CRUMB RUBBER PROCESSING IN THE TWENTY -FIRST CENTURY Presented by Terry A. Gray TAG Resource Recovery at the Third Southeast Regional Scrap Tire Management Conference Atlanta, Georgia October 31, 2000 PERSPECTIVE Crumb rubber has been produced for over thirty years, but producing it from whole scrap tires is still a young and rapidly evolving business. Until less than ten years ago, virtually all crumb rubber was made from buffing dust by simple size reduction and contaminant separation. Buffing dust is waste rubber removed during tire tread leveling prior to retreading. Since each separate tire section is composed of different elastomers designed to enhance specific performance requirements, crumb rubber produced from tread buffing dust is normally more uniform chemically than crumb rubber from whole tires and does not contain white specs from sidewalls. Therefore, it provides the comparison standard in some traditional markets. Today, ninety North American producers and marketers of crumb rubber are listed in the 2000 Scrap Tire and Rubber Users Directory, seventeen of them in Canada. Many of these companies use simple processes to convert buffings or factory wastes into crumb or recycled rubber products. At least thirty-five of these companies claim to use whole or shredded tires as"their raw material, including eleven within Canada. Some of these U.S. facilities were constructed in anticipation of dramatic market growth from U.S. federal ISTEA (Intermodal Surface Transportation Efficiency Act of 1991) legislation that mandated use of crumb rubber in increasing percentages of federally-funded asphalt roadway construction. Implementation of this legislation was repeatedly postponed, then totally rescinded. Other facilities have been e'ncouraged by loans and grants from states and provinces intended to show support for recycling objectives. Unrealistic market projections from equipment vendors have contributed to some facilities. As a result, on a total North American basis, there is significant excess production capacity, and established product markets are extremely price competitive. Many current participants are not profitable, and continuing business failures are probable. 1

Transcript

CRUMB RUBBER PROCESSING IN THE TWENTY -FIRST CENTURY

Presented byTerry A. Gray

TAG Resource Recovery

at theThird Southeast Regional Scrap Tire Management Conference

Atlanta, GeorgiaOctober 31, 2000

PERSPECTIVE

Crumb rubber has been produced for over thirty years, but producing it fromwhole scrap tires is still a young and rapidly evolving business. Until less than tenyears ago, virtually all crumb rubber was made from buffing dust by simple sizereduction and contaminant separation. Buffing dust is waste rubber removed duringtire tread leveling prior to retreading. Since each separate tire section is composed ofdifferent elastomers designed to enhance specific performance requirements, crumbrubber produced from tread buffing dust is normally more uniform chemically thancrumb rubber from whole tires and does not contain white specs from sidewalls.Therefore, it provides the comparison standard in some traditional markets.

Today, ninety North American producers and marketers of crumb rubber arelisted in the 2000 Scrap Tire and Rubber Users Directory, seventeen of them inCanada. Many of these companies use simple processes to convert buffings orfactory wastes into crumb or recycled rubber products. At least thirty-five of thesecompanies claim to use whole or shredded tires as"their raw material, including elevenwithin Canada.

Some of these U.S. facilities were constructed in anticipation of dramaticmarket growth from U.S. federal ISTEA (Intermodal Surface Transportation EfficiencyAct of 1991) legislation that mandated use of crumb rubber in increasing percentagesof federally-funded asphalt roadway construction. Implementation of this legislationwas repeatedly postponed, then totally rescinded. Other facilities have beene'ncouraged by loans and grants from states and provinces intended to show supportfor recycling objectives. Unrealistic market projections from equipment vendors havecontributed to some facilities. As a result, on a total North American basis, there is

significant excess production capacity, and established product markets are extremelyprice competitive. Many current participants are not profitable, and continuingbusiness failures are probable.

1

The purpose of this brief historical perspective is simply to recognize that thebusiness parameters and equipment utilized in scrap tire processing are undergoing anevolution as companies experience the realities of operations and marketing. As aresult, the objective of this discussion is simply to raise some questions and hopefullyprovide some guidance on both technical and business considerations associated withparticipation in this challenging industry.

REALITY VERSUS PERCEPTION

Crumb rubber production is a good story, starting with the ability to be paid forboth your raw material and product. It gets better as people salivate over apparenttipping fees of $1 or more per passenger tire and crumb selling prices of $300/ton ormore. It certainly sounds like a "can't fail" dream business, but dreams rarelywithstand the reality of daylight. There is more to crumb rubber production thansimply buying equipment, then wearing a path to your bank deposit window.

Performing meaningful "due diligence" prior to investing time and money incrumb rubber production is critical. Purchasing equipment may actually prove to becomparatively simple once business parameters have been adequately qefined.Critical issues include at least the following parameters, based on extensivediscussions with many industry participants, some of whom trumpeted their successuntil the day they declared bankruptcy. The focus is on differentiating reality frominitial perception.

Economic Support - Some states offer significant capital and/or operating subsidies toencourage development of viable production of crumb rubber and recycled rubberproducts. In addition, tipping fees are normally, c.harged for collection and/or disposalof scrap tires. If these subsidies or fees include tire collection and transportationresponsibilities, then associated capital and operating costs must be recognized anddeducted from the subsidy to define net e,conomic benefit to the processing business.The probability and impact of changes in subsidies or fees should also be carefully

assessed.

Product Markets - The rate of product market development has historically limitedgrowth of both large-scale and small-scale scrap tire processing. Elapsed time andcost associated with market development is generally under-estimated and has amajor impact on the economic viability of processing operations. It is critical tounderstand the time requirements associated with product testing, market introductionand distribution development. Accumulating product inventory while markets developis doubly expensive because it decreases revenue anticipated from product sales while

2

increasing working capital requirements. The combined result can be fatal to anotherwise well-conceived operation because, sooner or later, either financial resourcesor regulatory agencies will limit inventory of products and tires at the site.

Product Specifications - Time spent defining product specifications and processingrequirements generally saves money in implementation and minimizes lessons learnedthe hard (and expensive) way. Equipment that may be perfect for one applicationmay be technically or economically unsuitable for another. Considering evolutionarystages for markets and products can improve the probability that initial equipmentpurchases will have flexibility to serve future needs. Properly evaluating productvolumes, specifications, and timing are probably the most critical, and commonlyignored, steps in establishing a successful processing operation. Actual marketspecifications significantly impact processing methods and costs.

Product Pricinq - Apparent product pricing may not be real for important reasons:

(1 ) Pricing may be on a delivered basis, including significant transportation costs.At $1 .25/mile and 40,000 pounds/truckload, one-way trucking costs are about$0.01/pound for each 300 miles covered and would double if the truck returnsunloaded. Transportation costs to distant markets from remote facilities candestroy net revenue.

(2) Current pricing may be negatively impacted by your competition to displacecurrent suppliers. A new supplier often has to offer an economic advantage tobe considered, then the existing supplier attempts to protect his market bymatching the new offer, etc.

Raw Material Supply - Process and equipment performance requirements depend uponthe type and quantity of waste tires to be processed. Passenger tires are ,considerablyeasier to process than steel belted truck tires, especially with the introduction of new,long-life truck tire carcasses containing higher percentages of reinforcing wire. If aspecific type of tire casing is required, is it readily available now and in the future? Inmany of the less populated provinces, tire availability is a controlling factor.

Processinq Equipment/System Desiqn - Most crumb rubber processing systems areconceptually simple and should represent a careful balance of required economics,productivity and product quality. Economic compromises may be self-defeating ifsalable product is not consistently produced. In developing tire processing systems,multiple components are normally assembled in series, with the design of eachcomponent optimized for its specific task. However, the impact of series operation onoverall system reliability is often ignored. When multiple components are integrallyinterlocked in series, overall system reliability generally becomes the product of eachcomponent's reliability. For instance, the overall reliability of a process using 5

3

interlocked components with individual 90% -operating factors will be 0.9 X 0.9 X 0.9X 0.9 X 0.9 or 59%. When a system is designed with this perspective, overallproductivity can be enhanced by separating sections through interim storage to allowpartial production when one section is not functioning.

Placing equal emphasis on performance of all components can also improveproductivity, even in comparatively simple systems. Attention is often focused onmajor equipment, while simple equipment like conveyors and transfer points becomeafter-thoughts. However, an improperly designed transfer point that clogs frequentlycan have a more dramatic impact on system productivity than inadequate shreddermaintenance.

These are- just a few of the major points that should be addressed prior todeveloping a process or selecting equipment. It's generally far less expensive todefine critical parameters before the system is built than it is to modify, or completelyrebuild, the system later.

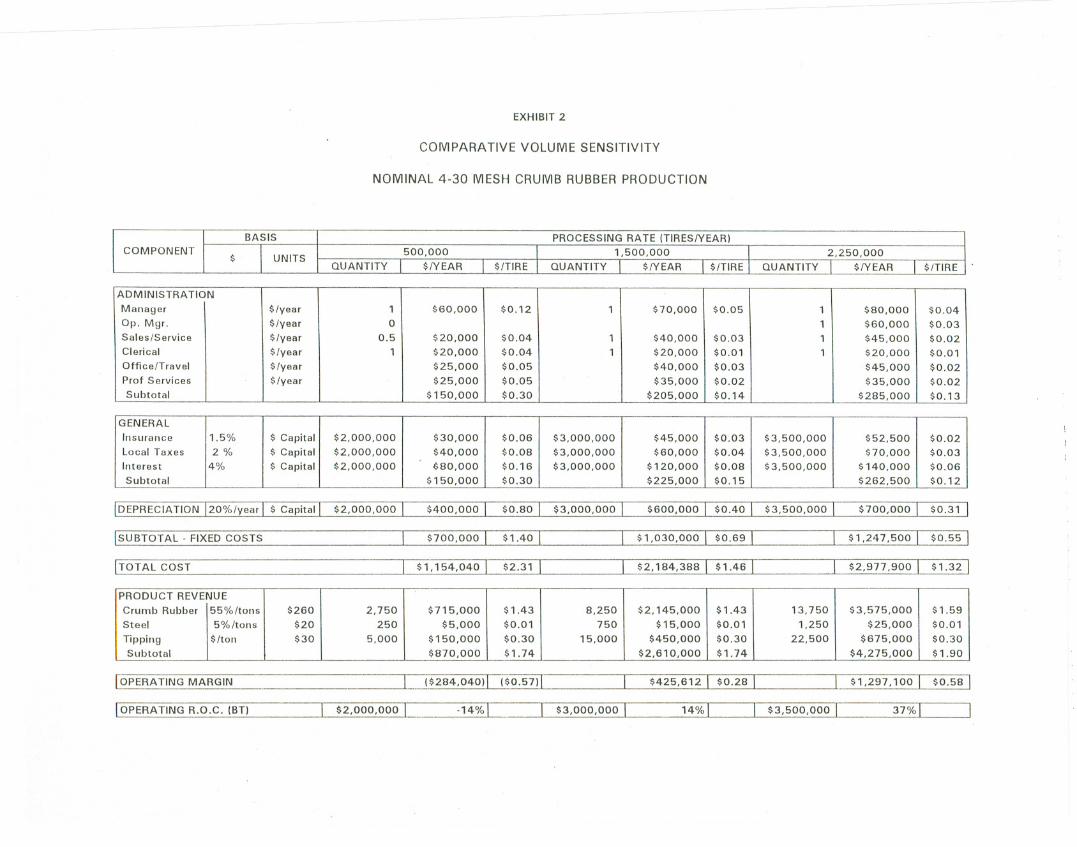

PROCESSING ECONOMICS

Properly constructed crumb rubber production facilities are capital-intensive. Ifthey aren't initially, they will be by the time they operate properly or fail, whichevercomes first. As a result of basic capital and operating parameters, crumb rubberproduction economics are extremely volume sensitive. Volume impact can beillustrated by comparing 3 processing rates for a facility producing a range of crumbproducts down to 30 mesh.

Each facility is unique in its productivity, system equipment, layout laborcosts, utility rates, product mix, etc. Since ,each operation will have differenteconomics, the following projections are intended only to provide a basis for volumecomparison purposes.

A crumb rubber facility has the same basic components regardless ofproduction capacity. Larger plants may have more components in series or parallel toincrease total capacity. Smaller plants that choose to have smaller equipmentgenerally fail. Equipment selection is dictated by tire construction and strength, sosmall equipment may not be durable even at low volume.

. Approximate variable cost projections for each of these processing rates areprovided in Exhibit I. Major cost components include labor, power, maintenance, andwaste disposal (if necessary). Projected labor costs include applicable taxes andbenefits, and are subject to wide variation based on location. It should be noted that

4

working supervisors capable of identifying and implementing proper operational andmaintenance procedures are a critical part of a successful operation. Crumb rubberprocesses require manual labor and monitoring positions regardless of processingvolume, so labor is also volume sensitive.

Power costs are also subject to wide variation depending upon a utility's ratebasis, and motors are not generally fully loaded during operation. Base rates formaximum demand can be similar for low or high volume facilities if not carefullycontrolled.

Maintenance costs are dependent on specific machinery and operatingconditions. However, knife life is generally shorter than projected by themanufacturer, and deferring necessary replacement normally results in accelerateddeterioration of other components including shafts, bearings, and cutting box.Equipment requires periodic major maintenance, as reflected in "other" costs, but thiscost is often not recognized during initial operation. It can't be ignored when themachine breaks down and requires $100,000 for rebuilding. Bead wire and fluff arenot recovered and recycled as easily or frequently as represented, and disposal costscan be significant.

As illustrated in Exhibit I, total variable cost per tire decreases about 15% as afunction of increasing volume. Limited volume sensitivity results from some of thesecosts being directly proportional to throughput.

Operators sometimes focus their attention on variable costs and fail torecognize the impact of fixed costs. However, fixed costs are economically significantand show considerably greater variation as a function of volume since administrativeand capital charges are not directly proportional to volume. Comparative fixed costs

are provided in Exhibit II, including administration, ~apital, and general components.

Administrative staffing is subject to wide variation depending on tire collectionand product marketing requirements. Administrative savings can be self-defeating ifinadequate time or resources are devoted to critical marketing or managementfunctions. Professional services such as legal, accounting, and technical assistanceare often ignored, resulting in higher ultimate cost associated with inefficient use ofmanagement time and resources. Equipment depreciation is a real cost in tireprocessing. Even with proper maintenance, equipment simply reaches a point wherereplacement is less expensive than continued repair and downtime. Insurance andproperty taxes can be significant. As a result, fixed costs per tire are extremelyvolume sensitive. Fixed costs show even greater variation if interest expensesassociated with borrowed capital are included.

Combined revenue from tipping fees and product sales must equal or exceed

5

total processing costs for a facility to remain economically viable on a long-term basis.As a result of this volume sensitivity, a small volume producer for captive use would

normally find it less expensive to purchase material than to produce it. Having crumbrubber available from comparatively high volume regional crumb rubber manufacturersshould prove to be an economic benefit to smaller manufacturers utilizing this rawmaterial.

CONSTRUCTIVE SUGGESTIONS

Ten years from now we will probably recognize that the North American crumbrubber industry was in its early adolescence in 2000. It has gained from experiences,but still makes many mistakes, some of them more than once. It has a long journeyto productive maturity. The following constructive suggestions are offered from anexperienced observers perspective based on extensive discussions with current andpast industry participants.

Suggestions for current participants include the following:

(1 ) Marketing - Don't complain about absence of markets if your definition ofmarketing is offering the lowest price to pre-existing customers. The survivorswill probably become proactive in market development, working with rubberproduct users, compounders, molders and inventors to increase market size.Hopefully, initial supply agreements will enhance revenue beyond developmentcosts.

(2) Cooperation - Crumb rubber producers today are inherently regional, but manypotential markets are national. As a result, it is economically difficult toaccelerate market development through national advertising, technical datadevelopment, market research and ca"se history publishing. If regionalcompanies chose to pool resources. 'to develop critical information,advertisements or case histories, each company would benefit in its geographicregion due to inherent transportation economics. Several companies areattempting to initiate such cooperatives, but it does require a basic change inmentality and approach.

(3) Pricing - Crumb rubber producers are commonly whipsawed by existingcustomers based on new entrants or desperate suppliers. Prices can dropprecipitously if the viability of the product or supplier are not carefullyevaluated. In some cases, prices stay depressed even after the competitiveproduct or company have failed to provide real competition. Understanding thecustomer's needs and competitors' products, then exercising patience in priceadjustments, could help to control price erosion.

6

(1 )

(4) Expanding Markets - Crumb rubber producers should consider becoming morepro-active in internal or cooperative development of finished products? Someentrepreneurs may have good ideas but lack resources for demonstrating theproducts. Can crumb rubber producers establish themselves as soundingboards and work cooperatively with others to accelerate development ofapplications? Can interests of all parties be protected by supply agreements oreven ownership participation?

(5) Operating Costs - Understanding "real" fixed and variable costs is a criticalcomponent in establishing appropriate product pricing for business viability.Ignoring economic reality results in business failures, and crumb rubber has hadits share. Controlling operating costs by deferring maintenance is anaccountant's solution and a businessman's failure.

(6) Professionalism - The industry wants, and needs, to be recognized asprofessional manufacturers of consistent, quality products and credibletechnical/marketing information. This recognition must be earned byappropriate behavior. Quality control should be real. More effort should bedevoted to demonstrating the technical and economic merits of a product orapplication, and less to bashing its industry competitor.

Suggestions for governmental agencies and regulators include:

(1 ) State regulators have a difficult challenge in attempting to force-fit maximumresource recovery objectives within limited markets and economics of scale.Perhaps states should reconsider open support of new crumb productionfacilities if tire supplies and/or product markets don't allow efficient operation ofexisting suppliers. There is no single solution to a scrap tire problem. Multiplealternatives, including crumb rubber, civil engineering and possibly even TDF,are required for successful waste tire management programs.

(2) Providing grants and low-cost loans to additional crumb rubber producers in asaturated market, as is being done in some states, lowers the capital andoperating cost basis of a new entrant, making it even more difficult for existingparticipants to survive.

Suggestions for those considering entrance into the crumb rubber market:

Carefully examine all critical business parameters before entering this "can'tmiss" opportunity. Recognize that product prices will be lower, operating costshigher and the learning curve longer than your most pessimistic projection.

7

(2) Be sure that there is an adequate uncommitted waste tire supply to supportprojected operating rates, and that it is unlikely to be eroded by future entrants.

(3) Be sure that you fully understand your projected markets, includingspecifications, competitive materials, development time and pricing sensitivities.

SUMMARY

The crumb rubber industry is in its adolescent evolutionary stage, wrestlingwith significant obstacles to sustained profitability. Some current participants havedeveloped a sound understanding of process operations, economics and markets.Converting this understanding into sustained profitability has been a challengerequiring a strong heart and stronger checkbook. Future participants should treadwith caution, evaluating reality as carefully as possible before entering. Dealing withadolescence is difficult, but this industry will hopefully mature into a successful,profitable adult member of our industrial society.

8

- - ---

EXHIBIT 1

COMPARATIVE VOLUME SENSITIVITY

NOMINAL 4-30 MESH CRUMB RUBBERPRODUCTION

POWER 900 $98,280 1200$262,080 J $0.17 I 1200 I $393,120 I $0.17 I

WASTE

DISPOSAL

2000 $30,000 6053 $90,788 9,000 $135,000 ~ISUBTOTAL - VARIABLE COSTS -~ $454,040 I $0.91 ,'--L!1,154,388 I $0.771 1_$1,730,400 L_$o.nl