56

PROSPECTUS

NAM IBBL ISLAMIC UNIT FUND

This Offer Document sets forth concisely the information about the Fund that a prospective investor ought to know before investment. This Offer Document should be read before making

an application for the Units and should be retained for future reference.

Initial Size of Issue BDT 15,00,00,000 (Fifteen crore)

Total Number of Units 1,50,00,000 (One Crore and Fifty lac)

Initial / Opening Price BDT 10 (Ten) per Unit

Sponsor:Islami Bank

Bangladesh Limited

Asset Manager:National Asset

Management Limited

Trustee & Custodian:Investment Corporation

of Bangladesh

Initial Subscription Opens June 06, 2017

Date of Prospectus Publication June 01, 2017

Investing in the NAM IBBL Islamic Unit Fund (hereinafter the Fund) bears certain risks that investors should carefully consider before investing in the Fund. Investment in the capital market and in the Fund bears certain risks that are normally associated with making investments in securities including loss of principal amount invested. There can be no assurance that the Fund will achieve its investment objectives. The Fund value can be volatile and no assurance can be given that investors will receive the amount originally invested. When investing in the Fund, investors should carefully consider the risk factors outlined in the document.

THE SPONSOR, ASSET MANAGEMENT COMPANY OR THE FUND IS NOT GURANTEEING ANY RETURNS

The particulars of the Fund have been prepared in accordance with wmwKDwiwUR I G·‡PÄ Kwgkb (wgDPz¨qvj

dvÛ) wewagvjv, 2001 as amended till date and filed with Bangladesh Securities and Exchange Commission of Bangladesh.

Registered Address:

Saiham Sky View Tower, Level-16, 45 Bijoynagar, Dhaka-1000, Bangladesh.Tel: +88 02 8391054,8391350, E-mail: [email protected], Web: www.nambd.com

Chapters Particulars Page no.

Fund Directory 5

Definitions and Elaborations of Abbreviated Terms 6

Fund Highlights 8

dv‡Ûi mswÿß weeiYx

9

Risk Factors 10

Chapter 1 Preliminary 12

1.1 Publication of Prospectus for Public Offering 12

1.2 Consent of the Bangladesh Securities and Exchange Commission 12

1.3 Listing of Fund 12

1.4 Availability of Documents for Inspection 12

1.5 Conditions under Section 2CC of the BSEC Ordinance,1969 12

1.6 General Information 15

1.7 Sale and Repurchase of Units 15

1.8 Declarations 15

1.9 Due-Diligence Certificate 17

Chapter 2 Background 21

2.1 Preamble to Formation of NAM IBBL Islamic Unit Fund 21

2.2 Capital Market of Bangladesh 21

2.3 Advantages of Investing in NAM IBBL Islamic Unit Fund 22

Chapter 3 The Fund 24

3.1 Formation of the Fund 24

3.2 Life of the Fund 24

3.3 Face Value and Denomination 24

3.4 Investment Objectives 24

3.5 Investment Policies 24

3.6 Investment Restrictions 25

3.7 Valuation Policy 25

3.8 Net Asset Value Calculation 26

3.9 Limitation of Expenses 26

3.10 Price Fixation Policy, Sale and Re-purchase Procedure 27

3.11 Winding up Policy 27

3.12 Investment Management 28

3.13 Dividend Policy 29

TABLE OF CONTENTS

Chapters Particulars Page no.

Chapter 4 The Shariah Supervisory Board 30

4.1 Member of Shariah Supervisory Board 30

4.2 Role and Responsibilities of Shariah Supervisory Board 31

Chapter 5 Investment Approach and Risk Control 32

Chapter 6 Formation, Management and Administration 33

6.1 Sponsor of the Fund 33

6.2 Trustee and Custodian of the Fund 33

6.3 Custodian of the Fund 33

6.4 Asset Manager 34

6.5 Auditors 37

6.6 Fees and Expenses 37

Chapter 7 Capital Structure and Rights of Unit Holders 40

7.1 Issue of Units 40

7.2 Sponsor’s Subscription 40

7.3 Rights of the Unit Holders 40

Chapter 8 Unit Subscription 42

8.1 Terms and Conditions of Unit Subscription 42

8.2 Collection Bank And Selling Agent 42

Chapter 9 Sales Agents 43

9.1 Selling Agents 43

9.2 Forms 43

TABLE OF CONTENTS

5NAM IBBL Islamic Unit Fund

FUND DIRECTORY

Sponsor Islami Bank Bangladesh Limited (IBBL)Islami Bank Tower, 40, Dilkusha C/ADhaka – 1000,BangladeshTel: +88 02 9563040

Trustee Investment Corporation of Bangladesh (ICB) 8, Rajuk Avenue (Level 14-17)Dhaka-1000, BangladeshTel: +88 02 9563455

Custodian Investment Corporation of Bangladesh (ICB) 8, Rajuk Avenue (Level 14-17)Dhaka-1000, BangladeshTel: +88 02 9563455

Asset Manager National Asset Management Ltd. (NAML)Saiham Sky View Tower, Level-1645 Bijoynagar, Dhaka-1000,Bangladesh, Tel: +88 02 8391054

Auditor Ahmed Zaker & Co.Saiham Sky View Tower (2nd Floor) 45 Bijoynagar, Dhaka-1000,Bangladesh, Tel: 8391440-3

Banker First Security Islami Bank Ltd.28, Topkhana Road Branch, Dhaka, Topkhana Road, Dhaka 1000, Bangladesh,Tel: +88 02 9563040

For prospectus or any other information please contact at following corporate office of the Asset Management Company:

National Asset Management LimitedSaiham Sky View Tower, Level-16, 45 Bijoynagar,Dhaka-1000, Bangladesh, Tel: +88 02 8391054, 8391350Email: [email protected], Website: www.nambd.com

Any person interested to get a prospectus may obtain from the Asset Management Company.

“If you have any query about this document, you may consult the Asset Management Company”

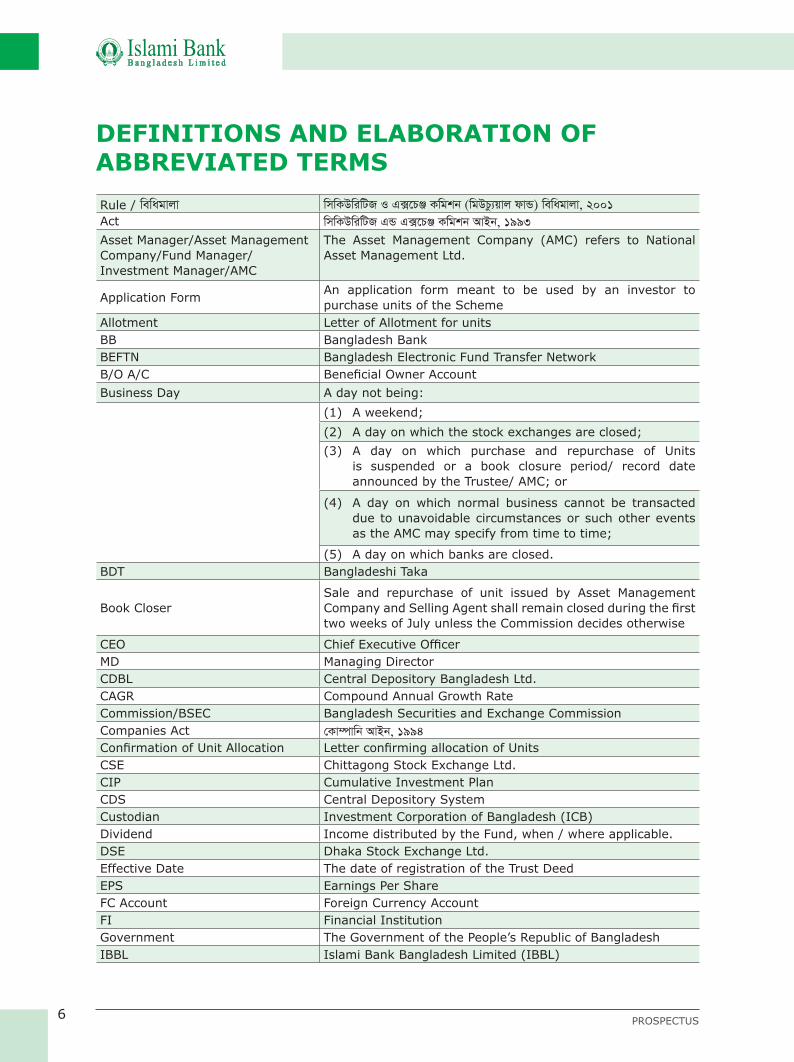

6 PROSPECTUS

DEFINITIONS AND ELABORATION OF ABBREVIATED TERMS

Rule / wewagvjv

wmwKDwiwUR I G·‡PÄ Kwgkb (wgDPz¨qvj dvÛ) wewagvjv, 2001

ActwmwKDwiwUR GÛ G·‡PÄ Kwgkb AvBb, 1993

Asset Manager/Asset Management Company/Fund Manager/Investment Manager/AMC

The Asset Management Company (AMC) refers to National Asset Management Ltd.

Application FormAn application form meant to be used by an investor to purchase units of the Scheme

Allotment Letter of Allotment for unitsBB Bangladesh BankBEFTN Bangladesh Electronic Fund Transfer NetworkB/O A/C Beneficial Owner Account

Business Day A day not being:

(1) A weekend;

(2) A day on which the stock exchanges are closed;

(3) A day on which purchase and repurchase of Units is suspended or a book closure period/ record date announced by the Trustee/ AMC; or

(4) A day on which normal business cannot be transacted due to unavoidable circumstances or such other events as the AMC may specify from time to time;

(5) A day on which banks are closed.BDT Bangladeshi Taka

Book CloserSale and repurchase of unit issued by Asset Management Company and Selling Agent shall remain closed during the first two weeks of July unless the Commission decides otherwise

CEO Chief Executive OfficerMD Managing DirectorCDBL Central Depository Bangladesh Ltd.CAGR Compound Annual Growth RateCommission/BSEC Bangladesh Securities and Exchange CommissionCompanies Act

†Kv¤úvwb AvBb, 1994

Confirmation of Unit Allocation Letter confirming allocation of UnitsCSE Chittagong Stock Exchange Ltd.CIP Cumulative Investment PlanCDS Central Depository SystemCustodian Investment Corporation of Bangladesh (ICB)Dividend Income distributed by the Fund, when / where applicable.DSE Dhaka Stock Exchange Ltd.Effective Date The date of registration of the Trust DeedEPS Earnings Per ShareFC Account Foreign Currency AccountFI Financial InstitutionGovernment The Government of the People’s Republic of BangladeshIBBL Islami Bank Bangladesh Limited (IBBL)

7NAM IBBL Islamic Unit Fund

ICB Investment Corporation of BangladeshISO Initial Subscription OfferingIPO Initial Public OfferingIssue Public IssueIDRA Insurance Development & Regulatory Authority of BangladeshMSND A/C Mudaraba Special Notice Deposit AccountMutual Fund/ The Fund/ Unit Fund/ Open End Mutual Fund

NAM IBBL Islamic Unit Fund

Non-Resident Bangladeshi/ NRB

Non-resident Bangladeshi (NRB) means Bangladeshi citizens staying abroad including all those who have dual citizenship provided they have a valid Bangladeshi passport or those, whose foreign passport bear a stamp from the concerned Bangladesh embassy/ High Commission to the effect that no visa is required to travel to Bangladesh

NAM National Asset Management Ltd.NAV Net Asset ValueNBFI Non-Banking Financial InstitutionNBR National Board of Revenue

Ongoing Offer PeriodOffer of units of the Fund after the closure of the initial offer period.

Offering Price Price of the Securities of the Fund being offered

Offer Document

This document issued by NAM IBBL Islamic Unit Fund, offering units of the Fund for subscription. Any modifications to the offer document will be made by way of an addendum which will be attached to offer document. On issuance of any such addendum, prior approval from BSEC is required and the offer document will be deemed to be updated by the addendum.

Prospectus

The advertisement or other documents (approved by the BSEC), which contain the investment and all other information in respect of the mutual fund, as required by the wewagvjv and is circulated to invite the public to invest in the mutual fund.

Purchase/ Subscription Subscription to/ purchase of units of the Fund

Purchase PriceThe price, calculated in the manner provided in this offer document, at which the units can be purchased.

Repurchase Repurchase of units by the Fund from a unit holder

Repurchase PricePrice at which the units can be redeemed/repurchased and calculated in the manner provided in this offer document.

RJSC Registrar of Joint Stock Companies and FirmsSponsor Islami Bank Bangladesh Limited (IBBL)SCS Shariah Complaint SecuritiesSales Agent/ Selling Agent/Point of Sales

AMC designated official points for accepting transaction/ service requests from investors.

Securities Units of the FundSubscription Application MoneyTrustee Investment Corporation of Bangladesh (ICB)The Scheme NAM IBBL Islamic Unit Fund

Unit HolderA person holding units of NAM IBBL Islamic Unit Fund offered under this offer document.

Unit Certificate/Certificate Unit Certificate of the Fund in dematerialized form under CDBLUnit One undivided share in the Fund

8 PROSPECTUS

FUND HIGHLIGHTS

Name NAM IBBL Islamic Unit Fund

Nature Open-End Mutual fund

Life and Size of the Fund Perpetual life and unlimited size

Sponsor Islami Bank Bangladesh Limited (IBBL)

Trustee Investment Corporation of Bangladesh (ICB)

Custodian Investment Corporation of Bangladesh (ICB)

Asset Manager National Asset Management Ltd. (NAML)

Initial Size of the FundBDT 15,00,00,000 (BDT fifteen crore) divided into 1,50,00,000 (One crore fifty lac) Units of Tk.10 (Taka ten) each

Face Value Tk.10 (Taka ten) per Unit

Objective

The objective of the NAM IBBL Islamic Unit Fund is to achieve superior risk adjusted return in the forms of capital appreciation, dividend income and to provide attractive dividend payments to the unit holders by investing the fund only in Shariah compliant instruments of capital market and money market.

Minimum Application Amount

Tk.5,000/- per application (500 Units) for individualsTk.50,000/- per application (5,000 Units) for institutions

TransparencyNAV will be calculated on a weekly basis and shall be published on the web-site of the Fund manager (www.nambd.com) and as prescribed in the Rule

Target GroupIndividuals –both resident and non-resident, institutions–both local and foreign, mutual funds and collective investment schemes are eligible to subscribe the Units of the Fund.

Shariah Supervisory Board

The Fund shall be managed under Shariah Law. In this regard, a “NAML Shariah Supervisory Guideline” was framed to ensure the compliance of Shariah Law which was submitted to Trustee and BSEC. Under this Guideline, a Shariah Supervisory board consisting of renowned Islamic Scholars of Bangladesh is formed. This board will work with NAML to ensure compliance of investment management as per Shariah Law.

DividendMinimum 70 (seventy) percent of realized income of the Fund will be distributed as dividend in Bangladeshi Taka in each accounting year.

Dividend DistributionThe dividend warrant will be distributed within 45 (forty-five) days from the date of declaration.

TransferabilityThe Units of the Fund are transferable by way of inheritance/ gift and/ or by specific operation of the law.

EncashmentThe Unit holders can surrender their units through the Asset Manager and through the Selling Agents appointed by the Asset Manager. So, investment in the Fund will be easily encashable.

Reports and Accounts

Every unit holder is entitled to receive annual report along with the yearly and half-yearly statements of accounts as and when published from the website (www.nambd.com). Every unit holders will also get quarterly statements of portfolio in NAML’s official website.

Tax Benefit

Income from a mutual fund or a unit fund up to Tk. 25,000.00 (Twenty-Five Thousand) is exempted from tax under Income Tax Ordinance 1984. Investment in the Fund would qualify for investment tax credit under section 44(2) of the Income Tax Ordinance, 1984.

9NAM IBBL Islamic Unit Fund

dv‡Ûi mswÿß weeiYx

bvg Gb G Gg AvBweweGj BmjvwgK BDwbU dvÛ

cÖK…wZ †e-‡gqv`x wgDPzqvj dvÛ|

dv‡Ûi †gqv`Kvj I AvKvi †e-‡gqv`x I mxgvnxb AvKvi|

D‡`¨v³v Bmjvgx e¨vsK evsjv‡`k wjwg‡UW (AvB we we Gj)|

U&ªvw÷ Bb‡f÷‡g›U K‡cv©‡ikb Ae evsjv‡`k (AvB wm we)|

†ndvRZKvix Bb‡f÷‡g›U K‡cv©‡ikb Ae evsjv‡`k (AvB wm we)|

m¤ú` e¨e¯’vcK b¨vkbvj G‡mU g¨v‡bRg¨v›U wjwg‡UW|

dv‡Ûi cÖv_wgK AvKvi

$ 15,00,00,000 (UvKv c‡bi †KvwU) wef³ 1,50,00,000 (GK †KvwU cÂvk jvL)

BDwb‡U hvi cÖwZwUi AwfwnZ g~j¨ 10 UvKv|

AwfwnZ g~j¨ UvKv 10 (`k) cªwZ †kqv‡ii g~j¨|

D‡Ïk¨

Gb G Gg AvBweweGj BmjvwgK BDwbU dv‡Ûi D‡Ïk¨ n‡”Q g~jabx jvf Ges jf¨vs‡ki gva¨‡g

SzuwK mgwš^Z wiUvb© cÖ`vb Kiv| GB dv‡Ûi gva¨‡g jf¨vsk wewb‡qvM Kvix‡`i †`qv nq cyuwRevRvi,

A_©evRvi, BZ¨vw` kixqvn m¤§Z c·Kv‡l wewb‡qv‡Mi gva¨‡g|

b~b¨Zg wewb‡qvM

UvKv 5000 e¨w³MZ Av‡e`‡bi wecix‡Z|

UvKv 50000 cÖwZôv‡bi Av‡e`‡bi wecix‡Z|

¯^”QZv

wewagvjv Abyhvqx dv‡Ûi NAV cÖwZ mßv‡n MYbv Kiv n‡e Ges m¤ú` e¨e¯’vc‡Ki I‡qe mvB‡U

cÖKvk Kiv n‡e| m¤ú` e¨e¯’vc‡Ki I‡qe mvB‡Ui wVKvbv n‡”Q (www.nambd.com)

m¤¢ve¨ wewb‡qvMKvix

e¨vw³ cÖevmx Ges †`‡k emevmKvix DfqB, cÖwZôvb-†`wk-we‡`kx DfqB, wgDPzqvj dvÛ Ges

mgwóMZ Znwe‡ji w¯‹g mg~n †h ¸‡jv AvBbMZ fv‡e MwVZ Zviv dv‡Ûi †kqvi µq Kivi ¯^ÿgZv

iv‡L|

kixqvn Z`viKx †evW©

GB dvÛ MVb Kiv n‡e kixqvn AvBb †gvZv‡eK| Gb G Gg kixqvn mycvifvBRvix MvBWjvBb

GB g‡g© MVb Kiv n‡q‡Q hv kixqvn AvBb Øviv cwiPvwjZ| MvBWjvBbwU Uªvw÷ Ges we Gm B

wmi wbKU †ck Kiv n‡q‡Q| GB MvBWjvB‡bi Aax‡b ¯^bvgab¨ BmjvwgK wPšÍvwe`‡`i wb‡q GKwU

kixqvn Dc‡`óv KwgwU MVb Kiv n‡q‡Q| Gb G Gg Ges GB Dc‡`óv gÛjxMb GK‡Î wewb‡qv‡Mi

wm×všÍ MÖnY K‡ib kixqvn MvBWjvBb ‡gvZv‡eK|

jf¨vsk

cÖwZwU wnmve eQ‡ii †k‡l evwl©K jv‡fi b~b¨Zg 70 (mËi) kZvsk A_© jf¨vsk wn‡m‡e evsjv‡`kx

UvKvq weZib Kiv n‡e|

jf¨vsk weZib jf¨vsk cÎ (wWwf‡WÛ Iqv‡i›U) jf¨vsk †NvlYvi 45 w`‡bi g‡a¨ weZib Kiv n‡e|

n¯’všÍi †hvM¨Zv DËivwaKvi/Dcnvi A_ev AvBb Øviv Aby‡gvw`Z fv‡e GB dv‡Ûi BDwbU mg~n n¯’všÍi Kiv hv‡e|

bM`vqb

BDwbU‡nvìviMY Zv‡`i BDwbU bM`vqb Ki‡Z cvi‡eb mivmwi m¤ú` e¨e¯’vc‡Ki gva¨‡g A_ev

m¤ú` e¨e¯’vc‡Ki wb‡qvMcÖvß weµq cÖwZwbwai gva¨‡g|

†cÖvm‡c±vm, evwl©K cÖwZ‡e`b

Ges wnmvemg~n

†h‡Kvb wewb‡qvMKvix m¤ú` e¨e¯’vc‡Ki I‡qe mvBU (www.nambd.com) ‡_‡K GB

†cÖvm‡c±vmwU †`L‡Z cvi‡eb| m¤ú` e¨e¯’vc‡Ki I‡qe mvBU G cÖKvwkZ evrmwiK I A_© evrmwiK

Avw_©K wee„wZ cÖ‡Z¨K BDwbU †nvìviMY cv‡eb| GQvov BDwbU †nvìviMY m¤ú` e¨e¯’vc‡Ki I‡qe

mvB‡U †cvU©‡dvwjIi cÖvwšÍK cÖwZ‡e`bI cv‡eb|

Ki‡iqvZ RwbZ myweav

Tax ordinance 1984- G wgDPzqvj dvÛ A_ev BDwbU dvÛ n‡Z Avq Gi 25,000 UvKv ch©šÍ

K‡ii AvIZvgy³ _vK‡e| BDwbU dv‡Û wewb‡qvM Tax ordinance 1984, Gi †mKkb 44(2)

Abyhvqx wewb‡qvM Ki m¤§vbx (Investment tax credit) myweav cv‡eb|

10 PROSPECTUS

RISK FACTORS

Investing in the NAM IBBL Islamic Unit Fund (hereinafter the Fund) involves certain considerations in addition to the risks normally associated with making investments in securities. The value of the Fund may go down as well as up and there can be no assurance that on redemption, or otherwise, investors will receive the amount originally invested. Accordingly, the Fund is only suitable for investment by investors who understand the risks involved and who are willing and able to withstand the risk of losing of their investments. In particular, prospective investors should consider the following risks:

1. General

There is no assurance that the Fund will be able to meet its investment objective and investors could potentially incur losses, including loss of principal when investing in the Fund. Investment in the Fund is not guaranteed by any government agency, the sponsor or the AMC. Mutual funds and securities investments are subject to market risks and there can be no assurance or guarantee that the Fund’s objectives will be achieved. As with any investment in securities, the Net Asset Value of the Fund may go up or down depending on the various factors and forces affecting the capital markets and Money Markets. Past performance of the Sponsors and their affiliates and the AMC do not indicate the future performance of the Fund. Investors should study this Offer Document carefully before making investment.

2. External Risk Factor

Performance of the Fund is substantially dependent on the macro economic situation and capital market as well as money market of Bangladesh. Political and social instability may have an adverse effect on the value of the Fund’s assets. Adverse natural calamities may impact the performance of the Fund.

3. Market Risk

The Bangladesh capital market is highly volatile and mutual fund prices and prices of securities can fluctuate significantly. The Fund may lose its value or incur a sizable loss on its investments due to such market volatility. Stock market trends indicate that prices of majority of all the listed securities move in unpredictable direction which may affect the value of the Fund. Furthermore, there is no guarantee that the market prices of the units of the Fund will fully reflect their underlying Net Asset Values.

4. Concentration Risk

Due to a limited number of listed securities in both the DSE and CSE, it may be difficult to invest the Fund’s assets in a widely-diversified portfolio as and when required to do so. Due to a very thin secondary bond/money market in Bangladesh, it would be difficult for the Fund Manager to swap between asset classes, if and when required. Limited options in the money market instruments will narrow the opportunity of short term or temporary investments of the Fund which may adversely impact the returns.

5. Dividend Risk

Despite careful investment selection of securities in the Fund, if the issuers fail to provide the expected dividend or fail to disburse the dividends declared in a timely manner, this will impact the income of the Fund and the overall return of the Fund.

6. Underlying Liquidity Risk

For investing unlisted equity securities by the Fund, may incur liquidity risk. In addition, market

11NAM IBBL Islamic Unit Fund

conditions and investment allocation may have an impact on the ability to sell securities during periods of market volatility, bond/money market while somewhat less liquid, lack a well-developed secondary market, which may restrict the selling ability of the Fund and may lead to the Fund incurring losses till the security is finally sold. While securities that are listed on the stock exchanges carry lower liquidity risk, the ability to sell these investments is limited by the overall trading volume on the stock exchanges and may lead to the Fund incurring losses till the security is finally sold.

7. Investment Strategy Risk

Since the Fund will be an actively managed investment portfolio; the Fund is subject to management of strategy risk. Although the AMC will apply its investment process and risk minimization techniques when making investment decisions for the Fund, there can be no guarantee that such process and techniques will produce the desired outcome.

8. Credit Risk

Since the Fund will seek to invest as per the wmwKDwiwUR I G·‡PÄ Kwgkb (wgDPy¨qvj dvÛ) wewagvjv, 2001 in both equity and Shariah complaint bonds, the credit risk of the Shariah complaint issuers is also associated with the Fund. Investments in Shariah complaint bonds are subject to the risk of an issuer’s inability to meet repayments on its obligations and market perception of the creditworthiness of the issuer.

9. Yield Risk

The Net Asset Value (NAV) of the Fund, to the extent invested in Shariah complaint bonds and Money Market securities will be affected by changes in the general level of yield. The NAV of the Fund is expected to increase from a fall in yield level in the economy while it would be adversely affected by an increase in yield. In addition, zero coupon securities do not provide periodic profit payments to the holder of the security; these securities are more sensitive to changes in yield available in the economy. Therefore, the yield risk of zero coupon securities is higher. The AMC may choose to invest in Shariah compliant zero coupon securities that offer attractive yields. This may increase the risk of the portfolio.

10. Issuer Risk

In addition to market and price risk, value of an individual security can, in addition, be subject to factors unique or specific to the issuer, including but not limited to management malfeasance, lack of accounting transparency, management performance, management decision to take financial leverage. Such risk can develop in an unpredictable fashion and can only be partially mitigated, and sometimes not at all, through research or due diligence. To the degree that the Fund is exposed to a security whose value declines due to issuer risk, the Fund’s value may be impaired.

12 PROSPECTUS

CHAPTER 1: PRELIMINARY

1.1 Publication of Prospectus for Public Offering

National Asset Management Limited has received Registration Certificate from the Bangladesh Securities and Exchange Commission (BSEC) under the Securities and Exchange Commission Law, 1993, and the Securities and Exchange Commission (Mutual Fund) Rules, 2001 made there under and also received consent for issuing prospectus of NAM IBBL Islamic Unit Fund for public offering. A complete copy of the prospectus is available for public inspection at Saiham Sky View Tower, Level-16, 45 Bijoynagar, Dhaka-1000, the registered office of National Asset Management Ltd., the asset manager of NAM IBBL Islamic Unit Fund, hereinafter referred to as the Fund.

1.2 Consent of the Bangladesh Securities and Exchange Commission (BSEC)

APPROVAL OF THE SECURITIES AND EXCHANGE COMMISSION HAS BEEN OBTAINED TO THE ISSUE/OFFER OF THE FUND UNDER THE SECURITIES AND EXCHANGE ORDINANCE, 1969; THE SECURITIES AND EXCHANGE COMMISSION (MUTUAL FUND) RULES, 2001. IT MUST BE DISTINCTLY UNDERSTOOD THAT IN GIVING THIS APPROVAL THE COMMISSION DOES NOT TAKE ANY RESPONSIBILITY FOR THE FINANCIAL SOUNDNESS OF THE FUND, ANY OF ITS SCHEMES OR THE ISSUE PRICE OF ITS UNITS OR FOR THE CORRECTNESS OF ANY OF THE STATEMENTS MADE OR OPINION EXPRESSED WITH REGARD TO THEM. SUCH RESPONSIBILITY LIES WITH THE ASSET MANAGER, TRUSTEE, SPONSOR AND/OR CUSTODIAN.”

1.3 Listing of Fund

The Fund, being an open-ended one, will not be listed with any stock exchanges of the country; hence the Units of the Fund will not be traded in the stock exchanges unless otherwise BSEC and stock exchange houses make arrangement in future. In that case, public communication will be made as per BSEC’s approval.

Units of the Fund will always be available for sale and surrender/ repurchase except on the last working day of every week and during book closure period/record date of the Fund at the office of the Asset Manager and the office so of authorized selling agents. Asset Manager shall disclose selling price and surrender/repurchase price of Units at the beginning of business operation on the first working day of every week as per the Rule.

1.4 Availability of Documents for Inspection

I. Copy of this prospectus will be available at the registered office of the Asset Manager and offices of the authorized selling agents of the Fund. This prospectus will also be available at the website of Bangladesh Securities and Exchange Commission (www.sec.gov.bd) and National Asset Management Ltd. (www.nambd.com).

II. Copy of the trust deed will be available for public inspection during the business hours at the office of the asset manager of the Fund. Investors will be able to purchase a copy of the trust deed by paying the price as determined by the Asset Manager.

1.5 Conditions under Section 2CC of the Securities & Exchange Ordinance, 1969

I. The Fund shall not account for any upward revaluation of its assets creating reserve without clearance from Bangladesh Securities and Exchange Commission;

II. The Fund shall not be involved in option trading, short selling or carry forward transaction;

III. A confirmation of Unit Allocation shall be issued at the cost of the Fund at par value of Tk. 10.00 (Taka ten) each within 90 (ninety) days from the date of sale of such Units;

13NAM IBBL Islamic Unit Fund

IV. Money receipt/acknowledgement slip issued at the time of sale of Units will be treated as allotment letter, which shall not be redeemable/transferable;

V. The annual report of the Fund/or its abridged version will be published within 45 (forty-five) days of the closure of each accounting year of the Fund;

VI. An annual report and details of wise investment and savings of the Fund shall be submitted to the Commission, Trustee and Custodian of the fund within 90 (ninety) days from the closure of the accounts;

VII. Half-yearly accounts/financial results of the Fund will be published in at least one English and another Bangla national daily newspapers within 30 (thirty) days from end of the period;

VIII. Dividend shall be paid within 45 (forty-five) days of its declaration, and a report shall be submitted to BSEC, Trustee and Custodian within 7 (seven) days of dividend distribution;

IX. Net Asset Value (NAV) of the Fund shall be calculated and disclosed publicly at least once a week.

X. The script wise detail portfolio statement consisting of capital market and other than capital market holdings of the fund shall be disclosed in the website of the AMC on quarterly basis within thirty (30) days of each quarter end;

XI. After initial public subscription, the sale and repurchase/surrender price of Units will be determined by the Asset Management Company. NAV at market price per unit calculated on a date shall form the highest sale price of units by rounding up the amount and shall be effective per unit up to next calculation of NAV of the Fund. Difference between sale and repurchase price shall primarily be Tk.0.30, which may be changed in future, but not be over 5% of the sale price of the Unit;

XII. BSEC may appoint auditors for special audit /investigation on the affairs of the Fund, if it so desires;

XIII. The Fund shall maintain separate bank account(s) to keep the sale proceeds of units and to meet up day-to-day transaction including payment against Repurchase of Units. All transactions of the account shall be made through banking channel and shall be properly documented;

XIV. The prospectus/abridged version of the prospectus shall be published in one widely circulated Bangla national daily newspaper. Provided that information relating to publication of prospectus be published in 2 national daily newspapers (Bengali and English) and one online newspaper;

XV. If abridged version of the prospectus is published in the newspaper, complete prospectus shall be made available to the applicants publishing it in their own website;

XVI. If the Fund manager fails to collect the minimum 40% of the initial target amount under wewa 48

of the wmwKDwiwUR I G·‡PÄ Kwgkb (wgDPy¨qvj dvÛ) wewagvjv, 2001, will refund the subscription money within 30 days without any deduction. In case of failure, the Fund manager will refund the same with an interest @18 percent per annum from its own account within the next month;

XVII. The AMC should ensure compliance of wewa 46 of the wmwKDwiwUR I G·‡PÄ Kwgkb (wgDP¨yqvj dvÛ)

wewagvjv, 2001.

XVIII.On achievement of 40% of the initial target amount, the Fund is allowed to commence investment activities of the Fund with permission of the Trustee;

XIX. The size of the Fund may be increased from time to time by the AMC subject to approval of the Trustee and with intimation to the Commission;

14 PROSPECTUS

XX. Confirmation of Unit Allocation of the sponsor’s contribution amounting to Tk.10,00,00,000/- (BDT Ten Crore) only shall be subject to a lock-in for a period of minimum three years from the date of formation of the fund and after that period entire holding may be transferred to any eligible institution who has the qualification to be a sponsor of a mutual fund with prior permission of BSEC.

XXI. A Confirmation of Unit Allocation amounting Tk. 10,00,00,000/- (66.67% of the Fund) will be issued in favor of the sponsor. The said confirmation letter shall be in the custody of the Trustee. No splitting of the Unit of Sponsor shall be made without prior approval of the Commission.

XXII. Annual fee of the fund shall be submitted to the commission on the fund size i.e. year end Asset Value at market price of the fund on advance basis as per Rule; and may adjust the fee in the next year if necessary.

XXIII. Please ensure that the following are adhered to:

(a) As per provisions contained in the wmwKDwiwUR I G·‡PÄ Kwgkb (wgDP¨yqvj dvÛ) wewagvjv, 2001 regarding limitation of time on closure of subscription, the initial public subscription will remain open for forty-five days or for a period up to achievement of the initial target amount, whichever is earlier;

(b) The paper cutting of the published prospectus and all other published documents/notices regarding the Unit Fund shall be submitted to the Commission within 24 hours of publication thereof;

(c) The Asset Management Company shall submit 10 (ten) copies of printed prospectus to the Commission for official record;

(d) The Asset Management Company shall ensure in writing to the Commission that the prospectus/ abridged version is published correctly and is a verbatim copy of the prospectus/abridged version vetted by the Commission;

(e) The AMC shall apply the spot buying rate (TT clean) of Sonali Bank prevalent on the date of opening of subscription for conversion of foreign currencies;

(f) The AMC shall submit to the Commission a diskette containing the vetted prospectus and its abridged version;

(g) All conditions imposed under Section 2CC of the Securities and Exchange Ordinance, 1969 must be complied with and be incorporated in the body of the prospectus and its abridged version;

(h) After due approval by the Trustee regarding issue and formation expenses, the AMC shall submit in details to the Commission regarding issue and formation expenses within 15 days of fund operation. The Auditor of the fund shall also put opinion about the above expanses in the initial financial statements of the fund.

(i) The Investment Policy and Guideline and information on constituents of Investment Committee of the Fund approved by the Board shall be submitted to the Commission within 30 (thirty) days from received of the consent letter. The Investment Policy and Guideline shall include among other issues, the investment delegation power of the Chief Executive Officer and the Committee separately and also the meeting resolution presentation process.

15NAM IBBL Islamic Unit Fund

1.6 General Information

i. This prospectus has been prepared by National Asset Management Ltd. based on the Trust Deed executed between the Trustee and the Sponsor of the Fund, which is approved by the Commission and available publicly. The information contained herein is true and correct in all material aspects and there is no other material fact, the commission of which would make any statement herein misleading.

ii. No person is authorized to give any information to make any representation not contained in this prospectus and if so given or made, such information or representation must not be relied upon as having been authorized by National Asset Management Ltd.

iii. The issue as contemplated in this document is made in Bangladesh is subject to the exclusive jurisdiction of the court of Bangladesh. Forwarding this prospectus to any person residing outside Bangladesh in no way implies that the issue is made in accordance with the laws of that country or is subject to the jurisdiction of the laws of that country.

1.7 Sale and Repurchase of Units

NAML will maintain two BO Accounts with Investment Corporation of Bangladesh, custodian of NAM IBBL Islamic Unit Fund for creation and redemption of units namely “NAM IBBL Islamic Unit Fund - Sale of units” and “NAML IBBL Islamic Unit Fund – Repurchase of units”.

For sale of units NAML will issue a certificate for the units sold and send it to ICB for setting-up of “Demat” request. After the acceptance of “Demat” setup by NAML from its terminal, units will be credited to the BO Account “NAM IBBL Islamic Unit Fund - Sale of units”. Then ICB will transfer the units from NAM IBBL Islamic Unit Fund - Sale of units to the unit holders BO Accounts as per instruction of NAML.

In the case of Redemption/Repurchase by the Asset Manager, the unit holder will transfer his/her/the institutional holders’ units to the NAM IBBL Islamic Unit Fund – Repurchase of units’ account. ICB will debit the unit certificates from the investor’s BO Accounts and transfer it to the NAM IBBL Islamic Unit Fund – Repurchase of units’ account. Simultaneously, the payment will be made through A/C payee Cheque or funds will be transferred to investor’s Bank Account through BEFTN as per the request of the client.

1.8 Declarations

a) Declaration about the Responsibility of the Sponsor

The Sponsor, whose name appears in this prospectus, accepts full responsibility for the authenticity and accuracy of the information contained in this prospectus and other documents regarding NAM IBBL Islamic Unit Fund. To the best of the knowledge and belief of the Sponsor, who has taken all reasonable care to ensure that all the conditions and requirements concerning this public offer and all the information contained in this document, drawn up by virtue of the Trust Deed of the Fund by the entrusted Asset Management Company, have been met and there is no other information or document, the omission of which may make any information or statements therein misleading. The Sponsor also confirms that full and fair disclosures have been made in this prospectus to enable the investors to make a decision for investment.

Sd/-

Md. Abdul Hamid MiahManaging Director & CEOIslami Bank Bangladesh Limited

16 PROSPECTUS

b) Declaration about the Responsibility of the Asset Management Company

This Prospectus has been prepared by us based on the Trust Deed, the Investment Management agreement, the wmwKDwiwUR I G·‡PÄ Kwgkb (wgDPy¨qvj dvÛ) wewagvjv, 2001, and other related agreements and examination of other documents as relevant for adequate disclosure of the Funds objectives and investment strategies to the investors. We also confirm that,

I. The prospectus is inconformity with the documents, materials and papers related to the public offer;

II. All the legal requirements of the public offer have been duly fulfilled; and

III. The disclosures made are true, fair and adequate for investment decision.

Investors should be aware that the value of investments in the Fund could be volatile and as such no guarantee can be made about the returns from the investments that the Fund will make. Like any other equity investment, only investors who are willing to accept a moderate degree of risk, should invest in the Fund. Investors are requested to pay careful attention to the risk factors as detailed in the Risk Factor section and to take proper cognizance of the risks associated with any investment in the Fund.

Sd/-

Md. AmanullahChief Executive OfficerNational Asset Management Limited

c) Declaration about the Responsibility of the Trustee

We, as Trustee of the NAM IBBL Islamic Unit Fund, accept the responsibility and confirm that we shall:

a. Be the guardian of the Fund, held in trust for the benefit of the Unit holders in accordance with the Rules and the Trust Deed;

b. Always act in the interest of the Unit holders;

c. Take all reasonable care to ensure that the Fund floated and managed by the Asset Management Company are in accordance with the Trust Deed and the Rules;

d. Make such disclosures by the Asset Management Company to the investors as are essential in order to keep them informed about any information, which may have any bearing on their investments; and

e. Take such remedial steps as are necessary to rectify the situation where we have reason to believe that the conduct of business of the Fund is not in conformity with relevant Rules.

Sd/-

Md. Taleb HossainAssistant General ManagerTrustee DepartmentInvestment Corporation of Bangladesh

17NAM IBBL Islamic Unit Fund

d) Declaration about the Responsibility of the Custodian

We, as Custodian of the NAM IBBL Islamic Unit Fund, accept the responsibility and confirm that we shall:

I. Keep all the securities of the Fund in safe custody and shall provide the highest security for the assets of the Fund; and

II. Preserve necessary documents and record so as to ascertain movement of assets of the Fund as per Rules.

Sd/-

Md. Shakhawat HossainAssistant General ManagerCustodian DepartmentInvestment Corporation of Bangladesh

1.9 Due Diligence Certificate

DUE DILIGENCE CERTIFICATE BY SPONSOR

PZy_© Zdwmj-(1) Gi 1(R) [wewa 43(3) `«óe¨]

ChairmanBangladesh Securities and Exchange Commission

Subject: NAM IBBL Islamic Unit Fund.

We, the sponsor to the above-mentioned forthcoming mutual fund, state as follows:

1. We, as the sponsor to the above mentioned fund, have examined the draft prospectus and other documents and materials as relevant to our decision; and

2. We warrant that we shall comply with the wmwKDwiwUR I G·‡PÄ Kwgkb (wgDP¨yqvj dvÛ) wewagvjv, 2001,

Bangladesh Securities and Exchange Commission (Public Issue) Rules, 2015, Trust Deed of the Fund and the Rules, orders, guidelines, directives, notifications and circulars that may be issued by the Bangladesh Securities and Exchange Commission from time to time in this respect.

WE CONFIRM THAT:

a) All information in the draft prospectus forwarded to the Commission is authentic and accurate;

b) We as sponsor of the fund as mentioned above will act as per clauses of the trust deed executed with the trustee and shall assume the duties and responsibilities as described in the trust deed and other constitutive documents;

c) We shall also abide by the wmwKDwiwUR I G·‡PÄ Kwgkb (wgDP¨yqvj dvÛ) wewagvjv, 2001, and conditions imposed by the Commission as regards of the fund; and

d) We shall act to our best for the benefit and interests of the unit holders of the fund.

For Sponsor

Sd/-(Md. Abdul Hamid Miah)Managing Director & CEOIslami Bank Bangladesh Limited

18 PROSPECTUS

DUE DILIGENCE CERTIFICATE BY TRUSTEE

PZy_© Zdwmj-(1) Gi 1(R) [wewa 43(3) `«óe¨]

ChairmanBangladesh Securities and Exchange Commission

Subject: NAM IBBL Islamic Unit Fund.

We, the under-noted trustee to the above-mentioned forthcoming mutual fund, state as follows:

1. We, while act as trustee to the above mentioned fund on behalf of the investors, have examined the draft prospectus and other documents and materials as relevant to our decision; and

2. We warrant that we shall comply with the Bangladesh Securities and Exchange Commission (Mutual Fund) Rules, 2001, Bangladesh Securities and Exchange Commission (Public Issue) Rules, 2015, Dhaka Stock Exchange (Listing) Regulations, 2015, Chittagong Stock Exchange (Listing) Regulations, 2015, Trust Deed of the Fund and the Rules, guidelines, circulars, orders and directions that may be issued by the Bangladesh Securities and Exchange Commission from time to time in this respect.

WE CONFIRM THAT:

a) All information and documents as are relevant to the issue have been received and examined by us and the draft prospectus forwarded to the Commission have been approved by us;

b) We have also collected and examined all other documents relating to the fund;

c) While examining the above documents, we find that all the requirements of the Bangladesh Securities and Exchange Commission (Mutual Fund) Rules, 2001 have been complied with;

d) We shall act as trustee to the issue as mentioned above as per provisions of the trust deed executed with the sponsor and shall assume the duties and responsibilities as described in the trust deed and other constitutive documents;

e) We shall also abide by the Bangladesh Securities and Exchange Commission (Mutual Fund) Rules, 2001 and conditions imposed by the Commission as regards of the fund; and

f) We shall act to our best for the benefit and sole interests of the unit holders of the fund;

For Trustee

Sd/-

Mohammed ShahjahanGeneral Manager, Trustee DivisionInvestment Corporation of Bangladesh (ICB)

19NAM IBBL Islamic Unit Fund

DUE DILIGENCE CERTIFICATE BY CUSTODIAN

PZy_© Zdwmj-(1) Gi 1(R) [wewa 43(3) `«óe¨]

ChairmanBangladesh Securities and Exchange Commission

Subject: NAM IBBL Islamic Unit Fund.

We, the under-noted custodian to the above-mentioned forthcoming mutual fund, state as follows:

1. We, while act as custodian to the above mentioned fund on behalf of the investors, shall comply with the Bangladesh Securities and Exchange Commission (Mutual Fund) Rules, 2001, Depository Act, 1999, Depository Regulation, 2000, Depository (User) Regulation, 2003, Trust Deed of the Fund and the Rules, guidelines, circulars, orders and directions that may be issued by the Bangladesh Securities and Exchange Commission from time to time in this respect.

WE CONFIRM THAT:

a) We will keep all the securities (both listed and unlisted) and Assets of the NAM IBBL Islamic Unit Fund including FDR receipts in safe and separate custody as per wewa 41 of wmwKDwiwUR I G·‡PÄ Kwgkb

(wgDP¨yqvj dvÛ) wewagvjv, 2001, and will provide highest security for the assets of the Fund;

b) We shall act as custodian to the issue as mentioned above as per provisions of the custodian agreement executed with the asset management company and shall assume the duties and responsibilities as described in the trust deed of the mentioned fund and other constitutive documents;

c) We shall also abide by the Bangladesh Securities and Exchange Commission (Mutual Fund) Rules, 2001 and conditions imposed by the Commission as regards of the fund; and

d) we shall act to our best for the benefit and sole interests of the unit holders of the fund;

For Custodian

Sd/-Mohammed ShahjahanGeneral Manager, Custodian DivisionInvestment Corporation of Bangladesh (ICB)

20 PROSPECTUS

DUE DILIGENCE CERTIFICATE BY ASSET MANAGER

PZy_© Zdwmj-(1) Gi 1(R) [wewa 43(3) `ªóe¨]

Chairman Bangladesh Securities and Exchange Commission

Subject: NAM IBBL Islamic Unit Fund.

We, the under-noted Asset Manager to the above mentioned forthcoming mutual fund, state as follows:

1. We, while act as asset manager to the above mentioned mutual fund, declare and certify that the information provided in the prospectus, is complete and true in all respects;

2. We further certify that we shall inform the Bangladesh Securities and Exchange Commission immediately of any change in the information of the fund; and

3. We warrant that we shall comply with the Securities and Exchange Ordinance, 1969, the Bangladesh Securities and Exchange Commission (Mutual Fund) Rules, 2001, Bangladesh Securities and Exchange Commission (Public Issue) Rules, 2015, Dhaka Stock Exchange (Listing) Regulations, 2015, Chittagong Stock Exchange (Listing) Regulations, 2015, and the Rules, guidelines, circulars, orders and directions that may be issued by the Bangladesh Securities and Exchange Commission from time to time in this respect.

WE CONFIRM THAT:

a) The draft prospectus forwarded to the Commission is in conformity with the documents, materials and papers relevant to the fund;

b) All the legal requirements connected with the said fund have been duly complied with; and

c) The disclosures made in the draft prospectus are true, fair and adequate to enable the investors to make a well-informed decision for investment in the proposed fund.

For the Asset Manager

Sd/-

Md. AmanullahChief Executive OfficerNational Asset Management Limited

21NAM IBBL Islamic Unit Fund

CHAPTER 2: BACKGROUND

2.1 Preamble to Formation of NAM IBBL Islamic Unit Fund

Open-end unit fund is a collective investment scheme which can issue and redeem units at any time. An investor will generally purchase units in the fund directly from the fund itself rather than from the existing unit holders. By investing in an open-end unit fund, the investors gain access to a thoroughly researched and professionally managed capital market portfolio, thereby increasing their diversity and reducing the overall risk associated with the capital market investments. Such funds allow the small investor to reap the benefits of a large diversified and professionally managed portfolio.

The NAM IBBL ISLAMIC UNIT FUND will provide an investment alternative for the existing retail investors in Bangladesh. It will also encourage new investors to join in and enjoy the returns of the capital market with minimal risks.

The parties to the fund are, Islami Bank Bangladesh Limited as Sponsor, National Asset Management Ltd. (NAM) as the Asset Manager, Investment Corporation of Bangladesh (ICB) as the Trustee and the Custodian of the Fund.

2.2 Capital Market of Bangladesh

The capital market is the engine of growth for an economy, and performs a critical role in acting as an intermediary between savers and companies seeking additional financing for business expansion. Vibrant capital market is likely to support a robust economy.

Bangladesh capital market where the Dhaka Stock Exchange (DSE) and the Chittagong Stock Exchange (CSE) play a dominant part has multiple roles in a nation’s economy. They provide avenues for investment and capital acquisition and also give an indication of overall economic condition.

At present, the capital market of Bangladesh has gained some positive momentum due to stability in economically and politically. The recent market experience made the government, the Bangladesh Securities and Exchange Commission (BSEC) and the key stakeholders to work on a long-term plan to make the market vibrant by improving mechanisms and coordination among the stakeholders. By introducing many new rules and regulations by BSEC including the demutualization of stock exchanges bring positive changes in the near future. BSEC has also published draft ordinance for launching of Exchange Traded Fund (ETF) which is under process to publish. Besides, Bangladesh Security Exchange Commission takes initiatives for launching country wide Financial Literacy Program to make investors more informative, and to educate investors for the investment in capital market. It is noteworthy that the leading global investment banks, Citi, Goldman Sachs, JP Morgan etc. have all identified Bangladesh as a key investment opportunity.

The economy is set to achieve 7.2 percent growth in FY 2017 and even higher in the coming years. Domestic individuals and institutions as well as Non-Resident Bangladeshis (NRBs) are showing tremendous interest on capital market investment. In 2016, equity market capitalization has changed 8.52 percent and market capitalization to GDP changed 19.63 percent amid a series of bearish trends throughout the year caused by various factors. Healthy corporate declarations by listed companies and optimistic investors pushed the market into positive trends.

Market will see further growth in the near future with the off-loading of shares of State Owned Enterprises (SOEs)and also from telecommunication sector. Therefore, a vibrant and responsive capital market is now of utmost importance to attract more and more domestic and foreign individual and institutional investors. All these signify that Bangladesh Capital market has enormous potential to become one of the leading emerging markets in South Asia. Price Earnings (PE) ratio at the end

22 PROSPECTUS

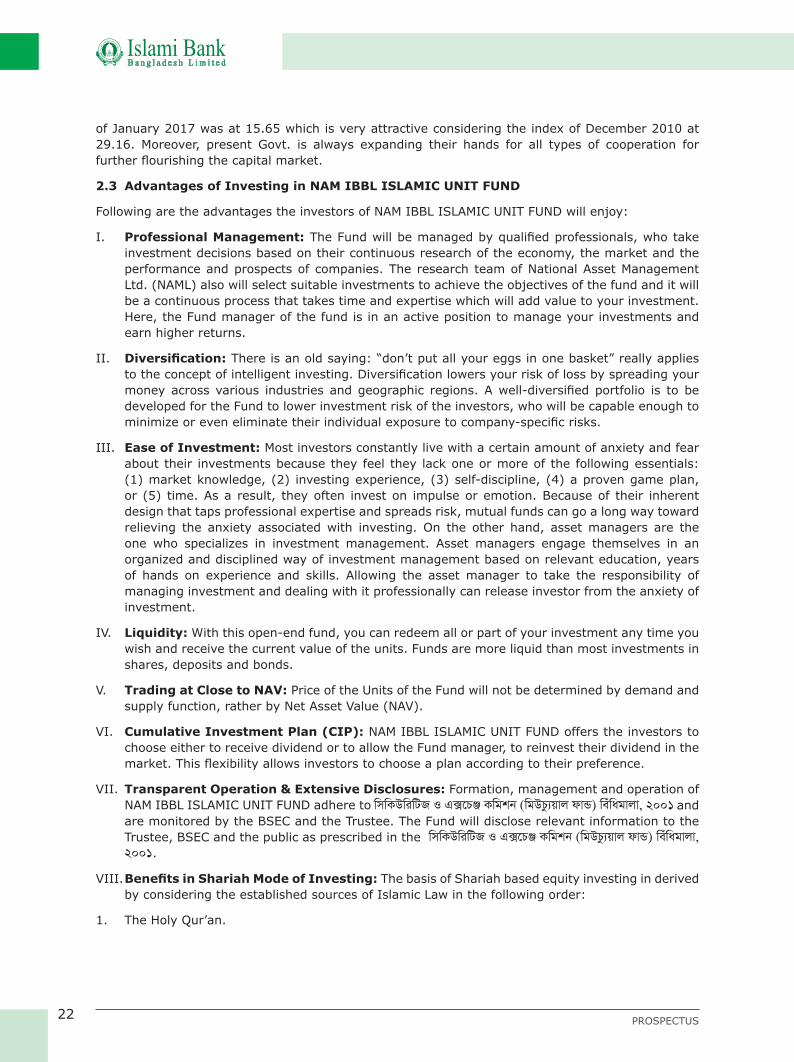

of January 2017 was at 15.65 which is very attractive considering the index of December 2010 at 29.16. Moreover, present Govt. is always expanding their hands for all types of cooperation for further flourishing the capital market.

2.3 Advantages of Investing in NAM IBBL ISLAMIC UNIT FUND

Following are the advantages the investors of NAM IBBL ISLAMIC UNIT FUND will enjoy:

I. Professional Management: The Fund will be managed by qualified professionals, who take investment decisions based on their continuous research of the economy, the market and the performance and prospects of companies. The research team of National Asset Management Ltd. (NAML) also will select suitable investments to achieve the objectives of the fund and it will be a continuous process that takes time and expertise which will add value to your investment. Here, the Fund manager of the fund is in an active position to manage your investments and earn higher returns.

II. Diversification: There is an old saying: “don’t put all your eggs in one basket” really applies to the concept of intelligent investing. Diversification lowers your risk of loss by spreading your money across various industries and geographic regions. A well-diversified portfolio is to be developed for the Fund to lower investment risk of the investors, who will be capable enough to minimize or even eliminate their individual exposure to company-specific risks.

III. Ease of Investment: Most investors constantly live with a certain amount of anxiety and fear about their investments because they feel they lack one or more of the following essentials: (1) market knowledge, (2) investing experience, (3) self-discipline, (4) a proven game plan, or (5) time. As a result, they often invest on impulse or emotion. Because of their inherent design that taps professional expertise and spreads risk, mutual funds can go a long way toward relieving the anxiety associated with investing. On the other hand, asset managers are the one who specializes in investment management. Asset managers engage themselves in an organized and disciplined way of investment management based on relevant education, years of hands on experience and skills. Allowing the asset manager to take the responsibility of managing investment and dealing with it professionally can release investor from the anxiety of investment.

IV. Liquidity: With this open-end fund, you can redeem all or part of your investment any time you wish and receive the current value of the units. Funds are more liquid than most investments in shares, deposits and bonds.

V. Trading at Close to NAV: Price of the Units of the Fund will not be determined by demand and supply function, rather by Net Asset Value (NAV).

VI. Cumulative Investment Plan (CIP): NAM IBBL ISLAMIC UNIT FUND offers the investors to choose either to receive dividend or to allow the Fund manager, to reinvest their dividend in the market. This flexibility allows investors to choose a plan according to their preference.

VII. Transparent Operation & Extensive Disclosures: Formation, management and operation of NAM IBBL ISLAMIC UNIT FUND adhere to

wmwKDwiwUR I G·‡PÄ Kwgkb (wgDPz¨qvj dvÛ) weuwagvjv, 2001 and are monitored by the BSEC and the Trustee. The Fund will disclose relevant information to the Trustee, BSEC and the public as prescribed in the wmwKDwiwUR I G·‡PÄ Kwgkb (wgDPz¨qvj dvÛ) weuwagvjv,

2001.

VIII. Benefits in Shariah Mode of Investing: The basis of Shariah based equity investing in derived by considering the established sources of Islamic Law in the following order:

1. The Holy Qur’an.

23NAM IBBL Islamic Unit Fund

2. The Hadith – the recorded statements and practices of Prophet Muhammad (PBUH).

3. The general consensus of the Islamic Scholars and analogies from the Holy Qur’an and Hadith.

Muslims are prohibited from participating in interest-based transactions, gambling, creating or consuming products made from pork, and more. Just this abbreviated list of prohibitions offers an idea of why Muslims can’t put their money into conventional banks or purchase conventional investment instruments. However, their need for investment remains unmet. This fund will assist them to channelize their funds into Shariah Complaint Securities.

In addition to that, Islamic funds ensure that balance sheets of the companies chosen are in compliance with Shariah rules. When companies pass Shariah rules, they are usually found having strong balance sheet. These companies are better able to protect themselves during economic downturn. Ultimately, the Islamic funds perform better in long run. That is why greater demand for Islamic Funds have been seen during global financial crisis of 2007-08. Islamic investments are based on business contracts that increase transparency and reduce speculation so that all contracting partners know what to expect and what risks are involved. Investors can expect these companies are better governed in the fund.

IX. Tax Advantage of investing in NAM IBBL ISLAMIC UNIT FUND:

1. Tax advantage on Income: Income from a mutual fund or a unit fund up to Tk. 25,000.00 (Twenty-Five Thousand) is exempted from tax under Income Tax Ordinance 1984.

2. Investment Tax credit: According to the current Income Tax Ordinance (ITO) 1984, section 44(2), amended in 2016, amount of allowable investment is – actual investment or 25% of the total (taxable) income or BDT 15,00,00,000.00 whichever is less.

Tax rebate rate is from 15% to 10% as per following schedule:

Total Income Rate of Tax Rebate

From BDT 10,00,001.00 to BDT 30,00,000.00

15% of eligible amount

From BDT 10,00,001.00 to BDT 30,00,000.00

a) BDT 250,000.00 of eligible amount at the rate of 15%

b) Remaining of the eligible amount at 12%

Above BDT 30,00,000.00

a) BDT 250,000.00 of eligible amount at the rate of 15%

b) Next BDT 5,00,000.00 of eligible at the rate of 15%

c) Remaining of the eligible amount at 10%

24 PROSPECTUS

CHAPTER 3: THE FUND

3.1 Formation

The Trust Deed of ‘NAM IBBL Islamic Unit Fund’ was registered on November 13, 2016 under the Trust Act, 1882, and Registration Act, 1908. The fund was registered by BSEC on December 26, 2016 under the wmwKDwiwUR I G·‡PÄ Kwgkb (wgDPz¨qvj dvÛ) weuwagvjv, 2001.

3.2 Life of the Fund

The Fund will be an open-end Shariah based mutual fund, with a perpetual life. Institutional, local and foreign, and individual investors, resident and non-resident, are eligible to invest in this Fund. The initial target size of the Fund will be Tk. 15,00,00,000 (Taka Fifteen crore) only divided into 1,50,00,000 (One crore and fifty lac) Units of Tk. 10 (Taka ten) each. Size of the Fund will be increased from time to time by the Asset Manager subject to approval of the Trustee and with due intimation to the BSEC.

3.3 Face Value and Denomination

Face value of each Unit will be Tk.10 (Taka Ten) only. Initially, unit holders of the Fund shall be issued with a confirmation of unit allocation letter by the Asset Manager at the cost of the Fund in any denomination but not less than 500 (five hundred) units for individuals and 5,000 (five thousand) units for institutions.

3.4 Investment Objective

NAM IBBL Islamic Unit Fund aims at earning superior risk adjusted return by maintaining a diversified portfolio and interest free return to the investor by investing fund only in Shariah compliant instruments in order to provide attractive dividend payments to its unit-holders.

3.5 Investment Policies

a) The Fund shall invest subject to the wewagvjv and only in those securities, deposits and investments approved by Bangladesh Securities and Exchange Commission and/or the Bangladesh Bank and/or the Insurance Development & Regulatory Authority (IDRA) of Bangladesh or any other competent authority in this regard.

b) The Asset Manager of the Fund shall form a Shariah Supervisory Board with two ex-officio members. The Shariah Supervisory Board will be responsible for monitoring the activities and investments of the Fund.

c) The fund shall only invest in any shares and securities that are permissible by the Shariah Law and approved by the Shariah Supervisory Board.

d) Not less than 60% of the total assets of the Fund shall be invested in capital market instruments out of which at least 50% will be invested in listed securities.

e) Not more than 15% of the total asset of the Fund shall be invested in pre-IPOs at one time.

f) All money collected under the Fund shall be invested only in en-cashable/transferable instruments, securities whether in money market or capital market or privately placed pre-IPO equity, preference shares, debentures or securitized debts.

g) The Fund shall get the securities purchased/ transferred in the name of the Fund.

h) Only the Asset Management Company will make the investment decision and place orders for securities to be purchases or sold for the scheme’s portfolio.

25NAM IBBL Islamic Unit Fund

3.6 Investment Restrictions

In making investment decisions, the following restrictions should be taken into due consideration:

a) The Fund shall not invest more than 10% of its total assets in any one particular company.

b) The Fund shall not invest in more than 15% of any company’s paid-up capital.

c) The Fund shall not invest more than 20% of its Assets in shares, debentures or the other securities of a single company or group.

d) The Fund shall not invest more than 25% of its total assets in shares, debentures or other securities in any one industry.

e) The Fund shall not invest in or lend to another Scheme managed by the same Asset Management Company.

f) The Fund shall not acquire any asset out of the Trust property, which involves the assumption of any unlimited liability or shall result in encumbrance of the Trust property in any way.

g) The Asset Management Company on behalf of the Fund shall not give or guarantee term loans for any purpose or take up any activity in contravention of the wewagvjv.

h) The fund shall follow the investment objectives and investment restrictions as per the Rule. However, the AMC shall follow the Shariah guidance suggested by the Shariah Supervisory Board for investment selections within the Rules.

i) The Fund shall buy and sell securities on the basis of deliveries and shall, in all cases of purchases, take delivery of securities and in all cases of sale, deliver the securities on the respective settlement dates as per the custom and practice of the Stock Exchange(s).

j) The Fund shall not involve in option trading or short selling or carry forward transactions.

k) The Fund shall not buy its own unit.

3.7 Valuation Policy

a) For listed securities held in the portfolio of the Fund, the average quoted closing market price at the Stock Exchange(s) on the date of valuation shall be taken into account for calculation of Net Asset Value (NAV) of the Fund or as specified in wewagvjv.

b) For securitized debts, debentures, margin or fixed deposits, held in the portfolio of the Fund, the accrued interest on such instruments on the date of valuation shall be taken into account for calculation of Net Asset Value (NAV) of the Fund.

c) The Fund shall fix the valuation method as specified in the wewagvjv.

d) The Fund shall follow the method approved by the Commission for valuation of the non-traded investments, if any, the Asset Management Company and the Trustee shall at least annually review the non-listed investments, if any, and the Trustee shall at least annually review the value of such investments. The auditors shall comment on such investments in the annual report of the Fund.

e) The valuation of those Listed Securities not traded within previous one month will be made with their reasonable value but shall not be more than the intrinsic value. Such valuation must be approved by the Trustee and commented upon by the Auditors in the Annual Report of the mutual fund but shall not be more than the intrinsic value of the securities.

f) The Valuation of non-listed securities will be made by the Asset Management Company with their reasonable value and approved by the Trustee and commented upon by the Auditors in the Annual report of the Fund.

26 PROSPECTUS

g) Once non-listed securities are valued, the valued amount will be considered for purpose of valuing the Fund’s assets in any interval of time until the securities are further revalued by the Asset Management Company.

h) The Asset Management Company and the Trustee will value the non-listed securities at least once in every three months.

i) In case of deferred expenses, accrued expenses for the period will be taken into account for determining total liabilities.

3.8 Net Asset Value (NAV) Calculation

Following the valuation criterion as set forth above, the Fund will use the following formula to derive NAV per unit:

Total NAV = VA - L T

NAV per unit = Total NAV / No. of units outstanding.

VA = Value of Total Assets of the Fund as on date

L T = Total liabilities of the Fund as on date

VA= Value of all securities in vault + Value of all securities placed in lien + Cash in hand and at bank + Value of all securities receivables + Receivables of proceeds of sale of investments + Dividend receivables, net of tax +Profit receivables, net of tax + Issue expenses net of amortization as on date + Printing, publication and stationery expenses amortized as on date.

L T = Value of all securities payable + Payable against purchase of investments + Payable as brokerage and custodial charges + Payable as Trustee fees + All other payables related to printing, publication and stationery + Accrued deferred expenses with regard to management fee, trustee fee, annual fee, audit fee and safe keeping fee.

3.9 Limitation of Expenses

i. All expenses should be clearly identified and appropriated to the Fund.

ii. The Asset Management Company may charge fund for Investment Management and Advisory fees.

iii. Asset Management Company may amortize the initial issue costs of the Fund over a period as provided for in the wewagvjv; Provided that initial issue expenses/Initial Public Offering (IPO) costs shall not exceed 5% of the collected amount of the Fund raised under the Scheme.

iv. In addition to the fees mentioned herein above the Asset Management Company may charge the Scheme of the Fund with the following recurring expenses, namely;

a) Marketing and selling expenses including commissions of the agents, if any;

b) Brokerage and Transaction costs;

c) Cost of registrar services for transfer of securities sold or redeemed;

d) Trusteeship fees;

e) Custodian fees;

f) Dematerialization fees and others;

g) Shariah Supervisory fee;

h) Re-registration fees, if any.

i) Relevant expenditure for calling meeting by the trustee committee; and

j) Other expenses applicable to the Mutual Fund.

27NAM IBBL Islamic Unit Fund

v. The expenses referred to herein above and any other fees payable or reimbursable to the Asset Management Company or the Trustee shall be charged to the Fund.

3.10 Price Fixation Policy, Sale & Repurchase Procedure

After completion of initial subscription, the Fund will be made open to the investors for regular buy-sale of Units. The date of re-opening shall be declared by the asset manager subject to the consent of the Trustee and with due intimation to the BSEC.

The asset manager shall calculate the Net Asset Value (NAV) per unit on the last working day of every week as per formula prescribed in the wewagvjv and shall disclose sales price and repurchase/ surrender price per unit determined on the basis of NAV before commencement of business operation of the first working day of the following week to the Commission and to the investors through at least one national daily, the website of the asset management company and the authorized selling agents of the Fund. The difference between sales price and repurchase/ surrender price shall primarily be 3 (three) percent of the face value of the Unit which may be changed in future with a maximum limit of 5 (five) percent of the sale price of the Unit. The Asset Manager may reduce the difference with the approval of the Trustee.

3.10.1 Sale and repurchase procedure is given below:

i. The Units of NAM IBBL Islamic Unit Fund, hereinafter referred to as the Fund, may be bought and surrendered through National Asset Management Ltd. and authorized selling agents appointed by NAML from time to time.

ii. Minimum purchase quantity for individual investors is 500 (five hundred) units and for institutional investors is 5,000 (five thousand) units.

iii. Application for purchase of units should be accompanied by an account payee cheque/ pay order/ bank draft in favor of “NAM IBBL Islamic Unit Fund” for the total value of Units.

iv. After clearance / encashment of cheque/ draft/ pay order the applicant will be issued with one unit allocation confirmation against every purchase with a denomination of number of units he / she / the Institutional investor applies for. The units will also be delivered to the Unit holder’s BO A/C.

v. Partial surrender (fraction of total units held under a Unit Allocation Confirmation) is allowed without any additional cost subject to minimum surrender quantity is 500 (five hundred) units both of individuals and institutions. Upon partial surrender, the unit holder will be issued with a new unit allocation confirmation representing the balance of his unit holding.

vi. All payments/ receipts in connection with or arising out of transactions in the units hereby applied for shall be in Bangladeshi Taka.

3.11 Winding up Policy

3.11.1 Procedure of Winding Up

i. If the total number of outstanding unit certificates held by the unit holders after repurchase at any point of time falls below 25% of the actual certificate issued, the Fund will be subject to be wound up.

ii. The Fund may be wound up on the happening of any event, which, in the opinion of the Trustee with approval from the Commission, requires the Scheme to be wound up.

iii. The Scheme may also be wound up if the Commission so directs in the interest of the unit holders.

28 PROSPECTUS

iv. Where a Scheme is to be wound up in pursuance to the above, the Trustee and the Asset Management Company shall give simultaneously separate notice of the circumstances leading to the winding up of the Scheme to the Commission and if winding up is permitted by the Commission, shall publish in two national daily newspapers including a Bangla newspaper having circulation all over Bangladesh.

3.11.2 Manner of Winding Up

i. The Trustee shall call a meeting within 30 days from the notice date of the unit holders of a Scheme to consider and pass necessary resolutions by three-fourth majority of the unit holders present and voting at the meeting for authorizing the Trustee to take steps for winding up of the Scheme. If it fails to have three-fourth majority mandate, the Commission shall have the power to supersede the mandate if situation demands such.

ii. The Trustee shall dispose of the assets of the Scheme of the Fund in the best interest of the unit holders;

Provided that the proceeds of sale made in pursuance of the wewagvjv, shall in the first instance be utilized towards discharge of such liabilities as are properly due under the Scheme and after making appropriate provision for meeting the expenses connected with such winding up, the balance shall be paid to the unit holders in proportion to their respective interest in the assets of the Scheme as on the date when the decision for winding up was taken.

iii. Within thirty days from the completion of the winding up, the Trustee shall forward to the Commission and the unit holders a report on the winding up containing particulars, such as circumstances leading to the winding up, the steps taken for disposal of assets of the Scheme before winding up, expenses of the Fund for winding up, net assets available for distribution to the unit holders and a certificate from the auditors of the Scheme of the Fund.

3.11.3 Effect of Winding Up

On and from the date of the notice of the winding up of the Fund, the Trustee or the Asset Management Company, as the case may be, shall

i. Cease to carry on any business activities of the open-end fund;

ii. Cease to create and cancel unit of the open-end fund;

iii. Cease to issue and redeem units of the open-end fund.

3.12 Investment Management

National Asset Management Ltd shall conduct the day to day management of the fund’s portfolio as the Asset Manager subject to the provisions laid down in the wewagvjv and trust deed and or NAML Shariah Supervisory Guideline or any general directions given by the Trustee, Shariah Supervisory Board and/or the Commission. Moreover, Asset Manager shall have discretionary authority over the Fund’s portfolio about investment decisions. For investment decision, an Investment Committee (IC) shall be formed comprising of the following:

Mr. Md. Amanullah MBA, Chief Executive Officer

Mr. Zakir Hussain Chowdhury, Manager (Investment)

Mr. Masum Alam, Senior Executive (Financial Analyst)

Chief Executive Officer will be heading the IC and have full authority for investment and exit decision within the frame work of wmwKDwiwUR I G·‡PÄ Kwgkb (wgDPz¨qvj dvÛ) wewagvjv, 2001 and parameters set in the investment policies and approved by the Board of Directors of NAML. IC shall review the present

29NAM IBBL Islamic Unit Fund

and future economic condition from the research report and regular updates from the IC and will take investment decision. IC shall deliberate and resolve the following matters in connection with investment:

Developing asset allocation strategy and investment guidelines subject to rules

Short, mid and long tenure investment policies of the fund and amending it from time to time as necessary

Develop and maintain investment guidelines and performance criteria for each investment along with entrustment of each asset class

Determine the Fund’s risk tolerance and investment horizon and communicate such to the working committee (WC) as risk management policies of the fund

Evaluate investment performance

Oversee the working committee

Monitoring fund cash flow, liquidity and overall net asset value (NAV) of the fund

Compare portfolio composition with desired composition and entrust portfolio rebalancing if necessary

Administrative decision including review of fund expenses and accounting control

3.13 Dividend Policy

The accounting year of the Fund shall be 1st July to 30th June every year;

All the unit holders have equal but proportionate right in respect of dividend. Dividend will be paid in Bangladeshi Taka.

The Fund shall distribute minimum 70% or as may be determined by this wewagvjv from time to time, of the annual net income of the Fund as dividend at the end of each accounting period after making provision for Bad and Doubtful Investments. The Fund shall create a Dividend Equalization Reserve by appropriation from the income of the Fund to ensure consistency in dividend payment.

Before declaration of dividend, the Asset Management Company shall make a provision in consultation with the auditors if market value of investments goes below the acquisition cost and the method of calculation of this provision will be incorporated in the notes of accounts.

Surpluses arising simply from the valuation of investments shall not be available for dividend.

Dividend warrants will be dispatched within 45 days from dividend declaration and the AMC shall submit a statement in this respect within next 7 days to the Commission, the Trustee and the Custodian.

Before registration for transfer of ownership, a transferee shall not possess any right to dividend declared.

There shall be a Cumulative Investment Plan (CIP) scheme in this Fund. Under this Scheme a unit holder instead of receiving dividend may re-invest such dividend income accrued for purchasing Unit at a concession rate.

30 PROSPECTUS

CHAPTER 4: THE SHARIAH SUPERVISORY BOARD

4.1 Member of Shariah Supervisory Board

The first Shariah Supervisory Board of the Fund constituted with the following members:

Dr. Hasan Mohammad Moinuddin Chairman

Janab Shah Mohammad Wali Ullah Member

Janab Abdur Raquib Member

Janab Md. Amanullah MBA Member Secretary

However, any change in the Shariah Supervisory Board is subject to compliance of the “Shariah Supervisory Guidance” and intimate it to the Commission.

Dr. Hasan Mohammad Moinuddin is the chairman of National Asset Management Limited’s Shariah Supervisory Board. He is currently working as Assistant Professor at International Islamic University Chittagong (IIUC), Dhaka Campus. He was awarded Doctor of Philosophy degree (Ph.D.) on the topic “Islamic Philosophy” from Ummul Qura University, Holy Makkah, Kingdom of Saudi Arabia in 1998.He has involved in various activities as Islamic researcher, columnist in Jeddah, K.S.A. He was also an Ex-Chairman, Bangladesh Students Association, Ummul Qura University, Makkah from 1994-1997. He is a member of Shariah Supervisory Committee of Islami Bank Bangladesh Limited.

Janab Shah Mohammad Wali Ullah is one of the members of National Asset Management Limited’s Shariah Supervisory Board. He currently holds the position of Pesh Imam & Khatib of Sobhanbagh Masjid & Madrashah Complex in Dhaka. He is a member secretary of Shariah supervisory committee of Social Islami Bank ltd. He has been engaged in many Islamic Institutions of Bangladesh. Besides, He has many writings of Islamic books and research papers on various topics in different newspapers, magazines, journals and memorandum.

Janab Abdur Raquib is another member of National Asset Management Limited’s Shariah Supervisory Board. He was the Professor and Dean of Business Administration and Economics at International University of Business Agriculture & Technology (IUBAT), Dhaka. He is also currently holds the position of Chairman at Social Safety Net Foundation. He has vast working experiences in different financial institutions, pharmaceutical company, NGO. He had been working as Managing Director of Islami Bank Bangladesh Ltd for seven years. He has also worked as Deputy Managing Director, Consultant and Executive Director in The Ibn SIna Pharmaceuticals Industries Ltd, BRAC Bank Ltd. and Bangladesh Bank respectively. He also has membership in different institutions and organization. He participated and contributed numerous papers in international and national seminars and workshop on different Financial Literacy topics. He has also many publications of research papers on various topics in different journals and memorandum.

Janab Md. Amanullah MBA is the member secretary of National Asset Management Limited’s Shariah Supervisory board. Janab Md. Amanullah has over 30 years of banking experience including very senior level working experience with country’s top state owned commercial and development banks. Janab Md. Amanullah was Managing Director of Bangladesh Shilpa Bank (BSB). He was Managing Director (Additional Charge) of Sonali Bank and was Deputy Managing Director and General Manager of the same bank. Janab Md. Amanullah joined Rupali Bank Limited as Senior Officer and

31NAM IBBL Islamic Unit Fund

worked in various capacities and later on assumed the position of Deputy General Manager of the same bank. Janab Md. Amanullah has extensive exposure to Capital Markets, General Banking, Credit Management, Treasury Management, Core Risk Management and Project Finance. He was head of Investment and Business Development Committee of Sonali Bank and was head of Credit Division of Rupali Bank Limited. He was also a nominated Director to the Board of Investment Corporation of Bangladesh (ICB). Janab Md. Amanullah did his MBA from the Institute of Business Administration (IBA), Dhaka University. He had advance training on Economics, Money & Banking from FISK University, Tennessee, USA. He also attended a seminar on Credit Analysis at CITI Corp School of Banking, New York, USA.

4.2 Role and Responsibilities of Shariah Supervisory Board

“Shariah Supervisory Board” means a body of Shariah experts who certifies the securities/assets as Shariah-compliant. A Shariah Supervisory Board performs the following responsibilities:

i. Prepares guidelines and methodologies for selecting/screening of companies/ securities/ instruments to be acceptable as per Shariah principles;

ii. Recommends companies/securities/instruments for investment, consistent with the guidelines and methodologies;

iii. Certifies/approves the criteria of identifying prohibited incomes and recommending distribution of those prohibited income to any charitable organization;

iv. Certifies at the end of each accounting year that all investments and incomes accounted for are Shariah compliant;

v. Any other responsibilities determined by the Commission or specified in the constitutive documents;

32 PROSPECTUS

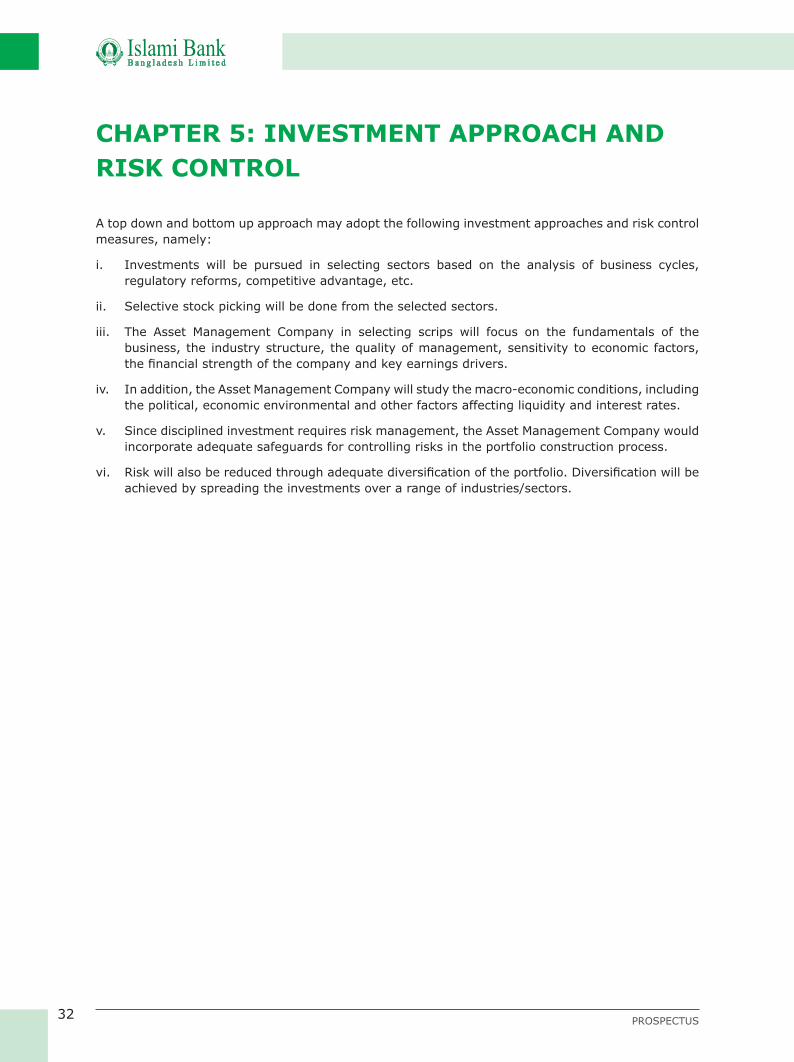

CHAPTER 5: INVESTMENT APPROACH AND RISK CONTROL

A top down and bottom up approach may adopt the following investment approaches and risk control measures, namely: