19

Topic: Project Cost Managment Presented by Muhammad Hanif (12PG142) Under the supervision of Sir Khalil Rehman Memon

| Date post: | 06-Aug-2015 |

| Category: |

Business |

| Upload: | honey-chachar |

| View: | 28 times |

| Download: | 1 times |

Topic: Project Cost Managment

Presented by Muhammad Hanif (12PG142)

Under the supervision of Sir Khalil Rehman Memon

Contents

©Objectives of Presentation

© Introduction

©What is PCM

©Cost Management Process

©Cost Types

Objectives of Presentation

Through this interaction, participants will enhance their:

Level of Knowledge and

Skills of project cost management

Introduction

• Cost Management(CM): Includes processes required to ensure that the project is completed within the approved budget.

• CM is a form of Management accounting that allows a business to predict impending expenditures to help reduce the chance of going over budget.

Project Cost Management (PCM) What is PCM?

You might think that PCM is managing the "costs" on your project.

The reality is that you must manage everything else that incurs cost .

Because if you don't, the costs will just keep on climbing.

Whether you like it or not!

What is PCM?Project Cost Management is

o Placing of responsibility on those in charge of any aspect of the project.• E.g. the managers, designers and implementers

o To perform their respective roles and responsibilities within prescribed limits.

• Specifically, agreed cost allowances or budgets

o Then collecting cost data and comparing it to the corresponding allowances.

o And taking appropriate management action.

o To contain the final results.

Cost Management Process

Estimate cost

Determine budget

Control cost

Estimate cost

• The Process of developing an approximation (estimate) for the cost of the resources (material and human) necessary to complete the project activities.

Determine budget1. It is useful to first understand where we are in the planning process.

2. An activity list was created and sequenced into a simple network diagram..

3. The amount of resources and the duration of each activity was then estimated to produce the project schedule baseline.

4. It is from this baseline that cost estimates for each activity was determined,

5. and it is determine budget that converts those individuals activity cost estimates into the budget itself.

Control cost• The practice of managing and/or reducing business expenses.

• Cost controls starts by the businesses identifying what their costs are and evaluate whether those costs are reasonable and affordable.

• Then, if necessary, they can look for ways to cut costs through methods such as cutting back, moving to a less expensive plan or changing service providers.

• The cost-control process seeks to manage expenses ranging from phone, internet and utility bills to employee payroll and outside professional services.

Cost TypesSunk Costs:

Fixed Costs:

Variable Costs:

Direct Costs:

Indirect Costs:

Opportunity Costs:

SUNK COST

• A cost that has already been incurred and cannot be recovered.

Fixed Cost

• Expenses that do not change as a function of the activity of a business, within the relevant period.

Variable Cost

• Cost that vary depending on a company's production volume; they rise as production increases and fall as production decreases.

Direct Cost

• Direct costs refer to materials, labor and expenses related to the production of a product.

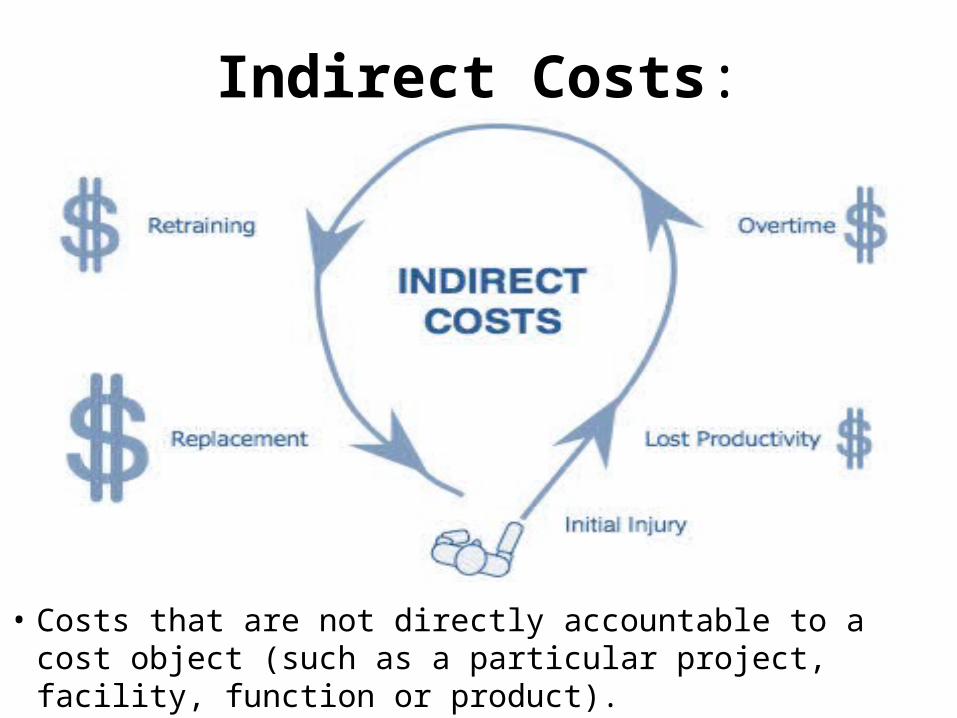

Indirect Costs:

• Costs that are not directly accountable to a cost object (such as a particular project, facility, function or product).

Opportunity Costs:

• When choosing between two options, it can be helpful to determine the opportunity cost of picking one option over the other to see which would be the most beneficial option.