337

P R E F A C E

The chemical industrial sector covers a very wide spectrum and while some areas like manufacture of chemical fertilizers and oil refining seem to have been well covered, other segments are yet to be developed. This study on the Prospects of Chemical Industry is aimed at suggesting the future course of action to promote the Chemical Sector as heart of strengthening the overall industrial base of Pakistan. It reviews the present status of Chemical Industry in Pakistan, analyses the import statistics, availability of raw materials and suitability of chemical plants locations. An effort has been made to review most of the sectors and to present an overall picture of the chemical process industry in Pakistan.

Views of the various stakeholders including the top companies and entrepreneurs have been taken and necessary recommendations have been made for future policies. The study is indicative in nature, potential areas of investment have been highlighted, detailed feasibility study shall however, be required for each project.

The manufacturing sector is considered the backbone of a country. The share of manufacturing sector in the GDP currently is around 18% in Pakistan. It is hoped that with the development of chemical industrial sector, share of manufacturing sector would significantly increase, contributing to the overall GDP.

The development of the proposed chemical industries would save foreign exchange through import substitution, help in the development and growth of downstream small and medium industry, contribute in providing jobs and poverty alleviation. It is hoped that this study, like several others preceding this one, will bring up to date information to the professionals and investors alike. May Allah, Almighty accept our effort and bring industrialization and self-reliance to Pakistan. Experts Advisory Cell Islamabad April 2003

MESSAGE FROM MINISTER FOR

INDUSTRIES & PRODUCTION

The economy of Pakistan has seen considerable growth in various sectors over the past few years. However, certain important sectors are still underdeveloped which need special attention of the Government. Historically, Pakistan has concentrated on low tech to medium technology type of industries. The development of Hi-tech and Engineering industry has by and large been attached low priority. To meet the rapidly increasing requirement of chemicals, dyes and pigments, industrial raw materials and other allied chemical products, it has become important to disseminate comprehensive information for planning the development of Chemical & Petrochemical Industry in Pakistan. Realizing the importance of this sector, Ministry of Industries and Production assigned a study on “Prospects of Chemical Industry in Pakistan” to Experts Advisory Cell. The main thrust of the study is to review the existing status of chemical industry, the availability of local raw materials, supply and

demand situation and to formulate practical recommendations to attract investment in this sector. As Pakistan’s economy is largely dependent on products made from agricultural produce such as cotton and related textiles being a major source of foreign exchange earning constitutes about 60% of total exports. Therefore, the Government’s priority is to improve the yield of agricultural products through quality inputs such as fertilizers and pesticides at affordable prices. The manufacturing sector is considered as the engine of economic growth. The share of manufacturing sector in the GDP currently is 17.7% in Pakistan. It is hoped that with the development of chemical industrial sector, share of

manufacturing sector would significantly increase, contributing to the overall GDP growth. Most of the raw materials and intermediates for dyes and pigments, paint & varnishes, pesticides, plastic and plasticizers are being imported. These raw materials belong to or derived from Petrochemicals, which presently have no base in the country. I am fully convinced that no appreciable progress is possible in the chemical sector without indigenous production of petrochemicals and other chemicals. The petrochemical groups constitute more than 76% of total chemical group import bill, which was over Rs 125 billion for the year 2001-02

The development of the proposed chemical industries would save foreign exchange through import substitution, help in the development and growth of downstream small and medium industries and contribute in providing jobs and poverty reduction.

Liaquat Ali Jatoi Minister for Industries &

I have advised Experts

Advisory Cell to circulate the report to all Industry stakeholders, Industry Associations and Chambers of Commerce & Industry to obtain their comments and recommendations so that a Chemical Vision is prepared for the approval of the Government.

The Government of Pakistan is determined to facilitate local and foreign entrepreneurs. An important step taken by the Government is that one desk facility services have been made available to the investors initially at Karachi, Lahore, Rawalpindi, Islamabad and Peshawar.

The study on “Prospects of Chemical Industry in Pakistan” prepared by Experts Advisory Cell is another step to facilitate investors. The Ministry and its support organizations are there to provide all possible assistance to investors to make their plans a success.

MESSAGE FROM SECRETARY

INDUSTRIES & PRODUCTION

The GDP of Pakistan has two sectors. The commodity sector and services sector each having 49.1% and 50.9% share in the economy respectively. Agriculture occupies 24.1% share in the overall economy while the share of manufacturing in GDP is 17.7%. The Ministry of Industries & Production has since last few years strived hard to create conducive environment for the growth of the industry, optimum utilization of industrial capacities, value addition and wastage reduction. The study on “Prospects of Chemical Industry in Pakistan” Is another effort to further the mission of the Ministry.

Pakistan’s major foreign exchange earnings are coming from export of cotton related products. However, Pakistan has not yet been able to even fully exploit the potential of value addition in the cotton sector which can multiply export earnings. Value addition is also required in chemicals, dyes and pigments which are generally petroleum based products.

Pakistan’s import of

chemicals related products ranges

between US$ 1.52 to 2.00 billion per

annum and represents 16 – 20% of

the total imports.

The per capita usage of petroleum and petroleum products including plastics is very low as compared with the developed countries. With the turnaround of economy, per capita income is now expected to increase. Efforts need to be made to increase the per capita income to US$ 900 – 1000 by year 2010. The share of manufacturing in the GDP of Pakistan is targeted to be raised to 25% from the present share of 17.7%. The target to achieve 15 million bales of cotton during the next few years shall require increase in the development of fertilizer, polyester fibre and pesticides industry.

Leather industry is another major contributor towards the export of Pakistan. The value addition of leather sector also requires quality chemical, dyes and pigments.

There is also a need to optimize the existing industrial base in the country and ensure different sub-sectors operate at their maximum capacity utilization and achieve maximum value addition in the agriculture products and by-products e.g. conversion of molasses and baggase to industrial alcohol and paper respectively.

Inorganic chemicals are mainly derived from mineral resource. Appropriate utilization of mineral sector is required in order to be self-reliant in chemicals. There is a big potential for export of these mineral based chemicals also. The global trade of chemical sector is around 10% of the total world trade whereas in case of Pakistan it constitutes only 2.1% of our exports.

All the above factors motivated us to initiate of the study on “Prospects of Chemical Industry in Pakistan” by the Experts Advisory

Cell. The study has been developed through extensive discussions with the stakeholders of the chemical sector. I hope this effort shall significantly contribute towards speeding up the process of industrialization in this sector.

The study has identified some products based on supply and demand gap. Since the feasibility depends on many factors I therefore, recommend that detailed techno-economic studies should be carried out to check feasibility of these projects.

In the end I request the chemical sector stakeholders, professionals and experts to study the report, recommendations and come forward with valuable suggestions so that Chemical Vision could be developed for the approval of the Government.

Secretary Industries & Production

April 2003

ACKNOWLEDGEMENT

This study on the Prospects of Chemical Industry in Pakistan covers

twenty (20) sub-sectors. It was necessary to involve concerned stakeholders and

experts in different sub-sectors to make the study useful. Therefore, various

stakeholders, professionals, officials and industrialists were consulted on several

occasions during the course of this study. The draft report was circulated in

August 2002 to selected industrialists, professionals and institutions. Industry

stakeholders showed keen interest and provided valuable comments and

suggestions. The final report has been amended wherever necessary by

incorporating these comments.

Special thanks to Sheikh Mahmood Ahmad, Ex-chairman FCCCL,

Adviser NUST, for his valuable input in finalizing the study especially the

recommendations.

Experts Advisory Cell (EAC) also acknowledges the cooperation

and contribution rendered by the following valuable stakeholders from

the public as well as private sector in compiling this report:

o A.T.S. synthetic (Pvt.) Ltd., Lahore:

Mian Anjum Nisar, Managing Director

o BASF Pakistan (Pvt.) Ltd., Karachi:

- Qazi Sajid Ali, Managing Director - Mr. Sajjad Saleem, Director Marketing

o Bombal Traders, Karachi:

Sheikh Ghulam Ahmad Bombal, Managing Director

o Colgate & Palmolive Pakistan Ltd., Karachi Mr. Sami H. Zaidi, Director

o CropLife Pakistan, Karachi: Mr. Asif M. Khan, Chairman

o Delta Industries (Pvt.) Ltd., Lahore:

Mr. Mohammad Sadiq, Head Chemical Unit o Dr. Farrukh S.M. Akhtar, Technical Advisor, Saudi Arabia o Engro Asahi Polymer & Chemicals Ltd., Karachi:

Mr. Asif Qadir, President o Engro Chemical Pakistan Ltd., Karachi:

Mr. Zafar A. Khan, President o Habib Sugar Mills, Karachi:

Syed Tanviruddin Ahmad, Director Projects

o ICI Pakistan Ltd., Karachi: - Mr. Azhar Ali Malik, Chief Executive - Mr. Pervaiz A. Khan, General Manager (Soda Ash Business) - Mr. Malik M. Akram, General Manager (Technical &

Engineering) - Mr. M. Afzal Jamil, Vice President PTA Manufacturing

o Industrial Chemicals (Pvt.) Ltd., Karachi: Mr. S. M. Zaheer Alam

o Ittehad Chemicals Ltd., Lahore: Mr. Ghulam Mustafa Khattri, Chief Executive

o Master Paint Industries (Pvt.) Ltd., Lahore:

Mr. Sufi Muhammad Amir, Commercial Director

o Mir & Associates, Industrial Consultants, Karachi: Mr. Amanullah Mir, Proprietor

o National Fertilizer Corporation (NFC), Lahore:

Mr. Abdul Mannan, General Manager (Tech. & Planning) o Olympia Chemicals Ltd., Lahore:

- Mr. Monim Bokhari, Office Manager - Mr. Masood Khaliq

o Pakistan Atomic Energy Commission, Islamabad:

Mr. Khalil Qureshi, Head Fuel Cycle o Pakistan Council of Scientific and Industrial Research (PCSIR),

Islamabad:

Dr. Anwar ul Haq, Chairman o Prime Chemicals (Pvt.) Ltd., Lahore:

Mr. M. Nazir Chaudhry, Managing Director

o Progressive Traders (Pvt.) Ltd., Karachi: Mr. Muhamamd Siddique Sheikh, Group Chairman

o Qaiser LG Petrochemicals, Lahore: Mr. Irfan Qaiser, Director

o Ravi Rayon Ltd., Lahore:

Dr. Fayyaz A. Mian, Consultant

o Sandal Dyestuff Industries (Pvt.) Ltd., Faisalabad: Dr. Salahuddin Munam, Director

o Sitara Chemical Industries Ltd., Faisalabad:

- Mian Muhammad Adrees, Chief Executive Officer. - Engr. Muhammad Khalil, Director Business Development - Mr. M. Yameen, Group Director Finance

o Small & Medium Enterprises Development Authority, Lahore:

Mr. Iqbal Mustafa, Chief Executive Officer

o Technology Management International (Pvt.) Ltd., Lahore: Dr. W.M. Butt

o Unilever Pakistan Ltd., Karachi:

- Mr. Sher Afzal Mazari, Head of Corporate Affairs - Mr. M. Qaiser Alam, Supply Chain Development Manager - Mr. Basharat Ahmad, Corporate Affairs Manager

EAC very gratefully acknowledges the very vital help

provided by all above professionals, which enabled the finalization of this

report.

Experts Advisory Cell Islamabad. April 2003

Table of Contents

Page No. Preface

Acknowledgement Executive Summary ................................................................................. i Importance of Chemical Industry ..........................................................1 Overview .............................................................................................3 Availability of Raw Material.................................................................. 10 Major Chemical Sub-sectors ................................................................. 15

o Petrochemicals, BTX, Carbon Black, MEG ................................ 16 o Fertilizers ............................................................................. 35 o Synthetic Fibers .................................................................... 41 o Alcohol from Molasses ........................................................... 52 o Pesticides ............................................................................. 59 o Plastics and Resins ................................................................ 67 o Paints and Varnishes ............................................................. 85 o Oleo Chemicals ..................................................................... 96 o Soaps, Detergents and Cosmetics........................................... 99 o Paper and Paper Board........................................................ 109 o Glass 123 o Soda Ash and Sodium Bicarbonate........................................ 127 o Caustic Soda, Chlorine and Related Products ......................... 131 o Sulphuric Acid, Hydrochloric Acid and Nitric Acid .................... 136 o Organic Chemicals............................................................... 139 o Specialty Chemicals ............................................................. 145 o Dyes and Pigments.............................................................. 147 o Textile and Tannery Chemicals ............................................. 155 o Water Treatment Chemicals ................................................. 159 o Food Chemicals................................................................... 160 o Essential Oils and Perfumes ................................................. 165

Recommendations .............................................................................. 166

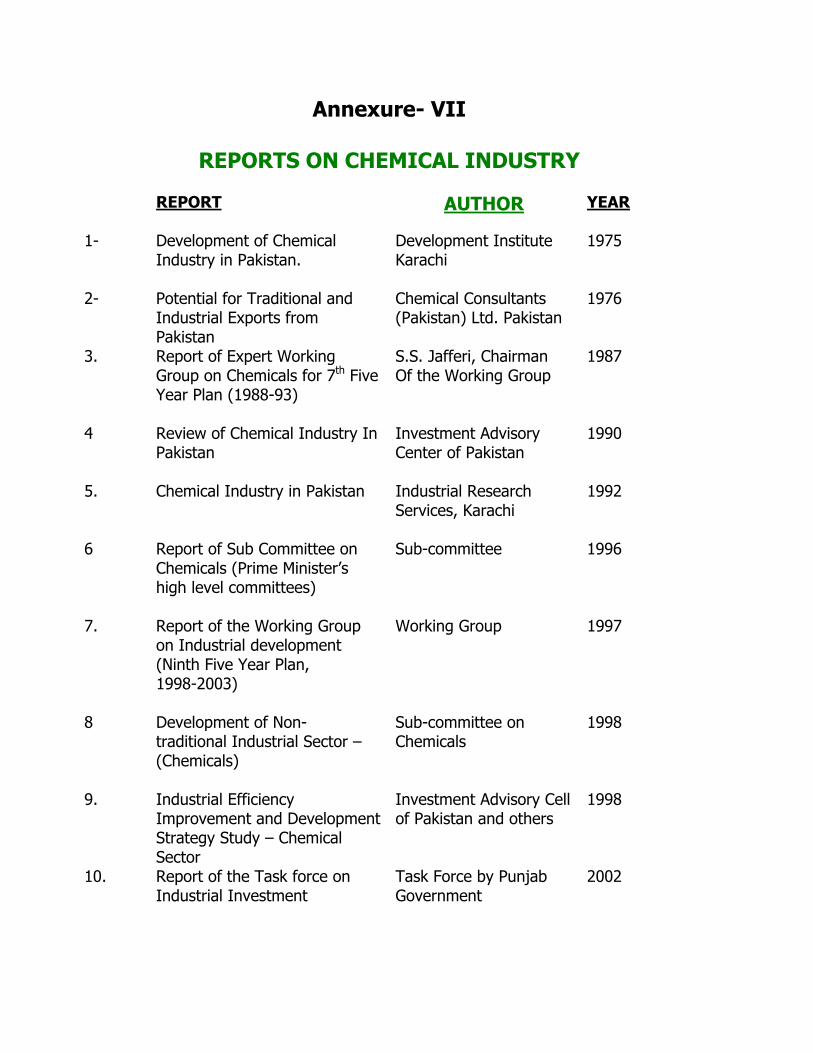

Annexures:

I- Coal Reserves in Pakistan .................................................... 172 II- Coal Analysis ...................................................................... 174 III- Mineral Resources of Pakistan .............................................. 175 IV- Minerals for Chemical Industry ............................................. 176 V- Specialty Chemicals ............................................................. 185 VI- Chemical Imports ................................................................ 194 VII- Synopsis from Previous Reports............................................ 200 VIII- Company Profiles ................................................................ 221 IX- Fertilizer Policy 2001 ........................................................... 289

Appendix: I. Scope of Chemical Sector Development in Pakistan

Glossary of Abbreviations

EXECUTIVE SUMMARY

All over the world the chemical industry is a major contributor to the

national economy, playing both direct and indirect role. In Pakistan while some

segments of chemical industry have received due attention, others remain

neglected. So far the investment in this field is estimated to be Rs 360 billion.

Import of chemical related products constitute 20% which is around US$ 2 billion

of total imports. Thus there is a vast potential for developing this sector through

import substitution and self reliance.

The objective of this study is to review the existing status of chemical

industry, the availability of local raw materials, supply & demand situation and to

consolidate practical recommendations to attract investment in this sector. As a

result of immense consultation with stakeholders following additional objectives

emerged for inclusion in the study.

o Increase share of manufacturing in GDP from existing 18%

(Partially through setting-up Petrochemical and Chemical

Industries) to 25%.

o Identify projects to become self reliant

o Enhancing value addition within existing units of chemical /

processing industry.

The country has already suffered due to lack of investment in basic

petrochemical and chemical industry. There is still time if the government takes

corrective measure to improve the situation.

Present Status

Locally available resources of natural gas, petroleum and coal are

being used mainly to meet the energy requirement of the country. They have not

been utilized for the manufacturing of chemicals where in some cases value-

addition can be ten fold. The only exception is the use of natural gas to produce

fertilizers. There exists vast potential to manufacture chemicals from reserves of

indigenous natural gas, coal and minerals.

Some organized chemical sectors are well developed. A few basic

chemicals like sulfuric acid, caustic soda, soda ash and chlorine have sufficient

installed capacities to meet the local demand.

Most of the raw materials and intermediates for dyes & pigments, paints &

varnishes, pesticides and plastics & plasticizers are being imported. These raw

materials and intermediates mainly belong to or derived from petrochemicals,

which have no base in Pakistan.

Dyes & pigments are being produced locally but only partially meet the

demand. Most of these raw materials are imported. Active ingredients used in

pesticides & insecticides are not produced locally but about 30 units are involved

in formulations based on imported raw materials. There is a strong need for

domestic production of some active ingredients.

Numerous units are involved in the production of soaps and

detergents. However there is heavy dependence on the imported tallow for

soaps and alkyl benzene, sulfonic acid for the production of detergents.

The down stream industries of plastics, plasticizers and polyester are well

developed but again depend on the imported petrochemical raw materials, i.e.

olefins, poly olefins and Benzene, Toulene & Xylene (BTX). The petrochemical

sector remained neglected in spite of numerous recommendations in the last

three decades to setup a naphtha or hydro cracker. No appreciable progress is

possible in the chemical sector without the indigenous production of

petrochemical building blocks like olefins (ethylene, propylene, butadiene) and

basic aromatics like BTX (benzene, toluene and xylene). Keeping in view the

importance of the basic petrochemicals, setting up of a petrochemical complex is

strongly recommended.

Petrochemicals As mentioned above, most of the basic petrochemicals are being imported

whereas their local production is essential not only to boost the chemical sector

but for the entire industrial sector as for instance in case of textile industry,

polyester, viscose, dyes and bleaching agents play a pivotal role. Olefins and

their derivatives are being imported in large quantities for their end-use in

plastics, paints, dyes & pigments, pesticides, detergents and rubber products.

Similarly, the import of BTX tops among the chemical group. Only a small

installed capacity for BTX production exists in National Refinery, Karachi. The

demand for xylene and toluene is substantial in the country. Xylene is used in

large quantities for the manufacturing of PTA for polyesters and as a solvent in

pesticides.

A summarized import list of important chemical groups is presented in

section-4. The list contains 11 chemical groups of which 6 belong to

petrochemicals. These petrochemical groups constitute more than 76% of the

total chemical group import bill of above Rs. 125 billion for the year 2001-02. It

is thus essential to make an indepth study for the local manufacturing of

petrochemicals.

Organic Chemicals

All organic chemicals are derived from petroleum, gas or agro based raw

materials. At present, only few organic chemicals are being manufactured locally

and that too in small quantities. There is urgent need to utilize the available

molasses for conversion into value added organic chemicals and to examine

techno commercial viability of setting up plants based on coal / oil / gas.

Inorganic Chemicals Inorganic chemicals are normally derived from mineral base, which is still

an under- developed sector in Pakistan. Several minerals are available in the

country but they have not been gainfully exploited. Salts of Sodium, Potassium,

Magnesium, Barium, Chromium and Aluminum can be manufactured from the

locally available ores if the infrastructure facilities at relevant mineral sites are

developed. Presently large quantities of inorganic salts are being imported. Total

imports of inorganic chemicals were more than Rs 5.08 billion in 2001-02. Atleast

some of these can be produced by relatively simpler processes/technologies.

Suggested Projects

As a result of preliminary investigation, following projects are indicated for

detailed techno-economic study.

1. Petrochemical Complex

A detailed techno-economic study is necessary. This study can consider all

possible routes including Natural gas, Associated gases, Naphtha, Molasses and

Coal.

Fertilizers

In the next 10 years there will be a shortage of around 1.2 million MTPY

of urea and 1.13 million MTPY of DAP. Therefore two plants of urea and DAP

with average capacity of 600,000 MTPY each would be required to meet the

future requirement of Fertilizer. Two urea plants are estimated to cost approx.

US$ 700 million. Two plants of DAP can be established at around US$ 500

million. Thus, an investment of US$ 1.2 billion in this sector appears justified.

o Manufacture of Phospahtic Fertilizer through Chlorine

As stated above, the domestic demand for DAP shall be 1.13 million

MTPY. Fauji-Jordan Fertilizer Company (FJFC) if revived can produce

450,000 MTPY. There would still be a huge shortage of 780,000 MTPY of

DAP or any other Phosphatic Fertilizer.

Phosphoric Acid can be produced using Hydrochloric acid (from locally

available surplus chlorine) and locally available phosphate rock using

Ishikawajima-Harima Heavy Industries (IHI) process. This phosphoric acid

in turn can be used to produce Phosphatic Fertilizers.

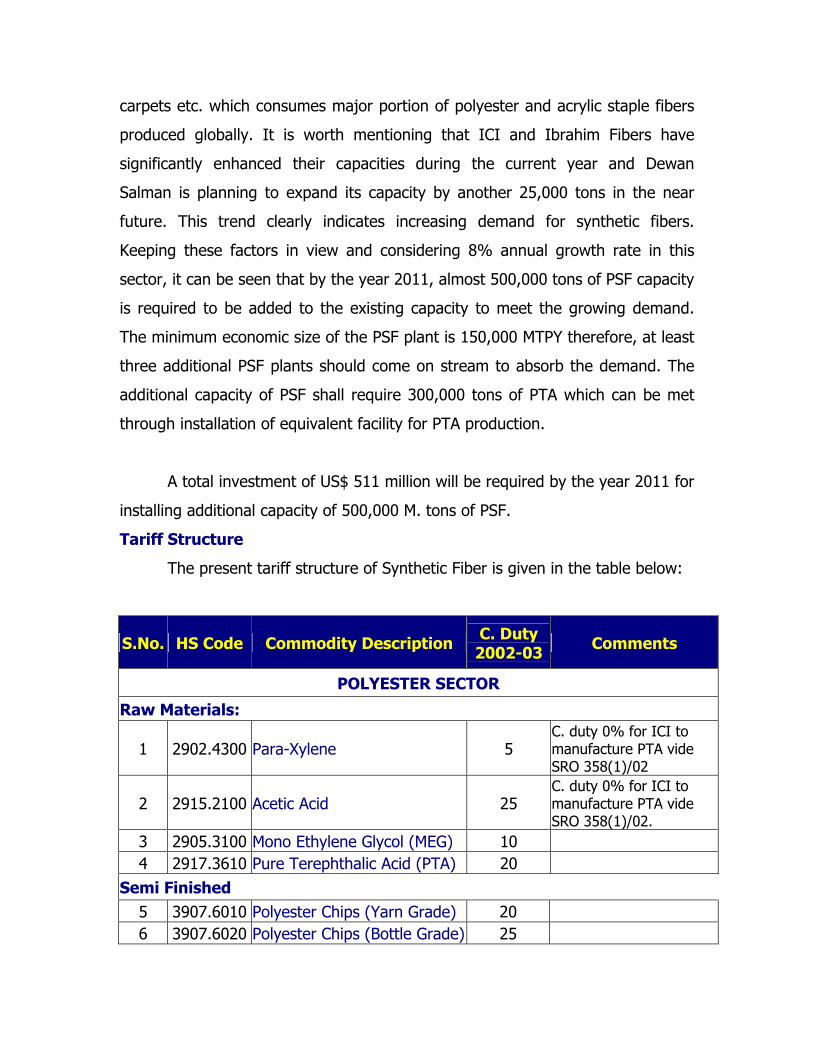

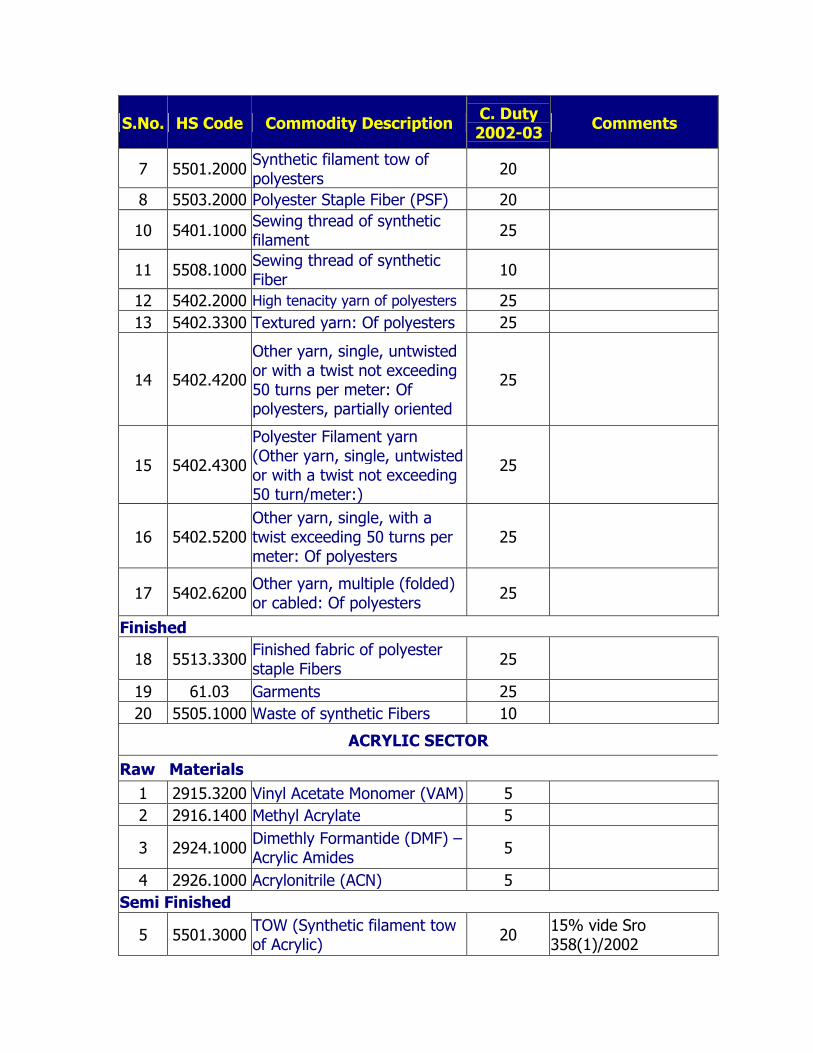

3. Polyester Fiber

Keeping in view, a 8% annual growth rate in this sector by the year 2011,

almost 500,000 tons of Polyester Staple Fiber (PSF) capacity is required to be

added to the existing capacity to meet the growing demand. The minimum

economic size of the PSF plant is 150,000 tons per annum, as such at least three

additional PSF plants can be expected to come on stream to absorb the demand.

The additional capacity of PSF will also make feasible the establishment of a

300,000 MTPY capacity of PTA plant. A total investment of approximately US$

511 million will be required by the year 2011 for installing additional capacity of

500,000 tons.

4. Organic Chemicals from Molasses

More than 2 million tons of molasses are available every year out of which

more than half is exported at a nominal rate of about Rs 2,000 per ton. Molasses

is a by-product of local sugar industry and can be converted to value-added

organic chemicals. The conversion of molasses to ethane can be the first step

which will enhance value addition for sugar industry.

Industrial alcohol, acetic acid, oxalic acid, citric acid, acetone,

pharmaceuticals, ether and ethyl acetate can be produced from molasses and

then a chain of other organic chemicals can be manufactured.

o Ethyl Alcohol

Ethyl Alcohol also known as Ethanol can be produced by fermentation of

the molasses. There are 76 Sugar mills in Pakistan producing around 2

million MTPY molasses. Only nine distilleries exist to produce alcohol from

the molasses out of which 5 are in operation. Normal Alcohol produced is

95% that is mostly being exported.

Optimum size of distillery would be 50,000 to 80,000 litres / day capacity,

this will be enough for about 2 sugar mills. A standard design and

engineering package may be purchased from abroad and distilleries may

be installed with local fabrication and packaging.

o Gasohol Anhydrous Ethanol with increased concentration of 99.9% can be blended

with gasoline, blend is called Gasohol and used as Automobile fuel.

At present, there is no programme in the country to use Ethyl Alcohol as

Gasohol in the automobiles. The present consumption of Petrol stands at

1.27 million tons per year. For a Gasohol programme, with 20%

substitution of petrol by Ethyl Alcohol, there will be a reduction in import

bill of crude oil. The quantity of Alcohol required would be 254 thousand

tons.

5. Manufacture of VCM (Vinyl Chloride Monomer) from Chlorine Gas

Conventional use of chlorine is 60% in petrochemicals and 40% in the

production of other solvents.

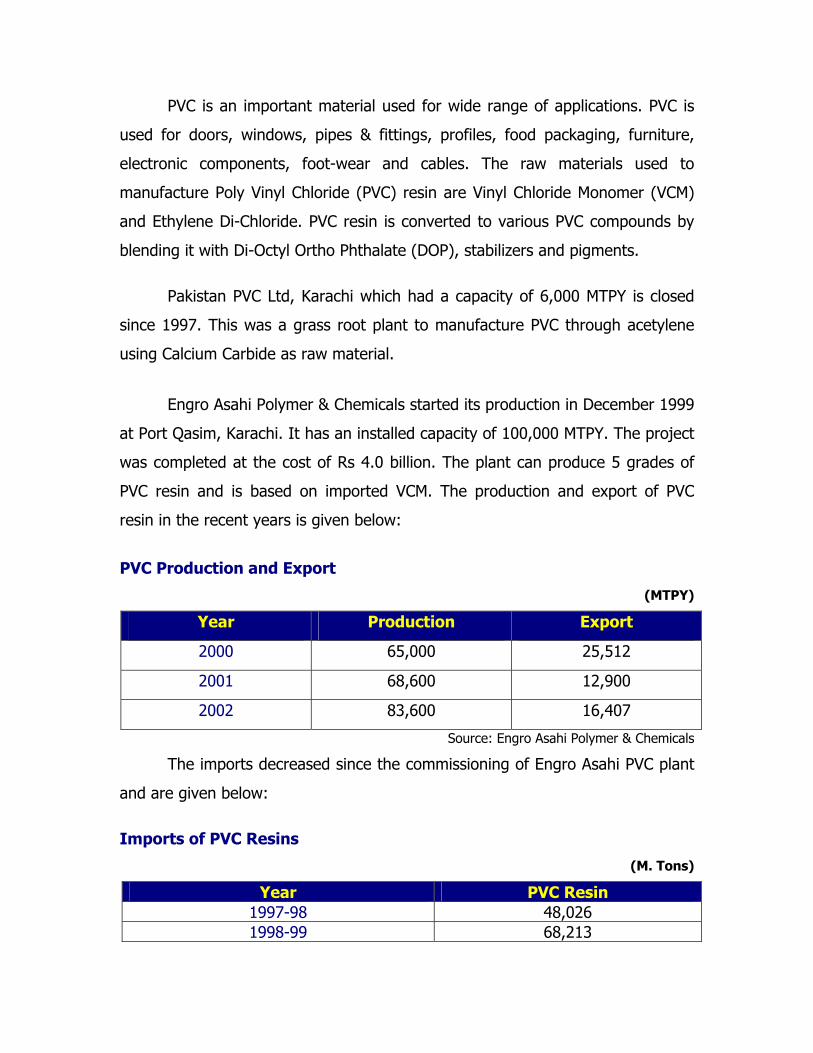

Engro Asahi has established PVC Resin manufacturing plant at Port Qasim.

The manufacturing process is from the polymerization of VCM. VCM currently is

being imported. This can be manufactured locally by utilizing the surplus chlorine

available in the country and imported ethylene. Engro’s Chemical handling

terminal can be used for the import of ethylene. Later as soon as petrochemical

complex is set up, import of ethylene can be substituted by local production.

Ethylene chloride can therefore by produced as a basic raw material for

Engro’s PVC Plant.

6. Methanol

Methanol is a petrochemical product produced by natural gas cracking.

Last five years import data is given below:

Methanol Import

Year Quantity Litres (000)

Quantity M. Tons

Value (Million Rs.)

1997-98 24,012 19,210 238 1998-99 19,771 15,817 184 1999-00 27,196 21,757 233 2000-01 33,763 27,010 438 2001-02 34,069 27,255 376 2002-03* 20,877 16,702 268

*July-December Source: Federal Bureau of Statistics Methanol is used as freezing point depressant and manufacture of

petrochemical products like formaldehyde, Acetic acid, Methyl Tertiary Butyl

Ether (MTBE), etc. The demand justifies setting up of a small unit meeting

domestic demand.

7. Paper from Bagasse or Cotton Sticks

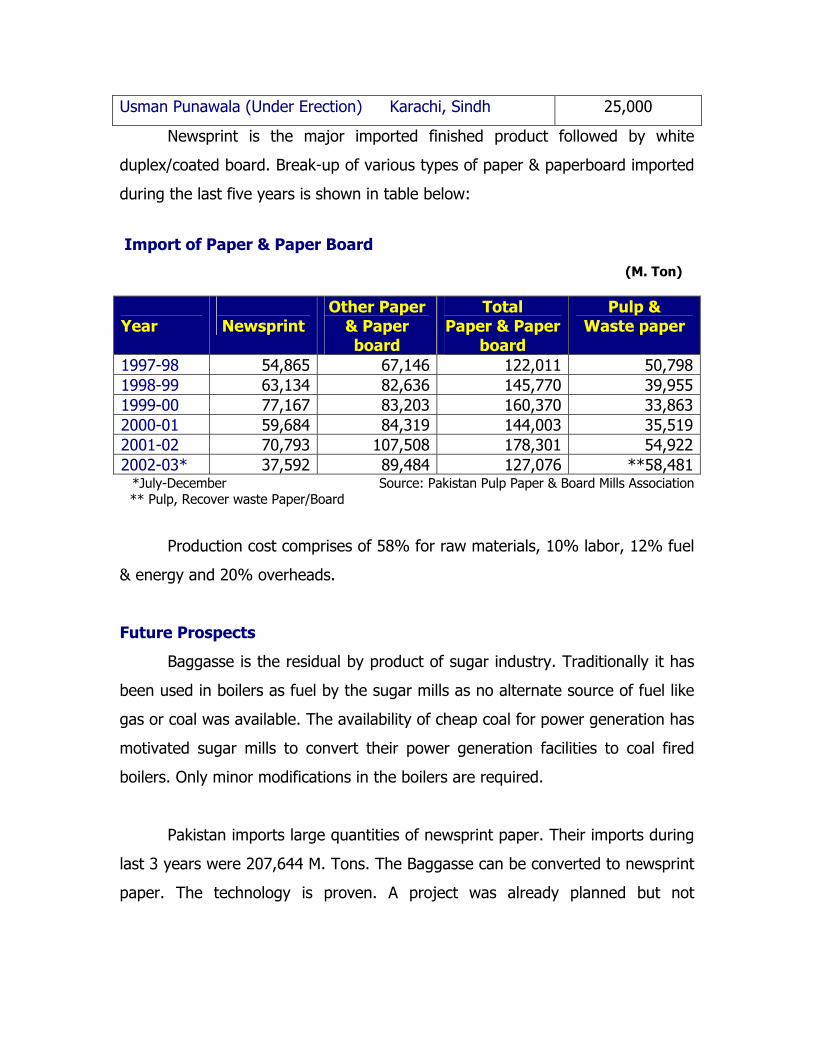

Bagasse is a by-product of sugar industry. It is not wasted but

traditionally being used by the sugar mills as a fuel for their boilers.

A project to make paper from bagasse was initiated in 1980’s but did not

materialize. Now with the possible exploitation of coal as cheaper fuel for boilers

like coal, it is expected that bagasse could be made available for paper

manufacturing. Paper will be a better value-added product as compared to

burning of bagasse as fuel only. About 76 sugar mills in the country produce

millions of tons of bagasse, most of it should be converted to make paper and

board.

Similarly, thousands of tons of cotton sticks are available every year from

the cotton crop. Presently, they are burnt as domestic fuel or wasted. They can

be economically converted to pulp for making paper and paper-board.

Wheat straw and river grass are already being used for paper making,

more mills can be planned on these raw materials.

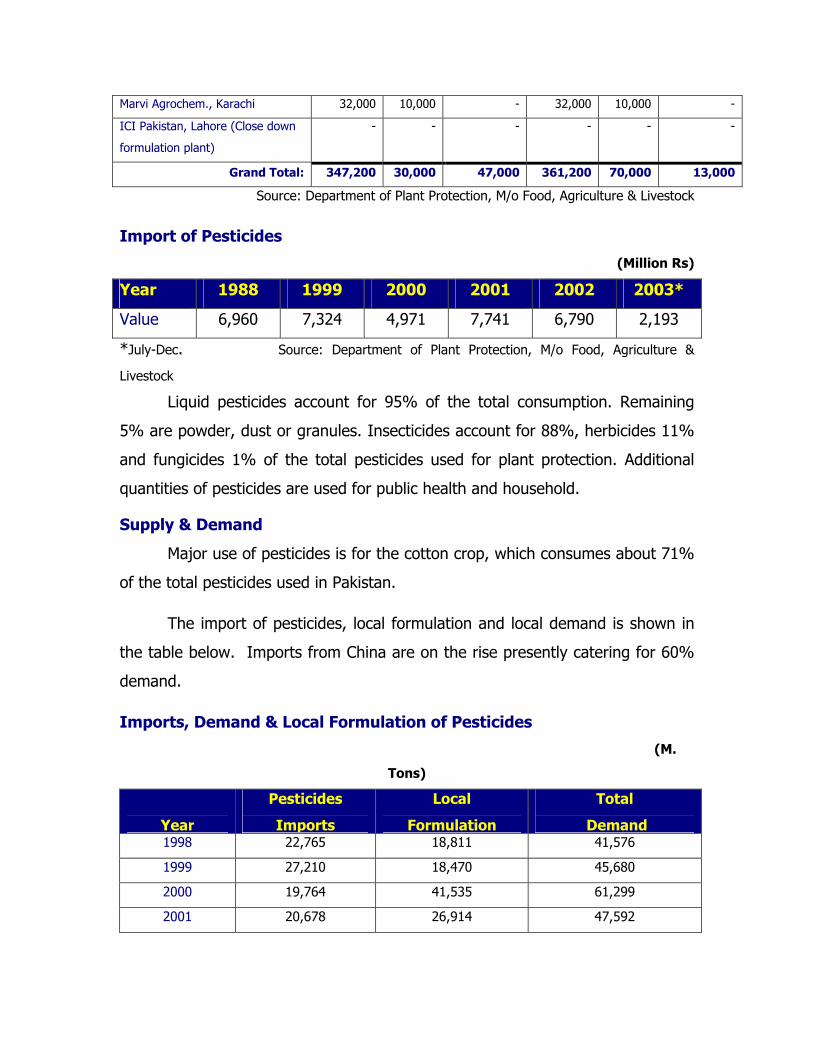

8. Pesticides

Pesticides have become essential for better output of the agricultural

products but this sector lacks a base in the country. The imports are rising,

exceeding Rs 7 billion during 2001-02. It is not possible to manufacture all active

ingredients in the country because of the absence of petrochemical base and the

lack of required R&D facilities. However, a few major active ingredients can be

manufactured utilizing Chinese experience. Special attention is required to be

given to the insecticides, used for cotton, (about 71% of total consumption in

the country) and their active ingredients (poisons) for their local manufacture.

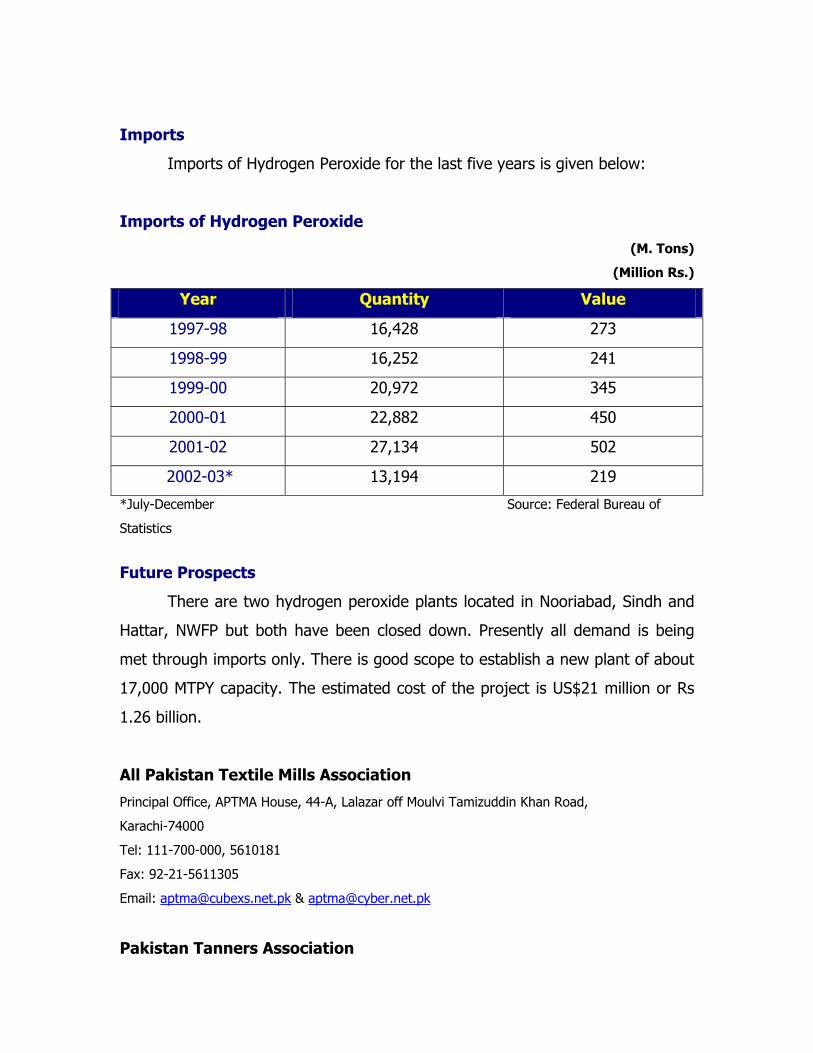

9. Hydrogen Peroxide

Hydrogen peroxide is extensively used in textile processing and in excess

of 20,000 M. tons are being imported every year. Two existing plants in Pakistan,

one in Nooriabad and other in Hattar, have closed down and all local demand is

being met through imports. There is scope to establish a modern technology

plant of about 17,000 MTPY capacity. The estimated cost of the project is US$21

million or Rs 1.26 billion. Hydrogen peroxide if set up within Ammonia complex

can save some capital cost.

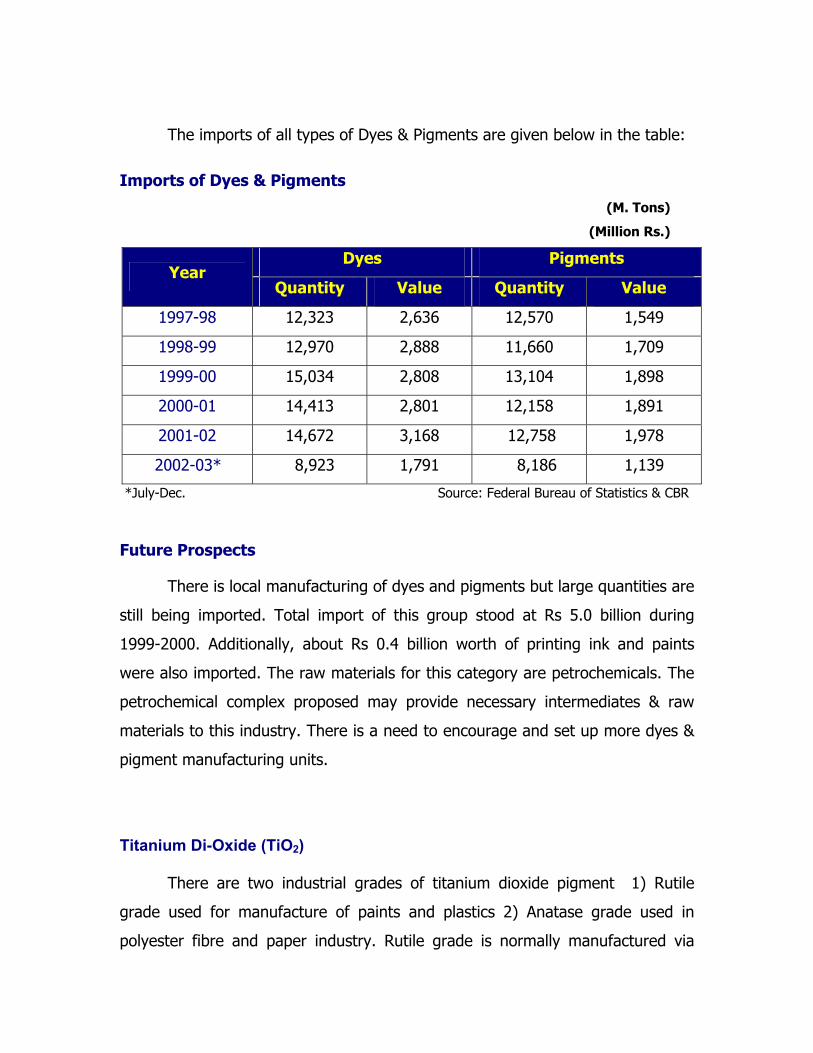

10. Dyes & Pigments

There is local manufacturing of dyes and pigments but large quantities are

still being imported. Total import of this group stood at about Rs 5.0 billion

during 2001-02. The raw materials for this category are petrochemicals.

11. Titanium Dioxide

There are two industrial grades of titanium dioxide pigment (i) Rutile

grade used for the manufacture of paints and plastics and (ii) Anatase grade

used in Polyester Fiber and paper industry.

It looks practical to establish a 10,000 MTPY facility to manufacture

anatase grade to cater needs of polyester fiber industry of Pakistan. Sulfuric acid

one of the major raw materials is being manufactured in Pakistan and other

material Ilmenite can be either imported or locally available Ilemenite can be

upgraded. The capital cost is estimated to be around US$ 35 million.

12. Alkyl Benzene Sulfonates (detergent base)

The rising demand for detergents calls for setting up manufacturing

facilities for its basic ingredient like, dodecylbenzene or tri-decylbenzene

sulfonate. There are few local producers based on imported raw materials.

Presently, more than Rs 1.5 billion worth of surface acting agents are being

imported. The proposed petrochemical complex in the country will provide

benzene locally to produce alkyl benzene and then the alkyl benzene sulfonates.

13. Essential Oils

There is variety of essential oils and they find use in perfume and food

industry. The raw materials are leaves and flowers of natural plants available in

Pakistan. These are high technology projects but purity of products gives value

addition. Because of the abundant flora and fauna available, production of

essential oils should be encouraged to substitute import of perfumes which are

more than Rs 0.5 billion per year. High quality essential oils can also be

exported. In this regard collaboration with France can be beneficial.

14. Inorganic Salts

Large quantities of inorganic chemicals are being imported totaling Rs 5.8

billion. These chemicals include selected inorganic salts worth Rs 1 billion.

Producing inorganic salts locally can save large foreign exchange. It is to

be noted that minerals for these inorganic salts are available in Pakistan and they

are relatively easier to manufacture. The costs for such projects are generally

low because most of the expertise and engineering facilities are available locally.

15. Manufacture Of Potassium Chlorate (KCLO3)

As evident from imports in recent years, the present demand for KCL03 is

about 3000 MTPY. Virtually the entire demand is in the match industry, which is

being met through imports. The manufacturing process for KCLO3 is based on

the electrolysis of potassium chloride in the presence of sodium chloride. The

total project cost of an economic sized plant with a capacity of 3000 MTPY is

broadly estimated at Rs. 180-200 million based on a budgetary Chinese price.

16. Manufacture of Basic Chromium Sulphate from Chromite (Cr2SO4)

Presently the entire demand for Basic Chromium Sulphate (BCS) used for

leather tanning, is being met from imports as well as from local production.

Considerable manufacturing capacity for BCS from chromite is presently

unutilized due to the closure of two plants for various reasons. Barring small

production of BCS from Chromite at Industrial Chemicals, Karachi. The entire

local production of BCS is confined to the manufacture of BCS from imported

sodium dichromate. This needs to be discouraged as the value addition in the

case of BCS to be manufactured from Chromite is far greater than BCS produced

from sodium dichromate. Moreover the foreign exchange savings are much

higher in the BCS production from Chromite as compared to BCS produced from

sodium dichromate.

17. Manufacture of Cigarette Filter Tows and other chemicals Ethyl Alcohol produced from Molasses can also be used for chain

production of Acetaldehyde, Acetic Acid, and Acetic Anhydride. Acetic Anhydride

when reacted with cotton linters from ginning mills gives Polymers which may be

used for production of x-ray films, Photo films, spectacle frames, cigarette filter

tows. Cigarette filter tows import alone is around Rs. 1 billion which may be

substitute following this chain production.

18. Smokeless Coal for fuel

Smokeless coal can be produced by proper blending of Coal, Calcium

Oxide and baggasse, all are abundantly available in Pakistan. This mixture does

not produce smoke or smell on combustion and therefore it is more acceptable

as domestic and industrial fuel. In 1989, M/s. JICA submitted a feasibility report

titled “Feasibility Study Report on Smokeless Coal Briquettes” to the Ministry of

Petroleum & Natural Resources and strongly recommended the use of smokeless

briquettes in the country. JICA’s recommended actions are supported in order to

utilize local coal resources.

19. Manufacture of Gum Rosin and Turpentine Oil

Vast forest of Pine trees exist in Hazara and Azad Kashmir. Gum

from these trees can be used for the production of Gum Rosin and Turpentine

oil. Some sort of mechanism needs to be evolved to encourage auctioning of

Pine tree areas for extraction of Gum instead of cutting them. Once gum is made

available. The technology is available locally. This local manufacture can result in

US$ 4 – 5 million saving of foreign exchange which is being spent in the import

of Gum rosin and Turpentine.

20. Manufacture of Vinyl Acetate Monomer and Butyl Acrylate

o Vinyl Acetate Monomer (VAM)

VAM is used for the manufacture of Poly Vinyl Acetate (PVA)

Emulsion. The current requirement of PVA Emulsion in the country

is around 35,000 MTPY. VAM requirement for this is around 15,000

MTPY which is currently being imported in bulk.

o Butyl Acrylate

Butyl Acrylate is used for the manufacture of Acrylic binders used in

Textile, leather and paint industries. The current requirement of

Acrylic binders in the country is around 20,000 M. Tons. For this

about 10,000 MTPY of Butyl Acrylate is required which is being

imported.

o Prospects

Both VAM and Butyl Acrylate can be manufactured locally if the

feedstock i.e. Propylene and Ethylene is made available. These can

be made available either through Petrochemical complex or import

via land route.

1. IMPORTANCE OF CHEMICAL INDUSTRY

Because of the wide variety of products it is difficult to agree on a

common definition of the chemical industry across countries. In particular, fibers,

rubber and plastic processing can be either included or excluded. Countries that

include fibers in Chemical Industry are: Germany, UK, Italy, Spain, Netherlands,

Ireland, Portugal, Greece, Sweden, Austria, Finland, Norway and Poland.

Countries excluding fibers are France, Belgium and Denmark. Belgium also

includes rubber and plastic products in the definition of chemical industry.

Chemicals are divided in two main categories from value addition

point of view. Those produced in large and bulk quantities but with lower value

addition are called Commodity Chemicals. Examples are fertilizers and soda

ash, etc. Specialty Chemicals are those produced in smaller quantities with

higher value addition. Examples are dyes & pigments, pharmaceuticals and

enzymes, etc.

Chemical sector plays a vital role in the economic development of

any country. Pakistan has not yet utilized potential of chemical sector. Realizing

the importance of this sector, this study was initiated by the Experts Advisory

Cell (EAC), as per directive of Minister and Secretary, Ministry of Industries and

Production. The main objective of the study was to highlight the constraints in

the development of the chemical industry, suggest policy recommendations and

identify potential projects based on supply and demand gap as well as possible

export considerations. Extensive discussions with experts, representatives of

trade and industry and chemical engineers of repute has led to the conclusion

that development of chemical industry is vitally important and a concerted effort

must be made to cover the lost ground.

Chemical sector is diversified and covers a vast range of products.

Following are the major end products under this sector:

o Petrochemicals o Soda Ash & Sodium

Bicarbonate

o Fertilizers o Caustic Soda & Chlorine

o Synthetic Fibers o Sulfuric Acid & Other acids

o Alcohol from Molasses o Organic Chemicals

o Pesticides o Dyes & Pigments

o Plastics & Resins o Textile & Tannery Chemicals

o Paints & Varnishes o Water Treatment Chemicals

o Oleo Chemicals & Soaps,

Detergents and Cosmetics

o Food Chemicals

o Paper & Paper board o Essential Oils

o Glass

464 452

225

184

63 50 48

-50

50

150

250

350

450

550

US

$ B

illio

n

WE

STE

RN

EU

RO

PE

US

A

JAP

AN

AS

IA

OTH

ER

EA

STE

RN

EU

RO

PE

LATIN

AM

ER

ICA

WORLD CHEMICAL SALES

2. OVERVIEW

2.1 GLOBAL

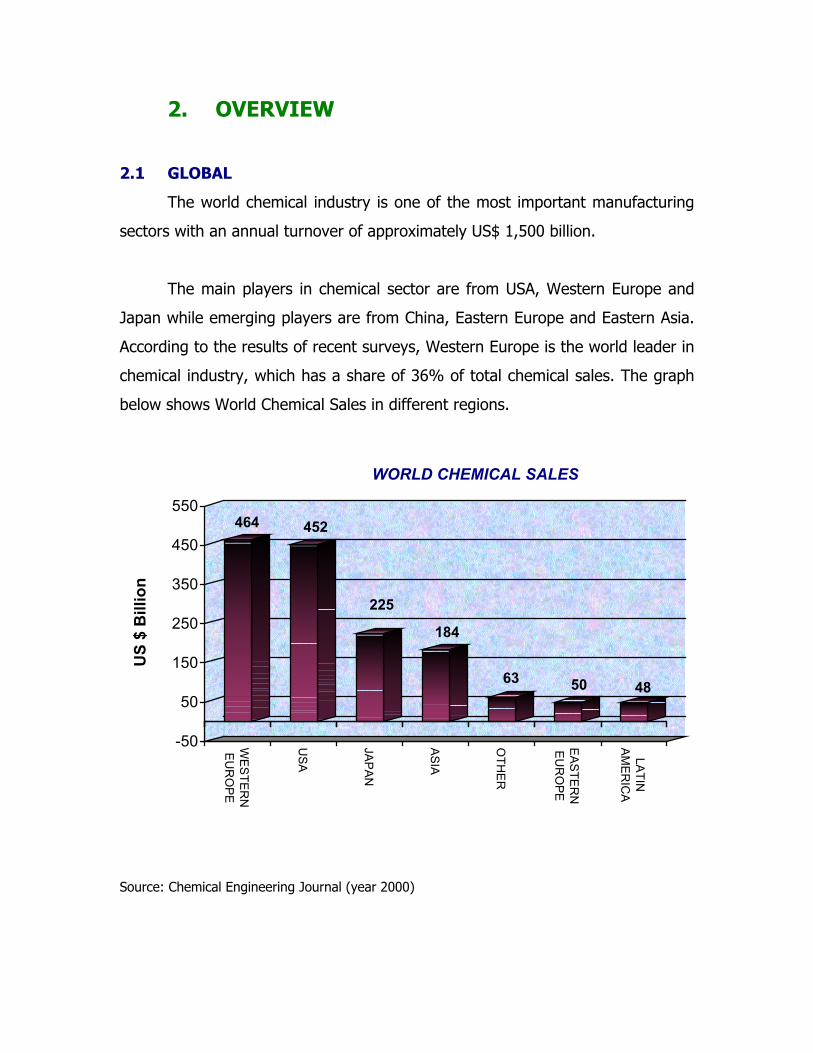

The world chemical industry is one of the most important manufacturing

sectors with an annual turnover of approximately US$ 1,500 billion.

The main players in chemical sector are from USA, Western Europe and

Japan while emerging players are from China, Eastern Europe and Eastern Asia.

According to the results of recent surveys, Western Europe is the world leader in

chemical industry, which has a share of 36% of total chemical sales. The graph

below shows World Chemical Sales in different regions.

Source: Chemical Engineering Journal (year 2000)

The chart below shows the distribution of sales of chemicals produced by

the Western European countries. Seven West European countries contributed

more than 88% chemical turn over as shown below.

7%

12% 9%11%

12%

8%

24% 17%

Belgium Itly Great Britian FranceGermany Spain Netherlands Others

The leading companies of the global chemical industry are BASF

(Germany), Du Pont (U.S.A.), Dow Chemical (U.S.A.), Exxon Mobil (U.S.A.),

Bayer (Germany), Total Fina Elf (France), Degussa (Germany), Shell

(U.K./Netherlands), ICI (U.K.), BP (U.K.), Akzo Nobel (Netherlands), Sumitomo

Chemical (Japan), Mitsubishi Chemical (Japan) and Mitsui Chemicals (Japan).

The world chemical sales and profits of 20 leading companies are shown

in table below.

Performance of Top 20 Chemical Companies

US$ Million

Company

Sales

Operating Profits

Capital

Spending

R&D

Spending1 BASF (Germany) 30,790.5 2,604.6 3,345.3 974.8

2 Dupont (U.S.A) 28,406.0 3,207.0 1,925.0 1,776.03 Dow Chemical

(U.S.A) 23,008.0 2,266.0 1,349.0 892.0

4 Exxon Mobil (U.S.A) 21,503.0 1,161.0 1,468.0 NA5 Bayer (Germany) 19,295.2 1,824.2 1,752.2 949.96 Total Final Elf

(France) 19,203.1 1,499.0 124.5 460.7

7 Degussa (Germany) 15,584.1 619.1 1,034.6 499.48 ICI (UK) 11,746.7 874.8 438.2 266.89 BP (UK) 11,247.0 760.0 1,585.0 NA10 Akzo Noble

(Netherlands) 9,364.3 769.3 470.8 267.2

11 Sumitomo Chemical (Japan)

9,354.3 749.3 516.0 NA

12 Mitsui Chemicals (Japan)

8,720.3 505.8 570.9 NA

13 Dai-Nippon Ink & Chemicals (Japan)

7,512.7 407.1 387.8 NA

14 Equistar (U.S.A) 7,495.0 334.0 NA NA

15 DSM (Netherlands) 7,295.0 620.0 566.6 243.216 Henkel (Germany) 7,215.8 599.8 782.2 185.217 SABIC (Saudi

Arabia 7,119.8 1,620.7 NA NA

18 Rhodia (France) 6,835.3 457.0 463.4 195.319 Air Liquide (France) 6,590.1 1,028.2 836.6 87.820 Union Carbide

(U.S.A) 6,526.0 596.0 459.0 152.0

TOTAL 264,812.2 22,502.9 18,075.1 6,950.3

Source: Chemical Engineering News July 2001

2.2 PAKISTAN

At the time of independence, chemical industry in Pakistan was practically

non-existent. Over the years, some traditional sectors have developed, however

the Chemical Industry in Pakistan is still at a very nascent stage.

In early 50’s, PIDC was setup by the Government, for industrialization of

the country. As a result, a large chemical estate comprising Pak American

Fertilizers, Maple Leaf Cement, Antibiotics (Penicillin) and Pak Dyes & Chemicals,

was established at Iskanderabad (DaudKhel), district Mianwali. This estate

played an important role and served as a nucleus for chemical industry in

Pakistan.

In 1960’s, another chemical complex was set up in private sector at Kala

Shah Kaku, Lahore. Chemical factories also started emerging at Karachi due to

the investment friendly policies which gave confidence to the investors.

In early 1970’s, private industries were nationalized with the result that

the fast growing chemical sector started to decline. The growth of chemical

sector could never pickup.

The imports of chemicals are on increase in value and volume terms. This

indicates the vast potential for the chemical industry in Pakistan. There were

some investments in the recent years in the production of Pure Terephthalic Acid

(PTA), fertilizers, polyesters and Poly Vinyl Chloride (PVC). However investments

in the petrochemicals complex and other chemicals are urgently required to be

self-reliant in basic organic and inorganic chemicals.

It is to be noted that huge capacities for petrochemical manufacturing are

available in the neighboring countries of Middle East, Far East and Iran. Experts

opine that a Petrochemical Complex should have been set-up when the tariff

protection was highest. However, ways and means need to be found, as setting

up of a Petrochemical Complex would result in hundreds of downstream small

and medium enterprises.

Some selected chemical sectors have developed to meet the local

demand. They include fertilizers, Polyesters, PTA, PVC and some basic chemicals.

Total investment in chemical industry stands at around Rs 360 billion as shown

below.

Investment in Chemical Sector

1947 to 2002

Sectors Units Fertilizers 10 87

Sugar 76 50

Synthetic Fibers + PTA 6 55

Cement 24 44

PVC + Others 1 (PVC)+ Others 35

Paper & Paper Board 97 28

Industrial Chemicals 18 22

Edible Oil 155 7

Glass 31 11

Pharmaceuticals 21

Total 360

Source: Respective Associations/Estimated figures

2.2.1 CHEMICAL IMPORTS

Pakistan’s total imports have exceeded US$ 10 billion out of which

chemicals imports constitute approximately US$ 2 billion. A detailed list of the

main chemicals imported during recent past (1997-98 to 2001-02) along with

their quantities & values is attached as Annexure-VI.

The import value of chemicals remained about 17% of total imports

during the last nine years and it was 15.5% in the year 2001-02. This situation

calls for special attention to the development of the chemical sector that

constitutes one of the major portions of Pakistan’s import bill.

Pakistan’s Imports

US$ Million

Year

Total Imports

Import of Chemicals

Chemicals Import %age

1991-92 9,253.3 1,468.9 15.91992-93 9,963.2 1,493.9 15.01993-94 8,561.6 1,494.0 17.51994-95 10,401.4 1,587.4 15.31995-96 11,804.8 2,187.4 18.51996-97 11,894.8 1,981.4 16.71997-98 10,116.4 1,791.5 17.71998-99 9,431.7 1,812.0 19.21999-00 10,309.4 1,997.2 19.42000-01 10,728.9 1,903.9 17.72001-02 10,403.8 1,354.3 15.5

Source: Economic Survey 2001-02

The import data of 2001-02 based on the major categories of chemicals is

presented below. It is noted that five top imports are of organic chemicals

(including petrochemicals), plastics & resins, pharmaceuticals, pesticides and

fertilizers. This suggests the direction of future investments in the chemical

sector in Pakistan.

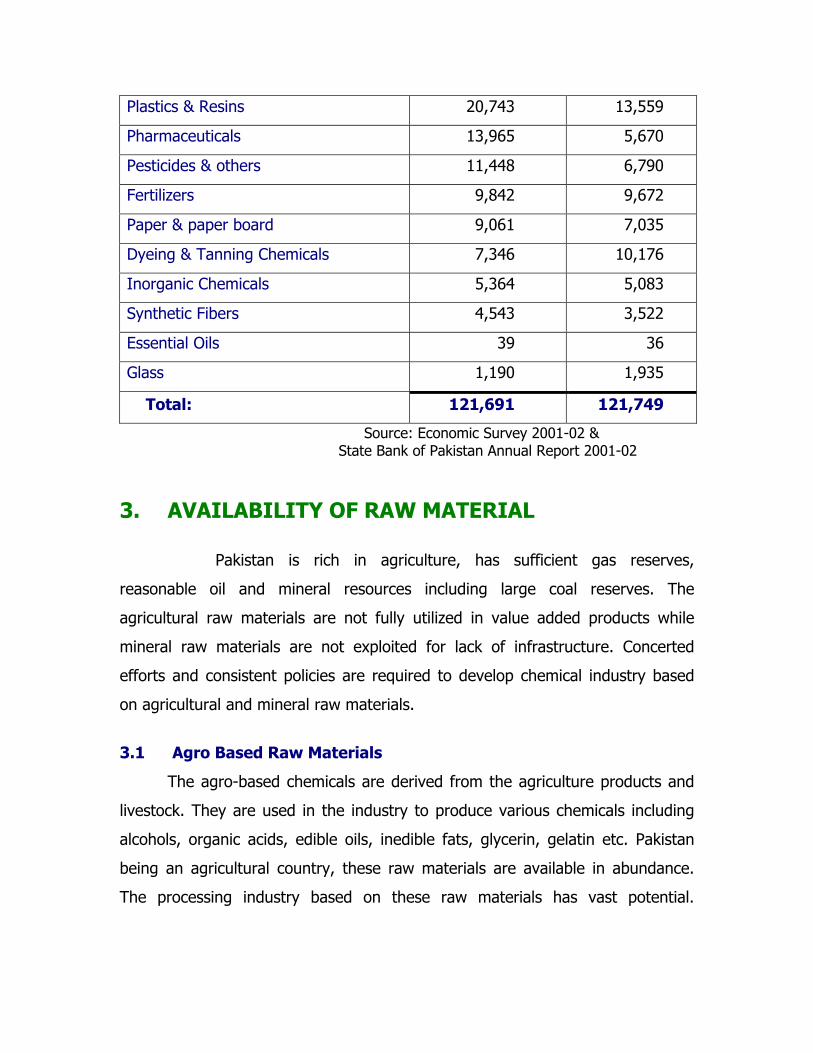

Chemical related groups Import (Million Rs.)

Chemical Group Imports 2000-01

Imports 2001-02

Organic Chemicals 38,150 58,271

Plastics & Resins 20,743 13,559

Pharmaceuticals 13,965 5,670

Pesticides & others 11,448 6,790

Fertilizers 9,842 9,672

Paper & paper board 9,061 7,035

Dyeing & Tanning Chemicals 7,346 10,176

Inorganic Chemicals 5,364 5,083

Synthetic Fibers 4,543 3,522

Essential Oils 39 36

Glass 1,190 1,935

Total: 121,691 121,749

Source: Economic Survey 2001-02 & State Bank of Pakistan Annual Report 2001-02

3. AVAILABILITY OF RAW MATERIAL

Pakistan is rich in agriculture, has sufficient gas reserves,

reasonable oil and mineral resources including large coal reserves. The

agricultural raw materials are not fully utilized in value added products while

mineral raw materials are not exploited for lack of infrastructure. Concerted

efforts and consistent policies are required to develop chemical industry based

on agricultural and mineral raw materials.

3.1 Agro Based Raw Materials

The agro-based chemicals are derived from the agriculture products and

livestock. They are used in the industry to produce various chemicals including

alcohols, organic acids, edible oils, inedible fats, glycerin, gelatin etc. Pakistan

being an agricultural country, these raw materials are available in abundance.

The processing industry based on these raw materials has vast potential.

Following agro based raw materials and by products are available for conversion

to chemicals.

o Molasses

o Bagasse

o Rice husk

o Vegetable Seeds

o Starches

o Cotton Linters

o Wheat straw

o Wood

o Animal fats and bones

3.2 Natural Gas

Pakistan has proven gas reserves of 43.37 trillion cubic ft out of

which 15.78 trillion cubic ft has been consumed leaving 27.58 trillion cubic ft. of

balance reserves as of year 2002. Present gas consumption based on last two

years average is 900 billion cubic ft per year. There have been more discoveries

of natural gas in the recent years. Substantial quantity of gas reserves are being

used for domestic consumption, commercial purposes, industrial raw material

and fuel.

NATURAL GAS CONSUMPTION BY SECTOR2001-02

0.90%2.70%

38.20%

18.40%17.50%

16.70%

4.90%

0.90% Power

Gen. Industry

Domestic

Fertilizer (feed)

Fertilizer (fuel)

Commercial

Cement

Transport (CNG)

An appropriate percentage (i.e. around 10%) of local gas resources

and the future gas imports from Tajikistan and Iran need to be dedicated for

producing value-added chemicals. Natural gas can be a raw material to produce

Ethylene (through acetylene route), Methanol and several downstream products.

3.3 Petroleum

Petroleum is another major source of several petrochemicals. World

wide 90 to 93% oil and gas is consumed for energy purposes and balance 7-10%

is converted to petrochemicals.

a) Crude Oil

Pakistan is deficient in crude oil resources. The left over oil reserves

are only 40.27* million Ton of Oil Equivalent (TOE) (300.2 million barrels).

Pakistan‘s present annual production rate is 3.1∗ million TOE (63,500 barrels per

day). Pakistan’s yearly requirement is 10.4* million TOE. Only 30% of the total

crude oil requirement is therefore met by local crude production.

Naphtha, an intermediate product from refinery, is important for

the manufacture of petrochemicals. Pakistan produced 462,197 tons of naphtha*

during 2001-02. 180,000 tons additional naphtha is available from Attock

Refinery after the implementation of lead-free gasoline from July 2002. Present

availability of naphtha is therefore, about 600,000 tons/year.

b) Associated Gases

Associated gases contain higher hydrocarbons like Ethane, Propane

and Butane, etc which are produced from the oil fields in Punjab and Sindh.

Presently, there are 0.6 trillion cubic ft (17.8 million TOE) reserves available and

the production rate is 40 billion cubic ft (1,143,000 TOE) per year. These gases

can be converted to ethylene, propylene etc. but the gathering of these gases at

one point require large and complex pipeline system. However, the quantity is

not enough for a viable project.

∗ Source: Energy Year Book 2002

3.4 Minerals

Inorganic chemicals are mainly based on mineral resources and are used

for producing intermediate and final products. The main mineral reserves

available in Pakistan for chemical industry are given below:

o Coal

o Rock Phosphate

o Iron

o Sulfur (from Oil and Coal)

o Magnesite (Magnesium Carbonate)

o Chromites

o Kaoline (China Clay)

o Gypsum (Calcium Sulphate)

o Limestone (Calcium Carbonate)

o Soapstone (Silicates)

o Barite (Barium Sulphate)

o Rock salt (Sodium Chloride)

o Copper

The development of Thar Coal Field (the largest reserves) require around

5 years time, therefore projects based on these reserves should have to be

planned accordingly.

Pakistan needs to concentrate on the development of Petrochemical and

Chemical industry to utilize indigenouous coal, iron ore, phosphate rock reserves

and rock salt. A list of mineral resources and their production in Pakistan is given

in Annexure-III. The use of various minerals in the chemical industry is given in

Annexure-IV.

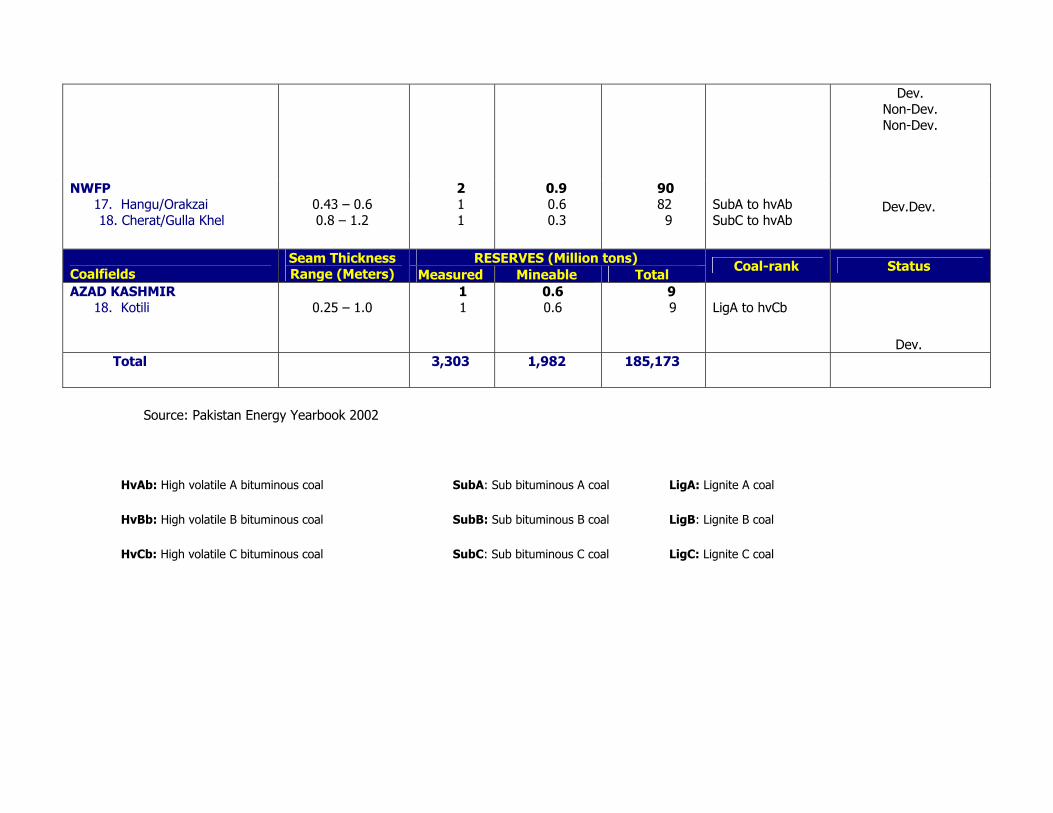

3.5 Coal

A total of 185,173 million tons of estimated coal reserves are available in

Pakistan with minable reserves of 1,982 million tons. Thar reserves in Sindh

Province are 175,506 million tons out of which 1,620 million tons are minable.

This coal having sulfur less than 3% and ash content with a range of 2.9 to

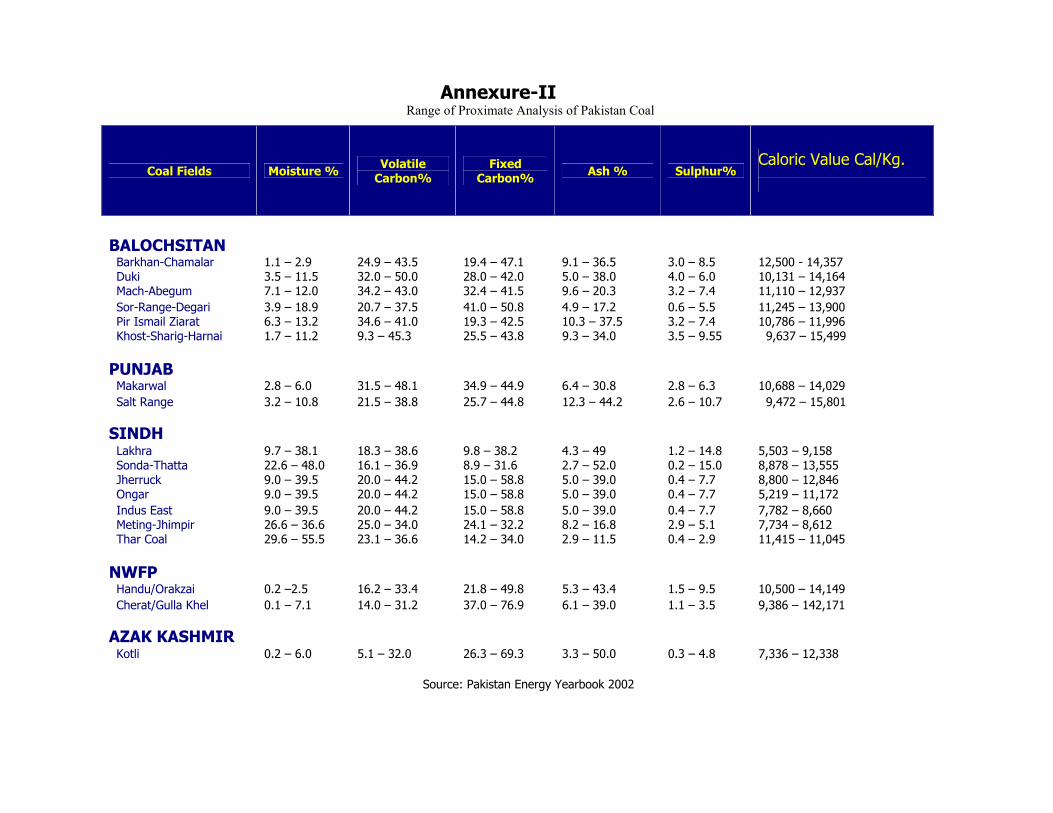

11.5% appear suitable for production of petrochemicals. Annexure I & II depict

coal reserves and analysis of Pakistani coal.

COAL CONSUMPTION BY SECTOR2001-02

Total: 4.24 Million Tonnes

72.50%

21.60%

5.90%Brick Kilns

Coke Use

Power

Generally, the value addition in chemical industry is much more than other

industrial sectors. It increases for commodity products to specialty and fine

chemicals and it is normally 10 to 200 folds taking crude oil value as the base.

Pakistan can exploit this situation only through vertical and horizontal

integration.

Although it is late yet no more time should be lost to develop

petrochemical industry in Pakistan. Local gas and coal reserves are in abundance

and they are of reasonable quality. Coal gasification technology to manufacture

petrochemicals is being used in USA, European countries and South Africa.

Technologies are available to manufacture chemicals from coal. Production of

value-added chemicals can make the project economically feasible. A suitable

technology may therefore, be acquired and used in Pakistan for Thar and Lakhra

coal reserves.

4. MAJOR CHEMICAL SUB-SECTORS

Pakistan has progressed well in the traditional sectors of fertilizers,

sugar, cement, caustic soda, soda ash and sulfuric acid. Other potential areas are

soaps, detergents, cosmetics, paints, dyes and pesticides. The petrochemical

sector needs much more attention because basic raw materials used for several

sub-sectors of chemical industry are not being manufactured in Pakistan, which

is only possible after the development of petrochemical industry.

Following sub-sectors have been discussed in the report:

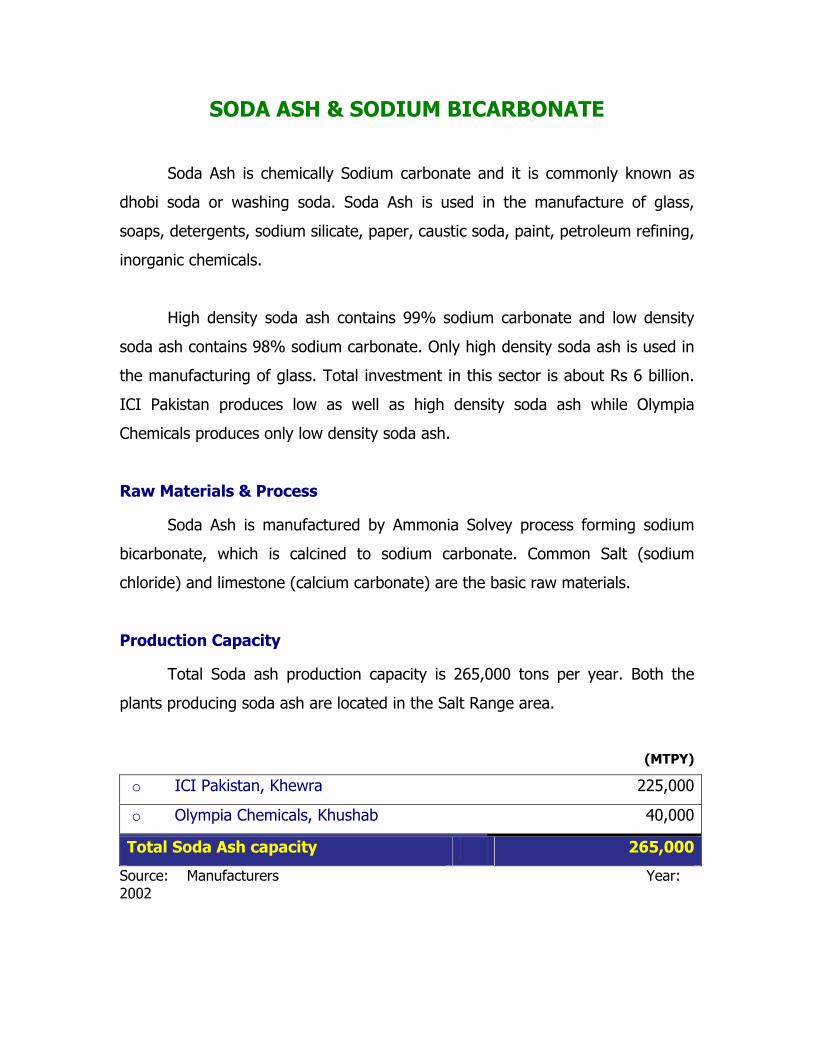

o Petrochemicals o Soda Ash & Sodium Bicarbonate

o Fertilizers o Caustic Soda & Chlorine

o Synthetic Fibers o Sulfuric Acid & Other acids

o Alcohol from Molasses o Organic Chemicals

o Pesticides o Dyes & Pigments

o Plastics & Resins o Textile & Tannery Chemicals

o Paints & Varnishes o Water Treatment Chemicals

o Oleo Chemicals

o Food Chemicals

o Soaps, Detergents and

Cosmetics

o Essential Oils

o Paper & Paper board

o Glass

PETROCHEMICALS, BTX, CARBON BLACK, MEG

Petrochemicals

Petrochemical products currently form an essential base for production of

wide range of industrial and consumer products. Petrochemical industry is

termed as one of the fastest growing industrial sub-sector and has very well

contributed to the objective of rapid progress and balanced expansion of

manufacturing sector.

Petrochemical products are broadly classified into two group i.e. basic and

end-products. The basic product group includes ethylene, propylene, butadiene

and aromatics, while the end-products include plastics, synthetic fibres and

elastomers. The petrochemical products offer to a large extent an ideal

substitute for conventional materials such as wood, metals, jute, natural rubber,

etc. in which Pakistan is deficient. Therefore, there is substantial scope for

development of petrochemical industry in Pakistan.

At present, the petrochemical industry of Pakistan is limited to production

of polyvinyl chloride (based on imported VCM), synthetic fibers, i.e. polyester,

polyamide, aromatics (Benzene, Toluene, Xylene), Purified Terephthalic Acid

(PTA) and carbon black.

During last three decades repeated efforts have been made to develop a

project capable of producing basic petrochemicals. In this connection numerous

studies have been carried out for production of basic petrochemicals i.e.

ethylene, propylene, etc. utilizing the alternate feed stocks i.e. naphtha,

associated gases (ethane, propane), natural gas and molasses (a by product of

sugar industry). However, despite interest and efforts no significant development

has taken place as far as production of basic petrochemicals are concerned.

The factors responsible for non-development of basic petrochemical

industry include:

o High capacity of world scale basic petrochemical production facilities.

o Complexity and high level of the technology involved.

o High level of capital outlay required.

o Market size limitations vis-à-vis world scale plants.

o Relatively lower differential in tariffs of imported raw material and end

products.

Pakistan has no facility to produce basic petrochemicals like Ethylene,

Propylene, Butadiene, Styrene, etc. and they are being imported in bulk. Out of

long list of petrochemicals, only few are being produced locally. They include

Pure Terephthalic Acid (PTA), BTX and carbon black.

Petrochemicals provide raw materials for plastics, detergents, dyes, paints

& varnishes and pesticides etc. They are also used as additives in the lubricating

oils. Most of the specialty and fine chemicals belong to the petrochemical group.

Their production and marketing is monopolized by few global giants.

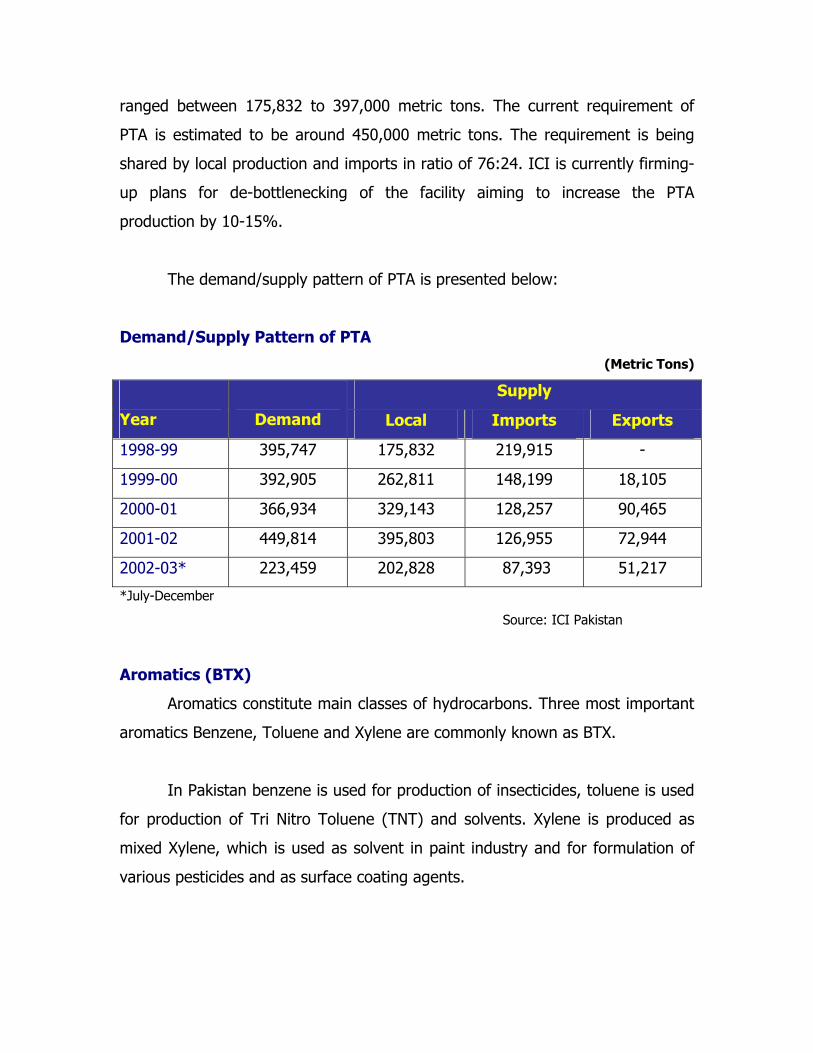

Pure Terephthalic Acid (PTA)

Purified Terepthalic Acid (PTA) is basic raw material for production of

polyesters. PTA is produced by oxidation of paraxylene in a solvent i.e. acetic

acid. Till recently, all the PTA requirements of the country were met through

imports. In 1998 ICI Pakistan setup PTA production facility at Port Qasim,

Karachi. The facility is capable of producing 400,000 MTPY of PTA with an

investment of US$ 450 million. The plant production during last four years

ranged between 175,832 to 397,000 metric tons. The current requirement of

PTA is estimated to be around 450,000 metric tons. The requirement is being

shared by local production and imports in ratio of 76:24. ICI is currently firming-

up plans for de-bottlenecking of the facility aiming to increase the PTA

production by 10-15%.

The demand/supply pattern of PTA is presented below:

Demand/Supply Pattern of PTA

(Metric Tons)

Supply

Year

Demand Local Imports Exports

1998-99 395,747 175,832 219,915 -

1999-00 392,905 262,811 148,199 18,105

2000-01 366,934 329,143 128,257 90,465

2001-02 449,814 395,803 126,955 72,944

2002-03* 223,459 202,828 87,393 51,217

*July-December

Source: ICI Pakistan

Aromatics (BTX)

Aromatics constitute main classes of hydrocarbons. Three most important

aromatics Benzene, Toluene and Xylene are commonly known as BTX.

In Pakistan benzene is used for production of insecticides, toluene is used

for production of Tri Nitro Toluene (TNT) and solvents. Xylene is produced as

mixed Xylene, which is used as solvent in paint industry and for formulation of

various pesticides and as surface coating agents.

Paraxylene and orthoxylene are derived from mixed Xylene. Paraxylene is

used as a raw material for production of PTA while orthoxylene is used for

production of phthalic anhydride.

Historically, BTX requirements of the country have been met from local

production and imports. The local production was from a small unit of National

Refinery Limited. The unit has a capacity of 25,500 MTPY of Benzene, Toluene

and Xylene. The unit uses reformat as feedstock. Throughout its existence the

plant has been operating at lower capacity owing to operational and production

economics. This unit is no longer in operation.

After start of ICI’s PTA production facility paraxylene imports have been

started. During the last two years the imports of paraxylene ranged between

250,000 to 300,000 metric tons.

Orthoxylene imports started in early 1990s, when phthalic anhydride plant

of Nimir Chemicals having capacity of 12,000 MTPY started production. During

last three years the imports of orthoxylene ranged between 2,500 to 3,500

metric tons.

BTX are the building blocks for PTA, polyesters, Nylon, DOP, polystyrene,

explosives, detergents, phenol, aniline and other down stream products. Large

quantities of Xylene and Toluene are being imported and total BTX imports were

312,791 tons with a value of Rs 7.9 billion during 2001-02.

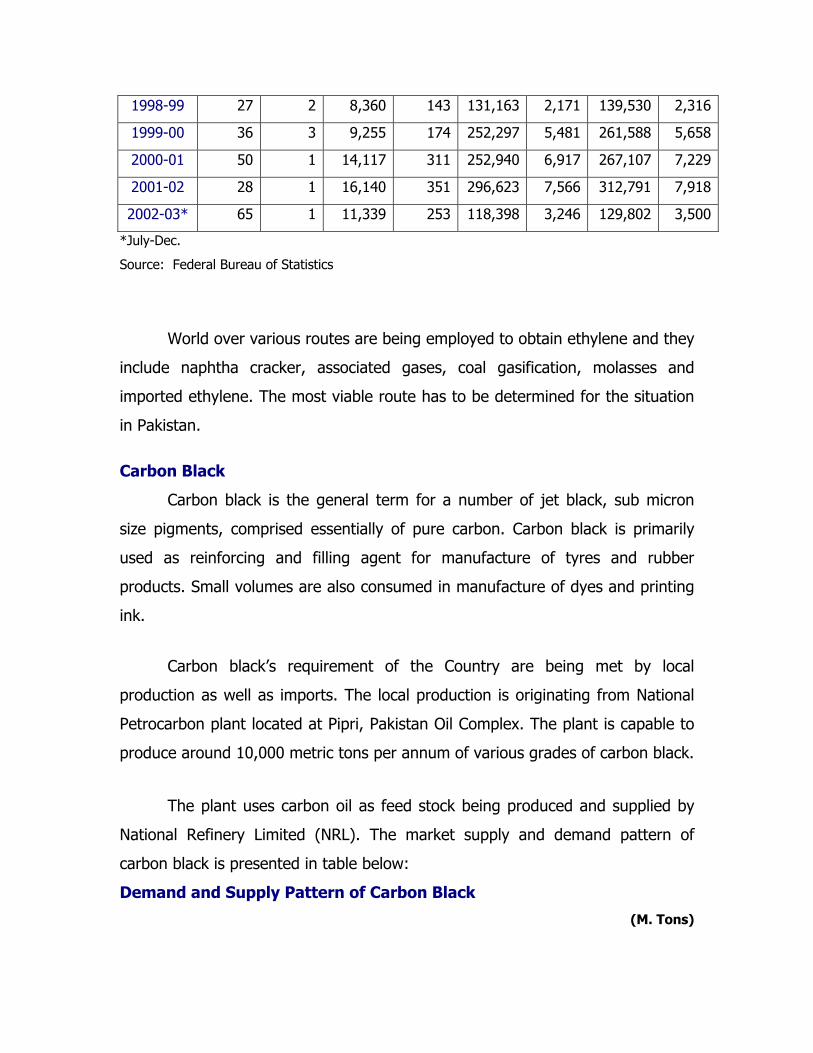

BTX Imports

(M. Tons)

(Million Rs.)

Benzene Toluene Xylene Total (BTX) Year Qty. Value Qty. Value Qty. Value Qty. Value

1997-98 49 2 6,205 113 14,827 281 21,081 396

1998-99 27 2 8,360 143 131,163 2,171 139,530 2,316

1999-00 36 3 9,255 174 252,297 5,481 261,588 5,658

2000-01 50 1 14,117 311 252,940 6,917 267,107 7,229

2001-02 28 1 16,140 351 296,623 7,566 312,791 7,918

2002-03* 65 1 11,339 253 118,398 3,246 129,802 3,500

*July-Dec.

Source: Federal Bureau of Statistics

World over various routes are being employed to obtain ethylene and they

include naphtha cracker, associated gases, coal gasification, molasses and

imported ethylene. The most viable route has to be determined for the situation

in Pakistan.

Carbon Black

Carbon black is the general term for a number of jet black, sub micron

size pigments, comprised essentially of pure carbon. Carbon black is primarily

used as reinforcing and filling agent for manufacture of tyres and rubber

products. Small volumes are also consumed in manufacture of dyes and printing

ink.

Carbon black’s requirement of the Country are being met by local

production as well as imports. The local production is originating from National

Petrocarbon plant located at Pipri, Pakistan Oil Complex. The plant is capable to

produce around 10,000 metric tons per annum of various grades of carbon black.

The plant uses carbon oil as feed stock being produced and supplied by

National Refinery Limited (NRL). The market supply and demand pattern of

carbon black is presented in table below:

Demand and Supply Pattern of Carbon Black

(M. Tons)

Supply Year Demand

Local Imports

1998-99 10,921 5,054 5,867

1999-00 11,369 6,153 5,216

2000-01 8,922 4,523 4,399

2001-02 8,212 5,148 3,064

2002-03* 3,274 2,638 1,587

*July-December

Source:

National Petrocarbon (Pvt.) Ltd. (2002-03*)

Historically very small quantity of carbon black has been exported.

The carbon black market of Pakistan has remained limited owing to

minimal expansion in local tyre/rubber products manufacturing capacity and its

production. This is primarily due to large scale, legal as well as illegal imports of

tyres in the country.

Mono-ethylene Glycol (MEG)

Mono-ethylene glycol (MEG) is one of the most important synthetic

organic liquid used for manufacturing of polyester fiber and as anti-freezing

agent. In Pakistan MEG is primarily being consumed as input for manufacturing

of polyester fiber and yarn. The quantum of MEG being consumed as anti-

freezing agent is very small. At present, all the requirements of MEG are being

met from imports. In 2001-02 122,000 metric tons of MEG was imported at a

value of Rs. 3.12 billion (US$ 52.14 million). The imports during 1997 – 2002 are

presented below:

Imports of Mono-ethylene Glycol (MEG)

(M. Tons)

(Million Rs.)

Imports

Year Quantity Value

1997-98 126,623 3,675

1998-99 166,792 3,251

1999-00 174,024 4,447

2000-01 174,943 4,828

2001-02 121,875 3,129

2002-03* 105,753 2,896 *July-December

Source: Federal Bureau of Statistics

The MEG requirements during last decade have been increasing at

an annual growth rate of 10%. By 2009-10 the MEG requirements will increase

to 260,000 metric tons, which justify the setting up of a Petrochemical Complex.

Demand Pattern

The demand pattern of major petrochemical products during 2002-2010 is

presented below:

Demand Pattern of Major End-Petrochemicals

(000 M. Tons)

Estimated Demand

Product

Consumption

2001-02 2005-06 2009-10

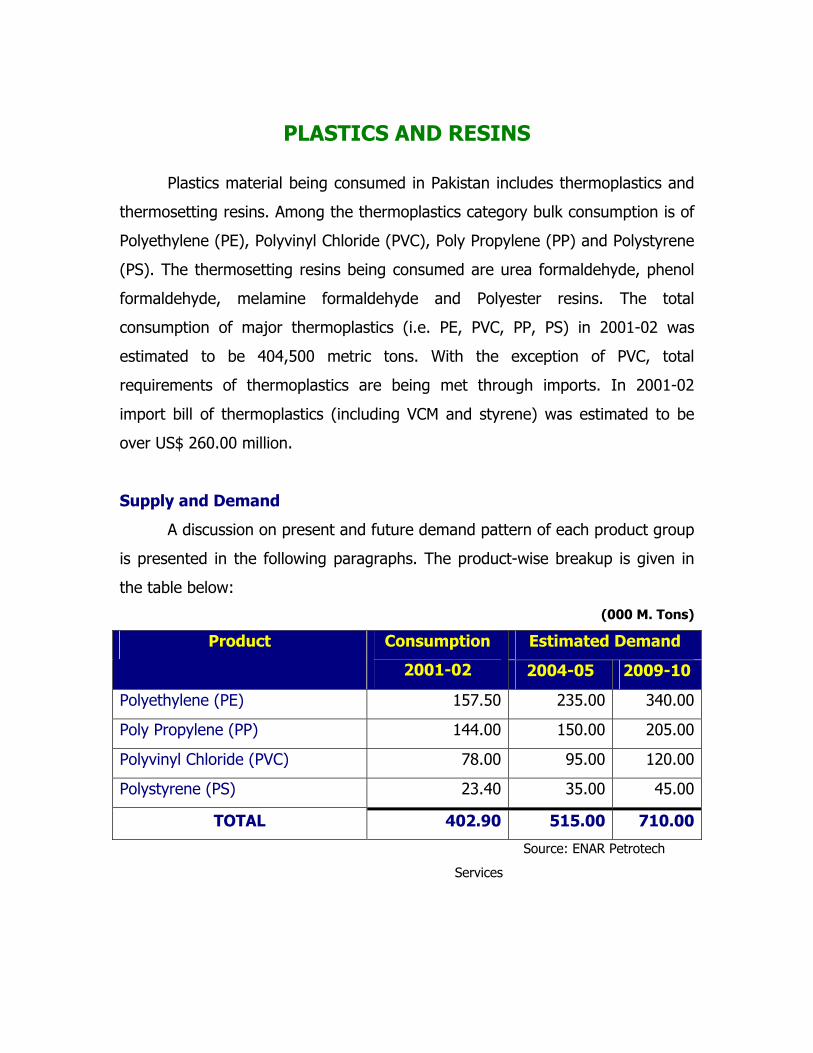

Plastic (PE, PP, PVC & PS) 403.00 515.00 710.00

Synthetic Fibres (Polyester,

Acrylic & Viscose, etc)

500.00 700.00 900.00

Polyester Inputs:

• PTA 450.00 570.00 720.00

• MEG 160.00 220.00 330.00

Aromatics BTX 20.00 25.00 30.00

Paraxylene 300.00 365.00 450.00

Synthetic Rubber 20.00 25.00 30.00

TOTAL 1,853.00 2,420.00 3,170.00

Source: Enar Petrotech Services

Future Prospects

The table above justifies setting up of a Petrochemical complex, however

the project shall be economical if a prudent policy is adopted and adequate

incentives are offered. The need for establishing the facilities to manufacture

basic petrochemical products has long been realized. All the previous reports on

chemicals sector have recommended the establishment of a petrochemical

complex through any viable route. The strongest of all recommendations was the

setting up a Hydro Cracker or Naphtha cracker plant.

The hydrocarbon resources of the country are largely being used for

energy requirements i.e. fuel. These could be utilized for the manufacturing of

high value-added petrochemicals. Natural gas is however also being used for the

manufacture of ammonia, as an intermediate for the production of fertilizers.

The import data provided in the table reveals that a major portion of

Pakistan’s total imports consist of petrochemicals, i.e., ethylene, propylene,

butadiene, benzene, toluene, xylene and their derivatives. It is thus, essential

that serious efforts be made to manufacture these petrochemicals locally in order

to save foreign exchange and to attain self-reliance.

The downstream industries based on Petrochemical products such as

paints, plastics, synthetic fibers, rubber, etc. have grown considerably.

Therefore, the petrochemical complex is very much needed to meet the

downstream growing demand in the country and to establish a strong backward

integration for the development of other non-traditional sectors.

Dr. Farrukh Akhtar, a consultant prepared a report regarding the

development of petrochemicals in Pakistan (Copy attached as appendix). He has

focused on the importance of this sector and has suggested to prepare a road

map for at least next 50 years. He has also emphasized on adopting a process of

identifying future projects.

World over various routes are being employed to obtain ethylene and they

include naphtha, associated gas, coal gasification, molasses and imported

ethylene. The most viable route has to be determined for the situation in

Pakistan. Options for the production of petrochemicals, available to Pakistan, are

detailed below:

o Naphtha Cracker

The technology for the production of petrochemicals from oil, by hydro

cracking or naphtha cracking, is well known and established. Naphtha is a

refinery by-product of crude oil. These are hydrogenated to get the desired basic

petrochemical olefins.

It is also to be noted that Pakistan depends heavily on crude oil imports.

Pakistan exported 392,411 MTPY of Naphtha during 2001-02.

The naphtha cracker helps to make olefins (ethylene, propylene etc) and

it has no direct role for the manufacturing of aromatics (BTX). The aromatics are

separated from the reformat of an oil refinery.

In order to know whether a naphtha cracker is viable in Pakistan, the

demand for down stream products (olefins) has been assessed and analyzed

below:

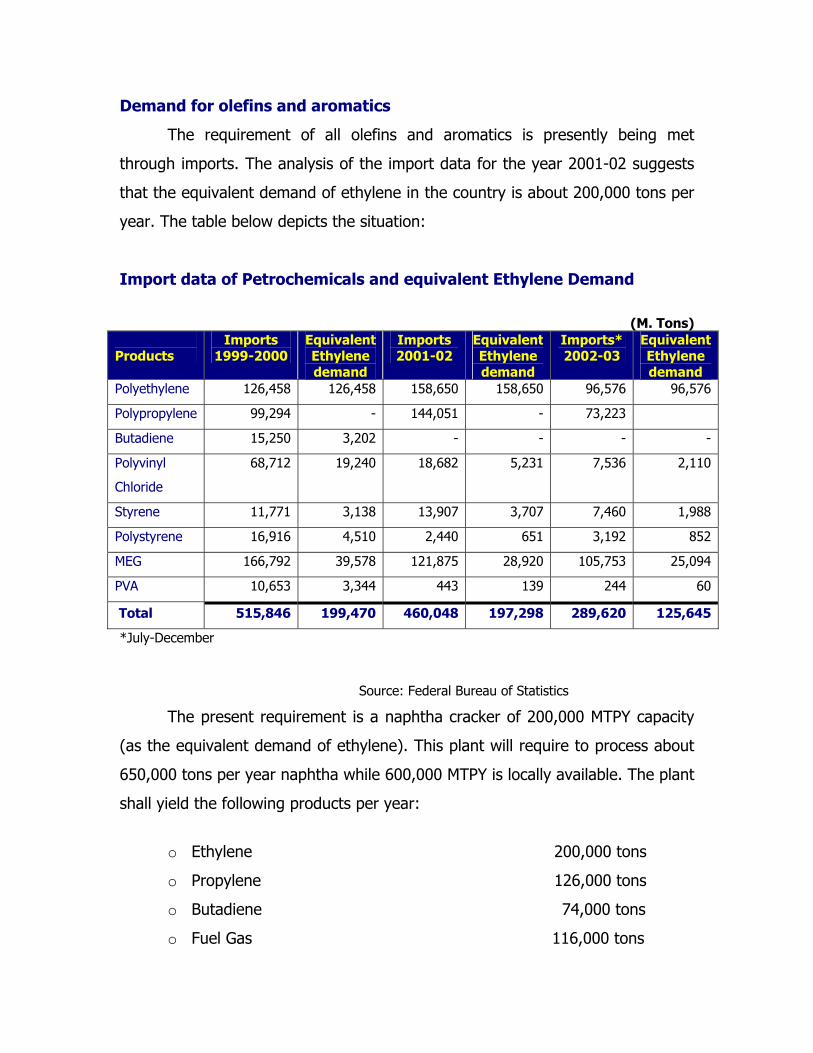

Demand for olefins and aromatics

The requirement of all olefins and aromatics is presently being met

through imports. The analysis of the import data for the year 2001-02 suggests

that the equivalent demand of ethylene in the country is about 200,000 tons per

year. The table below depicts the situation:

Import data of Petrochemicals and equivalent Ethylene Demand

(M. Tons) Products

Imports 1999-2000

EquivalentEthylene demand

Imports 2001-02

EquivalentEthylene demand

Imports* 2002-03

EquivalentEthylene demand

Polyethylene 126,458 126,458 158,650 158,650 96,576 96,576

Polypropylene 99,294 - 144,051 - 73,223

Butadiene 15,250 3,202 - - - -

Polyvinyl

Chloride

68,712 19,240 18,682 5,231 7,536 2,110

Styrene 11,771 3,138 13,907 3,707 7,460 1,988

Polystyrene 16,916 4,510 2,440 651 3,192 852

MEG 166,792 39,578 121,875 28,920 105,753 25,094

PVA 10,653 3,344 443 139 244 60

Total 515,846 199,470 460,048 197,298 289,620 125,645

*July-December

Source: Federal Bureau of Statistics

The present requirement is a naphtha cracker of 200,000 MTPY capacity

(as the equivalent demand of ethylene). This plant will require to process about

650,000 tons per year naphtha while 600,000 MTPY is locally available. The plant

shall yield the following products per year:

o Ethylene 200,000 tons

o Propylene 126,000 tons

o Butadiene 74,000 tons

o Fuel Gas 116,000 tons

o Gasoline 124,000 tons

Total 640,000 tons

It is to be noted that naphtha plant capacity is defined by the output of

ethylene from that plant. The cost of 200,000 M. tons naphtha cracker plant will

be approximately US$ 225 million. The approximate cost of down stream

polyethylene and polypropylene plants is likely to be US$ 400 million. Thus the

total cost of the petrochemical complex based on naphtha cracker comes out to

around US$ 625 million (courtesy Aftec (Pvt) Limited, Lahore).

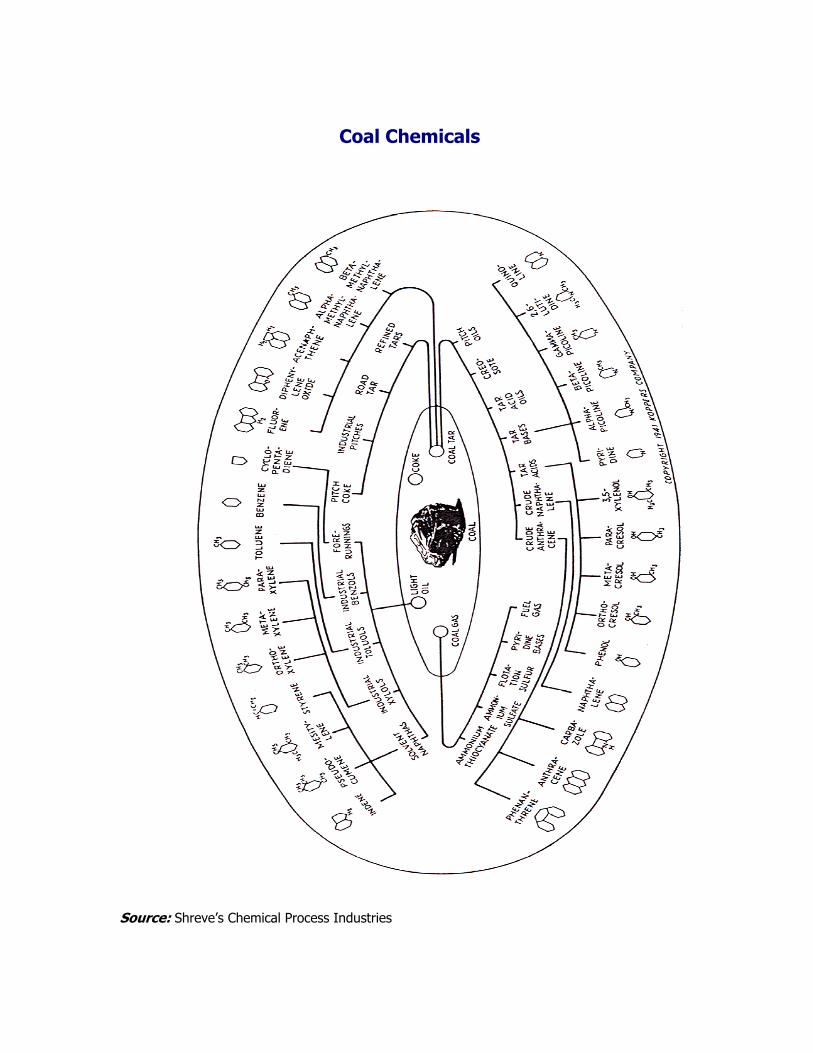

o Gasification of Coal

Another option for the manufacture of basic petrochemicals is the

gasification of coal. Numerous chemicals and fuels can be manufactured from

the gasification of coal as illustrated in the diagram below. In late 1950’s, Pak

American Fertilizers, Iskandarabad, Daudkhel was based on coal gasification

technology supplied by Lurgi to produce Ammonia and Ammonium Sulfate

fertilizer.

Sasol of South Africa are reported to have developed a technology for the

gasification of coal with high ash content. Sasol acquired the technology from

Lurgi, Germany. South African coal reserves are largely bituminous with relatively

high ash content (about 45%) and low sulfur content (1%). It is understood that

Sasol or similar technology can be adopted for Pakistani coal reserves.

Coal Chemicals

Source: Shreve’s Chemical Process Industries

Sasol, South Africa has developed the processes for production of

petrochemicals from coal by gasification. Coal under pressure and high

temperature, in the presence of steam and oxygen is converted to raw gas.

Condensate recovered from the subsequent cooling of gas, yields co-products

such as tar and oil. Nitrogenous compounds (Ammonia), sulfur and phenolic

compound are recovered. The purified synthesis gas after cooling is made

available for conversion to synthetic fuels and or chemical production.

The synthesis gas is cracked to produce ethylene, propylene and propane

whereas aromatics like benzene, toluene and xylene are produced form coal-tar.

In addition, fuel oil and diesel are produced. The advantage of SASOL process is

that it can process low-grade coal and a number of high value chemicals are

produced along with synthetic fuels.

SASOL built their first coal gasification plant producing liquid products in

1955. After fifty years, SASOL produces the equivalent of 150,000 barrels per

day of fuel and petrochemicals from coal via its indirect liquefaction process.

SASOL manufactures more than 200 chemical products exporting to more than

70 countries around the world. The company has grown to have a turn over of

3.7 billion dollars from which more than 50% is generated from chemicals.

It is strongly recommended to consider the coal gasification route and

utilize the vast coal reserves for the production of high value petrochemicals.

Suitable technologies are available in the world. Government initiatives are

needed to start the chain of actions for providing infrastructure in the coal field

area in order to consider utilization of local coal reserves.

o Associated Gases Route

Associated gases are another option to develop petrochemical base in

Pakistan. 40,176 million cubic ft of associated gases in the year 2001-02 are

accompanied by about 100,000 MTPY of condensate from various fields in Sindh

and Punjab. This condensate is rich in higher hydrocarbons, i.e. Ethane,

Propane, etc. and can be used for the production of basic organic chemicals like

ethylene, propylene etc.

This route is cheaper than the naphtha cracker route and only requires

dehydrogenation of ethane, propane etc. to convert them to ethylene, propylene

etc. The limited supply of associated gases and collection of all condensate on

one site are the main obstacles.

o Natural Gas Route

Natural gas with 96% methane can be used for the production of

methanol, ethylene, acetylene, subsequently formaldehyde and other

petrochemicals.

As a first step, natural gas is reformed to produce 8-9% acetylene in the

synthesis gas. After the removal of acetylene, the left over synthesis gas can be

used to manufacture methanol – an important building block for petrochemicals

like Methyl Tertiary Butyl Ether (MTBE), etc.

Sitara Chemicals Faisalabad planned a 30,000 MTPY Acetylene plant in

1997 based on the Chinese technology using natural gas as feedstock. The

proposal also included the production of VCM & PVC from the excess Chlorine

gas available. The project could not be materialized due to the non-availability of

natural gas at the proposed site.

A project is under consideration to import natural gas from central Asia. It

may be helpful to find the composition of that gas at this stage for its use as

feedstock for chemical industries.

Molasses

Molasses is another source for petrochemical products. Pakistan must tap

this resource as it is available in abundance. Due to its physical and chemical

properties molasses can be mixed directly with other products or it can be used

in more complex chemical processes for manufacture of high utility products.

Details are as under:

A) Direct Utilization o Fertilizer (Mixed with Urea) o Animal feed (Molasses meal, block

& liquid). o Coal Briquettes o Fuel

B) Distillery Industry o Industrial Alcohol o Anhydrous Alcohol o Potable Alcohol

C) Other Products o Gasohol o Acetic Acid o Acetone o Butanol o Citric Acid o Lactic Acid o Glycerol o Yeast o Monosodium Gluconate o L-Lysine o Itaconic Acid

o Aconitic Acid o Cigarette Filter Tows o Many other derivative products for

pharmaceutical and plastic

industry

The main utility may be as Gasohol blended with gasoline.

Recommendations for Petrochemicals

o It is recommended that a separate study on manufacturing of

petrochemicals should be conducted with the aim to determine the most viable route for the petrochemical production in Pakistan. The study should discuss merits and demerits based on all options given in the report.

o It is important to note that Pakistani coal is higher in moisture content

which may pose a limitation for its use in petrochemical manufacturing through Sasol technology. In that case, other technologies available from Shell or Texas etc should be considered.

o A long term policy should also be prepared for the development of

petrochemical sector in the country. This policy may become a part of the overall policy for the chemical sectors.

o It is suggested that a master flow chart for the organic chemicals should

be developed with the database. This database may be used for planning the petrochemical industry in Pakistan.

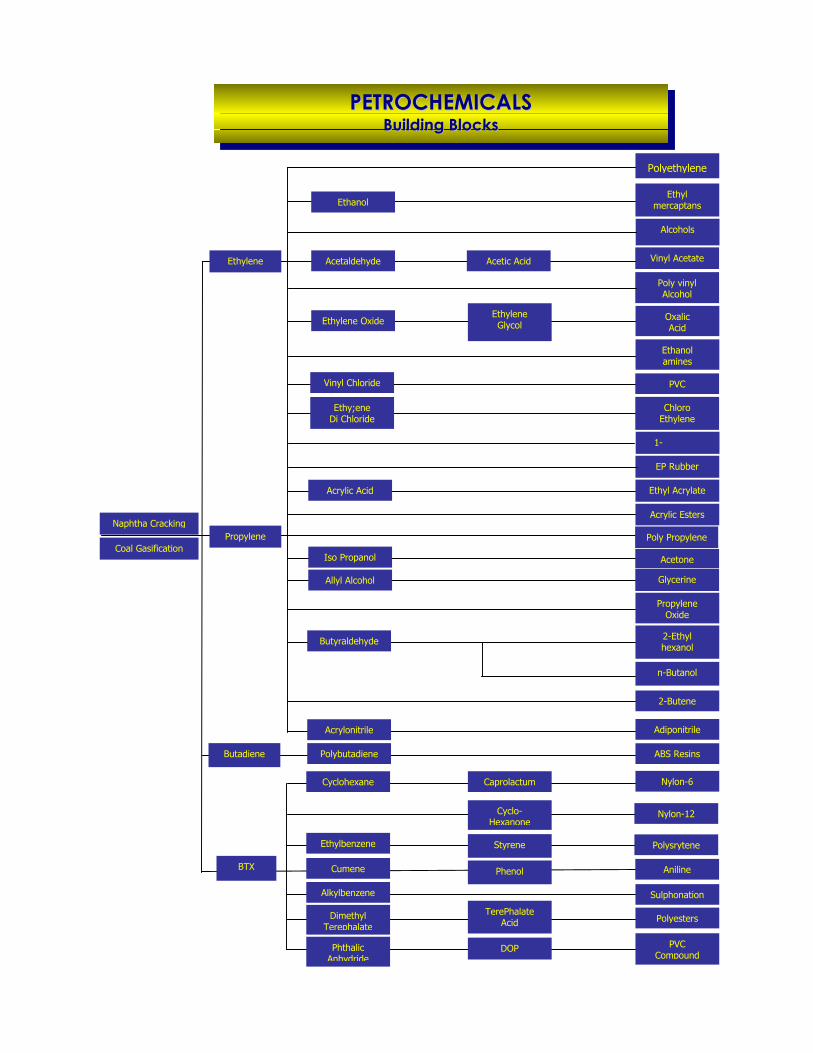

Propylene Oxide

PPEETTRROOCCHHEEMMIICCAALLSS BBuuiillddiinngg BBlloocckkss

Nylon-6

Nylon-12

Polysrytene

Aniline

Sulphonation

Polyesters

PVCCompound

Alcohols

Polyethylene

Ethylmercaptans Ethanol

Vinyl AcetateAcetaldehyde Acetic AcidEthylene

Ethanolamines

Acrylic Esters

2-Butene

Poly vinylAlcohol

1-

EP Rubber

OxalicAcid

Ethylene OxideEthylene Glycol

PVCVinyl Chloride

ChloroEthylene

Ethy;eneDi Chloride

Ethyl AcrylateAcrylic Acid

Poly PropylenePropylene Naphtha Cracking

Coal Gasification AcetoneIso Propanol

GlycerineAllyl Alcohol

2-Ethylhexanol

n-Butanol

Butyraldehyde

AdiponitrileAcrylonitrile

ABS ResinsPolybutadieneButadiene

Caprolactum

Cyclo-Hexanone

Ethylbenzene Styrene

CumeneBTX

Alkylbenzene

DimethylTerephalate

PhthalicAnhydride

TerePhalateAcid

DOP

Cyclohexane

Phenol

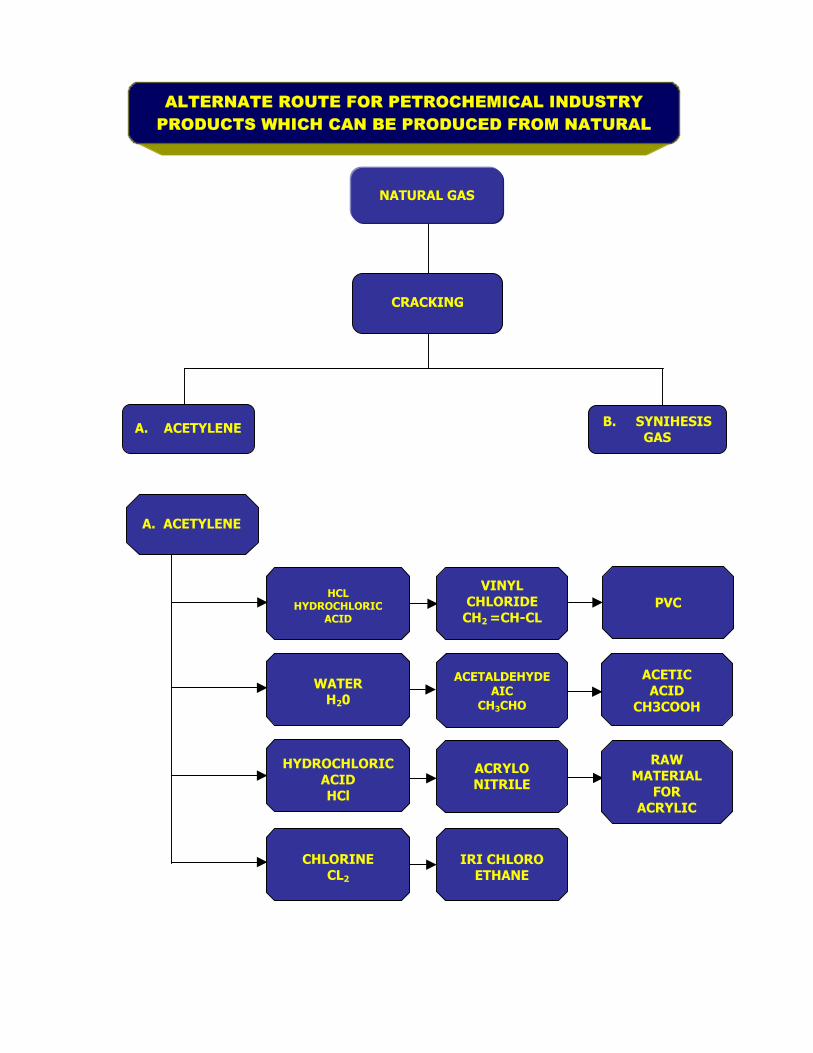

NATURAL GAS

CRACKING

A. ACETYLENE B. SYNIHESIS GAS

PVC

ACETIC ACID

CH3COOH

RAW MATERIAL

FOR ACRYLIC

A. ACETYLENE

HCL HYDROCHLORIC

ACID

VINYL CHLORIDE

CH2 =CH-CL

WATER

H20

ACETALDEHYDEAIC

CH3CHO

HYDROCHLORICACID HCl

ACRYLO NITRILE

CHLORINE

CL2

IRI CHLORO

ETHANE

ALTERNATE ROUTE FOR PETROCHEMICAL INDUSTRY PRODUCTS WHICH CAN BE PRODUCED FROM NATURAL

B. SYNTHESIS GAS

i. SYNTHESIS GAS

+ H2O

METHANOL

ii. METHANOL

+ OXYGEN

FORMALDEHYDE