41

Profitability and Ownership Structure of US Foreign Ventures Why US Joint Ventures Abroad Are Less Profitable Than Wholly Owned Ventures Ben Gomes-Casseres Mauricio Jenkins Peter ZÆmborsk

Profita

bili

ty a

nd O

wner

ship

Str

uct

ure

of U

S F

ore

ign V

entu

res

Wh

y U

S J

oin

t V

en

ture

s A

bro

ad

Are

Less

P

rofi

tab

le T

han

Wh

olly O

wn

ed

Ven

ture

s

Ben

Gom

es-C

asse

res

Mau

rici

o J

enki

ns

Pet

er Z

ámbors

ký

Low

pro

fita

bili

ty o

f U

S J

Vs

abro

ad

!U

S m

anufa

cturi

ng join

t ve

ntu

res

abro

ad e

arned

an a

vera

ge

3%

ret

urn

on a

sset

s in

1977-2

003

!W

holly

-ow

ned

man

ufa

cturing

affilia

tes

earn

ed 6

.4%

RO

A

Profita

bili

ty G

ap,

1977-2

003

Man

ufac

turin

g

-2.0

%

0.0%

2.0%

4.0%

6.0%

8.0%

10.0

%

12.0

% 1975

1980

1985

1990

1995

2000

2005

Maj

ority

Min

ority

Gap

Poss

ible

exp

lanat

ions

for

gap

We

test

ed for:

!Siz

e!

Age

!Tax

rat

es!

Non-d

ivid

end p

aym

ents

!M

NC�s

ow

ner

ship

-spec

ific

cap

abili

ties

Sty

lized

fac

ts e

mer

gin

g fro

m d

ata

1.

Ther

e is

a p

osi

tive

gap

on a

vera

ge

2.

It is

larg

est

in s

ecto

rs w

her

e U

S M

NCs

are

most

com

pet

itiv

e ab

road

3.

The

gap

shrinks

ove

r tim

e on a

vera

ge

Rel

ated

aca

dem

ic liter

atu

re

!D

esai, F

ole

y an

d H

ines

(2004)

found

shar

ply

dec

linin

g p

ropen

sity

of U

S

MN

Es

to form

JVs

abro

ad

!They

focu

s on t

he

det

erm

inan

ts o

f ow

ner

ship

str

uct

ure

to e

xpla

in t

his

Dec

linin

g u

se o

f JV

s by

US M

NEs

Shar

e of

JVs

on T

otal

No. o

f US

Fore

ign

Vent

ures

0%20%

40%

60%

80%

100%

1982

1989

1994

1997

Othe

r

JV S

hare

Does

glo

bal

izat

ion r

educe

rat

ional

e fo

r in

tern

atio

nal

alli

ance

s an

d J

Vs?

!G

lobaliz

atio

n r

educe

s tr

ade

bar

rier

s an

d c

om

munic

ations

cost

s, m

akin

g

inte

rnat

ional alli

ance

s m

ore

att

ract

ive

!O

n t

he

oth

er h

and,

it a

lso incr

ease

s th

e re

turn

to c

oord

inat

ing o

per

atio

ns

within

multin

ational firm

s

Profita

bili

ty D

eter

min

ants

Neg

lect

ed

!D

esai finds

retu

rn o

n a

sset

s (R

OA)

is

dec

reas

ing funct

ion o

f fo

reig

n t

ax r

ates

!Contr

ols

: af

filia

te lev

erag

e, s

ale

s,

countr

y G

DP

and G

DP

per

cap

ita

!They

don�t p

erfo

rm a

ny

furt

her

an

aly

sis

of

RO

A d

eter

min

ants

Profita

bili

ty G

ap N

ot

Exp

lore

d Y

et

!D

esai et

al did

not

unco

ver

the

pro

fita

bili

ty g

ap b

etw

een w

holly

and

par

tially

ow

ned

ven

ture

s

!N

eith

er d

id o

ther

res

earc

her

s

Profita

bili

ty G

ap D

efin

ed

!Pr

ofita

bili

ty�

Net

Inco

me/

Net

Ass

ets

!W

holly

-ow

ned

�m

ajority

-ow

ned

ve

ntu

res,

90%

of th

em a

re 1

00%

ow

ned

!Jo

int

Ven

ture

s�All

affilia

tes

min

us

maj

ority

-ow

ned

Incl

udes

50-5

0 J

Vs,

whic

h a

ccount

for

about

54%

of JV

affili

ates

Prev

iew

of

dat

a

!Sourc

e: U

S B

ure

au o

f Eco

nom

ic A

naly

sis

!1977 a

nd 1

982-2

003

!N

on-b

ank

affilia

tes

of

non-b

ank

par

ents

!In

dust

ry lev

el,

25 t

hre

e-dig

it s

ecto

rs!

2 &

1 d

igit s

ecto

rs,

countr

ies,

reg

ions

!Avg

. no.

of w

holly

ow

ned

fore

ign

ventu

res

in m

anufa

cturing:

6,3

49

!N

o.

of fo

reig

n m

anufa

cturing J

Vs:

856

Profita

bili

ty G

ap,

1977-2

003

Man

ufac

turin

g

-2.0

%

0.0%

2.0%

4.0%

6.0%

8.0%

10.0

%

12.0

% 1975

1980

1985

1990

1995

2000

2005

Maj

ority

Min

ority

Gap

Ques

tions

about

RO

A G

ap

!W

her

e an

d w

hen

is

it p

osi

tive

?!

In w

hic

h s

ecto

rs,

countr

ies,

reg

ions?

!W

her

e an

d w

hen

is

it n

egat

ive?

!

Why

is it

posi

tive

/neg

ative

?!

Is it

shrinki

ng?

Gro

win

g?

Wher

e?

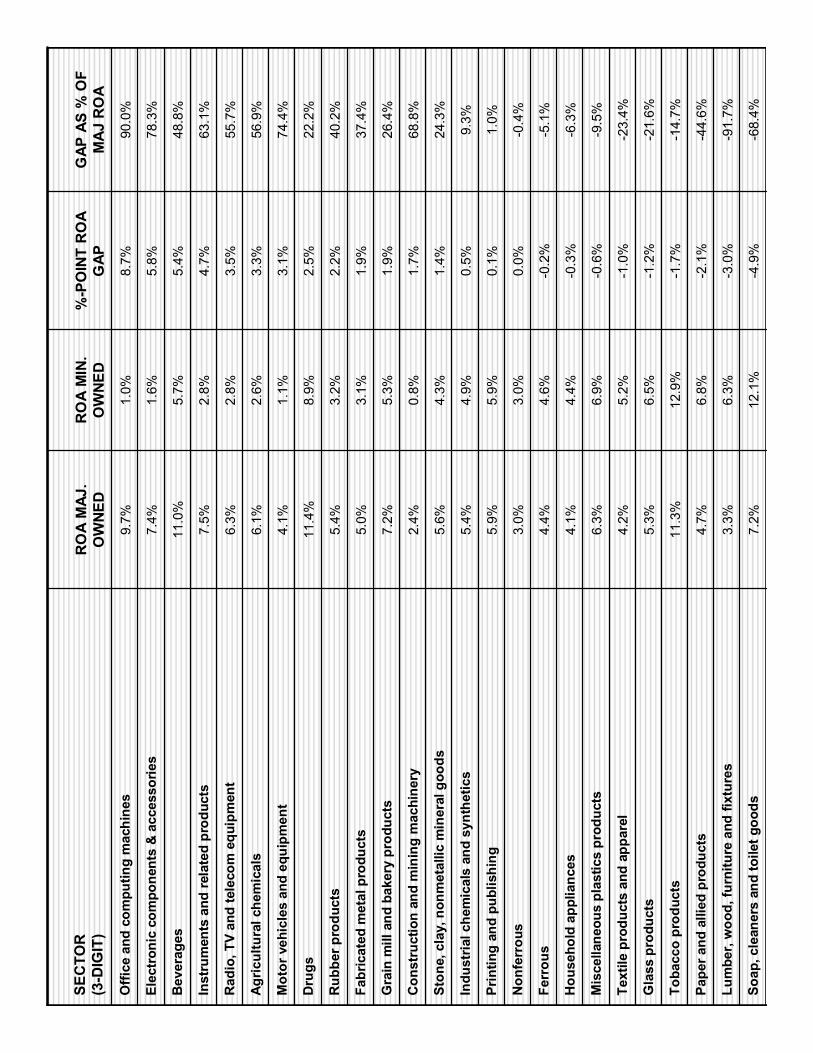

Top a

nd B

ott

om

3 S

ecto

rs b

y G

ap -4.9

Soa

p, c

lean

ers

and

toile

t goo

ds

-3.0

Lum

ber,

woo

d an

d fu

rnitu

re

-2.1

Pap

er a

nd a

llied

prod

ucts

5.4

Bev

erages

5.8

Ele

ctro

nic

com

ponen

ts e

tc

8.7

Offic

e m

ach

ines

, co

mpute

rs

RO

A G

ap

Sec

tor

(3-d

igit c

lass

ific

atio

n)

-68.

4%-4

.9%

12.1

%7.

2%So

ap, c

lean

ers

and

toile

t goo

ds

-91.

7%-3

.0%

6.3%

3.3%

Lum

ber,

woo

d, fu

rnitu

re a

nd fi

xtur

es

-44.

6%-2

.1%

6.8%

4.7%

Pape

r and

alli

ed p

rodu

cts

-14.

7%-1

.7%

12.9

%11

.3%

Toba

cco

prod

ucts

-21.

6%-1

.2%

6.5%

5.3%

Gla

ss p

rodu

cts

-23.

4%-1

.0%

5.2%

4.2%

Text

ile p

rodu

cts

and

appa

rel

-9.5

%-0

.6%

6.9%

6.3%

Mis

cella

neou

s pl

astic

s pr

oduc

ts

-6.3

%-0

.3%

4.4%

4.1%

Hou

seho

ld a

pplia

nces

-5.1

%-0

.2%

4.6%

4.4%

Ferr

ous

-0.4

%0.

0%3.

0%3.

0%N

onfe

rrou

s

1.0%

0.1%

5.9%

5.9%

Prin

ting

and

publ

ishi

ng

9.3%

0.5%

4.9%

5.4%

Indu

stria

l che

mic

als

and

synt

hetic

s

24.3

%1.

4%4.

3%5.

6%St

one,

cla

y, n

onm

etal

lic m

iner

al g

oods

68.8

%1.

7%0.

8%2.

4%C

onst

ruct

ion

and

min

ing

mac

hine

ry

26.4

%1.

9%5.

3%7.

2%G

rain

mill

and

bak

ery

prod

ucts

37.4

%1.

9%3.

1%5.

0%Fa

bric

ated

met

al p

rodu

cts

40.2

%2.

2%3.

2%5.

4%R

ubbe

r pro

duct

s

22.2

%2.

5%8.

9%11

.4%

Dru

gs

74.4

%3.

1%1.

1%4.

1%M

otor

veh

icle

s an

d eq

uipm

ent

56.9

%3.

3%2.

6%6.

1%Ag

ricul

tura

l che

mic

als

55.7

%3.

5%2.

8%6.

3%R

adio

, TV

and

tele

com

equ

ipm

ent

63.1

%4.

7%2.

8%7.

5%In

stru

men

ts a

nd re

late

d pr

oduc

ts

48.8

%5.

4%5.

7%11

.0%

Bev

erag

es

78.3

%5.

8%1.

6%7.

4%El

ectr

onic

com

pone

nts

& a

cces

sorie

s

90.0

%8.

7%1.

0%9.

7%O

ffice

and

com

putin

g m

achi

nes

GAP

AS

% O

F M

AJ

RO

A%

-PO

INT

RO

A G

APR

OA

MIN

. O

WN

ED

RO

A M

AJ.

OW

NED

SEC

TOR

(3-D

IGIT

)

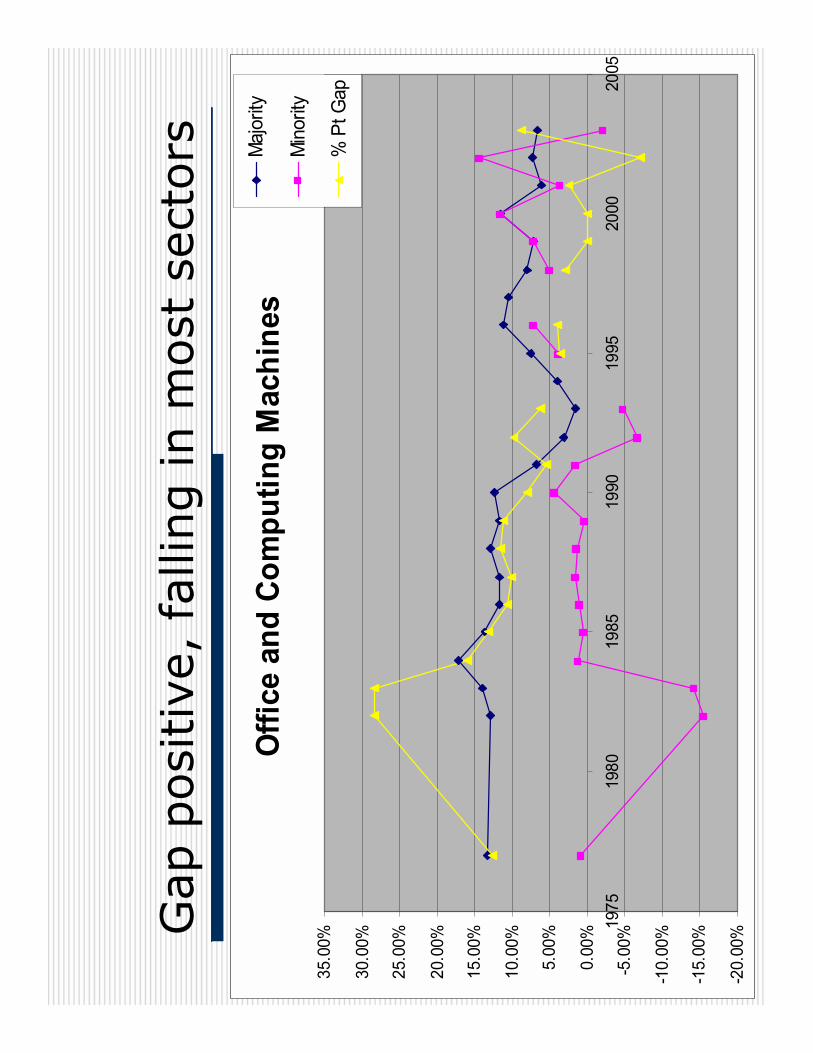

Gap

posi

tive

, fa

lling in m

ost

sec

tors

Offi

ce a

nd C

ompu

ting

Mac

hine

s

-20.

00%

-15.

00%

-10.

00%

-5.0

0%

0.00

%

5.00

%

10.0

0%

15.0

0%

20.0

0%

25.0

0%

30.0

0%

35.0

0%

1975

1980

1985

1990

1995

2000

2005

Maj

ority

Min

ority

% P

t Gap

But

in s

om

e st

ays

stab

le,

neg

ativ

e

Soap

s an

d To

iletr

ies

-25.

00%

-20.

00%

-15.

00%

-10.

00%

-5.0

0%

0.00

%

5.00

%

10.0

0%

15.0

0%

20.0

0%

25.0

0%

30.0

0%

1975

1980

1985

1990

1995

2000

2005

Maj

ority

Min

ority

% P

t Gap

Gap

clo

se t

o z

ero in s

om

e co

untr

ies

Unite

d Ki

ngdo

m

-15.

0%

-10.

0%

-5.0

%

0.0%

5.0%

10.0

%

15.0

% 1975

1980

1985

1990

1995

2000

2005

Maj

Min

Gap

Som

e re

gio

ns

are

closi

ng t

he

gap

Asia

and

Pac

ific

-5.0

%

0.0%

5.0%

10.0

%

15.0

% 1975

1980

1985

1990

1995

2000

2005

Maj

Min

Gap

Theo

retica

l Exp

lanation:

Ow

ner

ship

-spec

ific

cap

abili

ties

!O

wner

ship

-spec

ific

cap

abili

ties

of M

NE

!Ref

lect

com

pet

itiv

e ad

vanta

ge

of

MN

E

com

par

ed t

o loca

l riva

ls a

bro

ad

Det

erm

inan

ts

of ow

ner

ship

and p

rofita

bili

ty

!If

the

ow

ner

ship

-spec

ific

cap

abili

ties

ar

e st

rong,

MN

E lik

ely

to c

hoose

w

hole

ow

ner

ship

, pro

fits

hig

h

!If

they

are

wea

k, M

NE lik

ely

to s

eek

additio

nal ca

pabili

ties

fro

m loca

l firm

, pro

fits

lik

ely

to b

e lo

wer

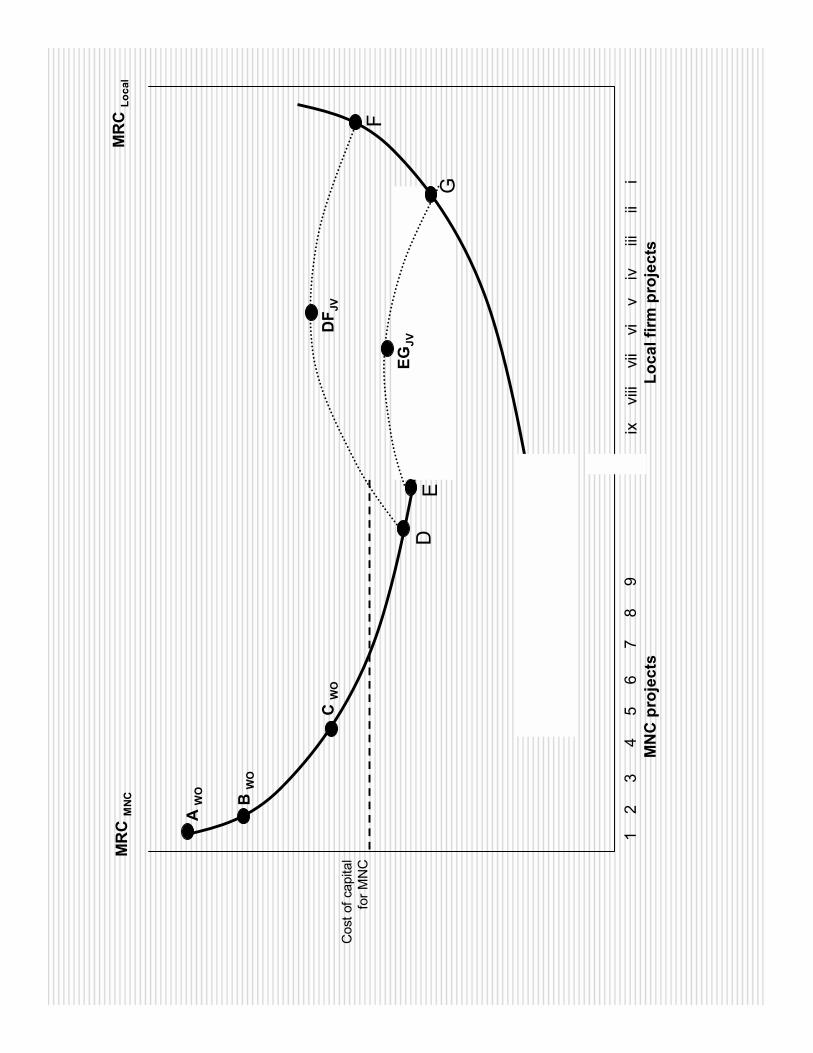

Inve

stm

ent p

roje

cts

or C

apita

l inv

este

d

Ret

urn

to th

e fir

m

Cos

t of c

apita

l

1

2

3

4

5

6

7

8

9

10

11

12

Mar

gina

l ret

urn

to c

apita

l (M

RC

)

Proj

ects

don

ePr

ojec

ts n

ot d

one

MR

C

MR

CM

NC

MR

CLo

cal

Exte

nt o

f com

petit

ive

adva

ntag

e of

MN

C

Cap

ital I

nves

ted

1

2

3

4

5

6

7

8

9

ix

v

iii

vii

vi

v

iv

i

ii

ii

i

MR

C M

NC

MR

C Lo

cal

MN

C p

roje

cts

Loca

l firm

pro

ject

s

Cos

t of c

apita

lfo

r MN

C

D

F

DF J

V

EG

EGJV

A W

O B W

O

C W

O

Mea

sure

s of

ow

ner

ship

-spec

ific

cap

abili

ties

!Should

ref

lect

inte

rnational

com

pet

itiv

e ad

vanta

ge

of

MN

E/i

ndust

ry

!Sal

es o

f U

S c

orp

ora

tions

abro

ad/

Sal

es o

f U

S c

orp

ora

tions

in t

he

US

!Sal

es o

f U

S f

irm

s ab

road/

Sal

es o

f al

l firm

s in

the

US

!Sal

es d

ata

from

BEA a

nd C

ensu

s of

US

Man

ufa

cture

rs

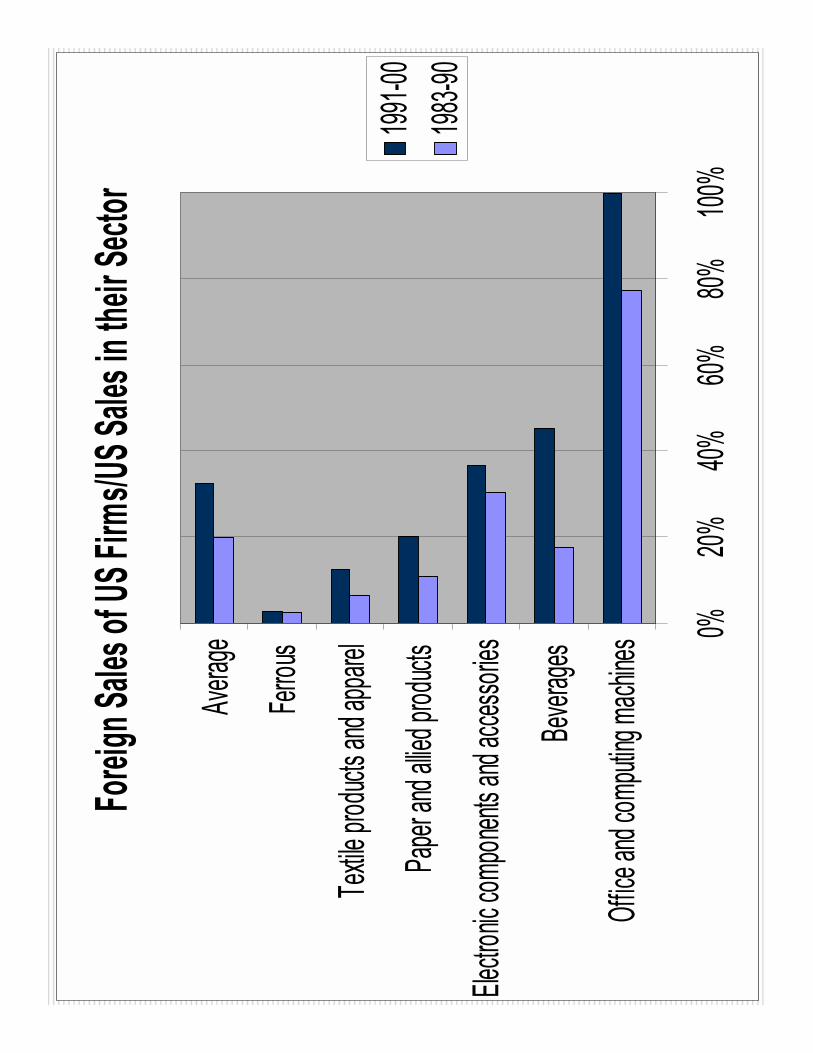

Forei

gn Sa

les of

US Fi

rms/U

S Sale

s in th

eir Se

ctor

0%20%

40%60%

80%100

%

Office

and c

omput

ing ma

chines

Bever

ages

Electro

nic co

mpone

nts an

d acce

ssories

Paper

and a

llied pro

ducts

Textile

produc

ts and

appare

l

Ferrou

s

Avera

ge

1991-0

0198

3-90

Sec

tors

with lar

ges

t gap

hav

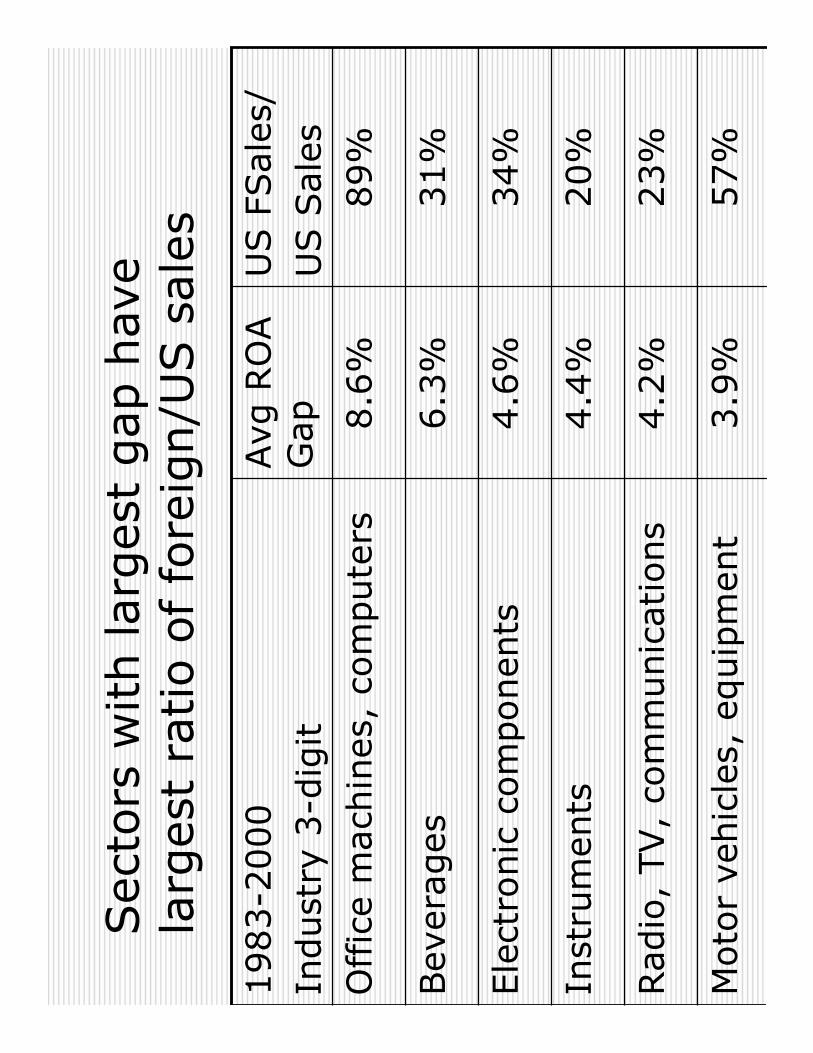

e la

rges

t ra

tio o

f fo

reig

n/U

S s

ales

57%

3.9

%M

oto

r ve

hic

les,

equip

men

t

23%

4.2

%Rad

io,

TV,

com

munic

ations

20%

4.4

%In

stru

men

ts

34%

4.6

%Ele

ctro

nic

com

ponen

ts

31%

6.3

%Bev

erages

89%

8.6

%O

ffic

e m

ach

ines

, co

mpute

rs

US F

Sal

es/

US S

ales

Avg

RO

A

Gap

1983-2

000

Indust

ry 3

-dig

it

Sec

tors

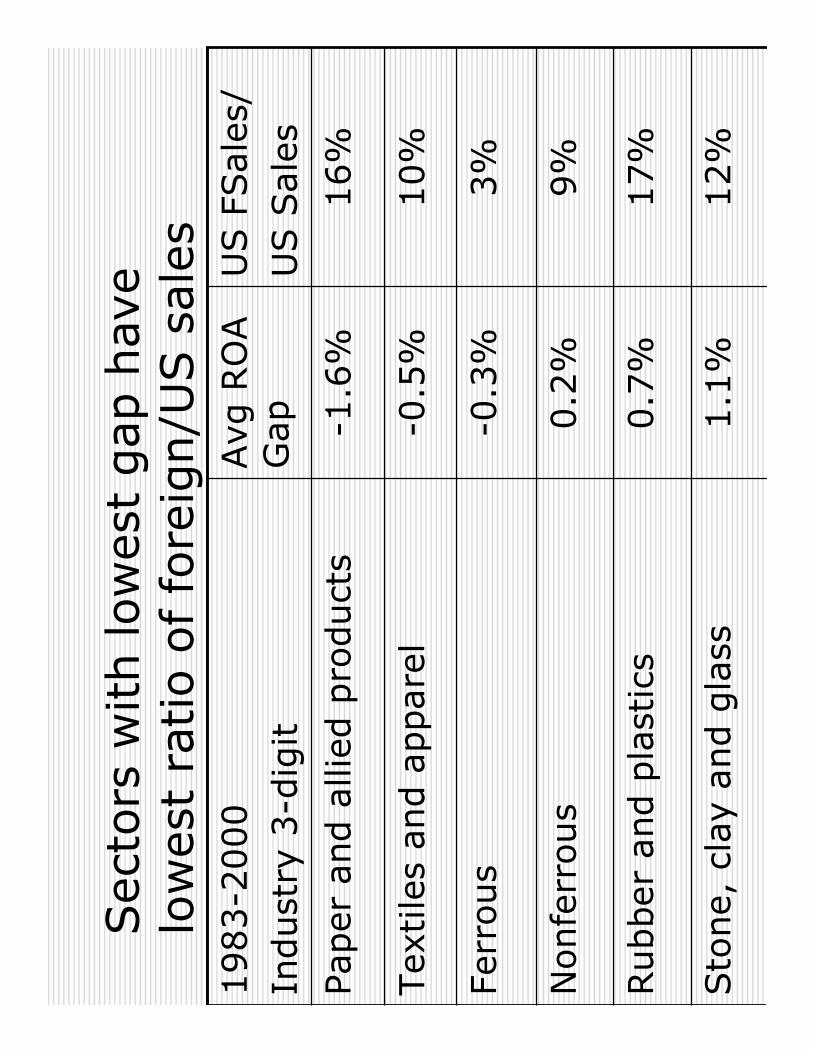

with low

est

gap

hav

e lo

wes

t ra

tio o

f fo

reig

n/U

S s

ales

12%

1.1

%Sto

ne,

cla

y and g

lass

17%

0.7

%Rubber

and p

last

ics

9%

0.2

%N

onfe

rrous

3%

-0.3

%Fe

rrous

10%

-0.5

%Tex

tile

s an

d a

ppare

l

16%

-1.6

%Paper

and a

llied

pro

duct

s

US F

Sal

es/

US S

ales

Avg

RO

A

Gap

1983-2

000

Indust

ry 3

-dig

it

Corr

elat

ion b

etw

een t

he

Gap

an

d t

he

sale

s ra

tios

is 0

.30

!Sale

s of U

S f

irm

s ab

road

/Sale

s of

all

firm

s in

the

US

�Corr

elation C

oef

fici

ent=

0.3

0

!Sale

s of U

S c

orp

ora

tions

abro

ad/

Sale

s of U

S c

orp

ora

tions

in t

he

US

�Corr

elation C

oef

fici

ent=

0.3

0

Lim

itat

ions

of sa

les

ratios

as

mea

sure

s of

intl.

com

p.

adva

nta

ge

!Fo

reig

n/d

om

estic

asse

t ra

tios

would

be

per

hap

s m

ore

appro

priate

!Fo

reig

n/d

om

estic

sale

s ra

tio h

as b

een

risi

ng in a

ll se

ctors

, w

hile

the

gap

has

bee

n s

hrinki

ng in m

ost

sec

tors

Lim

itations

of

dat

a

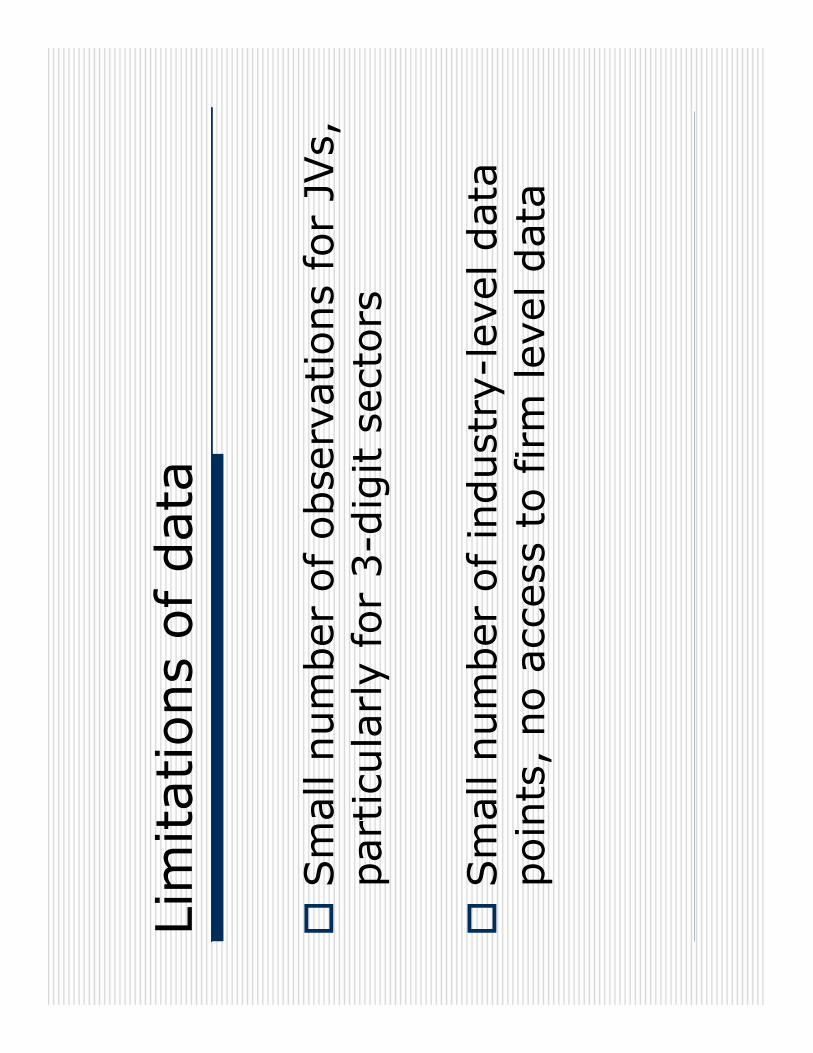

!Sm

all num

ber

of obse

rvat

ions

for

JVs,

par

ticu

larly

for

3-d

igit s

ecto

rs

!Sm

all num

ber

of

indust

ry-l

evel

dat

a poin

ts,

no a

cces

s to

firm

lev

el d

ata

Tes

ts for

stat

sig

nific

ance

of gap

!T-t

est

for

stat

sig

nific

ance

of

gap e

stim

ates

co

nfirm

s re

sults

for

most

1 &

2 d

igit s

ecto

rs

!O

nly

min

ing,

fabri

cate

d m

etal

s in

signific

ant

!M

any

3-d

igit s

ecto

rs h

ave

< t

han 2

0 J

Vs

1-d

igit indust

ries

, 1977-2

003

3.4

%**

7,19

232

7Fi

nance

-0.1

7615

Min

ing

2.0

%**

937

76Ser

vice

s

3.4

%**

6,34

985

6M

anufa

cturing

42.4

%**

1,72

632

0Pe

trole

um

1.0

%**

23,2

011,

911

All

indust

ries

Gap

# O

ther

# J

Vs

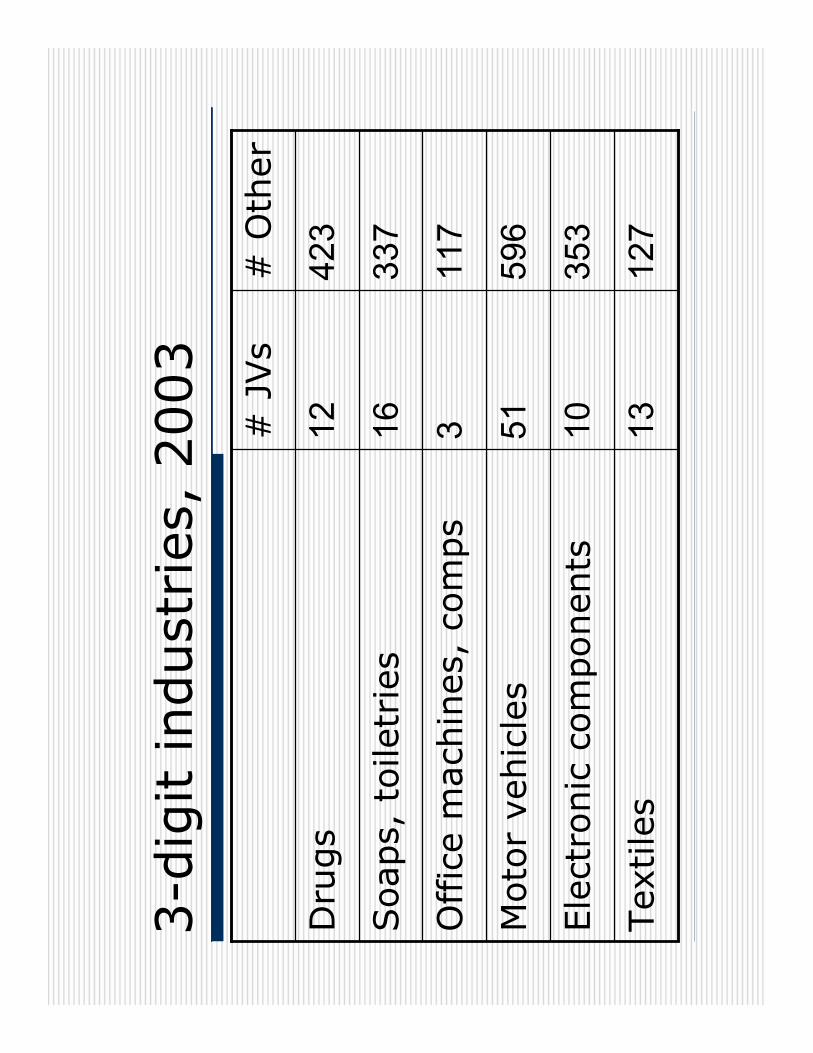

3-d

igit indust

ries

, 2003

127

13Tex

tile

s

353

10Ele

ctro

nic

com

ponen

ts

596

51M

oto

r ve

hic

les

117

3O

ffic

e m

ach

ines

, co

mps

337

16Soaps,

toile

trie

s

423

12D

rugs

# O

ther

# J

Vs

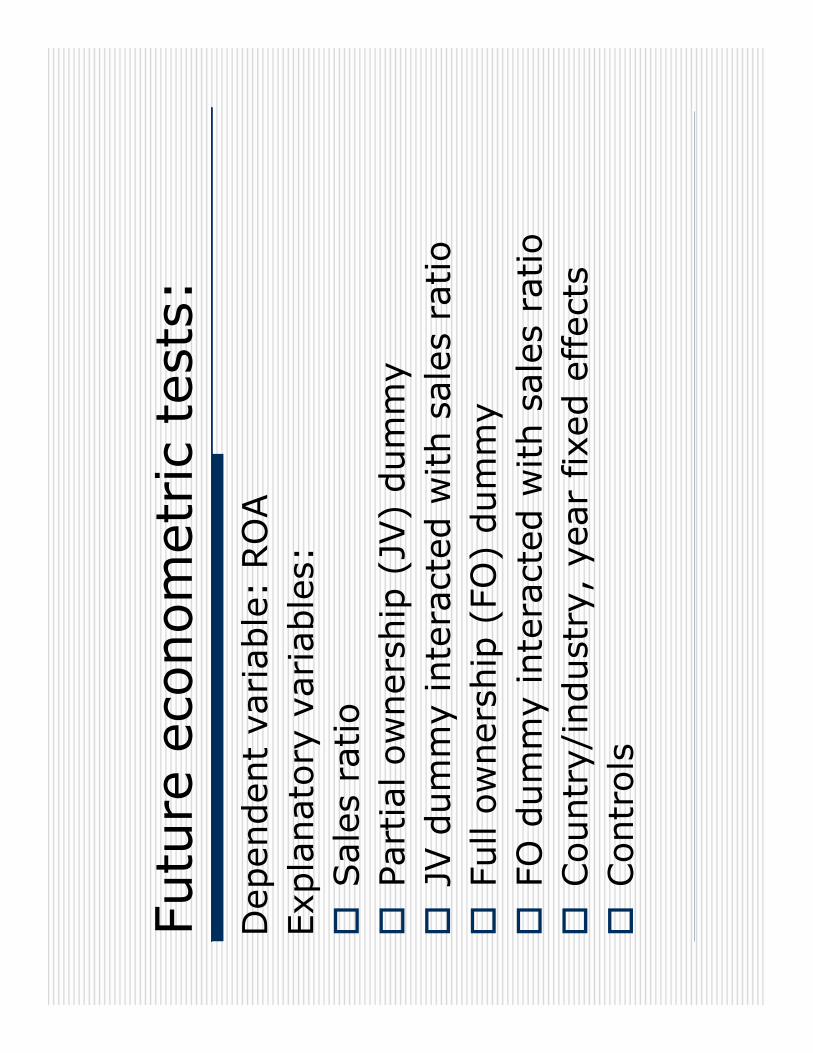

Futu

re e

conom

etric

test

s:D

epen

den

t va

riable

: RO

AExp

lanat

ory

var

iable

s:!

Sal

es r

atio

!Pa

rtia

l ow

ner

ship

(JV

) dum

my

!JV

dum

my

inte

ract

ed w

ith s

ales

ratio

!Fu

ll ow

ner

ship

(FO

) dum

my

!FO

dum

my

inte

ract

ed w

ith s

ales

rat

io!

Countr

y/in

dust

ry,

year

fix

ed e

ffec

ts!

Contr

ols

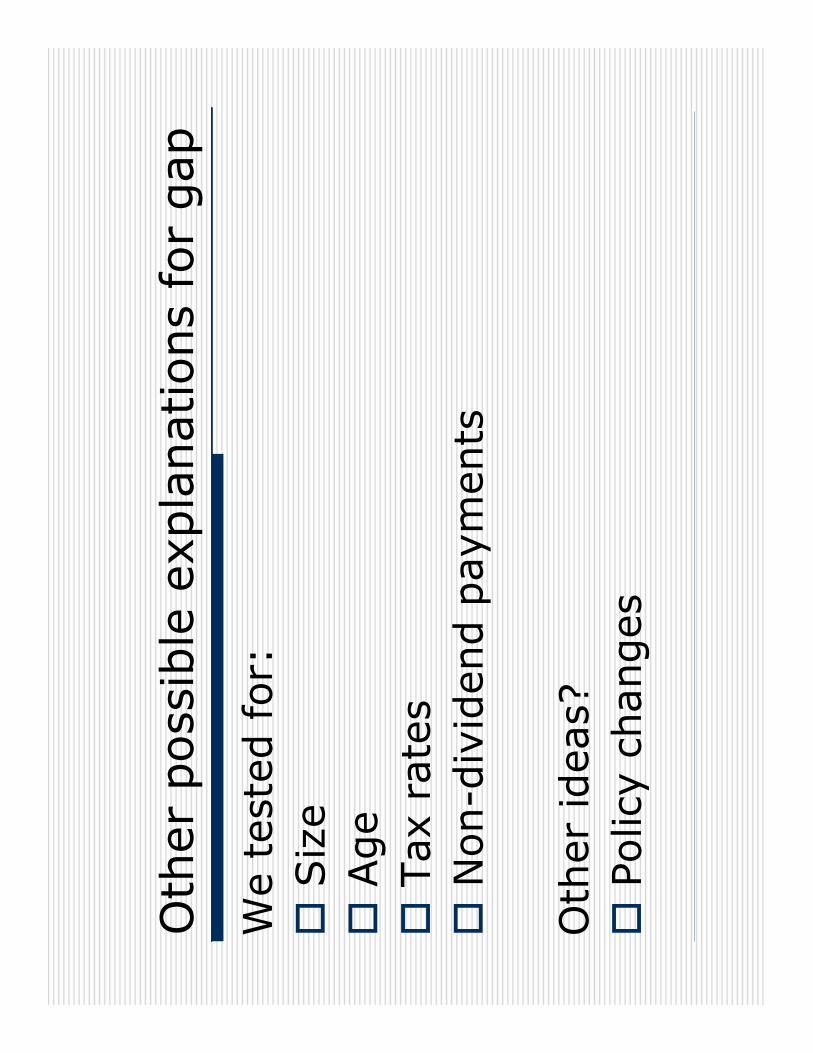

Oth

er p

oss

ible

exp

lanat

ions

for

gap

We

test

ed for:

!Siz

e!

Age

!Tax

rat

es!

Non-d

ivid

end p

aym

ents

Oth

er idea

s?!

Polic

y ch

anges

Post

script:

JVs

in I

ndia

and C

hin

a

!W

all Str

eet

Journ

alre

port

ed o

n t

he

tro

ub

les

of

inte

rnati

on

al

JVs

in I

nd

ia

!Chin

a Busi

nes

s O

nlin

ere

port

s on t

he

decl

inin

g n

um

bers

of

JVs

in C

hin

a

Cau

ses

of

falli

ng J

Vnum

ber

s in

India

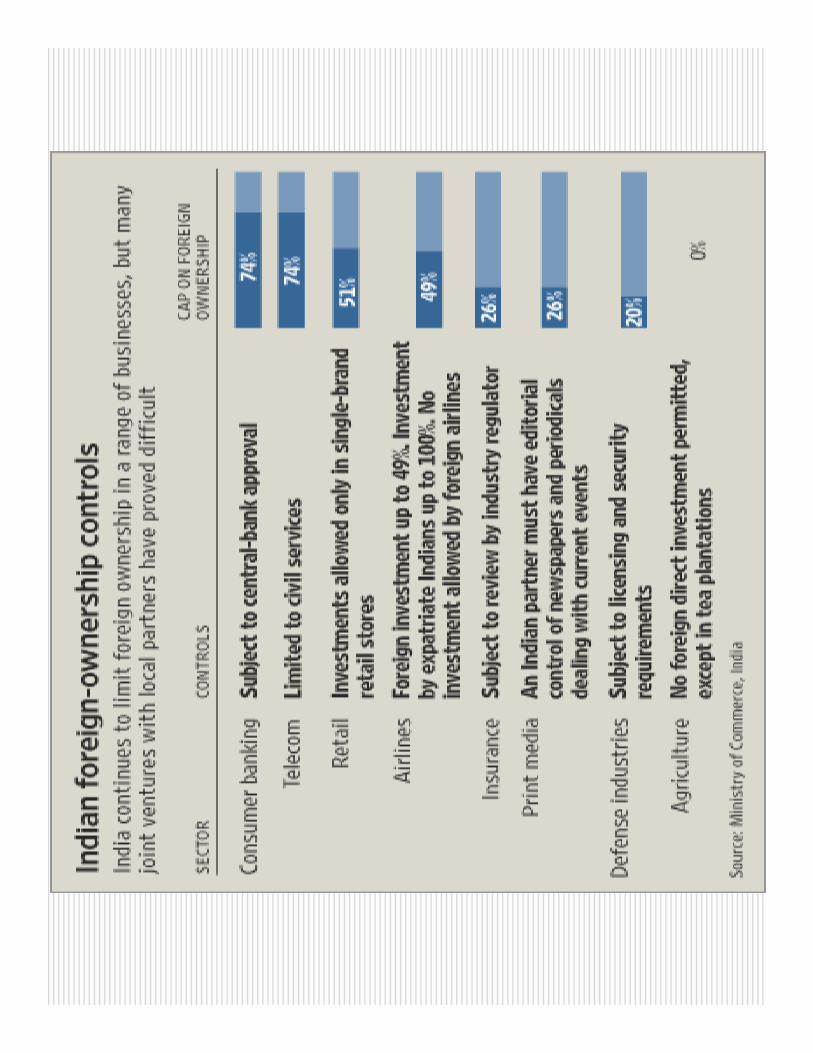

!Le

ss g

ove

rnm

ent

rest

rict

ions

!D

iffe

rence

s bet

wee

n p

artn

ers

!Cla

shes

ove

r ex

pan

sion p

lans

!Com

pet

ing inte

rest

s of firm

s

Dec

linin

g u

se o

f JV

s in

Chin

aSh

are

of J

Vs o

n FD

I flo

ws

to C

hina

0.00

%

20.0

0%

40.0

0%

60.0

0%

80.0

0%

100.

00%

120.

00%

2000

2001

2002

2003

2004

Oth

er

JVs

![untitled 2 [people.brandeis.edu]people.brandeis.edu/~sekuler/papers/SekulerNature1997.pdf · Presentation ofsound Figure I Percentage of reports of stimulus bouncing. In each trial,](https://static.documents.pub/doc/80x56/5f4e7aa9b6f9633f2c3bd2e4/untitled-2-sekulerpaperssekulernature1997pdf-presentation-ofsound-figure.jpg)