 4 0 . 4 0 . 4 0 . 4 0 . 4 0 . 4 0 . 4 0 . 41 5 Y 0 . 4 0 . 4 0 . 4 0 . 4 0 . 4 0 . 4 0 . 4 0 . 4 0 . 4 0 . 4 0 . 4 0 . 4 0 . 4 0 . 4 0 . 4 0 . 4 0 . 42 0 Y 0 . 4 0 . 4 0 . 4 0 . 4 0 . 4 0 . 4 0 . 4 0 . 4 0 . 4 0 . 4 0 . 4 0 . 4 0 . 4 0 . 4 0 . 4 0 . 4 0 . 42 5 Y 0 . 4 0 . 4 0 . 4 0 . 4 0 . 4 0 . 4 0 . 4 0 . 4 0 . 4 0 . 4 0 . 4 0 . 4 0 . 4 0 . 4 0 . 4 0 . 4 0 . 43 0 Y 0 . 4 0 . 4 0 . 4 0 . 4 0 . 4 0 . 4 0 . 4 0 . 4 0 . 4 0 . 4 0 . 4 0 . 4 0 . 4 0 . 4 0 . 4 0 . 4 0 . 4

Vertical axis : maturity of option, Horizontal axis: underlying

129

SABR: conclusion and drawback

Good parametrisation of market smileEasy numerical calibrationParameters interpretation in term of risk-management

Main drawback : each underlying modeled separately :so can be inconsistent for some exotic productsmain application of risk-management is for vanilla products.

130

Digital rate options and applications to exotic swapsComplex Products : digital, steepner, ratchet…Bermuda swaptionsCallablesAppendixes :Standard Deviations vs VolatilitiesSABRCorrelation issuesLGMRisk-Management of exotics

131

Correlations issues

Example of correlation matrix : in red tenor, expiry = maturity of the options expiry 1y

3m 6m 1y 2y 5y 10y 15y 20y 30y3m 1.00 0.90 0.74 0.67 0.46 0.43 0.41 0.38 0.376m 0.90 1.00 0.79 0.71 0.49 0.44 0.42 0.38 0.381y 0.74 0.79 1.00 0.87 0.83 0.76 0.73 0.68 0.622y 0.67 0.71 0.87 1.00 0.89 0.86 0.79 0.72 0.695y 0.46 0.49 0.83 0.89 1.00 0.92 0.91 0.85 0.84

10y 0.43 0.44 0.76 0.86 0.92 1.00 0.93 0.90 0.8815y 0.41 0.42 0.73 0.79 0.91 0.93 1.00 0.92 0.9220y 0.38 0.38 0.68 0.72 0.85 0.90 0.92 1.00 0.9530y 0.37 0.38 0.62 0.69 0.84 0.88 0.92 0.95 1.00

expiry 2y3m 6m 1y 2y 5y 10y 15y 20y 30y

3m 1.00 0.92 0.79 0.73 0.57 0.54 0.53 0.50 0.506m 0.92 1.00 0.83 0.76 0.60 0.56 0.54 0.51 0.511y 0.79 0.83 1.00 0.89 0.85 0.79 0.77 0.73 0.662y 0.73 0.76 0.89 1.00 0.89 0.86 0.81 0.76 0.725y 0.57 0.60 0.85 0.89 1.00 0.92 0.91 0.88 0.87

10y 0.54 0.56 0.79 0.86 0.92 1.00 0.93 0.91 0.8915y 0.53 0.54 0.77 0.81 0.91 0.93 1.00 0.93 0.9320y 0.50 0.51 0.73 0.76 0.88 0.91 0.93 1.00 0.9530y 0.50 0.51 0.66 0.72 0.87 0.89 0.93 0.95 1.00

expiry 5y3m 6m 1y 2y 5y 10y 15y 20y 30y

3m 1.00 0.96 0.88 0.85 0.76 0.75 0.74 0.72 0.726m 0.96 1.00 0.91 0.87 0.79 0.77 0.76 0.74 0.741y 0.88 0.91 1.00 0.93 0.87 0.85 0.83 0.82 0.752y 0.85 0.87 0.93 1.00 0.89 0.87 0.85 0.82 0.785y 0.76 0.79 0.87 0.89 1.00 0.94 0.93 0.91 0.91

10y 0.75 0.77 0.85 0.87 0.94 1.00 0.95 0.93 0.9215y 0.74 0.76 0.83 0.85 0.93 0.95 1.00 0.95 0.9420y 0.72 0.74 0.82 0.82 0.91 0.93 0.95 1.00 0.9630y 0.72 0.74 0.75 0.78 0.91 0.92 0.94 0.96 1.00

132

Correlations issues

expiry 7y3m 6m 1y 2y 5y 10y 15y 20y 30y

3m 1.00 0.97 0.90 0.88 0.81 0.80 0.79 0.78 0.786m 0.97 1.00 0.93 0.89 0.83 0.82 0.81 0.80 0.791y 0.90 0.93 1.00 0.93 0.88 0.86 0.85 0.84 0.792y 0.88 0.89 0.93 1.00 0.89 0.87 0.85 0.84 0.815y 0.81 0.83 0.88 0.89 1.00 0.94 0.93 0.92 0.92

10y 0.80 0.82 0.86 0.87 0.94 1.00 0.95 0.94 0.9315y 0.79 0.81 0.85 0.85 0.93 0.95 1.00 0.96 0.9520y 0.78 0.80 0.84 0.84 0.92 0.94 0.96 1.00 0.9630y 0.78 0.79 0.79 0.81 0.92 0.93 0.95 0.96 1.00

expiry 10y3m 6m 1y 2y 5y 10y 15y 20y 30y

3m 1.00 0.98 0.91 0.90 0.83 0.82 0.81 0.80 0.806m 0.98 1.00 0.94 0.91 0.85 0.84 0.83 0.82 0.821y 0.91 0.94 1.00 0.94 0.88 0.87 0.86 0.85 0.822y 0.90 0.91 0.94 1.00 0.89 0.87 0.86 0.85 0.835y 0.83 0.85 0.88 0.89 1.00 0.94 0.93 0.93 0.93

10y 0.82 0.84 0.87 0.87 0.94 1.00 0.95 0.94 0.9315y 0.81 0.83 0.86 0.86 0.93 0.95 1.00 0.96 0.9520y 0.80 0.82 0.85 0.85 0.93 0.94 0.96 1.00 0.9630y 0.80 0.82 0.82 0.83 0.93 0.93 0.95 0.96 1.00

133

Correlations issues

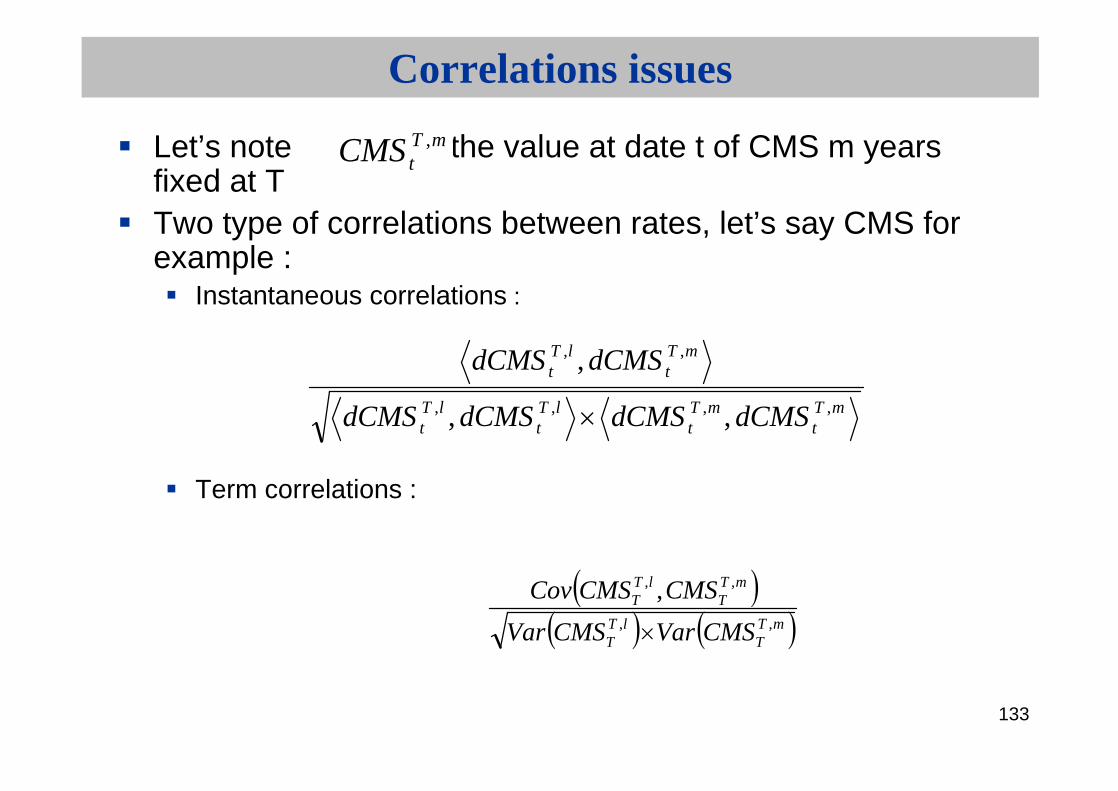

Let’s note the value at date t of CMS m yearsfixed at TTwo type of correlations between rates, let’s say CMS for example :

Instantaneous correlations :

Term correlations :

mTtCMS ,

mTt

mTt

lTt

lTt

mTt

lTt

dCMSdCMSdCMSdCMS

dCMSdCMS

,,,,

,,

,,

,

mTT

lTT

mTT

lTT

CMSVarCMSVar

CMSCMSCov,,

,, ,

134

Correlations issues

RemarksTerm correlations can be seen as a kind of average of instantaneouscorrelations (not true as volatilities are not constant) :

the instantaneous historical correlation of forwards swaps at horizon ? of maturities ? + t and ? + t ’ giving and estimate of the correlation for maturity T-?.Think to the risk managament of a 5Y CMS 10Y/2Y spread option, first youwill be exposed to the correlation between 10Y/2Y CMS in 5Years, in 4 years, …in 1years and finally to the correlation between CMS10Y and 2Y.

135

Correlations issues

For derivatives pricing/risk management (example : spreadoptions pricing), of course only term correlations are relevant.

136

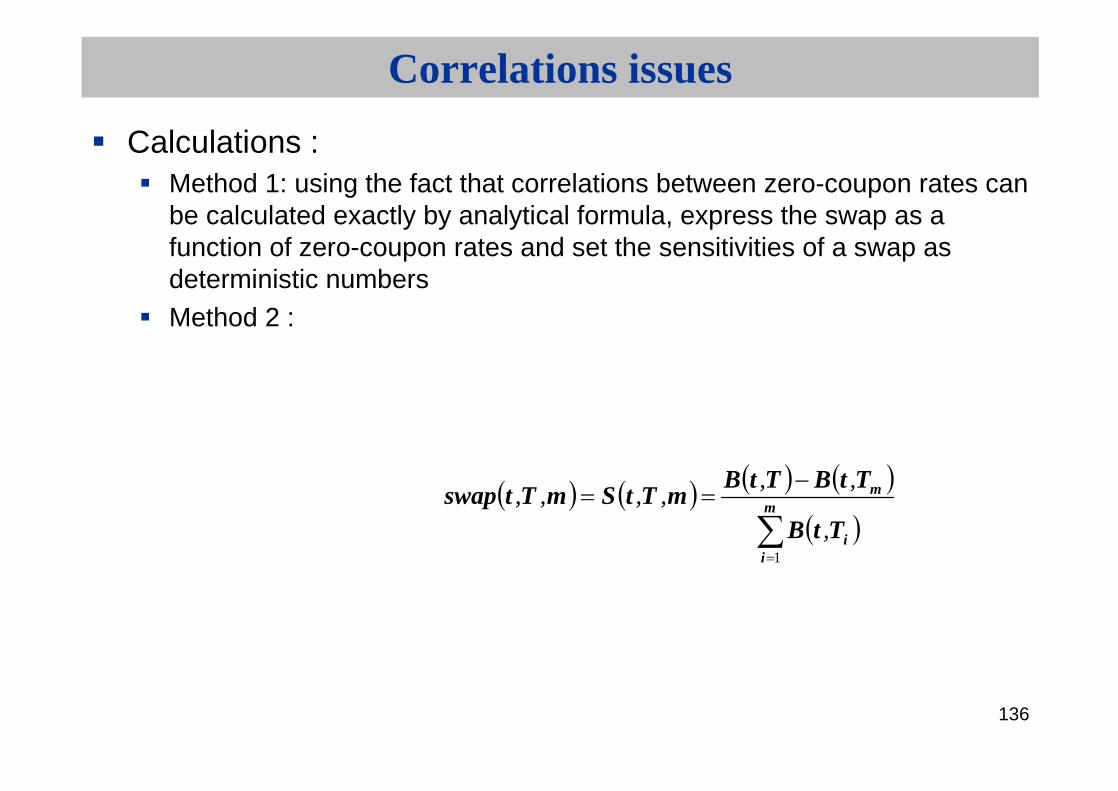

Correlations issues

Calculations : Method 1: using the fact that correlations between zero-coupon rates canbe calculated exactly by analytical formula, express the swap as a function of zero-coupon rates and set the sensitivities of a swap as deterministic numbersMethod 2 :

m

ii

m

TtB

TtBTtBmTtSmTtswap

1

,

,,,,,,

137

Correlations issues in LGM2F

A sketch of calculations :

22

11 tt dWTtBTtdWTtBTtTtdB ,,,,,

22

11 tmmtmmm dWTtBTtdWTtBTtTtdB ,,,,,

222

111

tmm

tmmm

dWTtBTtTtBTt

dWTtBTtTtBTtTtBTtBd

,,,,

,,,,,,

138

Correlations issues in LGM2F

2

1

12

22

1

1

11

11

tm

ii

m

iii

m

mm

tm

ii

m

iii

m

mm

dWTtB

TtBTt

TtBTtBTtBTtTtBTt

dWTtB

TtBTt

TtBTtB

TtBTtTtBTt

mTtSmTtdS

,

,,

,,

,,,,

,

,,

,,

,,,,

,,

,,

139

Correlations issues in LGM2F

Formula :

Tt

mm

T Tt

mt

m

dtett

ff

dtet

fdtet

fmTSLnVar

0

21

0 0

22

2222

2

212

2

,

Tt

nmnm

T Tt

nmt

nm

dtett

ffff

dtet

ffdtet

ffnTSLnmTSLnCov

0

21

0 0

22

222

2

21,,,

140

Correlations issues in LGM2F

By setting again some stochastic numbers as constant, we getagain the correlationsThe two methods give exactly the same results !

141

Correlations issues in LGM2F

If you take two independants brownians motions, and look atterm correlations between two CMS (for instance CMS2Y and CMS10Y, a canonical example for spreads products)

these correlations tend to degenerate very quick to a value very close to 1By choosing a correlation between the two brownians very negative

(typically -0.8), you can address this problem

142

Correlations issues in LGM2F

Example with constant volatilities, just for illustration purpose :

T1 2

0.15

0.34

T2 10

correl -0.8

sigma1 0.65%

sigma2 1.17%

Correl swaps 2Y/swap10Y

0.8200

0.8400

0.8600

0.8800

0.9000

0.9200

0.9400

0.9600

0.9800

1.0000

0.25 2.25 4.25 6.25 8.25 10.25 12.25 14.25 16.25 18.25

LGMwithout correl

LGMwith correl

143

Digital rate options and applications to exotic swapsComplex Products : digital, steepner, ratchet…Bermuda swaptionsCallablesAppendixes :Standard Deviations vs VolatilitiesSABRCorrelation issuesLGMRisk-Management of exotics

144

IR models : reminder on Models of the short rate

Vasicek model (1977),

z standard brownian motion

s standard deviation of the short rateb long term level of r, a mean reversionAnalytical formulas for today and any future date yield curve

Analytical formulas for european options on coupon bearing bondsPossibility of negative rates (normal model)

tdzdtrbadr )(

145

IR models : reminder on Models of the short rate

Cox Ingersoll (1985),

Rates are always nonnegative

As the short rate increase, its standard déviation increases

tdzrdtrbadr )(

146

IR models : reminder on Models of the short rate

Main drawback of these models : modeling only the dynamic of the short rate :

Yield curve today and in the future depends only on the short rate today

Models parameters

Impossibility to fit the yield curve today !Risk of mispricing !

147

How to solve this problem ?

Hull & White extended version of Vasicekmodel (1990) :

dr=(?(t)-ar)dt+sdzClosed formulas for all vanilla derivatives (caps, swaptions, europeanbond options)?(t) enables to fit exactly the today yield curveEasy Tree implementation for american, some callable products

148

How to solve this problem ?

Ho & Lee (1985 ) and Heath-Jarrow Morton (1987-1992 )Ho & Lee is essentially a discrete version of HJMSee Jamshidian (1991) for discrete version

Focus on HJM, and in fact LGM

149

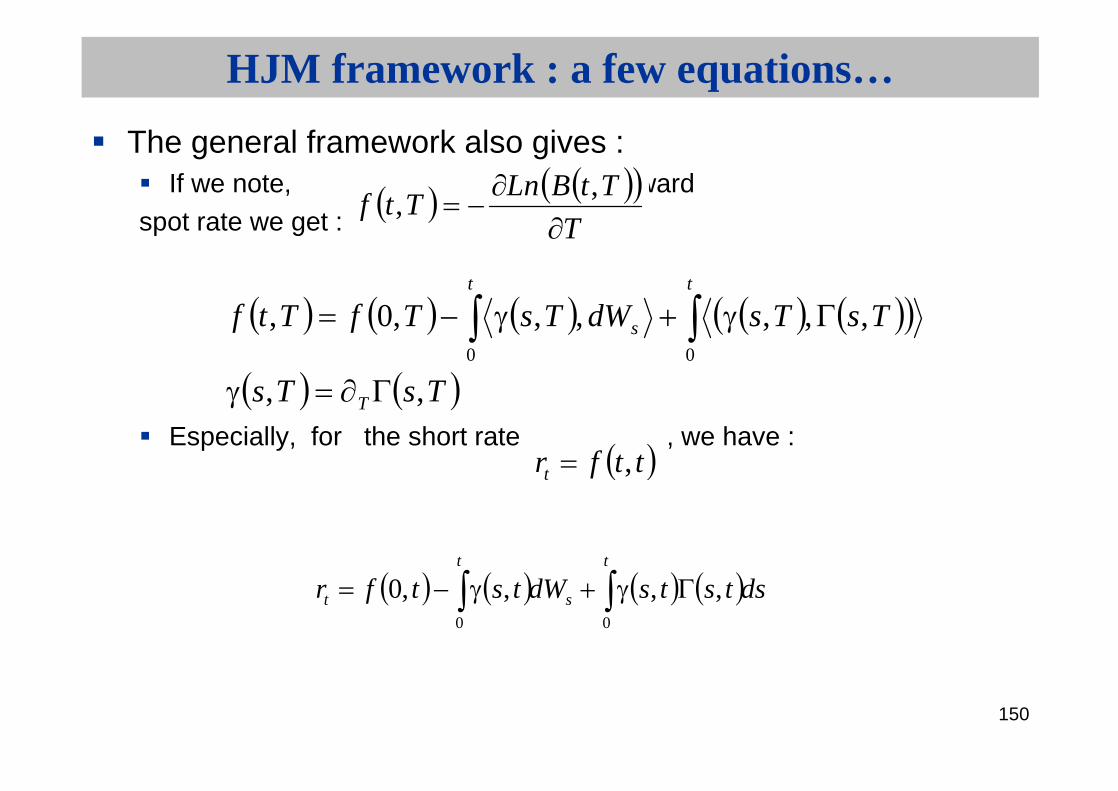

HJM framework : a few equations…

Main idea : Use the market yield curve as a starting point and model its dynamic over time, under the constraint that no arbitrage is possibleThe general equation of the model + the absence of arbitrage opportunities leads to the existence of a risk-neutral probability Q under which the dynamics of zero-coupon prices is :

tt dWTtdtrTtB

TtdB),,(

),(

),(

notor tsindependan

average, 0 have components motion,brownian sionalmultidimenW

ies volatilitlocal ofvector ,

t

Tt

150

HJM framework : a few equations…

The general framework also gives :If we note, the forward

spot rate we get :

Especially, for the short rate , we have :

T

TtBLnTtf

,,

TsTs

TsTsdWTsTfTtf

T

tt

s

,,

,,,,,,0,00

ttfrt ,

dststsdWtstfrt

s

t

t

00

,,,,0

151

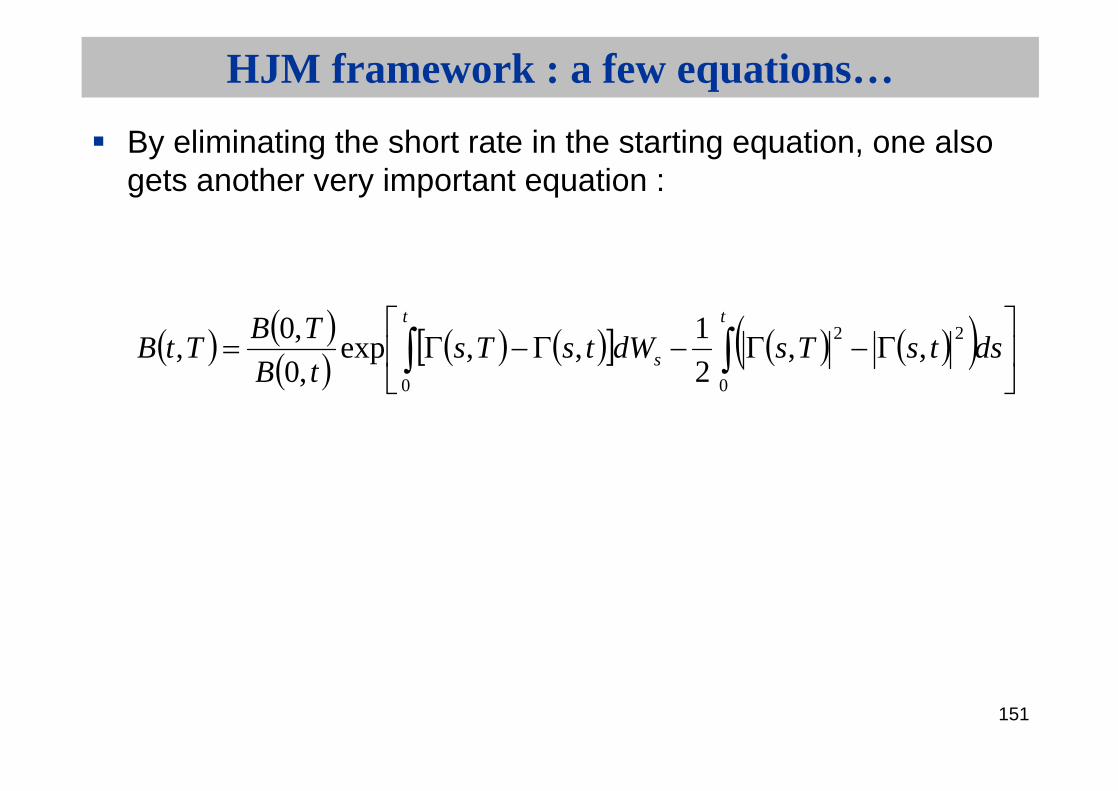

HJM framework : a few equations…

By eliminating the short rate in the starting equation, one alsogets another very important equation :

t t

s dstsTsdWtsTstB

TBTtB

0 0

22,,

2

1,,exp

,0

,0,

152

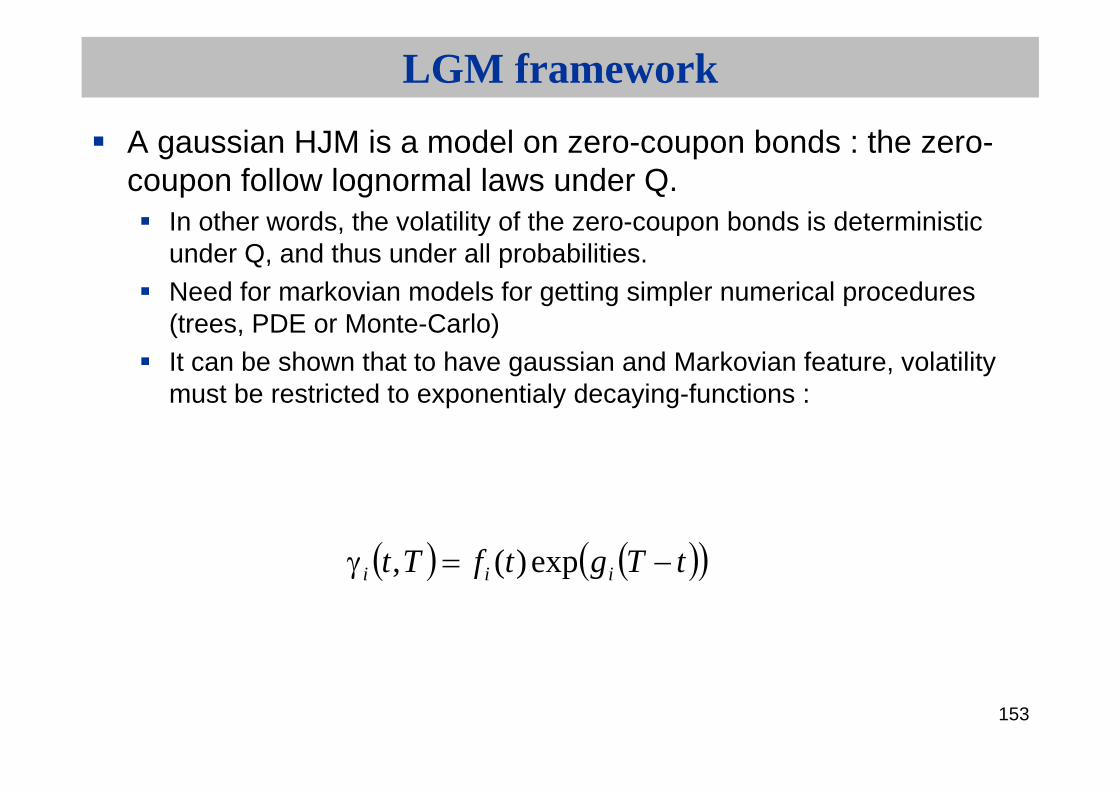

LGM framework

HJM is a very general framework : for practical implementation and use, need more specifications

LGM (Linear Gaussian Markov model)

153

LGM framework

A gaussian HJM is a model on zero-coupon bonds : the zero-coupon follow lognormal laws under Q.

In other words, the volatility of the zero-coupon bonds is deterministic under Q, and thus under all probabilities.Need for markovian models for getting simpler numerical procedures (trees, PDE or Monte-Carlo)It can be shown that to have gaussian and Markovian feature, volatility must be restricted to exponentialy decaying-functions :

tTgtfTt iii exp)(,

154

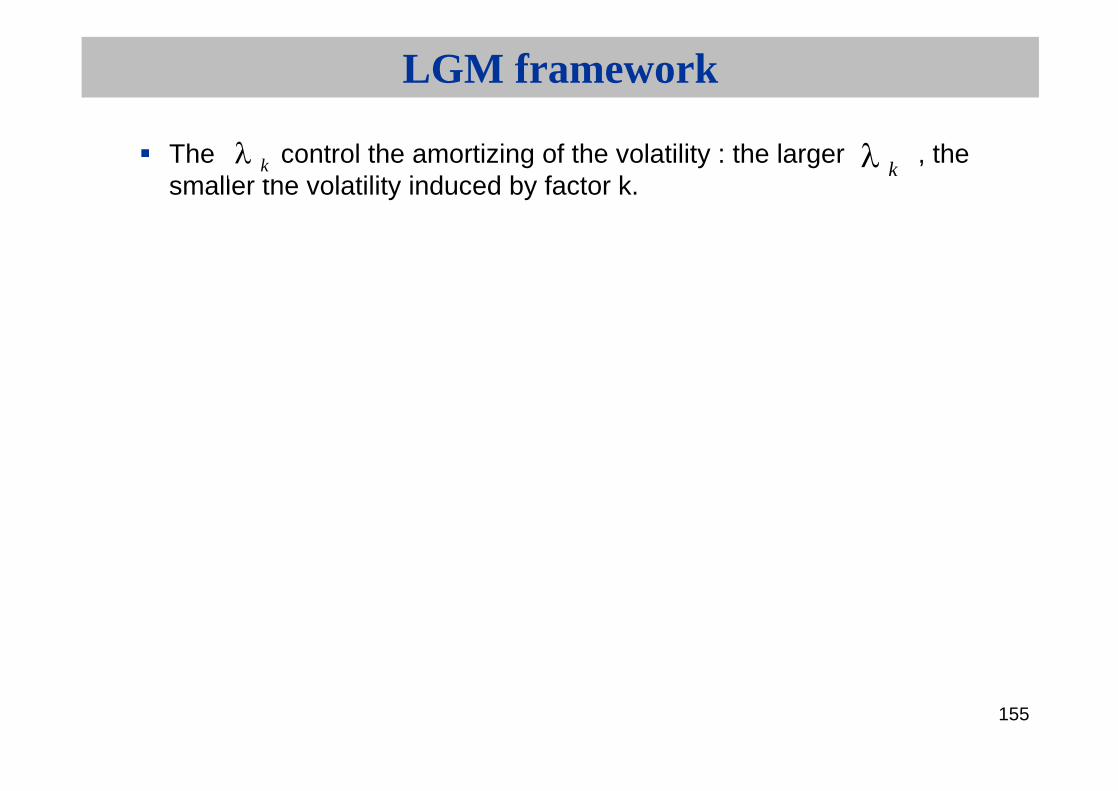

LGM framework

In practice, a good choice for volatilities is :

called mean-reversion parameters, are positive constant

as the instantaneous volatilities, piecewise constant

tTexpt

with

T,t,,T,tT,t

kk

kk

n

1

1

k

k

155

LGM framework

The control the amortizing of the volatility : the larger , the smaller the volatility induced by factor k.

k k

156

LGM-1F model features

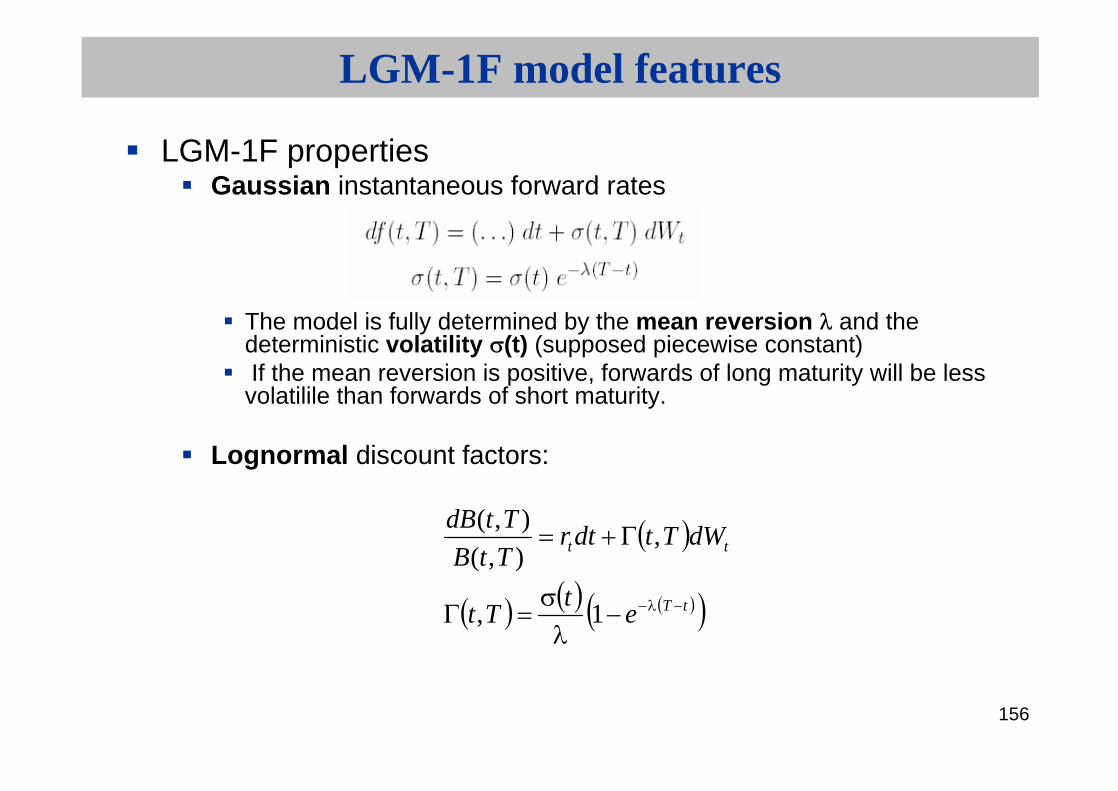

LGM-1F propertiesGaussian instantaneous forward rates

The model is fully determined by the mean reversion and the deterministic volatility (t) (supposed piecewise constant)If the mean reversion is positive, forwards of long maturity will be lessvolatilile than forwards of short maturity.

Lognormal discount factors:

tT

tt

et

Tt

dWTtdtrTtB

TtdB

1,

,),(

),(

157

LGM-1F model features

LGM-1F propertiesGaussian short rate, mean reverting

Forward Libor are shifted lognormal (constant = 1/coverage shift)

158

LGM-1F model features

Reconstruction formula for zero-coupon bonds :the whole dynamics of the curve can be summarized by a single

gaussian state variable :

See previous slide to see that is a gaussian variable.

Remark that :

tfrX tt ,0

tX

159

LGM-1F model features

Then :

Fundamental equation for all numerical methods.This is why we speak of Linear models : zero-coupon bonds canalways be seen as exponential of Linear sum of Gaussian state variables (whatever the number of factors)So zero-coupon rates are Linear sum of these state variables

duee

TtdsestT

t

tutTt

st 1, ,)(

0

22

160

LGM-1F model : vanilla pricing

Analytical formula for vanilla productsStraitghtforward B&S formula for caps & floors as Libor are shiftted Lognormal

161

LGM-1F model : vanilla pricing

For swaptions, let’s define call bond option as a derivative of pay-off :

T is the maturity of the option, is the start date of calibration product

0T

0,,,1

0, where

,,

10

10

i

n

n

iii

cni

TTTTK

TTKBTTBc

162

LGM-1F model : vanilla pricing

The pricing of call and put Bond option is analytical in LGM1F :

)(

)( and ,

)(

:by defined and

,,0

,0

,,,0,,0,,,,

,,,0,,0,,,,

0,

0,

1 0,

0,

0

0

10110

10110

00

0

xB

xBKK

xB

xBc

Kx

TT

ee

TB

TBF

TKFBSputcTBcTKTTPutBO

TKFBScallcTBcTKTTCallBO

TT

TTi

n

i TT

TTi

i

TTTTbsi

ii

n

ii

bsiiinini

n

ii

bsiiinini

ii

i

163

LGM-1F model : vanilla pricing

We use the reconstruction formula for these calculations, especially for the last equations.

164

LGM-1F model : vanilla pricing

Then a payer swaption can be seen as a modified put option :

Payer swaption

Receiver swaption is obtained as a call bond option with sameparameters.

1~

1

1-,1,for

)(,~

,,,,, 1,100

K

Kc

niKc

cTKTTPutBOKTTTswaptionpayer

nn

ii

niniene

165

LGM-1F model : calibration

Bootstrap calibration procedure

Bootstrap calibration, fast & exact

Procedure = calibration on a set of caplets/swaptions (possibly mixed) with strictly increasing expiries (i.e. one instrument by expiry date)

Choose a mean reversion , for example to match market bermuda price as bermuda are liquid

166

LGM-1F model : calibration

'T2

1 i2

…..

1T2T 3T ……

'T1

00T

3

i = so called instantaneous volatility between 1iT and iT , used to match the price of option

of maturity iT on underlying of maturity 'iT

instrument (libor for caplet or swap for a swaption ) for option of maturity iT , starts at iT ,

ends at 'iT

167

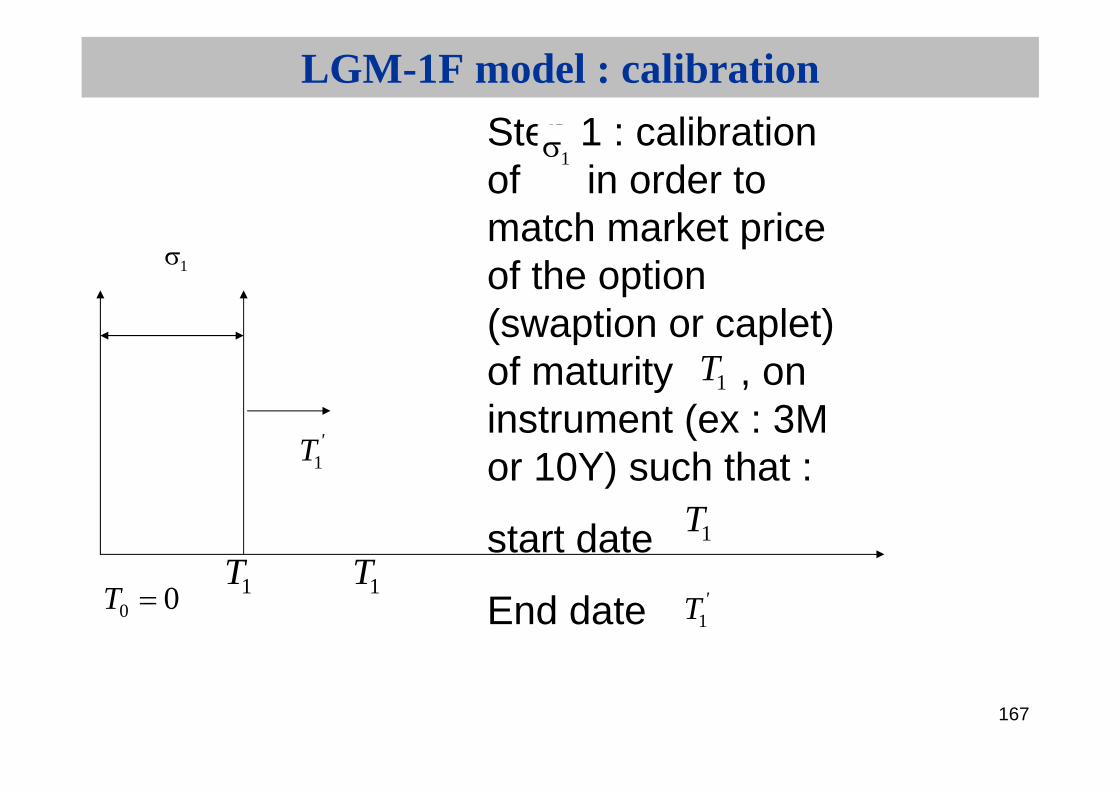

LGM-1F model : calibration

1T

1

1T

'T1

00T

Step 1 : calibration of in order to match market price of the option (swaption or caplet) of maturity , on instrument (ex : 3M or 10Y) such that :

start date

End date

1T

1T

'T1

1

168

LGM-1F model : calibration

2

2

'T2

1T 2T00T

Step 2 : calibration of in order to match market price of the option (swaption or caplet) of maturity ,on instrument such that :

start date

End date

2T

'T2

2T

169

LGM-1F model : calibration

Each instrument provides the variance of the state variable up to its expiry date

The short rate volatility (t), supposed piecewise constant, is then deduced iteratively

170

LGM-1F model calibration

One can iterate the above process to calibrate the mean reversion to a basket of instruments (e.g. to a cap)Depending on the product, we can use a diagonal of swaption (9Y in 1Y, 8Y in 2Y, …1Y in 9Y), for instance for bermudean swaptions ; the strike being the strike of bermudean swaptionsThe set of the calibration is choosen for each exotic product

171

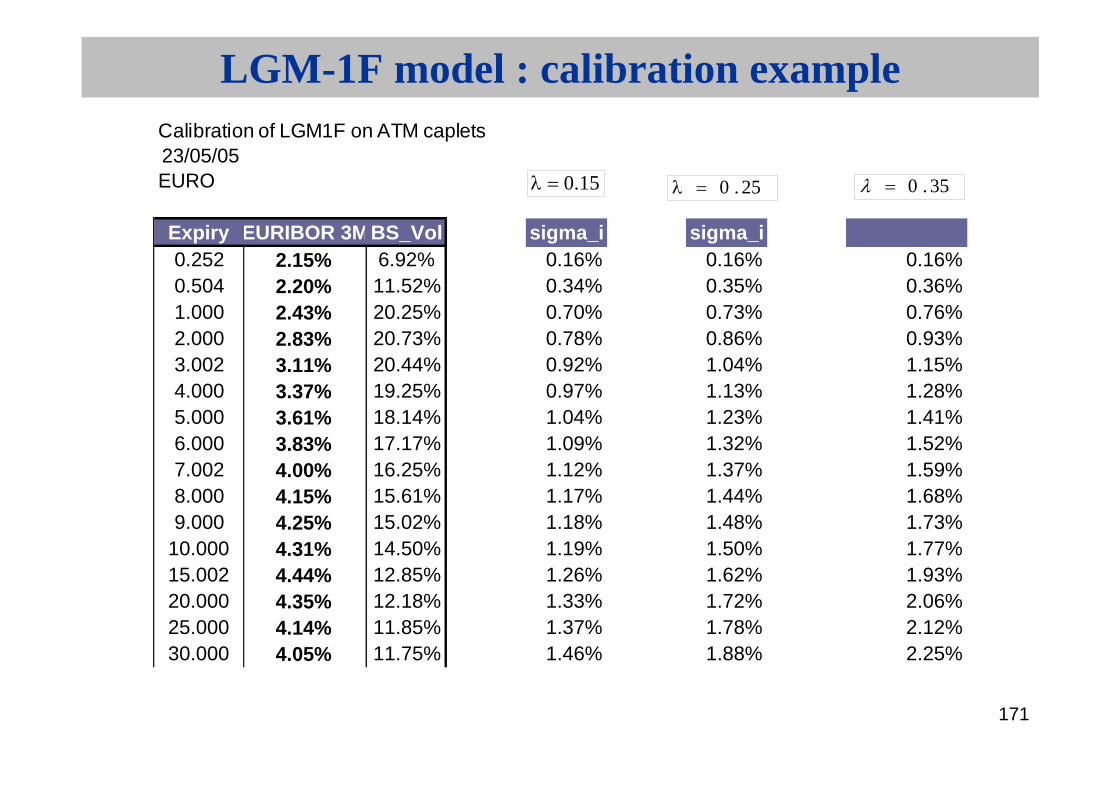

LGM-1F model : calibration exampleCalibration of LGM1F on ATM caplets23/05/05EURO

Expiry EURIBOR 3MBS_Vol sigma_i sigma_i0.252 2.15% 6.92% 0.16% 0.16% 0.16%0.504 2.20% 11.52% 0.34% 0.35% 0.36%1.000 2.43% 20.25% 0.70% 0.73% 0.76%2.000 2.83% 20.73% 0.78% 0.86% 0.93%3.002 3.11% 20.44% 0.92% 1.04% 1.15%4.000 3.37% 19.25% 0.97% 1.13% 1.28%5.000 3.61% 18.14% 1.04% 1.23% 1.41%6.000 3.83% 17.17% 1.09% 1.32% 1.52%7.002 4.00% 16.25% 1.12% 1.37% 1.59%8.000 4.15% 15.61% 1.17% 1.44% 1.68%9.000 4.25% 15.02% 1.18% 1.48% 1.73%

10.000 4.31% 14.50% 1.19% 1.50% 1.77%15.002 4.44% 12.85% 1.26% 1.62% 1.93%20.000 4.35% 12.18% 1.33% 1.72% 2.06%25.000 4.14% 11.85% 1.37% 1.78% 2.12%30.000 4.05% 11.75% 1.46% 1.88% 2.25%

15.0 25.0 35.0

172

LGM-1F model : calibration example

LGM1F and market smiles as of 23/5/2005calibration on ATM 3M caplets

8.00%

13.00%

18.00%

23.00%

28.00%

33.00%

38.00%

43.00%

48.00%

0 0.02 0.04 0.06 0.08 0.1 0.12 0.14

LGM 1Y

LGM 3Y

LGM 5Y

market 1Y

market 3Y

market 5Y

173

LGM-1F model features

Effect of mean reversion on non calibrated instrumentsResult:

If calibration to a short underlying (e.g. a caplet), the price of a long underlying instrument (e.g. a 15Y-term swaption) of same expiry willdecrease as the mean reversion increases

Analogously, if calibration to a long swaption, the price of a caplet of same expiry will increase as lambda increases.

174

LGM-1F model features

Effect of mean reversion on non calibrated instruments (continued)

Example :calibrate to a caplet (expiry = 2Y, term = 1Y), and graph the cumulative vol of B(t,2Y+x) / B(t, 2Y) on [0, 2Y] for various values of mean reversion .calibrate to a long swaption (expiry = 2Y, term = 20Y), and graph the cumulative vol of B(t,2Y+x) / B(t, 2Y) on [0, 2Y] for various values of meanreversion .

175

LGM-1F model features

Calibration on capletCumulative vol of B(t, T+x) / B(t,T)

0.00%

5.00%

10.00%

15.00%

20.00%

0 5 10 15 20

x (years)

lambda = 0.05

lambda = 0.10

Calibration on a 20Y-term swaptionCumulative vol of B(t, T+x) / B(t,T)

0.00%

5.00%

10.00%

15.00%

20.00%

25.00%

0 5 10 15 20

x (years)

lambda = 0.01

lambda = 0.10

176

LGM-1F model features

Effect of mean reversion on forward volatilitiesAssume that we have calibrated to the swaption (Tstart, Tend) (see below). Then the cumulative volatility of the model remains the same for any value of the mean reversion.

177

LGM-1F model features

But because of the exponential shape of the volatility, the forward volatility increases as the mean reversion increases. In the LGM-1F framework, the mean reversion controls the “repartition” of the volatility through time.