26

PROFITS FROM TRADE, BUSINESS, PROFESSION OR VOCATION

PROFITS

FROM

TRADE, BUSINESS, PROFESSION OR VOCATION

PREPARATION OF FINANCIAL STATEMENT Section 28 of IR Act.

Require to make up for each successive period of 12 months ending on March 31 of each year

Deviation

With approval from CGIR

SEPARATE ACCOUNTS -Person carried out any TBPV in several unit or undertaking.

-Exempted or difference rate apply for income tax purpose.

-Shall maintain and prepare statement of accounts in manner that such profit or income may be separately identified.

Section 106(11) of IR Act.

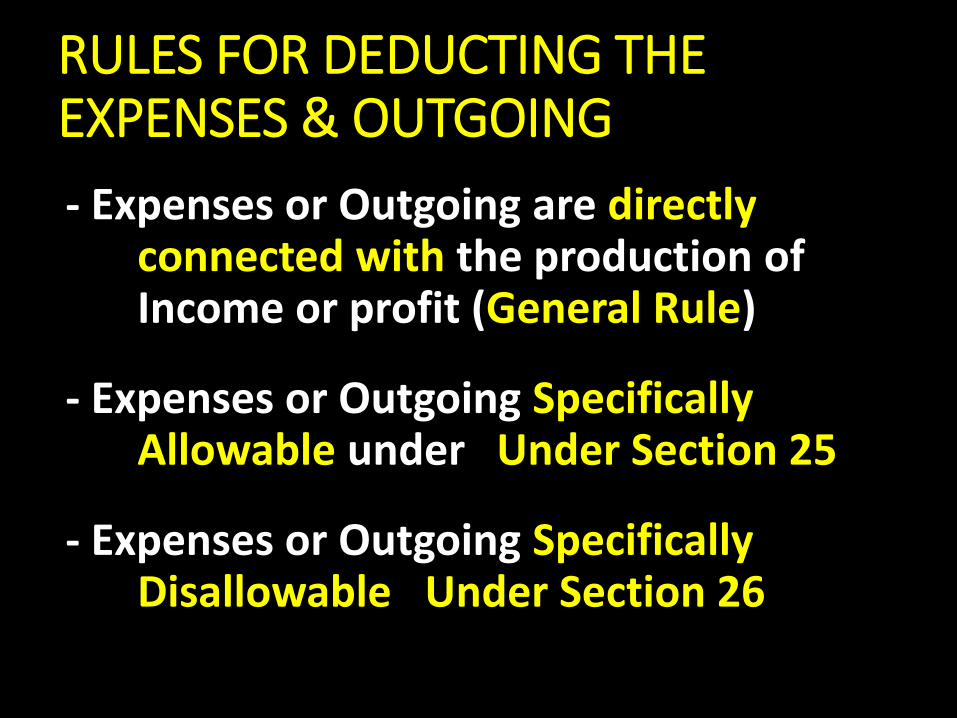

RULES FOR DEDUCTING THE EXPENSES & OUTGOING

- Expenses or Outgoing are directly connected with the production of Income or profit (General Rule)

- Expenses or Outgoing Specifically Allowable under Under Section 25

- Expenses or Outgoing Specifically Disallowable Under Section 26

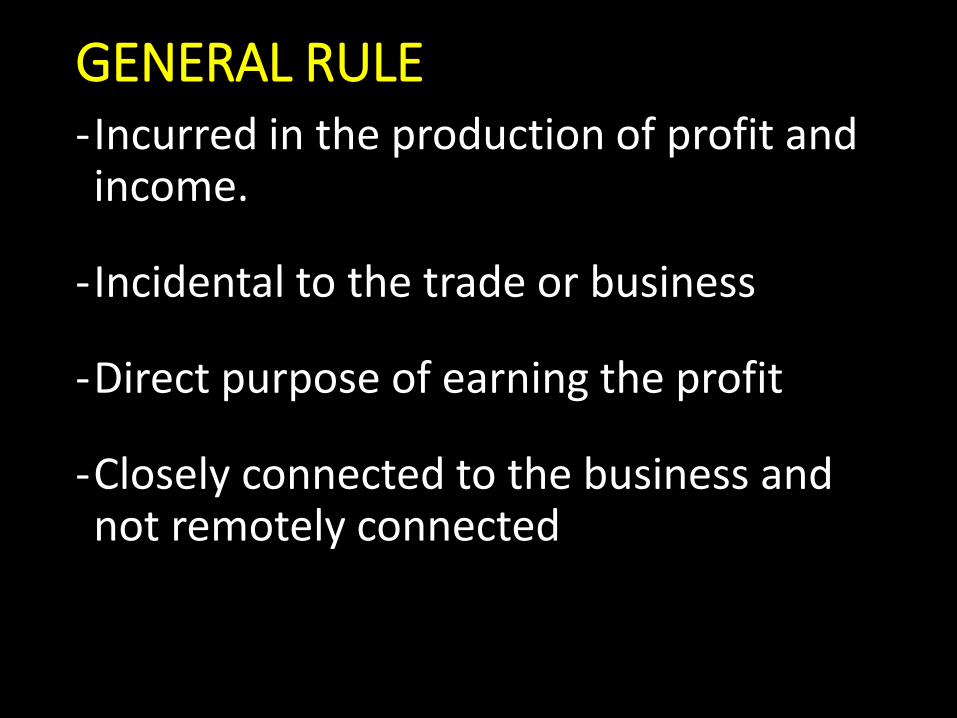

GENERAL RULE -Incurred in the production of profit and income.

-Incidental to the trade or business

-Direct purpose of earning the profit

-Closely connected to the business and not remotely connected

ADJUSTMENT RELATED TO ASSETS

Value of Assets

- Purchase - Cost of Purchase

- Assembly - Cost of Assembly

- Construction - Cost Construction

- Market value - any other way

Period of claim

Based on classification of assets

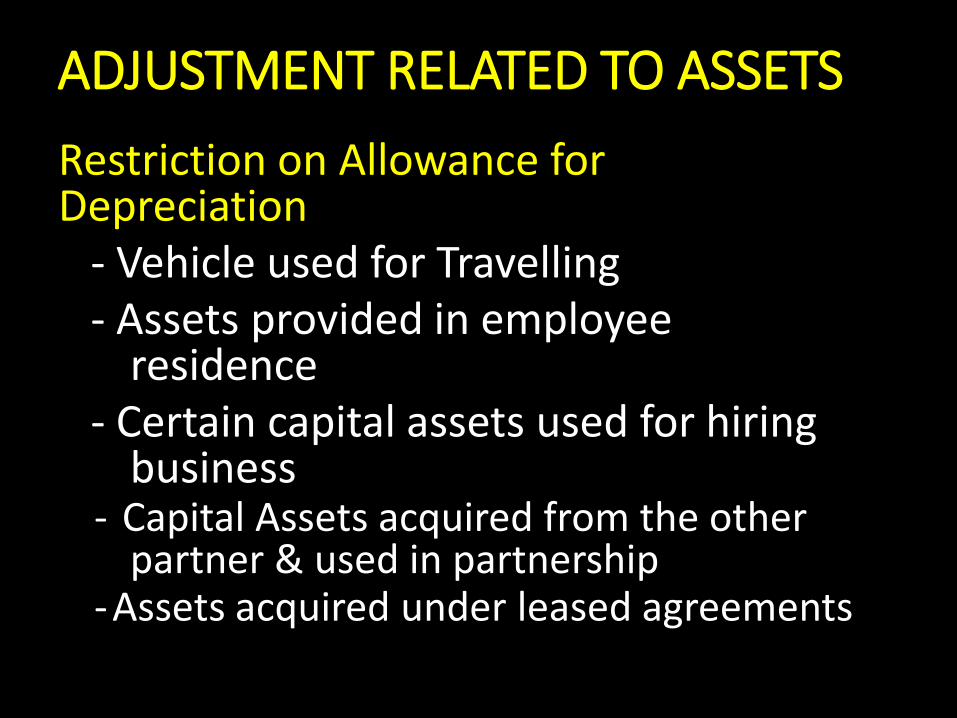

ADJUSTMENT RELATED TO ASSETS

Allowance for Depreciation - Condition to be satisfied - Qualified Building - Purchased Building

ADJUSTMENT RELATED TO ASSETS

Restriction on Allowance for Depreciation - Vehicle used for Travelling - Assets provided in employee residence - Certain capital assets used for hiring business

- Capital Assets acquired from the other partner & used in partnership

-Assets acquired under leased agreements

RESTRICTION ON ALLOWENCE FOR DEPRECIATION - Vehicle used for travelling

- Assets provided in employee's residence

- Certain capital asset used for hiring

- Capital asset acquired from the other partner and used in the partnership

- Asset acquired under the leasing agreement

DISPOSAL PROFIT OR LOSS ON FIXED ASSETS

Sales proceed of disposal xxx

Less : Tax Written Down Value (xxx)

Disposal profit for Tax purpose xxx

TAX WRITTEN DOWN VALUE Dep. allowance not claimed up to disposal Cost xxx

Less:

Dep. Allowance claimed (xxx)

Tax Written Down Value xxx

QUALIFING REPLACEMENT Condition to be satisfied

- Replace with similar asset - Replace within one year from the date of disposal - Full sale proceeds have been used to replace the asset

Additional condition - Taxable profit form disposed asset

IF RPLACEMENT SATISFIED

Profit from disposed asset is not taxed

Allowance for Dep. To new Asset Cost of the asset acquired xxx Less : Tax profit on disposed asset (xx) Cost for depreciation purpose xx

RENEWAL ALLOWENCE

Cost of renewed assets xxx

Less:

Sales proceed from disposal of

Old Assets (xxx)

Renewal Allowance xxx •

BAD & DOUBTFUL DEBTS

If Bad Debts - out of the Trade debtors - any recovery action taken - no any transaction with defaulter

If Doubtful Debts - out of the Trade debtors - Specific provision - Allowed - General provision – Not allowed

RESEACH EXPENSES

- Carrying on any scientific, industrial, agricultural or any other research for the upgrading of any business - Charring out through any Institution out side or Company itself - including capital expenditure •The amount equal to 300% of the expenditure

RESEACH EXPENSES

Double Deduction ( 200% )

Charring out research upgrading the of Business

Triple Deduction( 300% )

Charring out though any institute in Sri Lanka, that relating to high value agricultural products

TRAVETING EXPENSES WITHIN SRI LANKA If connection with Business – Allowed

But Provided that - More than one vehicle provided - Person who provided ,No relation with Business

- Not Allowed

EXPENCES IN TRAVELLING OUTSIDE SRI LANKA

A (i) promotion of the export of any articles or goods

(ii) provisions of any services for payment in foreign currency

(iii) carrying out a programme approved by Ceylon Tourist Board for the promotion of tourism, in case of an undertaking of any hotel.

And

B In case of expense in travelling outside Sri Lanka shall be deductible in ascertaining the profits subject to a maximum of 2% of profits arising from such business for the previous year of assessment.

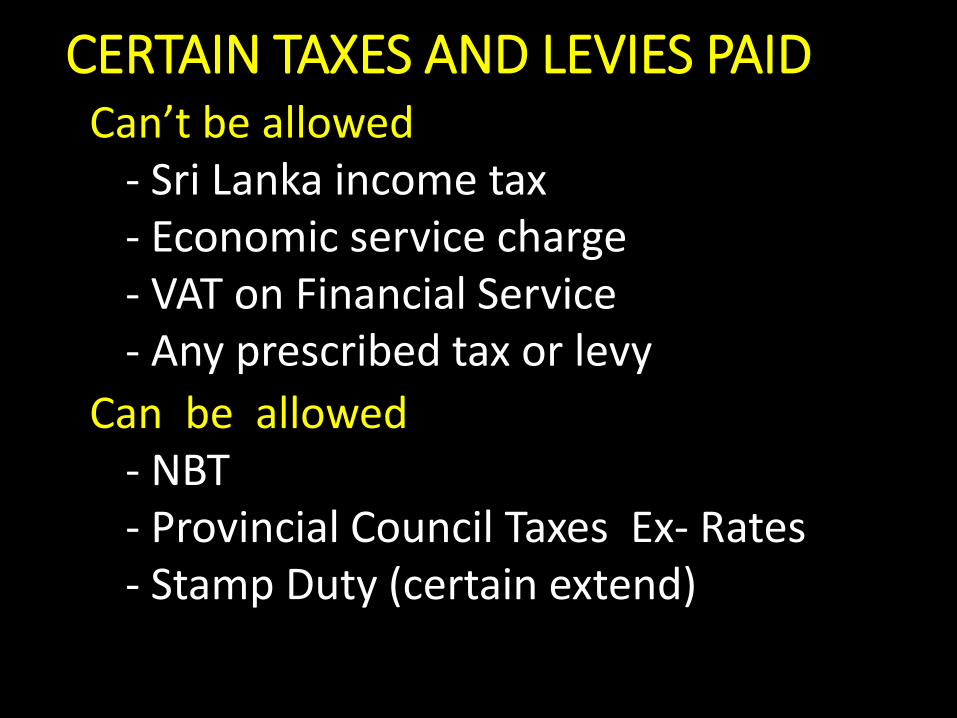

CERTAIN TAXES AND LEVIES PAID Can’t be allowed

- Sri Lanka income tax - Economic service charge - VAT on Financial Service - Any prescribed tax or levy

Can be allowed - NBT - Provincial Council Taxes Ex- Rates - Stamp Duty (certain extend)

EXPENSES ON PROVIDING ANY PLACE OF RESIDENCE TO EMPLOYEE

Rent expenses charged xxx

Less:

Housing Benefit of employee (xxx)

Amount of excess xxx

If gross remuneration

or Less than 600,000 ½ of excess

more than 600,000 ¾ of excess

LEASING ALLOWANCE

Maximum Lease allowance xxx

( rental Value x No. of rental)

*1/4 or 1/5

Rental paid for relevant Y/A xxx

Whichever Less

LEASED ASSETS DISPOSAL

Proceeds of the disposal xxx

Less:

Cost of Acquisition other than xxx

leasing rental paid

Amount to be liable xxx

MANAGEMENT FEE Rs. 2,000,000/-

whichever is

lower

1% of the turnover whichever is

higher

Amount of CGIR Approved

COST OF ADVERTISEMENT

25% of cost of advertisement –Disallowed

But allowed fully, - Recruitment of staff

- export trade of any article or goods, or - provision of any services for payment in foreign currency

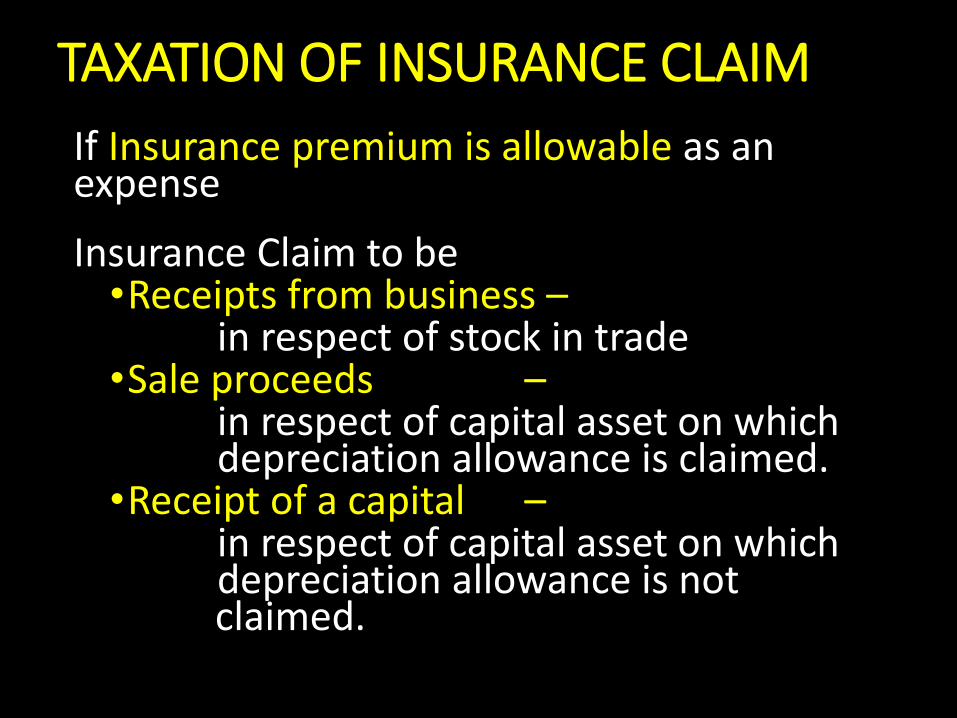

TAXATION OF INSURANCE CLAIM

If Insurance premium is allowable as an expense

Insurance Claim to be •Receipts from business – in respect of stock in trade •Sale proceeds – in respect of capital asset on which depreciation allowance is claimed.

•Receipt of a capital – in respect of capital asset on which depreciation allowance is not claimed.