18

Promotional Analysis UK Grocery Promotional Report July 2020

Promotional Analysis

UK Grocery Promotional ReportJuly 2020

Contents

1. Introduction

2. UK Promotional Landscape Overview - Total promotional participation- Promotional participation by retailer- Promotional participation by sector- Promotional shifts by category

3. Price & Promotion Spotlight: Health, Beauty & Personal Care - Promotions analysis

4. Summary & Supplier Recommendations - July summary & recommendations

CONTENTS

UK Promotional Report 2

Data in this report is sourced from Edge by Ascential Price & Promotion. Throughout, we refer to “promotional participation” - this is the share of all available listed lines that are on promotion in a given period.

To explore deeper insights for your category, please speak to your account manager or email [email protected]

The role of promotions in a changing retail landscape UK grocery retailers have faced significant disruption in the first half of 2020, with changing patterns of consumer demand resulting from COVID-19.

Going forward, intermittent lockdowns, a recessionary economic outlook and consumer uncertainty will continue to influence price and promotion decisions across the sector. We expect promotions to be used more strategically by retailers to manage demand, drive value perceptions and foster consumer loyalty.

In this new UK Grocery Promotional Report, we provide insight into the evolving promotional landscape across the UK, in order to equip retailers and suppliers with insights to inform future promotional strategies, in particular:

• Industry shifts in promotional participation over time, and how competitors are evolving their promotional strategies

• The promotional mechanics being utilized and gaining momentum

• Promotional dynamics by product sectors and categories

INTRODUCTION

UK Promotional Report

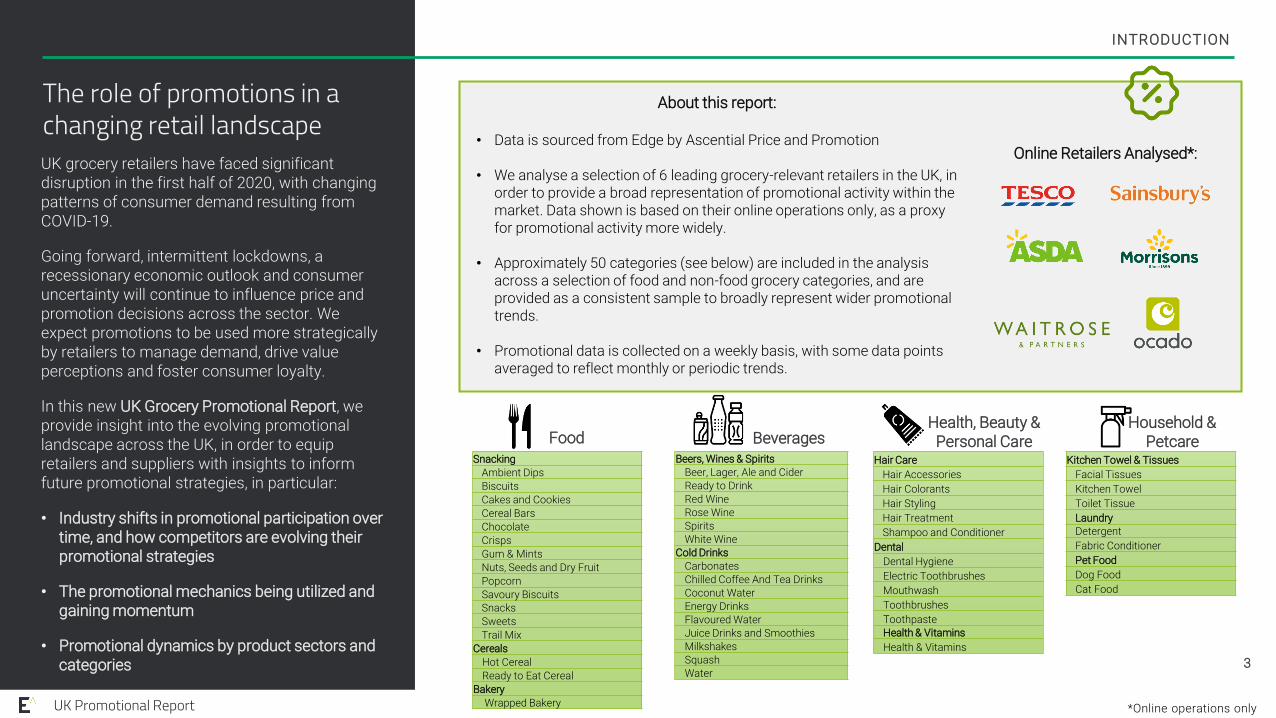

Our promotional analysis is based on the following categories:

3

Beers, Wines & Spirits

Beer, Lager, Ale and Cider

Ready to Drink

Red Wine

Rose Wine

Spirits

White Wine

Cold DrinksCarbonates

Chilled Coffee And Tea Drinks

Coconut Water

Energy Drinks

Flavoured Water

Juice Drinks and Smoothies

Milkshakes

Squash

Water

Snacking

Ambient Dips

Biscuits

Cakes and Cookies

Cereal Bars

Chocolate

Crisps

Gum & Mints

Nuts, Seeds and Dry Fruit

Popcorn

Savoury BiscuitsSnacks

Sweets

Trail Mix

Cereals

Hot Cereal

Ready to Eat Cereal

Bakery

Wrapped Bakery

Hair Care

Hair Accessories

Hair Colorants

Hair Styling

Hair Treatment

Shampoo and Conditioner

Dental

Dental Hygiene

Electric Toothbrushes

Mouthwash

Toothbrushes

ToothpasteHealth & Vitamins

Health & Vitamins

Kitchen Towel & Tissues

Facial Tissues

Kitchen Towel

Toilet Tissue

Laundry Detergent

Fabric Conditioner

Pet Food

Dog Food

Cat Food

Food BeveragesHealth, Beauty &

Personal CareHousehold &

Petcare

About this report:

• Data is sourced from Edge by Ascential Price and Promotion

• We analyse a selection of 6 leading grocery-relevant retailers in the UK, in order to provide a broad representation of promotional activity within the market. Data shown is based on their online operations only, as a proxy for promotional activity more widely.

• Approximately 50 categories (see below) are included in the analysis across a selection of food and non-food grocery categories, and are provided as a consistent sample to broadly represent wider promotional trends.

• Promotional data is collected on a weekly basis, with some data points averaged to reflect monthly or periodic trends.

Online Retailers Analysed*:

*Online operations only

UK Promotional Landscape Overview

UK Promotional Report 4

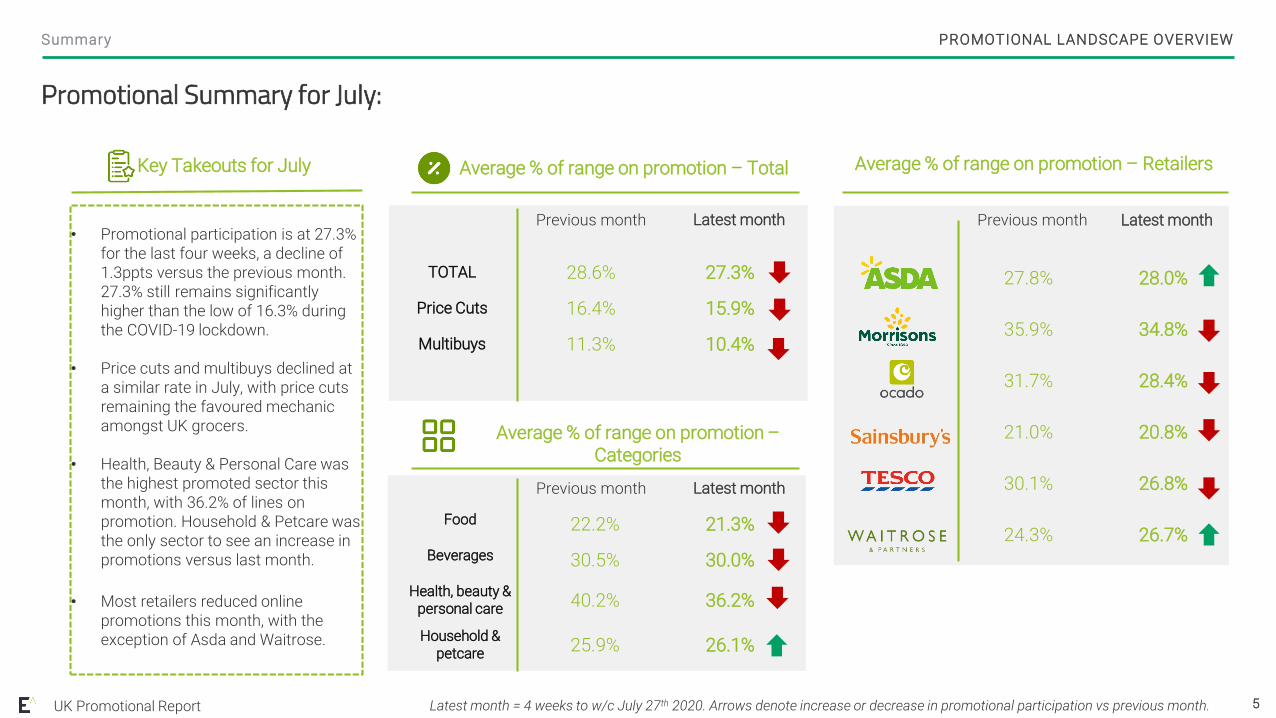

27.8% 28.0%

35.9% 34.8%

31.7% 28.4%

21.0% 20.8%

30.1% 26.8%

24.3% 26.7%Food 22.2% 21.3%

Beverages 30.5% 30.0%

Health, beauty & personal care 40.2% 36.2%

Household & petcare 25.9% 26.1%

Promotional Summary for July:

PROMOTIONAL LANDSCAPE OVERVIEW

UK Promotional Report

Summary

5

Average % of range on promotion – Total

Average % of range on promotion –Categories

Previous month Latest month

Average % of range on promotion – Retailers

Previous month Latest month• Promotional participation is at 27.3%

for the last four weeks, a decline of 1.3ppts versus the previous month. 27.3% still remains significantly higher than the low of 16.3% during the COVID-19 lockdown.

• Price cuts and multibuys declined at a similar rate in July, with price cuts remaining the favoured mechanic amongst UK grocers.

• Health, Beauty & Personal Care was the highest promoted sector this month, with 36.2% of lines on promotion. Household & Petcare was the only sector to see an increase in promotions versus last month.

• Most retailers reduced online promotions this month, with the exception of Asda and Waitrose.

Key Takeouts for July

Previous month Latest month

TOTAL 28.6% 27.3%

Price Cuts 16.4% 15.9%

Multibuys 11.3% 10.4%

Latest month = 4 weeks to w/c July 27th 2020. Arrows denote increase or decrease in promotional participation vs previous month.

PROMOTIONAL LANDSCAPE OVERVIEW

UK Promotional Report

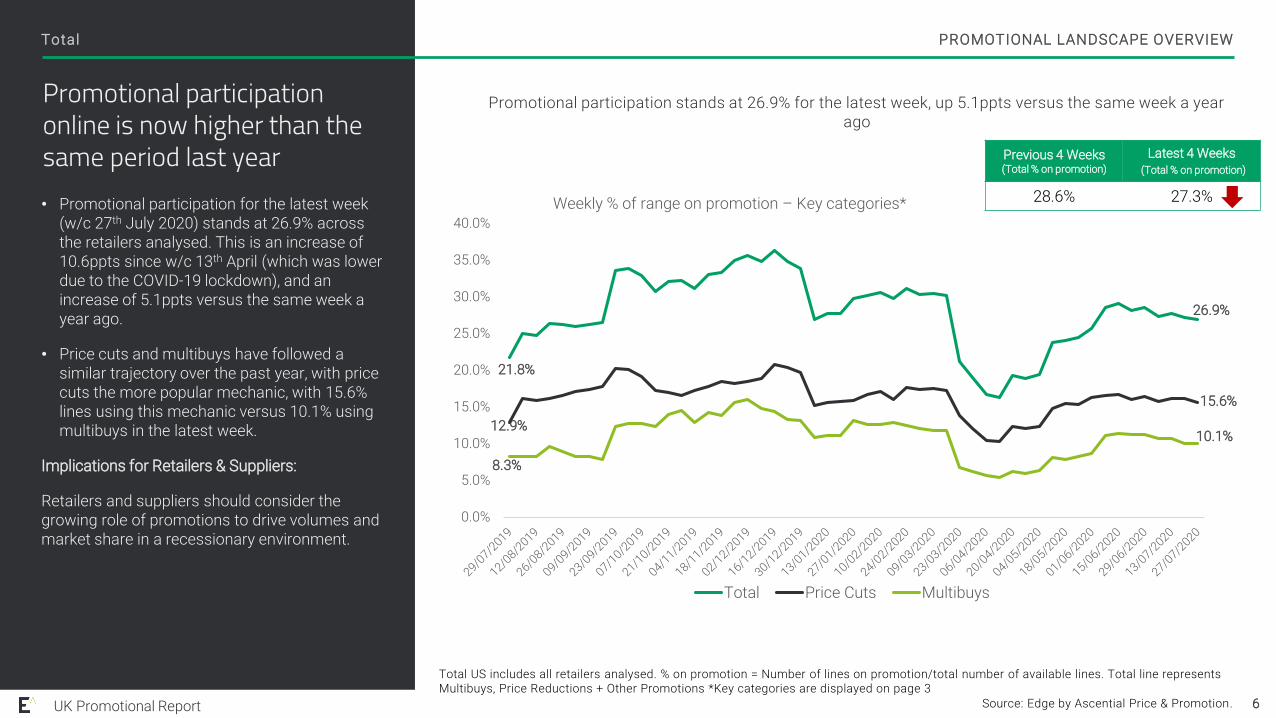

Promotional participation stands at 26.9% for the latest week, up 5.1ppts versus the same week a year ago

Promotional participation online is now higher than the same period last year • Promotional participation for the latest week

(w/c 27th July 2020) stands at 26.9% across the retailers analysed. This is an increase of 10.6ppts since w/c 13th April (which was lower due to the COVID-19 lockdown), and an increase of 5.1ppts versus the same week a year ago.

• Price cuts and multibuys have followed a similar trajectory over the past year, with price cuts the more popular mechanic, with 15.6% lines using this mechanic versus 10.1% using multibuys in the latest week.

Implications for Retailers & Suppliers:

Retailers and suppliers should consider the growing role of promotions to drive volumes and market share in a recessionary environment.

Total

6

Total US includes all retailers analysed. % on promotion = Number of lines on promotion/total number of available lines. Total line represents Multibuys, Price Reductions + Other Promotions *Key categories are displayed on page 3

21.8%

26.9%

12.9%

15.6%

8.3%

10.1%

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

35.0%

40.0%

Weekly % of range on promotion – Key categories*

Total Price Cuts Multibuys

Previous 4 Weeks (Total % on promotion)

Latest 4 Weeks(Total % on promotion)

28.6% 27.3%

Source: Edge by Ascential Price & Promotion.

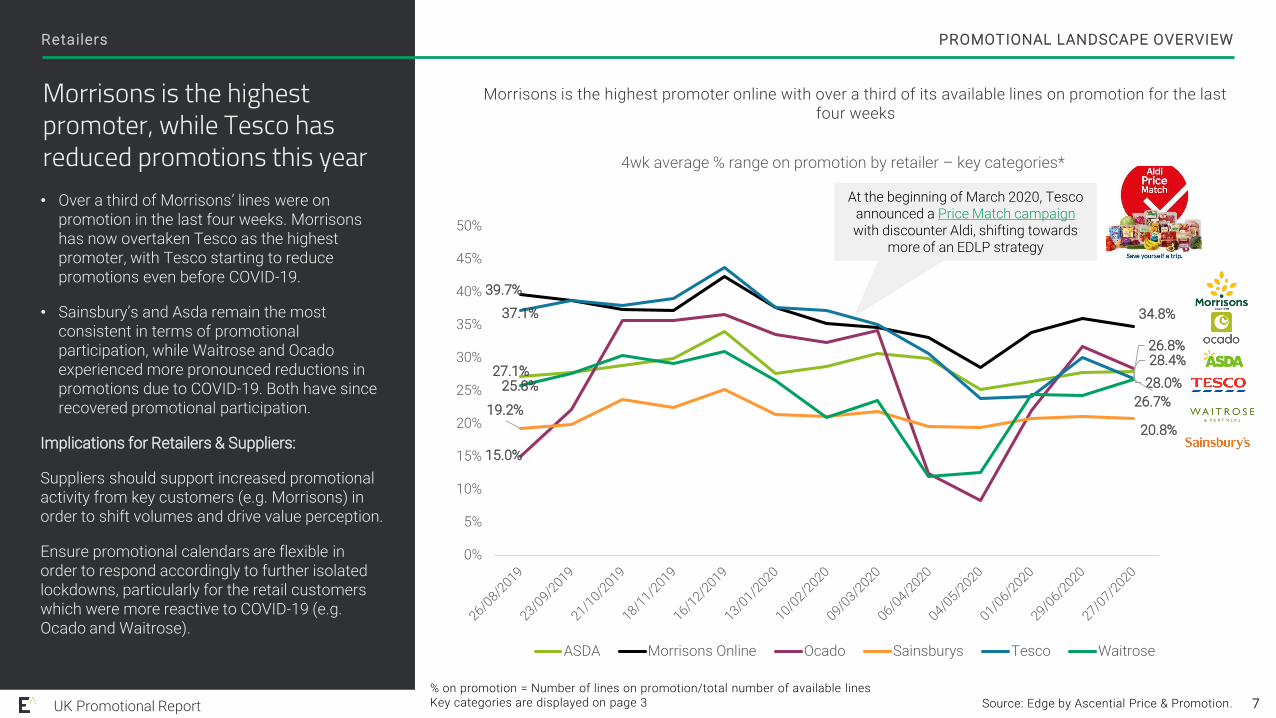

Morrisons is the highest promoter, while Tesco has reduced promotions this year• Over a third of Morrisons’ lines were on

promotion in the last four weeks. Morrisons has now overtaken Tesco as the highest promoter, with Tesco starting to reduce promotions even before COVID-19.

• Sainsbury’s and Asda remain the most consistent in terms of promotional participation, while Waitrose and Ocado experienced more pronounced reductions in promotions due to COVID-19. Both have since recovered promotional participation.

Implications for Retailers & Suppliers:

Suppliers should support increased promotional activity from key customers (e.g. Morrisons) in order to shift volumes and drive value perception.

Ensure promotional calendars are flexible in order to respond accordingly to further isolated lockdowns, particularly for the retail customers which were more reactive to COVID-19 (e.g. Ocado and Waitrose).

PROMOTIONAL LANDSCAPE OVERVIEW

UK Promotional Report

Morrisons is the highest promoter online with over a third of its available lines on promotion for the last four weeks

Retailers

7

27.1%28.0%

39.7%

34.8%

15.0%

28.4%

19.2%

20.8%

37.1%

26.8%

25.8%26.7%

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%

4wk average % range on promotion by retailer – key categories*

ASDA Morrisons Online Ocado Sainsburys Tesco Waitrose

% on promotion = Number of lines on promotion/total number of available lines Key categories are displayed on page 3 Source: Edge by Ascential Price & Promotion.

At the beginning of March 2020, Tesco announced a Price Match campaign with discounter Aldi, shifting towards

more of an EDLP strategy

16.8%

20.9%

25.1%

30.4%

28.6%

33.9%

18.4%

26.0%

0%

10%

20%

30%

40%

50%

60%

29Jul19

12Aug19

26Aug19

09Sep19

23Sep19

07Oct19

21Oct19

04Nov19

18Nov19

02Dec19

16Dec19

30Dec19

13Jan20

27Jan20

10Feb20

24Feb20

09Mar20

23Mar20

06Apr20

20Apr20

04May20

18May20

01Jun20

15Jun20

29Jun20

13Jul20

27Jul20

Weekly % of range on promotion – by category

Food Beverages Health, beauty & personal care Household & petcare

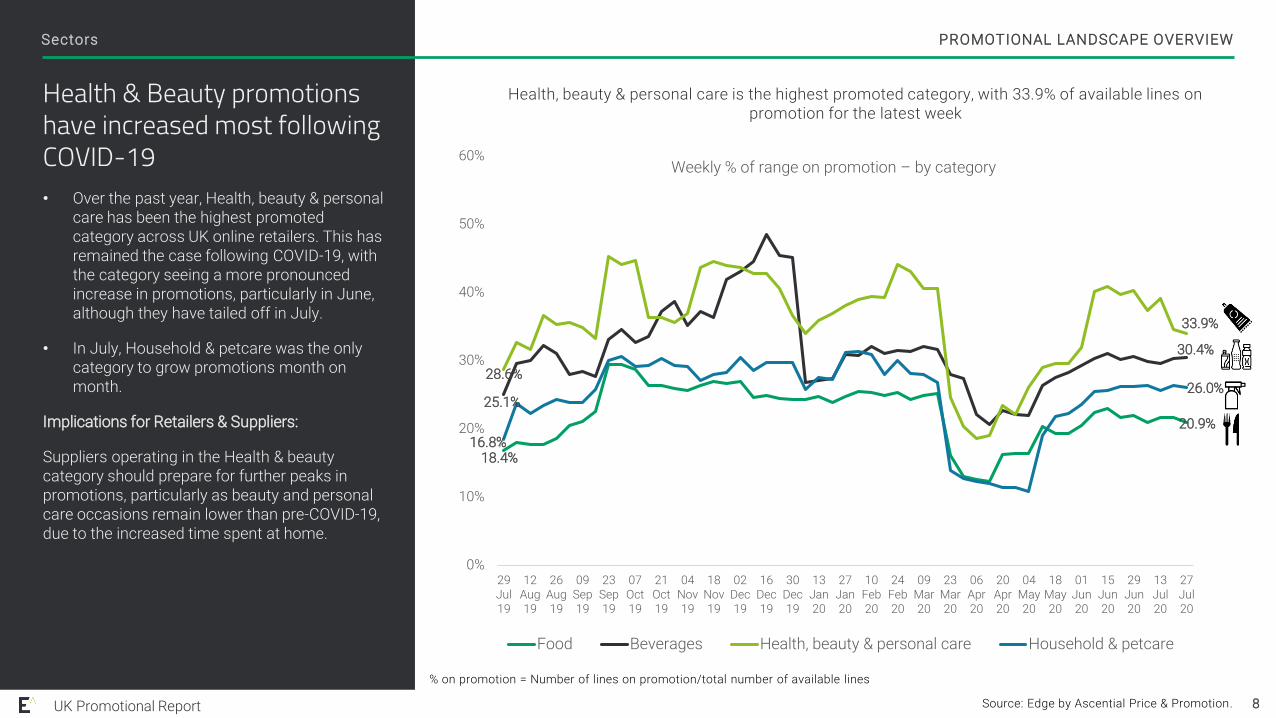

Health & Beauty promotions have increased most following COVID-19 • Over the past year, Health, beauty & personal

care has been the highest promoted category across UK online retailers. This has remained the case following COVID-19, with the category seeing a more pronounced increase in promotions, particularly in June, although they have tailed off in July.

• In July, Household & petcare was the only category to grow promotions month on month.

Implications for Retailers & Suppliers:

Suppliers operating in the Health & beauty category should prepare for further peaks in promotions, particularly as beauty and personal care occasions remain lower than pre-COVID-19, due to the increased time spent at home.

PROMOTIONAL LANDSCAPE OVERVIEW

UK Promotional Report

Health, beauty & personal care is the highest promoted category, with 33.9% of available lines on promotion for the latest week

Sectors

8

% on promotion = Number of lines on promotion/total number of available lines

Source: Edge by Ascential Price & Promotion.

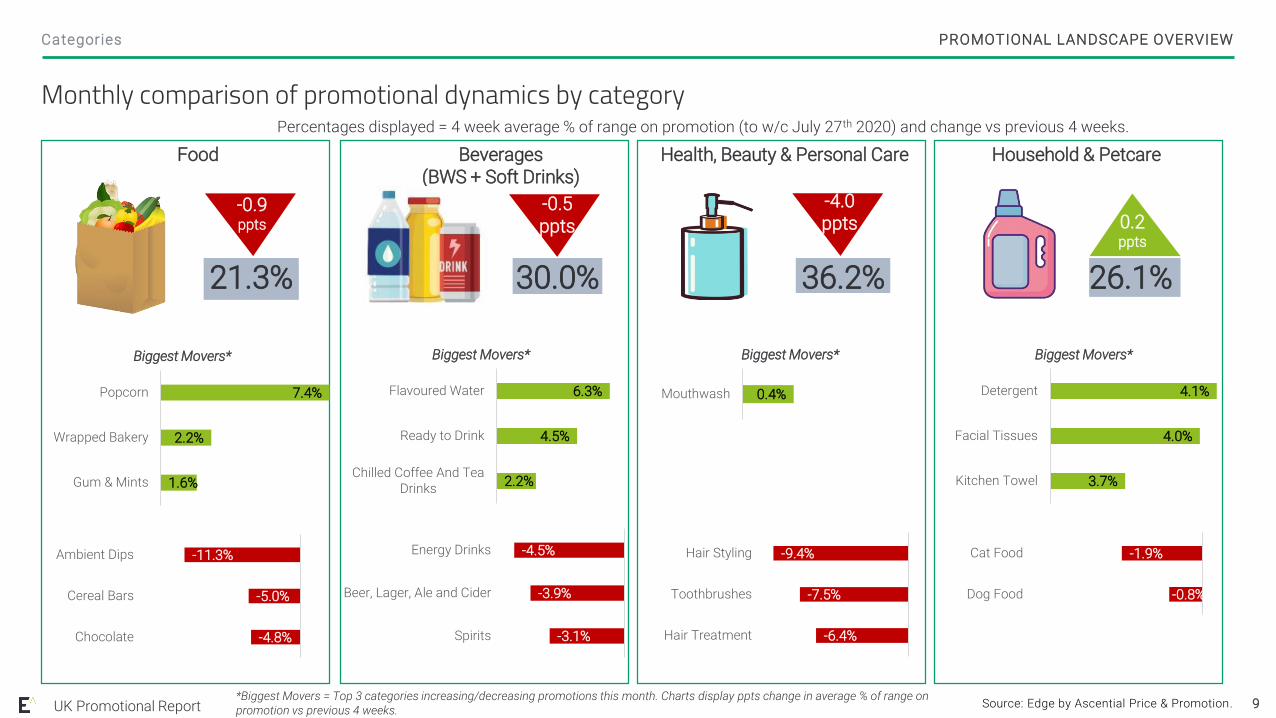

Monthly comparison of promotional dynamics by category

PROMOTIONAL LANDSCAPE OVERVIEW

UK Promotional Report

Categories

9

Food Beverages (BWS + Soft Drinks)

Health, Beauty & Personal Care Household & Petcare

7.4%

2.2%

1.6%

Popcorn

Wrapped Bakery

Gum & Mints

-4.8%

-5.0%

-11.3%

Chocolate

Cereal Bars

Ambient Dips

Biggest Movers*

Percentages displayed = 4 week average % of range on promotion (to w/c July 27th 2020) and change vs previous 4 weeks.

*Biggest Movers = Top 3 categories increasing/decreasing promotions this month. Charts display ppts change in average % of range on promotion vs previous 4 weeks.

21.3% 30.0% 36.2% 26.1%

-0.9ppts

-0.5ppts

-4.0ppts 0.2

ppts

6.3%

4.5%

2.2%

Flavoured Water

Ready to Drink

Chilled Coffee And TeaDrinks

-3.1%

-3.9%

-4.5%

Spirits

Beer, Lager, Ale and Cider

Energy Drinks

Biggest Movers*

0.4%Mouthwash

-6.4%

-7.5%

-9.4%

Hair Treatment

Toothbrushes

Hair Styling

Biggest Movers*

4.1%

4.0%

3.7%

Detergent

Facial Tissues

Kitchen Towel

-0.8%

-1.9%

Dog Food

Cat Food

Biggest Movers*

Source: Edge by Ascential Price & Promotion.

Spotlight: Health, Beauty & Personal Care

UK Promotional Report 10Total Health, Beauty & Personal Care includes Dental, Haircare and Health & Vitamins

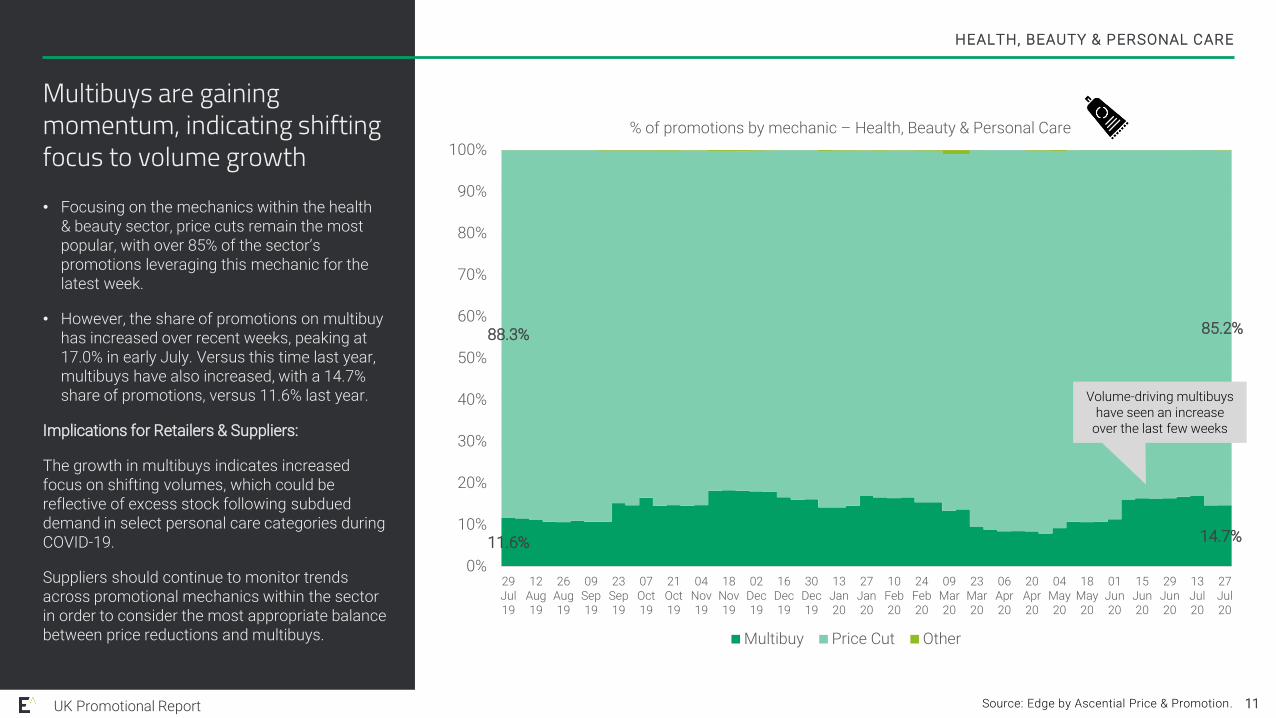

Multibuys are gaining momentum, indicating shifting focus to volume growth • Focusing on the mechanics within the health

& beauty sector, price cuts remain the most popular, with over 85% of the sector’s promotions leveraging this mechanic for the latest week.

• However, the share of promotions on multibuyhas increased over recent weeks, peaking at 17.0% in early July. Versus this time last year, multibuys have also increased, with a 14.7% share of promotions, versus 11.6% last year.

Implications for Retailers & Suppliers:

The growth in multibuys indicates increased focus on shifting volumes, which could be reflective of excess stock following subdued demand in select personal care categories during COVID-19.

Suppliers should continue to monitor trends across promotional mechanics within the sector in order to consider the most appropriate balance between price reductions and multibuys.

HEALTH, BEAUTY & PERSONAL CARE

UK Promotional Report 11Source: Edge by Ascential Price & Promotion.

11.6% 14.7%

88.3% 85.2%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

29Jul19

12Aug19

26Aug19

09Sep19

23Sep19

07Oct19

21Oct19

04Nov19

18Nov19

02Dec19

16Dec19

30Dec19

13Jan20

27Jan20

10Feb20

24Feb20

09Mar20

23Mar20

06Apr20

20Apr20

04May20

18May20

01Jun20

15Jun20

29Jun20

13Jul20

27Jul20

% of promotions by mechanic – Health, Beauty & Personal Care

Multibuy Price Cut Other

Volume-driving multibuys have seen an increase

over the last few weeks

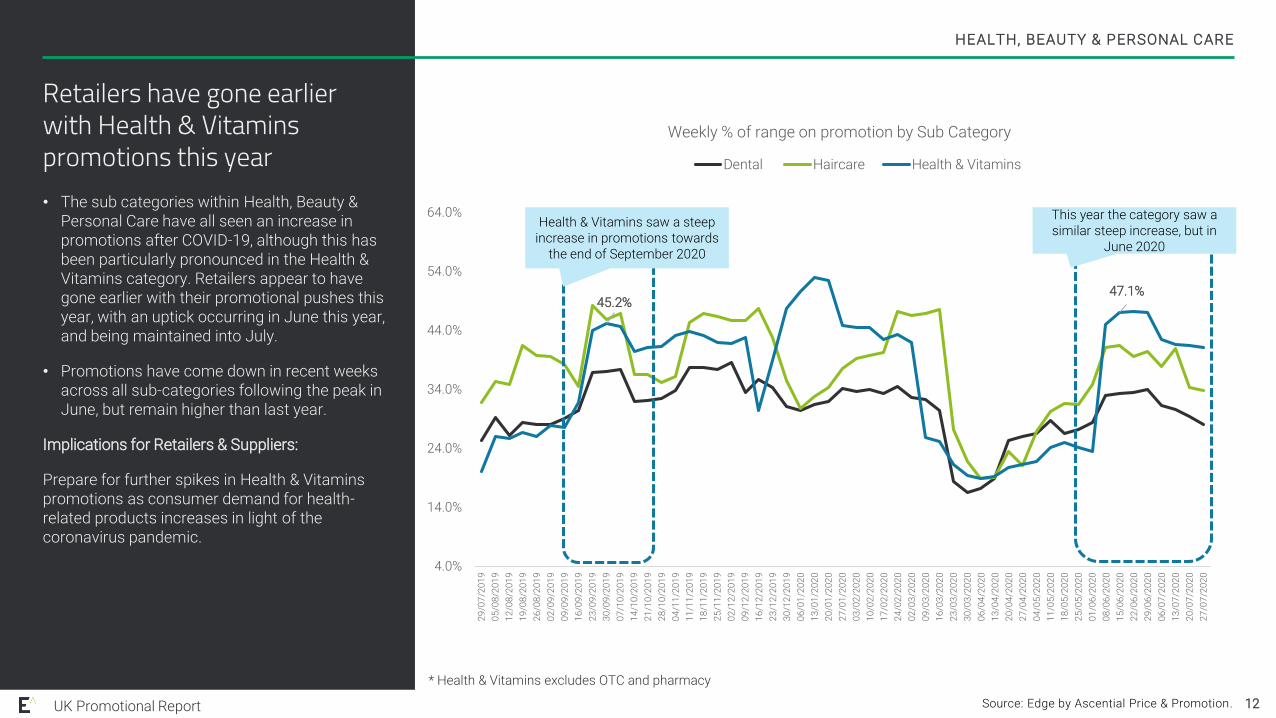

Retailers have gone earlier with Health & Vitamins promotions this year • The sub categories within Health, Beauty &

Personal Care have all seen an increase in promotions after COVID-19, although this has been particularly pronounced in the Health & Vitamins category. Retailers appear to have gone earlier with their promotional pushes this year, with an uptick occurring in June this year, and being maintained into July.

• Promotions have come down in recent weeks across all sub-categories following the peak in June, but remain higher than last year.

Implications for Retailers & Suppliers:

Prepare for further spikes in Health & Vitamins promotions as consumer demand for health-related products increases in light of the coronavirus pandemic.

HEALTH, BEAUTY & PERSONAL CARE

UK Promotional Report 12

45.2%47.1%

4.0%

14.0%

24.0%

34.0%

44.0%

54.0%

64.0%

29

/07

/20

19

05

/08

/20

19

12

/08

/20

19

19

/08

/20

19

26

/08

/20

19

02

/09

/20

19

09

/09

/20

19

16

/09

/20

19

23

/09

/20

19

30

/09

/20

19

07

/10

/20

19

14

/10

/20

19

21

/10

/20

19

28

/10

/20

19

04

/11

/20

19

11

/11

/20

19

18

/11

/20

19

25

/11

/20

19

02

/12

/20

19

09

/12

/20

19

16

/12

/20

19

23

/12

/20

19

30

/12

/20

19

06

/01

/20

20

13

/01

/20

20

20

/01

/20

20

27

/01

/20

20

03

/02

/20

20

10

/02

/20

20

17

/02

/20

20

24

/02

/20

20

02

/03

/20

20

09

/03

/20

20

16

/03

/20

20

23

/03

/20

20

30

/03

/20

20

06

/04

/20

20

13

/04

/20

20

20

/04

/20

20

27

/04

/20

20

04

/05

/20

20

11

/05

/20

20

18

/05

/20

20

25

/05

/20

20

01

/06

/20

20

08

/06

/20

20

15

/06

/20

20

22

/06

/20

20

29

/06

/20

20

06

/07

/20

20

13

/07

/20

20

20

/07

/20

20

27

/07

/20

20

Weekly % of range on promotion by Sub Category

Dental Haircare Health & Vitamins

Source: Edge by Ascential Price & Promotion.

Health & Vitamins saw a steep increase in promotions towards

the end of September 2020

This year the category saw a similar steep increase, but in

June 2020

* Health & Vitamins excludes OTC and pharmacy

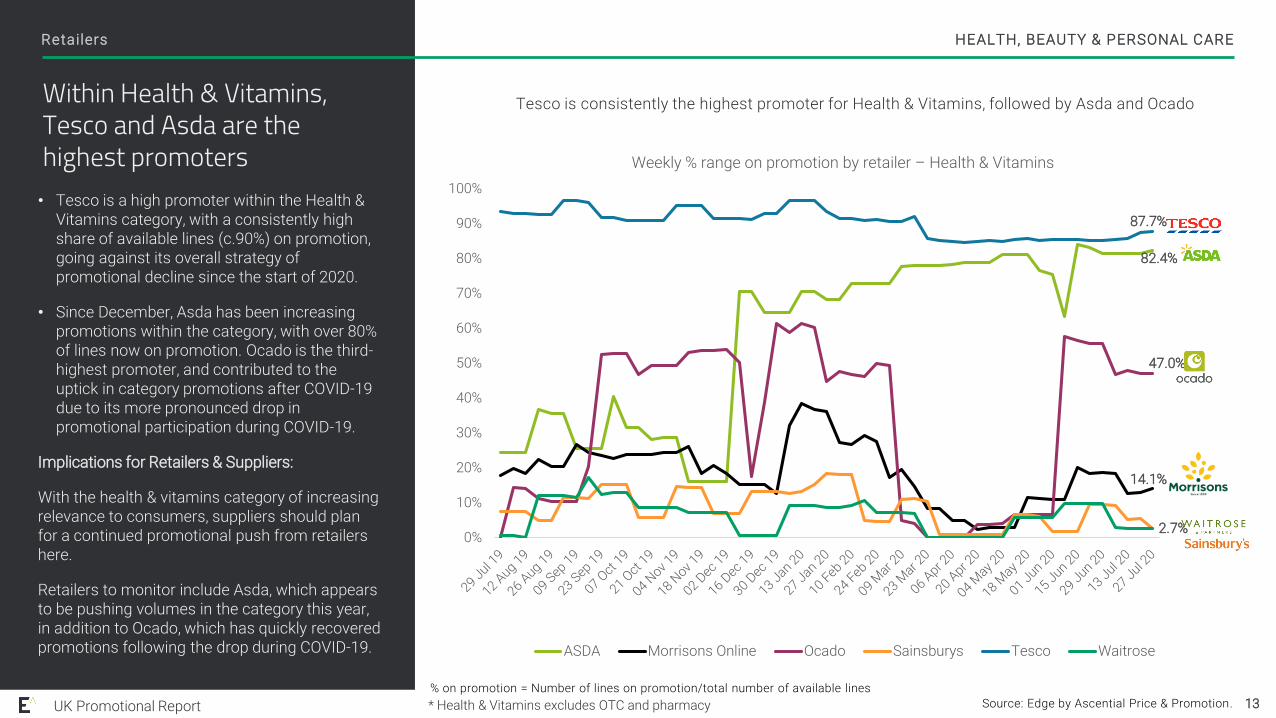

Within Health & Vitamins, Tesco and Asda are the highest promoters• Tesco is a high promoter within the Health &

Vitamins category, with a consistently high share of available lines (c.90%) on promotion, going against its overall strategy of promotional decline since the start of 2020.

• Since December, Asda has been increasing promotions within the category, with over 80% of lines now on promotion. Ocado is the third-highest promoter, and contributed to the uptick in category promotions after COVID-19 due to its more pronounced drop in promotional participation during COVID-19.

Implications for Retailers & Suppliers:

With the health & vitamins category of increasing relevance to consumers, suppliers should plan for a continued promotional push from retailers here.

Retailers to monitor include Asda, which appears to be pushing volumes in the category this year, in addition to Ocado, which has quickly recovered promotions following the drop during COVID-19.

HEALTH, BEAUTY & PERSONAL CARE

UK Promotional Report

Tesco is consistently the highest promoter for Health & Vitamins, followed by Asda and Ocado

Retailers

13

82.4%

14.1%

47.0%

87.7%

2.7%0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Weekly % range on promotion by retailer – Health & Vitamins

ASDA Morrisons Online Ocado Sainsburys Tesco Waitrose

% on promotion = Number of lines on promotion/total number of available lines

Source: Edge by Ascential Price & Promotion. * Health & Vitamins excludes OTC and pharmacy

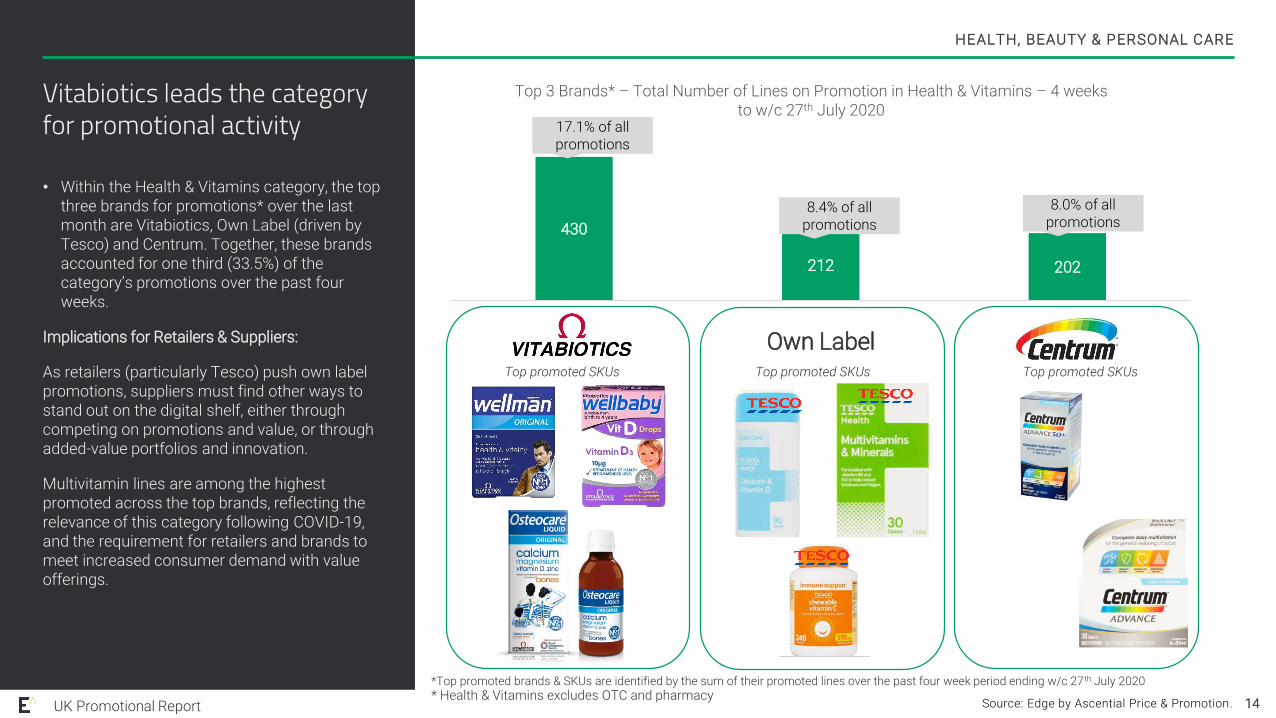

430

212 202

Vitabiotics Own Label Centrum

Top 3 Brands* – Total Number of Lines on Promotion in Health & Vitamins – 4 weeks to w/c 27th July 2020

Vitabiotics leads the category for promotional activity

• Within the Health & Vitamins category, the top three brands for promotions* over the last month are Vitabiotics, Own Label (driven by Tesco) and Centrum. Together, these brands accounted for one third (33.5%) of the category’s promotions over the past four weeks.

Implications for Retailers & Suppliers:

As retailers (particularly Tesco) push own label promotions, suppliers must find other ways to stand out on the digital shelf, either through competing on promotions and value, or through added-value portfolios and innovation.

Multivitamin lines are among the highest promoted across the top brands, reflecting the relevance of this category following COVID-19, and the requirement for retailers and brands to meet increased consumer demand with value offerings.

HEALTH, BEAUTY & PERSONAL CARE

UK Promotional Report 14

Own Label

17.1% of all promotions

8.4% of all promotions

8.0% of all promotions

*Top promoted brands & SKUs are identified by the sum of their promoted lines over the past four week period ending w/c 27th July 2020

Top promoted SKUs Top promoted SKUsTop promoted SKUs

Source: Edge by Ascential Price & Promotion. * Health & Vitamins excludes OTC and pharmacy

Summary & Recommendations

UK Promotional Report 15

Summary & Recommendations

SUMMARY

UK Promotional Report 16

UK online retailers have recovered promotions following COVID-19 • Over the last month, promotional participation stood at 27.3%, up from the low of 16.3% witnessed during COVID-19. Promotions have

reduced slightly (by 1.3ppts) versus June, indicating that the ‘recovery stage’ in promotions following COVID-19 has now passed. However, suppliers will need to ensure promotional calendars remain flexible going forward, in order to respond accordingly to further isolated lockdowns.

Price cuts remain the primary mechanic for UK online grocers• Of the 27.3% of lines on promotion in the past four weeks, 15.9% of these were price cuts, versus 10.4% using multibuys. Both mechanics

continue to follow a similar trajectory.

Morrisons has overtaken Tesco as the highest promoting retailer • In the last four weeks, 34.8% of Morrisons’ lines were on promotion, the highest of all the retailers analysed. Until March 2020, Tesco was

the highest promoting retailer, but this position has now dropped to fourth as Tesco continues to reduce promotional activity over time – a sign that it is shifting to more of an EDLP strategy.

Health, Beauty & Personal Care has seen the biggest spike in promotions following COVID-19, and out-promotes other sectors • Within the sector, Health & Vitamins is the currently the highest promoted category, driven by Tesco (where it is following a different

strategy to its overarching business), Asda and Ocado. Promotional peaks have occurred earlier this year than last, reflecting the increased consumer interest in the category following COVID-19, and the opportunity for retailers to strategically leverage promotions in this category in order to drive volumes and basket size.

Key Takeouts for July 2020

Access more data and insight on Price & Promotions

Deeper insight

Not tracking a category or retailer you’re interested in? Want to explore deeper insights within your category?

To access more insights, or request a category or retailer to be added this report, please contact us at:

PRICE + PROMO

Drive growth and margins with

optimal pricing and promotions

strategies

Researched and published by Planet Retail Limited

Company No: 3994702 (England & Wales)-Registered Office: c/o Ascential plc, The Prow, 1 Wilder Walk, London W1B 5AP

Terms of use and copyright conditions: © 2018, Ascential plc. All rights reserved. No part of this publication may be reproduced, stored in a retrieval system or transmitted in any form without our prior permission. Planet Retail, Ascential, and their affiliates are not liable for any omissions, errors or incorrect insertions, nor for any interpretations made from the document.

Boston 46 Farnsworth St, Boston, MA 02210

London 7 Savoy Court, London, WC2R 0EX

Frankfurt Eschersheimer Landstraße, 22 60322 Frankfurt

Shanghai 100 Yu Tong Road, Jing An District, Shanghai