Project Report On “To study the Strength of using CAMELS framework as a tool of Performance Evaluation for Banking Institutions ’’ Bank of Kathmandu Everest Bank NIC Bank (2009) Submitted by Shyam Kr. Ale Sunita Raj Vaidhya Kashi Nath Chaudhary Sita Bhattarai Bimala Basnet Submitted to: KFA, Katmandu 1

Transcript

Project Report On

“To study the Strength of using CAMELS framework as a tool of Performance Evaluation for Banking Institutions ’’

Bank of KathmanduEverest Bank

NIC Bank

(2009)

Submitted by Shyam Kr. Ale

Sunita Raj VaidhyaKashi Nath Chaudhary

Sita BhattaraiBimala Basnet

Submitted to: KFA, Katmandu

1

CERTIFICATE

This is to certify that Mr. Shyam Kr. Ale has completed her project report titled “To study the strength of using CAMELS framework as a tool of performance evaluation for Banking Institution’’ under my supervision. To the best of my knowledge and belief this if his original work and this. Wholly or partially has not been submitted for any degree of this or any other University.

Date: 2009-11-02Shanthosh Sharma(KFA Supervisor)

2

DECLARATION

I hereby declare that this project work entitled To study the strength of using CAMELS framework as a tool of performance evaluation for banking institutions is my work, carried out under the guidance of my company guide MR. Santosh Sharma. My report neither fully nor partially has ever been submitted for award of any other degree to either this university or any other university.

Shyam Kr. AleSunita Raj Vaidhya

Kashi Nath ChaudharySita Bhattarai

Bimala Basnet

3

ACKNOWLEDGMENT

Words are the dress of thoughts, appreciating and acknowledging those who areResponsible for the successful completion of the project.

My sincerity gratitude goes to Mr. Santosh Sharma who assigned me responsibility to work on this project and provided me all the help, guidance and encouragement to complete this project.

The encouragement and guidance given by Mr. Santosh Sharma have madethis a personally rewarding experience. I thank him for his support and inspiration, without which, understanding the intricacies of the project would have been exponentially difficult.

I am sincerely grateful to my parents and friends who provided me with the time and financial assistance and inspiration needed to prepare this training report in congenial manner.

WITH SINCERE THANKS

4

Shyam Kr. AleSunita Raj Vaidhya

Kashi Nath ChaudharySita Bhattarai

Bimala Basnet

Need of Project

Usually all persons want money for personal and commercial purposes. Banks are the oldest lending institutions in Nepal scenario. They areProviding all facilities to all citizens for their own purposes by their terms. To survive in this modern market every bank implements so many newInnovative ideas, strategies, and advanced technologies. For that they give each and every minute detail about their institution and projects to Public.

They are providing ample facilities to satisfy their customers i.e. Net Banking, Mobile Banking, Door to Door facility, Instant facility, Investmentfacility, Demat facility, Credit Card facility, Loans and Advances, Account facility etc. And such banks get success to create their own image in public and corporate world. These banks always accepts innovative notions in Indian banking scenario like Credit Cards, ATM machines, Risk Management etc.

So, as a student business economics I take keen interest in Nepalease economy and for that banks are the main source of development.So this must be the first choice for me to select this topic. At this stage every person must know about new innovation, technology of procedure new schemes and new ventures.

5

Meaning of Bank

The word bank means an organization where people and business can invest or borrow money; change it to foreign currency etc. According to Halsbury “ A Banker is an individual , Partnership or Corporation whose sole pre-dominant business is banking , that is the receipt of money on current or deposit account, and the payment of Cheque drawn and the collection of cheque paid in by a customer’’.

6

ABBREVIATIONS USED

BOK : Bank of Kathmandu Ltd.

HBL : Himalayan Bank Ltd.

NIC : Nepal Industrial and Commercial Bank

ATM : Automatic Teller Machine

BOD : Board of Directors

C : Capital

A : Assets

M : Management

E : Earnings

L : Liquidity

CAR : Capital Adequacy Ratio

CCR : Core Capital Ratio

NRB : Nepal Rastra Bank

TCF : Total Capital Fund

TRWA : Total Risk Weighted Assets

TCC : Total Core Capital

PL : Performing Loan

NPL : Non- Performing Loan

LLPTNPL : Loan Loss Provision To Non –Performing Loan

LLPTTL : Loan Loss Provision To Total Loan

LLP : Loan Loss Provision

TL : Total Loan

SE : Staff Efficiency

NPAT : Net Profit after Tax

EPS : Earning Per Share

ROA : Return on Assets

ROE : Return on Equity

CRR : Cash Reserve Ratio

C & B : Cash and Bank Balance

7

The Origin and Use of Banks

The Word ‘bank’ is derived form the Italian word ‘banko’ signifying a bench, which was erected in the market-place, where it was customary to exchange money. The Lombard Jews were the first to practice this exchange business, the first bench having been established in Italy A.D. 808. Some authorities assert that the Lombard merchants commenced the business of money-dealing, employing bills of exchange as remittances, about the beginning of the thirteenth century.

About the middle of the twelfth century it became evident, as the advantage of coined money was gradually acknowledged, that there must be some controlling power, some corporation which would undertake to keep the coins that were to bear the royal stamp up to a certain standard of value; as, independently of the ‘sweating’ which invention may place to the credit of the ingenuity of the Lombard merchants- all coins will, by wear or abrasion, become thinner, and consequently less valuable; and it is of the last importance, not only for the credit of a country , but for the easier regulation of commercial transactions, that the metallic currency be kept as nearly as possible up to the legal standard. Much unnecessary trouble and annoyance has been caused formerly by negligence in this respect. The gradual merging of the business of a goldsmith into a bank appears to have been the way in which banking, as we now understand the term, was introduced into England; and it was not until long after the establishment of banks in other countries-for state purposes, the regulation of the coinage, etc. That any large or similar institution was introduced into England. It is only within the last twenty years that printed cheque have been in use in that establishment. First commercial bank was Bank of Venice which was established in 1157 in Italy.

8

Origin of Banking in Nepal

Nepal's first commercial bank, the Nepal Bank Limited, was established in 1937. The government owned 51 percent of the shares in the bank and controlled its operations to a large extent. Nepal Bank Limited was headquartered in Kathmandu and had branches in other parts of the country.

There were other government banking institutions. Rastriya Banijya Bank (National Commercial Bank), a state-owned commercial bank, was established in 1966. The Land Reform Savings Corporation was established in 1966 to deal with finances related to land reforms.

There were two other specialized financial institutions. Nepal Industrial Development Corporation, a state-owned development finance organization headquartered in Kathmandu, was established in 1959 with United States assistance to offer financial and technical assistance to private industry. Although the government invested in the corporation, representatives from the private business sector also sat on the board of directors. The Co-operative Bank, which became the Agricultural Development Bank in 1967, was the main source of financing for small agribusinesses and cooperatives. Almost 75 percent of the bank was state-owned; 21 percent was owned by the Nepal Rastra Bank, and 5 percent by cooperatives and private individuals. The Agricultural Development Bank also served as the government's implementing agency for small farmers' group development projects assisted by the Asian Development Bank (see Glossary) and financed by the United Nations Development Programme. The Ministry of Finance reported in 1990 that the Agricultural Development Bank, which is vested with the leading role in agricultural loan investment, had granted loans to only 9 percent of the total number of farming families since 1965.

Since the 1960s, both commercial and specialized banks have expanded. More businesses and households had better access to the credit market although the credit market had not expanded.

In the mid-1980s, three foreign commercial banks opened branches in Nepal. The Nepal Arab Bank was co-owned by the Emirates Bank International Limited (Dubai), the Nepalese government, and the

Nepalese public. The Nepal Indosuez Bank was jointly owned by the French Banque Indosuez, Rastriya Banijya Bank, Rastriya Beema Sansthan (National Insurance Corporation), and the Nepalese public. Nepal Grindlays Bank was co-owned by a British firm called Grindlays Bank, local financial interests, and the Nepalese public.

Nepal Rastra Bank was created in 1956 as the central bank. Its function was to supervise commercial banks and to guide the basic monetary policy of the nation. Its major aims were to regulate the issue of paper money; secure countrywide circulation of Nepalese currency and achieve stability in its exchange rates; mobilize capital for economic development and for trade and industry growth; develop the banking system in the country, thereby ensuring the existence of banking facilities; and maintain the economic interests of the general public. Nepal Rastra Bank also was to oversee foreign exchange rates and foreign exchange reserves.

Prior to the establishment of Nepal Rastra Bank, Kathmandu had little control over its foreign currency holdings. Indian rupees were the prevalent medium of exchange in most parts of the country. Nepalese currency was used mostly in the Kathmandu Valley and the surrounding hill areas. The existence of a dual currency system made it hard for the government to know the status of Indian currency holdings in Nepal. The exchange rates between Indian and Nepalese rupees were determined in the marketplace. Between 1932 and 1955, the value of 100 Indian rupees varied between Rs71 and Rs177. The government entered the currency market with a form of fixed exchange rate between the two currencies in 1958. An act passed in 1960 sought to regulate foreign exchange transactions. Beginning in the 1960s, the government made special efforts to use Nepalese currency inside the country as a medium of exchange.

It was only after the signing of the 1960 Trade and Transit Treaty with India that Nepal had full access to foreign currencies other than the Indian rupee. Prior to the treaty, all foreign exchange earnings went to the Central Bank of India, and all foreign currency needs were provided by the Indian government. After 1960 Nepal had full access to all foreign currency transactions and directly controlled its exports and imports with countries other than India.

As a result of the treaty, the government had to separate Indian currency (convertible currency because of free convertibility) from other

10

currencies (nonconvertible currency because it was directly controlled by Nepal Rastra Bank). In 1991 government statistics still separated trade with India from trade with other countries. Tables showing international reserves listed convertible and nonconvertible foreign exchange reserves separately.

In the context of Nepal having adopted an open economy, an excessive level of liquidity will initially exert reassure on the balance of payments and foreign exchange reserve and subsequently cause adverse effects on he domestic price situation. Thus, it will be necessary to maintain a balanced monetary position to attain the economic growth rate envisaged in the plan. The sustainable economic growth can only be achieved if the monetary balance is maintained.

Another important objective of monetary management is to achieve maximum mobilization of internal resources.The monetary policy needs to be oriented towards encouraging the people to save through the creation of a competitive environment among banks and financial institutions and motivating the desirous entrepreneurs to mobilize the available resources through the collection of' the scattered savings in production and employmentGenerating programme in the country. In this perspective, it is necessary along with a planned process of economic development to initiate programmes that can create new financial bases for the economy, consolidate the existing ones and encourage healthy competition. A review of the requirements and availability of resourcesReveals that there is a tremendous resource gap between resource requirements arid its availability in the country;This is indeed indicative of the fact that a large share of private savings is still lying outside the domain of institutional systems, In this context, an efficient mobilization of internal resources can further enhance the participation of the private sector in the economic development of the nation.

11

Lists of Licensed Commercial Banks (Till October 24, 2009 A.D)

S.NO Name of BankDate of

Establishment (A.D)

Head Office

1. Nepal Bank Ltd 1937/11/15 Dharmapath, Kathmandu

2. Rastriya Banijiya Bank 1966/01/23 Shingadurbar plaza, Kathmandu

3. Nabil Bank Ltd. 1984/07/16 Shingadurbar plaza, Kathmandu

4. Nepal Investment Bank Ltd. (NBIL)

1886/02/27 Durbarmarg, Kathmandu

5. Standard Chartered Bank 1987/01/30 New Baneshwor , KTM

6. Himalayan Bank Ltd 1993/01/18 Thamel Kathmandu7. Nepal SBI Bank Ltd. 1993/07/07 Hattisar , KTM8. Nepal Bangladesh Bank Ltd. 1993/06/05 New Baneshwor,

KTM9. Everest Bank Ltd. 1994/10/18 Lazimpat, KTM10. Bank of Kathmandu Ltd 1995/03/12 Kamaladi, KTM11. Nepal Credit & Commercial Bank

Ltd.1996/10/14 Siddarthanagar, KTM

12. Lumbini Bank Ltd. 1998/07/17 Narayangadh, Chitwan

13. Nepal Industrial & Commercial Bank Ltd.

1998/07/21 Biratnagar, Morangq

14. Machhapuchhre Bank Ltd. 2000/10/03 Prithvi Chowk, Pokhara

15. Kumari Bank Ltd. 2001/04/03 Putalisadak, KTM16. Laxmi Bank Ltd. 2002/04/03 Adarshanagar,Birgung17. Siddhartha Bank Ltd. 2002/12/24 Kamaladi, KTM18. Agricultural Development Bank

Ltd.1968/10/19 Ramshahpath, KTM

19. Global Bank Ltd. 2007/01/02 Birjung, Parsa20. Citizens Bank Int’ Ltd. 2007/06/21 Kamaladi, KTM21. Prime Commercial Bank Ltd. 2007/09/24 Newroad, KTM22. Sunrise Bank Ltd. 2007 Garidhara, KTM23. Bank of Asia Ltd. 2007 Tripureshwor, KTM24. DCBL Bank Ltd. 2001/02/01 Kamaladi, KTM25. NMB Bank Ltd. 2008/05 Babarmahal, KTM26. KIST Bank Ltd. 2009/05/07 Anamnagar, KTM

12

Source: www.nrb.org.np

13

Introduction of Bank of Kathmandu

Bank of Kathmandu Limited has become a prominent name in the Nepalese banking sector. Bank of Kathmandu Ltd. Has become a glorify there corporate slogan “We make your life easier’’. For the success of the above slogan Bank of Kathmandu is committed to deliver quality service to customers, generating good return to shareholders , providing attractive incentives to employees and serving the community through stronger corporate social responsibility endeavor.

Bank of Kathmandu Limited (BOK) has today become a landmark in the Nepalese banking sector by being among the few commercial banks which is entirely managed by Nepalese professionals and owned by the general public.

BOK started its operation in March 1995 with the objective to stimulate the Nepalese economy and take it to newer heights. BOK also aims to facilitate the nation's economy and to become more competitive globally. To achieve these, BOK has been focusing on its set objectives right from the beginning. To highlight its few objectives:

To contribute to the sustainable development of the nation by mobilizing domestic savings and channeling them to productive areas

To use the latest banking technology to provide better, reliable and efficient services at a reasonable cost

To facilitate trade by making financial transactions easier, faster and more reliable through relationships with foreign banks and money transfer agencies

To contribute to the overall social development of Nepal

TECHNOLOGY

BOK's IT infrastructure has been designed, to facilitate, internal and customer convenience. Nationwide, all the branches are connected to the central database via Wide Area Network (WAN) powered by Finacle, state-of-the-art banking application software supported by hardware like SUN Fire V880 RISC server, VSAT etc. Internally, BOK relies on Information & Communication Technology (ICT), for a quick, reliable, efficient system. Banking operations are powered by Finacle, which is listed among the top 40 companies that have reshaped the global economy as per the Wired Magazine.

FINACLE

14

BOK takes pride in using Finacle, banking application software, “The Banker” Technology Award 2004.

Certified by Information Technology Association of using certified processes and methods

One of the first banking products to be JAVAtised to enable to operate effectively, provide better customer services challenges of the internet paradigm.

Is installed in more than 400 sites across the world.

INTERNET BANKING

With the aim of providing banking services at the customer's fingertips, BOK is starting Internet Banking and Alert Service very soon. In Internet Banking, BOK will provide Consumer e-banking (Core, Retail and Bill Payment) as well as Corporate e-banking facilities (Trade financing and web based Cash Management).

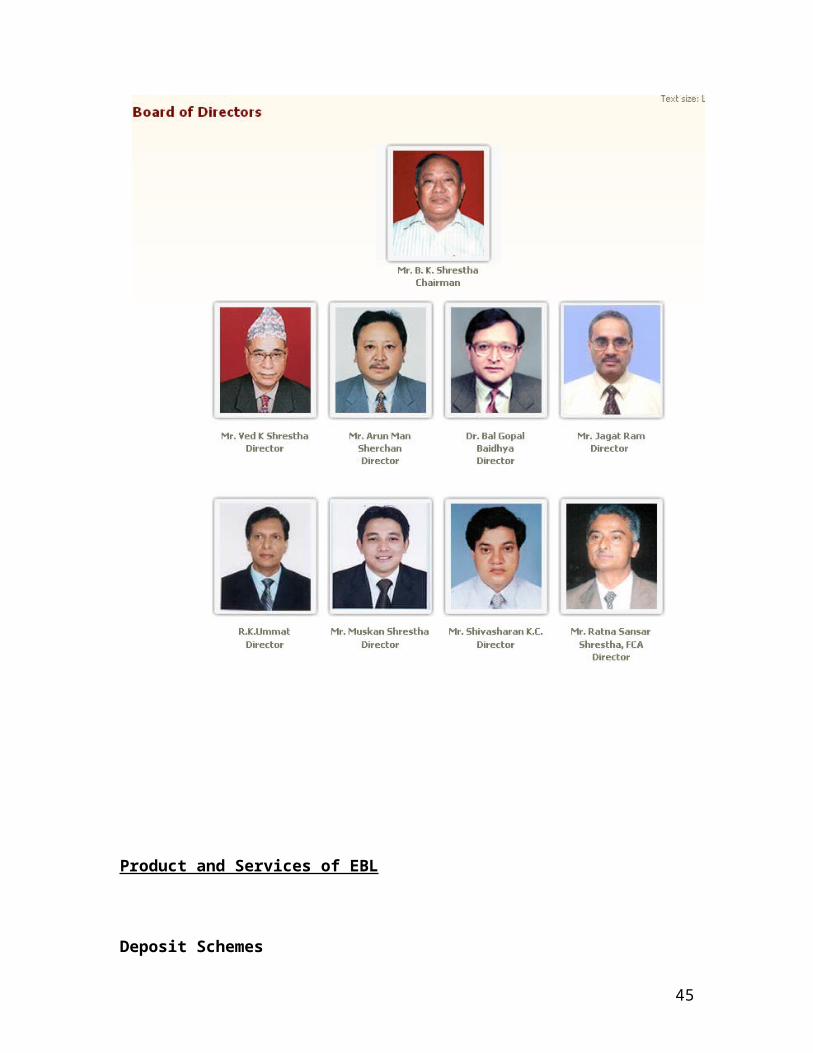

Board of Directors

Mr. Narendra Kumar Basnyat Chairman

Mr. Satya Narayan Manandhar Director

Mr. Bijaya Krishna Shrestha Director

15

Mr. Ramesh Nath Dhungel Director

Mr. Govinda Prasad Sharma Director

Dr. Hem Raj Subedee Director

Mr. Bishnu Prasad Banjade(Rep. of Rahul Investment P. Ltd)Director

16

Product of BOK

Product and Services Provide by BOK:-

1. Deposit Product: a. Current Account: To suit every business need BOK has tailor made Current account which rightly meets your needs in today's faced paced business. With advanced technological features all your banking needs are well taken care of. You can have access to your account from all our BOk branches in just few seconds.

FeaturesMinimum Balance - NPR 10,000 in Kathmandu Valley Branches and NPR 5,000 in Outside Valley Branches

Facilitiesi. Anywhere Branch Banking Services

ii. Extended Banking Hours in Kathmandu Valley Branchesiii. Standing Instruction is accepted looking at the feasibility of the

request.iv. Cash Managementv. Free Cheque book

b. Saving: Bank savings accounts are a critical part of everybody's financial picture. If you need a safe place to keep money, a bank savings account is often a good choice. Here’s a quick review of what savings accounts are and why you might want to have a bank savings account.

Saving account has some of the benefits listed below: 1. Easy access to Bank saving account.2. Bank saving account grows your money.3. Bank saving account are relatively save.

Some of the facilities given by BOK in saving account listed below: i. Ladder Saving : Ladder Savings of BOK not just helps you to save money but also helps your money to grow, with competitive interest rates on daily balance. This power packed account is well packaged with all the various banking services. You can earn interest up to 4.25% on daily balance in this savings scheme.

Features1. Interest is given on daily balance depending upon the amount deposited.2. Minimum balance to be maintained in this account is Rs.50,000 only.

17

3. Ledger fee of Rs.200 will be deducted from the account if the minimum balance is not maintained.

Facilities

1. Free Anywhere Branch Banking Services2. Free stop payment processing3. Free SMS banking.4. TC/BD issuance at special discount rate.5. ATM Card (No Issuance charge).6. Free Good for Payment.7. Free Balance Certificate issuance.8. On demand account statement.9. Unlimited withdrawals.10. Free Inward Service

ii. General Saving: General saving offers competitive rate of interest on daily balance.

Features1. Minimum balance to be maintained Rs. 15,000 only for Kathmandu Valley branches and Rs. 5000 for outside valley branches.

2. Interest is given on daily balance.

Faclilities :

1. Any where banking services.2. Free Cheque book

3. Extra hour banking services through evening counters(in Kathmandu Valley4. Non-restricted transactions for deposits and withdrawals ATM for easy transactions.5. Mobile Phone Bill Payment Services ( at standing instruction)

iii. Sajilo Bachat Yojana: To inculcate banking habits among customers BOk introduced Sajilo Bachat Khata with minimum balance of just Rs. 1000. As the name Sajilo Bachat Khata suggests it has been made easy, hassle-free, and affordable to general public. With Sajilo Bachat Khata one can have easy access to modern banking facilities like ATM, Mobile banking services etc.

Features

1. Easy and hassle-free account opening .2. Account Operating only at minimum balance of NPR 1000.00 3. Ledger Fee.

18

Facilities

1. Anywhere Banking Services at real time basis 2. Extra hour banking services through evening counters(in Kathmandu Valley 3. Non-restricted transactions for deposits and withdrawals 4. Free Cheque-book 5. Debit Card facilities for transaction 6. Mobile Phone Bill Payment Services ( at standing instruction)

Documentation

1. Two Recent Passport Size Photographs of Applicant/Account Operator 2. Evidence of Identification of Account Operator (Citizenship/Passport/Driving License/Voter's ID) 3. Introduction by an Accountholder of Bank of Kathmandu (If possible)

iv. Griha Laxmi Bachat: BOK has introduced a new saving product targeted especially for household/working women to offer them the best financial services and the best banking practices. The main purpose of the product is to inculcate women’s saving habits.

Features:

1. Minimum age should be 16 years to eligibility to open this account. 2. Minimum amount to be maintained is Rs. 5000 inside Kathmandu Valley and Rs. 2500 outside

Kathmandu Valley.

Facilities

1. 2.25% Interest on Daily Basis 2. Quarterly Interest Payment 3. ATM Card and Cheque Book facilities 4. Unlimited Withdrawl Facility 5. Telephone & Mobile Bill Payment 6. SMS Banking

19

v. Shunya Maujdat ma Sabaiko Bachat Khata:

Features:

1. Account Opening at Zero Balance 2. Quarterly Interest Payment 3. Visa Debit Card free with no renewal charge for 5 yrs 4. Free 50 hrs Internet subscription 5. No limitation on withdrawal 6. Utility bill payment Facility 7. Bok Click ( Internet Banking ) Facility 8. Deposit below Npr. 200.00 shall not be entertained

c. Call Account: To manage large volume of surplus funds of your organization you can open an Operative Call Account at Bank of Kathmandu and can earn additional earnings for your excess funds.

Features1. Either current or saving account to be maintained2. Interest Calculated on Daily Balance.3. Withdrawals from this account should be pre-informed.4. Deposits will be accepted only during working hours only.5. Cheque book will not be issued for this account.

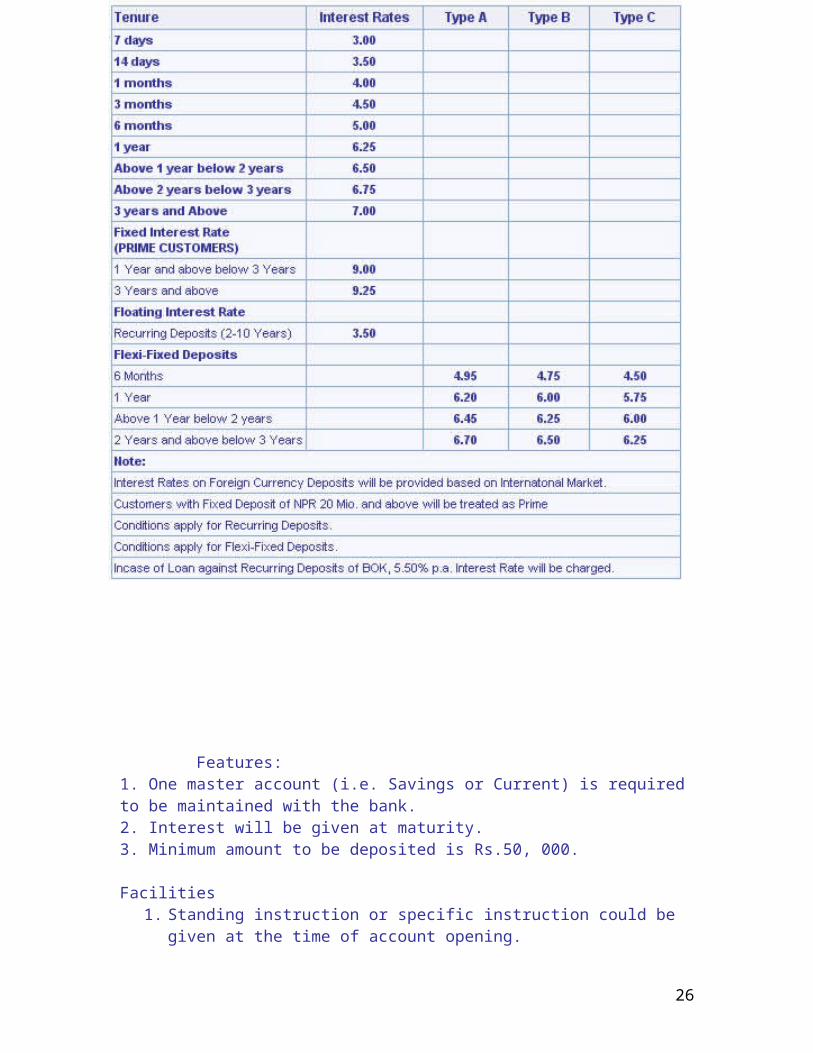

d. Term Deposit: 1. Fixed Deposit: Tenure ranging from seven days to over three years, Fixed Deposit at Bank of Kathmandu allows you to diversify your portfolio to best suite your investment plan.

20

Features:1. One master account (i.e. Savings or Current) is required to be maintained with the bank.2. Interest will be given at maturity.3. Minimum amount to be deposited is Rs.50, 000.

Facilities1. Standing instruction or specific instruction could be given at the time of account

opening.

Documentation1. For organization, a Board minute is required.2. For Individual 2 set of photographs and the copy of citizenship is required

3. Recurring Deposits:

21

To build up your savings BOK has introduced Recurring Savings Scheme where in monthly equated deposits over a fixed period of time yields higher returns.

1. Kopila Bachat Yojana for minors2. Mero Bachat Yojana for young age group

Features:

1. Flexible deposit facility. 2. Account for children below 16 years of age for Kopila Bachat and above 16 years for

Mero Bachat. 3. No automatic closure. 4. Quarterly interest payment. 5. Loan up to 90% available against the total account balance. 6. Minimum balance in multiples of Rs. 1000 inside valley & multiples of Rs 500 outside

valley. 7. Depending upon your requirement, savings plan for Recurring Saving Scheme can

range form 2 to 10 years.

2. Loan & Advances:

A. Corporate Credit (Loan):

1. Project Finance (Term Loan): Based on the viability of the project/proposal, Term Loan to finance the long-term financing need of a firm/company may be made available. This loan is normally provided up to 65% of the financing requirement with a maximum tenure of 60 months. Terms could vary depending upon the need of the project.

2. Working Capital Finance: Based on the nature of a business/transaction, various types of working capital facilities/loans may also be availed. Some of the commonly offered products under this category are as follows:

i. Overdraft: This revolving/open term facility enables a firm/company to manage their varying daily cash requirement.

ii. Demand / Short-term loan (Trade Finance): These facilities are normally provided to support one-off or any particular short-term transactions.

iii. Trust Receipt/ Importers Loan (Trade Finance): Majority of the businesses in Nepal depend on imported items. Short-Term Trust Receipt Loans are the most common/popular product available to finance such requirement.

iv. Export Loan: Export loan facilitates to the exporters to process/collect stocks for exports.

22

3. Consortium Lending / Finance / Credit: Bank of Kathmandu has developed skills in syndicating large project loans and has successfully applied them in tying-up a number of large deals.

3. Business Credit (Small & Medium):

1. Demand / Short-term loan (Trade Finance): These facilities are normally provided to support one-off or any particular short-term transactions.

2. Trust Receipt/ Importers Loan (Trade Finance): Majority of the businesses in Nepal depend on imported items. Short-Term Trust Receipt Loans are the most common/popular product available to finance such requirement.

3. Other Types of Business Credit (Loan):

i. Loan against Fixed Deposit: Loan against fixed deposit enables you to manage the short-term cash need without breaking the deposits.

ii. Loan Against Govt. Bond / 1st Class Bank Guarantee: A low cost secured loan product offered to you for managing your financing need.

iii. Priority Sector/ Deprived Sector Loan: By virtue of this product small entrepreneur/individual may also avail loan up to NPR 2.5 million.

iv. Consortium Financing: Bank of Kathmandu has developed skills in syndicating large project loans and has successfully applied them in tying-up a number of large deals.

4. Consumer Lending / Retail Credit :

1. Housing Loan:

Financing accommodation facility for individuals. Key terms:

• 0.5% p.a if prepaid within one year• 1% flat if prepaid after one year

Maximum Finance: 70% of the eligible expenses. Repayment System: Equated Monthly Installment. Tenure: Maximum 20 years.

2. Vehicle Loan:

23

i. Car4U Loan

Financing cars, vehicles for private use. Key terms:

Maximum Tenure Up to 8 years Interest rate 9% p.a - 10.5% p.a Processing fee 1 percent Maximum Finance: 80% of the cost of vehicle Maximum Tenure upto 6 years

ii. LCV Loan / Buses

Financing micro/ mini buses to be operated on commercial basis. Key terms: Indicative interest rate 12.0% Financing up to 70% of the vehicle Maximum Tenure of 4 years

iii. LCV Loan / Trucks

Financing brand new pick up trucks to be operated for transaction of goods. Key terms: Indicative interest rate 11.5% Financing up to 70% of the vehicle Maximum Tenure of 3 years

3. Education Loan:

Financing students for their graduation or post graduation studies. Key terms:

Maximum Tenure Up to 10 years Interest rate 11% p.a. Processing fee 1% Prepayment Fee 0.5% p.a on the prepaid amount within 1 year, 1% flat on prepaid amount after 1 years Restructing fee 0.25% p.a Loan Swap fee 2% p.a. on the outstanding amount

4. Festivity Loan:

24

Key terms:

Maximum Tenure Up to 10 years Interest rate 11% p.a Processing fee 1% Prepayment Fee 2 % flat on the prepaid loan

5. Foreign Employment Loan:

Financing eligible individuals recommended by His Majesty’s Government going abroad on a pre arranged employment through a recognized emplo9yment agency .

Key terms:

Indicative interest rate 11%. Financing up to NRP 100,000 or 80% of the Cost whichever is lover. Maximum, Tenure of 18 Months.

5. Development Credit: The goal of Development Credit is to provide quality financial services to marginalized groups and poorer sections of society through intermediaries e.g. Micro Finance Institutions, Co-operatives, Financial Intermediary Non Governmental Organizations, Development Banks, Community Based Organizations and other registered organizations.

Products:

1. General Micro Finance

This product has been devised for financing general micro finance loans to clients through partner institutions involved in offering Micro Finance services.

A micro finance loan is defined as a loan used for various income generating activities including, but not limited to, purchase of livestock, loans for mini-grocery stores, vegetable loans, etc. Non-income generating loans such as installing bio-gas units shall also be availed but only with prior approval from Bank of Kathmandu.

2. Agriculture and Forest Based Product Loan:

The product has been devised to allow farmers, agricultural cooperatives, community forest user groups and other registered institutions engaged in producing and processing agricultural and forest based products to have access to finance for funding working capital requirements, plantation expenditures and purchasing livestock and accessories.

3. Equpment Finance:

The product aims to finance the cost of equipments of various purposes to individuals, groups and institutions operating Small and Medium Enterprises with an objective to raise income in rural and urban areas of Nepal.

4. Vehicle and Accessories Finance:

The product has been devised for financing vehicles and vehicle related accessories to self-employed low income earning entrepreneurs. Loans will be of a Hire Purchase and on an owner-driver concept.

25

6. Other Products & Service:

Development CreditInternational Trade ( Letter of Credit , Bank Guarantees etc.)Global Banking Solutions (E-Fund Transfer)SWIFT TransferDemand DraftTraveler’s ChequeRemittanceDebit Card / ATM’SSalary ManagementCash ManagementGift ChequeSafe Deposit LockerGift ChequeSafe Deposit LockerNRN BankingBOK Visa Credit Card

Capital Structure:

Particulars Amount (Rs.)Authorized Share Capital 1000000000Issue Share Capital 603141300Paid Up Capital 603141300

Currently at present, BOK has been focusing land on retail banking consumer finance. Beside this, BOK this , BOK focuses on giving its best services to general public introducing new ways and means of services. It is slowly following sophisticated banking products and fee based services. It aims to continue the operation providing goods, services speeding in opening new branches within the different geographical location. Also, recently it has lunch internet Banking Services.

27

Corporate Social Responsibility:

As a true corporate citizen BOK has contribution towards the betterment of the society in every way possible. With endless possibilities, BOK aims at doing the most, in diverse avenues. Be it organizing HIV/AIDS walkathon, blood donation program or keeping environment clean, BOK constantly endeavors to reach out to those that need most support.

1. BOK has been supporting the deprived student of help to the helpless counsil ( DHARAN ) through its educational support program.

2. BOK supported a scholarship program organized by development and Equity for woman empowerment, Nepal for underprivileged students.

3. BOK with a mission to support BAL Mandir orphans Project, Naxal, supported 2nd annual dinner fundraiser at 1905, Kantipath. Organized by Nepal; Children’s Organization.

4. BOK made an effort to help schools in remote areas ( Far Western Region, Nepal )5. in order to enhance the quality education in that area by supporting a pilot Adop-A-

School program launched by asave the childrean Kathmandu.6. As a mission to create awareness and support for the treatment and rehabilitation

center for disabled children, BOK supported Hospital and Rehabilitation Center for disabled children ( HRDC ) to host the 3rd CMS Abilities Cup 2008.

7. BOK made an effort to create an opportunity for the disabled children to be self employed by providing them with computer trainings by supporting skill Development and Rehabilitation Center for Disable-Nepal.

8. BOK distributed clothes to the flood victims of Bank Districts through “ Hridaya Group’’ – Social Youth Organization.

9. As a part of its commitment to be socially responsible, BOK organized its 2nd of the knowledge series one day workshop “seize the future- A Visionary Leadership Workshop ‘’. The proceeds form the workshop plus an addition of two hundred and fifty thousand rupees were contributed to Hospital and Rehabilitation center for disable children ( HRDC ) in order to support the disabled children of Nepal.

10. Furthermore, the workshop was organized with an aim to create a perspective for the participant on both internal and external challenges that he/she is facing in leading the organization and to help them develop a plan of action to successfully tackle the challenges.

11. BOK is a committed supporter to TEWA in its Endeavour in building equitable, just and inclusive society (with special focus on Woman ) by increasing self reliance of Nepalese by reducing dependency on foreign donors.

12. BOK has been supporting TEWA to organize many fund raising events in the past years. TEWA with support of BOK recently organized ‘ Deep Prajwalan ‘ a fund raising event in support of rural Nepalese women’s groups for promoting equitable justice and peace in the society.

13. To make the world HIV/AIDS day, Bank of Kathmandu decided to do something different this time and donated full set of clothes and foodstuffs to 22 HIV positive children of Keta Keti Ashram, Bansbari and Kathmandu.

14. BOK joined hands with Traffic police post, Gaushala wigh an attempt to convey the Traffic social Massages by helping place banners in public vehicles ( with Traffic Massages ) in order to create social awareness among the people regarding the traffic rule.

15. BOK joined hands with Naxal Yuva Mandal in order to restore Naag Pokhari with its mission towards CSR focusing environment activities.

28

Branch & Network of Bank of Kathmandu

Head OfficeBank of Kathmandu Limited, P.O. Box 9044, Kamal Pokhari, Kathmandu, NepalSWIFT: BOKLNPKATelex: 2820 BOK NPTel: (977 1) 4414541Fax: (977 1) 4418990Email: [email protected]

Kamal Pokhari Branch Bank of Kathmandu LimitedKamalpokhari, Kathmandu, Nepal

Urlabari Branch Bank of Kathmandu LimitedUrlabri-4, Itahara Road, Urlabari, Nepal

Tel: 021-541881, 541882 Fax: 021-541883

ATM LOCATIONS

BOK owned ATMs

• Bank of Kathmandu Limited, Kamal Pokhari, Kathmandu• Bank of Kathmandu Limited, New Road, Kathmandu• Bank of Kathmandu Limited, Supreme Court, Singha Durbar, Kathmandu• Bank of Kathmandu Limited, Krishna Tower, New Baneshwor, Kathmandu

30

• Bank of Kathmandu Limited, Jawalkhel, Lalitpur • Bank of Kathmandu Limited, Nepalgunj• Bank of Kathmandu Limited, Pokhara • Bank of Kathmandu Limited, Namche • Bank of Kathmandu Limited, Surkhet • Bank of Kathmandu Limited, Ghorahi • Bank of Kathmandu Limited, Butwal • Bank of Kathmandu Limited, Chabahil, Chuchhepati, Kathmandu • Bank of Kathmandu Limited, New Baneshwor • Bank of Kathmandu Limited, Thamel • Bank of Kathmandu Limited, New Road Lounge, Dharmapath • Bank of Kathmandu Limited, Gyaneshwor • Bank of Kathmandu Limited, Tripureshwor • Bank of Kathmandu Limited, Kumaripati Lounge • Bank of Kathmandu Limited, Kohalpur • Bank of Kathmandu Limited, Tikapur • Bank of Kathmandu Limited, Guleriya • Bank of Kathmandu Limited, Bhaktapur• Bank of Kathmandu Limited, Attariya• Bank of Kathmandu Limited, Gongabu• Bank of Kathmandu Limited, Hetauda• Bank of Kathmandu Limited, Birgunj• Bank of Kathmandu Limited, Janakpur• Bank of Kathmandu Limited, Biratnagar• Bank of Kathmandu Limited, Itahari• Bank of Kathmandu Limited, Chabahil• Bank of Kathmandu Limited, Om Hospital

ATM location under SCT Network:

Inside Valley:1. Himalayan Bank Limited, Thamel. 2. Himalayan Bank Limited, Newroad. 3. Himalayan Bank Limited, Patan. 4. Himalayan Bank Limited, Mangal Bazar 5. Himalayan Bank Limited, Maharajgunj. 6. Himalayan Bank Limited, Bhaktapur. 7. Himalayan Bank Limited, New Road (Near Hot Breads.) 8. Bank of Kathmandu, Kamaladi. 9. Bank of Kathmandu, New Road. 10. Everest Bank Limited, New Baneshwor. 11. Everest Bank Limited, Khicha Pokhari, New Road. 12. Everest Bank Limited, Pulchowk. 13. Everest Bank Limited, TIA (Airport.) 14. Laxmi Bank Limited, Hattisar. 15. NCC Bank Limited, Chabahil. 16. NCC Bank Limited, Bagbazar. 17. Machhapuchchhre Bank limited, Putali sadak. 18. Blue Bird Department Store, Lazimpat. 19. Blue Bird Department Store, Tripureshwor. 20. Nanglo, Durbarmarg. 21. Hotel Garuda, Thamel. 22. Metro Mall Soaltee Compound, Tahachal. 23. Big C Shopping Center ,Gaushala, Kathamadu. 24. NIC Bank Limited, Kamaladi 25. Lumbini Bank Limited, Durbarmarg. 26. Suvam Convenience Store, Maharjgunj. 27. BhatBhateni Department Store, BhatBhateni. 28. Nabil Bank Limited, Kantipath 29. Nabil Bank Limited, New Road. 30. Nabil Bank Limited, Kupondole. 31. Nabil Bank Limited, Maharajgunj. 32. Thamel Mart, Thamel. 33. Bakery Café, Tridevi Marg, Thamel. 34. Gemini Grocer, Bouddha, Tushal.

31

35. Bhaktapur Durbar Square, Bhaktapur. 36. Nepal Bangladesh Bank Limited, Kathmandu Plaza. 37. Nepal Bangladesh Bank Limited, Kumaripati.

Outside the Valley:

38. Laxmi Bank Limited, Banepa. 39. Laxmi Bank Limited, Birgunj. 40. Bank of Kathmandu Limited, Pokhara. 41. Sudesh Emporium, Chipledhunga, Pokhara 42. NIC Bank Limited, Biratnagar 43. Machhapuchchhre Bank Limited, Jomsom 44. Lumbini Bank Limited, Narayanghad. 45. Nabil Bank Limited, Biratnagar. 46. Nabil Bank Limited, Dharan. 47. Nabil Bank Limited, Butwal. 48. Chipledhunga, Pokhara.

Everest BANK :

Everest bank Limited started its operation in 1994 with an objective is to provide an efficient banking services to various segments of the society. The bank is providing friendly services through its Branch Network. All the branches of the bank are connected through anywhere which helps customers to do all their transactions from any branches other than where they have their account.

To help Nepalese citizens working aboard, the bank has entered into arrangements with the banks and finance company in different countries which enable quick remittance of funds by the Nepalese citizens.

The bank has been focusing on expanding its operation outside Nepal and has identified some of the emerging economics which offer large business potential. Bank has also set up its representitive officers at New Delhi to support Nepalese Citizens remitting money and advising banking related sources.

Punjab National Bank of India, Our joint venture partner is the largest nationalized bank in India. PNB holds 20% equity in the bank.

Vision

To evolve & position the bank as a progressive, cost effective & customer

friendly institution providing comprehensive financial and related services.

To integrate the frontiers of technology & serving the various segments of

society.

To be committed to excellence in corporate values.

32

Mission

To provide excellent professional services & improve its position as a leader in

the field of financial related services.

To build & maintain a team of motivated and committed workforce with high

work ethos.

To use the latest technology aimed at customer satisfaction & act as an effective

catalyst for socio-economic developments.

Awards

The bank has been conferred with “Bank of the Year 2006, Nepal” by the banker,

a publication of financial times, London.

The bank was bestowed with the “NICCI Excellence award” by Nepal India

chamber of commerce for its spectacular performance under finance sector

Pioneering achievements

Recognizing the value of offerings a complete range of services, we have

pioneered in extending various customer friendly products such as Home Loan,

Home Equity Loan, Vehicle Loan, Loan Against Share, Loan Against Life

Insurance Policy and Loan for Professionals.

EBL was one of the first bank to introduce Any Branch Banking System (ABBS)

in Nepal.

EBL has introduced Mobile Vehicle Banking system to serve the segment

deprived of proper banking facilities through its Birtamod Branch, which is the

first of its kind.

Slogan of Everest Bank Limited

The slogan of the bank has remained as “…the name you can Bank upon”

33

Nepalese Promoters

50%

General Public30%

Joint Venture Partner

20%

Shareholding Pattern

50 % of the shares are owned by the local promoters, 20% by our joint venture partner

Punjab National Bank, India and 30% of the shares are owned by the general public.

Figure 3.3: Shareholding pattern

(Source: EBL annual report 2007/2008)

34

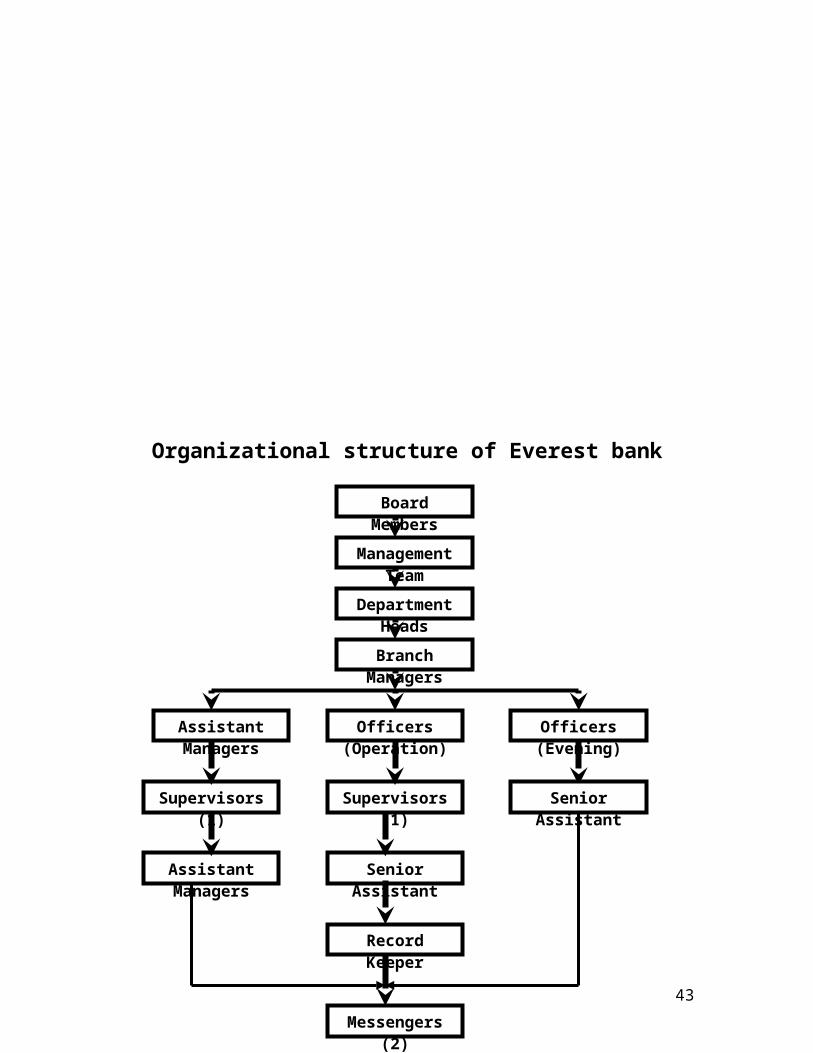

Organizational structure of Everest bank limited

Figure 3.8: Organizational Structure of EBL

35

Assistant Managers

Supervisors (1) Senior Assistant

Senior Assistant

Record Keeper

Messengers (2)

Supervisors (1)

Assistant Managers

Officers (Operation)

Board Members

Management Team

Department Heads

Branch Managers

Officers (Evening)

Board of Directors

36

Product and Services of EBL

Deposit Schemes

EBI offers a wide range of deposits Schemes in both local and foreign currencies to help us earn competitive interest rates in order to maximize higher returns on investments.

Current Account:EBL offers a wide range of products and services designed to make banking easier and to match each and every customer's requirements. This account is non-interest bearing account and there is no limit for withdrawal and deposits in this account. We provide internet user login for this account incase of single signatory.

EBL's Current Account offers you various benefits and flexibility.

◊ Free Cheque books

◊ Free monthly statement

◊ Unlimited Withdrawal

◊ Extended Banking Hour

◊ 365 days banking

◊ ATM cum Debit card in association with SCT.

◊ Free Statement on demand.

◊ Unlimited withdrawal.

◊ Evening counter facility.

Saving accounts:EBL saving account is a deposit account held at a bank maintained by a customer for the purpose of accumulating funds over a period of time while earning an interest. Saving account can be opened in NPR for the Nepalese citizen and USD for foreign citizens with valid password and job appointment letter.

Saving premium accounts: The savings that will shine bright in the future for you and your family.The minimum balance required for Saving Premium Fund Accounts shall be Rs. 1 lakhs.Interest is calculated on daily balance basis and paid half yearly.

Sunaulo Bhawishya Yojan: To cater to people who have the habit to save in a regular basis and avail the bulk sum at the end with a high yielding interest rate the bank launched the recurring deposit. The deposit is targeted among the middle class families who save for specific purpose like purchase of items, marriage etc. Sunaulo Bhavishya Yojana is most suitable for accumulating regular small savings into substantial amount. The bank can plan and provide for a large investment amount at a future date out of regular small savings. On maturity you shall get the principal amount (i.e. the installment) along with half yearly compounded interest.

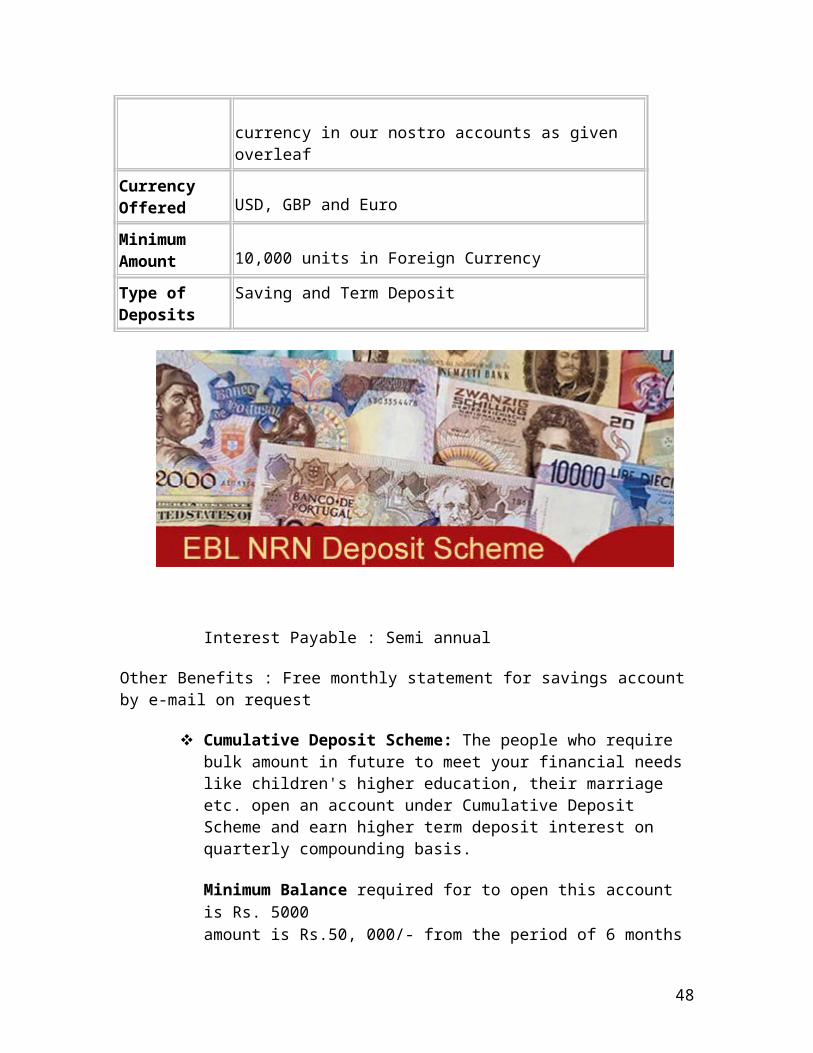

EBL NRN Deposit

EBL welcomes you to open Foreign Currency Deposits. As per the NRNs ordinance 2062 such deposits along with interest are fully repatriable.

Salient Features of EBL NRN Deposit SchemeAvail attractive interest rate on Foreign Currency along with additional 0.5% on NPR deposits.

Who can open Non Resident Nepalese (NRN) as defined in NRN ordinance 2062, Article No. 2

WhereAll our branches

How By credit received in convertible foreign currency in our nostro accounts as given overleaf

Currency Offered USD, GBP and Euro

Minimum Amount 10,000 units in Foreign Currency

Type of Deposits

Saving and Term Deposit

38

Interest Payable : Semi annual

Other Benefits : Free monthly statement for savings account by e-mail on request

Cumulative Deposit Scheme: The people who require bulk amount in future to meet your financial needs like children's higher education, their marriage etc. open an account under Cumulative Deposit Scheme and earn higher term deposit interest on quarterly compounding basis.

Minimum Balance required for to open this account is Rs. 5000

amount is Rs.50, 000/- from the period of 6 months upto 5 years. Period of

Deposit is 6 months upto 5 years

Maturity Value

Principal amount of deposit with upto date interest shall be paid on maturity

date.

.

Fixed Deposit: EBL has introduced several innovative schemes under Fixed Deposit designed to cater to the needs of various segments of customers to meet your specific requirement. You can open fixed deposit from 15 days to 5 years. The given interest rate remains unchanged during the period of the deposit. A certificate of Deposit (FDR) is issued only for fixed deposits. Minimum Balance required for fixed deposit is NPR: 10,000. Interest is paid on quarterly basis to the nominated account maintained at EBL.

Participation in the scheme

Any individual including a minor, Proprietorship/Partnership Firms,

Associations, Company/Corporate Bodies, Trust, Charitable and Education

39

Institutions, Municipalities, Government/Quasi Government Bodies, NGOs,

INGOs etc can open account under the scheme.

Minimum Balance

NPR: 10,000.00 is required for fixed deposit.

Interest Rate:

Interest is paid on quarterly basis to the nominated account maintained at

EBL.

Unfixed fixed deposit: This scheme allows benefits of higher term deposit rate with quarterly compounding interest while earning interest on it. Participation in the schemeThe scheme is suited for all categories of depositors like Individuals, Sole Prop. Concerns firm, Trusts and Limited Companies who wish to park their temporary surpluses in Fixed Deposits, thereby earning higher rates of interest as well as withdraw or repay the amount in between depending upon their needs.Participation is not for all the depositors. Blind, illiterate and minors cannot open this A/C.

Deposit AmountMinimum Rs. 50,000/-

Period of Deposit6 months upto 5 years

Maturity ValuePrincipal amount of deposit with upto date interest shall be paid on maturity date.

Premature CancellationAllowed at lower rate of interest

USD Account:Those individuals and companies who earns/ get funded in dollars can open USD Account at EBL branches.

Required documents for deposits:

40

Minimum Balances for accounts may vary across branches.For personal accounts:

Citizenship Certificate or Passport 2 PP size photos

Partnership Agreement deed Firm Registration Certificate Tax Certificate Citizenship Certificate of Partners 2 PP size photos of partners

Limited Company Account:

Registration Certificate Memorandum & Articles of Assocation Name, Address of directors & Office Bearers of the Limited Company with

copy Citizenship Certificate Name & Signatures of the Persons Authorised to Operate an account Operation Commencement Certificate (for Public Ltd. Co.) Resolution of Board of Directors regarding opening & conduct of an account Tax Certificate

Club Society & Association Account:

Registration Certificate List of Office Bearers Resolution Regarding Opening & Conduct of Account Name & Signature of the persons authorized to operate the account

- All EBL branches are now connected by ABBS.

Loan Products:

41

Rental loan

Home Loan: In order to meet the needs of home seekers, Everest Bank Ltd.

has launched a scheme for Direct Housing Finance for individuals for

construction /acquisition/ purchase of house/flat allotted by the private

builders or Development Authorities and also for carrying out repairs/

renovation/ additions/alteration to the house/flat.

Eligibility

1. Individuals in permanent service or having their own business whose gross

monthly income along with that of the spouse is at least double of the

monthly installment of the loan.

2. Age of the applicant normally shall not exceed 60 years at the time of loan

sanction.

Margin Money

Minimum 25%

Interest Rate

upto 5 years - 9.00% p.a

5-8 years - 9.50% p.a

Above 8 years - 10.50% p.a

Payment

Period: In equal monthly installments - maximum up to 20 years.

Repayment of the loan with interest shall not ordinarily extend beyond the

age of 65 years of borrower.

Home equity loan

Eligibility

42

Existing housing loan borrowers whose past repayment behavior is

satisfactory and the account is running regular & whose income level has

increased.

Age of the applicant should not exceed 57 years.

Purpose

For outright purchase of new house.

For additions/ construction over the existing house.

For purchase of vehicle.

For educational purpose.

For business Overdraft.

For personal OD/TL (for purchases, expenses, etc).

Amount of Loan

Minimum amount of the loan is Rs.2 lacs and maximum amount is Rs.15 lacs. 90% of the home equity value or required amount of loan whichever is lower.

Vehicle Loan: Individuals in permanent service or having their own business whose gross monthly income along with that of the spouse is at least double of the monthly installments can apply for the purchase of new Car/Van/Jeep at 9.50% per annum.The loan amount to 30 times the net monthly salary/income for Individuals and as per need basis for Business Concern, to be repaid in 60 to 84 Equated Monthly Installments.

Education Loan: EBL provides this loan to deserving students of Nepali Nationality for studies in SAARC countries or abroad at an interest rate of 10-10.50% against personal guarantee from the parents and a 100% security.

Future Lease Rental: This scheme has been specially designed keeping in mind the property owners of large commercial/residential buildings. As a measure to improve liquidity and enhance prospects for better use of money for the bank’s customer, the bank is providing loans against future lease rentals under this scheme.

43

Professional Loan: It is a scheme for financial professionals who are self

employed. The loan can be provided for the purchase purchase of equipment,

purchase of furniture, furnishing of the office premises and

Working Capital requirement. Loan against Mortgage: Loan against mortgage of immovable property will

be allowed to individuals, business employee for meeting their business and personal needs.

Loan against Life Insurance Policy (LIP): EBL has policy of advancing against the security of life Insurance Policies (LIP) to an extent of maximum 90% of surrender value of Life Insurance Policy at 8.5% payable on a quarterly basis.

Bike Loan: Individual having fixed source of income / existing credit clients / relatives of credit clients / staff members of different organizations/ wholesalers / dealers / retailers / business concerns with regular income source, valid driving license holder and citizenship certificate holder.

Share Loan: Individuals/Firms and Companies are eligible for share loan. Advances against primary security of physical share or shares in dematerialized from approved by head office to be granted to individuals / firms/ Companies to meet their requirements.

Tractor and Water Pump Finance: This loan is provided by EBL for the purchase of tractor or water pump sets as fixed term loan to a maximum of 80% of the proposed equipment and 5 years tenure at 9.5% interest.

Corporate Loan

1. Working Capital Finance

EBL provide the working capital requirement of business by assessing the current asset and liabilities. The business can draw up to a limit determined by the drawing power which is appraised on a regular basis. The bank has been successful in servicing the working capital needs especially of the trading units. The bank makes a continuous customer visit to ensure that the requirement is met on time and up to an optimum level.

2. Project Finance

Depending on the projects rate of return, repayment ability, cash flow and generation of cash surplus various projects are financed. The technical, financial, economical and managerial competencies are appraised in such cases and decisions are taken accordingly.

44

3. Trade Finance

Through an extensive global network that facilitates domestic and international transaction we are able to meet customer’s need of import, export, payments through offering facilities like LCs, SWIFT transfers, Guarantees etc. Trust Receipt loans are offered to retire import bills. The bank also offers pre shipment and post shipment loans as part of export finance.

4. Consortium Finance

The bank has been arranging for financial closure of various large projects through leading various consortium finance. We have offered such services to various business segments like Hydropower, Manufacturing Industry, Hospital etc. We would explore for such possibilities of finance in the form of lead as well as member bank in the future.

Remittance

Inward Remittance

India

Middle East and South East Asia (Remit from Everest Remit )

Rest of the world

Speed Remittance in India

EBL is providing Speed Remittance facility through which EBL customer can remit fund

from Nepal to CBS branches of PNB India. This is online fund transfer facility and

modern concept in remittance service in the history of Nepal.

Everest Remit (Online Product of EBL)

EBL has developed its own web-based remittance product known as EVEREST REMIT

and officially launched the same from UAE on 25th July, 2006. Currently, EBL receives

remittance payments from different Exchange Houses covering countries such as UAE,

Qatar, Bahrain, Malaysia and UK and are disbursed through its wide network.

Outward Remittance

Outward remittances of foreign currency in Nepal are subject to central bank's directives.

We provide you a convenient mode of your remittance/payment within the permitted

Associated with Smart Choice Technology (SCT), it facilitates wide sharing of

ATMs under SCT network from more than 350 Locations throughout Nepal.

Functionally, it can be called an electronic check, as the funds are withdrawn directly

from the bank account.

Everest Bank Ltd (EBL), a joint venture partner of Punjab National Bank (PNB) is

always committed towards excellent service for the people who believe in quality

banking. Introduction of EBL Debit card is a step in the same direction. EBL Debit card

can also be issued for all existing customers of Everest Bank Limited.

EBL Debit card is eligible for all existing customers for Everest Bank Ltd. EBL

Debit card can also be issued in joint accounts. It can be issued to both the account

holders and they may operate their transaction through ATM into same account.

Internet Banking

Currently following services are available through our internet banking.

Account summary/ Statements

Balance Inquiry

Fund Transfers

Bill Payments (Currently UTL Bill)

Offline Requests (Cheque books, remittance etc)

Various Alert(Email/SMS)

SMS Banking

Along with internet Banking, EBL has presented its SMS Banking services. Users are

automatically signed up for SMS Banking when they sign up for.

E-Banking etc.

46

Bank On Wheel

Everest Bank Limited has started its Mobile Banking operation since 26th September

2007. This service ‘Bank on Wheels’ as a banking product is the first of its kind in

Nepal. EBL is providing banking facilities at the customer home through mobile

banking.

Facility Provided through Mobile Banking

Cash Withdrawal (Not Exceeding NPR 5 Lacs per day)

ABBS Facility

Issuing Cheque Books

Issuing Account Statements

Issuing of ATM Cards etc.

Providing Information about Bank’s Products

Collection of Credit related files/filed inspection of the area

Other Services.

Branch less Banking

In an endeavor to provide banking facilities to large and well spread out sections

of the remote village, Everest Bank Limited (EBL) has introduced new product as

Everest Bank Ghar- Dailo Banking Sewa, on 17th June 2009, this service is

unique delivery channel in banking services to facilitate rural people in banking

with the help of sophisticated technology. This service is branchless banking

service through point of transaction (POT) machine by using smart cards.

This is a major leap forward towards inclusion through branchless banking. The

customer can avail the facility of banking at his/her own convenient time. Besides

that he/she will earn interest on the savings and this fund will remain secured.

NTC Prepaid Recharge

EBL is providing SMS bill payment and Mobile recharge facility to the NTC mobile user. With the help of this service the customer can make the bill payment or recharge pre-paid mobile at any time and any where.

Nepal Industrial & Commercial Bank Limited (NIC Bank)

Nepal Industrial & Commercial Bank Limited (NIC Bank) commenced its operation on 21 July 1998 from Biratnagar. The Bank was promoted by some of the prominent business houses of the country. The current shareholding pattern of the Bank constitutes of promoters holding 51% of the shares while 49% is held by the general public. NIC Bank has over 34,000 shareholders. The shares of the Bank are actively traded in Nepal Stock Exchange with current market capitalization of about NPR 10,493 million.

The Bank has grown rapidly with 22 branches throughout the country while several branches are planned to be opened this year. All branches are inter-connected through V-Sat and are capable of providing real time on-line transactions.

The Bank is the first commercial Bank in Nepal to have received ISO 9001:2000 certification for quality management system. Furthermore, NIC Bank became the 1st Bank in Nepal to be provided a line of credit by International Finance Corporation (IFC), an arm of World Bank Group under its Global Trade Finance Program, enabling the Bank's Letter of Credit and Guarantee to be accepted/ confirmed by more than 200 banks worldwide.

To add to these achievements, the Bank has also been awarded the "Bank of the Year 2007-Nepal" by the world-renowned financial publication of The Financial Times, U.K.-The Banker. This is the fruit of the Bank's outstanding performance backed by belief and support of its customers towards the Bank.

The Bank is run by professionals and believes in the highest standards of corporate governance.

The Board of Directors of the Bank is supported by a management team, which comprises of young, enthusiastic professionals. The Bank has successfully embarked on a multi-pronged strategy of consolidation, administrative streamlining, human resource up-skilling, strategic cost management, focused non-performing assets management, balance sheet and treasury management and controlled asset growth, in tandem with strengthening the credit culture as well as strategic marketing and sales.

NIC Bank's organizational structure is designed to support its business goals. However, it is flexible enough in seeking to ensure effective control and supervision and consistency in standards across all businesses at the same time. The organization structure is divided into five major areas viz Consumer Banking, Business Banking, Special Assets Management, Treasury and Liability Marketing and Transaction Banking all of which are supproted by the corporate center.

The Bank is committed towards providing financial services to its patrons by the means of efficient and cost effective service delivery through its Transaction Banking, Consumer Banking, Business Banking and Treasury divisions.

Consumer Banking comprises of consumer lending, retail credit products and banking services for individuals with dedicated teams. Consumer Banking services include home loans, auto loans, personal loans, education loans, travel

56

loans, etc.

Liability Marketing & Transaction Banking comprises of institutional and personal deposit products and transaction banking services including debit cards, ATMs, safe deposit lockers, payment services, drafts, remittance, SMS Banking, Travelers' Cheques, etc.

Business Banking group comprises of corporate banking business including credit products and other banking services. It also includes corporate transaction banking, trade finance services, foreign exchange and corporate financing solutions including project & infrastructure finance, working capital & term loan credit, structured financing, syndication, cash management and advisory services.

Special Assets Management division is responsible for managing non-performing and restructured loans.

Treasury is responsible for management of liquidity and exposure to market risk, mobilization of resources, balance sheet management, pricing, investor relations and international operation. The Bank's treasury division offers a full range of Risk Management and Cash Management products and provides effective Treasury advisory services.

Further, Treasury also leverages its strong relationships with financial institutions to provide a wide range of Banking services.

The Corporate center comprises all shared services and corporate functions including finance, secretarial, risk management, legal, human resources, branding and corporate communications.

The Compounded Annual Growth Rate (CAGR) of the Bank for the last 5 years is one of the highest in the industry. This shows that the Bank's performance has been consistent over the duration of five years. 5 year CAGR of key performance indicators of the Bank are as under.

NIC BANK’S Organizational structure is designed to support its business goals. And for the purpose, organizational structure is divided into five major areas:

1. Consumer Banking2. Business Banking3. Risky Management4. Treasury5. Liabilities Marketing And Transaction Banking

VisionTo become one of the most respectable banks in Nepal based on honorable conduct and long-term financial performance.

MissionTo become a leading bank in Nepal by providing complete financial solutions to our customers, superior value to our shareholders and promising growth opportunities to our employees.

57

The composition of the Board of Directors of the Bank is, as per the Company Act and Bank and Financial Institution Ordinance 2063. The Directors of the Bank are eminent personalities drawn from various fields. The Directors have been contributing their professional knowledge, experience and expertise in their respective areas of specialization for the development of the Bank. The Directors are fully committed to the Corporate governance model adopted by the Bank, which among others, encompasses the principles of full disclosure and transparency, social responsibility and accountability, "zero tolerance" compliance culture, business and customer confidentiality, intolerance of conflict of interests, and an independent management.

Jagdish Prasad Agrawal Chairman

Tulsi Ram Agrawal Director

Mr. Lokmanya Golchha Director

Nirmal Kumar Agrawal Director

Rajendra Aryal (Public Shareholder) Director

Birendra Kumar Sanghai (Public Shareholder) Director

Management Team

Sashin Joshi Chief Executive Officer

Niraj Shrestha General Manager - Business Banking

Bimal Daga Head - Credit Business Banking

Purna Man Napit Head Audit & Compliance

Bam Dev Dahal Manager - Projects and Strategic Sourcing

Bhanu Dabadi Manager - Consumer Lending

Deepak K. Shrestha Manager - Credit Consumer Banking

Sushil Bhattarai Manager - Information & Technology

Saroj Shrestha Relationship Manager - Business Banking

Bhesh Raj Khatiwada Relationship Manager - Business Banking

Rajesh Raj Gautam Manager - SME

58

Sanchita Gorkhali Manager - Human Resource

Shrina Joshi Manager - Corporate Affairs

Branch Managers

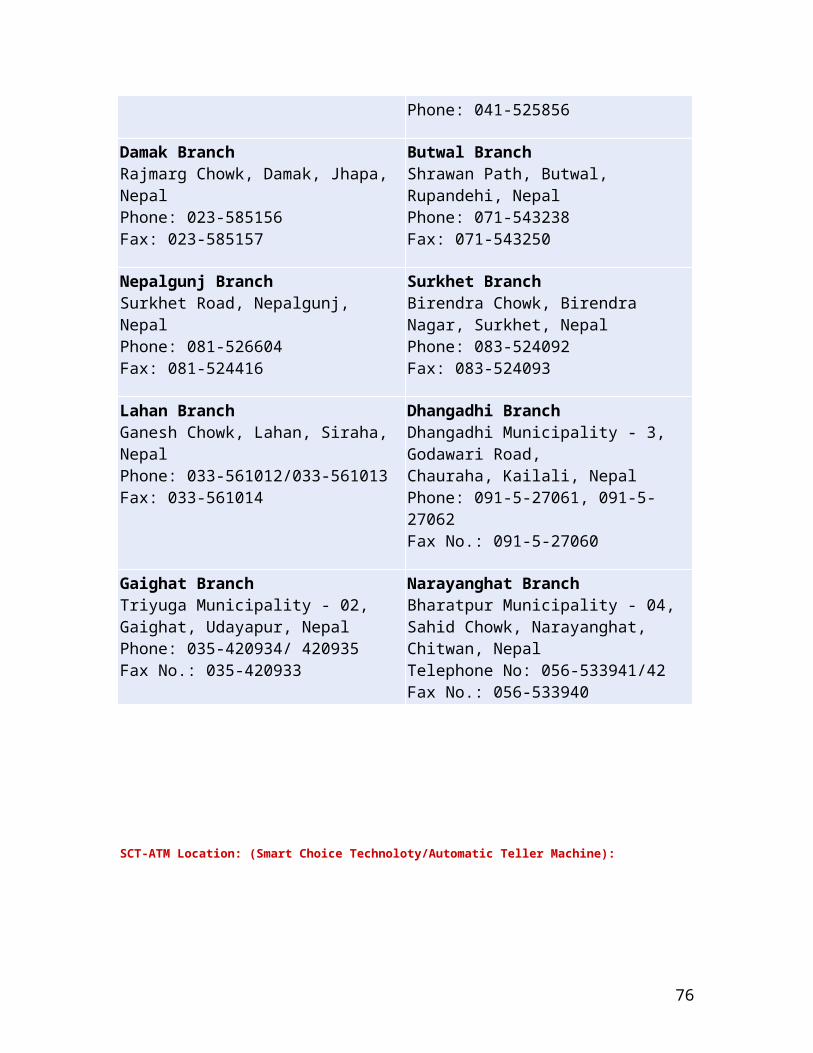

Arjun Kr. Chhetri New Road, Kathmandu

Binay Dahal Adarsh Nagar, Birgunj

Birendra Thakur Ganesh Chowk, Lahan

Bishnu Pandey Rajmarg Chowk, Damak

Yogendra Rana (Officiating) Mahendrapath, Dharan

Yuba Raj Dahal Birendra Nagar, Surkhet

Dinesh K. Sharma Ram Mandir Chowk, Janakpur

Jayendra Rawal Surkhet Road, Nepalgunj

Sangita Satyal (Officiating) Kamaladi, Kathmandu

Prajeeta Joshi Battisputali, Kathmandu

Priyanka Ranjit Suryavinayak, Bhaktapur

Rajendra Luitel Dhangadhi, Kailali

Ashok Gurung Shrawan Path, Butwal

Sameer Acharya Mahendra Pool, Pokhara

Shiva Gopal Risal Bhadrapur Road, Birtamod

Sudhir Agrawal Main Road, Biratnagar

Umesh Acharya Pulchowk, Lalitpur

Bal Krishna Shrestha Kirtipur, Kathmandu

Smriti Bhandari Samakhusi, Kathmandu

Arjun Shrestha Gaighat

Merina Dangol Satdobato

Sunil Rana Narayanghat

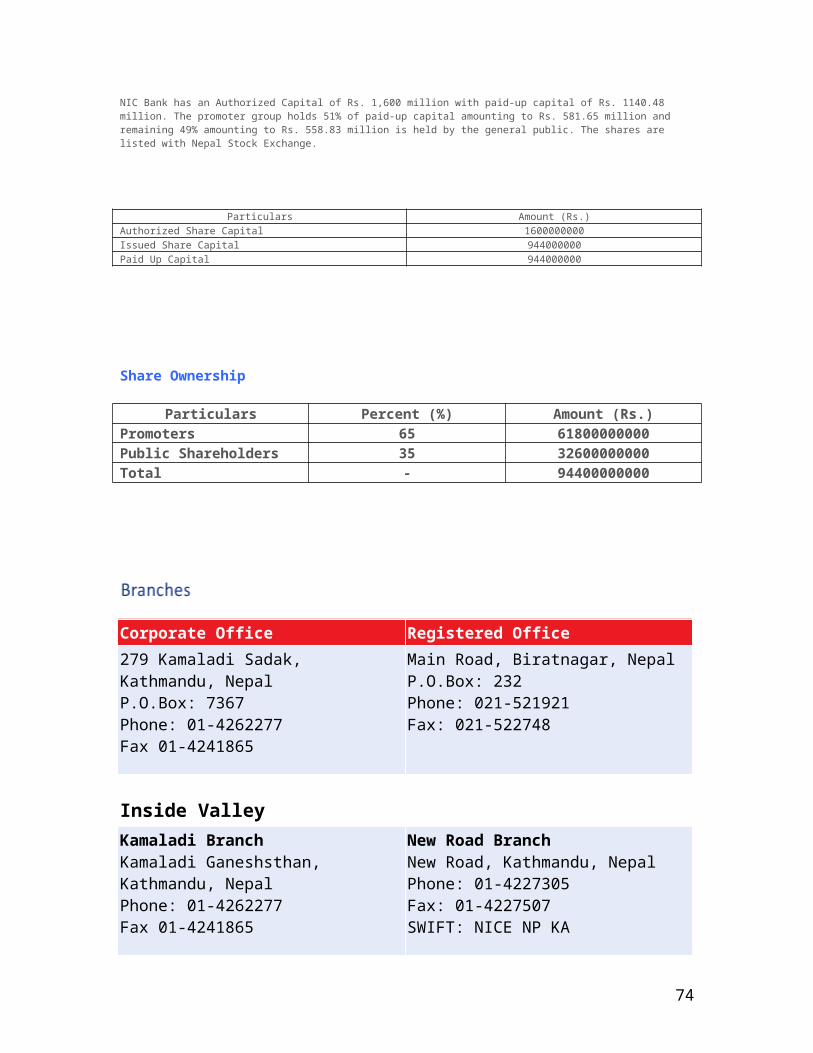

NIC Bank has an Authorized Capital of Rs. 1,600 million with paid-up capital of Rs. 1140.48 million. The promoter group holds 51% of paid-up capital amounting to Rs. 581.65 million and remaining 49% amounting to Rs. 558.83 million is held by the general public. The shares are listed with Nepal Stock Exchange.

59

Particulars Amount (Rs.)Authorized Share Capital 1600000000Issued Share Capital 944000000Paid Up Capital 944000000

9 Himalayan Bank Limited Bluebird Departmental Store Tripureshwor

10 Himalayan Bank Limited New road (Near Hot Bread)

11 Himalayan Bank Limited BhatbheteniDepartmental Store

12 Himalayan Bank Limited Teaching HospitalMaharajgunjKathmandu

13 Himalayan Bank Limited World Trade Center

62

TripureshworKathmandu

14 Himalayan Bank Limited Bisal Bazar PatanKathmandu

15 Himalayan Bank Limited Teku

16 Himalayan Bank Limited Halchowk

17 Bank of Kathamandu Kamaladi(Inside)

18 Bank of Kathamandu Kamaladi(Outside)

18 Bank of Kathamandu New road

19 Bank of Kathamandu Supreme Court

20 Bank of Kathamandu Jawalakhel

21 Bank of Kathamandu Krishna TowerNew Baneshwor

22 Everest Bank Limited New Baneshwor

23 Everest Bank Limited New Road

24 Everest Bank Limited TIA (Airport)

25 Everest Bank Limited Pulchowk

26 Everest Bank Limited Lazimpat

27 Everest Bank Limited Balaju

28 Everest Bank Limited New Baneshwor Near Apex College

29 Everest Bank Limited Gwarko

30 Laxmi Bank Limited Hattisar

31 NCC Bank Limited Bagbazar

32 NCC Bank Limited Chabahil

33 NIC Bank Limited Kamaladi

34 NIC Bank Ltd Bishalbazar Newroad

35 Machhapuchchhre Bank Limited Putalisadak

36 Machhapuchchhre Bank Limited Kathamandu Mall

37 Machhapuchchhre Bank Limited Nepal Rastra BankBaluwatar

38 Machhapuchchhre Bank Limited Thapathali

39 Machhapuchchhre Bank Limited Singha Durbar

40 Machapuchchhre Bank Ltd Kalimati

41 Machapuchchhre Bank Ltd NEARatnapark

42 Machapuchchhre Bank Ltd Mangal Bazar

43 Lumbini Bank Limited Durbar Marg

63

44 Hotel Garuda Thamel

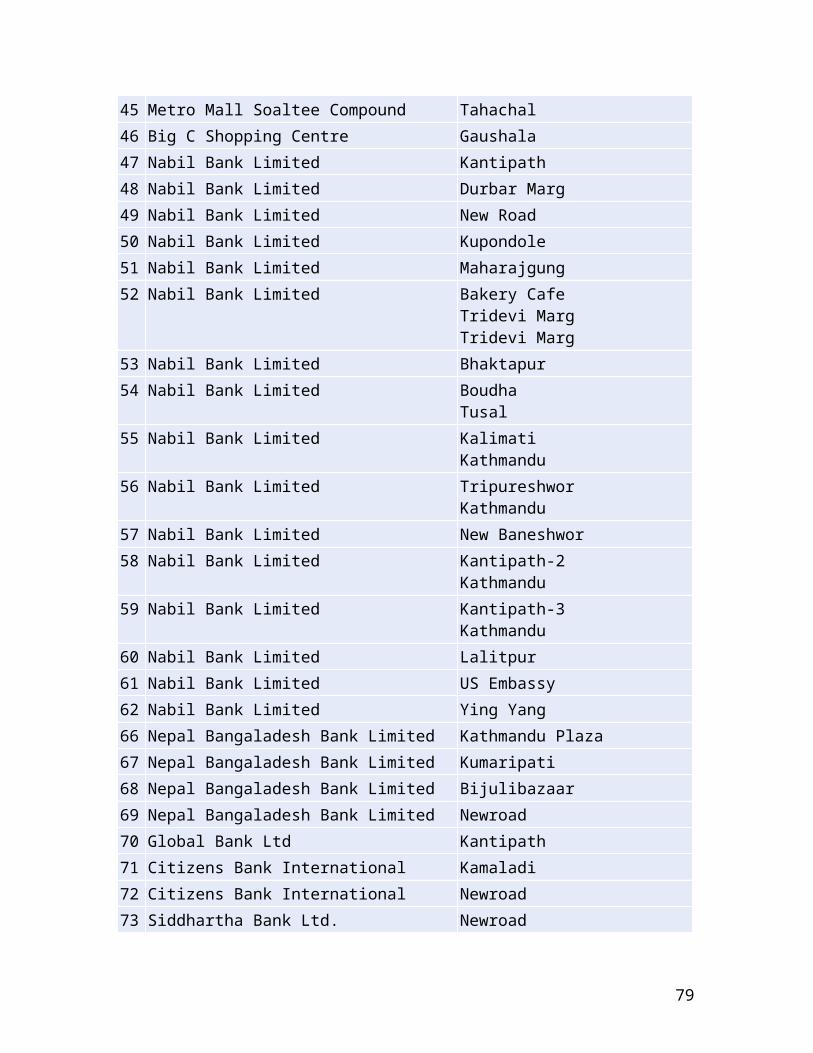

45 Metro Mall Soaltee Compound Tahachal

46 Big C Shopping Centre Gaushala

47 Nabil Bank Limited Kantipath

48 Nabil Bank Limited Durbar Marg

49 Nabil Bank Limited New Road

50 Nabil Bank Limited Kupondole

51 Nabil Bank Limited Maharajgung

52 Nabil Bank Limited Bakery CafeTridevi MargTridevi Marg

53 Nabil Bank Limited Bhaktapur

54 Nabil Bank Limited BoudhaTusal

55 Nabil Bank Limited KalimatiKathmandu

56 Nabil Bank Limited TripureshworKathmandu

57 Nabil Bank Limited New Baneshwor

58 Nabil Bank Limited Kantipath-2Kathmandu

59 Nabil Bank Limited Kantipath-3Kathmandu

60 Nabil Bank Limited Lalitpur

61 Nabil Bank Limited US Embassy

62 Nabil Bank Limited Ying Yang

66 Nepal Bangaladesh Bank Limited Kathmandu Plaza

67 Nepal Bangaladesh Bank Limited Kumaripati

68 Nepal Bangaladesh Bank Limited Bijulibazaar

69 Nepal Bangaladesh Bank Limited Newroad

70 Global Bank Ltd Kantipath

71 Citizens Bank International Kamaladi

72 Citizens Bank International Newroad

73 Siddhartha Bank Ltd. Newroad

74 Siddhartha Bank Ltd Old Baneshowr

75 KIST Merchant Banking and Finance Ltd Anamnagar

76 KIST Merchant Banking and Finance Ltd TripureshworNTC

77 KIST Merchant Banking and Finance Ltd Jawalakhel

64

78 KIST Merchant Banking and Finance Ltd Newroad

79 KIST Merchant Banking and Finance Ltd Sukedhara

80 Clean Energy Development Bank Ltd Sitapaila

81 Prime Commercial Bank Ltd Newroad

82 Development Credit Bank Ltd. Newroad

83 Vibor Bikas Bank Ltd. Tripureshwor

84 Prabhu Finance Company Ltd. Kantipath

85 IME Financial Institution Ltd. Gongabu

86 Kasthamandap Development Bank Ltd. Newroad

87 Nepal Development Employment And Promotion Bank Ltd.

Kamaladi

SCT-Outside Kathmandu Valley

S.N

Bank Location

2 Laxmi Bank Limited Birgunj

3 Bank of Kathamandu Pokhara

4 Bank Of Kathmandu Namche

5 Bank Of Kathmandu Nepalgunj

6 Bank Of Kathmandu Surkhet

7 Bank Of Kathmandu Ghorahi

8 Lumbini Bank Limited Narayanghad

9 Siddhartha Bank Limited Biratnagar

10 Lumbini Bank Limited Narayanghad

11 Nabil Bank Limited Biratnagar

12 Nabil Bank Limited Dharan

13 Nabil Bank Limited Butwal

14 Nabil Bank Limited Pokhara

15 Nabil Bank Limited Damak

16 Nabil Bank Limited Baglung

17 Nabil Bank Limited Narayangarh

18 Nabil Bank Limited Mahendranagar

19 Nabil Bank Limited Dhangadi

20 Nabil Bank Limited Itahari

21 Nabil Bank Limited Hetauda

22 Nabil Bank Limited Dang Ghorahi

65

23 Nabil Bank Limited Tulsipur

24 Nabil Bank Limited Birtamod

25 Nabil Bank Limited Pokhara

26 Nabil Bank Limited Bhairahawa

27 Machhapuchchhre Bank Limited Chipledhunga Pokhara

28 Machhapuchchhre Bank Limited Bagar Pokhara

29 Machhapuchchhre Bank Limited H/O Prithvi Chowk Pokhara

30 Machhapuchchhre Bank Limited Itahari

31 Himalayan Bank Limited Pokhara

32 Himalayan Bank Limited Birgunj

33 Himalayan Bank Limited Hetauda

34 Himalayan Bank Limited Bharatpur

35 Himalayan Bank Limited Bhairahawa

36 Himalayan Bank Limited PokharaLakeside

37 Himalayan Bank Limited Butwal

38 Himalayan Bank Limited Dharan

39 Himalayan Bank Limited PokharaLakeside

40 Everest Bank Ltd Pokhara

41 Everest Bank Ltd Janakpur

42 Everest Bank Ltd Narayangarh

43 KIST Merchant Banking and Finance Ltd. Pokhara

44 KIST Merchant Banking and Finance Ltd. Butwal

45 Paschimanchal Development Bank Ltd. Butwal

46 Siddhartha Development Bank Ltd. Butwal

47 Citizens Bank Biratnagar

48 Malika Vikas Bank Dhangadhi

49 Pashupati Development Bank Banepa

Reward & Achievements

- NIC Bank is the first commercial Bank in Nepal to receive ISO 9001:2000 Certificate for quality management system.

- NIC Bank become the first Bank in Nepal to be provided a line of credit by International Finance Corporation (IFC), an arm of World Bank Group under its global trade finance program, enabling the

66

banks letter of credit and guarantee to be acceptable conformed by more than 200 banks worldwide.

NIC Bank has been able to record substantial increments in balance sheet size and profit since last couple of

years. Key financial figures for the last five years are exhibited in the table below:

Net Profit / Total Assets (%) 1.69 1.60 1.36 0.93 1.52 1.15

Capital Adequacy Ratio (%) 14.6 13.1 12.20 13.54 13.29 13.75

Non Performing Loan / Total Loan (%)

0.9 0.9 1.10 2.60 3.78 3.92

Net Worth 1665 1303 918.0 766.5 684.2 620.4

Product and Services

The Bank believes in continuously offering new and value added services to its customers, with commitment to quality and value to its clients at the same time. Accordingly, the Bank has been in the forefront in launching innovative and superior products having unique customer friendly features with immense success.

The products and services offered by the NIC Bank through its branches all over the country are as follows:

1. Deposits

NIC Bank has maintained various type of deposits accounts as it’s the only main source of banking activity. Also has been providing different facilities in each account.

a. Current Account

67

NIC Bank is committed to making banking easier and more rewarding for you. That is why we have a service account best suited to firms/organizations to deposit and withdraw cash anytime through Counter or self-service devices.

This is an account designed for customers who are looking for a basic package of banking services by maintaining a minimum balance of as low as Rs.10, 000 only.

You get your money whenever it is needed.

b. Normal Saving Account

It can be opened with a minimum balance as low as NPR 5000 and helps to can interest of 3% p.a.

c. Call Account

It is similar to current a/c and does on daily basis yield interest.

d. Fixed Deposit Account

NIC Bank's Fixed Deposit Account is tailored to give you very competitive interest rates. You can be assured of maximizing the growth potential of your savings with us.

Earn premium interest rates from the Fixed Deposit Account's tier rate structure.

Let your money be safe with us and we will make your money work for you.

Tenures

Deposit Rates Prime (%p.a.) Others (%p.a.)

1 month 4.25 4.00

3-6 months 4.50 4.25

1 year 5.75 5.50

> 1 year to 2 years 6.00 5.75

> 2 year to 5 years 6.25 6.00

Above 5 years 6.50 6.25

Structured Deposits Negotiable

e. NIC Business Account

NIC Business Account (NBA) is an interest bearing account aimed at businesses. It is being targeted to Proprietorship firms, Enterprises, Partnership Firms, Private / Public Limited Companies, etc. who maintain/have a need for opening the accounts with bank. Still many firms and companies are out of reach of the banking. NIC Business Account encourages such businesses to maintain accounts by offering interest on daily balance with lot of free and discount banking facilities.

Its facilities include:

Free ABBS Facility

Free Mobile and Telephone Bill Payment

50% discount on locker

Salary Management Solution

F. NIC Life Saving Account

68

Features:

Interest rate of up to 5% p.a.

Free Life Insurances of Rs. 100,000 with Rs. 200,000 of accident cover

Free ATM card issuance

Free any Branch Banking Facility

Free inward remittances

25% discount on Locker Facility (subject to availability)

50% discount on Draft issuance

50% discount on Travelers Cheque Issuance

Multiple/Unlimited withdrawal facility

No maintenance fees

Free Statements upon request

Extended Banking hours including 365 days Banking

And many more benefits

g. Karmashil Bachat Khata ( KBK )

Karmashil Bachat Khata (KBK) specifically designed to provide an opportunity to save small amounts with high returns and various other facilities and cultivate banking habit. This account is developed to avail banking opportunity to middle level working professionals and low /middle class individuals working in various private/government/social organizations, students, retired professionals and farmers, etc.

Features:

Initial deposit of Rs.500

Interest rate of 3 % p.a.

Free NIC Cash Card issuance

Free SMS Banking facilities

Free ABBS facility

Telephone/mobile bill payment facility

25% discount on locker facility

50% discount on Draft & Travelers Cheque Issuance.

h. NIC Shareholder Saving Account ( NSS )

NIC Shareholder Saving Account ( NSS ) was launched in the year 2007 A.D. with the facility of 4% p.a. interest for the minimum balance of NPR 1000. The account provides accidental insurance up to NPR 1000. The account provides accidental insurance up to NPR 100000 and other facilities are like as above.

i. NIC Sikshya Kosh