PROCEEDINGS 29 PROMOTING EFFECTIVE COMPETITION IN UK POSTAL SERVICES Martin Cave Saul Estrin Jos Geeraerts John Ivers Bror Anders Månsson Gregor McGregor Richard Moriarty Ian Reay Frank Rodriguez Ian Senior David Sibbick

Transcript

PROCEEDINGS 29

PROMOTING EFFECTIVE COMPETITION IN UK POSTAL SERVICES

Martin CaveSaul Estrin

Jos GeeraertsJohn Ivers

Bror Anders MånssonGregor McGregor Richard Moriarty

PREFACE The CRI is pleased to publish the papers from Postcomm’s workshop on Promoting Effective Competition in UK Postal Services, which was held in association with the CRI, as its 29th set of Proceedings. Richard Moriarty, the Director of Competition and Regulation at Postcomm, sets out the scope of the Proceedings in the Introduction, and the order of the chapters reflects the order and themes of the day as they were discussed. We hope that the Proceedings will make a contribution to widening understanding of the debate, given the sensitive position which postal services have in the public’s mind. Competition and public services are not always seen as complementary and, given the self-evident problems of the rail sector at this time, it is important that regulation and regulatory policy is transparent and secures public confidence and support. The CRI is grateful to Postcomm for their support, both in working with CRI and assisting the publication of these Proceedings. The CRI would welcome comments on these Proceedings and further analytical work in the area. The CRI publishes work on regulation by a wide variety of authors, covering a range of regulatory topics and disciplines, in its International, Occasional and Technical Paper series. The purpose is to promote debate and better understanding about the regulatory framework and the processes of decision making and accountability. The views of authors are their own, and do not necessarily represent those of the CRI. Comments, enquiries or manuscripts to be considered for publication should be addressed to: Peter Vass, Director, CRI, School of Management, University of Bath, Bath, BA2 7AY. Peter Vass Director, CRI January 2002

iv

v

CONTENTS

Preface

iii

Introduction

Richard Moriarty

1

International experience

1 Full postal liberalisation – experience in Argentina, Finland, Sweden and New Zealand Ian Senior

3

2 Competing in Sweden Bror Anders Månsson

9

The customer view

3 Consumers come first Gregor McGregor

17

4 Business mailers’ views John Ivers

23

Market strategies for new entrants

5 Focusing on value-added services David Sibbick

29

6 Market strategies for new entrants Jos Geeraerts

33

Safeguarding universal service

7 Meeting the universal service obligation in posts Ian Reay and Frank Rodriguez

47

‘Regulatory’ economics and postal competition

8 How far can liberalisation of postal markets go? Martin Cave

75

9 The role of competition in the UK postal service Saul Estrin

89

vi

Richard Moriarty, Director, Competition and Regulation, Postcomm

1

INTRODUCTION Richard Moriarty Postcomm’s primary duty, as independent regulator for the UK postal market, is to ensure that customers continue to benefit from the universal service at an affordable and geographically uniform tariff. Subject to this duty, Postcomm has a duty to further the interests of postal users, where possible by promoting effective competition. As part of our on-going work in fulfilling these statutory duties, Postcomm, in association with the Centre for the study of Regulated Industries (CRI), hosted a Workshop on Promoting Effective Competition in UK Postal Services in October 2001. The aim of the workshop was to provide Postcomm and those attending with the opportunity to discuss the issues set out in Postcomm’s consultation document on promoting effective competition, published earlier in 2001. A diverse range of speakers presented their views on the following issues: International experience of postal liberalisation

• Ian Senior of NERA presented the effects liberalisation has had on

markets, particularly in Finland, Argentina and New Zealand. • A presentation by Bror Anders Månsson of CityMail outlined the

innovative new services and business practices that have been incorporated by operators in Sweden since the market was liberalised.

The consumer view on liberalisation • Gregor McGregor, Chief Executive of Postwatch, ran through the

potential benefits to UK consumers of a liberalised postal market.

INTRODUCTION

2

• Chairman of the Mail Users Association, John Ivers, looked at the benefits increased competition could bring to large mail users.

Market strategies for new entrants in the UK • David Sibbick, Director of Regulation at Hays DX, outlined brief

details of the interim licence granted to Hays DX in September 2001, and how this could influence the market entry strategies of other operators.

• Jos Geeraerts, a strategy consultant for TPG, gave a presentation on the changing nature of the postal market and how Royal PTT Post and TNT plan to adapt and exploit these changes.

Safeguarding the universal service obligation and the role of the regulated incumbent

• Ian Reay, accompanied by Frank Rodriguez, outlined Consignia’s

view on safeguarding the universal service in a competitive market, and how the incumbent plans to adapt to the on-set of competition.

The ‘business economics’ of postal liberalisation

• Martin Cave broadly analysed the postal services market regulation and from a theoretical point of view, and Saul Estrin concluded with a response on the role of competition in the UK postal service.

The audience, comprising largely of operators, large user groups, consultants and academics, ensured that there was a good deal of lively debate throughout the panel discussions and the workshop as a whole. This has, in turn, helped influence our thinking as we prepare to publish our proposals for promoting effective competition in the market, and I can only hope that the workshop proved to be as useful to those that attended as it was to Postcomm.

Ian Senior, Special Adviser, NERA 3

1 FULL POSTAL LIBERALISATION - EXPERIENCE IN ARGENTINA, FINLAND, SWEDEN AND NEW ZEALAND Ian Senior Introduction In 1970, having left Post Office headquarters, I wrote a monograph published by the Institute of Economic Affairs. It made the then revolutionary proposal that the letter monopoly in the UK should be abolished. An editorial in The Economist supported this proposal but elsewhere there was a deafening silence, not least from economists and the then Post Office. Since 1970 I have consistently argued that the postal monopoly was not a ‘natural’ monopoly. Clearly, conveying letters is unlike a utility service, such as water. The privatisation of water services has not produced additional pipelines and sewers running competitively along streets. I have always argued that the economies of scale that are found in collection, transportation, mechanised sorting and delivery could be significant, but did not add up to an economic case that the postal network was, overall, a natural monopoly. Other economists wrestled for years with pages of complex equations and concluded that more data and more research were needed. None started from the obvious point that a letter is just a thing to be carried. So are parcels, and neither Consignia nor other incumbents have had a monopoly of these.

INTERNATIONAL EXPERIENCE

4

Today, the arena for debate has moved forward a long way. The question is no longer if the postal market should be liberalised in the UK and the EU but how. There are really only two overall approaches: gradualism or a big bang. My early papers favoured the latter, but I concede that the experience of the utter rail chaos since liberalisation and privatisation suggests caution. Gradualism might entail, for example, reducing the letter monopoly by weight steps or value over a number of years. It might entail liberalising direct mail, which already is the case in Spain. But the fact is that a big bang approach has been implemented in four countries. In this chapter I am going to describe and comment on what has occurred in Argentina, Finland, New Zealand and Sweden. Where data are available I shall do so using the yardsticks shown below: • Main issues

- Universal service obligations - Number and nature of competitors - Financial impact on incumbents - Impact on services provided - Employment impact

• Diversification by incumbents • Conclusions Argentina Correo Argentino was privatised in September 1997. Its thirty year licence contains a universal service obligation (USO). Other suppliers have entered the market, no doubt on the basis of ‘cream-skimming’ which is a commercially sensible approach. However, Correo argues that the competitors have no USO, avoid employment laws and social taxes, and therefore have an unfair advantage.

IAN SENIOR

5

I am unable to comment on these claims, but a thirty year licence may be inflexible. Has the USO been quantified in a credible way? What proportion of letter traffic does Correo have? Does it have freedom to change its prices at will? What has been the overall effect of competition on quality of service to customers? Clearly it is necessary to distinguish between an uneven playing field caused by competitors not obeying general employment law, which is separate from the regulatory environment concerning Correo’s tariffs, and the USO. However, at this stage, I conclude that the Argentine model of postal liberalisation does not look promising, not least because Correo Argentino filed for Chapter 11 (protection against its creditors) in October 2001. Finland Although the postal monopoly was abolished in 1992, I believe that no significant competitors have entered the market. This is because they would have to pay a levy of up to 20 per cent of their turnover according to the population density of the area(s) they wished to serve. The intention evidently is to prevent cream skimming and to provide funds should it be deemed necessary to compensate Posti for its USO. The result has been a continuation of a stable monopoly environment. In the five years from 1996 turnover, profit and traffic volumes have all increased (22%, 11% and 10% respectively). Staff numbers have been steady implying increased productivity. There was some decrease in business customer satisfaction in 2000 (business, 73%, down from 83%, consumers, 75%, up from 63%) but annual figures fluctuate and emphasis should not be attached to a single year.

INTERNATIONAL EXPERIENCE

6

New Zealand The postal monopoly was abolished on 1 April 1998. New Zealand Post remains wholly owned by the government. It has a USO and is not compensated for it. Its ‘deeds of understanding’ with the government last three years. Under the current deed its standard letter rate is capped at NZ$ 0.45 (13.5p) but the actual rate is NZ$ 0.40 (12.1p). The Deed also covers frequency of deliveries and number of retail outlets (ie, counters); it requires that no rural delivery fee be charged and sets down an obligation for New Zealand Post to accept mail from other postal operators on terms at least as favourable as for other customers. Since liberalisation New Zealand Post has seen increased operating revenue but falling profits (net surplus down to 40% of 1996). The volume of mail and staff numbers are not disclosed. Some competing companies have their boxes on the streets but it is believed that their total volume of traffic is about five per cent. So far New Zealand Post is not complaining that New Zealand Post alone has the USO, as the following quotations illustrate:

“The incumbent postal operator can prosper in a deregulated market”. “The real challenge and threat is not competition on the streets of New Zealand but the growing challenge of electronic substitution and global distribution alliances”.

John Allen, CEO New Zealand Post Enterprises Group, March 2001

Sweden Post The letter monopoly was abolished in 1993 with five years of advance warning. Sweden Post remains owned by the government, which has

IAN SENIOR

7

the power to cap its prices. It has a USO. It receives payment for the delivery of Braille but not for the cost of service to sparsely populated areas. Sweden Post says that it would deliver universally, even without an obligation, but might require grouped mail boxes in sparse areas. About 50 competitors serve local areas, but collectively are thought to have only five per cent of the market. There has been litigation over Sweden Post’s pricing, which some new entrants have claimed to be predatory. In the period 1996-2000 operating revenue went up by 9.4% but profits fell sharply after liberalisation, and losses were made in 1999 and 2000. Staff numbers went down slightly in the period and the number of service points (counters) was down 7% in 1999, compared with 1993. The customer satisfaction index was up 7% in the period. The new technologies The incumbents in Finland, New Zealand and Sweden have all entered purposefully into e-technologies. For example: • in 2001 Finland’s Posti launched an electronic channel to allow

customers to read letters, pay invoices, deal with public authorities and other personal business on the Internet;

• New Zealand Post claims to be the leading e-business in New

Zealand; • Sweden Post will be introducing electronic services for

consumers based on contractual relationships, and describes traditional mail as ‘the old economy’.

Although the frequently predicted death of letters has been much exaggerated, these three incumbents evidently see their future as developing new profitable business in e-communication to

INTERNATIONAL EXPERIENCE

8

compensate for additional competition in letters and the likely decline in the letter market overall. Conclusions Argentina’s model of giving Correo a 30-year licence while apparently leaving competitors free to evade social security and other taxes does not seem applicable in the UK. Finland’s Posti still has an effective monopoly and remains profitable, but the absence of competition is no longer an option in the UK. New Zealand Post operates successfully without a letter monopoly yet still has a USO burden. Sweden Post has coped with competition but made losses in 1999 and 2000. Since Sweden Post may have 95 per cent of the market, these losses are hard to understand. Top managers in New Zealand Post and Sweden Post claim to welcome the spur of competition. By contrast Consignia is fighting liberalisation, in particular using a flawed USO calculation based on a totally hypothetical model of 20,000 to 30,000 ‘routes’, instead of on genuinely avoidable costs relating to individual services.

The attitudes of top managers in New Zealand Post and Sweden Post seem to be the key to their success in liberalised markets.

Bror Anders Månsson, Chairman, Citymail 9

2 COMPETING IN SWEDEN Editorial note∗Presentation by Bror Anders Månsson Ian Senior’s presentation on international experience was followed by Bror Anders Månsson from Sweden’s Citymail. As a ‘new entrant’ to the postal service, his perspective was clear, quoting from The Economist as follows:

“The predictable result of maintaining the monopolies is that state-owned postal and telecom services are a byword for inefficiency. Where competition has been introduced it has lowered the costs for almost everyone, while improving service”.

The Economist, January 7th 1995 He noted the overlapping time-scale for deregulation in telecommunications and mail distribution (1984-1996 and the early 1990s-2005 respectively). He also noted the ‘new information’ products (fax, internet, intranet and e-mail) and new business services (computer mail and couriers). New market definitions were also required, given domestic computer addressed mail (which change the logistics) and international computer addressed mail (with its cross-border issues). The historical milestones for the global postal market were set out as follows:

∗ This editorial note by Peter Vass has been prepared incorporating the relevant PowerPoint slides presented by Bror Anders Månsson

COMPETING IN SWEDEN

10

1910 Radiotelegraphy 1925 Telephone 1945 Telex 1955 EDP 1970 Cellular phones 1979 Telefax 1982 PC 1987 E-mail 1994 Internet

The business and operational characteristics of the computer mail segment (magazines, mail-order catalogues, statements of accounts, invoices etc) were set out as follows: • addresses stored in databases creates the opportunity to sort mail

when it is printed (pre-sorting); • production of mail takes place in large facilities. Production is

planned! Distribution is set to a certain time instead of overnight delivery;

as were the pre-requisites for efficient mail distribution: • capitalise on senders existing investments; • logical zipcode system which makes computer-sorting possible; • high quality of addresses. Looking ahead, key factors to take into account with respect to market growth were: • internet communication is about to change market structure; • market growth in computer addressed mail segment (5-7%); • e-mail is taking over person-to-person communication, reducing

the market segment office mail. Key customers would be those with large databases, including telecom, cable television and internet utilties, financial services and retailing. It was his view that the internet clarifies Citymail’s market

BROR ANDERS MÅNSSON

11

segment and exposes Sweden Post’s highest priced segment to competition. Key statistics for defining the postal market relate to how ‘mail enters the system’ and ‘means of delivery’. The breakdown for the former is mailbox (5%), office mail (40%) and computer addressed mail (55%). Figure 1 shows how those proportions are broken down by means of delivery:

Figure 1: Means of delivery

0

10

20

30

40

50

60

70

80

90

100

Computer addressed mail 55%

%

Office Mail 40%

Mailbox 5%

P. O. boxes

Mailman

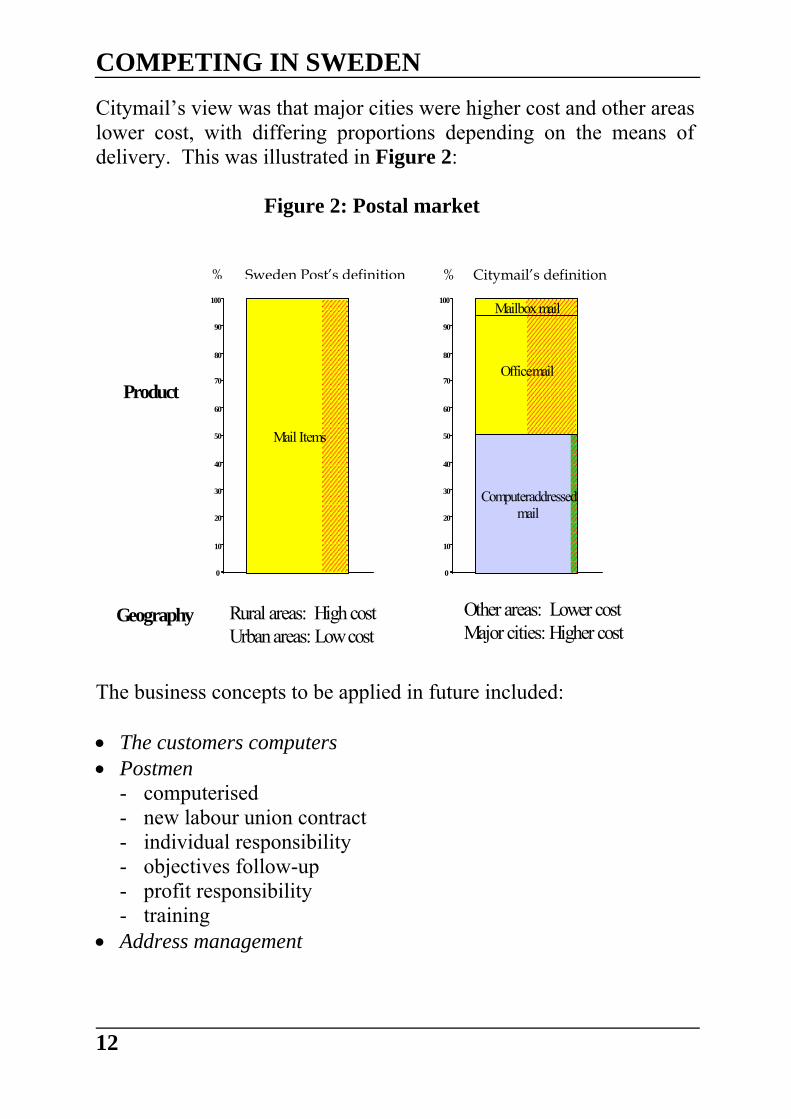

Citymail’s view of which geographical areas were higher or lower cost also differed from the traditional perspective (the ‘two myths of the postal world’), which states that long distance means high cost and that rural areas are high cost and urban areas low cost. This applies equally to all the means of delivery set out in Figure 1. Postal monopolies have always used the same arguments to prevent a deregulated postal market:

“Universal services in rural areas cannot be maintained if the monopolist can’t set high prices in other parts”.

COMPETING IN SWEDEN

12

Citymail’s view was that major cities were higher cost and other areas lower cost, with differing proportions depending on the means of delivery. This was illustrated in Figure 2:

Figure 2: Postal market

% Sweden Post’s definition % Citymail’s definition

0

10

20

30

40

50

60

70

80

90

100

Officemail

Mailbox mail

0

10

20

30

40

50

60

70

80

90

100

Geography

Product

Mail Items

Computeraddressedmail

Rural areas: High costUrban areas: Low cost

Other areas: Lower costMajor cities: Higher cost

The business concepts to be applied in future included: • The customers computers • Postmen

- computerised - new labour union contract - individual responsibility - objectives follow-up - profit responsibility - training

• Address management

BROR ANDERS MÅNSSON

13

The competitors’ problems, not surprisingly, related to issues of critical mass (geographical coverage), legal issues (monopoly, infrastructure access and selective geographical pricing) and credibility (financial strength). Developments were taking place, however, including the definition of the postal infrastructure, covering issues such as: • address-changes • redirection of mail • access to PO boxes • postal code system and new legislation in Sweden, covering: • jointly owned company for handling address changes; • cost-based access to PO boxes on equal terms; • specific postal code series for PO boxes to new postal

operators; • strengthened role for regulatory authority. Key dates for these developments were as follows:

1992 The Swedish Competition Authority established (1.7.92) 1993 The postal monopoly abolished (1.1.93)

The new Competition Act (1.7.93) 1994 The new Postal Act (1.3.94)

PTS (surveillance authority) established (1.3.94) 1997 A new Postal Act (1.1.97) 1998 A new Postal Act (1.7.98) 1999 A new Postal Act (1.7.99)

The competition law has sought to deal with issues of predatory pricing, and there has been a focus on ‘cream-skimming’ clauses, price adjustment clauses and prices in Stockholm (zones). Prices have fallen for computer addressed mail from SEK4.80 in 1991 to SEK2.75 in 2000 for computer addressed mail, but for office

COMPETING IN SWEDEN

14

mail the prices have risen from SEK5.00 to SEK8.00 over the same period. Sweden’s Post’s profit trends have been as shown in Figure 3.

Figure 3: Sweden Post profit trends

1200

1000

800

600

400

200

0

96/12 97/12 98/1297/06 98/06 99/06

MSEK

99/09-320

01/06

* Sweden Post excluding the postal giro

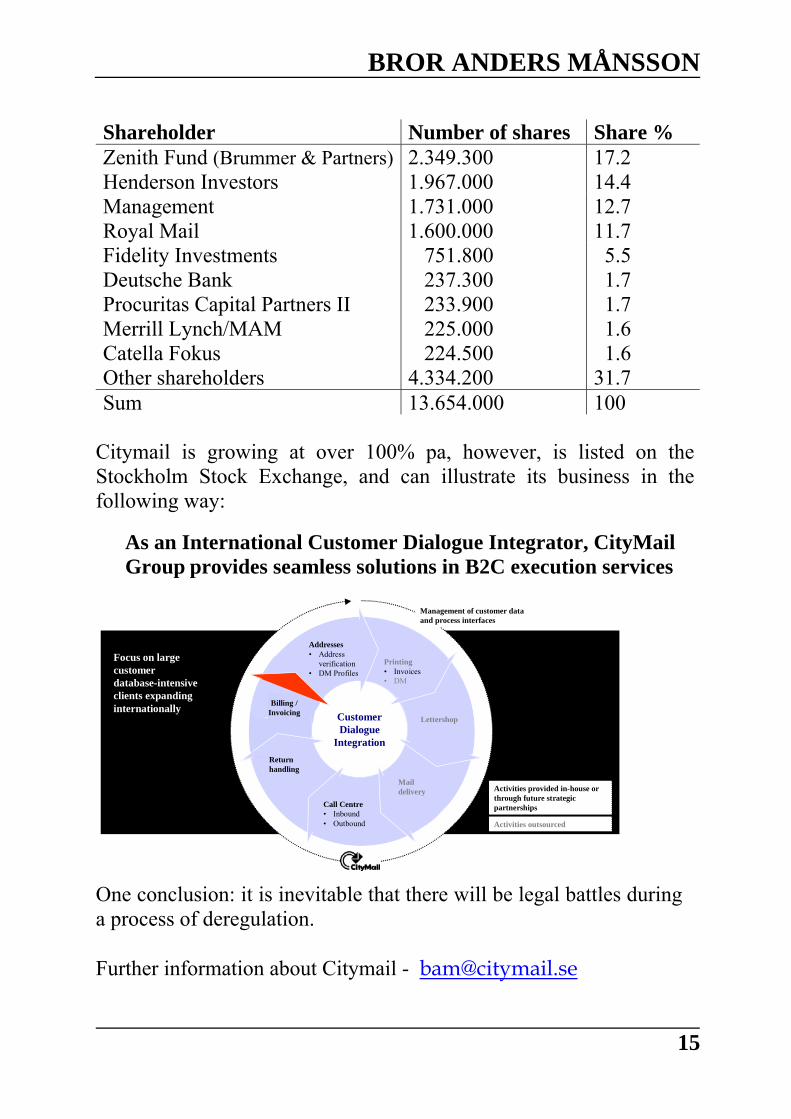

The cost of universal service for rural areas has also been judged to have come down dramatically. In the period 1991-1996 it was estimated to be 1300m SEK (Ulf Dahlsten) and in June 1997, by the Ministry of Communication (Őhrlings Coopers and Lybrand), less than 400m SEK, and, later in 1997 with respect to a proposal regarding the new Postal Act, less than 100m SEK. Sweden Post is still dominant, as shown by mail volumes in 2000: Sweden Post had 3263m items (95%), Citymail 150m items (4.4%) and others 14m items; all out of a total market of 3427m items. Citymail Group owns Citymail International and has joint ventures and projects (Citymail Sweden AB and Citymail Interactive). Its ownership structure is as follows:

BROR ANDERS MÅNSSON

15

Shareholder Number of shares Share % Zenith Fund (Brummer & Partners) 2.349.300 17.2 Henderson Investors 1.967.000 14.4 Management 1.731.000 12.7 Royal Mail 1.600.000 11.7 Fidelity Investments 751.800 5.5 Deutsche Bank 237.300 1.7 Procuritas Capital Partners II 233.900 1.7 Merrill Lynch/MAM 225.000 1.6 Catella Fokus 224.500 1.6 Other shareholders 4.334.200 31.7 Sum 13.654.000 100

Citymail is growing at over 100% pa, however, is listed on the Stockholm Stock Exchange, and can illustrate its business in the following way:

As an International Customer Dialogue Integrator, CityMailGroup provides seamless solutions in B2C execution services

Focus on largecustomerdatabase-intensiveclients expandinginternationally

Addresses• Address

verification• DM Profiles

Billing /Invoicing

One conclusion: it is inevitable that there will be legal battles during a process of deregulation. Further information about Citymail - [email protected]

3 CONSUMERS COME FIRST Gregor McGregor Introduction This chapter deliberately has the title ‘consumers come first’ because it is all too easy to be distracted by structures, pricing and the effects of competition and monopolies, and to forget that the fundamental objective of a service provider is to satisfy the needs of its customers. Competition vs regulated monopoly There are two basic choices facing the postal regulator: follow the route of competition or that of a regulated monopoly. On the one hand you can have a benign monopoly which is well regulated, achieving savings through scale and scope, delivering the universal service, and which is trusted and liked by customers. This would be a win, win, win situation. But the drawback of this model is that it is not stable. If we look at any state monopoly privatised over the last 20 years we see that management has come first, shareholders second and customers firmly in third place. Monopolies will inevitably seek to exploit their position, and the longer they maintain this position the worse the situation becomes. They deliver the wrong products, which do not meet customer needs, are over-priced and show no innovation. Monopolies will inevitably grow stronger than the regulator, who is captured so as to serve the monopoly’s interests rather than customer need. It is therefore essential to have competition to prevent both the regulator and the monopoly from becoming stale. Competition

CONSUMERS COME FIRST

18

equates to choice; so in order that customers’ needs are met, a mechanism must exist for competitors to enter the market to offer products and services denied them by the monopoly supplier. The process of ensuring that a choice is available will therefore ensure that the customer comes first. Universal postal service It is remarkable that it is only where a monopoly exists that an obligation to supply is imposed. There is, for example, no requirement for bread or newspapers to be delivered to the Outer Hebrides – but they still succeed in getting there. I would therefore suggest that the obligation to supply is an invention of the monopoly supplier in order to justify preserving its monopoly. Much work has been undertaken in the telecoms sector to calculate the cost of the universal postal service (USO), and we also commend the work which Postcomm itself has undertaken in this field. However, when looked at independently there is little evidence of the USO being a cost. And even if this should prove to be the case, the cost looks remarkably small. Indeed, it is our view that there are significant commercial opportunities available to the provider of a service which reaches everywhere, every day. Postwatch has therefore recently commissioned its own research into the opportunities available to a universal service provider with a view to demonstrating that this is in fact a net benefit rather than a burden. It is hoped that the results of this study will be available to inform Postcomm’s thinking on opening the postal market to competition, but unfortunately we are encountering some difficulties owing to Consignia’s reluctance to provide us with the necessary data.

GREGOR McGREGOR

19

Licensed and reserved areas The approach to introducing competition is confused by the complicated legal structure surrounding provision of postal services in the UK. However, this can be modelled as shown in Figure 1.

Here the outer ring represents the universal postal service (UPS), obligation of daily collection and delivery of items up to 20kg in weight at a uniform and affordable tariff. In the UK regime we then have the ‘licensed area’, shown as a middle ring representing items weighing less than 350g and costing less than £1 to handle. These familiar limits arise from the original European Directive. Outside this area, of course, significant competition already exists in the parcels market where some 4,000 operators are already in business offering good, competitive services. And finally there is the ‘reserved area’. This is a concept embedded in the Directive and it consists of a small core of services which is strictly necessary to subsidise the UPS. It is the existence of this reserved area which is at the heart of debate over the appropriate licensing regime. Although reducing this area

CONSUMERS COME FIRST

20

would act as a strong signal to the market that would be reflected in the licensing regime, the question remains as to whether there is a need to reserve any services in order to maintain a cross-subsidy, if provision of the UPS is indeed fully commercial (ie, not a financial burden). Indeed, it may be argued that in such circumstances it is therefore actually unlawful to license such activities. Opening competition Since Postwatch does not believe that the USO is a cost – but rather a benefit – the question arises as to how the market should be opened-up to competition. We believe that a temporary licensing regime is potentially extremely damaging because of the lack of certainty it creates and the disincentive to investment on the part of aspiring competitors. Indeed, more than that we believe that Postcomm’s licensing policy is actually back-to-front in that it would be more logical for competitors to enjoy licences lasting 15 years whilst the monopoly incumbent should be issued with a licence for a restricted period. Postwatch would also warn against making use of a regulatory blueprint of how the market is expected to develop. It is wrong for regulators divorced from market or commercial reality to construct regulatory policies designed to deliver particular theoretical outcomes. This is because it is not only impossible, but also counter-productive, to attempt to second-guess the market. The whole point of competition is to allow customers rather than the regulator (however well intentioned) to drive the process. There are three key strategies which can be used to open the market to competition. The first is that Postcomm should use its powers to encourage new entrants. It is simply not true that such competitors will immediately have a devastating effect on the position of the monopoly supplier. All previous experience has shown that any erosion of the incumbent’s market will be slow and gradual.

GREGOR McGREGOR

21

The second strategy is for Postcomm to make it clear to the market that there is no restriction on the consolidation of inland mail, and that the regulator sees this activity as being positively pro-competitive. The third strategy (an extension of the second) is to ensure that any competitor may make use of the postal network on exactly the same terms as the incumbent monopoly operator (Consignia). History has shown that in other industries the creation of workable access codes to allow this to happen has taken two to three years; but this must not deter those responsible from undertaking the task – which must be regarded as a very high priority. Where next? So, in conclusion, Postwatch believes that Consignia is showing all the signs of a typical 350 year old monopoly – alarmed, or even frightened by, the competition, and paranoid about protecting its monopoly. But competition should be seen as an opportunity not a threat, and we would urge Consignia’s management to approach it as such. The fact is that Consignia is not performing successfully as a company: its management, industrial relations and financial management are in a mess and it needs the spur of competition to turn it around. For the regulator’s part, Postcomm cannot ride the twin horses of defending a monopoly whilst at the same time introducing effective competition. And it is clear to us that the latter course of action is the only viable solution. The market needs a clear steer from Postcomm whose licensing regime must provide certainty for investment and business growth. It also needs a big step reduction in the licensed area threshold – this important message has already been addressed in Luxembourg earlier in the week. And, finally, a firm end date must be set for the complete liberalisation of the European postal market. Postwatch would advocate 2006, but unfortunately it appears that the powerful

CONSUMERS COME FIRST

22

monopolies will succeed in stringing this out. It is regrettable that the UK government saw fit to sit on this particular fence when they had an ideal opportunity to influence the debate – otherwise we might have seen greater and more rapid progress, which would undoubtedly have been to the benefit of consumers.

John Ivers, Chairman, Mail Users’ Association 23

4 BUSINESS MAILERS’ VIEWS

John Ivers Introduction This chapter gives you a brief outline of the Mail Users’ Association (MUA) and its stated aims and objectives, before looking in more detail at what business mailers want from the liberalisation process, and how they envisage the development of sustainable competition can be achieved. MUA was formed in the 1970s and is the UK’s only independent association of business users concerned wholly with commercially related postal matters. The organisation has been inputting to postal discussion for over thirty years and its membership is now drawn from a wide range of business interests including: • direct mail, banking and finance; • communications and utilities; • magazine publishing and postal related industries, such as

equipment manufacturers and mail consolidators . As a representative organisation, MUA’s primary objective is to secure a healthy and cost-effective set of postal services for all business users and their customers. This, MUA members believe, can be achieved in a thriving, competitive and customer responsive market, where users have a real choice of services tailored to their needs, and that means services which are well defined, predictable, reliable, and competitively priced. The postal operators who supply these services in our view therefore need to be:

BUSINESS MAILERS’ VIEWS

24

• flexible in their approach to customers, whose needs are continually changing;

• able to provide reliable, high quality services on a continuing

basis; • be customer focused in their approach to the products and services

they offer. You will not be surprised to hear, therefore, that the MUA fully supports Postcomm’s drive to promote effective competition in the marketplace, believing that the development of ‘sustainable’ alternatives will complement, and indeed enhance, the existing products and services supplied by Consignia, whilst at the same time offering realistic choices to businesses wishing to use this medium to reach their customers. You will note I emphasise the word ‘sustainable’ and I do so with good reason because I believe sustainability is synonymous with the promotion of effective competition. MUA members in the magazine sector of the market have first hand experience of developing alternative final delivery networks, when postal operators have had ‘insufficient’ volumes of mail at their disposal for them to sustain and grow their mailing operations. A key message coming from the business mail community, therefore, is that whatever liberalisation measures Postcomm decides to put in place, it is essential potential market entrants are allowed access to sufficient tranches of the market in order to sustain their operations whilst at the same time maintaining the high standards expected by business mailers. Business users’ requirements MUA has recently carried out research amongst its membership to ascertain the future needs and requirements of the industry. This

JOHN IVERS

25

research points to the fact that the business mailing community think mail will remain an important method of communication for many years to come, but that the first and second class services presently available are not good enough for all of their needs. There is a strong opinion amongst members that ‘predictability’ in the mailing services on offer is a key issue, as is the importance of better communication surrounding the services offered by postal operators. Mailers wish to have proactive notification of items not arriving at the agreed time, they would wish to be able to find out the status of mailed items on an ad-hoc basis, and be informed when items have arrived at their destination. In essence, business mailers want to play a more active role in the process of getting their messages to the final customer. All of the evidence MUA has collected from membership points to the fact that business customers are no longer happy with simply handing over their mail to a monopoly supplier, in the hope that it will arrive on time. Business mailers want to develop real partnerships with suppliers who can be relied upon to carry out this essential process and be fully informed of contingency arrangements, as and when they need to be implemented. So, returning to the million dollar question …. what does the industry want out of the liberalisation process? Business mailers consider it is essential that Postcomm develops a licensing regime which is transparent, not overly complicated, and designed to actively encourage market entrants. Ambiguity and uncertainty in so far as what competitors can and can’t do (and indeed for how long they will be permitted do it) will act as a brake on market development. MUA members also believe Postcomm must take a very proactive role in ensuring that Consignia is not allowed to abuse its dominant position through intimidatory behaviour or strategies that are deemed

BUSINESS MAILERS’ VIEWS

26

to be anti-competitive. This will require the regulator to devise a strong regulatory framework to control Consignia’s monopoly position. In order to create a level playing field on which to develop sustainable competition it is essential that Postcomm becomes fully involved in the development of a transparent, non-discriminatory ‘access code’, through which competitors can gain fair and level access to Consignia’s pipeline, and that Postcomm unequivocally confirms the legalities surrounding the consolidation of domestic mail. Business mailers believe it is essential that Consignia is in no way allowed to discriminate against alternative upstream providers, either in contractual terms, or through the tariffs Consignia offers competitors. Finally, but of equal importance, is the role that Postcomm, and indeed Postwatch, has to play in protecting consumer interests in terms of maintaining the integrity of mail operators, and the standards of service they offer, and it is this that business mailers believe should be a primary focus of the licensing regime. Promoting effective competition Turning to the question of how best to promote effective competition in the UK, the MUA believes that the best approach to achieving successful liberalisation is through the adoption of a spread of measures or approaches which could be adopted simultaneously. This raft of measures might include: • the issue of regional franchises for final delivery (particularly in

poor performance areas); • a stepped reduction in the weight and/or price thresholds of the

reserved area over a set period of time;

JOHN IVERS

27

• a stepped reduction in monopoly weight/price restrictions for specific product types (ie, direct mail) over a set period of time;

• the issue of licences for operators to compete with Consignia’s

upstream activities; • the licensing of operators with innovative products to compete

directly with the national carrier ( either regionally or nationally). By developing the market using a mixture of controllable options MUA members believe that Postcomm will be better able to protect the interests of the universal service. If, for unforeseen reasons, one liberalisation measure is found to be seriously impacting on the universal service, the speed of its liberalisation or introduction can be slowed, or adjusted, to safeguard the interests of the UK’s overall postal service. This balanced approach is seen by MUA members as being preferable to other forms of liberalisation by single category, as it will minimise the likelihood of Postcomm having to make major U-turns in liberalisation policy as a result of unforeseen changes in market circumstances. Conclusion So, in summary, the business mailing community supports postal liberalisation at the earliest possible juncture, believing it to be essential to the continued success of mail as a business communication medium. After all, we should not forget that the mail medium is no longer the only realistic option for businesses. Advances in technology are enhancing the attractiveness of alternative communication mediums, and many observers would argue that the real threat to UK postal services is not from competition, but rather from electronic

BUSINESS MAILERS’ VIEWS

28

substitution, particularly in an environment where postal quality of service is so low. In the light of this, it is essential that Postcomm, having identified the benefits competition would bring to the market, takes decisive action to open the market to full competition as soon as practicable. In terms of the messages that will act as forerunners within Europe, MUA members believe that Postcomm should support the setting of an early date for full liberalisation, with the development of a clear and rapid timetable towards it. A clear signal should also be sent to the UK postal industry through the announcement of a timetable for the stepped reduction of national monopoly thresholds. This will not only act as an assurance to the industry that the mail medium is now entering a regenerative phase, but it will also prepare UK consumers for a new, more dynamic market, and serve as a driver for change in rectifying Consignia’s present industrial relations problems. However, above all else, MUA cannot stress strongly enough the importance of Postcomm stating their intended direction at the earliest possible juncture in order to protect mail as a preferred business communication medium for the future. A lack of clear decision making in this area will allow the postal service to continue to ‘wither on the vine’, pushing customers away from its services and adversely affecting the UK economy.

MN20026 YEAR 2005/2006 SEMESTER 1 ECONOMIC ANALYSIS OF FINANCIAL DECISIONS Course lecturer: Peter Vass, School of Management The course will be assessed 100% by examination (3 questions from 5 or 6). The course does not lecture the contents of a particular textbook, and the examination will be based on the lectures and class work. The following textbooks include many relevant chapters which cover, perhaps in the same, and perhaps in a different, way the lectured and class material. They have been chosen as they are ‘mainstream’ or ‘core’ texts, but there are many other equally useful textbooks to be drawn from the accounting and finance literature. The key material from lectures will be distributed during the course, making a compendium at the end. The normal format each week is one lecture and one class (discussing and working through a pre-prepared exercise), giving a balance of knowledge and skills acquisition. MANAGEMENT AND COST ACCOUNTING, Drury, Thomson Learning, 4th, 5th or later edition; ACCOUNTING FOR MANAGERS, Glynn, Murphy, Perrin and Abraham, Thomson, 3rd edition; ECONOMICS, Begg, Fischer and Dornbusch, McGraw Hill, 5th or later edition; PRINCIPLES OF CORPORATE FINANCE, Brealey and Myers, McGraw Hill, 6th or later edition Reconciling NPV and IRRs (standard and modified) for Investment Decisions -The ‘normal’ investment series, multiple returns and the ‘true’ IRR; -Capital rationing and the extended yield, ‘average’ (terminal value) IRR; -Mutually exclusive projects and the incremental IRR; -Combining capital rationing and mutually exclusive projects: the ‘unique’ ranking list and incremental project returns (equivalence of accounting and IRR returns); -Typical problems and approaches: indivisibility, the standardised IRR, standardising the investment period by annuity, deferring mutually exclusive projects with capital rationing, misusing the discount rate to account for risk (the ‘hurdle’ rate of return). Integrating ‘accounted’ profit with ‘economic’ profit -The three costs of business and consistency with cash flows and NPV calculations Optimisation and Valuation with Multiple Constraints -Maximising contribution and minimising input costs with constraints; -‘Internal’ opportunity costs and marginal costs (or shadow prices) of constraints: the ‘dual’ solutions and their marginal interpretation. Optimal Decisions where Sales vary with Price -Estimating marginal revenue from demand data; -Optimising with incremental opportunity costs; -Linear demand curves - average and marginal revenue rules. Fixed Costs and Optimal Cost Allocations to Products -Traditional cost allocation methods (physical yield and net realisable value); -Joint costs and decentralised decision-making; allocations proportional to marginal revenue at optimal output; identifying by-products; Sectoral application: regulatory policy and method for essential service industries (such as water, energy, transport and communications) (see also COMPETITION IN REGULATED INDUSTRIES, edited by Helm and Jenkinson, OUP, 1998, for Ramsey Pricing etc) -Long run versus short run marginal cost with ‘lumpy’ investments; two-part tariffs; -Minimising loss of consumer welfare - Ramsey pricing for allocating fixed costs in regulated water, energy, transport and communications industries, and the tax burden; -Non-discrimination; stand-alone cost and incremental cost - its use in access pricing for natural monopoly infrastructure and networks.

Jos Geeraerts, Strategy Consultant, TPG 33

6 MARKET STRATEGIES FOR NEW ENTRANTS Jos Geeraerts Introduction In this chapter, TPG sets out its views on the development of the mail industry in the near future, and the consequences for its entry strategy towards new markets. TPG will demonstrate that mail is changing as a result of broader changes in the way people communicate, and that the innovative power of the mail industry is a vital requirement if it is to survive. We will indicate TPG's approach towards these developments, both in its home market in the Netherlands and elsewhere. Physical mail Physical mail is part of a highly competitive communications market. Traditionally, sending physical mail is a key way of communication. There are many other communication media, such as telephone, fax, television, radio and e-mail. Each is a potential threat to the postal industry, to varying degrees. In these times of increasing use of electronic media, this becomes more and more apparent. We estimate that alternative media are currently substituting for mail at a rate of 2% per annum, but expect the rate to increase dramatically. Once the ‘high tech’ image and related capital expense of having access to e-mail are gone (e-mail via television sets is predicted to ‘explode’ and e-mail communications are expected to increase substantially), there will be little to dissuade banks, insurance companies, direct marketers and other heavy users of postal services

MARKET STRATEGIES FOR NEW ENTRANTS

34

to use e-mail for communication.1 The predicted erosion of letter mail has taken longer than expected but its eventual decline could be much faster than predicted. In short, the use of physical mail as a communication medium is increasingly challenged by the use of other media and it is uncertain whether postal volumes will continue to grow in this dynamic market. Moreover it is certain that physical mail as a percentage of total messages sent will decrease dramatically in the coming ten years, as shown in Figure 1. It is important to realise that competition between media that convey messages is not the only relevant issue, but also the fact that the content of a message has to fit in a communications approach. A good example is the advertising market.

Direct mail, as part of the total advertising market, is an outstanding example of physical mail competing with other communication channels. How the UK market for advertising spending can be segmented is illustrated in Table 1.

1 Source: IDC. E-mail messages per day numbered 2.1 billion in 1998. This number is predicted to increase to 7.9 billion by 2002.

JOS GEERAERTS

35

Table 1: Segmentation and UK market size in 1999 Advertising spending

Direct Marketing Direct (Non-) Mail

Total advertising: £16.2bn

Total Direct Marketing: £5.3bn

Total Direct Mail: £2.5bn

Press Display: £5.2bn

Direct Mail: £1.9bn

Production Direct Mail: £1.0bn

Television: £4.3bn

Direct non-Mail: £0.6bn

Distribution Direct Mail: £0.9bn

Direct Marketing: £5.3bn

Teleservice: £2.7bn

Production Direct Non Mail: £0.4bn

Other: £1.3bn

On-line: £0.1bn

Distribution Direct Non Mail: £0.2bn

Source: DMA, Circular Distributors ltd, team analysis Direct mail is a relatively small part of the total advertising market, and the majority of the costs are incurred by the production of the mailings. In the UK, spending for distributing physically addressed direct mail accounts for only 6% of the total spending within the advertising market – so it is obvious that competition in this market is severe. The need to innovate The Direct Marketing Association (DMA) bluntly confirms this market reality, namely, that failure to introduce choice in the direct mail market will lead to users choosing alternative media:

MARKET STRATEGIES FOR NEW ENTRANTS

36

“Users are accustomed to and expect choice, postal services should not be [an] exception, users should have the opportunity to choose depending on their requirements. The downside for postal operators is if these needs are not met, users will turn to other direct marketing media, such as telemarketing and e-mail, to fulfil their advertising objectives. This, in essence, is the weakness of a monopoly market, where the weakest part of the mail chain could influence marketers’ decision to use other media”. 2

As can be concluded from this DMA statement, the weakness of postal operators is that we do not meet the changing demands of the market. In brief, DMA fears that incumbent postal operators do not have the capacity to innovate. To survive, businesses need to innovate. In the face of competition of immense and unprecedented strength, the postal services industry needs to evolve very rapidly to persuade heavy users to continue to use postal services. This is the key to survival because a universal postal service, at an affordable price, depends upon sufficient volumes to keep the unit cost of delivery down. Only 14% of mail is generated by households, and even less is paid by households.3 A delivery network based on such volumes alone would lead to either an enormous increase in postal tariffs or a need for governmental aid. The only way for postal services to innovate, and survive (without government subsidy), is to introduce new, value-added, efficient services which meet customers’ needs. If postal administrations and trade unions are allowed, ostrich-like, to focus on the preservation of revenues produced by their monopolies and of existing employment levels, they will risk putting the industry and all its employees in jeopardy. 2 DMA evidence to the House of Lords Select Committee, 15 September 2000. 3 UPU (1997), Post 2005, p.5. However, of this 14%, a large proportion of the postage cost is paid by businesses.

JOS GEERAERTS

37

Without liberalisation, competition within the physical mail market does not exist. Without competition, the incentive to innovate, improve and become efficient is purely theoretical. Without choice, customers who need better services than those being supplied can only migrate to other media. With limited budgets (as they all have), customers will move if they do not get the service they require for the acceptable price. TPG view on innovation TPG is taking this challenge to innovate extremely seriously. We have recognised our position not merely as a mail distributor, but as a party that facilitates communication for our customers. We consider physical mail as just one link in the communication chain of our customers, as illustrated in Figure 2.

Figure 2: Mail in the Communication Chain

Data ConversionPrintTelephoneElectronic

Mail Response Conversion

Collection Sorting DeliveryTransport

Data

TPG pursues two strategies that arise from looking at Figure 2. First, one can aim to improve on the mail side, which is the traditional core competence of incumbent postal operators. The second strategy helps customers to optimise their total communication chain. On the mail side, the approach we take is to broaden the traditional physical mailing process, and develop products that include also hybrid and electronic channels. Tests are currently going on in the Netherlands with such a product, and we are convinced that this will not be our last along those lines, as the following example illustrates:

MARKET STRATEGIES FOR NEW ENTRANTS

38

Privver - an example of innovation of mail

The development of internet presents Royal PTT Post with a new opportunity, another opportunity to provide a message-service that senders and receivers trust us to deliver. This opportunity is an electronic message service we will brand eDelivery. eDelivery is a personal mail box on the web, where consumers and businesses alike, any time anywhere receive and interact with their mail. These mails can be invoices, statements & overviews, direct mail offerings based on the consumer preferences, insurance documents, product guaranties, national lottery tickets, vouchers for special discounts, in short any type of mail one typically also receives in the letter box. All these features are an extension of the existing Royal PTT Post proposition and thus provides a natural fit. It is our strong believe that this proposition strengthens Royal PTT Post position as a trusted third party.

The second strategy that Royal PTT Post takes is to help customers to improve their total communication chain. TPG aims to optimise the total business-to-consumer and business-to-business communication process for clients. This means a broadening of the traditional approach of a service provider for physical distribution solely. For businesses the mailing process is just one step in a total communication chain. This process starts with the collection and selection of data and the conversion of the data through printing, telephone or electronic media, continues with the distribution and is followed by a response process which eventually results in data storage for future action. Therefore, a customer’s decision on the use of physical mail depends on the effectiveness and efficiency of this medium in the total communication chain. Strangely enough, all steps in this chain are carried out in a fully competitive environment, except for the physical mail distribution.

JOS GEERAERTS

39

TPG identifies the direct mail market as a good example of the value which alternative providers can create by optimising the communication chain of customers and tailoring the distribution system to the needs of the direct marketing industry. TPG’s entry in the UK mail market Essential for introducing real innovation is the creation of real alternatives to the incumbent. TPG offers an alternative by setting up its own networks. The TPG presence in UK is predominantly through TNT, but also through other brands that don’t carry the names TNT or Royal PTT Post. TNT Express mail services Recently TNT has acquired licences on special services in the financial services industry. These licences were necessary to protect already existing activities due to the re-monopolisation of special services under the Postal Services Act of 2000. TPG has always argued that, under the EC-directive and the EC competition rules, TNT and all other suppliers of special mail services should be exempt from needing to apply for these licences. TNT Logistics TNT logistics of course play an excellent role in the logistics of newspapers and periodicals. Newspapers and periodical distribution are not part of the reserved area. Circular Distributors Further, TPG has acquired this year Circular Distributors and Lason UK. Circular Distributors (CD) is a leading distributor of leaflets, newspapers and samples in the UK. CD’s distribution network covers 15% of UK households weekly by round-based distribution and 90%

MARKET STRATEGIES FOR NEW ENTRANTS

40

of UK households on a monthly basis through team distribution. CD is also a publisher of targeted marketing periodicals and collects and markets data and lifestyle information. Lason UK Lason UK is a major player in the data chain, especially in the provision of printing solutions. Lason is a leading company in document and data management services, a supplier of data-capture services, a supplier of data management and data manipulation services and a distributor of hybrid mail (print and mail and EDI services) Postal Preference Services Through its Postal Preference Service, a joint venture with Royal Mail, TPG builds up a database for customer preferences, which will enable the direct marketing industry to increase their cost-effectiveness. The Postal Preference Service is a consumer-fair™ service enabling consumers to take control of what information and offers they receive, thereby offering advertisers selected target groups of potential customers. It is the largest data collection programme in the UK. TNT International Mail This business has been providing cross-border business mail services to customers in the UK for over 14 years and now forms part of the global cross-border mail joint venture involving TPG (51%), Consignia plc (24.5%) and Singapore Post Private Limited (24.5%). TPG aims to develop business to consumer distribution networks in UK as part of a total solution for its customers, provided the conditions are right and enough mail is available to distribute under a licence.

JOS GEERAERTS

41

TPG prefers to co-operate in this with partners, either on the operational or on the commercial side. Conditions for developing activities TPG can only develop these activities if market conditions allow for it. The basic regulatory requirements that stimulate market entry are: • availability of a substantial market; • no predatory pricing by the incumbent; • legal certainty concerning re-monopolisation and the length of

licences (15 years) necessary to allow investments. Under these conditions, provided of course that there is sufficient market demand for new services, building new networks can be successful. Currently, in the UK, the available market is not substantial enough to make an entry in the UK mail distribution market. The available market consists of periodicals, un-addressed mail and correspondence weighing over 350 gram. It represents less than 10% of the entire letter mail market, and is very fragmented over customers. Liberalising specific parts of the market in the short term and growing towards full liberalisation in the mid-term is required to stimulate genuine competition and to drive efficiencies within Consignia plc. Liberalising specific parts of the market by reducing the weight/price limits is not the best way to introduce effective competition, since it makes it difficult for customers and new entrants to find each other. Few customers will look for an alternative distributor if they can offer only a limited part of their volume, the share that exceeds the weight limit, to this partner. The potential savings generally do not compare to the burden of having two suppliers. The same argument also applies to regional liberalisation.

MARKET STRATEGIES FOR NEW ENTRANTS

42

Direct mail, on the contrary, is a separate, readily identifiable mail flow emanating only from business customers. As such, it offers competitors to Consignia plc access to a market which has substantial volumes and which can be identified. Moreover, direct mail is a fast-growing, profitable segment and is a relatively immature market when compared with, for example, the USA, where direct mail volumes per capita are double the European average. Even taking account of the expansive definition of direct mail in the USA, the evidence is the European market has considerable growth potential. Introduction of competition in this segment would help making this potential come to life. Discussion is going on in many European countries on whether access to the existing logistical infrastructure of the incumbent is necessary in order to promote competition. TPG is convinced that this is not necessary. On the contrary, use of the network of the incumbent would imply that for a major part of the service, a new entrant relies on the quality of the incumbent, whereas innovation and real competition requires a completely new look at mail. We bring this belief into practice by setting up our own networks, that fit exactly the requirements of the service that we want to offer. Other Posts, like Consignia itself, have a similar approach. This can be illustrated by Consignia's stake in City Mail, a leading alternative distribution network in Sweden. Also, the following advertisement for a mail deliverer in the Netherlands illustrates this:

For the delivery of English mail in Amsterdam, we are looking for Mail Deliverers (male / female) You must have a drivers licence and know your way around the town very well. Further you must feel responsible for your work, and have no objection to waking up early. It concerns a full time job, working hours are 6 am to 3 pm. Interested? Please contact…

JOS GEERAERTS

43

Activities of TPG elsewhere in Europe TPG’s strategy does not only extend to the UK but to the whole of Europe. TPG aims to build business-to-consumer networks where possible, and has a presence, besides the UK, in Germany, Austria, Belgium, Italy and the Czech Republic. An example of a market entry could be found in TPG’s activities in Germany, illustrated by the following, an extract from a press release of 4 October 2001:

TPG and Hermes form alliance in German mail market

The joint venture will operate under the name EP Europost. “TPG N.V., through its subsidiary Royal PTT Post, and the Otto Group, through its subsidiary Hermes Versand Service, today signed an agreement to establish a joint venture for the delivery of addressed mail in Germany. In line with TPG’s international mail expansion strategy, the Mail division is building positions in the domestic European markets for unaddressed items, addressed mail and value added services, enabling it to offer customers a full range of physical and electronic distribution solutions. EP Europost focuses on the distribution of mass addressed mail. In close consultation with important pilot customers and their distribution partners, EP Europost has extensively tested the operational and IT structures in Germany, distributing items in an area covering approximately 9 million German households. EP Europost aims to service all 36 million addresses in Germany within the next few years. The JV will offer addressed distribution services throughout Germany at a competitive price/quality ratio to customers in the business-to-consumer and business-to-business market.

MARKET STRATEGIES FOR NEW ENTRANTS

44

The service offering will cover the entire process chain from collection, sorting, logistics and transport to delivery, returns, address services and complaints handling. The target group for EP Europost includes mail-order companies, publishers, direct mailers, government institutions, financial service providers and mailing houses. The products distributed include catalogues, direct mailings, weekly & monthly magazines, shopping magazines and the distribution of letters under various licenses”.

Preserving the universal service In the above, TPG has set out the grounds on which it is convinced that liberalising the postal market is the way to introduce effective competition. It is apparent that there is concern about the maintenance of the universal service if the market is liberalised. However, TPG is convinced that this concern is not justified: it strongly believes that it is possible to maintain a universal service in a liberalised market. The purpose of the universal service is to safeguard the ability of the general public to communicate regularly at a reasonable cost. The concept of universal service needs to be flexible and dynamic – to take account of the rapidly changing ways in which we communicate. Why should it not, for example, permit communication to be by any means (eg, provide email connection to remote areas) or allow delivery to local collection points rather than addresses – everyone needs to buy food yet there is no universal service obligation to sell bread to every address – or permit delivery on fewer than 5-6 days a week? 4

Even with the current definition of the universal service, however, there is no reason to have major concerns regarding its persistence. A

4 In principle, we support the need to provide special arrangements for the infirm and immobile.

JOS GEERAERTS

45

universal postal service has been preserved in fully liberalised postal markets in Sweden, New Zealand and Argentina. At the same time, Sweden is a fine example of how innovation has sprung from liberalisation; showing how a postal service can be flexible, dynamic and change with the developing society.5

Consignia has recently announced savings of up to £1.2bn. The total mail revenue of Consignia amounts to £4.7bn.6 This means that there exists a tremendous potential to improve efficiency, and as a result it is very unlikely that competitors will, in the short to mid-term, be able to gain such a high market shares that the universal service could be threatened. As there is no sign whatsoever that Consignia will no longer be able to maintain the universal service after the savings have been achieved, the savings program is the best possible evidence that liberalisation or its imminent arrival is the best way to drive efficiency, and there is no reason to doubt the maintenance of the universal service. However, in the very unlikely event that the universal service is jeopardised, there are sufficient safeguards available. PostComm could consider granting greater price flexibility to Consignia when providing competitive business mail services, in order to react to competition in a way which does not harm its overall economic condition. The function of the universal service is to ensure that all individuals, wherever they live in the United Kingdom, have access to a regular means of physical communication at an affordable price. The uniform tariff is designed not to prejudice such individuals who 5 Posten AG was recently investigating the possibility of making an ‘electronic post office’ in every household for the receipt of services, such as e –mail, distance shopping with automatic delivery request is under potential development (an ‘ordering fridge’ which would link to the postal delivery network is being developed between Ericsson and Electrolux), and production of e-stamps. It is also adapting its post offices network to meet the real requirements of its customers by increasingly appointing third party distributors or agents who, typically, have longer opening hours than the traditional post offices. 6 Source : PostComm, ‘Assessment of the costs and benefits of Consignia’s current USO provision’.

MARKET STRATEGIES FOR NEW ENTRANTS

46

live in more remote parts of the Kingdom and can be safeguarded. Allowing a commercial reaction to competitive prices in the business mail sector, taking into account different market conditions in order to distinguish between different customers, will help to preserve the universal service and allow competitive services to be offered to customers (but always subject to the prohibition on predatory pricing). As a final safeguard, PostComm could consider introducing a universal service fund which would apply to providers of domestic letter delivery services, under the appropriate conditions (eg, to ensure that competitors do not have to subsidise inefficiency or pricing discounts). This could cover the consequences of substantial volume loss of the universal service provider due to competition, and a contribution to this fund could be made by all operators in the universal service area that don't have a universal service obligation, depending on their market share in that specific area. This does, however, require a solid definition of the universal service and its costs.

Ian Reay, Liberalisation and Monopoly Policy Manager, and Frank Rodriguez, Head of Economics, Consignia

47

7 MEETING THE UNIVERSAL SERVICE OBLIGATION IN POSTS Ian Reay and Frank Rodriguez Introduction An increase in the competitive environment in postal markets is expected to produce benefits for customers by broadening choice and encouraging innovation. However, there is an inherent contradiction between full competition and maintaining the current public policy objectives of universal service and uniform tariff structures. The means of introducing competition, and the extent to which it should be permitted, are, therefore, important questions. The introduction of competition in other postal markets in Europe and elsewhere has only been possible by permitting significantly greater pricing flexibility than is compatible with the uniform tariff structure required by the Postal Services Act 2000. If, on balance, the view prevails that significant competition is required, then there will need to be a recognition that the universal service obligation and uniform tariff requirement, as currently defined, will not be sustainable financially, and that more market based pricing structures will have to be introduced. Deciding on the manner in which competition can be introduced into the postal sector cannot be done without explicitly taking into account the universal service obligation. There are recognised benefits of competition, but entry should be introduced in a careful way, with a long-term perspective, taking into account the specific factors of the industry concerned. Barriers to entry in postal markets are very low and entry does not require high levels of up-front investment. Postal service is labour intensive and deals with a product which is conveyed from a unique origin to a unique destination for hand delivery to a specific address.

MEETING THE USO IN POSTS

48

Consequently, quality of service depends on the performance of individuals on a day to day basis. A regulatory structure with a short term focus, and with incentive schemes which starve the incumbent universal service provider of the funds necessary for investment in quality improvements, innovation and growth, will lead to a decline in the industry concerned. The fate of a liberalised industry which is deprived of the funds necessary for investment in medium and long term capacity is demonstrated by the experiences of the electricity sector in California, where parts of the electricity system have come close to bankruptcy. The universal service obligation (USO) Provision is made in European legislation which limits the application of the European Competition rules to services of general economic interest, if the provision of the relevant service would otherwise be jeopardised, and this provision is reflected in the Competition Act 1998.1 The universal postal service is an example of such a service. The European Directive on postal services adopted in 1997 lays down minimum standards for the universal postal service.2 This states, in Article 3, that the universal service consists of a daily collection and a daily delivery to every address except at the discretion of the national regulatory authority. This applies to letters up to 2kg, packages up to 10kg (up to 20kg at the discretion of the national regulatory authority) and to registered and insured items. The European regulations, therefore, only specify an infrastructure; they do not specify any particular service (eg, first or second class) that should lie within the universal service. The Postal Services Act 2000 carries over into United Kingdom domestic legislation the provisions in the European Directive and 1 Schedule 3, Paragraph 4. 2 Directive No. 97/67/EC of the European Parliament and of the Council on common rules for the development of the internal market of Community postal services and the improvement of quality of service, Official Journal of the European Communities, 21/01/98, No. L15/14.

IAN REAY AND FRANK RODRIGUEZ

49

adds the additional requirement that the services should be provided at “affordable prices determined in accordance with a public tariff which is uniform throughout the United Kingdom” although “conclusions with customers of individual agreements as to prices shall not be taken to preclude the provision of a universal postal service”. 3 4

The ‘uniform tariff’ obligation in the Act introduced into legislation a provision that had been a political requirement previously but which, for the first time, was now specifically incorporated into the law. It is intended to protect the rural consumer, in particular, from increases in prices which would result from a tariff re-balancing that might, for example, follow from a close alignment of service prices to costs or from a segmentation of the postal market leading to differential pricing. Both of these would be commercial responses in a competitive postal market. The statement in the Act on the possibility of individual agreements as to prices would appear to negate the previous statement in the Act on the need for a uniform tariff since if an individual agreement led to a lower price then there would be no need for customers to avail themselves of the universal postal service at the geographically uniform price. The ‘uniform’ price becomes in practice a ‘maximum’ price so that the universal service at the uniform price becomes a service of last resort used only by customers who, for example by reason of location or extent of mailings, have no available alternative. The European Commission, in the current draft of the next Postal Directive which - if agreed - will take effect from 2003, has proposed a text which would limit the application of this pricing flexibility by requiring that special tariffs should take account of the avoided costs compared to the standard service.5

3 Part I, Section 4(1). 4 Part I, Section 4(2). 5 “Whenever universal service providers apply special tariffs, for example for services for businesses, bulk mailers or consolidators of mail from different customers, they shall apply the principles of transparency and non-

MEETING THE USO IN POSTS

50

In those utilities in which competition has already been introduced the regulator’s duty to promote competition has had shared primacy with other duties, whereas in the postal sector, as laid down in the Postal Services Act 2000, Postcomm’s primary duty is the provision of the universal postal service. The traditional view has been that competition is incompatible with universal service - particularly so when the provision of universal service is accompanied by a uniform tariff obligation. Hence the need for a reserved area to protect the revenues of the provider of that service. An alternative view is that the market place would of itself produce a universal service because that is what the customers of the service want. In one sense that is obviously true - if there is a need the market place will meet that need at the market price. It is because it overrides the market price that the uniform price is such a key impediment to introducing competition. No other public utility has a uniform price obligation in the way the postal service does. Introducing competition in a manner that does not enable the long term impact on this universal service to be clearly understood, carries the risk that Postcomm may fail in its primary duty. Postcomm rightly asserts that predicting the way that the market might develop with competition is difficult. They also acknowledge that it is not possible to predict the impact on Consignia’s ability to

discrimination with regard both to the tariffs and to the associated conditions. The tariffs shall take account of the avoided costs compared to the standard service covering the complete range of features offered for the clearance, transport, sorting and delivery of individual postal items and, together with the associated conditions, shall apply equally as between third parties and the equivalent service elements of the universal service providers themselves. Any such tariffs shall also be available to residential customers who post under similar conditions.”

In the Commission draft this text is in Article 9 but an amendment from the European Parliament proposes moving it to Article 12.

IAN REAY AND FRANK RODRIGUEZ

51

respond to competition whilst preserving the universal service. A gradual and controlled approach is therefore needed. Assessing the cost of universal postal service (the cost of the USO) Decisions relating to the future state of the postal market cannot be made on the basis of the current market situation but require a forward-looking assessment. The analysis should focus on understanding the issues involved in moving from a situation of a high degree of monopoly to one of greater competition, while continuing to meet the universal service obligation of a universal postal service at a uniform, affordable tariff. In other words the question that needs to be addressed is: • In moving from a situation in which monopoly protection is

removed but in which the obligation to provide universal service remains, what is the financial cost imposed on the universal service provider (USP)? (This is known as the entry pricing calculation and is also described more fully below. Note that financial cost here refers to loss of profitability)

Unfortunately this is not the approach that Postcomm has used in undertaking their estimates of the cost of the USO. Against a background of the clear purpose of introducing effective competition, Postcomm has released, simultaneously with its consultation document on effective competition, a ‘discussion document’ purporting to assess, using economic analysis, the costs and benefits of Consignia’s current universal service provision. However, in this document, the question that is tackled is: • In the current market situation of near monopoly, what costs could

Consignia save by not meeting the USO?

MEETING THE USO IN POSTS

52

(This is known as the net avoided cost calculation, which is also described more fully below and refers again to a loss of profitability).

After a long examination of this hypothetical question, the discussion document reaches the following conclusion in terms of the use of this exercise for informing Postcomm’s liberalisation programme:

“..analysis of the net cost of universal service does not