34

Protecting Your Portfolio From Inflation Keith Black, PhD, CFA, CAIA Showcase your Knowledge @CAIA_Keith Black @CAIAAssociation

Protecting Your Portfolio From

Inflation Keith Black, PhD, CFA, CAIA

Showcase your Knowledge @CAIA_Keith Black @CAIAAssociation

Inflation and Commodities– 2

About CAIA Association

The Global Leader in Alternative Investment Education

Non-profit established in 2002, based in Amherst, MA, with offices in Hong

Kong and London

Over 8,000 current charter holders in more than 80 countries

Over 24 vibrant chapters located in financial centers around the world

More than 120 educational and networking events each year

Offers AI education through the CAIA designation and the Fundamentals

of Alternatives certificate program

Inflation and Commodities– 3

Alternative Investment Education

Alternatives currently represent over $12 trillion in assets under management

and assets in liquid alternatives continue to rise.

The CAIA Association Mission:

Establish the CAIA designation as the benchmark for alternative

investment education worldwide

Promote professional development through continuing education,

innovative research and thought leadership

Advocate high standards of professional ethics

Connect industry professionals globally

Inflation and Commodities– 4

The CAIA Charter Designation

Globally recognized credential for professionals managing, analyzing,

distributing, or regulating alternative investments.

Highest standard of achievement in alternative investment education.

Comprehensive program comprised of a two-tier exam process:

Level I assesses understanding of various alternative asset classes

and knowledge of the tools and techniques used to evaluate the

risk-return attributes of each one.

Level II assesses application of the knowledge and analytics

learned in Level I within a portfolio management context.

Both levels include segments on ethics and professional

conduct.

Inflation and Commodities– 5

Fundamentals of Alternative Investments

The Fundamentals of Alternative Investments Certificate Program is a course

that provides a foundation of core concepts in alternative investments.

Fills a critical education gap for those who need to understand the evolving

landscape of alternative investments.

Online, 20-hour, self-paced course

Earns CE hours for the CIMA®, CIMC®, CPWA®, CFP® designations

Understand the core concepts in alternative investments

Gain confidence in discussing and positioning alternatives

Inflation and Commodities– 6

CAIA Curriculum

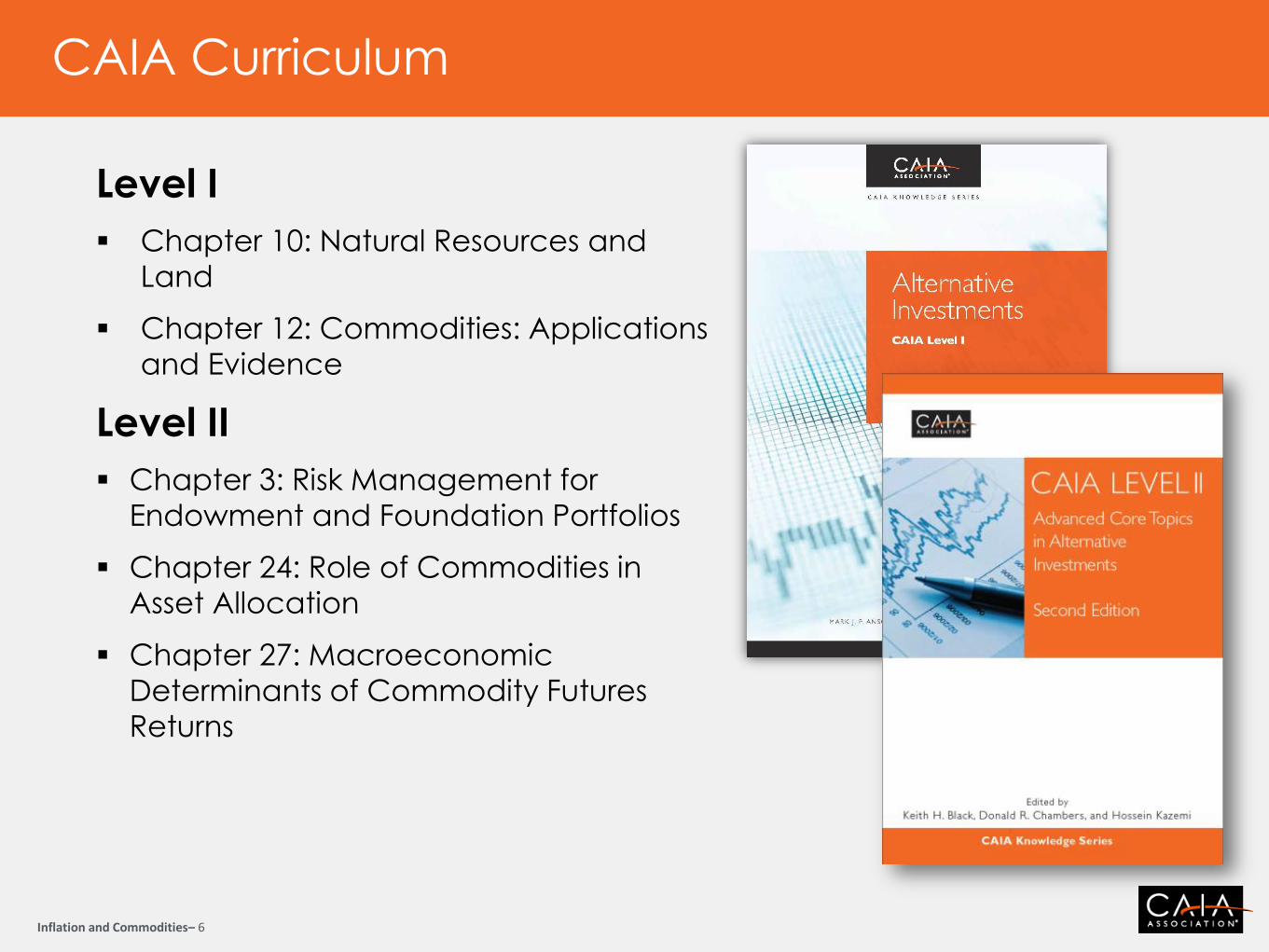

Level I

Chapter 10: Natural Resources and

Land

Chapter 12: Commodities: Applications

and Evidence

Level II

Chapter 3: Risk Management for

Endowment and Foundation Portfolios

Chapter 24: Role of Commodities in

Asset Allocation

Chapter 27: Macroeconomic

Determinants of Commodity Futures

Returns

Inflation and Commodities– 7

Why Hedge Inflation?

Most investors think in terms of nominal returns, especially in

the fixed income markets

However, rising inflation makes it more difficult to meet

terminal wealth goals in nominal terms

Investors with a greater need for inflation protection will

choose larger allocations to real assets

Endowments and foundations who seek to maintain

real spending while preserving the real value of the

endowment

Pensions who offer cost-of-living (COLA) adjustments

to their retirees

Corporations or individuals with fixed incomes, but

expenses that grow with inflation

Inflation and Commodities– 8

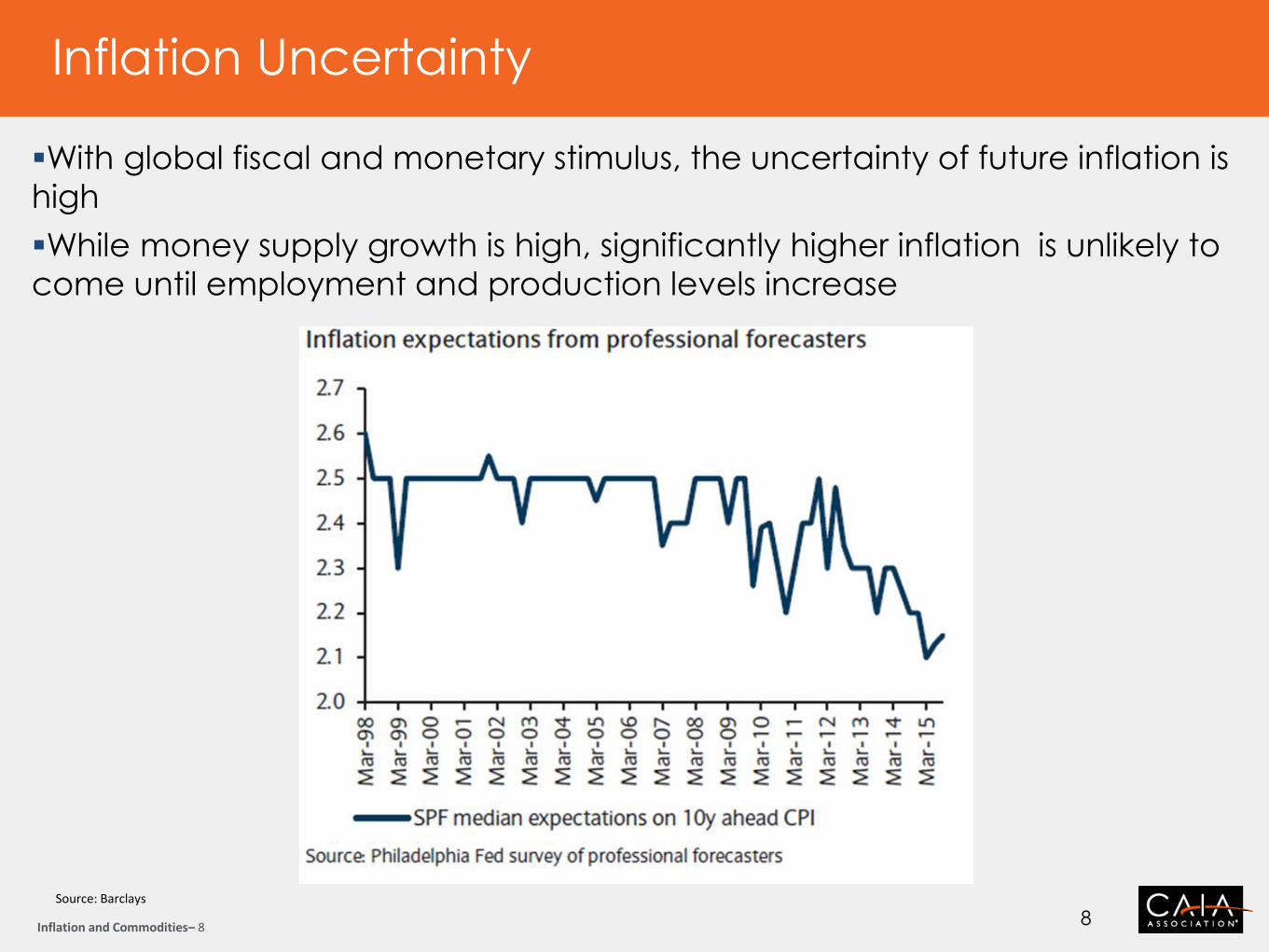

Inflation Uncertainty

With global fiscal and monetary stimulus, the uncertainty of future inflation is

high

While money supply growth is high, significantly higher inflation is unlikely to

come until employment and production levels increase

8 Source: Barclays

Inflation and Commodities– 9

Hedging Inflation

USCPI, 2015

Housing

33.2%

Medical and

Education

11.6%

Food and Energy

20.8%

Other Goods and

Services

34.4%

US Consumer Price Index, January 2016

Inflation and Commodities– 10

Inflation Betas

Where can institutional investors turn to hedge their inflation risk?

Studies have found that a few assets can hedge inflation risk (positive inflation beta), while the majority of institutional assets have a risk to rising inflation (negative inflation beta)

Within equities, smaller cap stocks and less capital intensive sectors have even greater inflation risk

In practice, many institutions build a real assets allocation, investing 5% to 20% of the portfolio in timberland, farmland, linkers and commodity futures

Assets with superior inflation protection may have lower risk-adjusted returns

20 Year US Treasuries

S&P 500 3 Month T-bills

10 Year TIPS

Farmland Commodity Futures

-3.1 -2.4 0.3 0.8 1.7 6.5

Bernstein Global Wealth Mgmt, “Deflating Inflation: Redefining the Inflation-Resistant Portfolio”, 2010

Inflation and Commodities– 11

Inflation-Linked Bonds

Sovereign debt issues offer a real yield with

an inflation-adjusted principal value

10 year US TIPS offer a real yield of

less than 0.4%

Break-even yield implies 1.55% future inflation, down from

2.5% last year

Bernstein estimates an inflation

beta of 0.8

Holding non-USD issues can hedge the

declining value of the dollar, but are more

sensitive to local country inflation

$2.3 trillion issued worldwide

Approximately 30% in US, 40% in UK

and Eurozone

30% in Canada, Australia, Japan,

Sweden, Iceland, Emerging Markets

Bernstein Global Wealth Management, “Deflating Inflation: Redefining the Inflation-Resistant Portfolio”, 2010 Barclays, “The Global Inflation-Linked Monthly Reflation and the Front End”, November 2015 11

Inflation and Commodities– 12

Equities

Equities have high long-term returns, but suffer in the short run from higher

interest rates during times of inflation

Firms in the natural resource, energy and real estate sectors have greater

inflation protection than broad equity indices

Energy and metals stocks have an inflation beta of 2, REITs of -2, and

S&P 500 of -2.4

Smaller stocks and less capital intensive stocks get hurt the most by rising

inflation

Rising Inflation Leaders to Higher Earnings… … but a Higher Discount Rate Hurts Valuations

Bernstein Global Wealth Mgmt, “Deflating Inflation: Redefining the Inflation-Resistant Portfolio”, 2010

Inflation and Commodities– 13

Real Estate and REITs

Real estate investments are a hybrid between fixed income

and equity securities, with inflation hedging potential

depending on property income and debt structure

Long-term leases are similar to fixed income instruments,

as fixed rate leases suffer from higher discount rates

Property equity can act like stocks, rising with long-term

inflation

Inflation and Commodities– 14

Timberland

Like real estate, the land value can be negatively affected by

inflation

Like commodities, timber values are positively affected by

inflation

Can be correlated to economic activity, especially housing

starts

Interesting real options characteristics, where waiting to

harvest during times of low prices can lead to another year of

biological growth

Martin, “The Long-Horizon Benefits of Traditional and New Real Assets in the Institutional Portfolio”, Journal of Alternative Investments, 2010

Inflation and Commodities– 15

Farmland

Unlike infrastructure or real estate, the supply of farmland is

fixed or shrinking despite growing demand for food

Returns may be leveraged to growth in population and

income in emerging markets

Commodity-based rents benefit from short-term inflation

Bernstein estimates an inflation beta of 1.7

Permanent crops, such as orchards or citrus, have different

characteristics than row crops

Row crops, such as corn or wheat, have annual option to

switch to a more profitable crop

Bernstein Global Wealth Mgmt, “Deflating Inflation: Redefining the Inflation-Resistant Portfolio”, 2010

Inflation and Commodities– 16

Infrastructure and MLPs

Toll roads, pipelines, ports and utilities can benefit from

inflation when user fees increase at a greater rate than

expenses

Infrastructure is a hybrid asset class, having characteristics

of fixed income, real estate and private equity

Many infrastructure assets have low price elasticity of

demand, making the cash flows somewhat recession

proof

Some contracts to operate regulated assets include

inflation escalation clauses

Investment opportunities may be large due to growing

energy demand, governmental budget deficits and

needs for infrastructure growth and rehabilitation

Inflation and Commodities– 17

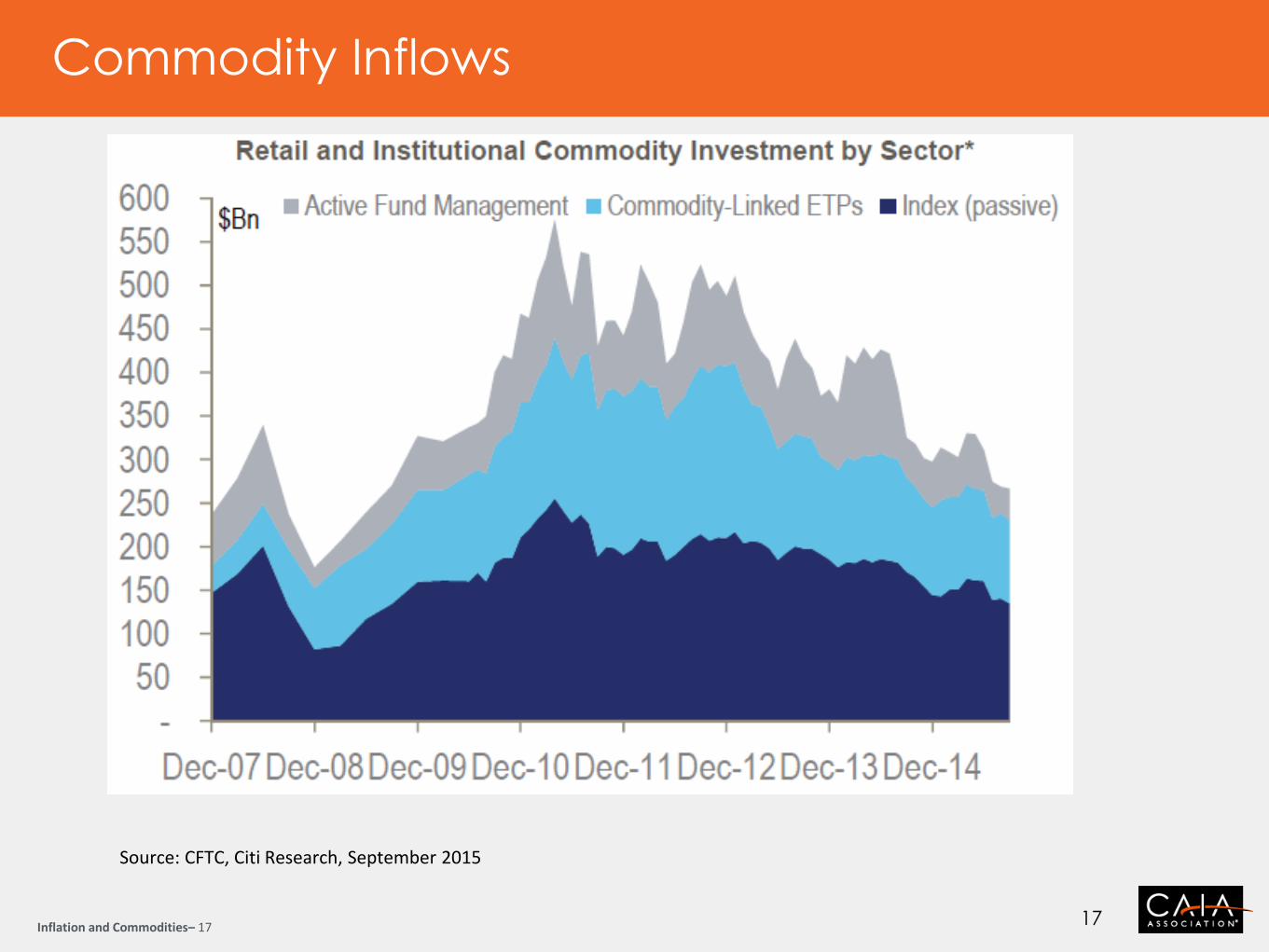

Commodity Inflows

17

Source: CFTC, Citi Research, September 2015

Inflation and Commodities– 18

Commodity Futures Indices

Energy

63%

Industrial

Metals

9%

Precious

Metals

3%

Grains,

Meats, Softs

24%

S&P GSCI Commodity Index, 2016 Weights

Energy

31%

Industrial

Metals

17%

Precious

Metals

16%

Grains,

Meats, Softs

36%

Bloomberg Commodity Index, 2016 Target Weights

S&P GSCI, 2016 Bloomberg, 2016

Inflation and Commodities– 19

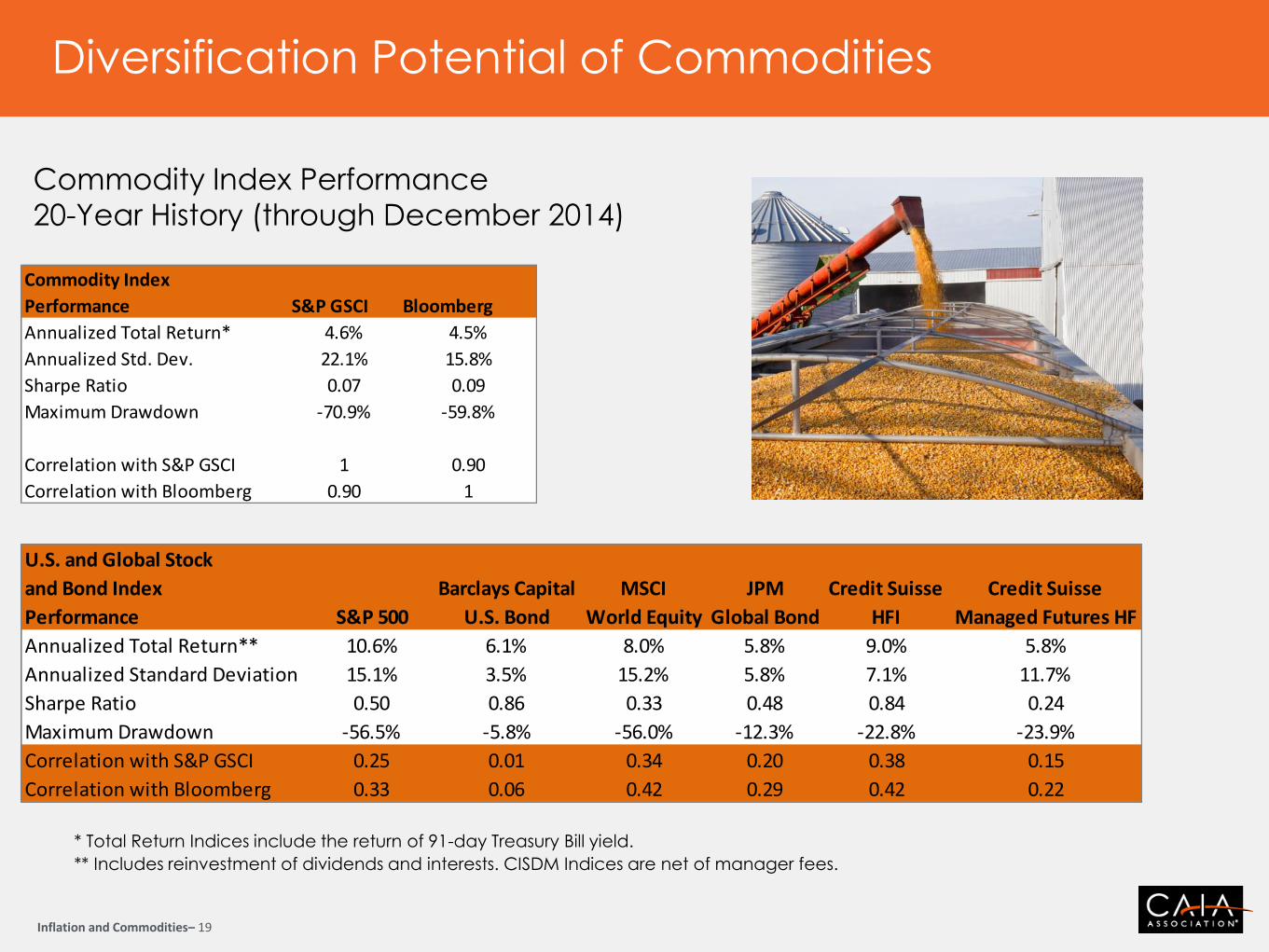

Diversification Potential of Commodities

* Total Return Indices include the return of 91-day Treasury Bill yield.

** Includes reinvestment of dividends and interests. CISDM Indices are net of manager fees.

Commodity Index Performance

20-Year History (through December 2014)

Commodity Index

Performance S&P GSCI Bloomberg

Annualized Total Return* 4.6% 4.5%

Annualized Std. Dev. 22.1% 15.8%

Sharpe Ratio 0.07 0.09

Maximum Drawdown -70.9% -59.8%

Correlation with S&P GSCI 1 0.90

Correlation with Bloomberg 0.90 1

U.S. and Global Stock

and Bond Index Barclays Capital MSCI JPM Credit Suisse Credit Suisse

Performance S&P 500 U.S. Bond World Equity Global Bond HFI Managed Futures HF

Annualized Total Return** 10.6% 6.1% 8.0% 5.8% 9.0% 5.8%

Annualized Standard Deviation 15.1% 3.5% 15.2% 5.8% 7.1% 11.7%

Sharpe Ratio 0.50 0.86 0.33 0.48 0.84 0.24

Maximum Drawdown -56.5% -5.8% -56.0% -12.3% -22.8% -23.9%

Correlation with S&P GSCI 0.25 0.01 0.34 0.20 0.38 0.15

Correlation with Bloomberg 0.33 0.06 0.42 0.29 0.42 0.22

Inflation and Commodities– 20

Attractive Correlation Characteristics

Commodity futures returns have attractive correlation

characteristics over long time periods

Gorton/Rouwenhorst, “Facts and Fantasies about Commodity Futures Ten Years Later”, 2015

Stocks Bonds Inflation

1 Year 0.04 -0.25 0.24

5 Years -0.26 -0.25 0.47

Inflation and Commodities– 21

Trends in Correlation

Bhardwaj/Gorton/Rouwenhorst, “Facts and Fantasies about Commodity Futures Ten Years Later”, 2015

Inflation and Commodities– 22

Commodity Stocks vs. Futures

Source: Wall Street Journal, August 2015

Inflation and Commodities– 23

Hedging Inflation

-0.50

-0.40

-0.30

-0.20

-0.10

0.00

0.10

0.20

0.30

0.40

0.50

0.60

Jan

-94

Jun

-94

No

v-9

4

Ap

r-9

5

Sep

-95

Feb

-96

Jul-

96

De

c-9

6

May

-97

Oct

-97

Mar

-98

Au

g-9

8

Jan

-99

Jun

-99

No

v-9

9

Ap

r-0

0

Sep

-00

Feb

-01

Jul-

01

De

c-0

1

May

-02

Oct

-02

Mar

-03

Au

g-0

3

Jan

-04

Jun

-04

No

v-0

4

Ap

r-0

5

Sep

-05

Feb

-06

Jul-

06

De

c-0

6

May

-07

Oct

-07

Mar

-08

Au

g-0

8

Jan

-09

Jun

-09

No

v-0

9

Ap

r-1

0

Sep

-10

Feb

-11

Jul-

11

De

c-1

1

May

-12

Oct

-12

Mar

-13

Au

g-1

3

Jan

-14

Jun

-14

No

v-1

4

36 Month Rolling Correlation to Inflation Stocks vs. Commodities

S&P 500, CPI Bloomberg Commodity Index , CPI

S&P 500, Bloomberg, 2014

Inflation and Commodities– 24

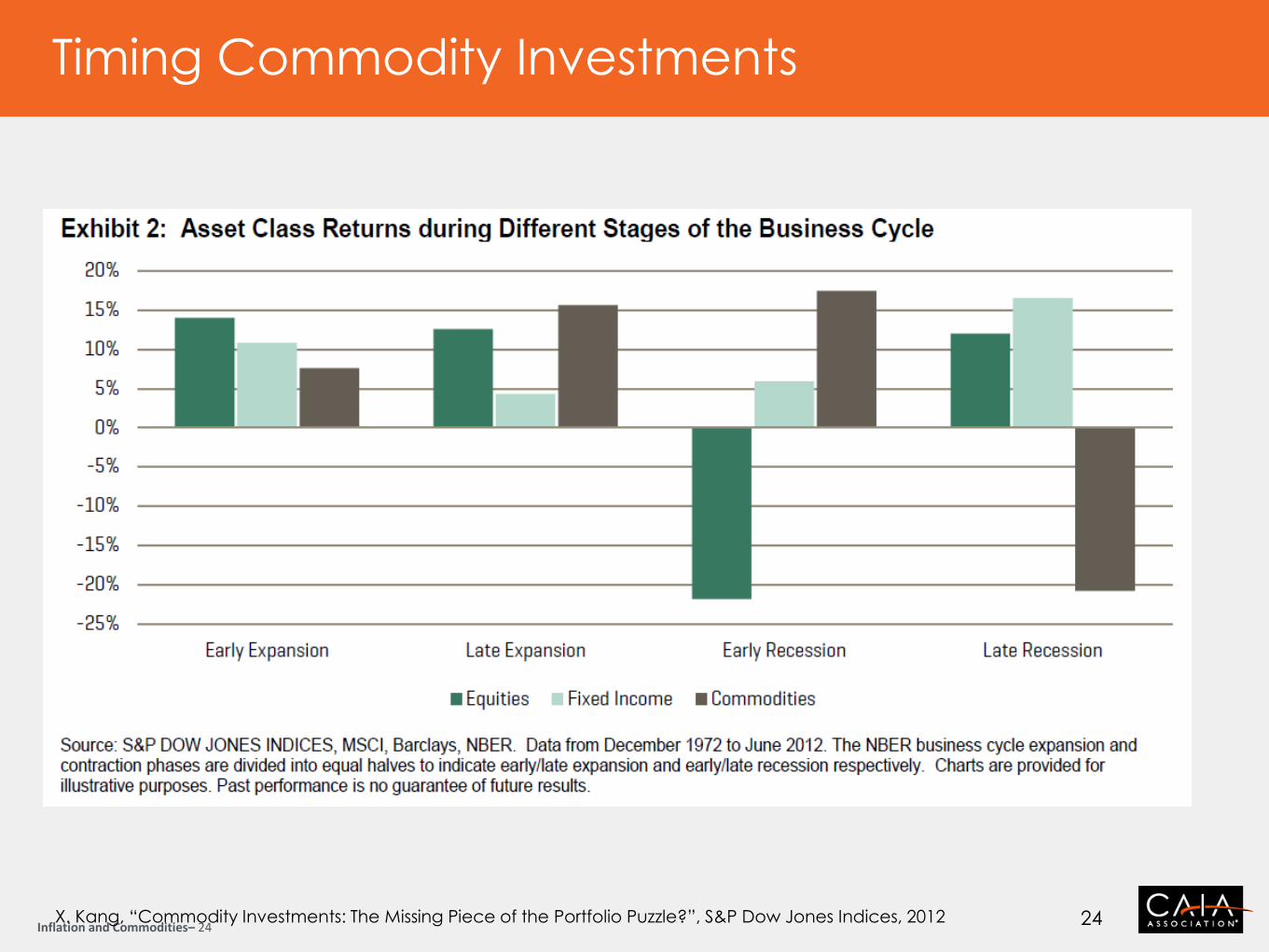

Timing Commodity Investments

X. Kang, “Commodity Investments: The Missing Piece of the Portfolio Puzzle?”, S&P Dow Jones Indices, 2012 24

Inflation and Commodities– 25

Supply Constraints

Commodities with supply constraints can have higher volatility and greater

upside potential

Energy and Industrial Metals (Volatility of 32% and 21%)

These commodities have the greatest supply constraints, as production is

subject to location, mining/drilling, refining and environmental issues

Agriculture (Volatility of 18%)

Supply shortages tend to be short lived, as next year’s growing/breeding

season may overcome this year’s shortages

Precious Metals (Volatility of 16%)

Supply has little impact, as metals are held for centuries as a store of value

and little is consumed

Inflation and Commodities– 26

The Role of Emerging Markets

The prices of many commodities are tied to the demand from Asian

emerging markets

India and China are rapidly gentrifying nations with over 2.5 billion of the

world’s 6.8 billion citizens

This consumption relative to world demand is falling. Consumption of

cement, steel, aluminum, coal and copper grew by over 10% annually

from 2006 to 2011, but growth has slowed in recent years

Chinese Commodity Consumption as a Portion of World Demand

Cement2 Soybeans1 Coal3 Copper1 Iron Ore1 Aluminum4

55% 66% 50% 44% 66% 45%

1) Wall Street Journal, 2013 2) Societe Generale, 2010 3) Energy Trends Inside, 2012 4) Morgan Stanley, 2012

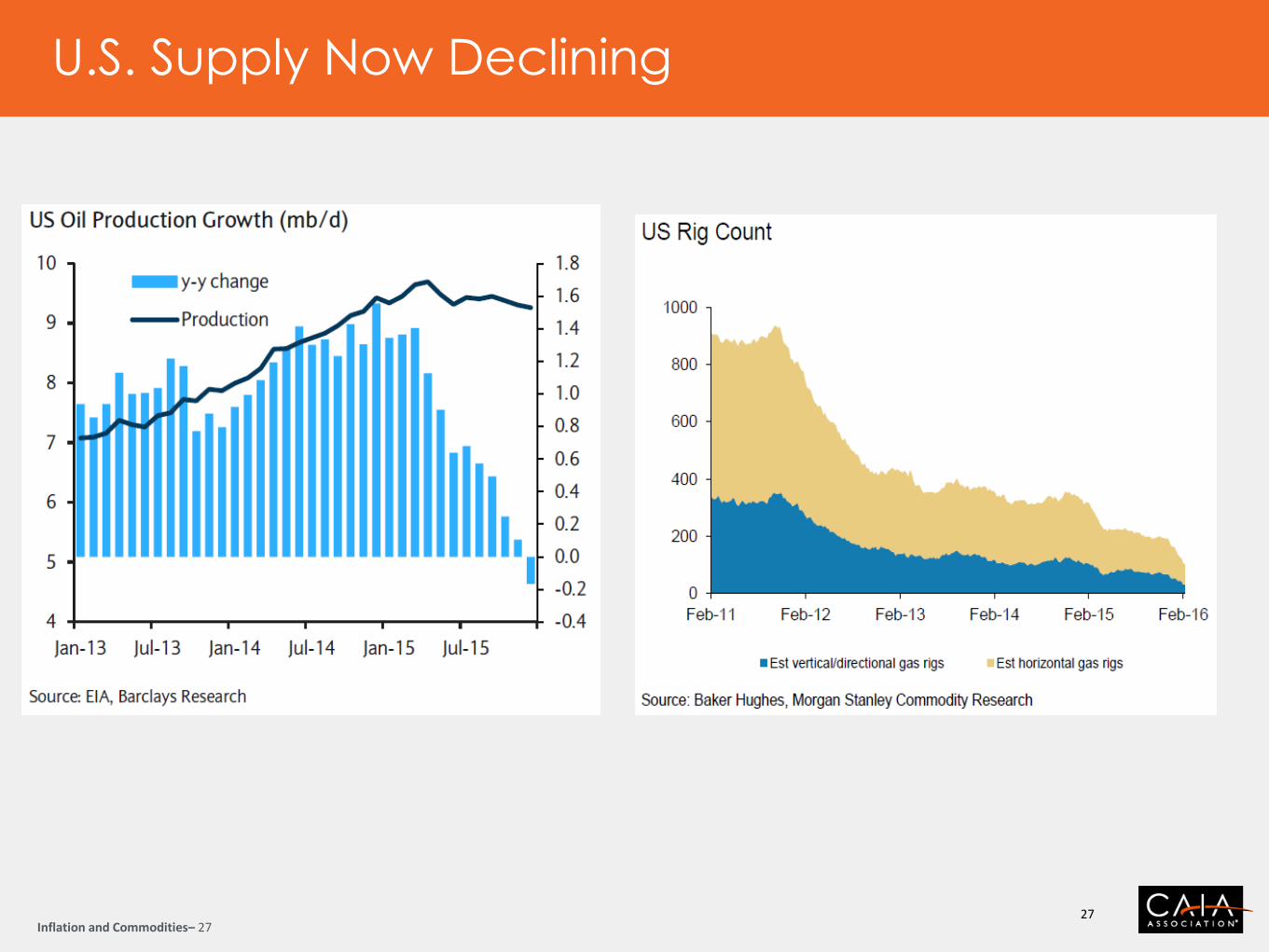

Inflation and Commodities– 27

U.S. Supply Now Declining

27

Inflation and Commodities– 28

But OPEC Supply Increasing

28

Inflation and Commodities– 29

Inventories are Still High

29

Inflation and Commodities– 30

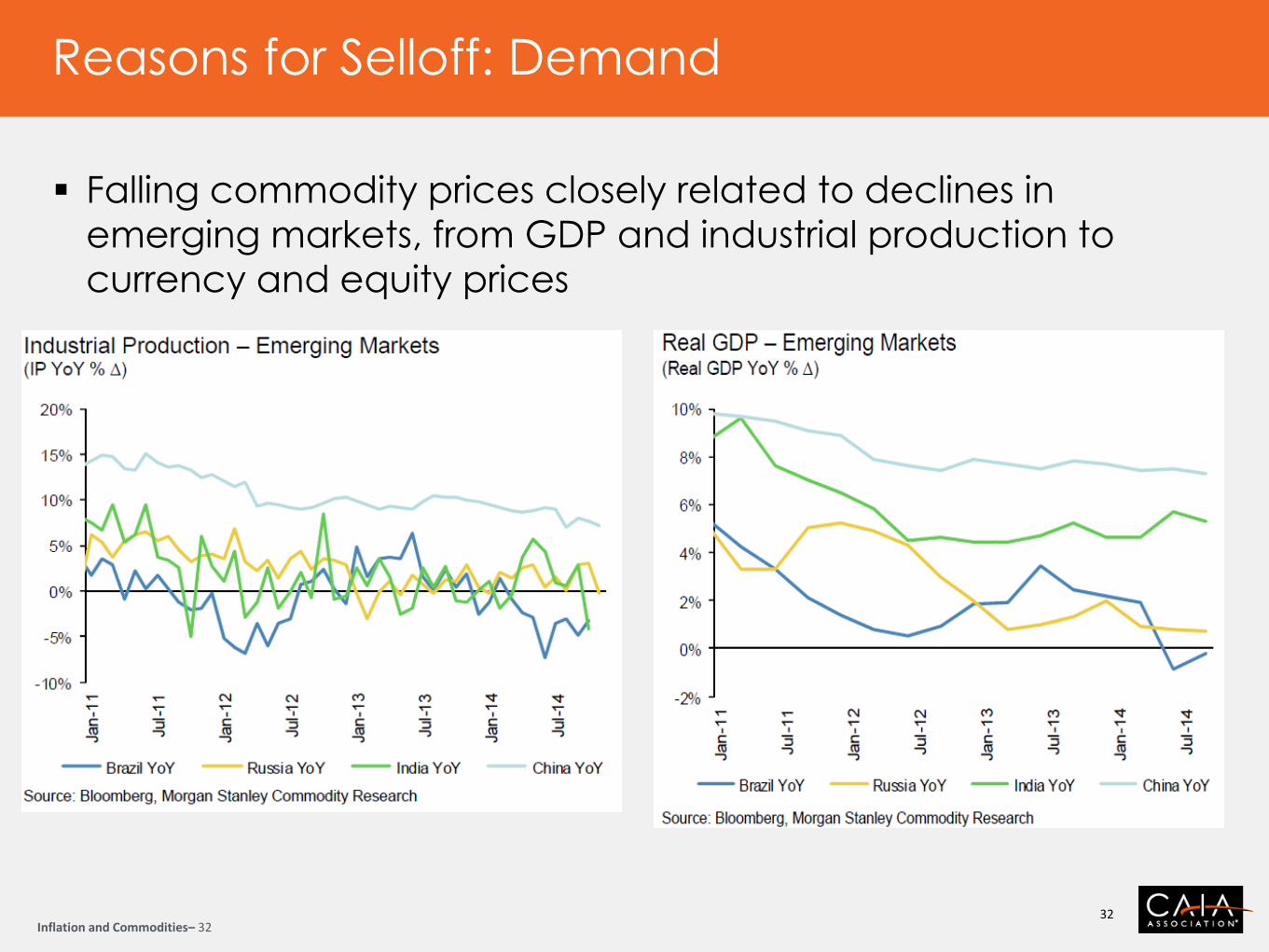

Reasons for Selloff: Demand

30

Inflation and Commodities– 31

Supply Outpacing Demand

31

Inflation and Commodities– 32

Reasons for Selloff: Demand

32

Falling commodity prices closely related to declines in

emerging markets, from GDP and industrial production to

currency and equity prices

Inflation and Commodities– 33

Reasons for Selloff? USD Strength

33

USD commodity prices falling much faster than when purchased using weak Euro or emerging market currencies Weak EM currencies encourage local producers to increase exports

Inflation and Commodities– 34

CAIA Curriculum

Level I

Chapter 10: Natural Resources and

Land

Chapter 12: Commodities: Applications

and Evidence

Level II

Chapter 3: Risk Management for

Endowment and Foundation Portfolios

Chapter 24: Role of Commodities in

Asset Allocation

Chapter 27: Macroeconomic

Determinants of Commodity Futures

Returns