70

Prof. Ian Giddy New York University Estimating and Reducing The Cost of Capital DBS Bank

| Date post: | 20-Dec-2015 |

| Category: |

Documents |

| View: | 218 times |

| Download: | 1 times |

Prof. Ian GiddyNew York University

Estimating and ReducingThe Cost of Capital

DBS Bank

Copyright ©2000 Ian H. Giddy Cost of Capital 2

PT Astra International

?

Copyright ©2000 Ian H. Giddy Cost of Capital 3

New Equity for Astra

What investors?Portfolio investorsFinancial investorsCorporate investors

What returns should they expect?= Risk-free rate+ Corporate risk+ Financial risk (leverage/debt mismatch)+ “Agency cost” premium+ Country risk

What restructuring?

Copyright ©2000 Ian H. Giddy Cost of Capital 4

Measuring the Cost of Capital

Cost of funding equal return that investors expect

Expected returns depend on the risks investors face (risk must be taken in context)

Cost of capitalCost of equityCost of debtWeighted average (WACC)

Copyright ©2000 Ian H. Giddy Cost of Capital 5

A $1 Investment in Different Types of Portfolios: 1926-1996

0.1

1

10

100

1000

10000

1925 1935 1945 1955 1965 1975 1985 1995

Index ($)

$4,495.99

$33.73

$13.54$8.85

$1,370.95

Small Company Stocks

Large Company Stocks

Long-Term Government Bonds

Treasury BillsInflation Year-End

Copyright ©2000 Ian H. Giddy Cost of Capital 6

Equity Risk

The risk (variance) on any individual investment can be broken down into two sources. Some of the risk is specific to the firm, and is called firm-specific, whereas the rest of the risk is market wide and affects all investments.

The risk faced by a firm can be fall into the following categories – (1) Project-specific; an individual project may have higher or lower cash

flows than expected. (2) Competitive Risk, which is that the earnings and cash flows on a project

can be affected by the actions of competitors. (3) Industry-specific Risk, which covers factors that primarily impact the

earnings and cash flows of a specific industry. (4) International Risk, arising from having some cash flows in currencies

other than the one in which the earnings are measured and stock is priced (5) Market risk, which reflects the effect on earnings and cash flows of

macro economic factors that essentially affect all companies

Copyright ©2000 Ian H. Giddy Cost of Capital 7

Equity versus Bond Risk

Uncertain

value

of future

cash flows

Uncertain

value

of future

cash flows

Contractual int. & principal

No upside

Senior claims

Control via restrictions

Contractual int. & principal

No upside

Senior claims

Control via restrictions

Assets Liabilities

Debt

Residual payments

Upside and downside

Residual claims

Voting control rights

Residual payments

Upside and downside

Residual claims

Voting control rights

Equity

Copyright ©2000 Ian H. Giddy Cost of Capital 8

Corporate Cash Flow Valuation: The Steps

Estimate the discount rate or rates to use in the valuation Discount rate can be either a cost of equity (if doing equity

valuation) or a cost of capital (if valuing the firm) Discount rate can be in nominal terms or real terms, depending

upon whether the cash flows are nominal or real Discount rate can vary across time.

Estimate the current earnings and cash flows on the asset, to either equity investors (CF to Equity) or to all claimholders (CF to Firm)

Estimate the future earnings and cash flows on the asset being valued, generally by estimating an expected growth rate in earnings.

Estimate when the firm will reach “stable growth” and what characteristics (risk & cash flow) it will have when it does.

Choose the right DCF model for this asset and value it.

Copyright ©2000 Ian H. Giddy Cost of Capital 9

Cashflow to FirmEBIT (1-t)- (Cap Ex - Depr)- Change in WC= FCFF

Expected GrowthReinvestment Rate* Return on Capital

FCFF1 FCFF2 FCFF3 FCFF4 FCFF5

Forever

Firm is in stable growth:Grows at constant rateforever

Terminal Value= FCFF n+1/(r-gn)

FCFFn.........

Cost of Equity Cost of Debt(Riskfree Rate+ Default Spread) (1-t)

WeightsBased on Market Value

Discount at WACC= Cost of Equity (Equity/(Debt + Equity)) + Cost of Debt (Debt/(Debt+ Equity))

Value of Operating Assets+ Cash & Non-op Assets= Value of Firm- Value of Debt= Value of Equity

Riskfree Rate :- No default risk- No reinvestment risk- In same currency andin same terms (real or nominal as cash flows

+Beta- Measures market risk X

Risk Premium- Premium for averagerisk investment

Type of Business

Operating Leverage

FinancialLeverage

Base EquityPremium

Country RiskPremium

DISCOUNTED CASHFLOW VALUATION

Copyright ©2000 Ian H. Giddy Cost of Capital 10

Let’s Start With the Cost of Debt

The cost of debt is the market interest rate that the firm has to pay on its borrowing. It will depend upon three components-(a) The general level of interest rates(b) The default premium(c) The firm's tax rate

Copyright ©2000 Ian H. Giddy Cost of Capital 11

What the Cost of Debt Is and Is Not…

The cost of debt isthe rate at which the company can borrow

at todaycorrected for the tax benefit it gets for

interest payments.

Cost of debt =k

d = LT Borrowing Rate(1 - Tax rate)

The cost of debt is not the interest rate at which the company

obtained the debt it has on its books.

Copyright ©2000 Ian H. Giddy Cost of Capital 12

Estimating the Cost of Debt

If the firm has bonds outstanding, and the bonds are traded, the yield to maturity on a long-term, straight (no special features) bond can be used as the interest rate.

If the firm is rated, use the rating and a typical default spread on bonds with that rating to estimate the cost of debt.

If the firm is not rated, and it has recently borrowed long term from a bank, use the interest

rate on the borrowing or estimate a synthetic rating for the company, and use the synthetic

rating to arrive at a default spread and a cost of debt The cost of debt has to be estimated in the same currency as

the cost of equity and the cash flows in the valuation.

Copyright ©2000 Ian H. Giddy Cost of Capital 13

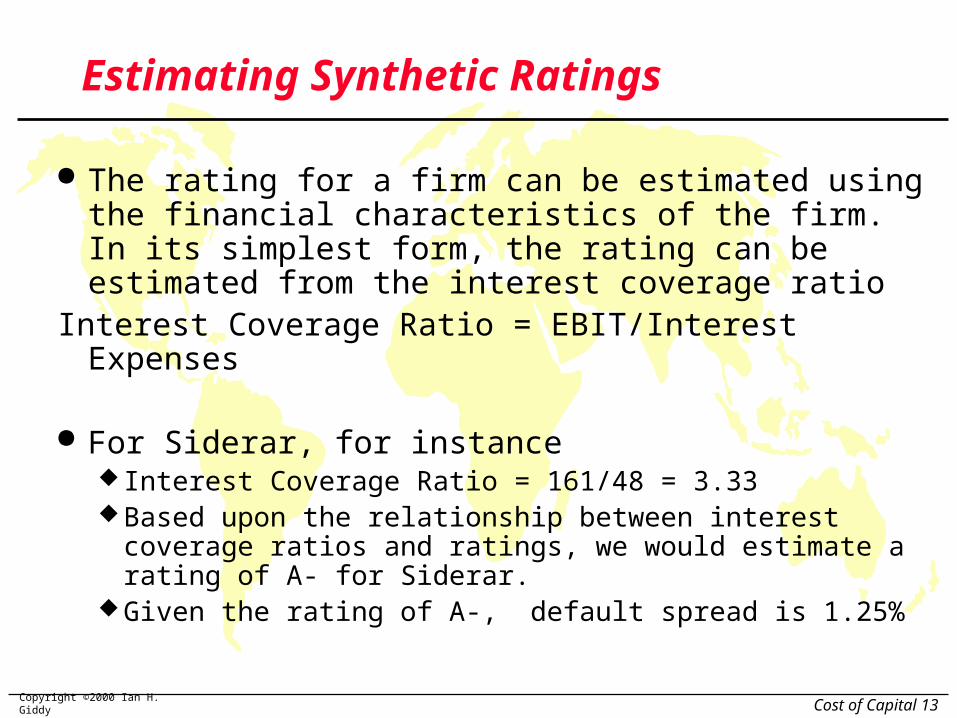

Estimating Synthetic Ratings

The rating for a firm can be estimated using the financial characteristics of the firm. In its simplest form, the rating can be estimated from the interest coverage ratio

Interest Coverage Ratio = EBIT/Interest Expenses

For Siderar, for instance Interest Coverage Ratio = 161/48 = 3.33Based upon the relationship between interest coverage

ratios and ratings, we would estimate a rating of A- for Siderar.

Given the rating of A-, default spread is 1.25%

Copyright ©2000 Ian H. Giddy Cost of Capital 14

Interest Coverage Ratios, Ratings and Default Spreads

If Interest Coverage Ratio is Estimated Bond Rating Default Spread

> 8.50 AAA 0.20%6.50 - 8.50 AA 0.50%5.50 - 6.50 A+ 0.80%4.25 - 5.50 A 1.00%3.00 - 4.25 A– 1.25%2.50 - 3.00 BBB 1.50%2.00 - 2.50 BB 2.00%1.75 - 2.00 B+ 2.50%1.50 - 1.75 B 3.25%1.25 - 1.50 B – 4.25%0.80 - 1.25 CCC 5.00%0.65 - 0.80 CC 6.00%0.20 - 0.65 C 7.50%< 0.20 D 10.00%

Copyright ©2000 Ian H. Giddy Cost of Capital 15

Other Factors Affecting RatiosMedians of Key Ratios : 1993-1995

AAA AA A BBB BB B CCCPretax Interest Coverage 13.50 9.67 5.76 3.94 2.14 1.51 0.96

EBITDA Interest Coverage 17.08 12.80 8.18 6.00 3.49 2.45 1.51Funds from Operations / Total Debt

(%) 98.2% 69.1% 45.5% 33.3% 17.7% 11.2% 6.7%

Free Operating Cashflow/ TotalDebt (%) 60.0% 26.8% 20.9% 7.2% 1.4% 1.2% 0.96%

Pretax Return on Permanent Capital(%) 29.3% 21.4% 19.1% 13.9% 12.0% 7.6% 5.2%

Operating Income/Sales (%) 22.6% 17.8% 15.7% 13.5% 13.5% 12.5% 12.2%Long Term Debt/ Capital 13.3% 21.1% 31.6% 42.7% 55.6% 62.2% 69.5%Total Debt/Capitalization 25.9% 33.6% 39.7% 47.8% 59.4% 67.4% 69.1%

AAA AA A BBB BB B CCCPretax Interest Coverage 13.50 9.67 5.76 3.94 2.14 1.51 0.96

EBITDA Interest Coverage 17.08 12.80 8.18 6.00 3.49 2.45 1.51Funds from Operations / Total Debt

(%) 98.2% 69.1% 45.5% 33.3% 17.7% 11.2% 6.7%

Free Operating Cashflow/ TotalDebt (%) 60.0% 26.8% 20.9% 7.2% 1.4% 1.2% 0.96%

Pretax Return on Permanent Capital(%) 29.3% 21.4% 19.1% 13.9% 12.0% 7.6% 5.2%

Operating Income/Sales (%) 22.6% 17.8% 15.7% 13.5% 13.5% 12.5% 12.2%Long Term Debt/ Capital 13.3% 21.1% 31.6% 42.7% 55.6% 62.2% 69.5%Total Debt/Capitalization 25.9% 33.6% 39.7% 47.8% 59.4% 67.4% 69.1%

Copyright ©2000 Ian H. Giddy Cost of Capital 16

Estimating Siderar’s Cost of Debt (in $)

Riskfree Rate = 6% Country default spread = 5.25% (Argentine

default spread) I am assuming that all Argentine companies have

to pay at least this spread. Rating for Siderar = A- Default spread = 1.25% Pre-tax cost of borrowing for first 5 years= 6%

+ 5.25% + 1.25% = 12.50% Pre-tax cost of borrowing after 5 years = 6%

+ 2.5% + 1.25% = 9.75%

Copyright ©2000 Ian H. Giddy Cost of Capital 17

The Cost of Equity

Equity is not free!

Expected return = Risk-free rate + Risk Premium

E(RRisky) = RRisk-free -+ Risk Premium

Copyright ©2000 Ian H. Giddy Cost of Capital 18

The Cost of Equity

Consider the standard approach to estimating cost of equity:

Cost of Equity = Rf + Equity Beta * (E(Rm) - Rf)where,

Rf = Riskfree rate

E(Rm) = Expected Return on the Market Index (Diversified Portfolio)

In practice, Short term government security rates are used as risk free rates Historical risk premiums are used for the risk premium Betas are estimated by regressing stock returns against market

returns

Copyright ©2000 Ian H. Giddy Cost of Capital 19

Private Business: Owner hasall his wealth invested in thebusiness

Venture Capitalist: Haswealth invested in a numberof companies in one sector

Publicly traded companywith investors who are diversified domesticallyorIPO to investors who aredomestically diversified

Publicly traded companywith investors who are diverisified globallyorIPO to global investors

Market Risk

Int’nl Risk

Sector Risk

Competitive Risk

Project Risk

Market Risk

Int’nl Risk

Sector Risk

Competitive Risk

Project Risk

Market Risk

Int’nl Risk

Sector Risk

Competitive Risk

Project Risk

Market Risk

Int’nl Risk

Sector Risk

Competitive Risk

Project Risk

TotalRisk

Risk added to sectorportfolio

Risk added to domestic portfolio

Risk added to global portfolio

StandardDeviation

Beta relative to sector

Beta relative to local index

Beta relative to global index

40%

25%

15%

10%

100/.4=250

100/.25=400

100/.15=667

100/.10=1000

Investor Type Cares about Risk Measure Cost ofEquity

Firm Value

Valuing a Firm from Different Risk PerspectivesFirm is assumed to have a cash flow of 100 each year forever.

Copyright ©2000 Ian H. Giddy Cost of Capital 20

Short Term Governments are Not Risk Free

On a riskfree asset, the actual return is equal to the expected return. Therefore, there is no variance around the expected return.

For an investment to be riskfree, then, it has to have No default risk No reinvestment risk

Match the duration of the analysis (generally long term) to the duration of the riskfree rate (also long term)

In emerging markets, there are two problems: The government might not be viewed as riskfree (Brazil,

Indonesia) There might be no market-based long term government rate

(China)

Copyright ©2000 Ian H. Giddy Cost of Capital 21

Estimating a Riskfree Rate

Estimate a range for the riskfree rate in local terms: Upper limit: Obtain the rate at which the largest, safest firms

in the country borrow at and use as the riskfree rate. Lower limit: Use a local bank deposit rate as the riskfree rate

Do the analysis in real terms (rather than nominal terms) using a real riskfree rate, which can be obtained in one of two ways – from an inflation-indexed government bond, if one exists set equal, approximately, to the long term real growth rate of

the economy in which the valuation is being done.

Do the analysis in another more stable currency, say US dollars.

Copyright ©2000 Ian H. Giddy Cost of Capital 22

Everyone uses historical premiums, but..

The historical premium is the premium that stocks have historically earned over riskless securities.

Practitioners never seem to agree on the premium; it is sensitive to How far back you go in history… Whether you use T.bill rates or T.Bond rates Whether you use geometric or arithmetic averages.

For instance, looking at the US:

Historical period Stocks - T.Bills Stocks - T.Bonds

Arith Geom Arith Geom

1926-1998 8.76% 6.95% 7.57% 5.91%

1962-1998 5.74% 4.63% 5.16% 4.46%

1981-1998 10.34% 9.72% 9.22% 8.02%

Copyright ©2000 Ian H. Giddy Cost of Capital 23

If you choose to use historical premiums….

Go back as far as you can. A risk premium comes with a standard error. Given the annual standard deviation in stock prices is about 25%, the standard error in a historical premium estimated over 25 years is roughly:

Standard Error in Premium = 25%/√25 = 25%/5 = 5% Be consistent in your use of the riskfree rate. Since we argued

for long term bond rates, the premium should be the one over TreasuryBonds

Use the geometric risk premium. It is closer to how investors think about risk premiums over long periods.

Never use historical risk premiums estimated over short periods.

For emerging markets, start with the base historical premium in the US and add a country spread, based upon the country rating and the relative equity market volatility.

Copyright ©2000 Ian H. Giddy Cost of Capital 24

Assessing Country Risk Using Currency Ratings: Latin America

Country Rating Default Spread over US T.Bond

Argentina Ba3 525Bolivia B1 600Brazil B2 750Chile Baa1 150Colombia Baa3 200Ecuador B3 850Paraguay B2 750Peru Ba3 525Uruguay Baa3 200Venezuela B2 750

Copyright ©2000 Ian H. Giddy Cost of Capital 25

Using Country Ratings to Estimate Equity Spreads Country ratings measure default risk. While default

risk premiums and equity risk premiums are highly correlated, one would expect equity spreads to be higher than debt spreads. One way to adjust the country spread upwards is to use

information from the US market. In the US, the equity risk premium has been roughly twice the default spread on junk bonds.

Another is to multiply the bond spread by the relative volatility of stock and bond prices in that market. For example,

Standard Deviation in Merval (Equity) = 42.87% Standard Deviation in Argentine Long Bond = 21.37% Adjusted Equity Spread = 5.25% (42.87/21.37) = 10.53%

Ratings agencies make mistakes. They are often late in recognizing and building in risk.

Copyright ©2000 Ian H. Giddy Cost of Capital 26

Ratings Errors: Ratings for Asia

Country July 1997 Rating January 1998 RatingsChina BBB+ BBB+Indonesia BBB CCC+India BB+ BB+ Japan AAA AAASouth Korea AA- BB+ Malaysia A+ A- Pakistan B+ B-Philippines BB+ BB+Singapore AAA AAATaiwan AA+ AA+Thailand A BBB-

Copyright ©2000 Ian H. Giddy Cost of Capital 27

From Country Spreads to Risk Premiums

Approach 1: Assume that every company in the country is equally exposed to country risk. In this case,

E(Return) = Riskfree Rate + Country Spread + Beta (US premium)Implicitly, this is what you are assuming when you use the local

Government’s dollar borrowing rate as your riskfree rate. Approach 2: Assume that a company’s exposure to country risk

is similar to its exposure to other market risk.

E(Return) = Riskfree Rate + Beta (US premium + Country Spread) Approach 3: Treat country risk as a separate risk factor and

allow firms to have different exposures to country risk (perhaps based upon the proportion of their revenues come from non-domestic sales)

E(Return)=Riskfree Rate+ (US premium) + Country Spread)

Copyright ©2000 Ian H. Giddy Cost of Capital 28

Estimating Exposure to Country Risk

Different companies should be exposed to different degrees to country risk. For instance, an Argentinan firm that generates the bulk of its revenues in North America should be less exposed to country risk in Argentina than one that generates all its business within Argentina.

The factor “” measures the relative exposure of a firm to country risk. One simplistic solution would be to do the following:

% of revenues domesticallyfirm/ % of revenues domesticallyavg

firm

For instance, if a firm gets 35% of its revenues domestically while the average firm in that market gets 70% of its revenues domestically

35%/ 70 % = 0.5 There are two implications

A company’s risk exposure is determined by where it does business and not by where it is located

Firms might be able to actively manage their country risk exposures

Copyright ©2000 Ian H. Giddy Cost of Capital 29

Estimating E(Return) for Siderar

Assume that the beta for Siderar is 0.71, and that the riskfree rate used is 6.00%. (US Long Term Bond rate)

Approach 1: Assume that every company in the country is equally exposed to country risk. In this case,

E(Return) = 6.00% + 10.53% + 0.71 (5.5%) = 20.44% Approach 2: Assume that a company’s exposure to country risk

is similar to its exposure to other market risk.E(Return) = 6.00% + 0.71 (5.5%+ 10.53%) = 17.38% Approach 3: Treat country risk as a separate risk factor and

allow firms to have different exposures to country risk (perhaps based upon the proportion of their revenues come from non-domestic sales)

E(Return)=6.00% + (5.5%) + 10.53%) = 21.49%In 1998, Siderar got 76.3% of its revenues from Argentina. The

average across all Argentinan firms is closer to 70%.

Copyright ©2000 Ian H. Giddy Cost of Capital 30

Estimating Beta

The standard procedure for estimating betas is to regress stock returns (Rj) against market returns (Rm) -

Rj = a + b Rm

where a is the intercept and b is the slope of the regression. The slope of the regression corresponds to the beta

of the stock, and measures the riskiness of the stock. This beta has three problems:

It has high standard error It reflects the firm’s business mix over the period of the

regression, not the current mix It reflects the firm’s average financial leverage over the

period rather than the current leverage.

Copyright ©2000 Ian H. Giddy Cost of Capital 31

Beta Estimation: The Old Fashioned Way

Copyright ©2000 Ian H. Giddy Cost of Capital 32

Determinants of Betas

Product or Service: The beta value for a firm depends upon the sensitivity of the demand for its products and services and of its costs to macroeconomic factors that affect the overall market. Cyclical companies have higher betas than non-cyclical firms Firms which sell more discretionary products will have higher betas

than firms that sell less discretionary products Operating Leverage: The greater the proportion of fixed costs

in the cost structure of a business, the higher the beta will be of that business. This is because higher fixed costs increase your exposure to all risk, including market risk.

Financial Leverage: The more debt a firm takes on, the higher the beta will be of the equity in that business. Debt creates a fixed cost, interest expenses, that increases exposure to market risk.

Copyright ©2000 Ian H. Giddy Cost of Capital 33

•Business Risk

Consider an investment in Tiffany’s. What kind of beta do you think this investment will have?

Much higher than one Close to one Much lower than one

Copyright ©2000 Ian H. Giddy Cost of Capital 34

•Measures of Operating Leverage

Fixed Costs Measure = Fixed Costs / Variable Costs

This measures the relationship between fixed and variable costs. The higher the proportion, the higher the operating leverage.

EBIT Variability Measure = % Change in EBIT / % Change in Revenues

This measures how quickly the earnings before interest and taxes changes as revenue changes. The higher this number, the greater the operating leverage.

Copyright ©2000 Ian H. Giddy Cost of Capital 35

•Equity Betas and Leverage

The beta of equity alone can be written as a function of the unlevered beta and the debt-equity ratio

L =

u (1+ ((1-t)D/E)

where

L = Levered or Equity Beta

u = Unlevered Beta

t = Corporate marginal tax rateD = Market Value of DebtE = Market Value of Equity

While this beta is estimated on the assumption that debt carries no market risk (and has a beta of zero), you can have a modified version:

L =

u (1+ ((1-t)D/E) -

debt (1-t) D/(D+E)

Copyright ©2000 Ian H. Giddy Cost of Capital 36

Solutions to the Regression Beta Problem

Modify the regression beta by changing the index used to estimate the beta adjusting the regression beta estimate, by bringing in information

about the fundamentals of the company Estimate the beta for the firm using

the standard deviation in stock prices instead of a regression against an index.

accounting earnings or revenues, which are less noisy than market prices.

Estimate the beta for the firm from the bottom up without employing the regression technique. This will require understanding the business mix of the firm estimating the financial leverage of the firm

Use an alternative measure of market risk that does not need a regression.

Copyright ©2000 Ian H. Giddy Cost of Capital 37

The Solution: Bottom-up Betas

The bottom up beta can be estimated by : Taking a weighted (by sales or operating income) average of the

unlevered betas of the different businesses a firm is in.

(The unlevered beta of a business can be estimated by looking at other firms in the same business)

Lever up using the firm’s debt/equity ratio

The bottom up beta will give you a better estimate of the true beta when It has lower standard error (SEaverage = SEfirm / √n (n = number of

firms) It reflects the firm’s current business mix and financial leverage It can be estimated for divisions and private firms.

j

j 1

j k

Operating Income j

Operating Income Firm

levered unlevered 1 (1 tax rate) (Current Debt/Equity Ratio)

Copyright ©2000 Ian H. Giddy Cost of Capital 38

Siderar’s Bottom-up Beta

Business Unlevered D/E Ratio Levered Riskfree Risk Cost of

Beta Beta Rate Premium Equity

Steel 0.68 5.97% 0.71 6.00% 16.03% 17.38%

Proportion of operating income from steel = 100%

Levered Beta for Siderar= 0.71

Assume now that Siderar decides to go into the retailing business, and that the unlevered beta for that business is 1.15. Assuming that 25% of Siderar’s business looking forward will come from this business, what will the firm’s beta be?

Copyright ©2000 Ian H. Giddy Cost of Capital 39

The Weighted Average Cost of Capital

The weights used to compute the cost of capital should be the market value weights for debt and equity.

There is an element of circularity that is introduced into every valuation by doing this, since the values that we attach to the firm and equity at the end of the analysis are different from the values we gave them at the beginning.

As a general rule, the debt that you should subtract from firm value to arrive at the value of equity should be the same debt that you used to compute the cost of capital.

Copyright ©2000 Ian H. Giddy Cost of Capital 40

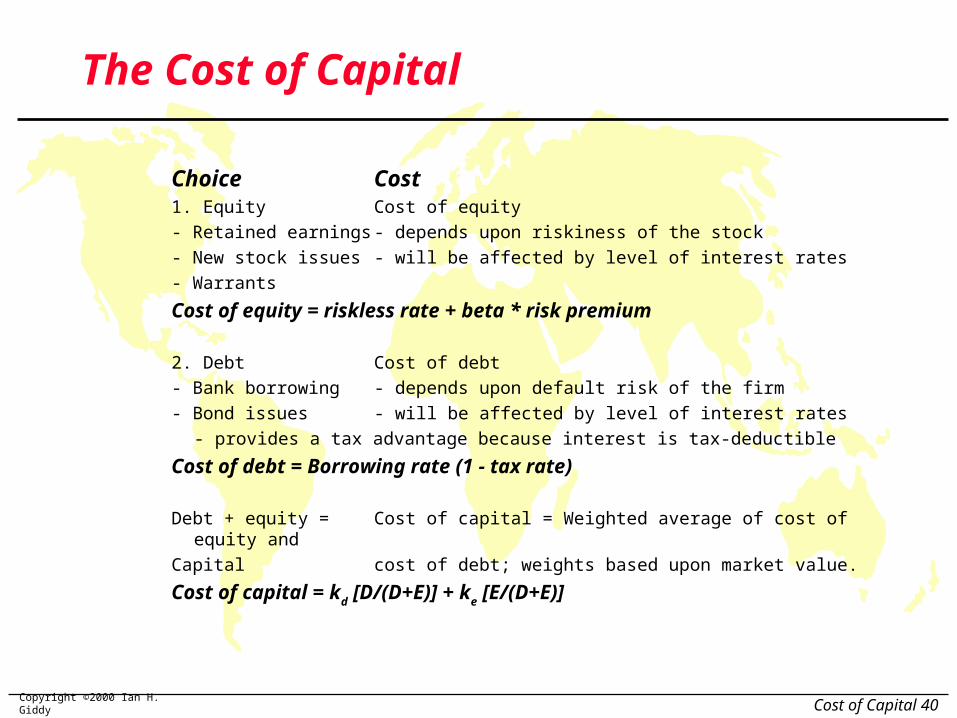

The Cost of Capital

Choice Cost1. Equity Cost of equity

- Retained earnings - depends upon riskiness of the stock

- New stock issues - will be affected by level of interest rates

- Warrants

Cost of equity = riskless rate + beta * risk premium

2. Debt Cost of debt

- Bank borrowing - depends upon default risk of the firm

- Bond issues - will be affected by level of interest rates

- provides a tax advantage because interest is tax-deductible

Cost of debt = Borrowing rate (1 - tax rate)

Debt + equity = Cost of capital = Weighted average of cost of equity and

Capital cost of debt; weights based upon market value.

Cost of capital = kd [D/(D+E)] + ke [E/(D+E)]

Copyright ©2000 Ian H. Giddy Cost of Capital 41

Estimating Cost of Capital: Siderar

EquityCost of Equity = 6.00% + 0.71 (16.03%) = 17.38%Market Value of Equity = 3.20* 310.89 = 995 million

(94.37%) Debt

Cost of debt = 6.00% + 5.25% + 1.25% (default spread) = 12.5%

Market Value of Debt = 59 Mil (5.63%) Cost of CapitalCost of Capital = 17.38%(.9437) + 12.5%(1-.3345)(.0563))

= 17.38%(.9437) + 8.32%(.0563) = 16.87%

Copyright ©2000 Ian H. Giddy Cost of Capital 42

Next, Minimize the Cost of Capital by Changing the Financial Mix

The first step in reducing the cost of capital is to change the mix of debt and equity used to finance the firm.

Debt is always cheaper than equity, partly because it lenders bear less risk and partly because of the tax advantage associated with debt.

But taking on debt increases the risk (and the cost) of both debt (by increasing the probability of bankruptcy) and equity (by making earnings to equity investors more volatile).

The net effect will determine whether the cost of capital will increase or decrease if the firm takes on more or less debt.

Copyright ©2000 Ian H. Giddy Cost of Capital 43

This is What We’re Trying to Do

D/(D+E) ke kd After-tax Cost of Debt WACC

0 10.50% 8% 4.80% 10.50%

10% 11% 8.50% 5.10% 10.41%

20% 11.60% 9.00% 5.40% 10.36%

30% 12.30% 9.00% 5.40% 10.23%

40% 13.10% 9.50% 5.70% 10.14%

50% 14% 10.50% 6.30% 10.15%

60% 15% 12% 7.20% 10.32%

70% 16.10% 13.50% 8.10% 10.50%

80% 17.20% 15% 9.00% 10.64%

90% 18.40% 17% 10.20% 11.02%

100% 19.70% 19% 11.40% 11.40%

D/(D+E) ke kd After-tax Cost of Debt WACC

0 10.50% 8% 4.80% 10.50%

10% 11% 8.50% 5.10% 10.41%

20% 11.60% 9.00% 5.40% 10.36%

30% 12.30% 9.00% 5.40% 10.23%

40% 13.10% 9.50% 5.70% 10.14%

50% 14% 10.50% 6.30% 10.15%

60% 15% 12% 7.20% 10.32%

70% 16.10% 13.50% 8.10% 10.50%

80% 17.20% 15% 9.00% 10.64%

90% 18.40% 17% 10.20% 11.02%

100% 19.70% 19% 11.40% 11.40%

Copyright ©2000 Ian H. Giddy Cost of Capital 44

Cost of Capital and Leverage: Method

Estimated Beta

With current leverage

From regression

Unlevered Beta

With no leverage

Bu=Bl/(1+D/E(1-T))

Levered Beta

With different leverage

Bl=Bu(1+D/E(1-T))

Cost of equity

With different leverage

E(R)=Rf+Bl(Rm-Rf)

Equity

Leverage, EBITDA

And interest cost

Interest Coverage

EBITDA/Interest

Rating

(other factors too!)

Cost of debt

With different leverage

Rate=Rf+Spread+?

Debt

Copyright ©2000 Ian H. Giddy Cost of Capital 45

Siderar: Optimal Debt Ratio

Debt Ratio Beta Cost of Equity Bond Rating Interest rate on debt Tax Rate Cost of Debt (after-tax) WACC Firm Value (G)0% 0.68 16.95% AAA 11.55% 33.45% 7.69% 16.95% $1,046

10% 0.73 17.76% AA 11.95% 33.45% 7.95% 16.78% $1,06420% 0.80 18.77% A- 12.75% 33.45% 8.49% 16.71% $1,07130% 0.88 20.07% B+ 14.25% 33.45% 9.48% 16.90% $1,05240% 0.99 21.81% B- 16.25% 33.45% 10.81% 17.41% $1,00150% 1.14 24.24% CCC 17.25% 33.45% 11.48% 17.86% $96160% 1.44 29.16% CC 18.75% 25.67% 13.94% 20.02% $80370% 1.95 37.29% C 20.25% 20.38% 16.12% 22.47% $67480% 2.93 52.94% C 20.25% 17.83% 16.64% 23.90% $61590% 5.86 99.87% C 20.25% 15.85% 17.04% 25.32% $565

Question: If Siderar’s current debt ratio is 60%, what do you recommend?

Copyright ©2000 Ian H. Giddy Cost of Capital 46

Siderar: Optimal Debt Ratio

Debt Ratio Beta Cost of Equity Bond Rating Interest rate on debt Tax Rate Cost of Debt (after-tax) WACC Firm Value (G)0% 0.68 16.95% AAA 11.55% 33.45% 7.69% 16.95% $1,046

10% 0.73 17.76% AA 11.95% 33.45% 7.95% 16.78% $1,06420% 0.80 18.77% A- 12.75% 33.45% 8.49% 16.71% $1,07130% 0.88 20.07% B+ 14.25% 33.45% 9.48% 16.90% $1,05240% 0.99 21.81% B- 16.25% 33.45% 10.81% 17.41% $1,00150% 1.14 24.24% CCC 17.25% 33.45% 11.48% 17.86% $96160% 1.44 29.16% CC 18.75% 25.67% 13.94% 20.02% $80370% 1.95 37.29% C 20.25% 20.38% 16.12% 22.47% $67480% 2.93 52.94% C 20.25% 17.83% 16.64% 23.90% $61590% 5.86 99.87% C 20.25% 15.85% 17.04% 25.32% $565

0

200

400

600

800

1000

1200

0% 20% 40% 60% 80% 100%

Debt Percentage

Va

lue

($

mil

lio

ns

)

0.00%

5.00%

10.00%

15.00%

20.00%

25.00%

30.00%

0% 20% 40% 60% 80% 100%

Debt Percentage

Co

st

of

Ca

pit

al

Copyright ©2000 Ian H. Giddy Cost of Capital 47

Case Study: Nokia 2000

Copyright ©2000 Ian H. Giddy Cost of Capital 48

A Framework for Getting to the Optimal

Is the actual debt ratio greater than or lesser than the optimal debt ratio?

Actual > OptimalOverlevered

Actual < OptimalUnderlevered

Is the firm under bankruptcy threat? Is the firm a takeover target?

Yes No

Reduce Debt quickly1. Equity for Debt swap2. Sell Assets; use cashto pay off debt3. Renegotiate with lenders

Does the firm have good projects?ROE > Cost of EquityROC > Cost of Capital

YesTake good projects withnew equity or with retainedearnings.

No1. Pay off debt with retainedearnings.2. Reduce or eliminate dividends.3. Issue new equity and pay off debt.

Yes No

Does the firm have good projects?ROE > Cost of EquityROC > Cost of Capital

YesTake good projects withdebt.

No

Do your stockholders likedividends?

YesPay Dividends No

Buy back stock

Increase leveragequickly1. Debt/Equity swaps2. Borrow money&buy shares.

Copyright ©2000 Ian H. Giddy Cost of Capital 52

AppendixMinimizing the Cost of Capital: Example

Weighted Average Cost of Capital and Debt Ratios

Debt Ratio

WA

CC

9.40%9.60%9.80%

10.00%10.20%10.40%10.60%10.80%11.00%11.20%11.40%

0

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Copyright ©2000 Ian H. Giddy Cost of Capital 53

Optimum Capital Structure and Cost of Capital

If the cash flows to the firm are held constant, and the cost of capital is minimized, the value of the firm will be maximized.

Copyright ©2000 Ian H. Giddy Cost of Capital 54

Applying Approach: The Textbook Example

D/(D+E) ke kd After-tax Cost of Debt WACC

0 10.50% 8% 4.80% 10.50%

10% 11% 8.50% 5.10% 10.41%

20% 11.60% 9.00% 5.40% 10.36%

30% 12.30% 9.00% 5.40% 10.23%

40% 13.10% 9.50% 5.70% 10.14%

50% 14% 10.50% 6.30% 10.15%

60% 15% 12% 7.20% 10.32%

70% 16.10% 13.50% 8.10% 10.50%

80% 17.20% 15% 9.00% 10.64%

90% 18.40% 17% 10.20% 11.02%

100% 19.70% 19% 11.40% 11.40%

D/(D+E) ke kd After-tax Cost of Debt WACC

0 10.50% 8% 4.80% 10.50%

10% 11% 8.50% 5.10% 10.41%

20% 11.60% 9.00% 5.40% 10.36%

30% 12.30% 9.00% 5.40% 10.23%

40% 13.10% 9.50% 5.70% 10.14%

50% 14% 10.50% 6.30% 10.15%

60% 15% 12% 7.20% 10.32%

70% 16.10% 13.50% 8.10% 10.50%

80% 17.20% 15% 9.00% 10.64%

90% 18.40% 17% 10.20% 11.02%

100% 19.70% 19% 11.40% 11.40%

Copyright ©2000 Ian H. Giddy Cost of Capital 55

WACC and Debt Ratios

Weighted Average Cost of Capital and Debt Ratios

Debt Ratio

WA

CC

9.40%9.60%9.80%

10.00%10.20%10.40%10.60%10.80%11.00%11.20%11.40%

0

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Copyright ©2000 Ian H. Giddy Cost of Capital 56

Current Cost of Capital: Disney

Equity Cost of Equity = 13.85% Market Value of Equity = $50.88 Billion Equity/(Debt+Equity ) = 82%

Debt After-tax Cost of debt = 7.50% (1-.36) = 4.80% Market Value of Debt = $ 11.18 Billion Debt/(Debt +Equity) = 18%

Cost of Capital = 13.85%(.82)+4.80%(.18) = 12.22%

Copyright ©2000 Ian H. Giddy Cost of Capital 57

Mechanics of Cost of Capital Estimation

1. Estimate the Cost of Equity at different levels of debt: Equity will become riskier -> Beta will increase -> Cost of

Equity will increase.

Estimation will use levered beta calculation

2. Estimate the Cost of Debt at different levels of debt: Default risk will go up and bond ratings will go down as debt

goes up -> Cost of Debt will increase.

To estimating bond ratings, we will use the interest coverage ratio (EBIT/Interest expense)

3. Estimate the Cost of Capital at different levels of debt

4. Calculate the effect on Firm Value and Stock Price.

Copyright ©2000 Ian H. Giddy Cost of Capital 58

Medians of Key Ratios : 1993-1995

AAA AA A BBB BB B CCCPretax Interest Coverage 13.50 9.67 5.76 3.94 2.14 1.51 0.96

EBITDA Interest Coverage 17.08 12.80 8.18 6.00 3.49 2.45 1.51Funds from Operations / Total Debt

(%) 98.2% 69.1% 45.5% 33.3% 17.7% 11.2% 6.7%

Free Operating Cashflow/ TotalDebt (%) 60.0% 26.8% 20.9% 7.2% 1.4% 1.2% 0.96%

Pretax Return on Permanent Capital(%) 29.3% 21.4% 19.1% 13.9% 12.0% 7.6% 5.2%

Operating Income/Sales (%) 22.6% 17.8% 15.7% 13.5% 13.5% 12.5% 12.2%Long Term Debt/ Capital 13.3% 21.1% 31.6% 42.7% 55.6% 62.2% 69.5%Total Debt/Capitalization 25.9% 33.6% 39.7% 47.8% 59.4% 67.4% 69.1%

AAA AA A BBB BB B CCCPretax Interest Coverage 13.50 9.67 5.76 3.94 2.14 1.51 0.96

EBITDA Interest Coverage 17.08 12.80 8.18 6.00 3.49 2.45 1.51Funds from Operations / Total Debt

(%) 98.2% 69.1% 45.5% 33.3% 17.7% 11.2% 6.7%

Free Operating Cashflow/ TotalDebt (%) 60.0% 26.8% 20.9% 7.2% 1.4% 1.2% 0.96%

Pretax Return on Permanent Capital(%) 29.3% 21.4% 19.1% 13.9% 12.0% 7.6% 5.2%

Operating Income/Sales (%) 22.6% 17.8% 15.7% 13.5% 13.5% 12.5% 12.2%Long Term Debt/ Capital 13.3% 21.1% 31.6% 42.7% 55.6% 62.2% 69.5%Total Debt/Capitalization 25.9% 33.6% 39.7% 47.8% 59.4% 67.4% 69.1%

Copyright ©2000 Ian H. Giddy Cost of Capital 59

Process of Ratings and Rate Estimation

We use the median interest coverage ratios for large manufacturing firms to develop “interest coverage ratio” ranges for each rating class.

We then estimate a spread over the long term bond rate for each ratings class, based upon yields at which these bonds trade in the market place.

Copyright ©2000 Ian H. Giddy Cost of Capital 60

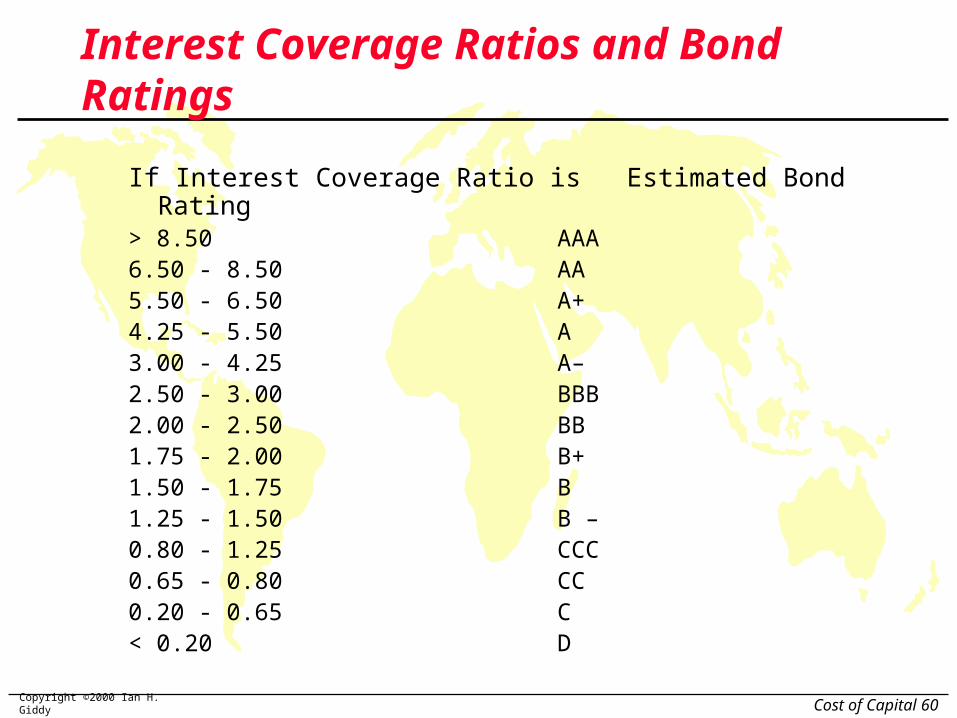

Interest Coverage Ratios and Bond Ratings

If Interest Coverage Ratio is Estimated Bond Rating> 8.50 AAA6.50 - 8.50 AA5.50 - 6.50 A+4.25 - 5.50 A3.00 - 4.25 A–2.50 - 3.00 BBB2.00 - 2.50 BB1.75 - 2.00 B+1.50 - 1.75 B1.25 - 1.50 B –0.80 - 1.25 CCC0.65 - 0.80 CC0.20 - 0.65 C< 0.20 D

Copyright ©2000 Ian H. Giddy Cost of Capital 61

Spreads Over Long Bond Rate for Ratings Classes

Rating Coverage gtSpreadAAA 0.20%AA 0.50%A+ 0.80%A 1.00%A- 1.25%BBB 1.50%BB 2.00%B+ 2.50%B 3.25%B- 4.25%CCC 5.00%CC 6.00%C 7.50%D 10.00%

Rating Coverage gtSpreadAAA 0.20%AA 0.50%A+ 0.80%A 1.00%A- 1.25%BBB 1.50%BB 2.00%B+ 2.50%B 3.25%B- 4.25%CCC 5.00%CC 6.00%C 7.50%D 10.00%

Copyright ©2000 Ian H. Giddy Cost of Capital 62

Current Income Statement for Disney: 1996

Revenues 18,739

-Operating Expenses 12,046

EBITDA 6,693

-Depreciation 1,134

EBIT 5,559

-Interest Expense 479

Income before taxes 5,080

-Taxes 847

Income after taxes 4,233 Interest coverage ratio= 5,559/479 = 11.61

(Amortization from Capital Cities acquisition not considered)

Copyright ©2000 Ian H. Giddy Cost of Capital 63

Estimating Cost of Equity

Current Beta = 1.25 Unlevered Beta = 1.09

Market premium = 5.5% T.Bond Rate = 7.00% t=36%Debt Ratio D/E Ratio Beta Cost of Equity

0% 0% 1.09 13.00%

10% 11% 1.17 13.43%

20% 25% 1.27 13.96%

30% 43% 1.39 14.65%

40% 67% 1.56 15.56%

50% 100% 1.79 16.85%

60% 150% 2.14 18.77%

70% 233% 2.72 21.97%

80% 400% 3.99 28.95%

90% 900% 8.21 52.14%

Copyright ©2000 Ian H. Giddy Cost of Capital 64

Disney: Beta, Cost of Equity and D/E Ratio

0.00

1.00

2.00

3.00

4.00

5.00

6.00

7.00

8.00

9.00

0% 10% 20% 30% 40% 50% 60% 70% 80% 90%

Debt Ratio

Be

ta

0.00%

10.00%

20.00%

30.00%

40.00%

50.00%

60.00%

Co

st

of

Eq

uit

y

BetaCost of Equity

Copyright ©2000 Ian H. Giddy Cost of Capital 65

Estimating Cost of Debt

D/(D+E) 0.00% 10.00% Calculation Details StepD/E 0.00% 11.11% = [D/(D+E)]/( 1 -[D/(D+E)])$ Debt $0 $6,207 = [D/(D+E)]* Firm Value 1

EBITDA $6,693 $6,693 Kept constant as debt changes.

Depreciation $1,134 $1,134 "EBIT $5,559 $5,559Interest $0 $447 = Interest Rate * $ Debt 2Taxable Income $5,559 $5,112 = OI - Depreciation - InterestTax $2,001 $1,840 = Tax Rate * Taxable IncomeNet Income $3,558 $3,272 = Taxable Income - Tax

Pre-tax Int. cov ∞ 12.44 = (OI - Deprec'n)/Int. Exp 3Likely Rating AAA AAA Based upon interest coverage 4Interest Rate 7.20% 7.20% Interest rate for given rating 5Eff. Tax Rate 36.00% 36.00% See notes on effective tax rate

After-tax kd 4.61% 4.61% =Interest Rate * (1 - Tax Rate)

Firm Value = 50,888+11,180= $62,068

Copyright ©2000 Ian H. Giddy Cost of Capital 66

The Ratings Table

If Interest Coverage Ratio is Estimated Bond Rating> 8.50 AAA

6.50 - 8.50 AA

5.50 - 6.50 A+

4.25 - 5.50 A

3.00 - 4.25 A–

2.50 - 3.00 BBB

2.00 - 2.50 BB

1.75 - 2.00 B+

1.50 - 1.75 B

1.25 - 1.50 B –

0.80 - 1.25 CCC

0.65 - 0.80 CC

0.20 - 0.65 C

< 0.20 D

Copyright ©2000 Ian H. Giddy Cost of Capital 67

Bond Ratings, Cost of Debt and Debt Ratios

WORKSHEET FOR ESTIMATING RATINGS/INTEREST RATESD/(D+E) 0.00% 10.00% 20.00% 30.00% 40.00% 50.00% 60.00% 70.00% 80.00% 90.00%D/E 0.00% 11.11% 25.00% 42.86% 66.67% 100.00% 150.00% 233.33% 400.00% 900.00%$ Debt $0 $6,207 $12,414 $18,621 $24,827 $31,034 $37,241 $43,448 $49,655 $55,862Operating Inc. $6,693 $6,693 $6,693 $6,693 $6,693 $6,693 $6,693 $6,693 $6,693 $6,693Depreciation $1,134 $1,134 $1,134 $1,134 $1,134 $1,134 $1,134 $1,134 $1,134 $1,134Interest $0 $447 $968 $1,536 $2,234 $3,181 $4,469 $5,214 $5,959 $7,262Taxable Income $5,559 $5,112 $4,591 $4,023 $3,325 $2,378 $1,090 $345 ($400) ($1,703)Tax $2,001 $1,840 $1,653 $1,448 $1,197 $856 $392 $124 ($144) ($613)Net Income $3,558 $3,272 $2,938 $2,575 $2,128 $1,522 $698 $221 ($256) ($1,090)Pre-tax Int. cov 12.44 5.74 3.62 2.49 1.75 1.24 1.07 0.93 0.77Likely Rating AAA AAA A+ A- BB B CCC CCC CCC CCInterest Rate 7.20% 7.20% 7.80% 8.25% 9.00% 10.25% 12.00% 12.00% 12.00% 13.00%Eff. Tax Rate 36.00% 36.00% 36.00% 36.00% 36.00% 36.00% 36.00% 36.00% 33.59% 27.56%Cost of debt 4.61% 4.61% 4.99% 5.28% 5.76% 6.56% 7.68% 7.68% 7.97% 9.42%

WORKSHEET FOR ESTIMATING RATINGS/INTEREST RATESD/(D+E) 0.00% 10.00% 20.00% 30.00% 40.00% 50.00% 60.00% 70.00% 80.00% 90.00%D/E 0.00% 11.11% 25.00% 42.86% 66.67% 100.00% 150.00% 233.33% 400.00% 900.00%$ Debt $0 $6,207 $12,414 $18,621 $24,827 $31,034 $37,241 $43,448 $49,655 $55,862Operating Inc. $6,693 $6,693 $6,693 $6,693 $6,693 $6,693 $6,693 $6,693 $6,693 $6,693Depreciation $1,134 $1,134 $1,134 $1,134 $1,134 $1,134 $1,134 $1,134 $1,134 $1,134Interest $0 $447 $968 $1,536 $2,234 $3,181 $4,469 $5,214 $5,959 $7,262Taxable Income $5,559 $5,112 $4,591 $4,023 $3,325 $2,378 $1,090 $345 ($400) ($1,703)Tax $2,001 $1,840 $1,653 $1,448 $1,197 $856 $392 $124 ($144) ($613)Net Income $3,558 $3,272 $2,938 $2,575 $2,128 $1,522 $698 $221 ($256) ($1,090)Pre-tax Int. cov 12.44 5.74 3.62 2.49 1.75 1.24 1.07 0.93 0.77Likely Rating AAA AAA A+ A- BB B CCC CCC CCC CCInterest Rate 7.20% 7.20% 7.80% 8.25% 9.00% 10.25% 12.00% 12.00% 12.00% 13.00%Eff. Tax Rate 36.00% 36.00% 36.00% 36.00% 36.00% 36.00% 36.00% 36.00% 33.59% 27.56%Cost of debt 4.61% 4.61% 4.99% 5.28% 5.76% 6.56% 7.68% 7.68% 7.97% 9.42%

Copyright ©2000 Ian H. Giddy Cost of Capital 68

Stated versus Effective Tax Rates

You need taxable income for interest to provide a tax savings In the Disney case, consider the interest expense at 70% and

80%70% Debt Ratio 80% Debt Ratio

EBIT $ 5,559 m $ 5,559 m

Interest Expense $ 5,214 m $ 5,959 m

Tax Savings $ 1,866 m $ 2,001m

Effective Tax Rate 36.00% 2001/5959 = 33.59%

Pre-tax interest rate 12.00% 12.00%

After-tax Interest Rate 7.68% 7.97% You can deduct only $5,559million of the $5,959 million of the

interest expense at 80%. Therefore, only 36% of $ 5,559 is considered as the tax savings.

Copyright ©2000 Ian H. Giddy Cost of Capital 69

Cost of Debt

0.00%

2.00%

4.00%

6.00%

8.00%

10.00%

12.00%

14.00%

0% 10% 20% 30% 40% 50% 60% 70% 80% 90%

Debt Ratio

Cos

t of D

ebt

Interest RateAT Cost of Debt

Copyright ©2000 Ian H. Giddy Cost of Capital 70

Disney’s Cost of Capital Schedule

Debt Ratio Cost of Equity AT Cost of Debt Cost of Capital

0.00% 13.00% 4.61% 13.00%

10.00% 13.43% 4.61% 12.55%

20.00% 13.96% 4.99% 12.17%

30.00% 14.65% 5.28% 11.84%

40.00% 15.56% 5.76% 11.64%

50.00% 16.85% 6.56% 11.70%

60.00% 18.77% 7.68% 12.11%

70.00% 21.97% 7.68% 11.97%

80.00% 28.95% 7.97% 12.17%

90.00% 52.14% 9.42% 13.69%

Copyright ©2000 Ian H. Giddy Cost of Capital 71

Disney: Cost of Capital Chart

10.50%

11.00%

11.50%

12.00%

12.50%

13.00%

13.50%

14.00%

0.00

%

10.00%

20.00%

30.00%

40.00%

50.00%

60.00%

70.00%

80.00%

90.00%

Debt Ratio

Cos

t of C

apita

l

Cost of Capital

Copyright ©2000 Ian H. Giddy Cost of Capital 72

Effect on Firm Value

Firm Value before the change = 50,888+11,180= $ 62,068WACCb = 12.22% Annual Cost = $62,068 *12.22%= $7,583 million

WACCa = 11.64% Annual Cost = $62,068 *11.64% = $7,226 million

WACC = 0.58% Change in Annual Cost = $ 357 million If there is no growth in the firm value, (Conservative Estimate)

Increase in firm value = $357 / .1164 = $3,065 million Change in Stock Price = $3,065/675.13= $4.54 per share

If there is growth (of 7.13%) in firm value over time, Increase in firm value = $357 * 1.0713 /(.1164-.0713) = $ 8,474 Change in Stock Price = $8,474/675.13 = $12.55 per share

Implied Growth Rate obtained by

Firm value Today =FCFF(1+g)/(WACC-g): Perpetual growth formula

$62,068 = $3,222(1+g)/(.1222-g): Solve for g

Copyright ©2000 Ian H. Giddy Cost of Capital 73

www.giddy.org

Ian Giddy

NYU Stern School of Business

Tel 212-998-0332; Fax 212-995-4233

http://www.giddy.org