1 Prospectus dated 27 November 2018 Mogo Finance Luxembourg Listing Prospectus EUR 25,000,000.00 9.50 % Senior Secured Bonds 2018/2022 (the “New Bonds”) to be consolidated and form a single series with the existing EUR 50,000,000.00 9.50 % Senior Secured Bonds 2018/2022 (the “Existing Bonds”) with a Term from 11 July 2018 until 10 July 2022 of 27 November 2018 International Securities Identification Number (ISIN): XS1831877755 Common Code: 183187775 Issue price of Existing Bonds: 100 per cent Issue price of New Bonds: 100 per cent plus accrued unpaid interests Mogo Finance (the “Issuer”), a public limited liability company (société anonyme) incorporated and existing under the laws of the Grand Duchy of Luxembourg has issued 9.50% senior secured bonds due 10 July 2022 for an initial aggregate principal amount of EUR 25,000,000.00 (the “New Bonds”), to be consolidated and form a single series with the 9.50% senior secured bonds due 10 July 2022 for an initial aggregate principal amount of EUR 50,000,000.00 (the “Existing Bonds” and, together with the New Bonds, the “Bonds”) as from 16 November 2018 (the “Issue Date”). The Bonds constitute direct, general, unconditional, unsubordinated and secured obligations of the Issuer. The Bonds will at all times rank pari passu in right of payment with all other present and future secured obligations of the Issuer and senior to all its existing and future subordinated debt. The Bonds are unconditionally and irrevocably guaranteed on a joint and several basis by AS “mogo” (Latvia), mogo OÜ (Estonia); UAB “mogo LT” (Lithuania), Mogo LLC (Georgia), Mogo sp. z o.o. (Poland), Mogo IFN SA (Romania), Mogo Bulgaria EOOD (Bulgaria), Mogo Loans SRL (Moldova), Mogo Albania sh.a. (Albania), OOO “Мого Кредит” (Belarus), SIA HUB 3 (Latvia), Risk Management Service OÜ (Estonia), MOGO Universal Credit Organization LLC (Armenia), ТОВ МОГО УКРАЇНА (Ukraine), AS “HUB 1” (Latvia), AS “HUB 2” (Latvia) and AS “HUB 4” (Latvia) (the “Guarantors” and each a “Guarantor”) under the terms and conditions set forth herein (collectively the “Guarantees” and each a “Guarantee”). The Bonds are further secured by the Transaction Securities (as defined below) granted by certain other direct and indirect subsidiaries of the Issuer (the “Pledgors” and, together with the Guarantors, the “Security Providers”). This document (the “Prospectus”) constitutes a prospectus pursuant to Article 5 para. 3 of the Directive 2003/71/EC of the European Parliament and of the Council of 4 November 2003 on the prospectus to be published when securities are offered to the public or admitted to trading as amended by the Directive 2010/73/EC of the European Parliament and of the Council in order for the Bonds to be admitted to trading on Frankfurt Stock Exchange’s regulated market segment . This Prospectus has been approved by the Luxembourg Commission for the Supervision of the Financial Sector (Commission de Surveillance du Secteur

Transcript

1

Prospectus dated 27 November 2018

Mogo Finance

Luxembourg

Listing Prospectus

EUR 25,000,000.00

9.50 % Senior Secured Bonds 2018/2022 (the “New Bonds”)

to be consolidated and form a single series with the existing

EUR 50,000,000.00

9.50 % Senior Secured Bonds 2018/2022 (the “Existing Bonds”)

with a Term from 11 July 2018 until 10 July 2022

of 27 November 2018

International Securities Identification Number (ISIN): XS1831877755

Common Code: 183187775

Issue price of Existing Bonds: 100 per cent

Issue price of New Bonds: 100 per cent plus accrued unpaid interests

Mogo Finance (the “Issuer”), a public limited liability company (société anonyme) incorporated and existing under the laws of the Grand Duchy of Luxembourg has issued 9.50% senior secured bonds due 10 July 2022 for an initial aggregate principal amount of EUR 25,000,000.00 (the “New Bonds”), to be consolidated and form a single series with the 9.50% senior secured bonds due 10 July 2022 for an initial aggregate principal amount of EUR 50,000,000.00 (the “Existing Bonds” and, together with the New Bonds, the “Bonds”) as from 16 November 2018 (the “Issue Date”).

The Bonds constitute direct, general, unconditional, unsubordinated and secured obligations of the Issuer. The Bonds will at all times rank pari passu in right of payment with all other present and future secured obligations of the Issuer and senior to all its existing and future subordinated debt. The Bonds are unconditionally and irrevocably guaranteed on a joint and several basis by AS “mogo” (Latvia), mogo OÜ (Estonia); UAB “mogo LT” (Lithuania), Mogo LLC (Georgia), Mogo sp. z o.o. (Poland), Mogo IFN SA (Romania), Mogo Bulgaria EOOD (Bulgaria), Mogo Loans SRL (Moldova), Mogo Albania sh.a. (Albania), OOO “Мого Кредит” (Belarus), SIA HUB 3 (Latvia), Risk Management Service OÜ (Estonia), MOGO Universal Credit Organization LLC (Armenia), ТОВ МОГО УКРАЇНА (Ukraine), AS “HUB 1” (Latvia), AS “HUB 2” (Latvia) and AS “HUB 4” (Latvia) (the “Guarantors” and each a “Guarantor”) under the terms and conditions set forth herein (collectively the “Guarantees” and each a “Guarantee”). The Bonds are further secured by the Transaction Securities (as defined below) granted by certain other direct and indirect subsidiaries of the Issuer (the “Pledgors” and, together with the Guarantors, the “Security Providers”).

This document (the “Prospectus”) constitutes a prospectus pursuant to Article 5 para. 3 of the Directive 2003/71/EC of the European Parliament and of the Council of 4 November 2003 on the prospectus to be published when securities are offered to the public or admitted to trading as amended by the Directive 2010/73/EC of the European Parliament and of the Council in order for the Bonds to be admitted to trading on Frankfurt Stock Exchange’s regulated market segment. This Prospectus has been approved by the Luxembourg Commission for the Supervision of the Financial Sector (Commission de Surveillance du Secteur

2

Financier – “CSSF”) and has been applied to be notified to the German Federal Financial Supervisory Authority (Bundesanstalt für Finanzdienstleistungsaufsicht – “BaFin”) in accordance with Article 19 of the Luxembourg Law of 10 July 2005 on prospectuses for securities, as amended. Pursuant to Article 7 para. 7 of the Luxembourg Law of 10 July 2005 on prospectuses for securities, as amended, by approving the Prospectus, the CSSF does not take any responsibility for the economic or financial soundness of the transaction and the Issuer’s quality and financial solvency. The approved prospectus may be downloaded from the Issuer’s website (www.mogofinance.com) and the website of the Luxembourg stock exchange (www.bourse.lu). Application has been made to the Frankfurt Stock Exchange for the Bonds to be admitted to trading on Frankfurt Stock Exchange’s regulated market segment (General Standard), segment for bonds of Deutsche Börse AG.

Investors should be aware, that an investment in the Bonds involves a risk and that, if certain risks, in particular those described under “Risk Factors”, occur, the investors may lose all or a very substantial part of their investment.

The distribution of this Prospectus may be limited by certain legislation. Any person who enters into possession of this Prospectus must take these limitations into consideration. The Bonds are not and will not be registered, particularly in accordance with the United States Securities Act of 1933, as amended (the “Securities Act”) or in accordance with securities law of individual states of the United States of America. Furthermore, they are not permitted to be offered or sold within the United States of America, or for the account or benefit of a person from the United States of America (as defined under Regulation S under the Securities Act), unless this ensues through an exemption of the registration requirements of the Securities Act or the laws of individual states of the United States of America or through a transaction, which is not subject to the aforementioned provisions.

TABLE OF CONTENTS

I. SUMMARY OF THE PROSPECTUS ................................................................. 7

A Introduction and Warnings ................................................................................. 7 B Issuer ................................................................................................................. 7 B(i) Guarantor – AS “mogo” (Latvia) .................................................................... 10 B(ii) Guarantor – mogo OÜ (Estonia) .................................................................. 13 B(iii) Guarantor – UAB “mogo LT” (Lithuania) ...................................................... 14 B(iv) Guarantor – Mogo LLC (Georgia) ............................................................... 15 B(v) Guarantor – Mogo sp. z o.o. (Poland) .......................................................... 16 B(vi) Guarantor – Mogo IFN SA (Romania) ......................................................... 17 B(vii) Guarantor – Mogo Bulgaria EOOD (Bulgaria) ............................................ 18 B(viii) Guarantor – Mogo Loans SRL (Moldova) .................................................. 19 B(ix) Guarantor – Mogo Albania sh.a. (Albania) .................................................. 20 B(x) Guarantor – OOO “Мого Кредит” (Belarus) ................................................. 21 B(xi) Guarantor – SIA HUB 3 (Latvia) .................................................................. 22 B(xii) Guarantor – Risk Management Service OÜ (Estonia) ................................ 23 B(xiii) Guarantor – MOGO Universal Credit Organization LLC (Armenia) ............ 24 B(xiv) Guarantor – ТОВ МОГО УКРАЇНА (Ukraine) ............................................ 25 B(xv) Guarantor – AS “HUB 1” (Latvia) ............................................................... 26 B(xvi) Guarantor – AS “HUB 2” (Latvia) ............................................................... 27 B(xvii) Guarantor – AS “HUB 4” (Latvia) .............................................................. 28 C Securities......................................................................................................... 29 D Risks ............................................................................................................... 31 E Offer ................................................................................................................ 34

II. GERMAN TRANSLATION OF THE SUMMARY (DEUTSCHE ÜBERSETZUNG DER ZUSAMMENFASSUNG) .................................................... 35

A Einführung und Warnhinweise ......................................................................... 35 B Emittent ........................................................................................................... 35 B(i) Garantiegeber – AS „mogo“ (Latvia) ............................................................. 39 B(ii) Garantiegeber – mogo OÜ (Estonia) ............................................................ 41 B(iii) Garantiegeber – UAB „mogo LT“ (Lithuania) ............................................... 43 B(iv) Garantiegeber – Mogo LLC (Georgia) ......................................................... 44 B(v) Garantiegeber – Mogo sp. z o.o. (Poland) ................................................... 45 B(vi) Garantiegeber – Mogo IFN SA (Romania) .................................................. 46 B(vii) Garantiegeber – Mogo Bulgaria EOOD (Bulgaria) ...................................... 47 B(viii) Garantiegeber – Mogo Loans SRL (Moldova) ........................................... 48 B(ix) Garantiegeber – Mogo Albania sh.a. (Albania) ............................................ 50 B(x) Garantiegeber – OOO „Мого Кредит“ (Belarus) .......................................... 51 B(xi) Garantiegeber – SIA HUB 3 (Latvia) ........................................................... 52 B(xii) Garantiegeber – Risk Management Service OÜ (Estonia).......................... 53 B(xiii) Garantiegeber – MOGO Universal Credit Organization LLC (Armenia) ..... 54 B(xiv) Garantiegeber – ТОВ МОГО УКРАЇНА (Ukraine) ..................................... 55 B(xv) Garantiegeber – AS „HUB 1“ (Latvia) ......................................................... 56 B(xvi) Garantiegeber – AS „HUB 2“ (Latvia) ........................................................ 58 B(xvii) Garantiegeber – AS „HUB 4“ (Latvia) ....................................................... 59 C Wertpapiere ..................................................................................................... 60 D Risiken ............................................................................................................ 63 E Angebot ........................................................................................................... 66

III. RISK FACTORS ........................................................................................... 68

1. RISK FACTORS RELATING TO THE ISSUER, THE GROUP AND OUR BUSINESS .......................................................................................................... 68

4

2. RISK FACTORS RELATING TO THE BONDS .......................................... 82 3. RISKS RELATED TO THE TRANSACTION SECURITIES, THE GUARANTEES AND THE SECURITY AGENT AGREEMENT............................ 89

IV. OVERVIEW OF THE GROUP ...................................................................... 94

V. GENERAL INFORMATION ........................................................................ 101

Responsibility Statement ................................................................................... 101 Subject of this Prospectus ................................................................................. 101 Hyperlinks ......................................................................................................... 101 Forward-looking Statements ............................................................................. 102 Third Party Information ...................................................................................... 102 Presentation of Financial Information ................................................................ 103 Further bonds regarding this Prospectus ........................................................... 103 MiFID II Product Governance ............................................................................ 104 Documents available for Inspection ................................................................... 104

VI. USE OF NET PROCEEDS ......................................................................... 105

VII. CAPITALIZATION ...................................................................................... 106

VIII. SELECTED FINANCIAL INFORMATION AND OPERATING DATA ...... 108

1. Selected consolidated statement of income data ..................................... 108 2. Selected consolidated statement of financial position data ...................... 109 3. Selected consolidated statement of cash flow data ................................. 112 4. Net debt ................................................................................................... 115 5. Key financial ratios .................................................................................. 116 6. Other financial data (EBITDA) (in Million EUR) ........................................ 117 7. Key performance indicators ..................................................................... 117 8. Auditors ................................................................................................... 121 9. Changes in the Financial or Trading Position........................................... 121

IX. SELECTED PORTFOLIO INFORMATION ................................................. 122

1. Loan portfolio........................................................................................... 122 2. Total loan portfolio by loan balance ......................................................... 123 3. Total loan portfolio by duration for which the repayment of loans are delayed1 ............................................................................................................ 123 4. Sale of repossessed car from agreement termination date ...................... 123 5. Classification of our loan portfolio ............................................................ 124 6. Performing loan portfolio by product ........................................................ 124 7. Non-performing loan portfolio by product ................................................. 124 8. Allowance for loan losses ........................................................................ 125

X. BUSINESS ................................................................................................. 126

a. Financial Leasing .................................................................................. 131 b. Leaseback ............................................................................................. 132 c. Installment Loans ..................................................................................... 134

XI. PHYSICAL FOOTPRINT ............................................................................ 136

XII. MARKETING .............................................................................................. 138

1. Marketing organization and development ................................................ 138

5

2. Potential customers ................................................................................. 139 3. Below The Line (BTL) Marketing channels .............................................. 139

a. Search Engine Marketing ...................................................................... 139 b. Paid Social media ads ........................................................................... 139 c. Display ads ............................................................................................... 139 d. E-mail and SMS marketing .................................................................... 140 e. Affiliate marketing .................................................................................. 140

4. Above The Line (ATL) Marketing channels .............................................. 140

XIII. UNDERWRITING AND REVIEW ............................................................. 141

1. Overview of the underwriting and review process .................................... 141 2. Loan application processing .................................................................... 142 3. Risk evaluation and Scoring .................................................................... 142 4. Vehicle inspection (in case of Financial Leasing and Leaseback) ............ 142 5. Final loan approval and loan issuance ..................................................... 142

XIV. PORTFOLIO MANAGEMENT ................................................................. 143

XV. INFORMATION TECHNOLOGY ................................................................ 146

XVI. CREDIT AND RISK MANAGEMENT ...................................................... 148

a. The Credit Risk ..................................................................................... 148 b. The Market Risk .................................................................................... 149 c. The Operational Risk ................................................................................ 149 d. The Reputational Risk ........................................................................... 149

XVII. COMPETITION ....................................................................................... 151

XVIII. INTELLECTUAL PROPERTY ................................................................. 154

XIX. REGULATORY FRAMEWORK ............................................................... 155

XX. INFORMATION ABOUT THE ISSUER ....................................................... 160

1. General Information about the Issuer ...................................................... 160 2. Share Capital and Shareholders of the Issuer ......................................... 161

XXI. INFORMATION ABOUT THE GROUP AND THE GUARANTORS ......... 164

1. History of the Group ................................................................................ 164 2. Beneficial ownership ................................................................................ 164 3. Issuer and Subsidiaries ........................................................................... 165 4. Information on about the Group and the Guarantors ................................ 167

a. AS “mogo” (Latvia) ................................................................................ 167 b. mogo OÜ (Estonia) ............................................................................... 172 c. UAB mogo LT (Lithuania) ......................................................................... 174 d. Mogo LLC (Georgia).............................................................................. 176 e. Mogo sp. z o.o. (Poland) ....................................................................... 179 f. Mogo IFN SA (Romania) .......................................................................... 182 g. Mogo Bulgaria EOOD (Bulgaria) ........................................................... 185 h. Mogo Loans SRL (Moldova) .................................................................. 187 i. Mogo Albania sh.a. (Albania) .................................................................... 190 j. OOO “Мого Кредит” (“OOO “Mogo Credit””) (Belarus) ........................... 192 k. SIA HUB 3 (Latvia) ................................................................................... 195 l. Risk Management Service OÜ (Estonia). ................................................. 197 m. MOGO Universal Credit Organization LLC (Armenia) ............................ 199 n. ТОВ МОГО УКРАЇНА ("MOGO UKRAINE" LLC ) (Ukraine) .................. 203

6

o. AS “HUB 1” ........................................................................................... 205 p. AS “HUB 2” ........................................................................................... 208 q. AS “HUB 4” ........................................................................................... 210

5. Organization Structure ............................................................................. 213 6. Properties of the Group ........................................................................... 214 7. Employees .............................................................................................. 214 8. Material Agreements ............................................................................... 215

a. Notes due 31 March 2021 ..................................................................... 215 b. Mezzanine Facility Agreement .............................................................. 215 c. Mintos....................................................................................................... 216 d. D.A.A. Investments Limited ................................................................... 220 e. V.M. Office Limited ................................................................................ 221 f. IN Finance ................................................................................................ 221 g. IVN Finance .......................................................................................... 221 h. Ardshinbank (Armenian Bank) ............................................................... 221

9. Related Party Transactions ..................................................................... 222 a. LOANS WITH RELATED PARTIES ...................................................... 222 b. CREDIT DERIVATIVE TRANSACTION (CREDIT DEFAULT SWAP).... 224

1. Management ........................................................................................... 226 2. Corporate Governance ............................................................................ 228 3. Audit Committee ...................................................................................... 229 4. Interest of directors and officers............................................................... 229 5. Litigation statement about directors and officers ...................................... 229 6. Change of Control over the Group ........................................................... 229

XXIII. TERMS AND CONDITIONS OF THE BONDS ........................................ 230

XXVII. LIMITATIONS ON VALIDITY AND ENFORCEABILITY OF THE GUARANTEES AND THE BONDS AND CERTAIN INSOLVENCY CONSIDERATIONS ............................................................................................. 316

XXX. DOCUMENTS INCORPORATED BY REFERENCE ............................... 333

I. SUMMARY OF THE PROSPECTUS

Summaries are made up of disclosure requirements known as elements (“Elements”). These Elements are numbered in Sections A - E (A.1 to E.7). This summary contains all the Elements required to be included in a summary for this type of securities and issuer. Because some Elements are not required to be addressed, there may be gaps in the numbering sequence of the Elements. Even though an Element may be required to be inserted in the summary because of the type of securities and issuer, it is possible that no relevant information can be given regarding the Element. In this case a short description of the Element is included in the summary with the mention of “not applicable”.

A Introduction and Warnings

A.1 Warnings The following summary should be read as an introduction to this prospectus (the “Prospectus”) and it contains selected information, which the Issuer views as being essential characteristics of and risks associated with the Issuer, and the Bonds. Any decision by an investor to invest in the Bonds should be based on consideration of this Prospectus as a whole.

Where a claim relating to the information contained in this Prospectus is brought before a court, the plaintiff investor might, under the national legislation of the Member State, have to bear the costs of translating this Prospectus before the legal proceedings are initiated.

Civil liability attaches only to those persons who have tabled this summary including any translation thereof, but only if this summary is misleading, inaccurate or inconsistent when read together with the other parts of this Prospectus or it does not provide, when read together with the other parts of this Prospectus, Key information in order to aid investors when considering whether to invest in such securities.

A.2

Consent regarding the subsequent use of the Prospectus

Not applicable. Consent regarding the use of the Prospectus for a subsequent resale or final placement of the Bonds (as defined under C.1) has not been granted.

B Issuer

B.1 Legal and commercial name of the Issuer.

Mogo Finance (the “Issuer”). Unless the context otherwise requires, references to “we”, “our”, “us”, “Mogo” or the “Group” refer to Mogo Finance and its direct and indirect subsidiaries.

B.2 Domicile and legal form of the Issuer, legislation, country of incorporation.

The Issuer’s domicile is in Luxembourg, Grand Duchy of Luxembourg (“Luxembourg”). The Issuer is a Luxembourg public limited liability company incorporated and operating under the laws of Luxembourg.

B.4b Known trends affecting the Guarantor and the industries in which it operates

Not applicable. There are no known trends affecting the Issuer and the industries in which it operates.

B.5 Description of the group and the Issuer’s position within the group.

The Group operates in 12 countries – Latvia, Lithuania, Estonia, Georgia, Poland, Romania, Bulgaria, Moldova, Belarus, Albania, Armenia and Ukraine – through direct and indirect subsidiaries of the Issuer. The Issuer is the holding company of the Group.

B.9 Profit forecast or estimate is made

Not applicable (as no profit forecasts or estimates are made).

B.10 Qualifications in the audit report on the historical financial

Not applicable (as the auditor’s reports incorporated by reference to this Prospectus do not contain any qualifications).

8

information.

B.12 Selected historical key financial information

The tables below present key selected consolidated financial information for the Group as at and for (i) the financial years ended 31 December 2016 and 31 December 2017, (ii) with respect to the statement of income data and cash flow data, the nine-month period ended 30 September 2017 and (iii) the nine-month period ended 30 September 2018. This information has been derived from the Issuer’s audited consolidated financial statements as at and for the year ended 31 December 2017 (including restated comparative financial information as at and for the financial year ended 31 December 2016) as well as from the unaudited financial reports as at and for the nine-month period ended 30 September 2018 (including comparative financial information for the nine-month period ended 30 September 2017) and the Group’s internal accounting system. The consolidated annual financial statements of the Group have been prepared in accordance with the International Financial Reporting Standards as adopted by the European Union (“IFRS”). The unaudited financial report for the nine months ended 30 September 2018 consists of the consolidated statement of financial position as at 30 September 2018 and the related consolidated statement of comprehensive income, the consolidated statement of changes in equity and the consolidated cash flow statement for the nine months ending 30 September 2018 and is prepared in accordance with the measurement and recognition principles of the IFRS.

1. Selected consolidated statement of income data

Year ended 31 December

2017

Year ended 31 December

2016

Nine-month period

ended 30 September

2018

Nine-month period

ended 30 September

2017

(Audited) (Unaudited)

(in Million EUR)

Interest and similar income ............................. 38.4 29.6 41.7 27.0

Net interest income ....................................... 29.0 22.4 29.1 20.5

Net profit for the period ................................ 9.0 5.6 2.4 7.4

Total comprehensive income for the year/period ................................................

8.5 5.6 2.5 7.2

2. Selected consolidated statement of financial position data

Year ended 31 December

2017

Year ended 31 December

2016

Nine-month period

ended 30 September

2018

(Audited) (Unaudited)

(in Million EUR)

Total assets .................................................... 112.5 71.0 158.8

9

Year ended 31 December

2017

Year ended 31 December

2016

Nine-month period

ended 30 September

2018

(Audited) (Unaudited)

(in Million EUR)

Non-current borrowings 70.8 51.9 120.1

Current borrowings .......................................... 25.8 3.4 17.4

Total equity ..................................................... 11.5 13.2 16.4

Total equity and liabilities ............................. 112.5 71.0 158.8

3. Selected consolidated statement of cash flow data

Year ended 31 December

2017

Year ended 31 December

2016

Nine-month period

ended 30 September 2018

Nine-month period

ended 30 September 2017

(Audited) (Unaudited)

(in Million EUR)

Operating profit before working capital changes

25.9 14.9 25.5 18.5

Cash generated to/from operations

(18.1) 7.8 (25.7) (7.7)

Net cash flows to/from operating activities

(18.8) 7.3 (26.8) (8.3)

Net cash flows to/from financing activities

23.0 (4.4) 29.6 10.0

Cash at the end of the year/period

5.2 2.2 6.5 3.3

No material adverse change in the prospects of the Issuer

There has been no material adverse change in the prospects of the Issuer since 31 December 2017.

Significant changes in the financial or trading position

Not applicable. There has been no significant change in the financial or trading position of the Issuer since 30 September 2018.

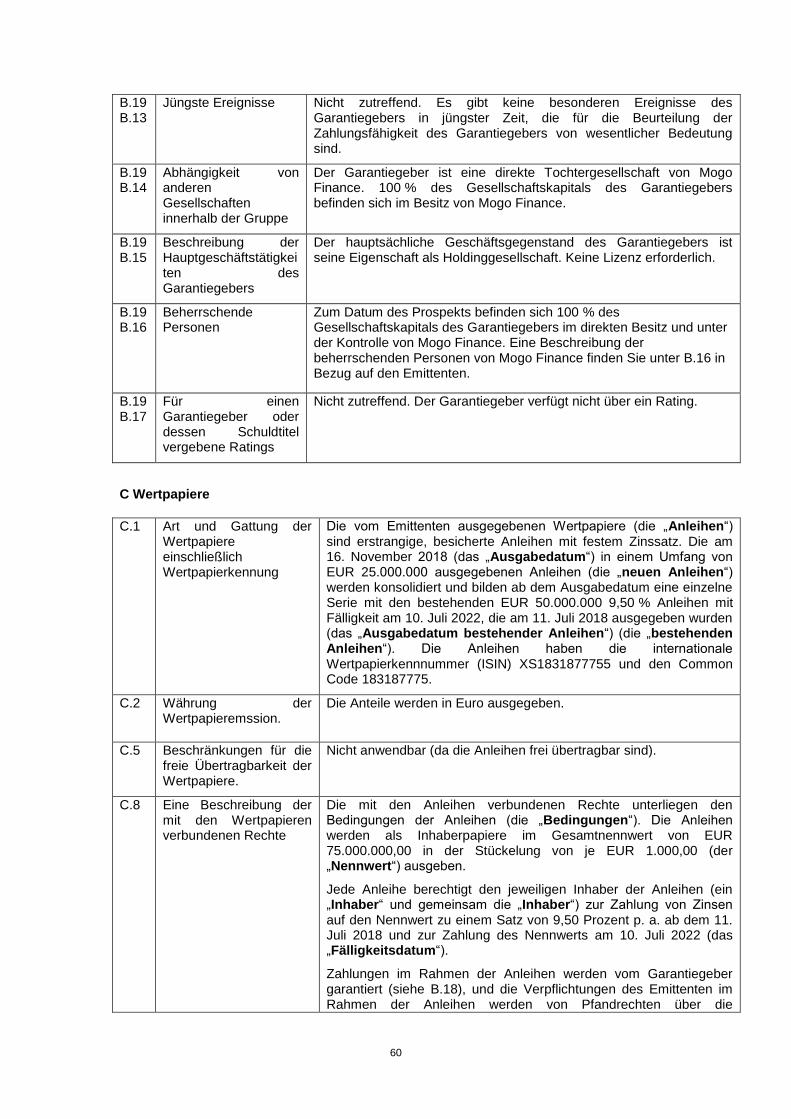

B.13 Recent events Not applicable. There are no recent events particular to the Issuer which are to a material extent relevant to the evaluation of the Issuer’s solvency.

B.14 Dependence upon other entities within the group

The Issuer is the holding company of the Group and has no relevant business or operational activities other than the financing of the Group companies. Therefore, the Issuer is dependent on payments of the operating entities of the Group.

B.15 Description of the Issuer’s principal

The Issuer provides financing to the Group companies. The Issuer is financed through its share capital, external debt and cash from the

10

activities activities of the Group’s operating companies.

B.16 Controlling persons The founders and beneficial owners of the Issuer are Aigars Kesenfelds, Alberts Pole, Kristaps Ozols and Māris Keišs (the “Founders”). The Founders are indirect shareholders of the Issuer, together controlling 94.875% of the voting share capital of the Issuer.

B.17 Credit ratings assigned to an Issuer or its debt securities

Not applicable. Neither the Issuer nor the Bonds are rated.

B.18 Nature and scope of the guarantee

The obligations of the Issuer under the Bonds will be guaranteed on a senior basis by the Guarantors (as defined below) under the terms and conditions outlined here (the “Guarantee”). All operative group companies will have to accede to the Guarantee as additional Guarantors within three months after the grant of the first loan to their customers.

The Guarantees shall be, unconditional, irrevocable, separate and independent from the obligations of the Issuer and shall exist irrespective of the validity and enforceability of the obligations of the Issuer. Each Guarantee constitutes an independent payment obligation in the form of a contract for the benefit of the Holders from time to time as third party beneficiaries.

“Security Agent” means Greenmarck Restructuring Solutions GmbH.

The intent and purpose of each Guarantee is to ensure that the Holders under all circumstances, whether factual or legal, and regardless of the validity and enforceability of the obligations of the Issuer or of any other grounds on the basis of which the Issuer may fail to effect payment, shall receive the amounts payable as principal, interest and other amounts to the Holders pursuant to the Terms and Conditions on due dates as provided in the Terms and Conditions.

Each Guarantee will rank pari passu with all of the relevant Guarantors’ existing and future senior unsecured debt and senior to all of their existing and future subordinated debt, notwithstanding certain limitation under the laws of the relevant Guarantor’s jurisdiction.

In addition, the validity and enforceability of the Guarantees will be subject to certain limitations.

B.19 Information about the guarantors

The Guarantees are granted by (i) AS “mogo” (Latvia), (ii) mogo OÜ (Estonia), (iii) UAB “mogo LT” (Lithuania), (iv) Mogo LLC (Georgia), (v) Mogo sp. z o.o. (Poland), (vi) Mogo IFN SA (Romania), (vii) Mogo Bulgaria EOOD (Bulgaria), (viii) Mogo Loans SRL (Moldova), (ix) Mogo Albania sh.a. (Albania), (x) OOO “Мого Кредит” (Belarus), (xi) SIA HUB 3 (Latvia), (xii) Risk Management Service OÜ (Estonia), (xiii) MOGO Universal Credit Organization LLC (Armenia), (xiv) ТОВ МОГО УКРАЇНА (Ukraine), (xv) AS “HUB 1” (Latvia), (xvi) AS “HUB 2” (Latvia) and (xvii) AS “HUB 4” (Latvia) (the “Guarantors”). All operative group companies will have to accede to the Guarantee as additional Guarantors within three months after the grant of the first loan to their customers.

B(i) Guarantor – AS “mogo” (Latvia)

B.19 B.1

Legal and commercial name

AS “mogo” (Latvia). The Guarantor operates under the commercial name “AS “mogo””.

B.19 B.2

Domicile and legal form of the Guarantor, legislation, country of

The Guarantor’s domicile is in Riga, Latvia. The Guarantor is a Latvian joint stock company incorporated and operating under the laws of Latvia.

11

incorporation.

B.19 B.4b

Known trends affecting the Guarantor and the industries in which it operates.

Not applicable. There are no known trends affecting the Guarantor and the industries in which it operates.

B.19 B.5

Description of the group and the Guarantor’s position within the group.

The Guarantor is a subsidiary of Mogo Finance. For a description of the Group please see B.5 in relation to the Issuer.

B.19 B.9

Profit forecast or estimate is made

Not applicable (as no profit forecasts or estimates are made).

B.19 B.10

Qualifications in the audit report on the historical financial information.

Not applicable. No audit report or financial information is being presented by the Guarantor.

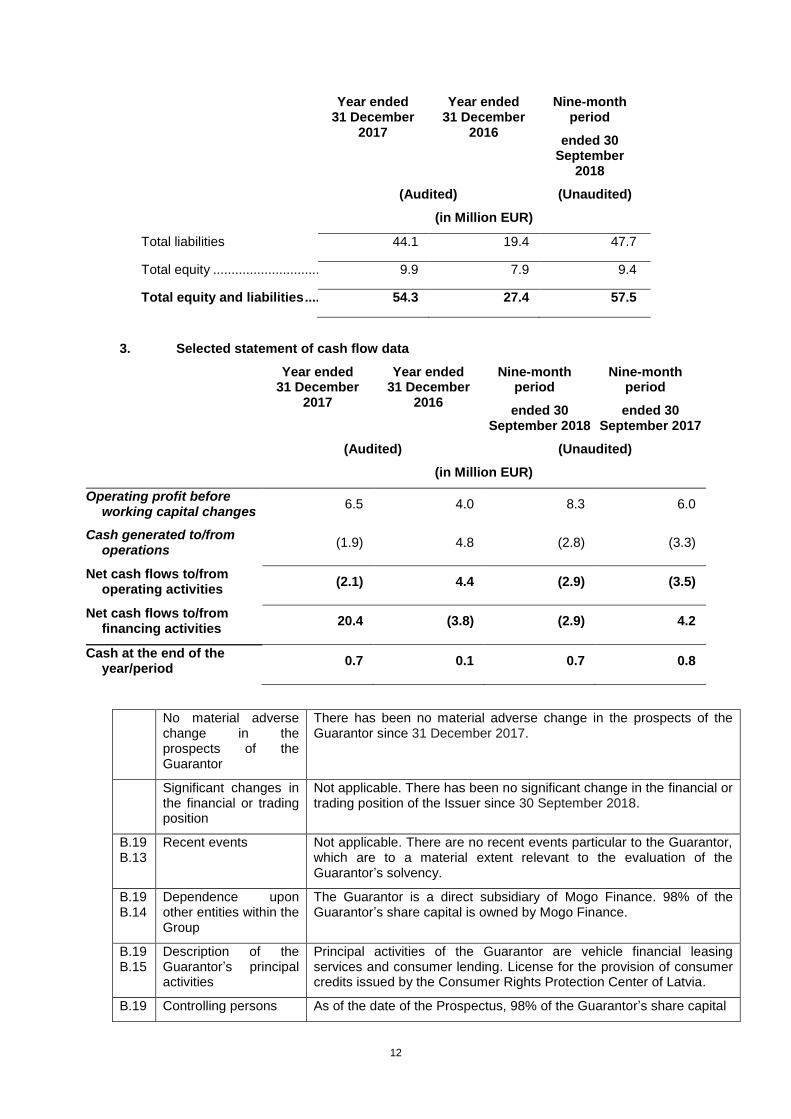

B.19 B.12

Selected historical key financial information

The tables below show certain selected summarised financial information which, without material changes, is derived from, and must be read together with, the Guarantor’s audited financial statements for the year ended 31 December 2017 and unaudited condensed interim financial statements for the nine months ended 30 September 2018 incorporated by reference in the Prospectus.

1. Selected statement of income data

Year ended 31 December

2017

Year ended 31 December

2016

Nine-month period

ended 30 September

2018

Nine-month period

ended 30 September

2017

(Audited) (Unaudited)

(in Million EUR)

Interest and similar income ............................. 13.8 10.3 13.0 9.4

Net interest income....................................... 10.9 8.1 8.1 7.6

Net profit for the period ................................ 3.6 2.6 1.6 2.9

Total comprehensive income for the year/period ................................................

3.6 2.6 1.6 2.9

2. Selected statement of financial position data

Year ended 31 December

2017

Year ended 31 December

2016

Nine-month period

ended 30 September

2018

(Audited) (Unaudited)

(in Million EUR)

Total assets .................................................... 54.3 27.4 57.5

12

Year ended 31 December

2017

Year ended 31 December

2016

Nine-month period

ended 30 September

2018

(Audited) (Unaudited)

(in Million EUR)

Total liabilities 44.1 19.4 47.7

Total equity ...................................................... 9.9 7.9 9.4

Total equity and liabilities ............................. 54.3 27.4 57.5

3. Selected statement of cash flow data

Year ended 31 December

2017

Year ended 31 December

2016

Nine-month period

ended 30 September 2018

Nine-month period

ended 30 September 2017

(Audited) (Unaudited)

(in Million EUR)

Operating profit before working capital changes

6.5 4.0 8.3 6.0

Cash generated to/from operations

(1.9) 4.8 (2.8) (3.3)

Net cash flows to/from operating activities

(2.1) 4.4 (2.9) (3.5)

Net cash flows to/from financing activities

20.4 (3.8) (2.9) 4.2

Cash at the end of the year/period

0.7 0.1 0.7 0.8

No material adverse change in the prospects of the Guarantor

There has been no material adverse change in the prospects of the Guarantor since 31 December 2017.

Significant changes in the financial or trading position

Not applicable. There has been no significant change in the financial or trading position of the Issuer since 30 September 2018.

B.19 B.13

Recent events Not applicable. There are no recent events particular to the Guarantor, which are to a material extent relevant to the evaluation of the Guarantor’s solvency.

B.19 B.14

Dependence upon other entities within the Group

The Guarantor is a direct subsidiary of Mogo Finance. 98% of the Guarantor’s share capital is owned by Mogo Finance.

B.19 B.15

Description of the Guarantor’s principal activities

Principal activities of the Guarantor are vehicle financial leasing services and consumer lending. License for the provision of consumer credits issued by the Consumer Rights Protection Center of Latvia.

B.19 Controlling persons As of the date of the Prospectus, 98% of the Guarantor’s share capital

13

B.16 is directly owned and controlled by Mogo Finance. For a description of the controlling persons of Mogo Finance please see B.16 in relation to the Issuer.

B.19 B.17

Credit ratings assigned to the Guarantor or its debt securities

Not applicable. The Guarantor is not rated.

B(ii) Guarantor – mogo OÜ (Estonia)

B.19 B.1

Legal and commercial name

mogo OÜ (Estonia). The Guarantor operates under the commercial name “mogo OÜ”.

B.19 B.2

Domicile and legal form of the Guarantor, legislation, country of incorporation.

The Guarantor’s domicile is in Tallinn, Estonia. The Guarantor is an Estonian private limited liability company incorporated and operating under the laws of Estonia.

B.19 B.4b

Known trends affecting the Guarantor and the industries in which it operates.

Not applicable. There are no known trends affecting the Guarantor and the industries in which it operates.

B.19 B.5

Description of the group and the Guarantor’s position within the group.

The Guarantor is a subsidiary of Mogo Finance. For a description of the Group please see B.5 in relation to the Issuer.

B.19 B.9

Profit forecast or estimate is made

Not applicable (as no profit forecasts or estimates are made).

B.19 B.10

Qualifications in the audit report on the historical financial information.

Not applicable. No audit report or financial information is being presented by the Guarantor.

B.19 B.12

Selected historical key financial information

Not applicable. No financial information is being presented by the Guarantor. Consolidated financial statements of the Group are incorporated by reference into this Prospectus. For a description of the selected historical key financial information of the Group please see B.12 in relation to the Issuer.

No material adverse change in the prospects of the Guarantor

For a description of the prospects of the Group please see B.12 in relation to the Issuer.

Significant changes in the financial or trading position

For a description of the significant changes in the financial or trading position of the Group please see B.12 in relation to the Issuer.

B.19 B.13

Recent events Not applicable. There are no recent events particular to the Guarantor, which are to a material extent relevant to the evaluation of the Guarantor’s solvency.

B.19 B.14

Dependence upon other entities within the Group

The Guarantor is a direct subsidiary of Mogo Finance. 100% of the Guarantor’s share capital is owned by Mogo Finance.

B.19 B.15

Description of the Guarantor’s principal activities

Principal activities of the Guarantor are vehicle financial leasing services. License for the provision of consumer credits issued by the Estonian Financial Supervision Authority.

B.19 B.16

Controlling persons As of the date of the Prospectus, 100% of the Guarantor’s share capital is directly owned and controlled by Mogo Finance. For a

14

description of the controlling persons of Mogo Finance please see B.16 in relation to the Issuer.

B.19 B.17

Credit ratings assigned to the Guarantor or its debt securities

Not applicable. The Guarantor is not rated.

B(iii) Guarantor – UAB “mogo LT” (Lithuania)

B.19 B.1

Legal and commercial name

UAB “mogo LT” (Lithuania). The Guarantor operates under the commercial name “UAB “mogo LT””.

B.19 B.2

Domicile and legal form of the Guarantor, legislation, country of incorporation.

The Guarantor’s domicile is in Vilnius, the Republic of Lithuania. The Guarantor is a Lithuanian private limited liability company incorporated and operating under the laws of Lithuania.

B.19 B.4b

Known trends affecting the Guarantor and the industries in which it operates.

Not applicable. There are no known trends affecting the Guarantor and the industries in which it operates.

B.19 B.5

Description of the group and the Guarantor’s position within the group.

The Guarantor is a subsidiary of Mogo Finance. For a description of the Group please see B.5 in relation to the Issuer.

B.19 B.9

Profit forecast or estimate is made

Not applicable (as no profit forecasts or estimates are made).

B.19 B.10

Qualifications in the audit report on the historical financial information.

Not applicable. No audit report or financial information is being presented by the Guarantor.

B.19 B.12

Selected historical key financial information

Not applicable. No financial information is being presented by the Guarantor. Consolidated financial statements of the Group are incorporated by reference into this Prospectus. For a description of the selected historical key financial information of the Group please see B.12 in relation to the Issuer.

No material adverse change in the prospects of the Guarantor

For a description of the prospects of the Group please see B.12 in relation to the Issuer.

Significant changes in the financial or trading position

For a description of the significant changes in the financial or trading position of the Group please see B.12 in relation to the Issuer.

B.19 B.13

Recent events Not applicable. There are no recent events particular to the Guarantor, which are to a material extent relevant to the evaluation of the Guarantor’s solvency.

B.19 B.14

Dependence upon other entities within the Group

The Guarantor is a direct subsidiary of Mogo Finance. 98% of the Guarantor’s share capital is owned by Mogo Finance.

B.19 B.15

Description of the Guarantor’s principal activities

Principal activities of the Guarantor are vehicle financial leasing services and consumer services. Included in the Public List of Consumer Credit Providers handled by the Bank of Lithuania allowing to provide crediting services for consumers.

B.19 B.16

Controlling persons As of the date of the Prospectus, 98% of the Guarantor’s share capital is directly owned and controlled by Mogo Finance. For a description of

15

the controlling persons of Mogo Finance please see B.16 in relation to the Issuer.

B.19 B.17

Credit ratings assigned to the Guarantor or its debt securities

Not applicable. The Guarantor is not rated.

B(iv) Guarantor – Mogo LLC (Georgia)

B.19 B.1

Legal and commercial name

Mogo LLC (Georgia). The Guarantor operates under the commercial name “Mogo LLC”.

B.19 B.2

Domicile and legal form of the Guarantor, legislation, country of incorporation.

The Guarantor’s domicile is in Tbilisi, Georgia. The Guarantor is a Georgian limited liability company incorporated and operating under the laws of Georgia.

B.19 B.4b

Known trends affecting the Guarantor and the industries in which it operates.

Not applicable. There are no known trends affecting the Guarantor and the industries in which it operates.

B.19 B.5

Description of the group and the Guarantor’s position within the group.

The Guarantor is a subsidiary of Mogo Finance. For a description of the Group please see B.5 in relation to the Issuer.

B.19 B.9

Profit forecast or estimate is made

Not applicable (as no profit forecasts or estimates are made).

B.19 B.10

Qualifications in the audit report on the historical financial information.

Not applicable. No audit report or financial information is being presented by the Guarantor.

B.19 B.12

Selected historical key financial information

Not applicable. No financial information is being presented by the Guarantor. Consolidated financial statements of the Group are incorporated by reference into this Prospectus. For a description of the selected historical key financial information of the Group please see B.12 in relation to the Issuer.

No material adverse change in the prospects of the Guarantor

For a description of the prospects of the Group please see B.12 in relation to the Issuer.

Significant changes in the financial or trading position

For a description of the significant changes in the financial or trading position of the Group please see B.12 in relation to the Issuer.

B.19 B.13

Recent events Not applicable. There are no recent events particular to the Guarantor, which are to a material extent relevant to the evaluation of the Guarantor’s solvency.

B.19 B.14

Dependence upon other entities within the Group

The Guarantor is a direct subsidiary of Mogo Finance. 98% of the Guarantor’s share capital is owned by Mogo Finance.

B.19 B.15

Description of the Guarantor’s principal activities

Principal activities of the Guarantor are vehicle financial leasing services. No license required.

B.19 B.16

Controlling persons As of the date of the Prospectus, 98% of the Guarantor’s capital is directly owned and controlled by Mogo Finance. For a description of the controlling persons of Mogo Finance please see B.16 in relation to

16

the Issuer.

B.19 B.17

Credit ratings assigned to the Guarantor or its debt securities

Not applicable. The Guarantor is not rated.

B(v) Guarantor – Mogo sp. z o.o. (Poland)

B.19 B.1

Legal and commercial name

Mogo sp. z o.o. (Poland). The Guarantor operates under the commercial name “Mogo sp. z o.o.”.

B.19 B.2

Domicile and legal form of the Guarantor, legislation, country of incorporation.

The Guarantor’s domicile is in Warsaw, Poland. The Guarantor is a Polish limited liability company incorporated and operating under the laws of Poland.

B.19 B.4b

Known trends affecting the Guarantor and the industries in which it operates.

Not applicable. There are no known trends affecting the Guarantor and the industries in which it operates.

B.19 B.5

Description of the group and the Guarantor’s position within the group.

The Guarantor is a subsidiary of Mogo Finance. For a description of the Group please see B.5 in relation to the Issuer.

B.19 B.9

Profit forecast or estimate is made

Not applicable (as no profit forecasts or estimates are made).

B.19 B.10

Qualifications in the audit report on the historical financial information.

Not applicable. No audit report or financial information is being presented by the Guarantor.

B.19 B.12

Selected historical key financial information

Not applicable. No financial information is being presented by the Guarantor. Consolidated financial statements of the Group are incorporated by reference into this Prospectus. For a description of the selected historical key financial information of the Group please see B.12 in relation to the Issuer.

No material adverse change in the prospects of the Guarantor

For a description of the prospects of the Group please see B.12 in relation to the Issuer.

Significant changes in the financial or trading position

For a description of the significant changes in the financial or trading position of the Group please see B.12 in relation to the Issuer.

B.19 B.13

Recent events Not applicable. There are no recent events particular to the Guarantor, which are to a material extent relevant to the evaluation of the Guarantor’s solvency.

B.19 B.14

Dependence upon other entities within the Group

The Guarantor is a direct subsidiary of Mogo Finance. 100% of the Guarantor’s share capital is owned by Mogo Finance.

B.19 B.15

Description of the Guarantor’s principal activities

Principal activities of the Guarantor are vehicle financial leasing services. No license required.

B.19 B.16

Controlling persons As of the date of the Prospectus, 100% of the Guarantor’s share capital is directly owned and controlled by Mogo Finance. For a description of the controlling persons of Mogo Finance please see B.16 in relation to the Issuer.

17

B.19 B.17

Credit ratings assigned to the Guarantor or its debt securities

Not applicable. The Guarantor is not rated.

B(vi) Guarantor – Mogo IFN SA (Romania)

B.19 B.1

Legal and commercial name

Mogo IFN SA (Romania). The Guarantor operates under the commercial name “Mogo IFN SA”.

B.19 B.2

Domicile and legal form of the Guarantor, legislation, country of incorporation.

The Guarantor’s domicile is in Bucharest, Romania. The Guarantor is a Romanian joint stock company incorporated and operating under the laws of Romania.

B.19 B.4b

Known trends affecting the Guarantor and the industries in which it operates.

Not applicable. There are no known trends affecting the Guarantor and the industries in which it operates.

B.19 B.5

Description of the group and the Guarantor’s position within the group.

The Guarantor is a subsidiary of Mogo Finance. For a description of the Group please see B.5 in relation to the Issuer.

B.19 B.9

Profit forecast or estimate is made

Not applicable (as no profit forecasts or estimates are made).

B.19 B.10

Qualifications in the audit report on the historical financial information.

Not applicable. No audit report or financial information is being presented by the Guarantor.

B.19 B.12

Selected historical key financial information

Not applicable. No financial information is being presented by the Guarantor. Consolidated financial statements of the Group are incorporated by reference into this Prospectus. For a description of the selected historical key financial information of the Group please see B.12 in relation to the Issuer.

No material adverse change in the prospects of the Guarantor

For a description of the prospects of the Group please see B.12 in relation to the Issuer.

Significant changes in the financial or trading position

For a description of the significant changes in the financial or trading position of the Group please see B.12 in relation to the Issuer.

B.19 B.13

Recent events Not applicable. There are no recent events particular to the Guarantor, which are to a material extent relevant to the evaluation of the Guarantor’s solvency.

B.19 B.14

Dependence upon other entities within the Group

The Guarantor is a direct subsidiary of Mogo Finance. 99.99% of the Guarantor’s share capital is owned by Mogo Finance and 0.01% of the share Capital is owned by AS “mogo”.

B.19 B.15

Description of the Guarantor’s principal activities

Principal activities of the Guarantor are vehicle financial leasing services. License for other credit services issued by the National Bank of Romania.

B.19 B.16

Controlling persons As of the date of the Prospectus, 100% of the Guarantor’s share capital is directly and indirectly owned and controlled by Mogo Finance. For a description of the controlling persons of Mogo Finance please see B.16 in relation to the Issuer.

B.19 Credit ratings assigned Not applicable. The Guarantor is not rated.

18

B.17 to the Guarantor or its debt securities

B(vii) Guarantor – Mogo Bulgaria EOOD (Bulgaria)

B.19 B.1

Legal and commercial name

Mogo Bulgaria EOOD (Bulgaria). The Guarantor operates under the commercial name “Mogo Bulgaria EOOD”.

B.19 B.2

Domicile and legal form of the Guarantor, legislation, country of incorporation.

The Guarantor’s domicile is in Sofia, Bulgaria. The Guarantor is a Bulgarian limited liability company incorporated and operating under the laws of Bulgaria.

B.19 B.4b

Known trends affecting the Guarantor and the industries in which it operates.

Not applicable. There are no known trends affecting the Guarantor and the industries in which it operates.

B.19 B.5

Description of the group and the Guarantor’s position within the group.

The Guarantor is a subsidiary of Mogo Finance. For a description of the Group please see B.5 in relation to the Issuer.

B.19 B.9

Profit forecast or estimate is made

Not applicable (as no profit forecasts or estimates are made).

B.19 B.10

Qualifications in the audit report on the historical financial information.

Not applicable. No audit report or financial information is being presented by the Guarantor.

B.19 B.12

Selected historical key financial information

Not applicable. No financial information is being presented by the Guarantor. Consolidated financial statements of the Group are incorporated by reference into this Prospectus. For a description of the selected historical key financial information of the Group please see B.12 in relation to the Issuer.

No material adverse change in the prospects of the Guarantor

For a description of the prospects of the Group please see B.12 in relation to the Issuer.

Significant changes in the financial or trading position

For a description of the significant changes in the financial or trading position of the Group please see B.12 in relation to the Issuer.

B.19 B.13

Recent events Not applicable. There are no recent events particular to the Guarantor, which are to a material extent relevant to the evaluation of the Guarantor’s solvency.

B.19 B.14

Dependence upon other entities within the Group

The Guarantor is a direct subsidiary of Mogo Finance. 100% of the Guarantor’s share capital is owned by Mogo Finance.

B.19 B.15

Description of the Guarantor’s principal activities

Principal activities of the Guarantor are vehicle financial leasing services. License for Financial Institution issued by the Bulgarian National Bank.

B.19 B.16

Controlling persons As of the date of the Prospectus, 100% of the Guarantor’s share capital is directly owned and controlled by Mogo Finance. For a description of the controlling persons of Mogo Finance please see B.16 in relation to the Issuer.

B.19 B.17

Credit ratings assigned to the Guarantor or its

Not applicable. The Guarantor is not rated.

19

debt securities

B(viii) Guarantor – Mogo Loans SRL (Moldova)

B.19 B.1

Legal and commercial name

Mogo Loans SRL (Moldova). The Guarantor operates under the commercial name “Mogo Loans SRL”.

B.19 B.2

Domicile and legal form of the Guarantor, legislation, country of incorporation.

The Guarantor’s domicile is in Chisinau, Moldova. The Guarantor is a Moldovan limited liability company incorporated and operating under the laws of Moldova.

B.19 B.4b

Known trends affecting the Guarantor and the industries in which it operates.

Not applicable. There are no known trends affecting the Guarantor and the industries in which it operates.

B.19 B.5

Description of the group and the Guarantor’s position within the group.

The Guarantor is a subsidiary of Mogo Finance. For a description of the Group please see B.5 in relation to the Issuer.

B.19 B.9

Profit forecast or estimate is made

Not applicable (as no profit forecasts or estimates are made).

B.19 B.10

Qualifications in the audit report on the historical financial information.

Not applicable. No audit report or financial information is being presented by the Guarantor.

B.19 B.12

Selected historical key financial information

Not applicable. No financial information is being presented by the Guarantor. Consolidated financial statements of the Group are incorporated by reference into this Prospectus. For a description of the selected historical key financial information of the Group please see B.12 in relation to the Issuer.

No material adverse change in the prospects of the Guarantor

For a description of the prospects of the Group please see B.12 in relation to the Issuer.

Significant changes in the financial or trading position

For a description of the significant changes in the financial or trading position of the Group please see B.12 in relation to the Issuer.

B.19 B.13

Recent events Not applicable. There are no recent events particular to the Guarantor, which are to a material extent relevant to the evaluation of the Guarantor’s solvency.

B.19 B.14

Dependence upon other entities within the Group

The Guarantor is a direct subsidiary of Mogo Finance. 100% of the Guarantor’s share capital is owned by Mogo Finance.

B.19 B.15

Description of the Guarantor’s principal activities

Principal activities of the Guarantor are vehicle financial leasing services. No license required.

B.19 B.16

Controlling persons As of the date of the Prospectus, 100% of the Guarantor’s share capital is directly owned and controlled by Mogo Finance. For a description of the controlling persons of Mogo Finance please see B.16 in relation to the Issuer.

B.19 B.17

Credit ratings assigned to the Guarantor or its debt securities

Not applicable. The Guarantor is not rated.

20

B(ix) Guarantor – Mogo Albania sh.a. (Albania)

B.19 B.1

Legal and commercial name

Mogo Albania sh.a. (Albania). The Guarantor operates under the commercial name “Mogo Albania sh.a.”.

B.19 B.2

Domicile and legal form of the Guarantor, legislation, country of incorporation.

The Guarantor’s domicile is in Tirana, Albania. The Guarantor is an Albanian joint stock company incorporated and operating under the laws of Albania.

B.19 B.4b

Known trends affecting the Guarantor and the industries in which it operates.

Not applicable. There are no known trends affecting the Guarantor and the industries in which it operates.

B.19 B.5

Description of the group and the Guarantor’s position within the group.

The Guarantor is a subsidiary of Mogo Finance. For a description of the Group please see B.5 in relation to the Issuer.

B.19 B.9

Profit forecast or estimate is made

Not applicable (as no profit forecasts or estimates are made).

B.19 B.10

Qualifications in the audit report on the historical financial information.

Not applicable. No audit report or financial information is being presented by the Guarantor.

B.19 B.12

Selected historical key financial information

Not applicable. No financial information is being presented by the Guarantor. Consolidated financial statements of the Group are incorporated by reference into this Prospectus. For a description of the selected historical key financial information of the Group please see B.12 in relation to the Issuer.

No material adverse change in the prospects of the Guarantor

For a description of the prospects of the Group please see B.12 in relation to the Issuer.

Significant changes in the financial or trading position

For a description of the significant changes in the financial or trading position of the Group please see B.12 in relation to the Issuer.

B.19 B.13

Recent events Not applicable. There are no recent events particular to the Guarantor, which are to a material extent relevant to the evaluation of the Guarantor’s solvency.

B.19 B.14

Dependence upon other entities within the Group

The Guarantor is a direct subsidiary of Mogo Finance. 100% of the Guarantor’s share capital is owned by Mogo Finance.

B.19 B.15

Description of the Guarantor’s principal activities

Principal activities of the Guarantor are vehicle financial leasing services. License for financial lease issued by the National Bank of Albania.

B.19 B.16

Controlling persons As of the date of the Prospectus, 100% of the Guarantor’s share capital is directly owned and controlled by Mogo Finance. For a description of the controlling persons of Mogo Finance please see B.16 in relation to the Issuer.

B.19 B.17

Credit ratings assigned to the Guarantor or its debt securities

Not applicable. The Guarantor is not rated.

21

B(x) Guarantor – OOO “Мого Кредит” (Belarus)

B.19 B.1

Legal and commercial name

OOO “Мого Кредит” (Belarus). The Guarantor operates under the commercial name “OOO “Мого Кредит”.

B.19 B.2

Domicile and legal form of the Guarantor, legislation, country of incorporation.

The Guarantor’s domicile is in Minsk, Belarus. The Guarantor is a Belarusian limited liability company incorporated and operating under the laws of Belarus.

B.19 B.4b

Known trends affecting the Guarantor and the industries in which it operates.

Not applicable. There are no known trends affecting the Guarantor and the industries in which it operates.

B.19 B.5

Description of the group and the Guarantor’s position within the group.

The Guarantor is a subsidiary of Mogo Finance. For a description of the Group please see B.5 in relation to the Issuer.

B.19 B.9

Profit forecast or estimate is made

Not applicable (as no profit forecasts or estimates are made).

B.19 B.10

Qualifications in the audit report on the historical financial information.

Not applicable. No audit report or financial information is being presented by the Guarantor.

B.19 B.12

Selected historical key financial information

Not applicable. No financial information is being presented by the Guarantor. Consolidated financial statements of the Group are incorporated by reference into this Prospectus. For a description of the selected historical key financial information of the Group please see B.12 in relation to the Issuer.

No material adverse change in the prospects of the Guarantor

For a description of the prospects of the Group please see B.12 in relation to the Issuer.

Significant changes in the financial or trading position

For a description of the significant changes in the financial or trading position of the Group please see B.12 in relation to the Issuer.

B.19 B.13

Recent events Not applicable. There are no recent events particular to the Guarantor, which are to a material extent relevant to the evaluation of the Guarantor’s solvency.

B.19 B.14

Dependence upon other entities within the Group

The Guarantor is an indirect subsidiary of Mogo Finance. 99.99% of the Guarantor’s share capital is owned by SIA HUB 3 and 0.01% of the share capital is owned by AS “mogo”.

B.19 B.15

Description of the Guarantor’s principal activities

Principal activities of the Guarantor are vehicle financial leasing services. License issued by the National Bank of Belarus.

B.19 B.16

Controlling persons As of the date of the Prospectus, 99.99% of the Guarantor’s share capital is indirectly owned and controlled by Mogo Finance. For a description of the controlling persons of Mogo Finance please see B.16 in relation to the Issuer.

B.19 B.17

Credit ratings assigned to the Guarantor or its debt securities

Not applicable. The Guarantor is not rated.

22

B(xi) Guarantor – SIA HUB 3 (Latvia)

B.19 B.1

Legal and commercial name

SIA HUB 3 (Latvia). The Guarantor operates under the commercial name “SIA HUB 3” (former name – SIA Mogo LT).

B.19 B.2

Domicile and legal form of the Guarantor, legislation, country of incorporation.

The Guarantor’s domicile is in Riga, Latvia. The Guarantor is a Latvian limited liability company incorporated and operating under the laws of Latvia.

B.19 B.4b

Known trends affecting the Guarantor and the industries in which it operates.

Not applicable. There are no known trends affecting the Guarantor and the industries in which it operates.

B.19 B.5

Description of the group and the Guarantor’s position within the group.

The Guarantor is a subsidiary of Mogo Finance. For a description of the Group please see B.5 in relation to the Issuer.

B.19 B.9

Profit forecast or estimate is made

Not applicable (as no profit forecasts or estimates are made).

B.19 B.10

Qualifications in the audit report on the historical financial information.

Not applicable. No audit report or financial information is being presented by the Guarantor.

B.19 B.12

Selected historical key financial information

Not applicable. No financial information is being presented by the Guarantor. Consolidated financial statements of the Group are incorporated by reference into this Prospectus. For a description of the selected historical key financial information of the Group please see B.12 in relation to the Issuer.

No material adverse change in the prospects of the Guarantor

For a description of the prospects of the Group please see B.12 in relation to the Issuer.

Significant changes in the financial or trading position

For a description of the significant changes in the financial or trading position of the Group please see B.12 in relation to the Issuer.

B.19 B.13

Recent events Not applicable. There are no recent events particular to the Guarantor, which are to a material extent relevant to the evaluation of the Guarantor’s solvency.

B.19 B.14

Dependence upon other entities within the Group

The Guarantor is a direct subsidiary of Mogo Finance. 100% of the Guarantor’s share capital is owned by Mogo Finance.

B.19 B.15

Description of the Guarantor’s principal activities

Principal activity of the Guarantor is being a holding entity. No license required.

B.19 B.16

Controlling persons As of the date of the Prospectus, 100% of the Guarantor’s share capital is directly owned and controlled by Mogo Finance. For a description of the controlling persons of Mogo Finance please see B.16 in relation to the Issuer.

B.19 B.17

Credit ratings assigned to the Guarantor or its debt securities

Not applicable. The Guarantor is not rated.

23

B(xii) Guarantor – Risk Management Service OÜ (Estonia)

B.19 B.1

Legal and commercial name

Risk Management Service OÜ (Estonia). The Guarantor operates under the commercial name “Risk Management Service OÜ”.

B.19 B.2

Domicile and legal form of the Guarantor, legislation, country of incorporation.

The Guarantor’s domicile is in Tallinn, Estonia. The Guarantor is an Estonian private limited liability company incorporated and operating under the laws of Estonia.

B.19 B.4b

Known trends affecting the Guarantor and the industries in which it operates.

Not applicable. There are no known trends affecting the Guarantor and the industries in which it operates.

B.19 B.5

Description of the group and the Guarantor’s position within the group.

The Guarantor is a subsidiary of Mogo Finance. For a description of the Group please see B.5 in relation to the Issuer.

B.19 B.9

Profit forecast or estimate is made

Not applicable (as no profit forecasts or estimates are made).

B.19 B.10

Qualifications in the audit report on the historical financial information.

Not applicable. No audit report or financial information is being presented by the Guarantor.

B.19 B.12

Selected historical key financial information

Not applicable. No financial information is being presented by the Guarantor. Consolidated financial statements of the Group are incorporated by reference into this Prospectus. For a description of the selected historical key financial information of the Group please see B.12 in relation to the Issuer.

No material adverse change in the prospects of the Guarantor

For a description of the prospects of the Group please see B.12 in relation to the Issuer.

Significant changes in the financial or trading position

For a description of the significant changes in the financial or trading position of the Group please see B.12 in relation to the Issuer.

B.19 B.13

Recent events Not applicable. There are no recent events particular to the Guarantor, which are to a material extent relevant to the evaluation of the Guarantor’s solvency.

B.19 B.14

Dependence upon other entities within the Group

The Guarantor is a direct subsidiary of Mogo Finance. 100% of the Guarantor’s share capital is owned by Mogo Finance.

B.19 B.15

Description of the Guarantor’s principal activities

Principal activities of the Guarantor are debt recovery services for the Group. No license required.

B.19 B.16

Controlling persons As of the date of the Prospectus, 100% of the Guarantor’s share capital is directly owned and controlled by Mogo Finance. For a description of the controlling persons of Mogo Finance please see B.16 in relation to the Issuer.

B.19 B.17

Credit ratings assigned to the Guarantor or its debt securities

MOGO Universal Credit Organization LLC (Armenia). The Guarantor operates under the commercial name “MOGO Universal Credit Organization LLC”.

B.19 B.2

Domicile and legal form of the Guarantor, legislation, country of incorporation.

The Guarantor’s domicile is in Armenia, Yerevan. The Guarantor is an Armenian private limited liability company incorporated and operating under the laws of Armenia.

B.19 B.4b

Known trends affecting the Guarantor and the industries in which it operates.

Not applicable. There are no known trends affecting the Guarantor and the industries in which it operates.

B.19 B.5

Description of the group and the Guarantor’s position within the group.

The Guarantor is a subsidiary of AS “HUB 1”. For a description of the Group please see B.5 in relation to the Issuer.

B.19 B.9

Profit forecast or estimate is made

Not applicable (as no profit forecasts or estimates are made).

B.19 B.10

Qualifications in the audit report on the historical financial information.

Not applicable. No audit report or financial information is being presented by the Guarantor.

B.19 B.12

Selected historical key financial information

Not applicable. No financial information is being presented by the Guarantor. Consolidated financial statements of the Group are incorporated by reference into this Prospectus. For a description of the selected historical key financial information of the Group please see B.12 in relation to the Issuer.

No material adverse change in the prospects of the Guarantor

For a description of the prospects of the Group please see B.12 in relation to the Issuer.

Significant changes in the financial or trading position

For a description of the significant changes in the financial or trading position of the Group please see B.12 in relation to the Issuer.

B.19 B.13

Recent events Not applicable. There are no recent events particular to the Guarantor, which are to a material extent relevant to the evaluation of the Guarantor’s solvency.

B.19 B.14

Dependence upon other entities within the Group

The Guarantor is an indirect subsidiary of Mogo Finance. 100% of the Guarantor’s share capital is owned by AS “HUB 1”.

B.19 B.15

Description of the Guarantor’s principal activities

Principal activities of the Guarantor are vehicle financial leasing services. License for financial lease issued by the Central Bank of Armenia.

B.19 B.16

Controlling persons As of the date of the Prospectus, 100% of the Guarantor’s share capital is directly owned and controlled by Mogo Finance. For a description of the controlling persons of Mogo Finance please see B.16 in relation to the Issuer.

B.19 B.17

Credit ratings assigned to the Guarantor or its debt securities

Not applicable. The Guarantor is not rated.

25

B(xiv) Guarantor – ТОВ МОГО УКРАЇНА (Ukraine)

B.19 B.1

Legal and commercial name

ТОВ МОГО УКРАЇНА (Ukraine). The Guarantor operates under the commercial name “ТОВ МОГО УКРАЇНА”.

B.19 B.2

Domicile and legal form of the Guarantor, legislation, country of incorporation.

The Guarantor’s domicile is in Kyiv, Ukraine. The Guarantor is an Ukrainian private limited liability company incorporated and operating under the laws of Ukraine

B.19 B.4b

Known trends affecting the Guarantor and the industries in which it operates.

Not applicable. There are no known trends affecting the Guarantor and the industries in which it operates.

B.19 B.5

Description of the group and the Guarantor’s position within the group.

The Guarantor is a subsidiary of Mogo Finance. For a description of the Group please see B.5 in relation to the Issuer.

B.19 B.9

Profit forecast or estimate is made

Not applicable (as no profit forecasts or estimates are made).

B.19 B.10

Qualifications in the audit report on the historical financial information.

Not applicable. No audit report or financial information is being presented by the Guarantor.

B.19 B.12

Selected historical key financial information

Not applicable. No financial information is being presented by the Guarantor. Consolidated financial statements of the Group are incorporated by reference into this Prospectus. For a description of the selected historical key financial information of the Group please see B.12 in relation to the Issuer.

No material adverse change in the prospects of the Guarantor

For a description of the prospects of the Group please see B.12 in relation to the Issuer.

Significant changes in the financial or trading position

For a description of the significant changes in the financial or trading position of the Group please see B.12 in relation to the Issuer.

B.19 B.13

Recent events Not applicable. There are no recent events particular to the Guarantor, which are to a material extent relevant to the evaluation of the Guarantor’s solvency.

B.19 B.14

Dependence upon other entities within the Group