19

Volume 10: Prospects for Real Estate: On Solid Foundations? In co-operation with the Economist Intelligence Unit Barclays Wealth Insights

| Date post: | 20-Aug-2015 |

| Category: |

Business |

| Upload: | the-economist-group |

| View: | 1,292 times |

| Download: | 3 times |

Volume 10: Prospects for Real Estate: On Solid Foundations?

In co-operation with the Economist Intelligence Unit

Barclays Wealth Insights

1

About Barclays Wealth

Written by the Economist Intelligence Unit and commissioned by Barclays Wealth, this tenth volume of Barclays

Wealth Insights looks at investor perceptions of the global real estate market.

It is based on two main strands of research. First, the Economist Intelligence Unit conducted a survey of more

than 2,000 high net worth individuals, with investable assets ranging from $800k to in excess of $48m (£500,000

to in excess of £30m)1. Respondents are based around the globe, with the highest numbers of respondents in the

United States, Hong Kong, India, Singapore, Canada, Spain, Switzerland, the United Arab Emirates, the United

Kingdom and Monaco. The survey took place between August and September 2009.

Second, the Economist Intelligence Unit conducted a series of interviews with economists, senior executives

and real estate experts from around the world. Our thanks are due to the interviewees for their time and insight.

About this report

Barclays Wealth is a leading global wealth manager, and the U.K.’s largest, with total client assets of $221 billion (£134

billion), as of June 30, 2009. With offices in 25 countries, Barclays Wealth serves affluent, high net worth and

intermediary clients worldwide, providing international and private banking, investment management, fiduciary

services, and brokerage.

Barclays Group is a major global financial services provider engaged in retail and commercial banking, credit cards,

investment banking, wealth management and investment management services with an extensive international

presence in Europe, the Americas, Africa and Asia.

With over 300 years of history and expertise in banking, Barclays operates in over 50 countries and employs over 145,000

people. Barclays moves, lends, invests and protects money for over 49 million customers and clients worldwide.

For further information about Barclays Wealth in the Americas, please visit www.barclayswealthamericas.com or

www.twitter.com/barclayswealth.

1. All currency conversions are based on exchange rates as of September 30, 2009, and in some instances are rounded up or down.

ForewordOur focus at Barclays Wealth is entirely on our clients and on the ways in which we can help them to protect,manage, enjoy and pass on their wealth. From the outset, we have invested in thought-provoking researchwhich we hope will give both us and our clients a better understanding of wealth globally.

Working in partnership with the Economist Intelligence Unit (EIU), we have developed the tenth volume ofBarclays Wealth Insights, a series of research reports which aim to provide a definitive picture of what beingwealthy means in the 21st century.

As well as consulting with more than 2,000 wealthy individuals globally, the EIU has worked with a panel ofinternational experts drawn from academia, industry and finance, to provide additional insights and perspectives.

In this report, Prospects for Real Estate: On Solid Foundations?, we examine the global outlook for residentialand commercial real estate markets through the eyes of high net worth investors.

As well as providing a compelling overview of the real estate investment landscape, the report also gives anindication of how investors’ attitudes towards the asset class have evolved since the start of the downturn.

Despite the turmoil, the findings suggest that investors are ready to increase their exposure to residential andcommercial real estate. Their reasons for and means of doing so are particularly interesting and demonstratethe emotional attachment that many investors have to real estate when compared to other forms ofinvestment.

I hope you find this report an informative and entertaining read.

Thomas L. Kalaris Chief Executive Barclays Wealth

32

Our Insights PanelAhmed Al Hatti, Chairman of Cayan Investment and Development

Liam Bailey, Head of Residential Research at Knight Frank

Yolande Barnes, Director of Research at Savills

Sean Brew, Head of Portfolio Asset Management at DTZ

Mark Carpenter, Director of the Property Division at Henderson New Star

Basil Demeroutis, Partner at Capricorn Investment Group

Willie Gething, Executive Chairman of Lennox Investment Management

Rory Gilbert, Head of U.K. High Net Worth, U.K. and Ireland Private Bank at Barclays Wealth

Philip Jeffcock, Real Estate Director at Barclays Wealth

Issam Kabbani, Chief Executive of Landmark SA, an affiliate of Synergy Asset Management

Audrey Klein, Managing Principal at Park Hill Estate, a subsidiary of Blackstone

Angus McIntosh, Partner and Head of Research at King Sturge

Ian McBryde, Director of Property Funds at F&C REIT Asset Management

Mark Meiklejon, Investment Director at Standard Life Investments

Laurent Nouvion, Head of the Rey/Nouvion Family Office in Monaco

David Salusbury, Chairman of the National Landlords Association

We would also like to thank the following individuals for their input:

Charles Beer, Senior Partner in Real Estate Tax at KPMG

Paul Bradley, Spokesperson for the Spanish Property Owners Guild

Sam Chandan, President and Chief Economist of the Faculty of Real Estate at The Wharton School of the University of Pennsylvania

Santosh Rungta, President of the Confederation of Real Estate Developers Associations of India

Greg Davies, Head of Behavioral Finance at Barclays Wealth

Michael Dicks, Head of Research at Barclays Wealth

Wayne Vandenburg, Chairman and CEO of TVO Groupe

Introduction

Although the financial crisis that has led to a severe globaleconomic downturn had many causes, real estate, in theshape of sub-prime loans in the U.S., can be regarded as a key catalyst. At the turn of this century, real estateattracted billions of dollars of investment as homeownersand investors around the world sought to capitalize on anintoxicating asset price boom and on the availability ofcheap credit. But for many, there was a hard landing tocome, and a reminder that, although real estate has beena source of huge new wealth around the world, it has alsoproved to be many investors’ undoing.

There is a temptation to regard real estate as a“straightforward” investment. Unlike other asset classes, it is universal. At some point in our lives, the vast majorityof us invest in bricks and mortar when we buy our ownhomes, so it can seem like a short leap to invest in realestate purely for financial gain. But while direct real estateinvestment may not have the financial complexity ofsome other financial products, it is by no means simple.

As evidence of a gradual economic recovery mounts,investors are once again eyeing real estate markets aftermany have fallen precipitously from earlier highs. Whilefew will have the confidence to call the bottom withcertaintly, a growing number of investors consider thatthe descent has been deep enough to start preparing

for the eventual upturn and are making selectiveinvestments. Indeed, in recent months, some real estatemarkets have bounced back strongly and are appreciatingin value.

This report, the tenth in the Barclays Wealth Insightsseries, examines the outlook for the global residentialand commercial real estate markets through the eyes ofhigh net worth individuals. Based on a major survey and a series of interviews with high-level real estateexperts, the report also looks at the advantages anddisadvantages of real estate investment and explores how investors manage real estate as part of a broaderinvestment portfolio.

54

Executive summaryWealthy investors expect to increase their assetallocation to real estate. Over the next two years,35 percent of respondents plan to increase theproportion of real estate in their portfolios (notincluding their primary residence), while 48 percentplan to maintain their current allocations. The mainreason that investors give for the increase is that theybelieve real estate offers better long-term prospectsthan other asset classes. Investors from the GulfCooperation Council (GCC) states and Canada aremost likely to increase their allocations — by anaverage of 4 percentage points — while Spanishinvestors are the only respondents who expect theiraverage allocation to real estate to fall.

Some investors may already have extremely highexposure to real estate. Almost six out of ten investorsfrom Spain, and just under 30 percent of those fromthe U.K. and India, say that 50 percent or more of theirportfolios are in real estate. Allocation also tends toincrease with wealth: Among those respondents with$48m (£30m) or more in assets, almost 40 percentsay that they have allocated more than half theirportfolio to real estate.

Investors can see opportunities in the real estatemarket, but the scarcity of credit is constraining theiroptions. Following a prolonged downturn in real estatemarkets around the world, high net worth investorsare once again eyeing opportunities in the sector.Three out of four wealthy investors say that residentialreal estate is looking attractive, but 60 percent ofthem say that tight credit conditions are preventingthem from taking the plunge. Respondents are slightlyless sanguine about opportunities in commercial realestate, with 68 percent saying that they are keen toexplore opportunities, but 73 percent of them feelhampered by the high cost of borrowing.

There is growing confidence about the medium-termoutlook for real estate, but prices may have further tofall in the near future. Although they recognize thatcurrent market conditions are throwing up significantinvestment opportunities, high net worth investorsgive a cautious assessment of the prospects for theirown real estate portfolio. Just under half expect anincrease in the overall value of their real estateinvestments over the next two years, while 29 percentexpect no change and 23 percent expect a decrease.Investors from India, Canada and Singapore are mostbullish about the future, while those from Spain areleast optimistic. More broadly, there are doubts aboutthe incipient recovery in real estate prices. Across theten focus markets, fewer than half of respondentsbelieve that prices have reached their lowest point intheir own markets.

A significantly greater proportion of women than menare keen on investing in real estate. When it comes toreal estate, the survey reveals a striking variation inthe attitudes of the two sexes. Nearly half the womensurveyed say real estate is a less risky investment thanstocks, whereas only 37 percent of men agree withthat view. Similarly, while 44 percent of women findbuying real estate more enjoyable than investing inother asset classes, just 28 percent of men feel thesame way. Women also tend to favor investing directlyin bricks and mortar more than men. While 34 percentof men are likely to invest in real estate indirectlythrough a fund, only 14 percent of women wouldprefer to go down that route.

Outside their own countries of residence, mostinvestors consider the U.S. to be the most attractivereal estate market. The U.S. tops the list by somemargin, while the U.K. ranks joint second. In bothmarkets, there have been precipitous price declines,so investors may be reasoning that there are bargainsto be had. However, there is also considerable interestin emerging investment destinations, such as Chinaand India, which are second and fourth on the listrespectively. The appeal of these countries is likely dueto a belief that rapid economic growth and risingwealth will fuel demand for real estate and lead tocapital gains and attractive yields over the long term.

Investors may be somewhat emotional in their approachto managing real estate investments compared withother asset classes. An emotional attachment to bricksand mortar — often stemming from the central rolethat homes play in people’s lives, but also due tofactors like prestige and location — can mean thathigh net worth investors are often unwilling to sell realestate at short notice and, therefore, they may be lessrigorous in measuring its performance as an assetclass. Investors also may not be taking advantage ofthe diversification possibilities within real estate as anasset class. For example, just 29 percent hold indirectreal estate investments, such as mutual funds and realestate investment trusts, when these can offer arelatively liquid way to gain exposure to real esateacross a wide range of sub-sectors and markets.

76

SectionOne: Trying timesfor real estate investors

Real estate is a significant source and store of wealth for highnet worth individuals around the world, a major destinationfor their capital and, in many cases, a source of hugepleasure and enjoyment. It is a long-term investment thatoffers the potential for income, capital gains and a hedgeagainst inflation.

But for investors in most areas of global real estate,the past few years have been a searing experience. Inthe U.S., the S&P/Case-Shiller Home Price Index,which is a composite of single-family home priceindices for the nine U.S. Census divisions, fell by 32percent from its high in the second quarter of 2006 tothe first quarter of 2009. More recently, however, ithas shown some signs of stabilizing, rising slightly inthe second quarter of 2009 for the first time in threeyears. The Federal Housing Finance Agency’s monthlyHouse Price Index, which is calculated using homesales price information from mortgages that havebeen sold to or guaranteed by Fannie Mae or FreddieMac, showed that in August, prices were 0.3 percentlower than in the month before and 3.6 percent lowerthan a year before. As of August, prices were 10.7percent below the April 2007 peak.

In the U.K., the Nationwide House Price Index fell from367 in the fourth quarter of 2007 to 298.7 in the firstquarter of 2009, a drop of 19 percent. Again, there wasstabilization in the second quarter of the year. That

stabilization is also seen in the August House PriceIndex put out by the Department for Communities and Local Government. It found that prices rose by0.5 percent from July to August; however, Augustprices were still down 5.6 percent from theyear before.

Following the trend in the U.S. and Europe, the realestate market in Dubai, which had enjoyed a spectacularboom over the past three years, has also suffered.According to Colliers International, a global affiliation ofindependently owned real estate services firms, therewas a year-on-year decline of 48 percent between thesecond quarter of 2008 and the second quarter of 2009.

Other regions of the world have fared somewhatbetter. During 2009, house prices have been boomingin China, for example, thanks largely to a massivegovernment stimulus package. According to theNational Bureau of Statistics, house prices rose bytwo percent from July to August 2009 in the nation’sbiggest cities, double the increase from June to July.

98

There are concerns, however, that the massiveliquidity that has been injected into the market couldcause an asset price bubble to form, as loosemonetary conditions help support unsustainableincreases in the Western world.

If prices are starting to stabilize in some residentialmarkets, the picture for commercial real estate is moremixed. With unemployment continuing to rise in manymarkets, albeit at a slower pace, demand forcommercial real estate in general is likely to remainmuted and lag behind a broader economic recovery.

The IPD (Investment Property Databank) GlobalProperty Index, which measures the combinedperformance of commercial real estate markets in 23countries, fell significantly in U.S. dollar terms during2008, showing returns of -10.1 percent compared with16 percent in 2007. The U.K. fared particularly badly,showing a return of -22.1 percent in 2008. However,demand for well-let, prime real estate is starting torecover in some places, with the IPD U.K. MonthlyProperty Index rising by 0.2 percent in August, the firsttime it has been positive in 26 months.

office started by the co-founder of eBay), suggests anoptimum figure of between six percent andeight percent, while Laurent Nouvion, who runs theNouvion family office in Monaco and has a strongpreference for real estate assets, holds up to 50 percent.

“There is no doubt that a certain amount of real estatecan provide return enhancement and diversificationbenefits in most investors’ portfolios,” says PhilipJeffcock, Director of Real Estate at Barclays Wealth.“The proportion of wealth allocated to real estateshould be reasonable given investors’ liquidityrequirements, and their ability to deal with thepossibility that they might have to sell an asset withpoor liquidity when things go bad.”

The average allocation to real estate of 28 percentamong the survey respondents conceals considerablevariation in allocations across regions. Spanishinvestors, for example, have the highest levels of realestate holdings out of the ten focus markets for thesurvey. On average, they allocate 51 percent of theirportfolio to real estate, while 59 percent haveallocations to real estate of 50 percent or more. Spainhas long had a strong cultural affinity with real estateownership and the government offers generous taxrelief on mortgage payments. It has also been a Meccafor foreign investors and speculators, especially duringthe housing boom of 1995 to 2007, which saw pricesrise by 300 percent.

What is the current approximate allocation to real estate in your overall investment portfolio(not including the primary real estate in which you live)?

Chart 2 – Average real estate holdings as a percentage of overall investment portfolio, by country

U.S.

U.K.

Canada

Singapore

Monaco

Spain

GCC

India

Switzerland

Hong Kong

Current holdings

Projected holdings in two years’ time

Source: Economist Intelligence Unit Survey, September 2009

23% 25%

28% 31%

25% 28%

23% 25%

25% 29%

17% 18%

26% 29%

32% 35%

51% 36%

33% 37%

-25%

-20%

-15%

-10%

-5%

0%

5%

10%

15%

20%

Switzerland

UK

USA

Spain

Canada

2006 2007 2008

Source: IPD national indexes (data for respective countries), September 2009

25%

Chart 1 – Total return on all real estate types between 2006-2008

The picture for the real estate investment trust (REIT)market is also mixed. Since the second quarter of 2009,the FTSE NAREIT Equity REIT index, which tracks U.S.REITs, has shown strong returns, after falling heavilyafter the collapse of Lehman Brothers. The indexdropped by more than two-thirds between mid-September 2008 and early March 2009, but rose by 30percent in the second quarter and more than 40percent in the third quarter. The pick-up inperformance has been fueled by a broader recovery inequity markets and a wave of equity issuances, as theindustry recapitalizes itself, often to take advantage ofdistressed assets in the real estate market. However,the index is still about 25 percent lower than it was ayear ago and there are many challenges ahead for themarket, including weak balance sheets and loomingdebt maturities.

Preference for real estate persists

Although the real estate market as a whole remainshighly uncertain, high net worth investors will continueto see the asset class as an important part of theirportfolio. Among the more than 2,000 high net worthinvestors surveyed for this report, the averageproportion of their portfolio allocated to real estate is28 percent, not including their main residence. Ofcourse, there is no one “right” allocation to real estatefor all investors. An investor’s own ideal position willdepend on a host of factors, including his or herinvestment horizon, risk appetite, location, age andpersonal preferences. Real estate experts questionedfor this report expressed a range of opinions aboutallocation. Basil Demeroutis, a Partner at CapricornInvestment Group (a multi-family

Investors from Switzerland have the lowest averageallocation to real estate, at 17 percent, and only14 percent have allocations of 50 percent or greater.Those from the U.S. and Monaco also have relativelylow allocations at 23 percent. In the case of Switzerlandand Monaco, which are both long-established realestate markets, there is some evidence that moreexperienced investors stayed out of the market asprices soared. “Although we have been investing in realestate for some 50 years, we stopped investing in 2006and 2007,” confirms Mr. Nouvion. “Prices were simplyfar too high. They had lost all sense of reality.”

The survey suggests that, in general, allocation to realestate increases with wealth. For example, investorswith assets of greater than £30m have an averageallocation to real estate of 37 percent, compared with36 percent for those with wealth between $16m and$48m (£10m and £30m), 31 percent for those withwealth between $2m and $16m (£1m and £10m), and23 percent for those with assets between $800k and$2m (£500k and £1m).

1110

Barclays Wealth Case Study

Contrarian view creates world of opportunities CNL Financial Group, a privately held real estateinvestment company based in Orlando, Florida, hasformed or acquired companies with more than $23billion in assets and has successfully used a“contrarian” investment approach for more than 35years. Launched in 1973 by founder and CEO JamesM. Seneff Jr., CNL aims to identify opportunities inundervalued real estate markets and protect againstlooming threats in markets that are performing well.

CNL was aggressive in buying discounted hotelproperties when the travel market suffered a sharpdownturn from the events of September 11, 2001.Conversely, CNL’s contrarian view served thecompany’s investors well in 2006 and 2007, whenCNL foresaw risks in the markets and sold over $15billion of real estate assets.

Now CNL views the world and opportunities for realestate investors very differently.

“There is a lot of pessimism right now, but we believethere are tremendous global opportunities in realestate, particularly because of complexities inadjusting markets,” says Mr. Seneff. “We believe thebest investment opportunities currently reside in the

United States, but we also see opportunitiesemerging elsewhere.”

For example, according to Mr. Seneff, in China therewill continue to be a significant population shift fromrural to urban areas. So CNL has created apartnership with Macquarie Group to find attractiveinvesting opportunities. The new Real EstateInvestment Trust (REIT), CNL Macquarie GlobalGrowth Trust, is focused on growth-oriented assetsaround the world. CNL’s acquisition strategy willtarget assets which are well located and designed,and have fundamental growth characteristics, buthave fallen out of favor or been impacted due to thecredit crunch.

One issue facing many wealthy investors is thedecision over how to best allocate the real estateportion of their portfolio. “As an individual has moreassets, there is a shift towards broader assetallocation to include real estate,” says Mr. Seneff.However, directly investing in commercial orresidential real estate exposes an investor to singlereal estate risk and requires maintenance of theasset whereas investing in a REIT or REITS canprovide a diversified real estate allocation.

What is the current approximate allocation to real estate in your overall investment portfolio (not including theprimary real estate in which you live)?

$800k-$2m

$2m-$16m

$16m-$48m

Over $48m

Current portfolio

Two years’ time

Source: Economist Intelligence Unit Survey, September 2009

23% 26%

31% 32%

36% 38%

37% 40%

Chart 3 – Weighted average allocation, by wealth band

It is important that investors hold a range of assetclasses, not just real estate, in order to have a diversifiedportfolio. Diversification is important for two reasons.2

First, it is difficult to predict which asset class will be thebest performer each year, so investors should hedgetheir bets. Second, some asset classes’ returns are moreclosely correlated than others — meaning their returnstend to go up and down in tandem — so it is vital thatinvestors have asset classes with differing characteristicsthat will outperform in different market conditions.Diversification helps raise returns for a given level of risk.

Real estate has generally been considered to have alow correlation with both equities and bonds,although correlations do fluctuate slightly over thecourse of an economic cycle. However, in the financialcrisis of 2008 and the subsequent economicdownturn, correlations spiked and many asset classesexperienced substantial losses. So whilediversification can help lower risk over the long term,there is still the potential for many asset classes tosuffer at the same time during short-term crises.

Upping the ante?

With some major global real estate markets stabilizingafter significant declines in value, investors areconsidering whether now may be the right time toincrease their allocation. In general, high net worthinvestors questioned for this survey plan a slightincrease to their overall allocation to real estate overthe next two years. On average, allocation will increasefrom 28 percent to 30 percent. For those who plan toincrease their allocation, the main reason cited is thatthey believe that real estate offers better long-termprospects than other asset classes. This suggestscontinuing uncertainty about the trajectory of financialassets and a desire for more tangible, “straightforward”investments after the turmoil of the financial crisis,which many people perceive to have been caused bycomplex financial instruments.

2. Diversification does not guarantee against loss.

Which of the following factors have been most influential in determining your increased allocation to real estate?

Chart 4 – Key reasons for increasing allocation to real estate, all respondents

0 15 30

Source: Economist Intelligence Unit Survey, September 2009

7.6%

15.2%

15.5%

17.3%

20.7%

23.3%

25.4%Belief that property has better long-term prospects than other asset classes

Desire to invest in an asset class that reflects my long-term time horizons

Desire to avoid “complex” financial investment products

Media coverage of “green shoots” of economic recovery

Belief that recent price falls mean that property is now undervalued

Concern about stability of financial investment providers

Desire to diversify overall investment portfolio

12 13

Breaking the survey results down by region, there is aremarkable consistency of opinion, with investors fromnine out of the ten markets expecting to increase theirallocation by between 1 percent and 4 percent. Themajor exception to this trend is Spain, where theaverage allocation for investors will fall by 15 percent,according to the survey. More dramatically, perhaps,13 percent of Spanish investors intend to reduce theirholdings of real estate to zero, bringing the total withno exposure to the real estate market from 15 percentto 28 percent. This striking finding suggests acontinuing lack of confidence in the Spanish realestate market, even after significant price declines.Asesores Financieros Internacionales (AFI) forecaststhat Spanish real estate prices will fall by 30 percentfrom peak to trough and that the market will not turnpositive until at least 2011.

A key reason for this gloomy forecast is a glut ofsupply. “There are over one million unsold newproperties in Spain which will need to be cleared outprior to any recovery,” says Paul Bradley, aspokesperson for the Spanish Property Owners Guild.“That will take at least another three to four years. Sothe ideal time to return is just prior to these unsoldproperties being cleared out, when new developmentbegins again.”

Investing with a home bias

Just over three-quarters of the investors questioned forthe survey invest primarily in their domestic market. Butasked about the overseas country where they saw thegreatest potential for returns, two interesting themesemerged. The first of these is that the market regardedas the most promising, by some margin, is the U.S.There is clearly a view that recent price declines, aweaker currency and the long-term prospects for theU.S. economy offer significant opportunities. Similarreasons are likely to influence the selection of the U.K.as the third most promising market.

Liam Bailey, Head of Residential Research at KnightFrank, a real estate agent, notes that the prime realestate in London has begun to see strong buyinginterest. “We have seen an increase in registered interestfor prime and super-prime real estate, which is usuallyan indication of coming price increases,” he says.

“There are over one million unsold

new properties in Spain which

will need to be cleared out prior to

any recovery.”

It is also clear that investors perceive opportunities forbargains amidst the fall-out from the crisis. The beliefthat recent price declines mean that real estate is nowundervalued is the second most important reason givenfor increasing allocation to real estate. Nonetheless,experts say that investors have, in general, become

much more discerning. “At the height of the bubble,many buyers lost sense of basic considerations:location, quality of building, reasonable financing andso on. However, today investors are much morediscerning; the real estate has to be exactly right,” saysYolande Barnes, Director of Research at Savills.

What do you expect to be the average percentage change in your real estate portfolio over the next two years?

Chart 5 – Expected average change (%) in real estate portfolio over next two years, by country

Source: Economist Intelligence Unit Survey, September 2009

U.S.

U.K.

Canada

Singapore

Monaco

GCC

Spain

India

Hong Kong

Switzerland 1%

2%

3%

4%

3%

2%

4%

3%

3%

-15%

Barclays Wealth Case Study

The long-term winning assetWoodbury Corporation, a 90-year-old family-ownedreal estate business, focuses on real estatedevelopment and management in the Western UnitedStates. They deem themselves “investor” rather than“merchant” developers. Based in Utah, they began bybuying and renovating homes and reselling them.Today, Woodbury controls over ten million square feetof retail, office, and hotel real estate space in a U.S.real estate portfolio worth more than $1.2 billion.

President Rick Woodbury sees global real estate as amarket with secular growth trends, “Real estate is agreat long term investment. Over the short andmedium terms real estate values may fluctuate;however, because land is finite, as the worldpopulation increases, supply and demand mandatesthat the value of well-conceived and located projectswill increase over the long term, even greater thanthe rate of inflation. The question is how and whenyou play and how much staying power you have.”

“In valuing real estate, we are not fancy. We focus onthe basics of location, layout, construction quality, andreplacement cost as well as true cash flow,” says

Woodbury. “We ensure stability by limiting our debtleverage and diversifying in enough properties andtenants so that no two or three properties have asignificant negative impact if the unexpected happens.”

Woodbury believes that real estate in the U.S. is nearthe bottom, creating ample opportunity for investors.“Over the last decade some have invested recklesslybecause of easy money and a misperception thatreal estate had little risk,” says Woodbury.“Commercial real estate became overvalued, butadjustments have taken place and are continuing totake place. We are excited about the currentopportunities,” Woodbury continues.

To capitalize on the current market opportunity on alarger scale the company is partnering with like-minded investment partners, such as the family officesof John R. Miller and Jonathan W. Bullen.3 By combiningefforts, Woodbury is able to deploy more capital acrossmore assets enhancing the already attractive riskreturn relationship.

3. For a quarter of a century, the Salt Lake City, Utah-based family offices have managed the wealth of the Bullen and Miller families. They initially gained real estateinvestment experience in the late 1980s. Partnering with a third-party operator, the family offices capitalized on the U.S. Savings & Loan crisis and subsequentgovernment Resolution Trust Corp. bailout in the 1990’s by acquiring multifamily apartments and commercial real estate at depressed prices. The value strategy yieldeda portfolio that is currently comprised of more than 9,000 apartment units and over two million square feet of office space located across the Western United States.

1514

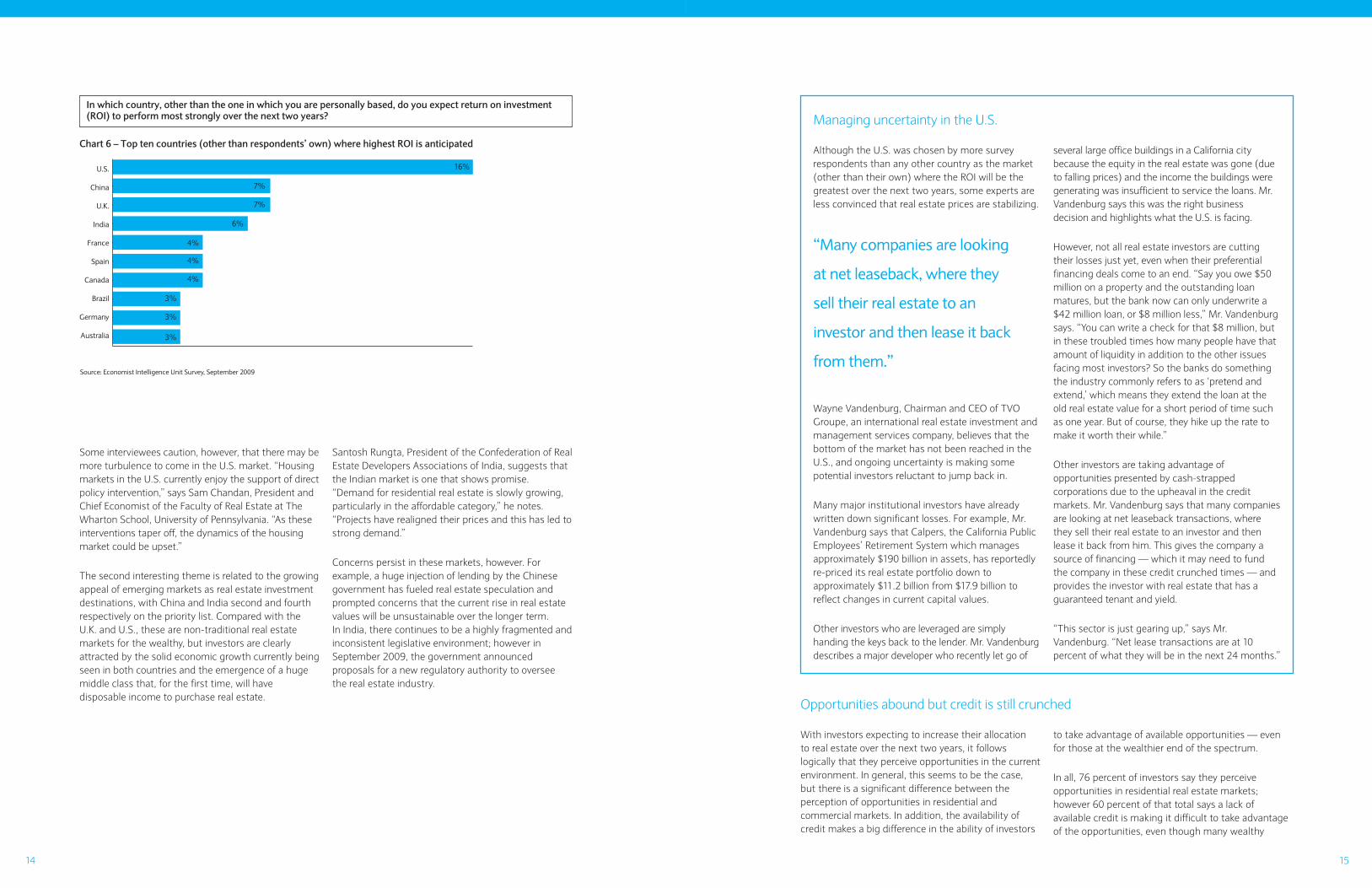

Managing uncertainty in the U.S.

Although the U.S. was chosen by more surveyrespondents than any other country as the market(other than their own) where the ROI will be thegreatest over the next two years, some experts areless convinced that real estate prices are stabilizing.

Wayne Vandenburg, Chairman and CEO of TVOGroupe, an international real estate investment andmanagement services company, believes that thebottom of the market has not been reached in theU.S., and ongoing uncertainty is making somepotential investors reluctant to jump back in.

Many major institutional investors have alreadywritten down significant losses. For example, Mr.Vandenburg says that Calpers, the California PublicEmployees’ Retirement System which managesapproximately $190 billion in assets, has reportedlyre-priced its real estate portfolio down toapproximately $11.2 billion from $17.9 billion toreflect changes in current capital values.

Other investors who are leveraged are simplyhanding the keys back to the lender. Mr. Vandenburgdescribes a major developer who recently let go of

several large office buildings in a California citybecause the equity in the real estate was gone (dueto falling prices) and the income the buildings weregenerating was insufficient to service the loans. Mr.Vandenburg says this was the right businessdecision and highlights what the U.S. is facing.

However, not all real estate investors are cuttingtheir losses just yet, even when their preferentialfinancing deals come to an end. “Say you owe $50million on a property and the outstanding loanmatures, but the bank now can only underwrite a$42 million loan, or $8 million less,” Mr. Vandenburgsays. “You can write a check for that $8 million, butin these troubled times how many people have thatamount of liquidity in addition to the other issuesfacing most investors? So the banks do somethingthe industry commonly refers to as ‘pretend andextend,’ which means they extend the loan at theold real estate value for a short period of time suchas one year. But of course, they hike up the rate tomake it worth their while.”

Other investors are taking advantage ofopportunities presented by cash-strappedcorporations due to the upheaval in the creditmarkets. Mr. Vandenburg says that many companiesare looking at net leaseback transactions, wherethey sell their real estate to an investor and thenlease it back from him. This gives the company asource of financing — which it may need to fundthe company in these credit crunched times — andprovides the investor with real estate that has aguaranteed tenant and yield.

“This sector is just gearing up,” says Mr.Vandenburg. “Net lease transactions are at 10percent of what they will be in the next 24 months.”

“Many companies are looking

at net leaseback, where they

sell their real estate to an

investor and then lease it back

from them.”

U.S.

China

U.K.

India

France

Spain

Canada

Brazil

Germany

Australia

Source: Economist Intelligence Unit Survey, September 2009

7%

16%

7%

6%

4%

4%

4%

3%

3%

3%

In which country, other than the one in which you are personally based, do you expect return on investment(ROI) to perform most strongly over the next two years?

Chart 6 – Top ten countries (other than respondents’ own) where highest ROI is anticipated

Some interviewees caution, however, that there may bemore turbulence to come in the U.S. market. “Housingmarkets in the U.S. currently enjoy the support of directpolicy intervention,” says Sam Chandan, President andChief Economist of the Faculty of Real Estate at TheWharton School, University of Pennsylvania. “As theseinterventions taper off, the dynamics of the housingmarket could be upset.”

The second interesting theme is related to the growingappeal of emerging markets as real estate investmentdestinations, with China and India second and fourthrespectively on the priority list. Compared with theU.K. and U.S., these are non-traditional real estatemarkets for the wealthy, but investors are clearlyattracted by the solid economic growth currently beingseen in both countries and the emergence of a hugemiddle class that, for the first time, will havedisposable income to purchase real estate.

Santosh Rungta, President of the Confederation of RealEstate Developers Associations of India, suggests thatthe Indian market is one that shows promise.“Demand for residential real estate is slowly growing,particularly in the affordable category,” he notes.“Projects have realigned their prices and this has led tostrong demand.”

Concerns persist in these markets, however. Forexample, a huge injection of lending by the Chinesegovernment has fueled real estate speculation andprompted concerns that the current rise in real estatevalues will be unsustainable over the longer term. In India, there continues to be a highly fragmented andinconsistent legislative environment; however inSeptember 2009, the government announcedproposals for a new regulatory authority to oversee the real estate industry.

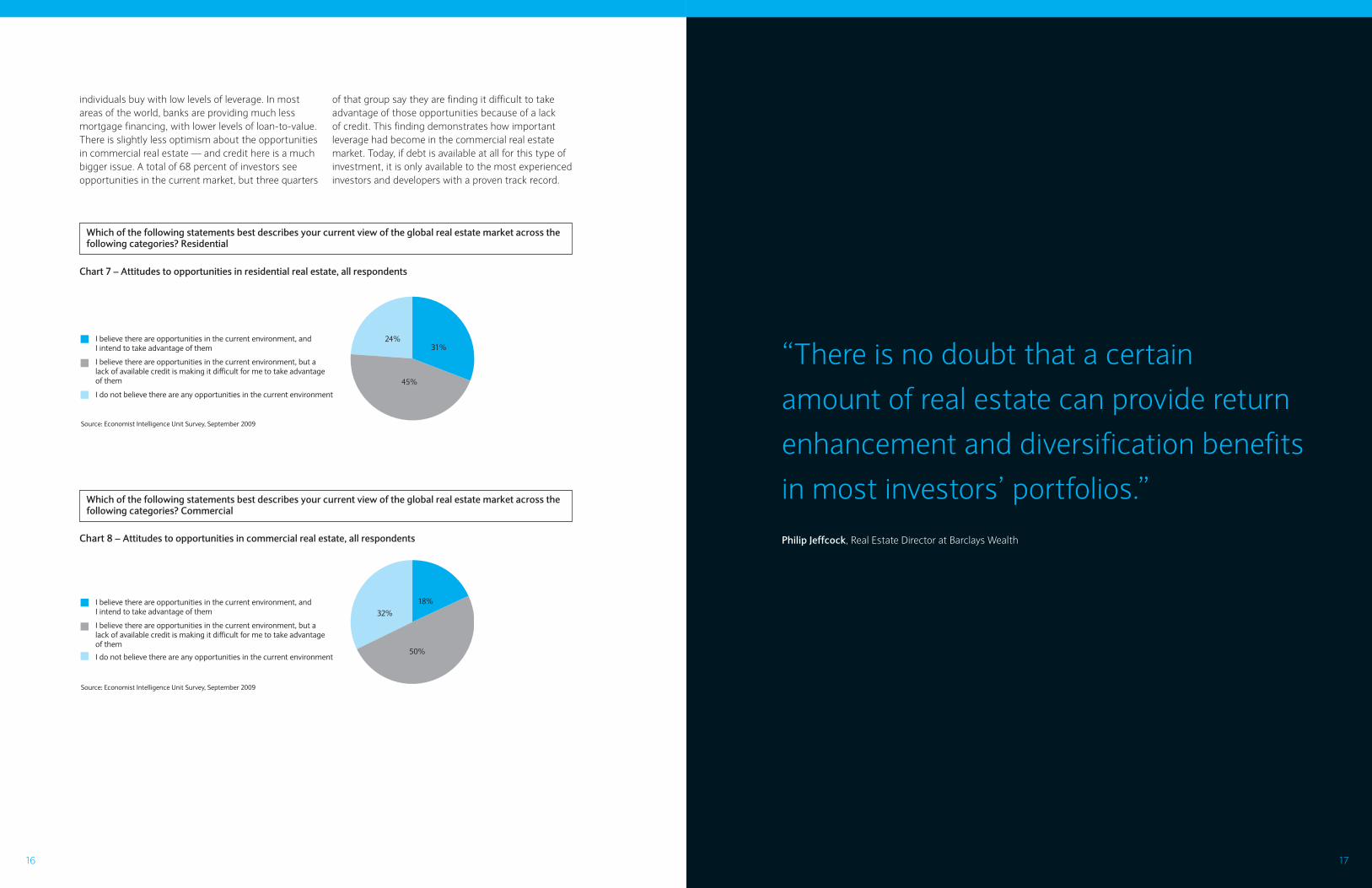

With investors expecting to increase their allocation to real estate over the next two years, it followslogically that they perceive opportunities in the currentenvironment. In general, this seems to be the case,but there is a significant difference between theperception of opportunities in residential andcommercial markets. In addition, the availability ofcredit makes a big difference in the ability of investors

to take advantage of available opportunities — evenfor those at the wealthier end of the spectrum.

In all, 76 percent of investors say they perceiveopportunities in residential real estate markets;however 60 percent of that total says a lack ofavailable credit is making it difficult to take advantageof the opportunities, even though many wealthy

Opportunities abound but credit is still crunched

1716

Which of the following statements best describes your current view of the global real estate market across thefollowing categories? Commercial

I believe there are opportunities in the current environment, and I intend to take advantage of them

I believe there are opportunities in the current environment, but a lack of available credit is making it difficult for me to take advantage of them

I do not believe there are any opportunities in the current environment

24%31%

45%

Source: Economist Intelligence Unit Survey, September 2009

I believe there are opportunities in the current environment, and I intend to take advantage of them

I believe there are opportunities in the current environment, but alack of available credit is making it difficult for me to take advantage of them

I do not believe there are any opportunities in the current environment

32%18%

50%

Source: Economist Intelligence Unit Survey, September 2009

individuals buy with low levels of leverage. In mostareas of the world, banks are providing much lessmortgage financing, with lower levels of loan-to-value.There is slightly less optimism about the opportunitiesin commercial real estate — and credit here is a muchbigger issue. A total of 68 percent of investors seeopportunities in the current market, but three quarters

of that group say they are finding it difficult to takeadvantage of those opportunities because of a lack of credit. This finding demonstrates how importantleverage had become in the commercial real estatemarket. Today, if debt is available at all for this type ofinvestment, it is only available to the most experiencedinvestors and developers with a proven track record.

Chart 8 – Attitudes to opportunities in commercial real estate, all respondents

Which of the following statements best describes your current view of the global real estate market across thefollowing categories? Residential

Chart 7 – Attitudes to opportunities in residential real estate, all respondents

“There is no doubt that a certain

amount of real estate can provide return

enhancement and diversification benefits

in most investors’ portfolios.”

Philip Jeffcock, Real Estate Director at Barclays Wealth

1918

The importance of local knowledge

Synergy Asset Management is a Geneva-basedfamily office that manages money for several highnet worth families in the Middle East and Europe.In 2008, Synergy, together with some privateinvestors, set up the Landmark Real Estate Fund, aSwiss-based real estate investment fund that aims toprovide solid, low-risk, steady returns in commercialand residential investment opportunities inSwitzerland and other parts of Europe.

Issam Kabbani, Chief Executive of Landmark, is astrong believer that real estate should be a key part of an investor’s portfolio as part of a medium to long-term investment strategy. “Overall, we recommendthat investors hold between 20 and 30 percent oftheir capital in yield-bearing real estate assets asopposed to new real estate developments. Wepropose a mix between residential and commercialproperties yielding between four percent andeight percent in exceptional cases. Investors who canafford more risk and a higher return can have theoption of participating in new developments, yieldingbetween 25 percent to 50 percent on capital.”

Over the past year, Mr. Kabbani has noticed a hugeincrease in investor interest in Swiss real estate, aspart of the flight to quality. “It was interesting tosee that while many other markets were affected by the crisis, the Swiss market came off quitelightly. In Switzerland, we hardly registered any drop in prices — on the contrary, we have morebidders than before on properties that were for sale than we normally would have.”

Today, however, Mr. Kabbani thinks investors havebecome much more prudent. “I think following thecrash many investors have gone back tofundamentals,” he says. “Real estate is a great asset,as long as you respect the fundamentals of location,quality of construction and sensible leveraging. Butthese were all forgotten during the bubble.”

Mr. Kabbani places a huge emphasis on theimportance of local information and local partners.“On a given block in Geneva, you might have one ortwo buildings that are always in demand and generatea great yield but 50 yards down the street it doesn’twork and it’s completely different. This is true in allreal estate markets. You need to have local alliances,otherwise you are exposing yourself to big risks.”

International investors also need to be aware of the impact of currency fluctuations. For example,dollar-based investors buying in Switzerland, whodid not hedge their currency exposure, will havebeen hurt badly in the past year by the depreciationof the CHF.

“Real estate is a great asset,

as long as you respect the

fundamentals of location,

quality of construction and

sensible leveraging.”

Since January 2008, has the market value of your real estate portfolio increased and do you expectit to do so in the next two years?

Chart 9 – Percent of respondents whose portfolios have increased/are projected to increase in value, by country

U.S.

U.K.

Canada

Singapore

Monaco

Spain

GCC

India

Switzerland

Hong Kong

23%

44%

40%

39%

15%

29%

35%

48%

34% 49%

52%

56%

33%

27%

41%

53%

55%

50%

January 2008 to present

Over next two years

Source: Economist Intelligence Unit Survey, September 2009

23% 45%

In general, there is guarded optimism among the highnet worth respondents that their real estate portfoliowill increase in value over the next two years. Just underhalf of respondents expect the value of their portfolio toincrease, but only 23 percent expect a decrease, withthe remainder expecting no change. Investors fromCanada, Singapore and India are most bullish about thefuture; those from Spain and the GCC least so.Interestingly, investors from the GCC are also most likely

to increase their allocation to real estate. This suggeststhat they may have a longer time horizon, and do notnecessarily expect prices to rise within the short tomedium-term. Of course, an increase in the value of aportfolio could be driven by two factors: first, the valueof properties could be rising; but second, investorscould be adding new properties to their portfolio, whichour figures on allocation suggest could be the case formany individuals.

Aside from the availability of credit, investors need tobe careful how they use leverage in their real estateinvestments, according to Mr. Jeffcock. “You areadding risk to what is already a very concentrated riskscenario,” he says. “You need to be careful that therisk-return relationships of your real estate portfoliomatch those of the rest of your portfolio. If you canreduce the level of leverage then you reduce the riskand you can therefore focus more on the returns.”

Another hurdle preventing investors from takingadvantage of current opportunities is the expectation

gap between buyers and sellers — in other words,sellers still expect higher prices than buyers areprepared to pay. “What’s happened in the past threemonths is a lot of people have suddenly woken up and decided to buy some real estate,” says AngusMcIntosh, a Partner and Head of Research at KingSturge. “But the problem is that now nobody wants tosell. So whereas there was quite a lot of stock aroundlast Christmas and few buyers, now there are quite afew buyers and very little prime stock. The market isactive for the best buildings; secondary investmentsare still very difficult to sell.”

2120

Section Two: Assessingthe asset class

Direct residential real estate has many characteristics thatset it apart from other, more traditional asset classes. Formany it seems to be a very long-term investment that ismeasured over decades rather than years, although thatmay have been forgotten by some during the real estatebubble. It is tangible and, to many investors, its permanenceoffers a perceived security that they may feel is lacking withother asset classes.

But there are significant challenges with holding

residential real estate in a portfolio that can cause

problems for investors. “People have a natural affinity

for real estate,” says Rory Gilbert, Head of U.K. High Net

Worth, U.K. and Ireland Private Bank at Barclays Wealth.

“But investors need to be wary, as this is an inefficient

market with low price transparency, illiquidity and high

transaction costs.”

When asked about the main advantages of holding

residential real estate in their portfolio, survey

respondents point to the potential for income through

rental as the biggest attraction. This was a finding that

surprised many of the experts questioned for our in-

depth interviews. In general, residential real estate

offers relatively low levels of returns, especially when

compared with commercial real estate. The consensus

of the experts was that residential real estate is best

seen as a source of capital growth, rather than

of income.

2322

“Real estate is best seen as a composite good,” saysMs. Barnes. “It provides a range of different functionsfor a real estate buyer. Clearly it is an investment asset.And there is an element of utility as people live inthese properties. But there are also elements oflifestyle, luxury and fashion that play a role in thedecision. Buyers tend to have a strong, often intense,emotional connection with their houses, even if it isnot their principal residence.”

This emotional relationship with real estate inevitablyimpacts the way investors deal with their real estateinvestments. According to Mr. Gething, there are severalways this can play out. “Buyers may be inclined to buysomewhere they find very attractive to them personallywhich may or may not be a good investment. They maypay more for it than a dispassionate buyer. And theymay not sell it when a return is offered that adispassionate investor would be happy to take. Theunshakeable rule maintained by the best real estateinvestors is never to fall in love with an asset.”

The risk of holding on to an asset too long is one thatemerges from the survey. Asked how they manage realestate compared with other investments, just33 percent say that their willingness to sell would begreater than with another asset class shouldcircumstances change. In other words, while investorsmay offload equities and other asset classes shouldthe need arise, they are less likely to do the same with

residential real estate — partly because it is a long-term, illiquid investment, but also partly because theydevelop an emotional attachment to it. Similarly, thesurvey found that just 18 percent of respondentswould hold real estate in their portfolios for less timethan other asset classes, supporting the idea of realestate as a long-term commitment.

For most people, buying a house is one of the biggestfinancial investments that they make, yet investorsoften pay less attention to this decision than theywould do with other comparable investments. Thesurvey suggests that even highly sophisticated privateinvestors may take a relatively simple approach tomanaging their residential real estate investments: they often make decisions independently of any adviceor, if they do seek a second opinion, they rely onfriends and family or estate agents. Professional,independent advice, according to the survey, is notalways sought, which suggests that investors could domore to improve the rigor of their investment process.

For example, almost one-third of investors rely onadvice from their family and friends (although they arenot the most widely consulted source of advice).Friends can be very influential on buying decisions, ifnot always from a financial perspective. “For manywealthy real estate buyers, the opinion and values oftheir peers matter a lot,” says Ms. Barnes.

“Yields on residential real estate will never compete withcommercial real estate,” says Willie Gething, ExecutiveChairman of Lennox Investment Management, anindependent adviser that helps wealthy investors buyproperties. “Today in central London, for example, youget yields of maybe four percent for prime real estate.You don’t buy residential real estate for income. Theyield merely helps you to service sensible levels of debt.Its real potential is for capital appreciation.”

Indeed, this is seen by survey respondents as thesecond biggest advantage of investing in real estate,followed by the long-term track record of residential realestate. Demographic pressures and demand for landwill, over the long term, continue to support residentialreal estate as an investment, believe some interviewees.“People are always going to need somewhere to live,”says David Salusbury, Chairman of the NationalLandlords Association. “And they aren’t making landanymore, as the saying goes. So I personally don’tbelieve as a landlord, that if you do it properly over thelong run, you’re going to go far wrong.”

There is no doubt that residential real estate offers somediversification possibilities, but many experts believe thatinvestors do not always think about this characteristic assystematically as they might with other assets. “We very

often see wealthy investors who have portfolios with anunhealthy concentration of one or two prestigeproperties, a Manhattan penthouse or house in Belgravia,which often accounts for a large proportion of their realestate holdings,” says Mr. Demeroutis. “These investorswould be better to spread their investment acrossdifferent markets and asset types.”

He suggests that investors should consider low-incomeor student housing across a spread of geographicallocations. “Your real estate investment doesn’t have tonecessarily look like somewhere you would like to live.In fact, that can be a dangerous investment philosophy.There are big concentration issues when you invest inone very expensive real estate in terms of risks: fire,environmental, market and so on.”

A personal relationship

This highlights a broader point, whereby investing in realestate is about much more than a pure financialinvestment. Residential real estate has a special place inprivate investors’ hearts, as well as their portfolios. For awealthy investor, residential real estate is seldom treatedsimply as an asset.

Which of the following factors do you consider to be most attractive about holding real estate investmentsin your portfolio?

Potential for income through rental

Potential for capital gains

Long-term performance track record

Overall portfolio diversification

Stability of investment

“Tangibility” of bricks-and-mortar investments

Ability to enjoy properties as primary and secondary homes

Ability to finance investments through debt

Hedge against inflation

Emotional attachment to bricks and mortar

Tax treatment of property

Attractive valuations in current market

Relatively low correlation with other asset classes

Source: Economist Intelligence Unit Survey, September 2009

39%

28.7%

28.4%

22.5%

19.9%

19.4%

18.5%

18.5%

14.8%

14.5%

14%

7.9%

5%

Chart 10 – Key advantages of investing in residential real estate, all respondents

Which of the following sources of advice do you turn to in order to assist you with your real estate investments?

Property consultant

Private bank/wealth manager

Estate agent

Friends and family

Commercial bank

Peers

Business partners

Accountant

Family office

Law firm

Other

Source: Economist Intelligence Unit Survey, September 2009

5.3%

7.9%

8.9%

11.9%

15.6%

15.6%

23.5%

32.1%

36.2%

38.2%

40.5%

Chart 11 – Sources of advice on real estate investment, all respondents

2524

Other interviewees suggest that investors may be lessthan rational in their buying decisions. “I think realestate as an asset class is where the worst elements ofbehavioral finance rear their head,” saysMr. Demeroutis. “Vanity is a huge factor in the purchaseof residential real estate, although buyers are reluctantto admit this. There are clearly so many other reasonsthat people buy real estate besides as an investment,although they may say that it is an investment.”

Many investors will not take any advice at all whenbuying real estate, preferring to go with their ownopinion and instinct. This is something that constantlysurprises Mr. Gething. “Not many people would spend$2m (£1m) on buying a painting without taking any

advice, but I have seen people spending $8m (£5m) onreal estate without getting any advice,” he says. “Theresidential real estate market is a jungle populated bysome rather wild animals: the developers, the agents,the owners. Some are very good and highlyprofessional. But many are not. It’s completelyunregulated — it really is a case of buyer beware.”

Mr. Nouvion highlights the importance of gettingappropriate advice — and taking the views of some inthe market with a pinch of salt. “You often find whenyour real estate is being sold that the agent tells youthat the real estate is a mediocre one, but if you are onthe buying side, it’s suddenly the world’s best,” he says.

There are interesting differences between men andwomen when it comes to residential real estateinvestments. Women are much more likely to rely on friends and family as a source of advice than men — indeed, it is their most widely consultedsource of information. They are also more likely thanmen to say that they find investing in real estate moreenjoyable than other asset classes, and are less likelyto invest indirectly, through funds.

“The residential real estate market

is a jungle populated by some

rather wild animals: the developers,

the agents, the owners.”

Which of the following factors do you consider to be the biggest disadvantages of holding residential realestate investments in your portfolio?

Cost of upkeep

Asset is relatively illiquid

Volatility of property prices

High transaction costs

Tendency for emotional attachment to get in the way of rational decisions

Volatility of demand from tenants

Time required to research and manage properties

Low returns compared with other asset classes

Rules and regulations associated with ownership

Lack of information about commercialproperty market

Source: Economist Intelligence Unit Survey, September 2009

46.7%

32.8%

31.8%

28.3%

24.6%

21.3%

20.3%

14.2%

14.1%

6.9%

Chart 12 – Disadvantages of holding residential real estate, all respondents

One of the lessons from the financial crisis is that, asan investment, real estate has certain limitations ordisadvantages which many investors did not take intoaccount, including the fact that its correlation withother asset classes may increase in times of stress.High net worth individuals should consider thesecarefully before making a commitment.

Cost of upkeep is cited as the biggest disadvantage ofresidential real estate. “There are all kinds ofmaintenance required when you come to residential realestate,” says Mr. Gething. “You need to be willing to setaside up to 20 percent of gross rents to cover this.”

Residential real estate’s relative lack of liquidity is alsocited as a major disadvantage. During the boom years,this was a characteristic of real estate investment thatmany investors seemingly forgot. “I think manyinvestors got used to the idea that you could haveboth high returns and high liquidity at the same time,”say Audrey Klein, Managing Principal at Park HillEstate, a subsidiary of Blackstone. “But that has alwaysbeen anomalous. And what we saw was that a lot ofthe so-called liquidity that investors thought theywere getting rapidly disappeared when therewere problems.”

Defying the downturn

There can be few areas of the world that show soclearly the dangers of over-development than theskyline of Dubai, which once had the highestconcentration of construction cranes in the world.Today, the cranes are idle, the market has stalledand there is a new mood of sobriety.

“Just a couple of years ago, anyone could buy apiece of land and become a developer,” says Ahmed Al Hatti, Chairman of Cayan Investment andDevelopment, a leading regional constructioncompany. “Today, everything has changed. It ismuch more focused on quality of project, locationand the developer’s previous projects. But forestablished, successful developers with a goodtrack record, there are good opportunities.”

In an environment where developers have sloweddown, closed or indeed gone under, Cayan is stillexpanding and recruiting. Cayan is focusing a lot ofattention on the Saudi market, which Mr. Al Hatti

believes has many interesting characteristics,including demographics. “There is a population ofaround 27 million people with some 40 percent ofthe population under the age of 15,” he says. “As aresult, there is a big demand for accommodationand a government that is working hard to developthe mortgage market.”

The demographic and regulatory changes currentlyunderway in Saudi Arabia could represent avaluable opportunity for investors. In a reportpublished in late 2008, Jones Lang LaSalleforecasted significant growth in both the residentialand commercial real estate sectors in the country.They highlighted a number of important drivers ofgrowth, including new mortgage laws aimed atsolving the current lack of mortgage financing andextending home ownership, a shortage of residentialunits, and growth rates in the office sector that areahead of those in other GCC countries.

Knowing the risks

2726

Commercial real estate plays an important role in theportfolio of many wealthy investors. Among thewealthiest survey respondents, who have more than$48m (£30m) in financial assets, 70 percent have someexposure to direct commercial real estate investments.

According to some interviewees, the commercial realestate market in some countries is currently lookingattractive. “I think it may be a good time to buycommercial real estate which is prime — well located,good quality and let to tenants with good covenantson long leases,” says Charles Beer, a Senior Partner inReal Estate Tax at KPMG in the U.K. “Supplies of suchreal estate are very limited, however.”

The commercial real estate market is very differentfrom the residential market. For one thing, theinvestment sizes are substantially larger; it is hard toget a foothold in the market for much less than $8m(£5m), according to Sean Brew, Head of Portfolio AssetManagement at global real estate adviser, DTZ. Inaddition, it is in many respects considerably moresophisticated. Aside from ultra high net worthindividuals, buyers tend to be institutional funds orcorporate buyers, who will research investments verycarefully and manage their portfolios on a continuousbasis. To compete in this market, individual investorsneed to adopt a highly professional approach.

“In my experience, private investors in commercial realestate as a group are highly entrepreneurial,” says Mr.Brew. “They are risk takers and they know what theywant. They are very proactive.”

The main advantage of investment in commercial realestate, according to respondents, is the yield that canbe obtained through rental. With many other assetsyielding relatively low returns as a result of record lowinterest rates, the returns from commercial real estatecan look attractive. Certainly, yields on commercial realestate are higher than in residential, becausebusinesses are prepared to pay more for space in agood location that helps them achieve their goals. Thismakes commercial real estate more suitable forgenerating income, but some experts caution againsthigh expectations.

“Commercial real estate is now providing good valueand, when people look at returns from otherinvestments, yields look attractive,” says Ian McBryde,Director of Property Funds at F&C REIT AssetManagement. “However, people need to be remindedthat some of the underlying fundamentals such astenant demand and vacancy rates are still not strong.”

With unemployment still rising, vacancy rates oncommercial real estate remain high — for example, thevoid rate in the U.K. is now at an all-time high, whichmeans that there is a risk that the investment will yieldno income at all. Investors should be aware thatdownturns in commercial real estate can last for years,rather than months; this is because commercialproperties take several years to develop, which canlead to a significant lag between supply and demand.

“With unemployment still rising,

vacancy rates on commercial real

estate remain high, which means

that there is a risk that

the investment will yield no

income at all.”

Commercial Which of the following factors do you consider to be most attractive about holding commercial real estateinvestments in your portfolio?

Potential for income through rental

Long-term performance track record

Potential for capital gains

Overall portfolio diversification

Stability of investment

Ability to finance investments through debt

Tax treatment of property

“Tangibility” of bricks-and-mortar investments

Hedge against inflation

Attractive valuations in current market

Emotional attachment to bricks and mortar

Relatively low correlation with other asset classes

Ability to enjoy properties as primary andsecondary homes

Hedge against inflation

Source: Economist Intelligence Unit Survey, September 2009

29.8%

18.8%

18%

16.7%

13.7%

13.7%

13.4%

12.9%

9.1%

8.4%

6.5%

4.7%

4.4%

2.8%

Chart 13 – Key advantages of commercial real estate investment

“I am less optimistic about commercial real estate ingeneral, at least from an equity perspective,” saysMr. Demeroutis. “I think there are some hugeunresolved problems overhanging the sector that Idon’t think anyone is dealing with — it will take timeand money to put this right. It’s fine if you can findwell-let buildings in the West End or Times Squarewith good tenants, but there is a limited supply ofproperties like this.”

Mark Carpenter, Director of the Property Division atHenderson New Star, a fund manager, is moreoptimistic about some markets’ ability to recoverquickly. “Some markets are bouncing back quicklywhile some are still experiencing severe problems,” hesays. “The U.K. was the first to drop, in Q2 2007, whilesome in the Far East and better quality properties inWestern Europe didn’t experience declines until atleast 12 months later. And as there was a time lag onthe way down, we thought there would be a mirror inthe recovery. But other areas are showing fasterimprovement than the U.K.”

Mr. Carpenter is particularly bullish on the Far East,partly due to a change in demand. “These are stillgrowth economies, even though the growth hasslowed,” he says. “In Q4 2008, after Lehman’s

bankruptcy, yields were hit by 200 basis points andinternational demand dried up, led by the NorthAmericans and Europeans. However they are nowbeing replaced by local wealthy individuals andcorporations, who are not very leveraged. It’s aninteresting change with the local players becoming the drivers and nudging prices up.”

Choosing the right investment vehicle

Diversification remains important in commercial realestate but it can be difficult to achieve throughphysical holdings due to the large sums of moneyinvolved, except for the very wealthiest investors. But the growth of real estate funds allows investors toachieve diversification across multiple types of realestate and location with smaller investments, and to gain access to the expertise of specialist managers.“In order to get the kind of diversification that we thinkreal estate as an asset class needs, and not get tied tosome very specific risks, it’s crucial for investors topool their money in some kind of fund structure to buya larger, more diversified pool of assets,” saysMr. Gilbert.

2928

Among the survey respondents, 29 percent say theyhold indirect real estate investments such as mutualfunds and REITs. However, there are wide variations inindirect holdings among the target countries. Investorsin Monaco are most likely to invest in real estateindirectly, with 61 percent having holdings. Investors inthe U.S. (48 percent), Canada (41 percent), Singapore(45 percent) and Hong Kong (42 percent) also favorindirect investments, while the U.K. and GCC arelukewarm, with just 17 percent having indirect realestate investments. Spanish investors are the leastlikely to invest indirectly, with just 3 percent havingthese holdings.

The survey also found that the wealthiest respondents— those who in theory are most able to make directinvestments in commercial real estate — are the mostlikely to invest indirectly. Almost 45 percent ofrespondents with investable assets in excess of $48m(£30m) hold indirect investments, while just 26 percentof respondents with $800k to $2m (£500k to £1m)invest indirectly. This may be due to better quality

advice received by the wealthiest or it may be due tothe fact that the wealthiest will have more investments— they are also the most likely to hold directcommercial real estate, with 70 percent of respondentswith assets in excess of $48m (£30m) holding directlywhile just 17 percent of respondents with $800k to$2m (£500k to £1m) having direct exposure.

There is also an interesting divide between the sexes.While 34 percent of male survey respondents holdindirect real estate investments, just 14 percent offemale respondents do.

“The survey also found that the

wealthiest respondents are the

most likely to invest indirectly.”

Which of the following types of real estate investment do you hold in your portfolio?

U.S.

U.K.

Canada

Singapore

Monaco

Spain

GCC

India

Switzerland

Hong Kong

Source: Economist Intelligence Unit Survey, September 2009

47.9%

17.4%

40.6%

44.7%

60.7%

2.6%

17.2%

35.6%

18.2%

42.1%

Chart 14 – Respondents who held indirect investments in real estate, by country

While real estate funds offer a lower entry point forinvestment in commercial real estate anddiversification, they are not without their problems.Their liquidity is often cited as an advantage — it ismuch easier to get out of a mutual fund than sell realestate — but investors need to read the fine print andunderstand each fund’s rules on redemptions.

For example, U.K. investors were caught out in late 2007and early 2008 when some real estate funds wereforced to suspend redemptions, and sometimes tradingentirely, as a result of lack of liquidity. Most funds tendedto keep between five percent and ten percent in cash inorder to meet investor redemptions, but when a wave ofinvestors decided they wanted out, the funds wereunable to cope, shrinking cash levels significantly andforcing the sale of real estate. “It was a psychologicalthing — people panicked,” says Mr. McBryde. “At thetime, it was like a run on a bank but most retail funds arenow stable and seeing positive inflows.”

Problems such as these have led investors to questionwhich type of fund structure is best suited for realestate investment. Open-ended funds, at the end ofevery day, issue shares to new investors and buy backshares from investors wishing to leave the fund — withinflows and outflows often canceling each other out.But when outflows greatly exceed inflows, and the cashcushions funds keep are depleted, there are problems.

This has led some investors to prefer closed-endedvehicles, such as real estate trusts or REITs. Thesefunds have a set number of shares, so once they are allin circulation investors must purchase them on thesecondary market rather than from the fund manager,and shares are not normally redeemable for cash orsecurities until the fund liquidates. This means thatthe fund manager is not forced to sell real estate inorder to meet redemptions, and investors may selltheir shares at any time — provided they can find abuyer. However, listed trusts and REITs are morecorrelated to equities than direct real estateinvestments or open-ended funds, because they arealso traded on the stock market.

The key is for investors to know what they are buyingand for real estate managers to be clear in theircommunications. “Institutional investors understand thatreal estate is a long-term investment and thattransactions are expensive and take time,” says MarkMeiklejon, Investment Director at Standard LifeInvestments. “But this can be a problem in the retailinvestment space if they don’t understand that directreal estate is illiquid. This has raised issues with somemanagers around how they communicate thisto investors.”

Which of the following types of real estate investment do you hold in your portfolio?

$800k-$2m

$2m-$16m

$16m-$48m

>$48m

Direct residential investments (not including primary residence)

Direct commercial investments (offices, retail, etc.)

Indirect real estate investments (e.g. Reits)

Source: Economist Intelligence Unit Survey, September 2009

60.9%

76.9%

77.8%

78.7% 69.7% 44.5%

51.4% 24.3%

30.8% 31.8%

17.2% 25.9%

Chart 15 – Percent of respondents holding different types of real estate investments, by wealth band

30 31

“Real estate prices are showing

early signs of stabilizing in some

major developed countries and, in

other markets such as China,

prices are even booming.”

Real estate prices are showing early signs of stabilizing insome major developed countries and, in other marketssuch as China, prices are even booming. This is anenvironment that offers considerable promise, althoughtight credit conditions will continue to hinder investors’ability to take advantage of these opportunities.

The survey showed that high net worth individuals inmost markets around the world are cautiouslyincreasing their allocation to real estate — or at leastmaintaining their current allocation — although theyrecognize that prices may still have further to fall inthe short term. These findings and the opinions of ourpanel emphasize the need to be highly selective withreal estate investments, and to remember that theasset class should be regarded as a long-terminvestment, not a source of quick gains.

Most investors in our survey currently focus on realestate in their home country, no doubt because it feelsfamiliar to them, and because information about localmarkets is more readily available. But when investorsdo look outside their own countries of residence, mostconsider the U.S. to be the most attractive real estatemarket, followed by China, the U.K. and India. This isan interesting and complex mix of established andemerging markets. Two of them (the U.S. and U.K.)have witnessed steep declines in real estate prices in

recent years and face a long-haul recovery, whereasChina and India are expected to deliver rapid economicgrowth that in turn should fuel demand for real estate.

There is always a danger with real estate investment,at least in the case of residential, that the heart canrule the head. Emotional attachment can get in theway of sound decision-making, leading investors tobuy assets because they like them or hang on to themfor too long when circumstances change. Wheninvesting with financial goals in mind, investors mustdisassociate themselves from these emotionalattachments and take an objective view.

This is especially important when it comes todiversification, both in terms of overall portfoliodiversification and diversification within the real estatecomponent. In order to spread their risk and gainaccess to a wider spectrum of real estate markets,investors should carefully consider their options, either by taking a more international view, addingcommercial real estate to their portfolio or investingindirectly through funds, which less than a third ofinvestors currently do.4

Investors must be careful to avoid overexposure to an asset class that in practice has been proven to bevulnerable to booms and busts. So while it can betempting to seek refuge in real estate as a safe haven,especially given the current widespread mistrust incomplex financial products, investors must rememberthat the tangibility of bricks and mortar and theirapparent promise of stability can sometimesprove illusory.

“Institutional investors understand

that real estate is a long-term

investment and that transactions

are expensive and take time.”

Time to put reason before emotion

4. Diversification does not guarantee against loss

3332

The Barclays Wealth View

Commercial real estate outlook

We are keeping a close eye on trends in real estateinvestment trusts (REITs) — which are a leveragedform of equity investment. Accordingly, it is notsurprising that these have roared back sincetroughing in early March. The FTSE NAREIT U.S. RealEstate Index Series has risen by more than 70 percentbetween March and October — although it is stillwell shy of its previous peak.

Despite recent rises, we believe that both U.S. andU.K. markets are still somewhat below their “fairvalues,” therefore we expect further gains in these

two REITs markets in 2010, and believe that Europeand non-Japan Asia look to be a good value too. For further details, see the October edition of ourquarterly Signpost publication.

REITs are, of course, only one way to invest incommercial real estate. We also monitor and analyzethe IPD’s commercial real estate series, which aredesigned to track underlying investment performancein the sector. The U.K. series appears to be somethinglike ten percent below “fair value” currently, as shownin the chart on page 34. So, we are a little lessoptimistic being long the IPD series than we are for REITs.

Chart 1 – U.S. residential house prices: actual vs. “fair value”

Index

0

1

2

3

4

5

6

7

ActualQuarter and year

“Fair value”

Q1 1981 Q1 1986 Q1 1991 Q1 1996 Q1 2001 Q1 2006 Q1 2009

Source: Barclays Wealth Economics

Chart 2 – U.K. residential house prices: actual vs. “fair value”

ActualQuarter and year

“Fair value”

Q1 1981 Q1 1986 Q1 1991 Q1 1996 Q1 2001 Q1 2006 Q1 2009

Index

0

1

2

3

4

5

6

7

Source: Barclays Wealth Economics

Contributed by Michael Dicks, Head of Research at Barclays Wealth, who has over 20 years ofexperience researching housing and real estatemarkets. Here he provides his opinions on some of the survey findings.

We found a number of the survey’s findingssurprising. Most obviously, survey respondents areclearly holding a much higher proportion of theirwealth in real estate than we would normally advise.