Asian Journal of Agriculture and Development, Vol. 8, No. 2 29 INTRODUCTION Khan Bank and XacBank in Mongolia are two recognized banks in the area of microfinance. They have widened the level of outreach and attained self-sustainability progressively, earning a worldwide reputation and exemplifying the “Mongolian Model of Microfinance” for performing well in the last 10 years. The factors influencing their progress, which were determined through interviews with bank staff in main and local branch offices as well as borrowers in various areas, were explored in this study. Two points were considered before data were analyzed. First, Mongolia is one of the least populated countries in the world. 1 Consequently, it would find it difficult to apply the Grameen model of group lending since this model was developed for densely populated countries like Bangladesh. Second, the use of land property rights as financial collateral has Progress of Mongolian Microfinance: A Case Study of Khan Bank and XacBank Orosoo Dulamragchaa University of Tokyo E-mail: [email protected]Yoichi Izumida University of Tokyo E-mail: [email protected]ABSTRACT This paper examines the activities of Mongolian financial intermediation and the factors influencing the progress of Mongolian microfinance. These were evaluated using data from household surveys in selected areas, financial statements of Khan Bank and XacBank, and information obtained from interviews with officers of said banks. The analysis found that the performance of these two banks improved significantly. Moreover, Mongolian microfinance advanced as innovative methods were introduced. The new concept of collateral is considered the most important development. Loans secured using various kinds of collateral and guarantee are effective in heightening loan recovery in Mongolian microfinance. 1 According to World Bank statistics (2010), Mongolia covers an area of 1.56 million square kilometers (km 2 ) and has a total population of approximately 2.7 million people. The population density is 1.7 people per km 2 , which shows that Mongolia has one of the lowest population densities worldwide.

Transcript

Asian Journal of Agriculture and Development, Vol. 8, No. 2 29

INTRODUCTION

Khan Bank and XacBank in Mongolia are two recognized banks in the area of microfinance. They have widened the level of outreach and attained self-sustainability progressively, earning a worldwide reputation and exemplifying the “Mongolian Model of Microfinance” for performing well in the last 10 years. The factors influencing their progress, which were determined through interviews

with bank staff in main and local branch offices as well as borrowers in various areas, were explored in this study.

Two points were considered before data were analyzed. First, Mongolia is one of the least populated countries in the world.1 Consequently, it would find it difficult to apply the Grameen model of group lending since this model was developed for densely populated countries like Bangladesh. Second, the use of land property rights as financial collateral has

Progress of Mongolian Microfinance: A Case Study of Khan Bank and XacBank

This paper examines the activities of Mongolian financial intermediation and the factors influencing the progress of Mongolian microfinance. These were evaluated using data from household surveys in selected areas, financial statements of Khan Bank and XacBank, and information obtained from interviews with officers of said banks. The analysis found that the performance of these two banks improved significantly. Moreover, Mongolian microfinance advanced as innovative methods were introduced. The new concept of collateral is considered the most important development. Loans secured using various kinds of collateral and guarantee are effective in heightening loan recovery in Mongolian microfinance.

1 According to World Bank statistics (2010), Mongolia covers an area of 1.56 million square kilometers (km2) and has a total population of approximately 2.7 million people. The population density is 1.7 people per km2, which shows that Mongolia has one of the lowest population densities worldwide.

Orosoo Dulamragchaa and Yoichi Izumida30

largest non-bank financial institutions in the country in late 2001: Goviin Ekhlel LLC and XAC LLC. Since its establishment, XacBank has successfully obtained investments from numerous international donors (e.g., International Finance Corporation, United States Agency for International Development, and Deutsche Bank) and domestic capital markets (Lamberte 2006; Minh-Huy 2006). With its unique individual lending approach, XacBank is expanding its business to cover new areas, including banking services for many rural customers.

In 2010, 14 commercial banks were operating in Mongolia; among them, Khan Bank and XacBank had a significant share. Khan Bank alone satisfied 22.5 percent of all demand for loans through 488 branches covering the countryside (Khan Bank, Annual Reports 2001-2009). Meanwhile, XacBank provided 7.4 percent of loans through 78 branches in 2009 (XacBank, Annual Reports 2000-2009). These indicators are superlative in Mongolia compared to other commercial banks. These two banks have distributed diversified loan products, such as loans for consumption, salaried workers, agriculture, business, and housing. In mid-2006, business loans and herder loans made up 30.4 percent and 25 percent of Khan Bank’s and XacBank’s loan portfolio, respectively (Philippe 2006). Khan Bank continues to provide herder loans while XacBank has stopped its herder lending services temporarily. Mongolia’s livestock sector has faced serious risk caused by snowstorms,3 which is why XacBank has

been restricted in Mongolia. Traditionally, there was no concept of land property.2 In a country where methods of group lending and land collateral are hardly used, how Khan Bank and XacBank provided financial services successfully is a big question.

Microfinance in Mongolia

Formal finance continues to intensify in Mongolia despite the prevalence of informal finance. Commercial banks are the major providers of microfinance in the country. Among formal financial institutions, Khan Bank is one of the better regarded, especially in rural areas. It has transitioned from a state-owned agricultural bank to a private institution. From the assets of the former state bank, the agricultural bank was established in 1991 primarily to serve the agriculture and livestock sectors. It went into crisis in 1996-1999 as corruption and mismanagement impaired its liquidity and financial position. In 2003, the Government of Mongolia and the Central Bank reinvested jointly in and privatized the institution. The Sawada Holding Co., Ltd. of Japan purchased the bank through a bidding process (Lamberte 2006; Philippe 2006) and gave it its current name. Khan Bank is now the most dominant bank in Mongolia, especially in rural areas.

XacBank is another important financial institution in rural areas in Mongolia. It was established through the merging of the two

2 According to the 1994 Law of Mongolia on Land and subsequent land laws, Mongolian citizens are allowed to own land except pastureland, common land, and state land. Land tenure or usage is classified into three types: land ownership, land possession (long-term leasing), and land use (short-term leasing). Land ownership means the right to control land legitimately with the freedom to sell, rent, or lease and to pledge as collateral with financial institutions. However, land possession and land use do not include the right to sell, buy, or put in a pledge as collateral. For details, see Open Society Forum (2004).

3 Mongolia often experiences dzud, which is a combination of multiple natural disasters. Summer drought results in inadequate pasture and poor production of hay, and is followed by heavy winter snow and winds. Dzud occurs when the winter conditions do not allow livestock to access pasture and obtain adequate hay and fodder due to heavy snow cover.

Asian Journal of Agriculture and Development, Vol. 8, No. 2 31

decided to wait for new government policies on livestock insurance.

Progress of Mongolian Microfinance

Criteria for progress

In measuring progress4 in rural finance, two criteria are generally pointed out: (1) self-sustainability and (2) level of outreach among targeted populations or contribution to some specific purpose of society (Yaron 1991; Adams et al. 1991; Egaitsu 1988). The former is a criterion of market efficiency while the latter is a measure of social equity. The problem with rural development finance in low-income countries is that efficiency and equity do not necessarily go together. Policy for equity through intervention causes serious market distortion. Moreover, many researchers have pointed out that cheap loans directed to specific policy purposes (e.g., poverty alleviation) sometimes fail to attain goals or merely aggravate the situation (World Bank 1989; Adams 1998).

In this study, sustainability is considered a determinant of progress in rural finance. If this criterion is not fulfilled, finance is just a temporary phenomenon—a situation that is unacceptable. However, the researchers believe that sustainability alone does not create progress. Successful rural finance should contribute to rural development. Hence, both sustainability and contribution should be considered when evaluating progress in rural finance.

Self-sustainability is defined by the following indicators: (1) magnitude of deposit mobilization, (2) high rate of loan recovery, and (3) reasonably low transaction costs (Yaron 1991). Contribution includes the level

of outreach among targeted populations. The growth rate of credit provision and of the number of borrowers may serve as a crude proxy to the level of outreach of rural finance. In low-income countries, the most critical social issue is poverty, which is why the contribution criterion should reflect contribution to poverty reduction. However, due to limitations in data availability, this paper does not discuss the impact of credits on poverty alleviation.

The expansion of credit and the level of outreach

Table 1 shows the changes in lending performance of Khan Bank and XacBank, particularly changes in the number of borrowers, amount of outstanding loans, and average loan size. In addition, to calculate the real growth rate of loan provision, the index of inflation was also included. The growth of loans, as expressed by changes in the number of borrowers, outstanding loans, and average loan amount of Khan Bank and XacBank, is remarkable. In 2001-2009, the average annual growth rate of outstanding loans was 66 percent at Khan Bank and 72 percent at XacBank. In terms of the real growth rates (i.e., deducting the inflation rate from the nominal rate), it was found that the average real growth rates of outstanding loans at Khan Bank (56.5%) and XacBank (62.2%) were very high.

Moreover, the average annual growth rates of the number of borrowers for Khan Bank and XacBank were 21 percent and 38 percent, respectively. Average loan size also increased by 36.7 percent for Khan Bank and 24.6 percent for XacBank. These figures show that the loan provision from both banks was successful in

4 In this paper, the term “progress” is used instead of “success.” To evaluate Mongolian microfinance as successful, more rigorous criteria should be provided. However, there is insufficient data to analyze the country’s microfinance situation rigorously.

Orosoo Dulamragchaa and Yoichi Izumida32

terms of improving outreach. However, they do not indicate improvement in financial services for poor people. Though the span of outreach improved, it was difficult to determine whether its depth improved as well.

Concerning the changes in the loan repayment period of Khan Bank (figures are not listed), short-term loans were still dominant. However, the share of short-term loans in Khan Bank’s total loans declined from 92.1 percent to 64.1 percent. The excessive concentration of short-term loans improved.

In terms of lending activities, Khan Bank’s business was bigger than XacBank’s in 2009. However, the difference in growth rate was noticeable. XacBank had higher growth in loan provision and number of borrowers.

Mobilization of deposits

In terms of fundraising, growth in deposits was also strong during the period of analysis (Table 2 and Table 3). The amount of deposits in 2009 was nearly triple the amount at the end of 2005 for both banks. Even when the inflation

rate is taken into account (Table 1), the high growth of deposits in real terms remains.

Between demand deposit and term deposit, the growth of term deposits was particularly strong. As deposit commodities, the two banks supply saving commodities such as demand deposits, time deposits, and certificates of deposit.

Deposits as a source of total funds covered more than 90 percent of Khan Bank’s total funds in 2001-2007. This figure fluctuated during these periods but was still more than 87 percent in 2009. Consequently, it can be said that Khan Bank has a stable independent source of funds. Meanwhile, XacBank’s source of funds was diversified, possibly because the bank has only been operating for a few years. However, the amount of deposits mobilized from the public increased significantly. Thus, it can be said that deposit mobilization improved significantly for both banks.

Table 1. Lending activities of Khan Bank and XacBank

XacBank Number of borrowers Thousand 6.5 Thousand 84.3 13 37.8Outstanding loans Billion 2.7 Billion 198.4 74.5 71.7Average loan amount Thousand 406.9 Million 2.4 5.8 24.6

Inflation index 100 205.8 2.1 9.5Source: Annual reports of Khan Bank and XacBank and National Statistical YearbooksNote: USD 1 = MNT 1240

Asian Journal of Agriculture and Development, Vol. 8, No. 2 33

Loan recovery

In Mongolia, loan quality is measured by aged portfolio at risk. Loans are considered overdue if the principal of the loan has been delinquent for more than one day or if the loan was rescheduled or refinanced. The number of tardy days is based on the due date of the earliest loan installment that is not fully paid. With this definition, the loan recovery performance of the two banks was described (Table 4).

The loan recovery performance of both banks is good. On the average, the overdue ratio of both banks was less than 2 percent for all years. XacBank’s overdue loan rate was slightly lower than Khan Bank’s in 2003,

2007, and 2009. Khan Bank’s overdue rate increased sharply in 2009 because of the worldwide financial crisis and dzud. The high risk of nomadic activities urged XacBank to stop providing loans to herders, which means it may be risk averse as far as herder loans are concerned. However, Khan Bank, the successor of the former agricultural bank, upheld its mission and continues to offer financial services to the agricultural and livestock sector.

Efficiency of financial intermediation

From balance sheets and profit and loss statements of the banks, it is possible to calculate the efficiency of financial intermediation (Table

Table 2. Sources of Khan Bank funds (end of year, billion MNT)

Source: Compiled from XacBank annual reportsNote: XacBank was established in late 2001, and then started to accept deposits; figures on borrowings in 1999 and 2001

were those of former non-bank financial institutions.

Orosoo Dulamragchaa and Yoichi Izumida34

5). As an illustration of their operations in 2006, both banks had profits of 3-6 percent, with around 8 percent payment to funds including deposits, 20 percent interest revenue, and 7-9 percent expenses.

It is notable that the ratio of interest revenue to assets declined steadily for both banks. Meanwhile, the ratio of interest payment remained at an almost constant level. The ratio of expenses to total bank assets for both banks decreased steadily. This trend indicates that the activities of both banks improved in terms of financial intermediation efficiency.

Khan Bank’s ratio of interest revenue to assets declined sharply in 2009. As suggested earlier, this was caused by the world financial crisis as well as the natural disaster in the winter

of 2009. The profit rate of XacBank was also hit badly in 2009. However, this could be a temporary phenomenon. As far as a general trend is concerned, the efficiency of financial intermediation for both banks is moving in a good direction.

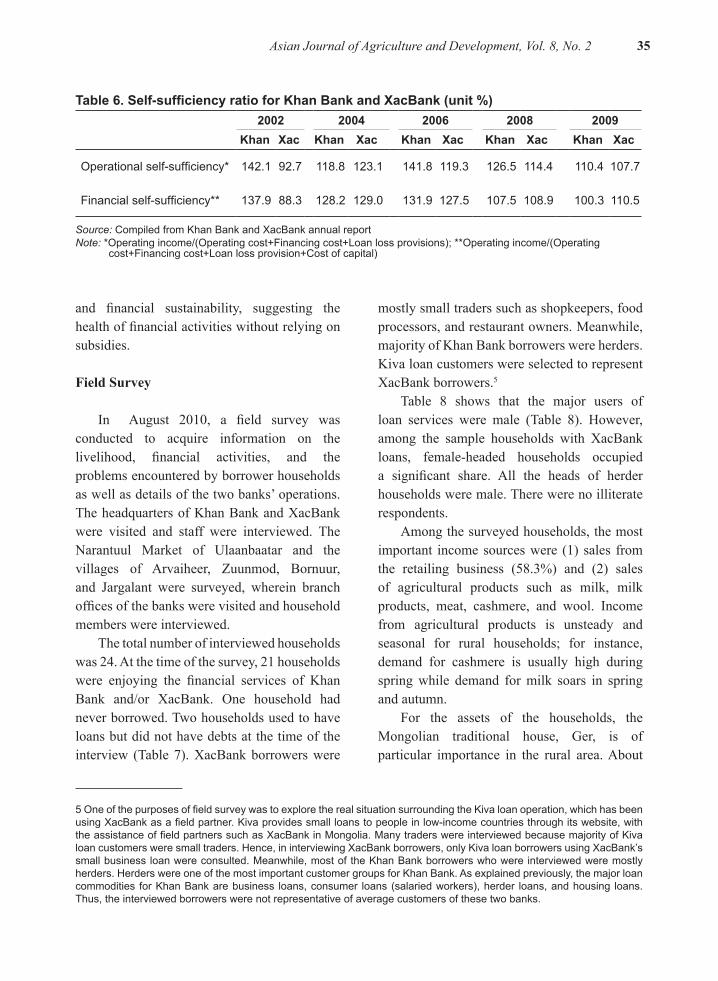

The analysis confirms that both banks fulfill the criteria (i.e., sustainability and contribution). However, sustainability has two more detailed indicators: operational self-sufficiency and financial self-sufficiency (Table 6). Apparently, both indicators for the two banks have been more than 100 percent. However, for Khan Bank, the latter indicator had approached the 100 percent line in 2009. This reflects the influence of the worldwide financial crises. Nonetheless, Khan Bank and XacBank have attained operational

Table 4. Overdue ratios of Khan Bank and XacBank

Unit2003 2007 2009

Khan Xac Khan Xac Khan XacGross loans and ad-vance

Source: Compiled from the annual reports of Khan Bank and XacBank

Table 5. Efficiency of financial intermediation by Khan Bank and XacBank (unit %)

2002 2004 2006 2008 2009

Khan Xac Khan Xac Khan Xac Khan Xac Khan Xac1. Ratio of interest revenue to assets* 22.41 24.18 20.69 24.03 20.06 19.70 18.06 16.79 13.82 14.74

2. Ratio of interest payment to assets** 7.76 4.92 10.98 7.99 8.21 8.38 7.35 8.31 6.83 8.00

3. Ratio of expenses to assets*** 11.52 20.88 8.38 12.09 7.02 9.08 6.72 6.99 5.62 6.02

4. Ratio of bank profit to assets**** 8.51 -2.04 3.95 4.90 6.48 3.47 4.12 2.29 1.44 1.13

Source: Compiled from Khan Bank and XacBank annual reportsNote: *Interest revenue/mid-year assets; **Interest payment to assets: interest payment/mid-year assets; ***Operational

expense/mid-year assets; ****Profit before tax/mid-year assets

Asian Journal of Agriculture and Development, Vol. 8, No. 2 35

Table 6. Self-sufficiency ratio for Khan Bank and XacBank (unit %) 2002 2004 2006 2008 2009

Source: Compiled from Khan Bank and XacBank annual report Note: *Operating income/(Operating cost+Financing cost+Loan loss provisions); **Operating income/(Operating

cost+Financing cost+Loan loss provision+Cost of capital)

and financial sustainability, suggesting the health of financial activities without relying on subsidies.

Field Survey

In August 2010, a field survey was conducted to acquire information on the livelihood, financial activities, and the problems encountered by borrower households as well as details of the two banks’ operations. The headquarters of Khan Bank and XacBank were visited and staff were interviewed. The Narantuul Market of Ulaanbaatar and the villages of Arvaiheer, Zuunmod, Bornuur, and Jargalant were surveyed, wherein branch offices of the banks were visited and household members were interviewed.

The total number of interviewed households was 24. At the time of the survey, 21 households were enjoying the financial services of Khan Bank and/or XacBank. One household had never borrowed. Two households used to have loans but did not have debts at the time of the interview (Table 7). XacBank borrowers were

mostly small traders such as shopkeepers, food processors, and restaurant owners. Meanwhile, majority of Khan Bank borrowers were herders. Kiva loan customers were selected to represent XacBank borrowers.5

Table 8 shows that the major users of loan services were male (Table 8). However, among the sample households with XacBank loans, female-headed households occupied a significant share. All the heads of herder households were male. There were no illiterate respondents.

Among the surveyed households, the most important income sources were (1) sales from the retailing business (58.3%) and (2) sales of agricultural products such as milk, milk products, meat, cashmere, and wool. Income from agricultural products is unsteady and seasonal for rural households; for instance, demand for cashmere is usually high during spring while demand for milk soars in spring and autumn.

For the assets of the households, the Mongolian traditional house, Ger, is of particular importance in the rural area. About

5 One of the purposes of field survey was to explore the real situation surrounding the Kiva loan operation, which has been using XacBank as a field partner. Kiva provides small loans to people in low-income countries through its website, with the assistance of field partners such as XacBank in Mongolia. Many traders were interviewed because majority of Kiva loan customers were small traders. Hence, in interviewing XacBank borrowers, only Kiva loan borrowers using XacBank’s small business loan were consulted. Meanwhile, most of the Khan Bank borrowers who were interviewed were mostly herders. Herders were one of the most important customer groups for Khan Bank. As explained previously, the major loan commodities for Khan Bank are business loans, consumer loans (salaried workers), herder loans, and housing loans. Thus, the interviewed borrowers were not representative of average customers of these two banks.

Orosoo Dulamragchaa and Yoichi Izumida36

Tabl

e 8.

Gen

eral

cha

ract

eris

tics

of th

e sa

mpl

e

Num

ber

of H

Hs

Hea

d of

Hou

seho

ldA

ge o

f hou

seho

ld h

ead

Aver

age

num

ber o

f fa

mily

mem

bers

Educ

atio

nal L

evel

Mal

eFe

mal

eH

ighe

stAv

erag

eLo

wes

tH

igh

scho

olSe

cond

ary

scho

olU

nive

rsity

Kha

n B

ank

Sm

all b

usin

ess

32

162

4535

4-

21

Her

der

44

-58

3925

4-

22

Xac

Ban

kS

mal

l bus

ines

s14

95

7352

.237

384

56

Non

-bor

row

ers

Sm

all b

usin

ess

22

-54

4944

3.5

-2

-H

erde

r1

1-

70-

-2

--

1To

tal

2418

6

4

119

Sou

rce:

Hou

seho

ld s

urve

y qu

estio

nnai

re 2

010

Tabl

e 7.

Num

ber o

f int

ervi

ewee

s by

bor

row

ing

activ

ity

Fina

ncia

l org

aniz

atio

n N

umbe

r of

hous

ehol

dsO

ccup

atio

n Sm

all

busi

ness

Her

der

Kha

n B

ank

73

4X

acB

ank

1414

From

Xac

Ban

k K

iva

loan

14

Xac

Ban

k ex

cept

Kiv

a lo

an

1C

urre

ntly

non

-bor

row

ers

2H

ave

neve

r acc

esse

d lo

an s

ervi

ces

1To

tal

2417

4S

ourc

e: S

urve

y qu

estio

nnai

reN

ote:

One

bor

row

er w

as a

Kiv

a lo

an c

lient

and

als

o ha

d a

loan

from

Xac

Ban

k. H

ence

, tha

t bor

row

er c

hose

mul

tiple

ans

wer

s.

Asian Journal of Agriculture and Development, Vol. 8, No. 2 37

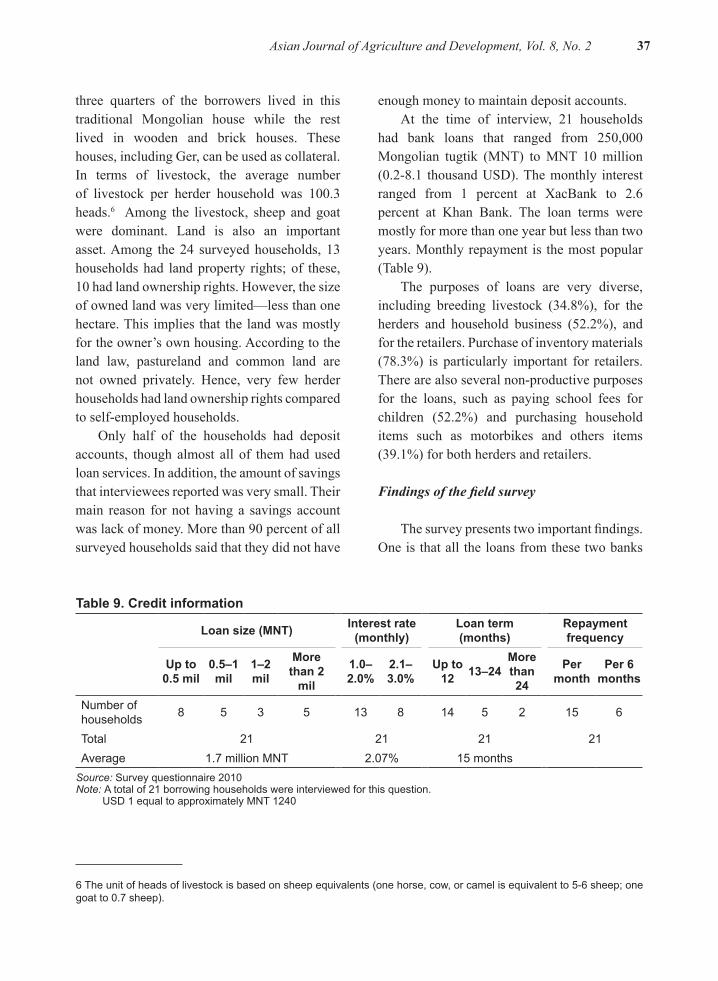

Table 9. Credit information

Loan size (MNT) Interest rate (monthly)

Loan term (months)

Repayment frequency

Up to 0.5 mil

0.5–1 mil

1–2 mil

More than 2

mil

1.0–2.0%

2.1–3.0%

Up to 12 13–24

More than 24

Per month

Per 6 months

Number of households 8 5 3 5 13 8 14 5 2 15 6

Total 21 21 21 21Average 1.7 million MNT 2.07% 15 months

Source: Survey questionnaire 2010Note: A total of 21 borrowing households were interviewed for this question. USD 1 equal to approximately MNT 1240

three quarters of the borrowers lived in this traditional Mongolian house while the rest lived in wooden and brick houses. These houses, including Ger, can be used as collateral. In terms of livestock, the average number of livestock per herder household was 100.3 heads.6 Among the livestock, sheep and goat were dominant. Land is also an important asset. Among the 24 surveyed households, 13 households had land property rights; of these, 10 had land ownership rights. However, the size of owned land was very limited—less than one hectare. This implies that the land was mostly for the owner’s own housing. According to the land law, pastureland and common land are not owned privately. Hence, very few herder households had land ownership rights compared to self-employed households.

Only half of the households had deposit accounts, though almost all of them had used loan services. In addition, the amount of savings that interviewees reported was very small. Their main reason for not having a savings account was lack of money. More than 90 percent of all surveyed households said that they did not have

enough money to maintain deposit accounts.At the time of interview, 21 households

had bank loans that ranged from 250,000 Mongolian tugtik (MNT) to MNT 10 million (0.2-8.1 thousand USD). The monthly interest ranged from 1 percent at XacBank to 2.6 percent at Khan Bank. The loan terms were mostly for more than one year but less than two years. Monthly repayment is the most popular (Table 9).

The purposes of loans are very diverse, including breeding livestock (34.8%), for the herders and household business (52.2%), and for the retailers. Purchase of inventory materials (78.3%) is particularly important for retailers. There are also several non-productive purposes for the loans, such as paying school fees for children (52.2%) and purchasing household items such as motorbikes and others items (39.1%) for both herders and retailers.

Findings of the field survey

The survey presents two important findings. One is that all the loans from these two banks

6 The unit of heads of livestock is based on sheep equivalents (one horse, cow, or camel is equivalent to 5-6 sheep; one goat to 0.7 sheep).

Orosoo Dulamragchaa and Yoichi Izumida38

were well secured with collateral. Another is that the borrowers did not obtain their desired loan amounts. The initial finding means that in Mongolia, a person without property to mortgage could not access loans. This is indirectly evidenced by the survey results. The second finding means that the amount of loans is constrained by the value of collateral.

All borrowers obtained loans by offering assets as collateral. In the case of loans for retailers, collateral such as Ger, other types of houses, and movable assets such as cars and motorcycles were widely used. In the case of loans to herders, livestock was the major form of collateral despite its variability and vulnerability to natural calamities. It should be noted that almost all kinds of assets are being used as collateral.

Staff in the main offices confirmed the presence of secured loans with collateral. Based on field survey results, the ratio of household borrowers using Ger and buildings was 60.9 percent. Meanwhile, the ratio of borrowers using movable assets was 56.5 percent.

The fact that the loans are secured by collateral leads to the next important finding: the amount of credit for existing or potential borrowers is constrained by the evaluated

value of the collateral.7 Many respondents complained that they failed to acquire the desired loan amount because of the limited evaluation of their collateral.

In this study, loan applications of 4 out of 21 cases were rejected due to lack of collateral. The number of households that were not able to get the desired amount of credits was 12 out of 21. The ratio of credit-constrained households was high (Table 10).

In Mongolia, it is very common for financial institutions to require collateral for loan provision. Moreover, it is unique that every kind of asset, both immovable and movable, is used for collateral. In addition, a personal (e.g., relatives, parents, sons, or daughters) or organizational (i.e., company that the borrower works for) guarantee is also used to secure consumption loans and loans for salaried workers. For example, if the applicant has insufficient collateral, family members who earn a good income can be responsible for the applicant’s debt.

The scope of collateral in Mongolian microfinance is wide and diverse. In the 1990s, after the transition period began, collateral was limited to immovable assets such as factories and houses. Almost all land in Mongolia was

Table 10. Credit constraints

Could not access loan services Could not borrow desired amountLoan application

was rejectedReason for the

rejectionCould not obtain desired amount Reason

No Yes Total Lack of collateral Other No Yes Total

Lack of collat-

eralOthers

Number of households 17 4 21 4 2 9 12 21 11 4

Source: Survey questionnaire 2010Note: Households selected multiple responses for reason of the rejection and could not obtain the desired loan amount

7 According to the bank manager, immovable, movable, and livestock assets are evaluated at 70 percent, 40 percent, and 30 percent of the market price, respectively. Moreover, herders who have at least 100 heads of livestock have the right to access loan provision.

Asian Journal of Agriculture and Development, Vol. 8, No. 2 39

not privatized; thus, land for financial collateral was seriously constrained. Furthermore, most financial institutions did not accept movable assets. Due to the lack of real estate to be pledged for loans, loan appraisal was conducted without appropriate measures for security. One factor for the financial crisis that started in 1996 was the lack of security in credit provision (Enkhkhuyag 2001).

The 1994 Land Law espoused the idea that land could be used as financial collateral, despite the fact that privatization of the major part of national land (pasture) was prohibited. In 2001, the Civil Law was amended to clarify the security on loan provision through collateral. It states that if borrowers fail to meet their contractual obligations, the loan collateral shall be transferred to the financial institutions. Also, with the expiration of the loan contract, financial institutions shall have the right to dispose of the collateral (Bank of Mongolia 2001). These changes in legal environment created the favorable conditions for financial institutions to develop effective measures in using immovable and movable assets as collateral.

Collateral, though expanded significantly to keep loan provisions secure, has restricted many poor households. Table 10 shows that more than half of the sampled households had experienced credit constraints. Moreover, livestock is vulnerable and risky as collateral due to serious natural calamities.8 Hence, overcoming credit constraints by minimizing the vulnerability of livestock collateral should be further researched.

Devices in Mongolian Microfinance9

As explained, the new concept of collateral was critical for Mongolian banks to provide financial services progressively. Thus, these banks have adopted several important measures.

The first device is promoting the application of new methods, which are mostly products of information technology development. Such methods include employment of customer information services provided by the credit bureau at the Central Bank, credit scoring, and mobile phone banking.

The Credit Information Bureau (CIB) was established in 1996 by the Bank of Mongolia (BoM). The CIB operated and accumulated a track record of borrowings manually until 2001. Now, CIB is using a computerized management information system (MIS). The CIB MIS allows lenders to get information on the borrowing situations of their customers, such as outstanding amounts of their loans from almost all financial institutions. The activity of CIB is useful in the provision of loan services for banks.

It is common for banks in Mongolia to use credit scoring in evaluating the creditworthiness of loan applicants. The scoring is based on a total evaluation of borrowers’ creditworthiness including operation risk, quality of collateral, credit record, and additional factors for evaluation of repayment capacity.10

Mobile phone banking seems to be a promising option as it offers wider access to potential customers with lower costs. This is

8 It was estimated that 12 million and 9.7 million animals died in 1998 and 2009, respectively. Of an estimated 190,000 herding households in 1998, 11,000 families lost all their animals (World Bank 2011).

9 Except for innovations mentioned in this section, the Mongolian Government provides strong assistance through basic statistical data via the National Statistical Office, and regulations via the Bank of Mongolia and the Financial Regulation Committee. Moreover, the local administration office provides the official data named “A” account (this official data includes all changes and movements of livestock) for rural bank branches.

10 Loan applicants’ operation risk – 50 points; quality of collateral – 30 points; credit records – 10 points; and additional factors for evaluation of repayment capacity – 10 points; total of 100 points.

Orosoo Dulamragchaa and Yoichi Izumida40

valid especially in a low population density country like Mongolia. Khan Bank was the first bank to introduce mobile phone banking in December 2007. XacBank followed with a mobile banking service called AMAR.

The second important device is utilizing incentive mechanisms for borrowers. These mechanisms include the following: (1) promoting on-time repayment by offering favorable interest rates for future loan applications of good customers, (2) putting money back into the saving accounts of on-time repayment customers in the case of Kiva loan borrowers (9% cash back on paid interest), and (3) banking services using mobile phones.

The third device refers to both banks’ personnel management. For instance, XacBank maximizes the energy and IT know-how of its staff, especially the younger generation, by offering salary and personal rating incentives. The workload given to officers is likewise adequate; hence, the officers do their work assignments effectively. It is also impressive that field officers know the economic situation of their customers very well. This is due to both banks’ policies. Each bank urges credit officers to conduct client visits. This “know your customer” approach, which encourages field staff to go to customers’ homes, is useful in determining the customers’ needs. It helps solve problems in information asymmetries in rural areas.

CONCLUSION

The performance of Khan Bank and XacBank as representatives of the Mongolian banking system is noteworthy. The growths of their services, including lending and deposits taking, loan recovery, and improvement in the efficiency of financial intermediation, were all satisfactory. These two banks have widened outreach and attained operational and financial sustainability.

Mongolian microfinance progressed when innovative methods especially the broadened definition of collateral were introduced. In addition, almost all kinds of assets, movable or immovable, qualify as collateral. The personal and organizational guarantee mechanism was also introduced and applied. New ideas on credit security have contributed immensely to the success of Mongolian microfinance.

Several challenges remain. First, XacBank and Khan Bank loans should reach the creditworthy poor without collateral. Second, borrowers’ credit is still constrained by the evaluated value of their collateral. Based on the survey, many borrowers complained that they did not obtain their desired loan amount because of limited evaluation of their collateral. Third, XacBank stopped herder loans in most areas due to many problems surrounding such loans, including high risk in Mongolia’s livestock sector. XacBank is now waiting for the new government program of livestock insurance.

Mongolian rural finance continues to face challenges. However, the methods used in the country are unique and can offer valuable insight on how to activate finance in less populated areas.

Asian Journal of Agriculture and Development, Vol. 8, No. 2 41

REFERENCES

Adams, D. W., H.Y. Chen, and M. Lamberte. 1991. Differences in Performances of Rural Financial Markets in Taiwan and the Philippines. Economics and Sociology Occasional Paper No. 1840. Ohio, USA: Department of Agricultural Economics and Rural Sociology, Ohio State University.

Bank of Mongolia and United Nations Development Program (UNDP) Mongolia. 2004. Subsector Review of the Legal Environment of Microfinance in Mongolia. Ulaanbaatar, Mongolia: UNDP.

Bank of Mongolia. 1999-2009. Annual Reports. Ulaanbaatar, Mongolia: Bank of Mongolia.

Egaitsu, F. 1988. “Rural Financial Markets: Two Schools of Thought.” In Farm Finance and Agricultural Development, 111-122. Tokyo, Japan: Asian Productivity Organization.

Enkhkhuyag, B. 2001. Lessons from the Past Ten Years (1991-2001) of Transition in the Banking System of Mongolia and Future Objectives. Ulaanbaatar, Mongolia: Monetary Policy and Research Department, Bank of Mongolia.

Vogel, R.C., and D. Sheets. 2006. “Rural Finance in Mongolia: Executive Summary.” In Beyond Microfinance, Building an Inclusive Rural Finance Market in Central Asia, edited by M.B. Lamberte, R.C. Vogel, R.T. Moyes, and N.A. Fernando, 159-175. Philippines: Asian Development Bank.

Minh-Huy, L., and I. Levard. 2006. “XacBank, Mongolia.” Planet Rating, April. http://www.planetrating.com/generer-pdf/PlanetRating_XacBank_2006_Final.pdf-142.htm

National Statistical Office (NSO) of Mongolia. 2000–2009. Mongolian Statistical Yearbooks. Ulaanbaatar, Monoglia: NSO.

Open Society Forum. 2004. Reforming Land Regulations in Mongolia: A Citizen’s Guide.

Ulaanbaatar, Mongolia: Open Society Forum in Mongolia.

Philippe, S., and J. Gutin. 2006. “Khan Bank, Mongolia.” Planet Rating, August. http://www.planetrating.com/generer-pdf/PlanetRating_Khan%20Bank311006.pdf-198.htm

The World Bank. 1989. World Development Report: Financial Systems and Development. Washington D.C., USA: The World Bank.

The World Bank. 2010. World Development Report: Development and Climate Change. Washington D.C., USA: The World Bank.