Page 1

PROTECTING AGAINST RISKS AND MAKING THE

MOST OF OPPORTUNITIES WITHIN THE CUSTOMS

SUPPLY CHAIN

10th Annual Forum on Global Customs Compliance

Brussels – May 27th 2015

Charles Barber – Kuehne + Nagel

Bruno Fransman – Avnet Europe Comm. V.A.

21/05/2015 Page 1

Page 2

Incoterm / Contract - Content / Trade Compliance addressed

Boycott

Sanctions

Restricted Party Screening

Export Control Status

AEO / Supply Chain Security

Classification

Origin

Valuation

FTA

Documentation

Exclusion Clauses

……………….

Strategic: Supply Chain

Scope

Contract

SOP

Liabilities Defined

Destination Work

Gaps – Seller / Buyer

Client - Owner of Trade Compliance

Competent...

Who are we seeing...

Reality

What does Client do

Does it reflect contract

Relationship with Freight Agent / TC Provider

FF/Client – recognition of who does what, where

and why - liabilities owned / assumed

Client value perceptions – is it valued

or simply “hand-holding “

Client / Parties Engaged

What do they want / need

What is their import plan

Has it been shared

Page 3

Client - Owner of Trade Compliance

Competent...

Who are we seeing...

p. 3

Translation

Operations: Supply Chain Can it go – Sanctions / End use / User

Pre-Plan / Inspections / Authorisations / RPS / Boycott

Customs / FTA

Incoterms / Contract

Export Licence

Pre-Advice

Sanctions

Country of Destination

RPS

Document Plan - Customs Clearance, Import Licence, Export

controlled inbound, Docs; originals – who / where

Payment delay – L/C / other

Docs in place / Customs Broker

Challenge / Import Licence

Duty / Taxes / Other Duties

IOR / Tax ID

Delivery

Customs Process

FTA/Pref.

Data Accuracy – Customs Classification, Valuation, Origin, export control status

Factors that Impact your Supply Chain

Page 4

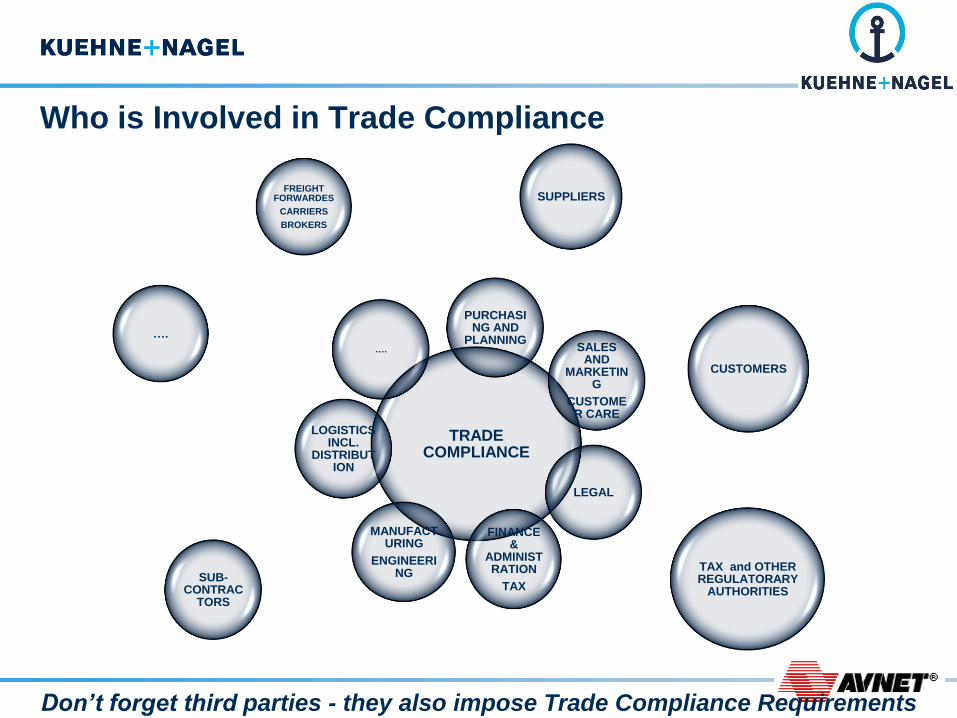

Who is Involved in Trade Compliance

TRADE COMPLIANCE

PURCHASING AND

PLANNING …. SALES

AND MARKETIN

G

CUSTOMER CARE

LEGAL

FINANCE &

ADMINISTRATION

TAX

MANUFACTURING

ENGINEERING

LOGISTICS INCL.

DISTRIBUTION

CUSTOMERS

SUB-CONTRAC

TORS

SUPPLIERS

TAX and OTHER REGULATORARY

AUTHORITIES

….

FREIGHT FORWARDES

CARRIERS

BROKERS

Don’t forget third parties - they also impose Trade Compliance Requirements

Page 5

Risk / Awareness Subject Areas

Main high level risks:

No policies, no support from Sr., Management (Culture)

No clarity of departmental roles and responsibilities

No in-house experience / knowledge

Imposition of trade compliance into existing roles with no training

No cross-functional training/exchange of knowledge

No clear view of the end-to-end supply chain

Not capturing/identifying the risks

Failure to communicate the trade compliance requirement

Not closing corrective actions / seeking improvement

Fear of decision making / “ownership” / accountability

5

Page 6

Risk / Awareness Subject Areas

Trade Compliance Requirements in Functional Roles Functions – All

Incoterms Functions – Engineering, Product Mgrs, Purchasing, Sales, Contracts, Operations, Supply Chain, Logistics, Legal

Value Added Tax (Sales Tax)

Functions – Sales, Sourcing, Finance, Tax, Contracts, Operations, Supply Chain, Logistics, Legal

Import / Export Classification

Functions – Engineering, Product Mgrs, Purchasing, Sales, Contracts, Operations, Supply Chain, Logistics,

Customs Valuation Functions – Purchasing, Contracts, Operations, Supply Chain, Logistics

Country of Origin and Origin Marking for Customs Functions – Engineering, Product Mgrs, Purchasing, Sales, Contracts, Operations, Supply Chain, Logistics,

End-Use & End-User Identification Functions – Purchasing, Sakes, Contracts, Operations, Legal

Restricted Party Screening Functions – Purchasing, Sales, Contracts, Operations, Supply Chain, Logistics, Finance, HR, Legal

Sanctions & Embargoes Functions – All

Restrictive Trade Practices or Boycotts Functions – Purchasing, Sales, Contracts, Operations, Supply Chain, Logistics, Finance, Legal

International Trade Transaction Recordkeeping Functions – Purchasing, Sales, Contracts, Operations, Supply Chain, Logistics, Finance, Legal

6

Page 7

Ex Co., UK

10% Time Spent

10000 Transactions

Risk Score

Duty Spend $256k

No

1

Related Role

Additional

resources

Re Exported 38%

65% Routed

Exp Cont’d

items <1%

32 ERP items

growth per

week

$? K Duty Saved

ERP

IBS

HTS

ECCN

Origin

Export 69%

EU 15%

Domestic 16%

Sales $55,440,772

Import 25%

EU 1%

Domestic 74%

Purchases $23,888,169

Imports

Exports

Restricted Party Screening

Completed / When / Who

End Use / End User

Verified / Contractual Protection

Desk-Level Procedures

Trade Program

Policy, Assessment, Training

GSP imports

Bi-lateral FTA

Import from Export to

Qatar

Actual

84% Potential

60%

Hong Kong

Kuwait

Page 8

Perceptions on Trade Compliance

• Trade compliance is a cost center with no financial benefit to the company, (we are

fee eaters not fee earners)

• Trade compliance slows down our supply chain, (but when something goes wrong it

is always customs)

• Trade compliance is “operational compliance” like completing and stamping docs

• Classification is easy; we only import components they are all “parts of”

• We sell to customers in the EU, no need for export control procedures or ECCNs

• Origin management is easy; we know where our vendors are located

• Our customs brokers/freight forwarders do everything for us, it isn’t our responsibility

• We have an export compliance team, so it is not our responsibility. They will see it

when we ship.

• Our competitors do it; if we don’t we lose sales & anyway I agreed to it in the contract

• We have done this for more then 20 years and never had problems with export

control authorities

• AEO is voluntary, but everything in it is a trade responsibility

• We sell everything Ex-works, so we don’t export and it is not our responsibility Should we be bothered – Maybe we should…

Page 9

Exercise

Break into Groups

Consider your Information

Take your time

And....

9

Page 10

Case 1

One of your sales people contacts you with the following request:

• He has a re-seller who wants to do business in Russia. He needs to be

supplied with highly encrypted security servers which are integrated by your

US contract manufacturer in Europe. The re-seller wants door-to-door delivery.

• And the sales person asks you if he can do the business. What do you do?

21/05/2015 Page 10

Page 11

Case 1 – continued…

After discussing with him you get a detailed overview of the intended flows:

• Your company buys all the components from vendors that are considered to be US

companies, these components are delivered from multiple locations (within and outside

the EU). The ship from locations bill you for the delivery of the components. All

components are directly sent to the Irish branch of your US Contractor where they will be

integrating all components to finished servers and ship it to your Warehouse in Belgium.

The Irish branch will bill you for the integration service.

• The servers are considered to be dual-use items.

• You sell through your re-seller located in Germany. The finished servers are shipped

door-to-door, directly from your warehouse to two different Russian end-customers. The

re-seller wants to have full landed cost services.

• Define all potential risks. Explain why?

• Do you have all facts needed. If not, what more do you need?

• Are there any suggestions that need to be made, if so please make these

21/05/2015 Page 11

Page 12

D2D contracts often have complex trade

situations; potential for errors…

Example – Complex transactions

Contract A Belgian Company sources components that are send to a integrator in

the EU (Ireland)

The integrator sends an invoice for the assembly

The integrator sends the finished product to the WH in Belgium of Company A

Company A sells the finished product to a DE re-seller who sells to a customer In Russia

Company A agrees to do full landed cost service and local tax management, i.e. door to door delivery

Goods are directly exported from the WH to the end-customer in Russia

Servers are highly encrypted

Customers in Russia are National Police in Moscow and a company active in the oil and gas industry

Risks IOR in Ireland

VAT on import in Ireland

Trade data (HTS, origin and ECCN) of components

Trade Data of finished d products

EOR in Belgium

Proof of export out of the EU

IOR in Russia

EU and US (Re-)Export license for export out of Belgium

EU and US sanctions against Russia

Certifications (FSB) needed for integrated systems

IATA lithium battery requirements

Opportunities customs arrangements such as Processing under customs control, IPR ?

Wrong flows & missing data can result in blocked shipments, increased costs, penalties and missed opportunities

Vendors

Non-EU

Vendors

EU

EU

Integrator

Company A

BE

Company A

WH

DE Re-seller Russian

customer

Inv components Inv Goods

Flow components Flow Goods

Inv Integration

Page 13

What could have happened

Example – Complex transactions

Assembly in by Integrator Integrator acts as IOR and pays import duties and import VAT

Integrator issues an invoice for the assembly charging local VAT

Delivery by Company A to end-customers in Russia - Export

Company A acts as exporter of record for customs purposes

Company A applies for the export license as they are the exporter for customs

Goods are exported with Company A’s sales invoice, which is added to the shipment

Company A raises an invoice for the supply of goods to DE exempt as an intra-community shipment

Company A has a global export license for Russia and ships goods under its global export license:

End-customer is National Policy => not Military End-customer is Oil and Gaz industry => HTS does not fall under the prohibited list

No IATA reporting has been done

Delivery by Company A to end-customer in Russia – Import

Company A appoints a broker with IOR services

Goods are imported in the name of the Russian end-customer based on our sales invoice

Due to full landed cost services all costs, customs handling fees, import duties and import VAT are re-charged to Company A

Wrong flows & missing data can result in blocked shipments, increased costs, penalties and missed opportunities

Vendors

Non-EU

Vendors

EU

EU

Integrator

Company A

BE

Company A

WH

DE Re-seller Russian

customer

Inv components Inv Goods

Flow components Flow Goods

Inv Integration

Page 14

How to avoid mistakes & reduce risks

Get full end-to-end picture: Ask questions over and over again

Cut transaction into pieces and Identify who should be involved

Vendors

Non-EU

EU

Integrator

X BE

X BE

WH

Vendors

EU

EU

Integrator

X BE

EU

Integrator

X BE

X BE

WH

X BE

X BE

WH

DE Re-seller Russian

Customers DDP

DDP

Page 15

How to avoid mistakes & reduce risks

When the analysis is finished, risks defined, corrective actions

fixed & a maintenance plan is in place:

Use cases as examples for newsletters

Train, Train and keep Training

Agree on how to work across functions

Create cross functional tailor made procedures & guidelines

Define rules dealing with how to avoid future risks/errors & identify who should

be doing what, owners & accountability

See if IT improvements can help

Follow-up: audit, maintain & continuous improvements

Page 16

Authorized Economic Operator (AEO)

AEO legislation – Voluntary – 2007 / 2008

In simple terms required that:

Traders evidenced compliance with existing EU Customs legislation, and

Across their supply chains...; for security all parties in the supply chain must be secure

Generally through written procedures addressing specific questions

Evidencing compliance with mandatory, existing EU Customs legislation

Customs Assumption – Traders already complying with existing laws

All that is required is to write that down / No more work really...

Raised the standard for demonstrable compliance (and real compliance practice)

Customs auditing / verification is simpler

Union Customs Code (1st May, 2016):

Numerous changes

AEO – Mandatory guarantee requirement for all non AEO traders wishing to use customs

processes such as PCC, IPR, Customs Warehousing, etc.

– Guarantee level for non AEO’s not yet determined...

– AEO – exempt...

HMRC already requesting AEO (c) Standard for applications/renewals

16

Page 17

UCC – Regulation Change

Main Changes in the Union Customs Code (1st May, 2016):

• BTI validity reduced to three years from six

• AEO – Introduction of self assessment procedure; a simplified regime allowing AEO traders to make

import and export entries in their records instead of submitting full declarations

• AEO – Introduction of a centralized clearance system for AEO traders allowing payment of customs

duties in their location irrespective of actual entry point to the EU

Requires sophisticated IT system particularly in respect of VAT and Excise

Implementation 2020...

• AEO – Potential for AEO traders to enjoy lower guarantee levels under the customs debt/duty

deferment scheme requirements (levels subject to UCCIP)

• AEO – Mandatory guarantee requirement for all non AEO traders wishing to use customs processes

such as PCC, IPR, Customs Warehousing

Guarantee level for non AEO’s not yet determined...

AEO – exempt...

HMRC already requesting AEO (c) Standard for renewals....

UCC, will bring further evolution, for example;

• Royalties, will the scope be extended....

• First Sale – currently will not survive...

17

Page 18

Export Compliance

18

Page 19

Company Amount ($) Note

BNP Paris Bas (June 2014) Sanction control 8,800,000,000

Weatherford (FCPA, Export Control , Sanction control) (2014)253,000,000

BAE Systems (2011) 79,000,000

Blackwater (2010) 42,000,000

Balli Group PLC & Balli Aviation Ltd (UK) (2010) 17,000,000 Five-year corporate period of probation

Chitron Electronics, Inc. (2011) 15,500,000 One Manager put in Jail for 3 years

PPG Paints Trading (Shanghai) Co., Ltd (2011) 3,750,000

TW Metals (2011) 575,000 With Prior Disclosure

Trek Lether(2011) 534,000

Applied Tech Inc. CEO (2011) 340,000 100 hrs community service, 2 yr probation

Arvin Meritor (2011) 100,000 With Prior Disclosure

USA Global Trade Related Penalties

19

Page 20

Applicability of export

compliance rules

Who must comply with these regulations:

EU law:

• European entities and individuals

• Foreign entities undertaking activities in/from the EU: e.g., U.S. entity registered in the EU and acting as exporter of record.

• Not really extraterritorial application: except brokering can be and certain restrictions/sanctions/prohibitions

US law (fully extraterritorial):

• U.S. citizens or permanent residents

• U.S. companies/branches

• Foreign subsidiaries

• Dealing in U.S.- origin products/certain foreign-made products

• Owned/controlled by U.S. persons/firms

• Foreign persons dealing in/using “US” products

• U.S. persons “controlling” or “facilitating” transaction

• Any person located in the U.S.

Page 21

Four Basic Questions

What is your item used

for?

End-Use

Restricted and prohibited

end-use Export Control Basics

Who you are

exporting to?

Denied Parties?

Restricted Parties?

What are you

exporting?

Controlled Items?

Where are you

Exporting to?

Embargo

Countries?

Page 22

Export compliance is applicable to:

What am I selling – Products, software or technology:

• Export control does not apply only to goods and services but technology can also be

controlled

What will the Product be used for – Although products are not controlled a

license requirement, restriction, prohibition or embargo can exist depending on

the end-use, destination or party involved in the transaction.

Who is involved? Parties (businesses and individuals): some parties/individuals

are banned; you cannot do business. Nationality of a person can also result in a

restriction/prohibition.

Which countries are involved: some countries are fully banned or do need

special attention (financial sanctions, Arms-embargo, etc.)

Applicability of export

compliance rules

Page 23

Restricted / Denied Party

Screening

23

Page 24

Restricted / Denied Party Screening

Screening is critical to compliance – Denied /Restricted Party Lists change everyday

Legal prohibitions differ for each list

Legal prohibitions apply differently depending on facts of a specific transaction

Remember your company’s reputation and public policy concerns!

24

Page 25

Why Screen

Screening is a risk management

process that prevents a company

from doing business with prohibited

and restricted entities, governments,

companies or persons

25

Page 26

Who to screen – Almost Everyone

Customers, Suppliers, Contractors & Business Partners

Visitors, Contracted Employees, Potential New Employees

End Destination Countries

All parties to the supply chain - Banks, Freight Forwarders, Agents, Distributors, Resellers, etc.

26

Page 27

What do I do with a “Match or Partial Match”?

Resolve false hits

• Using available information, follow your site procedure, with Sr., Management to determine if a true match

• Is listed entity the same entity that we want to do business with?

• If not a match, document as a false hit, and proceed

Real?

• Do not Proceed

• Discuss with Legal

27

Page 28

Sanctions & Embargoes

28

Page 29

What Are Sanctions & Embargoes?

We operate in a Global Political Environment and must recognize that certain

Countries do not consider other Countries as lawful trading partners.

Sanctions and Embargoes are a tool of Foreign Policy; they are fluid and can change

rapidly and are recognized as:

• Legal measures

• Taken by a nation (or group of nations, the United Nations, the European Union, etc.)

• That restrict or prohibit trade and financial transactions with a specified target(s)

• For the purpose of changing the behavior of the target(s)

Targets can be nations, entities, individuals, or a combination of these

Most common prohibitions on direct or indirect transactions are for: • Cuba, Syria, North Sudan, North Korea, Iran, Russia

Depending on the political situation, other countries may be added or removed from this list

• For example; Myanmar…

29

Page 30

What is Facilitation – US persons must not “facilitate” any transaction with

certain sanctioned or embargoed countries

Furthering a Transaction

Approvals to proceed

Discussions about transaction details

Discussions on how a transaction should proceed, or payment

Altering Procedures

Altering operating procedures to

permit a transaction to happen

Referrals

Referring business that we could not take to any other

company or person

30

Page 31

Sanctions – Liability

Whether Directly or Indirectly:

• Prohibits sales of products or services, investment, and all types of transactions with any listed

country, entity, or individual

• Requires diligence during business formation, order entry, shipment, and payment phases of

transactions

• Sales must conduct RPL screening during the marketing phase of a transaction

E.g. Exports, re-exports, and imports of goods or services:

• “Facilitation” of non-U.S. persons’ activities in embargoed countries

• Transactions involving embargoed country assets or property

• Transactions with “specially-designated” persons or entities

• New investment in embargoed country

• Referring prohibited business

• Structuring transactions purposely to avoid export control rules

Knowing and Knowingly

Page 32

Knowing or knowingly – Directly and Indirectly

Supply of software to a Turkish Telecom operator to allow them to provide

cloud computing services to their customers from their HQ in Turkey

The e-mail chain mentioned that they also installed the full telecom network in the

Middle East region including Syria (confirmed by Google search as well)

Page 33

Knowing or knowingly – Directly and Indirectly

Supply of an export controlled chip to a Spanish re-seller:

Re-seller sells to Spanish manufacturer for equipment to be used for “Satellites”

End-use is in China

Page 34

Knowing or knowingly – Directly and Indirectly

Supply of equipment to a French customer:

• The equipment was initially sourced from a US company

• Goods are shipped to Panama

• The Customer’s website states that Cuba is part of their distribution region

Page 35

Export Control Regimes

Australia Group –

www.australiagroup.net

Wassenaar Arrangement –

www.wassenaar.org/

Nuclear Suppliers Group –

www.nuclearsuppliersgroup.org/

Missile Technology Control Regime –

www.mtcr.info/english/index.html

p. 35

Page 36

ECCN – What is it?

Last 3 digits not harmonized – e.g. 500, 600 and 900 US series AND differences between countries/regions due to late implementation of Wassenaar updates =

different ECCN for same products (ERP trade date maintenance)

Page 37

Controlled Technology

What is “technology” and how can it be transferred

“Technology” means specific information necessary for the “development”, “production” or “use” of goods. This

information takes the form of ‘technical data’ or ‘technical assistance’.

NB 1: ‘Technical assistance’ may take forms such as instructions, skills, training, working knowledge and consulting

services and may involve the transfer of ‘technical data’.

NB 2: ‘Technical data’ may take forms such as blueprints, plans, diagrams, models, formulae, tables, engineering

designs and specifications, manuals and instructions written or recorded on other media or devices such as disk, tape,

read-only memories.

When is it subject to control

The export of ‘technology’ which is ‘required’ for the ‘development’, ‘production’ or ‘use’ of goods controlled in

Categories 0 to 9, is controlled according to the provisions of Categories 0 to 9.

‘Technology’ ‘required’ for the ‘development’, ‘production’ or ‘use’ of goods under control remains under control even

when applicable to non-controlled goods.

Controls do not apply to that ‘technology’ which is the minimum necessary for the installation, operation, maintenance

(checking) and repair of those goods which are not controlled or whose export has been authorized.

Controls on ‘technology’ transfer do not apply to information ‘in the public domain’, to ‘basic scientific research’ or to

the minimum necessary information for patent applications.

21/05/2015 Page 37

Page 38

Example – Providing Training

Training can be controlled when it meets the definition of technology

transfer (depends on the content of the training)

Even when training is non-controlled risks can still exist:

Export compliance restrictions can be an issue, e.g. Denied parties,

embargoed customers/countries

Giving training to a Nuclear Plant customer

Page 39

Example – Controlled “Technology”

The Integration centre gets a project to assemble controlled servers for the account

of a customer (contract manufacturing)

The integration centre uses a sub-contractor for installation of the encryption

software, testing of the finished products and review of the assembly process

To that purpose technical specifications (not publicly available) are provided by the

customer and will be provided by the Company to the sub-contractor.

After finishing, the full installation is sent to the customer’s premises where the

servers are integrated within the customer’s system and programming of the

encryption software takes place.

Nationality of integrators, engineers, programmers can be important

Page 40

EU – exporter under export control

Dual-use (goods)

Exporter (article 2): On whose behalf an export declaration is made, that is to say the person

who, at the time when the declaration is accepted, holds the contract with the consignee in the

third country and has the power for determining the sending of the item out of the customs

territory of the Community. If no export contract has been concluded or if the holder of the

contract does not act on its own behalf, the exporter shall mean the person who has the power

for determining the sending of the item out of the customs territory of the Community

Cooperation (article 11.1): If the dual-use items in respect of which an application has been

made for an individual export authorization to a destination not listed in Annex II., a or to any

destination in the case of dual-use items listed in Annex IV are or will be located in one or more

Member States other than the one where the application has been made, that fact shall be

indicated in the application. The competent authorities of the Member State to which the

application for authorization has been made shall immediately consult the competent authorities

of the Member State or States in question and provide the relevant information. The Member

State or States consulted shall make known within 10 working days any objections it or they

may have to the granting of such an authorization, which shall bind the Member State in which

the application has been made.

Exporter of Record for customs ≠ as exporter for export control ≠ as exporter for VAT

Page 41

EU – exporter under export control

Dual-Use:

Where the benefit of a right to dispose of the dual-use item belongs to a

person established outside the Community pursuant to the contract on

which the export is based, the exporter shall be considered to be the

contracting party established in the Community

EU – exporter under export control

Page 42

Software/licenses shipped electronically

Dual-Use:

Which decides to transmit or make available software or technology by

electronic media including by fax, telephone, electronic mail or by any

other electronic means to a destination outside the Community.

Page 43

EU export license – where to apply:

• For all other exports for which an authorization is required under this

Regulation, such authorization shall be granted by the competent

authorities of the Member State where the exporter is established.

Where to Apply

Page 44

OEM

South -

Africa

Company

A BE Vendor EU

PO flow

SO/Invoice flow

Goods flow

PO 1 PO 2

INV 1 INV 2

Shipment 1

Shipment 2

Company

A WH

Dual-Use: Exporter of Record

Page 45

Dual-Use: Exporter of Record

DE re-

seller

Company

A BE Vendor EU

PO flow

SO/Invoice flow

Goods flow

PO 1 PO 3

INV 1 INV 2

Shipment 1

Shipment 2

Company

A WH

OEM

South -

Africa

PO 2

INV 2

Page 46

Dual-Use: Exporter of Record

OEM

South -

Africa

Company

A BE

Vendor

EU

PO flow

SO/Invoice flow

Goods flow

PO 1 PO 2

INV 1 INV 2

Page 47

Dual-Use: Exporter of Record

OEM

South -

Africa

Company

A BE

Vendor

EU

PO flow

SO/Invoice flow

Goods flow

PO 1 PO 2

INV 1 INV 2

UK re-

seller

PO 2

INV 3

Page 48

Boycotts (U.S.)

48

Page 49

• Businesses in, or trading with, these countries or organizations may request

boycott language against Israel

Algeria

Bahrain

Comoros

Djibouti

Egypt

Gulf Coop. Council

Iraq

Jordan

Kuwait

Lebanon

Libya

Mauritania

Morocco

Oman

Palestinian Auth.

Qatar

Saudi

Arabia

Somalia

Sudan *

Syria *

Tunisia

U.A.E.

Yemen

Arab League Boycott of Israel

49

Page 50

Boycott Requests

Must be identified – review instructions, requests, etc., and consider does this need to be here. How does it impact the transaction/Client if removed. Who is the Client – is there any US involvement / why does this make a difference… Can be… Verbal Email Purchase order Letter of credit Contract language Request for proposal, bids, quotes Documentation

Some boycott requests are obvious; some requests may be obscured in the paperwork….

50

Page 51

Boycott Request – Example

Dear --------,

As part of the documentation required for Letter of Credit from the customer, we

are required to furnish a certificate confirming that the goods are neither of Israeli

origin nor do they contain Israel materials. Please confirm that you will be in a

position to issue such a certificate.

Regards,

51

Page 52

Boycott Request – Example

Supplier shall not, and shall prevent its Sub-suppliers from, importing or

using: goods or services from any country with which Saudi Arabia does not

maintain diplomatic relations; goods produced or services provided by any

Persons organized under the laws of any country with which Saudi Arabia

does not maintain diplomatic relations; or goods or services provided by any

Person who is a national or resident of any country with which Saudi Arabia

does not maintain diplomatic relations.

52

Page 53

U.S. Anti-boycott laws

Prevent U.S. citizens and companies from being used by foreign

governments to promote their agenda

Application

Arab League Boycott of Israel

India & Pakistan

Cost of Non-compliance - U.S. export penalties apply

Civil monetary penalties

Criminal penalties for knowing or willful violations

Sanctions (e.g. denial export privileges)

U.S. Anti-boycott Laws

53

Page 54

How do you control internal and external risk…

You need to gain control of:

The end to end supply chain, and

The planning and engagement stage

They (internal and external parties) are all Clients…

Summary

21/05/2015 Page 54

Page 55

Compliance = Protecting

against Risks

Trade Compliance” Risks Violations

• Consider an Authority perspective of some risks.

• Company “failure” to:

• Know the customer and end use(r) of product

• Know the ship from, ship to and end-destination of the products

• Comply with limitations and provisions

• Have the necessary knowledge (in-house)

• Properly classify products for export/import

• Conduct Restricted Party Screening

• Have process in place to avoid violations

• Work across departments

• Just a few examples…

• Is it just an Authority that should see risk in this way…

Page 56

• Feet from sourcing and

sales walk us to new places

all the time

Who we all should become

• Head from a lawyer

• Body from ISC team

• Work hand in hand with Sourcing, Security, HR, Finance, legal, tax, CP/S, warehousing, supply chain, engineering, etc

• A heart that we have defined for ourselves

• Multilingual

This is valid for all functions: Be a specialist become a generalist

Page 57

What is my position

within the Organization

• Describe Trade Compliance Activity:

• Have clear Policy on Trade Compliance

• Define clearly what is in-scope and what is out of scope for your function

• Examine activities being performed by trade resources to determine what is in

scope/out of scope

• Set expectations around support needed from and for Trade functions

• Understand how you impact others and how others impact you

• Understand key objectives of your Organization and other Departments

• Develop metrics for understanding whether objectives are met and use them for

internal marketing

• Calibrate resourcing to those objectives

• Determine best location for resources to be placed to accomplish those objectives

57

Page 58

Example – What we might not do

Responsibility Content Who

Product requirements conformity declaration/attestation, hazardous materials, REACH,

ROHS, WEEE, product qualification requirements (e.g. CE labeling,

radio frequency, voltage restrictions), consumer protection

requirements, etc

Part creation team

Intrastat VAT reporting of movements within the EU Finance/transportatio

n

Coding of

transport/broker

invoices

Allocation the proper cost centre to the transport/broker invoices.

Review of customs handling fees

Finance

Document retention:

archiving

Keep complete set of import and/or export records (invoice, customs

declaration, transport document, preferential certificates of origin

Finance/Partly Trade

Compliance

Foreign Corruption FCPA/Anti-Bribery Legal Council

Invoicing Creating correct invoices Customer Care

Sales and Purchase

orders

Entering, changing and maintaining all data elements of a PO/SO, e.g.

ship to, sold to, built to, etc.

Page 59

Sales and Trade Compliance

Communication and Integrated Processes Are Key to Success

Sales Activity Requirement Trade Impact

New customer set-up • Communication of export and documentation requirements

• Review any trade data compliance clauses in sales contract

• Review any terms of delivery clauses in sales contract

• Screen against Denied Party Lists

• Transport mode

• Red flags

•Customer type, e.g. re-seller, governmental, military, etc

• Duty consequences

• Preferential origin impact

• Admissibility issues

• Clearance cycle time

• Correct application of import of record in

country of destination

• Incoterms

• Export Control

New sales contract • Communication of export and documentation requirements

• Review any trade data compliance clauses in sales contract, e.g.

export control responsibilities

• Review any terms of delivery clauses in sales contract

• Duty consequences

• Preferential origin impact

• Admissibility issues, Export Control

• Clearance cycle time

• Correct application of exporter and importer

of record

• Incoterms

• Set of export documents

Drop shipments sales • Communication to trade compliance on drop shipment mode

• Review by trade Compliance to ensure adherence to export and

import regulations

• Export Control, e.g. who is responsible to apply for export license

• Duty consequences

• Trade impact: document requirements

• Correct application of exporter and importer

of record and correct set off documents to be

used for import and export

• Export Control

Complex transactions • Communicate to trade compliance team of any complex

transactions/contract: multiple parties involved, multiple locations

involved with sub-assembly and further assembly, sensitive

countries, etc

•Duty consequences

• Trade impact: document requirements

• Correct application of exporter and importer

of record and correct set off documents to be

used for import and export

• Tax registration impact

Page 60

Finance and Trade Compliance

Communication and Integrated Processes Are Key to Success

Finance Activity Requirement Trade Impact

Transfer Pricing • Review transfer pricing set-up for intercompany sales

• Review transfer pricing set-up for free of charge shipments

• Duty consequences

• Valuation risk exposure: correct customs

value declared at import

Royalty and license

contracts

• Communicate any existing or new Royalty and license contract

•Review any new Royalty and license contract with trade

compliance team

• Duty consequences

• Valuation risk exposure: potentially to be

added to the customs value of imported

goods

Assists: free of charge

or at a reduced price

• Communicate any assist provided to the manufacturer (tools,

drawings, know how, tools, moulds, etc) free of charge or at a

reduced price

• Review with Trade compliance team on potential inclusion in the

customs value of imported goods

• Duty consequences

• Valuation risk exposure: potentially to be

added to the customs value of imported

goods

Any other, such as

R&D, sales

commissions, works

of art, proceeds, cost

for testing, etc

• Communicate any similar cost items that do related to goods

being imported

• Review with Trade compliance team on potential inclusion in the

customs value of imported goods

•Duty consequences

• Valuation risk exposure: potentially to be

added to the customs value of imported

goods

Incoterms, drop

shipments, complex

transactions

• Review complex transactions with agreed incoterms, who is

doing what in the transaction chain

• Correct application of VAT exemptions

• Risk of VAT registration

Page 61

A Clear Trade Compliance Program

• Define Service Offerings:

• Trade Knowledge Centre

• Legal advice, training, procedures, guidelines, complex transactions, contract

reviews, etc.

• Risk avoidance, Continuous Improvements, Cost savings & Increased sales

• Self-assessment, internal operational audits

• Customs Broker Management

• AEO-certification

• Duty Minimization Program

• Export Control Compliance Program

• Internal Marketing

• Management Reporting = Metrics Reporting

• Volumes and values

• Duty spend and duty saved

• Sales realized under duty program

• Sales realized under Export Control Compliance

Page 62

Conclusion

Trade Compliance is not a stand alone organization, but is cross

functional:

• Everyone impacts trade compliance

• Trade compliance impacts all other functions

Trade Compliance is complex and errors can easily be made

Trade compliance offers more than “just” importing and exporting goods

• Protects the Company against any potential liability

• Helps to reduce costs, makes savings and facilitates trade in some markets

Page 63

And Consider…

When a mistake happens (however that happens)

Can you demonstrate it is only a mistake

Within a demonstrable process flow that demonstrates due

diligence for compliance

If not, expect the Authorities to examine at a detail level

because the mistake may simply be one of many.

Perfection is not a requirement

Demonstrable due diligence is…

p. 63

Page 64

Any Questions

We’ll always try to support the business need but

often the answer requires additional input from others

Page 66

Incoterms

Means international commercial terms

For international contracts for the sale of goods

ICC standard (current version 2010)

Can be varied by contract

Internationally recognised terms

66

Page 67

Incoterms

Traditionally considered as Four Groups

E = Departure

F = Main Carriage Unpaid

C = Main Carriage Paid

D = Arrival

67

Page 68

Incoterms EX Works

Ex - Works – (…named place…)

Seller places the goods at buyers disposal at the named place of delivery,

not loaded and not cleared for export. Risk of loss/damage passes to

buyer at delivery. Buyer must arrange loading, collection, export licenses,

export customs and documentation, freight, destination customs

clearance, import licenses, final delivery and payment of any customs

duties and taxes. Can be used for all modes of transport

Ex-works can be used for any mode of transport

Recommendation: to be used for domestic sales only

Same risk for: FCA WH and self-collect

68

Take Care when trading on this term

Page 69

Incoterms FCA

FCA – Free Carrier (... named place)

Seller delivers goods, cleared for export, to buyer’s carrier at the named

place. Delivery is completed when goods are loaded onto carrier's means

of transport, if named place is seller's premises, otherwise when goods

are placed at carrier's disposal on seller's means of transport not

unloaded. Risk of loss/damage passes to buyer at delivery. Can be used

for all modes of transport.

FCA can be used for any mode of transport

69

Page 70

Incoterms FOB [& FCA]

FOB – Free On Board ( ... named port of shipment)

Seller delivers, and risk of loss/damage passes to buyer, when goods

pass ship's rail at named port of shipment. Seller clears goods for

export. Only used for sea or inland waterway transport

FOB should only be used for

Sea and Inland Waterway Transport

70

Page 71

Incoterms – CIF & CIP

CIF – Cost, Insurance & Freight (…named port of destination)

Seller delivers, and risk of loss/damage passes to buyer, when goods pass ship's

rail at named port of shipment. Seller clears goods for export and must arrange

contract of carriage and insurance to named port of destination. Only used for sea

or inland waterway transport.

CIP – Cost & Insurance Paid to (…named place of destination)

Seller delivers goods to seller’s carrier, clears goods for export and must arrange

contract of carriage and insurance to named place of destination. Risk of

loss/damage passes to buyer at delivery. Can be used for all modes of transport.

CIP can be used for any mode of transport

71

Page 72

Incoterms – DAP

DAP – Delivered At Place (…named place of destination)

Seller delivers goods to buyer at named place of destination not

cleared for import and not unloaded. Risk of loss/damage passes to

buyer at delivery. Buyer must arrange customs clearance and payment

of any customs duties and taxes. Can be used for all modes of

transport.

DAP can be used for any mode of transport

72

Page 73

Incoterms – DDP

DDP – Delivered Duty Paid (…named place of destination)

Seller delivers goods to buyer at named place of destination

cleared for import and not unloaded. Risk of loss/damage passes

to buyer at delivery. Seller must arrange customs clearance and

payment of any customs duties and taxes. Can be used for all

modes of transport. Should not be used where the seller cannot

obtain an import license.

Take care when trading on this term

73

Page 74

Comparison between purchase on FCA & DDP

Do you know what it really costs

74

Purchasing FCA or DDP?

Unit Cost

• FCA (Origin) $100.00

• Sales Taxes 5% $ 5.00

• Freight Costs 10% $ 10.00

• Insurance 1% $ 1.00

• Duty 5% $ 5.80

• Tax 20% $ 24.36

• Total $146.16 DDP Unit

Page 75

Incoterms 2010 –

EXW (FCA WH or self-collect), and

DDP in sales

Examples follow

Page 76

EXW: Ex works:

Seller must make the goods available at Seller’s premises. Risk of loss transfers at Seller’s premises.

Page 77

EXW: Ex-Works

Seller Pro’s:

Only responsible to have goods packaged, ready for transport at seller’s

named facility;

Not responsible for loading/pre-carriage/export clearance in origin country;

Can be used for small package international courier shipments or

domestic small package shipments.

Page 78

EXW: Ex-Works

Seller Con’s:

No control over goods’ destination:

goods could be diverted to domestic markets;

Invoices can be swapped / replaced – this conflicts with -

• Exportation needs to be done based on documentation provided by the seller (invoices,

delivery note)

No control over the export clearance:

Inability to retrieve key documentation for duty drawback claims in origin country;

Inability to retrieve key documentation for proof of export, needed for exempted VAT sale

• No receipt of validated and certified export message out of the electronic customs system

High Risk for export of controlled goods

Seller’s responsibility: export based on Seller’s export authorization/license

Specific export control mentions need to be added on the export declaration (prepared by buyer)

Could be caught in risky “no-man’s land” – buyer in over his head, asks for

assistance in loading/pre-carriage/export clearance despite Incoterms.

• High risk of wrong export clearance, export documentation prepared wrongly by the buyer

Page 79

EXW: Ex-Works

Buyer Pro’s:

Complete visibility and control over shipment from outset to make

booking/loading changes as needed.

Ability to receive necessary shipment pre-alert information for security and

customs clearance activity;

Assurance that all links in supply chain are secure;

Access to documentation needed for Drawback claim in destination

country;

Mandates cooperation from Seller to ensure documentary/customs

compliance.

Page 80

EXW: Ex-Works

Buyer Con’s:

Shipper not even responsible to load conveyance for transport – could

lead to messy claims issues;

Buyer responsible for pre-carriage and export clearance in unfamiliar

country;

VAT or other domestic tax exemption – importer has shipment

documentation but does not have representation in origin country to

provide proof of export to supplier: VAT can be re-charged by supplier to

customer.

Bottom Line: EXW generally not recommended by Incoterms

Committee for international transactions

Intention during Incoterms 2010 negotiations: only to accept EXW for

quotation discussions.

Page 81

EXW - cases

BE Company selling to French customer and French customer selling to Indian end-customer

Goods need to be shipped from Belgium to India. French customer MUST organize transport

from Belgium to India. In case Indian customer organizes the transport first sale will be a local

sale (with EXW we do not control this)

>

VAT exempt

Customer responsible for export operations. However

Export Customs declaration needs to be completed in name of BE Company. Issue with EXW is

that we do not control that goods will properly be exported by our customer. If we do not get the

proof of export we face VAT that will have to be paid and is non-recoverable.

Export license (depending on the country):

• Customer in its capacity of exporter under Dual-Use (Entity that holds the contract with the first

entity outside the EU);

BE Company Customer

FR EXW

Indian end- Customer

CIP

Page 82

EXW - cases

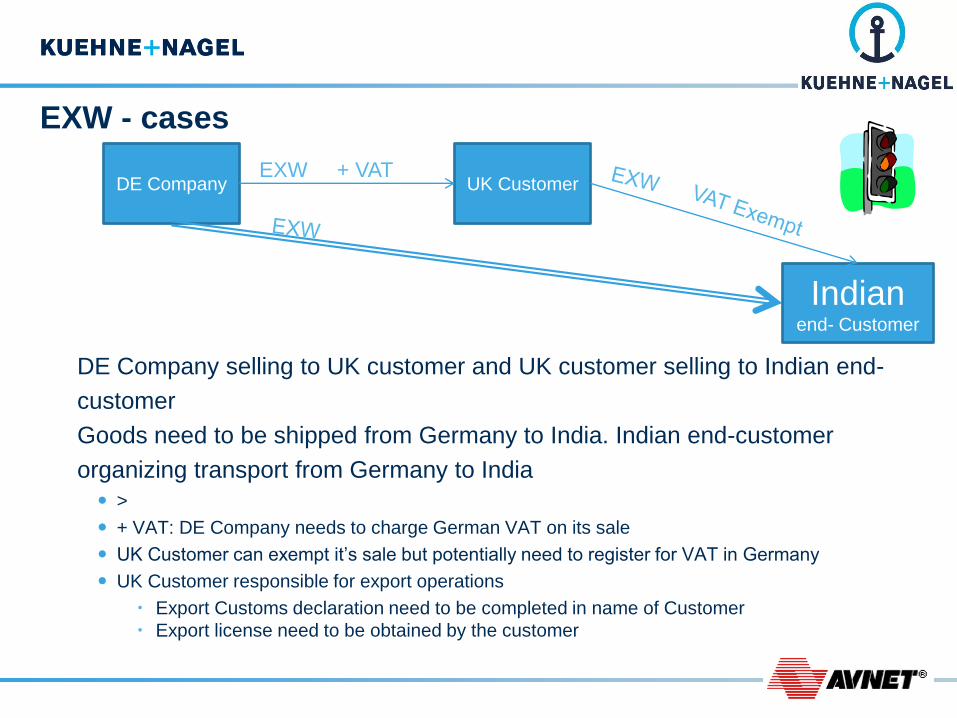

DE Company selling to UK customer and UK customer selling to Indian end-

customer

Goods need to be shipped from Germany to India. Indian end-customer

organizing transport from Germany to India

>

+ VAT: DE Company needs to charge German VAT on its sale

UK Customer can exempt it’s sale but potentially need to register for VAT in Germany

UK Customer responsible for export operations

Export Customs declaration need to be completed in name of Customer

Export license need to be obtained by the customer

DE Company UK Customer + VAT

Indian end- Customer

EXW

Page 83

DDP – Delivered Duty Paid Seller Pro’s:

Creates freight “critical mass” for ideal carriage contracts

Controls destination of freight for export compliance;

Maintains export documentation for Duty Drawback/VAT exemption;

May be used in domestic trade and in cases where Seller has strong,

established presence in destination country (to be used with caution);

Legal entity of seller must often be ”tax”, “VAT” and “Customs” registered in

country of import

Mandates cooperation from Buyer to ensure documentary/customs

compliance.

Page 84

DDP – Delivered Duty Paid (cont.)

Seller Con’s:

Responsible for cargo delivery and customs clearance in unfamiliar

country;

Seller might be responsible to register for tax purposes

Seller might be performing local sales after import (tax impact)

Many countries do not allow non-resident to be Importer of Record or

where possible may result in additional legal requirements

Can result in compulsory tax registration, e.g. for VAT

Can result in compulsory recognition as importer for customs purposes

Can result in setting up a legal entity in order to be able to act as importer;

Seller could be required to obtain import licenses in country of destination

May be responsible for meeting advanced security filing rules

Probability for confusion in responsibilities at destination is extremely high;

May cause payment delays if terms are somehow tied to Incoterms rules.

Page 85

DDP – Delivered Duty Paid (cont.) Buyer Pro’s:

Acceptable for small importers with no “critical mass” freight contracts;

Seller responsible for export clearance/license requirements;

May delay payment to Seller if somehow tied to Incoterms;

May be used in conjunction with “Vendor Managed Inventory” projects to

delay inventory liability for tax purposes;

Mandates cooperation from Seller to ensure documentary/customs

compliance.

Page 86

DDP – Delivered Duty Paid (cont.)

Buyer Con’s:

No visibility to freight for ISF/import customs compliance purposes;

Lose “critical mass” for ideal freight contracts;

Will need to obtain international freight/insurance costs for countries with

CIF-based declared value requirements;

No access to documentation for Duty Drawback claim in destination

country;

Seller often in over his head in destination country, requiring intervention

by Buyer.

Often applied wrongly: seller need to clear for import, however in practice

buyer performs import clearance: tax risk

Buyer is buying after import is performed in country of destination

(potential tax impact)

Bottom Line: Similar to EXW, this INCOTERMS rule is not recommended for

international transactions

Page 87

DE Company selling to UK customer and UK customer selling to Japanese end-customer

DE Company delivers from its WH in Germany To the end-customer in Japan

Goods need to be shipped to Japan. DE Company organizing transport from Germany to Japan

>

+ VAT exempt

DE Company responsible for export operations

Export Customs declaration need to be completed in name of DE Company

Export license

• UK Customer in its capacity of contracting party with customer outside the EU

DE Company responsible for import clearance in Japan

Potentially mandatory registration for TAX/VAT and customs purposes

Potentially responsible for any import license or other obligations

Potentially need to raise a local VAT sales invoice after import subject to Japanese VAT

UK Customer « buying » after import done by DE Company in Japan

Potentially facing tax risks as well

DE Company UK Customer + VAT exempt

Japanese end-

Customer

DDP

Page 88

Contact Details

Charles Barber

Director - Trade Compliance

Advisory Services

Kuehne + Nagel Ltd

Mob: + 44 (0) 7815 709546

[email protected]

Bruno Fransman

Regional Director

Global Trade Compliance Assurance

Avnet Europe Comm., VA

[email protected]

Office: +32 2 709 93 15

Mob: +32 470 927 106

www.avnet.com

21/05/2015 Page 88