A STUDY ON SIGNIFICANT DIFFERENCES IN CREDIT RATINGS BY RATING AGENCIES Summer Internship Report by Prateek Gupta, April-May, 2014 Mentor: Ms Manushree Saggar Assistant Vice President Faculty Advisor: Ms Nidhi Kaicker SBPPSE, AUD Faculty Mentor: Dr. Kartik Dave

Transcript

A STUDY ON SIGNIFICANT DIFFERENCES IN CREDIT

RATINGS BY RATING AGENCIES

Summer Internship Report by Prateek Gupta, April-May, 2014

Mentor: Ms Manushree Saggar

Assistant Vice President

Faculty Advisor: Ms Nidhi Kaicker SBPPSE, AUD

Faculty Mentor: Dr. Kartik Dave

2

Acknowledgement First, I express my sincere gratitude to Ms Manushree Saggar, Assistant Vice-

President, Banking and Finance, ICRA Limited for allowing me to conduct this

project under her auspices. I am especially grateful for her confidence and the

freedom she gave me to do this work.

As a supervisor, Ms Manushree Saggar supported me in all stages of this work. She is

the initiator of this project and always gave me constant encouragement and advice,

despite her busy agenda. Without a coherent and illuminating instruction, this project

would not have reached its present form. I would like to thank her for the patient and

continuous guidance, encouragement, meticulous suggestions she has provided

throughout my work.

My sincere thanks to Mr. Puneet Maheshwari, Senior Analyst, Banking and Finance,

ICRA Limited and Ms. Monica Sharma, HR manager, ICRA Limited for their

constant support, help and cooperation throughout the project and for making me feel

so welcomed at ICRA Limited.

I would like to acknowledge the assistance of Mr. Ravi Rao, Mr. Saurabh Mittal who

offered me valuable suggestions for this study and express my gratitude for giving

their vital inputs, without which the study would not have been possible.

I would also like to express my thanks to Ms. Nidhi Kaicker, Assistant Professor,

School of Business, Public Policy and Social Entrepreneurship, Ambedkar University

Delhi for all the support and assistance.

Lastly I would like to extend my sincere thanks to all members of the ICRA Limited,

and all those who contributed directly or indirectly to this project.

PRATEEK GUPTA

MBA, BATCH-2015

SCHOOL OF BUSINESS, PUBLIC POLICY AND SOCIAL ENTREPRENEUSHIP

Introduction ................................................................................................................................... 5 Importance of credit ratings ................................................................................................................... 5

Credit Rating in India ................................................................................................................. 7 Credit Rating in Recent Times .................................................................................................. 9

Executive Summary It has been observed that credit ratings of companies have been gaining a lot of

importance lately specially after the US financial crisis and investors often use these

ratings as important information for various financial purposes and investment

decisions. Therefore the aim of this report was to investigate if there were any

differences in the credit ratings provided by different credit rating agencies to the

same companies, and if any, why? For this purpose a dataset was prepared from

various secondary sources to sort out the same set of companies credit rated by the

two largest credit rating agencies in India i.e. CRISIL and ICRA Limited. The method

of research used was statistical analysis using SPSS software. The dataset was

analyzed using paired sample t test by comparing the means of ratings provided by the

two rating agencies for all the companies, industry sector wise and on the basis of

them being listed or not. The goal of this paper was to check whether the null

hypothesis i.e. “ There is no significant difference in the credit ratings given by

CRISIL and ICRA to the same set of companies” was true or false and the results

were surprising.

According to the statistical tests run, it showed that there were significant difference

in the ratings provided by two different rating agencies for all companies, core

industry sectors such as Chemicals, pharmaceuticals, textiles, education, health,

consumer services, construction and engineering and non-listed companies. There

were often different ratings given by these two agencies for the same companies.

Going further as to why these differences in the ratings even when the parameters on

which these companies are rated are usually the same, it was found that firstly credit

ratings are subjective and there is no fixed format or rationale followed by any rating

agency and it is the opinion of any individual rating agency. Secondly ICRA Limited

ratings reflect the likelihood that an obligator will default as well as loss given default

whereas CRISIL ratings reflect only the probability of default. Thirdly ICRA follows

a notching policy whereas CRISL doesn’t and this is the reason CRISIL rating is

usually more positive than ICRAs. All the above-mentioned reasons add to the

difference seen in the ratings given by these two agencies for the set of companies.

5

Chapter 1 Introduction Credit ratings are letter designations assigned by credit rating agencies, which

evaluate the credit worthiness of a debtor (a company in the case of corporate credit

ratings) based on its ability to pay back debt and the likelihood of default.

(Kaur & Kaur, 2011) in their study on rating methodologies of credit rating agencies

said Credit rating is the symbolic indicator of the current opinion of rating agencies

regarding the relative capability of issuer of debt instrument, to service the debt

obligations as per contract. The corporations with specialized functions namely,

assessment of the likelihood of the timely payments by an issuer on a financial

obligation is known as Credit Rating Agencies.

Importance of credit ratings In the post reforms period, with increase in activity and operations in the Indian

Financial sector, both new and existing companies are opting for finance from the

Indian Capital Market. The competition among the firms has also increased by an

excessive amount and the importance of credit ratings have also increased globally.

The importance of Credit Rating is significant as it can be seen as an investor service,

which establishes a link between risk & return. They also provide a yardstick against

which to measure the risk inherent in any instrument. Most importantly it helps in the

development of financial markets and therefore has an increased importance. Since an

investor uses the ratings to assess the risk level and compares the offered rate of

return with expected rate of return to optimize his risk return trade off. The risk

perception of a common investor in the absence of a rating system largely depends on

his familiarity and his knowledge of the financial market and the names of the

promoters and collaborators. Therefore, credit ratings play an important role of

reducing the knowledge gap or information symmetry between borrowers and lenders.

(Adelson, 2012) in a recent study observed that the importance of credit rating is

increasing was mainly due to the fact that there was a gap in distinction between high

risk borrower and low risk borrowers and the lenders charged all borrowers the same

rate of interest and volume of borrowing by low risk borrowers was suffering and

lenders would in turn misallocate productive resources away from low risk borrowers

which in turn would make the economic output suboptimal. It also helps the issuers of

6

debt instruments to price their issues correctly and to reach out to new investors.

Another way of describing the importance of credit rating is in terms of market

efficiency where they contribute to the operations of marketing. It helps to improve

market function and efficiency by reducing the ability of one investor to outperform

another by making better judgments about creditworthiness and puts investors on

equal footing. Given the systemic superstructure position that the Credit Rating

Agencies have come to occupy as information and insight gatekeepers, they play an

important role in the modern capital markets. Their importance is to various

stakeholders such as Investors, Issuers, Banks, and Regulators. To the investors, given

the vast amount of information available to them, some being valuable and some not,

CRAs play a useful role in helping investors sift through information and analyze the

credit risks they face when lending or purchasing. Issuers also rely on credit ratings as

an important tool to access investors and to reach a wider investor base. For Banks,

they are likely to save capital if they get loan rated, although it’s not mandatory under

BASEL II norms to get credit rating. The banks can save up capital if its credit rating

is high as their Risk weight1 would be less then and it is in turned passed on to the

borrower company in terms of reduced basis points. Regulators use ratings for

regulatory purposes. Firstly under BASEL II norms of the Basel Committee on

banking supervision, banking regulators can accredit credit rating agencies based on

some criteria and the ratings assigned by these External Credit Assessment

Institutions are used to assign risk weights to various bank exposures in calculating

capital charge. Thus, it provides comfort to the regulators in their assessment of

product risks and overall systemic risks. Secondly the increasing levels of default

resulting from easy availability of finance, has led to the growing importance of the

credit rating. The other factors are growth of information technology, Globalization of

financial markets, Increasing role of capital and money markets, Lack of government

safety measures, The trend towards privatization, Securitization of debt.

1 In terms of the minimum amount of capital that is required within banks and other institutions, based on a percentage of the assets, weighted by risk. For example, the loans that are secured by letter of credit would be weighted riskier than a mortgage loan that is secured with collateral.

7

Credit Rating in India (Kumar & Rao, 2012) in a recent study examined the Credit rating business in India

and declared the same to be a sweet spot as it is on the cusp of robust growth

potential, driven by three triggers: Strong capex cycle in Indian economy, lower

penetration of corporate bond market and regulatory push due to implementation of

Basel II norms.

Credit ratings are playing an increasingly important role in financial markets. In India,

rating is a more recent phenomenon, but the changing global perspectives on the

subject do impact the financial system. India was perhaps the first amongst

developing countries to set up a credit rating agency in 1988. The function of credit

rating was institutionalized when RBI made it mandatory for the issue of Commercial

Paper (CP) and subsequently by SEBI, when it made credit rating compulsory for

certain categories of debentures and debt instruments. In June 1994, RBI made it

mandatory for Non- Banking Financial Companies (NBFCs) to be rated. Credit rating

is optional for Public Sector Undertakings (PSUs) bonds and privately placed non-

convertible debentures up to Rs. 50 million. Fixed deposits of manufacturing

companies also have the option to get rated. The Reserve Bank of India liaises with

SEBI, on the issue of rating agencies’ adherence to IOSCO Code of Conduct

Fundamentals.

The Ratings industry in India has been built up to its present position over a period of

fifteen years. Over the years, credit ratings have evolved into a 90-crore market, with

four agencies providing rating services, and significant pull from investors for the

product. (Raghunathan & R. Varma) in a recent study examined that the ratings

business in India has seen two phases. During the first of these phases, there was no

experience of credit ratings, and virtually no awareness, on the part of investors and

issuers.

The second phase saw the advent of regulatory support for credit ratings, with the

introduction and increasing rigor of regulations covering primarily the markets for

public issue of debt and for fixed deposits, aimed at protecting smaller investors, these

measures also amounted to regulatory recognition of the role of credit ratings and the

quality of the effort put in till then, in estimating credit quality. With these measures,

credit ratings rapidly passed out of the arcane realm of high finance, and into the

8

lexicon of the individual market participant. This phase also saw the arrival of

competition, in the form of other domestic agencies entering the market.

In India the rating activities started with the incorporation of the Credit Rating

Information Services of India Ltd. (CRISIL) in 1987 which commenced its operations

of rating of companies in 1987-1988 and was promoted by Industrial Credit and

Investment Corporation of India Ltd. (ICICI) and Unit Trust of India (UTI). The

second rating agency Investment Information and Credit rating Agency of India Ltd.

(ICRA) was incorporated in 1991 and was jointly sponsored by Industrial Finance

Corporation of India (IFCI) and other financial institutions and banks. The other

rating agency, Credit Analysis and Research Ltd. (CARE), incorporated in April

1993, is a credit rating information and advisory services company promoted by

Industrial Development Bank of India (IDBI) jointly with Canara Bank, Unit Trust of

India (UTI), private sector banks and financial services companies. Another rating

agency Onicra Credit Rating Agency of India Ltd., which was incorporated in 1993, is

recognized as the pioneer of the concept of individual credit rating in India. Further

Duff and Phelps Credit Rating (India) Private Ltd. (DCR) was established in 1996,

which is presently known as Fitch Ratings India Private Ltd. One more rating agency

SME Rating Agency of India Limited (SMERA), which was a joint venture of SIDBI,

Dun & Bradstreet Information Services (D&B), Credit Information Bureau of India

Limited (CIBIL), and 11 other leading banks in the country, was established in 2005.

Further Duff and Phelps Credit Rating (India) Private Ltd. (DCR) was established in

1996, which is presently known as Fitch Ratings India Private Ltd. One more rating

agency SME Rating Agency of India Limited (SMERA), which was a joint venture of

SIDBI, Dun & Bradstreet Information Services (D&B), Credit Information Bureau of

India Limited (CIBIL), and 11 other leading banks in the country, was established in

2005. A new rating agency, Brickwork Ratings (BWR) that is based in Bangalore was

incorporated in 2007. Besides CRISIL (Standard & Poor), ICRA (Moody’s), CARE

and Fitch, Brickwork Ratings is the fifth Credit Rating Agency to be recognized by

SEBI.

9

Credit Rating in Recent Times Given the slump faced by economies globally and the rise in the number of

defaultees, it is about time that the economy had a strong credit rating system in place

to ensure smooth operation for the entire chain. The most significant change in recent

relates to emphasis on their accountability and more important, the caution in

regulators’ use of ratings. With the increasing market orientation of the Indian

economy, investors value a systematic assessment of two types of risks, namely –

business risk arising out of the open economy and linkages between money, capital

and foreign exchange markets and –payment risk. With a view to protect small

investors, who are the main target for unlisted corporate debt in the form of fixed

deposits with companies, credit rating has been made mandatory. In the recent times,

the world witnessed the worst financial crisis that began in the United States in 2007

with problems in the subprime mortgage market and credit rating agencies were

largely held responsible for it as they underestimated the risks associated with

structured credit products and failed to adjust their ratings quickly enough to

deteriorating market conditions. It is believed that the rating methods adopted by

different agencies and the differences in the ratings assigned by different credit rating

agency to the same company were significantly different, and were one of the main

reasons behind the crisis. Therefore the importance of credit ratings and regulation of

credit rating agencies has increased in the recent times. This happened mainly because

of the shortcomings such as they lowered the perception of credit risk by giving AAA

ratings to senior tranches of structured finance products like collateralized debt

obligations, same rating they gave to the government and corporate bonds yielding

systematically lower returns. Also there were flaws in rating methodologies such as

the lack of sufficient historical data relating to the US subprime market, an inability to

take into account the severe weakening of underwriting standards by originators,

overreliance on mathematical and statistical methodologies based on inadequate data,

failure to take account of interdependencies, disregard of conflict of interests. Since

then the agencies have been regulated strictly and in the US, they have been subject to

SEC oversight in the form of disclosure requirements. In the US CRA’s2 are officially

registered as NRSROs3, and the system was introduced in 1975, fundamentally

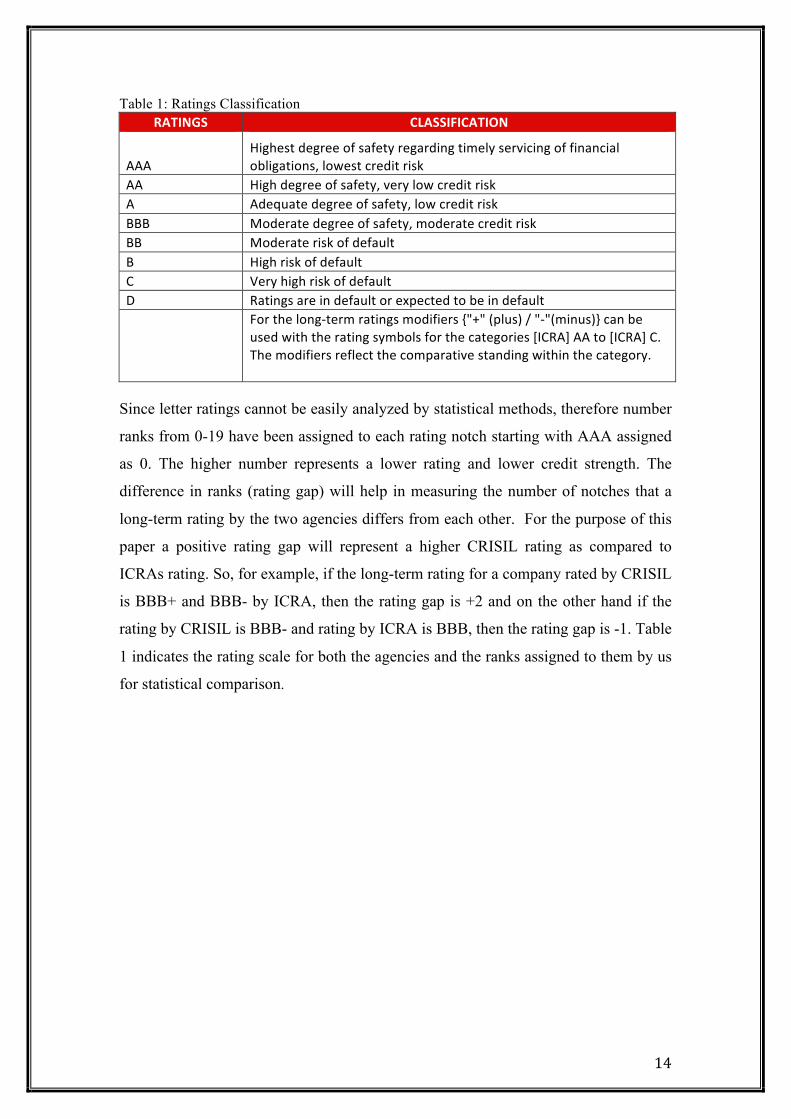

AAA Highest degree of safety regarding timely servicing of financial obligations, lowest credit risk

AA High degree of safety, very low credit risk A Adequate degree of safety, low credit risk BBB Moderate degree of safety, moderate credit risk BB Moderate risk of default B High risk of default C Very high risk of default D Ratings are in default or expected to be in default

For the long-‐term ratings modifiers {"+" (plus) / "-‐"(minus)} can be used with the rating symbols for the categories [ICRA] AA to [ICRA] C. The modifiers reflect the comparative standing within the category.

Since letter ratings cannot be easily analyzed by statistical methods, therefore number

ranks from 0-19 have been assigned to each rating notch starting with AAA assigned

as 0. The higher number represents a lower rating and lower credit strength. The

difference in ranks (rating gap) will help in measuring the number of notches that a

long-term rating by the two agencies differs from each other. For the purpose of this

paper a positive rating gap will represent a higher CRISIL rating as compared to

ICRAs rating. So, for example, if the long-term rating for a company rated by CRISIL

is BBB+ and BBB- by ICRA, then the rating gap is +2 and on the other hand if the

rating by CRISIL is BBB- and rating by ICRA is BBB, then the rating gap is -1. Table

1 indicates the rating scale for both the agencies and the ranks assigned to them by us

for statistical comparison.

15

Table 2: Ranking chart for CRISIL and ICRAs ratings CRISIL ICRA Rank AAA AAA 0 AA+ AA+ 1 AA AA 2 AA-‐ AA-‐ 3 A+ A+ 4 A A 5 A-‐ A-‐ 6

BBB+ BBB+ 7 BBB BBB 8 BBB-‐ BBB-‐ 9 BB+ BB+ 10 BB BB 11 BB-‐ BB-‐ 12 B+ B+ 13 B B 14 B-‐ B-‐ 15 C+ C+ 16 C C 17 C-‐ C-‐ 18 D D 19

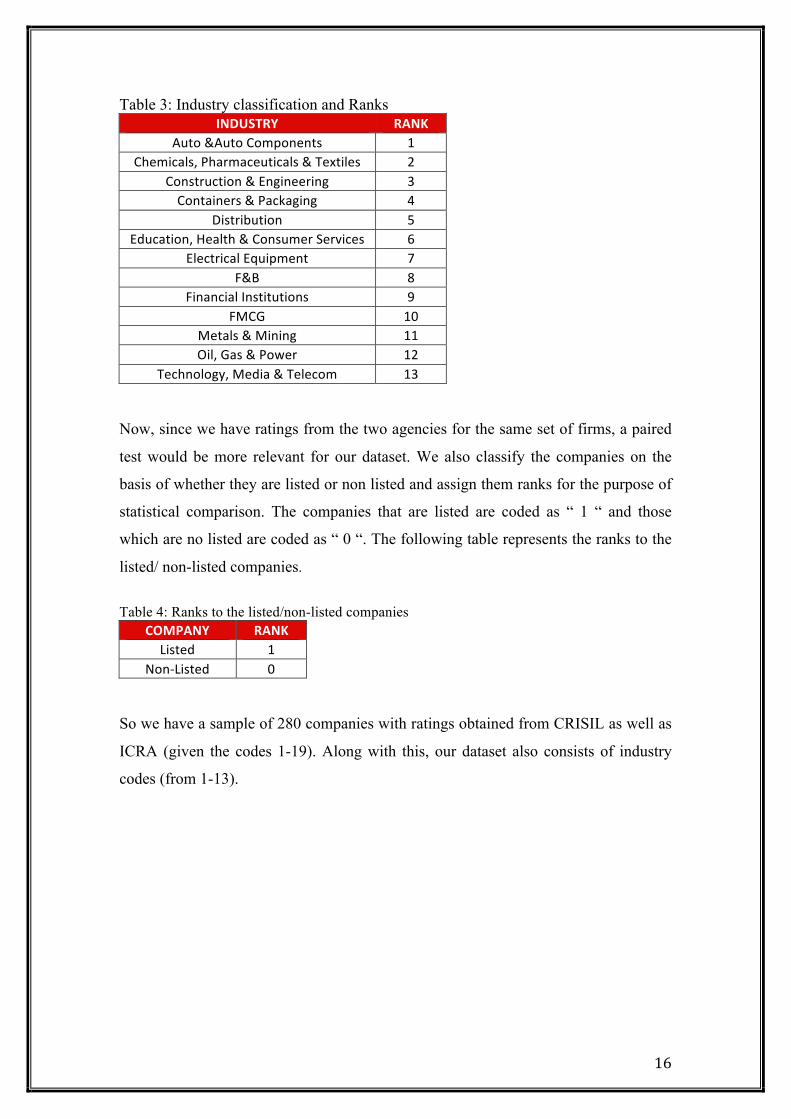

Source: CRISIL rating scan, ICRA rating guide, ICRA website The companies chosen belonged to several different industries and have been

classified by us into 13 different industries for the purpose of comparison. The

industries are namely; Technology, Media & Telecom, Financial Institutions,

FMCGs, Auto & Auto components, Metals & Mining, Chemicals, Pharmaceuticals &

Textiles, Construction & engineering, Oil & Gas, Education, Health & Consumer

Service, Containers & Packaging, Distribution, Electrical Equipment, F&B. These

industries have also been assigned ranks from 1-13 respectively. The following table

represents the industry sectors along with their ranks for the purpose of statistical

analysis.

16

Table 3: Industry classification and Ranks INDUSTRY RANK

Auto &Auto Components 1 Chemicals, Pharmaceuticals & Textiles 2

Construction & Engineering 3 Containers & Packaging 4

Distribution 5 Education, Health & Consumer Services 6

Electrical Equipment 7 F&B 8

Financial Institutions 9 FMCG 10

Metals & Mining 11 Oil, Gas & Power 12

Technology, Media & Telecom 13

Now, since we have ratings from the two agencies for the same set of firms, a paired

test would be more relevant for our dataset. We also classify the companies on the

basis of whether they are listed or non listed and assign them ranks for the purpose of

statistical comparison. The companies that are listed are coded as “ 1 “ and those

which are no listed are coded as “ 0 “. The following table represents the ranks to the

listed/ non-listed companies.

Table 4: Ranks to the listed/non-listed companies COMPANY RANK

Listed 1 Non-‐Listed 0

So we have a sample of 280 companies with ratings obtained from CRISIL as well as

ICRA (given the codes 1-19). Along with this, our dataset also consists of industry

codes (from 1-13).

17

Methodology Using the dataset constructed as mentioned above, we use the Paired difference t test

to check the following-

♦ Whether there is a significant difference in ratings for all companies

♦ Whether there is a significant differences in ratings for companies

disaggregated by industry sectors

♦ Whether there is a significant difference in ratings for listed companies and

non-listed companies

The test used is as follows:

• PAIRED DIFFERENCE t TEST:

o This t‐test compares one set of measurements with a second set from

the same sample. It is often used to compare “before” and “after”

scores in experiments to determine whether significant change has

occurred. A t-test is any statistical hypothesis test in which the test

statistic follows a Student's t distribution if the null hypothesis is

supported. It can be used to determine if two sets of data are

significantly different from each other.

The formula for t test is -‐

o In the above formula, x is the mean of the change scores, Δ is the

hypothesized difference (0 if testing for equal means), s is the sample

standard deviation and n is the sample size.

A paired difference t test will be used to test the null hypothesis that the average

ratings from both agencies do not differ significantly. We will run the tests for overall

sample, individual industry sectors, listed and unlisted companies and companies on

the basis of their market capitalization, which will help us to find the trends in

differences in credit ratings. We will be using simple t test (paired difference of

means test) first, as our objective is to see if any significant differences are there in

the means of the population. The t test is conducted on paired data where the null

hypothesis would be that there are no significant differences in the means of the

ratings given by CRISIL & ICRA. The paired t test assumes that the data are

measured on an interval or a ratio scale and are normally distributed.

18

For the purpose of our analysis, we will use hypothesis testing where:

Null hypothesis: H0: µ1 = µ2 (There is no significant difference in the ratings by two

agencies)

Alternate Hypothesis: H1: µ1 ≠ µ2 (There is a significant difference in the ratings by

two agencies)

Significance level is α = 0.05

• µ1 = mean value of the ratings assigned ICRA to the same set of companies

• µ2 = mean value of the ratings assigned by CRISIL to the same set of

companies

With the help of the methodology explained above, we would perform the statistical

paired sample t test in SPSS and analyze the results on the basis of the tables obtained

from performing the test. This will help us in checking whether our null hypothesis is

true or false i.e. whether there are any significant differences in the ratings assigned

by CRISIL and ICRA Limited to the same set of companies. The test would be

performed for all the companies, companies belonging to specific industry i.e.

industry wise whether the significant difference is there or not for any particular

industry and also whether there is any significant difference for companies which are

listed or non-listed.

19

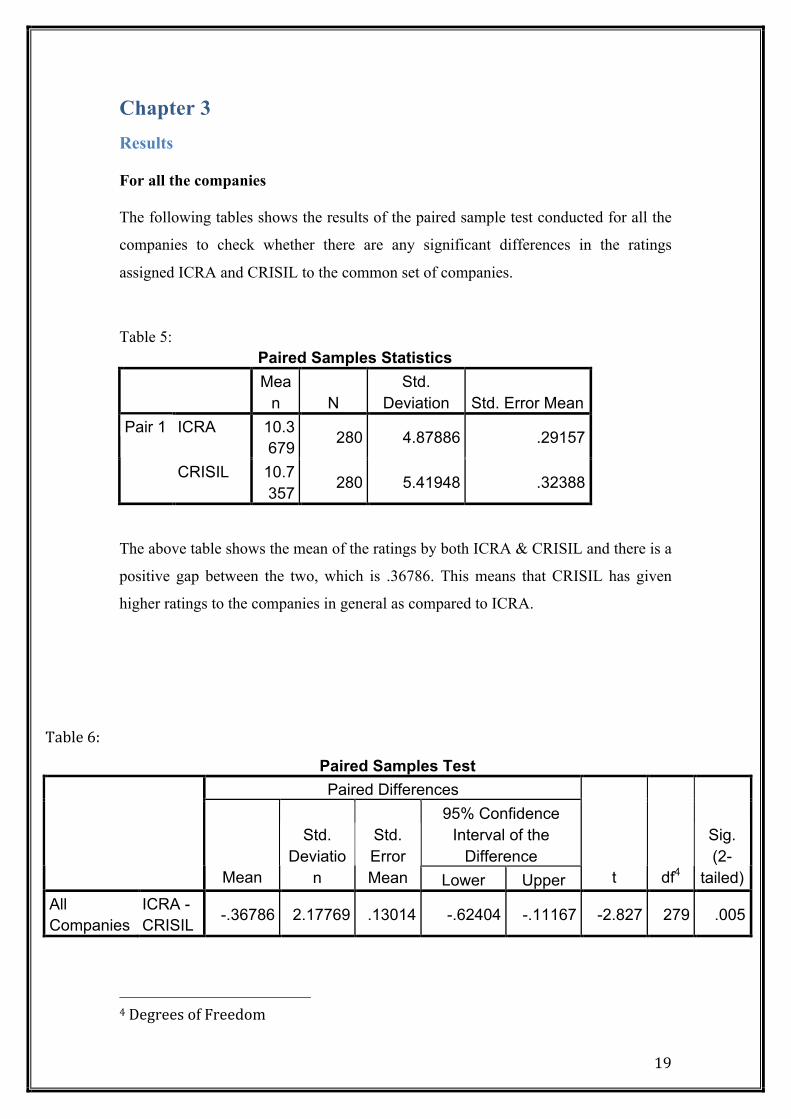

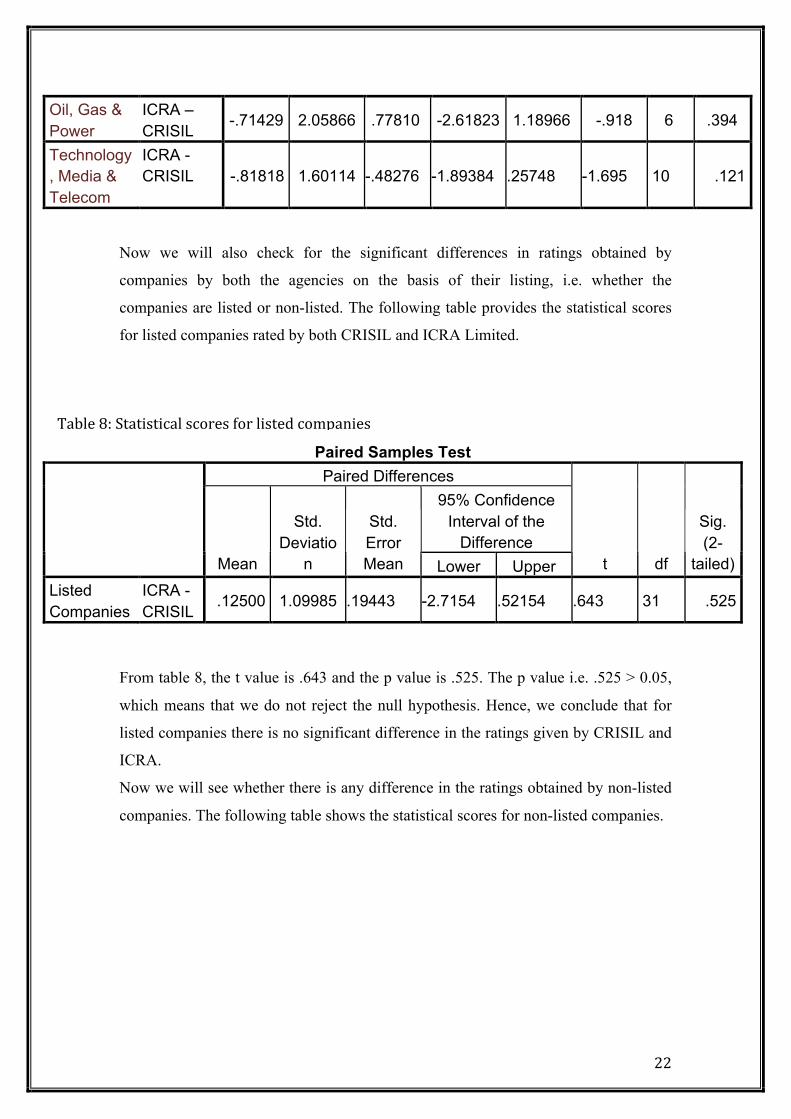

Chapter 3 Results For all the companies The following tables shows the results of the paired sample test conducted for all the

companies to check whether there are any significant differences in the ratings

assigned ICRA and CRISIL to the common set of companies.

Table 5:

Paired Samples Statistics

Mea

n N Std.

Deviation Std. Error Mean ICRA 10.3

679 280 4.87886 .29157 Pair 1

CRISIL 10.7357

280 5.41948 .32388

The above table shows the mean of the ratings by both ICRA & CRISIL and there is a

positive gap between the two, which is .36786. This means that CRISIL has given

higher ratings to the companies in general as compared to ICRA.

Table 9: Statistical scores for Non-‐Listed Companies

24

Chapter 4 Conclusion This paper analyzed the ratings from CRISIL and ICRA Limited to study the biases

and trends between the two rating agencies. The results were both encouraging and

surprising at the same time. The most important result was that ICRA’s ratings have

been consistently lower than the ratings given by CRISIL to the same set of

companies in most of the cases. The difference was statistically significant. As

suspected, there are biases and differences in the ratings for different industry sectors,

which are apparent in the difference in average ratings.

Again factors like one agency being overall more lenient or conservative or having

different rating policies for different industries maybe one of the reasons for this but

usually it has been observed that credit ratings are subjective. There are no standard or

agreed upon methods to measure the accuracy of credit ratings and this is partly

because of the subjective nature of credit ratings. Also the performance of credit

ratings may not be comparable across different industry standards, i.e. defaults and

rating changes may not be consistent for each rating category across sectors. Credit

rating agencies also use different analytical approaches and levels of subjectivity

when determining credit ratings. They may differ in the time horizon that their ratings

address. For example, some credit rating agencies aim for stability in ratings so they

assume a longer term horizon in their analysis whereas other credit rating agency

might prefer to address short term risks and events, that can lead to more variability in

their ratings. Additionally, some credit rating agencies’ ratings only reflect the

likelihood that an obligator will default, while others’ ratings also consider the

expected loss that may result from a default. Similar is the case with CRISIL and

ICRA, hence, the significant differences in their ratings for the same set of companies.

CRISIL’s ratings reflect the probability of default whereas ICRA considers loss given

default while determining credit ratings. Usually big rating agencies have almost a

similar rating rationale, so is the case with CRISIL and ICRA, they follow and

consider the same parameters while determining a credit rating for a company i.e.

Business Risk and Financial Risk yet sometimes within those parameters there might

be some differences and as we said that it is totally of a subjective nature, therefore

even when analyzing according to the same rationale, the analysis might be

25

subjective. One more reason could be that for CRISIL while doing bank ratings, it

does not follow notching while rating upper tier II and upper tier I capital and

assumes it to be the same whereas ICRA follows a notching policy which might add

to the reasons behind the differences in ratings by these two agencies.

Overall it appears that ICRA has a bias towards lower rating as compared to CRISIL.

It is imperative for investors, regulators and analysts to note that the two ratings are

not equivalent and should not be treated as the same as it provides valuable insights to

investors in taking financial investment decisions as these credit ratings help them to

compare risks associated with it and offers diverse views on the creditworthiness of

an investment.

26

Bibliography (n.d.). Retrieved from www.smallb.in: http://smallb.in/%20/fund-‐your-‐business%20/credit-‐rating%20/msme-‐rating%20/rating-‐agencies-‐india Adelson, M. H. (2012, May 17). S&P The Role of Credit Ratings in Financial System. Retrieved from www.standardandpoors.com: http://www.standardandpoors.com/ratings/articles/en/us/?articleType=HTML&assetID=1245333790527#ContactInfo Cantor, R., & Packer, F. (1997, May 30). Differences of opinion and selection bias in the credit rating industry. Journal of Banking & Finance . Cantor, R., & Packer, F. (1995, December). Multiple Ratings and Credit Standards: Differences of opinion in the credit rating industry. 32. 32. Federal Reserve Bank of New york. Elkhoury, M. (2008). Credit Rating Agencies and Their Potential Impact on developing Countries. United Nations Conference on Trade and Development. Ghosh, s. (March4, 2013). A study of Differences in Standarad & Poor's and Moody's Corporate Credit Ratings. The Leonard N. Stern School of Business. Glucksman Institute for Research in Securities Markets . Kaur, K., & Kaur, D. R. (2011). Credit Rating in India: A Study of Rating Methodology of Rating agencies. Global Journal of Management and Business Research , 11 (12). Krishnan, D. K., Nair, S. C., Tiwari, S. P., Nagpal, S. P., Sahajwala, M. R., & Jayasmhan, S. S. (December 2009). Report of the Committee on comprehensive regulation for credit rating agencies. Ministry of Finance, Capital Markets Division. Kumar, K. V., & Rao, S. H. (2012). Credit Rating: Role in Modern Financial System. IRJC of Marketing, Financial Services & Managament Research , 1 (8), 13. laere, E. V., Vantieghem, J., & Baesens, B. (2012). The difference between Moody's and S&P bank ratings: is discretion in the rating process causing a split? National University of Singapore, RMI. Pride, M. D. (2012). Swimming with The Curent: The role od Credit Rating Agencies in Contemporary Global Governance. Thesis, University of Sydney Business School, School of Political Economy. Raghunathan, V., & R. Varma, J. When AAA means B: The state of Credit Rating in India. Indian Institute of Management, Ahmedabad, India. Ryan, J. (2012). The Negative Impact of Credit Rating Agencies and Proposals for better regulation. German institute for International and Security Affairs, Research Division. SWP Research Division.

27

Utzig, S. (2010, January 26). The Financial Crisis and the Regulation of Credit Rating Agencies: A European Banking Perspective. ADBI Working Paper Series.

28

Annexure:

Company Overview

Description ICRA Limited (formerly Investment Information and Credit Rating Agency of India

Limited) was set up in 1991 by leading financial/investment institutions, commercial

banks and financial services companies as an independent and professional

Investment Information and Credit Rating Agency. Today, ICRA and its subsidiaries

together form the ICRA Group of Companies (Group ICRA). ICRA is a Public

Limited Company, with its shares listed on the Bombay Stock Exchange and the

National Stock Exchange. ICRA Limited is an independent and professional

investment information and credit rating agency. The Company operates in

Outsourced and Information Services, Consulting Services, Rating Services and

Professional and information technology (IT) Services. ICRA rates rupee

denominated debt instruments issued by manufacturing companies, commercial

banks, non-banking finance companies, financial institutions, public sector

undertakings and municipalities, among others. The Grading Services offered by

ICRA include Grading of: initial public offers (IPOs); microfinance institutions

(MFIs); construction entities; real estate developers and projects; healthcare entities,

and maritime training institutes. ICRA Management Consulting Services Limited

(IMaCS), a wholly owned subsidiary of ICRA Limited, is a multi-line management

consulting firm. The international Credit Rating Agency Moody’s Investors Service is

ICRA’s largest shareholder.

Key Offerings Rating Services

As an early entrant in the Credit Rating business, ICRA Limited (ICRA) is one of the

most experienced Credit Rating Agencies in the country today. ICRA rates rupee

denominated debt instruments issued by manufacturing companies, commercial

banks, non-banking finance companies, financial institutions, public sector

29

undertakings and municipalities, among others. ICRA also rates structured obligations

and sector-specific debt obligations such as instruments issued by Power, Telecom

and Infrastructure companies. The other services offered include Corporate

Governance Rating, Stakeholder Value and Governance Rating, Credit Risk Rating of

Debt Mutual Funds, Rating of Claims Paying Ability of Insurance Companies, Project

Finance Rating, and Line of Credit Rating. ICRA, along with National Small

Industries Corporation Limited (NSIC), offers a Performance and Credit Rating

Scheme for Small-Scale Enterprises in India. The service is aimed at enabling Small

and Medium Enterprises (SMEs) improve their access to institutional credit, increase

their competitiveness, and raise their market standing.

Grading Services

The Grading Services offered by ICRA employ pioneering concepts and

methodologies, and include Grading of: Initial Public Offers (IPOs); Microfinance

Institutions (MFIs); Construction Entities; Real Estate Developers and Projects;

Healthcare Entities; and Maritime Training Institutes. In IPO Grading, an ICRA-

assigned IPO Grade represents a relative assessment of the “fundamentals” of the

issue graded in relation to the universe of other listed equity securities in India. In

MFI Grading, the focus of ICRA’s grading exercise is on evaluating the candidate

institution’s business and financial risks. The Grading of Construction Entities seeks

to provide an independent opinion on the quality of performance of the entities

graded. Similarly, the Grading of Real Estate Developers and Projects seeks to make

property buyers aware of the risks associated with real estate projects, and with the

developers’ ability to deliver in accordance with the terms agreed. ICRA’s Healthcare

Gradings present an independent opinion on the quality of care provided by healthcare

entities. In the education sector, ICRA offers the innovative service of Grading of

Maritime Training Institutes in India.

Consulting Services

ICRA Management Consulting Services Limited (IMaCS), a wholly owned subsidiary

of ICRA Limited, is a multi-line management and development consulting firm with a

global operating footprint. IMaCS offers Consulting Services in Strategy, Risk

Management, Regulation & Reform, Transaction Advisory, Development Consulting

30

and Process Re-engineering. IMaCS’ clientele includes Banks and Financial Service

Companies, Corporate Entities, Institutional Investors, Governments, Regulators, and

Multilateral Agencies. Besides India, IMaCS has consulting experience across 35

countries in South East Asia, Northern Asia, West Asia, Africa, Western Europe, and

North America.

Software Development, Business Intelligence and Analytics and Engineering

Services

ICRA Techno Analytics Limited (ICTEAS), a wholly owned subsidiary of ICRA

Limited, offers a complete portfolio of Information Technology (IT) solutions to meet

the dynamic needs of present-day businesses. The services range from the traditional

development of client-server, web-centric and mobile applications to the generation of

cutting-edge Business Intelligence applications and analytics solutions. With years of

experience in data-mining and predictive data modeling, ICTEAS offers various

analytics solutions such as sales analytics and spend analytics. An in-depth knowledge

of various technology areas, coupled with its strengths in various verticals, enables

ICTEAS provide end-to-end services of excellent quality. It uses a mix of

onsite/offshore strategies to optimize bottom-line benefits for its customers. ICTEAS

is a Microsoft Gold Partner and is ISO 27001 certified. The Engineering Division of

ICTEAS offers multidisciplinary computer aided engineering design services. The

activities cover design and drawing in the mechanical, civil/structural, electrical and

instrumentation space. ICTEAS engineers and designers are well versed in AutoCAD,

MicroStation, PDS and Staad pro with experience in the Oil & Gas, Petrochemical

and Power Sectors. The services range from providing Engineering Design Services

to CAD Vectorisation and Conversion Services. Over the years, ICTEAS has

successfully deployed skilled resources to work for large engineering consulting

companies both in the domestic and international market.ICTEAS has two

subsidiaries, ICRA Sapphire Inc. (ICSAP) and Axiom Technologies Limited

(AXIOM). ICSAP is based in Connecticut, USA, while AXIOM operates out of

Kolkata, India.

31

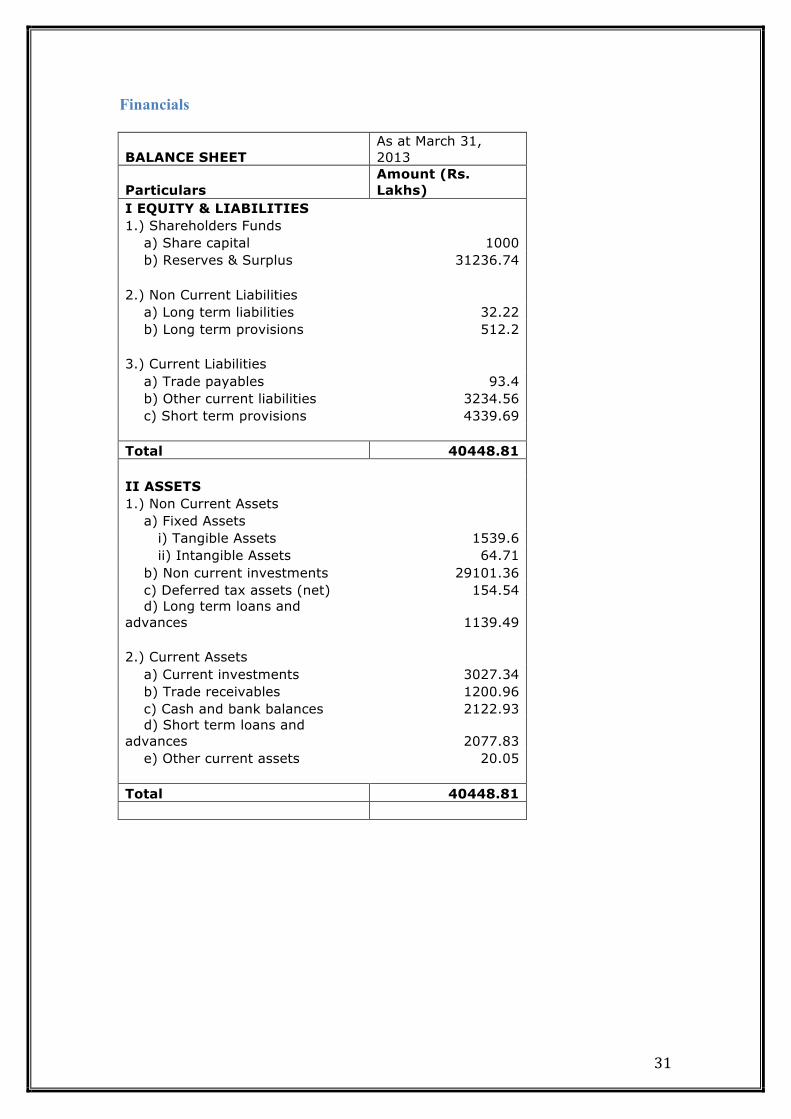

Financials

BALANCE SHEET As at March 31, 2013

Particulars Amount (Rs. Lakhs)

I EQUITY & LIABILITIES 1.) Shareholders Funds a) Share capital 1000 b) Reserves & Surplus 31236.74 2.) Non Current Liabilities a) Long term liabilities 32.22 b) Long term provisions 512.2 3.) Current Liabilities a) Trade payables 93.4 b) Other current liabilities 3234.56 c) Short term provisions 4339.69 Total 40448.81 II ASSETS 1.) Non Current Assets a) Fixed Assets i) Tangible Assets 1539.6 ii) Intangible Assets 64.71 b) Non current investments 29101.36 c) Deferred tax assets (net) 154.54 d) Long term loans and advances 1139.49 2.) Current Assets a) Current investments 3027.34 b) Trade receivables 1200.96 c) Cash and bank balances 2122.93 d) Short term loans and advances 2077.83 e) Other current assets 20.05 Total 40448.81

32

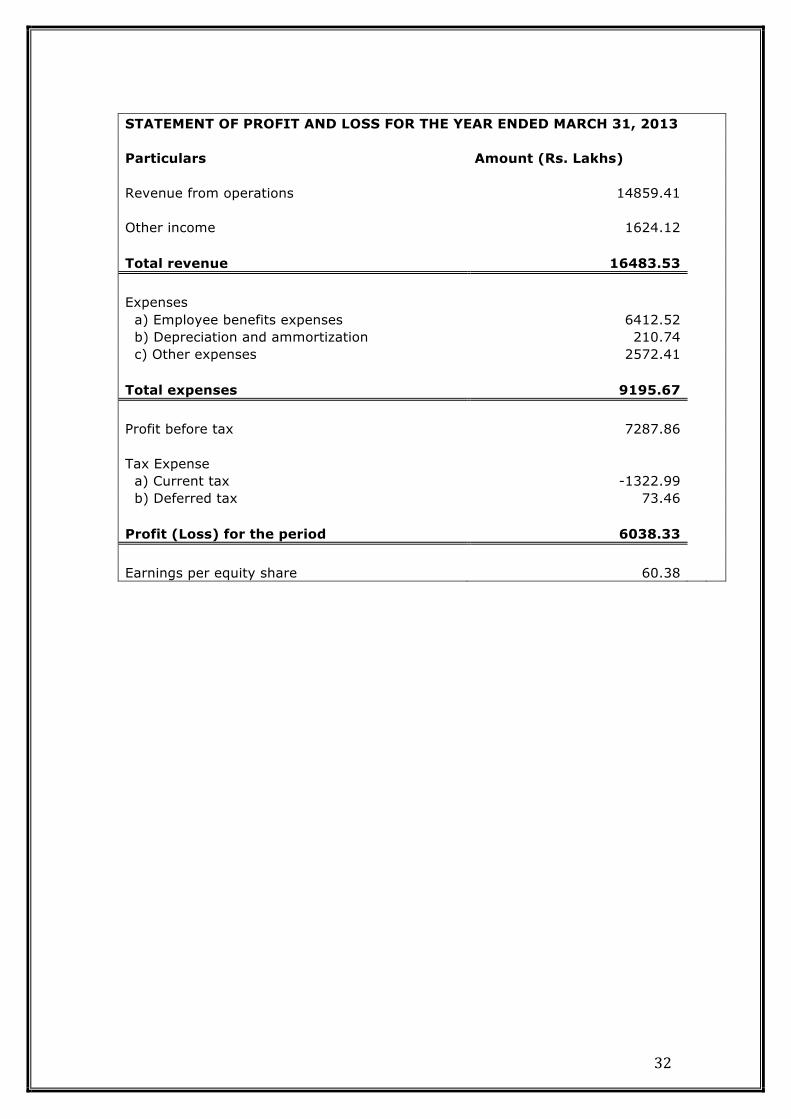

STATEMENT OF PROFIT AND LOSS FOR THE YEAR ENDED MARCH 31, 2013 Particulars Amount (Rs. Lakhs) Revenue from operations 14859.41 Other income 1624.12 Total revenue 16483.53

Expenses a) Employee benefits expenses 6412.52 b) Depreciation and ammortization 210.74 c) Other expenses 2572.41 Total expenses 9195.67

Profit before tax 7287.86 Tax Expense a) Current tax -1322.99 b) Deferred tax 73.46 Profit (Loss) for the period 6038.33

Earnings per equity share 60.38

33

Organizational Structure

Competitors The competitors for ICRA Limited are CRISIL, CARE and FITCH Ratings India Private Limited. However CRISIL is a head on competitor for ICRA and has a larger number of clients than ICRA. Credit Rating and Information Services of India Ltd. (CRISIL) is a global analytical company providing ratings, research and risk and policy advisory services. Its major shareholder is Standard & Poor’s. It is the largest credit rating agency in India, which pioneered ratings in India more than 20 years ago and is today the undisputed business leader with the largest number of rated entities and rating products i.e. around 41738 entities including 20000 small and medium enterprises. The market capitalization of ICRA and its competitors are shown in the following pie chart and table.

34

Company Name Market Capitalisation (Amount in Rs. Crores)

CRISIL 6431.99 CARE 2000

FITCH Ratings India Private Limited 1195.3

ICRA Limited 1190.45 CRISIL surely has its income and sales more than double the amount, which ICRA has. As on 2014, CRISILs Net Sales were Rs 11106 crores as compared to ICRAs Rs 2514 crores i.e. 442% of ICRA net sales. Its net profit margin is also 114% of ICRAs net profit margin.

11%

11%

19% 59%

Market Capitalization

ICRA

FITCH Ratings

CARE

CRISIL

35

Key Deliverables

Summer Internship report submitted to ICRA Limited is as follows:

Title: Understanding Rating Methodology for Housing Finance Companies and

analysis of GRUH Finance Limited in the same framework

36

GRUH FINANCE LIMITED

Mentor: Ms Manushree Saggar (Assistant Vice President)

37

Table of Contents

COMPANY OVERVIEW......................................................................................................... PRODUCTS OFFERED BY GRUH ....................................................................................... SHAREHOLDING PATTERN......................................................................................................... COMPANY’S MANAGEMENT........................................................................................................ BUSINESS RISK PROFILE .............................................................................................................

COMPANY ANALYSIS AND CREDIT PERSPECTIVE..................................................... PORTFOLIO TREND....................................................................................................................... IMPROVEMENT IN ASSET QUALITY INDICATORS............................................................... CAPITAL ADEQUACY..................................................................................................................... LIQUIDITY FACTORS..................................................................................................................... BORROWING PROFILE ................................................................................................................. EARNINGS PROFILE.......................................................................................................................

Company Overview GRUH Finance Limited is Housing Finance Company, with HDFC Limited as its parent company, being the largest shareholder of GRUH, holding 59.15% stake as on March 31, 2014. HDFC is the largest housing finance company (HFC) in India with highest-credit-quality ratings. GRUH offers loans to individuals for purchase, construction, repairs, and renovation of dwelling units. It also offers loans to self-employed segment where formal income proofs are not available. It also offers loans to professionals for purchase of office premises. GRUH has 142 offices across 7 states in India, namely Gujarat, Maharashtra, Karnataka, Rajasthan, Madhya Pradesh, Chhattisgarh and Tamil Nadu. GRUH Finance Limited is an HFC that was promoted by HDFC & AKFED on July 21, 1986 and it commenced its operations in 1988 in Ahmadabad. GRUH belongs to the HDFC group along with HDFC Limited and HDFC Bank, which is among the top player in the housing Finance Industry with a market share of around 18%. GRUH majorly offers Home Loans based on assessed income and caters to self-employed, professionals and salaried segment. GRUH Finance Limited is rated by two of the major credit rating agencies, i.e. ICRA and CRISIL and the ratings given by them for the long term, medium term and short term are as follows. These ratings indicate the highest safety as regards timely payment of interest and principal. TABLE1: GRUHs current rating GRUH FINANCE LIMITED Ratings as on 27 May, 2014

Long-Term Medium-Term Short-Term

ICRA AA+(Stable) MAAA (Stable) A1+ CRISIL AA+ FAAA A1+

Source: ICRA & CRISIL live rating list

Products offered by GRUH

• GRUH Suraksha: Loan offered to salaried individuals and professionals based on formal income proof for construction or purchase of dwelling units in villages, towns, cities for maximum 25 years. Loan is offered up to maximum 75%/80%/85% of the property cost. This loan is also offered under various amortization options such as daily, monthly and annually.

• GRUH Suvidha: Loan offered to professionals and self employed based on appraised income for construction or purchase of dwelling units in villages, cities and towns for maximum 15 years. It is offered for up to 75%/80%/85% of the property cost and is available under various variable rate option.

• GRUH Sajavat: Loan offered to salaried individuals, professionals and self employed to fund repair and renovation work in their existing dwelling units. It is offered up to 75%/80%/85% of the property cost

• GRUH Samruddhi: Loan offered to professionals for purchase of offices. This loan is offered up to 75%/80%/85% of the property cost.

39

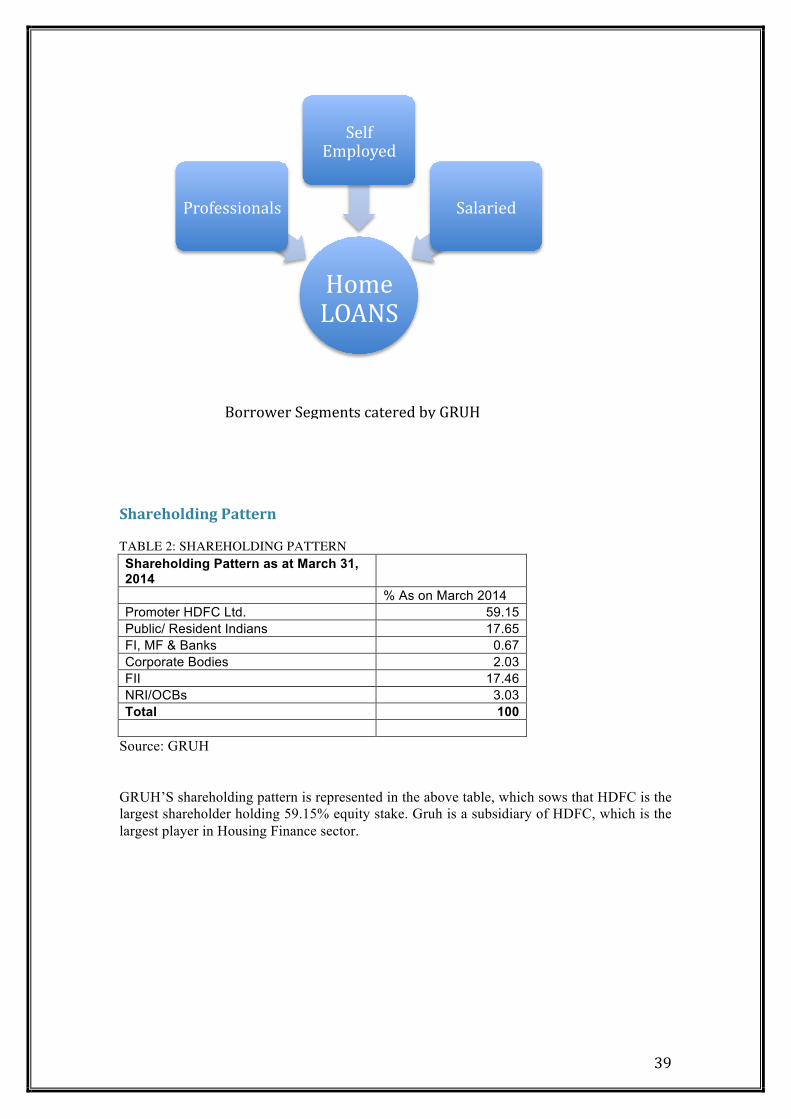

Shareholding Pattern TABLE 2: SHAREHOLDING PATTERN Shareholding Pattern as at March 31, 2014 % As on March 2014 Promoter HDFC Ltd. 59.15 Public/ Resident Indians 17.65 FI, MF & Banks 0.67 Corporate Bodies 2.03 FII 17.46 NRI/OCBs 3.03 Total 100

Source: GRUH GRUH’S shareholding pattern is represented in the above table, which sows that HDFC is the largest shareholder holding 59.15% equity stake. Gruh is a subsidiary of HDFC, which is the largest player in Housing Finance sector.

Home LOANS

Professionals

Self Employed

Salaried

Borrower Segments catered by GRUH

40

TABLE 3 Public Shareholding greater than 1% as on March31, 2014 % As on March 2014 Smallcap World Fund,INC 3.03% Wasatch International growth Fund 1.37% Route One Investment Co. L.P. A/c. Route One Fund I L.P. 1.14% Route One Investment Co. L.P. A/c. Route One Offshore master fund L.P 1.04% Acacia Partners, LP 1.03%

Source: GRUH GRUH’s public shareholding greater than 1% is shown in the table above with smallcap world fund, INC being the largest public shareholder. Company’s Management TABLE 4 Board of Directors

Mr. K.M Mistry Chairman (Non Executive) [Vice Chairman and CEO, HDFC Limited]

Mr. S.M Palia Independent Director Mr. Rohit C. Mehta Independent Director Mr. Praful Anubhai Independent Director Ms. Renu S Kamad Managing Director, HDFC Mr. K.G Krishnamurthy Independent Director Mr. Sudhin Choksey Managing Director Mr. S.G Mankad Independent Director Mr. Kamlesh shah Executive Director

Source: GRUH Company’s management is represented in the above table, with Mr. K.M Mistry as the chairman of the HDFC group. Gruh conducts outreach programs from each retail office to potential taluka places. The outreach-marketing program also serves as collection centre for collecting installments besides providing service of enquiry handling, file opening and effective disbursements. From the above chart we can see that Maharashtra has the highest number of talukas and it being the state with maximum number of talukas being serviced by Gruh i.e. 322/357.

41

Business Risk Profile CHART 1: Product wise Disbursements Growth

Source: GRUH In Total Gruh is doing well as compared to last year as it showed a 19% growth in overall disbursements whereas it is doing highly good in terms NRP Loans as it reported a 74% growth as compared to 2013, albeit on a much smaller base. In terms of geographical profile, Gruh is concentrated in Maharashtra (29% branches) and Gujarat (30% branches). The company has established a strong brand image in these regions so that even the new branches added in these states would generate business faster. It has opened 8 new offices in various states this year expanding its branch network to 142 from 134 across India.

1794.48 2231.34

82.6

143.76 297.31

202.37

0

500

1000

1500

2000

2500

3000

2012-‐13 2013-‐14

Amiunt is Rs. crore

Year

Developer Loans

NRP Loans

Individual Home Loans

42

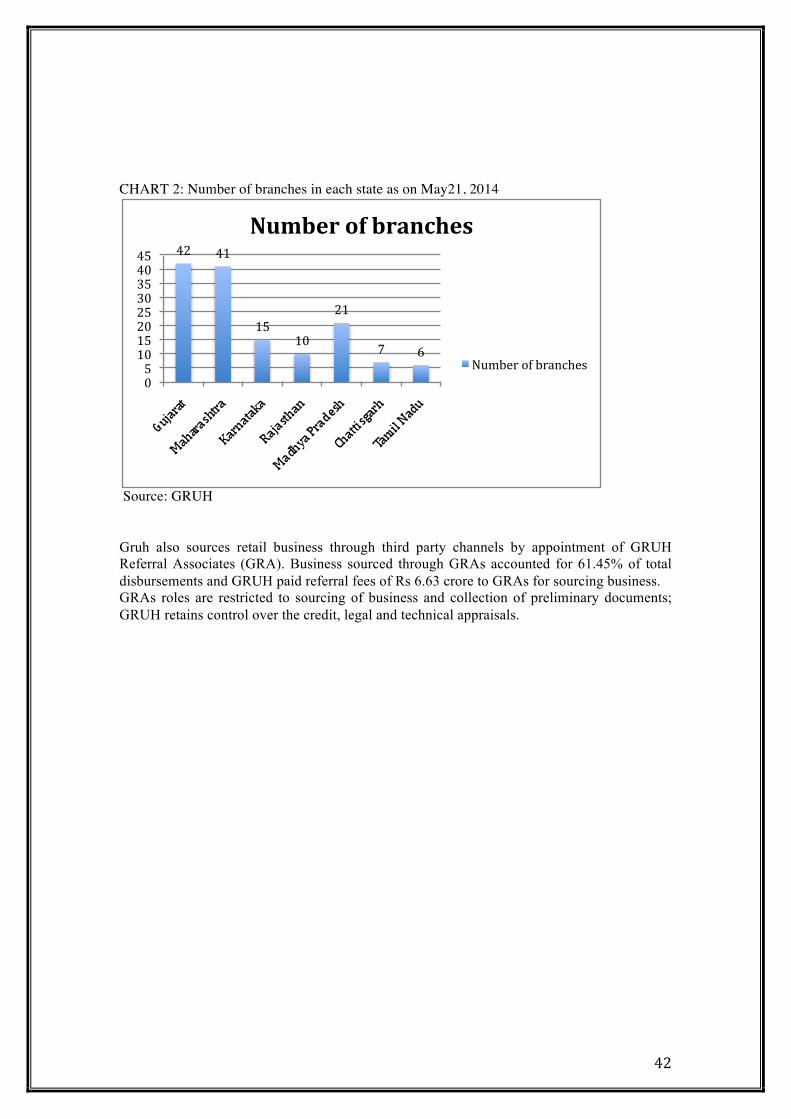

CHART 2: Number of branches in each state as on May21, 2014

Source: GRUH Gruh also sources retail business through third party channels by appointment of GRUH Referral Associates (GRA). Business sourced through GRAs accounted for 61.45% of total disbursements and GRUH paid referral fees of Rs 6.63 crore to GRAs for sourcing business. GRAs roles are restricted to sourcing of business and collection of preliminary documents; GRUH retains control over the credit, legal and technical appraisals.

42 41

15 10

21

7 6

0 5 10 15 20 25 30 35 40 45

Number of branches

Number of branches

43

Company Analysis and Credit Perspective TABLE 5

Key Financials

March, 2011

March, 2012

March, 2013

March, 2014

Equity Capital 35 35 36 36 Net Worth 318 386 491 607 Net Housing Loans 3177 4067 5438 7009 Total Assets 3381 4324 5588 7243.22 Total Income 359 508 648 846 Net Interest Income 139 175 214 271 PBT (reported) 126 163 197 244 PAT (reported) 92 120 146 177 Interest income/ATA 11.26% 12.61% 12.47% 13% Cost of average interest bearing funds 7.55% 9.08% 9.17% 9.12% Total operating income net of interest expenses/ATA 5.20% 5.10% 4.90% 3.74% Expenses/ATA 1.03% 1.01% 0.93% 0.87% Provisions & Charge offs/ATA 0.05% -0.10% 0.01% 0.03% PAT/ATA 3.03% 3.12% 2.94% 2.76 PAT/Average Net Worth 31.42% 34.21% 33.29% 32% Cost to income ratio 20% 20% 19% 19% Dividend payout ratio/PAT 49% 39% 36% 36% Dividend Rate 110% 115% 125% 150 Total Debt/Net worth (times) 9.33 9.94 10.01 11 Capital/risk weighted assets 13.32% 13.95% 14.56% 16.37 Tier 1 capital 12.98% 13.29% 12.93% 14.71%

Note: Amount in Rs. Crore Source: GRUH and ICRA Research

44

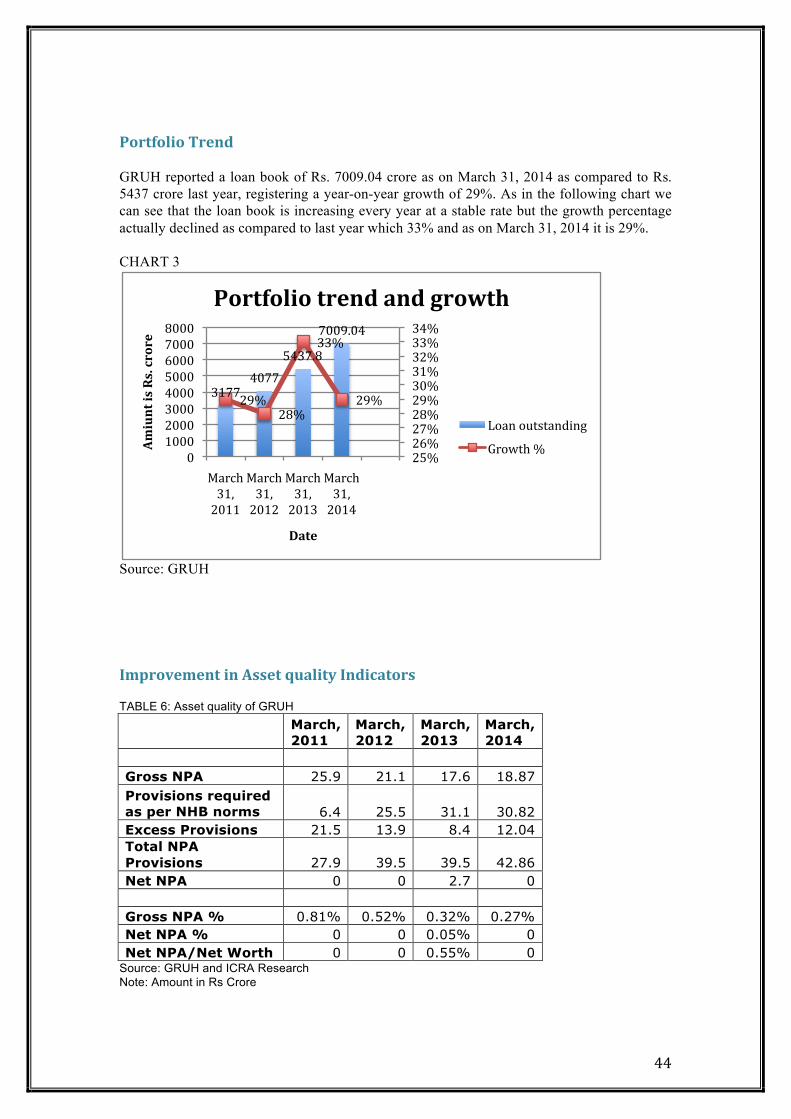

Portfolio Trend GRUH reported a loan book of Rs. 7009.04 crore as on March 31, 2014 as compared to Rs. 5437 crore last year, registering a year-on-year growth of 29%. As in the following chart we can see that the loan book is increasing every year at a stable rate but the growth percentage actually declined as compared to last year which 33% and as on March 31, 2014 it is 29%. CHART 3

Source: GRUH

Improvement in Asset quality Indicators TABLE 6: Asset quality of GRUH

March, 2011

March, 2012

March, 2013

March, 2014

Gross NPA 25.9 21.1 17.6 18.87 Provisions required as per NHB norms 6.4 25.5 31.1 30.82 Excess Provisions 21.5 13.9 8.4 12.04 Total NPA Provisions 27.9 39.5 39.5 42.86 Net NPA 0 0 2.7 0 Gross NPA % 0.81% 0.52% 0.32% 0.27% Net NPA % 0 0 0.05% 0 Net NPA/Net Worth 0 0 0.55% 0

Source: GRUH and ICRA Research Note: Amount in Rs Crore

3177 4077

5437.8

7009.04

29% 28%

33%

29%

25% 26% 27% 28% 29% 30% 31% 32% 33% 34%

0 1000 2000 3000 4000 5000 6000 7000 8000

March 31, 2011

March 31, 2012

March 31, 2013

March 31, 2014

Amiunt is Rs. crore

Date

Portfolio trend and growth

Loan outstanding

Growth %

45

Despite the difficult operating environment, GRUH has managed to maintain low levels of Gross NPA. The gross NPAs however increased a little as compared to 2013 from Rs. 17.6 crore to Rs. 18.87 crore but the Gross NPA% declined from 0.32% in 2013 to 0.27% in 2014 owing to increase in the advance base The net NPAs of the company stood at NIL as on March 31, 2014 (0.05% as on March 31, 2013). Nevertheless, GRUH has operated in this segment for over a decade, enjoys a good understanding of it and has an established in-house appraisal and recovery system, which has enabled it to manage risks so far Capital Adequacy TABLE 7: Capital Adequacy of GRUH

March, 2011

March, 2012

March, 2013

March, 2014

Loans and advances 3177 4067 5438 7009 % Growth 29% 28% 33.71% 28.89% CRAR 13.32% 13.95% 14.56% 16.37% Net Worth as a % of Total Assets 9.40% 8.92% 8.79% 8.38%

Note: Amount in Rs Crore Source: GRUH and ICRA research With a 29% growth in loan book in 2014, GRUH’s economic capital (net worth in relation to total assets) declined from 8.79% as on March 31, 2013 to 8.38% as on March 31, 2014. The loan book although grew from Rs. 5438 crore as on March 2013 to Rs. 7009 crore as on March 2014 yet the capital adequacy ratio increased from 14.56% in 2013 to 16.37% in 2014. This happened due to the change in risk weights. Also the gearing of the company is at 10.6 times as on March 31, 2014 which is moderate. One of the reasons for an increase in CRAR can be the regulatory change by National Housing Bank, because of which GRUH reported an increase in regulatory CRAR. The reduction in Risk weights for large ticket home loans (>Rs. 7.5 million) was from 125% to 75% and small ticket home loans (< Rs. 7.5 million) from 50-100% to 50%. CHART 4

As we see the trend line of Net Worth as a percentage of total assets for the last four years, it is evident that it has been on a declining trend and has been at 8.38% as on March 2014. Liquidity Factors As in the case of all housing finance companies, GRUH also has to manage the ALM gaps given the limited availability of long-term funds and the company has been relying on short-term funds for gap funding. The company parks its surplus funds in liquid fund schemes and short-term deposits with banks. TABLE 8: Asset Liability Maturity Gaps Asset-Liability Maturity gaps

Maturity Buckets Inflows Outflows Gap Cumulative Gap (CG)

CG as % of TA

1-30 days 35.1 9.39 25.71 25.71 0.4% 1-2 month 35.17 218.42 -183.25 -157.54 -2.2% 2-3 months 45.82 112 -66.18 -223.72 -3.1% 3-6 months 96.36 416.66 -320.3 -544.02 -7.5% 6 months -1year 226.65 636.7 -410.05 -954.07 -13.2% 1-3 years 882.51 1662.16 -779.65 -1733.72 -23.9% 3-5 years 669.55 1074.83 -405.28 -2139 -29.5% 5-7 years 689.86 644.35 45.51 -2093.49 -28.9% 7-10 years 1068.88 478.39 590.49 -1503 -20.8% More than 10 years 3312.1 1194.6 2117.5 614.5 8.5% Note: Amount in Rs. Crore Source: GRUH As from the above table we can see that the Asset- Liability maturity gap is around Rs. 954.07 crores for the maturity bucket 6 months – 1 year. The Company as on March 2014 reports Rs 15.67 crore as Cash in balance sheet and Rs. 67.50 crore as fixed deposits. The liquid amount with GRUH is quite in low proportion as compared to its gap which clearly shows that with its liquid assets it cannot match the gap but however if we talk about the financial flexibility of GRUH, it has a quite strong parentage i.e. HDFC Limited and it always has the option to borrow funds from its parents to match the asset-liability gap. Therefore we can say that the gap is not really a problem for GRUH. Also the company in order to pay for matured liabilities can opt for new short term or long term borrowings from various sources. Borrowing profile TABLE 9: Borrowing Mix of GRUH

Total 2967 27.72% 3833 29.19% 4915 28.23% 6443.93 31.11% Note: Amount in Rs crore Source: GRUH and ICRA Research

47

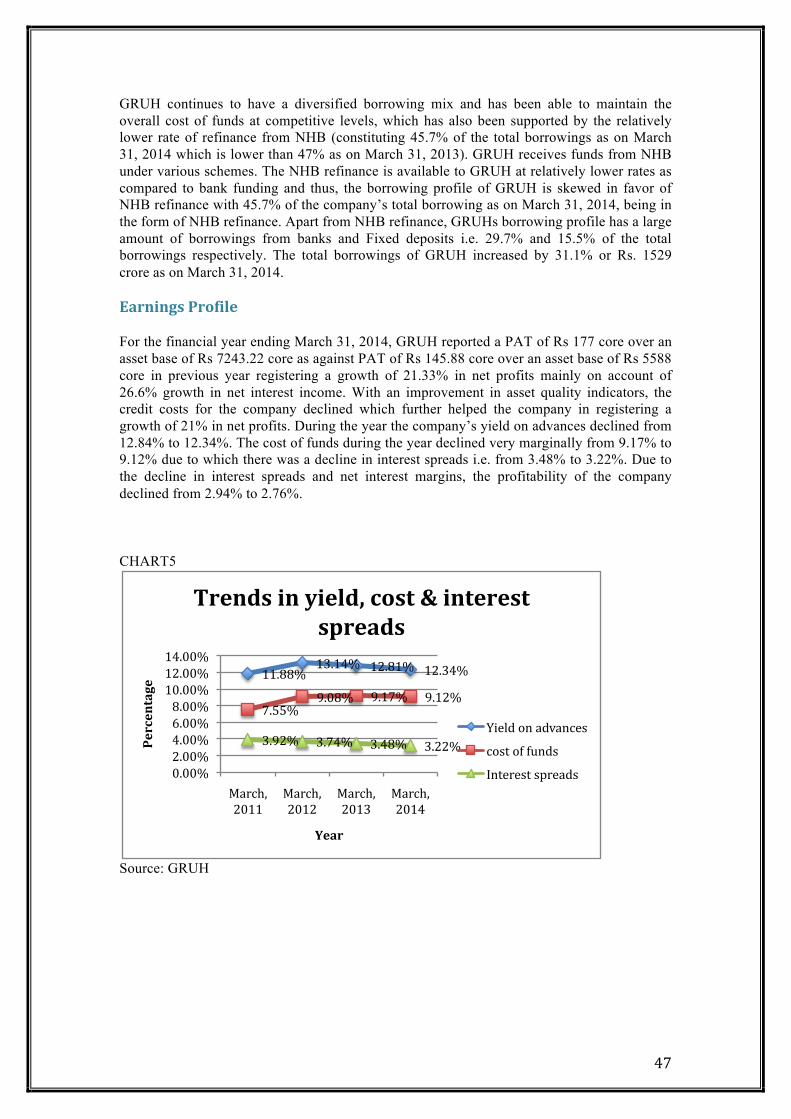

GRUH continues to have a diversified borrowing mix and has been able to maintain the overall cost of funds at competitive levels, which has also been supported by the relatively lower rate of refinance from NHB (constituting 45.7% of the total borrowings as on March 31, 2014 which is lower than 47% as on March 31, 2013). GRUH receives funds from NHB under various schemes. The NHB refinance is available to GRUH at relatively lower rates as compared to bank funding and thus, the borrowing profile of GRUH is skewed in favor of NHB refinance with 45.7% of the company’s total borrowing as on March 31, 2014, being in the form of NHB refinance. Apart from NHB refinance, GRUHs borrowing profile has a large amount of borrowings from banks and Fixed deposits i.e. 29.7% and 15.5% of the total borrowings respectively. The total borrowings of GRUH increased by 31.1% or Rs. 1529 crore as on March 31, 2014. Earnings Profile For the financial year ending March 31, 2014, GRUH reported a PAT of Rs 177 core over an asset base of Rs 7243.22 core as against PAT of Rs 145.88 core over an asset base of Rs 5588 core in previous year registering a growth of 21.33% in net profits mainly on account of 26.6% growth in net interest income. With an improvement in asset quality indicators, the credit costs for the company declined which further helped the company in registering a growth of 21% in net profits. During the year the company’s yield on advances declined from 12.84% to 12.34%. The cost of funds during the year declined very marginally from 9.17% to 9.12% due to which there was a decline in interest spreads i.e. from 3.48% to 3.22%. Due to the decline in interest spreads and net interest margins, the profitability of the company declined from 2.94% to 2.76%. CHART5

![(For Broker/Professional Use) - Alpha Ideasalphaideas.in/wp-content/uploads/2015/09/Fixed-Income_Securities_Note... · (PEL; rated [ICRA]AA(Stable) / [ICRA]A1+ by ICRA) and Piramal](https://static.documents.pub/doc/80x56/5ecea5672a2d2c6f9279e2eb/for-brokerprofessional-use-alpha-pel-rated-icraaastable-icraa1-by.jpg)