True Fiduciary Guidance Michael J. Chasnoff, CFP ® Principal and CEO Steven T. Condon, CFA Managing Principal 03.31.12 4901 Hunt Road | Suite 200 | Cincinnati, OH | 45242 | 513.792.6648 PH | 513.792.6644 FX | TruepointInc.com

Transcript

True Fiduciary Guidance

Michael J. Chasnoff, CFP®

Principal and CEO

Steven T. Condon, CFA

Managing Principal

03.31.12

4901 Hunt Road | Suite 200 | Cincinnati, OH | 45242 | 513.792.6648 PH | 513.792.6644 FX | TruepointInc.com

1

"The fiduciary acts at all times for the sole benefit and interests of another, with loyalty

to those interests. A fiduciary must not put personal interests before that duty, and must not

be in a situation where his fiduciary duty to clients conflicts with a fiduciary duty to any

other entity."

- John Bogle, founder and former CEO of Vanguard

Fiduciary GuidanceRole of the Advisor

2

What We Do

Partner with our clients to deliver insight, clarity and confidence to the management of their financial lives

How We Do It

Through the integration of highly qualified specialists and proven processes,

we provide superior, proactive wealth advisory services

The Results

585 client surveys have been completed over the past seven years;

over 98% of those clients indicated they would refer others to Truepoint based on their experience

About Truepoint Inc.Who We Are

3

We believe in challenging the industry’s traditional model of wealth management

True advisory firms are in the minority

– Independent, unbiased advice necessitates a fee-only compensation model

– A client-first focus is most effectively achieved in a privately owned firm that is fully controlled

by the same professionals who actively deliver advice to clients

It is the integration of expertise in multiple financial specializations that produces the

most value

A narrow focus only on the investment portfolio sacrifices the significant opportunity to add

value through integrated financial management

The seamless coordination of expertise across areas such as investment management, tax

management, wealth planning and estate & trust services is most powerful

The investment industry often exploits human emotion and lack of consumer awareness

The industry is designed to give advice based on the belief that the very markets they trade in

do not work

The overarching flaw is the concept that someone can predict the future—all traditional Wall

Street-investment advice involves forecasting some future event

About Truepoint Inc.Our Core Beliefs

4

About Truepoint Inc. Service Offerings

A single family office experience that

leverages Truepoint’s advisory platform

Suggested minimum assets of $25,000,000

Fees customized per family goals

Customized wealth management services

integrating multiple disciplines

Suggested minimum assets of $2,000,000

Tiered fee schedule begins at 0.80%

Investment management coupled with

financial advice and guidance

Suggested minimum assets of $500,000

Tiered fee schedule begins at 0.70%

5

Truepoint Financial Truepoint Capital Truepoint Family Office

Retirement income planning Financial statement preparation Generational education and planning

Withdrawal rate analysis Cash flow and budgeting projections Philanthropy and trust administration

Education planning Advanced tax planning and preparation Bill paying and banking

Employee benefit guidance Estate planning and asset ownership review Expense management and reporting

Charitable gift and succession planning Family counseling and governance

Corporate benefits review and analysis Lifestyle services

Insurance analysis and recommendation Family education

Document and record management Family bank

Strategic stock option management Family business services

College savings strategies

Debt management

About Truepoint Inc.A Wealth of Services

Investment policy statement and portfolio design

Investment manager/vehicle selection

Ongoing contingent portfolio rebalancing

Portfolio performance monitoring and reporting

Investment services are delivered across all service offerings

Additional services are progressive throughout the service offerings

6

Investment strategy should be rooted not in speculation, but rather in the science of

the capital markets

Decades of academic research and empirical data provide clear guidance for most

effectively capturing financial market returns

We focus on factors within the investor’s control

We focus on what works, versus what sells

We don’t speculate. We invest.

Our Investment PhilosophyBetter Investing Through Science

7

Conventional wisdom suggests that smart people, working diligently, can select stocks which are

mispriced by the market. These informed investors are also assumed to be able to time the market.

A study of the returns of 3,156 U.S. stock mutual funds from 1984 to 2006 generated these findings:

− Most funds achieving some of level of market outperformance did so simply by chance

− Only zero to 3% of active managers exhibit the skill sufficient to outperform

− Even if ―skilled‖ managers exist, they are indistinguishable on a forward-looking basis

Given the cost of active management, approximately three-quarters of investment managers have,

and will continue over the long-term, to underperform the overall market.

The Myth of Active ManagementFooled by Randomness

“Most investors, both institutional and individual, will find that the best way to own common stocks is through an index fund that

charges minimal fees. Those following this path are sure to beat the net results (after fees and expenses) delivered by the great majority of investment professionals.”

Warren Buffett

Chairman, Berkshire Hathaway

8

In the face of overwhelming evidence, why do investors keep playing a game they are likely to lose?

It is consistently encouraged by those who stand to profit the most—Wall Street and the

financial media

Investors are overconfident—a natural human condition not limited to investing

Active management is the triumph of hope over experience—but hope does spring eternal

Active investing is more exciting, and provides better cocktail chatter, than passive investing

The Myth of Active ManagementPlaying a Loser’s Game

“What‟s really quite remarkable in the investment world is that people are playing a game which, in some sense, cannot be played.

There are so many people out there in the market; the idea that any single individual without extra information or extra market

power can beat the market is extraordinarily unlikely.

“Yet the market is full of people who think they can do it and full of other people who believe them. This is one of the great mysteries of finance: Why do people believe they can do the impossible? And why do other people believe them?”

Daniel Kahneman

2002 Nobel Laureate (Economics)

9

Markets Work

– Prices reflect all available information and the aggregate opinion of market participants

– Prices move only in response to new information, which may be better or worse than expected

Diversification is Essential

– Diversification reduces uncertainty

– Concentrated investments add risk, with no additional expected return

Risk and Return are Related

– Exposure to meaningful risk factors determines expected return

– Asset allocation along size, value and market dimensions primarily determines the returns of a broadly

diversified portfolio

Control What You Can

– Maintain discipline and have a long-term view of investing

– Consider expenses and tax-efficiency of investment vehicles

Our Investment PhilosophyPrinciples and Beliefs

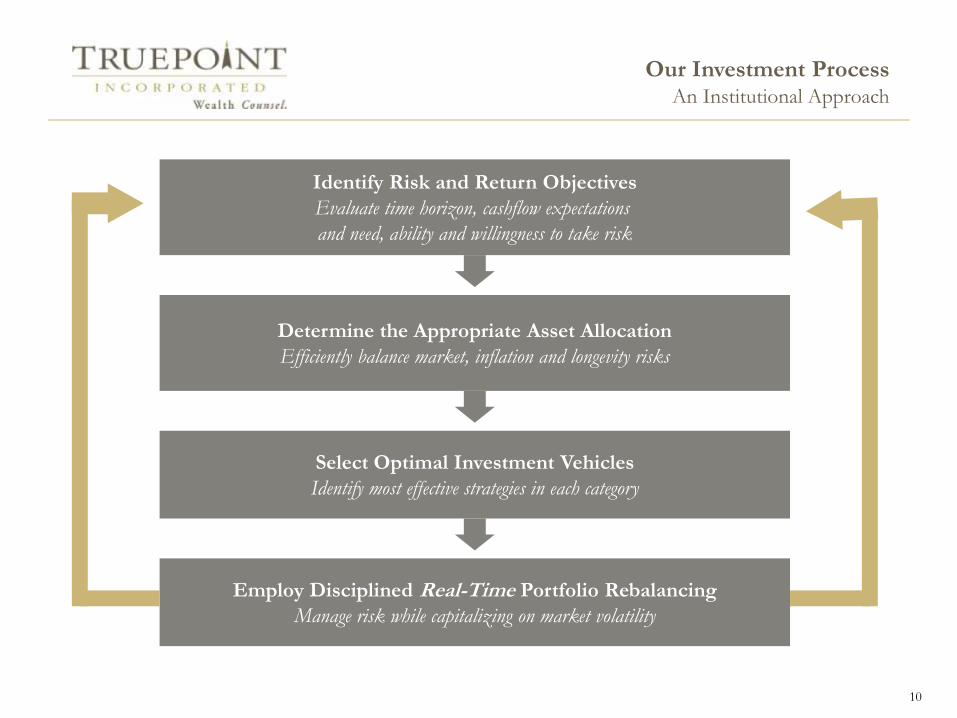

10

Our Investment ProcessAn Institutional Approach

Identify Risk and Return Objectives

Evaluate time horizon, cashflow expectations

and need, ability and willingness to take risk

Determine the Appropriate Asset Allocation

Efficiently balance market, inflation and longevity risks

Select Optimal Investment Vehicles

Identify most effective strategies in each category

Manage risk while capitalizing on market volatility

11

The Behavior GapDiscipline is Critical to Success

Total returns are annualized and represent the 20-year period ending 12/31/10. Average Investor return is based on an analysis by Dalbar Inc., which utilizes the net of

aggregate mutual fund sales, redemptions and exchanges each month as a measure of investor behavior.

Investors often impair their returns through emotional reactions (fear or greed) to market performance

A 2009 study concluded that aggressive trading by individuals reduces returns by about 4% per year

“The investor’s chief problem—and even his worst enemy—is likely to be himself.”

Benjamin Graham

Famed investor and mentor of Warren Buffet

10.50%

8.00% 7.70% 7.20%6.10%

4.70%

2.80% 2.60%

-1%

1%

3%

5%

7%

9%

11%

13%

15%

REITS Oil US Stocks Gold Bonds Foreign Stocks

Homes Average Investor

20-Year Annualized Returns

12Source: Investment Company Institute, J.P. Morgan Asset Management. Data are as of 6/30/11.

Emotion over LogicBuying High and Selling Low

On average, investors repeatedly invest in stocks at high points, and sell at low points

“If you can plug your ears to every attempt (by anyone) to predict what the markets will do, you will outperform nearly every other investor alive over the long run. Only the mantra

of „don‟t know and, I don‟t care‟ will get you there.”

Jason Zweig

Personal finance columnist, Wall Street Journal

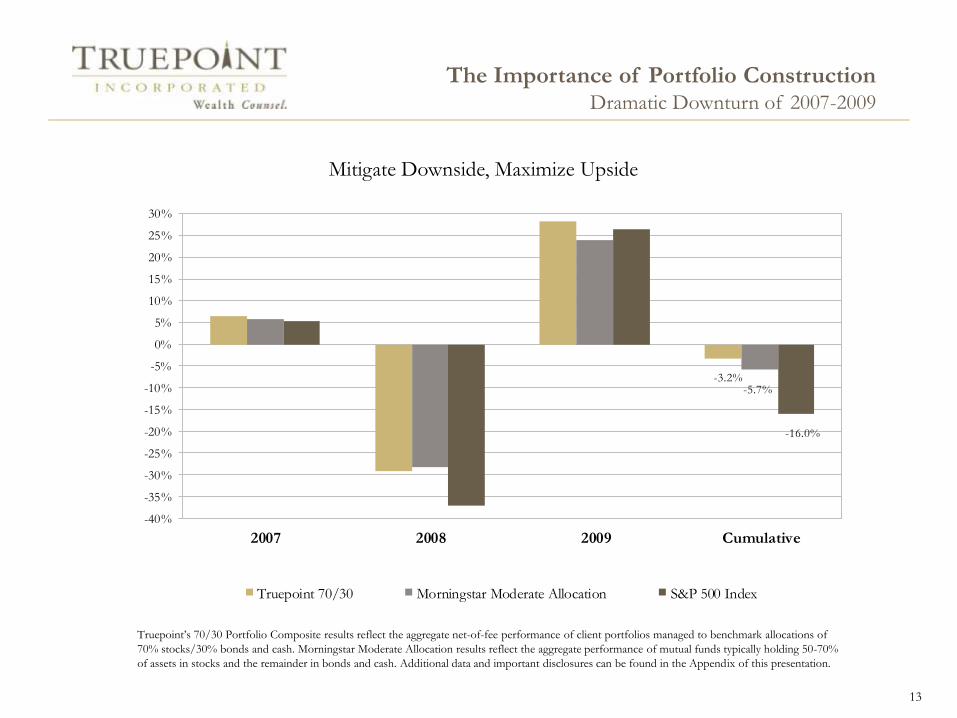

13

-3.2%-5.7%

-16.0%

-40%

-35%

-30%

-25%

-20%

-15%

-10%

-5%

0%

5%

10%

15%

20%

25%

30%

2007 2008 2009 Cumulative

Truepoint 70/30 Morningstar Moderate Allocation S&P 500 Index

Truepoint’s 70/30 Portfolio Composite results reflect the aggregate net-of-fee performance of client portfolios managed to benchmark allocations of

70% stocks/30% bonds and cash. Morningstar Moderate Allocation results reflect the aggregate performance of mutual funds typically holding 50-70%

of assets in stocks and the remainder in bonds and cash. Additional data and important disclosures can be found in the Appendix of this presentation.

Mitigate Downside, Maximize Upside

The Importance of Portfolio ConstructionDramatic Downturn of 2007-2009

14

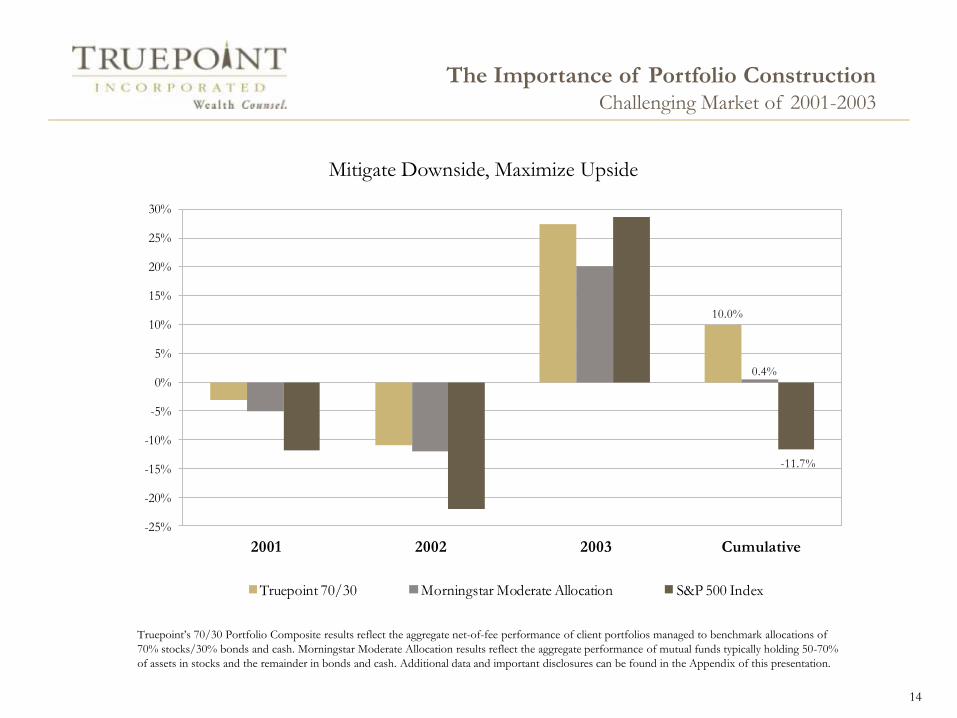

10.0%

0.4%

-11.7%

-25%

-20%

-15%

-10%

-5%

0%

5%

10%

15%

20%

25%

30%

2001 2002 2003 Cumulative

Truepoint 70/30 Morningstar Moderate Allocation S&P 500 Index

Mitigate Downside, Maximize Upside

The Importance of Portfolio ConstructionChallenging Market of 2001-2003

Truepoint’s 70/30 Portfolio Composite results reflect the aggregate net-of-fee performance of client portfolios managed to benchmark allocations of

70% stocks/30% bonds and cash. Morningstar Moderate Allocation results reflect the aggregate performance of mutual funds typically holding 50-70%

of assets in stocks and the remainder in bonds and cash. Additional data and important disclosures can be found in the Appendix of this presentation.